Recurring Legal Issues with Institutional Loans and Payment Plans. Presented by: Jason McCarter Rebecca Flake February 11, 2013

|

|

|

- Collin Hudson

- 8 years ago

- Views:

Transcription

1 Recurring Legal Issues with Institutional Loans and Payment Plans Presented by: Jason McCarter Rebecca Flake February 11, 2013

2 Agenda Loan vs. Payment Plan Regulation Z and Truth-in-Lending (TILA) Other Consumer Protection Laws Basic Contract Requirements Error Identification and Correction Other Legal Issues 2

3 Loan vs. Payment Plan Things to consider - The type of financing option should be driven by the student s needs and the school s needs What amount is financed? What period of time can it be repaid? What level of documentation is required? How you document the arrangement? What disclosures are necessary? Default rights under state law? 3

4 When is it a Private Education Loan? Charges interest Can cover payment plans and loans. Credit expressly, in whole or in part, for postsecondary educational expenses, e.g. tuition, books, supplies, room and board, etc. Despite a general TILA exception for larger loans, private education loans exceeding $25,000 are covered. 4

5 When is it a Payment Plan? Institutional credit is exempted from the requirements of Regulation Z if: (i) (i) the term is 90 days or less; or no interest rate will be charged and the term is one year or less, even if the credit is payable in more than four installments. 5

6 Truth-in-Lending Act - Regulation Z Basics: TILA requires creditors to provide accurate and meaningful disclosure to consumer-borrowers of the costs of credit.* TILA requires creditors to provide written (or qualifying electronic) disclosures to consumers prior to consummating credit transactions. Such disclosures must include certain key terms of the contemplated loan and be in formats prescribed by TILA. Generally overseen by the CFPB and the Fed. *The statutes can be found at 15 U.S.C et seq. Regulation Z can be found at 12 CFR et seq. 6

7 TILA - Regulation Z 2010 changes to Regulation Z: (I) (II) clarify the disclosure and timing requirements for private educational loans ; limit certain practices by creditors, including co-branding by outside lenders with educational institutions; (III) require a self-certification form signed by the consumer before consummating the loan; and (IV) require creditors with preferred lending arrangements with educational institutions to provide certain information to those institutions. 7

8 TILA for Private Educational Lenders Disclosure Requirements: Regulation Z now requires three particular sets of clear and conspicuous disclosures to the consumer-borrowers for private educational loans at the following stages of the loan process: (i) on or with the application (or in solicitations that require no applications); (ii) on or with the loan approval; and (iii) after the borrower accepts but at or before consummation of the loan. Self-Certification form 8

after the borrower accepts but at or before consummation of the loan.")

