Bequest Gold Rush. Study of high net worth philanthropy. Wealth transfer study. William D. Samers

|

|

|

- Phyllis Walton

- 8 years ago

- Views:

Transcription

1

2 Why in These Times?

3 Bequest Gold Rush Study of high net worth philanthropy Wealth transfer study William D. Samers

4 Strategic Plan: Steps to Success Create a need and a legacy case Integrate Legacy message must be core fundraising priority Fundraisers need legacy prospects/goals with accountability Systems and financials should include planned giving information Solicit and engage Executive Committee, Board, and high-level, long-time donors Select which gifts to promote Create marketing plan Understand motivations and how to solicit Seek legal advice Enhance donor recognition

5 Legacy Case Statement Long term vision and relevance of organization Future plans and needs How the money will be used Future sources of funds/endowment goal

6 Integration and Counting

7 Total Financial Resource Development Fiscal Year 2000 = $76,325, E+07 Pledges $28,633,000 3E+07 Outright cash $17,278, E+07 2E+07 Legacies and Bequests $10,663,000 Testamentary pledges $10,850,000 Charitable trusts and gift annuities $4,765,000 Commitments from bequests, living trusts $4,136, E+07 1E Cash or Equivalent Lifetime gifts Commitments Three Dimension of Charitable Giving William D. Samers

8 Work with Your CFO

9 Engage the Executive Committee and Find a Lay leader Champion

10 Focus on those who can make a difference

11 Focus on the Basics

12 FY 2010 Gifts by Type as a % of Total Planned Giving & Endowments Supporting Foundations 4% Trust for the Disabled 8% Endowment Gifts 9% Bequests 69% Life Income Gifts 10% William D. Samers

13 Marketing Plan Recognition yearbook and event legacy brochure Highlight/recognize PG&E donors at events Board meeting presentations Billing statements and direct mail (tagline/stuffer) Letterhead CEO/Chairperson message General newsletter Internal marketing to staff and lay people

14 Why Are These Gifts Different From All Other Gifts?

15 Annual Gifts Capital Projects Restricted Endowments General Endowments William D. Samers

16 Recognition Mr. Philip Altheim Dr. Miriam Caslow Ms. Cheryl Fishbein Mr. Richard L. Kay, Esq. Mrs. Joan Ginsburg Ms. Marcie Imberman Mrs. Bonnie Tisch Alisa F. Levin, Esq. Mr. John J. Pomerantz Mr. Lawrence Ruben Mr. Harvey Schulweis Mrs. Lynn Tobias Mr. Leonard A. Wilf Mr. Larry Zicklin

17 Endowment Recognition Opportunities Scholarships for Students/Tuition Assistance Chairs for Staff, Rabbis and Administrators Major School Trips Academic, Elective and Extra-Curricular Programs Facilities Teacher Excellence and other Training Programs Technology

18 Investment and Negotiation

19 Ethics and Disclosure Who do you represent? Donor or the organization? Honor restrictions Ensure charitable intent Consider timing issues Limit donor s giving What to disclose Costs and fees, assets, tax benefits, investment issues Investment vs. charitable gifts Where to disclose it Marketing materials Conversations Detailed proposals

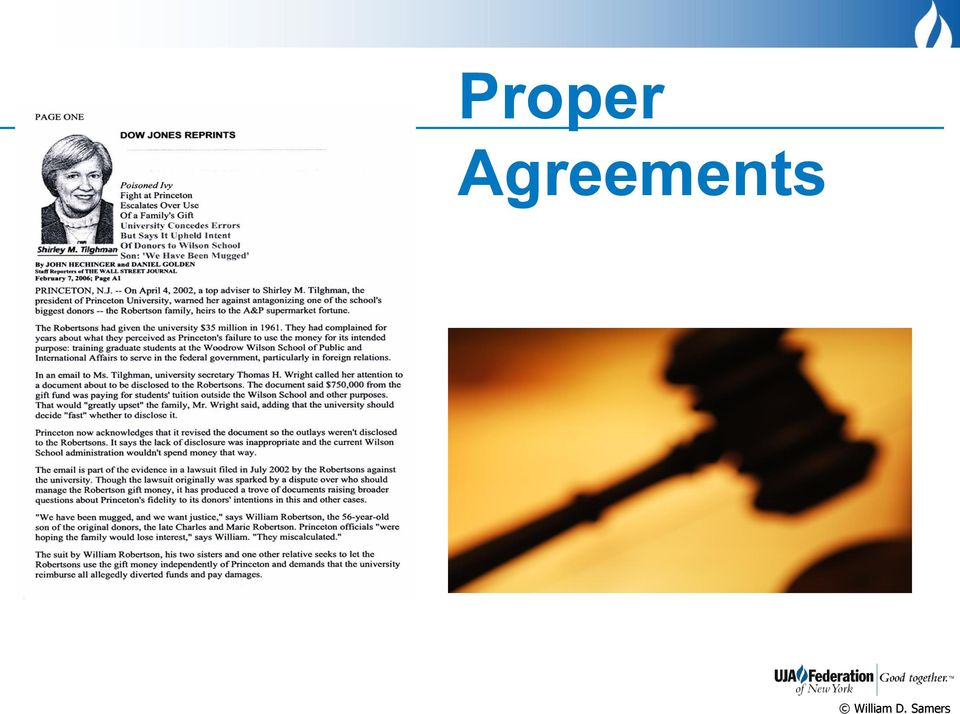

20 Proper Agreements William D. Samers

21 In House Consultant Attorney Accountant Financial planner

22 Outside Consultant

23 Delegate and Focus

24 Choosing the Right Gifts and Asking for Them

25 Over the Transom

26 Donor Motivations 1. Caring Heart 2. Recognition 3. Religious belief 4. Peer pressure 5. Mission critical 6. Content 7. Giving back 8. Reciprocity 9. Effect change 10. Drink the water 11. Counted 12. Financial Stability 13. Responsibility for Future 14. Family values 14. No/hate/love kids 15. Government vs. you 16. Name lives on/legacy 17. Exchange of value 18. Tax savings 19. Financially beneficial 20. Stewardship/cultivation 21. Financial sound org 22. Last chance to do good 23. Recession 3x effect 24. Reduce expenses 25. Program Affordability and enhancement 26. Alternative support

27 And One More Motivation

28 Big donors really matter Pyramid of Giving Campaigns based upon a large number of people each making equal gifts never works The larger the top of the pyramid the easier your campaign Remember gifts are both current and future money William D. Samers

29 Ways to Ask for Bequests

30 How to Ask: Key Phrases

31 The Less Personal Asks

32 Bequests

33 Testamentary Pledges

34 Gifts That Work Like Bequests Life Income Gifts IRA S Life Insurance Real Estate

35 IRA s & Life Insurance

36 Life Income Gifts

37 Real Estate

38 CANNOT WAIT

39 Creative Bequests Bequests lead to outright Virtual endowment Mortgage endowment Gift annuity proceeds reduction Trade-in Layaway Family philanthropy William D. Samers

