Florida International University

|

|

|

- Clifton Carter

- 9 years ago

- Views:

Transcription

1 Florida International University Finance Managers Meeting September 24,

2 Finance Managers Meeting Agenda AGENDA Budget Update Kenneth Jessell Activity Number & Department Hamza Lazrak & Ana Pineda Maintenance eform Affordable Care Act (PPACA) Carlos Flores Introduction: New Director of Purchasing Cecilia Hamilton Unrelated Business Income Tax Edgardo Salazar New Agency Policy & Accounting Topics Desiree Elias Business Services Update Jeff Krablin Tip of the Day Hamza Lazrak 2

3 Florida International University Budget Update September 24,

4 University Operating Budget FY FY Operating Budget of $1.2B Concessions, $0.7M, 0% DSO's, $38.6M, 3% Student Fees, $49.5M, 4% Other, $(7.0M), -1% E&G State Appropriations, $183.1M, 15% Contracts and Grants, $101.1M, 9% Auxiliary Enterprises, $171.6M, 14% E&G Tuition, $195.5M, 16% E&G Reserves, $4.0M, 0% E&G - College of Medicine, $42.7M, 4% Student Loans, $261.0M, 22% Student Financial Aid, $147.2M, 12% Other includes Self-Insurance Program, Principal Payment of Debt and Interfund Adjustments 4

5 Educational & General Operating Budget FY $ millions State Appropriations Base Budget 142 Restoration of FIU Share of $300M cut 24 Legislative Adjustments / Budget Passthroughs 8 PO&M and Legislative Specials Total State Appropriations E&G Tuition Budget 192 Incremental Tuition E&G Tuition Budget 196 TOTAL E&G REVENUES 379 E&G Base Expenditure Budget (363) PO&M, Legislative Specials & Passthroughs (17) 10-year Plan Investments Continuation (1) Additional need-based financial aid and advisors (2) TOTAL E&G EXPENDITURES (383) E&G ESTIMATED SHORTFALL (4) 5

10-year Plan Investments Continuation (1) Additional need-based financial aid and advisors (2) TOTAL E&G EXPENDITURES (383) E&G")

6 Educational & General Funding Gap University Carry Forward funds will be used to cover the E&G estimated shortfall $ millions FY Beginning Balance 83 Historical Carry Forward Expenditures in FY (47) Carry Forward FY Funds 13 FY Beginning Balance 49 E&G Funding GAP (4) Legislative Earmarked Funds (6) Capital Campaign Investment (3) Health Services Compliance (1) College and Area Commitments (12) FY Commitments: (26) Actions to address future budget shortfalls FIU will continue to monitor overall state budget Suspend Strategic Plan enrollment growth of 2,000 students per year Hire only strategic, mission critical positions Reduce operating expenditures while protecting STEM and other critical programs, anticipate 2% budget reduction FY Estimated Available Balance 23 Minimum Statutory Reserve 20 6

7 State Appropriations vs. Tuition Revenue $250 24,412 24,412 24,511 25,380 27,815 28,566 29,237 29,604 35,000 $ Millions $200 $150 $100 $229 $218 $106 $106 $203 $116 $179 $129 $182 $155 $174 $191 $166 $144 $195 $180 30,000 25,000 20,000 15,000 FTE 10,000 $50 5,000 $0 FY Before Budget Reductions FY FY FY FY FY FY FY Budget - Enrollment, FTE State Appropriations Tuition State Appropriations include General Revenue and Lottery, but exclude Financial Aid, and Risk Management ($3M), and College of Medicine 7

8 Auxiliary Enterprises FY FY revenue increase driven by academic auxiliaries, new student residence, Parkview Hall, and student health fee increase of $10.50 per semester 200 Revenue Growth $ 188 $ 195 $ $ 129 $ 145 $58 $63 $63 $ millions $49 $11 $22 $46 $50 $12 $26 $57 $13 $25 $76 $14 $14 $26 $29 $85 $89 0 FY Actuals FY Actuals FY Actuals FY Actuals FY Budget Academic Auxiliaries Housing Parking and Transportation Food service, retail operations, student health Actuals adjusted to remove DSO reimbursement revenue now reported under Contracts and Grants 8

9 Student Financial Aid FY % of total budget, comprising funding from student financial aid fees, support from federal and state financial aid awards, institutional programs, as well as numerous private scholarships Anticipate approximately 55% of students receiving financial aid will be Pell Grant recipients Challenges Substantial component of affordability of higher education to the student Stricter eligibility requirements for student financial aid will result in significant reduction in number of FIU students eligible for financial aid Implement initiatives to allow students to graduate faster Leverage existing programs to maximize available funds and raise money from private donors 9

10 Contracts and Grants FY % of total budget, comprising funding from different sources, including federal, state and local governmental agencies and private organizations, to support research, public service and training Challenges Impact of sequestration on ability to obtain new, federal research grants Focus on commercialization of FIU-related research Identification of cluster hiring opportunities Retain and recruit a world-class faculty 10

11 Fixed Capital Outlay Will receive $19M in FY but funding for future years is unclear PUBLIC EDUCATION CAPITAL OUTLAY (PECO) Utilities / Infrastructure / Capital Renewal/ Roofs (P,C,E) $0 Student Academic Support Center (MMC) $5,678,129 Minor Building Repair and Maintenance $3,603,832 TOTAL $9,281,961 CAPITAL IMPROVEMENT TRUST FUND PROJECTS (CITF) Recreation Center Expansion (MMC) $8,595,233 Wolf University Center Improvements (BBC) $1,108,352 TOTAL $9,703,585 11

Recreation Center Expansion (MMC) $8,595,233 Wolf University Center Improvements (BBC) $1,108,352 TOTAL")

12 What does the future hold? Economy showing signs of recovery nationwide and in Florida National unemployment down from 8.1% to 7.3% year over year as of August State general revenue estimates for FY and FY continue to reflect upward trend Additional demands on state revenue associated with health care / Medicaid Election year politics But Higher Education funding model has changed State no longer providing funding for enrollment growth since 2007 Moving toward performance based funding Little appetite for tuition and fee increases Stricter eligibility requirements for student financial aid Limited Public Education Capital Outlay (PECO) funding for capital projects Universities need to do more and better with less state funding Governing body emphasizing quality education at an affordable price Increased reliance on enrollment growth and new revenue sources 12

funding for capital projects Universities need to do")

