Monetary and Fiscal Policy Interactions with Debt Dynamics

|

|

|

- Bruce Grant Arnold

- 8 years ago

- Views:

Transcription

1 Moneary and Fiscal Policy Ineracions wih Deb Dynamics Sefano Gnocchi and Luisa Lamberini Preliminary and Incomplee November, 22 Absrac We analyze he ineracion beween commied moneary and discreionary fiscal policy in a model wih public deb, endogenous governmen expendiure, disorionary axaion and nominal rigidiies. Fiscal decisions lack commimen bu are Markov-perfec. Lack of commimen by he fiscal auhoriy generaes a unique sable seady-sae level of deb ha depends on he exen of is ime-consisency problem. Larger price adjusmen coss as well as a more inefficien level of oupu reduce he seady-sae level of deb. The ime-consisen, opimal response o shocks feaures sraegic use of he real ineres rae, which is reduced in response o budge deficis and vice versa for surpluses. Lack of commimen in fiscal policy leads o volaile ax raes and inflaion. Keyword: Moneary and fiscal policy ineracions, axaion, public deb, business cycle. JEL Codes: E24, E32, E52 Gnocchi graefully acknowledges financial suppor from he Spanish Minisry of Educaion and Science hrough gran ECO , he suppor of he Barcelona GSE Research Nework and of he Governmen of Caalonia; Luisa Lamberini graefully acknowledges financial suppor from he Swiss Naional Foundaion, Sinergia Gran CRSI UAB, Barcelona. Conac: sefano.gnocchi@uab.ca EPFL, Lausanne. Conac: luisa.lamberini@epfl.ch

2 Inroducion Characerizing he opimal moneary and fiscal policy mix is a classical problem ha he lieraure has repeaedly faced, finding differen soluions depending on he disorions he policy makers have o address, he insrumens hey have available and he way hey inerac. In his paper, we reassess his issue in an environmen where he Pareo efficien allocaion may no be implemenable, because markes are imperfecly compeiive, prices are sicky, lump-sum axes are no available and policy makers are independen auhoriies ha do no necessarily share he same abiliy o commi. As far as policy insrumens are concerned, we assume ha he cenral bank is responsible for seing he nominal ineres rae, while he fiscal policy maker has access o hree insrumens: non-coningen nominal deb, disorive axaion on labor and governmen expendiure. Pars of our complex policy problem have been sudied already in isolaion. However, his paper is novel in uncovering some imporan ineracions among hem. In paricular, in an environmen like ours, we show ha he opimal response o business cycle shocks and seady sae disorions are indissolubly linked hrough public deb in a way ha depends on moneary and fiscal policy coordinaion. Some auhors have admiedly emphasized ha opimal moneary policy is affeced by wheher he economy flucuaes around an efficien equilibrium or no. However, our poin, hough complemenary, is subsanially differen since our channel goes hrough deb dynamics and policy coordinaion. Inuiively, even hough moneary policy remains neural in he long-run, he fiscal policy maker has access o insrumens ha can permanenly change he level around which he economy flucuaes. In addiion, he incenives for he fiscal auhoriy of relying on deb and disorive axaion are affeced by he cenral bank s response o emporary shocks. I follows ha he widespread pracice of absracing from deb dynamics and seady sae disorions may be very misleading. On he one hand, such simplified environmen misses he long-run effecs of sabilizaion policies. On he oher hand, i does no ake ino accoun ha he opimal response o emporary shocks depends on how seady sae disorions are addressed. We conduc our analysis under wo alernaive policy regimes. As an ineresing benchmark, we firs consider he case of a Ramsey planner choosing all policy insrumens (henceforh, he full Ramsey case). Then, we analyze he opimal policy mix when he moneary auhoriy can commi, while he fiscal auhoriy acs under discreion 2

3 (henceforh, he case of fiscal discreion). The assumpion is moivaed by he differen insiuional environmens in which moneary and fiscal policies are conduced. In many counries, advanced and emerging, moneary and fiscal policies are decided by separae auhoriies. Insiuional reform in he 98s and 99s has made cenral banks independen from he reasuries, someime also giving hem an explici mandae o achieve specific goals in erms of inflaion and/or economic aciviy. Treasuries are no subjec o explici mandaes, bu hey follow he elecoral cycle and may be replaced a he nex elecion. Hence, he assumpion of commimen in fiscal policy seems a odds wih realiy. As an empirically relevan alernaive o he full Ramsey benchmark, we model he case of moneary commimen and fiscal discreion as a non-cooperaive game. Our findings conribue o he lieraure in several respecs. Firs, in he full Ramsey case inflaion sabilizaion generaes permanen changes in employmen, because of deb dynamics. The mechanism is sraighforward. In line wih he known resuls of he moneary policy lieraure, he price mark-up flucuaions induced by nominal rigidiies are responsible for making a srong case in favor of price sabiliy. Hence, he sock of deb is permanenly affeced by emporary shocks, because he marke of governmen bonds canno be compleed by resoring o inflaion flucuaions. On he oher hand, he ineres rae changes required o keep inflaion sable drive deb dynamics, which in urn permanenly feeds back o employmen hrough he required ax adjusmen. For example, consider an economy ha is endowed wih posiive public deb and ha is in an iniial sae disored by posiive ax raes and imperfecly compeiive markes. A posiive echnology shock riggers a fall in he nominal ineres rae ha permanenly reduces he ousanding public deb. Facing a lower expendiure for ineres rae paymens, he governmen can reduce ax-raes and increase hours worked. As a consequence, hours are no fully sabilized afer a echnology shock as i is he case in he baseline model. The resuling flucuaions are small, bu permanen. Therefore, as long as he cenral bank sabilizes inflaion, a sufficienly long sequence of emporary produciviy improvemens significanly and permanenly increases employmen. In general, size and magniude of he effec depend on size and magniude of he iniial level of deb. For insance, if he governmen sars wih asses, he mechanism oulined above is invered and a emporary and posiive produciviy shock permanenly reduces employmen. These resuls do no obain when prices are flexible, because inflaion flucuaions are no cosly and can hus be used o complee financial markes and make deb saionary. 3

4 Second, emporary shocks do no permanenly affec employmen under fiscal discreion. However, a link beween sabilizaion policy and seady sae disorions sill exiss, even hough i goes he oher way. In paricular, we find ha opimal inflaion sabilizaion generaes employmen flucuaions ha are more abrup on impac if he economy is disored on average. Once again, deb accumulaion and policy ineracion are responsible for his resul. I is well-known ha deb is saionary if he fiscal auhoriy canno commi even hough deb is non-coningen. For insance, Deboroli and Nunes (22) argue ha Markov perfec fiscal policy implies zero deb as a seady sae. In fac, only in a siuaion of balanced budge he discreionary policy maker does no have any incenive o generae unexpeced changes of he real ineres rae in her own favor. We addiionally find ha if prices are sicky and markes are imperfecly compeiive, he seady sae level of deb is negaive. This is because in our model a discreionary fiscal policy maker also has he incenive o generae surprise inflaion, so as o reduce seady sae disorions. Only for a negaive level of deb indeed he gains of unexpeced deflaion in erms of higher real ineres raes are compensaed by he gains of unexpeced inflaion in erms of higher employmen. I follows ha he cenral bank s response o shocks does no permanenly affec he employmen level since deb and ax raes are saionary and hen unaffeced in he long-run by changes in he nominal ineres rae. However he sabilizaion of inflaion pursued by he cenral bank coupled wih saionariy of deb links he volailiy of he nominal ineres rae o he volailiy of ax raes. The fiscal auhoriy indeed has o mach changes in ax raes wih changes in ineres rae paymens so as o keep deb consan in he long-run. This fac resuls in higher volailiy, on impac, of hours worked. The resul is quie counerinuiive: fiscal discreion and he lack of conrol of he nominal ineres rae on he par of he fiscal auhoriy do no imply excessively high or volaile deb. On he conrary, hey lead o excessively high volailiy of axes and hours a he ime he shock his. On he oher hand, he impac of he shock is emporary so ha axes and hours are less volaile a lower frequencies. In oher words, fiscal discreion, as opposed o he full Ramsey case, shifs he volailiy of employmen from he long-run o he shor-run. Finally, we find ha exogenous flucuaions in wage mark-ups do no imply high volailiy of inflaion, irrespecive of wheher moneary and fiscal policy are coordinaed. Also, he allocaion does no differ significanly under he wo policy regimes. Finally, under full Ramsey, ransiory changes of he ineres rae have a negligible impac on 4

argue ha Markov perfec fiscal policy implies zero deb as a seady sae.")

5 employmen in he long-run. All hose resuls can be explained by he fac ha policy makers have enough insrumens o cope wih he shock, since ax raes can be used o counerbalance changes in mark-ups. 2 Relevan lieraure Opimal moneary and fiscal policy are commonly invesigaed under he assumpion ha a single auhoriy chooses all policy insrumens. Lucas and Sokey (983) sudy he choice of opimal moneary and fiscal policy under commimen in real model wih perfec compeiion in goods and facor markes. The governmen faces an exogenous and sochasic process of public spending ha can be financed by levying disorionary income axes and/or issuing sae-coningen bonds. In his environmen he income ax and public deb inheri he dynamic properies of he exogenous sochasic disurbances. Chari, Chrisiano and Kehoe (99) exend he model by Lucas and Sokey (983) o a moneary economy where governmen issues nominal non-sae-coningen deb. Opimal fiscal policy implies ha he ax rae on labor remains essenially consan. On he oher hand, opimal moneary policy requires he governmen o inflae in response o bad shocks and deflae in response o good shocks. Hence, inflaion makes nominal deb saeconingen in real erms and i is highly volaile. In he model by Chari e al. (99) prices are flexible and inflaion is no cosly. Schmi-Grohé and Uribe (24) analyze a model wih imperfec compeiion and sicky produc prices; he fiscal side of he model assumes ha he governmen canno rely on lump-sum axes bu can only use disorionary income axes and ha i can only issue nominal one-period non-sae-coningen bonds. The key finding of his paper is ha opimal moneary and fiscal policy under commimen implies low inflaion volailiy while fiscal variables display near-uni roo behavior. This finding arises even for a very small degree of price sickiness. Aiyagari, Marce, Sargen and Seppala (22) sudy opimal policies in a real model wih commimen and find ha he dynamic behavior of fiscal variables depends on he abiliy of he governmen o issue sae-coningen real deb. Recen work has focused on discreionary policymaking while reaining he assumpion of a single policy auhoriy. Deboroli and Nunes (22) exend he model of Lucas and Sokey (983) wih endogenous public expendiure and sudy opimal policymaking in he absence of commimen. The key resul of his paper is ha lack of commimen 5

