American General Life Companies UPDATE. Reminder: Notice and Consent Requirements for Employer-Owned Life Insurance Remain in Effect

|

|

|

- Norma Norman

- 8 years ago

- Views:

Transcription

1 American General Life Companies UPDATE MARKETING July 21, 2011 Bulletin Reminder: Notice and Consent Requirements for Employer-Owned Life Insurance Remain in Effect Accessible. Accountable. Aligned. American General s Service Promise This bulletin is to remind you that the new requirements for employer-owned life insurance passed by the Pension Protection Act are now in effect. Failure to follow these requirements will result in the death benefi t of employer-owned life insurance becoming income-taxable upon the death of the insured. What needs to be done To avoid having income tax imposed on the death benefi t of an employer-owned life insurance policy, the employer must comply with the notice and consent requirements of the Act. Our September 2006 Advanced Sales Digest, posted on our Web site under Sales & Marketing/Advanced Sales/Executive Benefits/Producer Materials, offers a more detailed explanation of the requirements. Note that, in essence, any sort of key employee life insurance, life insurance used to fund a buy and sell arrangement, or non-qualifi ed deferred compensation arrangement can be subject to these requirements, so careful attention needs to be given to this review. There is a copy of this particular Advanced Sales Digest attached to this bulletin. Additionally, for the convenience of your client s legal counsel, we created and posted specimen notice and consent documents to assist an employer in complying with the notice and consent requirements of the Act. Additional questions should be directed to the Advanced Sales Team at (800) American General Life Companies, is the marketing name for a group of affi liated domestic life insurers, including American General Life Insurance Company and The United States Life Insurance Company in the City of New York. FOR PRODUCER USE ONLY NOT FOR DISSEMINATION TO THE PUBLIC

2 Informational ideas important to large and complex cases PARTNERING FOR EXCELLENCE Advanced Sales Vol II, Issue 4 Sept 2006 THE PENSION PROTECTION ACT OF 2006: NEW REQUIREMENTS FOR EMPLOYER-OWNED LIFE INSURANCE by Ed Sanchez, CLU, ChFC, MBA MSFS Advanced Sales Consultant AIG Life Brokerage The Pension Protection Act of 2006 was signed into law on August 17, Like most bills which Congress passes, this one did not limit itself to the topic which its title might suggest. Among its many provisions are changes to pensions, Individual Retirement Accounts, charitable giving, and employer-owned life insurance contracts. Because of its significant impact on employer owned life insurance, this Advanced Sales Digest focuses exclusively on the new employer owned life insurance requirements and the sales opportunities created by these provisions. What is employer-owned life insurance? An employer-owned life insurance contract is generally one which is owned by a person engaged in a trade or business and such person is directly or indirectly a beneficiary of the contract, and it covers the life of an insured who is an employee of the trade or business on the date the contract is issued. In essence, any sort of key employee life insurance, or any life insurance used to fund a stock redemption plan or informally fund a nonqualified deferred compensation plan can be covered by the Act. New Section 101(j) A new Code Section101(j) applies to company-owned life insurance (COLI) and Bank-Owned Life Insurance (BOLI) for policies issued after the date of enactment, August 17, Generally, it provides that, for employer owned life insurance, the amount excluded as an income tax free death benefit cannot exceed the premiums plus any other amounts paid by the policyholder for the contract. The excess over this amount is taxable income. Important exceptions to this income inclusion are built into the Act. A set of exception rules is included, and, also the notice and consent requirements which must be met. Let s take a look at the details. Exceptions Exceptions allow the death benefit of an employer-owned life insurance contract to be fully paid income tax free. First, one or more of the following must apply: 1) The insured must have been an employee at any time during the 12 months prior to his or her death, 2) the insured was a director or highly compensated employee at the time the contract was issued. In other words, the insured must have been a director, a 5 percent or greater owner at any time during the preceding year, or, have received in excess of $95,000 in the preceding year (adjusted for continued on next page For agent use only. Not for public dissemination.

3 inflation), or was one of the five highest paid officers, or among the highest paid 35 percent of all employees, or 3) death benefits are paid to a member of the insured s family, an individual designated by the insured (other than the employer), a trust established by any such person, or the insured s estate. Second, all three of the following notice and consent requirements must be met. Note that all three requirements must be met prior to the issuance of the COLI contract: 1) the employee must be notified in writing that the employer intends to insure the employee s life. The notice must state the maximum face amount for which the employee could be insured at the time the contract is issued. 2) the employee must provide the employer with written consent to being the insured and that the employer may continue the coverage after the employee terminates employment, and 3) the employee must be informed in writing that the employer will be the beneficiary of any death benefits, and the maximum amount of insurance for which the employee could be insured at issue is stated at the time of notification. Reporting and record keeping requirements (Section 60391) Employers who own one or more policies subject to this act issued after the date of enactment (August 17, 2006) are required to file an informational return with the Internal Revenue Service for each year that the contracts are owned. The filing must include: Thus, an employer will need to file some information regarding these policies at some unknown deadline each year. Currently, the IRS has offered no further guidance on this reporting or record keeping requirement. Effective Dates Section 101(j) rules generally apply to employer-owned contracts issued after August 17, 2006, the date of enactment. Opportunities Although these requirements add additional employer paperwork requirements for employer-owned life contracts, the needs for and benefits of employer-owned life insurance continue to far outweigh these requirements. The opportunities today lie in making prospective clients and their counsel aware of the new requirements, and staying abreast of additional guidance from the IRS as it becomes available. Updates and additional information helpful to your employer-owned sale will be forthcoming soon on the AIG Life Brokerage Web site. Stay tuned. This is a very general discussion of the provisions of the new law. No agent or client can rely on this as legal or tax advice. Each business must review these rules with advisors to determine how they apply to the unique situation of each business. For producer use only. Not for use with the public. 1) the number of employees at the end of the year, 2) the number of employees insured at the end of the year, 3) the total amount of insurance in force at the end of the year, 4) the employer s name, address, taxpayer ID number, and the nature of the employer s business, 5) that the employer has valid consent for each insured and the number of insured employees for whom such consent was not obtained. For Agent Use Only - Not for Dissemination to the Public. AIG Life Brokerage 1200 N. Mayfair Rd. Suite 300 Milwaukee WI /

4 Please Note: This is a specimen document provided for the convenience of legal counsel retained by employers contemplating the purchase and ownership of life insurance on an employee s life. The contents of this specimen document do not constitute and may not serve to provide legal, tax or accounting advice to any party to the agreement or their respective legal, tax or accounting counsel. Parties contemplating participation in any agreements or arrangements described below should consult and rely upon their own legal, tax and accounting counsel to determine the appropriate use of this specimen document or any portion thereof. NOTICE TO EMPLOYEE OF EMPLOYER S INTENT TO OBTAIN LIFE INSURANCE COVERAGE This Notice is provided by (name of employer) Employer to (name of employee) Employee. Pursuant to this Notice, Employee is hereby notified that, because of Employee s economic value to Employer, the Employer seeks to obtain one or more life insurance policies insuring the life of the Employee constituting a maximum face amount of (face amount in numbers), (face amount in words) (the Policy ), subject to Employee s written acknowledgement and consent that: 1. Employee understands and acknowledges that Employer may be the sole owner and beneficiary of any and all economic benefits derived from Employer s ownership of the Policy. 2. Employee understands and acknowledges that Employer may retain and continue all incidents, rights and benefits of ownership of the Policy and continue the insurance coverage purchased on the life of Employee after Employee s separation from service or termination of employment with Employer. 3. Employee understands and acknowledges that if the Policy is issued, Employee s ability to procure additional life insurance on his/her life may be limited. 4. Employee understands and acknowledges that Employer, as policy owner, may have access to non-public and personally identifiable information collected during the insurance application process. I have received, read, and understand this notice: Employee Date

