Cecilia J. Ross, 9DPH Director, Los Angeles Office of Public and Indian Housing. Joan S. Hobbs Regional Inspector General for Audit, 9DGA

|

|

|

- Baldric Turner

- 8 years ago

- Views:

Transcription

1 Issue Date March 30, 2004 Audit Case Number 2004-LA-1002 TO: Cecilia J. Ross, 9DPH Director, Los Angeles Office of Public and Indian Housing FROM: SUBJECT: Joan S. Hobbs Regional Inspector General for Audit, 9DGA Housing Authority of the City of Los Angeles Management of Legal Matters INTRODUCTION We previously completed a review of the Housing Authority of the City of Los Angeles (HACLA) procurement activities, including ongoing monitoring and management of resultant contracts, as they relate to its Resident Management Corporations/Resident Advisory Councils (RMCs). The review was initiated in response to several citizen complaints alleging irregularities with HACLA s RMCs and related contracting activities. Legal complications have precluded the issuance of a final audit report setting out the results of this review. However, as part of this review, we also identified problems related to HACLA s management of its legal affairs, including failure to advise HUD of significant legal matters. The results of our review, as it relates to this one matter, are set out in this audit memorandum. The audit was performed in accordance with generally accepted government auditing standards. In accordance with HUD Handbook REV-3, within 60 days please provide us, for each recommendation without a management decision, a status report on: (1) the corrective action taken; (2) the proposed corrective action and the date to be completed; or (3) why action is considered unnecessary. Additional status reports are required at 90 days and 120 days after report issuance for any recommendation without a management decision. Also, please furnish us copies of any correspondence or directives issued because of the audit. Should you or your staff have any questions, please contact me at (213) extension 3705.

. The review was initiated in response to several citizen complaints alleging irregularities with HACLA s RMCs and related contracting activities.")

2 SUMMARY During a limited review of the Housing Authority of the City of Los Angeles (HACLA) operations associated with its Resident Management Corporations/Resident Advisory Councils (RMCs) we identified problems with HACLA s management of legal matters. Specifically, HACLA incurred outside legal service fees and also entered into a $1.8 million litigation settlement agreement to resolve an employee lawsuit without obtaining required prior HUD notification and approval. HACLA also incurred unnecessary and ineligible attorney fees of $119,440 on behalf of a consultant and $47,227 in unnecessary attorney fees to monitor information requests and activities of the OIG during our review. In our opinion, these inappropriate actions were a result of inappropriate executive decisions and intentional disregard of HUD requirements on behalf of HACLA management. BACKGROUND The Housing Authority of the City of Los Angeles, California (HACLA) was organized as a Public Housing Authority (PHA) in 1938 to provide low-cost housing to individuals meeting criteria established by the U.S. Department of Housing and Urban Development (HUD). HACLA, one of the largest Public Housing Authorities (PHAs) in the nation, has more than 60 developments with over 8,000 units and 20,000 residents in its conventional public housing program. HACLA also administers Section 8 Programs with over 44,000 units and 95,000 residents. Programs administered by HACLA are designed to enable low-income families, the elderly, and persons with disabilities to obtain and reside in housing that is decent, safe, sanitary, and in good repair. OIG Hotline Complaint In July 2001 and September 2001, OIG received two separate complaints alleging similar HACLA contracting irregularities with its RMCs including: Kickbacks Unfair bidding practices Nonprofessional and unethical conduct Conflicts of interest Based on the nature of the OIG Hotline Complaints, OIG initiated a limited review focusing on the allegations received in the complaints. This review has been completed but other ongoing matters have precluded the issuance of our final audit report related to these issues. However, although not part of the original complaint review, we did identify concerns with HACLA s management of its legal affairs. We reviewed this matter and have set out the results of the review in this memorandum. 2

3 FINDING - HACLA DID NOT MANAGE ITS LEGAL AFFAIRS IN COMPLIANCE WITH APPLICABLE REQUIREMENTS AND COST GUIDELINES INELIGIBLE - $119,440 AND UNSUPPORTED - $47,227 HACLA incurred outside legal service fees and also entered into a $1.8 million litigation settlement agreement to resolve an employee lawsuit without obtaining required prior HUD notification and approval. HACLA also incurred unnecessary and ineligible attorney fees of $119,440 on behalf of a consultant and $47,227 in unnecessary attorney fees to monitor information requests and activities of the OIG during our review. In our opinion, these improper actions were a result of inappropriate executive decisions and intentional disregard for HUD requirements by HACLA management. In accordance with paragraphs 5-2 and 5-3c of HUD Handbook REV 4, Litigation, a Public Housing Authority (PHA) is required to notify HUD of pending litigation and obtain written concurrence prior to accepting a settlement offer arising out of litigation. Additionally, per paragraphs 3-3b(3) and 5-4 of the Litigation handbook, a PHA must obtain Regional Counsel approval prior to entering any litigation services contract with a private attorney(s) where the fee is expected to exceed $10,000. Costs are not allowable for payment from a Federal award unless they are necessary and reasonable for proper and efficient performance and administration of Federal awards (reference Section E of OMB Circular A-87, Cost Principles for State, Local, and Indian Tribal Governments). HACLA failed to adhere to these requirements in the management of their legal affairs as discussed below. Prior HUD notification of pending litigation and approval of settlements In November 1997 the first in a series of three lawsuits were initiated against HACLA by one of its employees for actions the employee claimed HACLA had taken against her as a result of whistle blower type activities reported by her. HACLA did not notify HUD of any of the three lawsuits as required by paragraph 5-2 of HUD Handbook REV 4, nor did it notify HUD prior to entering into agreements to settle the lawsuits. These agreements entered in May 2000 and March 2001 required payment to the employee of $1,860,000. Additionally, in October 2000 an additional quasi-related lawsuit was filed against HACLA (see below). Again, HACLA did not notify HUD of the lawsuit even though significant attorney fees were incurred. HACLA claimed that there was no requirement to notify HUD of the lawsuits and settlements as the litigation and settlement was handled by its insurance company. This claim is not valid. The applicable requirements do not differentiate between litigation handled by an insurance company and that handled directly by a PHA. Accordingly, all such litigation must be reported to HUD. This notification is necessary to allow HUD to fulfill its monitoring responsibilities and maintain awareness of significant matters, which could affect both the PHA and HUD. Further, HACLA s claim that settlement costs were 3

4 covered by insurance is not accurate. HACLA was required to pay $236,586 of the ultimate settlement charges. HACLA contracted with private attorneys without HUD concurrence and incurred $119,440 in ineligible charges and $47,227 in questionable charges HACLA entered into contracts with private attorneys without obtaining prior HUD written concurrence as required by paragraph 5-4 of HUD Handbook REV 4. Further, HACLA incurred $166,667 in attorney s fees which were not reasonable and necessary and accordingly, ineligible. In October 2000, a lawsuit was filed against HACLA and a consultant who had done significant business with HACLA and its RMCs. This consultant, who was also a central party in the lawsuits discussed above, asked that HACLA pay his legal fees relating to the lawsuit. HACLA agreed to this and entered a joint defense agreement with the consultant. On November 17, 2000 in accordance with the joint defense agreement, HACLA entered into a contract agreeing to pay an attorney selected by the consultant for an amount not to exceed $25,000 for the consultant s legal defense. In December 2000, the consultant replaced his attorney with another law firm, wherein HACLA entered into another sole source contract with this firm in an amount not to exceed $10,000. It should be noted that by the time this contract was executed, charges under the contract already exceeded the maximum price. Accordingly, on February 23, 2001, by which time over $30,000 in legal fees had been incurred, HACLA s board agreed to a contract amendment increasing the maximum contract price from $10,000 to $85,000 (HACLA could not locate this original contract amendment). In March 2002, the contract was again amended increasing the maximum payable to $135,000. As of September 2002, the total paid by HACLA for the consultant s legal defense under these series of contracts was $119,440. This includes at least $3,544 in charges for his attorney s dealings with the OIG during our audit of HACLA s operations. HACLA did not notify HUD of this lawsuit nor request written concurrence to its contracting with private attorneys for the litigation services involved in this lawsuit. In fact, documentation available indicates HACLA actively tried to avoid informing HUD of the suit and obtaining written approval of the contracts. For example, an between two HACLA employees, which was located in the contract file, states in part, does not advise entering into a new contract.entering into a new contract with this law firm would require HUD approval pursuant to HUD REG Rev., Ch. 5, Section 5-4 as provided for in the HUD Litigation Handbook. This demonstrates that HACLA was fully aware of its obligations to HUD, but chose to disregard them. When HACLA staff was questioned about paying the consultant s legal fees, they claimed it was in the best interest of HACLA and further stated they had obtained a legal opinion from the City Attorney s office to support their actions. When asked for a copy of this opinion, HACLA could not provide it, but instead provided an opinion dated November 2002, two years after the fact, wherein the City Attorney s office attempted to justify the payments on behalf of the consultant. However, in our opinion, the 4

