2. OBJECTIVES AND METHODOLOGY 2 3. COMMITTEE FINDINGS AND RECOMMENDATIONS 3

|

|

|

- Adela Thornton

- 8 years ago

- Views:

Transcription

1 REPORT CONTENTS SECTION 1. INTRODUCTION 1.1 The Finance and Public Accounts Committee 1.2 Committee Composition 1.3 Contact PAGE OBJECTIVES AND METHODOLOGY 2 3. COMMITTEE FINDINGS AND RECOMMENDATIONS 3 Annex I: Seychelles s Responses to the Recommendations of the Auditor General 5 Annex II: Supplementary Questions by the Committee and Responses of the Seychelles 9

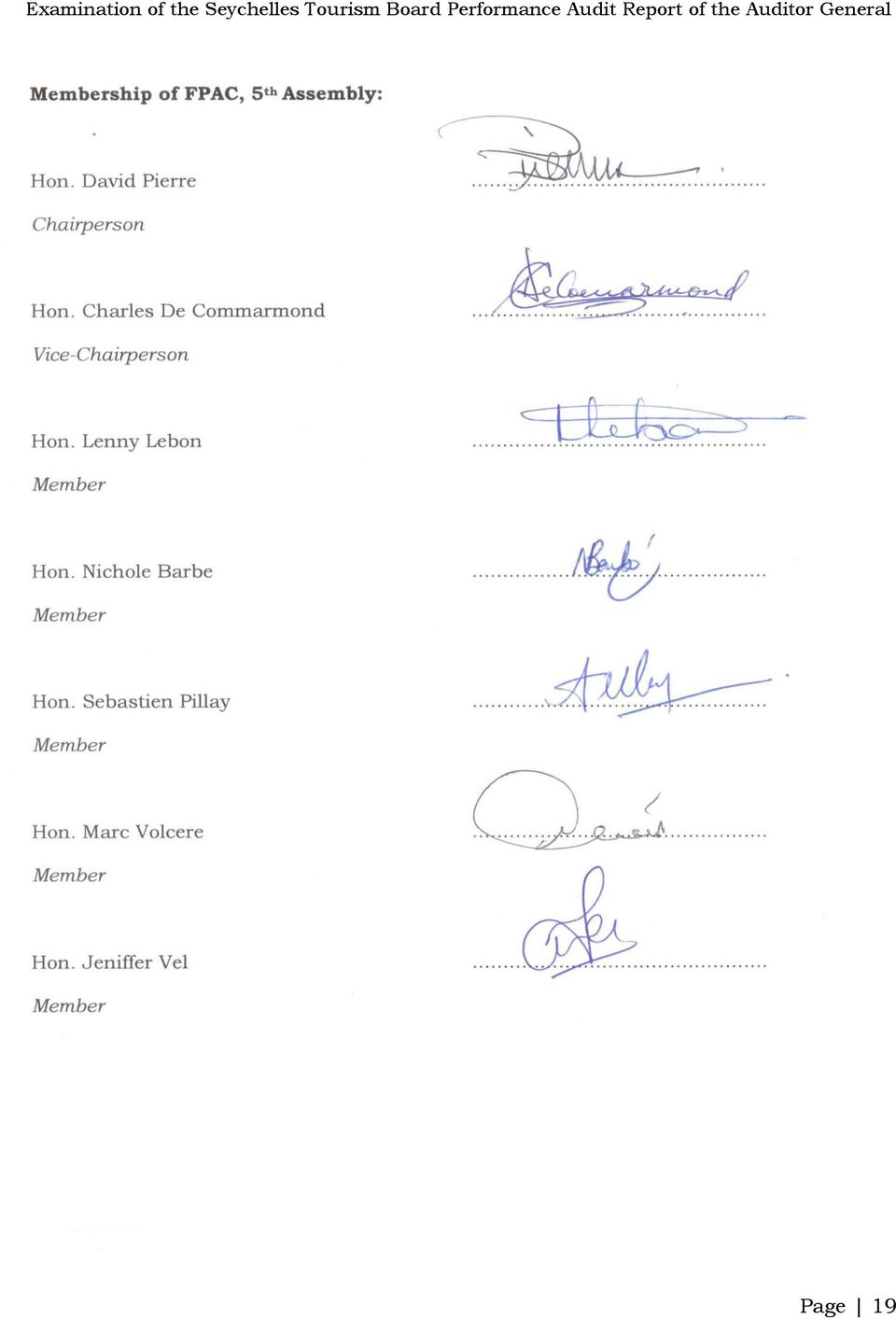

2 1. INTRODUCTION 1.1 THE FINANCE AND PUBLIC ACCOUNTS COMMITTEE The Finance and Public Accounts Committee (FPAC) is appointed by the National Assembly of Seychelles by the legal requirements of the Constitution of the Republic of Seychelles, the Standing Orders and the Rules of Procedure for Committees as the institutional mechanism for reporting on the effectiveness and efficiency of public financial management by the Government. Aside from its Annual Report which is produced from examining the Report of the Auditor General on the annual accounts of the Government, the FPAC has the mandate to scrutinize the Performance Audit Reports of the Auditor General of a particular Ministry, Department or Agency which is financed by the Government with public money. 1.2 COMMITTEE COMPOSITION The seven-members of the Committee are appointed by the National Assembly as soon as practicable after the beginning of each session of the Assembly. The current Committee appointed by the 5 th Assembly is chaired by the Leader of the Opposition and its composition is as follows: Hon. David Pierre The Chairperson Hon. Charles De Commarmond The Vice-Chairperson Hon. Marc Volcere Hon. Nichole Barbe Hon. Sebastien Pillay Hon. Lenny Lebon Hon. Jeniffer Vel Committee business is supported and facilitated by National Assembly Secretarial and Advisory personnel and is further assisted through the advice and guidance of the Auditor General. 1.3 CONTACT All correspondence relating to this report or other matters within the scope of the FPAC should in the first instance be addressed to: Committee Advisor Finance and Public Accounts Committee National Assembly of Seychelles P. O. Box 734 Ile du Port, Mahe Seychelles Tel: aappoo@nationalassembly.sc Page 1

3 2. OBJECTIVES AND METHODOLOGY In December 2011, the Auditor General published a Performance Audit Report on the Seychelles. This assignment was carried out in the period of June to October 2011 and in accordance with Section 13 of the Auditor General Act, The overall objective of this performance audit was: Whether the Seychelles has managed its offices, financial resources and stakeholder relationships well in order to ensure the success of its marketing and inspectorate roles? The report of the Auditor General centred its enquiries in three-areas: i. Seychelles s Financing and Managing of its Marketing Operations; ii. iii. Seychelles s Marketing; and Inspectorate Function of the Seychelles. The full report can be found at performance-audit-reports. The Committee conducted a Hearing on the content of the Performance Audit Report of the Auditor on the Seychelles on 12 th March The verbatim transcript of the Hearing can be found at 1:verbatims&catid=71:committees-of-the-national-assembly&Itemid=2. The Seychelles was represented at the Hearing by the current Chief Executive Officer, Mrs. Elsia Grandcourt and the Financial Controller, Mr. Jean- Francois Adeline. The Office of the Auditor General was represented at the Hearing by the Auditor General Mr. Marc Benstrong, Mrs. Marie-Lise Pierre and Mr. Antoine Fernandes in a technical and advisory role to the The issues and related recommendations of the Seychelles Performance Audit Report of the Auditor General and the responses from the Seychelles are summarised in the table shown at Annex I. Annex II provides detailed information on the supplementary questions by the Committee and the responses of the Seychelles. Page 2

4 3. COMMITTEE FINDINGS AND RECOMMENDATIONS The Committee is extremely disappointed that the senior management of the Seychelles have made limited progress in dealing with the findings and recommendations of the Performance Audit Report of the Auditor General. This is despite the report having been available for 15 months. The Seychelles has a maximum of one month from the date of the approval of this report by the National Assembly to respond to the recommendations of the The recommendations of the Committee on the Seychelles Performance Audit Report of the Auditor General are derived from the evidence from the hearing and subsequent documentation received from the Seychelles. Committee Recommendations to the Seychelles : i. The Seychelles will fully implement all seven-recommendations made by the Auditor General. ii. iii. iv. The Seychelles will provide details of the training proposals to improve the financial management skills of those currently lacking the necessary competencies. The Seychelles will provide its short to medium-term plans for implementing a star based classification scheme for hotels in the Seychelles as this is an internationally recognised standard used by potential visitors when selecting accommodation. In addition, the application of a classification scheme provides the basis for the inspection and evaluation of hotels. The Seychelles will provide the latest copy of the Cabinet Approved Tourism Master Plan. v. The Seychelles will provide a full explanation how it spent the additional R30 million received from Trade partners which were allocated to the Marketing Fund and the Operating expenses in the financial year vi. vii. viii. ix. The Seychelles will provide unambiguous evidence of an integrated operational and financial reporting system. The Seychelles will take measures to meet its statutory requirements in relation to establishing a code of practice and standards for tourism enterprises. The Seychelles will develop and implement an enforcement-driven strategy and options for enforcement actions. The Seychelles will develop and implement a risk based strategy and approach to its inspection activities. Page 3

5 x. The Seychelles will develop and distribute practical compliance guidance for the business community in respect of inspection activities. xi. xii. xiii. xiv. xv. xvi. xvii. The Seychelles will develop and introduce robust mechanisms to record visitor arrivals and produce quarterly reports on these including variances from period to period. The Seychelles will provide details of its allocated 2013 research budget and details and expected impacts of planned research activities in The Seychelles will provide evidence that the office in Singapore has now been closed and that no further rent paid other than that reported by the Auditor General. The Seychelles will provide documentary evidence of how the R6 million recorded as being spent on the Singapore office was actually spent in the China office. The Seychelles will provide detailed information on the Key Performance Indicators to be used in 2013 to measure the corporate success or failure of the organisation. The Seychelles will provide details of recommendations made by the UN-WTO Consultant to restructure the Seychelles with particular reference to the inspectorate function. The Seychelles will provide the explanation from the Licensing Authority as to why it did not revoke the licence of a tourism premise that was deemed unsatisfactory by the Seychelles inspectorate. Page 4