5 Acknowledged and Received by Employer: Employer s Authorized Representative Date Please Note: This is a specimen document provided for the convenience of legal counsel retained by employers contemplating the purchase and ownership of life insurance on an employee s life. The contents of this specimen document do not constitute and may not serve to provide legal, tax or accounting advice to any party to the agreement or their respective legal, tax or accounting counsel. Parties contemplating participation in any agreements or arrangements described below should consult and rely upon their own legal, tax and accounting counsel to determine the appropriate use of this specimen document or any portion thereof. EMPLOYEE CONSENT TO EMPLOYER OWNED LIFE INSURANCE Part One I, (name of employee), Employee, acknowledge that I have been notified in writing on (date of notice) that (name of employer), Employer, intends to purchase, own and maintain one or more life insurance policies insuring my life constituting a maximum face amount of (face amount in numbers) $, (face amount in words), (the Policy ). I hereby acknowledge and consent to the following: 1. I consent and agree to be the named insured under the Policy and understand that my ability to obtain additional insurance on my life in the future may be limited; 2. I consent and agree to undergo necessary and reasonable examinations with respect to Employer s acquisition of the Policy and to participate in good faith with respect to necessary and reasonable acts required by an insurer in order for the Employer to acquire the Policy;

6 3. I consent and agree, subject to the extent of any applicable laws 1, that Employer may retain all incidents, rights and benefits of ownership of the Policy, and continue the insurance coverage procured under the Policy after my separation from service or termination of employment with Employer; 4. I consent and agree to provide in timely manner all information requested by Employer and the insurer in connection with the issuance of the Policy; and 5. I consent and agree to an insurer s access to non-public personally identifiable information collected during the insurance application process. Part Two As of the anticipated issue date of (state the anticipated issue date), I expect to be (initial any applicable phrase(s)): 1. A director of Employer. 2. A five percent (5%) or greater owner of Employer at any time during the preceding year. 3. A recipient of more than $95,000 in compensation from Employer in the preceding year. 4. One of the five highest paid officers of Employer. 5. Among the highest paid 35% of all employees of Employer. Part Three I acknowledge that on the date of this Consent a representative of Employer met with me personally to review and explain the provisions of this Consent. Said representative answered my questions in terms that were understandable to me. I also understand and acknowledge that upon my death, unless otherwise mutually agreed to by Employer and me, Employer shall pay to my personally named beneficiary or beneficiaries the sum of (dollar amount or a percentage of the Policy death benefit payable) from the Policy death proceeds. Any proceeds paid under the Policy as a result of my death that exceed such stated amount shall be payable to Employer or its successor(s), assignee(s), beneficiary or beneficiaries. 1 State statutes may provide specific guidance with respect to the rights of employees consenting to serve as insureds under life insurance policies issued to and owned by their employers. Employees should retain independent legal counsel for advice with respect to the application of any such laws or statutes in their respective states of residence and/or employment.

7 This Consent is hereby entered into on the day and date listed below. Employee Date Acknowledged and Received by Employer: Employer s Authorized Representative Date

8 Informational ideas important to large and complex cases Advanced Sales Vol IV, Issue 1 March 2008 IRS ISSUES ANNUAL REPORTING FORM FOR EMPLOYER-OWNED LIFE INSURANCE by Ed Sanchez, CLU, ChFC, MBA, MSFS Section 101(j) of the Internal Revenue Code requires that, in order for the death proceeds of an employer-owned life insurance policy to be 100 percent income tax-free, the policy must satisfy certain statutory requirements. Passed in August 2006 as part of the Pension Protection Act, these requirements apply to employers who own or receive any benefit from life insurance on an employee s life. Most commonly, the requirements would apply to any key person life insurance, life insurance used for entity buy-sell purposes, or economic benefit regime split dollar life insurance (previously known as endorsement split dollar). Note that the form of business entity is irrelevant; the requirements apply to all employers whether they are corporations, pass through entities, or any other business form. Furthermore, it applies to any form of life insurance, including term, universal life, whole life, or any form of variable life or variable universal life which may be considered employer owned life insurance. BACKGROUND The Pension Protection Act of 2006 was signed into law on August 17, Among its many provisions were changes to pensions, Individual Retirement Accounts, charitable giving, and employer-owned life insurance contracts. What is employer-owned life insurance? An employer-owned life insurance contract is generally one which is owned by a person engaged in a trade or business and such person is directly or indirectly a beneficiary of the contract, and it covers the life of an insured who is an employee of the trade or business on the date the contract is issued. In essence, any sort of key employee life insurance, or any life insurance used to fund a stock redemption plan or informally fund a non-qualified deferred compensation plan, can be covered by the Act. Section 101(j) IRC Code Section 101(j) applies to company-owned life insurance (COLI) and Bank-Owned Life Insurance (BOLI) for policies issued after the date of enactment, August 17, Generally, it provides that, for employer owned life insurance, the amount excluded as an income tax free death benefit cannot exceed the premiums plus any other amounts paid by the policyholder for the contract. The excess over this amount is taxable income. continued on next page For agent use only. Not for public dissemination.