13 Florida International University Activity Number & Department Maintenance Request eform September 24,

14 Activity Number & Department Maintenance Request eform 14

15 Create New Department 15

16 New Activity Number Request Link of List of CIP 16

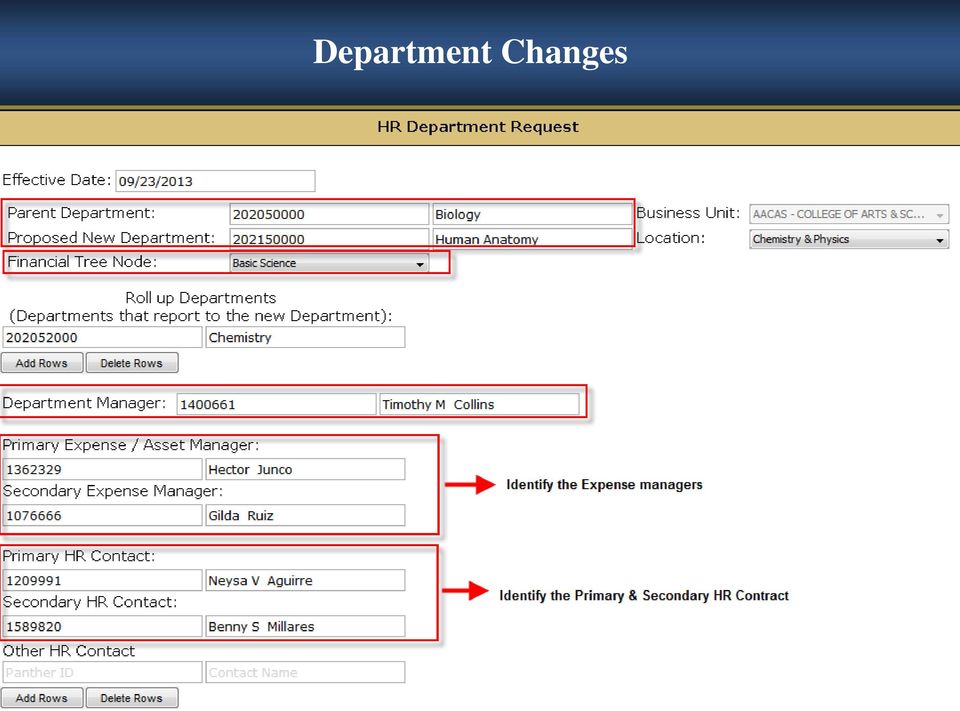

17 Department Changes 17

18 Activity Number & Department Maintenance eform The form will be located through the controller s office website or for your convenience, it will also be available within Panthersoft HR 18

19 Florida International University Patient Protection Affordable Care Act (PPACA) September 24,

")

20 PPACA Legislative Update Division of State Group Insurance (DSGI) Senate Bill 1802 was signed into Florida Law which provides that an OPS Temporary employee meeting certain criteria (working an average 30 hours or more) is eligible to participate in the state group health insurance program, etc. DSGI provided guidance to state agencies and universities to continue our efforts toward and stay on course for a January 1, 2014 implementation. 20

21 PPACA HR Update Division of Human Resources (DHR) DHR is continuing with the action plan for 2014 implementation. Recruitment Services continues to work with Department Heads to clean-up the temporary employee data. A Temporary Appointment Policy has been developed and is being reviewed to address the proper procedures for hiring and use of temporary workforce. 21

22 Fringe Benefit Pool Fiscal Year Fringe Benefit pool will absorb the additional cost of providing health insurance for temporary employees working more than 30 hours per week Fiscal Year Health benefits will be factored into the temporary employee fringe rate 22

23 Florida International University Introduction: New Director of Purchasing September 24,

24 Florida International University Unrelated Business Income Tax (UBIT) September 24,

25 FIU s Income Tax Exemption Often asked question? Isn t Florida International University (FIU) exempt from income tax? The answer is that it depends. Federal Income Tax Exemption: Generally, FIU is exempt from federal income tax for those activities which are related to the University s exempt purpose (such as education, research, and public service). The Internal Revenue Code provides that the exempt purposes of state universities include all purposes and functions described in IRC 501(c)(3): charitable, scientific, testing for public safety, literary, educational, to foster national or international amateur sports competition, or for the prevention of cruelty to children or animals. 25

26 What is UBIT? However, FIU is not exempt from income tax on activities which are unrelated to the exempt purpose. What is UBIT? Unrelated Business Income Tax (UBIT) is federal income tax imposed on non-profit organizations, including state colleges and universities, for conducting activities that are not related to the exempt purpose of the organization. Similar to for profit companies, which pay taxes on their profits, the IRS requires FIU to pay taxes on the net income that it earns on unrelated business income (UBI). 26

27 Income tax return (990-T) FIU is not prohibited from engaging in activities which generate UBI, but the IRS requires that FIU report the net operating results from these activities. Activities that are determined to produce UBI will be included on FIU s Exempt Organization Business Income Tax Return (Form 990-T), which is filed with the IRS each year. It is extremely important that all unrelated business activity is reported on the tax return because the IRS can assess costly penalties and interest for underpayment of taxes due to under reporting of income. 27

28 UBIT Defined For an activity to be considered an unrelated trade or business, all three of the following criteria must be satisfied: 1. The activity must be a trade or business; 2. The activity must be regularly carried on; and 3. The activity must not be substantially related to the exempt purpose of the organization If all three requirements are satisfied, then it s subject to UBIT unless the activity meets an exception or exclusion. These terms are given a specific meaning within the rules set forth by the IRS and several important exceptions exist, therefore guidelines for these criteria are available from the Tax Compliance office for your review. 28

29 Trade or Business The term trade or business generally includes any activity carried on for the production of income from the sale of goods or from the performance of services. A trade or business activity is one in which a profit is expected to be made. Do not report revenue from sales to other University departments, UBIT is only applicable to revenue generated from external sources. Do report external revenue even if the activity results in a loss for a particular year. 29

30 Regularly Carried On Business activities are considered regularly carried on if such activities show a frequency and continuity and are pursued in a manner similar to comparable commercial activities of non-exempt organizations. An activity should not be considered regularly carried on if it is on a very infrequent basis; for a short period of time during the year; or without competitive and promotional efforts. However, year round activities are regular even if they are conducted only one day a week. Further, seasonal activities may be regularly carried on even though they are conducted only for a short period each year. 30

31 Not Substantially Related To be considered exempt (non-taxable) income, there must be a substantial relationship between the activity that generates the revenue and the exempt purpose of the organization (i.e., the activity must contribute to the accomplishment of the exempt purpose, apart from the need to produce income). The mere fact that an activity generates funds that are then used for an exempt purposes does not mean that the activity is related to the exempt purposes. In looking at an activity, particular emphasis is placed on the size and extent of the activity. If an activity is conducted on a scale larger than reasonably necessary to carry out the exempt purpose, it is more likely to be treated as unrelated. 31

32 Exceptions to General Rule: An activity that otherwise satisfies the General Rule will not be subject to UBIT, if: Substantially all of the work is performed by a volunteer workforce substantially all (85%) the work is performed without compensation (the IRS construes compensation broadly) provided for the convenience of members (students, faculty, officers, staff) The IRS treats Alumni as part of the general public and not University members selling donated merchandise (thrift store exception) substantially all (85%) of the merchandise has been donated 32