6 does no lead o deb accumulaion. In fac, seady-sae deb is no longer indeerminae under discreion and deb converges back o such level. Ineresingly, he seady-sae of he economy involves no deb accumulaion a all. Niemann, Pichler and Sorger (2) sudy discreionary moneary and fiscal policies in a moneary model wih nominal nonsae-coningen deb. The seady-sae levesl of deb and inflaion depend on ransacion coss associaed wih privae consumpion and inflaion volailiy falls when prices are sicky. Campbell and Wren-Lewis (28) evaluae he welfare consequences of shocks a he efficien seady sae and find subsanially larger welfare coss of discreion relaive o commimen. The common resul among hese works is ha, when he moneary and fiscal auhoriies share he abiliy o commi or he lack of i, moneary policy bears he brun of burden of sabilizaion while fiscal policy is in some sense neural. In paricular, governmen spending does no play a role in macroeconomic sabilizaion, as emphasized by Galí and Monacelli (28) and Eser, Leih and Wren-Lewis (29). Unlike hese conribuions, our paper invesigaes he ineracion beween commied moneary policy and discreionary fiscal policies. The lieraure on he sraegic ineracion beween moneary and fiscal policy has ypically assumed a rich game-heoreic environmen in a simple model. Dixi and Lamberini (23) explicily model moneary and fiscal policies as a non-cooperaive game beween wo independen auhoriies. The cenral bank being can commi while he fiscal auhoriy acs under discreion. Their cenral bank is no benevolen bu conservaive as in Rogoff (985) and he model is saic. Adam and Billi (2) consider independen moneary and fiscal auhoriies acing under discreion o analyze he desirabiliy of making he cenral bank conservaive o eliminae he seady-sae inflaion bias. When hey consider commied moneary policy, heir analysis is limied o he seady sae. Gnocchi (22) analyzes he ineracion of moneary commimen and fiscal discreion in a dynamic moneary model wih sicky prices. In ha paper he asymmery in he policy regime leads o use of he fiscal insrumen ha imposes a negaive exernaliy on he cenral bank. In paricular, he volailiy of he governmen expendiure is inefficienly high and greaer han he one implied by he soluion of a Ramsey planner. This is because he governmen, hough sharing he same objecive funcion of he cenral bank, does no agree on he opimal sabilizaion plan implemened by he moneary auhoriy. The exising lieraure on moneary-fiscal and commimen-discreion ineracions absracs from disorionary axaion and nominal deb. This is he novely conribuion 6

7 of our paper. Exending he analysis in his direcion provides insigh on wheher discreionary fiscal policy generaes inefficien volailiy of deb and/or public spending and herefore provide a raionale for budge rules. 3 The Model This secion describes our infinie-horizon producion economy wih imperfecly compeiive goods and labor markes and sicky prices. The governmen provides public spending, which is financed by levying disorionary income axes and issuing one-period risk-free bonds. 3. Households The economy is inhabied by a coninuum of households. Each household consumes a coninuum of privae and public goods and sells differeniaed labor services o firms. Preferences for household i are described by a uiliy funcion defined over privae consumpion, public expendiure, and leisure: U = E = β ( χ) ln C (i) + χ ln G (N (i)) +ϕ, () + ϕ where β (, ) denoes he subjecive discoun facor and E denoes expecaions condiional on he informaion available a ime. C (i) is a CES aggregaor of privae consumpion by he represenaive household of each variey j, denoed by C (i, j) C (i) = ηp ηp ηp C (i, j) ηp dj, (2) where η p > is he elasiciy of subsiuion beween varieies. The aggregae price is defined as P = ηp P (j) ηp dj. (3) Each household supplies a differeniaed labor service; η w > is he elasiciy of subsiuion across labor varieies. Hence, he demand for labor ype i is ( W (i) N (i) = W ) η w, (4) The price index has he propery ha he minimum cos of a consumpion bundle C is P C. 7

8 where W (i) is he nominal wage of labor variey i and W is he aggregae wage, which is defined as 2 W = ηw W (i) ηw di. (5) Hours worked N (i) ener negaively in he uiliy funcion and ϕ is he inverse elasiciy of labor supply. The public good provided by he governmen, G, eners he uiliy funcion of privae households wih weigh χ > while privae consumpion eners he uiliy wih weigh χ. In each period household i can purchase nominal governmen deb B + (i) a he price /( + i ), where i is he nominal ineres rae. The nominal deb B + (i) pays one uni in nominal erms in period +. The budge consrain of household i in period is P C (i) + B +(i) + i = W (i)n (i)( τ ) + B (i), (6) where W (i) is he nominal wage and τ is he income ax. In real erms, he household budge consrain can be wrien as C (i) + b +(i) + i = w (i)n (i)( τ ) + bi π, (7) where b i + Bi + /P is real deb, w (i) W (i)/p is real wage and π P /P is he gross inflaion rae a ime. In each period household i chooses nominal wage W (i) and financial asses b i +. The firs-order condiions of he household s maximizaion problem for hese choices are, respecively, χ C (i)( + i ) = β χ, (8) C + (i)π + N (i) ϕ = w (i)( τ )( χ), Φ = ηw ΦC (i) η w exp µ w. (9) Firs-order condiion (8) is he sandard Euler equaion for non-sae-coningen bonds. Firs-order condiion (9) shows ha wo facors drive a wedge beween he marginal rae of subsiuion beween leisure and consumpion for households and he marginal rae of ransformaion: imperfec subsiuabiliy among labor ypes and he labor income ax. mu w is an exogenous shock o his wedge ha we inerpre as a wage mark-up shock. 2 As for he price index, he aggregae wage has he propery ha he minimum cos of a uni of composie labor inpu N is W N. 8

a he price /( + i ), where i is he nominal ineres rae. The nominal deb B + (i) pays one uni in nominal erms in period +.")

9 3.2 Firms Firms are indexed by j on he uni inerval, and each firm produces a variey wih a consan reurn o scale echnology Y (j) = z N (j). () Produciviy is idenical across firms and is denoed by z and N,j denoes he quaniy of labor hired by firm j in period. The effecive labor inpu of firm j is a CES aggregaor of he quaniy hired of each differeniaed labor service N (j) = ηw N (i, j) ηw ηw ηw di, () where he parameer η w > is he elasiciy of subsiuion among labor ypes. Firms do no have power in he labor marke, hen hey ake wages as given. Following Roemberg (982), we assume ha firms face quadraic price adjusmen coss given by where γ is he adjusmen cos. recovered by seing he parameer γ =. ( ) γ P (j) 2 2 P (j), (2) The benchmark of flexible prices can easily be Each period firms choose labor services N (j) and he price level a which o sell heir goods so as o maximize nominal profis. Formally, firm j maximizes ( ) } E {Q,+s P (j)y (j) ( τ p γ P (j) 2 )W N (j) P 2 P (j) s= subjec o where τ p is a subsidy he governmen can use o offse he seady sae disorions due o monopolisic compeiion and Q,+j is he nominal sochasic discoun facor in period. Q,+j is such ha E Q,+ = ( + i ). The demand for he variey produced by firm j is where Y denoes he level of aggregae demand. (3) ( ) P (j) ηp Y (j) = Y, (4) Le MC (j) = mc (j)p be he lagrangian muliplier on he consrain (4). firs-order condiions relaive o N (j) and P (j) are given by, respecively, P The mc (j) = ( τ p ) w z, (5) 9

10 π (π ) + β C ( ) π + (π + ) + ηp mc (j) ηp C + γ η p =. (6) Boh equaions are idenical across all firms so ha he j index can dropped. (5) saes ha he real marginal cos is he raio of he real wage and he marginal produciviy of labor. (6) is a sandard Phillips curve according o which curren inflaion depends posiively on fuure inflaion and curren marginal cos. 3.3 Governmen In each period he governmen provides he public good G. We assume ha his public good is he following CES aggregaor of differen varieies produced by firms G = ηp ηp ηp G (j) ηp dj, (7) where G (j) is he quaniy of public consumpion of variey j. Given aggregae governmen demand G, opimal inra-emporal allocaion across varieies implies ha governmen demand for each variey j is given by ( ) P (j) ηp G (j) = G. (8) P Governmen expendiures are financed by levying a disorionary labor income ax τ or by issuing one-period, risk-free, non-sae coningen nominal bonds B +. The budge consrain of he governmen (already wrien in real erms) is b + i + τ w N = b π + G + τ p. (9) In our model fiscal policy consiss in choosing he sequence of public expendiures and labor income ax raes {G, τ }. Of course, hese choices uniquely deermine he amoun of deb issued B +. We rea he subsidy τ p as a parameer ha we se equal o appropriae values depending on wheher we wan o consider allocaions wih a disored seady sae or he efficien allocaion. 3.4 Equilibrium Aggregae oupu in period Y is Y = ηp Y i ηp ηp (j) ηp dj. (2)

ηp dj, (7) where G (j) is he quaniy of public consumpion of variey j.")

11 Toal privae demand of variey j can be found by inegraing C (i, j) across households C (j) = i= C (i, j)di. (2) Since all firms are idenical, he labor demanded and he real wage are idenical across labor varieies. This implies ha all households are idenical. Marke clearing a he level of he single variey implies Y (j) = C (j) + G (j) + γ 2 ( ) P (j) 2 P (j), (22) Marke clearing in all goods markes implies he aggregae resource consrain Y = C + G + γ 2 (π ) 2. (23) Finally, i can be shown ha he aggregae producion funcion is given by Y = z N (24) where N is he aggregae labor inpu. The benchmark model is characerized by no disorions in he labor marke. Laer on, when sudying wage mark-up shocks, we explicily model imperfec compeiion in he labor marke semming from he supply of imperfecly subsiuable labor ypes N (i) wih elasiciy of subsiuion η w >. 3.5 Exogenous shocks Produciviy and wage markup are sochasic and evolve according o he following processes ln z = ρ z ln z + ɛ z, (25) µ w = ρ w µ w + ɛ w, (26) where ɛ z and ɛ w are i.i.d. shocks ha we assume o be uncorrelaed; ρ z, ρ w are auoregressive coefficiens. A he seady sae µ w =. 4 The Pareo-efficien allocaion The Pareo-efficien allocaion solves he problem of maximizing uiliy () subjec o equaions (2), (), (2) and o he resource consrain for each variey j (22). I can be

Finally, i can be shown ha he aggregae producion funcion is given by Y = z N (24) where N is he aggregae labor inpu. The benchmark model is characerized by no disorions in he labor marke.")

