Consultant and Independent Contractor Services Policies & Procedures

|

|

|

- Melinda Henderson

- 8 years ago

- Views:

Transcription

1 Consultant and Independent Contractor Services Policies & Procedures Effective Date: January 1, 1995 Updated: October 7, 2009 Table of Contents Foreword Purpose of Policy and Procedures How to Use the Manual Flow Chart Section I: Determining Employee-Employer Relationship o 20 Rule Test o "Employee or Independent Contractor? " article by R.C. Chip Goldsberry Section II: Internal Consultants o Internal Consultant Payment Form Section III: Independent Contractor/External Consultant o o o Conflict of Interest Certification Form Requisition for Purchase of Service Professional Services Agreement (PSA) Section IV: External Consultant o o Primary Business is NOT Consulting Contract and Payment Form for External Consultants Section V: Exceptions o Check Request Form Section VI: Contact Persons

2 Foreword Vanderbilt is subject to increasingly intense regulatory scrutiny from various branches of the federal government in the areas of consulting, independent contracting, and employee-employer relationships. These policies and procedures were developed to meet regulatory requirements while minimizing administrative burdens as much as possible. The policies and procedures are to be used in determining employee/employer relationships and in procuring and paying for consulting services. While the stricter policies may seem burdensome, Vanderbilt has much to lose if found not to be in compliance with the policies. The IRS has made clear its heightened level of attention to consulting arrangements. If someone has been paid as a consultant who in fact should have been classified as an employee, Vanderbilt will be liable for FICA and federal withholding taxes on the applicable payments, in addition to any interest and penalties which may apply. Vanderbilt also stands to lose substantial funds from federal contracts and grants if we do not have documented policies or if we are found to be in non-compliance with the federal requirement. The A-133 audit required by federal regulations and submitted to the federal government in July, 1993, pointed out a deficiency in that Vanderbilt did not have written policies for procuring and paying for consulting services. Our external audit firm is required to report any instances in which the University has failed to implement recommendations from the previous audit. The ultimate penalty for non-compliance with recommendations could be disallowed costs or withholding of research funds. These policies and procedures have been developed collaboratively among the various divisions of the University. Purpose of Policy and Procedures This manual sets forth a number of requirements, definitions, and procedures to be used when the need arises to retain the services of independent contractors (1) (including consultants). The Internal Revenue Service and various Government granting agencies have increased their level of attention in the areas of consulting, independent contracting, and employee-employer relationships. The Government's expectation is that Vanderbilt has in place policies and procedures in to ensure that: all payments for services performed by individuals who would be classified as employees under Internal Revenue Service guidelines are processed through Vanderbilt's payroll system, recording the appropriate FICA taxes and Federal income tax withholding amounts;

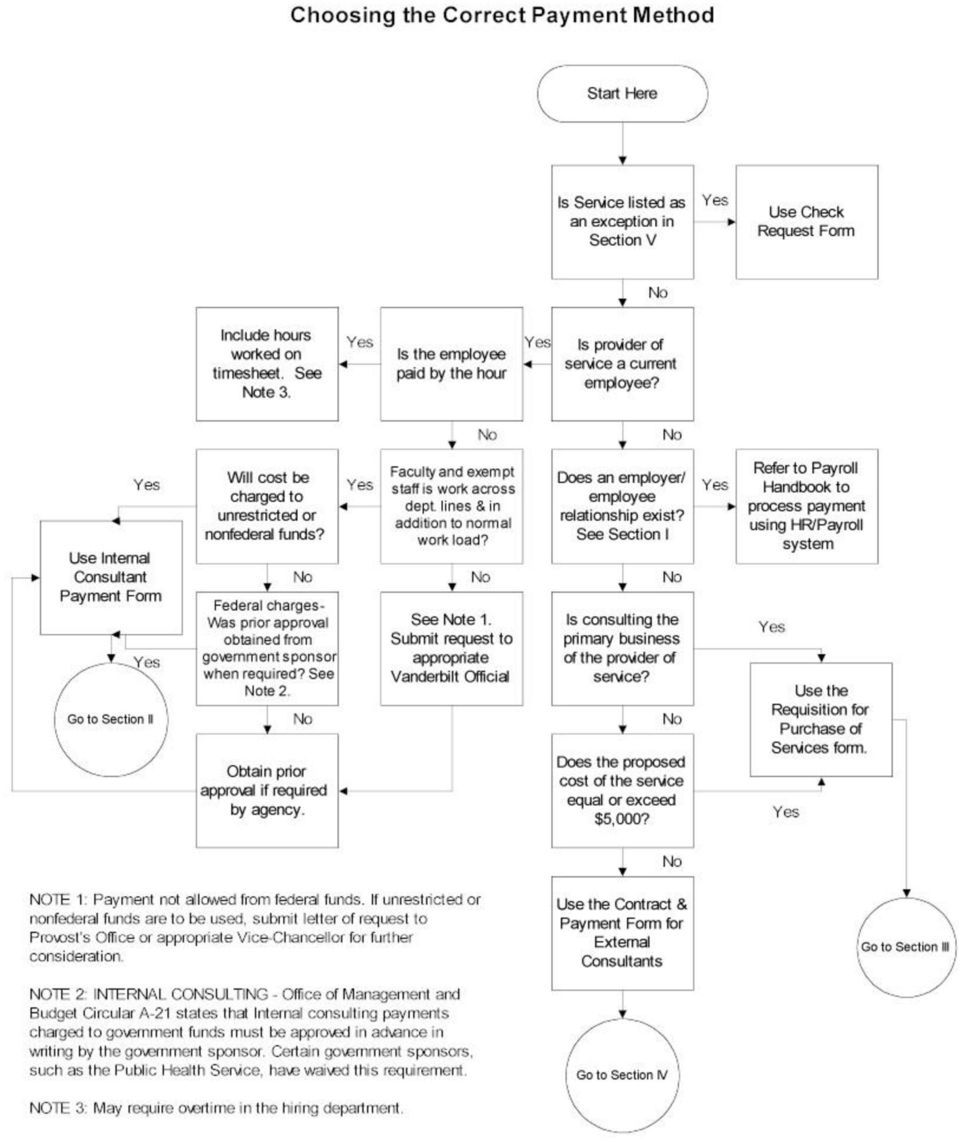

3 all agreements to retain services of independent contractors and external consultants are planned to allow for sufficient competition in pricing with written documentation retained for those of $10,000 or more; Vanderbilt faculty and exempt staff are not paid amounts in excess of stated annual salary for work performed on Government grants and contracts other than approved summer pay for faculty on academic year appointments, except in certain unusual circumstances that may require the Government's approval in advance; there is no conflict of interest for the independent contractor/external consultant or members of their family or those with whom the consultant has business or other ties for purposes of financial gain beyond that received directly for consulting services; payments made to independent contractors or external consultants are supported by sufficient documentation, including information regarding the work performed by each consultant and independent contractor and on what basis the fee was calculated and paid; and the procurement of services is conducted according to Vanderbilt University's Affirmative Action policies and procedures and applicable Government procurement regulations. (1) An Independent Contractor is an individual or firm hired to provide services over which the University has the right to control or direct only the result of the work and not the means and methods of accomplishing the result. For purposes of this policy, and external consultant (firm or individual) is a specific type of independent contractor often used, for example, to evaluate a project. An internal consultant is a faculty or staff member of Vanderbilt University and engaged to provide consulting services that are in addition to his/her normal workload and across departmental lines or that involve a separate or remote operation. How to Use this Manual There are two basic steps involved in securing and paying for consultant and independent contractor services. The first step is to determine the status of the service provider, and the second step is to initiate the appropriate paperwork based on the status determined in step one. The flow chart illustrates this process. STEP ONE: DETERMINE THE STATUS OF THE SERVICE PROVIDER from one of the alternatives below (Caution: Do not assume the provider is an independent contractor. Please review Section I.)

