Measuring the Impact of Financial Crisis on International Markets: An Application of the Financial Stress Index

|

|

|

- Lucas Joseph Randall

- 8 years ago

- Views:

Transcription

1 Measuring the Impact of Financial Crisis on International Markets: An Application of the Financial Stress Index Apostolos G. Christopoulos University of Athens, Department of Economics 5 Stadiou str., 10562, Athens, Greece axristop@econ.uoa.gr John Mylonakis 10 Nikiforou str., Glyfada, 16675, Athens, Greece imylonakis@vodafone.net.gr Christos Koromilas B Padodos Leeikon 10, Kalamata, Greece Chriskoromilas@yahoo.gr Received: March 1, 2011 Accepted: March 25, 2011 doi: /res.v3n1p22 Abstract The scope of paper is to examine whether the recent financial crisis has had any impact on international capital markets and more precisely on the 4 primary international stock markets of England, France, Japan, the United States and Greece. The research is based on the use of the Financial Stress Index (FSI) from July 2005 until December 2008 and August Research results showed that the recent financial crisis has had a negative impact on all examined markets, with the Tokyo stock exchange being the one mostly affected. It was, also, found increased variability of performances following the start of the financial crisis, a fact that is indicative of the presence of conditional heteroscedasticity. As far as the Greek market is concerned, the recent financial crisis has not affected in general the credit expansion towards enterprises and households; however, it has affected the credit expansion to enterprises and households on a case-to-case basis. Keywords: Financial crisis, Financial stress index, International stock exchanges, Capital market 1. Introduction As is widely known, the recent financial crisis was initially manifested in the US real estate market in August 2007 (Reinhart & Rogoff, 2008) and had as primary causes the drop of interest rates, the broad expansion of high-risk housing loans (subprime lending), the transfer of credit risk from the banks balance statements to investors through securitisation (Ephraim & Kassimatis, 2004) and the strong demand in terms of hedge funds for securitisation bonds (Petroff, 2008, Boston, 2007). The purpose of this paper is to investigate the impact of the recent financial crisis on the 4 primary international stock markets of England, France, Japan, the United States, as well as, on the Greek market. To this purpose, it is initially attempted to measure the impact on the four primary stock markets and the Greek Stock Exchange. 2. The Financial Stress Index In order for a disturbing financial incident to be regarded as an event of financial crisis, Illing and Liu (2006) have suggested the use of a Financial Stress Index (FSI), the values of which would mark the coming of a financial crisis when exceeding certain limits (Cardarelli et all, 2004). The FSI in each country is produced as the mean of the following indices: 22

2 Three indices that relate to the Banking System: the first is the beta index of the banking stocks (the beta index of banking stocks measures the covariance between the total returns of the banking sector index and the general capital market index); the second is the spread between interbank interest rates and the performance of Treasury Bills (namely the so-called TED spread that measures the premium charged by banking institutions in addition to the T-Bill interest rates); the third is the direction coefficient of the banking sector performance curve. Three indices that relate to the entire securities market: Firstly, the spreads of corporate bonds, secondly, the performance of the capital market and thirdly, the volatility of the capital market performance against time. One index that involves the foreign exchange market: The volatility of foreign exchange rates against time. The FSI index is the mean of the above seven indices. In order to calculate this mean index, each of the above seven individual indices is awarded a statistical weight, which is the reverse of the variance of each respective index; this aims at reducing the impact of the most volatile of the seven constituent indices on the resulting value of the FSI index (Longin, 2000). 3. Research Methodology In order to evaluate the effect of the financial crisis on international money markets, it is attempted to evaluate the following model using dummy variables (Illing & Liu (2006), Green, 2000). y d (1.1) t 0 t t Where y t : is the performance of the Stock Index during montht. d : Is a dummy variable which is characterised by: t It is therefore supposed that the "key date for our analysis is the month August of 2009, when the crisis started manifesting itself. The conditional mean of the above econometric model is as follows: 0 0 E y d (1.2) 1 0 E y d (1.3) From the above two equations it becomes evident that in the econometric model (1.1), the 0 factor represents the mean value of the Stock Index prior to the manifestation of the financial crisis, while the result of 0 indicates the mean value of the above index after the manifestation of the crisis. Therefore, the factor records the difference between the Stock Index mean value before and after the manifestation of the crisis. If the above factor is statistically important, it is then ascertained whether the crisis manifestation has had a positive or negative impact (depending on the positive or negative sign of the ˆ estimate) on the Stock Index. Then it is examined the zero hypothesis H : 0 0, which indicates that the manifestation of the financial crisis has zero impact on the Stock Index - against the alternative hypothesis of H : 0 1, which Published by Canadian Center of Science and Education 23