6 ANNEX I: SEYCHELLES TOURISM BOARD S TO THE RECOMMENDATIONS OF THE AUDITOR GENERAL PERFORMANCE AUDIT REPORT RECOMMENDATION STB RESPONSE EVALUATION OF 1. The lack of financial skills and awareness amongst the Board, senior management, and finance and non-finance staff remains a significant barrier to improving the management of financial resources in the Seychelles : Page The Seychelles should ensure that finance and nonfinance staff receives appropriate guidance, training and support in order to meet financial reporting requirements and to plan and manage budgets effectively. Currently all staff of the accounts unit who has been recruited understands the process of planning and managing budget. There are also other staff working and managing budgets... where there is still a lack of knowledge in budget preparation and management. Requests have been made for them to attend training sessions to provide them with the basic guidance to better prepare their budgets. This partially answers the Committee question. 2. Effective financial resource management is not embedded in the Seychelles : Page Managers in the Seychelles and overseas offices should be properly accountable for their financial resources and incentivised to use them effectively and efficiently. As a first-step, the Seychelles Tourism Board should build in an assessment of management of financial resources within the performance appraisal of all A uniform system of recording and reporting their financial information is done on a monthly basis. All office has to comply with this on a monthly basis as their full set of accounts is then checked for any anomalies/irregulariti es and posted into the accounting software QuickBooks. This is a satisfactory response to the Committee s question, re: the management of financial management. However, it does not provide an answer to the link between resource allocation and individual unit performance to see if the STB is achieving value for money. This issue is dealt with by an earlier recommendation in this report by the Page 5

7 PERFORMANCE AUDIT REPORT RECOMMENDATION STB RESPONSE EVALUATION OF staff, whether in the Seychelles or overseas. Committee to the STB calling for the establishment of key performance indicators. 3. The Seychelles does not integrate financial and operational performance information, making it difficult to evaluate the value-for-money of its work: Page The Financial Controller should capture information from the various sections and overseas offices and present integrated financial and operational performance data to the Board to enable it to compare costs and to establish a sound footing upon which to base decisions on resource allocation. As from August 2011, the STB has adopted and implemented the accounting package QuickBooks after which had enabled the Financial Controller to produce clear and concise financial information as addressed to the Board on a continuous basis. It is now adopting new project management software which will bring more budgetary control and thus better allocation of resources. This is a partial response to the recommendation and it is clear that much remains to be done. 4. There is a gap in the Seychelles s approach to inspection at a corporate level that is reflected in the lack of strategic leadership and published standards. The Seychelles has a key role to play in ensuring that businesses 4. The Seychelles should urgently deliver its legislative requirements to establish a code of practice and standards for tourism enterprises, so that businesses are clear about how the inspection process will operate. The Cabinet of Ministers approved back in November 2007 the National Harmonised Standards for Accommodation and Catering Enterprises; a code of practice for the tourism industry. However there were some objections from the local tourism trade and the classification project was placed on hold. Additionally, the STB This is an unsatisfactory response from the STB. Page 6

8 PERFORMANCE AUDIT REPORT operate to a high standard and thus meet visitor expectations: Page 4 5. RECOMMENDATION STB RESPONSE EVALUATION OF has also initiated the process for the introduction of a code of practice otherwise known as Standard Operating Procedures for the organisation itself. The works to prepare this document is well underway and expected completion if August The Seychelles s lack of an overall sanctioning strategy and culture weakens compliance by business. The non-existence of enforcement means that deterrence cannot be used as a way to ensure compliance: Page The Seychelles should develop an enforcement-driven strategy that delivers sanctioning options and enforcement actions proportionate to the seriousness or the persistence of compliance breach. Despite the provision of the STB Act of 2005, the STB is not a regulating body with enforcement powers. STB is always seen as a facilitator and in all its undertakings this is the preferred role. This is an unsatisfactory response from the STB. This is dealt with in an earlier recommendation in this report by the Committee to the STB. 6. The Seychelles has no coherent approach to risk and no consistent riskbased approach. We question whether the relative balance of inspection activity of the 6. We recommend that the Seychelles undertakes a review of its approach to inspection activity, building in risk as the driver for the inspection approach. STB is open to ideas for improving the service that it provides and will certainly take this recommendation on board. It must be noted however that indirectly this is being practiced by STB. This is an unsatisfactory response from the STB. This is dealt with in an earlier recommendation in this report by the Committee to the STB. Page 7

9 PERFORMANCE AUDIT REPORT Seychelles is effective across all of the areas of its remit: Page 4 5. RECOMMENDATION STB RESPONSE EVALUATION OF 7. The level of Seychelles face-to-face advice to businesses, through the inspection process, is substantial. We believe that this could be supported by published advice and guidance through the Seychelles website: Page The Seychelles should develop a strategy for inspection advice and guidance, as soon as possible, which ensures that businesses can and do receive quality practical advice on what to do in order to comply. We don t have the published documents, when the client will come to STB this is given to them and guidance is given. This is an unsatisfactory response from the STB. This is dealt with in an earlier recommendation in this report by the Committee to the STB. Page 8

10 ANNEX II: SUPPLEMENTARY QUESTIONS BY THE COMMITTEE AND OF THE SEYCHELLES TOURISM BOARD REPORT COMMITTEE QUESTIONS STB EVALUATION OF Background: What are you doing to increase market share? We continue with our, especially on our traditional markets, we continue with the marketing activities that is there to further grow the business, but we also look at diversification in going into new markets. This is a vague response to the question put by the However, the answer to this question should be shown in the Tourism Master Plan requested by the Committee in an in this report. How did you maintain a budget of R76.3 m? We managed to keep in within the allocation that was given and managed to fulfil the activities and all the plans and targets that had been set for the year. This more or less answers the question posed by the Strengthening the Strategic Approach: 1.7 Why was it that since 2005, you have been operating without a formal organizational strategy? Unfortunately I cannot explain what was there in the past why it was not done or implemented. question posed by the Is STB currently adopting a formal organizational strategy? From 2010 onwards I would say, we have started out, we ve mapped out, first it was a 5 year plan strategy and then every year we have strategy that is spelled out for the year and then further details are per the different markets. question posed by the What strategy are We have a strategy that Page 9

11 REPORT COMMITTEE QUESTIONS you using? STB at our annual meeting which we do together with the private sector, it s public, we publicize it, it was presented to all the private sector and whoever wants to have a copy of it. EVALUATION OF question posed by the Tourism Master Plan: 1.9 Has the Tourism Master Plan been completed? Today yes, the Master Plan is final, it s been presented to the Cabinet, it s been endorsed, there are recommendations, set key recommendations that have come out of there and recommendations are already being undertaken. Management of Finance is a Continuing Challenge: What is the status of your financial accounts? To date we have done 2007, it s been audited already, 2008 has been audited as well, 2009 and now, actually tomorrow they are coming to the office to do 2010 up till questions posed by the Since 2007 you have continuously been late with the submission of your financial accounts, what are you doing to improve this situation? One of my, my greatest, my mandate when I joined the STB is to clear the backlog, one of my priority. So, I can give you assurance that it will be. questions posed by the What was the R30 million additional funds used for in 2010? Was it used for the Marketing Yes there was the Sub- Marketing Committee and this precisely was for marketing. But can we give you This is not a satisfactory answer to the questions put by the Page 10

12 REPORT COMMITTEE QUESTIONS Fund Committee? STB more clarity. EVALUATION OF Importance of Incisive Leadership in the Management of Finance: 1.17 & 1.22 You have had 5 Financial Controllers in the last 6 years, what are you doing to ensure that this is not the case again for the next 5 or 6 years to come? What have we done is to in the first step to look at where the problem was and now that we have a Financial Controller we have a team as well that supports the work that is being done. We ve had constant dialogue and also close monitoring with the Financial Controller. question posed by the Have you made any attempt to evaluate the impact of this, and if yes, what are the results of this evaluation? No response. Can you honestly say that you now have a strong financial management system in place? I can, at the moment safely say yes, confidently to a degree that yes the accounting and financing yes is being followed properly. question posed by the STB Culture of Increasing Expenditure Coupled with Lack of Financial Management: 1.24 Has this area been reviewed? It s been referred to on numerous counts in this report that we focus only on the visitor arrivals, but there are also other measures whereby the performance is monitored. We have our annual report that is produced yearly, now we ve introduced that, we did the first one last year and this year also we re in the process of finalizing. We have the This is not a satisfactory response to the question put by the Page 11

13 REPORT COMMITTEE QUESTIONS STB monthly reports that are forwarded by our offices, whereby we monitor the activities that are done. EVALUATION OF Cost Effectiveness of Marketing: 1.29 Have you given this a priority? What have you achieved so far? I would say, once we have the system that we are now implementing it gives us a clear picture on once we venture into certain activities on certain markets... And looking at where the money is being spent and seeing the feedback we re getting it helps us to better plan and like I said initially, it helps us to be more smart in the approach that we take towards the different activities being undertaken in the various markets. questions put by the Core European Market: 2.6 Why has there been a gradual decrease in the ratio of European visitors as a percentage of the overall total? Because there was no proper mechanism to follow it and of course the arrival figures went down. This does not answer the question posed by the STB s Overseas Representation: 2.9, 2.12 & 2.13 How were the overseas offices operating without proper record keeping? Unfortunately I cannot really explain that part. Back then there was a problem with their accounting software they were using and probably no proper records were kept. This is an unsatisfactory response to the Committee question. Who was managing their In terms of who was the Financial Controller then, Committee s question. Page 12