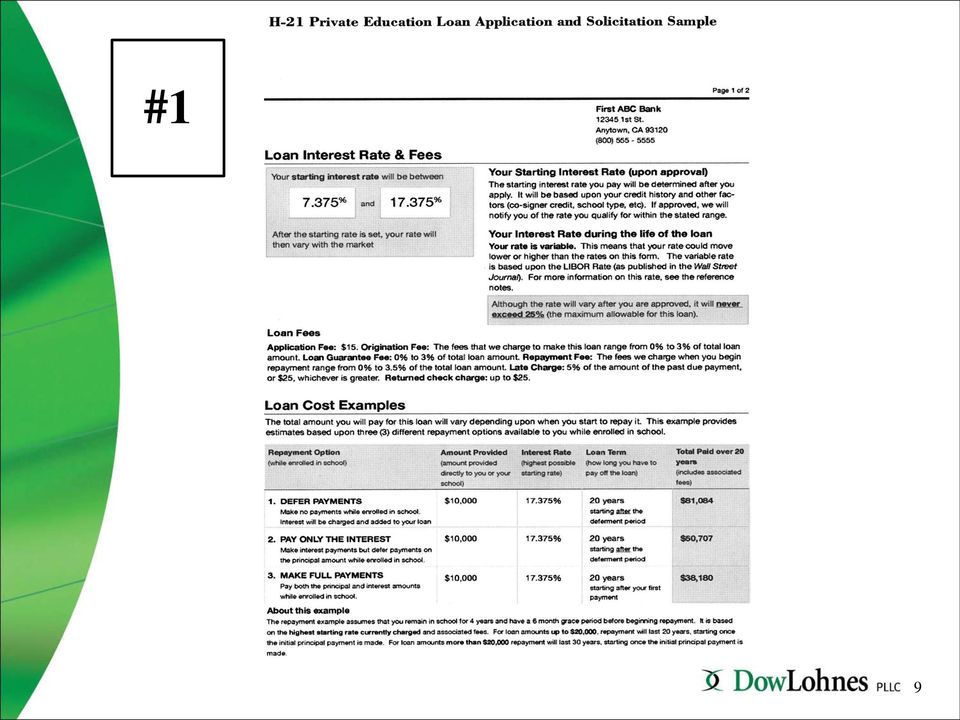

9 #1 9

10 10

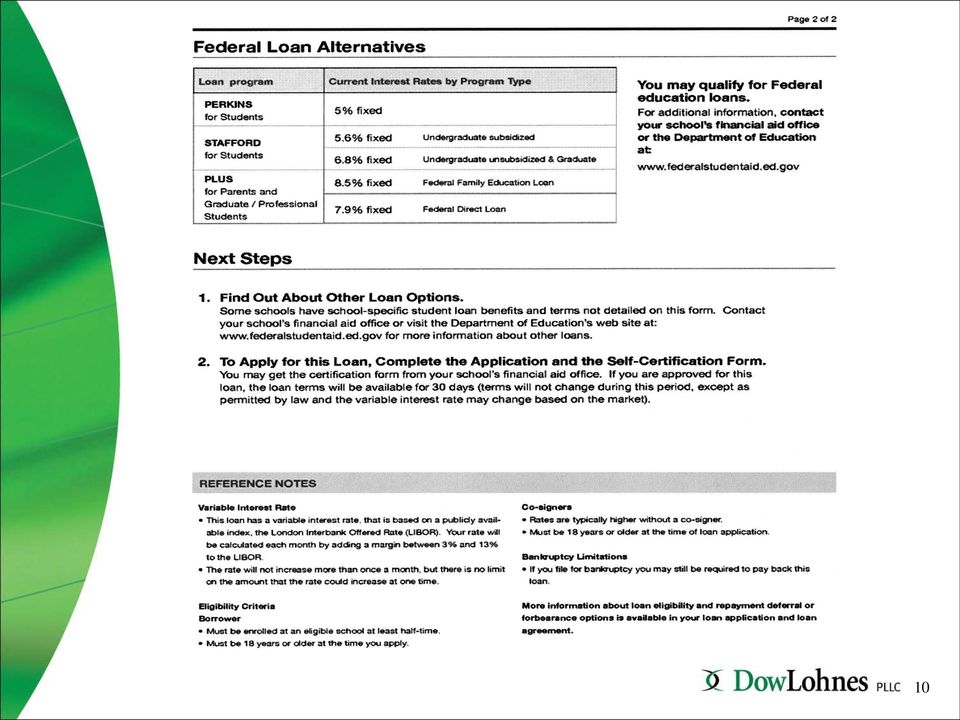

11 #2 11

12 12

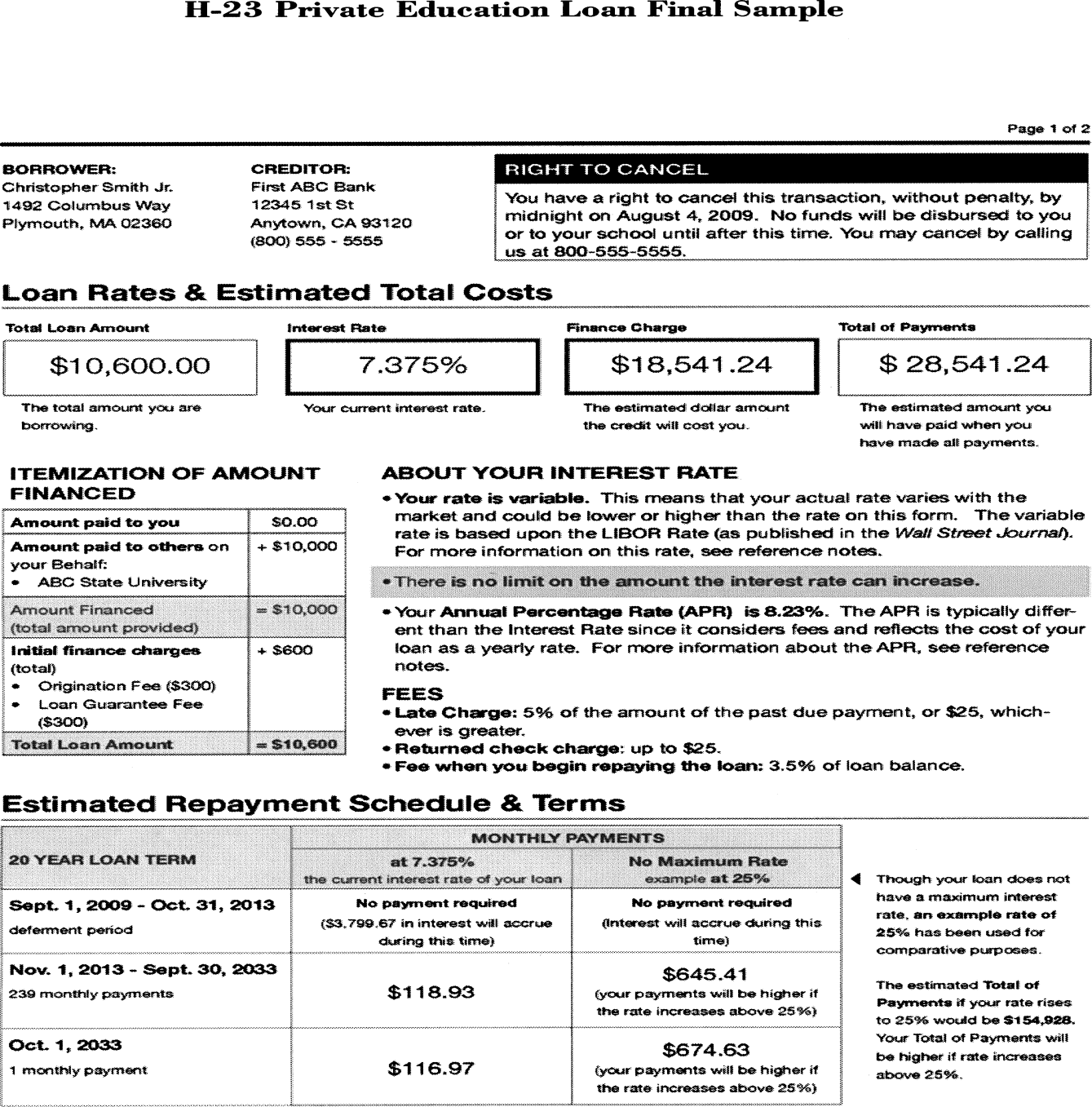

13 #3 13

14 14

15 Self- Certification OMB No. XXXX-XXXX Form Approved Exp. Date XX-XX-XXXX Important: Pursuant to Section 155 of the Higher Education Act of 1965, as amended, (HEA) and to satisfy the requirements of Section 128(e)(3) of the Truth in Lending Act, a lender must obtain a self-certification signed by the applicant before disbursing a private education loan. The school is required on request to provide this form or the required information only for students admitted or enrolled at the school. Throughout this Applicant Self-Certification, you and your refer to the applicant who is applying for the loan. The applicant and the student may be the same person. Instructions: Before signing, carefully read the entire form, including the definitions and other information on the following page. form to your lender. SECTION 1: NOTICES TO APPLICANT Return the signed Free or lower-cost Title IV federal, state, or school student aid may be available in place of, or in addition to, a private education loan. To apply for Title IV federal grants, loans and work-study, submit a Free Application for Federal Student Aid (FAFSA) available at or by calling FED-AID, or from the school s financial aid office. A private education loan may reduce eligibility for free or low-cost federal, state, or school student financial assistance. You are strongly encouraged to pursue the availability of free or lower-cost financial assistance with your school s financial aid office. The financial information required to complete this form can be obtained from the school s financial aid office. If the lender has provided this information, you should contact your school s financial aid office to verify this information and to discuss your financing options. SECTION 2: COST OF ATTENDANCE AND ESTIMATED FINANCIAL ASSISTANCE If information is not already entered below, obtain the needed information from the school financial aid office and enter it on the appropriate line. Sign and date where indicated. A. Student s cost of attendance for the period of enrollment covered by the loan $ B. Estimated financial assistance $ C. Difference between amounts A and B: Ω Warning: If you borrow more than the amount on line C, you risk reducing your eligibility for free or low-cost federal, state, or school financial aid $ SECTION 3: APPLICANT INFORMATION Enter or correct the information below. Name and Address of School Applicant Name (last, first, MI) Street Address City, State Date of Birth (mm/dd/yyyy) / / Address Zip Code Area Code / Telephone Number Home ( ) Period of Enrollment Covered by the Loan (mm/dd/yyyy) Other ( ) From / / to / / If the student is not the loan applicant, provide the student s name and date of birth. Student Name (last, first, MI) SECTION 4: APPLICANT SIGNATURE Student Date of Birth (mm/dd/yyyy) / / I certify that I have read and understood the notices in Section 1 and, to the best of my knowledge, the information provided on this form is true and correct. Signature of Applicant Date (mm/dd/yyyy) 15

16 SECTION 5: DEFINITIONS Cost of attendance is an estimation of tuition and fees, room and board, transportation and other costs for the period of enrollment covered by the loan, as determined by the school. A student s cost of attendance may be obtained from the school financial aid office. Estimated financial assistance is all federal, state, institutional (school), private and other sources of assistance used in determining eligibility for most Title IV student aid, including amounts of financial assistance used to replace the expected family contribution. The student s estimated financial assistance is determined by the school, and may be obtained from the school s financial aid office. A lender is a private education lender as defined in Section 140 of the Truth in Lending Act; and any other person engaged in the business of securing, making, or extending education loans on behalf of the lender. A period of enrollment is the academic year, academic term (such as semester, trimester, or quarter) or the number of weeks of instructional time for which the applicant is requesting student financial assistance. A private education loan is a loan provided by a private education lender that is not a Title IV loan and that is issued expressly for postsecondary education expenses to a borrower, regardless of whether the loan is provided through the school that the student attends or directly to the borrower from the private education lender. A private education loan does not include (1) An extension of credit under an open end consumer credit plan, a reverse mortgage transaction, a residential mortgage transaction, or any other loan that is secured by real property or a dwelling; or (2) An extension of credit in which the school is the lender if the term of the extension of credit is 90 days or less or an interest rate will not be applied to the credit balance and the term of the extension of credit is one year or less, even if the credit is payable in more than four installments. Title IV student aid includes the Federal Pell Grant Program, the Academic Competitiveness Grant (ACG) Program, the Federal Supplemental Educational Opportunity Grant (FSEOG) Program, the Leveraging Educational Assistance Partnership (LEAP) Program, the Federal Family Education Loan Program (FFELP), the Federal Work-Study (FWS) Program, the William D. Ford Federal Direct Loan (Direct Loan) Program, the Federal Perkins Loan Program, the National Science and Mathematics Access to Retain Talent Grant (National SMART Grant) Program, and the Teacher Education Assistance for College and Higher Education (TEACH) Grant Program. SECTION 6: PAPERWORK REDUCTION NOTICE Paperwork Reduction Notice: According to the Paperwork Reduction Act of 1995, no persons are required to respond to a collection of information unless it displays a currently valid OMB control number. The valid OMB control number for this information collection is 1845-XXXA. The time required to complete this information collection is estimated to average 0.25 hours (15 minutes) per response, including the time to review instructions, search existing data resources, gather and maintain the data needed, and complete and review the information collection. If you have any comments concerning the accuracy of the time estimate(s) or suggestions for improving this form, please write to: U.S. Department of Education, Washington, DC If you have any comments or concerns regarding the status of your individual submission of this form, contact your lender. 16

17 Other Consumer Protection Laws Student loans and payment plans are a form of consumer credit, so some or all of the following consumer protection bodies of law could come into play in certain cases: o Equal Credit Opportunity Act (ECOA) o Fair Credit Reporting Act (FCRA) o Fair Debt Collection Practices Act (FDCPA) o Red Flags Rule o State equivalents o State retail installment acts o State usury law o State licensing o Federal bankruptcy rules 17

18 Basic Contract Requirements Student loans and credit are a form of contract, written or otherwise. So it s prudent to keep in mind these basic contracting principles: Clear written terms (even if simple) Especially on the financial terms Signed or otherwise accepted by both parties in their legal names Maintained in provable format Good choice of law and jurisdiction Potentially, damage, jury, class action waivers and/or arbitration clauses 18

