Harrison 2012 Budget Implications of the Tax Levy Cap

|

|

|

- Andra Preston

- 8 years ago

- Views:

Transcription

1 Harrison 2012 Budget Implications of the Tax Levy Cap

2 THE TAX CAP CHAPTER 97 OF THE LAWS OF 2011 Tax Cap Overview ENACTED JUNE 24, 2011 Program bill originated with Governor Cuomo Bill amended and passed as part of omnibus bill Establishes a Tax Levy Limit on all local governments and most school districts (excludes NYC) Starts with fiscal years beginning in Expires June 15, 2016 unless rent control is extended

Starts with fiscal years beginning in 2012.")

3 Tax Cap Summary TAX CAP LIMITS TOTAL LEVY SET BY LOCAL GOVERNMENTS, NOT ASSESSED VALUE OR TAX RATE TOWN/VILLAGE OF HARRISON TOTAL LEVY FOR BUDGET YEAR 2011 $40,667, % $ 813, Amount Harrison Can Increase the 2012 Tax Levy over 2011 Prior to Exclusions for Pension which will be discussed later. THIS NUMBER IS FOR EXPLANATION PURPOSES ONLY AND DOES NOT INCLUDE ANY OTHER DISTRICTS THAT WE HAVE TO REPORT. LOCAL GOVERNMENTS MAY NOT ADOPT A BUDGET THAT REQUIRES A TAX LEVY THAT EXCEEDS THE PRIOR YEARS LEVY BY MORE THAN 2%, OR THE RATE OF INFLATION, WHICHEVER IS LESS, UNLESS THE GOVERNING BOARD FIRST ADOPTS A LOCAL LAW TO OVERRIDE THE LEVY LIMITATION. Rate of Inflation: Inflation factor, change in "the average of the national consumer price indexes determined by the United State Department of Labor for the twelve month period ending six months prior to the start of the coming fiscal year." The Office of the State Comptroller will calculate for Local Governments as the numbers are released.

4 Tax Cap Summary IN ADDITION TO THE TOWN/VILLAGE, THE TAX CAP COVERS ALL SPECIAL DISTRICTS SUCH AS, FIRE DISTRICTS,LIBRARY DISTRICTS, SEWER DISTRICTS, DRAINAGE DISTRICTS, REFUSE DISTRICTS AND SPECIAL DISTRICTS. OUR FIRE DISTRICTS (EXCLUDING PURCHASE FIRE), LIBRARY, SEWER, AND SPECIAL ASSESSMENT DISTRICTS ARE ALL INCLUDED IN OUR MUNICIPAL LEVY CAP CALCULATION SINCE WE ARE A CO-TERMINUS TOWN/VILLAGE, WE WILL HAVE TO DO TWO REPORTS, ONE FOR THE TOWN AND ONE FOR THE VILLAGE. IN ORDER TO STAY WITHIN THE CAP, EITHER REPORT CANNOT GO OVER THE 2% LEVY AMOUNT.

5 OVERRIDE THE LAW ALLOWS LOCAL GOVERNMENTS AND SCHOOL DISTRICTS TO OVERRIDE THE ANNUAL LEVY CAP. AN OVERRIDE IS GOOD FOR THAT FISCAL YEAR ONLY: WE CANNOT "OPT OUT" OF THE TAX CAP PERMANENTLY. OVERRIDE PROCESS: MUST FIRST ENACT A LOCAL LAW TO OVERRIDE BEFORE ADOPTING A FINAL BUDGET THAT REQUIRES A TAX LEVY ABOVE THE LIMIT. GOVERNING BOARD MUST APPROVE BY AT LEAST 60% OF VOTING POWER (i.e.: 3 OUT OF 5)

6 Exclusions THE LAW ALLOWS LOCAL GOVERNMENTS TO EXCLUDE FROM THE LEVY CALCULATION THE FOLLOWING: PENSION CONTRIBUTIONS DUE TO INCREASES IN THE STATEWIDE CONTRIBUTION RATE OVER 2 PERCENTAGE POINTS. EXPENDITURES RESULTING FROM COURT ORDERS OR JUDGEMENTS ARISING OUT OF TORT ACTIONS THAT EXCEED 5% OF THE TOTAL TAX LEVIED IN THE PRIOR FISCAL YEAR. (DOES NOT APPLY TO US THIS YEAR, NO EXCLUSION)

7 Pension Exclusion Calculator Hover here for sample salary projection Salary Base for bill to be paid in fiscal years beginning 2012:* State and Local Employee Retirement System (ERS) 13,290,837 Police and Fire Retirement System (PFRS) 8,470,235 Teachers Retirement System (TRS) Available from the Retirement System through a secure online application. For access to the Retirement System Employer Projection and Rates (EPR) Application, RTEmpSer@osc.state.ny.us or call Beth Wicks at or Patricia Engel at (For other levy limit questions, please call the Division of Local Government's Data Monitoring and Analysis Unit at ) Fall 2012 TRS payments will be based on actual July 1, 2011 June 30, 2012 salary base. The TRS system does not provide projections of this base. Excludable Percentage: State and Local Employee Retirement System (ERS) 0.60% Police and Fire Retirement System (PFRS) 2.20% Teachers Retirement System (TRS) See "Contribution Rates" Tab for data. (To get the value 0.6%, enter either "0.6%" or "0.006," not"0.6", since 0.6 is equal to 60%.) Pension Exclusion: ERS 79,745 PFRS 186,345 TRS * NOTE to Calendar Year LGs: Please use the salary base applicable to the bill you will pay in calendar 2012, taken from the Employer Projection and Rates (EPR) Application. If, like most entities, you will pay your bill in December 2012, use the column labeled "Projected Salaries 04/01/ /31/2013". If, like a few, you will be paying your pension bill in February 2012, use the column labeled, "Salary Estimates 04/01/ /31/2012". However, to minimize risk of audit, please note that you should only do this if you regularly pay your pension bill in February. ERS/PFRS Retirement Exclusions by Payment Date During Fiscal Years Starting in 2012 For State Percentage Excluded Pay in Fiscal Year ERS PFRS February 2012* April 1, March 31, % 1.4% December 2012 April 1, March 31, % 2.2% February 2013 April 1, March 31, % 2.2% * Applies to calendar year fiscal year entities only, and only that regularly pay in February.