40 Balloon Loans = Virtual Endowment

41 Home Mortgage = Mortgage Endowment

42 Mortgage Endowment Year Endowment value held at ACWIS at beginni ng of year Annual Paym ent by donor to ACWI S Amount sent to Instit ute from ACW IS Portion of Payme nt used for annual costs (intere st) Endowment earnings applied to annual amount sent to Institute Portion of payment applied to endowme nt (principal) Endowment value held at ACWIS at end of year 2007 $0 $272,000 $120,000 $120,000 0 $152,000 $152, $152,000 $272,000 $120,000 $110,880 $9,120 $161,120 $313, $313,120 $272,000 $120,000 $101,213 $18,787 $170,787 $483, $483,907 $272,000 $120,000 $90,966 $29,034 $181,034 $664, $664,942 $272,000 $120,000 $80,104 $39,896 $191,896 $856, $856,838 $272,000 $120,000 $68,590 $51,410 $203,410 $1,060, $1,060,248 $272,000 $120,000 $56,385 $63,615 $215,615 $1,275, $1,275,863 $272,000 $120,000 $43,448 $76,552 $228,552 $1,504, $1,504,415 $272,000 $120,000 $29,735 $90,265 $242,265 $1,746, $1,746,680 $272,000 $120,000 $15,199 $104,801 $256,801 $2,003,481

43 Trade In = Larger Endowment

44 Private Sample Sale

45 Lease = Limited Time Project

46 Limited Partnership = Matching Grant Anonymous alumnus pledges challenge grant: challenges Centre alumni to reclaim No. 1

47 Layaway Plan = Down Payment Locks Bequest Price

48 Private Equity Fund = Family Endowment

49 Reverse Mortgage = Gift Annuity Proceeds + Bequest Method to Calculate Value of Remaining Principal of Annuities: Column J refers to final remaining principal in a given year The chart on Page 2 is calculated as follows: Column D (Year End Principal) = Column A (Beginning Principal) +Column B [Deemed Earnings*] Column C [Distribution] Column H (Year End Principal) = Column E (Beginning Principal) +Column E [Deemed Earnings*] Column F [Distribution] = Column I is calculated as follows: A (Gift Annuity One) + E (Gift Annuity Two) Column J calculated as follows: D (Gift Annuity One) + H (Gift Annuity Two) = J *The earnings included in the formula are based on the historic rate of return for ACWIS gift annuity account. The rate of earnings for purposes of this Agreement shall be fixed in amount and shall not be subject to revision. In some cases the dollar amounts have been rounded. Should D/K establish additional charitable gift annuities with the ACWIS, and if he designates that those annuities be used for the purposes set forth in the Agreement, then the remaining principal of those annuities as of his death, will be calculated in accordance with the same assumptions and earnings rate applicable to Gift Annuity One and Gift annuity Two, and the testamentary pledge of D/K of $5,000, referred to in Section 1(a) of the Agreement, shall, in addition to any offsets because of the remaining principal balance of Gift Annuity One and Gift Annuity Two, be further reduced, dollar for dollar, by the remaining principal value of such additional gift annuities existing as of his death. As and when such additional gift annuities are established, the Table of Principal Values attached hereto shall be revised to encompass the additional gift annuity. At the point in any given year that D/K should die, the remaining principal will be valued as of the year end principal for the year in which death occurred (Column J) notwithstanding that all distributions for such year have not been made as of D/K s death. William D. Samers

50 Professional Estate Planning = Lead Trust/Remainder Trust

51 ETFs = General Funds Repackaged

52 After the Gift

53 Take Home

54 Staff Stanley Baumblatt Eva Bilick Rebecca Blake Samantha Claster Ali Fedder Stacy Ferber Veronica Fischmann Inna Galperin Shira Hudson Minal Jain Chong Kim Livia Kutsher Lyndsie Levine William Samers Diane Scherer Tami Smith Meredith Streit

55 William D. Samers Vice President Planned Giving & Endowments UJA-Federation of New York 130 East 59th Street - Rm 1061 New York, NY Phone: Fax: samersw@ujafedny.org William D. Samers

Executive Summary Planned Giving and Endowment Policies (For Donors and Donors Advisors)

") Appendix B Authority for Gift Acceptance Policies Executive Summary Planned Giving and Endowment Policies (For Donors and Donors Advisors) Independence Institute encourages and solicits outright and deferred

Appendix B Authority for Gift Acceptance Policies Executive Summary Planned Giving and Endowment Policies (For Donors and Donors Advisors) Independence Institute encourages and solicits outright and deferred

Legacy Society. A Lasting Commitment to Excellence

Legacy Society A Lasting Commitment to Excellence Strengthening the Future of the Council on Foreign Relations Today s Council on Foreign Relations continues to build on the extraordinary vision and effort

Legacy Society A Lasting Commitment to Excellence Strengthening the Future of the Council on Foreign Relations Today s Council on Foreign Relations continues to build on the extraordinary vision and effort

SAF Planned Giving Instrument Descriptions and FAQ s

SAF Planned Giving Instrument Descriptions and FAQ s The Society of American Foresters has a number of planned giving instruments available which provide a means for members and their families to financially

SAF Planned Giving Instrument Descriptions and FAQ s The Society of American Foresters has a number of planned giving instruments available which provide a means for members and their families to financially

Columbus Metropolitan Library Foundation Gift Acceptance Policy. Introduction

Columbus Metropolitan Library Foundation Gift Acceptance Policy Introduction Columbus Metropolitan Library Foundation (the Foundation ) is an organization recognized as exempt from federal income taxation

Columbus Metropolitan Library Foundation Gift Acceptance Policy Introduction Columbus Metropolitan Library Foundation (the Foundation ) is an organization recognized as exempt from federal income taxation

Mission: Our Vision: United Way Services of Geauga County unites people and resources to improve lives.

Create your legacy. Mission: United Way Services of Geauga County unites people and resources to improve lives. Our Vision: United Way Services of Geauga County is the organization recognized for collaborating

Create your legacy. Mission: United Way Services of Geauga County unites people and resources to improve lives. Our Vision: United Way Services of Geauga County is the organization recognized for collaborating

Sample Financial Policies

This document includes examples of one organization s (disguised as ABC) financial policies related to gift acceptance, expenditures, disbursements and investments. The samples may help other organizations

This document includes examples of one organization s (disguised as ABC) financial policies related to gift acceptance, expenditures, disbursements and investments. The samples may help other organizations

Getting Started in Planned Giving: Developing a Program on a Budget

Getting Started in Planned Giving: Developing a Program on a Budget Raising Funds for Your Organization s Future: Part III of A Series of Webinars about Planned Giving Sponsored by DC Bar Pro Bono Program

Getting Started in Planned Giving: Developing a Program on a Budget Raising Funds for Your Organization s Future: Part III of A Series of Webinars about Planned Giving Sponsored by DC Bar Pro Bono Program

frequently asked questions

endowing the future frequently asked questions about the salk s endowment What is the endowment? Endowment refers to assets that are invested for the long term and intended to provide a permanent source

endowing the future frequently asked questions about the salk s endowment What is the endowment? Endowment refers to assets that are invested for the long term and intended to provide a permanent source

Creating a Charitable Lead Annuity Trust. Planning for your family s financial future? Minimize taxes while helping Stanford.