19 Corrections/Errors/Audits Conduct routine reviews of procedures and forms to - Identify and correct any mistakes and obtain missing information Ensure enforceability of loans Minimize ongoing negative consequences Some bodies of law, like TILA, even specifically protect timely corrections: A creditor or assignee has no liability under this section... if within sixty days after discovering an error... the creditor or assignee notifies the person concerned of the error and makes whatever adjustments in the appropriate account are necessary to assure that the person will not be required to pay an amount in excess of the charge actually disclosed, or the dollar equivalent of the annual percentage rate actually disclosed, whichever is lower. 15 USC 1640(b) (emphasis added). 19

20 Other Legal Issues With Institutional Loans and Payment Plans Institutional loans and payment plans can be an important source of revenue for institutions, giving students attendance options they would not otherwise have, but they come with far amount of legal baggage that must be minded along the way. CFPB enforcement and oversight Disclosure of other funding options; exhaust Federal funding first 20

21 Resources Related Regulations: CFPB Guidance to Student Borrowers: Red Flags Rule: TILA for Private Education Lenders: Student Loans in Bankruptcy:

22 Contact Information Jason McCarter (770) Rebecca Flake (202)

23 Session Name: Recurring Legal Issues with Institutional Loans and Payment Plans Evaluation System APP or Web Enter Poll ID Enter Password sasfaa 23

Private Education Loan Applicant Self-Certification

2014/2015 Award Year Important: Pursuant to Section 155 of the Higher Education Act of 1965, as amended, (HEA) and to satisfy the requirements of Section 128(e)(3) of the Truth in Lending Act, a lender

2014/2015 Award Year Important: Pursuant to Section 155 of the Higher Education Act of 1965, as amended, (HEA) and to satisfy the requirements of Section 128(e)(3) of the Truth in Lending Act, a lender

Stephen M. Ross School of Business University of Michigan Office of Financial Aid 701 Tappan, Room E2420 Ann Arbor, MI 48109-1234

Stephen M. Ross School of Business Office of Financial Aid 701 Tappan, Room E2420 Ann Arbor, MI 48109-1234 Ross Tuition Reimbursement Loan Information and Application The Ross School of Business Loan Program

Stephen M. Ross School of Business Office of Financial Aid 701 Tappan, Room E2420 Ann Arbor, MI 48109-1234 Ross Tuition Reimbursement Loan Information and Application The Ross School of Business Loan Program

Health Resources and Services Administration Bureau of Health Professions Nurse Faculty Loan Program. Application Procedures

Health Resources and Services Administration Bureau of Health Professions Nurse Faculty Loan Program Application Procedures Prior to submitting your application for the Nurse Faculty Loan Program it is

Health Resources and Services Administration Bureau of Health Professions Nurse Faculty Loan Program Application Procedures Prior to submitting your application for the Nurse Faculty Loan Program it is

SECTION 1: INFORMATION ABOUT THE LOAN PROGRAM

APPLICATION FOR LOAN THE HARVEY M. THOMAS STUDENT LOAN FUND WELLS FARGO BANK, N.A., TRUSTEE DEADLINES FOR COMPLETED APPLICATION PACKETS ARE: May 1, 2016 SECTION 1: INFORMATION ABOUT THE LOAN PROGRAM The

APPLICATION FOR LOAN THE HARVEY M. THOMAS STUDENT LOAN FUND WELLS FARGO BANK, N.A., TRUSTEE DEADLINES FOR COMPLETED APPLICATION PACKETS ARE: May 1, 2016 SECTION 1: INFORMATION ABOUT THE LOAN PROGRAM The

Stephen M. Ross School of Business Financial Aid Office

Stephen M. Ross School of Business Financial Aid Office Ross Tuition Reimbursement Loan Information and Application The Ross School of Business offers short-term loans to students in the Evening, Executive

Stephen M. Ross School of Business Financial Aid Office Ross Tuition Reimbursement Loan Information and Application The Ross School of Business offers short-term loans to students in the Evening, Executive

TEXAS MEDICAL ASSOCIATION LOANS FOR MEDICAL STUDENTS AT THE UNIVERSITY OF TEXAS HEALTH SCIENCE CENTER AT HOUSTON

TEXAS MEDICAL ASSOCIATION LOANS FOR MEDICAL STUDENTS AT THE UNIVERSITY OF TEXAS HEALTH SCIENCE CENTER AT HOUSTON HOW TO APPLY Students may apply through the Student Financial Aid Office. Students must

TEXAS MEDICAL ASSOCIATION LOANS FOR MEDICAL STUDENTS AT THE UNIVERSITY OF TEXAS HEALTH SCIENCE CENTER AT HOUSTON HOW TO APPLY Students may apply through the Student Financial Aid Office. Students must

TopPick Student Loan Application

TopPick Student Loan Application Before completing any part of this application, please refer to the information page on our website at www.phef.org for qualifications, policies, and procedures. Submit

TopPick Student Loan Application Before completing any part of this application, please refer to the information page on our website at www.phef.org for qualifications, policies, and procedures. Submit

Interest Rate (highest possible starting rate) Amount Provided (amount provided directly to you or your school)

Amount Provided (amount provided directly to you or your school)") PALMETTO ASSISTANCE LOAN APPLICATION AND SOLICITATION DISCLOSURE STATEMENT Loan Interest Rate & Fees PO Box 102405, Columbia, SC 29224 (800) 347-2752 www.scstudentloan.org Your interest rate will be either

PALMETTO ASSISTANCE LOAN APPLICATION AND SOLICITATION DISCLOSURE STATEMENT Loan Interest Rate & Fees PO Box 102405, Columbia, SC 29224 (800) 347-2752 www.scstudentloan.org Your interest rate will be either

The Franklin Lindsay Student Aid Fund Application/Promissory Note Checklist

The Franklin Lindsay Student Aid Fund Application/Promissory Note Checklist Name of Student I am a: New Borrower Renewal Borrower Follow these steps to apply for your loan: REVIEW criteria to be sure you

The Franklin Lindsay Student Aid Fund Application/Promissory Note Checklist Name of Student I am a: New Borrower Renewal Borrower Follow these steps to apply for your loan: REVIEW criteria to be sure you

Alaska Supplemental Education Loan (ASEL) Application and Master Promissory Note

Application and Master Promissory Note") Alaska Supplemental Education Loan (ASEL) Application and Master Promissory Note The Alaska Commission on Postsecondary Education (ACPE) services the education loans owned by the Alaska Student Loan Corporation

Alaska Supplemental Education Loan (ASEL) Application and Master Promissory Note The Alaska Commission on Postsecondary Education (ACPE) services the education loans owned by the Alaska Student Loan Corporation

ALASKA SUPPLEMENTAL EDUCATION LOAN (ASEL) 2016/2017 APPLICATION AND PROMISSORY NOTE COSIGNER AGREEMENT PACKET

2016/2017 APPLICATION AND PROMISSORY NOTE COSIGNER AGREEMENT PACKET") Alaska Commission on Postsecondary Education P.O. Box 110505 Juneau, Alaska 99811-0505 ALASKA SUPPLEMENTAL EDUCATION LOAN (ASEL) 2016/2017 APPLICATION AND PROMISSORY NOTE COSIGNER AGREEMENT PACKET Customer

Alaska Commission on Postsecondary Education P.O. Box 110505 Juneau, Alaska 99811-0505 ALASKA SUPPLEMENTAL EDUCATION LOAN (ASEL) 2016/2017 APPLICATION AND PROMISSORY NOTE COSIGNER AGREEMENT PACKET Customer

UNEMPLOYMENT DEFERMENT SELF HELP PACKET

UNEMPLOYMENT DEFERMENT SELF HELP PACKET Unemployment Deferment A deferment is a way to postpone paying back your student loans for a certain period of time. This packet contains information about the federal

UNEMPLOYMENT DEFERMENT SELF HELP PACKET Unemployment Deferment A deferment is a way to postpone paying back your student loans for a certain period of time. This packet contains information about the federal

LOAN DISCHARGE APPLICATION: FALSE CERTIFICATION (ABILITY TO BENEFIT) William D. Ford Federal Direct Loan (Direct Loan) Program