4 The process used to secure and pay for services will vary depending on the status of the service provider. For example, employees are distinguished from independent contractors since employees are paid through the payroll system and independent contractors are not. Once an independent contractor status is determined, independent contractors would generally be paid through the purchasing system. However, an alternative payment process is described in Section IV for external independent contractors whose primary business is not consulting, and whose fee is less than $5,000. Following is a list of various types of service providers: A. Employee: Vanderbilt faculty/staff (paid for services as part of stated annual salary) B. Internal Consultant: Vanderbilt faculty/exempt staff (paid for services in addition to stated annual salary) C. Independent Contractor/External Consultant, 1. firm or individual: Primary business is providing the required service 2. individual: Primary business is NOT consulting and anticipated fee is $5,000 or more D. Independent Contractor/External Consultant, individual: Primary business is NOT consulting and anticipated fee is less than $5,000 E. Exceptions: See Section V of this manual for list of exceptions STEP TWO: INITIATE THE APPROPRIATE PAPERWORK BASED ON THE STATUS DETERMINED IN STEP ONE. Employee status "A": Employee status "B": Employee status "C1": Employee status "C2": Employee status "D": Exception status "E": No action required under the Independent Contractor/External Consultant Policy. Process using appropriate payroll forms. Reference the Vanderbilt University Payroll Handbook (copies available at the University Central Payroll Office). See Section II of this manual See Section III of this manual See Section III of this manual See Section IV of this manual See Section V of this manual

5

6 Determining Employee-Employer Relationship The first step in the process of retaining services is determining the status of the prospective service provider. It is most crucial to determine at the outset whether or not an employeeemployer relationship exists, as failure to classify persons as employees when an employeeemployer relationship exists can result in substantial taxes, interest, and penalties imposed upon Vanderbilt. When does an employee-employer relationship exist? An employee-employer relationship exists when Vanderbilt University (which includes any Vanderbilt faculty or staff member acting in an official capacity) has the ultimate right to direct and control an individual in the way he/she works both as to the final results and as to the details of when, where, and how the work is to be performed. The University does not need to actually exercise control; it is sufficient that the University has the right to do so. The relationship established with a firm, the specifications of the service to be performed, and associated factors need to be evaluated to determine the appropriated category of payment for such services. Unless there are clear facts to support a bona fide independent contractor/external consultant status or an exception status (see list in Section V), payment for services should be made on the basis of an employee-employer relationship. What factors are to be considered in determining whether an individual is an employee or an independent contractor? 1. If the relationship to Vanderbilt University of the individual whose services are being retained is currently solely one of faculty or staff member, an employee/employer relationship automatically exists and procedures for payment of services to employees should be followed. Refer to the Payroll Handbook available through University Central and Medical Payroll Offices. 2. The determination of employee/employer status for all others is made by reviewing criteria established by the Internal Revenue Service. Use the materials in this section (Section I) for assistance in determining whether or not the individual whose services are being retained should be paid as an employee or as an independent contractor/external consultant. Who should be called to offer assistance in interpreting specific circumstances to determine whether or not a prospective service provider would be considered an employee by the Internal Revenue Service? Because of Internal Revenue Service and other tax guidelines, it is important to select the appropriate method of payment. Detailed knowledge of the assignment/engagement is necessary in determining the appropriate payment method. The specific content of the engagement/assignment can be discussed with departmental and school business officers who in

has the ultimate right to direct and control")

7 turn can obtain interpretive assistance from Human Resource Service staff who frequently work with job design matters related to employee-employer relationships. See Section VI for persons who are available to offer assistance in this regard. NOTE: The IRS "20 Rule Test" for determining employee-employer relationship and an article entitled "Employee or Independent Contractor?" are found in this section to assist in determining if an employee-employer relationship exists with the service provider. What procedure should be used to pay an employee-consultant or an independent contractor/external consultant? Employee or Internal Consultant: If it is determined that the individual whose services are being retained is an employee, payment is made through the payroll system using properly executed and approved forms. Detail of processes and procedures are found in the Payroll Handbook available through the University Central Payroll Office. Faculty and exempt staff who meet the criteria for Internal Consultants should follow the payroll payment procedures as stated in Section II of this manual. Independent Contractor/External Consultant: If it is determined that the individual whose services are being retained is an independent contractor/external consultant, payment must be made using procedures established in Section III or Section IV of this manual, whichever is appropriate. Exceptions: If it is determined that the prospective service provider is an exception listed in Section V of this manual, payment should be processed on a check request form using the University Central or Medical Center demand check system. Section I 20 Rule Test Re: Employee/Employer Relationship See Following Article for Explanation of Guideline

8 Test # The Individual Must comply with the employing department's instruction about work Receives training from or at the direction of the University Provides services that are integrated into the University's business Renders services personally; cannot sub-contract the work Permitted to hire, supervise, and compensate assistants for the University Has a continuing working relationship with the University Employer/ Employee Status Yes Yes Yes Yes Consultant Ind. Cont. Status 7 Must following set hours of work Yes No 8 Works full time for the University Yes No 9 10 Reports regularly to the University employing department Department directs the sequence in which work is performed 11 Oral or written reports regularly submitted Yes No 12 Paid on a regular basis (i.e. bi-weekly, monthly) Yes No 13 Paid for business expenses Yes No 14 Uses University tools and materials Yes No 15 Lack a major investment in facilities used to perform services 16 Can make a profit or suffer a loss from their services No Yes 17 Work for more than one employer No Yes 18 Offers services to the public No Yes 19 Can be "fired" Yes No 20 May quit work at any time and not incur liability Yes No * Source: Internal Revenue Ruling Yes Yes Yes Yes Yes No No No No No No No No No

9 Section I "Employee or Independent Contractor?" Guidelines for Determining Employment Relationships by R.C. Chip Goldsberry The ability to correctly identify people engaged to provide goods or services as either employees or independent contractors can lower an institution's tax liability and increase its chances of withstanding an Internal Revenue Service audit. Recently IRS auditors have given high priority to correct classification of employment relationships and the tax implications of decisions made. The IRS has announced that its emphasis on employment relationships and tax reporting will continue in the foreseeable future. Employers are legally required to pay FICA, FUTA, and withheld income tax on the wages of workers classified as employees. If the worker is legitimately characterized as an independent contractor, the employer is not responsible for employment-related taxes. Definitions of the terms "employee" and "independent contractor" may provide a helpful context within which to make the correct employment decision. An employee is an individual who performs services that are subject to the will and control of an employer-both what must be done and how it must be done. The employer can allow the employee considerable discretion and freedom of action, so long as the employer has the legal right to control both the method and the result of the services. An independent contractor is an individual over whom the employer has the right to control or direct only the result of the work and not the means and methods of accomplishing the result. Determining the correct employment relationship is often an ambiguous task. The IRS has provided a list of 20 common law factors to assist in determining if the service provider is an employee or an independent contractor. These factors, which appear in IRS Revenue Ruling 87-41, are intended as guidelines rather than strict rules. The closeness of most of a situation's facts to one relationship or the other will often determine what the appropriate classification should be. If the proper relationship is unclear after analyzing these factors, the employer-employee relationship should be established. 20 RULE TEST 1. An employee is required to comply with instructions about when, where, and how to work. The employer's right to instruct, not the exercise of that right, is the key. Instruction may be oral or in written procedures or manuals. An independent contractor is hired to provide goods or services and is not instructed in great detail about how to provide the goods or services.

10 2. An employee is usually trained by one of the institution's experienced employees. Training indicates that the employer wants the services performed in a certain manner. An independent contractor ordinarily uses his or her own methods, is hired for his or her expertise, and receives no training from the institution that purchases services. 3. An employee's services are usually integrated into business operations, generally showing that direction and control are being exercised. Integration of services into the business operation occurs when the success or continuation of a business depends to an appreciable degree on the performance of services that are difficult to separate from the business operation. An independent contractor's services can usually stand alone and are not integrated into business operations. 4. An employee is hired to render services personally. If the employer is interested in who does the job as well as in getting the job done, it indicates that the employer is concerned about the methods used as well as the results of services performed. An independent contractor is hired to provide a service and often the employer does not care who performs that job. 5. An employee has little control over the hiring, supervising, and payment of assistants. Such action by an employer generally shows control over people on the job with whom assistants work. An independent contractor will hire, supervise, and pay other workers under a contract in which he or she agrees to provide materials labor and is responsible for the attainment of a given result. 6. An employee normally has a continuing relationship with the person for whom services are performed. Services may be continuing even though they are performed at irregular intervals, on a part-time basis, seasonally, or over a short term. An independent contractor has a defined relationship that typically ends when the services are completed. 7. An employee has set hours of work established by the employer, indicative of control. Such a condition bars the worker from allocating time to other work, which is a right of an independent contractor. An independent contractor tends to establish time use as a matter of right. 8. An employee usually devotes full time to the business of the employer. Full time does not necessarily mean an eight-hour day or five-day week. Its meaning varies depending on the intent of the parties.

11 An independent contractor is free to work when, for whom, and for as many employers as desired. 9. An employee typically does his or her work on the employer's premises which implies control, especially if the work could be performed elsewhere. Someone who works in the employer's place of business is at least physically within the employer's direction and supervision. However, performance of work off-site does not, of itself, mean that no right to control exists. An independent contractor usually does work that can be completed on or off the employer's premises. 10. An employee often must perform services in a prescribed sequence, which shows a level of employer control. Here, too, the right to set the sequence, not the exercise of that right, is the key. An independent contractor normally is free to perform services in any manner that produces desired results. 11. An employee submits or provides regular written or oral reports that indicate employer control. An independent contractor submits reports as specified by the contract and may provide them in the broadest of terms and with less frequency than an employee would. 12. An employee is usually paid for work by the hour, week, or month. The guarantee of a minimum salary or the granting of a drawing account at stated intervals with no requirement for repayment of the excess over earnings tends to indicate the existence of an employer-employee relationship. An independent contractor is customarily paid by the job in a lump sum or on a commission basis. 13. An employee is reimbursed or paid by the employer for business and traveling expenses, a factor that indicates control over the worker. An independent contractor is paid on a job basis and normally has to assume all expenses except those specified by contract. 14. An employee usually is furnished by the employer with any tools and materials needed, which is indicative of employer control over the worker. In some jobs employees customarily use their own hand tools. An independent contractor supplies the tools and equipment. 15. An employee normally does not have a significant investment in the facilities used in the job.