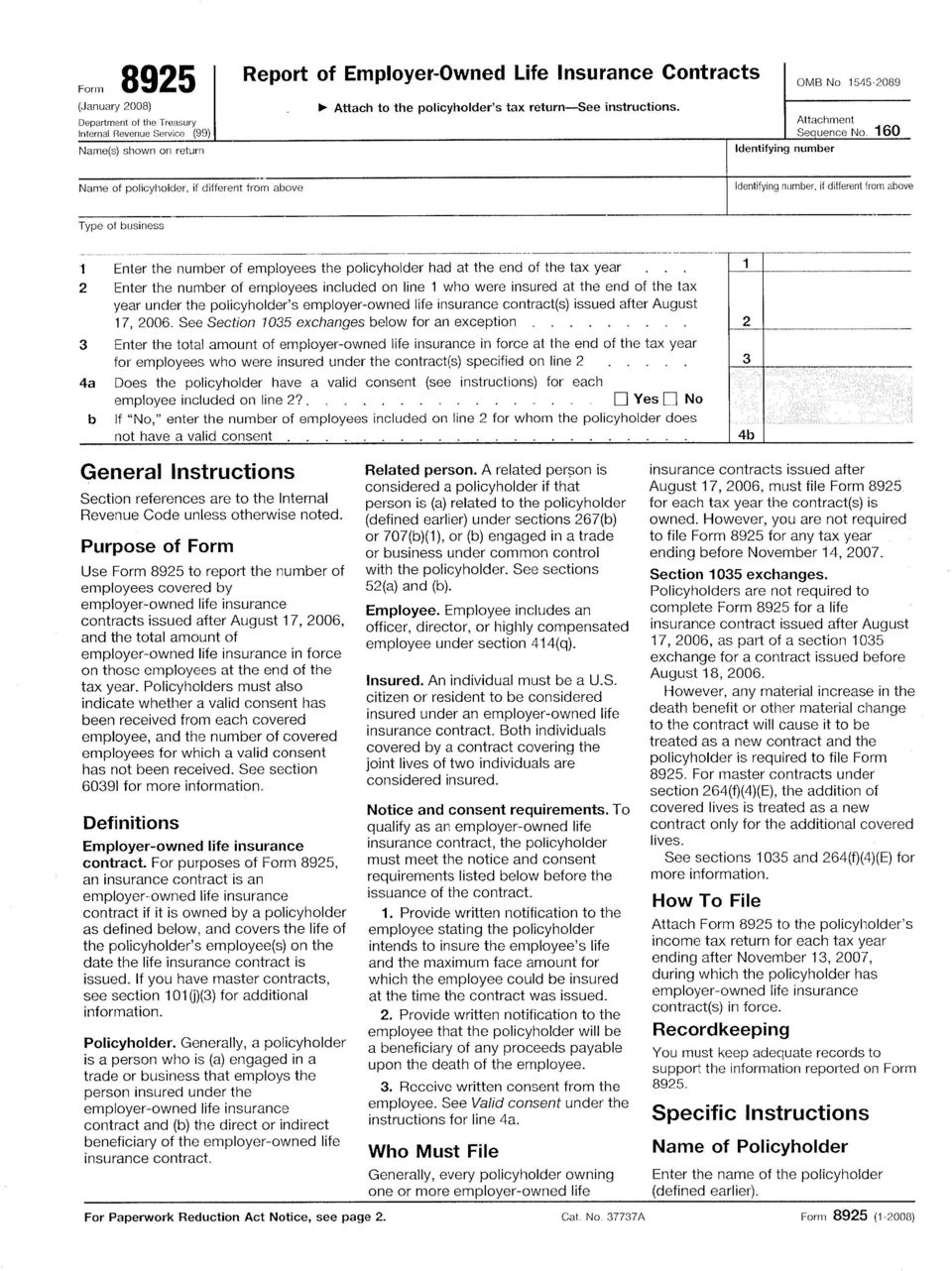

9 Important exceptions to this income inclusion are built into the Act. A set of exception rules is included, and, also the notice and consent requirements which must be met. Let s take a look at the details. EXCEPTIONS Exceptions allow the death benefit of an employer-owned life insurance contract to be fully paid income tax free. First, one or more of the following must apply: A) The insured must have been an employee at any time during the 12 months prior to his or her death; B) The insured was a director or highly compensated employee at the time the contract was issued. In other words, the insured must have been a director, a 5 percent or greater owner at any time during the preceding year, or, have received in excess of $105,000 in the preceding year (adjusted for inflation), or was one of the five highest paid officers, or among the highest paid 35 percent of all employees, or; C) Death benefits are paid to a member of the insured s family, an individual designated by the insured (other than the employer), a trust established by any such person, or the insured s estate. Second, ALL three of the following notice and consent requirements MUST be met. Note that all three requirements must be met prior to the issuance of the COLI contract: 1) The employee must be notified in writing that the employer intends to insure the employee s life. The notice must state the maximum face amount for which the employee could be insured at the time the contract is issued. 2) The employee must provide the employer with written consent to being the insured and that the employer may continue the coverage after the employee terminates employment, and; 3) The employee must be informed in writing that the employer will be the beneficiary of any death benefits, and the maximum amount of insurance for which the employee could be insured at issue, is stated at the time of notification. WHAT HAPPENS IF AN EMPLOYER DOES NOT COMPLY If the notice and consent requirements are not met by an employer, it will cause the policy death benefits in excess of premiums paid to become income taxable to the employer. Furthermore, unfortunately the Act or associated IRS regulations do not provide a remedy for correcting the error of not completing the forms prior to the date the policy is placed in force. Therefore, it is critical to be aware of these requirements and make your employer clients aware of the requirements. NEW REPORTING FORM IS ISSUED As a complementary provision to Section 101(j), Congress enacted section 6039I, which established reporting requirements with respect to employer-owned life insurance contracts. The Internal Revenue Service has now issued the reporting form that policyholders should complete and attach to their Form 1120 (or other tax form) on which they will be reporting their income taxes. The form is Form 8925 Report of Employer Owned Life Insurance Contracts. This IRS form is available by clicking on the hyperlink to the official forms site of the U.S. Government ( The hyperlink is located at Advanced Sales/Employer Owned Life Insurance. continued on next page

10 Sales opportunity: Making lemonade from lemons This represents another tremendous opportunity to bring extremely relevant, vital insurance information to business clients and prospects and thus create the opportunity to review all of their business life insurance needs: key person, buy and sell, deferred compensation, and others. Bringing these requirements to an employer s attention demonstrates your higher insurance knowledge level and should help create an enhanced trust relationship with your business client or prospect. Form 8925 is very straightforward. It consists of four lines which request 1) the number of employees of the employer; 2) the number of insured employees (those with policies issued after August 17, 2006) who were insured at the end of the tax year; 3) the total amount of employer-owned life insurance in force at the end of the tax year; and 4) whether the employer/policy holder has a valid consent for each employee. That s it. An important note: Even though the statute was effective for contracts issued after August 17, 2006, the Form 8925 does not require any reporting for any tax year ending before November 14, American General Life Insurance Company is solely a provider of insurance products. American General Life Insurance Company, its employees, agents, and/or representatives do not provide tax, legal or financial advice. The comments made in this article are for information/discussion purposes only. Any questions you may have should be discussed with your tax or legal advisor. For Agent Use Only - Not for Dissemination to the Public. AIG American General 1200 N. Mayfair Rd. Suite 300 Milwaukee WI /

11

12

13

LIFE INSURANCE TAXED? 101(J) Millennium Brokerage Group

Millennium Brokerage Group") LIFE INSURANCE TAXED? 101(J) Millennium Brokerage Group WHAT TO EXPECT... Death benefits on policies insuring employees of a business will be taxed as income unless the new rules are followed. 101(j) applies

LIFE INSURANCE TAXED? 101(J) Millennium Brokerage Group WHAT TO EXPECT... Death benefits on policies insuring employees of a business will be taxed as income unless the new rules are followed. 101(j) applies

Key Employee Life Insurance Forward to Counsel and Specimen Documents

Key Employee Life Insurance Forward to Counsel and Specimen Documents Contents 2 I) Introduction 2 II) Strategy/Technique Structure 3 III) Income Tax Implications 3 A. Taxation of the Premiums 3 B. Taxation

Key Employee Life Insurance Forward to Counsel and Specimen Documents Contents 2 I) Introduction 2 II) Strategy/Technique Structure 3 III) Income Tax Implications 3 A. Taxation of the Premiums 3 B. Taxation

LIFE INSURANCE PLANNING FOR CLOSELY- HELD BUSINESS

LIFE INSURANCE PLANNING FOR CLOSELY- HELD BUSINESS BY JOSHUA E. HUSBANDS PORTLAND OFFICE 2300 US BANCORP TOWER 111 SW FIFTH AVENUE PORTLAND, OREGON 97204 503-243-2300 503-241-8014 joshua.husbands@hklaw.com

LIFE INSURANCE PLANNING FOR CLOSELY- HELD BUSINESS BY JOSHUA E. HUSBANDS PORTLAND OFFICE 2300 US BANCORP TOWER 111 SW FIFTH AVENUE PORTLAND, OREGON 97204 503-243-2300 503-241-8014 joshua.husbands@hklaw.com

S CORPORATION STOCK REDEMPTION BUY-SELL (INCLUDING DISABILITY) (INCORPORATING THE SHORT TAX YEAR TECHNIQUE)

(INCORPORATING THE SHORT TAX YEAR TECHNIQUE)") S CORPORATION STOCK REDEMPTION BUY-SELL (INCLUDING DISABILITY) (INCORPORATING THE SHORT TAX YEAR TECHNIQUE) TECHNICAL PREFACE Life Insurance proceeds received by a C Corporation to fund a Stock Redemption

S CORPORATION STOCK REDEMPTION BUY-SELL (INCLUDING DISABILITY) (INCORPORATING THE SHORT TAX YEAR TECHNIQUE) TECHNICAL PREFACE Life Insurance proceeds received by a C Corporation to fund a Stock Redemption

Business Succession Planning

Business Succession Planning with Key Person Coverage and Buy-Sell Agreements Program Highlights & Fact Finder You put maximum effort into establishing and running your business. But are you taking the

Business Succession Planning with Key Person Coverage and Buy-Sell Agreements Program Highlights & Fact Finder You put maximum effort into establishing and running your business. But are you taking the

Coordinating Corporate Dollars

Coordinating Corporate Dollars A review of various ways you can use your corporate dollars to attract, retain and reward key personnel, to help meet your goals of business continuity and tax efficiency.

Coordinating Corporate Dollars A review of various ways you can use your corporate dollars to attract, retain and reward key personnel, to help meet your goals of business continuity and tax efficiency.

