Promoting Individual Savings for Retirement. Comprehensive Report September 25, 2013

|

|

|

- Juniper Rogers

- 8 years ago

- Views:

Transcription

1 Promoting Individual Savings for Retirement Comprehensive Report September 25,

2 Issue Members are not able to take advantage of a recent IRS ruling which provides new options for managing savings in retirement. 2

3 2012 IRS Ruling Internal Revenue Bulletin issued February 21, Allows a member of a 401(a) defined benefit plan to annuitize tax deferred retirement savings. Allow employees to maintain a sidecar savings account within defined benefit trust fund. 3

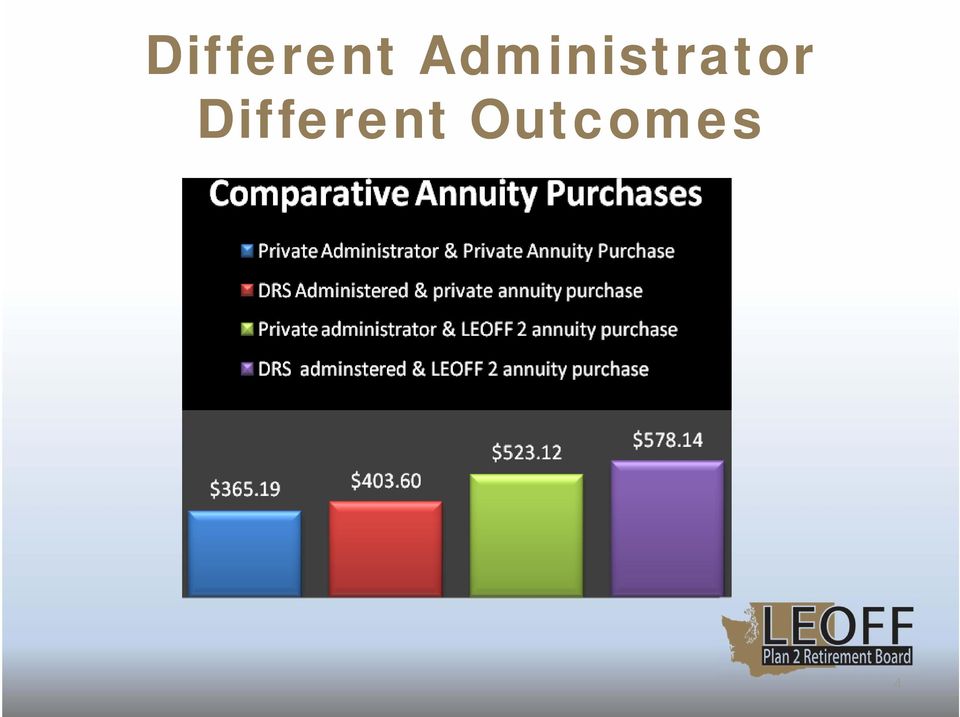

4 Different Administrator Different Outcomes 4

5 Board Option 1 Authorize LEOFF Plan 2 to annuitize rollovers of tax deferred savings. Allows members to leverage existing LEOFF Plan 2 infrastructure; Requires legislation; Requires consultation with Ice Miller. 5

6 Board Option 2 Establish a 401(a) savings plan within LEOFF 2. Would likely have administrative costs similar to the DRS Deferred Compensation Program. Preliminary research indicates it may be more restricted than 457 plan similar to the Plan 3 DC component. Requires consultation with Ice Miller. Requires legislation. 6

7 Board Option 3 Require LEOFF Employers to Offer DRS s Deferred Compensation Program to LEOFF Members. Combines 457 flexibility with low administrative fee; May need to account for existing local government contracts with private providers; Requires legislation. 7

8 Contact: Any Questions? Paul Neal Senior Legal Counsel Evergreen Park Dr, Olympia, WA PO Box Olympia, WA or

9 September 25, 2013 PROMOTING INDIVIDUAL SAVINGS FOR RETIREMENT COMPREHENSIVE REPORT By Paul Neal Senior Legal Counsel ISSUE Members are not able to take advantage of a recent IRS ruling which provides new options for managing savings in retirement. MEMBERS IMPACTED New options encouraging member s retirement savings as part of LEOFF Plan 2 would be available to all 16,805 active LEOFF Plan 2 members 1. OVERVIEW The LEOFF Plan 2 defined benefit Plan, the first leg of the three legged retirement stool, provides a defined lifetime payout that does not vary with investment return. Retirees must devise their own distribution strategy for the second leg of the stool, individual retirement savings. Members can reduce the risk of outliving their assets if they convert at least some of those assets into a lifetime annuity. LEOFF Plan 2 members may purchase an additional monthly benefit through the LEOFF Plan 2 trust fund by buying up to 5 years of additional service credit at the time retirement. Under current law, only Plan 3 members (TRS, PERS & SERS 2 ) can convert contributions to an annuity from their retirement system. Leveraging the existing LEOFF Plan 2 infrastructure to authorize accumulation of savings and/or converting that account to a monthly benefit through the LEOFF Plan 2 trust fund would provide a cost effective mechanism to encourage retirement savings. This can be particularly important for LEOFF Plan 2 members since many do not participate in social security through their employer. This report examines federal laws encouraging retirement savings, the costs of savings for retirement, different mechanisms for annuitizing retirement savings, a recent IRS ruling authorizing annuitizing retirement savings through LEOFF Plan 2, and provides options for further action. 1 Membership number as of June 30, 2011; Office of the State Actuary 2011 LEOFF Plan 2 Valuation Report. 2 Teachers Retirement System (TRS); Public Employees Retirement System (PERS); School Employees Retirement System (SERS).

10 BACKGROUND INFORMATION & POLICY ISSUES The LEOFF Plan 2 Retirement Board began studying ways to encourage increased retirement savings during the 2004 Interim. The Board recommended legislation allowing purchase of up to five years of service credit at retirement. The Legislature passed that recommendation in 2005 (HB 1269). That same year the Department of Retirement Systems (DRS) began offering the annuities through the Plan 3 programs. The Purchase of Annuity topic was studied by the Board during the 2006, 2007, 2008 and 2009 Interims reaching the Final Proposal stage in 2006, 2008 and 2009, but no legislation was recommended. The topic was deferred for joint consideration with the Select Committee on Pension Policy (SCPP) for the 2009 Interim. No further action was taken. The paradox is that investors recognize that their retirement savings will need to last longer than ever before but they aren't making plans to ensure they will actually have the money they need. There tends to be a false sense of security when it comes to Planning for retirement. We hope that the money will somehow be there when we need it but we're not taking the action required to ensure it is. This is a serious problem, and addressing it must become an urgent priority. Noel Archard, Head of BlackRock Canada. July 2013 SAVING FOR RETIREMENT Federal Law Encouraging Retirement Savings The federal tax code encourages individuals to save for, and invest in, retirement: Qualified deferred compensation plans, such as the IRS 457 plan offered through the Department of Retirement Systems (DRS) deferred compensation program, permit an individual to authorize pre tax salary deductions for deposit into a personal investment account. Many LEOFF Plan 2 employers offer these types of plans to employees. Upon separation from employment a member may leave the funds invested or select a distribution option. Members may transfer funds between government defined benefit pension Plans like LEOFF Plan 2 and deferred compensation accounts such as 457, 403(b), and 401(k) Plans. This helps members manage retirement savings as they change employers. Purchase of up to five years of service credit or air time was authorized in the Federal Pension Protection Act. Promoting Individual Savings For Retirement Page 2

11 A recent IRS revenue ruling 3 allows members with funds in a deferred compensation account maintained by an employer to roll the funds over into their defined benefit plan and convert those funds to an annuity from the defined benefit Plan. Using these federal provisions, some state and local government pension plans allow member fund transfers, including funds from tax deferred accounts, into the primary defined benefit plans to purchase additional service credit or an annuity. THE COST OF SAVING DEFERRED COMPENSATION FEES DRS operates a deferred compensation program under 26 U.S.C. 457, commonly called a "457 Plan". Washington s political subdivisions may participate in DRS s 457 Plan, or use another administrator, such as ICMA RC. Administrative fees vary significantly. Comparing private administrator fees to DRS s annual.13% fee can be challenging since private administrators tend to use variable fee schedules rather than the flat fee charged by DRS, as demonstrated by the fee comparison table included as Appendix A. The average net annual fee of the private 457 plan administrators examined in Appendix A is 1.29%, nearly 10 times the.13% charged by DRS. DRS s lower fees facilitate a larger accumulation from the same member contributions 4 : Effect of Fees on Account Balance $100,001 $90,484 Private Administrator Accumulation Figure 1 3 Internal Revenue Bulletin ; issued February 21, The comparison assumes $3,602 per year contribution for 15 years, earning interest at LEOFF PLAN 2 s assumed rate of 7.5%, less annual fees. Promoting Individual Savings For Retirement Page 3