12 An independent contractor often has a significant investment in facilities used in performing services. Facilities generally include equipment or premises necessary for the work, but not such items as tools, instruments, and clothing that are provided by employees as a common practice in their trade. 16. An employee usually does not realize a profit or suffer a loss as a result of the service provided. An independent contractor is in a position to realize a profit or suffer a loss as a result of services provided. 17. An employee tends to work exclusively for one employer. An independent contractor normally works for more than one employer at the same time. 18. An employee usually does not make services available to the general public. An independent contractor makes services available to the general public. "Making services available" may include hanging out a shingle, holding a business license, and having advertising and telephone directory listings. 19. An employee is subject to discharge, showing that control is exercised. Limitation of the right to discharge under a collective bargaining agreement does not detract from the existence of an employer-employee relationship. An independent contractor cannot be fired so long as results produced measure up to contract specifications. 20. An employee has the right to end the employment relationship at any time without incurring liability. An independent contractor usually agrees to complete a specific job and is responsible for its satisfactory completion or is legally obligated to make good for failure to complete the job. If administrators are still not sure whether a person is an employee or an independent contractor, they may file a Form SS-8 (Information for Use in Determining Whether a Worker Is an Employee for Federal Employment Tax Withholding) with the IRS to request an official determination. The Form SS-8 is available from local IRS offices. SAFE HARBOR FOR INDEPENDENT CONTRACTORS Until Congress enacts legislation on the classification of workers as independent contractors or employees, an employer can continue treating workers as independent contractors without incurring income tax withholding if:.a "reasonable basis" exists for not classifying the individual as an employee;

13 the employer did not or does not treat a similar individual as an employee; and the employer files all tax returns required to be filed (including information returns) on the basis that an individual is not an employee. An employer who meets the reasonable basis test can exclude an individual from employee status, if the employer reasonably relies on one of the following types of authority: judicial precedent, published rulings, or a technical advice memorandum ruling or a letter ruling issued to the employer; a past IRS audit of the employer in which the IRS did not assess employment tax deficiencies for amounts paid- to individuals holding positions substantially similar to a job held by an individual; a long-standing recognized practice of a significant segment of the industry in which an individual is engaged. These three tests are not the exclusive means of satisfying the reasonable basis requirement. An employer may also meet the reasonable basis requirement by general evidence that the individual functions as an independent contractor rather than as an employee. The safe harbor rules exclude technical personnel-such as engineers, computer programmers, systems analysts, or other similarly skilled workers-who are involved in three-party situations in which the specialist provides services for a client of a technical services firm pursuant to an arrangement between the firm and its client. These technical personnel, even if they are retained by a firm for the purpose of providing services to its clients, are treated as employees or independent contractors under the common law definitions discussed above. CONCLUSION Business officers need to assess if appropriate institutional mechanisms are in place that ensure correct employment relationship decisions are made. The assessment should begin with an examination of the current process for engaging independent contractors. A "review point" should be put in place that will test each situation for the proper employment relationship. Application of the 20 Rule Test can be a basic part of that review process. Procedures should be as nonbureaucratic as possible, yet complete enough to protect the institution in the event of an IRS audit. Some colleges and universities have placed their review point in the purchasing department, and others have chosen the human resources, accounting, or payroll areas. Business methods are changing, and business officers must change with them. Additional assistance may be obtained by reviewing IRS Code Section IRS Publication 539, Employment Taxes, is available from the IRS by calling FORM. Most payroll services also have information.

14 R.C. Chip Goldsberry is assistant director of personnel services for compensation and information systems at Purdue University. He is a member of the NACUBO Benefits and Personnel Committee. Section II Internal Consultants Request for internal consultant payments for Vanderbilt University faculty and exempt staff should be submitted only when both of the following conditions exist: a. The consultation is across departmental lines or involves a separate or remote operation. AND b. The work performed by the faculty or exempt staff member is in addition to his/her regular departmental workload. If these conditions are NOT met, a written letter of request for payment should be submitted to and approved by the appropriate Vice Chancellor (or designee) or Provost's Office prior to completion of an Internal Consultant Payment Form. When using government funds to pay for internal consulting, the budget for the grant or contract must have a specific budget line item for internal consultants or, absent this budget line item, when required, the initiating department must obtain written approval from the sponsoring agency. Payments for internal consulting by Vanderbilt Faculty or exempt staff are initiated by completing the attached Internal Consultant Payment Form. The consultant must certify that to the best of their knowledge and belief, in acting as a consultant, they will not use their position for purposes of financial gain beyond that received directly for consulting service nor will the work performed as a consultant on this project create the appearance of a conflict of interest for the consultant or members of their family or those with whom the consultant has business or other ties. All payments made to University faculty and exempt staff for internal consulting are processed through the payroll process, are subject to federal income tax and FICA withholding and reported on IRS form W-2 each calendar year.

15 Indicate the appropriate job code from the list below: Job Code Internal Consultant Account 9907 Faculty Faculty, Cost-Shared Exempt Staff Exempt Staff, Cost-Shared After all required approvals have been obtained (e.g. Department Heads, Directors, Deans, Provost, Vice Chancellor or designee), the form is routed to one of the two following areas: MEDICAL CENTER Unrestricted Centers Restricted Centers NOTE: UNIVERSITY CENTRAL Medical Payroll S-2311 MCN 2567 Medical Payroll S-2311 MCN 2567 Payroll Office Box 6310, Station B Contract & Grant Accounting VU Station B, Box The Internal Consultant Payment Form may be copied and used to initiate payment for internal consulting. Section III Independent Contractor/External Consultant Definition An independent contractor/external consultant is an individual or firm in the business of making recommendations based upon evaluations of circumstances, giving opinions on how to proceed with a given projects, or offering a proposal or plan. Independent contractors/external consultants perform a service or complete a specific task without supervision or control by the University. Examples of Independent Contractors/External Consultants May Include: Independent contractors/external consultants include program evaluators, scientists providing input on research projects, architects, landscaping companies, engineers, etc. providing services such as evaluation of programs, expert knowledge, independent opinions, painting, plumbing, electrical, air conditioning, heating, equipment repair, etc. Although the above types of services are generally performed as independent contractors, each situation should be evaluated on the

16 basis of its own facts by looking at the 20 criteria presented in Section I. Section V #3 contains examples of some specific types of independent contractors who are not paid using this method. Additional Criteria for Retaining Independent Contractors/External Consultants Independent contractors/external consultants may be engaged in those cases where the required knowledge or expertise is not available at the University and such services are needed only for a limited period of time. An independent contractor/external consultant relationship exists if an individual or firm is engaged to independently perform a specific task or service for a stated rate or total fee. The following characteristics are applicable to independent contractors/external consultants: There is no conflict of interest for the independent contractor/external consultant or members of their family or those with whom the consultant has business or other ties for purposes of financial gain beyond that received directly for consulting services. The Individual or firm is solely responsible for the manner and details of performance. However, their performance should not interfere with or disrupt the education, research, or patient care objectives of the University. The University defines/controls the final results or end products only. The individual or firm may or may not carry out his/her duties at the site of the project. All activities of the independent contractor/external consultant are conducted at his/her own risk. Thus, the University can require the individual or firm to have minimum insurance coverage as a condition of service. The University must retain a sufficient level of control over the content of work to insure that it receives adequate value for its money. Procedures The following procedures for independent contractors/external consultants are to be used for all non-employee services with two exceptions: Exception #1: The abbreviated process described in Section IV of this manual should be used for external consultants whose primary business is NOT consulting and where the cumulative dollar value of services to be retained is less than $5,000. An example would be a professor from another university who is retained by Vanderbilt to evaluate a program or project. The professor's primary business is not consulting; rather it is his/her appointment as a faculty member at the other university. Exception #2: Certain independent contractors/external consultants may be paid by use of check request forms through the University Central or Medical Center demand check system. A list of these exceptions is found in Section V of this manual.

17 For all other independent contractors/external consultants, the following procedures must be used: 1. Complete an Independent Contractor/External Consultant Requisition S Req form. Do not authorize an independent contractor/external consultant to commence work or submit an invoice for payment until a purchase order and contract (where applicable) have been issued by Procurement Services. 2. Send the standard Vanderbilt Conflict of Interest Form to the independent contractor/external consultant and request their signature attesting that there is no conflict of interest. The certification statement of this policies and procedures document must be signed by the service provider and attached to the Independent Contractor/External Consultant Requisition S Req form. 3. Complete and send the Vanderbilt Professional Services Agreement (PSA) to the consultant/contractor for their signature. The department representative endorses the completed PSA and routes the original documents to Procurement Services. Completing the PSA involves filling in the blanks with information relative to the consultant/independent contractor and the specific engagement and attaching the Statement of Work Professional Services Agreement (PSA).doc 4. There are several questions on the Independent Contractor/External Consultant Requisition S Req form that address the issue of employee-employer relationship. If you answered YES to any of these questions, please consult Section I of this manual to determine if an employee-employer relationship exists. 5. Attached the appropriate documentation on competitive bids received or documentation for sole source procurement. When using funds from government contracts and grants, attach documentation of sponsoring agency approval for sole source procurement, if required. 6. Route through the required signature authorities for your area. Procurement Services should receive the completed requisition at least two weeks prior to the anticipated start of services or tasks. 7. For services costing $10,000 or more, written documentation of competitive bidding is required as an attachment to the Services, Independent Contractor/External Consultant Requisition S Req form. Such bidding may be conducted by the department and/or Procurement Services as the complexity, sensitivity, or government regulations may dictate. If competitive bids are not obtained, written documentation justifying a sole source purchase is required.