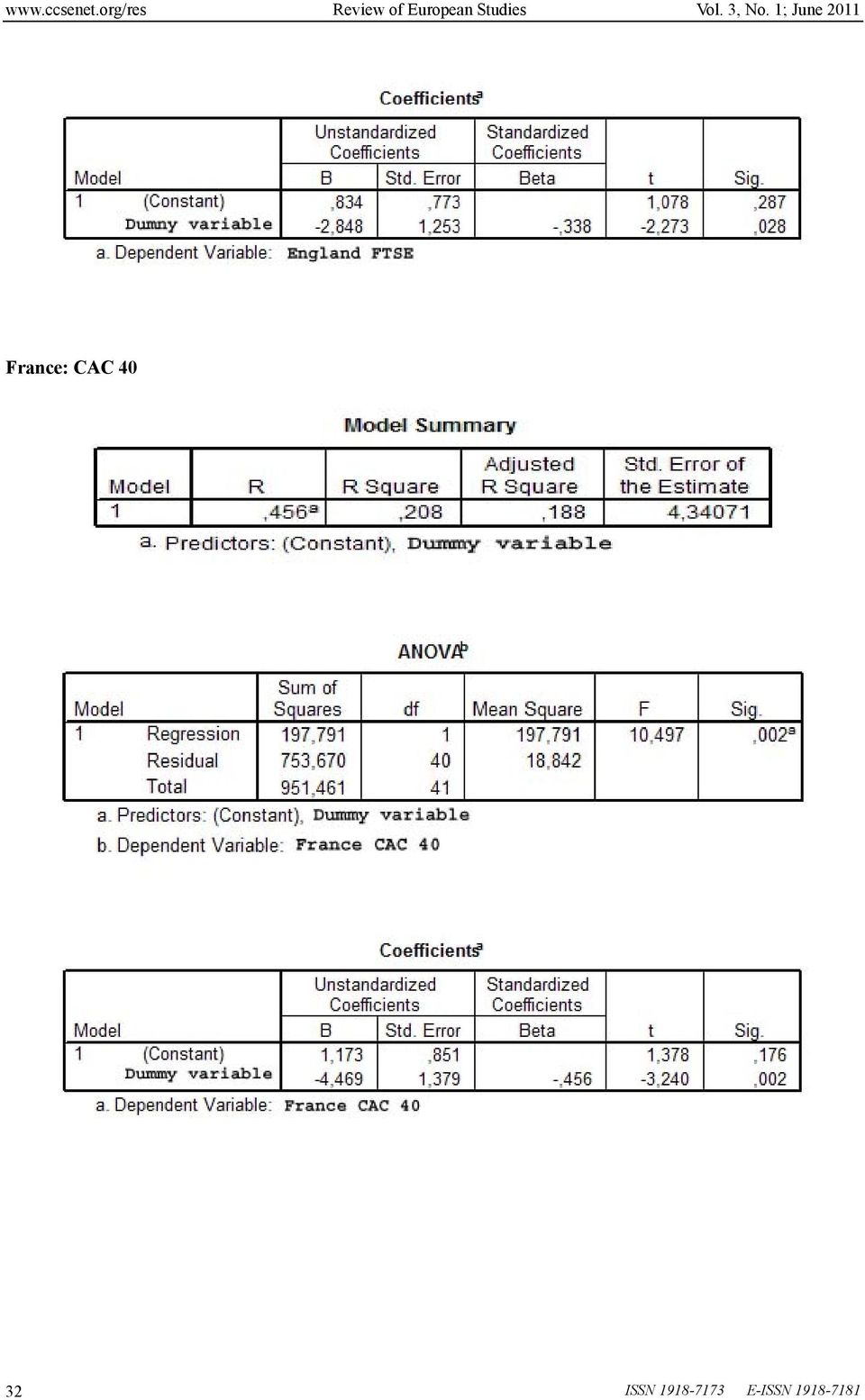

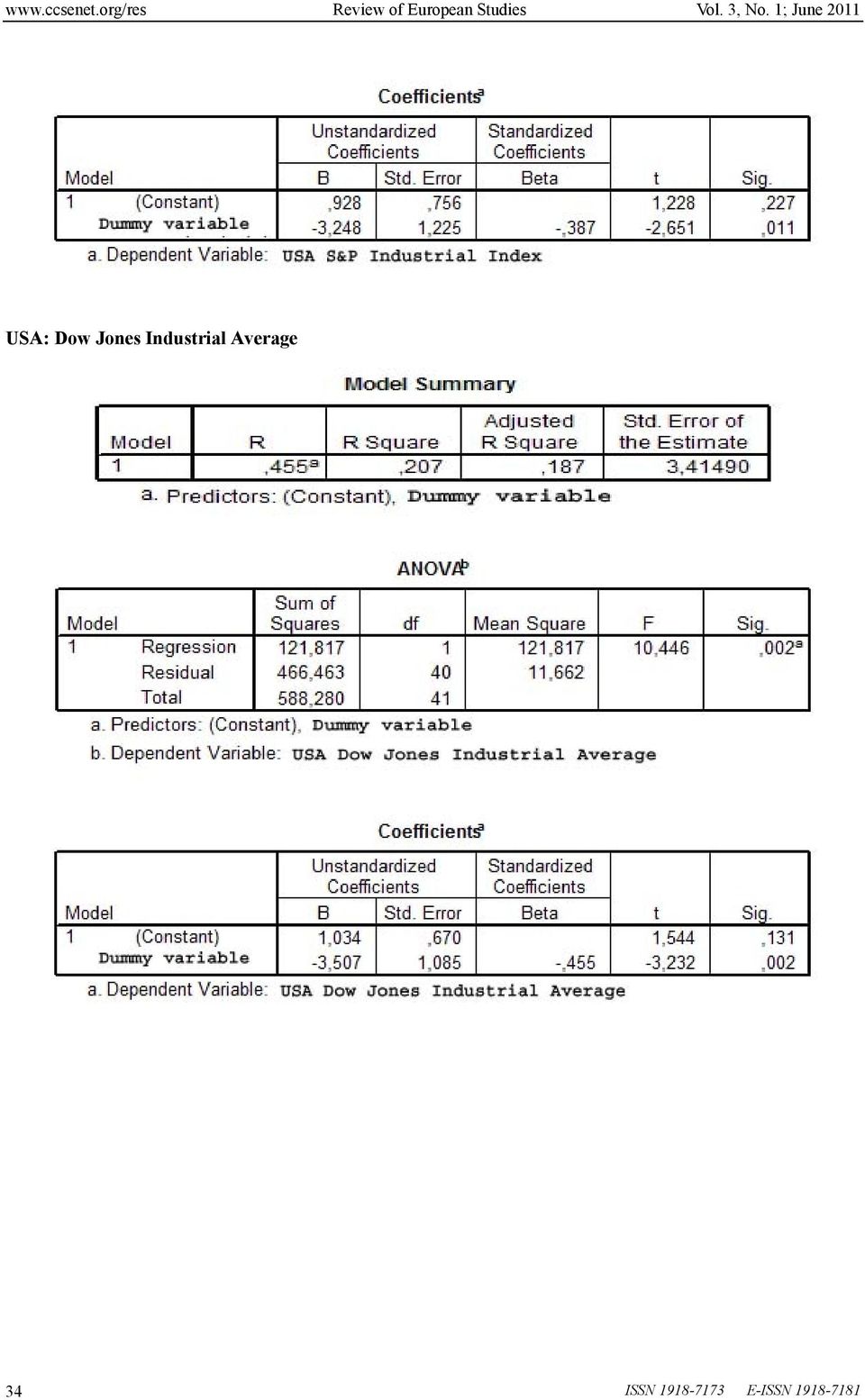

3 indicates that the manifestation of the financial crisis has some impact, either positive or negative, on the Stock Index. The data used for this analysis have been drawn from the database of the Naftemporiki economic newspaper and involve the performance of the four main stock indices: a) the English FTSE, b) the French CAC 40, c) the Japanese Nikkei 225, and d) the USA Dow Jones Industrial Average. 4. Research Results 4.1 The impact of the crisis on international capital markets Based on the above econometric model, it is attempted to examine whether the recent financial crisis has had any impact on international capital markets. It is assumed that the "key date for our analysis is the month August of 2009, when the crisis started manifesting itself. The time period before the manifestation of the crisis ends in July 2005, while the time period after the crisis ends in December Based on the above time limits, the results from the evaluation of the econometric model (Annex) are shown in the Table 1. The data presented in the Table 1 clearly show that the recent financial crisis has had a negative impact on all examined markets, with the Tokyo stock exchange being the one mostly affected. More specifically, prior to the start of the crisis, the average monthly performance of the Nikkei 225 index was 1.47%, while after the crisis the same was decreased by 4.97 %. France followed the same pattern, as its CAC 40 average monthly performance prior to the start of the crisis was 1.1%, while after the crisis the same was reduced by 4.47 percentage points. The least affected was the London index. Diagram 1 illustrates the progress of performances across time, as well as, the FTSE closing prices starting from July 2005 until December The Diagram 1 shows increased variability of performances following the start of the financial crisis, a fact that is indicative of the presence of conditional heteroscedasticity. Namely, the variability of the FTSE Stock Index performances changes depending on the time period examined. More specifically, it is observed that the variability is greater during the time of market decline in the period of 2007: :12 and lower during the time of rising markets. Table 2 examines certain results of descriptive statistics with regard to the previous index. During the rising market phase, the average monthly performance of the FTSE Stock Index was 0.903% with a standard deviation (variability) of 2.28%. However, during the declining market phase, the variability of performances of the FTSE Stock Index has more than doubled reaching 5.55%. Similar events have, also, been recorded with the remaining three Stock Indices. 4.2 The impact of the crisis on the credit expansion of Greek Credit Institutions The profitability of a financial institution is directly associated with the size (and the quality) of its lending portfolio, since a bank profits from the margin between its (average) lending and borrowing interest rates. Therefore, the ratio of its loans to its total assets is indicative of a bank s credit expansion. Since 2003, there has been significant increase in the activities of Greek banking institutions, with their loans accounting for almost half of their total activities (Diagram 5). The question is whether the recent financial crisis has affected the credit expansion of domestic banking institutions. The answer to that question comes through the estimate of the econometric model used. The results of such estimate are presented in Table 3. Table 3 data clearly shows that the recent financial crisis has not affected in general the credit expansion towards enterprises and households; however, it has affected the credit expansion to enterprises and households on a case-to-case basis. More specifically, prior to the start of the financial crisis, the average loans to enterprises as a percentage of the total assets of domestic credit institutions were 26.96%; the same percentage after the manifestation of the crisis was reduced by 3.28%. To the contrary, as far as households are concerned, prior to the start of the crisis the average loans to households were 22.82% of the total assets of credit institutions; the same percentage after the manifestation of the crisis was increased by 3.11%. Indeed, the crisis has neither reduced housing credit nor consumer credit. Diagram 6 shows the progress of housing and consumer credit as a percentage of the assets of domestic credit institutions. From the econometric model used, it emerges that the average housing and consumer credit values as a percentage of the total assets of domestic credit institutions were 15.06% and 7.14%, respectively; the same percentages after the manifestation of the crisis increased by 2.19% for housing credit and 0.89% for consumer credit. As evidenced, what the crisis created was in fact a delay in the (average monthly) rate of growth of credit expansion (Table 4). 24