5 justification claimed is not valid. The consultant, under the terms of his contracts with HACLA and its RMCs, was required to have valid professional liability insurance of at least $1,000,000. Such insurance, if it had been obtained, should have covered the consultant s legal fees and would not have necessitated a joint defense agreement. However, HACLA had not required the consultant to adhere to his contract and obtain liability insurance. In fact, based upon information provided by the consultant, such liability insurance was not obtained until September 2000, five years after he had begun contracting with HACLA. Payment of legal fees by the consultant, which should have been his responsibility, is not a reasonable and necessary expense and accordingly, the $119,440, and any additional related expenses, are ineligible charges for any federal grant program and must be refunded by HACLA from non-federal funds. An additional $47,227 in outside legal fees was incurred by HACLA without obtaining prior HUD notification and concurrence. Further, these fees were, in our opinion, not reasonable and necessary charges. In fact, the charges were for assisting HACLA in dealing with OIG s review, including responding to requests for information deemed necessary for our review. Such interference ended up impeding the efficient conduct of our review without benefiting HACLA s housing programs. HACLA claims the $47,227 was paid using other non-hud funds. However, specific documentation needs to be provided to support this claim and if not substantiated, HACLA would be required to refund the $47,227 to its federally funded housing programs. AUDITEE COMMENTS We provided our draft report to HACLA on January 29, 2004 and discussed this draft with HACLA representatives at an exit conference on February 10, Additionally, on February 17, 2004 and March 19, 2004, HACLA provided written comments and additional information in response to the draft report and the exit conference. We have included HACLA s March 19, 2004 (final) written comments in Attachment B to the report and have summarized them below. HACLA stated that the questioned legal costs have now been paid from non-federal funding and provided a schedule to document this claim. Additionally, HACLA stated that it thought that it had tight controls to monitor outside legal services and ensure that contractors meet basic contractual obligations. HACLA stated that it has consistently obtained HUD approval for all substantive legal matters and obtained HUD approval of legal contracts and settlements as appropriate and that its failure to do so for the items discussed in our report was an oversight. However, HACLA had concerns about the report s discussion of management s apparent intentional violation of HUD requirements relating to prior HUD approval of contracts for legal services. HACLA felt that this was not accurate and asked that the conclusions related to this be removed from the report. HACLA provided additional comments on the defense of a contractor and stated that litigation between the Jordan Downs RMC and the Housing Authority was the result of the contractor stepping forward as a whistleblower and felt it would send the wrong message to the public if they did not defend him. 5

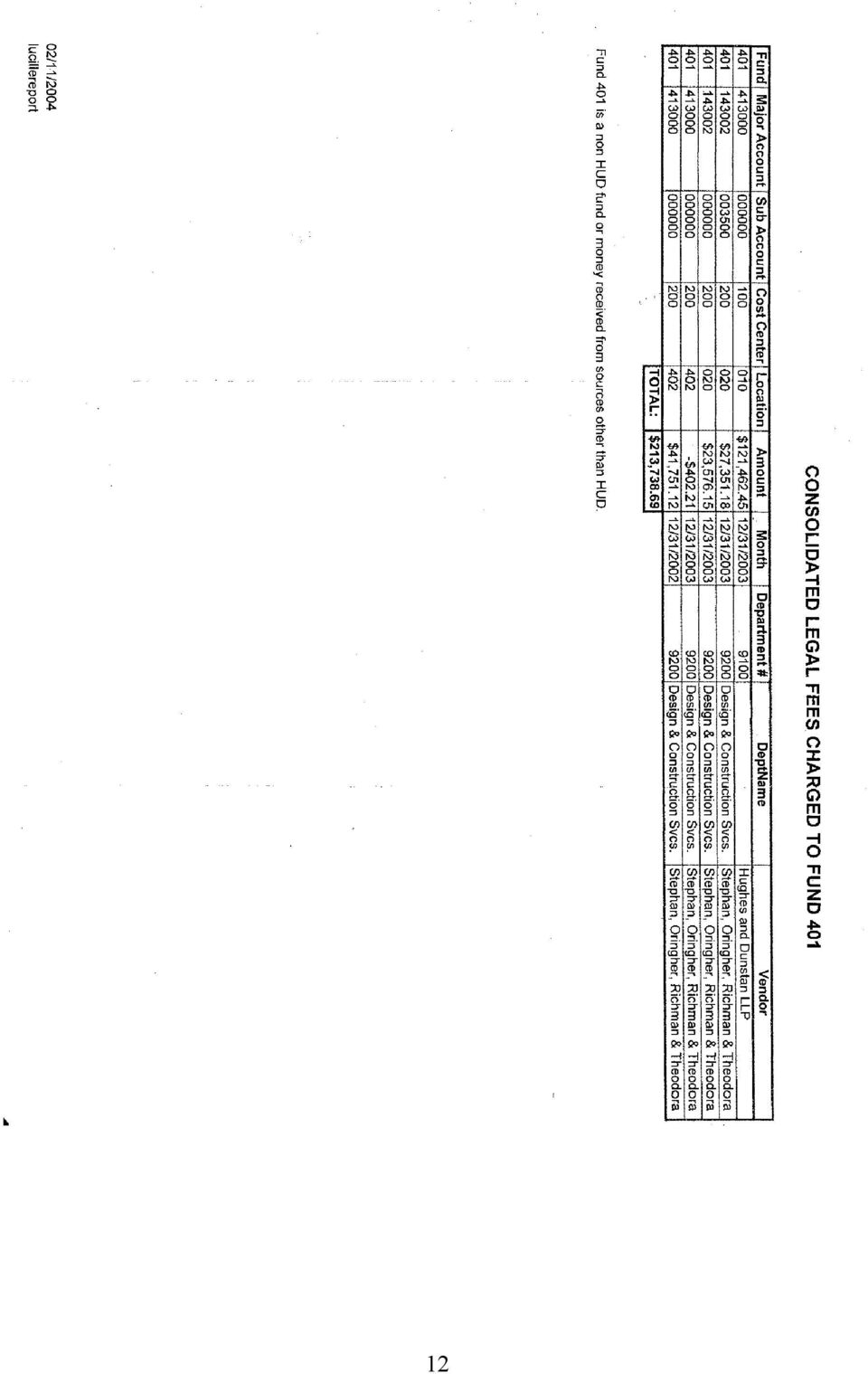

6 OIG EVALUATION OF AUDITEE COMMENTS Documentation supplied by HACLA to support the use of Non-HUD funds was simply a spreadsheet claiming to summarize cost transfers to Fund 401 Non-HUD Funds. During the course of our audit we documented the use of federal funds for legal costs and HACLA s documentation does not serve to support their claim that these transfers were actually made nor does it identify the source of funding accounted for in Fund 401. Therefore, additional information and documentation needs to be submitted to substantiate HACLA s claimed payment of questioned legal fees from non-federal; funds. In relation to the sufficiency of HACLA s controls over legal matters and enforcement of basic contract requirements, it was apparent (as discussed in the finding) that these controls and procedures were not adequate to ensure that legal fees were appropriate, required HUD approval of legal matters was obtained and contractors met basic contract requirements. Accordingly, HACLA needs to establish additional controls and procedures that will ensure future compliance in these matters. Further, we believe that our comments relating to apparent intentional violation of HUD requirements do not warrant change, as they are supported by s in HACLA s own files, which clearly demonstrated an intentional circumvention of HUD requirements. Finally, with respect to HACLA s comments regarding the defense of the contractor, the contractor was required to carry professional liability insurance in his position with the Resident Management Corporations and should have provided his own defense. Further, in our opinion, the case was not a simple whistleblower case, but involved serious accusations relating to the contractor s activities and actions as they related to fulfillment of his contractual obligations. (This whistleblower case was a different case than that which was discussed in the report). RECOMMENDATIONS We recommend your office require HACLA to: A Repay, using non-federal funds, its conventional low-rent program the $119,440 in ineligible legal fees incurred in defending its consultant; B Provide documentation to your office evidencing that non-federal funds were used to pay the $47,227 in legal costs relating to our audit and if not substantiated, repay the funds to the applicable program; C Establish procedures to ensure that legal fees are incurred only when they are reasonable and necessary for its housing operations and to obtain the required HUD approval for outside legal services and legal settlements; and D Implement policies and procedures to ensure that contractors meet basic contract requirements, including obtaining of required liability insurance. 6

7 Appendix A SCHEDULE OF QUESTIONED COSTS AND FUNDS PUT TO BETTER USE Recommendation Type of Questioned Cost Funds Put to Number Ineligible 1/ Unsupported 2/ Better Use 3/ A 119,440 B 47,227 1/ Ineligible costs are costs charged to a HUD-financed or HUD-insured program or activity that the auditor believes are not allowable by law, contract or Federal, State or local policies or regulations. 2/ Unsupported costs are costs charged to a HUD-financed or HUD-insured program or activity and eligibility cannot be determined at the time of audit. The costs are not supported by adequate documentation or there is a need for a legal or administrative determination on the eligibility of the costs. Unsupported costs require a future decision by HUD program officials. This decision, in addition to obtaining supporting documentation, might involve a legal interpretation or clarification of Departmental policies and procedures. 3/ Funds Put to Better Use are costs that will not be expended in the future if our recommendations are implemented. 7

8 Appendix B AUDITEE COMMENTS 8

9 9

10 10

11 11

12 12

MEMORANDUM FOR: K.J. Brockington, Director, Los Angeles Office of Public Housing, 9DPH