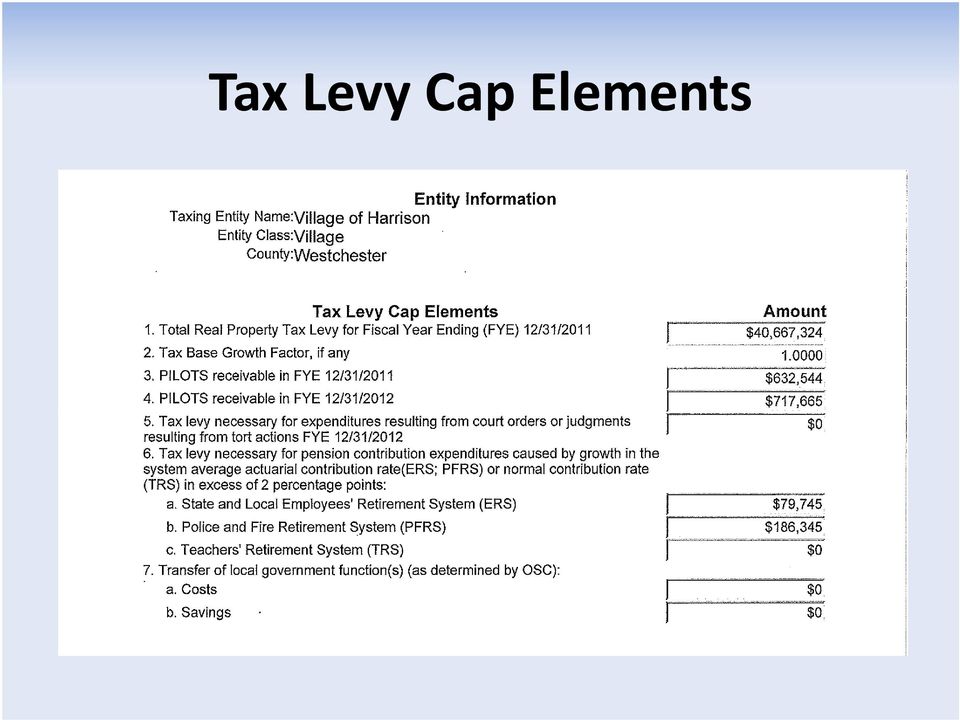

8 Tax Levy Cap Elements

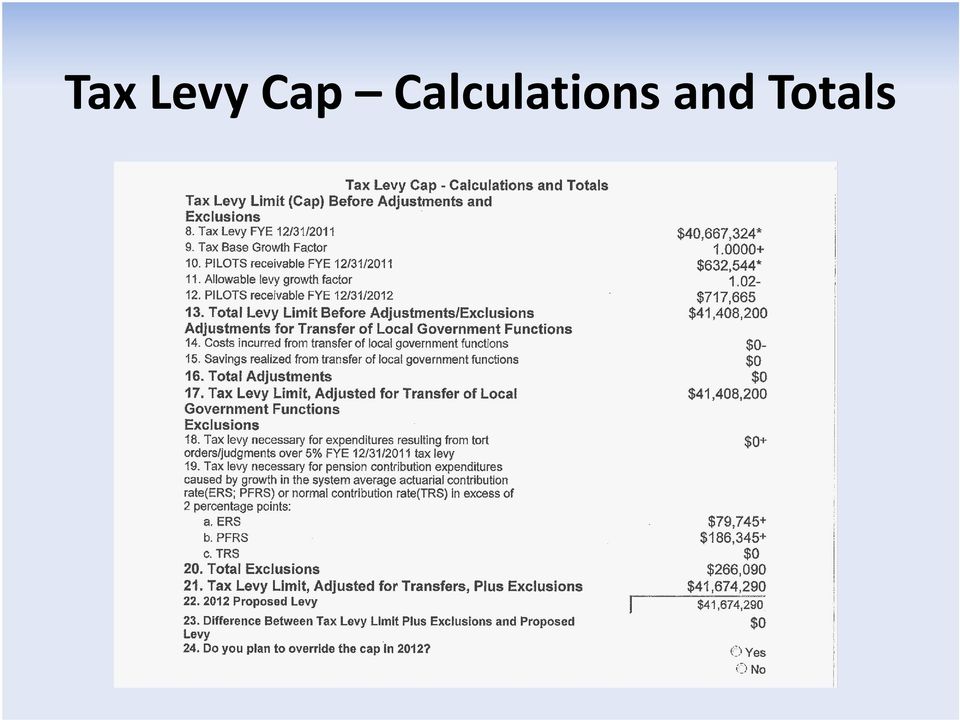

9 Tax Levy Cap Calculations and Totals

10 Tax Rate Increase THE TAX LEVY CAP OF 2% IS ON THE LEVY NOT THE TAX RATE INCREASE THE 2% TAX LEVY CAP ALLOWS THE INCREASE IN THE LEVY FOR THE TOWN,LIBRARY, HIGHWAY, AND VILLAGE FUNDS FOR A TOTAL OF $1,006,966. THIS EQUATES TO A TAX RATE INCREASE OF 4.571% THE ASSESSMENT ROLL WENT FROM $139,855,816 IN THE 2011 TAX YEAR, TO $137,054,166 FOR THE 2012 TAX YEAR. THIS REDUCTION IN THE ASSESSMENT ROLL EQUATES TO A 2.044% INCREASE IN THE TAX RATE. THE 2% DOLLAR LEVY INCREASE OF $1,006,996, EQUATES TO A TAX RATE INCREASE OF 2.527%.

11 2012 Impact of Tax Rate Increase of 4.571% DOLLAR ANNUAL ESTIMATED UNIFORM INCREASE INCREASE HOME PERCENTAGE ASSESSMENT PER FOR TOWN VALUE OF VALUE THOUSAND TAXES 2012 $ 250, % $ 4, $ $ $ 500, % $ 9, $ $ $ 600, % $ 10, $ $ $ 650, % $ 11, $ $ $ 700, % $ 12, $ $ $ 750, % $ 13, $ $ $ 1,000, % $ 18, $ $ $ 2,000, % $ 36, $ $ IN ORDER TO TAKE THE TAX RATE INCREASE DOWN BY 1%, WE HAVE TO FIND $398,500 IN EXPENDITURE CUTS OR REVENUE INCREASES

12 Challenges TAX CAP 2% DOLLAR LEVY CHALLENGES $ 1,006, Amount we can collect from taxpayers above the 2011 amount $ 40,667, Levy $ 41,674, Total amount for 2012 we can collect from taxpayers FOR THE 2012 BUDGET WE HAVE THE FOLLOWING INCREASE IN MAJOR EXPENDITURE ITEMS NYS Retirement $ 315, Major Medical $1,000, Judgments and Claims $ 100, %Raises and Steps $ 650, Debt Service $ 100, TOTAL MAJOR EXP.INCREASE 2012 $2,165, AMOUNT WE CAN LEVY $1,006, EXPENDITURE CUTS OR INCREASED NON PROPERTY TAX REVENUE NEEDED TO MEET THE 2% TAX LEVY CAP $1,158,034.00

Overview of the Real Property Tax Levy Limit ( Tax Cap ) Law

Law") Overview of the Real Property Tax Levy Limit ( Tax Cap ) Law Presented by Nora McCabe Assistant Director, Policy and Research Office of the State Comptroller Thomas P. DiNapoli Division of Local Government

Overview of the Real Property Tax Levy Limit ( Tax Cap ) Law Presented by Nora McCabe Assistant Director, Policy and Research Office of the State Comptroller Thomas P. DiNapoli Division of Local Government

Property Tax Cap Fiscal Years Beginning 2014

New York State Office of the State Comptroller Thomas P. DiNapoli State Comptroller Property Tax Cap Fiscal Years Beginning Property Tax Cap Instructions The State Legislature and the Governor enacted

New York State Office of the State Comptroller Thomas P. DiNapoli State Comptroller Property Tax Cap Fiscal Years Beginning Property Tax Cap Instructions The State Legislature and the Governor enacted

Real Property Tax Cap Information Frequently Asked Questions

Real Property Tax Cap Information Frequently Asked Questions Notice: The answers listed below supplement the guidance issued by the New York State Department of Taxation and Finance and the New York State

Real Property Tax Cap Information Frequently Asked Questions Notice: The answers listed below supplement the guidance issued by the New York State Department of Taxation and Finance and the New York State

Plan for Today s Webinar

An Update to the Property Tax Levy Limit and Multiyear Financial Planning as an Effective Strategy Presented by Yvonne Martinez and Elizabeth Davis LGSA Research Office of the State Comptroller Thomas

An Update to the Property Tax Levy Limit and Multiyear Financial Planning as an Effective Strategy Presented by Yvonne Martinez and Elizabeth Davis LGSA Research Office of the State Comptroller Thomas

THE BASE FORMULA PRIOR SCHOOL-YEAR TAX LEVY X TAX BASE GROWTH FACTOR + PILOTS RECEIVED IN PRIOR SCHOOL YEAR

New York s Tax Levy Limit Formula: How does it add up? The quantity change factor, determined by the Dept. of Taxation and Finance for each district by Feb. 1. It s the year-to-year increase in the full

New York s Tax Levy Limit Formula: How does it add up? The quantity change factor, determined by the Dept. of Taxation and Finance for each district by Feb. 1. It s the year-to-year increase in the full

GFOA NYS UNDERSTANDING THE NEW REAL PROPERTY TAX LEVY CAP. New York State Government Finance Officers' Association, Inc.