12 showed ha Pareo-efficiency requires C (j) = C ; Y (j) = Y ; N (j) = N. (27) The marginal rae of subsiuion beween leisure and privae consumpion and beween leisure and public consumpion mus be equal o he corresponding marginal rae of ransformaion. This implies z = N ϕ C χ = N ϕ The opimaliy condiions yield he efficien allocaion G χ. (28) N = ; Y = z ; C = ( χ)z ; G = χz. (29) 5 The Ramsey problem The Ramsey planner chooses moneary and fiscal policy {G, τ, b, i } = under commimen so as o maximize expeced lifeime uiliy. We refer o his case as Full Ramsey (FR). The lagrangian of he FR problem is L FR = E { +λ b +λ p λ p = β ( χ) ln C + χ ln G (N ) +ϕ + λ f z N C G γ + ϕ 2 (π ) 2 χ C ( + i ) + β χ C + π + +λ s + λb β b + τ w N b G τ p + i π χ C ( + i ) + β χ C π +βλ s b+ + + τ + w + N + b G + τ p + i + π + ( C β (π + ) + ηp C + π + γ z N mc ηp η p β C ( (π ) + ηp C π γ z N mc ηp η p + ) π (π ) ) } π (π ), We subsiue for τ from he labor-leisure radeoff (9) and for w from he firms opimaliy condiion (5). The Ramsey planner maximizes equaion (3) relaive o he variables C, N, G, π, mc, b, i. The firs-order condiions are repored in Appendix A. We ake he Ramsey planner soluion as our benchmark. (3) This problem has been analyzed before see for example Schmi-Grohé and Uribe (24), Niemann e al. (2), and Campbell and Wren-Lewis (28), so we describe is soluion briefly. I is known ha fiscal variables follow a random walk under opimal policymaking in he absence of real 2

5 The Ramsey problem The Ramsey planner chooses moneary and fiscal policy {G, τ, b, i } = under commimen so as o maximize expeced lifeime uiliy. We refer o his case as Full Ramsey (FR).")

13 sae-coningen deb. More precisely, Lucas and Sokey (983) show ha deb and ax raes inheri he sochasic process of he exogenous shocks when deb is sae coningen, hereby overurning he random-walk resul of Barro (979). Chari e al. (99) analyze opimal policy in a flexible-price model where governmen can only issue nominal nonsae-coningen deb and find ha prices respond o shocks so as o make he real deb sae coningen. As confirmed by Aiyagari e al. (22), he key feaure in deermining he dynamic behavior of ax raes and deb is wheher markes are complee or can be compleed by flexible prices. Schmi-Grohé and Uribe (24) assume price-adjusmen coss and find ha, under opimal policy, ax raes and deb follow a random walk. Even a modes degree of price sickiness is sufficien o reduce significanly he opimal degree of inflaion volailiy and hereby resoring he random-walk behavior of fiscal variables. When γ > and changing prices is cosly, our model predics a near-uni roo componen ino labor income ax raes and governmen deb. The mirror image of his resul is ha he seady-sae level of governmen deb is indeerminae. 3 This implies ha he iniial deb level is ypically calibraed in DSGE models. An aspec ha has no received much aenion is ha he Ramsey planner s incenive o undo he disorions in he economy varies wih seady-sae level of deb. We urn o his issue nex. 5. Opimal policies and he level of deb To keep he analysis simpler, we absrac from imperfec subsiuabiliy among labor ypes, namely we se η w. Hence labor markes are perfecly compeiive. Our benchmark economy feaures wo disorions: a) imperfec compeiion in he goods marke; b) price-adjusmen coss. To illusrae how he seady-sae level of deb affecs opimal policies, we analyze he dynamic responses of he economy saring a differen levels of deb and under differen parameer calibraions. The deep parameers of he model are se according o Table. We sar from he efficien equilibrium of our model. This is he allocaion where a labor subsidy compleely eliminaes he monopolisic disorion semming from imperfec compeiion in he goods marke. Since lump-sum axes do no exis in our model, he labor subsidy as well as he provision of he public good mus be financed wih ineres 3 The rank of our sysem of eleven equaions is equal o en a he seady sae because he firs-order condiion relaive o b (4) and he one relaive o λ b are idenical. 3

, he key feaure in deermining he dynamic behavior of ax raes and deb is wheher markes are complee or can be compleed by flexible prices.")

14 Table : Benchmark Calibraion Parameer Mnemonic Value Weigh of G in uiliy χ.5 Weigh of C in uiliy χ.85 Elas. subs. goods η p Price sickiness γ 4 Serial corr. ech. ρ z Serial corr. wage mkup ρ w Discoun facor β.99 Frisch elasiciy ϕ receips on governmen asses. This implies ha a he efficien seady sae: b eff = /ηp χ β, τ eff = η p, Ceff = χ, G eff = χ, N eff = Y eff =. Noice ha he lagrangian mulipliers on he governmen budge consrain λ s, on he euler equaion λ b, and on he Phillips curve λ p are equal o zero a he efficien seady sae. The values of he macroeconomic variables of ineres are summarized in Table 2. In words, public asses mus be 24 imes GDP for he ineres income o be sufficienly high o finance subsidies and G. Since public asses are privae liabiliies in our model, he assumpion of commimen o repay on he side of privae agens may appear unrealisic wih such high level of indebedness. Bu we consider he efficien seady sae as a heoreical benchmark and mainain he assumpion ha all debs are repaid privae or public. We consider wo cases: flexible and sicky prices. Figure presens he impulse responses of our key variables o a echnological shock. Impulse responses are presened as percenage poin deviaion from he absolue value of he seady sae. In our specific case, boh public deb and labor income ax raes are negaive a he seady sae, i.e. he governmen is a ne credior b < and i provides a labor subsidy τ <. A posiive response of he variable b measures an increase in b, which is an increase in public deb or a reducion in public asses. Similarly, a posiive response of τ measures an increase in ax raes, namely higher income ax raes or lower income subsidy raes. 4

15 Table 2: Efficien seady sae Variable Symbol Value Consumpion C.85 Governmen expendiure G.5 Hours worked N Real deb b Income ax τ -. Gross inflaion π c.5 g n in mc infl ax b.4-2 z γ= γ= Figure : Ramsey policies a he efficien allocaion: Technology shock 5

16 Under flexible prices (γ = ), a echnological improvemen of one percenage poin raises privae and public spending by exacly he same proporion. The ax rae, hours, he marginal cos and public deb are compleely sabilized. On he oher hand, inflaion falls by one percen and he nominal ineres rae falls on impac. Subsidy oulays increase because he marginal produciviy of labor and wages increase. Higher governmen oulays, as measured by subsidy plus governmen spending, are financed by an increase in he real revenues from he sale of public asses due o deflaion. As a resul, governmen deb does is also compleely sabilized. When he economy is a is efficien seady sae and prices are flexible, fiscal variables do no follow a random walk because prices make real public deb sae coningen. The presence of sicky prices (γ = 4) alers hese findings significanly. Inflaion does no fall as much because i implies a cos in erms of resources. In fac, inflaion falls only by 2%. Hence, he windfall from higher real revenues from he sale of public asses is no enough o finance higher oulays on labor subsidies and governmen spending on public goods. The Ramsey planner faces a rade-off beween smoohing he effecs of he shock in he shor run and is long-run consequences. Raising ax raes reduces he budge defici bu depress hours and economic aciviy; on he oher hand, failing o raise he income ax generaes a larger defici, which means a lower level of public asses and a lower subsidy o labor in he long run. The nominal ineres rae is reduced, bu he reducion is less han half ha under flexible prices. Inuiively, he price of governmen asses would raise excessively and i would be impossible for consumers o purchase such asses wihou reducing privae consumpion. Noice ha governmen spending on he public good G increases more han under flexible prices as he Ramsey planner uses G o sabilize demand. Price-adjusmen coss reduce he volailiy of inflaion and make real governmen deb (or asses) non-sae-coningen. Following a echnological shock, fiscal variables display random-walk behavior and fail o reurn o heir iniial seady-sae values. Public asses are reduced, labor ax raes increase and governmen expendiure fall in he long run. As a resul, consumpion and hours are also reduced a he new seady sae. We now consider a echnological shock in economies characerized by differen iniial levels of public deb. In he firs economy public deb is equal o % of GDP; in he second economy he governmen is a credior and public deb is equal o - % of GDP. The seady sae of hese economies are summarized in Table 3. In he economy wih posiive public deb he ax rae is 7.35% a he seady sae and hours worked are 6

