FINANCIAL PLANNING IN UNCERTAIN TIMES

|

|

|

- Ophelia Lester

- 8 years ago

- Views:

Transcription

1 NONPROFIT FINANCIAL MANAGEMENT TRAINING FINANCIAL PLANNING IN UNCERTAIN TIMES Developed by Nonprofits Assistance Fund As the economy rebounds, nonprofit leaders know that the effects of the recession will continue to impact their budgets for years to come. Sound financial management must be aligned with other strategies if nonprofit organizations are going to survive and thrive. Attendees of this workshop will learn how to assess their organization s current financial position and business model, gauge budget risks and uncertainties, and examine organizational goals and priorities. Using practical examples, we will discuss different tools and techniques for scenario planning and multi-year budgeting.

2 WHO WE ARE OUR MISSION IS TO BUILD FINANCIALLY HEALTHY NONPROFITS THAT FOSTER COMMUNITY VITALITY Sustainability looks different today. Meeting the challenge of a changed environment requires a deep understanding of how mission and money work together. Nonprofi ts Assistance Fund s fi nancial experts are here to help you strengthen your capacity to address unexpected events, fi nance new opportunities, and realize strategic goals. We fulfi ll our mission by helping you thrive. HOW WE CAN HELP Financial Advice When you need a trusted advisor, we are here to help. We can answer your immediate questions, increase your understanding of your organization s situation, and work with you to develop effective fi nancial practices. Nonprofit Lending For us, it s more than a loan. Our lending team understands the nuances of nonprofi ts. We craft fi nancial solutions for your unique needs and will stick with you to address the unexpected, setting you up for success. Trainings and Resources Having the right tools to manage your organization s money is essential to success. Our trainings and resources will help you develop practical skills, engage in strategic thinking, and build advanced fi nancial management capabilities. OUR TRAINERS Michael Anderson, Training Program Manager and Loan Officer: Michael holds a Master of Public Policy degree from the Humphrey Institute of Public Affairs. He serves as adjunct faculty at the University of Minnesota and on the board of PRG, Inc., a nonprofi t community development corporation. Kate Barr, Executive Director: Kate leads the strategic direction of our organization, developed our core training curriculum, and is a popular national speaker, trainer, and writer on nonprofi t management and fi nance. A former Senior Vice President of Riverside Bank, Kate holds a Master s degree from Hamline University and is adjunct faculty at Hamline and the Humphrey Institute. She also serves on the board of Neighborhood Development Center, Partners for the Common Good, and Western Bank. Steve Boland, Loan Officer: Steve has previously worked for Congressman Bruce Vento and served as Executive Director of the Saint Paul Neighborhood Network, Summit-University Planning Council, and the Greater Frogtown Community Development Corporation. He is pursuing a Master of Nonprofi t Management from Hamline University and serves on the board of Sparc. Phil Hatlie, Loan Officer: Phil has a special expertise in charter school fi nancing and management. Previously he served as Director of Finance and Administration for the Greater Minneapolis Council of Churches and Twin Cities Habitat for Humanity and Director of Operations for the HECUA. Phil serves on the board of the MN Conference United Church of Christ and on committees for Hearth Connection and Habitat for Humanity of Minnesota. Janet Ogden-Brackett, Loan Fund Manager: Janet has served as the Director of Operations and Financial Manager at Minnesota Environmental Initiative and worked at a CPA fi rm. She has participated in the Minnesota Council of Nonprofi ts Leadership Institute and is on the board of LegalCorps and Family Tree Clinic.

3 FINANCIAL PLANNING IN UNCERTAIN TIMES GOALS FOR TODAY S WORKSHOP 1. Gain analytical tools to assist in understanding an organization s current financial position and current business model 2. Learn different techniques and approaches to having practical conversations critical to organizational decision-making 3. Explore factors to consider when scenario planning and multi-year budgeting through case examples 3

4 ASSESSING YOUR CURRENT FINANCIAL POSITION BALANCE SHEET (STATEMENT OF FINANCIAL POSITION) Financial assets and obligations as of a specific date Assets are what is owned Current assets Long-term assets Liabilities are what is owed Current liabilities Long-term liabilities Net Assets are equal to Net Worth, Equity, or Retained Earnings Unrestricted, temporarily restricted, permanently restricted Change in Net Assets: surplus or loss amount from the Income Statement for the same period All changes in Net Assets flow from the Income Statement. 4

5 5

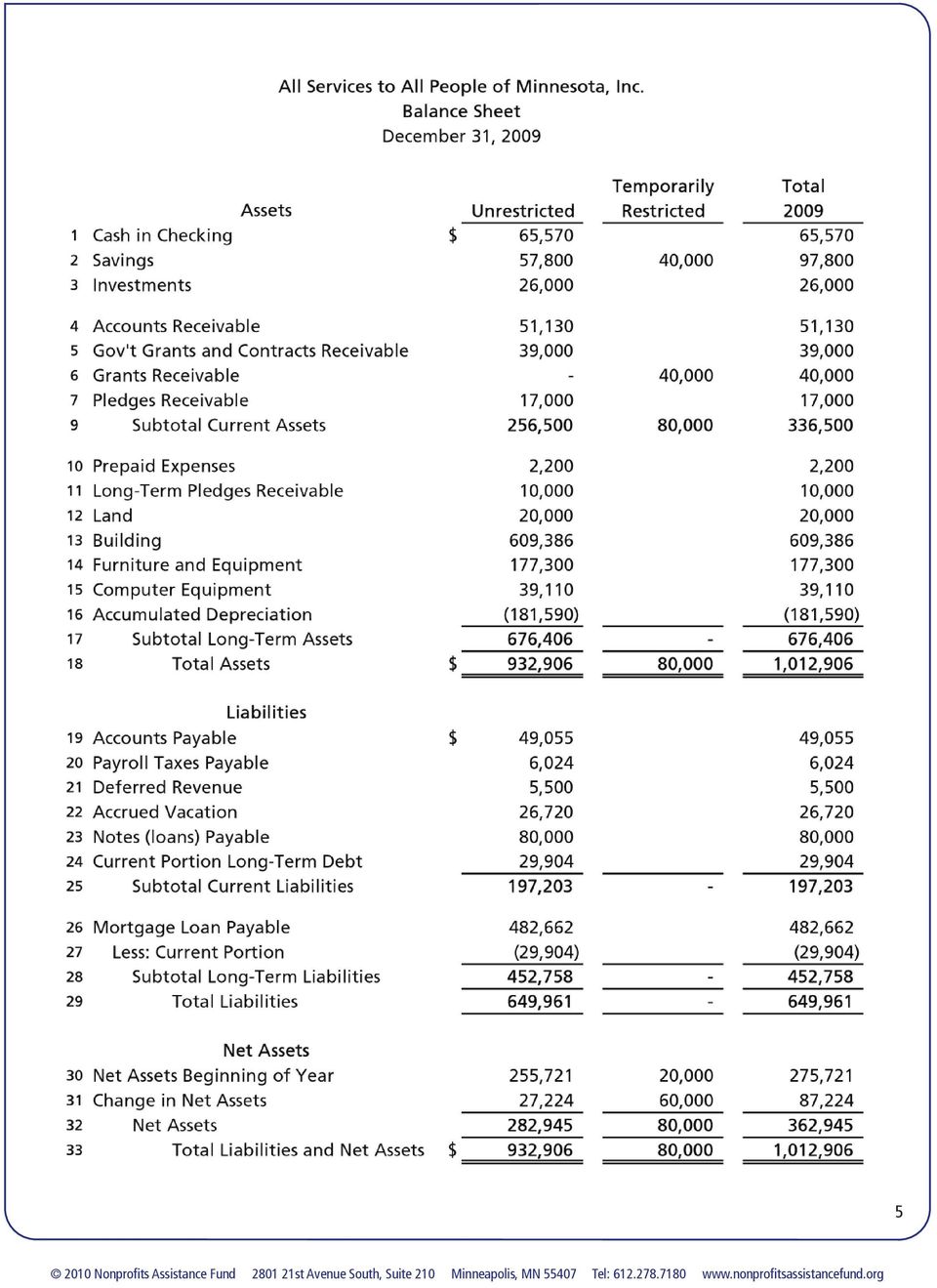

6 DAYS CASH ON HAND This calculation measures how many days expenses can be covered with the current balance of unrestricted cash. DAYS CASH ON HAND Cash and current investments Daily cash required Daily cash required = Annual expense budget minus non-cash expenses, passthrough funds, and unusual, one-time expenses / 365 *Unrestricted cash only Example: 6