12 ANNUITIZING ASSETS Annuities can convert retirement savings into a guaranteed monthly income (this process is called annuitization) for a specified period of time. A life annuity provides that income for the member s lifespan in exchange for a lump sum dollar amount paid up front. Deferred compensation plans do not normally allow for the distribution of assets in the form of an annuity directly from the fund. LEOFF Plan 2 members wishing to annuitize their retirement savings must purchase the annuity through an insurance company. The price/value of the annuity depends in part upon the features selected by the purchaser. The terms and conditions of an annuity contract specify features such as whether the annuity will be for a single life or a joint annuity (like a survivor benefit feature), the payment frequency, adjustments for cost of living, and death provisions. Different methods for annuitizing assets are listed below, though not all are currently available to LEOFF Plan 2 members. Trust Fund Annuity Purchase TRS Plan 3, SERS Plan 3, and PERS Plan 3 members and survivors may convert some or all of the funds from their Plan 3 member account to a life annuity, RCW The features and options of the Plan 3 annuities administered by DRS are detailed in Appendix B. This option is not available to LEOFF Plan 2 members. DRS calculates the annuity that can be purchased for a given lump sum using an age based actuarial table to compute the monthly benefit per $1.00 of accumulation for defined benefits. There is no limit on the amount of funds in the member account that can be converted to an annuity. RCW also allows TRS Plan 1, 2 and 3 members to purchase additional benefits through a member reserve contribution which is actuarially converted to a monthly benefit at the time of retirement. The statute was passed to provide teachers with out of state service credit a mechanism for transferring contributions from a prior system into TRS 5. Service Credit Purchase LEOFF Plan 2 members can annuitize retirement savings by purchasing up to five years of additional service credit at the time of retirement. To purchase service credit under this option the member pays the actuarial present value of the resulting increase in the member's benefit. A member may pay all or part of the cost of the additional service credit with an eligible transfer from a qualified retirement plan. For more information on the history and methodology for calculating service credit purchases, see Appendix C. 5 See Laws of 1991 c ] Promoting Individual Savings For Retirement Page 4

13 The federal 5 year air time limit works out to a maximum of $86,484 that could be converted to a monthly benefit by the average LEOFF Plan 2 member 6, see Appendix C. This is a key difference between a Plan 3 annuity conversion and a service credit purchase: the Plan 3 conversion does not have a maximum amount limit. Commercial Market Annuity Retirement savings can be annuitized by purchasing an annuity policy through insurance agents, financial planners, banks and life insurance carriers. However, only life insurance companies issue policies. Generally, commercial market annuities do not offer all the same features as the Plan 3 trust fund annuity and do not provide as favorable a payout. A primary reason for the payout difference is the different interest rate used to calculate the value of the annuity. Private insurers use a lower interest rate, due in part to the inclusion of a reasonable profit: [A] private insurer will provide the annuity based on an interest rate of about 4 percent, whereas DRS will provide the annuity based on an interest rate of about 8%. 7. The interest rate differential drives a significant difference in payout amounts between private annuity contracts and contributions annuitized through the trust fund. Five different insurance companies quoted the monthly annuity with a 3% annual COLA they would provide the average LEOFF Plan 2 retiree 6 for $100,000: Insurance Company Quote American General $389 Aviva $402 Fidelity & Guaranty Life $421 Genworth Life Insurance $406 Integrity Life Insurance $400 Average $404 If that same average LEOFF Plan 2 member were able to leverage the institutional advantages of the retirement system by annuitizing $100,000 within the LEOFF Plan 2 system, the payout would be $ That s a 43% increase over the average commercial quote, or $174 more per month for life. 6 Age 56 with 17 years of service credit and a final average salary of $5000 per month State Actuary 2010 fiscal note on the Board s purchase of annuity proposal. 8 $100,000 x (conversion factor from DRS table for 56 year old LEOFF member) = $ monthly life annuity Promoting Individual Savings For Retirement Page 5

14 The chart below uses the 15 year accumulations calculated in figure 1 and estimates the annuity those accumulations would purchase from either an insurance company or the LEOFF Plan 2 trust fund. Figure 2 Current state law does not allow annuitization of retirement savings through the LEOFF Plan 2 trust fund. A recent IRS ruling gives the green light to such a program. NEWLY AVAILABLE ALTERNATIVE: ANNUITIZATION THROUGH 401(A) PLAN Federal tax law allows public defined benefit plans to add a member savings account within the plan, sometimes referred to as a companion account or sidecar. Contributions to the employee savings account may be made by the employer or the employee and may be either pre tax or after tax depending on plan design. Under the recent IRS ruling cited above, a retirement savings account can be annuitized within the 401(a) defined benefit plan to obtain an additional monthly benefit paid through the trust fund. This can be done either through a employee savings account administered within the 401(a) plan or by rolling over retirement savings from another plan such as a 457 plan. A sidecar plan administered through LEOFF Plan 2 could leverage the institutional advantages available to active members as participants in an existing state administered Plan. Those advantages include the lower fees charged by DRS to administer the savings plan, and the more favorable annuity payout when purchased through the existing LEOFF Plan 2 trust fund. Promoting Individual Savings For Retirement Page 6

15 Potential Risks The purchase of an annuity through the LEOFF Plan 2 trust fund would not have a cost to the system 9 under current actuarial assumptions. There is, however, a potential risk to the fund if those assumptions change or actual experience falls below assumed levels. When an annuity is purchased, the member locks in the actuarial assumptions in place at that time. A subsequent change in assumptions may knock the annuity out of actuarial equivalency. For instance, the Actuary s 2010 fiscal note assumed a trust fund annuity would be calculated using the fund s 8% interest assumption. The Board has since reduced that assumption to 7.5%. An annuity locked in with an 8% interest assumption would be too high under a 7.5% assumption, causing a $12,980 actuarial loss to the fund 9. POLICY OPTIONS The specifics of options available to the Board are in many ways a function of federal tax laws. DRS has received some guidance from the law firm of Ice Miller as of this writing. The LEOFF Plan 2 Board staff had additional questions which are still pending at this time. The options presented below, while accurate in broad strokes, may have to be modified in subsequent presentations depending on future tax law guidance. Additionally, option 1 could be combined with either option 2 or option 3. Option 1: Propose Legislation authorizing LEOFF Plan 2 to accept roll overs of tax deferred savings and annuitize those amounts through the plan upon retirement. Under this option the Board would direct staff to develop legislation authorizing DRS to accept roll overs from LEOFF Plan 2 members for annuitization at the time of retirement. Further guidance is required to determine what types of roll overs are allowable under federal tax laws and what limitations, if any, there are on annuitization of rolled over amounts. Option 2: Propose Legislation establishing a 410(a) savings plan within LEOFF 2 to accept contributions from LEOFF Plan 2 members. Under this option the Board would direct staff to develop legislation establishing a sidecar savings plan within LEOFF Plan 2 that could accept member contributions for distribution following retirement. Preliminary research indicates that this vehicle would be less flexible that a 457 plan such as that administered by DRS s Deferred Compensation Program. Member contributions may be required to follow the same rules as Plan 3 contributions. A member could be required to select a rate upon enrollment. Like the Plan 3 contribution rates, once selected the rate could not be changed except upon change of employment. Voluntary member contributions, which could apparently fluctuate, would be after tax. 9 See OSA fiscal note on 2010 annuity purchase proposal, Appendix C. Promoting Individual Savings For Retirement Page 7

16 Option 3: Require LEOFF Employers to Offer DRS s Deferred Compensation Program to LEOFF Members. This option provides a more flexible plan than the 401(a) option. The Board would propose legislation requiring all LEOFF Plan 2 employers to offer the state administered 457 plan. This would ensure that LEOFF 2 members can avail themselves of a plan with the lowest possible administrative fees. SUPPORTING INFORMATION Appendix A: Deferred Compensation Fee Comparison Appendix B: Plan 3 annuity purchase option features Appendix C: Service Credit Purchase history and example Appendix D: OSA draft fiscal note Promoting Individual Savings For Retirement Page 8

17 Appendix A DEFERRED COMPENSATION FEE ANALYSIS An approximation of annual fees for private administration of a 457 deferred compensation plan was derived by working from a table developed by The City of Duluth in 2013 to allow employees to compare costs of 4 different 457 Plan administrator. Fees were highly variable. Board staff averaged the fees of each provider and then averaged those to derive a net average estimated annual fee. Given the small sample and the assumptions that had to be made in averaging, this is a ball park figure provided solely for purposes of comparison. Hartford Life Deferred Compensation Plan Original data Average fee ICMA Retirement Corporation Deferred Compensation Plan Original data Minnesota State NationwideDeferred Deferred Compensation Program Compensation Plan MNDCP (Great West) Average Original data fee Average Original data fee Average fee Annual No 0 % No. 0% No 0% No. 0% Account Fees Daily Asset Based Charges bps.825 % 0.55% administration fees on all assets; additional.55% 0.10% annual administrative fee, charged only on the first $100,000.1% 0.50% annual administrative fee on all variable fund assets. 0.25%.375% 0.15% fee on assets in nonproprietary funds. in an individual account. annual administrative fee on fixed account option. Fund Operating Expenses Net fee estimate Average for all plans Varies by investment option, from 0.0% to 2.42% 1.21% Fund expenses range from 0.46% to 1.40%.93% Fund expenses range from 0.01% to 0.93%..47% Fund expenses range from 0.00% to 1.40% % 1.48%.57% 1.075% 1.29%.7% Promoting Individual Savings For Retirement Page 9