14 REPORT COMMITTEE QUESTIONS finances? STB the latest one I know before the current one we have was Mr. Domingue. EVALUATION OF What kind of research or surveys does the STB conduct to measure or value effectively the impact and outcomes of its marketing? The research that we are doing is not only based at the trade, but consumer as well, and also it s looking at the different market segmentation to further develop our different niche markets that we have at base. Committee s question. Why don t you feel that research is a priority? The allocation to research was not significant then, but we have re-looked at that because we realize the importance, especially now that we are going into new emerging markets. This partially answers the Committee s question. Asian Office Impact: 2.25 Why is STB still paying rental charges if the office is nonoperational? The Singapore office was closed when it was almost during the same time that Air Seychelles ceased the operation in Singapore which was as at early 2011, but the office was unmanned. But where it says here that it was unmanned, it was not unmanned it was the presence of the Director that was not there. But we had STB personnel there and we were in the process of deciding to put a Manager to take over from whoever had moved. This partially answers the Committee s question. This now is engulfed by This partially answers Page 13

15 REPORT COMMITTEE QUESTIONS What has happened to the R6 million allocated in the 2011 budget for the Singapore office? STB the China office. EVALUATION OF the Committee s question. Success is Managed Through Arrival Numbers Only: 2.38 What means of measuring success are you using currently? We have the monthly reports that we receive from the office based on the activities that is done. And also we are looking at the press clippings that come in and the various feedback that we get from the trade as well. Although this only partially addresses the question of the Committee this issue is dealt with by an earlier recommendation in this report by the Do you find it as a useful indicator of performance? But we are also in the process of re-looking at how we measure the performance of the output that we have on the marketing. We are in the process of re-looking also at specific rating indicating to performance. Partial response to the question from the Code of Practice and Standards: Why is STB not complying with their Act? With regards to compliance to the Act, there is the criteria set that the SP uses when we go out into the monitoring or visiting of the establishments when we go out with the other bodies. We realise that we don t have such a document but the importance of having it we ve realised that it s there. Page 14

16 REPORT COMMITTEE QUESTIONS Why have you made no further progress towards meeting the requirements of the Act, despite the approval of Cabinet? STB The harmonised standards that were approved by the Cabinet has not been delivered I would say probably because of these issues that was there which needs to be re-looked at. EVALUATION OF Has this monitoring programme been put into action? Not at the moment, not as yet. Work of the Inspectorate: 3.19 Are all establishments being inspected currently? Not necessarily so. I would say today based on the inspection being done we do more than 50%, even more than that. What strategy are you using for inspection? It s under discussion now because we had also a UN/WTO Consultant coming to look at the structure of STB, now that we fall under Ministry on how the operation will be, certain recommendations have been made in regards to this structure. This is a partial response to the question posed by the There is a Lack of Proactive Management Support for the Standards and Product Enhancement Section: 3.25, 3.26 & 3.29 Has a decision been taken to separate the Inspectorate function from STB? Why was the previous CEO not in favour of the Standards and You re marketing a destination and the product which is important so it goes hand in hand. So, for the moment it s not separated yet. Would it work to separate it if you have a proper mechanism in place because there is a Page 15

17 REPORT COMMITTEE QUESTIONS Product Enhancement Section being part of STB? STB certain degree of overlap. EVALUATION OF Has this issue been addressed? Has the STB taken a step to develop a coherent view and understanding of the inspectorate role and requirements? But what I have done with the HR is re-looked at how for example the going out for the inspections and I won t say they have low morale right now I think they are more or less hopeful that something will be done about this section. The Inspectorate Section has no Enforcement Powers: 3.32 Has there been any move to amend the STB Act with respect to this issue? or, No. We still today don t have the enforcement ability. Have you developed any enforcement capabilities as proposed by the Auditor General outside of the Act? No. Transparent Reporting Making Businesses and the Public Aware and Getting them on Board: Is this being done? Have you implemented the rating system? 3.34 yes, the annual reporting, but it s only like I said the publishing of the inspectorate work that is not there, but the annual report is. If we implemented it yet, no, but it was a point that was discussed at our last year s marketing meeting and it s a point that we will take up, we This is a partial answer to the Committee s question. Page 16

18 REPORT COMMITTEE QUESTIONS STB should take it up along the year. But we haven t started anything yet. EVALUATION OF Liaising with and Understanding Businesses: 3.36, 3.40 & 3.41 Are you conducting this analysis to identify problems within businesses? Yes we are engaging with the businesses, it s through the various forums, meetings that they have. question of the Have you published any documents with guidance and/or advice to businesses? We don t have the published documents, but the set criteria are there. Did the Seychelles Licensing Authority provide any explanations as to why they did not revoke that license? I would have to re-visit the case. This does not answer the question put by the Why was no action taken against that particular business? Unable to respond as the decision was taken by the Seychelles Licensing Authority. Have you developed that kind of relationship yet to ensure that SLA delivers a consistent approach/respons e? Well, I suppose now with the new structure and, I mean not a new structure, but being within a Ministry it s like it has to be decided to what extent we allow STB to say ok,. and say that the place has to be closed down. This does not answer the question put by the Committee and is dealt with in an earlier recommendation in this report by the Page 17

19 REPORT COMMITTEE QUESTIONS STB EVALUATION OF Performance Management: 3.43 What is senior management doing to solve this issue? Because the inspectors that are within that section has been there for a long time now, they ve established a rapport with the different operators that are there, and before yes, the perception was that they come in and they re more or less looked at as, you re not helping them with it but the approach I think has changed now and the inspectors they are very much aware of this on how they approach when they go to these establishments. This does not answer the question put by the Committee and is dealt with in an earlier recommendation in this report by the Page 18

20 Page 19

Commission for Ethical Standards in Public Life in Scotland

Commission for Ethical Standards in Public Life in Scotland REPORT TO PARLIAMENT Laid before the Scottish Parliament by the Public Appointments Commissioner for Scotland in pursuance of Section 2(8) a

Commission for Ethical Standards in Public Life in Scotland REPORT TO PARLIAMENT Laid before the Scottish Parliament by the Public Appointments Commissioner for Scotland in pursuance of Section 2(8) a

LORD CHANCELLOR S CODE OF PRACTICE ON THE MANAGEMENT OF RECORDS UNDER

LORD CHANCELLOR S CODE OF PRACTICE ON THE MANAGEMENT OF RECORDS UNDER SECTION 46 OF THE FREEDOM OF INFORMATION ACT 2000 NOVEMBER 2002 Presented to Parliament by the Lord Chancellor Pursuant to section

LORD CHANCELLOR S CODE OF PRACTICE ON THE MANAGEMENT OF RECORDS UNDER SECTION 46 OF THE FREEDOM OF INFORMATION ACT 2000 NOVEMBER 2002 Presented to Parliament by the Lord Chancellor Pursuant to section

Rolls Royce s Corporate Governance ADOPTED BY RESOLUTION OF THE BOARD OF ROLLS ROYCE HOLDINGS PLC ON 16 JANUARY 2015

Rolls Royce s Corporate Governance ADOPTED BY RESOLUTION OF THE BOARD OF ROLLS ROYCE HOLDINGS PLC ON 16 JANUARY 2015 Contents INTRODUCTION 2 THE BOARD 3 ROLE OF THE BOARD 5 TERMS OF REFERENCE OF THE NOMINATIONS

Rolls Royce s Corporate Governance ADOPTED BY RESOLUTION OF THE BOARD OF ROLLS ROYCE HOLDINGS PLC ON 16 JANUARY 2015 Contents INTRODUCTION 2 THE BOARD 3 ROLE OF THE BOARD 5 TERMS OF REFERENCE OF THE NOMINATIONS

GOVERNANCE AND ACCOUNTILIBILITY FRAMEWORK 2012-2013

Schedule 4.1 STANDING ORDERS FOR THE WELSH HEALTH SPECIALISED SERVICES COMMITTEE See separate document: Schedule 4.1 This Schedule forms part of, and shall have effect as if incorporated in the Local Health

Schedule 4.1 STANDING ORDERS FOR THE WELSH HEALTH SPECIALISED SERVICES COMMITTEE See separate document: Schedule 4.1 This Schedule forms part of, and shall have effect as if incorporated in the Local Health

Implementation Plan: Development of an asset and financial planning management. Australian Capital Territory

Implementation Plan: Development of an asset and financial planning management framework for TAMS Australian Capital Territory NATIONAL PARTNERSHIP AGREEMENT TO SUPPORT LOCAL GOVERNMENT AND REGIONAL DEVELOPMENT

Implementation Plan: Development of an asset and financial planning management framework for TAMS Australian Capital Territory NATIONAL PARTNERSHIP AGREEMENT TO SUPPORT LOCAL GOVERNMENT AND REGIONAL DEVELOPMENT

PRESIDENT'S OFFICE. No. 1901. 27 November 1996 NO. 102 OF 1996: NATIONAL SMALL BUSINESS ACT, 1996.