33 Exclusions to General Rule: The following are exclusions from UBIT: Passive investment income is not considered UBI Interest Dividends Annuities Royalties Payments with respect to securities loans, and Any other incomes from routine investments Real property rental income (where no personal services are provided) 513(i) Safe Harbor Qualified Sponsorship Payments A payment of money, property or services where the sponsor has no expectation of receiving any substantial return benefit. The use or acknowledgement of a sponsor s name or logo is exempt. 33

34 College & University Compliance Project In 2008, the IRS sent compliance questionnaires to approximately 400 tax-exempt colleges and universities. After examination of the questionnaire responses, 34 colleges and universities were chosen for audit. The audits resulted in UBI tax ( UBIT ) increases for 90% of the colleges and universities examined; over 180 changes to the amounts of UBIT reported on Forms 990-T (Exempt Organization Business Income Tax Return); and the disallowance of more than $170 million in losses and net operating losses. The major reasons for adjustments to UBI were: a) misclassification of an activity as a trade or business, b) misallocation of expenses, c) errors in computation or substantiation, and d) misclassification of related activities. The release of the report reinforces the continuing trend of increased scrutiny by the IRS upon tax-exempt colleges and universities. 34

35 Contact Information: Each department is responsible for accounting and documenting for unrelated business income. An was sent to all department heads/budget managers on September 9 th with additional UBIT information and links to the UBIT questionnaire, located on the Controller s webpage. Tax Compliance services will be holding a UBIT workshop to answer questions and assist with the questionnaire: Campus Support Complex Room CSC1123 Thursday, September 26 th (9:30 am 11:30am) Contact me at [email protected] or : Edgar Salazar, CPA Associate Controller Tax Compliance Services Office of the Controller CSC 319 T: F: E: [email protected] 35

36 Florida International University New Agency Policy and Accounting Topics September 24,

37 Agency Guidelines Agency Fund: A fund established to record the administration of monies for which the University acts as a fiscal agent on behalf of an outside Principal. Use of these monies primarily benefit the Principal and incidentally benefit the University via its affiliation to the Principal. Agency activities are not operating activities of the University. Agency funds are not considered University monies or charitable contributions to the University; outstanding agency funds are liabilities to the Principal and will be remanded to the Principal at their request or at the completion of the agency activity. Principal: A sponsoring entity outside the University that authorizes the University to act as its agent, subject to the Principal's general control and instructions as expressed through the Sponsor. Sponsor: a University faculty or staff employee authorized by the Principal to act on its behalf and who assumes responsibility for the proper administration and monitoring of the agency fund. The monitoring responsibilities of the Sponsor cannot be delegated. 37

38 Agency Guidelines The following constitute agency activities: Student organizations or clubs sponsored by a separate legal entity (e.g. fraternity or student chapter of national organization). Employee organizations (e.g. unions). Conferences or events offered by an outside professional organization and administered by the University on an ongoing basis, spanning multiple fiscal years or one-time events exceeding $7,500 in annual deposits. The following do not constitute agency activities: Fundraising activities. Revenue-sharing agreements between the university and outside parties. Student deposits for tuition or study abroad educational programs. Deposits wherein the University acts in a capacity of a bank, (e.g. FIU One Card balances due to students and employees). Withholding taxes or other amounts (e.g. sales taxes, insurance). Note that while these activities do not meet the criteria to be established as an agency, the outstanding balances do represent liabilities and should be accounted for as such in the corresponding fund which the activity supports. The exception above is fundraising and study abroad activities, which are auxiliaries and as such have revenues and expenses. 38

39 Agency Guidelines Financial Management and Accounting Principles 1.Disbursements of agency monies are subject to the University s prescribed procurement practices, including applicable competitive solicitation requirements and guidelines for allowable expenditures. 2.The resources of the University will not be used in support of the sponsoring entity without appropriate reimbursement for direct and indirect costs. In those cases where the use of resources of the University is not significant, the Office of Auxiliary & Enterprise Development may waive such reimbursement. 3.Campus service department recharges for goods and services ordered by and rendered to the Principal will be directly charged to the agency activity. 4. Agency monies cannot be used to compensate University employees. 39

40 Agency Guidelines 5. Residual balances for this fund group will be recorded as liabilities in account # Unexpended Agency Funds. Receipts and disbursements of these are accordingly classified as additions to, and deductions from, the liability account rather than as revenues and expenditures which will affect fund balance. The Office of the Controller will request that the Sponsor confirm that the liability balance in the agency activity is due to the Principal on an annual basis. 6. Agency funds must have a positive cash balance at all times. Accounting may enforce this provision by not processing a disbursement that will create or increase an overdraft. 7. The Sponsor will identify an alternative source of funds to cover any possible overdraft of agency funds when requesting creation of the agency activity. 8. No interest will be credited to outstanding agency cash balances. 40

41 Florida International University Business Services Update September 24,

42 Florida International University Reporting Tip September 24,

43 Florida International University Finance Managers Meeting September 24,

JAMISON MANAGEMENT AND DEVELOPMENT HC 68, Box 79-S, Gila Hot Springs, Silver City, New Mexico 575-536-9339 [email protected]

JAMISON MANAGEMENT AND DEVELOPMENT HC 68, Box 79-S, Gila Hot Springs, Silver City, New Mexico 575-536-9339 [email protected] Compiled by Suzanne Jamison for informational purposes only. This does not

JAMISON MANAGEMENT AND DEVELOPMENT HC 68, Box 79-S, Gila Hot Springs, Silver City, New Mexico 575-536-9339 [email protected] Compiled by Suzanne Jamison for informational purposes only. This does not

Form 990 and Tax Update Olivia A. Hutton, CPA

Form 990 and Tax Update Olivia A. Hutton, CPA Certified Public Accountants and Consultants Connecting depth and insight with community values. Your 990 should prove that you are: Organized and operated

Form 990 and Tax Update Olivia A. Hutton, CPA Certified Public Accountants and Consultants Connecting depth and insight with community values. Your 990 should prove that you are: Organized and operated

How To Be A Good Fundraiser

A Legal Checklist for Not-for-Profit Organizations This 10-point checklist is written to help busy charitable organizations stay on top of today s regulatory compliance requirements. For further information,

A Legal Checklist for Not-for-Profit Organizations This 10-point checklist is written to help busy charitable organizations stay on top of today s regulatory compliance requirements. For further information,

PRIVATE FOUNDATION CAUTION: The purposes of this memorandum are to assist you, the directors of your private foundation, and your accountant in:

CHERRY CREEK CORPORATE CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

CHERRY CREEK CORPORATE CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

Unrelated Business Income Robyn Miller, Staff Attorney Pro Bono Partnership of Atlanta Tim Phillips, Senior Counsel, American Cancer Society

Unrelated Business Income Robyn Miller, Staff Attorney Pro Bono Partnership of Atlanta Tim Phillips, Senior Counsel, American Cancer Society September 15, 2010 Mission of Pro Bono Partnership of Atlanta:

Unrelated Business Income Robyn Miller, Staff Attorney Pro Bono Partnership of Atlanta Tim Phillips, Senior Counsel, American Cancer Society September 15, 2010 Mission of Pro Bono Partnership of Atlanta:

A Basic Guide to Corporate Philanthropy

A Basic Guide to Corporate Philanthropy Stephanie L. Petit November 2009 A business has reached a point where it wants to give back. It s had a year better than it expected in this economy, and it knows

A Basic Guide to Corporate Philanthropy Stephanie L. Petit November 2009 A business has reached a point where it wants to give back. It s had a year better than it expected in this economy, and it knows

University of Utah Tax Services & Payroll Accounting Tax Overview

University of Utah Tax Services & Payroll Accounting Tax Overview Presented by: Kelly Peterson, CPA Tax Manager Tax Services website: www.tax.utah.edu Phone: 581-6699 Email: [email protected]

University of Utah Tax Services & Payroll Accounting Tax Overview Presented by: Kelly Peterson, CPA Tax Manager Tax Services website: www.tax.utah.edu Phone: 581-6699 Email: [email protected]

UBIT. Unrelated Business Income Tax. Presented March 27, 2012 by: Dale S. Zuehls CPA JD PhD CGMA CFF ABV ACFE Zuehls, Legaspi & Company

UBIT Unrelated Business Income Tax Presented March 27, 2012 by: Dale S. Zuehls CPA JD PhD CGMA CFF ABV ACFE Zuehls, Legaspi & Company UBI Presentation Major Topics to be Covered Brief History & Overview

UBIT Unrelated Business Income Tax Presented March 27, 2012 by: Dale S. Zuehls CPA JD PhD CGMA CFF ABV ACFE Zuehls, Legaspi & Company UBI Presentation Major Topics to be Covered Brief History & Overview

UBIT TER Sweet Kyle R. ZumBerge Tax Attorney, The University of Texas System

UBIT TER Sweet Kyle R. ZumBerge Tax Attorney, The University of Texas System 2013 Winter Conference February 3 5,2013 Omni Austin Hotel Downtown Austin, Texas 2 UBIT TER Sweet Outline UBIT Background General

UBIT TER Sweet Kyle R. ZumBerge Tax Attorney, The University of Texas System 2013 Winter Conference February 3 5,2013 Omni Austin Hotel Downtown Austin, Texas 2 UBIT TER Sweet Outline UBIT Background General

501 (c)(3) TAX EXEMPTION

(3) TAX EXEMPTION") 501 (c)(3) TAX EXEMPTION 501(c) Tax Exemption What is 501 (c)(3)? Should we be a 501 (c)(3)? How do we get 501 (c)(3) status? Who is eligible under 501(c)(3)? By-Laws Requirements How to Apply Responding

501 (c)(3) TAX EXEMPTION 501(c) Tax Exemption What is 501 (c)(3)? Should we be a 501 (c)(3)? How do we get 501 (c)(3) status? Who is eligible under 501(c)(3)? By-Laws Requirements How to Apply Responding

Transfer Pricing Issues for Tax Exempt Organizations December 5, 2012. Scrutiny on the Rise & Continuing. Scrutiny on the Rise & Continuing 12/5/2012

Transfer Pricing Issues for Tax Exempt Organizations December 5, 2012 Mike Engle Partner Kansas City Office [email protected] Will James Principal St. Louis Office [email protected] Senator Baucus & Senator

Transfer Pricing Issues for Tax Exempt Organizations December 5, 2012 Mike Engle Partner Kansas City Office [email protected] Will James Principal St. Louis Office [email protected] Senator Baucus & Senator

Income Tax Issues Affecting Small Nonprofit Organizations

Income Tax Issues Affecting Small Nonprofit Organizations A free resource provided by the Virginia Society of Certified Public Accountants 2 Income Tax Issues Affecting Small Nonprofit Organizations A

Income Tax Issues Affecting Small Nonprofit Organizations A free resource provided by the Virginia Society of Certified Public Accountants 2 Income Tax Issues Affecting Small Nonprofit Organizations A

SAFE Credit Underwriting Guidelines for Non-Profit Lending. Organization Type: NON-PROFIT ORGANIZATIONS. Bridge Loan Guidelines.

Introduction The Credit Underwriting Guidelines (CUG) manual is designed for use with products delivered to faith-based and non-profit organizations. The guidelines herein govern the granting of credit

Introduction The Credit Underwriting Guidelines (CUG) manual is designed for use with products delivered to faith-based and non-profit organizations. The guidelines herein govern the granting of credit

FORMING AND OPERATING A PRIVATE FOUNDATION

FORMING AND OPERATING A PRIVATE FOUNDATION SIMPSON THACHER & BARTLETT LLP FEBRUARY 7, 2001 TABLE OF CONTENTS Page I. Choosing a private foundation...1 II. Forming a private foundation... 1 A. Choosing

FORMING AND OPERATING A PRIVATE FOUNDATION SIMPSON THACHER & BARTLETT LLP FEBRUARY 7, 2001 TABLE OF CONTENTS Page I. Choosing a private foundation...1 II. Forming a private foundation... 1 A. Choosing

Unrelated Business Income Taxes (UBIT), Weill Cornell Medical College - Qatar

, Weill Cornell Medical College - Qatar") INTERIM Issued: June 4, 2004 CORNELL UNIVERSITY POLICY LIBRARY Unrelated Business Income Taxes (UBIT), Weill Cornell Medical College - Qatar POLICY 3.15.2 Responsible Executive: Dean, POLICY STATEMENT

INTERIM Issued: June 4, 2004 CORNELL UNIVERSITY POLICY LIBRARY Unrelated Business Income Taxes (UBIT), Weill Cornell Medical College - Qatar POLICY 3.15.2 Responsible Executive: Dean, POLICY STATEMENT

Income Tax Issues Affecting Small Nonprofit Organizations

Income Tax Issues Affecting Small Nonprofit Organizations A free resource provided by the Virginia Society of Certified Public Accountants 2 Income Tax Issues Affecting Small Nonprofit Organizations A

Income Tax Issues Affecting Small Nonprofit Organizations A free resource provided by the Virginia Society of Certified Public Accountants 2 Income Tax Issues Affecting Small Nonprofit Organizations A

The University of Georgia Service Center Policy

TABLE OF CONTENTS The University of Georgia Service Center Policy 1. INTRODUCTION... 4 2. SCOPE... 4 2.1. Recharge Activities... 4 2.2. Service Centers... 4 2.3. Specialized Service Centers... 4 3. INTENT....

TABLE OF CONTENTS The University of Georgia Service Center Policy 1. INTRODUCTION... 4 2. SCOPE... 4 2.1. Recharge Activities... 4 2.2. Service Centers... 4 2.3. Specialized Service Centers... 4 3. INTENT....