William D. Ford Federal Direct Loan (Direct Loan) Program") LOAN DISCHARGE APPLICATION: FALSE CERTIFICATION (ABILITY TO BENEFIT) William D. Ford Federal Direct Loan (Direct Loan) Program OMB No. 1845-0058 Form Approved Exp. Date 08/31/2017 Federal Family Education

LOAN DISCHARGE APPLICATION: FALSE CERTIFICATION (ABILITY TO BENEFIT) William D. Ford Federal Direct Loan (Direct Loan) Program OMB No. 1845-0058 Form Approved Exp. Date 08/31/2017 Federal Family Education

Alaska Family Education Loan (FEL) Application and Promissory Note

Application and Promissory Note") Section One: Disclosures A. Eligibility Requirements: In order to qualify for a loan, a borrower must: 1. be a U.S. citizen or an eligible non-citizen, and an Alaska resident. To meet the residency requirement

Section One: Disclosures A. Eligibility Requirements: In order to qualify for a loan, a borrower must: 1. be a U.S. citizen or an eligible non-citizen, and an Alaska resident. To meet the residency requirement

LOAN DISCHARGE APPLICATION: SCHOOL CLOSURE William D. Ford Federal Direct Loan (Direct Loan) Program, Federal Family

Program, Federal Family") LOAN DISCHARGE APPLICATION: SCHOOL CLOSURE William D. Ford Federal Direct Loan (Direct Loan) Program, Federal Family Page 1 of 5 OMB No. 1845-0058 Form Approved Exp. Date 08/31/2017 Education Loan (FFEL)

LOAN DISCHARGE APPLICATION: SCHOOL CLOSURE William D. Ford Federal Direct Loan (Direct Loan) Program, Federal Family Page 1 of 5 OMB No. 1845-0058 Form Approved Exp. Date 08/31/2017 Education Loan (FFEL)

ECONOMIC HARDSHIP DEFERMENT SELF HELP PACKET

ECONOMIC HARDSHIP DEFERMENT SELF HELP PACKET Economic Hardship Deferment A deferment is a way to postpone paying back your student loans for a certain period of time. The economic hardship deferment is

ECONOMIC HARDSHIP DEFERMENT SELF HELP PACKET Economic Hardship Deferment A deferment is a way to postpone paying back your student loans for a certain period of time. The economic hardship deferment is

ECONOMIC HARDSHIP DEFERMENT REQUEST Federal Family Education Loan Program

HRD ECONOMIC HARDSHIP DEFERMENT REQUEST Federal Family Education Loan Program Use this form only if all of your outstanding Federal Family Education Loan (FFEL) Program loans were made on or after July

HRD ECONOMIC HARDSHIP DEFERMENT REQUEST Federal Family Education Loan Program Use this form only if all of your outstanding Federal Family Education Loan (FFEL) Program loans were made on or after July

Income-Based (IBR) / Pay As You Earn / Income-Contingent (ICR) Repayment Plan Request OMB No. 1845-0102 Form Approved

/ Pay As You Earn / Income-Contingent (ICR) Repayment Plan Request OMB No. 1845-0102 Form Approved") IBR/PAYE/ICR SECTION 1: BORROWER IDENTIFICATION Please enter or correct the following information. Check this box if any of your information has changed. SSN - - Name Address City, State, Zip Code Telephone

IBR/PAYE/ICR SECTION 1: BORROWER IDENTIFICATION Please enter or correct the following information. Check this box if any of your information has changed. SSN - - Name Address City, State, Zip Code Telephone

Form Completion. Before you submit your deferment form, did you:

Enclosed is the Parent PLUS Borrower Deferment application you requested. Please read all the instructions before completing the form. If you are requesting a deferment for more than one child, please

Enclosed is the Parent PLUS Borrower Deferment application you requested. Please read all the instructions before completing the form. If you are requesting a deferment for more than one child, please

MILITARY SERVICE AND POST-ACTIVE DUTY STUDENT DEFERMENT REQUEST William D. Ford Federal Direct Loan (Direct Loan) Program/Federal Family

Program/Federal Family") MIL MILITARY SERVICE AND POST-ACTIVE DUTY STUDENT DEFERMENT REQUEST William D. Ford Federal Direct Loan (Direct Loan) Program/Federal Family OMB No. 1845-0080 Form Approved Exp. Date 9/30/2016 Education

MIL MILITARY SERVICE AND POST-ACTIVE DUTY STUDENT DEFERMENT REQUEST William D. Ford Federal Direct Loan (Direct Loan) Program/Federal Family OMB No. 1845-0080 Form Approved Exp. Date 9/30/2016 Education

Enclosed is the Economic Hardship Deferment application you requested. Please read all the instructions before completing the form.

Enclosed is the Economic Hardship Deferment application you requested. Please read all the instructions before completing the form. Note for Co-Makers (spousal consolidation or PLUS loan made before April

Enclosed is the Economic Hardship Deferment application you requested. Please read all the instructions before completing the form. Note for Co-Makers (spousal consolidation or PLUS loan made before April

Private Loan Application and Promissory Note Section A. Student Information (Please use black or blue ink, and do not use correction fluid.) 1. Student Last Name Student First Name MI 2. Date of Birth

Private Loan Application and Promissory Note Section A. Student Information (Please use black or blue ink, and do not use correction fluid.) 1. Student Last Name Student First Name MI 2. Date of Birth

IMPORTANT INFORMATION FOR REQUESTING THE 6% SCRA INTEREST RATE BENEFIT

Enclosed is the Military Deferment application you requested. Please read all the instructions, eligibility requirements, and definitions in Section 6 before completing the form. Note for Co-Makers (spousal

Enclosed is the Military Deferment application you requested. Please read all the instructions, eligibility requirements, and definitions in Section 6 before completing the form. Note for Co-Makers (spousal

TITLE X PRIVATE STUDENT LOAN IMPROVEMENT

122 STAT. 3478 PUBLIC LAW 110 315 AUG. 14, 2008 (E) MINORITY BUSINESS. The term minority business includes HUBZone small business concerns (as defined in section 3(p) of the Small Business Act (15 U.S.C.

122 STAT. 3478 PUBLIC LAW 110 315 AUG. 14, 2008 (E) MINORITY BUSINESS. The term minority business includes HUBZone small business concerns (as defined in section 3(p) of the Small Business Act (15 U.S.C.

For additional information, contact your financial aid office or the U. S. Department of Education at: www.federalstudentaid.ed.

Pennsylvania Private Loan Marketplace http://pennsylvania.privateloanmarketplace.com/ Once you and your family have considered institutional and federal loan options, you can use the Pennsylvania Private

Pennsylvania Private Loan Marketplace http://pennsylvania.privateloanmarketplace.com/ Once you and your family have considered institutional and federal loan options, you can use the Pennsylvania Private

Session #32. Student Loan Consumerism. Gail McLarnon U.S. Department of Education Brent Lattin Federal Reserve Board

Session #32 Student Loan Consumerism Gail McLarnon U.S. Department of Education Brent Lattin Federal Reserve Board Today s Topics Disclosures and requirements subject to regulation by the Department of

Session #32 Student Loan Consumerism Gail McLarnon U.S. Department of Education Brent Lattin Federal Reserve Board Today s Topics Disclosures and requirements subject to regulation by the Department of

1/17/2012. The Honorable Richard Cordray Director, Consumer Financial Protection Bureau 1500 Pennsylvania Ave, NW Washington, DC 20220

1/17/2012 The Honorable Richard Cordray Director, Consumer Financial Protection Bureau 1500 Pennsylvania Ave, NW Washington, DC 20220 Dear Mr. Cordray, On behalf of the National Association of College

1/17/2012 The Honorable Richard Cordray Director, Consumer Financial Protection Bureau 1500 Pennsylvania Ave, NW Washington, DC 20220 Dear Mr. Cordray, On behalf of the National Association of College

QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS)

(CLOSED-END HOME MORTGAGE TRANSACTIONS)") QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS) Type of (2) Contents of Truth in Lending Statements 226.17 226.36 Early s 226.19(a)(1)

QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS) Type of (2) Contents of Truth in Lending Statements 226.17 226.36 Early s 226.19(a)(1)

Talent Amendment Limitations on Terms of Consumer Credit Extended to Service Members and Dependents

Talent Amendment Limitations on Terms of Consumer Credit Extended to Service Members Dependents Background Department of Defense (DoD) regulations implementing the consumer protection provisions of the

Talent Amendment Limitations on Terms of Consumer Credit Extended to Service Members Dependents Background Department of Defense (DoD) regulations implementing the consumer protection provisions of the

For additional information, contact your financial aid office or the U. S. Department of Education at: www.federalstudentaid.ed.