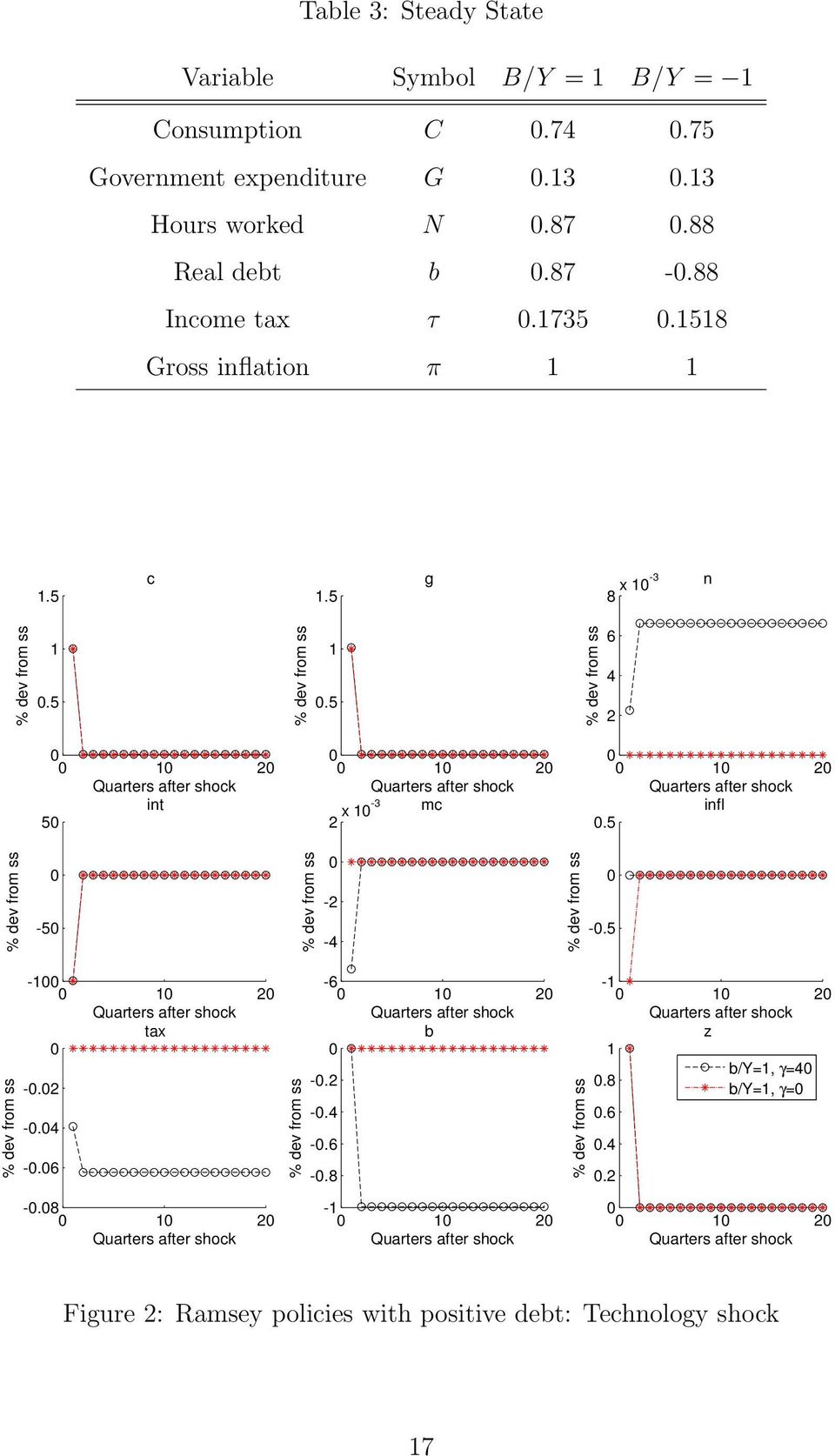

17 Table 3: Seady Sae Variable Symbol B/Y = B/Y = Consumpion C Governmen expendiure G.3.3 Hours worked N Real deb b Income ax τ Gross inflaion π.5 c.5 g 8 x -3 n in x mc -3 2 infl ax b z.8 b/y=, γ=4 b/y=, γ= Figure 2: Ramsey policies wih posiive deb: Technology shock 7

18 well below heir efficien level. As a resul, he seady sae of our economy is disored and oupu is below is efficien level. The economy wih public credi (negaive public deb) has a seady-sae ax rae of 5.8%, which raises hours and oupu relaive o he economy wih public deb. The opimal responses in he economy wih posiive public deb are illusraed in Figure 2. Under flexible prices he opimal response is idenical o he response wih flexible prices a he efficien allocaion. Under sicky prices inflaion is sabilized. The Ramsey planner reduces he labor income ax rae, which in urn sabilizes (alhough no compleely) hours and he marginal cos. The reducion in he nominal ineres rae raises he price of public deb and helps generae a budge surplus ha proporionally reduces public deb. Fiscal variables as well as privae consumpion and hours display near-uni roo behavior. Figure 3 shows he impulse responses o a echnological shocks under Ramsey-opimal policies for he economy wih an iniial level of public credi equal o percen of GDP, namely b/y =, under flexible and sicky prices. Once again, he Ramsey planner chooses o sabilize inflaion under price-adjusmen coss. Saring wih a ne posiive asse posiion he opimal policy calls for an increase in he labor income ax rae ha reduces he supply of hours. Lower ax revenues and higher governmen spending on public-good provision lead o a budge defici ha reduces public credi permanenly. When prices are flexible, inflaion is opimally used o make deb sae-coningen. The level of public deb does no maer for opimal policies. 4 On he oher hand, when prices are sicky he level of public deb maers for he fiscal response. Budge surpluses arise in he presence of public deb; deficis in he presence of public credi. The longrun response of he ax rae drives he public deb oward zero; he shor-run response ensures ha he marginal cos is sabilized so as o keep inflaion sable. When deb is equal o zero, he Ramsey planner does no have an incenive o use inflaion o reduce is repaymen. The ax rae and hours are unchanged and addiional ax revenues semming from higher real wages are used o increase governmen expendiure leaving he budge in balance. Consider now a wage mark-up shock. A he efficien seady sae wih flexible prices (γ = ) he ax rae is reduced so as o fully sabilize labor supply and he marginal cos. The shorfall in ax revenues is compensaed by deflaion ha raises real receips 4 Of course, he level of public deb maers for allocaion and herefore for welfare. 8

hours and he marginal cos.")

19 c g n in x mc infl ax.2-2 b - 2 z b/y=-, γ=4 b/y=-, γ= Figure 3: Ramsey policies wih posiive asses: Technology shock 9

20 from ousanding credi. The economy is fully sabilized see Figure 4. Wih adjusmen coss in prices he Ramsey planner prefers o keep inflaion sable and o no generae higher receips from ousanding credi. The income ax is reduced bu no as much as under price flexibiliy o limi he budge defici and he long-run increase of public deb. The ineres rae goes up o reduce curren consumpion and sabilize labor supply; governmen spending is slighly increased o compensae he fall in aggregae demand. Figure 5 displays he impulse responses in an economy wih public deb equal o GDP following a markup shock. Wih flexible prices, he dynamics of inflaion is opposie from before. Following a wage markup shock inflaion increases o reduce he real value of public deb; labor income axes fall bu no enough o sabilize labor supply. Wih sicky prices, public deb is no inflaed away and he consequen shorfall in revenues leads o a defici and o a larger deb in he long run. 6 The ineracion of moneary commimen and fiscal discreion This secion considers he case where moneary and fiscal policies are conduced by wo separae and independen auhoriies. The moneary auhoriy can credibly commi o fuure policies while he fiscal auhoriies canno do so and herefore i conducs fiscal policy under discreion. Because he wo auhoriies are independen, we analyze he equilibrium of a non-cooperaive game. We assume ha boh policymakers are benevolen and maximize social welfare. Hence, he differences in policies ha we will find relaive o he Ramsey allocaion are due o he lack of coordinaion among he wo auhoriies and/or he lack of commimen abiliy on he side of he fiscal auhoriy. The game can be formally described as follows. Le s = (s,..., s ) be he hisory of exogenous evens, where s = (z, µ w ). We can hen consisenly define moneary and fiscal sraegies. A moneary sraegy is a sae coningen plan of acions σ m = { i (s, b ) } mapping he hisory of exogenous evens ino values of he nominal ineres rae. We resric he moneary sraegy no o respond o fiscal variables 5 : 5 The sraegies we resric o are ofen labelled as open loop. Responding o fiscal variables, i.e. closed loop sraegies, may allow he cenral bank o susain equilibria ha are welfare improving, as compared o he ones we consider. However, he opimaliy of closed loop sraegies crucially relies on he possibiliy of perfecly 2

21 c.2 g n in 2 x -3 mc.2 infl ax.5..5 b.5 mushock = = Figure 4: Ramsey policies a he efficien allocaion: Wage markup shock 2

22 c g n in 4 x -3 mc infl ax b mushock = =4 2 Figure 5: Ramsey policies wih posiive deb: Wage markup shock 22

23 inuiively, he cenral bank canno use ou of equilibrium hreas o affec fiscal behavior. For convenience, we reduce he dimension of he sysem of equaions defining he se of compeiive equilibria by subsiuing for τ from he labor-leisure radeoff (9). As a consequence, we do no need o define a sraegy for ax raes. Also, we use he firms opimaliy condiion (5) o eliminae from he definiion of he equilibrium he real wage ha we hus rerieve ex-pos afer solving for he game. Hence, fiscal policy sraegies are sequences σ b = { b (s, b ) } and σ g = { G (s, b ) }. Similarly, we can define he coninuaion of sraegies from any hisory s as σ m, = { i r (s r, b s ) } r, σ b, = { b r (s r, b r s ) } r and σ g, = { G (s r, b r s ) }, respecively. We allow he rules r for deb and governmen expendiure o be condiional on he sae b, since he fiscal policy maker acs sequenially and is free o revise her plans a any ime. In conras, by he assumpion of moneary commimen, he cenral bank chooses σ m a he beginning of he game and i canno be changed laer on so ha he moneary rule can only be condiional on b. For he sake of concision, we label he vecor of policy sraegies as σ = (σ m, σ b, σ g ), while σ denoes is coninuaion. The evens of he game unfold according o he following ime-line. A a sage ha one may consider as consiuional, he cenral bank commis once and for all o σ m. Then, in every period : a) shocks occur and hey are perfecly observed by all agens and auhoriies; b) he fiscal auhoriy chooses is fiscal ools and he moneary auhoriy implemens he plan i commied o a he consiuional sage; c) privae agens form expecaions abou fuure variables; d) economic variables realize. Our iming assumpion implies ha he cenral bank leads boh he fiscal policymaker and privae agens while he fiscal policymaker leads privae agens only. We focus on he sraegic ineracion beween he moneary and fiscal auhoriies and regard households and firms as non-sraegic. Therefore, heir opimal behaviors ac as consrains in defining a compeiive equilibrium, which we formally represen as a collecion of rules observing fiscal variables, a debaable assumpion given ha reliable daa on public expendiure, ax revenues and deficis are released wih non-rivial lags. Gnocchi (22) discusses he case in an environmen similar o ours where lump-sum axes are available and he governmen budge is balanced. In such a case, if he moneary auhoriy has noisy informaion abou he acions of he fiscal policy maker, he opimal open loop converges o he opimal closed loop sraegy when he noise grows large. In oher words, open loop sraegies provide he correc limiing behavior. 23