Global Benefits & Compensation

ALBANY AMSTERDAM ATLANTA AUSTIN BOSTON CHICAGO DALLAS DELAWARE DENVER FORT LAUDERDALE HOUSTON LAS VEGAS LONDON* LOS ANGELES MIAMI NEW JERSEY NEW YORK ORANGE COUNTY ORLANDO PALM BEACH COUNTY PHILADELPHIA

ALBANY AMSTERDAM ATLANTA AUSTIN BOSTON CHICAGO DALLAS DELAWARE DENVER FORT LAUDERDALE HOUSTON LAS VEGAS LONDON* LOS ANGELES MIAMI NEW JERSEY NEW YORK ORANGE COUNTY ORLANDO PALM BEACH COUNTY PHILADELPHIA

This Notice provides guidance concerning the treatment of employer-owned

Part III - Administrative, Procedural, and Miscellaneous Treatment of Certain Employer-Owned Life Insurance Contracts Notice 2009-48 PURPOSE This Notice provides guidance concerning the treatment of employer-owned

Part III - Administrative, Procedural, and Miscellaneous Treatment of Certain Employer-Owned Life Insurance Contracts Notice 2009-48 PURPOSE This Notice provides guidance concerning the treatment of employer-owned

Life Insurance: Business Applications

Life Insurance: Business Applications What is business life insurance? Life insurance is an important part of a business. It may be used as a funding mechanism for your buy-sell agreement and as business

Life Insurance: Business Applications What is business life insurance? Life insurance is an important part of a business. It may be used as a funding mechanism for your buy-sell agreement and as business

Nonqualified Deferred Compensation Plans Why Administration Matters

Nonqualified Deferred Compensation Plans Why Administration Matters By: Howard D. Stern, FSA Vice President & Actuary The Pangburn Company HOWARD D. STERN, FSA is Vice President and Actuary with the Pangburn

Nonqualified Deferred Compensation Plans Why Administration Matters By: Howard D. Stern, FSA Vice President & Actuary The Pangburn Company HOWARD D. STERN, FSA is Vice President and Actuary with the Pangburn

Bank Owned Life Insurance. Kirk A. Pelikan 414-223-2529 kapelikan@michaelbest.com

Bank Owned Life Insurance Kirk A. Pelikan 414-223-2529 kapelikan@michaelbest.com BOLI: The Basics BOLI is a life insurance policy purchased by a bank to insure the life of a certain employee. Product has

Bank Owned Life Insurance Kirk A. Pelikan 414-223-2529 kapelikan@michaelbest.com BOLI: The Basics BOLI is a life insurance policy purchased by a bank to insure the life of a certain employee. Product has

Business Su c c e s s i o n Pl a n n i n g

Business Su c c e s s i o n Pl a n n i n g w i t h Key Pe r s o n Co v e r a g e and Buy-Sell Agreements Program Highlights & Fact Finder You put maximum effort into establishing and running your business.

Business Su c c e s s i o n Pl a n n i n g w i t h Key Pe r s o n Co v e r a g e and Buy-Sell Agreements Program Highlights & Fact Finder You put maximum effort into establishing and running your business.

The Pension Protection Act of 2006 New EOLI Legislation Potentially Taxes Typical Insurance Arrangements

ALERT: Tax December 2006 EOLI Legislation Potentially Taxes Typical Our previous Alert, The Pension Protection Act of 2006 Changes Affecting Life Insurance Products, reviewed legislation under the Pension

ALERT: Tax December 2006 EOLI Legislation Potentially Taxes Typical Our previous Alert, The Pension Protection Act of 2006 Changes Affecting Life Insurance Products, reviewed legislation under the Pension

Business Insurance: Split Dollar Life Insurance

Element Insurance Partners 13520 California Street Suite 290 Omaha, NE 68154 402-614-2661 dhenry@elementinsurancepartners.com www.elementinsurancepartners.com Business Insurance: Split Dollar Life Insurance

Element Insurance Partners 13520 California Street Suite 290 Omaha, NE 68154 402-614-2661 dhenry@elementinsurancepartners.com www.elementinsurancepartners.com Business Insurance: Split Dollar Life Insurance

Twelve Life Insurance Mistakes that Aren t Cheaper by the Dozen. IFS-A156125 Ed. 11/08 Exp. 11/10

Twelve Life Insurance Mistakes that Aren t Cheaper by the Dozen IFS-A156125 Ed. 11/08 Exp. 11/10 1 This material has been prepared by The Prudential Insurance Company of America. It is designed to provide

Twelve Life Insurance Mistakes that Aren t Cheaper by the Dozen IFS-A156125 Ed. 11/08 Exp. 11/10 1 This material has been prepared by The Prudential Insurance Company of America. It is designed to provide

Insurance-Related Best Practices Guide for Buy-Sell Agreements

Insurance-Related Best Practices Guide for Buy-Sell Agreements The buy-sell agreement review and feedback process at the Principal Financial Group has allowed us to observe many different drafting approaches

Insurance-Related Best Practices Guide for Buy-Sell Agreements The buy-sell agreement review and feedback process at the Principal Financial Group has allowed us to observe many different drafting approaches

Comprehensive Split Dollar

Advanced Markets Client Guide Comprehensive Split Dollar Crafting a plan to meet your needs. John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company New York (John

Advanced Markets Client Guide Comprehensive Split Dollar Crafting a plan to meet your needs. John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company New York (John

Understanding the Income Taxation of Life Insurance

A Reference Guide for Individuals and Businesses Understanding the Income Taxation of Life Insurance Answers to Frequently Asked Questions Tax Insights Contents 1 General Questions 4 Non-MEC Policy Questions

A Reference Guide for Individuals and Businesses Understanding the Income Taxation of Life Insurance Answers to Frequently Asked Questions Tax Insights Contents 1 General Questions 4 Non-MEC Policy Questions

White Paper Corporate Owned Life Insurance

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

FREQUENTLY ASKED QUESTIONS BUSINESS CONTINUATION

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA BUSINESS STRATEGIES Key Person Life Insurance FREQUENTLY ASKED QUESTIONS BUSINESS CONTINUATION When should a business and its owners consider buying insurance

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA BUSINESS STRATEGIES Key Person Life Insurance FREQUENTLY ASKED QUESTIONS BUSINESS CONTINUATION When should a business and its owners consider buying insurance

Side-by-Side Business Insurance Plan Comparisons

Side-by-Side Insurance Plan Comparisons Small Strategies & Solutions Protect and grow your business with proper planning The success of your business is based on your hard work and the efforts of key employees.

Side-by-Side Insurance Plan Comparisons Small Strategies & Solutions Protect and grow your business with proper planning The success of your business is based on your hard work and the efforts of key employees.

AALU Bulletin No: 08-22 March 6, 2008 Subject: Section 101(j) Review

Review") Premier analysis of federal legislative and regulatory developments for the nation s 2,000 most advanced life insurance planners, focusing on business, estate, qualified and nonqualified retirement planning.

Premier analysis of federal legislative and regulatory developments for the nation s 2,000 most advanced life insurance planners, focusing on business, estate, qualified and nonqualified retirement planning.

The trusted source of actionable technical and marketplace knowledge for AALU members the nation s most advanced life insurance professionals.

The trusted source of actionable technical and marketplace knowledge for AALU members the nation s most advanced life insurance professionals. This report has been prepared exclusively for Albert Gibbons,

The trusted source of actionable technical and marketplace knowledge for AALU members the nation s most advanced life insurance professionals. This report has been prepared exclusively for Albert Gibbons,

Executive Benefits for Nonprofit & Tax-Exempt Organizations

Executive Benefits for Nonprofit & Tax-Exempt Organizations Recruit, Retain, and Reward Your Top Talent with Nonqualified Retirement or Estate Planning Benefits As a nonprofit or tax-exempt organization,

Executive Benefits for Nonprofit & Tax-Exempt Organizations Recruit, Retain, and Reward Your Top Talent with Nonqualified Retirement or Estate Planning Benefits As a nonprofit or tax-exempt organization,

Notice 97-34, 1997-1 CB 422, 6/02/1997, IRC Sec(s). 6048

. 6048") Notice 97-34, 1997-1 CB 422, 6/02/1997, IRC Sec(s). 6048 Returns of foreign trusts foreign gift reporting requirements tax This notice provides guidance regarding the new foreign trust and foreign gift

Notice 97-34, 1997-1 CB 422, 6/02/1997, IRC Sec(s). 6048 Returns of foreign trusts foreign gift reporting requirements tax This notice provides guidance regarding the new foreign trust and foreign gift

Effective Planning with Life Insurance

Effective Planning with Life Insurance The Tax Considerations... Ken Knox, CLU, ChFC Regional Director The Penn Mutual Life Insurance Company 1304529TM_Sept17 Retirement Planning Case Scenario #1... Client

Effective Planning with Life Insurance The Tax Considerations... Ken Knox, CLU, ChFC Regional Director The Penn Mutual Life Insurance Company 1304529TM_Sept17 Retirement Planning Case Scenario #1... Client

Endorsement Split-Dollar

Endorsement Split-Dollar Allowing an Executive to Share in the Benefits of an Employer-Owned Life Insurance Policy AD-OC-859A Endorsement Split-Dollar Searching for Executive Benefit Solutions Retaining