UNDERSTANDING THE NEW REAL PROPERTY TAX LEVY CAP (How the Real Property Tax Levy Percentage Cap and the Real Property Tax Rate Differ) It seems everywhere you turn people are talking about the Tax Cap.

UNDERSTANDING THE NEW REAL PROPERTY TAX LEVY CAP (How the Real Property Tax Levy Percentage Cap and the Real Property Tax Rate Differ) It seems everywhere you turn people are talking about the Tax Cap.

New York State Property Tax Cap

New York State Property Tax Cap Chapter 97 of the Laws of 2011 Goals: Facts Terminology Old and New What the law really is What the Public s perception may be When is 2% not really 2% How it affects us

New York State Property Tax Cap Chapter 97 of the Laws of 2011 Goals: Facts Terminology Old and New What the law really is What the Public s perception may be When is 2% not really 2% How it affects us

Property Tax Levy Cap

Published October 2011 Understanding New York s Property Tax Levy Cap as it relates to public schools In this first year of New York s property tax cap, details about its provisions and implementation

Published October 2011 Understanding New York s Property Tax Levy Cap as it relates to public schools In this first year of New York s property tax cap, details about its provisions and implementation

NYS Public School Budgeting 101: Understanding the Basics of a School Budget

NYS Public School Budgeting 101: Understanding the Basics of a School Budget Dr. Karen Geelan, Superintendent Mr. Michael Watson, Business Official Allegany-Limestone Central School District Agenda Welcome

NYS Public School Budgeting 101: Understanding the Basics of a School Budget Dr. Karen Geelan, Superintendent Mr. Michael Watson, Business Official Allegany-Limestone Central School District Agenda Welcome

A How To Guide to Shared Services and Cooperation

A How To Guide to Shared Services and Cooperation Presented by Laird Petrie and Angela Lauria-Gunnink Office of the State Comptroller Thomas P. DiNapoli Division of Local Government and School Accountability

A How To Guide to Shared Services and Cooperation Presented by Laird Petrie and Angela Lauria-Gunnink Office of the State Comptroller Thomas P. DiNapoli Division of Local Government and School Accountability

New York State Office of the State Comptroller Thomas P. DiNapoli State Comptroller

Thomas P. DiNapoli State Comptroller Property Tax Data Real Property Tax Levies, Taxable Full Value and Full Value Tax Rates Note: The table presented for 2013 and 2014 replaces the information shown in

Thomas P. DiNapoli State Comptroller Property Tax Data Real Property Tax Levies, Taxable Full Value and Full Value Tax Rates Note: The table presented for 2013 and 2014 replaces the information shown in

New York State Property Tax Freeze Credit Fact Sheet

New York State Property Tax Freeze Credit Fact Sheet The Property Tax Freeze Credit is a two-year tax relief program that reimburses qualifying New York State homeowners for increases in local property

New York State Property Tax Freeze Credit Fact Sheet The Property Tax Freeze Credit is a two-year tax relief program that reimburses qualifying New York State homeowners for increases in local property

GOVERNOR S PROGRAM BILL 2011 MEMORANDUM

GOVERNOR S PROGRAM BILL 2011 MEMORANDUM AN ACT to amend the retirement and social security law, the education law and the administrative code of the city of New York, in relation to persons joining the

GOVERNOR S PROGRAM BILL 2011 MEMORANDUM AN ACT to amend the retirement and social security law, the education law and the administrative code of the city of New York, in relation to persons joining the

Property Tax Cap and Tax Freeze Legislation Details for Fire Districts. Topics for Today s Session. Property Tax Cap - Summary

Property Tax Cap and Tax Freeze Legislation Details for Fire Districts Presented by Ingrid Otto-Jones, CPA Senior Examiner, Monitoring and Analysis Unit Office of the State Comptroller Thomas P. DiNapoli

Property Tax Cap and Tax Freeze Legislation Details for Fire Districts Presented by Ingrid Otto-Jones, CPA Senior Examiner, Monitoring and Analysis Unit Office of the State Comptroller Thomas P. DiNapoli

Navigating through Year Two. Property Tax Levy Cap

Published March 2013 Navigating through Year Two of New York s Property Tax Levy Cap With year one of New York s property tax cap now behind us, details about the law s provisions and impact continue to

Published March 2013 Navigating through Year Two of New York s Property Tax Levy Cap With year one of New York s property tax cap now behind us, details about the law s provisions and impact continue to

2016-17 Property Tax Cap Guidebook January 2016

2016-17 Property Tax Cap Guidebook January 2016 Prepared by: Kathy Beardsley Charles Cowen Rose Fiddemon Michele Levings Jay O Connor Brady Regan Alyssa Stall State Aid & Financial Planning Service January

2016-17 Property Tax Cap Guidebook January 2016 Prepared by: Kathy Beardsley Charles Cowen Rose Fiddemon Michele Levings Jay O Connor Brady Regan Alyssa Stall State Aid & Financial Planning Service January

Course Objectives. What are Property Taxes? 2/14/2012. Tax Settlements

2/14/2012 Tax Settlements Presented by: Local Government Services 1 Course Objectives To enhance your understanding of how to read and record the information contained on your tax settlement sheets To

2/14/2012 Tax Settlements Presented by: Local Government Services 1 Course Objectives To enhance your understanding of how to read and record the information contained on your tax settlement sheets To

Addressing the Unintended Consequences of the Property Tax Cap

Addressing the Unintended Consequences of the Property Tax Cap June 10, 2015 In 2011 New York established a property tax cap for school districts, counties and municipalities. The cap essentially limits

Addressing the Unintended Consequences of the Property Tax Cap June 10, 2015 In 2011 New York established a property tax cap for school districts, counties and municipalities. The cap essentially limits

What You Need to Know about the Tax Levy Cap

1. What is the tax levy cap? The tax levy cap is a law that places strong restrictions on how school districts can raise revenues. At its basic level, the tax levy cap legislation makes it very difficult

1. What is the tax levy cap? The tax levy cap is a law that places strong restrictions on how school districts can raise revenues. At its basic level, the tax levy cap legislation makes it very difficult

What if I Work After Retirement?

L I F E Changes What if I Work After Retirement? New York State Office of the State Comptroller Thomas P. DiNapoli New York State and Local Retirement System Employees Retirement System Police and Fire

L I F E Changes What if I Work After Retirement? New York State Office of the State Comptroller Thomas P. DiNapoli New York State and Local Retirement System Employees Retirement System Police and Fire

Most New Yorkers do not want tax relief to come at the expense of their public schools.

Published October 2011 In this first year of New York s property tax cap, details about its provisions and implementation continue to evolve. This publication answers some questions that parents, taxpayers

Published October 2011 In this first year of New York s property tax cap, details about its provisions and implementation continue to evolve. This publication answers some questions that parents, taxpayers

Budget Summary. The City of New York Executive Budget Fiscal Year 2014. Michael R. Bloomberg, Mayor

The City of New York Executive Budget Fiscal Year 2014 Michael R. Bloomberg, Mayor Offi ce of Management and Budget Mark Page, Director Budget Summary Financial Plan Summary Fiscal Years 2013-2017 TABLE

The City of New York Executive Budget Fiscal Year 2014 Michael R. Bloomberg, Mayor Offi ce of Management and Budget Mark Page, Director Budget Summary Financial Plan Summary Fiscal Years 2013-2017 TABLE

5 YEAR FINANCIAL PLAN (2013-2017)

") CITY OF RICHMOND 5 YEAR FINANCIAL PLAN (2013-2017) BYLAW NO. 8990 EFFECTIVE DATE February 25, 2013 - 2 - Bylaw 8990 5 Year Financial Plan (2013-2017) The Council of the City of Richmond enacts as follows:

CITY OF RICHMOND 5 YEAR FINANCIAL PLAN (2013-2017) BYLAW NO. 8990 EFFECTIVE DATE February 25, 2013 - 2 - Bylaw 8990 5 Year Financial Plan (2013-2017) The Council of the City of Richmond enacts as follows:

Tax Levy Limit. Plattsburgh CSD 2013 2014

Tax Levy Limit Plattsburgh CSD 2013 2014 Review Tax levy limit Introduced 2011 discussed as trade for mandate relief, but was ultimately coupled with NYC rent control legislation Applies to school districts

Tax Levy Limit Plattsburgh CSD 2013 2014 Review Tax levy limit Introduced 2011 discussed as trade for mandate relief, but was ultimately coupled with NYC rent control legislation Applies to school districts

2% TAX LEVY CAP (PROPERTY TAX CAP) Board of Education and Public Presentation October 26, 2011 November 30, 2011

Board of Education and Public Presentation October 26, 2011 November 30, 2011") 2% TAX LEVY CAP (PROPERTY TAX CAP) Board of Education and Public Presentation October 26, 2011 November 30, 2011 Context: Challenges Facing Schools Implementation of a Tax Levy Cap Reduction in State Aid

2% TAX LEVY CAP (PROPERTY TAX CAP) Board of Education and Public Presentation October 26, 2011 November 30, 2011 Context: Challenges Facing Schools Implementation of a Tax Levy Cap Reduction in State Aid

Things New Yorkers Should Know About. Public Retirement Benefits in New York State

Things New Yorkers Should Know About Public Retirement Benefits in New York State October 2010 INTRODUCTION Citizens Budget Commission One Penn Plaza, Suite 640 New York, NY 10119 411 State Street Albany,

Things New Yorkers Should Know About Public Retirement Benefits in New York State October 2010 INTRODUCTION Citizens Budget Commission One Penn Plaza, Suite 640 New York, NY 10119 411 State Street Albany,

Tax Cap & Tax Freeze Credit Update

Tax Cap & Tax Freeze Credit Update Description & Opportunities John Clarkson, Town Supervisor Michael Cohen, Town Comptroller August 27, 2014 Property Tax Cap vs Tax Freeze Credit Both are NYS programs

Tax Cap & Tax Freeze Credit Update Description & Opportunities John Clarkson, Town Supervisor Michael Cohen, Town Comptroller August 27, 2014 Property Tax Cap vs Tax Freeze Credit Both are NYS programs

New York State Office of the State Comptroller Thomas P. DiNapoli State Comptroller

Thomas P. DiNapoli State Comptroller Understanding the Constitutional Tax Limit Counties Understanding Tax Limits Counties 2 Taxing Capacity How it Is Calculated...2 Five-Year Average Full Valuation of

Thomas P. DiNapoli State Comptroller Understanding the Constitutional Tax Limit Counties Understanding Tax Limits Counties 2 Taxing Capacity How it Is Calculated...2 Five-Year Average Full Valuation of

2014-15 New York State Budget Summary

2014-15 New York State Budget Summary Taxes Property Tax Freeze The final budget includes an amended version of Governor Cuomo s property tax freeze proposal. Under the final plan, homeowners will receive

2014-15 New York State Budget Summary Taxes Property Tax Freeze The final budget includes an amended version of Governor Cuomo s property tax freeze proposal. Under the final plan, homeowners will receive

October 1995. New York State Chief Fiscal Officers of Counties, Cities, Towns and Villages

October 1995 TO: FROM: SUBJECT: New York State Chief Fiscal Officers of Counties, Cities, Towns and Villages New York State Office of the State Comptroller, Division of Municipal Affairs New Tax Enforcement

October 1995 TO: FROM: SUBJECT: New York State Chief Fiscal Officers of Counties, Cities, Towns and Villages New York State Office of the State Comptroller, Division of Municipal Affairs New Tax Enforcement

ANNUAL TAX LEVY PACKET

ANNUAL TAX LEVY PACKET OF THE OREGON PARK DISTRICT FOR THE 2013 TAX YEAR We Create Fun for a Lifetime OREGON PARK DISTRICT ANNUAL TAX LEVY PACKET FOR THE 2013 TAX YEAR CONTENTS 2012 Tax Year District Statement

ANNUAL TAX LEVY PACKET OF THE OREGON PARK DISTRICT FOR THE 2013 TAX YEAR We Create Fun for a Lifetime OREGON PARK DISTRICT ANNUAL TAX LEVY PACKET FOR THE 2013 TAX YEAR CONTENTS 2012 Tax Year District Statement

The Education Dollar. A Look at Spending and Funding Trends

The Education Dollar A Look at Spending and Funding Trends September 2015 Executive Summary This annual study examines school district spending and funding over a ten-year period. The study identifies

The Education Dollar A Look at Spending and Funding Trends September 2015 Executive Summary This annual study examines school district spending and funding over a ten-year period. The study identifies

Description of Budget Cycle

Description of Budget Cycle The budget process in the City of Yonkers begins in December each year when budget preparation packages are sent to departments by the Office of Management and Budget. The departments

Description of Budget Cycle The budget process in the City of Yonkers begins in December each year when budget preparation packages are sent to departments by the Office of Management and Budget. The departments

City of Milwaukee. Comparative Revenue and Expenditure Report. W. Martin Morics Comptroller

of Milwaukee Comparative Revenue and Expenditure Report W. Martin Morics Comptroller June 2006 Table of Contents I. Introduction... 2 II. Revenue Sources... 3 Page III. Local Taxes...4 IV. Property Taxes...5

of Milwaukee Comparative Revenue and Expenditure Report W. Martin Morics Comptroller June 2006 Table of Contents I. Introduction... 2 II. Revenue Sources... 3 Page III. Local Taxes...4 IV. Property Taxes...5

S earching. Tax Relief. for Property. As New York considers a property tax cap, many wonder what it would mean for the state s schools

E ducation leaders across the state understand the need for property tax relief. However, many are concerned that if a property tax cap is enacted in New York as the Governor and many lawmakers have proposed

E ducation leaders across the state understand the need for property tax relief. However, many are concerned that if a property tax cap is enacted in New York as the Governor and many lawmakers have proposed

New York State Office of the State Comptroller Thomas P. DiNapoli State Comptroller

Thomas P. DiNapoli State Comptroller Understanding the Constitutional Tax Limit Cities Understanding Tax Limits Cities 2 Taxing Capacity How it Is Calculated...2 Five-Year Average Full Valuation of Taxable

Thomas P. DiNapoli State Comptroller Understanding the Constitutional Tax Limit Cities Understanding Tax Limits Cities 2 Taxing Capacity How it Is Calculated...2 Five-Year Average Full Valuation of Taxable

Township High School District #113 2014 Levy for Fiscal Year 2015-16

Township High School District #113 2014 Levy for Fiscal Year 2015-16 District #113 Vision Mission - Goals Vision Township High School District 113 provides a rigorous, equitable, student-centered education,

Township High School District #113 2014 Levy for Fiscal Year 2015-16 District #113 Vision Mission - Goals Vision Township High School District 113 provides a rigorous, equitable, student-centered education,

ANNUAL REPORT ON LOCAL GOVERNMENTS. Office of the New York State Comptroller. Thomas P. DiNapoli State Comptroller

Office of the New York State Comptroller Thomas P. DiNapoli State Comptroller 2015 ANNUAL REPORT ON LOCAL GOVERNMENTS FEBRUARY 2016 TABLE OF CONTENTS Division Mission 2 Comptroller s Message 3 Executive

Office of the New York State Comptroller Thomas P. DiNapoli State Comptroller 2015 ANNUAL REPORT ON LOCAL GOVERNMENTS FEBRUARY 2016 TABLE OF CONTENTS Division Mission 2 Comptroller s Message 3 Executive

Who Provides Services on Long Island?