24 A = { C (s, b ; σ), N (s, b ; σ), π (s, b ; σ), mc (s, b ; σ) } (3) saisfying households and firms opimaliy condiions for any s, given policies σ. Similarly, a coninuaion compeiive equilibrium from any hisory s, given b, is a collecion of rules A = { C (s r s, b ; σ), N (s r s, b ; σ), π (s r s, b ; σ), mc (s r s, b ; σ) } r (32) saisfying households and firms opimaliy condiions for any s r, r,, given he coninuaion of policy sraegies σ. An oucome of he game G = {A, σ}, as well is coninuaion G = {A, σ }, is a pair formed by a compeiive equilibrium and a policy profile. Given an oucome of he game G, is coninuaions G naurally induce sequences C r, N r and G r, for all possible fuure hisories s r, r. Hence, he benevolen fiscal policy maker can easily evaluae any G by compuing U f (G ) = E { r= β r ( χ) ln C r + χ ln G r (N r) +ϕ } = ( χ) ln C + χ ln G (N ) +ϕ + ϕ + ϕ + βe U f (G + ) (33) The oucome G is opimal for he fiscal policy maker if for any s and for any σ m, fiscal decisions saisfy he following properies: a) G and b obain from σ g and σ b, respecively; b) every coninuaion G maximizes U f (G ), given he coninuaion G +. Inuiively, we require sequenial raionaliy and a plan is opimal for he fiscal policy maker if is coninuaion bes serves her fuure ineress a each poin in ime. Since opimaliy of fiscal policy is defined for any moneary rule. 6, a degree of freedom is lef o choose moneary policy opimally. We can hen finally define he equilibrium of he policy game as an oucome maximizing U f (G ), subjec o he consrain ha G mus also be opimal for he fiscal policy maker 7 The nex secions clarify he way we compue he equilibrium of he policy game. 6 The condiion is necessary o invoke perfecion of he equilibrium oucome of he game. 7 The equilibrium noion we use closely follows from Klein, Krusell and Rios-Rull (28). 24

25 6. The fiscal policy problem We characerize oucomes ha are opimal for he fiscal policy maker by adoping a primal approach. This implies ha he governmen decides no only on fiscal variables bu also on privae secor choice variables, subjec o he consrain ha hey mus be consisen wih an implemenable compeiive equilibrium, given her policy choices and given σ m. The fiscal auhoriy does no decide on he nominal ineres rae i which i insead akes as given. In order o saisfy a naural crierion of raionaliy, we require he fiscal auhoriy o ake ino accoun he effec of her decisions a on he fuure economic variables ha ener her maximizaion problem a. More precisely, her decision on b affecs fuure economic variables by deermining he fuure endogenous sae of he economy ha in urn affecs curren consumpion, labor and inflaion. Sill, he fiscal policy maker canno commi o carry ou specific policies in he fuure so ha she akes as given he coninuaion oucome of he game, i.e. she akes as given boh her coninuaion sraegy and he associaed coninuaion compeiive equilibrium. auhoriy s opimal policy problem can be wrien recursively as Formally, he fiscal L f (b, s ) = ( χ) ln C (i) + χ ln G (N (i)) +ϕ (34) + ϕ + λ f z N C G γ 2 (π ) 2 + λ χ b C ( + i ) βe χ C(b, s + )Π(b, s + ) + λ s b + τ w N b G τ p + + i π λ p C βe C(b, s + )Π(b, s + ) (Π(b, s + ) )+ η p ( ) γ z N mc ηp η p π (π ) + βe L f (b, s + ) The fiscal auhoriy maximizes (34) relaive o C, N, G, π, mc, b 8. λ f is he lagrangian muliplier for he fiscal problem on he resource consrain, λ b is he lagrangian muliplier on he euler equaion of he households, λ s is he lagrangian muliplier on he governmen budge consrain, and λ p is he lagrangian muliplier on he Phillips curve. C(b, s + ) and Π(b, s + ) are differeniable 9 ime-invarian funcions describing privae secor s decisions as funcions of endogenous and exogenous sae variables. These funcions are defined o be consisen wih sae coningen rules of consumpion and inflaion saisfying he 8 The firs-order condiions associaed o his maximizaion are repored in Appendix B. 9 Differeniabiliy is a recurren resricion in he lieraure. See as an example Deboroli and Nunes (22) and Ellison and Rankin (27) who apply he same equilibrium concep o opimal fiscal and/or moneary policy problems for he case of disorive axaion and deb. 25

26 following condiions: a) hey consiue a compeiive equilibrium; b) hey solve he opimizaion program (34). As an example, we illusrae a recursion for a generic period and variable Π. A a hisory s given b, he fiscal auhoriy chooses b and funcion Π generaes π + = Π(b, s + ) for any realizaion of he shocks s +. According o our definiion of opimaliy, π + has acually o coincide wih he oucome of a coninuaion compeiive equilibrium, i.e. π + (s + s, b ) and has o be par of he soluion o he program (34) a he hisory s The moneary policy problem The moneary auhoriy chooses moneary policy under commimen and aking ino consideraion ha fiscal policy is chosen independenly and wihou commimen by he fiscal auhoriy. Once again we apply a primal approach o solve his problem so ha he moneary auhoriy decides no only moneary policy i bu also a) privae secor s variables subjec o he consrains ha allocaions consiue a compeiive equilibrium; b) he equilibrium oucome is opimal for he fiscal policy maker and hus saisfies he firs order condiions associaed o he problem (34). Formally, he maximizaion problem of he moneary auhoriy is saed in Appendix B. Inuiively, he maximizaion problem of he moneary auhoriy is now augmened by four firs-order condiions (5) o (53) ha describe he fiscal auhoriy s choice. 6.3 Seady Saes We now focus on seady-sae equilibria of he model wih moneary commimen and fiscal discreion. There exis wo non-sochasic seady saes. The firs seady sae is he efficien allocaion ha implemens he firs-bes allocaion described in secion 4. A his seady sae all consrains are slack wih he excepion of he resource consrain. The firs-bes allocaion can be implemened because he fiscal auhoriy has large posiive claims agains he privae secor o finance governmen spending and labor subsidies ha undo he disorion due o monopolisic compeiion. The efficien allocaion is a sable equilibrium. The second seady sae is repored in Table 4. The level of public deb a his seady Niemann e al. (2) find also wo seady saes in a similar model where boh moneary and fiscal policies are discreionary. 26

27 sae is negaive, which implies ha he governmen has ne posiive claims relaive o he privae secor. Neverheless, hese claims are no large enough o finance governmen expendiure and a labor subsidy large enough o eliminae he disorion from monopolisic compeiion. In fac, he fiscal auhoriy mus resor o posiive labor income axes ha make he seady sae disored. The seady-sae level deb wih fiscal discreion is equal o b = γ η p π2 (2π ). (35) This expression comes from evaluaing he firs-order condiion for he fiscal auhoriy (52) a he seady sae. Wih flexible prices γ =, governmen deb is equal o zero a he seady sae; as γ becomes posiive, he seady-sae level of deb becomes negaive. The discreionary fiscal auhoriy has an incenive o use inflaion o achieve wo goals. Firs, i aims o manipulae he real ineres rae. If he governmen is a debor (b > ), i has an incenive o increase inflaion so o reduce he real ineres rae paymens. Vice versa, when he governmen is a credior (b < ), he incenive is o reduce inflaion so as o raise real ineres raes. Second, he fiscal auhoriy aims o raise oupu because he seady sae is disored and inflaion raises oupu in he presence of price-adjusmen coss. The incenive of he fiscal auhoriy o use inflaion disappears for he level of deb in (35). Inuiively, governmen credi relaive o he privae secor needs o be large enough o generae an incenive o reduce inflaion ha exacly counerbalances he incenive o raise inflaion for simulaing he economy. These incenives are capured by he inerplay of he parameers γ and η p. When prices are flexible and γ =, he seady sae level of deb is zero. Moneary policy is neural and changes in he inflaion rae do no simulae oupu in he shor run, no maer how large he seady-sae disorion is. On he oher hand, as γ increases inflaion becomes more cosly and, given he seadysae disorion, b needs o fall o eliminae he incenive o resor o inflaion. When he disorion semming from monopolisic compeiion becomes smaller, i.e. η p increases, he incenive o simulae he economy is reduced and he seady-sae level of public credi falls. Wihou monopolisic disorion (η p ) he seady sae wih discreionary fiscal policy feaures a zero level of deb. In his case he fiscal auhoriy does no face an incenive o raise oupu and i is only wih a zero ne asse posiion relaive o he privae secor ha he fiscal auhoriy will no manipulae he real ineres rae. Deboroli and Nunes (22) consider a real model wihou monopolisic compeiion wih discreionary 27

28 Table 4: Disored seady sae wih fiscal discreion Variable Symbol Value Consumpion C.75 Governmen expendiure G.4 Hours worked N.89 Real deb b Income ax τ.277 Gross inflaion π fiscal policy and find ha he seady sae has zero deb. Our seing ness such oucome. 6.4 Dynamics We now urn o he analysis of he ineracion of commied moneary and discreionary fiscal policies in response o shocks. We limi our aenion o he case where γ = 4 and price adjusmens are cosly. Figure 6 repors he impulse responses of he variables following a echnology shock. For exposiional purposes, we assume ha he shock occurs in period ; he nominal ineres rae is repored in levels. The blue sarred line presens he impulse responses for he model wih Ramsey moneary and Discreionary fiscal policy (RD in he figure and henceforh); he red circled lines are he impulse responses o he same shock under he Ramsey planner (FR). We assume ha same iniial seady sae for boh economies as described in Table 4. Because he iniial deb b is given and equal o is seady-sae level, inflaion does no move following he echnological shock. Hence, inflaion is fully sabilized boh under RD and under FR in he period when he shock is realized. Afer his period, however, any change in he level of deb generaes a change in inflaion. The discreionary fiscal auhoriy reduces axes o limi he fall in hours; he nominal ineres rae is reduced on impac, raising he bond prices paid by he fiscal auhoriy, and governmen expendiure increases o keep he marginal uiliy from privae and public consumpion in line. The fiscal auhoriy runs a budge defici ha reduces is credi relaive o privae secor, namely b + > b. As b raises above is seady-sae level, he 28

29 c.5 g n. mc x infl i b ax revenues r y.5 2 z FR RD Figure 6: Moneary commimen and fiscal discreion: Technology shock, γ = 4 29