Endorsement Split-Dollar Allowing an Executive to Share in the Benefits of an Employer-Owned Life Insurance Policy AD-OC-859A Endorsement Split-Dollar Searching for Executive Benefit Solutions Retaining

32 Irrevocable Life Insurance Trusts 2.1

2 Income Tax Issues CHAPTER OVERVIEW This chapter discusses selected key income tax issues concerning life insurance and ILITs. 1 Recent changes in the Internal Revenue Code now permit an insured to receive

2 Income Tax Issues CHAPTER OVERVIEW This chapter discusses selected key income tax issues concerning life insurance and ILITs. 1 Recent changes in the Internal Revenue Code now permit an insured to receive

DIVORCE AND LIFE INSURANCE, QUALIFIED PLANS AND IRAS 2013-2015

DIVORCE AND LIFE INSURANCE, QUALIFIED PLANS AND IRAS 2013-2015 I. INTRODUCTION In a divorce, property is generally divided between the spouses. Generally, all assets of the spouses, whether individual,

DIVORCE AND LIFE INSURANCE, QUALIFIED PLANS AND IRAS 2013-2015 I. INTRODUCTION In a divorce, property is generally divided between the spouses. Generally, all assets of the spouses, whether individual,

Protect your business, your family, and your legacy.

An Educational Guide for Business Owners Protect your business, your family, and your legacy. Take a closer look at buy-sell agreements. Needs-based Strategies Your business is probably your single largest

An Educational Guide for Business Owners Protect your business, your family, and your legacy. Take a closer look at buy-sell agreements. Needs-based Strategies Your business is probably your single largest

Executive Bonus Arrangements using Life Insurance. Producer Guide. For agent use only. Not for public distribution.

Executive Bonus Arrangements using Life Insurance Producer Guide For agent use only. Not for public distribution. Executive Bonus Arrangements using Life Insurance To remain competitive and profitable,

Executive Bonus Arrangements using Life Insurance Producer Guide For agent use only. Not for public distribution. Executive Bonus Arrangements using Life Insurance To remain competitive and profitable,

Non-Qualifi ed Fringe Benefi t Planning

Employee benefi t packages are increasingly viewed as an important form of compensation. The right mix of salary and other benefits can attract, and keep, top-quality employees. Non-Qualifi ed Fringe Benefi

Employee benefi t packages are increasingly viewed as an important form of compensation. The right mix of salary and other benefits can attract, and keep, top-quality employees. Non-Qualifi ed Fringe Benefi

Key Person Insurance. Protect your business from the loss of a key person with life insurance payable to the business.

Key Person Insurance Protect your business from the loss of a key person with life insurance payable to the business. We offer you this concept piece to help you understand how life insurance can be used

Key Person Insurance Protect your business from the loss of a key person with life insurance payable to the business. We offer you this concept piece to help you understand how life insurance can be used

KEY FACTORS WHEN CONSIDERING A ROTH IRA CONVERSION

KEY FACTORS WHEN CONSIDERING A ROTH IRA CONVERSION PERTINENT INFORMATION Mr. Kugler has accumulated $1,000,000 in a traditional IRA. Mrs. Kugler is the designated beneficiary (DB) and their daughter is

KEY FACTORS WHEN CONSIDERING A ROTH IRA CONVERSION PERTINENT INFORMATION Mr. Kugler has accumulated $1,000,000 in a traditional IRA. Mrs. Kugler is the designated beneficiary (DB) and their daughter is

Taxation of Business Owned Life Insurance: The Trap is Set. By Joshua E. Husbands

Taxation of Business Owned Life Insurance: The Trap is Set By Joshua E. Husbands Life insurance has long been accepted and regarded as a valuable tool in planning for business contingencies and succession.

Taxation of Business Owned Life Insurance: The Trap is Set By Joshua E. Husbands Life insurance has long been accepted and regarded as a valuable tool in planning for business contingencies and succession.

A Selective Executive Retirement Plan

A Selective Executive Retirement Plan Since salary alone is often not enough, what can a corporation do to retain its existing key executives and attract new ones? Table of Contents Page Dual Problems

A Selective Executive Retirement Plan Since salary alone is often not enough, what can a corporation do to retain its existing key executives and attract new ones? Table of Contents Page Dual Problems

Life Insurance: Business Applications

Infinex Financial Group located at The Milford Bank John A. Kuehnle Financial Professional 33 Broad Street Milford, CT 06460 203-783-5782 jkuehnle@infinexgroup.com http://www.milfordbank.com Life Insurance:

Infinex Financial Group located at The Milford Bank John A. Kuehnle Financial Professional 33 Broad Street Milford, CT 06460 203-783-5782 jkuehnle@infinexgroup.com http://www.milfordbank.com Life Insurance:

CHAPTER 9 BUSINESS INSURANCE

CHAPTER 9 BUSINESS INSURANCE Just as individuals need insurance for protection so do businesses. Businesses need insurance to cover potential property losses and liability losses. Life insurance also is

CHAPTER 9 BUSINESS INSURANCE Just as individuals need insurance for protection so do businesses. Businesses need insurance to cover potential property losses and liability losses. Life insurance also is

Life Insurance Income Taxation in brief

Life Insurance Income Taxation in brief Income Tax Treatment of Life Insurance Tax deferred growth Tax favored withdrawals Tax free death benefit Tax Deferred Growth Gain due to cash value growth in life

Life Insurance Income Taxation in brief Income Tax Treatment of Life Insurance Tax deferred growth Tax favored withdrawals Tax free death benefit Tax Deferred Growth Gain due to cash value growth in life

PRIVATE NON-EQUITY SPLIT DOLLAR INSURANCE AGREEMENT [For a Single Life Policy]

![PRIVATE NON-EQUITY SPLIT DOLLAR INSURANCE AGREEMENT [For a Single Life Policy]](/thumbs/26/9190936.jpg "PRIVATE NON-EQUITY SPLIT DOLLAR INSURANCE AGREEMENT [For a Single Life Policy]") PRIVATE NON-EQUITY SPLIT DOLLAR INSURANCE AGREEMENT [For a Single Life Policy] Form A Designed to meet split dollar definition in regulations Two alternatives: secured by, or to be made from Sample for

PRIVATE NON-EQUITY SPLIT DOLLAR INSURANCE AGREEMENT [For a Single Life Policy] Form A Designed to meet split dollar definition in regulations Two alternatives: secured by, or to be made from Sample for

Split-Dollar Insurance and the Closely Held Business By: Larry Brody, Esq., Richard Harris, CLU and Martin M. Shenkman, Esq.

Split-Dollar Insurance and the Closely Held Business By: Larry Brody, Esq., Richard Harris, CLU and Martin M. Shenkman, Esq. Introduction Split-dollar is a mechanism for owning and paying for life insurance

Split-Dollar Insurance and the Closely Held Business By: Larry Brody, Esq., Richard Harris, CLU and Martin M. Shenkman, Esq. Introduction Split-dollar is a mechanism for owning and paying for life insurance

Key Person Life in brief

Key Person Life in brief Key Person Life Insurance Key person life insurance is life insurance that a business owns on its valued and skilled employees to partially indemnify the business for the loss

Key Person Life in brief Key Person Life Insurance Key person life insurance is life insurance that a business owns on its valued and skilled employees to partially indemnify the business for the loss

Buy-Sell Planning. Succession Planning for Business Owners. Guiding you through life. SALES STRATEGY BUSINESS. Advanced Markets. Situation.