Who Provides Services on Long Island? An Introduction to the Long Island Index's New Interactive Map www.longislandindexmaps.org June 2012 Report written by Erika Rosenberg, CGR Government Services on

Who Provides Services on Long Island? An Introduction to the Long Island Index's New Interactive Map www.longislandindexmaps.org June 2012 Report written by Erika Rosenberg, CGR Government Services on

FILED 2 9 2gag AMENDED ANNUAL T.4.X LEVY OWINANCE 2009

AMENDED ANNUAL T.4.X LEVY OWINANCE 2009 An Ordinance levying taxes for all town purposes for VILLAGE OF GIFFORD, Champaign County, State of Illinois for the tax year 2009, collectible in 2010. Be it ORDAINED

AMENDED ANNUAL T.4.X LEVY OWINANCE 2009 An Ordinance levying taxes for all town purposes for VILLAGE OF GIFFORD, Champaign County, State of Illinois for the tax year 2009, collectible in 2010. Be it ORDAINED

518-689-7208 (Office) 518-424-3245 (Cell) agregory@corningplace.com

518-424-3245 (Cell) agregory@corningplace.com") For Immediate Release: November 1, 2011 Contact: Andrew Gregory 518-689-7208 (Office) 518-424-3245 (Cell) agregory@corningplace.com New Statewide Coalition Unveils Let New York Work: A Common Agenda for

For Immediate Release: November 1, 2011 Contact: Andrew Gregory 518-689-7208 (Office) 518-424-3245 (Cell) agregory@corningplace.com New Statewide Coalition Unveils Let New York Work: A Common Agenda for

Essential Programs & Services State Calculation for Funding Public Education (ED279):

:") Essential Programs & Services State Calculation for Funding Public Education (ED279): Maine s Funding Formula for Sharing the Costs of PreK-12 Education between State and Local: 1. Determine the EPS Defined

Essential Programs & Services State Calculation for Funding Public Education (ED279): Maine s Funding Formula for Sharing the Costs of PreK-12 Education between State and Local: 1. Determine the EPS Defined

Proposition 2½ Ballot Questions Requirements and Procedures

Massachusetts Department of Revenue Division of Local Services Navjeet K. Bal, Commissioner Robert G. Nunes, Deputy Commissioner & Director of Municipal Affairs Proposition 2½ Ballot Questions Requirements

Massachusetts Department of Revenue Division of Local Services Navjeet K. Bal, Commissioner Robert G. Nunes, Deputy Commissioner & Director of Municipal Affairs Proposition 2½ Ballot Questions Requirements

CHAPTER 234 HOUSE BILL 2131 AN ACT AMENDING SECTIONS 12-348, 41-1007 AND 42-2064, ARIZONA REVISED STATUTES; RELATING TO TAX ADJUDICATIONS.

Senate Engrossed House Bill State of Arizona House of Representatives Fifty-second Legislature First Regular Session 0 CHAPTER HOUSE BILL AN ACT AMENDING SECTIONS -, -00 AND -0, ARIZONA REVISED STATUTES;

Senate Engrossed House Bill State of Arizona House of Representatives Fifty-second Legislature First Regular Session 0 CHAPTER HOUSE BILL AN ACT AMENDING SECTIONS -, -00 AND -0, ARIZONA REVISED STATUTES;

LEGISLATIVE SERVICES AGENCY OFFICE OF FISCAL AND MANAGEMENT ANALYSIS 301 State House (317) 232-9855

232-9855") LEGISLATIVE SERVICES AGENCY OFFICE OF FISCAL AND MANAGEMENT ANALYSIS 301 State House (317) 232-9855 FISCAL IMPACT STATEMENT LS 7482 DATE PREPARED: Mar 30, 2001 BILL NUMBER: SB 199 BILL AMENDED: Mar 29,

LEGISLATIVE SERVICES AGENCY OFFICE OF FISCAL AND MANAGEMENT ANALYSIS 301 State House (317) 232-9855 FISCAL IMPACT STATEMENT LS 7482 DATE PREPARED: Mar 30, 2001 BILL NUMBER: SB 199 BILL AMENDED: Mar 29,

Utah State Retirement Systems Overview. September 9, 2009 Prepared by the Office of Legislative Research and General Counsel

Utah State Retirement Systems Overview September 9, 2009 Prepared by the Office of Legislative Research and General Counsel Utah State Retirement Systems Six Participant Systems Judges Public Employees

Utah State Retirement Systems Overview September 9, 2009 Prepared by the Office of Legislative Research and General Counsel Utah State Retirement Systems Six Participant Systems Judges Public Employees

150-303-405 (Rev. 6-09)

") A Brief History of Oregon Property Taxation 150-303-405-1 (Rev. 6-09) 150-303-405 (Rev. 6-09) To understand the current structure of Oregon s property tax system, it is helpful to view the system in a

A Brief History of Oregon Property Taxation 150-303-405-1 (Rev. 6-09) 150-303-405 (Rev. 6-09) To understand the current structure of Oregon s property tax system, it is helpful to view the system in a

THE STATE EDUCATION DEPARTMENT Room 475 EBA Office of Educational Management Services Albany, NY 12234 (518) 474-6541

474-6541") THE STATE EDUCATION DEPARTMENT Room 475 EBA Office of Educational Management Services Albany, NY 12234 (518) 474-6541 Fund Balance - Reservations and Designations The following Reserve Funds are available

THE STATE EDUCATION DEPARTMENT Room 475 EBA Office of Educational Management Services Albany, NY 12234 (518) 474-6541 Fund Balance - Reservations and Designations The following Reserve Funds are available

New York Property Tax Cap Implications for School Districts

New York Property Tax Cap Implications for School Districts Deborah H. Cunningham Director For Education and Research New York State Association of School Business Officials December 17, 2014 dcunningham@nysasbo.org

New York Property Tax Cap Implications for School Districts Deborah H. Cunningham Director For Education and Research New York State Association of School Business Officials December 17, 2014 dcunningham@nysasbo.org

NEW PHILADELPHIA CITY SCHOOLS FIVE-YEAR FORECAST 2015-2019

Real Estate Tax Assumptions NEW PHILADELPHIA CITY SCHOOLS FIVE-YEAR FORECAST 2015-2019 REVENUE ASSUMPTIONS Real estate taxes had increased at approximately 1.1% to 2.0% through 2013 and a 0.5% increase

Real Estate Tax Assumptions NEW PHILADELPHIA CITY SCHOOLS FIVE-YEAR FORECAST 2015-2019 REVENUE ASSUMPTIONS Real estate taxes had increased at approximately 1.1% to 2.0% through 2013 and a 0.5% increase

Adopt Resolution 13-03 to Levy Taxes for the Year 2013 as

Dr. Bruce Law Superintendent of Schools IX. TO: FROM: Administration Reports / Possible Action B. Business 1. Resolution 13-03 to Levy Taxes for the Year 2013 Board of Education Dr. Bruce Law Superintendent

Dr. Bruce Law Superintendent of Schools IX. TO: FROM: Administration Reports / Possible Action B. Business 1. Resolution 13-03 to Levy Taxes for the Year 2013 Board of Education Dr. Bruce Law Superintendent

SCHOOL LOCAL PROPERTY TAX OPTION 1999 Legislation

STATE OF OREGON LEGISLATIVE REVENUE OFFICE H-197 State Capitol Building Salem, Oregon 97310-1347 Research Report (503) 986-1266 Research Report # 5-99 SCHOOL LOCAL PROPERTY TAX OPTION 1999 Legislation

STATE OF OREGON LEGISLATIVE REVENUE OFFICE H-197 State Capitol Building Salem, Oregon 97310-1347 Research Report (503) 986-1266 Research Report # 5-99 SCHOOL LOCAL PROPERTY TAX OPTION 1999 Legislation

2013-2014 Executive Budget Proposal

2013-2014 Executive Budget Proposal The Executive Budget Proposal encompasses a $142.6 billion spending plan, closes a $1.3 billion budget gap and assumes new revenue of over $7 billion in emergency federal