PRESIDENT'S OFFICE No. 1901. 27 November 1996 NO. 102 OF 1996: NATIONAL SMALL BUSINESS ACT, 1996. It is hereby notified that the President has assented to the following Act which is hereby published for

PRESIDENT'S OFFICE No. 1901. 27 November 1996 NO. 102 OF 1996: NATIONAL SMALL BUSINESS ACT, 1996. It is hereby notified that the President has assented to the following Act which is hereby published for

Inspection Wales Remit Paper

Inspection Wales Remit Paper A summary of the remits of the Welsh public sector audit and inspection bodies and the Inspection Wales Programme Issued: July 2015 Document reference: 376A2015 Contents Summary

Inspection Wales Remit Paper A summary of the remits of the Welsh public sector audit and inspection bodies and the Inspection Wales Programme Issued: July 2015 Document reference: 376A2015 Contents Summary

College Governance Statement of Principles, Scheme of Delegation and Terms of Reference

College Governance Statement of Principles, Scheme of Delegation and Terms of Reference 1. Principles: 1.1 Background This document sets out the principles underpinning the College Corporation s work.

College Governance Statement of Principles, Scheme of Delegation and Terms of Reference 1. Principles: 1.1 Background This document sets out the principles underpinning the College Corporation s work.

Consultation: Auditing and ethical standards

Consultation Financial Reporting Council December 2014 Consultation: Auditing and ethical standards Implementation of the EU Audit Directive and Audit Regulation The FRC is responsible for promoting high

Consultation Financial Reporting Council December 2014 Consultation: Auditing and ethical standards Implementation of the EU Audit Directive and Audit Regulation The FRC is responsible for promoting high

Agenda item number: 5 FINANCE AND PERFORMANCE MANAGEMENT OVERVIEW AND SCRUTINY COMMITTEE FUTURE WORK PROGRAMME

Agenda item number: 5 COMMITTEE FINANCE AND PERFORMANCE MANAGEMENT OVERVIEW AND SCRUTINY COMMITTEE DATE TUESDAY 17 JUNE 2003 TITLE OF REPORT RESPONSIBLE OFFICER FUTURE WORK PROGRAMME Ann Joyce, Head of

Agenda item number: 5 COMMITTEE FINANCE AND PERFORMANCE MANAGEMENT OVERVIEW AND SCRUTINY COMMITTEE DATE TUESDAY 17 JUNE 2003 TITLE OF REPORT RESPONSIBLE OFFICER FUTURE WORK PROGRAMME Ann Joyce, Head of

Code of Corporate Governance

www.surreycc.gov.uk Making Surrey a better place Code of Corporate Governance October 2013 1 This page is intentionally blank 2 CONTENTS PAGE Commitment to good governance 4 Good governance principles

www.surreycc.gov.uk Making Surrey a better place Code of Corporate Governance October 2013 1 This page is intentionally blank 2 CONTENTS PAGE Commitment to good governance 4 Good governance principles

Corporate Governance Statement

Corporate Governance Statement The Board of Directors of APN Outdoor Group Limited (APO) is responsible for the overall corporate governance of APO, including establishing the corporate governance framework

Corporate Governance Statement The Board of Directors of APN Outdoor Group Limited (APO) is responsible for the overall corporate governance of APO, including establishing the corporate governance framework

Corporate Health and Safety Policy

Corporate Health and Safety Policy Publication code: ED-1111-003 Contents Foreword 2 Health and Safety at Work Statement 3 1. Organisation and Responsibilities 5 1.1 The Board 5 1.2 Chief Executive 5 1.3

Corporate Health and Safety Policy Publication code: ED-1111-003 Contents Foreword 2 Health and Safety at Work Statement 3 1. Organisation and Responsibilities 5 1.1 The Board 5 1.2 Chief Executive 5 1.3

GOVERNMENT OF BERMUDA Ministry of Education. Public School Reorganization: A Consultation

GOVERNMENT OF BERMUDA Ministry of Education Public School Reorganization: A Consultation March 2015 GOVERNMENT OF BERMUDA Ministry of Education 14 Waller s Point Road St. David s DD 03 Bermuda P.O. Box

GOVERNMENT OF BERMUDA Ministry of Education Public School Reorganization: A Consultation March 2015 GOVERNMENT OF BERMUDA Ministry of Education 14 Waller s Point Road St. David s DD 03 Bermuda P.O. Box

Health and Safety Policy Part 1 Policy and organisation

Health and Safety Policy Part 1 Policy and organisation ICO H&S Policy Policy and organisation, June 2014 Page 1 of 6 1. Scope 1.1 The Health and Safety policy applies to all employees of the Information

Health and Safety Policy Part 1 Policy and organisation ICO H&S Policy Policy and organisation, June 2014 Page 1 of 6 1. Scope 1.1 The Health and Safety policy applies to all employees of the Information

Financial Services Guidance Note Outsourcing

Financial Services Guidance Note Issued: April 2005 Revised: August 2007 Table of Contents 1. Introduction... 3 1.1 Background... 3 1.2 Definitions... 3 2. Guiding Principles... 5 3. Key Risks of... 14

Financial Services Guidance Note Issued: April 2005 Revised: August 2007 Table of Contents 1. Introduction... 3 1.1 Background... 3 1.2 Definitions... 3 2. Guiding Principles... 5 3. Key Risks of... 14

F I N A N C I A L R E G U L A T I O N S

F I N A N C I A L R E G U L A T I O N S South Downs National Park Authority March 2014 Page 0 of 17 F I N A N C I A L R E G U L A T I O N S Contents Page 1 INTRODUCTION Purpose of Financial Regulations

F I N A N C I A L R E G U L A T I O N S South Downs National Park Authority March 2014 Page 0 of 17 F I N A N C I A L R E G U L A T I O N S Contents Page 1 INTRODUCTION Purpose of Financial Regulations

Request for feedback on the revised Code of Governance for NHS Foundation Trusts

Request for feedback on the revised Code of Governance for NHS Foundation Trusts Introduction 8 November 2013 One of Monitor s key objectives is to make sure that public providers are well led. To this

Request for feedback on the revised Code of Governance for NHS Foundation Trusts Introduction 8 November 2013 One of Monitor s key objectives is to make sure that public providers are well led. To this

October 2014. Board Member Recruitment

October 2014 Board Member Recruitment Queens Cross Housing Association is an innovative and dynamic communitybased housing association located in the north west of Glasgow. The housing sector is facing

October 2014 Board Member Recruitment Queens Cross Housing Association is an innovative and dynamic communitybased housing association located in the north west of Glasgow. The housing sector is facing

There is strong Government. Uganda: performance contracting, budget reporting and budget monitoring SUMMARY

COUNTRY LEARNING NOTES Uganda: performance contracting, budget reporting and budget monitoring Margaret Kakande & Natasha Sharma * July 2012 SUMMARY The Government of Uganda has introduced performance

COUNTRY LEARNING NOTES Uganda: performance contracting, budget reporting and budget monitoring Margaret Kakande & Natasha Sharma * July 2012 SUMMARY The Government of Uganda has introduced performance

INSPECTION MANUAL FOR CREDIT RATING AGENCIES

Tentative translation Only Japanese text is authentic INSPECTION MANUAL FOR FINANCIAL INSTRUMENTS BUSINESS OPERATORS (SUPPLEMENT) INSPECTION MANUAL FOR CREDIT RATING AGENCIES Executive Bureau, Securities

Tentative translation Only Japanese text is authentic INSPECTION MANUAL FOR FINANCIAL INSTRUMENTS BUSINESS OPERATORS (SUPPLEMENT) INSPECTION MANUAL FOR CREDIT RATING AGENCIES Executive Bureau, Securities

How To Be Accountable To The Health Department

CQC Corporate Governance Framework Introduction This document describes the components of CQC s Corporate Governance Framework: what it is intended to achieve, what the components of the Framework are

CQC Corporate Governance Framework Introduction This document describes the components of CQC s Corporate Governance Framework: what it is intended to achieve, what the components of the Framework are

Telford College of Arts and Technology

FURTHER EDUCATION COMMISSIONER ASSESSMENT SUMMARY Telford College of Arts and Technology JANUARY 2016 Assessment Background Telford College of Arts and Technology (TCAT) is a medium sized general FE College

FURTHER EDUCATION COMMISSIONER ASSESSMENT SUMMARY Telford College of Arts and Technology JANUARY 2016 Assessment Background Telford College of Arts and Technology (TCAT) is a medium sized general FE College

Budget development and management within departments

V I C T O R I A Auditor General Victoria Budget development and management within departments Ordered to be printed by Authority. Government Printer for the State of Victoria No. 39, Session 2003-2004

V I C T O R I A Auditor General Victoria Budget development and management within departments Ordered to be printed by Authority. Government Printer for the State of Victoria No. 39, Session 2003-2004

Steve Turpie, Chair of Audit Committee David Swales, Assistant Director of Finance

PRESENTED BY: PREPARED BY: DATE PREPARED: 27 June 2013 1 Background 1.1 The Audit Committee of West Suffolk NHS Foundation Trust is established under Board delegation with approved Terms of Reference that

PRESENTED BY: PREPARED BY: DATE PREPARED: 27 June 2013 1 Background 1.1 The Audit Committee of West Suffolk NHS Foundation Trust is established under Board delegation with approved Terms of Reference that

GLASGOW SCHOOL OF ART OCCUPATIONAL HEALTH AND SAFETY POLICY. 1. Occupational Health and Safety Policy Statement 1

GLASGOW SCHOOL OF ART OCCUPATIONAL HEALTH AND SAFETY POLICY CONTENTS PAGE 1. Occupational Health and Safety Policy Statement 1 2. Occupational Health and Safety Management System 2 3. Organisational Management

GLASGOW SCHOOL OF ART OCCUPATIONAL HEALTH AND SAFETY POLICY CONTENTS PAGE 1. Occupational Health and Safety Policy Statement 1 2. Occupational Health and Safety Management System 2 3. Organisational Management

Business Plan 2016-2017

Business Plan 2016-2017 March 2016 Contents Introduction... 3 About us... 5 Role of Registrar... 5 Objectives for 2016-17... 5 Work programme for 2016/17... 6 Activity 1 Continue to operate an accessible,

Business Plan 2016-2017 March 2016 Contents Introduction... 3 About us... 5 Role of Registrar... 5 Objectives for 2016-17... 5 Work programme for 2016/17... 6 Activity 1 Continue to operate an accessible,

PUREPROFILE LTD. ACN 167 522 901 CONTINUOUS DISCLOSURE AND COMMUNICATION POLICY

PUREPROFILE LTD. ACN 167 522 901 CONTINUOUS DISCLOSURE AND COMMUNICATION POLICY Contents 1 Overview 3 2 Continuous Disclosure Requirements and Procedures 3 3 Disclosure Responsibilities 4 4 Potentially

PUREPROFILE LTD. ACN 167 522 901 CONTINUOUS DISCLOSURE AND COMMUNICATION POLICY Contents 1 Overview 3 2 Continuous Disclosure Requirements and Procedures 3 3 Disclosure Responsibilities 4 4 Potentially

PUBLIC FINANCE MANAGEMENT ACT

LAWS OF KENYA PUBLIC FINANCE MANAGEMENT ACT CHAPTER 412C Revised Edition 2014 [2013] Published by the National Council for Law Reporting with the Authority of the Attorney-General www.kenyalaw.org [Rev.