Guiding you through life. SALES STRATEGY BUSINESS Buy-Sell Planning Succession Planning for Owners Situation owners should plan to protect their business in case of the sudden death, retirement, or disability

Guiding you through life. SALES STRATEGY BUSINESS Buy-Sell Planning Succession Planning for Owners Situation owners should plan to protect their business in case of the sudden death, retirement, or disability

Key Employee Life Insurance Checklist

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA Key Employee Life Insurance Checklist The following checklist details the items that are generally needed to properly complete a key employee life insurance

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA Key Employee Life Insurance Checklist The following checklist details the items that are generally needed to properly complete a key employee life insurance

Blueprints for Business. Executive Bonus Arrangements Using Life Insurance Producer Guide. Your future. Made easier. SM LIFE

Blueprints for Business Executive Bonus Arrangements Using Life Insurance Producer Guide These materials are not intended to be used to avoid tax penalties and were prepared to support the promotion or

Blueprints for Business Executive Bonus Arrangements Using Life Insurance Producer Guide These materials are not intended to be used to avoid tax penalties and were prepared to support the promotion or

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions Life s better when we re connected Table of contents Find your questions review

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions Life s better when we re connected Table of contents Find your questions review

Salary Reduction Simplified Employee Pension (SAR-SEP) Plan Employer Adoption Agreement For Use with the Traditional IRA Application

Plan Employer Adoption Agreement For Use with the Traditional IRA Application") december 2011 Salary Reduction Simplified Employee Pension (SAR-SEP) Plan Employer Adoption Agreement For Use with the Traditional IRA Application Employer s Guide to the SAR-SEP Plan Salary Reduction

december 2011 Salary Reduction Simplified Employee Pension (SAR-SEP) Plan Employer Adoption Agreement For Use with the Traditional IRA Application Employer s Guide to the SAR-SEP Plan Salary Reduction

UNDERWRITING. Financial Underwriting Highlighter. What Is Financial Underwriting? WHY IS FINANCIAL UNDERWRITING IMPORTANT? INSURABLE INTEREST

CREATED EXCLUSIVELY FOR FINANCIAL PROFESSIONALS UNDERWRITING Financial Underwriting Highlighter What Is Financial Underwriting? Financial Underwriting is the evaluation of a prospective insured s personal

CREATED EXCLUSIVELY FOR FINANCIAL PROFESSIONALS UNDERWRITING Financial Underwriting Highlighter What Is Financial Underwriting? Financial Underwriting is the evaluation of a prospective insured s personal

White Paper Life Insurance Coverage on a Key Employee

White Paper Life Insurance Coverage on a Key Employee www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC,

White Paper Life Insurance Coverage on a Key Employee www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC,

S I M P L E. Savings incentive match plan for employees. Participant application kit

S I M P L E Savings incentive match plan for employees Participant application kit SIMPLE IRA PARTICIPANT INSTRUCTIONS Follow these instructions if you are an employee whose employer has an existing SIMPLE

S I M P L E Savings incentive match plan for employees Participant application kit SIMPLE IRA PARTICIPANT INSTRUCTIONS Follow these instructions if you are an employee whose employer has an existing SIMPLE

Business Planning. Buy/Sell Insurance. What would your business do without you?

Business Planning Buy/Sell Insurance What would your business do without you? 2 Add life to your business You know what it takes to run a successful company. But what would happen to your business if something

Business Planning Buy/Sell Insurance What would your business do without you? 2 Add life to your business You know what it takes to run a successful company. But what would happen to your business if something

Business Owner s Bonus Plan. Producer Guide. For agent/registered representative use only. Not for public distribution.

Business Owner s Bonus Plan Producer Guide For agent/registered representative use only. Not for public distribution. Business Owner s Bonus Plan Producer Guide The Business Owner s Bonus Plan is a personally

Business Owner s Bonus Plan Producer Guide For agent/registered representative use only. Not for public distribution. Business Owner s Bonus Plan Producer Guide The Business Owner s Bonus Plan is a personally

CORPORATE-OWNED LIFE INSURANCE (Last Updated 2/28/02)

") I. Applicability... 1 A. Scope... 1 B. Review Factors... 1 II. Special Filing Requirements... 1 A. Submission Letter... 1 III. Contract Provisions... 2 A. Group Life Insurance Exceptions For Employee Benefit

I. Applicability... 1 A. Scope... 1 B. Review Factors... 1 II. Special Filing Requirements... 1 A. Submission Letter... 1 III. Contract Provisions... 2 A. Group Life Insurance Exceptions For Employee Benefit

Premier Choice Annuity Application

Premier Choice Annuity Application Issued by First Security Benefit Life Insurance and Annuity Company of New York. Questions? Call our Customer Service Center at 1-800-888-2461. 1. Choose Type of Annuity

Premier Choice Annuity Application Issued by First Security Benefit Life Insurance and Annuity Company of New York. Questions? Call our Customer Service Center at 1-800-888-2461. 1. Choose Type of Annuity

ADVISING CLIENTS ABOUT LIFE INSURANCE: A PRIMER 1. By Andrew J. Willms, J.D. LL.M. John C. Zimdars, Jr., CLU ChFC. Introduction

ADVISING CLIENTS ABOUT LIFE INSURANCE: A PRIMER 1 By Andrew J. Willms, J.D. LL.M. John C. Zimdars, Jr., CLU ChFC Introduction Over the last several years, tax reform has made tax planning increasingly

ADVISING CLIENTS ABOUT LIFE INSURANCE: A PRIMER 1 By Andrew J. Willms, J.D. LL.M. John C. Zimdars, Jr., CLU ChFC Introduction Over the last several years, tax reform has made tax planning increasingly

Life Insurance in Qualified Plans. Producer Guide. For agent use only. Not for public distribution.

Life Insurance in Qualified Plans Producer Guide For agent use only. Not for public distribution. Life Insurance In Qualified Plans While qualified plans are a tremendous retirement savings vehicle, they

Life Insurance in Qualified Plans Producer Guide For agent use only. Not for public distribution. Life Insurance In Qualified Plans While qualified plans are a tremendous retirement savings vehicle, they

TABLE OF CONTENTS PAGE GENERAL INFORMATION B-3 CERTAIN FEDERAL INCOME TAX CONSEQUENCES B-3 PUBLISHED RATINGS B-7 ADMINISTRATION B-7

STATEMENT OF ADDITIONAL INFORMATION INDIVIDUAL VARIABLE ANNUITY ISSUED BY JEFFERSON NATIONAL LIFE INSURANCE COMPANY AND JEFFERSON NATIONAL LIFE ANNUITY ACCOUNT G ADMINISTRATIVE OFFICE: P.O. BOX 36840,

STATEMENT OF ADDITIONAL INFORMATION INDIVIDUAL VARIABLE ANNUITY ISSUED BY JEFFERSON NATIONAL LIFE INSURANCE COMPANY AND JEFFERSON NATIONAL LIFE ANNUITY ACCOUNT G ADMINISTRATIVE OFFICE: P.O. BOX 36840,

WAIT-AND-SEE CORPORATE BUY-SELL AGREEMENT

WAIT-AND-SEE CORPORATE BUY-SELL AGREEMENT FOR FINANCIAL PROFESSIONAL USE ONLY-NOT FOR PUBLIC DISTRIBUTION. Specimen documents are made available for educational purposes only. This specimen form may be

WAIT-AND-SEE CORPORATE BUY-SELL AGREEMENT FOR FINANCIAL PROFESSIONAL USE ONLY-NOT FOR PUBLIC DISTRIBUTION. Specimen documents are made available for educational purposes only. This specimen form may be

PROTECTING BUSINESS OWNERS AND PRESERVING BUSINESSES FOR FUTURE GENERATIONS

BASICS OF BUY-SELL PLANNING A buy-sell arrangement (or business continuation agreement ) is an arrangement for the disposition of a business interest upon a specific triggering event such as a business

BASICS OF BUY-SELL PLANNING A buy-sell arrangement (or business continuation agreement ) is an arrangement for the disposition of a business interest upon a specific triggering event such as a business

Life Insurance Coverage on a Key Employee

Raymond James Financial Services Bill Poland, CRPS, CRPC Financial Advisor 108 State Street Suite 200 Greensboro, NC 27408 336-272-7584 800-821-5941 bill.poland@raymondjames.com Life Insurance Coverage

Raymond James Financial Services Bill Poland, CRPS, CRPC Financial Advisor 108 State Street Suite 200 Greensboro, NC 27408 336-272-7584 800-821-5941 bill.poland@raymondjames.com Life Insurance Coverage

Educational Series. Supplemental Executive Retirement Plan (SERP)

") Supplemental Executive Retirement Plan (SERP) Supplemental Executive Retirement Plans (SERP) Guide What is a Supplemental Executive Retirement Plan (SERP)? A supplemental executive retirement plan is a

Supplemental Executive Retirement Plan (SERP) Supplemental Executive Retirement Plans (SERP) Guide What is a Supplemental Executive Retirement Plan (SERP)? A supplemental executive retirement plan is a