18 Services, Independent Contractor/External Consultant Requisition S Req (MC 2995) form is ordered from the VUMC Copy Center VUMC Copy Center Forms Ordering using an 1180 internal purchasing form. 8. Procurement Services reviews the contract and, if approved, signs the agreement and issues a Purchase Order. Work may commence upon issuance of the Purchase Order. 9. Invoices from the independent contractor/external consultant are processed using Disbursement Services procedures. Even in cases where no fees are involved and only travel expenses are paid, the travel expenses must be processed through Disbursement Services. The Purchase Order number must appear on all consultant invoices. 10. Payments to individuals or partnerships who are independent contractors/external consultants are reported to the IRS on Form 1099 Miscellaneous in accordance with IRS regulations. For individuals or partnerships who are independent contractors/external consultants, please indicate the Social Security Number or Tax ID Number of the service provider. Subcontracts for "Substantive Work": The procedures outlined above are not applicable to Subcontracts for "substantive work" on government and non-government grants and contracts. Subcontracts for substantive work are processed by the offices of Sponsored Research and Contracts Administration in the Medical Center and the Division of Sponsored Research for University Central colleges, schools and divisions. Section IV External Consultant Primary Business is not Consulting Fee is Less than $5,000 The following abbreviated procedure is available for retaining external consultants whose primary business is not consulting, and whose fee is less than $5,000: Procedure 1. Prior to commencement of work, complete Section A of the Contract and Payment Form for External Consultants. Obtain the required signatures and approvals in your area including the approval of the Provost/Vice Chancellor or designee. This section should be completed prior to the individual commencing work at Vanderbilt University. 2. When services are completed, complete Section B of the Contract and Payment Form for External Consultants to include travel related expenses and total amount to be paid to the consultant. Section B also requires the signature of the Provost/Vice Chancellor or Designee. A separate check request form is NOT needed when using the "Contract and Payment Form for External Consultants."

19 3. If progress payments are required, complete Section A of the Contract and Payment Form for External Consultants for the total amount due for services to be provided. When issuing progress payments, use photocopies of the approved form for each progress payment. However, Section B must be completed for each progress payment and include the required original approval signatures. Total of progress payments cannot exceed original amount approved in Section A. 4. Payments using this form will be made through the existing demand check process. NOTE: If the total amount of the fee for services is expected to be $5,000 or more, follow procedures outlined under Section III of this manual. The attached Contract and Payment Form for External Consultants may be copied and used to initiate payment for external consultant services which are less than $5,000. Section V Exceptions Payments for the following types of services are processed by completing a Check Request Form: 1. Visiting Speakers: A one-time payment to an external speaker that consists of the speaker fee and the speaker's travel expenses, if reimbursed. Account has been established for this purpose. (Guest Speakers who are Vanderbilt faculty or exempt staff must be paid through the Personnel/Payroll process using the Internal Consultant Payment Form). 2. Subject Participants: Payments to individuals who volunteer to participate in a Vanderbilt program or project, often a sponsored research project, for a nominal fixed amount not based on any University academic or service requirements. Medical Students are NOT permitted to participate as subjects in research studies. 3. Legal, Public Accounting, Real Estate, and Other Special Expenditures: Payments for special services such as legal fees, public accounting fees, real estate services, outside catering fees, business-related entertainment fees, scholarship/fellowship/traineeship stipends, travel agency invoices, and conference registration fees. Payments to external employment agencies (1) for temporary help may be paid by check request form. Payments requested on a demand check request form will be returned to the originating department if they are determined to meet the definition of consulting or independent contractor services subject to the requirement of Section II, III, or IV of this manual.

20 (1) When temporary assistance is needed (positions to be filled for less than three months ONLY), departments should call Vanderbilt Temporary Services (VTS), a division of Human Resource Services at A pool of staff is available for clerical, technical, and support services positions. Temporary staff complete timesheets in their employing departments and are paid through the payroll system. Section VI Contact Persons Determining whether or not an employee/employer relationship exists: Human Resources Susan Mezger Financial Management Karen Nanney Warren Beck Craig Carmichel Federal Grant and Contract Policy: University Division of Sponsored Research John Childress Contract and Grant Accounting (OGCA) Michelle Vazin Medical Center Office Contracts & Grant Management (OCGM) Libby Salberg, Director Procurement Procedures

21 Procurement Services Charles Nicholas, Director Andrea Netterville, Purchasing Agent Invoicing and Payment Procedures Disbursement Services Kathryn James, Director University Affirmative Action Policies and Procedures Opportunity Development Center Sam Starks

Contracting and purchase of Professional Services (Independent Contractors or External Consultants)

") Effective Date: January 1, 1995 Updated: October 7, 2009 Updated: May 5, 2013 Updated: February 4, 2015 Foreword Contracting and purchase of Professional Services (Independent Contractors or External Consultants)

Effective Date: January 1, 1995 Updated: October 7, 2009 Updated: May 5, 2013 Updated: February 4, 2015 Foreword Contracting and purchase of Professional Services (Independent Contractors or External Consultants)

This section incorporates the IRS guidelines that are currently in effect.

Guidelines on How to Determine the Classification of Independent Contractors versus Employees Overview The University classifies and pays individuals who provide services as employees, unless the nature

Guidelines on How to Determine the Classification of Independent Contractors versus Employees Overview The University classifies and pays individuals who provide services as employees, unless the nature

GUIDELINES FOR DETERMINING EMPLOYEE OR INDEPENDENT CONTRACTOR RELATIONSHIPS

GUIDELINES FOR DETERMINING EMPLOYEE OR INDEPENDENT CONTRACTOR RELATIONSHIPS Under University policy, contracts will generally only be entered into with independent contractors (IC). Independent contractors

GUIDELINES FOR DETERMINING EMPLOYEE OR INDEPENDENT CONTRACTOR RELATIONSHIPS Under University policy, contracts will generally only be entered into with independent contractors (IC). Independent contractors

January 19, 2007. Comptrollers Office. Independent Contractor vs. Employee Discussion EXCERPTS FROM IRS. Rev. Rul. 87-41 1987-1 C.B.

January 19, 2007 Comptrollers Office Independent Contractor vs. Employee Discussion EXCERPTS FROM IRS Rev. Rul. 87-41 1987-1 C.B. 296 Section 3111 -- Social Security Tax Liability Summary THE INTERNAL

January 19, 2007 Comptrollers Office Independent Contractor vs. Employee Discussion EXCERPTS FROM IRS Rev. Rul. 87-41 1987-1 C.B. 296 Section 3111 -- Social Security Tax Liability Summary THE INTERNAL

NORTH CAROLINA STATE UNIVERSITY EMPLOYEE VS. INDEPENDENT CONTRACTOR REFERENCE GUIDE

JULY 1, 2014 NORTH CAROLINA STATE UNIVERSITY EMPLOYEE VS. INDEPENDENT CONTRACTOR REFERENCE GUIDE DWAINE COOK NC STATE UNIVERSITY Campus Box 7205 Raleigh, NC 27695 Contents EMPLOYEE VS. INDEPENDENT CONTRACTOR

JULY 1, 2014 NORTH CAROLINA STATE UNIVERSITY EMPLOYEE VS. INDEPENDENT CONTRACTOR REFERENCE GUIDE DWAINE COOK NC STATE UNIVERSITY Campus Box 7205 Raleigh, NC 27695 Contents EMPLOYEE VS. INDEPENDENT CONTRACTOR

1. PURPOSE. 1.2 This policy statement applies to all service providers except temporary personnel who are paid through an employment agency.

Memo to: All UH-Downtown/PS Holders UH-Downtown/PS 02.A.23 Issue No. 3 From: William Flores, President Effective date: 07/09/2015 Page 1 of 5 Subject: Employees and Independent Contractors 1. PURPOSE 1.1

Memo to: All UH-Downtown/PS Holders UH-Downtown/PS 02.A.23 Issue No. 3 From: William Flores, President Effective date: 07/09/2015 Page 1 of 5 Subject: Employees and Independent Contractors 1. PURPOSE 1.1

A Taxing Question: Are CFI's employees or independent contractors?

A Taxing Question: Are CFI's employees or independent contractors? The question of proper classification of workers as either employees or independent contractors is a continuing source of controversy

A Taxing Question: Are CFI's employees or independent contractors? The question of proper classification of workers as either employees or independent contractors is a continuing source of controversy

Employee or Independent Contractor?