7 Cash = $65,570 + $57,800 + $26,000 = $149,370 Daily cash required = ($878,325 - $6,000 - $40,970) / 365 = $2, days cash on hand 7

/ 365 = $2,277 65 days")

8 CURRENT RATIO An indication of the organization s ability to pay obligations in a timely way (within 12 months). A current ratio of less than 1 can be an indication of a future cash flow problem. CURRENT RATIO Current assets Current liabilities Example: Current assets = $256,500 Current liabilities = $197,

9 NET ASSET RESERVE RATIO The net asset reserve ratio measures the financial cushion an organization has in order to ensure the stable delivery of programs and services in the event of unforeseen circumstances. NET ASSET RESERVE RATIO Unrestricted net assets Total annual expenses / 365 Example: 9

10 Unrestricted net assets = $282,945 Total daily expenses = $878,325 / 365 = $2, days of expenses available in net asset reserves 10

11 UNDERSTANDING YOUR BUSINESS MODEL INCOME STATEMENT (STATEMENT OF ACTIVITIES) Amounts of income and expenses for a certain period of time Resulting change in net assets surplus (profit) or deficit (loss) Income categories Support: voluntary contributions that can be cash or in-kind Revenue: income earned from delivery of goods and services Expense categories Personnel expenses are usually the largest component of total expenses Operating expenses Program expenses Change in Net Assets Variously labeled Surplus/Deficit, Profit/Loss, Excess of Revenue Over Expenses, and other terms 11

12 12

13 RELIANCE RATIO The reliance ratio measures an organization s dependence on certain sources or certain types of income. RELIANCE RATIO Amount of largest type of income Total income SINGLE RELIANCE RATIO Single largest income source (grant, contract, client) Total income Example: Amount of largest type of income = $330,000 Total income = $905, % of income reliant on one income type 13

Total income Example: Amount of largest type of income =")

14 CUNA (PROFITABILITY) RATIO The CUNA ratio measures the amount of unrestricted net assets retained for reserves or organizational cushion. The target ratio depends on how much reserve or cushion is already on hand. CUNA RATIO Change in unrestricted net assets Total unrestricted income Example: Change in unrestricted net assets = $27,224 Total unrestricted income = $905,549 3% of unrestricted income retained for reserves 14

15 TREND ANALYSIS (YOU RE HEADING SOMEWHERE) 15

16 TREND ANALYSIS (YOU RE HEADING SOMEWHERE) 16

17 TREND ANALYSIS GRAPHICS 17

18 GAUGING RISKS TO YOUR INCOME BUDGET What are general risks that could affect all funding sources? What are risks specific to particular funding sources? Funding Source Current Reliance Risks Unique to Source Risk Treatment in Budget DHS Contract 55% ($340,000) Foundation A 6% ($35,000) Individual Gifts 12% ($74,000) Workshop Fees 21% ($129,800) Unallotment, rate reductions Likely not a good fit with new foundation priorities Lots of small and mid-sized donors keeps risk low. Five at >$5,000 are biggest risk. Demand increasing, clients ability to pay may be at risk (minor) No discount, included at current funding level $20,000 transition grant included Forecasting 10% decrease Slight increase over current year 18

No discount, included at current funding level $20,000 transition grant included Forecasting 10% decrease Slight")

19 GENERATING AND UNDERSTANDING PROGRAM-BASED REPORTS 19

20 HOW FLEXIBLE ARE YOUR EXPENSES? Scenario Planning Approaches Highly flexible expenses Budget by project Avoid fixed expenses Short-term horizon Adapt to new information Low financial risk Flexible and fixed expenses Mix of short-term project and line-by-line budget scenarios Annual budget timeline Develop at least two scenario options Low-medium financial risk Significant fixed expenses Requires program planning for all areas considering redesign, contraction, or elimination Line-by-line expense options Two year budget timeline Develop at least two scenario options, including use of any reserves Medium-high financial risk 20

21 STRATEGIC DECISION-MAKING REVIEW OF ANALYSIS Liquidity analysis Balance sheet strength Income risk and reliance Trend analysis Program financial results (RE)ITERATION OF ORGANIZATIONAL GOALS AND PRIORITIES Board and staff leadership revisit goals that have been laid out in strategic plans, work plans, etc. What is most important to the organization? How nimble is the organization? 21

22 CONSIDER MISSION IMPACT AND FINANCIAL IMPACT What is the right program mix for the organization? Which programs require subsidy? Is there subsidy available? What should the organization do more or less of? 22

23 UTILIZE IDEA SCREENS Use a customized numeric scale to complete the rubric below to screen different strategies or approaches. The scorecard that results leads to a tactical plan with well-considered risks and benefits. Strategy 1 Strategy 2 Strategy 3 Mission Impact Financial Impact Need/Demand Alignment with Skills and Identity Likely to Succeed Measurable Impact TOTAL 23

24 ORGANIZATIONAL COST-BENEFIT ANALYSIS Strategy 1: Increase participant fees Costs to the Organization Benefits to the Organization Mission Current Year Financial Org Capacity Mission Future Years Financial Org Capacity 24

25 UNDERSTAND YOUR FINANCIAL MANAGEMENT CULTURE What types of languages and attitudes are prevalent when discussing organizational finance? Scarcity: cut, cut, cut we never have sufficient resources Possiblity: rethinking, revisioning, innovative and creative Inertia: we could never possibly change that How dynamic is your budget? 25

26 UNDERSTAND YOUR FINANCIAL MANAGEMENT CULTURE Professionalization Are internal controls in place and regarded? Is there a quality expectation of financial reports? Are reports prepared in a timely manner? Roles and Responsibilities Who is involved in strategic conversations? Who is involved in financial decisions? Executive staff, board members, program staff Transparency and communication What kind of language is used to describe financial position? How easily accessible is financial information? Risk tolerance How is prospective income treated in the budget? How willing is the organization to take on new projects? How willing is the organization to invest internal resources in building capacity, such as program development and staff training? 26

27 SCENARIO PLANNING SCENARIO PLANNING CONSIDERATIONS How will scenarios differ? Consider the entire realistic realm of possibilities, particularly in the income budget Are income sources variable by percentage or all-or-nothing? What events would trigger a change in course? How flexible are your expenses? How could they become more flexible? 27

28 BE WELL CLINIC INCOME SCENARIO 1 28

29 BE WELL CLINIC EXPENSE SCENARIO 1 29

30 BE WELL CLINIC IMPACT SCENARIO 1 30

31 BE WELL CLINIC INCOME SCENARIO 2 31

32 BE WELL CLINIC EXPENSE SCENARIO 2 32

33 BE WELL CLINIC IMPACT SCENARIO 2 33

34 BE WELL CLINIC INCOME SCENARIO 3 34

35 BE WELL CLINIC EXPENSE SCENARIO 3 35

36 BE WELL CLINIC EXPENSE SCENARIOS SUMMARY 36

37 BE WELL CLINIC SCENARIO PLANNING SUMMARY 37

38 FINANCIAL FORECASTING PURPOSE OF FINANCIAL FORECASTING Provide an action plan to achieve strategic goals Translate strategic plans into financial plans Confirm priorities Identify capacity needs Prepare for organizational changes to support goals Create SMART goals to implement financial plan Specific Measurable Attainable Realistic Timely 38

39 FINANCIAL FORECASTING STEPS Use strategic plan to identify financial requirements Prepare simple budget plan for core ongoing activities Estimate costs to achieve strategic goals Costs of new activities that will be ongoing Costs of new special projects Costs of added organizational capacity Identify need for resources to support new costs Resources of ongoing revenue to pay expenses Resources of special project revenue Resources of time to plan and implement Resources of skills to plan and implement Ask and consider: What is our optimal income mix? Honestly assess feasibility of financial needs Prioritize and balance Implement and monitor 39