LAWS OF KENYA PUBLIC FINANCE MANAGEMENT ACT CHAPTER 412C Revised Edition 2014 [2013] Published by the National Council for Law Reporting with the Authority of the Attorney-General www.kenyalaw.org [Rev.

KATHARINE HOUSE HOSPICE JOB DESCRIPTION. Advanced Nurse Practitioner (Independent Prescriber)

") KATHARINE HOUSE HOSPICE JOB DESCRIPTION Advanced Nurse Practitioner (Independent Prescriber) Post Holder: Area of Work: Responsible to: Vacant Day Therapies Director of Nursing Services Mission To offer

KATHARINE HOUSE HOSPICE JOB DESCRIPTION Advanced Nurse Practitioner (Independent Prescriber) Post Holder: Area of Work: Responsible to: Vacant Day Therapies Director of Nursing Services Mission To offer

FOREIGN INVESTMENT COMMITTEE

FOREIGN INVESTMENT COMMITTEE GUIDELINE ON THE ACQUISITION OF INTERESTS, MERGERS AND TAKE-OVERS BY LOCAL AND FOREIGN INTERESTS Economic Planning Unit, Prime Minister s Department CONTENTS I. INTRODUCTION...

FOREIGN INVESTMENT COMMITTEE GUIDELINE ON THE ACQUISITION OF INTERESTS, MERGERS AND TAKE-OVERS BY LOCAL AND FOREIGN INTERESTS Economic Planning Unit, Prime Minister s Department CONTENTS I. INTRODUCTION...

Introduction to Guest House Classification Scheme. Registration & Classification

Registration & Classification 1. INTRODUCTION 1.1. Fáilte Ireland 1.2. Registration and Classification 2. MANDATORY GUEST HOUSE CLASSIFICATION SCHEME 2.1. Minimum Requirements 2.2. Point Scoring Opportunities

Registration & Classification 1. INTRODUCTION 1.1. Fáilte Ireland 1.2. Registration and Classification 2. MANDATORY GUEST HOUSE CLASSIFICATION SCHEME 2.1. Minimum Requirements 2.2. Point Scoring Opportunities

PUBLIC FINANCE MANAGEMENT ACT NO. 1 OF 1999

PUBLIC FINANCE MANAGEMENT ACT NO. 1 OF 1999 as amended by Public Finance Management Amendment Act, No. 29 of 1999 ACT To regulate financial management in the national government and provincial governments;

PUBLIC FINANCE MANAGEMENT ACT NO. 1 OF 1999 as amended by Public Finance Management Amendment Act, No. 29 of 1999 ACT To regulate financial management in the national government and provincial governments;

MALAYSIAN CODE ON CORPORATE GOVERNANCE

MALAYSIAN CODE ON CORPORATE GOVERNANCE 2012 ii Malaysian Code on Corporate Governance 2012 Contents iii CONTENTS Foreword v Corporate Governance in Malaysia ix Corporate Governance Principles and Recommendations

MALAYSIAN CODE ON CORPORATE GOVERNANCE 2012 ii Malaysian Code on Corporate Governance 2012 Contents iii CONTENTS Foreword v Corporate Governance in Malaysia ix Corporate Governance Principles and Recommendations

AGENCY MANAGEMENT FRAMEWORK FOR INSURANCE AGENT

GENERAL INSURANCE ASSOCIATION OF SINGAPORE AGENCY MANAGEMENT FRAMEWORK FOR INSURANCE AGENT APPENDIX B1 OF GIARR General Insurance Association of Singapore 180 Cecil Street, #15-01 Bangkok Bank Building

GENERAL INSURANCE ASSOCIATION OF SINGAPORE AGENCY MANAGEMENT FRAMEWORK FOR INSURANCE AGENT APPENDIX B1 OF GIARR General Insurance Association of Singapore 180 Cecil Street, #15-01 Bangkok Bank Building

Code of Audit Practice

Code of Audit Practice APRIL 2015 Code of Audit Practice Published pursuant to Schedule 6 Para 2 of the Local Audit and Accountability This document is available on our website at: www.nao.org.uk/ consultation-code-audit-practice

Code of Audit Practice APRIL 2015 Code of Audit Practice Published pursuant to Schedule 6 Para 2 of the Local Audit and Accountability This document is available on our website at: www.nao.org.uk/ consultation-code-audit-practice

Job Description. Legal Services. Organisation Advertising Description. Fixed term for 12 months. Grade Grade 8

Job Description Post Title and Post Number Organisation Advertising Description Post Number Full Time/Part Time Duration Post is open to: Employment Solicitor - 42643Z2015 Legal Services 42643Z2015 Part

Job Description Post Title and Post Number Organisation Advertising Description Post Number Full Time/Part Time Duration Post is open to: Employment Solicitor - 42643Z2015 Legal Services 42643Z2015 Part

1.1 Terms of Reference Y P N Comments/Areas for Improvement

1 Scope of Internal Audit 1.1 Terms of Reference Y P N Comments/Areas for Improvement 1.1.1 Do Terms of Reference: a) Establish the responsibilities and objectives of IA? b) Establish the organisational

1 Scope of Internal Audit 1.1 Terms of Reference Y P N Comments/Areas for Improvement 1.1.1 Do Terms of Reference: a) Establish the responsibilities and objectives of IA? b) Establish the organisational

Information Governance Strategy :

Item 11 Strategy Strategy : Date Issued: Date To Be Reviewed: VOY xx Annually 1 Policy Title: Strategy Supersedes: All previous Strategies 18/12/13: Initial draft Description of Amendments 19/12/13: Update

Item 11 Strategy Strategy : Date Issued: Date To Be Reviewed: VOY xx Annually 1 Policy Title: Strategy Supersedes: All previous Strategies 18/12/13: Initial draft Description of Amendments 19/12/13: Update

Regulators Code July 2013

July 2013 Foreword In the Autumn Statement 2012 Government announced that it would introduce a package of measures to improve the way regulation is delivered at the frontline such as the Focus on Enforcement

July 2013 Foreword In the Autumn Statement 2012 Government announced that it would introduce a package of measures to improve the way regulation is delivered at the frontline such as the Focus on Enforcement

Healthwatch Oxfordshire Board of Directors

Healthwatch Oxfordshire Board of Directors Date of Meeting: October 14 th 2014 Paper No: 9 Title of Presentation: Amendments to contract with OCC This paper is for Discussion Decision x Information Purpose

Healthwatch Oxfordshire Board of Directors Date of Meeting: October 14 th 2014 Paper No: 9 Title of Presentation: Amendments to contract with OCC This paper is for Discussion Decision x Information Purpose

Declaration to be submitted by directors in the Applicant Company 1

Form SNBFI/D1 Name of the Applicant Company: Declaration to be submitted by directors in the Applicant Company 1 1. Personal Details 1.1 Full name: 1.2 National Identity Card number: 1.3 Passport number:

Form SNBFI/D1 Name of the Applicant Company: Declaration to be submitted by directors in the Applicant Company 1 1. Personal Details 1.1 Full name: 1.2 National Identity Card number: 1.3 Passport number:

States of Jersey Comptroller & Auditor General

States of Jersey Comptroller & Auditor General Code of Audit Practice (Prepared under Article 18 of the Comptroller and Auditor General (Jersey) Law 2014) 28 November 2014 Foreword Independent external

States of Jersey Comptroller & Auditor General Code of Audit Practice (Prepared under Article 18 of the Comptroller and Auditor General (Jersey) Law 2014) 28 November 2014 Foreword Independent external

CHARTER TIO Board of Directors

CHARTER TIO Board of Directors Date: 3 June 2014 TIO Board of Directors Charter Introduction This Charter has been adopted by the Board of Directors of Telecommunications Industry Ombudsman Limited (TIO

CHARTER TIO Board of Directors Date: 3 June 2014 TIO Board of Directors Charter Introduction This Charter has been adopted by the Board of Directors of Telecommunications Industry Ombudsman Limited (TIO

Compliance Review Report Internal Audit and Risk Management Policy for the New South Wales Public Sector

Compliance Review Report Internal Audit and Risk Management Policy for the New South Wales Public Sector Background The Treasury issued TPP 09-05 Internal Audit and Risk Management Policy for the New South

Compliance Review Report Internal Audit and Risk Management Policy for the New South Wales Public Sector Background The Treasury issued TPP 09-05 Internal Audit and Risk Management Policy for the New South