Employee or Independent Contractor? Introduction An important question arises when a church hires, retains or selects a new person to perform a particular job for the church - is the person an employee

Employee or Independent Contractor? Introduction An important question arises when a church hires, retains or selects a new person to perform a particular job for the church - is the person an employee

SECURING AND PAYING FOR CONSULTANTS AND INDEPENDENT CONTRACTORS

SECURING AND PAYING FOR CONSULTANTS AND INDEPENDENT CONTRACTORS PURPOSE The primary purpose of this policy and procedure statement is to guide the Seminary in three areas: (1) To properly classify employees,

SECURING AND PAYING FOR CONSULTANTS AND INDEPENDENT CONTRACTORS PURPOSE The primary purpose of this policy and procedure statement is to guide the Seminary in three areas: (1) To properly classify employees,

6.5.2 Individual Consultants

6.5.2 Individual Consultants There are legal distinctions and ramifications between retaining a consultant and hiring an employee. For example, the State incurs liabilities for withholding and/or the payment

6.5.2 Individual Consultants There are legal distinctions and ramifications between retaining a consultant and hiring an employee. For example, the State incurs liabilities for withholding and/or the payment

UNIVERSITY OF HOUSTON SYSTEM ADMINISTRATIVE MEMORANDUM. SECTION: Human Resources NUMBER: 02.A.24

UNIVERSITY OF HOUSTON SYSTEM ADMINISTRATIVE MEMORANDUM SECTION: Human Resources NUMBER: 02.A.24 AREA: General SUBJECT: Employees and Independent Contractors 1. PURPOSE 1.1. This document provides guidelines

UNIVERSITY OF HOUSTON SYSTEM ADMINISTRATIVE MEMORANDUM SECTION: Human Resources NUMBER: 02.A.24 AREA: General SUBJECT: Employees and Independent Contractors 1. PURPOSE 1.1. This document provides guidelines

Independent Contractor or Employee? Worker Classification Rules under IRS Guidelines

Independent Contractor or Employee? Worker Classification Rules under IRS Guidelines Christine F. Miller (512) 495-6039 (512) 505-6339 FAX Email: cmiller@mcginnislaw.com 1 Introduction What do AT&T, JPMorgan

Independent Contractor or Employee? Worker Classification Rules under IRS Guidelines Christine F. Miller (512) 495-6039 (512) 505-6339 FAX Email: cmiller@mcginnislaw.com 1 Introduction What do AT&T, JPMorgan

PRESENT LAW AND BACKGROUND RELATING TO WORKER CLASSIFICATION FOR FEDERAL TAX PURPOSES

PRESENT LAW AND BACKGROUND RELATING TO WORKER CLASSIFICATION FOR FEDERAL TAX PURPOSES Scheduled for a Public Hearing before the SUBCOMMITTEE ON SELECT REVENUE MEASURES and the SUBCOMMITTEE ON INCOME SECURITY

PRESENT LAW AND BACKGROUND RELATING TO WORKER CLASSIFICATION FOR FEDERAL TAX PURPOSES Scheduled for a Public Hearing before the SUBCOMMITTEE ON SELECT REVENUE MEASURES and the SUBCOMMITTEE ON INCOME SECURITY

BRANDEIS UNIVERSITY POLICY

BRANDEIS UNIVERSITY POLICY Policy: Consultant/Independent Contractor Responsible Office: Office of Financial Affairs and Treasury Services Responsible Official: Senior Vice President for Finance and Treasurer,

BRANDEIS UNIVERSITY POLICY Policy: Consultant/Independent Contractor Responsible Office: Office of Financial Affairs and Treasury Services Responsible Official: Senior Vice President for Finance and Treasurer,

Independent Contracting

Independent Contracting USED BY PERMISSION From AAPA: 950 North Washington Street, Alexandria, VA 22314 www.aapa.org Deciding to practice as an independent contractor requires consideration of many factors.

Independent Contracting USED BY PERMISSION From AAPA: 950 North Washington Street, Alexandria, VA 22314 www.aapa.org Deciding to practice as an independent contractor requires consideration of many factors.

School District Obligations Under the New Federal Health Care Law: Is Your District Going to Play or Pay the Penalty?

TM MISSOURI SCHOOL BOARDS ASSOCIATION HELPING SCHOOL BOARDS SUCCEED School District Obligations Under the New Federal Health Care Law: Is Your District Going to Play or Pay the Penalty? Click to jump to

TM MISSOURI SCHOOL BOARDS ASSOCIATION HELPING SCHOOL BOARDS SUCCEED School District Obligations Under the New Federal Health Care Law: Is Your District Going to Play or Pay the Penalty? Click to jump to

Independent Contractors RF Policies and Procedures

Office of Grants Management ARE YOU INDEPENDENT? Independent Contractors RF Policies and Procedures February 24, 2009 1 What Are Our Goals? Defining Independent Contractors (IC) Identifying and completing

Office of Grants Management ARE YOU INDEPENDENT? Independent Contractors RF Policies and Procedures February 24, 2009 1 What Are Our Goals? Defining Independent Contractors (IC) Identifying and completing

Payments for Professional Services

Payments for Professional Services 512-471-8802 askus@austin.utexas.edu www.utexas.edu/business/accounting Contents INTRODUCTION 3 Authorization of Professional (Individual) Services Procedures 3 Purchasing

Payments for Professional Services 512-471-8802 askus@austin.utexas.edu www.utexas.edu/business/accounting Contents INTRODUCTION 3 Authorization of Professional (Individual) Services Procedures 3 Purchasing

Employee vs. Independent Contractor: Protecting Your Company

Attorney Stephen A. DiTullio DeWitt Ross & Stevens S.C. 2 E. Mifflin Street, Suite 600 Madison, WI 53703 (608) 252 9362 sad@dewittross.com 1 Background Facts & Statistics 60% of all businesses use independent

Attorney Stephen A. DiTullio DeWitt Ross & Stevens S.C. 2 E. Mifflin Street, Suite 600 Madison, WI 53703 (608) 252 9362 sad@dewittross.com 1 Background Facts & Statistics 60% of all businesses use independent

Employee or Independent Contractor? Avoiding Misclassification. By: Kristin N. Zielmanski

Employee or Independent Contractor? Avoiding Misclassification By: Kristin N. Zielmanski Whether an individual working for your business qualifies as an employee or an independent contractor is a question

Employee or Independent Contractor? Avoiding Misclassification By: Kristin N. Zielmanski Whether an individual working for your business qualifies as an employee or an independent contractor is a question

INDEPENDENT CONTRACTOR vs. EMPLOYEE:

INDEPENDENT CONTRACTOR vs. EMPLOYEE: IMPROPERLY TREATING A D.C. OR LMT AS AN INDEPENDENT CONTRACTOR INSTEAD OF AN EMPLOYEE CAN LEAD TO AN IRS AUDIT, FINES, PENALTIES AND PAYMENT OF UNCOLLECTED TAXES By,

INDEPENDENT CONTRACTOR vs. EMPLOYEE: IMPROPERLY TREATING A D.C. OR LMT AS AN INDEPENDENT CONTRACTOR INSTEAD OF AN EMPLOYEE CAN LEAD TO AN IRS AUDIT, FINES, PENALTIES AND PAYMENT OF UNCOLLECTED TAXES By,

INDEPENDENT CONTRACTOR AGREEMENT - OR -

INDEPENDENT CONTRACTOR AGREEMENT INSTRUCTIONS 1. It is the end-users responsibility to do the following prior to the contractor providing services: Complete all sections of the ICA and obtain the appropriate

INDEPENDENT CONTRACTOR AGREEMENT INSTRUCTIONS 1. It is the end-users responsibility to do the following prior to the contractor providing services: Complete all sections of the ICA and obtain the appropriate

Instructions for Completing the Authorization for Professional Services (APS) Form

Form") Instructions for Completing the Authorization for Professional Services (APS) Form Purpose This form is required for authorization to engage and pay individuals as guest lecturers and for other one-time,

Instructions for Completing the Authorization for Professional Services (APS) Form Purpose This form is required for authorization to engage and pay individuals as guest lecturers and for other one-time,

North Carolina Department of State Treasurer

RICHARD H. MOORE TREASURER North Carolina Department of State Treasurer State and Local Government Finance Division and the Local Government Commission T. Vance Holloman DEPUTY TREASURER Memorandum #1079

RICHARD H. MOORE TREASURER North Carolina Department of State Treasurer State and Local Government Finance Division and the Local Government Commission T. Vance Holloman DEPUTY TREASURER Memorandum #1079

Guide to the Determination of Employee/Independent Contractor Status

Employee/Contractor Website Guide to the Determination of Employee/Independent Contractor Status Related Links: Introduction At times, services are provided to the University under arrangements other than

Employee/Contractor Website Guide to the Determination of Employee/Independent Contractor Status Related Links: Introduction At times, services are provided to the University under arrangements other than

WHAT ARE THE CONSEQUENCES OF INCORRECTLY CHARACTERIZING AN INDIVIDUAL AS A CONTRACTOR AND NOT AN EMPLOYEE?