40 40

41 41

42 42

43 HOW TO USE TODAY S WORKSHOP 1. Ensure that key organizational decision-makers have a shared understanding of the organization s financial health, business model, and financial risks. 2. Revisit important organizational documents such as strategic plans and work plans. If necessary, revisit conversations to be certain that there is agreement on key organizational goals and priorities. 3. Consider what will be necessary to become a more financially dynamic and flexible organization by reviewing cost structures. Look forward; think about how to properly balance an emphasis on annual budgeting with scenario planning and multi-year financial forecasting. 43

Financial Planning for Sustainable Nonprofits. Developed by Nonprofits Assistance Fund Presented by Curtis Klotz, CPA

Financial Planning for Sustainable Nonprofits Developed by Nonprofits Assistance Fund Presented by Curtis Klotz, CPA Who We Are Nonprofits Assistance Fund s mission is to build financially healthy nonprofits

Financial Planning for Sustainable Nonprofits Developed by Nonprofits Assistance Fund Presented by Curtis Klotz, CPA Who We Are Nonprofits Assistance Fund s mission is to build financially healthy nonprofits

Analyzing Financial Information Using Ratios

Analyzing Financial Information Using s A resource article by Kate Barr, executive director, Nonprofits Assistance Fund Leaders of nonprofits who seek to understand the organization s financial situation

Analyzing Financial Information Using s A resource article by Kate Barr, executive director, Nonprofits Assistance Fund Leaders of nonprofits who seek to understand the organization s financial situation

2011 Nonprofit Finance Fund. Sound Financial Planning: Tools for Managing Through a Downturn and Beyond. Presented by. Renée Jacob, Associate Director

Nonprofit Finance Fund Sound Financial Planning: Tools for Managing Through a Downturn and Beyond Presented by Renée Jacob, Associate Director Nonprofit Finance Fund Philip Rosenbloom, Associate Nonprofit

Nonprofit Finance Fund Sound Financial Planning: Tools for Managing Through a Downturn and Beyond Presented by Renée Jacob, Associate Director Nonprofit Finance Fund Philip Rosenbloom, Associate Nonprofit

Characteristics of Financially Healthy Nonprofits

Resource packet for Navigating Nonprofit Financials Characteristics of Financially Healthy Nonprofits 1 Overview of Nonprofit Financial Statements Audit 2 Statement of Financial Position (Balance Sheet)

Resource packet for Navigating Nonprofit Financials Characteristics of Financially Healthy Nonprofits 1 Overview of Nonprofit Financial Statements Audit 2 Statement of Financial Position (Balance Sheet)

Nonprofit Finance Fund. Sound Financial Planning Tools for Managing Through a Downturn and Beyond. Presented by

Nonprofit Finance Fund Sound Financial Planning Tools for Managing Through a Downturn and Beyond Presented by Emily Guthman, Associate Director Nonprofit Finance Fund Renée Jacob, Associate Director Nonprofit

Nonprofit Finance Fund Sound Financial Planning Tools for Managing Through a Downturn and Beyond Presented by Emily Guthman, Associate Director Nonprofit Finance Fund Renée Jacob, Associate Director Nonprofit

Managing Restricted Funds

Managing Restricted Funds A resource article by Nonprofits Assistance Fund Unique accounting standards require that nonprofit organizations report contributed income in one of three categories unrestricted,

Managing Restricted Funds A resource article by Nonprofits Assistance Fund Unique accounting standards require that nonprofit organizations report contributed income in one of three categories unrestricted,

Nonprofit Finance Fund. Demystifying Financial Statements: Assessing the Nonprofit Business Model. March 2013

Nonprofit Finance Fund Demystifying Financial Statements: Assessing the Nonprofit Business Model Presented by Alice Antonelli Senior Finance Advisor Nonprofit Finance Fund March 2013 Overview: Nonprofit

Nonprofit Finance Fund Demystifying Financial Statements: Assessing the Nonprofit Business Model Presented by Alice Antonelli Senior Finance Advisor Nonprofit Finance Fund March 2013 Overview: Nonprofit

Financial Health Analysis. Sample Choir. Overview 1. Dashboard 2

Report Sample Choir Page Overview 1 Dashboard 2 Overall Annual Performance Overview 3 Unrestricted Revenue & Expenses 4 Unrestricted Surplus (Deficit) 5 Separating Operating Revenue from Capital 7 Revenue

Report Sample Choir Page Overview 1 Dashboard 2 Overall Annual Performance Overview 3 Unrestricted Revenue & Expenses 4 Unrestricted Surplus (Deficit) 5 Separating Operating Revenue from Capital 7 Revenue

Cool Spring Analytics

Understanding Financial Statements 1 by Patricia Egan and Nancy Sasser Welcome to the world of numbers, arguably the least understood aspect of service as a trustee. In this article we will describe the

Understanding Financial Statements 1 by Patricia Egan and Nancy Sasser Welcome to the world of numbers, arguably the least understood aspect of service as a trustee. In this article we will describe the

Functional Title Classification FLSA Status Reports To Team Purpose

Functional Title Classification FLSA Status Reports To Team Purpose Vice President of Marketing and Engagement Director, Marketing & Communications UWW 400 N Exempt President & CEO Marketing & Engagement

Functional Title Classification FLSA Status Reports To Team Purpose Vice President of Marketing and Engagement Director, Marketing & Communications UWW 400 N Exempt President & CEO Marketing & Engagement

Assessing Nonprofit Financial Health

Nonprofit Finance Fund Assessing Nonprofit Financial Health Presented by: Rebecca Thomas, Vice President Nonprofit Finance Fund April 19, 2012 Presented in collaboration with: Overview: Nonprofit Finance

Nonprofit Finance Fund Assessing Nonprofit Financial Health Presented by: Rebecca Thomas, Vice President Nonprofit Finance Fund April 19, 2012 Presented in collaboration with: Overview: Nonprofit Finance

Understanding Nonprofit Financials

Understanding Nonprofit Financials The Basics Before you recommend a grant, consider reviewing the nonprofit s financials. Financials are easy to access in many cases, and they contain a host of insights

Understanding Nonprofit Financials The Basics Before you recommend a grant, consider reviewing the nonprofit s financials. Financials are easy to access in many cases, and they contain a host of insights

Charities Review Council Financial Session. Barbara Clare MAP for Nonprofits Chief Financial Officer bclare@mapfornonprofits.org

Charities Review Council Financial Session Barbara Clare MAP for Nonprofits Chief Financial Officer bclare@mapfornonprofits.org Session Objectives Review and understanding of basic financial statement

Charities Review Council Financial Session Barbara Clare MAP for Nonprofits Chief Financial Officer bclare@mapfornonprofits.org Session Objectives Review and understanding of basic financial statement

Minnesota Council of Nonprofits, Inc. Consolidated Financial Statements Years Ended December 31, 2013 and 2012 (With Independent Auditor's Report

Consolidated Financial Statements Years Ended December 31, 2013 and 2012 (With Independent Auditor's Report Thereon) MINNESOTA COUNCIL OF NONPROFITS INDEPENDENT AUDITOR S REPORT... 3 FINANCIAL STATEMENTS

Consolidated Financial Statements Years Ended December 31, 2013 and 2012 (With Independent Auditor's Report Thereon) MINNESOTA COUNCIL OF NONPROFITS INDEPENDENT AUDITOR S REPORT... 3 FINANCIAL STATEMENTS

Balance Sheets: What Do They Really Tell You?

ANNUAL MEETING HANDOUT Balance Sheets: What Do They Really Tell You? This working session showed attendees what to look for on the balance sheet, how to do calculations to gauge a museum s health and ways

ANNUAL MEETING HANDOUT Balance Sheets: What Do They Really Tell You? This working session showed attendees what to look for on the balance sheet, how to do calculations to gauge a museum s health and ways

Best Practices module

Best Practices module FINANCIAL MANAGEMENT Prepared By: David Hall (Economic Planning Group) and Rick Duckles (BC Forest Discovery Centre) Content BCMA / Best Practices Modules Page 1. Introduction Page

Best Practices module FINANCIAL MANAGEMENT Prepared By: David Hall (Economic Planning Group) and Rick Duckles (BC Forest Discovery Centre) Content BCMA / Best Practices Modules Page 1. Introduction Page

Child Care Center. Financial Planning and Facilities Development Manual

Child Care Center Financial Planning and Facilities Development Manual All Rights Reserved. Copyright 2009 Insight Center for Community Economic Development TABLE OF CONTENTS About the Manual... 1 Services

Child Care Center Financial Planning and Facilities Development Manual All Rights Reserved. Copyright 2009 Insight Center for Community Economic Development TABLE OF CONTENTS About the Manual... 1 Services

Budgeting for High-Performing Nonprofits. 2014 Plan A Advisors, Inc.