A Sole Proprietor Insured Buy-Sell Plan

A Sole Proprietor Insured Buy-Sell Plan At a sole proprietor s death, the business is dissolved and all business assets and liabilities become part of the sole proprietor's personal estate. Have you evaluated

A Sole Proprietor Insured Buy-Sell Plan At a sole proprietor s death, the business is dissolved and all business assets and liabilities become part of the sole proprietor's personal estate. Have you evaluated

Security Benefit Advanced Choice Annuity Application Individual Single Purchase Payment Deferred Annuity

Security Benefit Advanced Choice Annuity Application Individual Single Purchase Payment Deferred Annuity Issued by Security Benefit Life Insurance Company. Questions? Call our National Service Center at

Security Benefit Advanced Choice Annuity Application Individual Single Purchase Payment Deferred Annuity Issued by Security Benefit Life Insurance Company. Questions? Call our National Service Center at

Distributions and Rollovers from

Page 1 of 6 Frequently Asked Questions about Distributions and Rollovers from Retirement Accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one

Page 1 of 6 Frequently Asked Questions about Distributions and Rollovers from Retirement Accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one

Key Person Life Insurance

Key Person Life Insurance The Concept Key person life insurance helps reimburse a business for economic loss when a key employee dies. The insurance covers the life of an employee who is critical to the

Key Person Life Insurance The Concept Key person life insurance helps reimburse a business for economic loss when a key employee dies. The insurance covers the life of an employee who is critical to the

Tax Planning with Life Insurance

Antell & Company Financial Strategies Jim Antell, CLU, ChFC, REBC 150 Bank Street Burlington, VT 05401 802-318-9149 802-318-9148 jim.antell@lpl.com www.antellcompany.com Tax Planning with Life Insurance

Antell & Company Financial Strategies Jim Antell, CLU, ChFC, REBC 150 Bank Street Burlington, VT 05401 802-318-9149 802-318-9148 jim.antell@lpl.com www.antellcompany.com Tax Planning with Life Insurance

CLIENT INSTRUCTIONS FOR IRREVOCABLE LIFE INSURANCE TRUSTS, ANNUAL EXCLUSION GIFTS & ADMINISTRATION

CLIENT INSTRUCTIONS FOR IRREVOCABLE LIFE INSURANCE TRUSTS, ANNUAL EXCLUSION GIFTS & ADMINISTRATION In General Life insurance ownership through an Irrevocable Life Insurance Trust ( ILIT ) can remove the

CLIENT INSTRUCTIONS FOR IRREVOCABLE LIFE INSURANCE TRUSTS, ANNUAL EXCLUSION GIFTS & ADMINISTRATION In General Life insurance ownership through an Irrevocable Life Insurance Trust ( ILIT ) can remove the

Understanding Life Insurance: A Lesson in Life Insurance

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Questions 3 Types of Term 4 Term Variations

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Questions 3 Types of Term 4 Term Variations

Life Insurance Professional Analysis and Review

NATIONAL ASSOCIATION OF INSURANCE AND FINANCIAL ADVISORS FLORIDA 1836 Hermitage Blvd, Suite 200, Tallahassee, FL 32308 Contact: Paul S. Brawner (850) 422-1701 brawner@faifa.org This self study course is

NATIONAL ASSOCIATION OF INSURANCE AND FINANCIAL ADVISORS FLORIDA 1836 Hermitage Blvd, Suite 200, Tallahassee, FL 32308 Contact: Paul S. Brawner (850) 422-1701 brawner@faifa.org This self study course is

Frequently asked questions

Page 1 of 6 Frequently asked questions Distributions and rollovers from retirement accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one of several

Page 1 of 6 Frequently asked questions Distributions and rollovers from retirement accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one of several

Life Insurance Beneficiary Designations. Producer Guide. For agent use only. Not for public distribution.

Life Insurance Beneficiary Designations Producer Guide For agent use only. Not for public distribution. One of the most important decisions the owner of a life insurance policy makes is deciding who to

Life Insurance Beneficiary Designations Producer Guide For agent use only. Not for public distribution. One of the most important decisions the owner of a life insurance policy makes is deciding who to

Business Life Insurance Strategies Guide

Business Life Insurance Strategies Guide Nationwide Business Solutions Group In this guide, Nationwide assumes that universal or variable universal life insurance is used for each of the strategies, unless

Business Life Insurance Strategies Guide Nationwide Business Solutions Group In this guide, Nationwide assumes that universal or variable universal life insurance is used for each of the strategies, unless

Presented by: David Hayward, CLU, ChFC, FLMI Marketing Consultant

Key Person Insurance Presented by: David Hayward, CLU, ChFC, FLMI Marketing Consultant National Life Group is a trade name of National Life Insurance Company, Montpelier, VT, Life Insurance Company of

Key Person Insurance Presented by: David Hayward, CLU, ChFC, FLMI Marketing Consultant National Life Group is a trade name of National Life Insurance Company, Montpelier, VT, Life Insurance Company of

PayFlex Health Savings Account (HSA) Frequently Asked Questions

Frequently Asked Questions") OVERVIEW AND ELIGIBILITY REQUIREMENTS What is a Health Savings Account? A Health Savings Account ( HSA ) is a tax-advantaged healthcare account created for the purpose of saving and paying for qualified

OVERVIEW AND ELIGIBILITY REQUIREMENTS What is a Health Savings Account? A Health Savings Account ( HSA ) is a tax-advantaged healthcare account created for the purpose of saving and paying for qualified

Items to Note before Selling an Annuity (Fixed Indexed, Fixed and Variable)

") Items to Note before Selling an Annuity (Fixed Indexed, Fixed and Variable) In Good Order Requirements To ensure your new business application will be complete and in good order, please provide Security

Items to Note before Selling an Annuity (Fixed Indexed, Fixed and Variable) In Good Order Requirements To ensure your new business application will be complete and in good order, please provide Security

Divorce and Life Insurance. in brief

Divorce and Life Insurance in brief Divorce and Life Insurance Introduction In a divorce, property is divided between the spouses. In addition, a divorce decree may require that one spouse pay alimony

Divorce and Life Insurance in brief Divorce and Life Insurance Introduction In a divorce, property is divided between the spouses. In addition, a divorce decree may require that one spouse pay alimony

It s All About the Business

It s All About the Business Planning Strategies Integrated with Life Insurance to Help a Business Owner Accomplish Goals for Retirement, Business Perpetuation, Successful Business Transition, and Estate

It s All About the Business Planning Strategies Integrated with Life Insurance to Help a Business Owner Accomplish Goals for Retirement, Business Perpetuation, Successful Business Transition, and Estate

Understanding Life Insurance: A Lesson in Life Insurance

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Questions 3 Types of Term 4 Term Variations

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Questions 3 Types of Term 4 Term Variations

Understanding Life Insurance: A Lesson in Life Insurance

Understanding Life Insurance: A Lesson in Life Insurance If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Insurance Questions

Understanding Life Insurance: A Lesson in Life Insurance If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Insurance Questions

Applies only to discounted stock rights exercised during 2006.