Rolling Orange Creating a Charitable Lead Annuity Trust Planning for your family s financial future? Minimize taxes while helping Stanford. Seeking Solutions, Educating Leaders Through a Stanford charitable

Rolling Orange Creating a Charitable Lead Annuity Trust Planning for your family s financial future? Minimize taxes while helping Stanford. Seeking Solutions, Educating Leaders Through a Stanford charitable

GIFT ACCEPTANCE POLICY

GIFT ACCEPTANCE POLICY INTRODUCTION This policy (the Policy ) is designed to assure that all gifts to, or for the use of, Grinnell College are structured to benefit Grinnell College while ensuring fidelity

GIFT ACCEPTANCE POLICY INTRODUCTION This policy (the Policy ) is designed to assure that all gifts to, or for the use of, Grinnell College are structured to benefit Grinnell College while ensuring fidelity

CHARITABLE GIVING: DOING WELL BY DOING GOOD AND THE LAWYER S ROLE IN THE CHARITABLE GIVING PROCESS

CHARITABLE GIVING: DOING WELL BY DOING GOOD AND THE LAWYER S ROLE IN THE CHARITABLE GIVING PROCESS James C. Provenza, J.D., CPA Attorney At Law Chicago phone: 847-729-3939 Rockford phone: 815-298-0664

CHARITABLE GIVING: DOING WELL BY DOING GOOD AND THE LAWYER S ROLE IN THE CHARITABLE GIVING PROCESS James C. Provenza, J.D., CPA Attorney At Law Chicago phone: 847-729-3939 Rockford phone: 815-298-0664

GIFT PLANNING GIve The GIFT of KNowLedGe

GIFT PLANNING Give the Gift of Knowledge Would you like to make a gift to Syracuse University, but assume it is beyond your financial means? Long-term strategic planning may be the answer you are looking

GIFT PLANNING Give the Gift of Knowledge Would you like to make a gift to Syracuse University, but assume it is beyond your financial means? Long-term strategic planning may be the answer you are looking

SAMPLE Gift Acceptance Policies and Procedures for Annual Fundraising

SAMPLE Gift Acceptance Policies and Procedures for Annual Fundraising A. Cash Gifts and Pledges 1. Unrestricted Gifts of Cash Gifts given without restriction on the use of the gift. a) Unrestricted gifts

SAMPLE Gift Acceptance Policies and Procedures for Annual Fundraising A. Cash Gifts and Pledges 1. Unrestricted Gifts of Cash Gifts given without restriction on the use of the gift. a) Unrestricted gifts

About the VSE Survey and Data Miner Guide

About the VSE Survey and Data Miner Guide This guide is intended to help Voluntary Support of Education (VSE) survey participants and Data Miner users better understand the VSE survey and to serve as an

About the VSE Survey and Data Miner Guide This guide is intended to help Voluntary Support of Education (VSE) survey participants and Data Miner users better understand the VSE survey and to serve as an

Real Estate Gifts. Major and Planned Gifts Fact Sheets

Real Estate Gifts A primary residence, vacation home, farm, or undeveloped lot often represents a major asset that may be used to make a substantial charitable gift. Particularly in the case of greatly

Real Estate Gifts A primary residence, vacation home, farm, or undeveloped lot often represents a major asset that may be used to make a substantial charitable gift. Particularly in the case of greatly

Gift planning newsletter from Cornell University Spring 2013. American Taxpayer Relief Act: How it Affects You. 2013 Tax Brackets

Financial Planner Gift planning newsletter from Cornell University Spring 2013 American Taxpayer Relief Act: How it Affects You Just before the country would have rolled off the fiscal cliff, Congress

Financial Planner Gift planning newsletter from Cornell University Spring 2013 American Taxpayer Relief Act: How it Affects You Just before the country would have rolled off the fiscal cliff, Congress

GIVE AND YOU SHALL RECEIVE CHARITABLE GIVING, CREATING A PLAN THAT S RIGHT FOR YOU

GIVE AND YOU SHALL RECEIVE CHARITABLE GIVING, CREATING A PLAN THAT S RIGHT FOR YOU Contents 1 Give and you shall receive 3 Techniques summary 5 Planning for charitable giving NOT FDIC OR NCUA INSURED NOT

GIVE AND YOU SHALL RECEIVE CHARITABLE GIVING, CREATING A PLAN THAT S RIGHT FOR YOU Contents 1 Give and you shall receive 3 Techniques summary 5 Planning for charitable giving NOT FDIC OR NCUA INSURED NOT

Guide to CHRIS Kids Planned Giving: The Shade Tree Society

Guide to CHRIS Kids Planned Giving: The Shade Tree Society "People have made at least a start at understanding when they plant shade trees under which they know full well they will never sit." - Elton

Guide to CHRIS Kids Planned Giving: The Shade Tree Society "People have made at least a start at understanding when they plant shade trees under which they know full well they will never sit." - Elton

GIFT ACCEPTANCE POLICY COMPASSPOINT

Grantee charities may find that adoption and implementation of a Gift Acceptance Policy will provides reassurance to grantors. In any event, the charity will want to review these policies carefully and

Grantee charities may find that adoption and implementation of a Gift Acceptance Policy will provides reassurance to grantors. In any event, the charity will want to review these policies carefully and

Major and Planned Gifts Fact Sheets

Charitable Gift Annuities Charitable gift annuities, or CGAs, are one of the oldest and most reliable charitable options and have particular appeal to retirees and senior citizens. Religious organizations

Charitable Gift Annuities Charitable gift annuities, or CGAs, are one of the oldest and most reliable charitable options and have particular appeal to retirees and senior citizens. Religious organizations

A GUIDE TO FREE THE KIDS PLANNED GIVING PROGRAM

A GUIDE TO FREE THE KIDS PLANNED GIVING PROGRAM What is more liberating than the knowledge that you are loved? This is what we do here create a place of security and love where children can be freed from

A GUIDE TO FREE THE KIDS PLANNED GIVING PROGRAM What is more liberating than the knowledge that you are loved? This is what we do here create a place of security and love where children can be freed from

Millersville University Foundation Gift Acceptance Policy

Accepted: November 9, 1999 Revised: February 2014 Millersville University Foundation Gift Acceptance Policy Policy Statement Millersville University and the Millersville University Foundation strongly

Accepted: November 9, 1999 Revised: February 2014 Millersville University Foundation Gift Acceptance Policy Policy Statement Millersville University and the Millersville University Foundation strongly

Methods of Giving. Create Your Texas A&M Legacy GIVING

Methods of Giving Create Your Texas A&M Legacy GIVING What is the Texas A&M Foundation? Founded in 1953, the Texas A&M Foundation is a nonprofit organization that encourages major gifts and manages endowments

Methods of Giving Create Your Texas A&M Legacy GIVING What is the Texas A&M Foundation? Founded in 1953, the Texas A&M Foundation is a nonprofit organization that encourages major gifts and manages endowments

INDEX 546 / THE COMPLETE GUIDE TO PLANNED GIVING

INDEX This index is nonconventional in that I added items that are not included in this book. Maybe they will get into the next edition. However, I didn t want my readers to go crazy searching for things

INDEX This index is nonconventional in that I added items that are not included in this book. Maybe they will get into the next edition. However, I didn t want my readers to go crazy searching for things

Planned Giving: When It Is Not All That You Do JAMES K. PHELPS, J.D.,

Planned Giving: When It Is Not All That You Do THURSDAY, NOVEMBER 19, 2015 JAMES K. PHELPS, J.D., ACFRE PRINCIPAL JKP FUNDRAISING LLC Objectives learn basic components of a planned giving program determine

Planned Giving: When It Is Not All That You Do THURSDAY, NOVEMBER 19, 2015 JAMES K. PHELPS, J.D., ACFRE PRINCIPAL JKP FUNDRAISING LLC Objectives learn basic components of a planned giving program determine