4 Even though lending constitutes the primary activity of banking institutions, it cannot be regarded as a reliable source of liquidity for banks. On the other hand, banking institutions, the assets of which contain a generous number of short-term securities find themselves in a more favourable state when compared with banking institutions the assets of which are dominated by loans, even if such loans have been issued in the most prudent manner (Georgiadis, 2005). Those opposing to the above allegations assert that what is important in loan approval is not the liquidity loss it entails for the bank (usually due to long-term nature), but rather the financial ability of the borrower to repay his liabilities towards the bank in due time The impact of the crisis on the interest rates of Greek banks Domestic interest rates prior to the accession of Greece to the Euro Zone had a steadily declining course. Diagram 7 illustrates the historical progress of the lending weighted average interest rate to households during the period (Lekkos, 2006), in the three countries with the highest respective interest rates (Greece, France and Portugal), as well as, the EU-10 average. As shown in Diagram 7, during the period prior to the accession of Greece to the Euro Zone, the lending interest rates of Greek banks were significantly higher than the European average (by approximately six percentage points). After that, the accession of Greece to the Euro Zone in 2001 resulted in a severe decline of lending interest rates, which by the end of 2004 were higher than the European average by approximately 1.25%. Diagram 8 shows the historical progress of consumer credit interest rates from January 2003 until January In order to examine whether the recent financial crisis has affected domestic consumer credit interest rates, an assessment is performed using the main econometric model used based on the above scheme. The data of Table 6 show that the recent financial crisis has not affected consumer credit interest rates. Only credit card interest rates have presented a statistically significant, yet only slight increase of 97 baseline points. Therefore, the Greek banking sector continues to aim at gaining profits from the great margin that exists between lending and borrowing interest rates (Diagram 9). As emerges from the Diagram 9, the margin between lending and borrowing interest rates, namely the interest rate margin, is higher in Greece as compared with the Euro Zone equivalent by 1.17%. According to Malliaropoulos (2006), such difference in interest rate profit margins may be attributed to Greece s higher inflation rates as compared with the countries of the Euro Zone. 5. Conclusions One of the main reasons of the recent financial crisis was the increasing use of loan securitisation, a practice that has already started since the 1980s and has enabled banking institutions to significantly loosen their financing criteria, due to the fact they can transfer the credit risks entailed in lending via securitisation (Goodhart, 2006). Based on this process, financial institutions sell claims to customers (i.e. loans), namely to Special Purpose Vehicles, companies which issue bonds commonly known as asset backed securities (ABS), which they later sell to investors (Driffill et all, 2006). However, the practice of securitisation has gained great significance during the latest years, resulting in the issue of CDO bonds, (collaterised debt obligations), which are based on ABS bonds, namely the initial bonds issued as part of the securitisation practice. However, CDOs, also known as toxic bonds, were not usually the subect of negotiations in secondary markets and that is why prices not always existed for these. Moreover, the assessment of the credit capacity of toxic bond issuers (namely the CDOs) was not always accurate. The buyers of ABS and CDO bonds received their interest coupon on a periodical basis, the payment of which depended on cash flows produced by securitised loans (Tully, 2007a,b). When borrowers of securitised housing loans in the United States became unable to repay their obligations, CDO buyers found themselves in a position where they held bonds with extremely low rating. The owners of such bonds included certain banks (as well as subsidiaries of bank s that were awarded guarantees for buying securities), which became subsequently exposed to serious problems both in terms of solvency (as the losses from such bonds needed to be recorded) and liquidity (owed to their subsidiaries). This has created conditions of uncertainty in the market, as it was not known from the beginning (summer of 2007) which banking institutions had problems or the extent of such problems. As a result, interest rates of the interbank market started in turn to rise (Baur & Niels, 2008). This survey has shown that the financial crisis has had no effect on the overall credit expansion of Greek banking institutions towards enterprises and households. Yet, on an individual basis, the crisis has resulted in a decline in bank loans issued to enterprises as a percentage of the total assets of domestic credit institutions by 328 baseline Published by Canadian Center of Science and Education 25

, but rather the financial")

5 units. With regard to the increase in household lending, it was found that the average housing credit as a percentage of the total assets of domestic credit institutions increased from 15.06% by 2.19%, while consumer credit increased to a lesser extent from 7.14% by 89 baseline points. As a result, the financial crisis has had an indirect impact on the Greek economy by increasing the cost of money due to the reluctance of banks to lend one another. This cost also affects the cost of lending both for individual and corporate customers. References Baur, D. G., Schulze, N. (2009). Financial market stability - A test. Journal of International Financial Markets, Institutions & Money, Issue 3, Boston, W. (2007). Which Way Out? Time, November 12, Cardarelli, R., Elekdag, S. & Lall S. (2010). Financial stress and economic contractions. Journal of Financial Stability, Elsevier, forthcoming. Driffill, J., Rotondi Z., Savona, P. & Zazzara, C. (2006). Monetary policy and financial stability: What role for the futures market?. Journal of Financial Stability, Vol. 2, Ephraim, C. & Kassimatis, K. (2004). Country financial risk and stock market performance: the case of Latin America. Journal of Economics and Business, Vol. 56, Georgiadis, N. (2006). The Trend of Economic Figures of Large Commercial Banks during the 2 nd semester Investment Research & Analysis Journal, September. Goodhart, C.A.E. (2006). A framework for assessing financial stability?. Journal of Banking & Finance, Vol. 30, Green, W. (2000). Econometric Analysis, 4 th ed. Prentice Hall International, Inc, Illing, Μ and Liu, Y. (2006). Measuring Financial Stress in a Developed Country: An Application to Canada. Journal of Financial Stability, Vol. 2, pp International Monetary Fund, IMF. (2009). Global Financial Stability Report. Chapter 1, October, 5. Lekkos, I. (2006). The margins between Loans and Deposits in Greece and Eurozone. Economy and Markets, EFG Eurobank, Division of Research and Forecasting, February 21, 1-5. Longin, F. M. (2000). From value at risk to stress testing: The extreme value approach. Journal of Banking & Finance, Vol. 24, Issue 7, Malliaropoulos, D. (2006). Bank Interest rates and Inflation: do Greek banks debit interests at higher rates?. EFG Eurobank, Division of Research and Forecasting, February 21, pp Petroff, E. (2008). Who is to Blame for the Subprime Crisis? [Online] Available: Reinhart, C. & Rogoff, K. (2008). Is the 2007 U.S. Sub-Prime Financial Crisis So Different? An International Historical Comparison. NBER Working Paper No Tully, S. (2007a). Why the Private equity pubble is bursting? Fortune. Tully, S. (2007b). Wall Street s Money Machine Breaks Down. Fortune, November. 26

. Financial market stability - A test.")

6 Table 1. Results of the impact of the crisis on international capital markets Stock Index 0, t / se.. FTSE CAC Nikkei S& P Industrial Index Dow Jones Industrial Average Table 2. The impact of conditional heteroscedasticity on the performances of the FTSE Stock Index Rising market 2005: :07 Declining market 2007: :12 Average monthly performance (%) Median monthly performance (%) Maximum monthly performance (%) Minimum monthly performance (%) Standard deviation of monthly performance (%) Table 3. The results on the impact of the crisis on the credit expansion towards enterprises and households Accounting element 0, t / se.. Loans to enterprises and households Loans to enterprises Loans to households Source: Bank of Greece, following data processing Table 4. Results on the impact of the crisis on housing and consumer credit Accounting element 0, t / se.. Housing Credit Consumer Credit , Source: Bank of Greece, following data processing Table 5. The Monthly Rate of Growth of Credit AVERAGE MONTHLY RATE OF GROWTH Time Period Housing Loans Consumer Loans Loans to Enterprises Loans to Enterprises and Households Before the crisis (2003: :08) 2.03% 2.04% 0.82% 1.36% After the crisis (2007: :01) 0.71% 0.59% 0.81% 0.73% Source: Bank of Greece, following data processing Published by Canadian Center of Science and Education 27

1.630-0.890 Maximum monthly performance (%) 3.610 6.760 Minimum monthly performance (%) -4.970-13.020 Standard deviation of monthly performance (%) 2.288 5.")

7 Table 6. Results of the crisis' impact on domestic consumer credit interest rates Consumer Credit Interest Rate 0, t / se.. Credit Cards Loans up to 1 year Loans 1-5 years Loans over 5 years Source: Bank of Greece, following data processing Diagram 1. The progress and performance of the FTSE Stock Index (England) in the 2005 period: : 12 Diagram 2. The progress and performance of the CAC 40 Stock Index (France) in the 2005 period: : 12 28

in the 2005 period: 07-2008: 12 Diagram 2.")

in the 2005 period: 07-2008: 12 Diagram 5.")