30 fiscal auhoriy has an incenive o raise inflaion. As shown in Figure 6, inflaion jumps he period following he echnological shock and as soon as b raises above seady sae even if inflaion is cosly. Relaive o he Ramsey planner, inflaion fails o be sabilized. The wo economies display differen dynamics following he echnological shock and hese differences are due o he lack of commimen on he side of fiscal policy. The echnology shock generaes a budge defici ha raises public deb above is seady-sae level. This, in urn, generaes posiive inflaion from period + onward. Curren inflaion π a he ime of he shock is perfecly sabilized under eiher scenario; however, under FR fuure expeced inflaion is sabilized while under RD his is no he case. This explains why he marginal cos falls a under discreion due o a higher ax rae and a lower wage. The dynamics of he economy afer period + are driven by he differen longrun adjusmen under RD and FR. Fiscal variables as well as consumpion, hours and oupu display near-uni roo behavior: he credi of he fiscal auhoriy vis-a-vis he privae secor is reduced and he new labor ax rae is permanenly higher. Under RD he economy reurns o is iniial seady sae and he adjusmen process of public credi drives he adjusmen process of inflaion. Figure 7 illusraes he impulse responses o a wage markup shock. As before, we compare he responses in he economy wih moneary commimen and fiscal discreion o hose in he economy wih full commimen. The economy sars a he seady sae described in Table 4. A wage markup shock can be inerpreed as a shock o he elasiciy of subsiuion among labor ypes ha emporarily raises he wedge beween he marginal rae of subsiuion beween leisure and consumpion and he marginal rae of ransformaion. As a resul, he wage iincreases wihou an increase in produciviy. Ramsey-opimal policies fully sabilize inflaion and he marginal cos. They do so by reducing he labor income ax rae, which limis he reducion in hours so as o keep he real wage consan. Lower ax raes combined wih lower hours reduce ax revenues. Governmen spending is cu in line wih he reducion in privae consumpion, which falls also in response o higher nominal ineres rae. The laer policy makes borrowing by households more cosly.the resuling budge defici reduces permanenly public claims agains he privae secor. The dynamic response of he economy wih fiscal discreion fails o sabilize inflaion and he marginal cos. A he ime of he shock iniial claims are a heir seady sae level and inflaion remains sable. The fiscal auhoriy reduces axes bu no as much as 3

Economics Honors Exam 2008 Solutions Question 5

Economics Honors Exam 2008 Soluions Quesion 5 (a) (2 poins) Oupu can be decomposed as Y = C + I + G. And we can solve for i by subsiuing in equaions given in he quesion, Y = C + I + G = c 0 + c Y D + I

Economics Honors Exam 2008 Soluions Quesion 5 (a) (2 poins) Oupu can be decomposed as Y = C + I + G. And we can solve for i by subsiuing in equaions given in he quesion, Y = C + I + G = c 0 + c Y D + I

11/6/2013. Chapter 14: Dynamic AD-AS. Introduction. Introduction. Keeping track of time. The model s elements

Inroducion Chaper 14: Dynamic D-S dynamic model of aggregae and aggregae supply gives us more insigh ino how he economy works in he shor run. I is a simplified version of a DSGE model, used in cuing-edge

Inroducion Chaper 14: Dynamic D-S dynamic model of aggregae and aggregae supply gives us more insigh ino how he economy works in he shor run. I is a simplified version of a DSGE model, used in cuing-edge

The Real Business Cycle paradigm. The RBC model emphasizes supply (technology) disturbances as the main source of

disturbances as the main source of") Prof. Harris Dellas Advanced Macroeconomics Winer 2001/01 The Real Business Cycle paradigm The RBC model emphasizes supply (echnology) disurbances as he main source of macroeconomic flucuaions in a world

Prof. Harris Dellas Advanced Macroeconomics Winer 2001/01 The Real Business Cycle paradigm The RBC model emphasizes supply (echnology) disurbances as he main source of macroeconomic flucuaions in a world

4. International Parity Conditions

4. Inernaional ariy ondiions 4.1 urchasing ower ariy he urchasing ower ariy ( heory is one of he early heories of exchange rae deerminaion. his heory is based on he concep ha he demand for a counry's currency

4. Inernaional ariy ondiions 4.1 urchasing ower ariy he urchasing ower ariy ( heory is one of he early heories of exchange rae deerminaion. his heory is based on he concep ha he demand for a counry's currency

II.1. Debt reduction and fiscal multipliers. dbt da dpbal da dg. bal

Quarerly Repor on he Euro Area 3/202 II.. Deb reducion and fiscal mulipliers The deerioraion of public finances in he firs years of he crisis has led mos Member Saes o adop sizeable consolidaion packages.

Quarerly Repor on he Euro Area 3/202 II.. Deb reducion and fiscal mulipliers The deerioraion of public finances in he firs years of he crisis has led mos Member Saes o adop sizeable consolidaion packages.

BALANCE OF PAYMENTS. First quarter 2008. Balance of payments

BALANCE OF PAYMENTS DATE: 2008-05-30 PUBLISHER: Balance of Paymens and Financial Markes (BFM) Lena Finn + 46 8 506 944 09, lena.finn@scb.se Camilla Bergeling +46 8 506 942 06, camilla.bergeling@scb.se

BALANCE OF PAYMENTS DATE: 2008-05-30 PUBLISHER: Balance of Paymens and Financial Markes (BFM) Lena Finn + 46 8 506 944 09, lena.finn@scb.se Camilla Bergeling +46 8 506 942 06, camilla.bergeling@scb.se

MNB Working papers 2010/5. The role of financial market structure and the trade elasticity for monetary policy in open economies

MNB Working papers 21/5 Karin Rabisch The role of financial marke srucure and he rade elasiciy for moneary policy in open economies The role of financial marke srucure and he rade elasiciy for moneary

MNB Working papers 21/5 Karin Rabisch The role of financial marke srucure and he rade elasiciy for moneary policy in open economies The role of financial marke srucure and he rade elasiciy for moneary

Optimal Monetary Policy When Lump-Sum Taxes Are Unavailable: A Reconsideration of the Outcomes Under Commitment and Discretion*

Opimal Moneary Policy When Lump-Sum Taxes Are Unavailable: A Reconsideraion of he Oucomes Under Commimen and Discreion* Marin Ellison Dep of Economics Universiy of Warwick Covenry CV4 7AL UK m.ellison@warwick.ac.uk

Opimal Moneary Policy When Lump-Sum Taxes Are Unavailable: A Reconsideraion of he Oucomes Under Commimen and Discreion* Marin Ellison Dep of Economics Universiy of Warwick Covenry CV4 7AL UK m.ellison@warwick.ac.uk

Real exchange rate variability in a two-country business cycle model

Real exchange rae variabiliy in a wo-counry business cycle model Håkon Trevoll, November 15, 211 Absrac Real exchange rae flucuaions have imporan implicaions for our undersanding of he sources and ransmission

Real exchange rae variabiliy in a wo-counry business cycle model Håkon Trevoll, November 15, 211 Absrac Real exchange rae flucuaions have imporan implicaions for our undersanding of he sources and ransmission

INSTRUMENTS OF MONETARY POLICY*

Aricles INSTRUMENTS OF MONETARY POLICY* Bernardino Adão** Isabel Correia** Pedro Teles**. INTRODUCTION A classic quesion in moneary economics is wheher he ineres rae or he money supply is he beer insrumen

Aricles INSTRUMENTS OF MONETARY POLICY* Bernardino Adão** Isabel Correia** Pedro Teles**. INTRODUCTION A classic quesion in moneary economics is wheher he ineres rae or he money supply is he beer insrumen

Efficient Risk Sharing with Limited Commitment and Hidden Storage

Efficien Risk Sharing wih Limied Commimen and Hidden Sorage Árpád Ábrahám and Sarola Laczó March 30, 2012 Absrac We exend he model of risk sharing wih limied commimen e.g. Kocherlakoa, 1996) by inroducing

Efficien Risk Sharing wih Limied Commimen and Hidden Sorage Árpád Ábrahám and Sarola Laczó March 30, 2012 Absrac We exend he model of risk sharing wih limied commimen e.g. Kocherlakoa, 1996) by inroducing

Working Paper Monetary aggregates, financial intermediate and the business cycle

econsor www.econsor.eu Der Open-Access-Publikaionsserver der ZBW Leibniz-Informaionszenrum Wirschaf The Open Access Publicaion Server of he ZBW Leibniz Informaion Cenre for Economics Hong, Hao Working

econsor www.econsor.eu Der Open-Access-Publikaionsserver der ZBW Leibniz-Informaionszenrum Wirschaf The Open Access Publicaion Server of he ZBW Leibniz Informaion Cenre for Economics Hong, Hao Working

Stochastic Optimal Control Problem for Life Insurance

Sochasic Opimal Conrol Problem for Life Insurance s. Basukh 1, D. Nyamsuren 2 1 Deparmen of Economics and Economerics, Insiue of Finance and Economics, Ulaanbaaar, Mongolia 2 School of Mahemaics, Mongolian

Sochasic Opimal Conrol Problem for Life Insurance s. Basukh 1, D. Nyamsuren 2 1 Deparmen of Economics and Economerics, Insiue of Finance and Economics, Ulaanbaaar, Mongolia 2 School of Mahemaics, Mongolian

PROFIT TEST MODELLING IN LIFE ASSURANCE USING SPREADSHEETS PART ONE

Profi Tes Modelling in Life Assurance Using Spreadshees PROFIT TEST MODELLING IN LIFE ASSURANCE USING SPREADSHEETS PART ONE Erik Alm Peer Millingon 2004 Profi Tes Modelling in Life Assurance Using Spreadshees

Profi Tes Modelling in Life Assurance Using Spreadshees PROFIT TEST MODELLING IN LIFE ASSURANCE USING SPREADSHEETS PART ONE Erik Alm Peer Millingon 2004 Profi Tes Modelling in Life Assurance Using Spreadshees

Why Did the Demand for Cash Decrease Recently in Korea?

Why Did he Demand for Cash Decrease Recenly in Korea? Byoung Hark Yoo Bank of Korea 26. 5 Absrac We explores why cash demand have decreased recenly in Korea. The raio of cash o consumpion fell o 4.7% in

Why Did he Demand for Cash Decrease Recenly in Korea? Byoung Hark Yoo Bank of Korea 26. 5 Absrac We explores why cash demand have decreased recenly in Korea. The raio of cash o consumpion fell o 4.7% in

Debt management and optimal fiscal policy with long bonds 1

Deb managemen and opimal fiscal policy wih long bonds Elisa Faraglia 2 Alber Marce 3 and Andrew Sco 4 Absrac We sudy Ramsey opimal fiscal policy under incomplee markes in he case where he governmen issues

Deb managemen and opimal fiscal policy wih long bonds Elisa Faraglia 2 Alber Marce 3 and Andrew Sco 4 Absrac We sudy Ramsey opimal fiscal policy under incomplee markes in he case where he governmen issues

Duration and Convexity ( ) 20 = Bond B has a maturity of 5 years and also has a required rate of return of 10%. Its price is $613.