Opportunities for Giving. Olmsted Medical Center Women s Health Pavilion

Opportunities for Giving Olmsted Medical Center Women s Health Pavilion Our Mission The delivery of exceptional patient care focusing on caring, quality, safety, and service. Our Vision To be the healthcare

Opportunities for Giving Olmsted Medical Center Women s Health Pavilion Our Mission The delivery of exceptional patient care focusing on caring, quality, safety, and service. Our Vision To be the healthcare

Gift Acceptance Policy

Gift Acceptance Policy Purpose The purpose of this Gift Acceptance Policy is to establish the guidelines according to which the Catholic Community Foundation of Los Angeles (the Foundation ) accepts gifts

Gift Acceptance Policy Purpose The purpose of this Gift Acceptance Policy is to establish the guidelines according to which the Catholic Community Foundation of Los Angeles (the Foundation ) accepts gifts

XIV. Accounting for Gifts, Endowment Earnings and Other Projects

XIV. Accounting for Gifts, Endowment Earnings and Other Projects A. Overview: RIT receives gifts and other income to support the operations of the University. Gifts that are restricted for use by the donor

XIV. Accounting for Gifts, Endowment Earnings and Other Projects A. Overview: RIT receives gifts and other income to support the operations of the University. Gifts that are restricted for use by the donor

www.plannedgiving.com (800) 873-9203 success@plannedgiving.com Gayle Union, CFRE Matt Hugg Viken Mikaelian

873-9203 success@plannedgiving.com Gayle Union, CFRE Matt Hugg Viken Mikaelian") Gayle Union, CFRE Matt Hugg Viken Mikaelian $495 00 Bequest Contents and Overview This is not the actual toolkit. Tool k it Two toolkits in one: 1Marketing 2Stewardship This kit contains everything you

Gayle Union, CFRE Matt Hugg Viken Mikaelian $495 00 Bequest Contents and Overview This is not the actual toolkit. Tool k it Two toolkits in one: 1Marketing 2Stewardship This kit contains everything you

Ways to Give. A guide to gift planning at Canisius College

Ways to Give A guide to gift planning at Canisius College Past generations of Canisius College alumni and friends demonstrated their leadership and loyalty with planned gifts to the college - legacies

Ways to Give A guide to gift planning at Canisius College Past generations of Canisius College alumni and friends demonstrated their leadership and loyalty with planned gifts to the college - legacies

GOOD LAND TRUST Fundraising Plan

GOOD LAND TRUST Fundraising Plan OVERVIEW OF THE FUNDRAISING PLAN Background The Good Land Trust is a land trust working in Ecotopia actively protecting natural resources and the open landscapes that define

GOOD LAND TRUST Fundraising Plan OVERVIEW OF THE FUNDRAISING PLAN Background The Good Land Trust is a land trust working in Ecotopia actively protecting natural resources and the open landscapes that define

LONG BEACH ROTARY SCHOLARSHIP FOUNDATION GIFT ACCEPTANCE POLICY

Approved by the Board of Directors on 6/1/11 LONG BEACH ROTARY SCHOLARSHIP FOUNDATION GIFT ACCEPTANCE POLICY To ensure compliance with applicable legal and fiduciary requirements and to provide guidance

Approved by the Board of Directors on 6/1/11 LONG BEACH ROTARY SCHOLARSHIP FOUNDATION GIFT ACCEPTANCE POLICY To ensure compliance with applicable legal and fiduciary requirements and to provide guidance

A Guide to Planned Giving. your Mills your legacy

A Guide to Planned Giving your Mills your legacy MILLS COLLEGE, a thriving liberal arts college for women with graduate programs for women and men, is a very special institution. Since Mills founding in

A Guide to Planned Giving your Mills your legacy MILLS COLLEGE, a thriving liberal arts college for women with graduate programs for women and men, is a very special institution. Since Mills founding in

GIFT ACCEPTANCE POLICIES

GIFT ACCEPTANCE POLICIES The Montana Community Foundation (MCF) solicits and accepts outright gifts with income dedicated immediately to the charitable needs of the community, planned gifts with split

GIFT ACCEPTANCE POLICIES The Montana Community Foundation (MCF) solicits and accepts outright gifts with income dedicated immediately to the charitable needs of the community, planned gifts with split

Outright Gift of Cash or Securities

Planned giving is a technique of including charitable giving in your financial plan. Currently, the federal and state governments encourage philanthropy by providing advantageous tax treatments for gifts

Planned giving is a technique of including charitable giving in your financial plan. Currently, the federal and state governments encourage philanthropy by providing advantageous tax treatments for gifts

Major and Planned Gifts Fact Sheets

Comparison of Life Income Gifts Charitable Gift Annuity vs. Charitable Remainder Trust Rescue Rehab Rehome Major and Planned Gifts Fact Sheets Major and Planned Gifts Overview Beneficiary Designations

Comparison of Life Income Gifts Charitable Gift Annuity vs. Charitable Remainder Trust Rescue Rehab Rehome Major and Planned Gifts Fact Sheets Major and Planned Gifts Overview Beneficiary Designations

Next Plateau Consulting LLC December, 2008

Next Plateau Consulting LLC Frank Washelesky 455 N. Cityfront Plaza Dr. NBC Tower - Suite 2600 Chicago, IL 60611-5379 312-670-0500 fwashelesky@next-plateau.com www.next-plateau.com Charitable Giving Page

Next Plateau Consulting LLC Frank Washelesky 455 N. Cityfront Plaza Dr. NBC Tower - Suite 2600 Chicago, IL 60611-5379 312-670-0500 fwashelesky@next-plateau.com www.next-plateau.com Charitable Giving Page

OESF and Other Tax Advantages

Philanthropic Estate Planning Guide Oral and Maxillofacial Surgery Foundation 9700 W. Bryn Mawr Avenue Rosemont, IL 60018 Phone: 866-278-9221 Fax: 847-678-6254 E-Mail: info@omsfoundation.org Web site:

Philanthropic Estate Planning Guide Oral and Maxillofacial Surgery Foundation 9700 W. Bryn Mawr Avenue Rosemont, IL 60018 Phone: 866-278-9221 Fax: 847-678-6254 E-Mail: info@omsfoundation.org Web site:

Development Policies and Procedures. Fundraising Policies and Procedures

Development Policies and Procedures Purpose: The purpose of this policy is to: Establish procedures for all fundraising on behalf of Habitat for Humanity of Greater Baton Rouge(HFHGBR) Establish guidelines

Development Policies and Procedures Purpose: The purpose of this policy is to: Establish procedures for all fundraising on behalf of Habitat for Humanity of Greater Baton Rouge(HFHGBR) Establish guidelines

Gifts to the Foundation or Endowed Gifts Help ensure that the residents of St. Mary s Home will continue

Gifts to the Foundation or Endowed Gifts Help ensure that the residents of will continue to receive the comprehensive care they need, long into the future. Your gift to either Foundation or an endowed

Gifts to the Foundation or Endowed Gifts Help ensure that the residents of will continue to receive the comprehensive care they need, long into the future. Your gift to either Foundation or an endowed

Sample Bequest Language

Contents Introduction... Page 2 Alternative Bequests... Page 2 Bequest to an Existing Fund... Page 3 Unrestricted Bequest... Page 4 Bequest to Create an Area of Interest Discretionary Fund... Page 5 Bequest

Contents Introduction... Page 2 Alternative Bequests... Page 2 Bequest to an Existing Fund... Page 3 Unrestricted Bequest... Page 4 Bequest to Create an Area of Interest Discretionary Fund... Page 5 Bequest

OFFICIAL POLICY. Policy Statement

OFFICIAL POLICY 4.2 Gift Acceptance Policy 1/19/16 Policy Statement The College of Charleston encourages the solicitation and acceptance of philanthropic contributions to advance and fulfill the mission

OFFICIAL POLICY 4.2 Gift Acceptance Policy 1/19/16 Policy Statement The College of Charleston encourages the solicitation and acceptance of philanthropic contributions to advance and fulfill the mission

This policy applies to all departments and individuals involved in the Campaign for Carleton.