8 Diagram 3. The progress and performance of the Nikkei 225 Stock Index (Japan) in the 2005 period: : 12 Diagram 4. The progress and performance of the S& P Industrial Stock Index (USA) in the 2005 period: : 12 Diagram 5. Loans to households and enterprises issued by domestic credit institutions (2003: :01) Source: Bank of Greece, following data processing Published by Canadian Center of Science and Education 29

Source: Bank of Greece, following data processing")

9 Diagram 6. Housing and Consumer Credit (2003: :01) Source: Bank of Greece, following data processing Source: Bank of Greece Diagram 8. Consumer Credit Interest Rates, 2003: :01 30

10 Diagram 9. Interest Rate Margin in Greece and the Euro Zone September 2005 Source: EFG Eurobank (2006) Annex Evaluation results on the impact of the crisis on international capital markets UK: FTSE Published by Canadian Center of Science and Education 31

11 France: CAC 40 32

12 Japan: Nikkei 225 USA: S&P Industrial Index Published by Canadian Center of Science and Education 33

13 USA: Dow Jones Industrial Average 34

Introduction to Investments FINAN 3050

Introduction to Investments FINAN 3050 : Introduction (Syllabus) Investments Background and Issues (Chapter 1) Financial Securities (Chapter 2) Syllabus General Information The course is going to be organized

Introduction to Investments FINAN 3050 : Introduction (Syllabus) Investments Background and Issues (Chapter 1) Financial Securities (Chapter 2) Syllabus General Information The course is going to be organized

CHAPTER 2. Asset Classes. the Money Market. Money market instruments. Capital market instruments. Asset Classes and Financial Instruments

2-2 Asset Classes Money market instruments CHAPTER 2 Capital market instruments Asset Classes and Financial Instruments Bonds Equity Securities Derivative Securities The Money Market 2-3 Table 2.1 Major

2-2 Asset Classes Money market instruments CHAPTER 2 Capital market instruments Asset Classes and Financial Instruments Bonds Equity Securities Derivative Securities The Money Market 2-3 Table 2.1 Major

Research. What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields?

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

CHAPTER 12 CHAPTER 12 FOREIGN EXCHANGE

CHAPTER 12 CHAPTER 12 FOREIGN EXCHANGE CHAPTER OVERVIEW This chapter discusses the nature and operation of the foreign exchange market. The chapter begins by describing the foreign exchange market and

CHAPTER 12 CHAPTER 12 FOREIGN EXCHANGE CHAPTER OVERVIEW This chapter discusses the nature and operation of the foreign exchange market. The chapter begins by describing the foreign exchange market and

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

How To Invest In Stocks And Bonds

Review for Exam 1 Instructions: Please read carefully The exam will have 21 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Review for Exam 1 Instructions: Please read carefully The exam will have 21 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Bank Liabilities Survey. Survey results 2013 Q3

Bank Liabilities Survey Survey results 13 Q3 Bank Liabilities Survey 13 Q3 Developments in banks balance sheets are of key interest to the Bank of England in its assessment of economic conditions. Changes

Bank Liabilities Survey Survey results 13 Q3 Bank Liabilities Survey 13 Q3 Developments in banks balance sheets are of key interest to the Bank of England in its assessment of economic conditions. Changes

Financial Instruments. Chapter 2

Financial Instruments Chapter 2 Major Types of Securities debt money market instruments bonds common stock preferred stock derivative securities 1-2 Markets and Instruments Money Market debt instruments

Financial Instruments Chapter 2 Major Types of Securities debt money market instruments bonds common stock preferred stock derivative securities 1-2 Markets and Instruments Money Market debt instruments

Market Linked Certificates of Deposit

Market Linked Certificates of Deposit This material was prepared by Wells Fargo Securities, LLC, a registered brokerdealer and separate non-bank affiliate of Wells Fargo & Company. This material is not

Market Linked Certificates of Deposit This material was prepared by Wells Fargo Securities, LLC, a registered brokerdealer and separate non-bank affiliate of Wells Fargo & Company. This material is not

FACTORS AFFECTING THE LOAN SUPPLY OF BANKS

FACTORS AFFECTING THE LOAN SUPPLY OF BANKS Funding resources The liabilities of banks operating in Estonia mainly consist of non-financial sector deposits, which totalled almost 11 billion euros as at

FACTORS AFFECTING THE LOAN SUPPLY OF BANKS Funding resources The liabilities of banks operating in Estonia mainly consist of non-financial sector deposits, which totalled almost 11 billion euros as at

Theories of Exchange rate determination

Theories of Exchange rate determination INTRODUCTION By definition, the Foreign Exchange Market is a market 1 in which different currencies can be exchanged at a specific rate called the foreign exchange

Theories of Exchange rate determination INTRODUCTION By definition, the Foreign Exchange Market is a market 1 in which different currencies can be exchanged at a specific rate called the foreign exchange

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007 IPP Policy Briefs n 10 June 2014 Guillaume Bazot www.ipp.eu Summary Finance played an increasing

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007 IPP Policy Briefs n 10 June 2014 Guillaume Bazot www.ipp.eu Summary Finance played an increasing

INSTITUTIONAL INVESTORS, THE EQUITY MARKET AND FORCED INDEBTEDNESS

INSTITUTIONAL INVESTORS, THE EQUITY MARKET AND FORCED INDEBTEDNESS Jan Toporowski Economics Department The School of Oriental and African Studies University of London Published in in S. Dullien, E. Hein,

INSTITUTIONAL INVESTORS, THE EQUITY MARKET AND FORCED INDEBTEDNESS Jan Toporowski Economics Department The School of Oriental and African Studies University of London Published in in S. Dullien, E. Hein,

Econ 330 Exam 1 Name ID Section Number

Econ 330 Exam 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If during the past decade the average rate of monetary growth

Econ 330 Exam 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If during the past decade the average rate of monetary growth

Rigensis Bank AS Information on the Characteristics of Financial Instruments and the Risks Connected with Financial Instruments

Rigensis Bank AS Information on the Characteristics of Financial Instruments and the Risks Connected with Financial Instruments Contents 1. Risks connected with the type of financial instrument... 2 Credit

Rigensis Bank AS Information on the Characteristics of Financial Instruments and the Risks Connected with Financial Instruments Contents 1. Risks connected with the type of financial instrument... 2 Credit

How do CFDs work? CFD trading is similar to traditional share dealing, with a few exceptions.

What is a CFD? A CFD is an agreement to exchange the difference between the opening and closing prices of the share, index or commodity between the time at which a contract is opened and the time at which

What is a CFD? A CFD is an agreement to exchange the difference between the opening and closing prices of the share, index or commodity between the time at which a contract is opened and the time at which

I. Introduction. II. Financial Markets (Direct Finance) A. How the Financial Market Works. B. The Debt Market (Bond Market)

A. How the Financial Market Works. B. The Debt Market (Bond Market)") University of California, Merced EC 121-Money and Banking Chapter 2 Lecture otes Professor Jason Lee I. Introduction In economics, investment is defined as an increase in the capital stock. This is important

University of California, Merced EC 121-Money and Banking Chapter 2 Lecture otes Professor Jason Lee I. Introduction In economics, investment is defined as an increase in the capital stock. This is important

Specifics of national debt management and its consequences for the Ukrainian economy

Anatoliy Yepifanov (Ukraine), Vyacheslav Plastun (Ukraine) Specifics of national debt management and its consequences for the Ukrainian economy Abstract This article is about the specifics of the national

Anatoliy Yepifanov (Ukraine), Vyacheslav Plastun (Ukraine) Specifics of national debt management and its consequences for the Ukrainian economy Abstract This article is about the specifics of the national

Consolidated Quarterly Report of Baader Bank AG as at 31.03.2015

Consolidated Quarterly Report of Baader Bank AG as at 31.03.2015 OVERVIEW OF KEY FIGURES RESULTS OF OPERATIONS Q1 2015 Q1 2014 Change in % Net interest income EUR thousand -95 869 >-100.0 Current income

Consolidated Quarterly Report of Baader Bank AG as at 31.03.2015 OVERVIEW OF KEY FIGURES RESULTS OF OPERATIONS Q1 2015 Q1 2014 Change in % Net interest income EUR thousand -95 869 >-100.0 Current income

An Alternative Way to Diversify an Income Strategy

Senior Secured Loans An Alternative Way to Diversify an Income Strategy Alternative Thinking Series There is no shortage of uncertainty and risk facing today s investor. From high unemployment and depressed

Senior Secured Loans An Alternative Way to Diversify an Income Strategy Alternative Thinking Series There is no shortage of uncertainty and risk facing today s investor. From high unemployment and depressed

Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market

Communications P.O. Box, CH-8022 Zurich Telephone +41 44 631 31 11 Fax +41 44 631 39 10 Zurich, 13 September 2007 Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market The

Communications P.O. Box, CH-8022 Zurich Telephone +41 44 631 31 11 Fax +41 44 631 39 10 Zurich, 13 September 2007 Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market The

1. a. (iv) b. (ii) [6.75/(1.34) = 10.2] c. (i) Writing a call entails unlimited potential losses as the stock price rises.