Ohio Private Loan Marketplace http://ohio.privateloanmarketplace.com/ Once you and your family have considered institutional and federal loan options, you can use the Ohio Private Loan Marketplace to instantly

Ohio Private Loan Marketplace http://ohio.privateloanmarketplace.com/ Once you and your family have considered institutional and federal loan options, you can use the Ohio Private Loan Marketplace to instantly

DISCHARGE APPLICATION: TOTAL AND PERMANENT DISABILITY IMPORTANT INFORMATION William D. Ford Federal Direct Loan Program

OMB No. 1845-0065 Fo rm Ap pro ved Exp. Date 6/30/2016 DISCHARGE APPLICATION: TOTAL AND PERMANENT DISABILITY IMPORTANT INFORMATION William D. Ford Federal Direct Loan Program TPD- APP Federal Family Education

OMB No. 1845-0065 Fo rm Ap pro ved Exp. Date 6/30/2016 DISCHARGE APPLICATION: TOTAL AND PERMANENT DISABILITY IMPORTANT INFORMATION William D. Ford Federal Direct Loan Program TPD- APP Federal Family Education

Federal Direct Consolidation Loan Request to Add Loans William D. Ford Federal Direct Loan Program

Federal Direct Consolidation Loan Request to Add Loans William D. Ford Federal Direct Loan Program OMB No. 1845-0053 Form Approved Exp. Date 04/30/2016 WARNING: Any person who knowingly makes a false statement

Federal Direct Consolidation Loan Request to Add Loans William D. Ford Federal Direct Loan Program OMB No. 1845-0053 Form Approved Exp. Date 04/30/2016 WARNING: Any person who knowingly makes a false statement

William D. Ford Federal Parent Loan

NEW YORK CITY COLLEGE OF TECHNOLOGY William D. Ford Federal Parent Loan 2015-2016 Office of Financial Aid Namm G-13 2015-2016 Things you should know before you become a William D. Ford Federal Parent Loan

NEW YORK CITY COLLEGE OF TECHNOLOGY William D. Ford Federal Parent Loan 2015-2016 Office of Financial Aid Namm G-13 2015-2016 Things you should know before you become a William D. Ford Federal Parent Loan

For additional information, contact your financial aid office or the U. S. Department of Education at: www.federalstudentaid.ed.

Private Student Loan Marketplace http://www.privateloanmarketplace.com/ Once you and your family have considered institutional and federal loan options, you can use the Private Student Loan Marketplace

Private Student Loan Marketplace http://www.privateloanmarketplace.com/ Once you and your family have considered institutional and federal loan options, you can use the Private Student Loan Marketplace

Loan Originator Compensation Requirements under the Truth In Lending Act

BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1026 [Docket No. CFPB-2013-0013] RIN 3170-AA37 Loan Originator Compensation Requirements under the Truth In Lending Act (Regulation Z); Prohibition on

BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1026 [Docket No. CFPB-2013-0013] RIN 3170-AA37 Loan Originator Compensation Requirements under the Truth In Lending Act (Regulation Z); Prohibition on

Mon. ICBA Summary of the Military Lending Act Updated Regulation. August 2015. Month Year. Contact:

ICBA Summary of the Military Lending Act Updated Regulation August 2015 Month Year Mon Contact: Joe Gormley Assistant Vice President & Regulatory Counsel joseph.gormley@icba.org www.icba.org ICBA Summary

ICBA Summary of the Military Lending Act Updated Regulation August 2015 Month Year Mon Contact: Joe Gormley Assistant Vice President & Regulatory Counsel joseph.gormley@icba.org www.icba.org ICBA Summary

A. Introduction B. Background

1700 G Street, N.W., Washington, DC 20552 CFPB Compliance Bulletin 2015-06 Date: November 23, 2015 Subject: Requirements for Consumer Authorizations for Preauthorized Electronic Fund Transfers A. Introduction

1700 G Street, N.W., Washington, DC 20552 CFPB Compliance Bulletin 2015-06 Date: November 23, 2015 Subject: Requirements for Consumer Authorizations for Preauthorized Electronic Fund Transfers A. Introduction

Office of Financial Aid and Veterans Affairs 5100 Black Horse Pike Mays Landing, NJ 08330 Federal Direct PLUS Loan Application Information Sheet

Office of Financial Aid and Veterans Affairs 5100 Black Horse Pike Mays Landing, NJ 08330 Federal Direct PLUS Loan Application Information Sheet Step 1: Complete a Free Application for Federal Student

Office of Financial Aid and Veterans Affairs 5100 Black Horse Pike Mays Landing, NJ 08330 Federal Direct PLUS Loan Application Information Sheet Step 1: Complete a Free Application for Federal Student

This list provides acronyms and common terms that can assist with the preparation of Policies and Procedures.

This list provides acronyms and common terms that can assist with the preparation of Policies and Procedures. Ability to Benefit ATB One of the criteria used to establish student eligibility in order to

This list provides acronyms and common terms that can assist with the preparation of Policies and Procedures. Ability to Benefit ATB One of the criteria used to establish student eligibility in order to

Loan Originator Compensation Requirements under the Truth In Lending Act

BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1026 [Docket No. CFPB-2013-0013] RIN 3170-AA37 Loan Originator Compensation Requirements under the Truth In Lending Act (Regulation Z); Prohibition on

BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1026 [Docket No. CFPB-2013-0013] RIN 3170-AA37 Loan Originator Compensation Requirements under the Truth In Lending Act (Regulation Z); Prohibition on

A.W. Winn Brindle Memorial Education Loan 2016/2017 Application and Promissory Note

A.W. Winn Brindle Memorial Education Loan 2016/2017 Application and Promissory Note COSIGNER AGREEMENT PACKET Loan Terms and Conditions Alaska Commission on Postsecondary Education P.O. Box 110505 Juneau,

A.W. Winn Brindle Memorial Education Loan 2016/2017 Application and Promissory Note COSIGNER AGREEMENT PACKET Loan Terms and Conditions Alaska Commission on Postsecondary Education P.O. Box 110505 Juneau,

Private Education Loans

Truth in Lending Act Rules for Private Education Loans Please note that the following material is presented only for educational purposes and constitutes only the opinions of the presenter. The material

Truth in Lending Act Rules for Private Education Loans Please note that the following material is presented only for educational purposes and constitutes only the opinions of the presenter. The material

Division of Student Life & Enrollment Office of Enrollment Management

2015-2016 FEDERAL DIRECT GRADUATE PLUS LOAN APPLICATION LSU ONLINE If you wish to apply for the Federal Direct Graduate PLUS Loan for the 2015-2016 academic year, you must complete all sections of this

2015-2016 FEDERAL DIRECT GRADUATE PLUS LOAN APPLICATION LSU ONLINE If you wish to apply for the Federal Direct Graduate PLUS Loan for the 2015-2016 academic year, you must complete all sections of this

How To Fill Out A Federal Loan Rehabilitation Form

RAP FINANCIAL DISCLOSURE FOR REASONABLE AND AFFORDABLE REHABILITATION PAYMENTS William D. Ford Federal Direct Loan (Direct Loan) Program Page 1 of 5 OMB No. 1845-0120 Form Approved Exp. Date 03/31/2017

RAP FINANCIAL DISCLOSURE FOR REASONABLE AND AFFORDABLE REHABILITATION PAYMENTS William D. Ford Federal Direct Loan (Direct Loan) Program Page 1 of 5 OMB No. 1845-0120 Form Approved Exp. Date 03/31/2017

USC CENTER FOR HIGHER EDUCATION POLICY ANALYSIS COSTS:

USC CENTER FOR HIGHER EDUCATION POLICY ANALYSIS COLLEGE COSTS: A CALIFORNIA STUDENT GUIDE TO PAYING FOR COLLEGE Are you concerned about paying for college? Do you think that attending your college of choice

USC CENTER FOR HIGHER EDUCATION POLICY ANALYSIS COLLEGE COSTS: A CALIFORNIA STUDENT GUIDE TO PAYING FOR COLLEGE Are you concerned about paying for college? Do you think that attending your college of choice

Policy Guidance on Supervisory and Enforcement Considerations Relevant to Mortgage

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION Policy Guidance on Supervisory and Enforcement Considerations Relevant to Mortgage Brokers Transitioning to Mini-Correspondent Lenders AGENCY:

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION Policy Guidance on Supervisory and Enforcement Considerations Relevant to Mortgage Brokers Transitioning to Mini-Correspondent Lenders AGENCY:

Regulatory Practice Letter

RPL Number 10-17 Financial Services Regulatory Practice Regulatory Practice Letter ADVISORY Amendments to Mortgage Loan Provisions under Regulation Z Executive Summary The Federal Reserve Board ( Fed )

RPL Number 10-17 Financial Services Regulatory Practice Regulatory Practice Letter ADVISORY Amendments to Mortgage Loan Provisions under Regulation Z Executive Summary The Federal Reserve Board ( Fed )

Borrower Information 1. Last Name First Name MI. State # 8. Lender Name City State Zip Code

Federal Family Education Loan Program (FFELP) Federal Stafford Loan Master Promissory Note WARNING: Any person who knowingly makes a false statement or misrepresentation on this form is subject to penalties

Federal Family Education Loan Program (FFELP) Federal Stafford Loan Master Promissory Note WARNING: Any person who knowingly makes a false statement or misrepresentation on this form is subject to penalties

(1) ECMC has obtained substantial private student loan debt relief for current and former Corinthian students.