Policy Name: Originating/Responsible Department: Approval Authority: Date of Original Policy: Last Updated: March 2010 Campaign Policy University Advancement Senior Management Committee Mandatory Revision

Policy Name: Originating/Responsible Department: Approval Authority: Date of Original Policy: Last Updated: March 2010 Campaign Policy University Advancement Senior Management Committee Mandatory Revision

Making a Gift of Real Estate

Making a Gift of Real Estate Thinking of selling your home, commercial building, or investment property? Enjoy tax benefits, generate income, and help Stanford with a gift of real estate. Making a Gift

Making a Gift of Real Estate Thinking of selling your home, commercial building, or investment property? Enjoy tax benefits, generate income, and help Stanford with a gift of real estate. Making a Gift

Charitable Giving. 2012 Page 1 of 7, see disclaimer on final page

Charitable Giving 2012 Page 1 of 7, see disclaimer on final page By leaving money to charity when you die, the full amount of your charitable gift may be deducted from the value of your taxable estate.

Charitable Giving 2012 Page 1 of 7, see disclaimer on final page By leaving money to charity when you die, the full amount of your charitable gift may be deducted from the value of your taxable estate.

Bridgepoint Health Foundation

POLICY: Gifts to the Foundation must align with the Mission, Vision, Values and priorities of the Foundation and the Hospital. The Foundation reserves the right to decline a gift that does not meet these

POLICY: Gifts to the Foundation must align with the Mission, Vision, Values and priorities of the Foundation and the Hospital. The Foundation reserves the right to decline a gift that does not meet these

EXHIBIT A to Campaign Reporting Standards Policy 09.130

EXHIBIT A to Campaign Reporting Standards Policy 09.130 UNCW Campaign Counting and Crediting Guidelines The following policies concerning the valuation of gifts closely follow the CASE Campaign Standards.

EXHIBIT A to Campaign Reporting Standards Policy 09.130 UNCW Campaign Counting and Crediting Guidelines The following policies concerning the valuation of gifts closely follow the CASE Campaign Standards.

c. Restricted Gifts for Existing Activities. A gift, other than an in-kind gift, may be restricted to an existing activity, purpose, or mission of

The mission of is to share the love and grace of Jesus Christ with all people and to invite them to fullness of faith in God. 1. Purpose of the Policy a. To create and sustain positive donor relationships

The mission of is to share the love and grace of Jesus Christ with all people and to invite them to fullness of faith in God. 1. Purpose of the Policy a. To create and sustain positive donor relationships

Overview of the Philanthropic Impact of the American Taxpayer Relief Act of 2012

January 3, 2013 Overview of the Philanthropic Impact of the American Taxpayer Relief Act of 2012 A WHITE PAPER by Robert Sharpe Overview of the Philanthropic Impact of the American Taxpayer Relief Act

January 3, 2013 Overview of the Philanthropic Impact of the American Taxpayer Relief Act of 2012 A WHITE PAPER by Robert Sharpe Overview of the Philanthropic Impact of the American Taxpayer Relief Act

Gift planning newsletter from Cornell University Spring 2014 Plan for Cornell. And be counted.

Financial Planner Gift planning newsletter from Cornell University Spring 2014 Plan for Cornell. And be counted. Cornell has played a vital part in shaping your life. Now, as we approach Cornell s Sesquicentennial

Financial Planner Gift planning newsletter from Cornell University Spring 2014 Plan for Cornell. And be counted. Cornell has played a vital part in shaping your life. Now, as we approach Cornell s Sesquicentennial

GIFT REPORTING STANDARDS UA PPS No. 01.03 Issue No. 1 Effective Date: 1/1/2008 Review: 1/1/E3Y 01. PRINCIPLES OF GIFT REPORTING. 01.01.

GIFT REPORTING STANDARDS UA PPS No. 01.03 Issue No. 1 Effective Date: 1/1/2008 Review: 1/1/E3Y 01. PRINCIPLES OF GIFT REPORTING 01.01. Types of Gifts Gifts to Texas State University-San Marcos (Texas State)

GIFT REPORTING STANDARDS UA PPS No. 01.03 Issue No. 1 Effective Date: 1/1/2008 Review: 1/1/E3Y 01. PRINCIPLES OF GIFT REPORTING 01.01. Types of Gifts Gifts to Texas State University-San Marcos (Texas State)

SAMPLE GIFT ACCEPTANCE POLICIES

SAMPLE GIFT ACCEPTANCE POLICIES ABC Charity, a nonprofit organization headquartered in City, State, encourages the solicitation and acceptance of gifts to ABC Charity (hereinafter referred to as ABC) for

SAMPLE GIFT ACCEPTANCE POLICIES ABC Charity, a nonprofit organization headquartered in City, State, encourages the solicitation and acceptance of gifts to ABC Charity (hereinafter referred to as ABC) for

Roth the Traditional IRA or Give it to Charity? 1 By: Lester B. Law, Mitchell Drossman and Richard S. Franklin, Esq.

Roth the Traditional IRA or Give it to Charity? 1 By: Lester B. Law, Mitchell Drossman and Richard S. Franklin, Esq. Lester B. Law is a Senior Vice President in the National Wealth Strategies Planning

Roth the Traditional IRA or Give it to Charity? 1 By: Lester B. Law, Mitchell Drossman and Richard S. Franklin, Esq. Lester B. Law is a Senior Vice President in the National Wealth Strategies Planning

Ridgefield Library Gift Acceptance Policy

Ridgefield Library Purpose The purpose of this ( this Policy ) is to give guidance and counsel to those individuals within the Ridgefield Library ( the Library ) concerned with the planning, promotion,

Ridgefield Library Purpose The purpose of this ( this Policy ) is to give guidance and counsel to those individuals within the Ridgefield Library ( the Library ) concerned with the planning, promotion,

PLANNED GIVING. A White Paper By DYAUS WEALTH MANAGEMENT

PLANNED GIVING A White Paper By DYAUS WEALTH MANAGEMENT PREPARED BY: DYAUS WEALTH MANAGEMENT LLC 25 WEST 43 RD STREET, NEW YORK, SUITE 1511, NY 10036 WWW.DYAUS.COM Securities and Investment Advisory Services

PLANNED GIVING A White Paper By DYAUS WEALTH MANAGEMENT PREPARED BY: DYAUS WEALTH MANAGEMENT LLC 25 WEST 43 RD STREET, NEW YORK, SUITE 1511, NY 10036 WWW.DYAUS.COM Securities and Investment Advisory Services

A Guide to GIFT PLANNING

A Guide to GIFT PLANNING A A Guide to Gift Planning What is gift planning? The integration of personal, financial, and estate planning goals with a lifetime or testamentary charitable giving An opportunity

A Guide to GIFT PLANNING A A Guide to Gift Planning What is gift planning? The integration of personal, financial, and estate planning goals with a lifetime or testamentary charitable giving An opportunity

SAMPLE FUND DEVELOPMENT POLICIES MANUAL

TABLE OF CONTENTS Organizational Mission Page Number I. Introduction A. Fund development polices B. Authoritative committee C. Overview of document format II. III. IV. Policies to be included Policy components

TABLE OF CONTENTS Organizational Mission Page Number I. Introduction A. Fund development polices B. Authoritative committee C. Overview of document format II. III. IV. Policies to be included Policy components

Gift Acceptance and Administration Policy LIGHTHOUSE OF PINELLAS FOUNDATION, INC.