20 = Bond B has a maturity of 5 years and also has a required rate of return of 10%. Its price is $613.") Graduae School of Business Adminisraion Universiy of Virginia UVA-F-38 Duraion and Convexiy he price of a bond is a funcion of he promised paymens and he marke required rae of reurn. Since he promised

Graduae School of Business Adminisraion Universiy of Virginia UVA-F-38 Duraion and Convexiy he price of a bond is a funcion of he promised paymens and he marke required rae of reurn. Since he promised

A One-Sector Neoclassical Growth Model with Endogenous Retirement. By Kiminori Matsuyama. Final Manuscript. Abstract

A One-Secor Neoclassical Growh Model wih Endogenous Reiremen By Kiminori Masuyama Final Manuscrip Absrac This paper exends Diamond s OG model by allowing he agens o make he reiremen decision. Earning a

A One-Secor Neoclassical Growh Model wih Endogenous Reiremen By Kiminori Masuyama Final Manuscrip Absrac This paper exends Diamond s OG model by allowing he agens o make he reiremen decision. Earning a

CRISES AND THE FLEXIBLE PRICE MONETARY MODEL. Sarantis Kalyvitis

CRISES AND THE FLEXIBLE PRICE MONETARY MODEL Saranis Kalyviis Currency Crises In fixed exchange rae regimes, counries rarely abandon he regime volunarily. In mos cases, raders (or speculaors) exchange

CRISES AND THE FLEXIBLE PRICE MONETARY MODEL Saranis Kalyviis Currency Crises In fixed exchange rae regimes, counries rarely abandon he regime volunarily. In mos cases, raders (or speculaors) exchange

Debt Relief and Fiscal Sustainability for HIPCs *

Deb Relief and Fiscal Susainabiliy for HIPCs * Craig Burnside and Domenico Fanizza December 24 Absrac The enhanced HIPC iniiaive is disinguished from previous deb relief programs by is condiionaliy ha

Deb Relief and Fiscal Susainabiliy for HIPCs * Craig Burnside and Domenico Fanizza December 24 Absrac The enhanced HIPC iniiaive is disinguished from previous deb relief programs by is condiionaliy ha

Measuring macroeconomic volatility Applications to export revenue data, 1970-2005

FONDATION POUR LES ETUDES ET RERS LE DEVELOPPEMENT INTERNATIONAL Measuring macroeconomic volailiy Applicaions o expor revenue daa, 1970-005 by Joël Cariolle Policy brief no. 47 March 01 The FERDI is a

FONDATION POUR LES ETUDES ET RERS LE DEVELOPPEMENT INTERNATIONAL Measuring macroeconomic volailiy Applicaions o expor revenue daa, 1970-005 by Joël Cariolle Policy brief no. 47 March 01 The FERDI is a

Working Paper Capital Mobility, Consumption Substitutability, and the Effectiveness of Monetary Policy in Open Economies

econsor www.econsor.eu Der Open-Access-Publikaionsserver der ZBW Leibniz-Informaionszenrum Wirschaf The Open Access Publicaion Server of he ZBW Leibniz Informaion Cenre for Economics Pierdzioch, Chrisian

econsor www.econsor.eu Der Open-Access-Publikaionsserver der ZBW Leibniz-Informaionszenrum Wirschaf The Open Access Publicaion Server of he ZBW Leibniz Informaion Cenre for Economics Pierdzioch, Chrisian

How To Calculate Price Elasiciy Per Capia Per Capi

Price elasiciy of demand for crude oil: esimaes for 23 counries John C.B. Cooper Absrac This paper uses a muliple regression model derived from an adapaion of Nerlove s parial adjusmen model o esimae boh

Price elasiciy of demand for crude oil: esimaes for 23 counries John C.B. Cooper Absrac This paper uses a muliple regression model derived from an adapaion of Nerlove s parial adjusmen model o esimae boh

Chapter 10 Social Security 1

Chaper 0 Social Securiy 0. Inroducion A ypical social securiy sysem provides income during periods of unemploymen, ill-healh or disabiliy, and financial suppor, in he form of pensions, o he reired. Alhough

Chaper 0 Social Securiy 0. Inroducion A ypical social securiy sysem provides income during periods of unemploymen, ill-healh or disabiliy, and financial suppor, in he form of pensions, o he reired. Alhough

Analysis of tax effects on consolidated household/government debts of a nation in a monetary union under classical dichotomy

MPRA Munich Personal RePEc Archive Analysis of ax effecs on consolidaed household/governmen debs of a naion in a moneary union under classical dichoomy Minseong Kim 8 April 016 Online a hps://mpra.ub.uni-muenchen.de/71016/

MPRA Munich Personal RePEc Archive Analysis of ax effecs on consolidaed household/governmen debs of a naion in a moneary union under classical dichoomy Minseong Kim 8 April 016 Online a hps://mpra.ub.uni-muenchen.de/71016/

Real Business Cycles Theory

Real Business Cycles Theory Research on economic flucuaions has progressed rapidly since Rober Lucas revived he profession s ineres in business cycle heory. Business cycle heory is he heory of he naure

Real Business Cycles Theory Research on economic flucuaions has progressed rapidly since Rober Lucas revived he profession s ineres in business cycle heory. Business cycle heory is he heory of he naure

LECTURE: SOCIAL SECURITY HILARY HOYNES UC DAVIS EC230 OUTLINE OF LECTURE:

LECTURE: SOCIAL SECURITY HILARY HOYNES UC DAVIS EC230 OUTLINE OF LECTURE: 1. Inroducion and definiions 2. Insiuional Deails in Social Securiy 3. Social Securiy and Redisribuion 4. Jusificaion for Governmen

LECTURE: SOCIAL SECURITY HILARY HOYNES UC DAVIS EC230 OUTLINE OF LECTURE: 1. Inroducion and definiions 2. Insiuional Deails in Social Securiy 3. Social Securiy and Redisribuion 4. Jusificaion for Governmen

The Greek financial crisis: growing imbalances and sovereign spreads. Heather D. Gibson, Stephan G. Hall and George S. Tavlas

The Greek financial crisis: growing imbalances and sovereign spreads Heaher D. Gibson, Sephan G. Hall and George S. Tavlas The enry The enry of Greece ino he Eurozone in 2001 produced a dividend in he

The Greek financial crisis: growing imbalances and sovereign spreads Heaher D. Gibson, Sephan G. Hall and George S. Tavlas The enry The enry of Greece ino he Eurozone in 2001 produced a dividend in he

Chapter 7. Response of First-Order RL and RC Circuits

Chaper 7. esponse of Firs-Order L and C Circuis 7.1. The Naural esponse of an L Circui 7.2. The Naural esponse of an C Circui 7.3. The ep esponse of L and C Circuis 7.4. A General oluion for ep and Naural

Chaper 7. esponse of Firs-Order L and C Circuis 7.1. The Naural esponse of an L Circui 7.2. The Naural esponse of an C Circui 7.3. The ep esponse of L and C Circuis 7.4. A General oluion for ep and Naural

DOES TRADING VOLUME INFLUENCE GARCH EFFECTS? SOME EVIDENCE FROM THE GREEK MARKET WITH SPECIAL REFERENCE TO BANKING SECTOR

Invesmen Managemen and Financial Innovaions, Volume 4, Issue 3, 7 33 DOES TRADING VOLUME INFLUENCE GARCH EFFECTS? SOME EVIDENCE FROM THE GREEK MARKET WITH SPECIAL REFERENCE TO BANKING SECTOR Ahanasios

Invesmen Managemen and Financial Innovaions, Volume 4, Issue 3, 7 33 DOES TRADING VOLUME INFLUENCE GARCH EFFECTS? SOME EVIDENCE FROM THE GREEK MARKET WITH SPECIAL REFERENCE TO BANKING SECTOR Ahanasios

Research on Inventory Sharing and Pricing Strategy of Multichannel Retailer with Channel Preference in Internet Environment

Vol. 7, No. 6 (04), pp. 365-374 hp://dx.doi.org/0.457/ijhi.04.7.6.3 Research on Invenory Sharing and Pricing Sraegy of Mulichannel Reailer wih Channel Preference in Inerne Environmen Hanzong Li College

Vol. 7, No. 6 (04), pp. 365-374 hp://dx.doi.org/0.457/ijhi.04.7.6.3 Research on Invenory Sharing and Pricing Sraegy of Mulichannel Reailer wih Channel Preference in Inerne Environmen Hanzong Li College

International Risk Sharing: Through Equity Diversification or Exchange Rate Hedging?

WP/09/38 Inernaional Risk Sharing: Through Equiy Diversificaion or Exchange Rae Hedging? Charles Engel and Akio Masumoo 2009 Inernaional Moneary Fund WP/09/38 IMF Working Paper Research Deparmen Inernaional

WP/09/38 Inernaional Risk Sharing: Through Equiy Diversificaion or Exchange Rae Hedging? Charles Engel and Akio Masumoo 2009 Inernaional Moneary Fund WP/09/38 IMF Working Paper Research Deparmen Inernaional

Cointegration: The Engle and Granger approach

Coinegraion: The Engle and Granger approach Inroducion Generally one would find mos of he economic variables o be non-saionary I(1) variables. Hence, any equilibrium heories ha involve hese variables require

Coinegraion: The Engle and Granger approach Inroducion Generally one would find mos of he economic variables o be non-saionary I(1) variables. Hence, any equilibrium heories ha involve hese variables require

Optimal Monetary Policy in a Small Open Economy with Home Bias

Opimal Moneary Policy in a Small Open Economy wih Home Bias Eser Faia y Universia Pompeu Fabra Tommaso Monacelli z IGIER, Universià Bocconi and CEPR Firs draf: January 2006 This draf: June 2007 Absrac

Opimal Moneary Policy in a Small Open Economy wih Home Bias Eser Faia y Universia Pompeu Fabra Tommaso Monacelli z IGIER, Universià Bocconi and CEPR Firs draf: January 2006 This draf: June 2007 Absrac

Interest Rates and the Market For New Light Vehicles

Federal Reserve Bank of New York Saff Repors Ineres Raes and he Marke For New Ligh Vehicles Adam Copeland George Hall Louis Maccini Saff Repor No. 741 Sepember 2015 This paper presens preliminary findings

Federal Reserve Bank of New York Saff Repors Ineres Raes and he Marke For New Ligh Vehicles Adam Copeland George Hall Louis Maccini Saff Repor No. 741 Sepember 2015 This paper presens preliminary findings

Optimal Investment and Consumption Decision of Family with Life Insurance

Opimal Invesmen and Consumpion Decision of Family wih Life Insurance Minsuk Kwak 1 2 Yong Hyun Shin 3 U Jin Choi 4 6h World Congress of he Bachelier Finance Sociey Torono, Canada June 25, 2010 1 Speaker

Opimal Invesmen and Consumpion Decision of Family wih Life Insurance Minsuk Kwak 1 2 Yong Hyun Shin 3 U Jin Choi 4 6h World Congress of he Bachelier Finance Sociey Torono, Canada June 25, 2010 1 Speaker