ECMC has obtained substantial private student loan debt relief for current and former Corinthian students.") February 2, 2015 Hon. Richard Cordray Director Consumer Financial Protection Bureau 1700 G St. NW Washington, DC 20552 RE: ECMC Group, Inc. s purchase of certain Corinthian Colleges, Inc. assets Dear Director

February 2, 2015 Hon. Richard Cordray Director Consumer Financial Protection Bureau 1700 G St. NW Washington, DC 20552 RE: ECMC Group, Inc. s purchase of certain Corinthian Colleges, Inc. assets Dear Director

Federal Direct PLUS Loan Master Promissory Note William D. Ford Federal Direct Loan Program

Federal Direct PLUS Loan Master Promissory Note William D. Ford Federal Direct Loan Program Warning: Any person who knowingly makes a false statement or misrepresentation on this form or any accompanying

Federal Direct PLUS Loan Master Promissory Note William D. Ford Federal Direct Loan Program Warning: Any person who knowingly makes a false statement or misrepresentation on this form or any accompanying

SECTION A: BORROWER INFORMATION READ THE INSTRUCTIONS IN SECTION G BEFORE COMPLETING THIS SECTION

Federal Direct Stafford/Ford Loan Federal Direct Unsubsidized Stafford/Ford Loan Master Promissory Note William D. Ford Federal Direct Loan Program Warning: Any person who knowingly makes a false statement

Federal Direct Stafford/Ford Loan Federal Direct Unsubsidized Stafford/Ford Loan Master Promissory Note William D. Ford Federal Direct Loan Program Warning: Any person who knowingly makes a false statement

Examination Procedures

After completing the risk assessment and examination scoping, examiners should use these procedures, in conjunction with the compliance management system review procedures, to conduct an education loan

After completing the risk assessment and examination scoping, examiners should use these procedures, in conjunction with the compliance management system review procedures, to conduct an education loan

IC 24-4.5-7 Chapter 7. Small Loans

IC 24-4.5-7 Chapter 7. Small Loans IC 24-4.5-7-101 Citation Sec. 101. This chapter shall be known and may be cited as Uniform Consumer Credit Code Small Loans. As added by P.L.38-2002, SEC.1. IC 24-4.5-7-102

IC 24-4.5-7 Chapter 7. Small Loans IC 24-4.5-7-101 Citation Sec. 101. This chapter shall be known and may be cited as Uniform Consumer Credit Code Small Loans. As added by P.L.38-2002, SEC.1. IC 24-4.5-7-102

Federal Register / Vol. 74, No. 156 / Friday, August 14, 2009 / Rules and Regulations

41194 Federal Register / Vol. 74, No. 156 / Friday, August 14, 2009 / Rules and Regulations FEDERAL RESERVE SYSTEM 12 CFR Part 226 [Regulation Z; Docket No. R 1353] Truth in Lending AGENCY: Board of Governors

41194 Federal Register / Vol. 74, No. 156 / Friday, August 14, 2009 / Rules and Regulations FEDERAL RESERVE SYSTEM 12 CFR Part 226 [Regulation Z; Docket No. R 1353] Truth in Lending AGENCY: Board of Governors

What must I do to have any remaining balances on my Direct Loans forgiven under the PSLF Program?

Dear Federal Student Loan Borrower: Thank you for your interest in the Direct Loan Public Service Loan Forgiveness (PSLF) Program. The PSLF Program was established by Congress with the passage of the College

Dear Federal Student Loan Borrower: Thank you for your interest in the Direct Loan Public Service Loan Forgiveness (PSLF) Program. The PSLF Program was established by Congress with the passage of the College

Overview of Federal Student Aid Programs

Overview of Federal Student Aid Programs This training will provide an overview of the Title IV programs and information about additional federal, state, and other sources of financial aid. OBJECTIVES:

Overview of Federal Student Aid Programs This training will provide an overview of the Title IV programs and information about additional federal, state, and other sources of financial aid. OBJECTIVES:

Federal Direct Consolidation Loan Application and Promissory Note William D. Ford Federal Direct Loan Program

Federal Direct Consolidation Loan Application and Promissory Note William D. Ford Federal Direct Loan Program OMB No. 1845-0053 Form Approved Exp. Date 04/30/2016 WARNING: Any person who knowingly makes

Federal Direct Consolidation Loan Application and Promissory Note William D. Ford Federal Direct Loan Program OMB No. 1845-0053 Form Approved Exp. Date 04/30/2016 WARNING: Any person who knowingly makes

Metropolitan Community College s Administration of the Title IV Programs FINAL AUDIT REPORT

Metropolitan Community College s Administration of the Title IV Programs FINAL AUDIT REPORT ED-OIG/A07K0003 May 2012 Our mission is to promote the efficiency, effectiveness, and integrity of the Department's

Metropolitan Community College s Administration of the Title IV Programs FINAL AUDIT REPORT ED-OIG/A07K0003 May 2012 Our mission is to promote the efficiency, effectiveness, and integrity of the Department's

*BORROWER S NAME *SCHOOL ATTENDING SCHOOL CODE (IF KNOWN) * REQUIRED INFORMATION

* REQUIRED INFORMATION") National Education Servicing 200 West Monroe, Suite 700 Chicago, IL 60606-5075 Toll Free: 1-800-345-4325 Fax: 1-800-345-9588 www.nationaled.net Dear Student Loan Borrower: Thank you for selecting NATIONAL

National Education Servicing 200 West Monroe, Suite 700 Chicago, IL 60606-5075 Toll Free: 1-800-345-4325 Fax: 1-800-345-9588 www.nationaled.net Dear Student Loan Borrower: Thank you for selecting NATIONAL

Compliance Bulletin and Policy Guidance: Mortgage Servicing Transfers

1700 G Street, N.W., Washington, DC 20552 Bulletin 2014-01 Date: August 19, 2014 Subject: Compliance Bulletin and Policy Guidance: Mortgage Servicing Transfers The Bureau of Consumer Financial Protection

1700 G Street, N.W., Washington, DC 20552 Bulletin 2014-01 Date: August 19, 2014 Subject: Compliance Bulletin and Policy Guidance: Mortgage Servicing Transfers The Bureau of Consumer Financial Protection

When do I have to start following the TILA-RESPA rule and using the new Integrated Disclosures?

............................................................................................. Overview of the TILA-RESPA Rule.............................................................................................

............................................................................................. Overview of the TILA-RESPA Rule.............................................................................................