![1. a. (iv) b. (ii) [6.75/(1.34) = 10.2] c. (i) Writing a call entails unlimited potential losses as the stock price rises.](/thumbs/39/20115486.jpg "1. a. (iv) b. (ii) [6.75/(1.34) = 10.2] c. (i) Writing a call entails unlimited potential losses as the stock price rises.") 1. Solutions to PS 1: 1. a. (iv) b. (ii) [6.75/(1.34) = 10.2] c. (i) Writing a call entails unlimited potential losses as the stock price rises. 7. The bill has a maturity of one-half year, and an annualized

1. Solutions to PS 1: 1. a. (iv) b. (ii) [6.75/(1.34) = 10.2] c. (i) Writing a call entails unlimited potential losses as the stock price rises. 7. The bill has a maturity of one-half year, and an annualized

Econ 202 Section H01 Midterm 2

, Spring 2010 March 16, 2010 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section H01 Midterm 2 Multiple Choice. 2.5 points each. 1. What would

, Spring 2010 March 16, 2010 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section H01 Midterm 2 Multiple Choice. 2.5 points each. 1. What would

Transact Guide to Investment Risks

Integrated Financial Arrangements plc Transact Guide to Investment Risks Integrated Financial Arrangements plc A firm authorised and regulated by the Financial Conduct Authority INTRODUCTION Transact operates

Integrated Financial Arrangements plc Transact Guide to Investment Risks Integrated Financial Arrangements plc A firm authorised and regulated by the Financial Conduct Authority INTRODUCTION Transact operates

Use of fixed income products within a company's portfolio

Theoretical and Applied Economics Volume XIX (2012), No. 10(575), pp. 5-14 Use of fixed income products within a company's portfolio Vasile DEDU The Bucharest University of Economic Studies vdedu03@yahoo.com

Theoretical and Applied Economics Volume XIX (2012), No. 10(575), pp. 5-14 Use of fixed income products within a company's portfolio Vasile DEDU The Bucharest University of Economic Studies vdedu03@yahoo.com

Answers to Review Questions

Answers to Review Questions 1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for investment funds. The nominal rate of interest is the actual

Answers to Review Questions 1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for investment funds. The nominal rate of interest is the actual

Futures Price d,f $ 0.65 = (1.05) (1.04)

(1.04)") 24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

funds KEY This is an important document. Please keep it safe for future reference.

SELECT PORTFOLIO bond (wealth managers) funds KEY FEATURES. This is an important document. Please keep it safe for future reference. SELECT PORTFOLIO BOND (wealth managers) FUNDS KEY FEATURES 2 WHAT ARE

SELECT PORTFOLIO bond (wealth managers) funds KEY FEATURES. This is an important document. Please keep it safe for future reference. SELECT PORTFOLIO BOND (wealth managers) FUNDS KEY FEATURES 2 WHAT ARE

FIXED INCOME INSTRUMENTS IN THE CAPITAL MARKET IN ROMANIA

FIXED INCOME INSTRUMENTS IN THE CAPITAL MARKET IN ROMANIA CIPRIAN ALEXANDRU Abstract The presence of government bonds on the Bucharest Stock Exchange has changed the behavior of institutional investors

FIXED INCOME INSTRUMENTS IN THE CAPITAL MARKET IN ROMANIA CIPRIAN ALEXANDRU Abstract The presence of government bonds on the Bucharest Stock Exchange has changed the behavior of institutional investors

Lecture 12/13 Bond Pricing and the Term Structure of Interest Rates

1 Lecture 1/13 Bond Pricing and the Term Structure of Interest Rates Alexander K. Koch Department of Economics, Royal Holloway, University of London January 14 and 1, 008 In addition to learning the material

1 Lecture 1/13 Bond Pricing and the Term Structure of Interest Rates Alexander K. Koch Department of Economics, Royal Holloway, University of London January 14 and 1, 008 In addition to learning the material

High interest rates have contributed to a stronger currency

Financial markets and Central Bank measures: 1 High interest rates have contributed to a stronger currency The króna has appreciated after the extension of the exchange rate band and the Central Bank s

Financial markets and Central Bank measures: 1 High interest rates have contributed to a stronger currency The króna has appreciated after the extension of the exchange rate band and the Central Bank s

SAMPLE MID-TERM QUESTIONS

SAMPLE MID-TERM QUESTIONS William L. Silber HOW TO PREPARE FOR THE MID- TERM: 1. Study in a group 2. Review the concept questions in the Before and After book 3. When you review the questions listed below,

SAMPLE MID-TERM QUESTIONS William L. Silber HOW TO PREPARE FOR THE MID- TERM: 1. Study in a group 2. Review the concept questions in the Before and After book 3. When you review the questions listed below,

Saving and Investing. Chapter 11 Section Main Menu

Saving and Investing How does investing contribute to the free enterprise system? How does the financial system bring together savers and borrowers? How do financial intermediaries link savers and borrowers?

Saving and Investing How does investing contribute to the free enterprise system? How does the financial system bring together savers and borrowers? How do financial intermediaries link savers and borrowers?

Individual Savings Account Fund menu

Individual Savings Account Fund menu This fund menu lists all the funds available on our Individual Savings Account (ISA). Your financial adviser will be able to help you choose the right combination of

Individual Savings Account Fund menu This fund menu lists all the funds available on our Individual Savings Account (ISA). Your financial adviser will be able to help you choose the right combination of

1 Regional Bank Regional banks specialize in consumer and commercial products within one region of a country, such as a state or within a group of states. A regional bank is smaller than a bank that operates

1 Regional Bank Regional banks specialize in consumer and commercial products within one region of a country, such as a state or within a group of states. A regional bank is smaller than a bank that operates

INVESTMENT DICTIONARY

INVESTMENT DICTIONARY Annual Report An annual report is a document that offers information about the company s activities and operations and contains financial details, cash flow statement, profit and

INVESTMENT DICTIONARY Annual Report An annual report is a document that offers information about the company s activities and operations and contains financial details, cash flow statement, profit and

Web. Chapter FINANCIAL INSTITUTIONS AND MARKETS

FINANCIAL INSTITUTIONS AND MARKETS T Chapter Summary Chapter Web he Web Chapter provides an overview of the various financial institutions and markets that serve managers of firms and investors who invest

FINANCIAL INSTITUTIONS AND MARKETS T Chapter Summary Chapter Web he Web Chapter provides an overview of the various financial institutions and markets that serve managers of firms and investors who invest

Proposed regulatory framework for haircuts on securities financing transactions

Proposed regulatory framework for haircuts on securities financing transactions Instructions for the Quantitative Impact Study (QIS2) for Regulated Financial Intermediaries (Banks and Broker-Dealers) 5

Proposed regulatory framework for haircuts on securities financing transactions Instructions for the Quantitative Impact Study (QIS2) for Regulated Financial Intermediaries (Banks and Broker-Dealers) 5

CHAPTER 22: FUTURES MARKETS

CHAPTER 22: FUTURES MARKETS PROBLEM SETS 1. There is little hedging or speculative demand for cement futures, since cement prices are fairly stable and predictable. The trading activity necessary to support

CHAPTER 22: FUTURES MARKETS PROBLEM SETS 1. There is little hedging or speculative demand for cement futures, since cement prices are fairly stable and predictable. The trading activity necessary to support

HSBC Mutual Funds. Simplified Prospectus June 15, 2016

HSBC Mutual Funds Simplified Prospectus June 15, 2016 Offering Investor Series, Advisor Series, Premium Series, Manager Series and Institutional Series units of the following Funds: Cash and Money Market

HSBC Mutual Funds Simplified Prospectus June 15, 2016 Offering Investor Series, Advisor Series, Premium Series, Manager Series and Institutional Series units of the following Funds: Cash and Money Market

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT PROBLEM SETS 1. In formulating a hedge position, a stock s beta and a bond s duration are used similarly to determine the expected percentage gain or loss

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT PROBLEM SETS 1. In formulating a hedge position, a stock s beta and a bond s duration are used similarly to determine the expected percentage gain or loss

Friends Life Online Stakeholder Pension Fund guide

Friends Life Online Stakeholder Pension Fund guide This guide describes the funds available for investment under our Friends Life Online Stakeholder Pension and sets out their aims. Which funds can I choose

Friends Life Online Stakeholder Pension Fund guide This guide describes the funds available for investment under our Friends Life Online Stakeholder Pension and sets out their aims. Which funds can I choose

Fund guide. Prudence Bond Prudence Managed Investment Bond

Fund guide Prudence Bond Prudence Managed Investment Bond Introduction to this guide We know that choosing which fund may be best for you isn t easy there are many options and everyone is different so

Fund guide Prudence Bond Prudence Managed Investment Bond Introduction to this guide We know that choosing which fund may be best for you isn t easy there are many options and everyone is different so

Chapter 3 - Selecting Investments in a Global Market

Chapter 3 - Selecting Investments in a Global Market Questions to be answered: Why should investors have a global perspective regarding their investments? What has happened to the relative size of U.S.