U.S. Department of Housing and Urban Development Office of Inspector General Region IX 611 West Sixth Street, Suite 1160 Los Angeles, CA 90017 Voice (213) 894-8016 Fax (213) 894-8115 Issue Date May 5,

U.S. Department of Housing and Urban Development Office of Inspector General Region IX 611 West Sixth Street, Suite 1160 Los Angeles, CA 90017 Voice (213) 894-8016 Fax (213) 894-8115 Issue Date May 5,

Cecilia Ross Director, Los Angeles Office of Public Housing, 9DPH. Joan S. Hobbs Regional Inspector General for Audit, 9DGA

Issue Date January 21, 2005 Audit Case Number 2005-LA-1805 TO: Cecilia Ross Director, Los Angeles Office of Public Housing, 9DPH FROM: SUBJECT: Joan S. Hobbs Regional Inspector General for Audit, 9DGA

Issue Date January 21, 2005 Audit Case Number 2005-LA-1805 TO: Cecilia Ross Director, Los Angeles Office of Public Housing, 9DPH FROM: SUBJECT: Joan S. Hobbs Regional Inspector General for Audit, 9DGA

Harlan Stewart, Director, Region X Office of Public Housing, 0APH. Joan S. Hobbs, Regional Inspector General for Audit, Seattle, Region X, 0AGA

Issue Date January 9, 2009 Audit Report Number 2009-SE-1001 TO: Harlan Stewart, Director, Region X Office of Public Housing, 0APH FROM: Joan S. Hobbs, Regional Inspector General for Audit, Seattle, Region

Issue Date January 9, 2009 Audit Report Number 2009-SE-1001 TO: Harlan Stewart, Director, Region X Office of Public Housing, 0APH FROM: Joan S. Hobbs, Regional Inspector General for Audit, Seattle, Region

Roger E. Miller, Director, Office of Insured Healthcare Facilities, HI. Mona Fandel, Region X Regional Counsel, 0AC

Issue Date April 15, 2009 Audit Report Number 2009-SE-1002 TO: Roger E. Miller, Director, Office of Insured Healthcare Facilities, HI Mona Fandel, Region X Regional Counsel, 0AC FROM: Joan S. Hobbs, Regional

Issue Date April 15, 2009 Audit Report Number 2009-SE-1002 TO: Roger E. Miller, Director, Office of Insured Healthcare Facilities, HI Mona Fandel, Region X Regional Counsel, 0AC FROM: Joan S. Hobbs, Regional

William J. Daley, Regional Counsel, 6AC. Henry S. Czauski, Acting Director of Departmental Enforcement Center, CV

Issue Date March 21, 2008 Audit Report Number 2008-FW-1008 TO: Gretchen Marchand Director, Multifamily Housing Division, 6JHMLAX William J. Daley, Regional Counsel, 6AC Henry S. Czauski, Acting Director

Issue Date March 21, 2008 Audit Report Number 2008-FW-1008 TO: Gretchen Marchand Director, Multifamily Housing Division, 6JHMLAX William J. Daley, Regional Counsel, 6AC Henry S. Czauski, Acting Director

Walter Kreher, Director, Multifamily Program Center, 2FHM. Alexander C. Malloy, Regional Inspector General for Audit, 2AGA INTRODUCTION

Issue Date September 27, 2004 Audit Case Number 2004-NY-1005 TO: Walter Kreher, Director, Multifamily Program Center, 2FHM FROM: Alexander C. Malloy, Regional Inspector General for Audit, 2AGA SUBJECT:

Issue Date September 27, 2004 Audit Case Number 2004-NY-1005 TO: Walter Kreher, Director, Multifamily Program Center, 2FHM FROM: Alexander C. Malloy, Regional Inspector General for Audit, 2AGA SUBJECT:

Waterbury Housing Authority, Waterbury, CT

Waterbury Housing Authority, Waterbury, CT Allocation of Costs to Asset Management Projects Office of Audit, Region 1 Boston, MA Audit Report Number: 2015-BO-1004 September 30, 2015 To: From: Subject:

Waterbury Housing Authority, Waterbury, CT Allocation of Costs to Asset Management Projects Office of Audit, Region 1 Boston, MA Audit Report Number: 2015-BO-1004 September 30, 2015 To: From: Subject:

AUDIT REPORT SAVANNAH TRACE APARTMENTS MULTIFAMILY EQUITY SKIMMING KALAMAZOO, MICHIGAN 2005-CH-1012 AUGUST 4, 2005

AUDIT REPORT SAVANNAH TRACE APARTMENTS MULTIFAMILY EQUITY SKIMMING KALAMAZOO, MICHIGAN 2005-CH-1012 AUGUST 4, 2005 OFFICE OF AUDIT, REGION V CHICAGO, ILLINOIS Issue Date August 4, 2005 Audit Report Number

AUDIT REPORT SAVANNAH TRACE APARTMENTS MULTIFAMILY EQUITY SKIMMING KALAMAZOO, MICHIGAN 2005-CH-1012 AUGUST 4, 2005 OFFICE OF AUDIT, REGION V CHICAGO, ILLINOIS Issue Date August 4, 2005 Audit Report Number

Scott G. Davis, Director, Disaster Recovery and Special Issues Division, DGBD

Issue Date July 20, 2010 Audit Report Number 2010-FW-1005 TO: FROM: Scott G. Davis, Director, Disaster Recovery and Special Issues Division, DGBD //signed// Gerald R. Kirkland Regional Inspector General

Issue Date July 20, 2010 Audit Report Number 2010-FW-1005 TO: FROM: Scott G. Davis, Director, Disaster Recovery and Special Issues Division, DGBD //signed// Gerald R. Kirkland Regional Inspector General

The City of New York, Office of Management and Budget, New York, NY

The City of New York, Office of Management and Budget, New York, NY Community Development Block Grant Disaster Recovery Funds, Business Loan and Grant Program Office of Audit, Region 2 New York New Jersey

The City of New York, Office of Management and Budget, New York, NY Community Development Block Grant Disaster Recovery Funds, Business Loan and Grant Program Office of Audit, Region 2 New York New Jersey

Public Housing Operating and Capital Fund Program Central Office Cost Center Fees

OFFICE OF AUDIT REGION 9 LOS o ANGELES, CA Office of Public and Indian Housing Washington, DC Public Housing Operating and Capital Fund Program Central Office Cost Center Fees 2014-LA-0004 JUNE 30, 2014

OFFICE OF AUDIT REGION 9 LOS o ANGELES, CA Office of Public and Indian Housing Washington, DC Public Housing Operating and Capital Fund Program Central Office Cost Center Fees 2014-LA-0004 JUNE 30, 2014

AUDIT REPORT FIRST SOURCE FINANCIAL USA HENDERSON, NEVADA 2005-LA-1003. May 12, 2005 OFFICE OF AUDIT PACIFIC/HAWAII REGION LOS ANGELES, CALIFORNIA

AUDIT REPORT FIRST SOURCE FINANCIAL USA HENDERSON, NEVADA 2005-LA-1003 May 12, 2005 OFFICE OF AUDIT PACIFIC/HAWAII REGION LOS ANGELES, CALIFORNIA 1 Issue Date May 12, 2005 Audit Report Number 2005-LA-1003

AUDIT REPORT FIRST SOURCE FINANCIAL USA HENDERSON, NEVADA 2005-LA-1003 May 12, 2005 OFFICE OF AUDIT PACIFIC/HAWAII REGION LOS ANGELES, CALIFORNIA 1 Issue Date May 12, 2005 Audit Report Number 2005-LA-1003

OFFICE OF AUDIT REGION 9 LOS ANGELES, CA. Marina Village Apartments Sparks, NV. Section 221(d)(4) Multifamily Insurance Program

(4) Multifamily Insurance Program") OFFICE OF AUDIT REGION 9 LOS ANGELES, CA Marina Village Apartments Sparks, NV Section 221(d)(4) Multifamily Insurance Program 2014-LA-1001 OCTOBER 24, 2013 Issue Date: October 24, 2013 Audit Report Number:

OFFICE OF AUDIT REGION 9 LOS ANGELES, CA Marina Village Apartments Sparks, NV Section 221(d)(4) Multifamily Insurance Program 2014-LA-1001 OCTOBER 24, 2013 Issue Date: October 24, 2013 Audit Report Number:

OFFICE OF AUDIT REGION 3 PHILADELPHIA, PA. U.S. Department of Housing and Urban Development, Washington, DC. Home Equity Conversion Mortgage Program

OFFICE OF AUDIT REGION 3 PHILADELPHIA, PA U.S. Department of Housing and Urban Development, Washington, DC Home Equity Conversion Mortgage Program 2014-PH-0001 SEPTEMBER 30, 2014 Issue Date: September

OFFICE OF AUDIT REGION 3 PHILADELPHIA, PA U.S. Department of Housing and Urban Development, Washington, DC Home Equity Conversion Mortgage Program 2014-PH-0001 SEPTEMBER 30, 2014 Issue Date: September

OFFICE OF AUDIT REGION 9 LOS ANGELES, CA. The Lending Company, Inc. Phoenix, AZ. Single Family Housing Mortgage Insurance Program