LIGHTHOUSE OF PINELLAS FOUNDATION, INC. Contents I. INTRODUCTION... 2 A. Mission... 2 B. Purpose of... 2 C. Administrative Responsibility... 2 D. Ethical Standards... 2 1. NCPG and AFP Guidelines... 2

LIGHTHOUSE OF PINELLAS FOUNDATION, INC. Contents I. INTRODUCTION... 2 A. Mission... 2 B. Purpose of... 2 C. Administrative Responsibility... 2 D. Ethical Standards... 2 1. NCPG and AFP Guidelines... 2

Charitable Gift Annuity (CGA)

") Charitable Gift Annuity (CGA) High income and high net worth clients by nature seem to be more giving people than the general public (mainly because they have the extra money to give). There are many different

Charitable Gift Annuity (CGA) High income and high net worth clients by nature seem to be more giving people than the general public (mainly because they have the extra money to give). There are many different

COMMUNITY FOUNDATION OF ANNE ARUNDEL COUNTY GIFT AND FUND ACCEPTANCE POLICY

About This Policy COMMUNITY FOUNDATION OF ANNE ARUNDEL COUNTY GIFT AND FUND ACCEPTANCE POLICY The purpose of this policy is to establish criteria for accepting gifts to Community Foundation of Anne Arundel

About This Policy COMMUNITY FOUNDATION OF ANNE ARUNDEL COUNTY GIFT AND FUND ACCEPTANCE POLICY The purpose of this policy is to establish criteria for accepting gifts to Community Foundation of Anne Arundel

Gift Acceptance and Administration Policy

(INSERT NAME OF ORGANIZATION HERE) Page 1 of 16 Table of Contents I. INTRODUCTION...3 a. Mission...3 b. Purpose of...3 c. Administrative Responsibility...3 d. Ethical Standards...3 i. NCPG and AFP Guidelines...3

(INSERT NAME OF ORGANIZATION HERE) Page 1 of 16 Table of Contents I. INTRODUCTION...3 a. Mission...3 b. Purpose of...3 c. Administrative Responsibility...3 d. Ethical Standards...3 i. NCPG and AFP Guidelines...3

Fundraising Policies Suite Special Olympics Ontario

Fundraising Policies Suite Special Olympics Ontario SOO Fundraising Policies Suite Page 1 Table of Contents Introduction... 1 Ethical Fundraising... 1 Fundraising Solicitations... 1 Treatment of Donors

Fundraising Policies Suite Special Olympics Ontario SOO Fundraising Policies Suite Page 1 Table of Contents Introduction... 1 Ethical Fundraising... 1 Fundraising Solicitations... 1 Treatment of Donors

Join the Founders Society

Join the Founders Society When you include the Alzheimer s Association in your long-term financial plans, you have the opportunity to become a member of the Founders Society, which recognizes those who

Join the Founders Society When you include the Alzheimer s Association in your long-term financial plans, you have the opportunity to become a member of the Founders Society, which recognizes those who

Donor-Advised Fund. Policies and Guidelines

Donor-Advised Fund Policies and Guidelines New Jersey Health Charitable Gift Fund 120 Albany Street Tower II, Suite 850 New Brunswick, NJ 08901 (908) 315-5870 Introduction Thank you for your interest in

Donor-Advised Fund Policies and Guidelines New Jersey Health Charitable Gift Fund 120 Albany Street Tower II, Suite 850 New Brunswick, NJ 08901 (908) 315-5870 Introduction Thank you for your interest in

Life Insurance: Lone Ranger or Black Bart?

Life Insurance: Lone Ranger or Black Bart? Bryan Clontz, CFP President, Charitable Solutions, LLC bryan@charitablesolutionsllc.com (404) 375-5496 Agenda Life Insurance Defined Key Tax and Appraisal Points

Life Insurance: Lone Ranger or Black Bart? Bryan Clontz, CFP President, Charitable Solutions, LLC bryan@charitablesolutionsllc.com (404) 375-5496 Agenda Life Insurance Defined Key Tax and Appraisal Points

National Conference on Philanthropic Planning

National Conference on Philanthropic Planning October 4-6, 2011 San Antonio, Texas Conference Presentation Paper Partnership for Philanthropic Planning 2011. All rights reserved. The Model Standards after

National Conference on Philanthropic Planning October 4-6, 2011 San Antonio, Texas Conference Presentation Paper Partnership for Philanthropic Planning 2011. All rights reserved. The Model Standards after

worked for the Child Respite Care Center, Westside Early Childhood Foundation. Greg comes to us with 16 years of professional working experience

E-Newsletter Foundation News 2nd Round CLASS- ROOM GRANTS The CB Community Education Foundation is proud to announce the award of a Special 2nd Round of Classroom Grant Awards totaling $44,250.00. This

E-Newsletter Foundation News 2nd Round CLASS- ROOM GRANTS The CB Community Education Foundation is proud to announce the award of a Special 2nd Round of Classroom Grant Awards totaling $44,250.00. This

Planned giving: Creative solutions to estate taxation issues

Planned giving: Creative solutions to estate taxation issues By DEWAYNE OSBORN, CGA, CFP, and LARRY FROSTIAK, CA, CFP, TEP Introduction Summary of facts Structural solution to address the testators wishes

Planned giving: Creative solutions to estate taxation issues By DEWAYNE OSBORN, CGA, CFP, and LARRY FROSTIAK, CA, CFP, TEP Introduction Summary of facts Structural solution to address the testators wishes

IN CALIFORNIA THROUGH YOUR ESTATE PLAN

CHARITABLE GIFTING IN CALIFORNIA THROUGH YOUR ESTATE PLAN If charitable giving is important to you then you should include a gifting strategy in your estate plan that will allow you to maximize your donations

CHARITABLE GIFTING IN CALIFORNIA THROUGH YOUR ESTATE PLAN If charitable giving is important to you then you should include a gifting strategy in your estate plan that will allow you to maximize your donations

Congregational Endowment Guide

Congregational Endowment Guide A helpful resource for your planned giving program Brought to you by Thrivent Financial for Lutherans and the Lutheran Community Foundation Thrivent.com Contents Committing

Congregational Endowment Guide A helpful resource for your planned giving program Brought to you by Thrivent Financial for Lutherans and the Lutheran Community Foundation Thrivent.com Contents Committing

Make a Gift to National Stroke Association

Make a Gift to National Stroke Association Your gift today can help further National Stroke Association s mission to reduce the incidence and impact of stroke. If you are in interested in making a charitable

Make a Gift to National Stroke Association Your gift today can help further National Stroke Association s mission to reduce the incidence and impact of stroke. If you are in interested in making a charitable

Fundraising and Sponsorship Policy MUSEUM STRATHROY-CARADOC

Fundraising and Sponsorship Policy MUSEUM STRATHROY-CARADOC 1. INTRODUCTION As a non-profit organization, Museum Strathroy-Caradoc is always actively looking for ways to fundraise and gain sponsorship.