2013-2014 Executive Budget Proposal The Executive Budget Proposal encompasses a $142.6 billion spending plan, closes a $1.3 billion budget gap and assumes new revenue of over $7 billion in emergency federal

School Spending and Proposed Taxes are Contained as School Districts Draw on Savings

School Spending and Proposed Taxes are Contained as School Districts Draw on Savings May 2014 For use of NYSASBO data or analyses, please use the following source citation: SOURCE: New York State Association

School Spending and Proposed Taxes are Contained as School Districts Draw on Savings May 2014 For use of NYSASBO data or analyses, please use the following source citation: SOURCE: New York State Association

M E M O R A N D U M. Mayor Prussing and Members of the Urbana City Council

M E M O R A N D U M TO: Mayor Prussing and Members of the Urbana City Council FROM: Interim Comptroller RE: Property Tax Levy DATE: November 7, 2013 Attached for your consideration is the 2013 property

M E M O R A N D U M TO: Mayor Prussing and Members of the Urbana City Council FROM: Interim Comptroller RE: Property Tax Levy DATE: November 7, 2013 Attached for your consideration is the 2013 property

A Primer for New Jersey Budget and Tax Levy Caps

New Jersey Education Association Division of Research & Economic Services Rich Brown Associate Director Research & Economic Services June 2010 A Primer for New Jersey Budget and Tax Levy Caps Primer on

New Jersey Education Association Division of Research & Economic Services Rich Brown Associate Director Research & Economic Services June 2010 A Primer for New Jersey Budget and Tax Levy Caps Primer on

SB0001 Enrolled - 2 - LRB098 05457 JDS 35491 b

SB0001 Enrolled LRB098 05457 JDS 35491 b 1 AN ACT concerning public employee benefits. 2 Be it enacted by the People of the State of Illinois, 3 represented in the General Assembly: 4 Section 1. Legislative

SB0001 Enrolled LRB098 05457 JDS 35491 b 1 AN ACT concerning public employee benefits. 2 Be it enacted by the People of the State of Illinois, 3 represented in the General Assembly: 4 Section 1. Legislative

Page Intentionally Left Blank

Page Intentionally Left Blank Department Description The Debt Management Department conducts planning, structuring, and issuance activities for all City financings to fund cash flow needs and to provide

Page Intentionally Left Blank Department Description The Debt Management Department conducts planning, structuring, and issuance activities for all City financings to fund cash flow needs and to provide

Adopting a City Budget and Property Tax Rate Training Austin Texas February 2015

Adopting a City Budget and Property Tax Rate Training Austin Texas February 2015 Leela R. Fireside, Assistant City Attorney, Austin Texas. (contact info: leela.fireside@austintexas.gov or (512) 974-2163)

Adopting a City Budget and Property Tax Rate Training Austin Texas February 2015 Leela R. Fireside, Assistant City Attorney, Austin Texas. (contact info: leela.fireside@austintexas.gov or (512) 974-2163)

Town of Westborough Advisory Finance Committee Analysis of Levy Limit Growth Westborough s Immunity to Proposition 2 ½

Town of Westborough Advisory Finance Committee Analysis of Levy Limit Growth Westborough s Immunity to Proposition 2 ½ Abstract Massachusetts Proposition 2 ½ was intended to limit municipal tax growth.

Town of Westborough Advisory Finance Committee Analysis of Levy Limit Growth Westborough s Immunity to Proposition 2 ½ Abstract Massachusetts Proposition 2 ½ was intended to limit municipal tax growth.

Local Government Expenditure and Revenue Limits

Local Government Expenditure and Revenue Limits Prepared by Russ Kava and Rick Olin Wisconsin Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 Local Government Expenditure and Revenue

Local Government Expenditure and Revenue Limits Prepared by Russ Kava and Rick Olin Wisconsin Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 Local Government Expenditure and Revenue

WICKLIFFE BOARD OF EDUCATION 5-Year Financial Plan (SM-7) Assumptions: Fiscal Year 15 January 12, 2015

Assumptions: Fiscal Year 15 January 12, 2015") Exhibit 11 WICKLIFFE BOARD OF EDUCATION 5-Year Financial Plan (SM-7) Assumptions: Fiscal Year 15 January 12, 2015 The Ohio General Assembly enacted House Bill 412 requiring public school systems annually

Exhibit 11 WICKLIFFE BOARD OF EDUCATION 5-Year Financial Plan (SM-7) Assumptions: Fiscal Year 15 January 12, 2015 The Ohio General Assembly enacted House Bill 412 requiring public school systems annually

State of North Dakota Office Of State Tax Commissioner

State of North Dakota Office Of State Tax Commissioner RYAN RAUSCHENBERGER, COMMISSIONER Bismarck, North Dakota July 2015 Schedule of Levy Limitations Applicable To The Authority Of The Political Subdivisions

State of North Dakota Office Of State Tax Commissioner RYAN RAUSCHENBERGER, COMMISSIONER Bismarck, North Dakota July 2015 Schedule of Levy Limitations Applicable To The Authority Of The Political Subdivisions

TOWN OF MONSON - CERTIFICATION OF APPROPRIATIONS. Voters in Attendance Prec. A 126 Prec. B 153 Prec. C 163 Total: 442

TOWN OF MONSON - CERTIFICATION OF APPROPRIATIONS Date of Town Meeting: 14-May-12 Town Meeting Type: Annual X Special Voters in Attendance Prec. A 126 Prec. B 153 Prec. C 163 Total: 442 Art Total From From

TOWN OF MONSON - CERTIFICATION OF APPROPRIATIONS Date of Town Meeting: 14-May-12 Town Meeting Type: Annual X Special Voters in Attendance Prec. A 126 Prec. B 153 Prec. C 163 Total: 442 Art Total From From

How To Limit A Tax Extension In The United States

Page 2 The Property Tax Extension Limitation Law, A Technical Manual Table of Contents Introduction Purpose... 6 Summary The PTELL does not cap individual property assessments... 7 The PTELL limits the

Page 2 The Property Tax Extension Limitation Law, A Technical Manual Table of Contents Introduction Purpose... 6 Summary The PTELL does not cap individual property assessments... 7 The PTELL limits the

School & Local Public Safety Protection Act of 2012 Governor's Initiative. Our Children, Our Future 2012: The Education Initiative Molly Munger / PTA

What does the initiative do? School & Local Public Safety Protection Act of 2012 Governor's Would increase income tax rates on personal incomes in excess of a quarter million dollars per year, and increase

What does the initiative do? School & Local Public Safety Protection Act of 2012 Governor's Would increase income tax rates on personal incomes in excess of a quarter million dollars per year, and increase

New York's Tax Levy Law May Not Be Fair

, Pliblisbl.'ci Octoba ]() II rn Ibis/irsl year o/n

, Pliblisbl.'ci Octoba ]() II rn Ibis/irsl year o/n

2015 -- H 5915 S T A T E O F R H O D E I S L A N D

LC000 01 -- H 1 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO PUBLIC OFFICERS AND EMPLOYEES - RETIREMENT SYSTEM - CONTRIBUTIONS AND BENEFITS Introduced

LC000 01 -- H 1 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO PUBLIC OFFICERS AND EMPLOYEES - RETIREMENT SYSTEM - CONTRIBUTIONS AND BENEFITS Introduced

3/16/2012 SCHOOL FINANCE SCHOOL FINANCE SCHOOL FINANCE

SCHOOL FINANCE HB 2200 (formerly SB 450 bi-partisan plan) On Senate General Orders $74 base budget per pupil increase 2013 and 2014. Maximum LOB: 31% to 32% in 2013 and 33% in 2014. No mandatory election

SCHOOL FINANCE HB 2200 (formerly SB 450 bi-partisan plan) On Senate General Orders $74 base budget per pupil increase 2013 and 2014. Maximum LOB: 31% to 32% in 2013 and 33% in 2014. No mandatory election