ALAMO COLLEGES FOUNDATION, INC. (A Texas nonprofit Foundation) AUDITED FINANCIAL STATEMENTS. Year Ended December 31, 2012

AUDITED FINANCIAL STATEMENTS. Year Ended December 31, 2012") R. D. Harrison, CPA Certified Public Accountant Member American Institute of Certified Public Accountants Registered with the Public Company Accounting Oversight Board ALAMO COLLEGES FOUNDATION, INC. AUDITED

R. D. Harrison, CPA Certified Public Accountant Member American Institute of Certified Public Accountants Registered with the Public Company Accounting Oversight Board ALAMO COLLEGES FOUNDATION, INC. AUDITED

NORTH CAROLINA COMMUNITY COLLEGE SYSTEM R. Scott Ralls, Ph.D. President

NORTH CAROLINA COMMUNITY COLLEGE SYSTEM R. Scott Ralls, Ph.D. President 20 May 2014 IMPORTANT INFORMATION MEMORANDUM TO: FROM: RE: Members of the State Board of Community Colleges, Community College Presidents,

NORTH CAROLINA COMMUNITY COLLEGE SYSTEM R. Scott Ralls, Ph.D. President 20 May 2014 IMPORTANT INFORMATION MEMORANDUM TO: FROM: RE: Members of the State Board of Community Colleges, Community College Presidents,

Overview of the Unrelated Business Income Tax

Overview of the Unrelated Business Income Tax Michele A. W. McKinnon Although organizations described in Internal Revenue Code section 501(c)(3) are exempt from federal income tax, certain activities can

Overview of the Unrelated Business Income Tax Michele A. W. McKinnon Although organizations described in Internal Revenue Code section 501(c)(3) are exempt from federal income tax, certain activities can

2015 NEVADA TAX REFORMS. Commerce Tax, Modified Business Tax, Business License Fee

Joshua J. Hicks Attorney at Law 775.622.9450 tel 775.622.9554 fax [email protected] 2015 NEVADA TAX REFORMS Commerce Tax, Modified Business Tax, Business License Fee Current as of June 10, 2015 A. Commerce

Joshua J. Hicks Attorney at Law 775.622.9450 tel 775.622.9554 fax [email protected] 2015 NEVADA TAX REFORMS Commerce Tax, Modified Business Tax, Business License Fee Current as of June 10, 2015 A. Commerce

FISCAL SPONSORSHIP AGREEMENT

FISCAL SPONSORSHIP AGREEMENT This Agreement is made by and between Software Freedom Conservancy ( Conservancy ) and FIXME-CONTRIBUTOR-NAMES (the FIXME-SIGNATORIES ) on behalf of the project known as FIXME-PROJECT-NAME

FISCAL SPONSORSHIP AGREEMENT This Agreement is made by and between Software Freedom Conservancy ( Conservancy ) and FIXME-CONTRIBUTOR-NAMES (the FIXME-SIGNATORIES ) on behalf of the project known as FIXME-PROJECT-NAME

The Legal Essentials of Starting a Nonprofit Organization

The Legal Essentials of Starting a Nonprofit Organization July 2010 Stephen Falla Riff, Esq. Legal Aid Society Community Development Project Copyright 2010 The Legal Aid Society What this Presentation

The Legal Essentials of Starting a Nonprofit Organization July 2010 Stephen Falla Riff, Esq. Legal Aid Society Community Development Project Copyright 2010 The Legal Aid Society What this Presentation

1. The organization mission or most significant activities that you wish to highlight this year:

Form 990 Questionnaire For All Organizations Core Form Heading & Pt I Summary 1. The organization mission or most significant activities that you wish to highlight this year: 2. Total number of volunteers

Form 990 Questionnaire For All Organizations Core Form Heading & Pt I Summary 1. The organization mission or most significant activities that you wish to highlight this year: 2. Total number of volunteers

How to Avoid Ten IRS Land Mines for Nonprofit Charities

How to Avoid Ten IRS Land Mines for Nonprofit Charities The drive to increase revenue leads many nonprofit organizations to start up business activities. Easy profits are expected, but tax traps waiting

How to Avoid Ten IRS Land Mines for Nonprofit Charities The drive to increase revenue leads many nonprofit organizations to start up business activities. Easy profits are expected, but tax traps waiting

BP 3600 RULES FOR AUXILIARY ORGANIZATIONS

BP 3600 RULES FOR AUXILIARY ORGANIZATIONS References: Education Code Sections 72670 et seq.; 76060, 76063, 76064, 72241, 72303 Title 5 Sections 59250 et seq. The Napa Valley Community College District

BP 3600 RULES FOR AUXILIARY ORGANIZATIONS References: Education Code Sections 72670 et seq.; 76060, 76063, 76064, 72241, 72303 Title 5 Sections 59250 et seq. The Napa Valley Community College District

LEGISLATIVE RESEARCH COMMISSION PDF VERSION

CHAPTER 272 PDF p. 1 of 5 CHAPTER 272 (SB 289) AN ACT relating to the Nursing Workforce Foundation. Be it enacted by the General Assembly of the Commonwealth of Kentucky: SECTION 1. A NEW SECTION OF KRS

CHAPTER 272 PDF p. 1 of 5 CHAPTER 272 (SB 289) AN ACT relating to the Nursing Workforce Foundation. Be it enacted by the General Assembly of the Commonwealth of Kentucky: SECTION 1. A NEW SECTION OF KRS

HOUSE BILL 2587 AN ACT

Senate Engrossed House Bill State of Arizona House of Representatives Fifty-second Legislature First Regular Session 2015 HOUSE BILL 2587 AN ACT AMENDING SECTIONS 35-142 AND 35-315, ARIZONA REVISED STATUTES;

Senate Engrossed House Bill State of Arizona House of Representatives Fifty-second Legislature First Regular Session 2015 HOUSE BILL 2587 AN ACT AMENDING SECTIONS 35-142 AND 35-315, ARIZONA REVISED STATUTES;

Guide for Non-profit Organization Financial Administrative Form

Guide for Non-profit Organization Financial Administrative Form This general guidance is provided by the State Education Department (SED) to assist non-profit organizations in completing the Non-profit

Guide for Non-profit Organization Financial Administrative Form This general guidance is provided by the State Education Department (SED) to assist non-profit organizations in completing the Non-profit

Frequently asked Questions

Frequently asked Questions By NONPROFITS About Taxes (2014 Revised Edition) ANSWERS* TO QUESTIONS FREQUENTLY ASKED ABOUT - COMPENSATION & BENEFITS We heard that our pastor is both an employee and an independent

Frequently asked Questions By NONPROFITS About Taxes (2014 Revised Edition) ANSWERS* TO QUESTIONS FREQUENTLY ASKED ABOUT - COMPENSATION & BENEFITS We heard that our pastor is both an employee and an independent

Club & LSC Financial Management. Jill J. Goodwin, CPA Waugh & Goodwin, LLP [email protected]

Club & LSC Financial Management Jill J. Goodwin, CPA Waugh & Goodwin, LLP [email protected] Form 990 Forms 1099 and W 2 State taxes Other current issues TAX ISSUES Form 990 File Form 990, 990