EMPLOYEE/INDEPENDENT CONTRACTOR PAYROLL POLICY Purpose StFX has developed a policy to provide guidance on the appropriate methods of payment for services provided to StFX University and whether or not

EMPLOYEE/INDEPENDENT CONTRACTOR PAYROLL POLICY Purpose StFX has developed a policy to provide guidance on the appropriate methods of payment for services provided to StFX University and whether or not

Independent Contractor vs. Employer; Identifying the correct classification

Independent Contractor vs. Employer; Identifying the correct classification Version 3A February 15, 2013 Disclaimer: This guide is solely intended to be a free advisory source. All the information contained

Independent Contractor vs. Employer; Identifying the correct classification Version 3A February 15, 2013 Disclaimer: This guide is solely intended to be a free advisory source. All the information contained

SNURE LAW OFFICE, PSC

SNURE LAW OFFICE, PSC A Professional Services Corporation Clark B. Snure Retired Of counsel Thomas G. Burke Joseph F. Quinn Brian K. Snure brian@snurelaw.com MEMORANDUM To: Washington Fire Protection Districts

SNURE LAW OFFICE, PSC A Professional Services Corporation Clark B. Snure Retired Of counsel Thomas G. Burke Joseph F. Quinn Brian K. Snure brian@snurelaw.com MEMORANDUM To: Washington Fire Protection Districts

BLOOMFIELD COLLEGE. Policy on Independent Contractors; Honorariums; and Prizes, Awards, Gifts & Scholarships

BLOOMFIELD COLLEGE Policy on Independent Contractors; Honorariums; and Prizes, Awards, Gifts & Scholarships Administration & Finance 7/1/2013 Table of Contents INDEPENDENT CONTRACTOR POLICY... 2 Background...

BLOOMFIELD COLLEGE Policy on Independent Contractors; Honorariums; and Prizes, Awards, Gifts & Scholarships Administration & Finance 7/1/2013 Table of Contents INDEPENDENT CONTRACTOR POLICY... 2 Background...

THEME: INDEPENDENT CONTRACTOR vs. EMPLOYEE. By John W. Day, MBA

THEME: INDEPENDENT CONTRACTOR vs. EMPLOYEE By John W. Day, MBA ACCOUNTING TERM: Independent Contractor An individual who contracts with an entity to perform a service independent of the entity s management

THEME: INDEPENDENT CONTRACTOR vs. EMPLOYEE By John W. Day, MBA ACCOUNTING TERM: Independent Contractor An individual who contracts with an entity to perform a service independent of the entity s management

4. EMPLOYMENT LAW. LET S GO LEGAL: The Right Road to Compliance & Protection KNOW KNOW MORE. 1. Minimum Wage & Overtime

4. EMPLOYMENT LAW KNOW There are five key areas of Employment Law for nonprofit to be aware of: 1. Minimum Wage & Overtime: Federal, State, and in some cases Local law regulates employers pay practices

4. EMPLOYMENT LAW KNOW There are five key areas of Employment Law for nonprofit to be aware of: 1. Minimum Wage & Overtime: Federal, State, and in some cases Local law regulates employers pay practices

SPECIAL REPORT CLASSIFYING WORKERS AS EMPLOYEES OR INDEPENDENT CONTRACTORS (04-03-14)

") SPECIAL REPORT CLASSIFYING WORKERS AS EMPLOYEES OR INDEPENDENT CONTRACTORS (04-03-14) This Special Report was written by Daniel P. Hale, J.D., CPCU, ARM, CRM, LIC, AIC, AIS, API of Marsh & McLennan Agency

SPECIAL REPORT CLASSIFYING WORKERS AS EMPLOYEES OR INDEPENDENT CONTRACTORS (04-03-14) This Special Report was written by Daniel P. Hale, J.D., CPCU, ARM, CRM, LIC, AIC, AIS, API of Marsh & McLennan Agency

Clergy and Non Clergy Compensation

Clergy and Non Clergy Compensation Parish treasurers are responsible for monitoring the salary and housing compensation for clergy. They need to keep abreast of the median family income for their area.

Clergy and Non Clergy Compensation Parish treasurers are responsible for monitoring the salary and housing compensation for clergy. They need to keep abreast of the median family income for their area.

School District Obligations Under the New Federal Health Care Law:

A special thanks to the following who provided technical assistance in drafting this guidance: Leza Conliffe National School Boards Association Ken Mason Spencer Fane Britt & Browne LLP Don Tatman Tatman

A special thanks to the following who provided technical assistance in drafting this guidance: Leza Conliffe National School Boards Association Ken Mason Spencer Fane Britt & Browne LLP Don Tatman Tatman

Independent Contractors: Utah

CHRISTINA M. JEPSON AND NICOLE G. FARRELL, PARSONS BEHLE & LATIMER, WITH PRACTICAL LAW LABOR & EMPLOYMENT A Q&A guide to state law on independent contractor status for private employers in Utah. This Q&A

CHRISTINA M. JEPSON AND NICOLE G. FARRELL, PARSONS BEHLE & LATIMER, WITH PRACTICAL LAW LABOR & EMPLOYMENT A Q&A guide to state law on independent contractor status for private employers in Utah. This Q&A

James R. Favor & Company

Sigma Alpha Epsilon Fraternity Independent Contractors A Review of Exposures & Risk Management Recommendations Since 1979 James R. Favor & Company has been developing and providing effective risk management

Sigma Alpha Epsilon Fraternity Independent Contractors A Review of Exposures & Risk Management Recommendations Since 1979 James R. Favor & Company has been developing and providing effective risk management

EMPLOYEE/INDEPENDENT CONTRACTOR DETERMINATION CHECKLIST

EMPLOYEE/INDEPENDENT CONTRACTOR DETERMINATION CHECKLIST Note: This form must be completed by the department and reviewed and approved by Disbursement Services BEFORE making a commitment to an individual

EMPLOYEE/INDEPENDENT CONTRACTOR DETERMINATION CHECKLIST Note: This form must be completed by the department and reviewed and approved by Disbursement Services BEFORE making a commitment to an individual

James R. Favor & Company

James R. Favor & Company Phi Delta Theta Fraternity Minimum Insurance Requirements for Independent Contractors Before Independent Contractor agreements are finalized and any work is performed, Written

James R. Favor & Company Phi Delta Theta Fraternity Minimum Insurance Requirements for Independent Contractors Before Independent Contractor agreements are finalized and any work is performed, Written

University of Illinois at Chicago Effort Reporting Policies

University of Illinois at Chicago Effort Reporting Policies As a recipient of sponsored funds, the University must assure Federal and other sponsors that the assignment of time and associated salary and

University of Illinois at Chicago Effort Reporting Policies As a recipient of sponsored funds, the University must assure Federal and other sponsors that the assignment of time and associated salary and

WORKING DRAFT. Proposed Employee Misclassification Workers Compensation Coverage Model Act

WORKING DRAFT Proposed Employee Misclassification Workers Compensation Coverage Model Act To be considered by the NCOIL Workers Compensation Insurance Committee on July 10, 2009. Sponsored for discussion

WORKING DRAFT Proposed Employee Misclassification Workers Compensation Coverage Model Act To be considered by the NCOIL Workers Compensation Insurance Committee on July 10, 2009. Sponsored for discussion

IRS Looks Closely at Independent Contractors

Hospitality Review Volume 11 Issue 1 Hospitality Review Volume 11/Issue 1 Article 2 1-1-1993 IRS Looks Closely at Independent Contractors John M. Tarras Michigan State University, shbsirc@msu.edu Follow

Hospitality Review Volume 11 Issue 1 Hospitality Review Volume 11/Issue 1 Article 2 1-1-1993 IRS Looks Closely at Independent Contractors John M. Tarras Michigan State University, shbsirc@msu.edu Follow

Policy Statement The University is committed to ensuring that effort reports completed in connection with sponsored projects are accurate.