18 APPENDIX B CURRENT ANNUITY PURCHASE FEATURES The purchase of annuity currently administered by DRS through the Plan 3 programs includes the following features: WSIB Investment Program Annuity Features and Options Contract Provider Washington State Minimum Purchase Price $25,000 Annuity Payment Frequency Monthly Rescission Period 15 calendar days from date of purchase Single Life Annuity Provides regular payment for as long as annuitant lives. Automatic 3% Annual Cost of Living Adjustment (COLA) Conversion option to Joint Life Annuity Balance Refund Joint Life Annuity Provides regular payment for as long as member or joint annuitant is alive. Joint annuitant survivorship options: 100%, 66 2/3%, or 50% Automatic 3% Annual COLA Monthly payment pops up to Single Life Annuity amount if joint annuitant predeceases member. Balance Refund Annuitant The member/owner who purchases the annuity; the payee who receives lifetime monthly payments. Balance Refund Any remaining balance equal to the original purchase price minus the total of all annuity payments made to the single or joint annuitants, may be refunded to the specified beneficiary. Conversion Option If a single life annuity is purchased and then a subsequent marriage occurs, a one time opportunity is available to convert to a joint life annuity with the new spouse as the joint annuitant. If a joint annuity is purchased with someone other than a spouse named as the joint annuitant, the annuity may be converted to a single life annuity after payments have begun. Joint Annuitant The person designated to receive an ongoing payment in the event of the annuitant s death. Pop up An increase from a joint annuity payment amount to the full single life annuity amount if the annuitant outlives the joint annuitant. Rescission Period A period of time (typically 7 to 15 days) during which the terms of the contract may be canceled or altered Promoting Individual Savings For Retirement Page 10

Conversion option to Joint Life Annuity Balance Refund Joint Life Annuity Provides regular payment for as long as member or joint annuitant is")

19 APPENDIX C SERVICE CREDIT PURCHASE Since 2005 the inception of the service credit purchase of air time benefit through August of 2007, 15 service credit purchase billings have been requested from DRS and paid in full. The average cost of all fifteen billings was $103,045. The average benefit increase from the fifteen billings was $597 per month. The average break even point is just over 14 years, or age 69. A five year service credit purchase by an average LEOFF Plan 2 retiree who, at the time of retirement, is 56 with 17 years of service, and a monthly final average salary of $5,000 is detailed below: Service Credit Purchase Calculation 1. Calculate Base Benefit: 2% 17 YOS $5,000 = $1,700 per month 2. Add 5 Years Of Air Time : 2% 22 YOS $5,000 = $2,200 per month 3. Calculate Increase in Monthly Benefit from Additional Service Credit: $2,200 $1,700 = $500 increase per month 4. Calculate Service Credit Purchase Cost: $ = $86, The factor for the Monthly benefit per $1.00 of accumulation for defined benefit Plans for an age 56 LEOFF Plan 2 member from WAC Promoting Individual Savings For Retirement Page 11

20 APPENDIX D OSA FISCAL NOTE OF 2010 ANNUITY PURCHASE PROPOSAL Attached Separately Promoting Individual Savings For Retirement Page 12

Select Committee on Pension Policy I s s u e P a p e r November 18, 2014. Annuity Purchase. Background. What Is An Annuity?

Issue In Brief Members of certain plans in the state s retirement systems currently have the option to purchase an expanded actuarially equivalent annuity benefit at retirement. Should an expanded annuity

Issue In Brief Members of certain plans in the state s retirement systems currently have the option to purchase an expanded actuarially equivalent annuity benefit at retirement. Should an expanded annuity

Teachers Retirement Association. Marriage Dissolution: Dividing TRA Benefits

Teachers Retirement Association Marriage Dissolution: Dividing TRA Benefits Marriage Dissolution: Dividing TRA Benefits Preface This booklet is designed to give all parties involved in a marriage dissolution

Teachers Retirement Association Marriage Dissolution: Dividing TRA Benefits Marriage Dissolution: Dividing TRA Benefits Preface This booklet is designed to give all parties involved in a marriage dissolution

Benefits Payable upon Death

Chapter 13 Benefits Payable upon Death Active Contributing Member Retired Member Other Considerations Beneficiary Designations Taxes Additional Information Application Procedures Benefits for Part-time

Chapter 13 Benefits Payable upon Death Active Contributing Member Retired Member Other Considerations Beneficiary Designations Taxes Additional Information Application Procedures Benefits for Part-time

Retroactive Duty Related Death & Disability Benefits. Initial Consideration

Retroactive Duty Related Death & Disability Benefits Initial Consideration LEOFF Plan 2 Retirement Board May 28, 2008 Issue Description Some of the duty related death and disability pension benefits were

Retroactive Duty Related Death & Disability Benefits Initial Consideration LEOFF Plan 2 Retirement Board May 28, 2008 Issue Description Some of the duty related death and disability pension benefits were

Deferred Retirement Option Plan (DROP)

") Deferred Retirement Option Plan (DROP) Any Group G member who meets the requirements for a normal retirement may elect to participate in the DROP for up to three years. Sick leave may be used as credited

Deferred Retirement Option Plan (DROP) Any Group G member who meets the requirements for a normal retirement may elect to participate in the DROP for up to three years. Sick leave may be used as credited

Income for Life Annuity Program* Immediate Annuities for Retirement Income

Income for Life Annuity Program* Immediate Annuities for Retirement Income *ICMA-RC partners with select insurance companies that make annuities available through the Income for Life Annuity program. Participating

Income for Life Annuity Program* Immediate Annuities for Retirement Income *ICMA-RC partners with select insurance companies that make annuities available through the Income for Life Annuity program. Participating

Table of Contents. Participant Section

Table of Contents Participant Section Introduction...1 Planning Ahead...1 Distribution Making Your Choice...2 Other Considerations...5 Joint Life and Survivor Expectancy Table...7 Single Life Expectancy

Table of Contents Participant Section Introduction...1 Planning Ahead...1 Distribution Making Your Choice...2 Other Considerations...5 Joint Life and Survivor Expectancy Table...7 Single Life Expectancy

WISCONSIN BUYER S GUIDE TO FIXED DEFERRED ANNUITIES

Annuity Service Center: P.O. Box 79905, Des Moines, Iowa 50325-0905 WISCONSIN BUYER S GUIDE TO FIXED DEFERRED ANNUITIES WHAT IS AN ANNUITY? An annuity is a written contract between you and a life insurance

Annuity Service Center: P.O. Box 79905, Des Moines, Iowa 50325-0905 WISCONSIN BUYER S GUIDE TO FIXED DEFERRED ANNUITIES WHAT IS AN ANNUITY? An annuity is a written contract between you and a life insurance

Individual Health Savings Accounts

July 22, 2015 Individual Health Savings Accounts INITIAL CONSIDERATION By Ryan Frost Research and Policy Manager 360 586 2325 ryan.frost@leoff.wa.gov ISSUE STATEMENT There is a gap in healthcare coverage

July 22, 2015 Individual Health Savings Accounts INITIAL CONSIDERATION By Ryan Frost Research and Policy Manager 360 586 2325 ryan.frost@leoff.wa.gov ISSUE STATEMENT There is a gap in healthcare coverage

TEACHERS RETIREMENT ASSOCIATION A MINNESOTA PUBLIC PENSION FUND

TEACHERS RETIREMENT ASSOCIATION A MINNESOTA PUBLIC PENSION FUND 2011 Welcome! What is TRA? The Teachers Retirement t Association (TRA) is a public retirement t system that was founded in 1931 to provide

TEACHERS RETIREMENT ASSOCIATION A MINNESOTA PUBLIC PENSION FUND 2011 Welcome! What is TRA? The Teachers Retirement t Association (TRA) is a public retirement t system that was founded in 1931 to provide

Texas Municipal Retirement System TMRSFACTS. A brief overview of your retirement plan

Texas Municipal Retirement System TMRSFACTS A brief overview of your retirement plan Table of Contents What Is TMRS? 1 How Does TMRS Work? 2 How Do I Keep Up with My Account? 4 How Do I Contact TMRS? 5

Texas Municipal Retirement System TMRSFACTS A brief overview of your retirement plan Table of Contents What Is TMRS? 1 How Does TMRS Work? 2 How Do I Keep Up with My Account? 4 How Do I Contact TMRS? 5