Chapter 3 - Selecting Investments in a Global Market Questions to be answered: Why should investors have a global perspective regarding their investments? What has happened to the relative size of U.S.

Fixed Income Portfolio Management. Interest rate sensitivity, duration, and convexity

Fixed Income ortfolio Management Interest rate sensitivity, duration, and convexity assive bond portfolio management Active bond portfolio management Interest rate swaps 1 Interest rate sensitivity, duration,

Fixed Income ortfolio Management Interest rate sensitivity, duration, and convexity assive bond portfolio management Active bond portfolio management Interest rate swaps 1 Interest rate sensitivity, duration,

Investment Bond. Funds key features. This is an important document. Please keep it safe for future reference.

Investment Bond Funds key features. This is an important document. Please keep it safe for future reference. 2 WHAT ARE THE FUNDS KEY FEATURES? This document is part of the information we provide you to

Investment Bond Funds key features. This is an important document. Please keep it safe for future reference. 2 WHAT ARE THE FUNDS KEY FEATURES? This document is part of the information we provide you to

U.S. Treasury Securities

U.S. Treasury Securities U.S. Treasury Securities 4.6 Nonmarketable To help finance its operations, the U.S. government from time to time borrows money by selling investors a variety of debt securities

U.S. Treasury Securities U.S. Treasury Securities 4.6 Nonmarketable To help finance its operations, the U.S. government from time to time borrows money by selling investors a variety of debt securities

CHAPTER 11 INTRODUCTION TO SECURITY VALUATION TRUE/FALSE QUESTIONS

1 CHAPTER 11 INTRODUCTION TO SECURITY VALUATION TRUE/FALSE QUESTIONS (f) 1 The three step valuation process consists of 1) analysis of alternative economies and markets, 2) analysis of alternative industries

1 CHAPTER 11 INTRODUCTION TO SECURITY VALUATION TRUE/FALSE QUESTIONS (f) 1 The three step valuation process consists of 1) analysis of alternative economies and markets, 2) analysis of alternative industries

1. Definition of cash components

Opinion n 2015-06 of 3 July 2015 relating to Central Government Accounting Standard 10 Cash Components On 3 July 2015 the Public Sector Accounting Standards Council adopted this Opinion relating to Central

Opinion n 2015-06 of 3 July 2015 relating to Central Government Accounting Standard 10 Cash Components On 3 July 2015 the Public Sector Accounting Standards Council adopted this Opinion relating to Central

Fund descriptions, their charges and risk warnings

Fund descriptions, their charges and risk warnings This document was produced in March 2015 and is accurate at that date. When reviewing your fund choices you should refer to up-to-date information, available

Fund descriptions, their charges and risk warnings This document was produced in March 2015 and is accurate at that date. When reviewing your fund choices you should refer to up-to-date information, available

44 ECB STOCK MARKET DEVELOPMENTS IN THE LIGHT OF THE CURRENT LOW-YIELD ENVIRONMENT

Box STOCK MARKET DEVELOPMENTS IN THE LIGHT OF THE CURRENT LOW-YIELD ENVIRONMENT Stock market developments are important for the formulation of monetary policy for several reasons. First, changes in stock

Box STOCK MARKET DEVELOPMENTS IN THE LIGHT OF THE CURRENT LOW-YIELD ENVIRONMENT Stock market developments are important for the formulation of monetary policy for several reasons. First, changes in stock

The Business Credit Index

The Business Credit Index April 8 Published by the Credit Management Research Centre, Leeds University Business School April 8 1 April 8 THE BUSINESS CREDIT INDEX During the last ten years the Credit Management

The Business Credit Index April 8 Published by the Credit Management Research Centre, Leeds University Business School April 8 1 April 8 THE BUSINESS CREDIT INDEX During the last ten years the Credit Management

FACULTY OF COMMERCE DEPARTMENT OF FINANCE BACHELOR OF COMMERCE HONOURS DEGREE IN FINANCE PART IV

FACULTY OF COMMERCE DEPARTMENT OF FINANCE BACHELOR OF COMMERCE HONOURS DEGREE IN FINANCE PART IV 2 nd SEMESTER FINAL EXAMINATION MAY 2012 INTERNATIONAL FINANCE II [CFI 4202] TIME ALLOWED: 3 HOURS INSTRUCTIONS

FACULTY OF COMMERCE DEPARTMENT OF FINANCE BACHELOR OF COMMERCE HONOURS DEGREE IN FINANCE PART IV 2 nd SEMESTER FINAL EXAMINATION MAY 2012 INTERNATIONAL FINANCE II [CFI 4202] TIME ALLOWED: 3 HOURS INSTRUCTIONS

Monetary and Financial Trends First Quarter 2011. Table of Contents

Financial Stability Directorate Monetary and Financial Trends First Quarter 2011 Table of Contents Highlights... 1 1. Monetary Aggregates... 3 2. Credit Developments... 4 3. Interest Rates... 7 4. Domestic

Financial Stability Directorate Monetary and Financial Trends First Quarter 2011 Table of Contents Highlights... 1 1. Monetary Aggregates... 3 2. Credit Developments... 4 3. Interest Rates... 7 4. Domestic

CHAPTER 15 INTERNATIONAL PORTFOLIO INVESTMENT SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 15 INTERNATIONAL PORTFOLIO INVESTMENT SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. What factors are responsible for the recent surge in international portfolio

CHAPTER 15 INTERNATIONAL PORTFOLIO INVESTMENT SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. What factors are responsible for the recent surge in international portfolio

Q3/2010 Interim report as of September 30, 2010

Q3/2010 Interim report as of September 30, 2010 Overview of key figures 01.01.-30.09.2010 01.01.-30.09.2009 Change in % Net fee and commission income EUR million 25,89 27,03-4,2 Net trading income EUR

Q3/2010 Interim report as of September 30, 2010 Overview of key figures 01.01.-30.09.2010 01.01.-30.09.2009 Change in % Net fee and commission income EUR million 25,89 27,03-4,2 Net trading income EUR

15.433 Investments. Assignment 1: Securities, Markets & Capital Market Theory. Each question is worth 0.2 points, the max points is 3 points

Assignment 1: Securities, Markets & Capital Market Theory Each question is worth 0.2 points, the max points is 3 points 1. The interest rate charged by banks with excess reserves at a Federal Reserve Bank

Assignment 1: Securities, Markets & Capital Market Theory Each question is worth 0.2 points, the max points is 3 points 1. The interest rate charged by banks with excess reserves at a Federal Reserve Bank

Commercial paper collateralized by a pool of loans, leases, receivables, or structured credit products. Asset-backed commercial paper (ABCP)

") GLOSSARY Asset-backed commercial paper (ABCP) Asset-backed security (ABS) Asset-backed securities index (ABX) Basel II Call (put) option Carry trade Collateralized debt obligation (CDO) Collateralized

GLOSSARY Asset-backed commercial paper (ABCP) Asset-backed security (ABS) Asset-backed securities index (ABX) Basel II Call (put) option Carry trade Collateralized debt obligation (CDO) Collateralized

PROFESSIONAL FIXED-INCOME MANAGEMENT

MARCH 2014 PROFESSIONAL FIXED-INCOME MANAGEMENT A Strategy for Changing Markets EXECUTIVE SUMMARY The bond market has evolved in the past 30 years and become increasingly complex and volatile. Many investors

MARCH 2014 PROFESSIONAL FIXED-INCOME MANAGEMENT A Strategy for Changing Markets EXECUTIVE SUMMARY The bond market has evolved in the past 30 years and become increasingly complex and volatile. Many investors

RISK FACTORS AND RISK MANAGEMENT

Bangkok Bank Public Company Limited 044 RISK FACTORS AND RISK MANAGEMENT Bangkok Bank recognizes that effective risk management is fundamental to good banking practice. Accordingly, the Bank has established

Bangkok Bank Public Company Limited 044 RISK FACTORS AND RISK MANAGEMENT Bangkok Bank recognizes that effective risk management is fundamental to good banking practice. Accordingly, the Bank has established

Chapter 12. Page 1. Bonds: Analysis and Strategy. Learning Objectives. INVESTMENTS: Analysis and Management Second Canadian Edition

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 12 Bonds: Analysis and Strategy Learning Objectives Explain why investors buy bonds. Discuss major considerations

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 12 Bonds: Analysis and Strategy Learning Objectives Explain why investors buy bonds. Discuss major considerations