2014 League of Municipalities Convention

2014 League of Municipalities Convention Compliance with Selected Local Finance Notices Joseph P Monzo November 20, 2014 Agenda LFN 2000-14 Managing Police Off Duty Employment LFN 2002-1 Managing Accumulated

2014 League of Municipalities Convention Compliance with Selected Local Finance Notices Joseph P Monzo November 20, 2014 Agenda LFN 2000-14 Managing Police Off Duty Employment LFN 2002-1 Managing Accumulated

Overview of Teacher Retirement System of Texas

Overview of Teacher Retirement System of Texas Tom Guerin Revised September 2011 Revised 10/21/09 TRS retirement plan benefits are funded by member, state, and employer contributions to the trust fund,

Overview of Teacher Retirement System of Texas Tom Guerin Revised September 2011 Revised 10/21/09 TRS retirement plan benefits are funded by member, state, and employer contributions to the trust fund,

Adopt Resolution 12-04 to Levy Taxes for the Year 2012 as

Dr. Nicholas D. Wahl Dr. Bruce Law Troy A. Courtney Dr. Joyce Powell Jeffrey T. Eagan Superintendent of Assistant Superintendent Director of Director of Business Manager Schools for Instruction Human Resources

Dr. Nicholas D. Wahl Dr. Bruce Law Troy A. Courtney Dr. Joyce Powell Jeffrey T. Eagan Superintendent of Assistant Superintendent Director of Director of Business Manager Schools for Instruction Human Resources

Agreement to Provide Tourism Promotion Services between The City of Ontario & The Chamber of Commerce

Agreement to Provide Tourism Promotion Services between The City of Ontario & The Chamber of Commerce This Agreement entered into between the City of Ontario, a municipal corporation organized under the

Agreement to Provide Tourism Promotion Services between The City of Ontario & The Chamber of Commerce This Agreement entered into between the City of Ontario, a municipal corporation organized under the

THE PEOPLE OF THE STATE OF MICHIGAN ENACT:

State financing and management; authorities; Michigan financial review commission; expand to include certain school districts. State financing and management: authorities; Retirement: pension oversight;

State financing and management; authorities; Michigan financial review commission; expand to include certain school districts. State financing and management: authorities; Retirement: pension oversight;

Charter Schools An Integral Part of the Utah Public Education System

Charter Schools An Integral Part of the Utah Public Education System Prepared by the Office of Legislative Research & General Counsel January 25,2011 What is a Charter School? Charter schools are public

Charter Schools An Integral Part of the Utah Public Education System Prepared by the Office of Legislative Research & General Counsel January 25,2011 What is a Charter School? Charter schools are public

Results. Success. Savings.

The New York State Property Tax Cap: Results. Success. Savings. 2015 Report Office of Governor Andrew M. Cuomo Executive Summary Local property taxes in New York are some of the highest in the country,

The New York State Property Tax Cap: Results. Success. Savings. 2015 Report Office of Governor Andrew M. Cuomo Executive Summary Local property taxes in New York are some of the highest in the country,

PROPERTY TAX CAPS AND SCHOOL COSTS

N O R T H S H O R E S C H O O L S B O A R D O F E D U C A T I O N 1 1 2 F R A N K L I N A V E N U E S E A C L I F F, N E W Y O R K POSITION PAPER PROPERTY TAX CAPS AND SCHOOL COSTS O C T O B E R, 2 0 0

N O R T H S H O R E S C H O O L S B O A R D O F E D U C A T I O N 1 1 2 F R A N K L I N A V E N U E S E A C L I F F, N E W Y O R K POSITION PAPER PROPERTY TAX CAPS AND SCHOOL COSTS O C T O B E R, 2 0 0

Working Budget for 2015-16 School Year. Community Budget Forum & Online Meeting March 3, 2015

Working Budget for 2015-16 School Year Community Budget Forum & Online Meeting March 3, 2015 Tonight s Agenda Welcome & explanation of tonight s meeting Board President James Maughan Budget Overview Superintendent

Working Budget for 2015-16 School Year Community Budget Forum & Online Meeting March 3, 2015 Tonight s Agenda Welcome & explanation of tonight s meeting Board President James Maughan Budget Overview Superintendent

5 YEAR FINANCIAL PLAN (2015-2019)

") BYLAW NO. 9220 EFFECTIVE DATE April 13, 2015 CONSOLIDATED FOR CONVENIENCE ONLY This is a consolidation of the bylaws listed below. The amendment bylaws have been combined with the original bylaw for convenience

BYLAW NO. 9220 EFFECTIVE DATE April 13, 2015 CONSOLIDATED FOR CONVENIENCE ONLY This is a consolidation of the bylaws listed below. The amendment bylaws have been combined with the original bylaw for convenience

TOWN OF MANCHESTER, MARYLAND. FINANCIAL STATEMENTS June 30, 2015

FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT... 1 MANAGEMENT S DISCUSSION AND ANALYSIS... 3 FINANCIAL STATEMENTS... 13 Government wide Financial Statements Statement of Net Position...14

FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT... 1 MANAGEMENT S DISCUSSION AND ANALYSIS... 3 FINANCIAL STATEMENTS... 13 Government wide Financial Statements Statement of Net Position...14

State of New Jersey Local Government Services

State of New Jersey Local Government Services Year: 2015 Municipal User Friendly Budget MUNICIPALITY: 526 2 Municode: 1908 Filename: 1908_fba_2015.xlsm Website: greentwp.com Phone Number: 908-852-9333

State of New Jersey Local Government Services Year: 2015 Municipal User Friendly Budget MUNICIPALITY: 526 2 Municode: 1908 Filename: 1908_fba_2015.xlsm Website: greentwp.com Phone Number: 908-852-9333

BUDGET AND FINANCIAL PLAN SUMMARY FILE

BUDGET AND FINANCIAL PLAN SUMMARY FILE BUDGETED REVENUES, EXPENDITURES, AND CHANGES IN CURRENT NET ASSETS Last Year (Actual) 2013 Current Year (Estimated) 2014 Adopted 2015 Proposed 2016 Proposed 2017

BUDGET AND FINANCIAL PLAN SUMMARY FILE BUDGETED REVENUES, EXPENDITURES, AND CHANGES IN CURRENT NET ASSETS Last Year (Actual) 2013 Current Year (Estimated) 2014 Adopted 2015 Proposed 2016 Proposed 2017

1976 ORDINANCES AND RESOLUTIONS

1976 ORD&RESPage 1 of 13 1976 ORDINANCES AND RESOLUTIONS Ord./Res.# 1-76 An ordinance amending ordinance no. 17-73, Board of Control, Section 2. 2-76 An ordinance authorizing the Mayor to enter into an

1976 ORD&RESPage 1 of 13 1976 ORDINANCES AND RESOLUTIONS Ord./Res.# 1-76 An ordinance amending ordinance no. 17-73, Board of Control, Section 2. 2-76 An ordinance authorizing the Mayor to enter into an

AD VALOREM TAX ADOPTED BUDGET

AD VALOREM TAX ADOPTED BUDGET AGGREGATE TAX RATE AMENDMENT APPROPRIATION ASSESSED VALUE BALANCE FORWARD BALANCE FORWARD - CAPITAL A tax levied on the assessed value of real property (also known as "property

AD VALOREM TAX ADOPTED BUDGET AGGREGATE TAX RATE AMENDMENT APPROPRIATION ASSESSED VALUE BALANCE FORWARD BALANCE FORWARD - CAPITAL A tax levied on the assessed value of real property (also known as "property

FY16 City Council Public Hearing and Financial Summary Notice... 373

Legal Forms Table of Contents FY16 Adopted Budget Resolution... 357 Exhibit A Expenditure Appropriations by Fund... 359 Exhibit B Fund Names... 365 FY16 State Shared Revenues Resolution... 367 FY16 State