Effort Reporting: Certifying Effort on Sponsored Projects Scope This document sets forth the University s policy on certification of effort expended on sponsored project awards administered by Alabama

Effort Reporting: Certifying Effort on Sponsored Projects Scope This document sets forth the University s policy on certification of effort expended on sponsored project awards administered by Alabama

Commonwealth of Kentucky, hereinafter referred to at the University or as the First Party, and

Rev. 2/11 UNIVERSITY OF KENTUCKY STANDARD CONTRACT FOR PERSONAL SERVICES THIS CONTRACT is made and entered into this day of, 20, by and between UNIVERSITY OF KENTUCKY, (Agency) Personal Service Contract

Rev. 2/11 UNIVERSITY OF KENTUCKY STANDARD CONTRACT FOR PERSONAL SERVICES THIS CONTRACT is made and entered into this day of, 20, by and between UNIVERSITY OF KENTUCKY, (Agency) Personal Service Contract

Enrolled Copy H.B. 29

1 PROFESSIONAL EMPLOYER ORGANIZATION 2 RELATED AMENDMENTS 3 2007 GENERAL SESSION 4 STATE OF UTAH 5 Chief Sponsor: James A. Dunnigan 6 Senate Sponsor: Curtis S. Bramble 7 8 LONG TITLE 9 General Description:

1 PROFESSIONAL EMPLOYER ORGANIZATION 2 RELATED AMENDMENTS 3 2007 GENERAL SESSION 4 STATE OF UTAH 5 Chief Sponsor: James A. Dunnigan 6 Senate Sponsor: Curtis S. Bramble 7 8 LONG TITLE 9 General Description:

Date: July 10, 2015. CSU Presidents. Vice Chancellor Human Resources. Colleagues:

Office of the Chancellor 401 Golden Shore, 4 th Floor Long Beach, CA 90802-4210 562-951-4411 Email: hradmin@calstate.edu Date: July 10, 2015 To: From: Subject: CSU Presidents Lori Lamb Vice Chancellor

Office of the Chancellor 401 Golden Shore, 4 th Floor Long Beach, CA 90802-4210 562-951-4411 Email: hradmin@calstate.edu Date: July 10, 2015 To: From: Subject: CSU Presidents Lori Lamb Vice Chancellor

$&71R SENATE BILL NO. 1105 (SUBSTITUTE FOR SENATE BILL 812 BY SENATOR SCHEDLER)

") Regular Session, 2001 $&71R SENATE BILL NO. 1105 (SUBSTITUTE FOR SENATE BILL 812 BY SENATOR SCHEDLER) BY SENATOR SCHEDLER AN ACT To enact Part XXV of Chapter 1 of Title 22 of the Louisiana Revised Statutes

Regular Session, 2001 $&71R SENATE BILL NO. 1105 (SUBSTITUTE FOR SENATE BILL 812 BY SENATOR SCHEDLER) BY SENATOR SCHEDLER AN ACT To enact Part XXV of Chapter 1 of Title 22 of the Louisiana Revised Statutes

BSM Connection elearning Course

BSM Connection elearning Course Basics of Medical Practice Finance: Part 1 2009, BSM Consulting All rights reserved. Table of Contents OVERVIEW... 1 FORMS OF DOING BUSINESS... 1 BUSINESS FORMATS AT A GLANCE...

BSM Connection elearning Course Basics of Medical Practice Finance: Part 1 2009, BSM Consulting All rights reserved. Table of Contents OVERVIEW... 1 FORMS OF DOING BUSINESS... 1 BUSINESS FORMATS AT A GLANCE...

BYLAWS OF THE UNIVERSITY O F TEXAS HEALTH SCIENCE CENTER AT SAN ANTONIO SCHOOL OF ALLIED HEALTH SCIENCES FACULTY PRACTICE PLAN

BYLAWS OF THE UNIVERSITY O F TEXAS HEALTH SCIENCE CENTER AT SAN ANTONIO SCHOOL OF ALLIED HEALTH SCIENCES FACULTY PRACTICE PLAN UT Allied Health Partners ARTICLE I PURPOSE The purpose of the UT Allied Health

BYLAWS OF THE UNIVERSITY O F TEXAS HEALTH SCIENCE CENTER AT SAN ANTONIO SCHOOL OF ALLIED HEALTH SCIENCES FACULTY PRACTICE PLAN UT Allied Health Partners ARTICLE I PURPOSE The purpose of the UT Allied Health

Reimbursement of Business Expenditures to Faculty, Staff, and Students

[Minor revision posted 4/15/16 (replaces 8/27/13 edition)] Operating Policy and Procedure : Reimbursement of Business Expenditures to Faculty, Staff, and Students DATE: April 15, 2016 PURPOSE: The purpose

[Minor revision posted 4/15/16 (replaces 8/27/13 edition)] Operating Policy and Procedure : Reimbursement of Business Expenditures to Faculty, Staff, and Students DATE: April 15, 2016 PURPOSE: The purpose

University of Colorado Health Sciences Center Administrative Policy for Faculty Compensation

Policy: 1 Page: 1 of 8 I. Purpose, Reference, and Responsibility A. Purpose The purpose of this policy is to establish guidelines for faculty compensation. B. Reference 1. University of Colorado Administrative

Policy: 1 Page: 1 of 8 I. Purpose, Reference, and Responsibility A. Purpose The purpose of this policy is to establish guidelines for faculty compensation. B. Reference 1. University of Colorado Administrative

Accounts Payable Workshop. Boston University Office of the Comptroller

Accounts Payable Workshop Boston University Office of the Comptroller Accounts Payable Workshop Topics of Discussion Accounts Payable Organization Purchases Covered by University Purchasing Policy Receipt

Accounts Payable Workshop Boston University Office of the Comptroller Accounts Payable Workshop Topics of Discussion Accounts Payable Organization Purchases Covered by University Purchasing Policy Receipt

The supply of materials and services for the University must be undertaken as follows:

9.4 PURCHASING 9.4.1 Introduction Bellarmine University operates under a Central Purchasing system. Central Purchasing allows the University to take a comprehensive and coordinated approach to supplying

9.4 PURCHASING 9.4.1 Introduction Bellarmine University operates under a Central Purchasing system. Central Purchasing allows the University to take a comprehensive and coordinated approach to supplying

Staff Wage and Salary Guidelines

Staff Wage and Salary Guidelines Preface These procedures apply to staff employed by the University of Southern California. In the event of a discrepancy between these procedures and guidelines and a collective

Staff Wage and Salary Guidelines Preface These procedures apply to staff employed by the University of Southern California. In the event of a discrepancy between these procedures and guidelines and a collective

58 JOURNAL OF COURT REPORTING / APRIL 2001

?? 58 JOURNAL OF COURT REPORTING / APRIL 2001 B Y P E T E R W A C H T Independent contractor status remains a hot issue for freelance reporters. If you don t know and follow the requirements, an unpleasant

?? 58 JOURNAL OF COURT REPORTING / APRIL 2001 B Y P E T E R W A C H T Independent contractor status remains a hot issue for freelance reporters. If you don t know and follow the requirements, an unpleasant

CONSULTING AGREEMENT

CONSULTING AGREEMENT Agreement No. 2000398 Agreement dated 3/28/2000 by and between UserEdge Technical Personnel. ("USEREDGE") and CONSULTANT S CO., Tax ID No.99-9999999, including individually and collectively,

CONSULTING AGREEMENT Agreement No. 2000398 Agreement dated 3/28/2000 by and between UserEdge Technical Personnel. ("USEREDGE") and CONSULTANT S CO., Tax ID No.99-9999999, including individually and collectively,

PREVAILING WAGE RESOURCE BOOK 2010 SCA COMPLIANCE PRINCIPLES

INTRODUCTION DISCHARGING WAGE AND FRINGE BENEFIT OBLIGATIONS EMPLOYEE NOTIFICATION AND POSTER TIMELY PAYMENT OF WAGES AND FRINGE BENEFITS HOURS WORKED BONA FIDE FRINGE BENEFITS FRINGE BENEFIT REQUIREMENTS

INTRODUCTION DISCHARGING WAGE AND FRINGE BENEFIT OBLIGATIONS EMPLOYEE NOTIFICATION AND POSTER TIMELY PAYMENT OF WAGES AND FRINGE BENEFITS HOURS WORKED BONA FIDE FRINGE BENEFITS FRINGE BENEFIT REQUIREMENTS

EMPLOYMENT ISSUES 2012-2013 BROKER-IN-CHARGE ANNUAL REVIEW INTRODUCTION

2012-2013 BROKER-IN-CHARGE ANNUAL REVIEW EMPLOYMENT ISSUES Outline: Introduction Business Entity Forms Employee versus Independent Contractor? Internal Revenue Service Criteria Unemployment Tax Purposes

2012-2013 BROKER-IN-CHARGE ANNUAL REVIEW EMPLOYMENT ISSUES Outline: Introduction Business Entity Forms Employee versus Independent Contractor? Internal Revenue Service Criteria Unemployment Tax Purposes

By: Alan H. Morgan, CPL amorgan1@flash.net (713) 805 6851

805 6851") By: Alan H. Morgan, CPL amorgan1@flash.net (713) 805 6851 The independent contractor status of land professionals has been challenged by the Internal Revenue Service and state employment agencies for many

By: Alan H. Morgan, CPL amorgan1@flash.net (713) 805 6851 The independent contractor status of land professionals has been challenged by the Internal Revenue Service and state employment agencies for many

Contracts and Grants Accounting Policies and Procedures

Introduction Contracts and Grants Accounting Policies and Procedures Contracts and grants are important to Auburn University. Much of the research that Auburn faculty, staff, and students undertake is

Introduction Contracts and Grants Accounting Policies and Procedures Contracts and grants are important to Auburn University. Much of the research that Auburn faculty, staff, and students undertake is

NPSA GENERAL PROVISIONS

NPSA GENERAL PROVISIONS 1. Independent Contractor. A. It is understood and agreed that CONTRACTOR (including CONTRACTOR s employees) is an independent contractor and that no relationship of employer-employee

NPSA GENERAL PROVISIONS 1. Independent Contractor. A. It is understood and agreed that CONTRACTOR (including CONTRACTOR s employees) is an independent contractor and that no relationship of employer-employee

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS TABLE of CONTENTS A Letter to Employers.3 The Student Loan Program...4 Collection Authority...4 The Basic Steps Employers Follow for