Records management in English local government: the effect of Freedom of Information. Elizabeth Shepherd e.shepherd@ucl.ac.uk

Records management in English local government: the effect of Freedom of Information Elizabeth Shepherd e.shepherd@ucl.ac.uk Overview of presentation Research context: FOI Act 2000; role of Information

Records management in English local government: the effect of Freedom of Information Elizabeth Shepherd e.shepherd@ucl.ac.uk Overview of presentation Research context: FOI Act 2000; role of Information

Industrial Accidents - A Review of the Procurement Act, 2005

Protocol to ensure the provision of forensic pathology services in the event of regulatory action taken by the Human Tissue Authority in England and Wales Version: 2.4 Approved by: Last Amendment: 14th

Protocol to ensure the provision of forensic pathology services in the event of regulatory action taken by the Human Tissue Authority in England and Wales Version: 2.4 Approved by: Last Amendment: 14th

GUIDELINE NO. 22 REGULATORY AUDITS OF ENERGY BUSINESSES

Level 37, 2 Lonsdale Street Melbourne 3000, Australia Telephone.+61 3 9302 1300 +61 1300 664 969 Facsimile +61 3 9302 1303 GUIDELINE NO. 22 REGULATORY AUDITS OF ENERGY BUSINESSES ENERGY INDUSTRIES JANUARY

Level 37, 2 Lonsdale Street Melbourne 3000, Australia Telephone.+61 3 9302 1300 +61 1300 664 969 Facsimile +61 3 9302 1303 GUIDELINE NO. 22 REGULATORY AUDITS OF ENERGY BUSINESSES ENERGY INDUSTRIES JANUARY

HEWLETT-PACKARD COMPANY CORPORATE GOVERNANCE GUIDELINES

HEWLETT-PACKARD COMPANY CORPORATE GOVERNANCE GUIDELINES These Corporate Governance Guidelines have been adopted by the Board of Directors (the Board ) of Hewlett-Packard Company ( HP ). These guidelines,

HEWLETT-PACKARD COMPANY CORPORATE GOVERNANCE GUIDELINES These Corporate Governance Guidelines have been adopted by the Board of Directors (the Board ) of Hewlett-Packard Company ( HP ). These guidelines,

PUBLIC FINANCE MANAGEMENT ACT NO. 1 OF 1999

PUBLIC FINANCE MANAGEMENT ACT NO. 1 OF 1999 [ASSENTED TO 2 MARCH, 1999] [DATE OF COMMENCEMENT: 1 APRIL, 2000] (Unless otherwise indicated) (English text signed by the President) NATIONAL TREASURY This

PUBLIC FINANCE MANAGEMENT ACT NO. 1 OF 1999 [ASSENTED TO 2 MARCH, 1999] [DATE OF COMMENCEMENT: 1 APRIL, 2000] (Unless otherwise indicated) (English text signed by the President) NATIONAL TREASURY This

INTERNAL REGULATIONS OF THE AUDIT AND COMPLIANCE COMMITEE OF BBVA COLOMBIA

ANNEX 3 INTERNAL REGULATIONS OF THE AUDIT AND COMPLIANCE COMMITEE OF BBVA COLOMBIA (Hereafter referred to as the Committee) 1 INDEX CHAPTER I RULES OF PROCEDURE OF THE BOARD OF DIRECTORS 1 NATURE 3 2.

ANNEX 3 INTERNAL REGULATIONS OF THE AUDIT AND COMPLIANCE COMMITEE OF BBVA COLOMBIA (Hereafter referred to as the Committee) 1 INDEX CHAPTER I RULES OF PROCEDURE OF THE BOARD OF DIRECTORS 1 NATURE 3 2.

Part 1 National Treasury

PUBLIC FINANCE MANAGEMENT ACT 1 OF 1999 [ASSENTED TO 2 MARCH 1999] [DATE OF COMMENCEMENT: 1 APRIL 2000] (Unless otherwise indicated) (English text signed by the President) as amended by Public Finance

PUBLIC FINANCE MANAGEMENT ACT 1 OF 1999 [ASSENTED TO 2 MARCH 1999] [DATE OF COMMENCEMENT: 1 APRIL 2000] (Unless otherwise indicated) (English text signed by the President) as amended by Public Finance

Civil Aviation Authority. Regulatory Enforcement Policy

Civil Aviation Authority Regulatory Enforcement Policy PAGE 2 REGULATORY ENFORCEMENT POLICY Civil Aviation Authority This policy is subject to a phased implementation process please therefore check applicability

Civil Aviation Authority Regulatory Enforcement Policy PAGE 2 REGULATORY ENFORCEMENT POLICY Civil Aviation Authority This policy is subject to a phased implementation process please therefore check applicability

Consultation Conclusions to the Consultation Paper on the Regulation of Sponsors and Compliance Advisers

Consultation Conclusions to the Consultation Paper on the Regulation of Sponsors and Compliance Advisers Hong Kong April 2006 Table of Contents Page Part A Executive Summary... 3 Part B Overview of the

Consultation Conclusions to the Consultation Paper on the Regulation of Sponsors and Compliance Advisers Hong Kong April 2006 Table of Contents Page Part A Executive Summary... 3 Part B Overview of the

UNICEF International Public Sector Accounting Standards (IPSAS) Project Implementation Plan July 2009

Project Implementation Plan July 2009") UNICEF International Public Sector Accounting Standards (IPSAS) Project Implementation Plan July 2009 I. Introduction The adoption of IPSAS by UNICEF represents major organisational change. This implementation

UNICEF International Public Sector Accounting Standards (IPSAS) Project Implementation Plan July 2009 I. Introduction The adoption of IPSAS by UNICEF represents major organisational change. This implementation

ASPG Conference, Perth Jonathan O'Dea - October 2013. "Financial Overseers and their Oversight A NSW Public Accounts Committee Perspective"

ASPG Conference, Perth Jonathan O'Dea - October 2013 "Financial Overseers and their Oversight A NSW Public Accounts Committee Perspective" OVERVIEW Statutory Officers play central roles as financial overseers

ASPG Conference, Perth Jonathan O'Dea - October 2013 "Financial Overseers and their Oversight A NSW Public Accounts Committee Perspective" OVERVIEW Statutory Officers play central roles as financial overseers

I. The Role of the Board of Directors II. Director Qualifications III. Director Independence IV. Director Service on Other Public Company Boards

Corporate Governance Guidelines The Board of Directors (the Board ) of (the Corporation ) has adopted these governance guidelines. The guidelines, in conjunction with the Corporation s articles of incorporation,

Corporate Governance Guidelines The Board of Directors (the Board ) of (the Corporation ) has adopted these governance guidelines. The guidelines, in conjunction with the Corporation s articles of incorporation,

FREEDOM OF INFORMATION (SCOTLAND) ACT 2002 CODE OF PRACTICE ON RECORDS MANAGEMENT

ACT 2002 CODE OF PRACTICE ON RECORDS MANAGEMENT") FREEDOM OF INFORMATION (SCOTLAND) ACT 2002 CODE OF PRACTICE ON RECORDS MANAGEMENT November 2003 Laid before the Scottish Parliament on 10th November 2003 pursuant to section 61(6) of the Freedom of Information

FREEDOM OF INFORMATION (SCOTLAND) ACT 2002 CODE OF PRACTICE ON RECORDS MANAGEMENT November 2003 Laid before the Scottish Parliament on 10th November 2003 pursuant to section 61(6) of the Freedom of Information

COLLECTIVE INVESTMENT SCHEMES ACT 2008 COLLECTIVE INVESTMENT SCHEMES (REGULATED FUND) REGULATIONS 2010

REGULATIONS 2010") Statutory Document No. 161/10 COLLECTIVE INVESTMENT SCHEMES ACT 2008 COLLECTIVE INVESTMENT SCHEMES (REGULATED FUND) REGULATIONS 2010 1 Title 2 Commencement 3 Interpretation INDEX THE GOVERNING BODY 4 Composition

Statutory Document No. 161/10 COLLECTIVE INVESTMENT SCHEMES ACT 2008 COLLECTIVE INVESTMENT SCHEMES (REGULATED FUND) REGULATIONS 2010 1 Title 2 Commencement 3 Interpretation INDEX THE GOVERNING BODY 4 Composition

2015 EDUCATION PAYROLL LIMITED STATEMENT OF INTENT

2015 EDUCATION PAYROLL LIMITED STATEMENT OF INTENT Published in August 2015 Education Payroll Limited 2015 EDUCATION PAYROLL LIMITED STATEMENT OF INTENT CONTENTS Foreword 3 Who We Are 4 What We Do 5 How

2015 EDUCATION PAYROLL LIMITED STATEMENT OF INTENT Published in August 2015 Education Payroll Limited 2015 EDUCATION PAYROLL LIMITED STATEMENT OF INTENT CONTENTS Foreword 3 Who We Are 4 What We Do 5 How

EPFL CONSTITUTION EPFL GENERAL ASSEMBLY Madrid, 14 November 2007

EPFL CONSTITUTION EPFL GENERAL ASSEMBLY Madrid, 14 November 2007 ASSOCIATION OF EUROPEAN PROFESSIONAL FOOTBALL LEAGUES Association Switzerland CONSTITUTION 2 Index 1. Statutes 2. Annex 1 - List of EPFL

EPFL CONSTITUTION EPFL GENERAL ASSEMBLY Madrid, 14 November 2007 ASSOCIATION OF EUROPEAN PROFESSIONAL FOOTBALL LEAGUES Association Switzerland CONSTITUTION 2 Index 1. Statutes 2. Annex 1 - List of EPFL

Lord Chancellor s Code of Practice on the management of records issued under section 46 of the Freedom of Information Act 2000