Part III Administrative, Procedural, and Miscellaneous Compliance Resolution Program for Employees Other than Corporate Insiders for Additional 2006 Taxes Arising Under 409A due to the Exercise of Stock

Part III Administrative, Procedural, and Miscellaneous Compliance Resolution Program for Employees Other than Corporate Insiders for Additional 2006 Taxes Arising Under 409A due to the Exercise of Stock

THE IRREVOCABLE LIFE INSURANCE PRESERVATION TRUST HANDBOOK

THE IRREVOCABLE LIFE INSURANCE PRESERVATION TRUST HANDBOOK This handbook is not to be used in lieu of appropriate legal advice. INSURANCE PRESERVATION TRUST HANDBOOK Page 1 IRREVOCABLE INSURANCE TRUST

THE IRREVOCABLE LIFE INSURANCE PRESERVATION TRUST HANDBOOK This handbook is not to be used in lieu of appropriate legal advice. INSURANCE PRESERVATION TRUST HANDBOOK Page 1 IRREVOCABLE INSURANCE TRUST

DESCRIPTION OF THE PLAN

DESCRIPTION OF THE PLAN PURPOSE 1. What is the purpose of the Plan? The purpose of the Plan is to provide eligible record owners of common stock of the Company with a simple and convenient means of investing

DESCRIPTION OF THE PLAN PURPOSE 1. What is the purpose of the Plan? The purpose of the Plan is to provide eligible record owners of common stock of the Company with a simple and convenient means of investing

H I G H L I G H T E R Financial Underwriting

UNDERWRITING H I G H L I G H T E R Financial Underwriting What Is Financial Underwriting? Why Is Financial Underwriting Important? Insurable Interest Premium Payer Affordability Financial Underwriting

UNDERWRITING H I G H L I G H T E R Financial Underwriting What Is Financial Underwriting? Why Is Financial Underwriting Important? Insurable Interest Premium Payer Affordability Financial Underwriting

Business Continuation Planning with Life Insurance

Business Continuation Planning with Life Insurance Maintaining Business Continuity After the Death or Retirement of a Business Owner AD-OC-745C Business Continuation Planning Using Life Insurance FUTURES

Business Continuation Planning with Life Insurance Maintaining Business Continuity After the Death or Retirement of a Business Owner AD-OC-745C Business Continuation Planning Using Life Insurance FUTURES

INDIVIDUAL HEALTH SAVINGS ACCOUNT APPLICATION

INDIVIDUAL HEALTH SAVINGS ACCOUNT APPLICATION ACCOUNT HOLDER S INFORMATION Last Name First Name Middle Initial Street Address City State Zip Code Social Security No. Date of Birth Daytime Phone Health

INDIVIDUAL HEALTH SAVINGS ACCOUNT APPLICATION ACCOUNT HOLDER S INFORMATION Last Name First Name Middle Initial Street Address City State Zip Code Social Security No. Date of Birth Daytime Phone Health

Advanced Sales EXCELLENCE PARTNERING FOR ACCOUNTS RECEIVABLE FINANCING. Informational ideas important to large and complex cases

Advanced Sales Informational ideas important to large and complex cases PARTNERING FOR EXCELLENCE Vol II, Issue 2 May 2006 ACCOUNTS RECEIVABLE FINANCING by Glenn H. Plotkin, J.D., M.S., CFP, CLU, ChFC,

Advanced Sales Informational ideas important to large and complex cases PARTNERING FOR EXCELLENCE Vol II, Issue 2 May 2006 ACCOUNTS RECEIVABLE FINANCING by Glenn H. Plotkin, J.D., M.S., CFP, CLU, ChFC,

Pension Protection Act of 2006 Makes Changes To Defined Benefit Governmental and Church Plans

Important Information Legislation November 2006 Pension Protection Act of 2006 Makes Changes To Defined Benefit Governmental and Church Plans This is one of a series of Pension Analyst publications providing

Important Information Legislation November 2006 Pension Protection Act of 2006 Makes Changes To Defined Benefit Governmental and Church Plans This is one of a series of Pension Analyst publications providing

Executive Compensation Strategies. For Academic, Medical, Research and Cultural Institutions

Executive Compensation Strategies For Academic, Medical, Research and Cultural Institutions For institutional investor use only. Not for use with or distribution to the public. TIAA-CREF: A leading provider

Executive Compensation Strategies For Academic, Medical, Research and Cultural Institutions For institutional investor use only. Not for use with or distribution to the public. TIAA-CREF: A leading provider

Savings Incentive Match Plan for Employees of Small Employers (SIMPLE) Not for Use With a Designated Financial Institution

Not for Use With a Designated Financial Institution") Form 5304-SIMPLE (Rev. March 2012) Department of the Treasury Internal Revenue Service Name of Employer Savings Incentive Match Plan for Employees of Small Employers (SIMPLE) Not for Use With a Designated

Form 5304-SIMPLE (Rev. March 2012) Department of the Treasury Internal Revenue Service Name of Employer Savings Incentive Match Plan for Employees of Small Employers (SIMPLE) Not for Use With a Designated

A Business Split-Dollar Life Insurance Plan

A Business Split-Dollar Life Insurance Plan Since salary alone is often not enough, what steps can your business take to retain your key employees? Table of Contents Page What Is a Business Split-Dollar

A Business Split-Dollar Life Insurance Plan Since salary alone is often not enough, what steps can your business take to retain your key employees? Table of Contents Page What Is a Business Split-Dollar

Life Insurance Coverage on a Key Employee

Center for Wealth Management Susan A. Myers, CPA, CFP, CLTC Robert J. Moore Justin M. Williamson 755 W. Big Beaver Rd, Ste 600 Troy, MI 48084 248-680-0490 smyers1@metlife.com www.center4wealthmgmt.com

Center for Wealth Management Susan A. Myers, CPA, CFP, CLTC Robert J. Moore Justin M. Williamson 755 W. Big Beaver Rd, Ste 600 Troy, MI 48084 248-680-0490 smyers1@metlife.com www.center4wealthmgmt.com

APPENDIX IV-10 FORM HUD 1731 - PROSPECTUS GINNIE MAE I MORTGAGE-BACKED SECURITIES (CONSTRUCTION AND PERMANENT LOAN SECURITIES)

") GINNIE MAE 5500.3, REV. 1 APPENDIX IV-10 FORM HUD 1731 - PROSPECTUS GINNIE MAE I MORTGAGE-BACKED SECURITIES (CONSTRUCTION AND PERMANENT LOAN SECURITIES) Applicability: Purpose: Prepared by: Prepared in:

GINNIE MAE 5500.3, REV. 1 APPENDIX IV-10 FORM HUD 1731 - PROSPECTUS GINNIE MAE I MORTGAGE-BACKED SECURITIES (CONSTRUCTION AND PERMANENT LOAN SECURITIES) Applicability: Purpose: Prepared by: Prepared in:

Sample Gift Acceptance Policy

Introduction Sample Gift Acceptance Policy In order to protect the interests of (organization name) and the persons and other entities that support its programs these policies are designed to assure that

Introduction Sample Gift Acceptance Policy In order to protect the interests of (organization name) and the persons and other entities that support its programs these policies are designed to assure that

Key Person, Split Dollar & Deferred Compensation Combination. Three Needs One Policy Presentation

Three Needs One Policy Presentation Does the business identify with the following? The business relies on one or more executives for generating the bulk of the revenue or for acquiring most of the new

Three Needs One Policy Presentation Does the business identify with the following? The business relies on one or more executives for generating the bulk of the revenue or for acquiring most of the new

Estate Tax Concepts. for Edward and Tina Collins

Estate Tax Concepts for Edward and Tina Collins Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: joseph.davis@aol.com

Estate Tax Concepts for Edward and Tina Collins Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: joseph.davis@aol.com

[LOGO] ROGERS COMMUNICATIONS INC. DIVIDEND REINVESTMENT PLAN. November 1, 2010

![[LOGO] ROGERS COMMUNICATIONS INC. DIVIDEND REINVESTMENT PLAN. November 1, 2010](/thumbs/30/14484201.jpg "[LOGO] ROGERS COMMUNICATIONS INC. DIVIDEND REINVESTMENT PLAN. November 1, 2010") [LOGO] ROGERS COMMUNICATIONS INC. DIVIDEND REINVESTMENT PLAN November 1, 2010 Rogers Communications Inc. Dividend Reinvestment Plan Table of Contents SUMMARY... 3 DEFINITIONS... 4 ELIGIBILITY... 6 ENROLLMENT...

[LOGO] ROGERS COMMUNICATIONS INC. DIVIDEND REINVESTMENT PLAN November 1, 2010 Rogers Communications Inc. Dividend Reinvestment Plan Table of Contents SUMMARY... 3 DEFINITIONS... 4 ELIGIBILITY... 6 ENROLLMENT...

Succession Planning. Succession Planning. James F. Weber, CPA, CGMA Managing Member

James F. Weber, CPA, CGMA Managing Member This session is eligible for 1 Continuing Education Hour and 1 Contact Hour. To earn these hours you must: Have your badge scanned at the door Attend 90% of this

James F. Weber, CPA, CGMA Managing Member This session is eligible for 1 Continuing Education Hour and 1 Contact Hour. To earn these hours you must: Have your badge scanned at the door Attend 90% of this