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS TABLE of CONTENTS A Letter to Employers.3 The Student Loan Program...4 Collection Authority...4 The Basic Steps Employers Follow for

Oklahoma Income Tax Withholding Tables

Oklahoma Income Tax Withholding Tables 2015 Effective Date: January 1, 2015 Oklahoma Tax Commission 2501 North Lincoln Boulevard Oklahoma City, Oklahoma 73194 Packet OW-2 January 2015 Table of Contents

Oklahoma Income Tax Withholding Tables 2015 Effective Date: January 1, 2015 Oklahoma Tax Commission 2501 North Lincoln Boulevard Oklahoma City, Oklahoma 73194 Packet OW-2 January 2015 Table of Contents

The attached instructions are for employers who have employees that are subject to wage garnishment in connection with the Federal Student Loan

The attached instructions are for employers who have employees that are subject to wage garnishment in connection with the Federal Student Loan Program. 1 THE STUDENT LOAN PROGRAM PROGRAM OVERVIEW The

The attached instructions are for employers who have employees that are subject to wage garnishment in connection with the Federal Student Loan Program. 1 THE STUDENT LOAN PROGRAM PROGRAM OVERVIEW The

GUIDELINES TO UNIVERSITY OF MARYLAND CONSULTANT AGREEMENT <$5,000

GUIDELINES TO UNIVERSITY OF MARYLAND CONSULTANT AGREEMENT

GUIDELINES TO UNIVERSITY OF MARYLAND CONSULTANT AGREEMENT

BFB-BUS-77: Independent Contractor Guidelines

University of California Policy BFB-BUS-77 BFB-BUS-77: Independent Contractor Guidelines Responsible Officer: AVP - Chief Procurement Officer Responsible Office: PS - Procurement Services Issuance Date:

University of California Policy BFB-BUS-77 BFB-BUS-77: Independent Contractor Guidelines Responsible Officer: AVP - Chief Procurement Officer Responsible Office: PS - Procurement Services Issuance Date:

WORKER CLASSIFICATION

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II djohnston@becpas.com

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II djohnston@becpas.com

Independent Contractor Versus Employee Status

12 Independent Contractor Versus Employee Status Failing to appropriately classify a worker as an employee or an independent contractor can have serious consequences. Companies that misclassify workers

12 Independent Contractor Versus Employee Status Failing to appropriately classify a worker as an employee or an independent contractor can have serious consequences. Companies that misclassify workers

Compensation Methods for Architectural Services

Compensation Methods for Architectural Services Compensation Methods for Architectural Services By: Thomas R. Gossen, AIA, PE Secretary/Treasurer and Chief Operating Officer Gossen Livingston Associates,

Compensation Methods for Architectural Services Compensation Methods for Architectural Services By: Thomas R. Gossen, AIA, PE Secretary/Treasurer and Chief Operating Officer Gossen Livingston Associates,

EXEMPT VS. NON-EXEMPT Identifying Employee Classification

EXEMPT VS. NON-EXEMPT Identifying Employee Classification Employee Classification Keeping it all straight The comptroller of a small company notices that her accounting clerk works a lot of overtime. In

EXEMPT VS. NON-EXEMPT Identifying Employee Classification Employee Classification Keeping it all straight The comptroller of a small company notices that her accounting clerk works a lot of overtime. In

Rationale, Process and Procedures

Independent Contractors (IC) @ Kent State University Rationale, Process and Procedures Presented by: The Division of Business and Finance The Office of General Counsel The Division of Human Resources 1

Independent Contractors (IC) @ Kent State University Rationale, Process and Procedures Presented by: The Division of Business and Finance The Office of General Counsel The Division of Human Resources 1

Funds that have been obligated by a funding agency for a particular project either as a grant, contract, or cooperative agreement.

Academic Year Salary Academic year salaries are based on the individual faculty member's regular compensation for the continuous period which, under CCU's policies, constitutes the basis of his/her salary.

Academic Year Salary Academic year salaries are based on the individual faculty member's regular compensation for the continuous period which, under CCU's policies, constitutes the basis of his/her salary.

INDEPENDENT SERVICE PROVIDER CONTRACT (ISP)

") INDEPENDENT SERVICE PROVIDER CONTRACT (ISP) INSTRUCTIONS FOR USE: The purpose of this form is to be used for contracts with individuals engaged in technical, professional or specialized skills such as

INDEPENDENT SERVICE PROVIDER CONTRACT (ISP) INSTRUCTIONS FOR USE: The purpose of this form is to be used for contracts with individuals engaged in technical, professional or specialized skills such as

Procedures and Guidelines for External Grants and Sponsored Programs

Definitions: Procedures and Guidelines for External Grants and Sponsored Programs 1. Grant and Contract Financial Administration Office (Grants Office): The office within the Accounting Operations Area

Definitions: Procedures and Guidelines for External Grants and Sponsored Programs 1. Grant and Contract Financial Administration Office (Grants Office): The office within the Accounting Operations Area

INDEPENDENT CONTRACTORS AND WORKER S COMPENSATION IN WISCONSIN

INDEPENDENT CONTRACTORS AND WORKER S COMPENSATION IN WISCONSIN Department of Workforce Development Worker s Compensation Division Bureau of Insurance Programs 201 E. Washington Ave., Rm. C100 P.O. Box

INDEPENDENT CONTRACTORS AND WORKER S COMPENSATION IN WISCONSIN Department of Workforce Development Worker s Compensation Division Bureau of Insurance Programs 201 E. Washington Ave., Rm. C100 P.O. Box

Common Payroll Pitfalls. Presented by: Christopher Brown, SPHR January 25, 2012

Common Payroll Pitfalls Presented by: Christopher Brown, SPHR January 25, 2012 1 Who is an Employee An employer-employee relationship generally exists if the person contracting for services has the right

Common Payroll Pitfalls Presented by: Christopher Brown, SPHR January 25, 2012 1 Who is an Employee An employer-employee relationship generally exists if the person contracting for services has the right

Coverage Questions for Subcontractors, General Contractors, and Independent Contractors

Coverage Questions for Subcontractors, General Contractors, and Independent Contractors 1. Which employers must carry workers' compensation coverage? 418.115 (a) (b) (c) (d) (e) All private employers regularly

Coverage Questions for Subcontractors, General Contractors, and Independent Contractors 1. Which employers must carry workers' compensation coverage? 418.115 (a) (b) (c) (d) (e) All private employers regularly

JAN 2 2 2016. changing and increasing numbers of individuals are facing. decisions on whether to choose to become entrepreneurs and go

THE SENATE TWENTY-EIGHTH LEGISLATURE, 0 STATE OF HAWAII JAN 0 A BILL FOR AN ACT S.B. NO.Mf RELATING TO EMPLOYMENT SECURITY. BE IT ENACTED BY THE LEGISLATURE OF THE STATE OF HAWAII: 0 SECTION. The legislature

THE SENATE TWENTY-EIGHTH LEGISLATURE, 0 STATE OF HAWAII JAN 0 A BILL FOR AN ACT S.B. NO.Mf RELATING TO EMPLOYMENT SECURITY. BE IT ENACTED BY THE LEGISLATURE OF THE STATE OF HAWAII: 0 SECTION. The legislature

THE ARCHDIOCESE OF SAINT PAUL AND MINNEAPOLIS

THE ARCHDIOCESE OF SAINT PAUL AND MINNEAPOLIS 2015 EMPLOYMENT LAW UPDATE SEMINAR Pay Issues Affecting Exempt (and Non-Exempt) Employees P R E S E N T E D B Y T h o m a s B. W i e s e r INTRODUCTION The

THE ARCHDIOCESE OF SAINT PAUL AND MINNEAPOLIS 2015 EMPLOYMENT LAW UPDATE SEMINAR Pay Issues Affecting Exempt (and Non-Exempt) Employees P R E S E N T E D B Y T h o m a s B. W i e s e r INTRODUCTION The

Samford University Purchasing Card (PCARD) Program Policy and Procedures May 1, 2016

Program Policy and Procedures May 1, 2016") Samford University Purchasing Card (PCARD) Program Policy and Procedures May 1, 2016 1 Table of Contents I. Overview A. Introduction..3 B. Definitions.... 3 II. Card Issuance A. Cardholder Eligibility...4

Samford University Purchasing Card (PCARD) Program Policy and Procedures May 1, 2016 1 Table of Contents I. Overview A. Introduction..3 B. Definitions.... 3 II. Card Issuance A. Cardholder Eligibility...4

Independent Contractors

Independent Contractors Employee/Worker or True Independent Contractor??? Proper Classification Duck Theory Looks like a Duck, Walks like a Duck, It must be a Duck Document Procedures Independent Contractor?????

Independent Contractors Employee/Worker or True Independent Contractor??? Proper Classification Duck Theory Looks like a Duck, Walks like a Duck, It must be a Duck Document Procedures Independent Contractor?????

Agenda. IRS Payroll Tax Audit Initiatives. Auditor of State David Yost 2011 Local Government Official s Conference Employment Tax Update