Florida Retirement System Pension Plan D R O P. Deferred Retirement Option Program

Florida Retirement System Pension Plan D R O P Deferred Retirement Option Program Department of Management Services Division of Retirement July 2011 DISCLAIMER If questions of interpretation arise as a

Florida Retirement System Pension Plan D R O P Deferred Retirement Option Program Department of Management Services Division of Retirement July 2011 DISCLAIMER If questions of interpretation arise as a

State Defined Contribution and Hybrid Pension Plans

State Defined Contribution and Hybrid Pension Plans Ronald Snell June 2010 The overwhelming majority of statewide retirement plans for public employees and for teachers are traditional defined benefit

State Defined Contribution and Hybrid Pension Plans Ronald Snell June 2010 The overwhelming majority of statewide retirement plans for public employees and for teachers are traditional defined benefit

Death Benefits For City of San Diego Members, Survivors & Beneficiaries

Death Benefits For City of San Diego Members, Survivors & Beneficiaries Beneficiaries of SDCERS Members are eligible for certain Death Benefits that are dependent on the status of the SDCERS Member at

Death Benefits For City of San Diego Members, Survivors & Beneficiaries Beneficiaries of SDCERS Members are eligible for certain Death Benefits that are dependent on the status of the SDCERS Member at

Membership Handbook. Louisiana State Employees Retirement System

Membership Handbook Louisiana State Employees Retirement System as of February 2015 Initial Benefit Option (La. R.S. 11:446(A)(5)) The Initial Benefit Option (IBO) is an optional method of retirement which

Membership Handbook Louisiana State Employees Retirement System as of February 2015 Initial Benefit Option (La. R.S. 11:446(A)(5)) The Initial Benefit Option (IBO) is an optional method of retirement which

Teachers Retirement System of the City of New York. TDA Program Summary. Tax-Deferred Annuity Program

Teachers Retirement System of the City of New York TDA Program Summary Tax-Deferred Annuity Program Tax-Deferred Annuity Program Teachers Retirement System of the City of New York TRS Tax-Deferred Annuity

Teachers Retirement System of the City of New York TDA Program Summary Tax-Deferred Annuity Program Tax-Deferred Annuity Program Teachers Retirement System of the City of New York TRS Tax-Deferred Annuity

Retiree Life Insurance Initial Consideration

Retiree Life Insurance Initial Consideration LEOFF Plan 2 Retirement Board August 22, 2007 Overview Issue Background Comparison Issue Survivor Option Actuarial Reduction Background Purpose of Reduction

Retiree Life Insurance Initial Consideration LEOFF Plan 2 Retirement Board August 22, 2007 Overview Issue Background Comparison Issue Survivor Option Actuarial Reduction Background Purpose of Reduction

How To Determine The Cost Of A Juror Retirement Plan

GAO United States Government Accountability Office Report to Congressional Committees September 2008 FEDERAL PENSIONS Judicial Survivors Annuities System Costs GAO-08-1104 September 2008 Accountability

GAO United States Government Accountability Office Report to Congressional Committees September 2008 FEDERAL PENSIONS Judicial Survivors Annuities System Costs GAO-08-1104 September 2008 Accountability

The Individual Annuity

The Individual Annuity a re s o u rc e i n yo u r r e t i r e m e n t an age of Decision Retirement today requires more planning than for previous generations. Americans are living longer many will live

The Individual Annuity a re s o u rc e i n yo u r r e t i r e m e n t an age of Decision Retirement today requires more planning than for previous generations. Americans are living longer many will live

Overview of Teacher Retirement System of Texas

Overview of Teacher Retirement System of Texas Tom Guerin Revised September 2011 Revised 10/21/09 TRS retirement plan benefits are funded by member, state, and employer contributions to the trust fund,

Overview of Teacher Retirement System of Texas Tom Guerin Revised September 2011 Revised 10/21/09 TRS retirement plan benefits are funded by member, state, and employer contributions to the trust fund,

How To Get A Retirement Plan In Wisconsin Retirement System

YOUR BENEFIT HANDBOOK ETF P O Box 7931 Madison, WI 53707-7931 ET-2119 (REV 10/13) TABLE OF CONTENTS INTRODUCTION... 2 VESTING REQUIREMENTS... 2 WISCONSIN RETIREMENT SYSTEM... 3 Retirement Benefits...

YOUR BENEFIT HANDBOOK ETF P O Box 7931 Madison, WI 53707-7931 ET-2119 (REV 10/13) TABLE OF CONTENTS INTRODUCTION... 2 VESTING REQUIREMENTS... 2 WISCONSIN RETIREMENT SYSTEM... 3 Retirement Benefits...

FG Immediate-Income. Single Premium Immediate Annuity. ADV 1011 (01-2011) Fidelity & Guaranty Life Insurance Company Rev.

Fidelity & Guaranty Life Insurance Company Rev.") Single Premium Immediate Annuity ADV 1011 (01-2011) Fidelity & Guaranty Life Insurance Company Rev. 07-2014 12-715 Single Premium Immediate Annuity Americans are living longer than ever before. Source:

Single Premium Immediate Annuity ADV 1011 (01-2011) Fidelity & Guaranty Life Insurance Company Rev. 07-2014 12-715 Single Premium Immediate Annuity Americans are living longer than ever before. Source:

Generic Local School District, Ohio Notes to the Basic Financial Statements For the Fiscal Year Ended June 30, 2015

Note 2 - Summary of Significant Accounting Policies Pensions For purposes of measuring the net pension liability, information about the fiduciary net position of the pension plans and additions to/deductions

Note 2 - Summary of Significant Accounting Policies Pensions For purposes of measuring the net pension liability, information about the fiduciary net position of the pension plans and additions to/deductions

Payment Options. Retirement Benefit

Payment Options Retirement Benefit Table of contents Choosing your benefit payment option... 2 Life Annuities... 5 Fixed Period Benefit... 7 Installment Benefit... 8 Combination of Benefits... 10 Single

Payment Options Retirement Benefit Table of contents Choosing your benefit payment option... 2 Life Annuities... 5 Fixed Period Benefit... 7 Installment Benefit... 8 Combination of Benefits... 10 Single

You Have an Important Choice to Make!

You Have an Important Choice to Make! July 04 As a new employee, you must choose one of three retirement plans available to eligible State University System employees. They are the: State University System

You Have an Important Choice to Make! July 04 As a new employee, you must choose one of three retirement plans available to eligible State University System employees. They are the: State University System

Title IV Treatment of Rollovers from Defined Contribution Plans to Defined Benefit Plans

[Billing Code 7709-02-P] PENSION BENEFIT GUARANTY CORPORATION 29 CFR Parts 4001, 4022, and 4044 RIN 1212-AB23 Title IV Treatment of Rollovers from Defined Contribution Plans to Defined Benefit Plans AGENCY:

[Billing Code 7709-02-P] PENSION BENEFIT GUARANTY CORPORATION 29 CFR Parts 4001, 4022, and 4044 RIN 1212-AB23 Title IV Treatment of Rollovers from Defined Contribution Plans to Defined Benefit Plans AGENCY:

Retirement System. IRS Compliance Policy I\5165269.7

Retirement System IRS Compliance Policy August 2015 Table of Contents I. SECTION 1. PUBLIC EMPLOYEES RETIREMENT SYSTEM TIERS 1, 2, AND 3 DEFINED BENEFIT PLAN...2 A. Rollover Distributions Compliance with

Retirement System IRS Compliance Policy August 2015 Table of Contents I. SECTION 1. PUBLIC EMPLOYEES RETIREMENT SYSTEM TIERS 1, 2, AND 3 DEFINED BENEFIT PLAN...2 A. Rollover Distributions Compliance with

Service Retirement. Plans of Payment AND. For members enrolled in the Defined Contribution Plan

Service Retirement AND Plans of Payment For members enrolled in the Defined Contribution Plan 2015 2016 Service Retirement Overview Table of Contents Service Retirement Overview...1 Benefit calculation...2

Service Retirement AND Plans of Payment For members enrolled in the Defined Contribution Plan 2015 2016 Service Retirement Overview Table of Contents Service Retirement Overview...1 Benefit calculation...2

GTE SALARIED APPENDIX WINDSTREAM PENSION PLAN SUMMARY PLAN DESCRIPTION

GTE SALARIED APPENDIX WINDSTREAM PENSION PLAN SUMMARY PLAN DESCRIPTION () This document is being provided exclusively by your employer, which retains responsibility for the content. No affiliate of Bank

GTE SALARIED APPENDIX WINDSTREAM PENSION PLAN SUMMARY PLAN DESCRIPTION () This document is being provided exclusively by your employer, which retains responsibility for the content. No affiliate of Bank

Choosing Your Retirement Plan Optional Retirement Plan for Higher Education VRS Hybrid Retirement Plan Membership Date: On or after January 1, 2014