4. FINANCIAL POSITION AND RISK EXPOSURE OF HOUSEHOLDS AND BUSINESSES

4. FINANCIAL POSITION AND RISK EXPOSURE OF HOUSEHOLDS AND BUSINESSES In 215 H1, households remained oriented towards savings, as shown by the expansion in deposits level. Lending to households expanded

4. FINANCIAL POSITION AND RISK EXPOSURE OF HOUSEHOLDS AND BUSINESSES In 215 H1, households remained oriented towards savings, as shown by the expansion in deposits level. Lending to households expanded

Paper F9. Financial Management. Fundamentals Pilot Paper Skills module. The Association of Chartered Certified Accountants

Fundamentals Pilot Paper Skills module Financial Management Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Do NOT open this paper

Fundamentals Pilot Paper Skills module Financial Management Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Do NOT open this paper

CHAPTER 6 ASSET-LIABILITY MANAGEMENT: DETERMINING AND MEASURING INTEREST RATES AND CONTROLLING INTEREST-SENSITIVE AND DURATION GAPS

CHAPTER 6 ASSET-LIABILITY MANAGEMENT: DETERMINING AND MEASURING INTEREST RATES AND CONTROLLING INTEREST-SENSITIVE AND DURATION GAPS Goals of This Chapter: The purpose of this chapter is to explore the

CHAPTER 6 ASSET-LIABILITY MANAGEMENT: DETERMINING AND MEASURING INTEREST RATES AND CONTROLLING INTEREST-SENSITIVE AND DURATION GAPS Goals of This Chapter: The purpose of this chapter is to explore the

The History of Crisis. Background Information: The Financial Crisis and Fair Value

The History of Crisis What is going on? Privatisation of money supply Financialisation: commodification of money and debt (linked to accounting) Deregulated global flow of capital (but not labour) (linked

The History of Crisis What is going on? Privatisation of money supply Financialisation: commodification of money and debt (linked to accounting) Deregulated global flow of capital (but not labour) (linked

Chapter 2. Practice Problems. MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 2 Practice Problems MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Assume that you borrow $2000 at 10% annual interest to finance a new

Chapter 2 Practice Problems MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Assume that you borrow $2000 at 10% annual interest to finance a new

The Young Investor s Guide To Understanding The Terms Used In Investing.

The Young Investor s Guide To Understanding The Terms Used In Investing. The Young Investor Dictionary compliments of Integrity Mutual Funds. YOUNG INVESTOR DICTIONARY Asset Something of value. The property

The Young Investor s Guide To Understanding The Terms Used In Investing. The Young Investor Dictionary compliments of Integrity Mutual Funds. YOUNG INVESTOR DICTIONARY Asset Something of value. The property

18 ECB STYLISED FACTS OF MONEY AND CREDIT OVER THE BUSINESS CYCLE

Box 1 STYLISED FACTS OF MONEY AND CREDIT OVER THE BUSINESS CYCLE Over the past three decades, the growth rates of MFI loans to the private sector and the narrow monetary aggregate M1 have displayed relatively

Box 1 STYLISED FACTS OF MONEY AND CREDIT OVER THE BUSINESS CYCLE Over the past three decades, the growth rates of MFI loans to the private sector and the narrow monetary aggregate M1 have displayed relatively

The International Certificate in Banking Risk and Regulation (ICBRR)

") The International Certificate in Banking Risk and Regulation (ICBRR) The ICBRR fosters financial risk awareness through thought leadership. To develop best practices in financial Risk Management, the authors

The International Certificate in Banking Risk and Regulation (ICBRR) The ICBRR fosters financial risk awareness through thought leadership. To develop best practices in financial Risk Management, the authors

Course Syllabus For Banking and Financial Management Department

For Banking and Financial Management Department School Year First Year First year Second year Third year Fifth year Fifth year Fifth year Fifth year Name of course Financial Accounting principles Intermediate

For Banking and Financial Management Department School Year First Year First year Second year Third year Fifth year Fifth year Fifth year Fifth year Name of course Financial Accounting principles Intermediate

How To Understand The Risks Of Financial Instruments

NATURE AND SPECIFIC RISKS OF THE MAIN FINANCIAL INSTRUMENTS The present section is intended to communicate to you, in accordance with the Directive, general information on the characteristics of the main

NATURE AND SPECIFIC RISKS OF THE MAIN FINANCIAL INSTRUMENTS The present section is intended to communicate to you, in accordance with the Directive, general information on the characteristics of the main

Close Brothers Close Brothers Finance plc (incorporated with limited liability in England and Wales with registered number 4322721)

") SUPPLEMENTARY PROSPECTUS DATED 9 APRIL Close Brothers Close Brothers Finance plc (incorporated with limited liability in England and Wales with registered number 4322721) 1,000,000,000 Euro Medium Term

SUPPLEMENTARY PROSPECTUS DATED 9 APRIL Close Brothers Close Brothers Finance plc (incorporated with limited liability in England and Wales with registered number 4322721) 1,000,000,000 Euro Medium Term

RISK DISCLOSURE STATEMENT PRODUCT INFORMATION

This statement sets out the risks in trading certain products between Newedge Group ( NEWEDGE ) and the client (the Client ). The Client should note that other risks will apply when trading in emerging

This statement sets out the risks in trading certain products between Newedge Group ( NEWEDGE ) and the client (the Client ). The Client should note that other risks will apply when trading in emerging

DFA INVESTMENT DIMENSIONS GROUP INC.

PROSPECTUS February 28, 2015 Please carefully read the important information it contains before investing. DFA INVESTMENT DIMENSIONS GROUP INC. DFA ONE-YEAR FIXED INCOME PORTFOLIO Ticker: DFIHX DFA TWO-YEAR

PROSPECTUS February 28, 2015 Please carefully read the important information it contains before investing. DFA INVESTMENT DIMENSIONS GROUP INC. DFA ONE-YEAR FIXED INCOME PORTFOLIO Ticker: DFIHX DFA TWO-YEAR

No. 03/11 BATH ECONOMICS RESEARCH PAPERS

Sovereign Credit Default Swaps and the Macroeconomy Yang Liu and Bruce Morley No. 03/11 BATH ECONOMICS RESEARCH PAPERS Department of Economics 1 Sovereign Credit Default Swaps and the Macroeconomy Yang

Sovereign Credit Default Swaps and the Macroeconomy Yang Liu and Bruce Morley No. 03/11 BATH ECONOMICS RESEARCH PAPERS Department of Economics 1 Sovereign Credit Default Swaps and the Macroeconomy Yang

Investing Practice Questions

Investing Practice Questions 1) When interest is calculated only on the principal amount of the investment, it is known as: a) straight interest b) simple interest c) compound interest d) calculated interest

Investing Practice Questions 1) When interest is calculated only on the principal amount of the investment, it is known as: a) straight interest b) simple interest c) compound interest d) calculated interest

THE CDS AND THE GOVERNMENT BONDS MARKETS AFTER THE LAST FINANCIAL CRISIS. The CDS and the Government Bonds Markets after the Last Financial Crisis

THE CDS AND THE GOVERNMENT BONDS MARKETS AFTER THE LAST FINANCIAL CRISIS The CDS and the Government Bonds Markets after the Last Financial Crisis Abstract In the 1990s, the financial market had developed

THE CDS AND THE GOVERNMENT BONDS MARKETS AFTER THE LAST FINANCIAL CRISIS The CDS and the Government Bonds Markets after the Last Financial Crisis Abstract In the 1990s, the financial market had developed

Debt Portfolio Management Quarterly Report

Ministry of Finance Debt and Financial Assets Management Department Debt Portfolio Management Quarterly Report First Half of 2015 17 July 2015 Ministry of Finance Debt Portfolio Management Quarterly Report

Ministry of Finance Debt and Financial Assets Management Department Debt Portfolio Management Quarterly Report First Half of 2015 17 July 2015 Ministry of Finance Debt Portfolio Management Quarterly Report

Consolidated and Non-Consolidated Financial Statements

May 13, 2016 Consolidated and Non-Consolidated Financial Statements (For the Period from April 1, 2015 to March 31, 2016) 1. Summary of Operating Results (Consolidated) (April 1,

May 13, 2016 Consolidated and Non-Consolidated Financial Statements (For the Period from April 1, 2015 to March 31, 2016) 1. Summary of Operating Results (Consolidated) (April 1,

Lecture 16: Financial Crisis

Lecture 16: Financial Crisis What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows in financial markets, with the result that financial

Lecture 16: Financial Crisis What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows in financial markets, with the result that financial