OFFICE OF AUDIT REGION 9 LOS ANGELES, CA The Lending Company, Inc. Phoenix, AZ Single Family Housing Mortgage Insurance Program 2013-LA-1008 AUGUST 20, 2013 Issue Date: August 20, 2013 Audit Report Number:

OFFICE OF AUDIT REGION 9 LOS ANGELES, CA The Lending Company, Inc. Phoenix, AZ Single Family Housing Mortgage Insurance Program 2013-LA-1008 AUGUST 20, 2013 Issue Date: August 20, 2013 Audit Report Number:

AUDIT REPORT USE OF PROJECT FUNDS TIMBERLAKE CARE CENTER KANSAS CITY, MISSOURI 2004-KC-1002. March 10, 2004 OFFICE OF AUDIT, REGION 7 KANSAS CITY, KS

AUDIT REPORT USE OF PROJECT FUNDS TIMBERLAKE CARE CENTER KANSAS CITY, MISSOURI March 10, 2004 OFFICE OF AUDIT, REGION 7 KANSAS CITY, KS Issue Date March 10, 2004 Audit Case Number TO: Herman Ransom, Director,

AUDIT REPORT USE OF PROJECT FUNDS TIMBERLAKE CARE CENTER KANSAS CITY, MISSOURI March 10, 2004 OFFICE OF AUDIT, REGION 7 KANSAS CITY, KS Issue Date March 10, 2004 Audit Case Number TO: Herman Ransom, Director,

William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH Robert Jennings, Director, Richmond Office of Public Housing, 3FPH

Issue Date October 17, 2005 Audit Report Number 2006-PH-1002 TO: William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH Robert Jennings, Director, Richmond Office of Public Housing,

Issue Date October 17, 2005 Audit Report Number 2006-PH-1002 TO: William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH Robert Jennings, Director, Richmond Office of Public Housing,

Community Development Block Grant Program

OFFICE OF AUDIT REGION 1 BOSTON, MA 1 City of Worcester, MA Community Development Block Grant Program 2013-BO-1002 JULY 29, 2013 Issue Date: July 29, 2013 Audit Report Number: 2013-BO-1002 TO: Robert Shumeyko

OFFICE OF AUDIT REGION 1 BOSTON, MA 1 City of Worcester, MA Community Development Block Grant Program 2013-BO-1002 JULY 29, 2013 Issue Date: July 29, 2013 Audit Report Number: 2013-BO-1002 TO: Robert Shumeyko

Brian D. Montgomery, Assistant Secretary for Housing, Federal Housing Commissioner, H

Issue Date December 12, 2006 Audit Report Number 2007-LA-1002 TO: Brian D. Montgomery, Assistant Secretary for Housing, Federal Housing Commissioner, H FROM: Joan S. Hobbs, Regional Inspector General for

Issue Date December 12, 2006 Audit Report Number 2007-LA-1002 TO: Brian D. Montgomery, Assistant Secretary for Housing, Federal Housing Commissioner, H FROM: Joan S. Hobbs, Regional Inspector General for

UPDATED. OIG Guidelines for Evaluating State False Claims Acts

UPDATED OIG Guidelines for Evaluating State False Claims Acts Note: These guidelines are effective March 15, 2013, and replace the guidelines effective on August 21, 2006, found at 71 FR 48552. UPDATED

UPDATED OIG Guidelines for Evaluating State False Claims Acts Note: These guidelines are effective March 15, 2013, and replace the guidelines effective on August 21, 2006, found at 71 FR 48552. UPDATED

K.J. Brockington, Director, Los Angeles Office of Public Housing, 9DPH. Tanya E. Schulze, Regional Inspector General for Audit, Region IX, 9DGA

Issue Date November 4, 2010 Audit Report Number 2011-LA-1002 TO: K.J. Brockington, Director, Los Angeles Office of Public Housing, 9DPH FROM: Tanya E. Schulze, Regional Inspector General for Audit, Region

Issue Date November 4, 2010 Audit Report Number 2011-LA-1002 TO: K.J. Brockington, Director, Los Angeles Office of Public Housing, 9DPH FROM: Tanya E. Schulze, Regional Inspector General for Audit, Region

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF INSPECTOR GENERAL

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF INSPECTOR GENERAL April 20, 2015 MEMORANDUM NO: 2015-PH-1805 Memorandum TO: FROM: SUBJECT: William A. Wilkins Director, Office of Public Housing,

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF INSPECTOR GENERAL April 20, 2015 MEMORANDUM NO: 2015-PH-1805 Memorandum TO: FROM: SUBJECT: William A. Wilkins Director, Office of Public Housing,

William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH

Issue Date December 19, 2007 Audit Report Number 2008-PH-1004 TO: William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH FROM: SUBJECT: John P. Buck, Regional Inspector General for

Issue Date December 19, 2007 Audit Report Number 2008-PH-1004 TO: William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH FROM: SUBJECT: John P. Buck, Regional Inspector General for

Community Planning and Development Community Development Block Grant and HOME Investment Partnerships Program

OFFICE OF AUDIT REGION 4 ATLANTA, GA The City of Huntsville, AL Community Planning and Development Community Development Block Grant and HOME Investment Partnerships Program 2014-AT-1005 MAY 29, 2014 Issue

OFFICE OF AUDIT REGION 4 ATLANTA, GA The City of Huntsville, AL Community Planning and Development Community Development Block Grant and HOME Investment Partnerships Program 2014-AT-1005 MAY 29, 2014 Issue

Administration of Grant HAVA

Administration of Grant Funds Authorized by HAVA Role of the Grants Office in the Administration of HAVA Funds Issue Guidance Make Grant Awards Provide Oversight and Monitoring Provide Technical Assistance

Administration of Grant Funds Authorized by HAVA Role of the Grants Office in the Administration of HAVA Funds Issue Guidance Make Grant Awards Provide Oversight and Monitoring Provide Technical Assistance

Allen Mortgage, Limited Liability Corporation, Single Family Housing Mortgage Insurance Program

OFFICE OF AUDIT REGION 5 CHICAGO, IL Allen Mortgage, Limited Liability Corporation, Single Family Housing Mortgage Insurance Program Centennial Park, AZ 2012-CH-1015 September 30, 2012 Issue Date: September

OFFICE OF AUDIT REGION 5 CHICAGO, IL Allen Mortgage, Limited Liability Corporation, Single Family Housing Mortgage Insurance Program Centennial Park, AZ 2012-CH-1015 September 30, 2012 Issue Date: September

DEVELOPMENT COST CERTIFICATION AUDIT GUIDANCE

CHAPTER 5. DEVELOPMENT COST CERTIFICATION AUDIT GUIDANCE 5-1 Program Objective. Multifamily projects are an integral part of the U.S. Department of Housing and Urban Development s (HUD) housing programs,

CHAPTER 5. DEVELOPMENT COST CERTIFICATION AUDIT GUIDANCE 5-1 Program Objective. Multifamily projects are an integral part of the U.S. Department of Housing and Urban Development s (HUD) housing programs,

OFFICE OF AUDIT REGION 8 DENVER, CO. Utah Housing Corporation West Valley City, UT. Federal Housing Administration s Preforeclosure Sale Program

OFFICE OF AUDIT REGION 8 DENVER, CO Utah Housing Corporation West Valley City, UT Federal Housing Administration s Preforeclosure Sale Program 2013-DE-1001 MAY 15, 2013 U.S. DEPARTMENT OF HOUSING AND URBAN

OFFICE OF AUDIT REGION 8 DENVER, CO Utah Housing Corporation West Valley City, UT Federal Housing Administration s Preforeclosure Sale Program 2013-DE-1001 MAY 15, 2013 U.S. DEPARTMENT OF HOUSING AND URBAN

2IÀFHRI,QVSHFWRU*HQHUDO

2IÀFHRI,QVSHFWRU*HQHUDO Santa Clara Pueblo, New Mexico, Needs Assistance to Ensure Compliance with FEMA Public Assistance Grant Requirements OIG-14-128-D August 2014 Washington, DC 20528 I www.oig.dhs.gov

2IÀFHRI,QVSHFWRU*HQHUDO Santa Clara Pueblo, New Mexico, Needs Assistance to Ensure Compliance with FEMA Public Assistance Grant Requirements OIG-14-128-D August 2014 Washington, DC 20528 I www.oig.dhs.gov

Brian D. Montgomery Assistant Secretary for Housing Federal Housing Commissioner, H

Issue Date February 10, 2009 Audit Report Number 2009-FW-1005 TO: Brian D. Montgomery Assistant Secretary for Housing Federal Housing Commissioner, H Henry S. Czauski, Acting Director, Departmental Enforcement

Issue Date February 10, 2009 Audit Report Number 2009-FW-1005 TO: Brian D. Montgomery Assistant Secretary for Housing Federal Housing Commissioner, H Henry S. Czauski, Acting Director, Departmental Enforcement

Miami-Dade County, Miami, FL

OFFICE OF AUDIT REGION 4 ATLANTA, GA Miami-Dade County, Miami, FL HOME Investment Partnerships Program 2014-AT-1010 SEPTEMBER 11, 2014 Issue Date: September 11, 2014 Audit Report Number: 2014-AT-1010 TO:

OFFICE OF AUDIT REGION 4 ATLANTA, GA Miami-Dade County, Miami, FL HOME Investment Partnerships Program 2014-AT-1010 SEPTEMBER 11, 2014 Issue Date: September 11, 2014 Audit Report Number: 2014-AT-1010 TO:

Mount Carmel Baptist Church in Hattiesburg, Mississippi, Needs Assistance to Ensure Compliance with FEMA Public Assistance Grant Requirements

Mount Carmel Baptist Church in Hattiesburg, Mississippi, Needs Assistance to Ensure Compliance with FEMA Public Assistance Grant Requirements September 30, 2015 DHS OIG HIGHLIGHTS Mount Carmel Baptist

Mount Carmel Baptist Church in Hattiesburg, Mississippi, Needs Assistance to Ensure Compliance with FEMA Public Assistance Grant Requirements September 30, 2015 DHS OIG HIGHLIGHTS Mount Carmel Baptist

City of Paterson, NJ. HOME Investment Partnerships Program. Office of Audit, Region 2 New York-New Jersey

City of Paterson, NJ HOME Investment Partnerships Program Office of Audit, Region 2 New York-New Jersey Audit Report Number: 2015-NY-1005 April 30, 2015 To: From: Subject: Anne Marie Uebbing Director Community

City of Paterson, NJ HOME Investment Partnerships Program Office of Audit, Region 2 New York-New Jersey Audit Report Number: 2015-NY-1005 April 30, 2015 To: From: Subject: Anne Marie Uebbing Director Community

John C. Weicher, Assistant Secretary for Housing-Federal Housing Commissioner, H INTRODUCTION

Issue Date April 21, 2004 Audit Case Number 2004-AT-1005 TO: John C. Weicher, Assistant Secretary for Housing-Federal Housing Commissioner, H FROM: SUBJECT: James D. McKay Regional Inspector General for

Issue Date April 21, 2004 Audit Case Number 2004-AT-1005 TO: John C. Weicher, Assistant Secretary for Housing-Federal Housing Commissioner, H FROM: SUBJECT: James D. McKay Regional Inspector General for

FEMA Should Recover $312,117 of $1.6 Million Grant Funds Awarded to the Pueblo of Jemez, New Mexico

FEMA Should Recover $312,117 of $1.6 Million Grant Funds Awarded to the Pueblo of Jemez, New Mexico March 21, 2016 DHS OIG HIGHLIGHTS FEMA Should Recover $312,117 of $1.6 Million Grant Funds Awarded to

FEMA Should Recover $312,117 of $1.6 Million Grant Funds Awarded to the Pueblo of Jemez, New Mexico March 21, 2016 DHS OIG HIGHLIGHTS FEMA Should Recover $312,117 of $1.6 Million Grant Funds Awarded to

CONTRACT ADMINISTRATION AND MANAGEMENT GUIDE

CONTRACT ADMINISTRATION AND MANAGEMENT GUIDE STATE OF IDAHO DEPARTMENT OF ADMINISTRATION DIVISION OF PURCHASING REVISED 01 01 14 Table of Contents I. Purpose... 1 II. Overview of Contract Management and

CONTRACT ADMINISTRATION AND MANAGEMENT GUIDE STATE OF IDAHO DEPARTMENT OF ADMINISTRATION DIVISION OF PURCHASING REVISED 01 01 14 Table of Contents I. Purpose... 1 II. Overview of Contract Management and

Report Number: A-03-04-002 13

DEPARTMENT OF HEALTH & HUMAN SERVICES OFFICE OF INSPECTOR GENERAL OFFICE OF AUDIT SERVICES 150 S. INDEPENDENCE MALL WEST SUITE 3 16 PHILADELPHIA, PENNSYLVANIA 19 106-3499 Report Number: A-03-04-002 13

DEPARTMENT OF HEALTH & HUMAN SERVICES OFFICE OF INSPECTOR GENERAL OFFICE OF AUDIT SERVICES 150 S. INDEPENDENCE MALL WEST SUITE 3 16 PHILADELPHIA, PENNSYLVANIA 19 106-3499 Report Number: A-03-04-002 13

Public Housing and Housing Choice Voucher Program Expenditures

OFFICE OF AUDIT REGION 1 895 BOSTON, MA The Housing Authority of the City of Bridgeport, CT Public Housing and Housing Choice Voucher Program Expenditures 2014-BO-1001 JANUARY 23, 2014 Issue Date: January

OFFICE OF AUDIT REGION 1 895 BOSTON, MA The Housing Authority of the City of Bridgeport, CT Public Housing and Housing Choice Voucher Program Expenditures 2014-BO-1001 JANUARY 23, 2014 Issue Date: January

The University of Texas at Tyler Office of Sponsored Research (OSR) Time and Effort Reporting Policy

Time and Effort Reporting Policy") The University of Texas at Tyler Office of Sponsored Research (OSR) Time and Effort Reporting Policy Applicability This Time and Effort Reporting Policy applies to all individuals receiving funding in

The University of Texas at Tyler Office of Sponsored Research (OSR) Time and Effort Reporting Policy Applicability This Time and Effort Reporting Policy applies to all individuals receiving funding in

The City of New York, Office of Management and Budget, New York, NY

The City of New York, Office of Management and Budget, New York, NY Community Development Block Grant Disaster Recovery Assistance Funds, Administration Costs Office of Audit, Region 2 New York New Jersey

The City of New York, Office of Management and Budget, New York, NY Community Development Block Grant Disaster Recovery Assistance Funds, Administration Costs Office of Audit, Region 2 New York New Jersey

FROM: Alexander C. Malloy, District Inspector General for Audit, 2AGA

Issue Date March 11, 1999 Audit Case Number - TO: Joan K. Spilman, Director of Public Housing, 2CPH FROM: Alexander C. Malloy, District Inspector General for Audit, 2AGA SUBJECT: Cohoes Housing Authority

Issue Date March 11, 1999 Audit Case Number - TO: Joan K. Spilman, Director of Public Housing, 2CPH FROM: Alexander C. Malloy, District Inspector General for Audit, 2AGA SUBJECT: Cohoes Housing Authority

U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER Special Attention of All Multifamily Hub Directors Notice H 2011-05

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER Special Attention of All Multifamily Hub Directors Notice H 2011-05

SEP 2 7 201'1. Andrew Velasquez III Regional Administrator, Region V Federal EmergenCY~,M nagement Agency

Office ofinspector General u.s. Department of Homeland Security Washington, DC 20528 Homeland Security SEP 2 7 201'1 MEMORANDUM FOR: Andrew Velasquez III Regional Administrator, Region V Federal EmergenCY~,M

Office ofinspector General u.s. Department of Homeland Security Washington, DC 20528 Homeland Security SEP 2 7 201'1 MEMORANDUM FOR: Andrew Velasquez III Regional Administrator, Region V Federal EmergenCY~,M

AUDIT TIPS FOR MANAGING DISASTER-RELATED PROJECT COSTS

AUDIT TIPS FOR MANAGING DISASTER-RELATED PROJECT COSTS Department of Homeland Security Office of Inspector General September 2012 I. Introduction The Department of Homeland Security (DHS), Office of Inspector

AUDIT TIPS FOR MANAGING DISASTER-RELATED PROJECT COSTS Department of Homeland Security Office of Inspector General September 2012 I. Introduction The Department of Homeland Security (DHS), Office of Inspector

Seattle Regional Office Seattle Federal Office Building Office of Public Housing 909 First Avenue, Suite 360 Seattle, WA 98104-1000.

U.S. Department of Housing and Urban Development Seattle Regional Office Seattle Federal Office Building Office of Public Housing 909 First Avenue, Suite 360 Seattle, WA 98104-1000 January 27, 2006 PHA

U.S. Department of Housing and Urban Development Seattle Regional Office Seattle Federal Office Building Office of Public Housing 909 First Avenue, Suite 360 Seattle, WA 98104-1000 January 27, 2006 PHA

Vicki B. Bott, Deputy Assistant Secretary for Single Family Housing, HU

Issue Date October 25, 2010 Audit Report Number 2011-AT-1001 TO: Vicki B. Bott, Deputy Assistant Secretary for Single Family Housing, HU FROM: //signed// James D. McKay, Regional Inspector General for

Issue Date October 25, 2010 Audit Report Number 2011-AT-1001 TO: Vicki B. Bott, Deputy Assistant Secretary for Single Family Housing, HU FROM: //signed// James D. McKay, Regional Inspector General for

Office of Inspector General

DEPARTMENT OF HOMELAND SECURITY < Office of Inspector General Letter Report: Review of DHS Financial Systems Consolidation Project OIG-08-47 May 2008 Office of Inspector General U.S. Department of Homeland

DEPARTMENT OF HOMELAND SECURITY < Office of Inspector General Letter Report: Review of DHS Financial Systems Consolidation Project OIG-08-47 May 2008 Office of Inspector General U.S. Department of Homeland

----------------------------------------------------------------------- DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT. [Docket No.