Fundraising and Sponsorship Policy MUSEUM STRATHROY-CARADOC 1. INTRODUCTION As a non-profit organization, Museum Strathroy-Caradoc is always actively looking for ways to fundraise and gain sponsorship.

GIFT ACCEPTANCE POLICY

GIFT ACCEPTANCE POLICY Revision Approved: April 2014, President s Cabinet Related Policies: Smith College Endowment Investment Policy Statement (approved October 2009) Named Endowed Fund Gift Levels (approved

GIFT ACCEPTANCE POLICY Revision Approved: April 2014, President s Cabinet Related Policies: Smith College Endowment Investment Policy Statement (approved October 2009) Named Endowed Fund Gift Levels (approved

GIVING WITH THE SEATTLE FOUNDATION

To submit this form electronically, click the submit button. You will need to come into The Seattle Foundation office to sign the form. Alternately, you can print out the form by clicking the print Giving

To submit this form electronically, click the submit button. You will need to come into The Seattle Foundation office to sign the form. Alternately, you can print out the form by clicking the print Giving

Counting and Reporting Policy for the Comprehensive Campaign July 1, 2012 through June 30, 2017

Counting and Reporting Policy for the Comprehensive Campaign July 1, 2012 through June 30, 2017 Table of Contents: Overview 4 Purpose 4 Counting and Reporting Methodology 5 Outright Gifts 6 Assignments

Counting and Reporting Policy for the Comprehensive Campaign July 1, 2012 through June 30, 2017 Table of Contents: Overview 4 Purpose 4 Counting and Reporting Methodology 5 Outright Gifts 6 Assignments

Large or small, whatever the size of your estate, it is important to plan. If you do not

Starting to Plan Your Estate Large or small, whatever the size of your estate, it is important to plan. If you do not have a will, a court will select your heirs and distribute your property as prescribed

Starting to Plan Your Estate Large or small, whatever the size of your estate, it is important to plan. If you do not have a will, a court will select your heirs and distribute your property as prescribed

THE CAMPAIGN FOR UT CAMPAIGN COUNTING GUIDELINES

THE CAMPAIGN FOR UT CAMPAIGN COUNTING GUIDELINES 1) CURRENT GIFTS & MATCHING GIFTS 2 2) PLEDGES 3 3) PLANNED GIFTS 4 a) BEQUEST EXPECTANCIES 4 b) IRREVOCABLE LIFE INCOME (SPLIT INTEREST) GIFTS 5 c) CHARITABLE

THE CAMPAIGN FOR UT CAMPAIGN COUNTING GUIDELINES 1) CURRENT GIFTS & MATCHING GIFTS 2 2) PLEDGES 3 3) PLANNED GIFTS 4 a) BEQUEST EXPECTANCIES 4 b) IRREVOCABLE LIFE INCOME (SPLIT INTEREST) GIFTS 5 c) CHARITABLE

The joy of charitable giving: Strategies and opportunities

The joy of charitable giving: Strategies and opportunities Vanguard research September 2013 Executive summary. The tax benefits available through various charitable giving strategies can play a critical

The joy of charitable giving: Strategies and opportunities Vanguard research September 2013 Executive summary. The tax benefits available through various charitable giving strategies can play a critical

Gift planning newsletter from Cornell University Fall 2014 Meeting Year-End Financial Goals

Financial Planner Gift planning newsletter from Cornell University Fall 2014 Meeting Year-End Financial Goals When Winston Churchill said, It is a riddle wrapped in a mystery inside an enigma, he wasn

Financial Planner Gift planning newsletter from Cornell University Fall 2014 Meeting Year-End Financial Goals When Winston Churchill said, It is a riddle wrapped in a mystery inside an enigma, he wasn

Giving Today to Guarantee Tomorrow: Charitable Gifts of Life Insurance

Giving Today to Guarantee Tomorrow: Charitable Gifts of Life Insurance A gift of life insurance can represent a substantial future gift to a favorite charity at relatively little cost to you. Table of

Giving Today to Guarantee Tomorrow: Charitable Gifts of Life Insurance A gift of life insurance can represent a substantial future gift to a favorite charity at relatively little cost to you. Table of

Estate Planning and Planned Giving

Estate Planning and Planned Giving Presented By Richard S. Niedermayer and John Tompkins Agenda Estate planning Why have a will? New Wills Act amendments Taxation on death Charitable bequests Charitable

Estate Planning and Planned Giving Presented By Richard S. Niedermayer and John Tompkins Agenda Estate planning Why have a will? New Wills Act amendments Taxation on death Charitable bequests Charitable

Giving Reference Guide

Giving Reference Guide Changing Lives and Building Healthy Communities Through Planned Giving Thank you for considering Lancaster General Health in your charitable giving plans. As a leading healthcare

Giving Reference Guide Changing Lives and Building Healthy Communities Through Planned Giving Thank you for considering Lancaster General Health in your charitable giving plans. As a leading healthcare

BROOKINGS PARTNERS. TogEThER, WE ShaPE ThE FuTuRE. Dr. Paula Clayton Enriching the Residency Experience RECOGNIZING THE IMPORTANCE OF PLANNED GIFTS

BROOKINGS PARTNERS RECOGNIZING THE IMPORTANCE OF PLANNED GIFTS SUMMER 2013 TogEThER, WE ShaPE ThE FuTuRE Dr. Paula Clayton Enriching the Residency Experience Passion. A Gift for Scientific Discovery &

BROOKINGS PARTNERS RECOGNIZING THE IMPORTANCE OF PLANNED GIFTS SUMMER 2013 TogEThER, WE ShaPE ThE FuTuRE Dr. Paula Clayton Enriching the Residency Experience Passion. A Gift for Scientific Discovery &

Charitable Planned Giving

` Insuring the Future In this Newsletter: Charitable Planned Giving Legislative Changes John Jordan, CFP CERTIFIED FINANCIAL PLANNER Phone: (519) 272-3112 Toll Free: (866) 272-3112 Fax: (519) 662-6414

` Insuring the Future In this Newsletter: Charitable Planned Giving Legislative Changes John Jordan, CFP CERTIFIED FINANCIAL PLANNER Phone: (519) 272-3112 Toll Free: (866) 272-3112 Fax: (519) 662-6414

our stewardship Donor-Advised Funds at The Denver Foundation: a simple, powerful, and highly personal approach to giving.