Budgeting for High-Performing Nonprofits 2014 Plan A Advisors, Inc. Budgeting for High-Performing Nonprofits 2 Budget to support your vision. Like a strategic plan, your nonprofit s budget is a kind of

Budgeting for High-Performing Nonprofits 2014 Plan A Advisors, Inc. Budgeting for High-Performing Nonprofits 2 Budget to support your vision. Like a strategic plan, your nonprofit s budget is a kind of

Critical Elements in Nonprofit Financial Statements

Nonprofit Finance Fund Critical Elements in Nonprofit Financial Statements Presented by Jina Paik Associate Nonprofit Finance Fund Bill Holmes Associate Nonprofit Finance Fund This webinar was made possible

Nonprofit Finance Fund Critical Elements in Nonprofit Financial Statements Presented by Jina Paik Associate Nonprofit Finance Fund Bill Holmes Associate Nonprofit Finance Fund This webinar was made possible

NONPROFITS ASSISTANCE FUND FINANCIAL STATEMENTS YEARS ENDED MARCH 31, 2015 AND 2014

FINANCIAL STATEMENTS YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS STATEMENTS OF FINANCIAL POSITION 3 STATEMENTS OF ACTIVITIES 5 STATEMENTS OF CASH FLOWS

FINANCIAL STATEMENTS YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS STATEMENTS OF FINANCIAL POSITION 3 STATEMENTS OF ACTIVITIES 5 STATEMENTS OF CASH FLOWS

Working Capital Concept & Animation

Working Capital Concept & Animation Meaning A measure of both a company's efficiency and its short-term financial health. The working capital is calculated as: Working Capital = Current Assets Current

Working Capital Concept & Animation Meaning A measure of both a company's efficiency and its short-term financial health. The working capital is calculated as: Working Capital = Current Assets Current

Rouch, Jean. Cine-Ethnography. Minneapolis, MN, USA: University of Minnesota Press, 2003. p 238

Minneapolis, MN, USA: University of Minnesota Press, 2003. p 238 http://site.ebrary.com/lib/uchicago/doc?id=10151154&ppg=238 Minneapolis, MN, USA: University of Minnesota Press, 2003. p 239 http://site.ebrary.com/lib/uchicago/doc?id=10151154&ppg=239

Minneapolis, MN, USA: University of Minnesota Press, 2003. p 238 http://site.ebrary.com/lib/uchicago/doc?id=10151154&ppg=238 Minneapolis, MN, USA: University of Minnesota Press, 2003. p 239 http://site.ebrary.com/lib/uchicago/doc?id=10151154&ppg=239

Farmer-to-Consumer Marketing: The Series

Farmer-to-Consumer Marketing #6 Financial Management Scope of Financial Management Managing the financial affairs of a direct marketing operation includes: Raising capital Identifying financial objectives

Farmer-to-Consumer Marketing #6 Financial Management Scope of Financial Management Managing the financial affairs of a direct marketing operation includes: Raising capital Identifying financial objectives

How to Prepare a Cash Flow Forecast

The Orangeville & Area Small Business Enterprise Centre (SBEC) 87 Broadway, Orangeville ON L9W 1K1 519-941-0440 Ext. 2286 or 2291 sbec@orangeville.ca www.orangevillebusiness.ca Supported by its Partners:

The Orangeville & Area Small Business Enterprise Centre (SBEC) 87 Broadway, Orangeville ON L9W 1K1 519-941-0440 Ext. 2286 or 2291 sbec@orangeville.ca www.orangevillebusiness.ca Supported by its Partners:

LONG TERM FINANCIAL PLAN (INTERIM) 2012/13 to 2022/23

2012/13 to 2022/23") LONG TERM FINANCIAL PLAN (INTERIM) 2012/13 to 2022/23 INTRODUCTION Long term financial planning is a key element of the Integrated Planning and Reporting Framework. It is the mechanism that enables local

LONG TERM FINANCIAL PLAN (INTERIM) 2012/13 to 2022/23 INTRODUCTION Long term financial planning is a key element of the Integrated Planning and Reporting Framework. It is the mechanism that enables local

ORGANIZATIONAL CAPACITY ASSESSMENT TOOL

ORGANIZATIONAL CAPACITY ASSESSMENT TOOL 1 CAPACITY ASSESSMENT The Capacity Assessment Tool is a useful guide to help you focus a discussion about the resources and practices your organization already has

ORGANIZATIONAL CAPACITY ASSESSMENT TOOL 1 CAPACITY ASSESSMENT The Capacity Assessment Tool is a useful guide to help you focus a discussion about the resources and practices your organization already has

Cr. Temporarily Restricted Donations $10,000.00

Hello, I am Ned Smith and today I will give you a high level overview of the revenues commonly generated by non profits. We will also discuss when the different revenues can be recognized and their main

Hello, I am Ned Smith and today I will give you a high level overview of the revenues commonly generated by non profits. We will also discuss when the different revenues can be recognized and their main

School of Accounting Florida International University Strategic Plan 2012-2017

School of Accounting Florida International University Strategic Plan 2012-2017 As Florida International University implements its Worlds Ahead strategic plan, the School of Accounting (SOA) will pursue

School of Accounting Florida International University Strategic Plan 2012-2017 As Florida International University implements its Worlds Ahead strategic plan, the School of Accounting (SOA) will pursue

Why Do Balance Sheets Matter? Rodney Christopher

Grantmakers in the Arts GIAreader Ideas and Information on Arts and Culture Vol. 22 No. 1, Spring 2011 Why Do Balance Sheets Matter? Rodney Christopher Reprinted from the Grantmakers in the Arts Reader,

Grantmakers in the Arts GIAreader Ideas and Information on Arts and Culture Vol. 22 No. 1, Spring 2011 Why Do Balance Sheets Matter? Rodney Christopher Reprinted from the Grantmakers in the Arts Reader,

How To Read A University Or College'S Financial Statement

Understanding College and University Financial Statements By Rudy Fichtenbaum Professor of Economics Department of Economics Wright State University Dayton, OH 45435 (937) 775-3085 rfichtenbaum@sbcglobal.net

Understanding College and University Financial Statements By Rudy Fichtenbaum Professor of Economics Department of Economics Wright State University Dayton, OH 45435 (937) 775-3085 rfichtenbaum@sbcglobal.net

Draft for discussion purposes. April 14, 2014 FINANCIAL STATEMENTS DRAFT EXCELLENCE CANADA. December 31, 2013

Draft for discussion purposes April 14, 2014 FINANCIAL STATEMENTS EXCELLENCE CANADA CONTENTS Page INDEPENDENT AUDITOR'S REPORT 1 FINANCIAL STATEMENTS Balance sheet 3 Statement of changes in net assets

Draft for discussion purposes April 14, 2014 FINANCIAL STATEMENTS EXCELLENCE CANADA CONTENTS Page INDEPENDENT AUDITOR'S REPORT 1 FINANCIAL STATEMENTS Balance sheet 3 Statement of changes in net assets

2/7/14 FINANCIAL PLANNING. What is a Financial Plan? Most people SEE what is obvious, but very few UDERSTAND or ACT on what they see.