Choosing Your Retirement Plan Optional Retirement Plan for Higher Education VRS Hybrid Retirement Plan Membership Date: On or after January 1, 2014 A comparison guide to help you select the best plan for

Choosing Your Retirement Plan Optional Retirement Plan for Higher Education VRS Hybrid Retirement Plan Membership Date: On or after January 1, 2014 A comparison guide to help you select the best plan for

The Individual Annuity

The Individual Annuity a resource in your retirement an age of Decision Retirement today requires more planning than for previous generations. Americans are living longer many will live 20 to 30 years

The Individual Annuity a resource in your retirement an age of Decision Retirement today requires more planning than for previous generations. Americans are living longer many will live 20 to 30 years

Planning Retirement. Information for BCGEU Pension Plan Members

Planning Retirement Information for BCGEU Pension Plan Members January 2012 PAGE ONE PAGE TWO PAGE THREE PAGE FOUR PAGE FIVE PAGE SIX PAGE SEVEN PAGE EIGHT PAGE NINE PAGE TWELVE TABLE OF CONTENTS Preparing

Planning Retirement Information for BCGEU Pension Plan Members January 2012 PAGE ONE PAGE TWO PAGE THREE PAGE FOUR PAGE FIVE PAGE SIX PAGE SEVEN PAGE EIGHT PAGE NINE PAGE TWELVE TABLE OF CONTENTS Preparing

Excerpts from IRI Annuity Fact Book Variable Annuity 101 An annuity is often viewed as life insurance in reverse. Whereas life insurance protects an individual against premature death, an annuity protects

Excerpts from IRI Annuity Fact Book Variable Annuity 101 An annuity is often viewed as life insurance in reverse. Whereas life insurance protects an individual against premature death, an annuity protects

Caution: Withdrawals made prior to age 59 ½ may be subject to a 10 percent federal penalty tax.

Annuity Distributions What are annuity distributions? How are annuity distributions made? How are your annuity payouts computed if you elect to annuitize? Who are the parties to an annuity contract? How

Annuity Distributions What are annuity distributions? How are annuity distributions made? How are your annuity payouts computed if you elect to annuitize? Who are the parties to an annuity contract? How

Understanding DROP. Deferred Retirement Option Program. Overview

Understanding DROP Deferred Retirement Option Program Fairfax County Retirement Systems 2015 PLEASE NOTE: The provisions referenced in this slide presentation are relevant for employees who were Fairfax

Understanding DROP Deferred Retirement Option Program Fairfax County Retirement Systems 2015 PLEASE NOTE: The provisions referenced in this slide presentation are relevant for employees who were Fairfax

The Commuted Value Option at GM

The Commuted Value Option at GM In the September 2012 Detroit 3 negotiations, the CAW agreed to the Ford and GM request on commuted value (CV) options. After December 31, 2012, CAW members retiring with

The Commuted Value Option at GM In the September 2012 Detroit 3 negotiations, the CAW agreed to the Ford and GM request on commuted value (CV) options. After December 31, 2012, CAW members retiring with

billion, while annuity reserves (Table 8.2) increased 6 percent to $2.5 trillion.

increased 6 percent to $2.5 trillion.") 8annuities Annuities are financial contracts that pay a steady stream of income for either a fixed period of time or for the lifetime of the annuity owner (the annuitant). Most pension and retirement plan

8annuities Annuities are financial contracts that pay a steady stream of income for either a fixed period of time or for the lifetime of the annuity owner (the annuitant). Most pension and retirement plan

Sacramento Metropolitan Fire District Retirement Benefit Options

Personal Information Sacramento Metropolitan Fire District Retirement Benefit Options If this is an initial request, and not a change in a current distribution, remember to have your former employer complete

Personal Information Sacramento Metropolitan Fire District Retirement Benefit Options If this is an initial request, and not a change in a current distribution, remember to have your former employer complete

County of Fresno Retirement Benefit Options

County of Fresno Retirement Benefit Options NRM-13003CA-FR.1 Things to Remember c Complete all of the sections on the Retirement Benefit Options form that apply to your request. c If you are requesting

County of Fresno Retirement Benefit Options NRM-13003CA-FR.1 Things to Remember c Complete all of the sections on the Retirement Benefit Options form that apply to your request. c If you are requesting

How To Get A Pension Plan In The United States

New Hire Retirement Plan Election Michigan Public School Employees Retirement System For public school employees who first work on or after September 4, 2012 Welcome to the Michigan Public School Employees

New Hire Retirement Plan Election Michigan Public School Employees Retirement System For public school employees who first work on or after September 4, 2012 Welcome to the Michigan Public School Employees

DEATH BENEFITS. Department of Employee Trust Funds P. O. Box 7931 Madison, WI 53707-7931 etf.wi.gov ET-6101 (REV 5/13)

") DEATH BENEFITS Department of Employee Trust Funds P. O. Box 7931 Madison, WI 53707-7931 etf.wi.gov ET-6101 (REV 5/13) 4 The Department of Employee Trust Funds (ETF) administers three programs that provide

DEATH BENEFITS Department of Employee Trust Funds P. O. Box 7931 Madison, WI 53707-7931 etf.wi.gov ET-6101 (REV 5/13) 4 The Department of Employee Trust Funds (ETF) administers three programs that provide

GENERAL INCOME TAX INFORMATION

NEW YORK STATE TEACHERS RETIREMENT SYSTEM GENERAL INCOME TAX INFORMATION TABLE OF CONTENTS Taxes on Loans from the Annuity Savings Fund 1 (Tier 1 and 2 Members Only) Taxes on the Withdrawal of the Annuity

NEW YORK STATE TEACHERS RETIREMENT SYSTEM GENERAL INCOME TAX INFORMATION TABLE OF CONTENTS Taxes on Loans from the Annuity Savings Fund 1 (Tier 1 and 2 Members Only) Taxes on the Withdrawal of the Annuity

The Revised Pension Plan of

The Revised Pension Plan of A Guide to the Pension Plan for Queen s Staff and Faculty Prepared by Pension Services, Department of Human Resources Fleming Hall, Stewart-Pollock Wing 78 Fifth Field Company

The Revised Pension Plan of A Guide to the Pension Plan for Queen s Staff and Faculty Prepared by Pension Services, Department of Human Resources Fleming Hall, Stewart-Pollock Wing 78 Fifth Field Company

ANNUITY AND REFUNDS HANDBOOK FOR TIER 1 PARTICIPANTS

ANNUITY AND REFUNDS HANDBOOK FOR TIER 1 PARTICIPANTS "INQUIRE BEFORE YOU RETIRE" Our experienced counselors are here to help you navigate through the benefits in order to make an informed decision that

ANNUITY AND REFUNDS HANDBOOK FOR TIER 1 PARTICIPANTS "INQUIRE BEFORE YOU RETIRE" Our experienced counselors are here to help you navigate through the benefits in order to make an informed decision that

Kansas Legislator Briefing Book 2015

K a n s a s L e g i s l a t i v e R e s e a r c h D e p a r t m e n t Q-1 Kansas Public Employees Retirement System Retirement Plans and History Retirement Kansas Legislator Briefing Book 2015 Q-1 Kansas

K a n s a s L e g i s l a t i v e R e s e a r c h D e p a r t m e n t Q-1 Kansas Public Employees Retirement System Retirement Plans and History Retirement Kansas Legislator Briefing Book 2015 Q-1 Kansas

What to Consider When Faced With the Pension Election Decision

PENSION ELECTION Key Information About Your Pension (Optional Forms of Benefits) Pension Math and Factors to Consider Pension Maximization What Happens if Your Company Files for Bankruptcy and Your Company

PENSION ELECTION Key Information About Your Pension (Optional Forms of Benefits) Pension Math and Factors to Consider Pension Maximization What Happens if Your Company Files for Bankruptcy and Your Company

Retirement Facts 10. Voluntary Contributions Under the Civil Service Retirement System

Retirement Facts 10 Voluntary Under the Civil Service Retirement System This is a non-technical summary of the laws and regulations on the subject. It should not be relied upon as a sole source of information.

Retirement Facts 10 Voluntary Under the Civil Service Retirement System This is a non-technical summary of the laws and regulations on the subject. It should not be relied upon as a sole source of information.

TRADITIONAL PLAN MEMBER GUIDE S U R S STATE UNIVERSITIES RETIREMENT SYSTEM

TRADITIONAL PLAN MEMBER GUIDE S U R S STATE UNIVERSITIES RETIREMENT SYSTEM SURS MISSION STATEMENT To secure and deliver the retirement benefits promised to our members. This booklet is intended to serve

TRADITIONAL PLAN MEMBER GUIDE S U R S STATE UNIVERSITIES RETIREMENT SYSTEM SURS MISSION STATEMENT To secure and deliver the retirement benefits promised to our members. This booklet is intended to serve

Reuter Benefits Group Plan Member Newsletter September 2009

Reuter Benefits Group Plan Member Newsletter September 2009 Accessing Your Retirement Savings As you approach retirement, you will need to turn your Pension and RRSP, as well as any nonregistered savings,

Reuter Benefits Group Plan Member Newsletter September 2009 Accessing Your Retirement Savings As you approach retirement, you will need to turn your Pension and RRSP, as well as any nonregistered savings,

Payouts. Protection. In One Place.