Lord Chancellor s Code of Practice on the management of records issued under section 46 of the Freedom of Information Act 2000 Lord Chancellor s Code of Practice on the management of records issued under

Lord Chancellor s Code of Practice on the management of records issued under section 46 of the Freedom of Information Act 2000 Lord Chancellor s Code of Practice on the management of records issued under

Information governance in the Department of Health and the NHS

Information governance in the Department of Health and the NHS Harry Cayton, National Director for Patients and the Public, Chair, Care Record Development Board. Introduction I was asked by the Programme

Information governance in the Department of Health and the NHS Harry Cayton, National Director for Patients and the Public, Chair, Care Record Development Board. Introduction I was asked by the Programme

The Optima Building 58 Robertson Street Glasgow G2 8DU. Ironmills Road Dalkeith Midlothian EH22 1LE

SQA's Quality Framework: a guide for centres The Optima Building 58 Robertson Street Glasgow G2 8DU Ironmills Road Dalkeith Midlothian EH22 1LE Customer Contact Centre Tel: 0845 279 1000 Fax: 0845 213

SQA's Quality Framework: a guide for centres The Optima Building 58 Robertson Street Glasgow G2 8DU Ironmills Road Dalkeith Midlothian EH22 1LE Customer Contact Centre Tel: 0845 279 1000 Fax: 0845 213

Hospitality Services Service Level Standards

Hospitality Services Service Level Standards Contents 1. Introduction and Purpose 2. Customer Promise 3. Definition of Services 4. Performance Tracking and Reporting 5. Complaints Management 6. Training

Hospitality Services Service Level Standards Contents 1. Introduction and Purpose 2. Customer Promise 3. Definition of Services 4. Performance Tracking and Reporting 5. Complaints Management 6. Training

HEALTH AND SAFETY POLICY AND PROCEDURES

HEALTH AND SAFETY POLICY AND PROCEDURES 1 Introduction 1. The Health and Safety at Work etc. Act 1974 places a legal duty on the University to prepare and revise as often as may be appropriate, a written

HEALTH AND SAFETY POLICY AND PROCEDURES 1 Introduction 1. The Health and Safety at Work etc. Act 1974 places a legal duty on the University to prepare and revise as often as may be appropriate, a written

Audit and risk assurance committee handbook

Audit and risk assurance committee handbook March 2016 Audit and risk assurance committee handbook March 2016 Crown copyright 2016 This publication is licensed under the terms of the Open Government Licence

Audit and risk assurance committee handbook March 2016 Audit and risk assurance committee handbook March 2016 Crown copyright 2016 This publication is licensed under the terms of the Open Government Licence

IAF Informative Document. Transition Planning Guidance for ISO 9001:2015. Issue 1 (IAF ID 9:2015)

") IAF Informative Document Transition Planning Guidance for ISO 9001:2015 Issue 1 (IAF ID 9:2015) Issue 1 Transition Planning Guidance for ISO 9001:2015 Page 2 of 10 The (IAF) facilitates trade and supports

IAF Informative Document Transition Planning Guidance for ISO 9001:2015 Issue 1 (IAF ID 9:2015) Issue 1 Transition Planning Guidance for ISO 9001:2015 Page 2 of 10 The (IAF) facilitates trade and supports

Corporate Policy. Data Protection for Data of Customers & Partners.

Corporate Policy. Data Protection for Data of Customers & Partners. 02 Preamble Ladies and gentlemen, Dear employees, The electronic processing of virtually all sales procedures, globalization and growing

Corporate Policy. Data Protection for Data of Customers & Partners. 02 Preamble Ladies and gentlemen, Dear employees, The electronic processing of virtually all sales procedures, globalization and growing

The NHS Foundation Trust Code of Governance

The NHS Foundation Trust Code of Governance www.monitor-nhsft.gov.uk The NHS Foundation Trust Code of Governance 1 Contents 1 Introduction 4 1.1 Why is there a code of governance for NHS foundation trusts?

The NHS Foundation Trust Code of Governance www.monitor-nhsft.gov.uk The NHS Foundation Trust Code of Governance 1 Contents 1 Introduction 4 1.1 Why is there a code of governance for NHS foundation trusts?

Regulation on the implementation of the Norwegian Financial Mechanism 2009-2014

Regulation on the implementation of the Norwegian Financial Mechanism 2009-2014 adopted by the Norwegian Ministry of Foreign Affairs pursuant to Article 8.8 of the Agreement between the Kingdom of Norway

Regulation on the implementation of the Norwegian Financial Mechanism 2009-2014 adopted by the Norwegian Ministry of Foreign Affairs pursuant to Article 8.8 of the Agreement between the Kingdom of Norway

Aberdeen City Council. Performance Management Process. External Audit Report o: 2008/19

Aberdeen City Council Performance Management Process External Audit Report o: 2008/19 Draft Issued: 11 February 2009 Final Issued: 6 April 2009 Contents Pages Pages Management Summary Introduction 1 Background

Aberdeen City Council Performance Management Process External Audit Report o: 2008/19 Draft Issued: 11 February 2009 Final Issued: 6 April 2009 Contents Pages Pages Management Summary Introduction 1 Background

National Occupational Standards. Compliance

National Occupational Standards Compliance NOTES ABOUT NATIONAL OCCUPATIONAL STANDARDS What are National Occupational Standards, and why should you use them? National Occupational Standards (NOS) are statements

National Occupational Standards Compliance NOTES ABOUT NATIONAL OCCUPATIONAL STANDARDS What are National Occupational Standards, and why should you use them? National Occupational Standards (NOS) are statements

How To Help Your Educational Psychology Service Self Evaluate

Quality Management in Local Authority Educational Psychology Services Self-evaluation for quality improvement Quality Management in Local Authority Educational Psychology Services Self-evaluation for quality

Quality Management in Local Authority Educational Psychology Services Self-evaluation for quality improvement Quality Management in Local Authority Educational Psychology Services Self-evaluation for quality

Risk Management Committee Charter

Ramsay Health Care Limited ACN 001 288 768 Risk Management Committee Charter Approved by the Board of Ramsay Health Care Limited on 29 September 2015 Ramsay Health Care Limited ABN 57 001 288 768 Risk

Ramsay Health Care Limited ACN 001 288 768 Risk Management Committee Charter Approved by the Board of Ramsay Health Care Limited on 29 September 2015 Ramsay Health Care Limited ABN 57 001 288 768 Risk

Health and Safety Policy and Procedures

Health and Safety Policy and Procedures Health & Safety Policy & Procedures Contents s REVISION AND AMENDMENT RECORD : Summary of Change Whole Policy 4.0 05 Nov 08 Complete re-issue Whole Policy 4.1 10

Health and Safety Policy and Procedures Health & Safety Policy & Procedures Contents s REVISION AND AMENDMENT RECORD : Summary of Change Whole Policy 4.0 05 Nov 08 Complete re-issue Whole Policy 4.1 10

Corporate Performance Management Customer Care Team

Corporate Performance Management Customer Care Team Title Annual Report 2009/2010 Subject Children s Services complaints and representations Creator Heather Maybury Version 7.0 Date July 2010 Status draft

Corporate Performance Management Customer Care Team Title Annual Report 2009/2010 Subject Children s Services complaints and representations Creator Heather Maybury Version 7.0 Date July 2010 Status draft

Guide to the Performance Management Framework

Guide to the Performance Management Framework November 2012 Contents Contents... Guide to the Performance Management Framework...1 1. Introduction...4 1.1 Purpose of the guidelines...4 1.2 The performance

Guide to the Performance Management Framework November 2012 Contents Contents... Guide to the Performance Management Framework...1 1. Introduction...4 1.1 Purpose of the guidelines...4 1.2 The performance

EIH Limited (A member of TheOberoi Group)

") EIH Limited (A member of TheOberoi Group) POLICY FOR DETERMINATION AND DISCLOSURE OF MATERIAL EVENTS 1. Statutory Mandate The Board of Directors (The Board ) of EIH Limited ( the Company ) has adopted

EIH Limited (A member of TheOberoi Group) POLICY FOR DETERMINATION AND DISCLOSURE OF MATERIAL EVENTS 1. Statutory Mandate The Board of Directors (The Board ) of EIH Limited ( the Company ) has adopted

VISION FOR LEARNING AND DEVELOPMENT

VISION FOR LEARNING AND DEVELOPMENT As a Council we will strive for excellence in our approach to developing our employees. We will: Value our employees and their impact on Cardiff Council s ability to

VISION FOR LEARNING AND DEVELOPMENT As a Council we will strive for excellence in our approach to developing our employees. We will: Value our employees and their impact on Cardiff Council s ability to

HEALTH SERVICE EXECUTIVE NATIONAL FINANCIAL REGULATION INTRODUCTION TO NATIONAL FINANCIAL REGULATIONS NFR - 00

HEALTH SERVICE EXECUTIVE NATIONAL FINANCIAL REGULATION INTRODUCTION TO NATIONAL FINANCIAL REGULATIONS NFR - 00 Ver 3.0 9/10/2014 NFR 00 Introduction to Section 1: Introduction to 1.1-1.10 Introduction

HEALTH SERVICE EXECUTIVE NATIONAL FINANCIAL REGULATION INTRODUCTION TO NATIONAL FINANCIAL REGULATIONS NFR - 00 Ver 3.0 9/10/2014 NFR 00 Introduction to Section 1: Introduction to 1.1-1.10 Introduction

CHECKLIST ISO/IEC 17021:2011 Conformity Assessment Requirements for Bodies Providing Audit and Certification of Management Systems

Date(s) of Evaluation: CHECKLIST ISO/IEC 17021:2011 Conformity Assessment Requirements for Bodies Providing Audit and Certification of Management Systems Assessor(s) & Observer(s): Organization: Area/Field