Club & LSC Financial Management Jill J. Goodwin, CPA Waugh & Goodwin, LLP [email protected] Form 990 Forms 1099 and W 2 State taxes Other current issues TAX ISSUES Form 990 File Form 990, 990

DEBT FINANCING POLICIES

DEBT FINANCING POLICIES 1801 Debt Financing Selection 1802 Determination of Debt Capacity 1803 Debt Management Operation 1804 Debt Management Capital Projects 1805 Bank Lines of Credit 1806 Bank Letters

DEBT FINANCING POLICIES 1801 Debt Financing Selection 1802 Determination of Debt Capacity 1803 Debt Management Operation 1804 Debt Management Capital Projects 1805 Bank Lines of Credit 1806 Bank Letters

UNIVERSITY OF OKLAHOMA/NORMAN CAMPUS OFFICE OF RESEARCH SERVICES Procedures Guide. Recharge Center Operations

UNIVERSITY OF OKLAHOMA/NORMAN CAMPUS OFFICE OF RESEARCH SERVICES Procedures Guide Recharge Center Operations Overview 3 Establishing a Recharge Center 3 Information that Will Need to be Determined 3 Rate

UNIVERSITY OF OKLAHOMA/NORMAN CAMPUS OFFICE OF RESEARCH SERVICES Procedures Guide Recharge Center Operations Overview 3 Establishing a Recharge Center 3 Information that Will Need to be Determined 3 Rate

PTA Treasurer s Training. Being Accountable and Transparent

PTA Treasurer s Training Being Accountable and Transparent Duties of the PTA Treasurer Maintain accurate, detailed financial records Help prepare the PTA Budget Receive & disburse funds Present a Treasurer

PTA Treasurer s Training Being Accountable and Transparent Duties of the PTA Treasurer Maintain accurate, detailed financial records Help prepare the PTA Budget Receive & disburse funds Present a Treasurer

Accounting for Colleges & Universities. Chapter 17

Accounting for Colleges & Universities Chapter 17 Learning Objectives Understand why most government C&Us choose to report as business-type only special purpose governments Explain unique aspects of C&U

Accounting for Colleges & Universities Chapter 17 Learning Objectives Understand why most government C&Us choose to report as business-type only special purpose governments Explain unique aspects of C&U

Senate Bill No. 2 CHAPTER 673

Senate Bill No. 2 CHAPTER 673 An act to amend Section 6254 of the Government Code, to add Article 3.11 (commencing with Section 1357.20) to Chapter 2.2 of Division 2 of the Health and Safety Code, to add

Senate Bill No. 2 CHAPTER 673 An act to amend Section 6254 of the Government Code, to add Article 3.11 (commencing with Section 1357.20) to Chapter 2.2 of Division 2 of the Health and Safety Code, to add

Introduction to Tax-Exempt Status

State of California Franchise Tax Board Introduction to Tax-Exempt Status Some organizations that may apply for exemption status Business Leagues Cemeteries Chambers of Commerce Charitable Organizations

State of California Franchise Tax Board Introduction to Tax-Exempt Status Some organizations that may apply for exemption status Business Leagues Cemeteries Chambers of Commerce Charitable Organizations

Collaborative For Children. Financial Statements and Independent Auditors Report for the years ended December 31, 2011 and 2010

Financial Statements and Independent Auditors Report for the years ended December 31, 2011 and 2010 Blazek & Vetterling C ERTIFIED P UBLIC A CCOUNTANTS Independent Auditors Report To the Board of Directors

Financial Statements and Independent Auditors Report for the years ended December 31, 2011 and 2010 Blazek & Vetterling C ERTIFIED P UBLIC A CCOUNTANTS Independent Auditors Report To the Board of Directors

Elements of Local School Accounting II

Elements of Local School Accounting II LSFM Certificate Program March 2015 Bryant Conference Center Tuscaloosa, Alabama 1 Elements of Local School Accounting II Board Policies and Procedures Accounting

Elements of Local School Accounting II LSFM Certificate Program March 2015 Bryant Conference Center Tuscaloosa, Alabama 1 Elements of Local School Accounting II Board Policies and Procedures Accounting

Operating an IRS-Compliant Gymnastics Booster Club

Operating an IRS-Compliant Gymnastics Booster Club Presented by Marc Jacobs, Esq. and Kevin Warren, Esq. [email protected] [email protected] Attorneys at Michelman & Robinson, LLP December 3, 2014 Why

Operating an IRS-Compliant Gymnastics Booster Club Presented by Marc Jacobs, Esq. and Kevin Warren, Esq. [email protected] [email protected] Attorneys at Michelman & Robinson, LLP December 3, 2014 Why

University of Central Florida Foundation, Inc. (A Discrete Component Unit of the University of Central Florida)

") University of Central Florida Foundation, Inc. (A Discrete Component Unit of the University of Central Florida) Single Audit Report Year Ended June 30, 2015 Contents Independent Auditor s Report 1 Management

University of Central Florida Foundation, Inc. (A Discrete Component Unit of the University of Central Florida) Single Audit Report Year Ended June 30, 2015 Contents Independent Auditor s Report 1 Management

ATTACHMENT D CHARTER SCHOOLS IN MICHIGAN

ATTACHMENT D CHARTER SCHOOLS IN MICHIGAN Introduction In December of 1993, Michigan became the ninth state to pass charter school legislation. The current charter school statute applicable to this RFP

ATTACHMENT D CHARTER SCHOOLS IN MICHIGAN Introduction In December of 1993, Michigan became the ninth state to pass charter school legislation. The current charter school statute applicable to this RFP

Non-cash Donations & Sales. Accounting and IRS Reporting

Non-cash Donations & Sales Accounting and IRS Reporting Contact Information Julie L. Sokolowski, CPA Shareholder Wall, Einhorn & Chernitzer, PC CPAs & Advisors 555 East Main Street, Suite 1600 Norfolk,

Non-cash Donations & Sales Accounting and IRS Reporting Contact Information Julie L. Sokolowski, CPA Shareholder Wall, Einhorn & Chernitzer, PC CPAs & Advisors 555 East Main Street, Suite 1600 Norfolk,

WITH REPORTS OF INDEPENDENT AUDITORS

As of and for the Years Ended JUNE 30, 2013 AND JUNE 30, 2014 Financial Statements and Schedule of Expenditures of Federal Awards WITH REPORTS OF INDEPENDENT AUDITORS AUDITED FINANCIAL STATEMENTS Independent

As of and for the Years Ended JUNE 30, 2013 AND JUNE 30, 2014 Financial Statements and Schedule of Expenditures of Federal Awards WITH REPORTS OF INDEPENDENT AUDITORS AUDITED FINANCIAL STATEMENTS Independent

Ohio University (a component unit of the State of Ohio) Financial Statements for the Years Ended June 30, 2014 and 2013

Financial Statements for the Years Ended June 30, 2014 and 2013") (a component unit of the State of Ohio) Financial Statements for the Years Ended Contents Independent Auditor s Report 1-3 Financial Statements Management s Discussion and Analysis 4-14 Statements of Net

(a component unit of the State of Ohio) Financial Statements for the Years Ended Contents Independent Auditor s Report 1-3 Financial Statements Management s Discussion and Analysis 4-14 Statements of Net

Financial Report to the Board of Trustees

Financial Report to the Board of Trustees February 27, 2013 FY12 Closeout and FY13 Six Month Update Financial Report to the Board of Trustees February 27 2013 Table of Contents Page(s) University of Connecticut

Financial Report to the Board of Trustees February 27, 2013 FY12 Closeout and FY13 Six Month Update Financial Report to the Board of Trustees February 27 2013 Table of Contents Page(s) University of Connecticut

SUBCHAPTER XI. GENERAL POLICE REGULATIONS.