Payouts. Protection. In One Place. ING Single Premium Immediate Annuity issued by ING USA Annuity and Life Insurance Company Your future. Made easier. Payouts. Protection. In today s financial world, some

Payouts. Protection. In One Place. ING Single Premium Immediate Annuity issued by ING USA Annuity and Life Insurance Company Your future. Made easier. Payouts. Protection. In today s financial world, some

Teacher Retirement System Fact Sheet

Teacher Retirement System Fact Sheet Teacher Retirement System History 1. In 1936, the Teacher Retirement System of Texas (TRS) is a pension trust fund that was established in the Texas Constitution. 2.

Teacher Retirement System Fact Sheet Teacher Retirement System History 1. In 1936, the Teacher Retirement System of Texas (TRS) is a pension trust fund that was established in the Texas Constitution. 2.

Chapter 19 Retirement Products: Annuities and Individual Retirement Accounts

Chapter 19 Retirement Products: Annuities and Individual Retirement Accounts Overview Thus far we have examined life insurance in great detail. Life insurance companies also market a product that addresses

Chapter 19 Retirement Products: Annuities and Individual Retirement Accounts Overview Thus far we have examined life insurance in great detail. Life insurance companies also market a product that addresses

MINNEAPOLIS EMPLOYEES RETIREMENT FUND JANUARY 2004 MINNEAPOLIS, MINNESOTA MINNEAPOLIS EMPLOYEE RETIREMENT FUND (612) 335-5950

335-5950") MINNEAPOLIS EMPLOYEES RETIREMENT FUND JANUARY 2004 MINNEAPOLIS, MINNESOTA MINNEAPOLIS EMPLOYEE RETIREMENT FUND (612) 335-5950 1 RETIREMENT BOARD MEMBERS Agnes M.Gay President Dennis W. Schulstad Vice President

MINNEAPOLIS EMPLOYEES RETIREMENT FUND JANUARY 2004 MINNEAPOLIS, MINNESOTA MINNEAPOLIS EMPLOYEE RETIREMENT FUND (612) 335-5950 1 RETIREMENT BOARD MEMBERS Agnes M.Gay President Dennis W. Schulstad Vice President

Payouts. Protection. In One Place.

Payouts. Protection. In One Place. ING Single Premium Immediate Annuity ANNUITIES Your future. Made easier. Payouts. Protection. In today s financial world, some products provide payout options. Others

Payouts. Protection. In One Place. ING Single Premium Immediate Annuity ANNUITIES Your future. Made easier. Payouts. Protection. In today s financial world, some products provide payout options. Others

Summary Plan Description

Summary Plan Description Prepared for DePauw University Retirement Plan January 2012 TABLE OF CONTENTS Page INTRODUCTION...1 ELIGIBILITY...1 Am I eligible to participate in the Plan?...1 What requirements

Summary Plan Description Prepared for DePauw University Retirement Plan January 2012 TABLE OF CONTENTS Page INTRODUCTION...1 ELIGIBILITY...1 Am I eligible to participate in the Plan?...1 What requirements

SUPPLEMENTAL ANNUITY COLLECTIVE TRUST

DS-0448-1299 SUPPLEMENTAL ANNUITY COLLECTIVE TRUST Regular and Tax-Sheltered Prepared and Distributed By New Jersey Division of Pensions and Benefits PO Box 295 Trenton, New Jersey 08625-0295 October 1999

DS-0448-1299 SUPPLEMENTAL ANNUITY COLLECTIVE TRUST Regular and Tax-Sheltered Prepared and Distributed By New Jersey Division of Pensions and Benefits PO Box 295 Trenton, New Jersey 08625-0295 October 1999

CSRS Cost-of-Living Adjustments FERS Chapter 2

CSRS Cost-of-Living Adjustments FERS i Table of Contents Subchapter 2A CSRS Part 2A1 General Information Section 2A1.1-1 Overview... 1 A. Introduction... 1 B. Topics Covered... 1 C. Organization of Subchapter...

CSRS Cost-of-Living Adjustments FERS i Table of Contents Subchapter 2A CSRS Part 2A1 General Information Section 2A1.1-1 Overview... 1 A. Introduction... 1 B. Topics Covered... 1 C. Organization of Subchapter...

1999 Academic Pension Plan

1999 Academic Pension Plan TABLE OF CONTENTS Introduction... 3 Eligibility... 3 Enrolling in the Plan... 3 Contributions... 3 Defined Benefit Component:... 3 Defined Contribution Component:... 4 Other

1999 Academic Pension Plan TABLE OF CONTENTS Introduction... 3 Eligibility... 3 Enrolling in the Plan... 3 Contributions... 3 Defined Benefit Component:... 3 Defined Contribution Component:... 4 Other

District of Columbia Teachers Retirement Plan

District of Columbia Teachers Retirement Plan SUMMARY PLAN DESCRIPTION 2012 District of Columbia Teachers Retirement Plan Summary Plan Description This booklet is a Summary Plan Description (SPD) of the

District of Columbia Teachers Retirement Plan SUMMARY PLAN DESCRIPTION 2012 District of Columbia Teachers Retirement Plan Summary Plan Description This booklet is a Summary Plan Description (SPD) of the

CONSUMER S GUIDE TO. Annuities. Be secure and confident in the decisions you make

A CONSUMER S GUIDE TO Annuities Be secure and confident in the decisions you make Americans are living longer than ever before. How will they fund these extra years? There are many different approaches.

A CONSUMER S GUIDE TO Annuities Be secure and confident in the decisions you make Americans are living longer than ever before. How will they fund these extra years? There are many different approaches.

Retirement Programs. For New Faculty and Staff

Retirement Programs For New Faculty and Staff January 2015 Table of Contents Introduction................................................... 1 Choosing Your Retirement Annuity Program at SUNY................

Retirement Programs For New Faculty and Staff January 2015 Table of Contents Introduction................................................... 1 Choosing Your Retirement Annuity Program at SUNY................

GUIDELINE NO.X DEFINED CONTRIBUTION PENSION PLANS GUIDELINE

GUIDELINE NO.X DEFINED CONTRIBUTION PENSION PLANS GUIDELINE JULY 13, 2012 Table of Contents PURPOSE... 3 EXISTING CAPSA GUIDANCE RELATED TO DC PENSION PLANS... 3 APPLICATION OF THE DC PENSION PLANS GUIDELINE...

GUIDELINE NO.X DEFINED CONTRIBUTION PENSION PLANS GUIDELINE JULY 13, 2012 Table of Contents PURPOSE... 3 EXISTING CAPSA GUIDANCE RELATED TO DC PENSION PLANS... 3 APPLICATION OF THE DC PENSION PLANS GUIDELINE...

GROUP LIFE INSURANCE

GROUP LIFE INSURANCE Public Employees Retirement System (PERS) and Teachers Pension and Annuity Fund (TPAF) CONTRIBUTORY AND NONCONTRIBUTORY GROUP LIFE INSURANCE As an active employee in the PERS or TPAF

GROUP LIFE INSURANCE Public Employees Retirement System (PERS) and Teachers Pension and Annuity Fund (TPAF) CONTRIBUTORY AND NONCONTRIBUTORY GROUP LIFE INSURANCE As an active employee in the PERS or TPAF

For IPERS Beneficiaries. Important Information About IPERS Death Benefits

For IPERS Beneficiaries Important Information About IPERS Death Benefits For IPERS Beneficiaries Important Information About IPERS Death Benefits IPERS provides financial protection to members beneficiaries.

For IPERS Beneficiaries Important Information About IPERS Death Benefits For IPERS Beneficiaries Important Information About IPERS Death Benefits IPERS provides financial protection to members beneficiaries.