DOCUMENT REQUEST - COMPLIANCE REVIEWS - LENDING

Please prepare the Summary of Information items. Electronic format is preferred. () to be provided Pre-Exam () - to be available upon rrival COMPLINCE REVIEWS General Provide the names, titles, e-mail

Please prepare the Summary of Information items. Electronic format is preferred. () to be provided Pre-Exam () - to be available upon rrival COMPLINCE REVIEWS General Provide the names, titles, e-mail

**PAGES 1, 2, AND 3 OF THIS FORM MUST BE SUBMITTED FOR YOUR APPLICATION TO BE PROCESSED.**

Federal Family Education Loan Program (FFELP) Federal Consolidation Loan Application and Promissory Note WARNING: Any person who knowingly makes a false statement or misrepresentation on this form or any

Federal Family Education Loan Program (FFELP) Federal Consolidation Loan Application and Promissory Note WARNING: Any person who knowingly makes a false statement or misrepresentation on this form or any

TOTAL AND PERMANENT DISABILITY DISCHARGE. Self-Help Packet

TOTAL AND PERMANENT DISABILITY DISCHARGE Self-Help Packet GETTING STARTED GETTING STARTED You can cancel your federal student loans based on a permanent and total disability. All federal loan borrowers

TOTAL AND PERMANENT DISABILITY DISCHARGE Self-Help Packet GETTING STARTED GETTING STARTED You can cancel your federal student loans based on a permanent and total disability. All federal loan borrowers

Closed School Loan Discharge Packet

Closed School Loan Discharge Packet If you attended a school that closed before you were able to complete your diploma or degree, you may be eligible for a cancellation, or discharge, of the federal student

Closed School Loan Discharge Packet If you attended a school that closed before you were able to complete your diploma or degree, you may be eligible for a cancellation, or discharge, of the federal student

Federal Direct Consolidation Loan Application and Promissory Note

RETURN THIS PAGE Federal Direct Consolidation Loan Application and Promissory Note WARNING: Any person who knowingly makes a false statement or misrepresentation on this form or any accompanying documentation

RETURN THIS PAGE Federal Direct Consolidation Loan Application and Promissory Note WARNING: Any person who knowingly makes a false statement or misrepresentation on this form or any accompanying documentation

Break Out Session: Mortgage Loan Underwriting and Pricing

Break Out Session: Mortgage Loan Underwriting and Pricing Agenda Ability to Repay (ATR)/Qualified Mortgages (QMs) Effective Date: Applications received on or after January 10, 2014 2013 Home Ownership

Break Out Session: Mortgage Loan Underwriting and Pricing Agenda Ability to Repay (ATR)/Qualified Mortgages (QMs) Effective Date: Applications received on or after January 10, 2014 2013 Home Ownership

Federal Student Aid Public Service Loan Forgiveness Program

Federal Student Aid Public Service Loan Forgiveness Program Dear Federal Student Loan Borrower: Thank you for your interest in the Direct Loan Public Service Loan Forgiveness (PSLF) Program. The PSLF Program

Federal Student Aid Public Service Loan Forgiveness Program Dear Federal Student Loan Borrower: Thank you for your interest in the Direct Loan Public Service Loan Forgiveness (PSLF) Program. The PSLF Program

NEW JERSEY CITY UNIVERSITY. Guide to Financial Aid

NEW JERSEY CITY UNIVERSITY Guide to Financial Aid Fastfact: NJCU graduates include a fashion magazine art director, a NJ Assembly person, a police captain, a news anchor and a corporate vice president!

NEW JERSEY CITY UNIVERSITY Guide to Financial Aid Fastfact: NJCU graduates include a fashion magazine art director, a NJ Assembly person, a police captain, a news anchor and a corporate vice president!

Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD).

.") Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD). Page 1 Closing Information Date Issued Date the CD

Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD). Page 1 Closing Information Date Issued Date the CD

New Servicing Rules under Regulation Z Periodic Statements & Adjustable Rate Mortgages Notices

New Servicing Rules under Regulation Z Periodic Statements & Adjustable Rate Mortgages Notices FIS Regulatory Advisory Services www.fisregulatoryservices.com New Servicing i Rules under Regulation Z Periodic

New Servicing Rules under Regulation Z Periodic Statements & Adjustable Rate Mortgages Notices FIS Regulatory Advisory Services www.fisregulatoryservices.com New Servicing i Rules under Regulation Z Periodic

Student Loan Collection and the CFPB

Student Loan Collection and the CFPB Consumer Financial Protection Bureau o Generally! Established under Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act (12 U.S.C. 5301 et seq.)!

Student Loan Collection and the CFPB Consumer Financial Protection Bureau o Generally! Established under Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act (12 U.S.C. 5301 et seq.)!

A Guide to Sensible Borrowing & Loan Request Form

stafford loans STAFFORD LOANS 2010-2011 A Guide to Sensible Borrowing & Loan Request Form Pursue all other alternatives first Get the facts about each loan program What are Federal Direct Loans Budget

stafford loans STAFFORD LOANS 2010-2011 A Guide to Sensible Borrowing & Loan Request Form Pursue all other alternatives first Get the facts about each loan program What are Federal Direct Loans Budget

Alumni Award Recipients are students who are children or grandchildren of Ottawa University graduates.

Financial Assistance at The College The College has a program of scholarships and grants. This is gift aid that does not have to be repaid. Institutional aid is awarded in a nondiscriminatory fashion,

Financial Assistance at The College The College has a program of scholarships and grants. This is gift aid that does not have to be repaid. Institutional aid is awarded in a nondiscriminatory fashion,

The New Mortgage Servicing Rules. FMS East Coast Regional Conference September 17, 2013

The New Mortgage Servicing Rules FMS East Coast Regional Conference September 17, 2013 What are the new Mortgage Servicing Rules? Ability to Repay/Qualified Mortgage Rule 2013 HOEPA Rule Loan Originator

The New Mortgage Servicing Rules FMS East Coast Regional Conference September 17, 2013 What are the new Mortgage Servicing Rules? Ability to Repay/Qualified Mortgage Rule 2013 HOEPA Rule Loan Originator

Truth in Lending Act

Comptroller s Handbook CC-TILA Consumer Compliance (CC) Truth in Lending Act December 2014 Office of the Comptroller of the Currency Washington, DC 20219 Contents Introduction...1 Background and Summary...

Comptroller s Handbook CC-TILA Consumer Compliance (CC) Truth in Lending Act December 2014 Office of the Comptroller of the Currency Washington, DC 20219 Contents Introduction...1 Background and Summary...

For additional information, contact your financial aid office or the U. S. Department of Education at: www.federalstudentaid.ed.

Private Student Loan Marketplace http://www.privateloanmarketplace.com/ Revised 3/30/1 Once you and your family have considered institutional and federal loan options, you can use the Private Student Loan

Private Student Loan Marketplace http://www.privateloanmarketplace.com/ Revised 3/30/1 Once you and your family have considered institutional and federal loan options, you can use the Private Student Loan

For additional information, contact your financial aid office or the U. S. Department of Education at: www.federalstudentaid.ed.

Private Student Loan Marketplace Revised 3/28/11 http://www.privateloanmarketplace.com/ Once you and your family have considered institutional and federal loan options, you can use the Private Student

Private Student Loan Marketplace Revised 3/28/11 http://www.privateloanmarketplace.com/ Once you and your family have considered institutional and federal loan options, you can use the Private Student

Federal Consolidation Loan Application and Promissory Note

Federal Family Education Loan Program (FFELP) Federal Consolidation Loan Application and Promissory Note WARNING: Any person who knowingly makes a false statement or misrepresentation on this form is subject

Federal Family Education Loan Program (FFELP) Federal Consolidation Loan Application and Promissory Note WARNING: Any person who knowingly makes a false statement or misrepresentation on this form is subject

AMERICAN BAR ASSOCIATION CONSUMER FINANCIAL SERVICES COMMITTEE SPRING MEETING SAN FRANCISCO, CALIFIORNIA

AMERICAN BAR ASSOCIATION CONSUMER FINANCIAL SERVICES COMMITTEE SPRING MEETING SAN FRANCISCO, CALIFIORNIA TILA-RESPA INTEGRATED DISCLOSURE RULE BACKGROUND, TILA LIABILITIES & OPERATIONAL CONCERNS I. OVERVIEW

AMERICAN BAR ASSOCIATION CONSUMER FINANCIAL SERVICES COMMITTEE SPRING MEETING SAN FRANCISCO, CALIFIORNIA TILA-RESPA INTEGRATED DISCLOSURE RULE BACKGROUND, TILA LIABILITIES & OPERATIONAL CONCERNS I. OVERVIEW

Module 3. The disclosure requirements are discussed separately below.