Legal Forms Table of Contents FY16 Adopted Budget Resolution... 357 Exhibit A Expenditure Appropriations by Fund... 359 Exhibit B Fund Names... 365 FY16 State Shared Revenues Resolution... 367 FY16 State

Understanding Washington s Property Tax. Dean Carlson, Ways and Means Staff

Understanding Washington s Property Tax Dean Carlson, Ways and Means Staff Constitutional Requirements All taxes on real estate must be uniform within a taxing district. Tax uniformity requires both an

Understanding Washington s Property Tax Dean Carlson, Ways and Means Staff Constitutional Requirements All taxes on real estate must be uniform within a taxing district. Tax uniformity requires both an

Accounting and Reporting Manual

Office of the New York State Comptroller Division of Local Government and School Accountability Accounting and Reporting Manual Thomas P. DiNapoli State Comptroller For additional copies of this report

Office of the New York State Comptroller Division of Local Government and School Accountability Accounting and Reporting Manual Thomas P. DiNapoli State Comptroller For additional copies of this report

Town of Clinton Budget Recommendations

Town of Clinton Budget Recommendations Fiscal Year 2016 July 1, 2015 June 30, 2016 20-May-15 Fiscal Year 2015 Fiscal Year 2016 114 - Moderator Moderator Salary 100.00 100.00 Moderator Misc. Expense 50.00

Town of Clinton Budget Recommendations Fiscal Year 2016 July 1, 2015 June 30, 2016 20-May-15 Fiscal Year 2015 Fiscal Year 2016 114 - Moderator Moderator Salary 100.00 100.00 Moderator Misc. Expense 50.00

PROPOSED AMENDMENT TO ADD SECTION 5.1 TO ARTICLE XIII OF THE ILLINOIS CONSTITUTION

PROPOSED AMENDMENT TO ADD SECTION 5.1 TO ARTICLE XIII OF THE ILLINOIS CONSTITUTION That will be submitted to the voters November 6, 2012. This pamphlet includes the proposed amendment; explanation of the

PROPOSED AMENDMENT TO ADD SECTION 5.1 TO ARTICLE XIII OF THE ILLINOIS CONSTITUTION That will be submitted to the voters November 6, 2012. This pamphlet includes the proposed amendment; explanation of the

Property Tax Relief: The $7 Billion Reality

August 2008 Property Tax Relief: The $7 Billion Reality In the spring of 2006, Texas lawmakers passed a massive package of school finance reforms. School tax rates for maintenance and operations were to

August 2008 Property Tax Relief: The $7 Billion Reality In the spring of 2006, Texas lawmakers passed a massive package of school finance reforms. School tax rates for maintenance and operations were to

School District - Understanding the Capital Project and General Fund Types

SIGNIFICANT BUDGET AND ACCOUNTING REQUIREMENTS BASIS OF PRESENTATION FUND ACCOUNTING The District uses funds to report on its financial position and the result of its operations. A fund is defined as a

SIGNIFICANT BUDGET AND ACCOUNTING REQUIREMENTS BASIS OF PRESENTATION FUND ACCOUNTING The District uses funds to report on its financial position and the result of its operations. A fund is defined as a

County Government Efficiency Plans

County Government Efficiency Plans New York State Association of Counties October 2015 Hon. Maggie Brooks President Stephen J. Acquario Executive Director County Government Efficiency Plans NYSAC October

County Government Efficiency Plans New York State Association of Counties October 2015 Hon. Maggie Brooks President Stephen J. Acquario Executive Director County Government Efficiency Plans NYSAC October

LEGISLATURE OF THE STATE OF IDAHO Sixty-third Legislature Second Regular Session - 2016 IN THE HOUSE OF REPRESENTATIVES HOUSE BILL NO.

LEGISLATURE OF THE STATE OF IDAHO Sixty-third Legislature Second Regular Session - 0 IN THE HOUSE OF REPRESENTATIVES HOUSE BILL NO. BY REVENUE AND TAXATION COMMITTEE 0 0 0 AN ACT RELATING TO TAXING DISTRICT

LEGISLATURE OF THE STATE OF IDAHO Sixty-third Legislature Second Regular Session - 0 IN THE HOUSE OF REPRESENTATIVES HOUSE BILL NO. BY REVENUE AND TAXATION COMMITTEE 0 0 0 AN ACT RELATING TO TAXING DISTRICT

Estimating 2009 Circuit Breaker Credits: A 12-Step Guide for Indiana Local Governments

Estimating 2009 Circuit Breaker Credits: A 12-Step Guide for Indiana Local Governments Larry DeBoer Department of Agricultural Economics Purdue University June 2008 Indiana s 2008 property tax reform complicates

Estimating 2009 Circuit Breaker Credits: A 12-Step Guide for Indiana Local Governments Larry DeBoer Department of Agricultural Economics Purdue University June 2008 Indiana s 2008 property tax reform complicates

TASA Summary of Education Related Senate Interim Charges. 80 th Legislature

TASA Summary of Education Related Senate Interim Charges 80 th Legislature Education Study the effectiveness of public school programs serving special education students, including autistic students. Specifically,

TASA Summary of Education Related Senate Interim Charges 80 th Legislature Education Study the effectiveness of public school programs serving special education students, including autistic students. Specifically,

The primary focus of state and local government is to provide basic services,

Tax Relief and Local Government The primary focus of state and local government is to provide basic services, such as public safety, education, a safety net of health care and human services, transportation,

Tax Relief and Local Government The primary focus of state and local government is to provide basic services, such as public safety, education, a safety net of health care and human services, transportation,

AUDITING PROCEDURES REPORT Issued under P.A. 2 of 1968, as amended. Filing is mandatory.

Michigan Dept. of Treasury, Local Audit & Finance Division 496 (3-98), Formerly L-3147 AUDITING PROCEDURES REPORT Issued under P.A. 2 of 1968, as amended. Filing is mandatory. Local Government Type: City

Michigan Dept. of Treasury, Local Audit & Finance Division 496 (3-98), Formerly L-3147 AUDITING PROCEDURES REPORT Issued under P.A. 2 of 1968, as amended. Filing is mandatory. Local Government Type: City

PEORIA PUBLIC SCHOOLS DISTICT PRELIMINARY DISCUSSION OF FISCAL YEAR 2016 BUDGET. March 23, 2015

PEORIA PUBLIC SCHOOLS DISTICT 150 PRELIMINARY DISCUSSION OF FISCAL YEAR 2016 BUDGET March 23, 2015 Mark Wilcockson, Chief Financial Officer Carla Eman, Director of Budgets and Compliance Michael McKenzie,

PEORIA PUBLIC SCHOOLS DISTICT 150 PRELIMINARY DISCUSSION OF FISCAL YEAR 2016 BUDGET March 23, 2015 Mark Wilcockson, Chief Financial Officer Carla Eman, Director of Budgets and Compliance Michael McKenzie,

2011 BUDGET PRESENTATION

2011 BUDGET PRESENTATION 2010 Kingwood Township Tax Distribution Municipal Open Space 1.5% Local Municipal Tax 9.5% County Tax 16.3% Library 1.4% County Open Space 1.7% Regional School 25.2% District School

2011 BUDGET PRESENTATION 2010 Kingwood Township Tax Distribution Municipal Open Space 1.5% Local Municipal Tax 9.5% County Tax 16.3% Library 1.4% County Open Space 1.7% Regional School 25.2% District School

Understanding the Budget Process

Office of the New York State Comptroller Division of Local Government and School Accountability LOCAL GOVERNMENT MANAGEMENT GUIDE Understanding the Budget Process Thomas P. DiNapoli State Comptroller For

Office of the New York State Comptroller Division of Local Government and School Accountability LOCAL GOVERNMENT MANAGEMENT GUIDE Understanding the Budget Process Thomas P. DiNapoli State Comptroller For