Preparing for Retirement

Preparing for Retirement Preparing for Retirement Your UC Pension Lump Sum Cashout Retirement payment vs. paycheck Additional UC sources of retirement income Other sources of retirement income To your

Preparing for Retirement Preparing for Retirement Your UC Pension Lump Sum Cashout Retirement payment vs. paycheck Additional UC sources of retirement income Other sources of retirement income To your

Voya Single Premium Immediate Annuity

Voya Single Premium Immediate Annuity issued by Voya Insurance and Annuity Company Payouts. Protection. In One Place. Payouts. Protection. In One Place. In today s financial world, some products provide

Voya Single Premium Immediate Annuity issued by Voya Insurance and Annuity Company Payouts. Protection. In One Place. Payouts. Protection. In One Place. In today s financial world, some products provide

The Hartford Saver Solution SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT

The Hartford Saver Solution SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT THE HARTFORD SAVER SOLUTION SM FIXED INDEX ANNUITY DISCLOSURE STATEMENT This Disclosure Statement provides important information

The Hartford Saver Solution SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT THE HARTFORD SAVER SOLUTION SM FIXED INDEX ANNUITY DISCLOSURE STATEMENT This Disclosure Statement provides important information

TEACHERS AND STATE EMPLOYEES RETIREMENT SYSTEM. your retirement benefits

TEACHERS AND STATE EMPLOYEES RETIREMENT SYSTEM your retirement benefits Department of State Treasurer Raleigh, NC Revised January 2014 NORTH CAROLINA DEPARTMENT OF STATE TREASURER RETIREMENT SYSTEMS DIVISION

TEACHERS AND STATE EMPLOYEES RETIREMENT SYSTEM your retirement benefits Department of State Treasurer Raleigh, NC Revised January 2014 NORTH CAROLINA DEPARTMENT OF STATE TREASURER RETIREMENT SYSTEMS DIVISION

VOLUNTARY FACULTY SEPARATION INCENTIVE PROGRAM (FSIP) 2016 Frequently Asked Questions (FAQs)

2016 Frequently Asked Questions (FAQs)") VOLUNTARY FACULTY SEPARATION INCENTIVE PROGRAM (FSIP) 2016 Frequently Asked Questions (FAQs) The 2016 FSIP Program 1. Q. What is the 2016 Faculty Separation Incentive Program (FSIP)? A. The 2016 NJIT Faculty

VOLUNTARY FACULTY SEPARATION INCENTIVE PROGRAM (FSIP) 2016 Frequently Asked Questions (FAQs) The 2016 FSIP Program 1. Q. What is the 2016 Faculty Separation Incentive Program (FSIP)? A. The 2016 NJIT Faculty

Palladium. Immediate Annuity - NY. Income For Now... Income For Life! A Single Premium Immediate Fixed Annuity Product of

Palladium Immediate Annuity - NY Income For Now... Income For Life! A Single Premium Immediate Fixed Annuity Product of Income A Guaranteed Income for as Long as You Need It One of the major fears we face

Palladium Immediate Annuity - NY Income For Now... Income For Life! A Single Premium Immediate Fixed Annuity Product of Income A Guaranteed Income for as Long as You Need It One of the major fears we face

A GUIDE TO INVESTING IN ANNUITIES

A GUIDE TO INVESTING IN ANNUITIES What Benefits Do Annuities Offer in Planning for Retirement? Oppenheimer Life Agency, Ltd. Oppenheimer Life Agency, Ltd., a wholly owned subsidiary of Oppenheimer & Co.

A GUIDE TO INVESTING IN ANNUITIES What Benefits Do Annuities Offer in Planning for Retirement? Oppenheimer Life Agency, Ltd. Oppenheimer Life Agency, Ltd., a wholly owned subsidiary of Oppenheimer & Co.

IncomeSource. Issuers: Integrity Life Insurance Company National Integrity Life Insurance Company. Single Premium Immediate Annuity

IncomeSource Single Premium Immediate Annuity RISK MANAGEMENT FINANCIAL SOLUTIONS Issuers: Integrity Life Insurance Company National Integrity Life Insurance Company CF-10-29000-1209 Create Retirement

IncomeSource Single Premium Immediate Annuity RISK MANAGEMENT FINANCIAL SOLUTIONS Issuers: Integrity Life Insurance Company National Integrity Life Insurance Company CF-10-29000-1209 Create Retirement

Chapter 14. Agenda. Individual Annuities. Annuities and Individual Retirement Accounts

Chapter 14 Annuities and Individual Retirement Accounts Agenda 2 Individual Annuities Types of Annuities Taxation of Individual Annuities Individual Retirement Accounts Individual Annuities 3 An annuity

Chapter 14 Annuities and Individual Retirement Accounts Agenda 2 Individual Annuities Types of Annuities Taxation of Individual Annuities Individual Retirement Accounts Individual Annuities 3 An annuity

Domestic Relations Orders (DRO) Questions Answers

Questions Answers") FPPA Domestic Relations Orders (DRO) Questions Answers for FPPA & Administered Pension Plans For your convenience, FPPA has compiled a listing of the most frequently requested information. We hope this

FPPA Domestic Relations Orders (DRO) Questions Answers for FPPA & Administered Pension Plans For your convenience, FPPA has compiled a listing of the most frequently requested information. We hope this

Choosing a Retirement Program

Revised July 1, 2011 S TATE R ETIREMENT AND P ENSION S YSTEM Choosing a Retirement Program Maryland Optional Retirement Plan Highlights of the SRPS & ORP Retirement Programs ABOUT THIS BOOK About This

Revised July 1, 2011 S TATE R ETIREMENT AND P ENSION S YSTEM Choosing a Retirement Program Maryland Optional Retirement Plan Highlights of the SRPS & ORP Retirement Programs ABOUT THIS BOOK About This

Financial Services Commission of Ontario Commission des services financiers de l Ontario

Financial Services Commission of Ontario Commission des services financiers de l Ontario SECTION: Life Income Fund/Locked-In Retirement Account INDEX NO.: L050-500 TITLE: LIF Explanation and Tables for

Financial Services Commission of Ontario Commission des services financiers de l Ontario SECTION: Life Income Fund/Locked-In Retirement Account INDEX NO.: L050-500 TITLE: LIF Explanation and Tables for

Earning Cash Balance Pay Credits

You Have a Choice New Cash Balance Pension You Have a Choice The important thing to understand is this: If you were hired through December 31, 2012 you don t have to change to the new cash balance pension

You Have a Choice New Cash Balance Pension You Have a Choice The important thing to understand is this: If you were hired through December 31, 2012 you don t have to change to the new cash balance pension

How To Get A Pension From The Retirement Plan

Defined Contribution Plan Distribution Kit for CSU Safe Harbor Participants University of California Retirement System (UCRS) UBEN 143 CSU (R3/99) Use the form in the back of this kit if you have left

Defined Contribution Plan Distribution Kit for CSU Safe Harbor Participants University of California Retirement System (UCRS) UBEN 143 CSU (R3/99) Use the form in the back of this kit if you have left

Attainment of age 50 when age plus contributory service equals 70 (excluding military service)

") RETIREMENT BENEFITS: Contributions MPFRS is funded by employee and employer contributions. An active employee currently contributes 8.5% of his or her gross monthly salary, and the employer currently contributes

RETIREMENT BENEFITS: Contributions MPFRS is funded by employee and employer contributions. An active employee currently contributes 8.5% of his or her gross monthly salary, and the employer currently contributes

Voya Single Premium Immediate Annuity

Voya Single Premium Immediate Annuity issued by Voya Insurance and Annuity Company Payouts. Protection. In One Place. Payouts. Protection. In One Place. In today s financial world, some products provide

Voya Single Premium Immediate Annuity issued by Voya Insurance and Annuity Company Payouts. Protection. In One Place. Payouts. Protection. In One Place. In today s financial world, some products provide

Employee Pension Guide. Pension Plan for Salaried Employees of Union Pacific Corporation and Affiliates

Employee Pension Guide Pension Plan for Salaried Employees of Union Pacific Corporation and Affiliates OVERVIEW OF THE PLAN The following provides a brief overview of the Pension Plan for Salaried Employees

Employee Pension Guide Pension Plan for Salaried Employees of Union Pacific Corporation and Affiliates OVERVIEW OF THE PLAN The following provides a brief overview of the Pension Plan for Salaried Employees

Annuity Principles and Concepts Session Five Lesson Two. Annuity (Benefit) Payment Options

Payment Options") Annuity Principles and Concepts Session Five Lesson Two Annuity (Benefit) Payment Options Life Contingency Options - How Income Payments Can Be Made To The Annuitant. Pure Life versus Life with Guaranteed

Annuity Principles and Concepts Session Five Lesson Two Annuity (Benefit) Payment Options Life Contingency Options - How Income Payments Can Be Made To The Annuitant. Pure Life versus Life with Guaranteed

UNO-VEN Retirement Plan. Summary Plan Description As in effect January 1, 2012

Summary Plan Description As in effect January 1, 2012 In the event of any conflict between this Summary Plan Description (SPD) and the actual text of the UNO-VEN Retirement Plan, the more detailed provisions

Summary Plan Description As in effect January 1, 2012 In the event of any conflict between this Summary Plan Description (SPD) and the actual text of the UNO-VEN Retirement Plan, the more detailed provisions

12/13/2010. O:/SCPP/2010/12-14-10_Full/4.LumpSumDutyDeathBen.pptx -

Select Committee on Pension Policy Lump Sum DutyDeath Death Benefit Darren Painter, Senior Policy Analyst December 14, 2010 How Did This Issue Come Before The SCPP? Stakeholders are requesting the SCPP

Select Committee on Pension Policy Lump Sum DutyDeath Death Benefit Darren Painter, Senior Policy Analyst December 14, 2010 How Did This Issue Come Before The SCPP? Stakeholders are requesting the SCPP

What You Need to Know as the Recipient of a Lump-Sum Payment An MTRS Q&A guide for our active and inactive members

What You Need to Know as the Recipient of a Lump-Sum Payment An MTRS Q&A guide for our active and inactive members For the MTRS member About your annuity savings account... 1 Withdrawing your balance.....