FINANCIAL PLANNING Financial Planning for Small Business Success!! Preparing and Using Financial Records!! Grace Matiru, PhD. Faculty Associate, Dewey House for Civic Engagement, and Adjunct, Community

FINANCIAL PLANNING Financial Planning for Small Business Success!! Preparing and Using Financial Records!! Grace Matiru, PhD. Faculty Associate, Dewey House for Civic Engagement, and Adjunct, Community

Christy Eckoff, Director of Gift Planning The Community Foundation for Greater Atlanta

Christy Eckoff, Director of Gift Planning The Community Foundation for Greater Atlanta Gwyneth Gaul, Director of Development The Pittsburgh Foundation History & Background History of The Community Foundation

Christy Eckoff, Director of Gift Planning The Community Foundation for Greater Atlanta Gwyneth Gaul, Director of Development The Pittsburgh Foundation History & Background History of The Community Foundation

Minnesota Council of Nonprofits Strategic Plan 2010-2014 Approved by majority vote of the board of directors, November 17, 2009

Approved by majority vote of the board of directors, November 17, 2009 Our Vision Nonprofit organizations accomplish their missions for a healthy, cooperative and just society. Our Mission MCN informs,

Approved by majority vote of the board of directors, November 17, 2009 Our Vision Nonprofit organizations accomplish their missions for a healthy, cooperative and just society. Our Mission MCN informs,

Department Higher Education and Training

Department Higher Education and Training REPORTING by COUNCILS on PUBLIC HIGHER EDUCATION INSTITUTION s activities HEMIS institute 5 th August 2015 Dr EL van Staden: Chief Director University Academic

Department Higher Education and Training REPORTING by COUNCILS on PUBLIC HIGHER EDUCATION INSTITUTION s activities HEMIS institute 5 th August 2015 Dr EL van Staden: Chief Director University Academic

4 BEST PRACTICES IN FINANCIAL PLANNING FOR HIGHER EDUCATION

4 BEST PRACTICES IN FINANCIAL PLANNING FOR HIGHER EDUCATION PROJECT TEAM: Jason H. Sussman, Managing Director, Kaufman, Hall & Associates, LLC, and Chief Executive Officer, Axiom Software, LLC Charles

4 BEST PRACTICES IN FINANCIAL PLANNING FOR HIGHER EDUCATION PROJECT TEAM: Jason H. Sussman, Managing Director, Kaufman, Hall & Associates, LLC, and Chief Executive Officer, Axiom Software, LLC Charles

ADVICE FOR THE FAMILY AND THE FAMILY BUSINESS

ADVICE FOR THE FAMILY AND THE FAMILY BUSINESS We are dedicated to helping our clients assess and achieve their business and personal aspirations. Each of our clients has specific concerns, needs and objectives.

ADVICE FOR THE FAMILY AND THE FAMILY BUSINESS We are dedicated to helping our clients assess and achieve their business and personal aspirations. Each of our clients has specific concerns, needs and objectives.

K-12 Entrepreneurship Standards

competitiveness. The focus will be on business innovation, change and issues related to the United States, which has achieved its highest economic performance during the last 10 years by fostering and

competitiveness. The focus will be on business innovation, change and issues related to the United States, which has achieved its highest economic performance during the last 10 years by fostering and

Quarterly Financial and Transparency Report

Quarterly Financial and Transparency Report 3 rd Quarter 2015 SUMMARY Alloya s year-to-date net income as of September 30, 2015, was $3.9 million compared to $6.3 million for the same period in 2014. Earnings

Quarterly Financial and Transparency Report 3 rd Quarter 2015 SUMMARY Alloya s year-to-date net income as of September 30, 2015, was $3.9 million compared to $6.3 million for the same period in 2014. Earnings

Developing Your Business Plan

Developing Your Business Plan Developing a Business Plan for Trade Adjustment Assistance Kevin Klair Center for Farm Financial Management University of Minnesota Developing a Business Plan A business plan

Developing Your Business Plan Developing a Business Plan for Trade Adjustment Assistance Kevin Klair Center for Farm Financial Management University of Minnesota Developing a Business Plan A business plan

Financial Reports Balance Sheet

Financial Reports Balance Sheet It s the end of the month. The church board is looking to you to print reports that show the financial status of the church. How is that assignment going for you? Do the

Financial Reports Balance Sheet It s the end of the month. The church board is looking to you to print reports that show the financial status of the church. How is that assignment going for you? Do the

Performance Review Sample Continuing Care Community

Performance Review Sample Continuing Care Community For the period ended 06/30/2012 Provided By Perkins & Co 503.221.0336 Page 1 / 16 This report is designed to assist you in your organization's development.

Performance Review Sample Continuing Care Community For the period ended 06/30/2012 Provided By Perkins & Co 503.221.0336 Page 1 / 16 This report is designed to assist you in your organization's development.

I N T R O D U C I N G T H E MSS SPEAKERS

I N T R O D U C I N G T H E MSS SPEAKERS Your group will hit the ground running with a fresh perspective when you book an MSS Speaker for your next event. Imagine having Barry Habib, Sue Woodard or Jim

I N T R O D U C I N G T H E MSS SPEAKERS Your group will hit the ground running with a fresh perspective when you book an MSS Speaker for your next event. Imagine having Barry Habib, Sue Woodard or Jim

Nonprofit Finance Fund Cultural Data Project. Getting to Know the Financial Health Analysis (FHA) Presented by:

Presented by:") Nonprofit Finance Fund Cultural Data Project Getting to Know the Financial Health Analysis (FHA) Presented by: Rebecca Thomas Vice President Nonprofit Finance Fund Joanna Reiner Senior Specialist, Finance

Nonprofit Finance Fund Cultural Data Project Getting to Know the Financial Health Analysis (FHA) Presented by: Rebecca Thomas Vice President Nonprofit Finance Fund Joanna Reiner Senior Specialist, Finance

EVERGREEN COMMUNITY CHURCH FINANCIAL STATEMENTS YEARS ENDED DECEMBER 31, 2012 AND 2011

FINANCIAL STATEMENTS YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS REPORT 1 FINANCIAL STATEMENTS STATEMENTS OF ASSETS, LIABILITIES AND NET ASSETS MODIFIED CASH BASIS 3 STATEMENTS OF SUPPORT,

FINANCIAL STATEMENTS YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS REPORT 1 FINANCIAL STATEMENTS STATEMENTS OF ASSETS, LIABILITIES AND NET ASSETS MODIFIED CASH BASIS 3 STATEMENTS OF SUPPORT,

PLANNING FOR SUCCESS P a g e 0

PLANNING FOR SUCCESS P a g e 0 PLANNING FOR SUCCESS P a g e 1 Planning for Success: Your Guide to Preparing a Business and Marketing Plan This guide is designed to help you put together a comprehensive,

PLANNING FOR SUCCESS P a g e 0 PLANNING FOR SUCCESS P a g e 1 Planning for Success: Your Guide to Preparing a Business and Marketing Plan This guide is designed to help you put together a comprehensive,

Financial Statements June 30, 2014 Habitat for Humanity of Utah County

Financial Statements Habitat for Humanity of Utah County www.eidebailly.com Table of Contents Independent Auditor s Report... 1 Financial Statements Statement of Financial Position... 2 Statement of Activities...

Financial Statements Habitat for Humanity of Utah County www.eidebailly.com Table of Contents Independent Auditor s Report... 1 Financial Statements Statement of Financial Position... 2 Statement of Activities...

Director, Office of Health IT and e Health; State Government HIT Coordinator. Deputy Director, Office of Health IT and e Health

Assignment Location: Minnesota Department of Health St. Paul, Minnesota Primary Mentor: Secondary Mentor: Martin LaVenture, PhD, MPH, FACMI Director, Office of Health IT and e Health; State Government

Assignment Location: Minnesota Department of Health St. Paul, Minnesota Primary Mentor: Secondary Mentor: Martin LaVenture, PhD, MPH, FACMI Director, Office of Health IT and e Health; State Government

Management Consulting Fund

The application process for all grant programs is now ONLINE ONLY 4:30 p.m. Deadline Management Consulting Fund Funds of up to $1,500 for small management consulting projects designed to strengthen the

The application process for all grant programs is now ONLINE ONLY 4:30 p.m. Deadline Management Consulting Fund Funds of up to $1,500 for small management consulting projects designed to strengthen the

Strategic Planning as an Iterative and Integrated Process NACUBO Conference

Strategic Planning as an Iterative and Integrated Process NACUBO Conference September 22, 2014 2014 Plan A Advisors Session Goals Through a case study of the Strategic Planning Process conducted with Pratt

Strategic Planning as an Iterative and Integrated Process NACUBO Conference September 22, 2014 2014 Plan A Advisors Session Goals Through a case study of the Strategic Planning Process conducted with Pratt

3205 Willow Lane Harrisburg, PA 17110-9343

(717) 576-5984 www.advanceyourmission.net 3205 Willow Lane Harrisburg, PA 17110-9343 ADVISORY NOTES June 2010 INTRODUCTION Many nonprofit organizations planning a facilities project will need to secure