Efficient Subsidization of Human Capital Accumulation with Overlapping Generations and Endogenous Growth. Wolfram F. Richter and Christoph Braun

Efficien Subsidizaion of uman Capial Accumulaion wih Overlapping eneraions and Endogenous rowh by Wolfram F. Richer and Chrisoph Braun T Dormund niversiy April 29 Firs Draf o be presened a he Conference

Efficien Subsidizaion of uman Capial Accumulaion wih Overlapping eneraions and Endogenous rowh by Wolfram F. Richer and Chrisoph Braun T Dormund niversiy April 29 Firs Draf o be presened a he Conference

Journal Of Business & Economics Research September 2005 Volume 3, Number 9

Opion Pricing And Mone Carlo Simulaions George M. Jabbour, (Email: jabbour@gwu.edu), George Washingon Universiy Yi-Kang Liu, (yikang@gwu.edu), George Washingon Universiy ABSTRACT The advanage of Mone Carlo

Opion Pricing And Mone Carlo Simulaions George M. Jabbour, (Email: jabbour@gwu.edu), George Washingon Universiy Yi-Kang Liu, (yikang@gwu.edu), George Washingon Universiy ABSTRACT The advanage of Mone Carlo

Risk Modelling of Collateralised Lending

Risk Modelling of Collaeralised Lending Dae: 4-11-2008 Number: 8/18 Inroducion This noe explains how i is possible o handle collaeralised lending wihin Risk Conroller. The approach draws on he faciliies

Risk Modelling of Collaeralised Lending Dae: 4-11-2008 Number: 8/18 Inroducion This noe explains how i is possible o handle collaeralised lending wihin Risk Conroller. The approach draws on he faciliies

Network Effects, Pricing Strategies, and Optimal Upgrade Time in Software Provision.

Nework Effecs, Pricing Sraegies, and Opimal Upgrade Time in Sofware Provision. Yi-Nung Yang* Deparmen of Economics Uah Sae Universiy Logan, UT 84322-353 April 3, 995 (curren version Feb, 996) JEL codes:

Nework Effecs, Pricing Sraegies, and Opimal Upgrade Time in Sofware Provision. Yi-Nung Yang* Deparmen of Economics Uah Sae Universiy Logan, UT 84322-353 April 3, 995 (curren version Feb, 996) JEL codes:

DYNAMIC MODELS FOR VALUATION OF WRONGFUL DEATH PAYMENTS

DYNAMIC MODELS FOR VALUATION OF WRONGFUL DEATH PAYMENTS Hong Mao, Shanghai Second Polyechnic Universiy Krzyszof M. Osaszewski, Illinois Sae Universiy Youyu Zhang, Fudan Universiy ABSTRACT Liigaion, exper

DYNAMIC MODELS FOR VALUATION OF WRONGFUL DEATH PAYMENTS Hong Mao, Shanghai Second Polyechnic Universiy Krzyszof M. Osaszewski, Illinois Sae Universiy Youyu Zhang, Fudan Universiy ABSTRACT Liigaion, exper

MACROECONOMIC FORECASTS AT THE MOF A LOOK INTO THE REAR VIEW MIRROR

MACROECONOMIC FORECASTS AT THE MOF A LOOK INTO THE REAR VIEW MIRROR The firs experimenal publicaion, which summarised pas and expeced fuure developmen of basic economic indicaors, was published by he Minisry

MACROECONOMIC FORECASTS AT THE MOF A LOOK INTO THE REAR VIEW MIRROR The firs experimenal publicaion, which summarised pas and expeced fuure developmen of basic economic indicaors, was published by he Minisry

Asymmetric Labor Market Institutions in the EMU and the Volatility of Inflation and Unemployment Differentials

D I S C U S S I O N P A P E R S E R I E S IZA DP No. 6488 Asymmeric Labor Marke Insiuions in he EMU and he Volailiy of Inflaion and Unemploymen Differenials Mirko Abbrii Andreas I. Mueller April 2012 Forschungsinsiu

D I S C U S S I O N P A P E R S E R I E S IZA DP No. 6488 Asymmeric Labor Marke Insiuions in he EMU and he Volailiy of Inflaion and Unemploymen Differenials Mirko Abbrii Andreas I. Mueller April 2012 Forschungsinsiu

The real interest rate gap as an inflation indicator

The real ineres rae gap as an inflaion indicaor Kaharine S. Neiss* and Edward Nelson** * Srucural Economic Analysis Division, Moneary Analysis, Bank of England. E-mail: kaharine.neiss@bankofengland.co.uk

The real ineres rae gap as an inflaion indicaor Kaharine S. Neiss* and Edward Nelson** * Srucural Economic Analysis Division, Moneary Analysis, Bank of England. E-mail: kaharine.neiss@bankofengland.co.uk

Sovereign debt management and fiscal vulnerabilities

Sovereign deb managemen and fiscal vulnerabiliies Alessandro Missale 1 Absrac A wide consensus has emerged on he role of deb managemen in reducing fiscal vulnerabiliy by providing insurance agains macroeconomic

Sovereign deb managemen and fiscal vulnerabiliies Alessandro Missale 1 Absrac A wide consensus has emerged on he role of deb managemen in reducing fiscal vulnerabiliy by providing insurance agains macroeconomic

The Grantor Retained Annuity Trust (GRAT)

") WEALTH ADVISORY Esae Planning Sraegies for closely-held, family businesses The Granor Reained Annuiy Trus (GRAT) An efficien wealh ransfer sraegy, paricularly in a low ineres rae environmen Family business

WEALTH ADVISORY Esae Planning Sraegies for closely-held, family businesses The Granor Reained Annuiy Trus (GRAT) An efficien wealh ransfer sraegy, paricularly in a low ineres rae environmen Family business

Lecture Note on the Real Exchange Rate

Lecure Noe on he Real Exchange Rae Barry W. Ickes Fall 2004 0.1 Inroducion The real exchange rae is he criical variable (along wih he rae of ineres) in deermining he capial accoun. As we shall see, his

Lecure Noe on he Real Exchange Rae Barry W. Ickes Fall 2004 0.1 Inroducion The real exchange rae is he criical variable (along wih he rae of ineres) in deermining he capial accoun. As we shall see, his

Fiscal consolidation in an open economy with sovereign premia

Fiscal consolidaion in an open economy wih sovereign premia Aposolis Philippopoulos y (Ahens Universiy of Economics and Business, and CESifo) Peros Varhaliis (Ahens Universiy of Economics and Business)

Fiscal consolidaion in an open economy wih sovereign premia Aposolis Philippopoulos y (Ahens Universiy of Economics and Business, and CESifo) Peros Varhaliis (Ahens Universiy of Economics and Business)

Journal of Economic Dynamics & Control

Journal of Economic Dynamics & Conrol 37 (213) 1796 1813 Conens liss available a SciVerse ScienceDirec Journal of Economic Dynamics & Conrol journal homepage: www.elsevier.com/locae/jedc Search fricions,

Journal of Economic Dynamics & Conrol 37 (213) 1796 1813 Conens liss available a SciVerse ScienceDirec Journal of Economic Dynamics & Conrol journal homepage: www.elsevier.com/locae/jedc Search fricions,

Performance Center Overview. Performance Center Overview 1

Performance Cener Overview Performance Cener Overview 1 ODJFS Performance Cener ce Cener New Performance Cener Model Performance Cener Projec Meeings Performance Cener Execuive Meeings Performance Cener

Performance Cener Overview Performance Cener Overview 1 ODJFS Performance Cener ce Cener New Performance Cener Model Performance Cener Projec Meeings Performance Cener Execuive Meeings Performance Cener

Morningstar Investor Return

Morningsar Invesor Reurn Morningsar Mehodology Paper Augus 31, 2010 2010 Morningsar, Inc. All righs reserved. The informaion in his documen is he propery of Morningsar, Inc. Reproducion or ranscripion

Morningsar Invesor Reurn Morningsar Mehodology Paper Augus 31, 2010 2010 Morningsar, Inc. All righs reserved. The informaion in his documen is he propery of Morningsar, Inc. Reproducion or ranscripion

Price Controls and Banking in Emissions Trading: An Experimental Evaluation

This version: March 2014 Price Conrols and Banking in Emissions Trading: An Experimenal Evaluaion John K. Sranlund Deparmen of Resource Economics Universiy of Massachuses-Amhers James J. Murphy Deparmen

This version: March 2014 Price Conrols and Banking in Emissions Trading: An Experimenal Evaluaion John K. Sranlund Deparmen of Resource Economics Universiy of Massachuses-Amhers James J. Murphy Deparmen

LEASING VERSUSBUYING

LEASNG VERSUSBUYNG Conribued by James D. Blum and LeRoy D. Brooks Assisan Professors of Business Adminisraion Deparmen of Business Adminisraion Universiy of Delaware Newark, Delaware The auhors discuss

LEASNG VERSUSBUYNG Conribued by James D. Blum and LeRoy D. Brooks Assisan Professors of Business Adminisraion Deparmen of Business Adminisraion Universiy of Delaware Newark, Delaware The auhors discuss

Efficient Subsidization of Human Capital Accumulation with Overlapping Generations and Endogenous Growth

DISCSSION PAPER SERIES IZA DP No. 4629 Efficien Subsidizaion of uman Capial Accumulaion wih Overlapping eneraions and Endogenous rowh Wolfram. Richer Chrisoph Braun December 29 orschungsinsiu zur Zukunf

DISCSSION PAPER SERIES IZA DP No. 4629 Efficien Subsidizaion of uman Capial Accumulaion wih Overlapping eneraions and Endogenous rowh Wolfram. Richer Chrisoph Braun December 29 orschungsinsiu zur Zukunf

DISCUSSION PAPER. Emissions Targets and the Real Business Cycle. Intensity Targets versus Caps or Taxes. Carolyn Fischer and Michael R.

DISCUSSION PAPER November 2009 RFF DP 09-47 Emissions Targes and he Real Business Cycle Inensiy Targes versus Caps or Taxes Carolyn Fischer and Michael R. Springborn 66 P S. NW Washingon, DC 20036 202-328-5000

DISCUSSION PAPER November 2009 RFF DP 09-47 Emissions Targes and he Real Business Cycle Inensiy Targes versus Caps or Taxes Carolyn Fischer and Michael R. Springborn 66 P S. NW Washingon, DC 20036 202-328-5000

Interest Rates, Inflation, and Federal Reserve Policy Since 1980. Peter N. Ireland * Boston College. March 1999