What You Need to Know as the Recipient of a Lump-Sum Payment An MTRS Q&A guide for our active and inactive members For the MTRS member About your annuity savings account... 1 Withdrawing your balance.....

CSRS Alternative Annuity Elections FERS Chapter 53

CSRS Alternative Annuity Elections FERS i Table of Contents Subchapter 53A CSRS... 1 Part 53A1 General Information... 1 Section 53A1.1-1 Overview... 1 A. Introduction... 1 B. Topics Covered... 1 C. Organization

CSRS Alternative Annuity Elections FERS i Table of Contents Subchapter 53A CSRS... 1 Part 53A1 General Information... 1 Section 53A1.1-1 Overview... 1 A. Introduction... 1 B. Topics Covered... 1 C. Organization

BENEFITS RETIREMENT HANDBOOK

The University of Houston BENEFITS RETIREMENT HANDBOOK Rev 10/07 UNIVERSITY OF HOUSTON BENEFITS RETIREMENT HANDBOOK TABLE OF CONTENTS SECTION I DEFINITION OF A RETIREE 3 SECTION II RETIREE INSURANCE BENEFITS

The University of Houston BENEFITS RETIREMENT HANDBOOK Rev 10/07 UNIVERSITY OF HOUSTON BENEFITS RETIREMENT HANDBOOK TABLE OF CONTENTS SECTION I DEFINITION OF A RETIREE 3 SECTION II RETIREE INSURANCE BENEFITS

Retirement Plan for Bargaining Unit Employees of Florida Progress Corporation

Document title: AUTHORIZED COPY Retirement Plan for Bargaining Unit Employees of Florida Progress Corporation Document number: HRI-PGNF-00013 Applies to: Keywords: Progress Energy Florida, Inc. (bargaining

Document title: AUTHORIZED COPY Retirement Plan for Bargaining Unit Employees of Florida Progress Corporation Document number: HRI-PGNF-00013 Applies to: Keywords: Progress Energy Florida, Inc. (bargaining

LAKEHEAD UNIVERSITY EMPLOYEE PENSION PLAN MEMBER BOOKLET

LAKEHEAD UNIVERSITY EMPLOYEE PENSION PLAN MEMBER BOOKLET 2011 1 TABLE OF CONTENTS Introduction... 3 Eligibility... 4 Contributions... 5 Individual Account... 8 Short Term Account... 8 Retirement Dates...

LAKEHEAD UNIVERSITY EMPLOYEE PENSION PLAN MEMBER BOOKLET 2011 1 TABLE OF CONTENTS Introduction... 3 Eligibility... 4 Contributions... 5 Individual Account... 8 Short Term Account... 8 Retirement Dates...

MEMBERS Future Income Annuity

MEMBERS Future Income Annuity GUARANTEED INCOME FOR LIFE Move confidently into the future MFA-875346-034-046 A financial services company serving financial institutions and their clients worldwide. It

MEMBERS Future Income Annuity GUARANTEED INCOME FOR LIFE Move confidently into the future MFA-875346-034-046 A financial services company serving financial institutions and their clients worldwide. It

Participant Name (First) (Middle Initial) (Last) Social Security Number I.D. Number. Participant Address (Street) City State ZIP Code + 4

(Middle Initial) (Last) Social Security Number I.D. Number. Participant Address (Street) City State ZIP Code + 4") Mailing Address: Des Moines, IA 50392-0001 Principal Life Insurance Company Early Withdrawal of Benefits Without Guaranteed Accounts No Spousal Consent Needed CTD00603 Complete this form to withdraw part

Mailing Address: Des Moines, IA 50392-0001 Principal Life Insurance Company Early Withdrawal of Benefits Without Guaranteed Accounts No Spousal Consent Needed CTD00603 Complete this form to withdraw part

An Overview of TRS and ORP

An Overview of TRS and ORP For Employees Eligible to Elect ORP Prepared by: Texas Higher Education Coordinating Board Staff Distributed by: Texas Public Institutions of Higher Education (revised August

An Overview of TRS and ORP For Employees Eligible to Elect ORP Prepared by: Texas Higher Education Coordinating Board Staff Distributed by: Texas Public Institutions of Higher Education (revised August

Palladium Single Premium Immediate Annuity With

Palladium Single Premium Immediate Annuity With Cost Of Living Adjustment Income For Now... Guaranteed Income For Life! A Single Premium Immediate Annuity Issued By Income for Your Needs Now and in the

Palladium Single Premium Immediate Annuity With Cost Of Living Adjustment Income For Now... Guaranteed Income For Life! A Single Premium Immediate Annuity Issued By Income for Your Needs Now and in the

How To Pay Out Of Pocket

CHAPTER 15. UNIFORM RETIREMENT SYSTEM FOR JUSTICES AND JUDGES Subchapter Section 1. General Provisions... 590:15-1-1 3. Excess Contributions... 590:15-3-1 5. Excess Benefit Plan and Trust... 590:15-5-1

CHAPTER 15. UNIFORM RETIREMENT SYSTEM FOR JUSTICES AND JUDGES Subchapter Section 1. General Provisions... 590:15-1-1 3. Excess Contributions... 590:15-3-1 5. Excess Benefit Plan and Trust... 590:15-5-1

STATE EMPLOYEES RETIREMENT SYSTEM - DEFINED BENEFIT PLANS -

STATE EMPLOYEES RETIREMENT SYSTEM - DEFINED BENEFIT PLANS - PROCEDURES AND GUIDELINES FOR DETERMINING QUALIFIED STATUS OF A DOMESTIC RELATIONS ORDER I. INTRODUCTION The State Employees Retirement System

STATE EMPLOYEES RETIREMENT SYSTEM - DEFINED BENEFIT PLANS - PROCEDURES AND GUIDELINES FOR DETERMINING QUALIFIED STATUS OF A DOMESTIC RELATIONS ORDER I. INTRODUCTION The State Employees Retirement System

Summary Plan Description

Summary Plan Description Prepared for The College of Wooster Defined Contribution Plan July 2011 TABLE OF CONTENTS INTRODUCTION...3 ELIGIBILITY...4 A. Am I eligible to participate in the Plan?...4 B. What

Summary Plan Description Prepared for The College of Wooster Defined Contribution Plan July 2011 TABLE OF CONTENTS INTRODUCTION...3 ELIGIBILITY...4 A. Am I eligible to participate in the Plan?...4 B. What

PRELIMINARY DRAFT No. 3036 PREPARED BY LEGISLATIVE SERVICES AGENCY 2013 GENERAL ASSEMBLY DIGEST

*PD3036* PRELIMINARY DRAFT No. 3036 PREPARED BY LEGISLATIVE SERVICES AGENCY 2013 GENERAL ASSEMBLY DIGEST Citations Affected: IC 5-10.2-4-7; IC 5-10.3-8-15; IC 5-10.4-5; IC 5-10.5. Synopsis: Indiana public

*PD3036* PRELIMINARY DRAFT No. 3036 PREPARED BY LEGISLATIVE SERVICES AGENCY 2013 GENERAL ASSEMBLY DIGEST Citations Affected: IC 5-10.2-4-7; IC 5-10.3-8-15; IC 5-10.4-5; IC 5-10.5. Synopsis: Indiana public

Annuity Payment Plans

Member s Guide to: Annuity Payment Plans Members Guide to: Annuity Payment Plans www.op-f.org At retirement, you are faced with the important decision of choosing an annuity payment plan that can directly

Member s Guide to: Annuity Payment Plans Members Guide to: Annuity Payment Plans www.op-f.org At retirement, you are faced with the important decision of choosing an annuity payment plan that can directly

MassMutual Single Premium Immediate Annuity

ANNUITIES MassMutual Single Premium Immediate Annuity Retirement Can Be An Exciting Journey INVEST INSURE RETIRE Peter and Gail Doherty will celebrate their 40th wedding anniversary later this year. When

ANNUITIES MassMutual Single Premium Immediate Annuity Retirement Can Be An Exciting Journey INVEST INSURE RETIRE Peter and Gail Doherty will celebrate their 40th wedding anniversary later this year. When

The individual. A Resource for Your Retirement

Retirement today requires more planning than for previous generations. Americans are living longer many will live 20 to 30 years or more in retirement. Finding a way to make savings last over such a long

Retirement today requires more planning than for previous generations. Americans are living longer many will live 20 to 30 years or more in retirement. Finding a way to make savings last over such a long