(717) 576-5984 www.advanceyourmission.net 3205 Willow Lane Harrisburg, PA 17110-9343 ADVISORY NOTES June 2010 INTRODUCTION Many nonprofit organizations planning a facilities project will need to secure

Contribution 787 1,368 1,813 983. Taxable cash flow 682 1,253 1,688 858 Tax liabilities (205) (376) (506) (257)

(376) (506) (257)") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2012 Answers 1 (a) Calculation of net present value (NPV) As nominal after-tax cash flows are to be discounted, the nominal

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2012 Answers 1 (a) Calculation of net present value (NPV) As nominal after-tax cash flows are to be discounted, the nominal

Assessing Organizational Readiness for Fundraising From Non-Grant Sources

Assessing Organizational Readiness for Fundraising From Non-Grant Sources While many organizations have a history of successful fundraising from grant sources, they often seek to diversify their funding

Assessing Organizational Readiness for Fundraising From Non-Grant Sources While many organizations have a history of successful fundraising from grant sources, they often seek to diversify their funding

CENTERPIECE FOCUS ON: THE BALANCE SHEET

CENTERPIECE FOCUS ON: THE BALANCE SHEET U SING THE B ALANCE S HEET TO D IAGNOSE Y OUR T HEATRE S F INANCIAL H EALTH BY PATRICIA EGAN & NANCY SASSER OF COOL SPRING ANALYTICS Theatres across the country

CENTERPIECE FOCUS ON: THE BALANCE SHEET U SING THE B ALANCE S HEET TO D IAGNOSE Y OUR T HEATRE S F INANCIAL H EALTH BY PATRICIA EGAN & NANCY SASSER OF COOL SPRING ANALYTICS Theatres across the country

Financial Planning for Fishing Families

Financial Planning for Fishing Families A Financial Planning Workshop for Fishing Families Trade Adjustment Assistance Program -- 2011 Dedicated to helping Maine small business succeed. Maine Small Business

Financial Planning for Fishing Families A Financial Planning Workshop for Fishing Families Trade Adjustment Assistance Program -- 2011 Dedicated to helping Maine small business succeed. Maine Small Business

Liquidity Cash Flow Planning and Stress Testing Model. User s Guide. Version 2.1

Liquidity Cash Flow Planning and Stress Testing Model User s Guide Version 2.1 Table of Contents INTRODUCTION...1 MODEL STRUCTURE...2 BASE CASE ASSUMPTIONS...3 KEY LIQUIDITY VARIABLES...3 WORKSHEET MAINTENANCE...3

Liquidity Cash Flow Planning and Stress Testing Model User s Guide Version 2.1 Table of Contents INTRODUCTION...1 MODEL STRUCTURE...2 BASE CASE ASSUMPTIONS...3 KEY LIQUIDITY VARIABLES...3 WORKSHEET MAINTENANCE...3

CITY OF ALEXANDRIA, VIRGINIA FINANCIAL MANAGEMENT SELF-ASSESSMENT USING STANDARD AND POORS RATING CRITERIA. June 2009

CITY OF ALEXANDRIA, VIRGINIA FINANCIAL MANAGEMENT SELF-ASSESSMENT USING STANDARD AND POORS RATING CRITERIA June 2009 Revenue and Expenditure Assumptions Are the organization s financial assumptions and

CITY OF ALEXANDRIA, VIRGINIA FINANCIAL MANAGEMENT SELF-ASSESSMENT USING STANDARD AND POORS RATING CRITERIA June 2009 Revenue and Expenditure Assumptions Are the organization s financial assumptions and

MINNESOTA COUNCIL OF CHURCHES MINNEAPOLIS, MINNESOTA FINANCIAL STATEMENTS DECEMBER 31, 2012 AND 2011

MINNEAPOLIS, MINNESOTA FINANCIAL STATEMENTS DECEMBER 31, 2012 AND 2011 TABLE OF CONTENTS Page INDEPENDENT AUDITOR S REPORT 1-2 FINANCIAL STATEMENTS Statements of Financial Position 3-4 Statements of Activities

MINNEAPOLIS, MINNESOTA FINANCIAL STATEMENTS DECEMBER 31, 2012 AND 2011 TABLE OF CONTENTS Page INDEPENDENT AUDITOR S REPORT 1-2 FINANCIAL STATEMENTS Statements of Financial Position 3-4 Statements of Activities

Taking the Guesswork Out of Vendor Selection: Minnesota s Charter School Consultant Survey

PROMISING PRACTICE Taking the Guesswork Out of Vendor Selection: Minnesota s Charter School Consultant Survey Center for School Change, Hubert H. Humphrey Institute of Public Affairs, University of Minnesota

PROMISING PRACTICE Taking the Guesswork Out of Vendor Selection: Minnesota s Charter School Consultant Survey Center for School Change, Hubert H. Humphrey Institute of Public Affairs, University of Minnesota

SMALL BUSINESS OWNER S HANDBOOK

SMALL BUSINESS OWNER S HANDBOOK PART II: FINANCIAL PLANNING FOR SMALL BUSINESSES Introduction Financial Planning Methods of Financing Your Business Other Types of Funds & Financing How to Approach Lenders

SMALL BUSINESS OWNER S HANDBOOK PART II: FINANCIAL PLANNING FOR SMALL BUSINESSES Introduction Financial Planning Methods of Financing Your Business Other Types of Funds & Financing How to Approach Lenders

YOUR SMALL BUSINESS SCORECARD. Your Small Business Scorecard. David Oetken, MBA CPM

Your Small Business Scorecard David Oetken, MBA CPM 1 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting ideas, deliver desirable products or services,

Your Small Business Scorecard David Oetken, MBA CPM 1 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting ideas, deliver desirable products or services,

Quarterly Financial and Transparency Report

Quarterly Financial and Transparency Report 1 st Quarter 2015 SUMMARY Alloya s net income for the quarter ended March 31, 2015 was $1.2 million compared to $2.1 million for the first quarter of 2014. Earnings

Quarterly Financial and Transparency Report 1 st Quarter 2015 SUMMARY Alloya s net income for the quarter ended March 31, 2015 was $1.2 million compared to $2.1 million for the first quarter of 2014. Earnings

XIV. Accounting for Gifts, Endowment Earnings and Other Projects

XIV. Accounting for Gifts, Endowment Earnings and Other Projects A. Overview: RIT receives gifts and other income to support the operations of the University. Gifts that are restricted for use by the donor

XIV. Accounting for Gifts, Endowment Earnings and Other Projects A. Overview: RIT receives gifts and other income to support the operations of the University. Gifts that are restricted for use by the donor

BOISE RESCUE MISSION, INC. (a nonprofit organization) CONSOLIDATED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION

CONSOLIDATED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION") (a nonprofit organization) CONSOLIDATED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION Years Ended September 30, 2014 and 2013 TABLE OF CONTENTS Page Independent Auditors Report...3 Consolidated Statements

(a nonprofit organization) CONSOLIDATED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION Years Ended September 30, 2014 and 2013 TABLE OF CONTENTS Page Independent Auditors Report...3 Consolidated Statements

Liquidity and Working Capital Analysis

8 Lecture Liquidity and Working Capital Analysis Liquidity and Working Capital Operating Activity Additional Liquidity Measures Current assets Current Liabilities Working Capital Current ratio Cash-based

8 Lecture Liquidity and Working Capital Analysis Liquidity and Working Capital Operating Activity Additional Liquidity Measures Current assets Current Liabilities Working Capital Current ratio Cash-based

Using dashboard reports. Selecting KPIs

WHITE PAPER When you have accurate, timely and actionable financial information, you re able to make smarter business decisions. Key Performance Indicators (KPIs) can provide a clear picture of your company

WHITE PAPER When you have accurate, timely and actionable financial information, you re able to make smarter business decisions. Key Performance Indicators (KPIs) can provide a clear picture of your company

Fiscal Year 2015 Integrated Financial Plan. 2015 Operating Plan 2015 Capital Plan 2015 Financing Plan

Fiscal Year Integrated Financial Operating Capital Financing EXECUTIVE SUMMARY Despite the ongoing efforts A Deep Financial Hole (as of September 30, ) of the Postal Service to Liabilities exceed assets