SUBCHAPTER XI. GENERAL POLICE REGULATIONS. Article 37. Lotteries, Gaming, Bingo and Raffles. Part 2. Bingo and Raffles. 14-309.5. Bingo. (a) The purpose of the conduct of bingo is to insure a maximum availability

SUBCHAPTER XI. GENERAL POLICE REGULATIONS. Article 37. Lotteries, Gaming, Bingo and Raffles. Part 2. Bingo and Raffles. 14-309.5. Bingo. (a) The purpose of the conduct of bingo is to insure a maximum availability

Instructions for Schedule A (Form 990 or 990-EZ)

") 2010 Instructions for Schedule A (Form 990 or 990-EZ) Public Charity Status and Public Support Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

2010 Instructions for Schedule A (Form 990 or 990-EZ) Public Charity Status and Public Support Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

Instructions for Schedule L (Form 990 or 990-EZ)

") 2010 Instructions for Schedule L (Form 990 or 990-EZ) Transactions With Interested Persons Department of the Treasury Internal Revenue Service State whether the transaction has been Section references

2010 Instructions for Schedule L (Form 990 or 990-EZ) Transactions With Interested Persons Department of the Treasury Internal Revenue Service State whether the transaction has been Section references

LOUISIANA SALES TAX & NON-PROFIT ORGANIZATIONS

LOUISIANA SALES TAX & NON-PROFIT ORGANIZATIONS A Brief Overview of the Louisiana Sales Tax Laws and How they Apply to Non-Profit Organizations Presented by Cary B Bryson Bryson Law Firm, L.L.C. Sales Taxes:

LOUISIANA SALES TAX & NON-PROFIT ORGANIZATIONS A Brief Overview of the Louisiana Sales Tax Laws and How they Apply to Non-Profit Organizations Presented by Cary B Bryson Bryson Law Firm, L.L.C. Sales Taxes:

UDAAP & UBIT: Legal Issues Affecting the Student Loan Industry

UDAAP & UBIT: Legal Issues Affecting the Student Loan Industry 2015 Education Finance Council Mid-Year Membership Meeting July 10, 2015 Jonathan L. Pompan Carrie Garber Siegrist Partner and Co-Chair CFPB

UDAAP & UBIT: Legal Issues Affecting the Student Loan Industry 2015 Education Finance Council Mid-Year Membership Meeting July 10, 2015 Jonathan L. Pompan Carrie Garber Siegrist Partner and Co-Chair CFPB

Private foundations Establishing a vehicle for your charitable vision

Private foundations Establishing a vehicle for your charitable vision I didn t know where to start. The advice I received on creating a private foundation pointed me in the right direction, and now I m

Private foundations Establishing a vehicle for your charitable vision I didn t know where to start. The advice I received on creating a private foundation pointed me in the right direction, and now I m

2014-2015 Tax Update: Another Year For Tax Breaks By Kurt J. Kilwein, CPA, CFP, Partner and Olga Zarney, CPA, MBT, Manager

WINTER 2014-2015 2014-2015 Tax Update: Another Year For Tax Breaks By Kurt J. Kilwein, CPA, CFP, Partner and Olga Zarney, CPA, MBT, Manager Individual Taxation Many of the tax breaks which expired at the

WINTER 2014-2015 2014-2015 Tax Update: Another Year For Tax Breaks By Kurt J. Kilwein, CPA, CFP, Partner and Olga Zarney, CPA, MBT, Manager Individual Taxation Many of the tax breaks which expired at the

Kirsten Volpi Senior Vice President for Finance and Administration

TO: FROM: Board of Trustees Kirsten Volpi Senior Vice President for Finance and Administration DATE: May 23, 2011 SUBJECT: FY 2012 Budget I. BACKGROUND INFORMATION Fiscal Year 2012 Operating Budget Summary

TO: FROM: Board of Trustees Kirsten Volpi Senior Vice President for Finance and Administration DATE: May 23, 2011 SUBJECT: FY 2012 Budget I. BACKGROUND INFORMATION Fiscal Year 2012 Operating Budget Summary

2. Corporations Fully Exempt These corporations qualify for the full income tax exemption:

T. Exempt Corporations (G.S. 105-125, G.S. 105-130.11, G.S. 105-130.12) 1. Preliminary Statement Some types of corporations are fully exempt from income and franchise taxes, whereas others are conditionally

T. Exempt Corporations (G.S. 105-125, G.S. 105-130.11, G.S. 105-130.12) 1. Preliminary Statement Some types of corporations are fully exempt from income and franchise taxes, whereas others are conditionally

CALIFORNIA STATE UNIVERSITY, SAN MARCOS. Financial Statements. June 30, 2005 and 2004. (With Independent Auditors Report Thereon)

") Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Management s Discussion and Analysis 3 Financial Statements: Statements of Net Assets

Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Management s Discussion and Analysis 3 Financial Statements: Statements of Net Assets

How To Account For A 501(C) Organization

Organization") Accounting Accounting Finance and Finance Alliances for Alliances PRESENTED BY: JANET MALASIG IEEE-ISTO CONTROLLER IEEE-ISTO and member Programs Program Financial Statements Membership Dues Accounting

Accounting Accounting Finance and Finance Alliances for Alliances PRESENTED BY: JANET MALASIG IEEE-ISTO CONTROLLER IEEE-ISTO and member Programs Program Financial Statements Membership Dues Accounting

FLORIDA HIGH SCHOOL FOR ACCELERATED LEARNING - WEST PALM BEACH CAMPUS, INC. d/b/a QUANTUM HIGH SCHOOL

LEARNING - WEST PALM BEACH CAMPUS, INC. Financial Statements with Independent Auditors Reports Thereon June 30, 2015 CONTENTS Page Management s Discussion and Analysis 1 6 Report of Independent Auditors

LEARNING - WEST PALM BEACH CAMPUS, INC. Financial Statements with Independent Auditors Reports Thereon June 30, 2015 CONTENTS Page Management s Discussion and Analysis 1 6 Report of Independent Auditors

SCHOOL BOARD OF BROWARD COUNTY, FL INTERNAL FUNDS ACCOUNTING GENERAL POLICY

Page 1 of 9 GENERAL POLICY TOPICS IN BULLETIN: I. INTERNAL ACCOUNTS POLICIES II. RESPONSIBILITY - PRINCIPAL III. RESPONSIBILITY - BOOKKEEPER IV. EMPLOYEE RESTRICTIONS V. ACCOUNTING FOR STUDENT ACTIVITIES