Page 1 of 29 Module 3 Adverse Action Disclosures - Section 615(a) and (b); 15 U.S.C. 1681m(a) and (b) Section 615(a)-(b) requires users of consumer reports, such as creditors, to make certain disclosures

Page 1 of 29 Module 3 Adverse Action Disclosures - Section 615(a) and (b); 15 U.S.C. 1681m(a) and (b) Section 615(a)-(b) requires users of consumer reports, such as creditors, to make certain disclosures

Rules Governing the. Forgivable Education Loans for Service Program

Rules Governing the Forgivable Education Loans for Service Program A Program of the State of North Carolina Administered by the State Education Assistance Authority 10 T.W. Alexander Drive P. O. Box 13663

Rules Governing the Forgivable Education Loans for Service Program A Program of the State of North Carolina Administered by the State Education Assistance Authority 10 T.W. Alexander Drive P. O. Box 13663

House of Representatives

House of Representatives General Assembly File No. 44 February Session, 2002 Substitute House Bill No. 5073 House of Representatives, March 18, 2002 The Committee on Banks reported through REP. DOYLE of

House of Representatives General Assembly File No. 44 February Session, 2002 Substitute House Bill No. 5073 House of Representatives, March 18, 2002 The Committee on Banks reported through REP. DOYLE of

Tennessee Good Funds Law (as amended)

") Tennessee Good Funds Law (as amended) 47-32-101 Short Title This act shall be known and may be cited as the "Residential Closing Funds Distribution Act of 2005". 47-32-102 Chapter Definitions (1) "Agricultural

Tennessee Good Funds Law (as amended) 47-32-101 Short Title This act shall be known and may be cited as the "Residential Closing Funds Distribution Act of 2005". 47-32-102 Chapter Definitions (1) "Agricultural

New Loan Origination and Mortgage Servicing Rules

5/15/ New Loan Origination and Mortgage Servicing Rules Personal Finance Seminar for Professionals University of Maryland Extension Presenter: Diane Cipollone, Esq. Director of Training National Fair Housing

5/15/ New Loan Origination and Mortgage Servicing Rules Personal Finance Seminar for Professionals University of Maryland Extension Presenter: Diane Cipollone, Esq. Director of Training National Fair Housing

Implications of the Federal Right of Rescission for Lenders and Borrowers

Implications of the Federal Right of Rescission for Lenders and Borrowers An Interactive Day of Building an Effective Community Response to Foreclosures in Wisconsin December 12, 2007 Disclaimer The views

Implications of the Federal Right of Rescission for Lenders and Borrowers An Interactive Day of Building an Effective Community Response to Foreclosures in Wisconsin December 12, 2007 Disclaimer The views

How To Write A Federal Consolidation Loan

Federal Family Education Loan Program (FFELP) Federal Consolidation Loan Application and Promissory Note Guarantor, Program, or Lender Identification OMB No. 1845-0036 Form approved Exp. date 10/31/2006

Federal Family Education Loan Program (FFELP) Federal Consolidation Loan Application and Promissory Note Guarantor, Program, or Lender Identification OMB No. 1845-0036 Form approved Exp. date 10/31/2006

The Federal Register published the proposed rule on August 23, 2012.

CFPB Issues Draft RESPA-TILA Proposed Rules On July 9, the Consumer Financial Protection Bureau ( Bureau or CFPB ) released draft proposed rules and model forms that combine the required disclosures under

CFPB Issues Draft RESPA-TILA Proposed Rules On July 9, the Consumer Financial Protection Bureau ( Bureau or CFPB ) released draft proposed rules and model forms that combine the required disclosures under

PAL ReFi Loan. Why refinance? When is my first monthly payment due? What if I need to postpone my monthly payments?

PAL ReFi Loan Why refinance? The advantages of refinancing your education loans with SC Student Loan are*: The convenience and ease of having one monthly payment to one lender; A fixed interest rate for

PAL ReFi Loan Why refinance? The advantages of refinancing your education loans with SC Student Loan are*: The convenience and ease of having one monthly payment to one lender; A fixed interest rate for

Enclosed is a Teacher Loan Forgiveness Application. Please read all the instructions before completing the form.

Enclosed is a Teacher Loan Forgiveness Application. Please read all the instructions before completing the form. Summary of Eligibility You may be considered for Teacher Loan Forgiveness if: you do not

Enclosed is a Teacher Loan Forgiveness Application. Please read all the instructions before completing the form. Summary of Eligibility You may be considered for Teacher Loan Forgiveness if: you do not

HOME OWNERSHIP EQUITY PROTECTION ACT OF 1994. Raymond Natter 1

HOME OWNERSHIP EQUITY PROTECTION ACT OF 1994 Raymond Natter 1 Recent Congressional attention to the problems of predatory mortgage lending has led for calls for the Federal Reserve Board to use its authority

HOME OWNERSHIP EQUITY PROTECTION ACT OF 1994 Raymond Natter 1 Recent Congressional attention to the problems of predatory mortgage lending has led for calls for the Federal Reserve Board to use its authority

Financial Services Update June 11, 2013

Financial Services Update June 11, 2013 HIGHLIGHTS Federal Regulatory Developments: CFPB Amends Examination Manual State Regulatory Developments: Texas Proposes Constitutional Amendment Regarding Reverse

Financial Services Update June 11, 2013 HIGHLIGHTS Federal Regulatory Developments: CFPB Amends Examination Manual State Regulatory Developments: Texas Proposes Constitutional Amendment Regarding Reverse

Print the entire PLUS MPN/Application document with this cover letter

National Education Servicing 200 West Monroe, Suite 700 Chicago, IL 60606-5075 Toll Free: 1-800-345-4325 Fax: 1-800-345-9588 www.nationaled.net Dear Graduate PLUS Loan Applicant: Thank you for selecting

National Education Servicing 200 West Monroe, Suite 700 Chicago, IL 60606-5075 Toll Free: 1-800-345-4325 Fax: 1-800-345-9588 www.nationaled.net Dear Graduate PLUS Loan Applicant: Thank you for selecting

The University of Texas System. 1. Title. Student Financial Aid Code of Conduct. 2. Policy

1. Title 2. Policy Student Financial Aid Code of Conduct Sec. 1 Applicability. This policy provides a Student Financial Aid Code of Conduct. The following entities are required to comply with this policy

1. Title 2. Policy Student Financial Aid Code of Conduct Sec. 1 Applicability. This policy provides a Student Financial Aid Code of Conduct. The following entities are required to comply with this policy

Graduate Student Loan Request Form 2013-2014

Graduate Student Loan Request Form 2013-2014 Please read and complete each section of this form. If you fill out this form incorrectly or leave blanks, this form will be returned to you for completion;

Graduate Student Loan Request Form 2013-2014 Please read and complete each section of this form. If you fill out this form incorrectly or leave blanks, this form will be returned to you for completion;

Please see Section IX. for Additional Information:

The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) BILL: CS/SB 626 Prepared By: The

The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) BILL: CS/SB 626 Prepared By: The

Direct PLUS Loans - Do I Qualify?

Federal Direct PLUS Loan Application and Master Promissory Note William D. Ford Federal Direct Loan Program Warning: Any person who knowingly makes a false statement or misrepresentation on this form or

Federal Direct PLUS Loan Application and Master Promissory Note William D. Ford Federal Direct Loan Program Warning: Any person who knowingly makes a false statement or misrepresentation on this form or

Section 10: Fair Credit Reporting Act (FCRA) Policy

Policy") Section 10: Fair Credit Reporting Act (FCRA) Policy Summary of Regulation The Fair Credit Reporting Act (FCRA) regulates Consumer Reporting Agencies (CRAs), users of consumer reports, and furnishers of

Section 10: Fair Credit Reporting Act (FCRA) Policy Summary of Regulation The Fair Credit Reporting Act (FCRA) regulates Consumer Reporting Agencies (CRAs), users of consumer reports, and furnishers of

IMPORTANT NOTICE FOR ALL DEAL LOANS APPROVED

IMPORTANT NOTICE FOR ALL DEAL LOANS APPROVED Bank of North Dakota (BND) is required to disclose and collect specific documents from each borrower prior to disbursing the DEAL loan funds to the school.

IMPORTANT NOTICE FOR ALL DEAL LOANS APPROVED Bank of North Dakota (BND) is required to disclose and collect specific documents from each borrower prior to disbursing the DEAL loan funds to the school.

Financial Aid. Eligibility Requirements for Federal Student Aid. University of California, Irvine 2015-2016 1. On This Page:

University of California, Irvine 2015-2016 1 Financial Aid On This Page: Financial Aid Eligibility Requirements for Federal Student Aid UCI Policies on Satisfactory Academic Progress for Financial Aid

University of California, Irvine 2015-2016 1 Financial Aid On This Page: Financial Aid Eligibility Requirements for Federal Student Aid UCI Policies on Satisfactory Academic Progress for Financial Aid