Fiscal Year Integrated Financial Operating Capital Financing EXECUTIVE SUMMARY Despite the ongoing efforts A Deep Financial Hole (as of September 30, ) of the Postal Service to Liabilities exceed assets

Child Care Center Facility Development Checklists

BUILDING CHILD CARE Child Care Center Facility Development Checklists When planning to expand, renovate, build or purchase a child care center, it is essential to think through the entire process by breaking

BUILDING CHILD CARE Child Care Center Facility Development Checklists When planning to expand, renovate, build or purchase a child care center, it is essential to think through the entire process by breaking

FINANCIAL MANAGEMENT OF ALL VOLUNTEER ORGANIZATIONS (AVO)

") FINANCIAL MANAGEMENT OF ALL VOLUNTEER ORGANIZATIONS (AVO) AACRAO Leadership Meeting, December 1, 2012 Presentation Agenda Nonprofit Financial Outlook Governance Role Financial Analysis Tax Reporting Risk

FINANCIAL MANAGEMENT OF ALL VOLUNTEER ORGANIZATIONS (AVO) AACRAO Leadership Meeting, December 1, 2012 Presentation Agenda Nonprofit Financial Outlook Governance Role Financial Analysis Tax Reporting Risk

The Income Statement and Statement of Functional Expense. Barbara Clemenson, CPA, CFRE

The Income Statement and Statement of Functional Expense Barbara Clemenson, CPA, CFRE Outline Review of the Income Statement The 990 Income Statement Numberless Analysis Statement of Functional Expenses

The Income Statement and Statement of Functional Expense Barbara Clemenson, CPA, CFRE Outline Review of the Income Statement The 990 Income Statement Numberless Analysis Statement of Functional Expenses

Application Questions for Bush Foundation Community Innovation Grant

Application Questions for Bush Foundation Community Innovation Grant PROJECT NARRATIVE 1. Provide a two sentence summary of the proposed work (50 words max) E Democracy s Engagement Tech initiative, led

Application Questions for Bush Foundation Community Innovation Grant PROJECT NARRATIVE 1. Provide a two sentence summary of the proposed work (50 words max) E Democracy s Engagement Tech initiative, led

HOW TO LAND AN SBA Loan

HOW TO LAND AN SBA Loan by Ron Box, CPA/CITP/CFF With all of the uncertainty around maintaining a predictable flow of capital to businesses, a commercial loan provided by a bank but guaranteed by the federal

HOW TO LAND AN SBA Loan by Ron Box, CPA/CITP/CFF With all of the uncertainty around maintaining a predictable flow of capital to businesses, a commercial loan provided by a bank but guaranteed by the federal

Nonprofit Finance Fund. Preparing Your Organization to Apply for a Loan. Anne Dyjak Chief Credit Officer & Vice President Nonprofit Finance Fund

Nonprofit Finance Fund Preparing Your Organization to Apply for a Loan Anne Dyjak Chief Credit Officer & Vice President Nonprofit Finance Fund June 2010 Agenda Introductions Considering a Loan? What types

Nonprofit Finance Fund Preparing Your Organization to Apply for a Loan Anne Dyjak Chief Credit Officer & Vice President Nonprofit Finance Fund June 2010 Agenda Introductions Considering a Loan? What types

Municipal Clean Audit Efficiency Series Effective Cash Management

Municipal Clean Audit Efficiency Series Effective Cash Management Introduction The fi nancial performance of the South African local government has recently come under signifi cant scrutiny. This has led

Municipal Clean Audit Efficiency Series Effective Cash Management Introduction The fi nancial performance of the South African local government has recently come under signifi cant scrutiny. This has led

Case Western Reserve University Consolidated Financial Statements for the Year Ending June 30, 2001

Contents Report of Independent Accountants 1 Part 1 Consolidated Financial Statements Consolidated Balance Sheet 2 Consolidated Statement of Activities 3 Consolidated Statement of Cash Flows 4 Part 2 Summary

Contents Report of Independent Accountants 1 Part 1 Consolidated Financial Statements Consolidated Balance Sheet 2 Consolidated Statement of Activities 3 Consolidated Statement of Cash Flows 4 Part 2 Summary

Fiscal Year 2015 Integrated Financial Plan

Fiscal Year Integrated Financial Operating Capital Financing Integrated Financial EXECUTIVE SUMMARY Unaudited - A Deep Financial Hole (as of September 30, 2014) Liabilities exceed assets by approximately

Fiscal Year Integrated Financial Operating Capital Financing Integrated Financial EXECUTIVE SUMMARY Unaudited - A Deep Financial Hole (as of September 30, 2014) Liabilities exceed assets by approximately

FINANCIAL EDUCATION AND CAPABILITY MEASUREMENT TOOLS - ADULT

FINANCIAL EDUCATION AND CAPABILITY MEASUREMENT TOOLS - ADULT The Success Measures Financial Education and Capability Tools document changes in consumers financial attitudes,behaviors, and resilience resulting

FINANCIAL EDUCATION AND CAPABILITY MEASUREMENT TOOLS - ADULT The Success Measures Financial Education and Capability Tools document changes in consumers financial attitudes,behaviors, and resilience resulting

Policies, Procedures and Guidelines

Policies, Procedures and Guidelines Complete Policy Title: Debt Management Policy Approved by: Board of Governors Policy Number (if applicable): n/a Date of Most Recent Approval: April 16, 2015 Date of

Policies, Procedures and Guidelines Complete Policy Title: Debt Management Policy Approved by: Board of Governors Policy Number (if applicable): n/a Date of Most Recent Approval: April 16, 2015 Date of

Financial Statements. Canadian Baptist Ministries December 31, 2014

Financial Statements Canadian Baptist Ministries INDEPENDENT AUDITORS' REPORT To the Members of Canadian Baptist Ministries We have audited the accompanying financial statements of Canadian Baptist Ministries,

Financial Statements Canadian Baptist Ministries INDEPENDENT AUDITORS' REPORT To the Members of Canadian Baptist Ministries We have audited the accompanying financial statements of Canadian Baptist Ministries,

THE DO S & DON TS OF ENDOWMENTS

THE DO S & DON TS OF ENDOWMENTS Presented by David Dahlin, CEO, Colorado Springs Fine Arts Center Cari Karns, Development Director, Colorado Springs Fine Arts Center Steven Sauer, CPA, Senior Manager,

THE DO S & DON TS OF ENDOWMENTS Presented by David Dahlin, CEO, Colorado Springs Fine Arts Center Cari Karns, Development Director, Colorado Springs Fine Arts Center Steven Sauer, CPA, Senior Manager,

Income, Expenses and Budget module

Income, Expenses and Budget module Trainer s introduction The skills to control your personal income, expenses and budget are the most basic tools that people need in their financial toolkit. But many

Income, Expenses and Budget module Trainer s introduction The skills to control your personal income, expenses and budget are the most basic tools that people need in their financial toolkit. But many

A. To strategically utilize debt to fund mission critical projects;

Policy concerning: page 1 of 5 DEBT POLICY I. GOALS AND OBJECTIVES Teaching and learning form the core of Westfield State University s institutional mission. The university s strategic plan identifies

Policy concerning: page 1 of 5 DEBT POLICY I. GOALS AND OBJECTIVES Teaching and learning form the core of Westfield State University s institutional mission. The university s strategic plan identifies

City Utilities Strategic Plan November 26, 2013

November 26, 2013 TABLE OF CONTENTS Purpose... 3 Strategic Planning Task Force... 4 Strategic Managment System... 5 Strategic Plan Development Process... 9 Key Terms and Definitions... 10 City Utilities

November 26, 2013 TABLE OF CONTENTS Purpose... 3 Strategic Planning Task Force... 4 Strategic Managment System... 5 Strategic Plan Development Process... 9 Key Terms and Definitions... 10 City Utilities

COMMON APPLICATION FOR PRO BONO SERVICES

COMMON APPLICATION FOR PRO BONO SERVICES Looking for pro bono? You can use this document to describe your need for pro bono to a potential provider: We ve started with the basic questions that most providers

COMMON APPLICATION FOR PRO BONO SERVICES Looking for pro bono? You can use this document to describe your need for pro bono to a potential provider: We ve started with the basic questions that most providers

Local Government Operational Guidelines. Number 18 June 2013. Financial Ratios

Local Government Operational Guidelines Number 18 June 2013 Page 2 of 20 1. Introduction This guideline is intended to provide a clear explanation of each ratio required to be included in the annual financial

Local Government Operational Guidelines Number 18 June 2013 Page 2 of 20 1. Introduction This guideline is intended to provide a clear explanation of each ratio required to be included in the annual financial

School of Oriental and African Studies Financial Strategy 2012-2017

School of Oriental and African Studies Financial Strategy 2012-2017 1. Introduction This document sets out the School s Financial Strategy for the period 2012-2017. The Financial Strategy examines The

School of Oriental and African Studies Financial Strategy 2012-2017 1. Introduction This document sets out the School s Financial Strategy for the period 2012-2017. The Financial Strategy examines The

SAFE Credit Underwriting Guidelines for Non-Profit Lending. Organization Type: NON-PROFIT ORGANIZATIONS. Bridge Loan Guidelines.