[Federal Register: December 29, 2010 (Volume 75, Number 249)] [Notices] [Page 82042-82053] From the Federal Register Online via GPO Access [wais.access.gpo.gov] [DOCID:fr29de10-98] -----------------------------------------------------------------------

[Federal Register: December 29, 2010 (Volume 75, Number 249)] [Notices] [Page 82042-82053] From the Federal Register Online via GPO Access [wais.access.gpo.gov] [DOCID:fr29de10-98] -----------------------------------------------------------------------

Gwinnett County, Georgia, Generally Accounted for and Expended FEMA Public Assistance Grant Funds According to Federal Requirements

Gwinnett County, Georgia, Generally Accounted for and Expended FEMA Public Assistance Grant Funds According to Federal Requirements February 20, 2015 HIGHLIGHTS Gwinnett County, Georgia, Generally Accounted

Gwinnett County, Georgia, Generally Accounted for and Expended FEMA Public Assistance Grant Funds According to Federal Requirements February 20, 2015 HIGHLIGHTS Gwinnett County, Georgia, Generally Accounted

California State University Construction Claims Program

The California State University Construction Claims Program Manual for State Funded Streamlined Projects Capital Planning, Design and Construction Office of the Chancellor 401 Golden Shore Long Beach,

The California State University Construction Claims Program Manual for State Funded Streamlined Projects Capital Planning, Design and Construction Office of the Chancellor 401 Golden Shore Long Beach,

CHAPTER 11 APPEALS AND DISPUTES

CHAPTER 11 APPEALS AND DISPUTES In this Chapter look for... 11. General 11.1 Deleted 11.2 Administrative Appeals 11.3 Disputes 11.4 Alternative Dispute Resolution (ADR) 11. General. The Virginia Public

CHAPTER 11 APPEALS AND DISPUTES In this Chapter look for... 11. General 11.1 Deleted 11.2 Administrative Appeals 11.3 Disputes 11.4 Alternative Dispute Resolution (ADR) 11. General. The Virginia Public

NOTICE OF PENDING CLASS ACTION AND PROPOSED SETTLEMENT

Karen Washington v. Key Health Medical Solutions Inc. NOTICE OF PENDING CLASS ACTION AND PROPOSED SETTLEMENT READ THIS NOTICE FULLY AND CAREFULLY; THE PROPOSED SETTLEMENT MAY AFFECT YOUR RIGHTS! IF YOU

Karen Washington v. Key Health Medical Solutions Inc. NOTICE OF PENDING CLASS ACTION AND PROPOSED SETTLEMENT READ THIS NOTICE FULLY AND CAREFULLY; THE PROPOSED SETTLEMENT MAY AFFECT YOUR RIGHTS! IF YOU

All Western Mortgage, Inc., Las Vegas, NV

OFFICE OF AUDIT REGION 9 LOS ANGELES, CA All Western Mortgage, Inc., Las Vegas, NV FHA Loan Origination 2013-LA-1005 MAY 22, 2013 Issue Date: May 22, 2013 Audit Report Number: 2013-LA-1005 TO: Charles

OFFICE OF AUDIT REGION 9 LOS ANGELES, CA All Western Mortgage, Inc., Las Vegas, NV FHA Loan Origination 2013-LA-1005 MAY 22, 2013 Issue Date: May 22, 2013 Audit Report Number: 2013-LA-1005 TO: Charles

Charles S. Coulter, Deputy Assistant Secretary for Single Family Housing, HU

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF INSPECTOR GENERAL MEMORANDUM NO: 2013-LA-0801 October 3, 2012 MEMORANDUM FOR: Charles S. Coulter, Deputy Assistant Secretary for Single Family

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF INSPECTOR GENERAL MEMORANDUM NO: 2013-LA-0801 October 3, 2012 MEMORANDUM FOR: Charles S. Coulter, Deputy Assistant Secretary for Single Family

To: All Vendors, Agents and Contractors of Hutchinson Regional Medical Center

To: All Vendors, Agents and Contractors of Hutchinson Regional Medical Center From: Corporate Compliance Department Re: Deficit Reduction Act of 2005 Dear Vendor/Agent/Contractor: Under the Deficit Reduction

To: All Vendors, Agents and Contractors of Hutchinson Regional Medical Center From: Corporate Compliance Department Re: Deficit Reduction Act of 2005 Dear Vendor/Agent/Contractor: Under the Deficit Reduction

CORPORATE INTEGRITY AGREEMENT I. PREAMBLE

CORPORATE INTEGRITY AGREEMENT BETWEEN THE OFFICE OF INSPECTOR GENERAL OF THE DEPARTMENT OF HEALTH AND HUMAN SERVICES AND MAXIM HEALTHCARE SERVICES, INC. I. PREAMBLE Maxim Healthcare Services, Inc. (Maxim)

CORPORATE INTEGRITY AGREEMENT BETWEEN THE OFFICE OF INSPECTOR GENERAL OF THE DEPARTMENT OF HEALTH AND HUMAN SERVICES AND MAXIM HEALTHCARE SERVICES, INC. I. PREAMBLE Maxim Healthcare Services, Inc. (Maxim)

DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs Need Improvement

Report No. DODIG-2015-068 I nspec tor Ge ne ral U.S. Department of Defense JA N UA RY 1 4, 2 0 1 5 DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs

Report No. DODIG-2015-068 I nspec tor Ge ne ral U.S. Department of Defense JA N UA RY 1 4, 2 0 1 5 DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs

Charles S. Coulter, Deputy Assistant Secretary for Single Family Housing, HU

Issue Date February 6, 2012 Audit Report Number 2012-NY-1006 TO: Charles S. Coulter, Deputy Assistant Secretary for Single Family Housing, HU FROM: SUBJECT: Edgar Moore, Regional Inspector General for

Issue Date February 6, 2012 Audit Report Number 2012-NY-1006 TO: Charles S. Coulter, Deputy Assistant Secretary for Single Family Housing, HU FROM: SUBJECT: Edgar Moore, Regional Inspector General for

OIG/GSA Exclusion Review Policy HS 9006

OIG/GSA EXCLUSION REVIEW PURPOSE: Federal law prohibits entities that participate in federal health care programs (including Medicare, Medicaid, and other governmental programs), such as UCLA Healthcare,

OIG/GSA EXCLUSION REVIEW PURPOSE: Federal law prohibits entities that participate in federal health care programs (including Medicare, Medicaid, and other governmental programs), such as UCLA Healthcare,

ELMWOOD NEIGHBORHOOD ASSOCIATION V. CITY OF BERKELEY ALAMEDA COUNTY SUPERIOR COURT CASE NO. RG14722983 MUTUAL RELEASE AND SETTLEMENT AGREEMENT

ELMWOOD NEIGHBORHOOD ASSOCIATION V. CITY OF BERKELEY ALAMEDA COUNTY SUPERIOR COURT CASE NO. RG14722983 MUTUAL This Release and Settlement Agreement ("AGREEMENT") is entered into by and between Defendant

ELMWOOD NEIGHBORHOOD ASSOCIATION V. CITY OF BERKELEY ALAMEDA COUNTY SUPERIOR COURT CASE NO. RG14722983 MUTUAL This Release and Settlement Agreement ("AGREEMENT") is entered into by and between Defendant

Case 3:06-cv-00701-MJR-DGW Document 526 Filed 07/20/15 Page 1 of 8 Page ID #13631 IN THE UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF ILLINOIS

Case 3:06-cv-00701-MJR-DGW Document 526 Filed 07/20/15 Page 1 of 8 Page ID #13631 IN THE UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF ILLINOIS ANTHONY ABBOTT, et al., ) ) No: 06-701-MJR-DGW Plaintiffs,

Case 3:06-cv-00701-MJR-DGW Document 526 Filed 07/20/15 Page 1 of 8 Page ID #13631 IN THE UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF ILLINOIS ANTHONY ABBOTT, et al., ) ) No: 06-701-MJR-DGW Plaintiffs,

AN ACT IN THE COUNCIL OF THE DISTRICT OF COLUMBIA

AN ACT IN THE COUNCIL OF THE DISTRICT OF COLUMBIA To amend the District of Columbia Procurement Practices Act of 1985 to make the District s false claims act consistent with federal law and thereby qualify

AN ACT IN THE COUNCIL OF THE DISTRICT OF COLUMBIA To amend the District of Columbia Procurement Practices Act of 1985 to make the District s false claims act consistent with federal law and thereby qualify

This policy applies to UNTHSC employees, volunteers, contractors and agents.