November 2012. Figure 1: New issuance (US$ billion) presents attractive opportunities

presents attractive opportunities") November 2012 Emerging market corporate bonds attractive opportunities in a dynamic sector In a world where traditional fixed income investments, such as core government bonds, offer very low returns to

November 2012 Emerging market corporate bonds attractive opportunities in a dynamic sector In a world where traditional fixed income investments, such as core government bonds, offer very low returns to

[Translation] - 2 - (Millions of Yen) Amount. Account. (Liabilities) Current liabilities 4,655. Short-term loans payable 1,000. Income taxes payable

![[Translation] - 2 - (Millions of Yen) Amount. Account. (Liabilities) Current liabilities 4,655. Short-term loans payable 1,000. Income taxes payable](/thumbs/26/7641733.jpg "[Translation] - 2 - (Millions of Yen) Amount. Account. (Liabilities) Current liabilities 4,655. Short-term loans payable 1,000. Income taxes payable") Financial Report for the 25th Business Year 1-5-1 Marunouchi, Chiyoda-ku, Tokyo Citigroup Japan Holdings Corp. Anthony P. Della Pietra, Jr., Representative Director, President and CEO Balance Sheet (for

Financial Report for the 25th Business Year 1-5-1 Marunouchi, Chiyoda-ku, Tokyo Citigroup Japan Holdings Corp. Anthony P. Della Pietra, Jr., Representative Director, President and CEO Balance Sheet (for

Assignment 10 (Chapter 11)

") Assignment 10 (Chapter 11) 1. Which of the following tends to cause the U.S. dollar to appreciate in value? a) An increase in U.S. prices above foreign prices b) Rapid economic growth in foreign countries

Assignment 10 (Chapter 11) 1. Which of the following tends to cause the U.S. dollar to appreciate in value? a) An increase in U.S. prices above foreign prices b) Rapid economic growth in foreign countries

RISK DISCLOSURE STATEMENT

RISK DISCLOSURE STATEMENT You should note that there are significant risks inherent in investing in certain financial instruments and in certain markets. Investment in derivatives, futures, options and

RISK DISCLOSURE STATEMENT You should note that there are significant risks inherent in investing in certain financial instruments and in certain markets. Investment in derivatives, futures, options and

Correlation of International Stock Markets Before and During the Subprime Crisis

173 Correlation of International Stock Markets Before and During the Subprime Crisis Ioana Moldovan 1 Claudia Medrega 2 The recent financial crisis has spread to markets worldwide. The correlation of evolutions

173 Correlation of International Stock Markets Before and During the Subprime Crisis Ioana Moldovan 1 Claudia Medrega 2 The recent financial crisis has spread to markets worldwide. The correlation of evolutions

Development of Money Markets

Development of Money Markets Mats Filipsson International Monetary Fund Monetary and Exchange Affairs Department Workshop on Developing Government Bond Markets in APEC Economies Shanghai, November 12 15,

Development of Money Markets Mats Filipsson International Monetary Fund Monetary and Exchange Affairs Department Workshop on Developing Government Bond Markets in APEC Economies Shanghai, November 12 15,

FIN 432 Investment Analysis and Management Review Notes for Midterm Exam

FIN 432 Investment Analysis and Management Review Notes for Midterm Exam Chapter 1 1. Investment vs. investments 2. Real assets vs. financial assets 3. Investment process Investment policy, asset allocation,

FIN 432 Investment Analysis and Management Review Notes for Midterm Exam Chapter 1 1. Investment vs. investments 2. Real assets vs. financial assets 3. Investment process Investment policy, asset allocation,

Chapter 14 Foreign Exchange Markets and Exchange Rates

Chapter 14 Foreign Exchange Markets and Exchange Rates International transactions have one common element that distinguishes them from domestic transactions: one of the participants must deal in a foreign

Chapter 14 Foreign Exchange Markets and Exchange Rates International transactions have one common element that distinguishes them from domestic transactions: one of the participants must deal in a foreign

Fundamentals of Futures and Options (a summary)

") Fundamentals of Futures and Options (a summary) Roger G. Clarke, Harindra de Silva, CFA, and Steven Thorley, CFA Published 2013 by the Research Foundation of CFA Institute Summary prepared by Roger G.

Fundamentals of Futures and Options (a summary) Roger G. Clarke, Harindra de Silva, CFA, and Steven Thorley, CFA Published 2013 by the Research Foundation of CFA Institute Summary prepared by Roger G.

FIN 684 Fixed-Income Analysis From Repos to Monetary Policy. Funding Positions

FIN 684 Fixed-Income Analysis From Repos to Monetary Policy Professor Robert B.H. Hauswald Kogod School of Business, AU Funding Positions Short-term funding: repos and money markets funding trading positions

FIN 684 Fixed-Income Analysis From Repos to Monetary Policy Professor Robert B.H. Hauswald Kogod School of Business, AU Funding Positions Short-term funding: repos and money markets funding trading positions

Term Structure of Interest Rates

Appendix 8B Term Structure of Interest Rates To explain the process of estimating the impact of an unexpected shock in short-term interest rates on the entire term structure of interest rates, FIs use

Appendix 8B Term Structure of Interest Rates To explain the process of estimating the impact of an unexpected shock in short-term interest rates on the entire term structure of interest rates, FIs use

Reading the balance of payments accounts

Reading the balance of payments accounts The balance of payments refers to both: All the various payments between a country and the rest of the world The particular system of accounting we use to keep

Reading the balance of payments accounts The balance of payments refers to both: All the various payments between a country and the rest of the world The particular system of accounting we use to keep

Index Solutions A Matter of Weight

Index Solutions A Matter of Weight Newsletter No. 11 Our current newsletter is about weight, or more precisely the weighting of equities in an index. Non-market capitalization weighted indices are at present

Index Solutions A Matter of Weight Newsletter No. 11 Our current newsletter is about weight, or more precisely the weighting of equities in an index. Non-market capitalization weighted indices are at present

HSBC Mutual Funds. Simplified Prospectus June 8, 2015

HSBC Mutual Funds Simplified Prospectus June 8, 2015 Offering Investor Series, Advisor Series, Premium Series, Manager Series and Institutional Series units of the following Funds: HSBC Global Corporate

HSBC Mutual Funds Simplified Prospectus June 8, 2015 Offering Investor Series, Advisor Series, Premium Series, Manager Series and Institutional Series units of the following Funds: HSBC Global Corporate

Staying alive: Bond strategies for a normalising world

Staying alive: Bond strategies for a normalising world Dr Peter Westaway Chief Economist, Europe Vanguard Asset Management November 2013 This document is directed at investment professionals and should

Staying alive: Bond strategies for a normalising world Dr Peter Westaway Chief Economist, Europe Vanguard Asset Management November 2013 This document is directed at investment professionals and should

Chapter 3 Fixed Income Securities

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Fixed-income securities. Stocks. Real assets (capital budgeting). Part C Determination

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Fixed-income securities. Stocks. Real assets (capital budgeting). Part C Determination

Financial-Institutions Management. Solutions 6

Solutions 6 Chapter 25: Loan Sales 2. A bank has made a three-year $10 million loan that pays annual interest of 8 percent. The principal is due at the end of the third year. a. The bank is willing to

Solutions 6 Chapter 25: Loan Sales 2. A bank has made a three-year $10 million loan that pays annual interest of 8 percent. The principal is due at the end of the third year. a. The bank is willing to

2. UK Government debt and borrowing

2. UK Government debt and borrowing How well do you understand the current UK debt position and the options open to Government to reduce the deficit? This leaflet gives you a general background to the

2. UK Government debt and borrowing How well do you understand the current UK debt position and the options open to Government to reduce the deficit? This leaflet gives you a general background to the

1300 307 853 cfds@commsec.com.au commsec.com.au. Important Information

CommSec CFDs: Introduction to Indices We re here to help To find out more, call us on 1300 307 853, from 8am Monday to 6am Saturday, email us at cfds@commsec.com.au or visit our website at commsec.com.au.

CommSec CFDs: Introduction to Indices We re here to help To find out more, call us on 1300 307 853, from 8am Monday to 6am Saturday, email us at cfds@commsec.com.au or visit our website at commsec.com.au.

Licensed by the California Department of Corporations as an Investment Advisor

Licensed by the California Department of Corporations as an Investment Advisor The Impact of the Alternative Minimum Tax (AMT) on Leverage Benefits My associate Matthias Schoener has pointed out to me

Licensed by the California Department of Corporations as an Investment Advisor The Impact of the Alternative Minimum Tax (AMT) on Leverage Benefits My associate Matthias Schoener has pointed out to me