Introduction The Credit Underwriting Guidelines (CUG) manual is designed for use with products delivered to faith-based and non-profit organizations. The guidelines herein govern the granting of credit

Introduction The Credit Underwriting Guidelines (CUG) manual is designed for use with products delivered to faith-based and non-profit organizations. The guidelines herein govern the granting of credit

CLUB RATIO PRIVATE ANALYSIS AND FINANCIAL OPERATIONS HEALTH OF THE CLUB TRACKING THE FINANCIAL WHY CLUBS MONITOR RATIOS LIQUIDITY RATIOS

FINANCIAL RATIO ANALYSIS AND PRIVATE CLUB OPERATIONS TRACKING THE FINANCIAL HEALTH OF THE CLUB B Y P H I L I P N E W M A N Private clubs are mission driven serving members is the primary goal. Accordingly,

FINANCIAL RATIO ANALYSIS AND PRIVATE CLUB OPERATIONS TRACKING THE FINANCIAL HEALTH OF THE CLUB B Y P H I L I P N E W M A N Private clubs are mission driven serving members is the primary goal. Accordingly,

services NEW ZEALAND INSTITUTE OF ARCHITECTS INCORPORATED GUIDE TO ARCHITECTS SERVICES

1 e services NEW ZEALAND INSTITUTE OF ARCHITECTS INCORPORATED GUIDE TO ARCHITECTS SERVICES 01 contents 02 guide to architects services 03 architecture in new zealand 04 an architect s skills 05 an architect

1 e services NEW ZEALAND INSTITUTE OF ARCHITECTS INCORPORATED GUIDE TO ARCHITECTS SERVICES 01 contents 02 guide to architects services 03 architecture in new zealand 04 an architect s skills 05 an architect

COALITION PROVISIONAL AUTHORITY ORDER NUMBER 95 FINANCIAL MANAGEMENT LAW AND PUBLIC DEBT LAW

COALITION PROVISIONAL AUTHORITY ORDER NUMBER 95 FINANCIAL MANAGEMENT LAW AND PUBLIC DEBT LAW Pursuant to my authority as Administrator of the Coalition Provisional Authority (CPA) and under the laws and

COALITION PROVISIONAL AUTHORITY ORDER NUMBER 95 FINANCIAL MANAGEMENT LAW AND PUBLIC DEBT LAW Pursuant to my authority as Administrator of the Coalition Provisional Authority (CPA) and under the laws and

Financial Analysis 201: Assessing Nonprofit Financial Health

Nonprofit Finance Fund Financial Analysis 201: Assessing Nonprofit Financial Health Presented to Presented by David Greco, Vice President Nonprofit Finance Fund This presentation is generously sponsored

Nonprofit Finance Fund Financial Analysis 201: Assessing Nonprofit Financial Health Presented to Presented by David Greco, Vice President Nonprofit Finance Fund This presentation is generously sponsored

FINANCIAL MANAGEMENT MODEL

THE URBAN INSTITUTE FINANCIAL MANAGEMENT MODEL FOR LOCAL GOVERNMENTS I. INTRODUCTION The brochure is meant for local governments: mayors, city secretaries, financial department heads and heads of other

THE URBAN INSTITUTE FINANCIAL MANAGEMENT MODEL FOR LOCAL GOVERNMENTS I. INTRODUCTION The brochure is meant for local governments: mayors, city secretaries, financial department heads and heads of other

Opportunity. for Greater Relevance LEVERAGING ENTERPRISE RISK MANAGEMENT: By Janice M. Abraham, Robert Baird, and Frank Neugebauer

LEVERAGING ENTERPRISE RISK MANAGEMENT: Opportunity for Greater Relevance By Janice M. Abraham, Robert Baird, and Frank Neugebauer Enterprise Risk Management (ERM) gained a foothold in higher education

LEVERAGING ENTERPRISE RISK MANAGEMENT: Opportunity for Greater Relevance By Janice M. Abraham, Robert Baird, and Frank Neugebauer Enterprise Risk Management (ERM) gained a foothold in higher education

2009 Nonprofit Finance Fund. Cash Flow Webinar. This webinar was made possible with funding from MetLife Foundation. Presented by

Nonprofit Finance Fund Cash Flow Webinar Presented by Carolyn Hubbard Analyst Nonprofit Finance Fund Philip Rosenbloom Associate Nonprofit Finance Fund October 13, 2009 This webinar was made possible with

Nonprofit Finance Fund Cash Flow Webinar Presented by Carolyn Hubbard Analyst Nonprofit Finance Fund Philip Rosenbloom Associate Nonprofit Finance Fund October 13, 2009 This webinar was made possible with

FCMAT Chief Executive Officer Joel D. Montero

About FCMAT The Fiscal Crisis and Management Assistance Team (FCMAT) was created by legislation in 1992 as an independent and external state agency. FCMAT s mission is to provide proactive and preventive

About FCMAT The Fiscal Crisis and Management Assistance Team (FCMAT) was created by legislation in 1992 as an independent and external state agency. FCMAT s mission is to provide proactive and preventive

pm4dev, 2007 management for development series Project Management Organizational Structures PROJECT MANAGEMENT FOR DEVELOPMENT ORGANIZATIONS

pm4dev, 2007 management for development series Project Management Organizational Structures PROJECT MANAGEMENT FOR DEVELOPMENT ORGANIZATIONS PROJECT MANAGEMENT FOR DEVELOPMENT ORGANIZATIONS A methodology

pm4dev, 2007 management for development series Project Management Organizational Structures PROJECT MANAGEMENT FOR DEVELOPMENT ORGANIZATIONS PROJECT MANAGEMENT FOR DEVELOPMENT ORGANIZATIONS A methodology

Short-term Financial Planning and Management.

Short-term Financial Planning and Management. This topic discusses the fundamentals of short-term nancial management; the analysis of decisions involving cash ows which occur within a year or less. These

Short-term Financial Planning and Management. This topic discusses the fundamentals of short-term nancial management; the analysis of decisions involving cash ows which occur within a year or less. These

Fiduciary Asset Management. A Discretionary Investment Management Solution

Fiduciary Asset Management A Discretionary Investment Management Solution 01 / MORGAN STANLEY The Fiduciary Asset Management program is designed to provide a customized, discretionary solution to help

Fiduciary Asset Management A Discretionary Investment Management Solution 01 / MORGAN STANLEY The Fiduciary Asset Management program is designed to provide a customized, discretionary solution to help

83. Standard 9. Financial Resources. 1. Description. 1.1. Financial stability

83. Standard 9. Financial Resources 1. Description 1.1. Financial stability Bentley University has not reported an operating deficit since it became a not-for-profit organization in 1948. Fiscal year 2012

83. Standard 9. Financial Resources 1. Description 1.1. Financial stability Bentley University has not reported an operating deficit since it became a not-for-profit organization in 1948. Fiscal year 2012

Bruce R. Butler, CFP Executive Financial Services Director Senior Vice President - Wealth Management

Bruce R. Butler, CFP Executive Financial Services Director Senior Vice President - Wealth Management 227 West Monroe Street Suite 3400, Chicago, IL 60606 312-917-7416 / MAIN 800-334-2446 / TOLL-FREE 312-648-3344

Bruce R. Butler, CFP Executive Financial Services Director Senior Vice President - Wealth Management 227 West Monroe Street Suite 3400, Chicago, IL 60606 312-917-7416 / MAIN 800-334-2446 / TOLL-FREE 312-648-3344