Date(s) of Evaluation: CHECKLIST ISO/IEC 17021:2011 Conformity Assessment Requirements for Bodies Providing Audit and Certification of Management Systems Assessor(s) & Observer(s): Organization: Area/Field

Australian Charities and Not-for-profits Commission: Regulatory Approach Statement

Australian Charities and Not-for-profits Commission: Regulatory Approach Statement This statement sets out the regulatory approach of the Australian Charities and Not-for-profits Commission (ACNC). It

Australian Charities and Not-for-profits Commission: Regulatory Approach Statement This statement sets out the regulatory approach of the Australian Charities and Not-for-profits Commission (ACNC). It

Electronic Payment Schemes Guidelines

BANK OF TANZANIA Electronic Payment Schemes Guidelines Bank of Tanzania May 2007 Bank of Tanzania- Electronic Payment Schemes and Products Guidleness page 1 Bank of Tanzania, 10 Mirambo Street, Dar es

BANK OF TANZANIA Electronic Payment Schemes Guidelines Bank of Tanzania May 2007 Bank of Tanzania- Electronic Payment Schemes and Products Guidleness page 1 Bank of Tanzania, 10 Mirambo Street, Dar es

Information Pack for Applicants to the MIDLANDS CONNECT PROJECT TEAM

Information Pack for Applicants to the MIDLANDS CONNECT PROJECT TEAM I. Midlands Connect: Strategic Context and progress to date The Midlands Connect (MC) Partnership started in 2014 and brings together

Information Pack for Applicants to the MIDLANDS CONNECT PROJECT TEAM I. Midlands Connect: Strategic Context and progress to date The Midlands Connect (MC) Partnership started in 2014 and brings together

AUDIT COMMITTEE TERMS OF REFERENCE

AUDIT COMMITTEE TERMS OF REFERENCE 1. Purpose The Audit Committee will assist the Board of Directors (the "Board") in fulfilling its oversight responsibilities. The Audit Committee will review the financial

AUDIT COMMITTEE TERMS OF REFERENCE 1. Purpose The Audit Committee will assist the Board of Directors (the "Board") in fulfilling its oversight responsibilities. The Audit Committee will review the financial

Institutional Certified Evaluation and Accreditation of Universities General Principles: 2012-2019

Institutional Certified Evaluation and Accreditation of Universities General Principles: 2012-2019 NIAD-UE National Institution for Academic Degrees and University Evaluation National Institution for Academic

Institutional Certified Evaluation and Accreditation of Universities General Principles: 2012-2019 NIAD-UE National Institution for Academic Degrees and University Evaluation National Institution for Academic

Financial transactions sometimes lacked proper signing authorities;

STRENGTHENING FINANCIAL MANAGEMENT IN THE GOVERNMENT OF NUNAVUT DEPARTMENT OF FINANCE MARCH 2007 Introduction For a number of years the Auditor General of Canada has commented on the need for improved

STRENGTHENING FINANCIAL MANAGEMENT IN THE GOVERNMENT OF NUNAVUT DEPARTMENT OF FINANCE MARCH 2007 Introduction For a number of years the Auditor General of Canada has commented on the need for improved

TO BE PRESENTED BY CHAMA M MFULA AND LOVENESS M MAYAKA

PARLIAMENTARY INFORMATION SERVICES: THE ROLE OF THE LIBRARY AND RESAERCH DEPARTMENTS IN THE ZAMBIAN PARLIAMENT IN HELPING MEMBERS OF PARLIAMENT MAKE BETTER LAWS TO BE PRESENTED BY CHAMA M MFULA AND LOVENESS

PARLIAMENTARY INFORMATION SERVICES: THE ROLE OF THE LIBRARY AND RESAERCH DEPARTMENTS IN THE ZAMBIAN PARLIAMENT IN HELPING MEMBERS OF PARLIAMENT MAKE BETTER LAWS TO BE PRESENTED BY CHAMA M MFULA AND LOVENESS

SCHOOLS FORUM Agenda Item 10 WEST SUSSEX COUNTY COUNCIL MAINTAINED SCHOOLS EMPLOYMENT SUPPORT SERVICE LEVEL AGREEMENT

SCHOOLS FORUM Agenda Item 10 4 TH DECEMBER 2014 WEST SUSSEX COUNTY COUNCIL MAINTAINED SCHOOLS EMPLOYMENT SUPPORT SERVICE LEVEL AGREEMENT REPORT BY THE DIRECTOR OF WORKFORCE, ORGANISATIONAL DEVELOPMENT

SCHOOLS FORUM Agenda Item 10 4 TH DECEMBER 2014 WEST SUSSEX COUNTY COUNCIL MAINTAINED SCHOOLS EMPLOYMENT SUPPORT SERVICE LEVEL AGREEMENT REPORT BY THE DIRECTOR OF WORKFORCE, ORGANISATIONAL DEVELOPMENT

Implementation of a Quality Management System for Aeronautical Information Services -1-

Implementation of a Quality Management System for Aeronautical Information Services -1- Implementation of a Quality Management System for Aeronautical Information Services Chapter IV, Quality Management

Implementation of a Quality Management System for Aeronautical Information Services -1- Implementation of a Quality Management System for Aeronautical Information Services Chapter IV, Quality Management

INTOSAI. Performance Audit Subcommittee - PAS. Designing performance audits: setting the audit questions and criteria

INTOSAI Performance Audit Subcommittee - PAS Designing performance audits: setting the audit questions and criteria 1 Introduction A difficult phase in performance auditing is planning and designing. In

INTOSAI Performance Audit Subcommittee - PAS Designing performance audits: setting the audit questions and criteria 1 Introduction A difficult phase in performance auditing is planning and designing. In

A Guide to Corporate Governance for QFC Authorised Firms

A Guide to Corporate Governance for QFC Authorised Firms January 2012 Disclaimer The goal of the Qatar Financial Centre Regulatory Authority ( Regulatory Authority ) in producing this document is to provide

A Guide to Corporate Governance for QFC Authorised Firms January 2012 Disclaimer The goal of the Qatar Financial Centre Regulatory Authority ( Regulatory Authority ) in producing this document is to provide

CODE OF PRACTICE APPOINTMENT TO POSITIONS IN THE CIVIL SERVICE AND PUBLIC SERVICE MERIT PROBITY ACCOUNTABILITY

CODE OF PRACTICE APPOINTMENT TO POSITIONS IN THE CIVIL SERVICE AND PUBLIC SERVICE MERIT PROBITY BEST PRACTICE ACCOUNTABILITY CONSISTENCY Published in 2007 by the Commission for Public Service Appointments

CODE OF PRACTICE APPOINTMENT TO POSITIONS IN THE CIVIL SERVICE AND PUBLIC SERVICE MERIT PROBITY BEST PRACTICE ACCOUNTABILITY CONSISTENCY Published in 2007 by the Commission for Public Service Appointments

STATUTORY INSTRUMENTS SUPPLEMENT No. 1 11th May, 2012.

THE EAST AFRICAN COMMUNITY STATUTORY INSTRUMENTS SUPPLEMENT No. 1 11th May, 2012. to the East African Community Gazette No. 7 of 11th May, 2012. Printed by the Uganda Printing and Publishing Corporation,

THE EAST AFRICAN COMMUNITY STATUTORY INSTRUMENTS SUPPLEMENT No. 1 11th May, 2012. to the East African Community Gazette No. 7 of 11th May, 2012. Printed by the Uganda Printing and Publishing Corporation,

Act on Insurance. The National Council of the Slovak Republic has adopted the following Act: SECTION I PART ONE GENERAL PROVISIONS

Act on Insurance Full wording of Act No 8/2008 Coll. of 28 November 2007 on Insurance and on amendments and supplements to certain laws, as amended by Act No 270/2008 Coll., Act No 552/2008 Coll., Act

Act on Insurance Full wording of Act No 8/2008 Coll. of 28 November 2007 on Insurance and on amendments and supplements to certain laws, as amended by Act No 270/2008 Coll., Act No 552/2008 Coll., Act

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

. Board Charter - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 1. Interpretation 1.1 In this Charter: Act means the Companies

. Board Charter - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 1. Interpretation 1.1 In this Charter: Act means the Companies

Nomination & Remuneration Policy

Nomination & Remuneration Policy I. PREAMBLE Pursuant to Section 178 of the Companies Act, 2013 and Clause 49 of the Listing Agreement, the Board of Directors of every listed Company shall constitute the

Nomination & Remuneration Policy I. PREAMBLE Pursuant to Section 178 of the Companies Act, 2013 and Clause 49 of the Listing Agreement, the Board of Directors of every listed Company shall constitute the

Corporate Health and Safety Policy

Corporate Health and Safety Policy November 2013 Ref: HSP/V01/13 EALING COUNCIL Table of Contents PART 1: POLICY STATEMENT... 3 PART 2: ORGANISATION... 4 2.1 THE COUNCIL:... 4 2.2 ALLOCATION OF RESPONSIBILITY...

Corporate Health and Safety Policy November 2013 Ref: HSP/V01/13 EALING COUNCIL Table of Contents PART 1: POLICY STATEMENT... 3 PART 2: ORGANISATION... 4 2.1 THE COUNCIL:... 4 2.2 ALLOCATION OF RESPONSIBILITY...

Explanation where the company has partially applied or not applied King III principles

King Code of Corporate Governance for South Africa, 2009 (King III) checklist The Board of Directors (the Board) of Famous Brands Limited (Famous Brands or the company) is fully committed to business integrity,

King Code of Corporate Governance for South Africa, 2009 (King III) checklist The Board of Directors (the Board) of Famous Brands Limited (Famous Brands or the company) is fully committed to business integrity,