Policies of the University of North Texas Health Science Center 3.102 Detecting and Responding to Fraud, Waste and Abuse Chapter 3 Compliance Policy Statement UNTHSC developed and implemented a Compliance

Policies of the University of North Texas Health Science Center 3.102 Detecting and Responding to Fraud, Waste and Abuse Chapter 3 Compliance Policy Statement UNTHSC developed and implemented a Compliance

OFFICE OF AUDIT REGION 6 FORT WORTH, TX. State of Texas Austin, TX. State Community Development Block Grant Disaster Recovery Program

OFFICE OF AUDIT REGION 6 FORT WORTH, TX State of Texas Austin, TX State Community Development Block Grant Disaster Recovery Program 2014-FW-1004 July 15, 2014 Issue Date: July 15, 2014 Audit Report Number:

OFFICE OF AUDIT REGION 6 FORT WORTH, TX State of Texas Austin, TX State Community Development Block Grant Disaster Recovery Program 2014-FW-1004 July 15, 2014 Issue Date: July 15, 2014 Audit Report Number:

Detecting, Preventing, and Reporting FRAUD

U.S. Department of Housing and Urban Development Office of Inspector General Office of Investigation Detecting, Preventing, and Reporting FRAUD Guidelines for Public Housing Authorities to Take Charge

U.S. Department of Housing and Urban Development Office of Inspector General Office of Investigation Detecting, Preventing, and Reporting FRAUD Guidelines for Public Housing Authorities to Take Charge

Maryland Health Benefit Exchange

Audit Report Maryland Health Benefit Exchange October 2015 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning this report contact:

Audit Report Maryland Health Benefit Exchange October 2015 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning this report contact:

ADMINISTRATION POLICY MEMORANDUM

ADMINISTRATION POLICY MEMORANDUM POLICY TITLE: FRAUD AND ABUSE POLICY NUMBER: JCAHO FUNCTION AREA: POLICY APPLICABLE TO: POLICY EFFECTIVE DATE: POLICY REVIEWED: MCH-1083 Leadership All Employees January

ADMINISTRATION POLICY MEMORANDUM POLICY TITLE: FRAUD AND ABUSE POLICY NUMBER: JCAHO FUNCTION AREA: POLICY APPLICABLE TO: POLICY EFFECTIVE DATE: POLICY REVIEWED: MCH-1083 Leadership All Employees January

The Alabama Department of Economic and Community Affairs, Montgomery, AL

The Alabama Department of Economic and Community Affairs, Montgomery, AL Community Development Block Grant Disaster Recovery Funds Office of Audit, Region 4 Atlanta, GA Audit Report Number: 2015-AT-1010

The Alabama Department of Economic and Community Affairs, Montgomery, AL Community Development Block Grant Disaster Recovery Funds Office of Audit, Region 4 Atlanta, GA Audit Report Number: 2015-AT-1010

U.S. ELECTION ASSISTANCE COMMISSION OFFICE OF INSPECTOR GENERAL FINAL REPORT USE OF APPROPRIATED FUNDS TO SETTLE A CLAIM

U.S. ELECTION ASSISTANCE COMMISSION OFFICE OF INSPECTOR GENERAL FINAL REPORT USE OF APPROPRIATED FUNDS TO SETTLE A CLAIM EVALUATION REPORT NO. I-EV-EAC-01-10 SEPTEMBER 2010 U.S. ELECTION ASSISTANCE COMMISSION

U.S. ELECTION ASSISTANCE COMMISSION OFFICE OF INSPECTOR GENERAL FINAL REPORT USE OF APPROPRIATED FUNDS TO SETTLE A CLAIM EVALUATION REPORT NO. I-EV-EAC-01-10 SEPTEMBER 2010 U.S. ELECTION ASSISTANCE COMMISSION

United States Department of Agriculture. OFFICE OF INSPECTOR GENERAl

United States Department of Agriculture OFFICE OF INSPECTOR GENERAl Review of Expenditures Made by the Office of the Assistant Secretary for Civil Rights 50099-0001-12 September 2015 10401-0001-22 Review

United States Department of Agriculture OFFICE OF INSPECTOR GENERAl Review of Expenditures Made by the Office of the Assistant Secretary for Civil Rights 50099-0001-12 September 2015 10401-0001-22 Review

55144-1-5 Page: 1 of 5. Pharmacy Fraud, Waste and Abuse Policy. 1.0 Compliance Assurance. 2.0 Procedure

Pharmacy Fraud, Waste and Abuse Policy 1.0 Compliance Assurance This Fraud Waste and Abuse Policy ( Policy ) reiterates the commitment of this pharmacy to comply with the standards of conduct established

Pharmacy Fraud, Waste and Abuse Policy 1.0 Compliance Assurance This Fraud Waste and Abuse Policy ( Policy ) reiterates the commitment of this pharmacy to comply with the standards of conduct established

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY OFFICE OF THE COMPTROLLER OF THE CURRENCY ) ) ) ) ) ) ) ) ) ) ) ) STIPULATION AND CONSENT ORDER

) ) ) ) ) ) ) ) ) ) ) STIPULATION AND CONSENT ORDER") UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY OFFICE OF THE COMPTROLLER OF THE CURRENCY #2005-12 In the Matter of: Chicago Title Insurance Company Settlement Agent for: Whitney National Bank New

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY OFFICE OF THE COMPTROLLER OF THE CURRENCY #2005-12 In the Matter of: Chicago Title Insurance Company Settlement Agent for: Whitney National Bank New

(LABOR HOUSING LOAN AND GRANT TO A NONPROFIT CORPORATION)

") Form RD 3560-41 ` FORM APPROVED (02-05) OMB NO 0575-0189 (LABOR HOUSING LOAN AND GRANT TO A NONPROFIT CORPORATION) LOAN AND GRANT RESOLUTION OF, 20 RESOLUTION OF THE BOARD OF DIRECTORS OF PROVIDING FOR

Form RD 3560-41 ` FORM APPROVED (02-05) OMB NO 0575-0189 (LABOR HOUSING LOAN AND GRANT TO A NONPROFIT CORPORATION) LOAN AND GRANT RESOLUTION OF, 20 RESOLUTION OF THE BOARD OF DIRECTORS OF PROVIDING FOR

INSTITUTIONAL COMPLIANCE PLAN

INSTITUTIONAL COMPLIANCE PLAN Responsible Party: Board of Trustees Contact: Institutional Compliance Office Original Effective Date: 02/16/2012 Last Revised Date: 10/13/2014 Contents I. SCOPE OF THE PLAN...

INSTITUTIONAL COMPLIANCE PLAN Responsible Party: Board of Trustees Contact: Institutional Compliance Office Original Effective Date: 02/16/2012 Last Revised Date: 10/13/2014 Contents I. SCOPE OF THE PLAN...

Department of Defense INSTRUCTION

Department of Defense INSTRUCTION NUMBER 7640.02 April 15, 2015 IG DoD SUBJECT: Policy for Follow-Up on Contract Audit Reports References: See Enclosure 1 1. PURPOSE. This instruction reissues DoD Instruction

Department of Defense INSTRUCTION NUMBER 7640.02 April 15, 2015 IG DoD SUBJECT: Policy for Follow-Up on Contract Audit Reports References: See Enclosure 1 1. PURPOSE. This instruction reissues DoD Instruction

SCAN Health Plan Policy and Procedure Number: CRP-0067, False Claims Act & Deficit Reduction Act 2005

Health Plan Policy and Procedure Number: CRP-0067, False Claims Act & Deficit Reduction Act 2005 Approver Approval Stage Date Chris Zorn Approval Event (Authoring) 12/09/2013 Nancy Monk Approval Event

Health Plan Policy and Procedure Number: CRP-0067, False Claims Act & Deficit Reduction Act 2005 Approver Approval Stage Date Chris Zorn Approval Event (Authoring) 12/09/2013 Nancy Monk Approval Event

In total, Massachusetts overstated its Medicaid claim for reimbursement by $5,312,447 (Federal share).

.") Page 2 Wynethea Walker In total, Massachusetts overstated its Medicaid claim for reimbursement by $5,312,447 (Federal share). Massachusetts did not provide specific guidance to local education agencies

Page 2 Wynethea Walker In total, Massachusetts overstated its Medicaid claim for reimbursement by $5,312,447 (Federal share). Massachusetts did not provide specific guidance to local education agencies

PITTSBURGH CARE PARTNERSHIP, INC. COMMUNITY LIFE PROGRAM POLICY AND PROCEDURE MANUAL. False Claims Act Explanation and Reporting Requirements

SUBJECT: False Claims Act Explanation and Reporting Requirements NUMBER: 1004 CROSS REFERENCE NUMBER: 1823 REG. REF.: 31 U.S.C. 37-29 PURPOSE: POLICY: The purposes of this policy are to describe the Federal

SUBJECT: False Claims Act Explanation and Reporting Requirements NUMBER: 1004 CROSS REFERENCE NUMBER: 1823 REG. REF.: 31 U.S.C. 37-29 PURPOSE: POLICY: The purposes of this policy are to describe the Federal

Department of Homeland Security Office of the Inspector General. Office of Emergency Management Oversight. Audit Division- Eastern District

Department of Homeland Security Office of the Inspector General Office of Emergency Management Oversight Audit Division- Eastern District Introduction The Department of Homeland Security (DHS), Office

Department of Homeland Security Office of the Inspector General Office of Emergency Management Oversight Audit Division- Eastern District Introduction The Department of Homeland Security (DHS), Office

Frank L. Davis, General Deputy Assistant Secretary for Housing, H. //signed// Ronald J. Hosking, Regional Inspector General for Audit, 7AGA

Issue Date May 13, 2005 Audit Report Number 2005-KC-1006 TO: FROM: Frank L. Davis, General Deputy Assistant Secretary for Housing, H //signed// Ronald J. Hosking, Regional Inspector General for Audit,

Issue Date May 13, 2005 Audit Report Number 2005-KC-1006 TO: FROM: Frank L. Davis, General Deputy Assistant Secretary for Housing, H //signed// Ronald J. Hosking, Regional Inspector General for Audit,