Your GenerositY our stewardship Donor-Advised Funds at The Denver Foundation: a simple, powerful, and highly personal approach to giving. Donor-advised funds provide a convenient and flexible tool for

Your GenerositY our stewardship Donor-Advised Funds at The Denver Foundation: a simple, powerful, and highly personal approach to giving. Donor-advised funds provide a convenient and flexible tool for

Methods of Giving to the University of Florida

Gift Planning Guide Methods of Giving to the University of Florida 4 Cash 5 Appreciated Securities 6 Retirement Plan Assets 7 Charitable Lead Trust 8 Life Income Gifts 10 Real Estate I am pleased to have

Gift Planning Guide Methods of Giving to the University of Florida 4 Cash 5 Appreciated Securities 6 Retirement Plan Assets 7 Charitable Lead Trust 8 Life Income Gifts 10 Real Estate I am pleased to have

Endowments and Foundations

Endowments and Foundations Trends in Healthcare Philanthropy and the Use of Separate Foundations In the June 5, 2011 edition of The New York Times, a full-page ad framed in violet announced NYU Langone

Endowments and Foundations Trends in Healthcare Philanthropy and the Use of Separate Foundations In the June 5, 2011 edition of The New York Times, a full-page ad framed in violet announced NYU Langone

Tampa Hillsborough Action Plan Gift Acceptance Procedures

Tampa Hillsborough Action Plan Gift Acceptance Procedures Purpose The purpose of these procedures is to implement the Gift Acceptance Policy adopted by the Board of Directors of Tampa Hillsborough Action

Tampa Hillsborough Action Plan Gift Acceptance Procedures Purpose The purpose of these procedures is to implement the Gift Acceptance Policy adopted by the Board of Directors of Tampa Hillsborough Action

Financial Planner. Two Alumnae, Two Ways to Give. Gift planning newsletter from Cornell University Spring 2012. Penny Mills, MBA 82

Financial Planner Gift planning newsletter from Cornell University Spring 2012 Two Alumnae, Two Ways to Give Both Penny Mills and Phyllis Blair have enjoyed influential and groundbreaking careers. Both

Financial Planner Gift planning newsletter from Cornell University Spring 2012 Two Alumnae, Two Ways to Give Both Penny Mills and Phyllis Blair have enjoyed influential and groundbreaking careers. Both

Estate and Gift Tax Planning: 2013 Update

Estate and Gift Tax Planning: 2013 Update Moira S. Laidlaw, Esq. Two Depot Plaza, Suite 203 Bedford Hills, New York 10507 mlaidlaw@laidlawfirm.com Disclaimer This is an overview not a complete statement

Estate and Gift Tax Planning: 2013 Update Moira S. Laidlaw, Esq. Two Depot Plaza, Suite 203 Bedford Hills, New York 10507 mlaidlaw@laidlawfirm.com Disclaimer This is an overview not a complete statement

Maroon LOGO 2. THE campaign for the

THE campaign for the ARCHDIOCESE of philadelphia Planned Giving Guidebook Table of Contents Table of Contents HERITAGE OF In t r o d u c t io n 2 Be q u e s t s 3 Charitable Gift Annuity 4 Charitable

THE campaign for the ARCHDIOCESE of philadelphia Planned Giving Guidebook Table of Contents Table of Contents HERITAGE OF In t r o d u c t io n 2 Be q u e s t s 3 Charitable Gift Annuity 4 Charitable

ENDOWMENT GIVING ESSENTIALS

ENDOWMENT GIVING ESSENTIALS Long Beach, CA 8 November 2014 Don Hill Don Hill Consulting Lynne Hansen United Church Funds Our Mission Our mission Invest responsibly. Strengthen ministry. United Church Funds

ENDOWMENT GIVING ESSENTIALS Long Beach, CA 8 November 2014 Don Hill Don Hill Consulting Lynne Hansen United Church Funds Our Mission Our mission Invest responsibly. Strengthen ministry. United Church Funds

How to Use a Schwab Charitable Donor-Advised Fund

A better way to give. What is Schwab Charitable? A Schwab Charitable donor-advised fund account is a simple, tax-smart investment solution for charitable giving. You can open a Schwab Charitable account

A better way to give. What is Schwab Charitable? A Schwab Charitable donor-advised fund account is a simple, tax-smart investment solution for charitable giving. You can open a Schwab Charitable account

Better Retirement Exit Strategies with Life Insurance

Better Retirement Exit Strategies with Life Insurance Presented by: Joe Chenoweth, CLU, ChFC, AEP Vice President, Estate & Financial Planning* A4TN-1113-05E2 16479 Dallas Parkway, Suite 850 Addison, Texas

Better Retirement Exit Strategies with Life Insurance Presented by: Joe Chenoweth, CLU, ChFC, AEP Vice President, Estate & Financial Planning* A4TN-1113-05E2 16479 Dallas Parkway, Suite 850 Addison, Texas

The Wood s Homes Foundation. Financial Statements December 31, 2014

Financial Statements April 22, 2015 Independent Auditor s Report To the Board of Directors of Wood s Homes Foundation We have audited the accompanying financial statements of Wood s Homes Foundation, which

Financial Statements April 22, 2015 Independent Auditor s Report To the Board of Directors of Wood s Homes Foundation We have audited the accompanying financial statements of Wood s Homes Foundation, which

Gift acceptance policy

Gift acceptance policy Gift Acceptance Policy Introduction The LSU Foundation is a private, not-for-profit entity organized under the laws of the State of Louisiana (hereinafter referred to as the Foundation

Gift acceptance policy Gift Acceptance Policy Introduction The LSU Foundation is a private, not-for-profit entity organized under the laws of the State of Louisiana (hereinafter referred to as the Foundation

I DON T KNOW ANYTHING ABOUT YOU, BUT Introducing Planned Gifts into Most All Conversations. By Pentera Webinar presenter Pamela Jones Davidson, J.D.

I DON T KNOW ANYTHING ABOUT YOU, BUT Introducing Planned Gifts into Most All Conversations By Pentera Webinar presenter Pamela Jones Davidson, J.D. I DON T KNOW ANYTHING ABOUT YOU, BUT Introducing Planned

I DON T KNOW ANYTHING ABOUT YOU, BUT Introducing Planned Gifts into Most All Conversations By Pentera Webinar presenter Pamela Jones Davidson, J.D. I DON T KNOW ANYTHING ABOUT YOU, BUT Introducing Planned

A Lasting Legacy: Three Generations, Three Scholarships, Three-Part Giving

Summer 2008 Issue 29 A Lasting Legacy: Three Generations, Three Scholarships, Three-Part Giving Andrew Scala 11, John Scala 80, Bob Scala 56M (MS), 58M (PhD), and Janet Scala 55N We feel very strongly

Summer 2008 Issue 29 A Lasting Legacy: Three Generations, Three Scholarships, Three-Part Giving Andrew Scala 11, John Scala 80, Bob Scala 56M (MS), 58M (PhD), and Janet Scala 55N We feel very strongly

Direct Marketing & Planned Giving: The Reese s Peanut Butter Cup of Fundraising

Direct Marketing & Planned Giving: The Reese s Peanut Butter Cup of Fundraising Meg Roberts, CFRE, Impact Communications Mohammad Zaidi, ACLU Foundation Bruce Makous, ChFC, CAP, CFRE, ACLU of Pennsylvania

Direct Marketing & Planned Giving: The Reese s Peanut Butter Cup of Fundraising Meg Roberts, CFRE, Impact Communications Mohammad Zaidi, ACLU Foundation Bruce Makous, ChFC, CAP, CFRE, ACLU of Pennsylvania

PARISH BULLETIN INSERTS

PARISH BULLETIN INSERTS The goal of this parish bulletin calendar (below) is NOT for parishes to use them every week. We understand parishes do not always have space. Should your parish wish to include

PARISH BULLETIN INSERTS The goal of this parish bulletin calendar (below) is NOT for parishes to use them every week. We understand parishes do not always have space. Should your parish wish to include