Page 1 of 9 GENERAL POLICY TOPICS IN BULLETIN: I. INTERNAL ACCOUNTS POLICIES II. RESPONSIBILITY - PRINCIPAL III. RESPONSIBILITY - BOOKKEEPER IV. EMPLOYEE RESTRICTIONS V. ACCOUNTING FOR STUDENT ACTIVITIES

AUDIT AND FINANCE COMMITTEE

Item: AF: I-4 AUDIT AND FINANCE COMMITTEE Wednesday, February 16, 2011 SUBJECT: REVIEW OF FAU INTERCOLLEGIATE ATHLETICS PROGRAM INDEPENDENT ACCOUNTANT S REPORT ON AGREED-UPON PROCEDURES FOR THE YEAR ENDED

Item: AF: I-4 AUDIT AND FINANCE COMMITTEE Wednesday, February 16, 2011 SUBJECT: REVIEW OF FAU INTERCOLLEGIATE ATHLETICS PROGRAM INDEPENDENT ACCOUNTANT S REPORT ON AGREED-UPON PROCEDURES FOR THE YEAR ENDED

Federal requirements: annual information return

Thursday, October 01, 2009 Annual filing requirements for California nonprofit organizations Failure to file may lead to fines, suspension, forfeiture of corporate status, or even loss of exemption. By:

Thursday, October 01, 2009 Annual filing requirements for California nonprofit organizations Failure to file may lead to fines, suspension, forfeiture of corporate status, or even loss of exemption. By:

BUDGET in BRIEF. University of Wisconsin Madison Budget Report 2014 2015

BUDGET in BRIEF University of Wisconsin Madison Budget Report 2014 2015 This document is intended to provide an easy-to-understand glimpse of UW Madison s budget picture. Spending information included

BUDGET in BRIEF University of Wisconsin Madison Budget Report 2014 2015 This document is intended to provide an easy-to-understand glimpse of UW Madison s budget picture. Spending information included

Instructions for Schedule A (Form 990 or 990-EZ)

") 2014 Instructions for Schedule A (Form 990 or 990-EZ) Public Charity Status and Public Support Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

2014 Instructions for Schedule A (Form 990 or 990-EZ) Public Charity Status and Public Support Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

Executive Summary. Model Structure. General Economic Environment and Assumptions

Executive Summary The (LTFP) report is an update from the preliminary report presented in January 2009 and reflects the Mayor s Proposed Budget for Fiscal Year 2010 and Fiscal Year 2011. Details of the

Executive Summary The (LTFP) report is an update from the preliminary report presented in January 2009 and reflects the Mayor s Proposed Budget for Fiscal Year 2010 and Fiscal Year 2011. Details of the

HARDSHIP WITHDRAWAL ELECTION. To the Plan Administrator of., Participant.

HARDSHIP WITHDRAWAL ELECTION To the Plan Administrator of Re: ( Plan ):, Participant. 1. Withdrawal Election. As permitted by the Plan, I elect to withdraw the following portion of my Vested Account Balance

HARDSHIP WITHDRAWAL ELECTION To the Plan Administrator of Re: ( Plan ):, Participant. 1. Withdrawal Election. As permitted by the Plan, I elect to withdraw the following portion of my Vested Account Balance

FINANCIAL MANAGEMENT POLICIES AND PROCEDURES

FINANCIAL MANAGEMENT POLICIES AND PROCEDURES 1. GENERAL PURPOSE The purpose of these policies is to establish guidelines for developing financial goals and objectives, making financial decisions, reporting

FINANCIAL MANAGEMENT POLICIES AND PROCEDURES 1. GENERAL PURPOSE The purpose of these policies is to establish guidelines for developing financial goals and objectives, making financial decisions, reporting

Instructions for Schedule A (Form 990 or 990-EZ) Public Charity Status and Public Support

Public Charity Status and Public Support") 2009 Instructions for Schedule A (Form 990 or 990-EZ) Public Charity Status and Public Support Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

2009 Instructions for Schedule A (Form 990 or 990-EZ) Public Charity Status and Public Support Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

BYLAWS OF NEMOA ARTICLE I. NAME AND LOCATION

BYLAWS OF NEMOA ARTICLE I. NAME AND LOCATION The name of the association is NEMOA (the Association ), a Maine nonprofit corporation organized and existing pursuant to the Maine Nonprofit Corporation Act,

BYLAWS OF NEMOA ARTICLE I. NAME AND LOCATION The name of the association is NEMOA (the Association ), a Maine nonprofit corporation organized and existing pursuant to the Maine Nonprofit Corporation Act,

Nonprofit Board of Directors: The Legal Basis for Good Governance

Nonprofit Board of Directors: The Legal Basis for Good Governance Focusing On: The inter-related State and Federal laws which underlie the creation and structure of nonprofits as well as the basic legal

Nonprofit Board of Directors: The Legal Basis for Good Governance Focusing On: The inter-related State and Federal laws which underlie the creation and structure of nonprofits as well as the basic legal

BYLAWS OF THE UNIVERSITY O F TEXAS HEALTH SCIENCE CENTER AT SAN ANTONIO SCHOOL OF ALLIED HEALTH SCIENCES FACULTY PRACTICE PLAN

BYLAWS OF THE UNIVERSITY O F TEXAS HEALTH SCIENCE CENTER AT SAN ANTONIO SCHOOL OF ALLIED HEALTH SCIENCES FACULTY PRACTICE PLAN UT Allied Health Partners ARTICLE I PURPOSE The purpose of the UT Allied Health

BYLAWS OF THE UNIVERSITY O F TEXAS HEALTH SCIENCE CENTER AT SAN ANTONIO SCHOOL OF ALLIED HEALTH SCIENCES FACULTY PRACTICE PLAN UT Allied Health Partners ARTICLE I PURPOSE The purpose of the UT Allied Health

State Cashflow Management

Informational Paper 77 State Cashflow Management Wisconsin Legislative Fiscal Bureau January, 2009 State Cashflow Management Prepared by Dave Loppnow Wisconsin Legislative Fiscal Bureau One East Main,

Informational Paper 77 State Cashflow Management Wisconsin Legislative Fiscal Bureau January, 2009 State Cashflow Management Prepared by Dave Loppnow Wisconsin Legislative Fiscal Bureau One East Main,

Chapter V: Special Rules for Establishing and Operating a Super PAC that is a Nonconnected Committee

Chapter V: Special Rules for Establishing and Operating a Super PAC that is a Nonconnected Committee The Connection Strategies for Creating and Operating 501(c)(3)s, 501(c)(4)s and Political Organizations

Chapter V: Special Rules for Establishing and Operating a Super PAC that is a Nonconnected Committee The Connection Strategies for Creating and Operating 501(c)(3)s, 501(c)(4)s and Political Organizations