PHI Air Medical, L.L.C. Compliance Plan

Page No. 1 of 13 Introduction: The PHI Air Medical, L.L.C. is to be used by employees, contractors and vendors to get a high level understanding of the key regulatory requirements relating to our participation

Page No. 1 of 13 Introduction: The PHI Air Medical, L.L.C. is to be used by employees, contractors and vendors to get a high level understanding of the key regulatory requirements relating to our participation

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF INSPECTOR GENERAL

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF INSPECTOR GENERAL April 18, 2013 MEMORANDUM NO: 2013-LA-1803 Memorandum TO: Charles S. Coulter Deputy Assistant Secretary for Single Family Housing,

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT OFFICE OF INSPECTOR GENERAL April 18, 2013 MEMORANDUM NO: 2013-LA-1803 Memorandum TO: Charles S. Coulter Deputy Assistant Secretary for Single Family Housing,

The City of Atlanta, Georgia, Effectively Managed FEMA Public Assistance Grant Funds Awarded for Severe Storms and Flooding in September 2009

The City of Atlanta, Georgia, Effectively Managed FEMA Public Assistance Grant Funds Awarded for Severe Storms and Flooding in September 2009 May 19, 2015 DHS OIG HIGHLIGHTS The City of Atlanta, Georgia,

The City of Atlanta, Georgia, Effectively Managed FEMA Public Assistance Grant Funds Awarded for Severe Storms and Flooding in September 2009 May 19, 2015 DHS OIG HIGHLIGHTS The City of Atlanta, Georgia,

SHO #08-004. October 28, 2008. Dear State Health Official:

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop S2-26-12 Baltimore, Maryland 21244-1850 Center for Medicaid and State Operations SHO #08-004

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop S2-26-12 Baltimore, Maryland 21244-1850 Center for Medicaid and State Operations SHO #08-004

NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED ON BEHALF OF THE COMMUNITY ACTION PARTNERSHIP OF NATRONA COUNTY FOR

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED ON BEHALF OF THE COMMUNITY ACTION PARTNERSHIP OF NATRONA COUNTY FOR

Project Management Procedures

1201 Main Street, Suite 1600 Columbia, South Carolina 29201 Project Management Procedures Start Up The grant becomes effective upon return of one copy of the grant award executed by the Chief Executive

1201 Main Street, Suite 1600 Columbia, South Carolina 29201 Project Management Procedures Start Up The grant becomes effective upon return of one copy of the grant award executed by the Chief Executive

Avoiding Medicaid Fraud. Odyssey House of Utah Questions? Contact your Program Director or Emily Capito, Director of Operations

Avoiding Medicaid Fraud Odyssey House of Utah Questions? Contact your Program Director or Emily Capito, Director of Operations MEDICAID FRAUD OVERVIEW Medicaid Fraud The Medicaid Program provides medical

Avoiding Medicaid Fraud Odyssey House of Utah Questions? Contact your Program Director or Emily Capito, Director of Operations MEDICAID FRAUD OVERVIEW Medicaid Fraud The Medicaid Program provides medical

Request for Quotes Small Purchase (Hourly Rate Pricing) Accounting Services

Accounting Services") Request for Quotes Small Purchase (Hourly Rate Pricing) Accounting Services I. Instructions Upland Housing Authority (UHA) is seeking price quotations from qualified individuals or organizations to provide

Request for Quotes Small Purchase (Hourly Rate Pricing) Accounting Services I. Instructions Upland Housing Authority (UHA) is seeking price quotations from qualified individuals or organizations to provide

Memo. Professional Accounts, LLC. Corporate Compliance Program

Professional Accounts, LLC Memo To: All Employees and Vendors From: Lee Frans, Executive Director Date: April 2, 2012 Re: Corporate Compliance Program Our mission as an organization has been to deliver

Professional Accounts, LLC Memo To: All Employees and Vendors From: Lee Frans, Executive Director Date: April 2, 2012 Re: Corporate Compliance Program Our mission as an organization has been to deliver

Fraud, Waste and Abuse: Compliance Program. Section 4: National Provider Network Handbook

Fraud, Waste and Abuse: Compliance Program Section 4: National Provider Network Handbook December 2015 2 Our Philosophy Magellan takes provider fraud, waste and abuse We engage in considerable efforts

Fraud, Waste and Abuse: Compliance Program Section 4: National Provider Network Handbook December 2015 2 Our Philosophy Magellan takes provider fraud, waste and abuse We engage in considerable efforts

Reports of Compliance Concerns and Violations

The University of Chicago Medical Center Compliance Manual (UCHHS;BSD;UCPP) Reports of Compliance Concerns and Violations Issued: November 1, 1999 Reports of Compliance Concerns and Violations Revised:

The University of Chicago Medical Center Compliance Manual (UCHHS;BSD;UCPP) Reports of Compliance Concerns and Violations Issued: November 1, 1999 Reports of Compliance Concerns and Violations Revised:

September 2008 Report No. AUD-08-016. Controls Over Contractor Payments for Relocation Services AUDIT REPORT

September 2008 Report No. AUD-08-016 Controls Over Contractor Payments for Relocation Services AUDIT REPORT Report No. AUD-08-016 September 2008 Controls Over Contractor Payments for Relocation Services

September 2008 Report No. AUD-08-016 Controls Over Contractor Payments for Relocation Services AUDIT REPORT Report No. AUD-08-016 September 2008 Controls Over Contractor Payments for Relocation Services

Napa County, California, Needs Additional Technical Assistance and Monitoring to Ensure Compliance with Federal Regulations

Napa County, California, Needs Additional Technical Assistance and Monitoring to Ensure Compliance with Federal Regulations OIG-15-135-D August 28, 2015 August 28, 2015 Why We Did This On August 24, 2014,

Napa County, California, Needs Additional Technical Assistance and Monitoring to Ensure Compliance with Federal Regulations OIG-15-135-D August 28, 2015 August 28, 2015 Why We Did This On August 24, 2014,

Policies and Procedures: WVUPC Policy Pursuant to the Requirements of the Deficit Reduction Act of 2005

POLICY/PROCEDURE NO.: B-17 Effective date: Jan. 1, 2007 Date(s) of review/revision: Nov. 1, 2015 Policies and Procedures: WVUPC Policy Pursuant to the Requirements of the Deficit Reduction Act of 2005

POLICY/PROCEDURE NO.: B-17 Effective date: Jan. 1, 2007 Date(s) of review/revision: Nov. 1, 2015 Policies and Procedures: WVUPC Policy Pursuant to the Requirements of the Deficit Reduction Act of 2005

REGISTRATION ELIGIBLITY DISPUTE RESOLUTION POLICY

REGISTRATION ELIGIBLITY DISPUTE RESOLUTION POLICY 1.0 Title: Registration Eligibility Dispute Resolution Policy Version Control: 1.0 Date of Implementation: 2015-03-16 2.0 Summary This Registration Eligibility

REGISTRATION ELIGIBLITY DISPUTE RESOLUTION POLICY 1.0 Title: Registration Eligibility Dispute Resolution Policy Version Control: 1.0 Date of Implementation: 2015-03-16 2.0 Summary This Registration Eligibility

Final. National Health Care Billing Audit Guidelines. as amended by. The American Association of Medical Audit Specialists (AAMAS)

") Final National Health Care Billing Audit Guidelines as amended by The American Association of Medical Audit Specialists (AAMAS) May 1, 2009 Preface Billing audits serve as a check and balance to help ensure

Final National Health Care Billing Audit Guidelines as amended by The American Association of Medical Audit Specialists (AAMAS) May 1, 2009 Preface Billing audits serve as a check and balance to help ensure

NOTICE OF PROPOSED SETTLEMENT OF CLASS ACTION LAWSUIT

NOTICE OF PROPOSED SETTLEMENT OF CLASS ACTION LAWSUIT ATTENTION: All people with disabilities, as defined by the Americans with Disabilities Act, who are within the City of Los Angeles and the jurisdiction

NOTICE OF PROPOSED SETTLEMENT OF CLASS ACTION LAWSUIT ATTENTION: All people with disabilities, as defined by the Americans with Disabilities Act, who are within the City of Los Angeles and the jurisdiction

2IÀFHRI,QVSHFWRU*HQHUDO

2IÀFHRI,QVSHFWRU*HQHUDO FEMA Should Recover $8.0 Million of $26.6 Million in Public Assistance Grant Funds Awarded to St. Stanislaus College Preparatory in Mississippi Hurricane Katrina OIG-14-95-D May

2IÀFHRI,QVSHFWRU*HQHUDO FEMA Should Recover $8.0 Million of $26.6 Million in Public Assistance Grant Funds Awarded to St. Stanislaus College Preparatory in Mississippi Hurricane Katrina OIG-14-95-D May

Standards of. Conduct. Important Phone Number for Reporting Violations

Standards of Conduct It is the policy of Security Health Plan that all its business be conducted honestly, ethically, and with integrity. Security Health Plan s relationships with members, hospitals, clinics,

Standards of Conduct It is the policy of Security Health Plan that all its business be conducted honestly, ethically, and with integrity. Security Health Plan s relationships with members, hospitals, clinics,