Ref: B9/32C. 25 February 2011

|

|

|

- Jean Copeland

- 8 years ago

- Views:

Transcription

1 Ref: B9/32C 25 February 2011 Mr Allan Chiang Privacy Commissioner for Personal Data Office of the Privacy Commissioner for Personal Data 12/F, 248 Queen s Road East Wanchai Hong Kong BY FAX AND BY HAND Dear Allan, Sharing of Positive Mortgage Data Further to my letter to you dated 23 February 2011, I am writing regarding the comments of the Hong Kong Bar Association ( HKBA ) in its submission on the Consultation Document which it has posted on its website. Our views, mainly in relation to legal issues raised by the HKBA, are set out below. Please also note that we have in parallel initiated discussions with the HKBA in order to address the points raised in its submission to your office. Paragraph 9 The HKBA remarked in paragraph 9 that the Code of Practice on Consumer Credit Data (the Code ) has shifted from a pro-privacy initiative to a mechanism for legitimising privacy-intrusion. We do not think this is a reasonable description of the purpose or intention of introducing positive or negative credit data sharing which in our view involves important public interest concerns. Specifically, we are of the view that any change in the law or the Code is about finding the right balance between the privacy interests of individuals and the public interest at a given point of time as the right to personal data privacy is not absolute. The principal objective of the industry proposal is to promote responsible lending and borrowing and prevent overborrowing and in so doing enhance the overall financial stability in Hong

2 - 2 - Kong. We note that HKBA itself also recognises that reducing risk of defaults is a laudable aim. Paragraphs 23 to 34 According to the HKBA (see paragraphs 31 & 32 of its submissions), since there is no evidence on the extent to which individuals are taking on mortgages in relation to non-residential property and the delinquency rates in relation to such mortgages, or evidence that the borrowers are being untruthful, the case for saying that the additional data which the credit reference agency ( CRA ) should be permitted to collect are necessary and not excessive (for the purpose of assessing the credit worthiness of the individuals to which the data relate) does not begin to be made out. The HKBA further states in paragraph 33 that unless and until such a case is made out on the basis of compelling evidence, the proposal to expand the mortgage data that the CRA is permitted to collect must be rejected because it has not been shown that DPP1(1) would be complied with. The reason why we have not provided the evidence mentioned is because without positive mortgage data sharing, we have no means of collecting such data as customers are unlikely to admit they have been untruthful and they do not necessarily borrow only from one bank but from different banks so each bank is not able to conduct a proper and comprehensive credit risk assessment. There are nevertheless anecdotal evidence of property borrowers getting mortgage loans from different banks. You would recall in November last year we sent you the attached newspaper clipping (at Annex 1) of a pensioner who was speculating in property by borrowing from multiple banks who were unable to verify her credit worthiness due to a lack of positive mortgage data sharing. There is no reason to assume that this type of behaviour is exceptional. Furthermore, from a legal perspective, DPP1(1) provides that: (1) Personal data shall not be collected unless (a) the data are collected for a lawful purpose directly related to a function or activity of the data user who is to use the data; (b) subject to paragraph (c), the collection of the data is necessary for or directly related to that purpose; and (c) the data are adequate but not excessive in relation to that purpose.

should be permitted to collect are necessary and not excessive (for the purpose of assessing the credit worthiness of the individuals to which the data relate) does not begin")

3 - 3 - It is important to note that there is no requirement under DPP1(1) that the purpose for which the data is collected has to be substantiated or validated by evidence. DPP 1(1) places no limit on the purpose for which data may be collected, as long as it is collected for a lawful purpose, which is directly related to a function or activity of the data user. The industry proposal is therefore clearly consistent with DPP1(1)(a) since the data are collected by the CRA for a lawful purpose directly related to its function or activity as a credit reference agency, i.e. to create a credit profile of borrowers for credit risk assessment purposes. DPP1(1)(c) then requires the data to be adequate but not excessive in relation to that purpose. DPP1(b) provides that subject to (c), the collection is necessary for or directly related to such a lawful purpose. We would also like to draw reference to the book entitled Data Protection Principles of Personal Data (Privacy) Ordinance from the Privacy Commissioner s perspective (2nd Edition) published by your office. According to paragraph 5.9 of the book, the Privacy Commissioner has expressed the view that in considering whether the collection of data is in compliance with DPP(1) in the absence of any applicable code of practice, the following are relevant factors to be considered: (a) (b) (c) (d) (e) the particular function or activity to which the collection of the data concerned is considered directly related; the degree of sensitivity of such data; the legitimate purposes to be served in collecting the personal data and the adverse impact on personal data privacy; whether there is a real need (i.e. the likelihood of such need arising) for the data to be collected in order to carry out that function or activity; and whether there is any realistic and less privacy intrusive alternative for attaining the purpose of collection. In the context of the industry proposal which will require changes to the Code, we and the industry have considered carefully the above factors. The data that will be contributed by the credit providers to the CRA are set out in paragraph 4.2(b)(i) of the Consultation Document, which according to the industry, are the minimum that are necessary to enable the CRA to identify accurately each individual involved in a consumer mortgage loan and compile the mortgage count. Indeed, it has been indicated in paragraph 5.31 of the Consultation Document that subject to the determination on the types

(c) then requires the data to be adequate but not excessive in relation to that purpose.")

4 - 4 - of mortgage loans to be covered under Issue 1, the proposed types of data items to be contributed and assessed represent the minimum amount of data necessary for the purposes of assessing the credit risk of consumer credit applications. Besides, it is proposed that the credit providers will have access to the mortgage count only, instead of the entirety of the data contributed to the CRA by credit providers as set out in paragraph 4.2(b)(i) of the Consultation Document. There is also no realistic alternative for achieving the purpose of collection of the data in respect of pre-existing mortgages. Based on the above, we have been advised by our Office of the General Counsel that there is no contravention of DPP1(1), and the data that are to be collected by the CRA as a credit reference agency appear to be necessary, adequate and not excessive. Paragraphs 39 to 50 The HKBA takes the view that the transfer of the positive mortgage data to the CRA would be contrary to DPP3 (see paragraphs 44 and 47 of its submission). DPP3 is set out below: Personal data shall not, without the prescribed consent of the data subject, be used for any purpose other than (a) (b) the purpose for which the data were to be used at the time of collection of the data; or a purpose directly related to the purpose referred to in paragraph (a). The HKBA relies on the guidance provided by your office 1 on how you would interpret DPP3: In assessing whether the act in question is done for a directly related purpose and thus covered by DPP3(b), the Commissioner will take into account factors such as: the nature of the transaction giving rise to the need for using the personal data; and 1 The HKBA quoted paragraph 7.25 from the older version of the book entitled Data Protection Principles of Personal Data (Privacy) Ordinance from the Privacy Commissioner s perspective, Office of the Privacy Commissioner for Personal Data, August The same paragraph appears in the 2010 version at paragraph 7.26.

(i) of the Consultation Document. There is also no realistic alternative for achieving the purpose of collection of the data in respect of pre-existing mortgages.")

5 - 5 - the reasonable expectation of the data subject. (Emphasis added.) The HKBA argues that since the transfer of the positive mortgage data to the CRA was not permitted under the Code at the time when the data were collected, the data subject would not have expected this to occur. Accordingly, it takes the view that the transfer will not be done for the purpose for which the data were to be used at the time of collection of the data or for a directly related purpose. First and foremost, we would like to point out the stance adopted by your office as demonstrated by paragraph 1.12 of the aforesaid guidance is for reference only and it was stated in the guidance that such stance shall not bind your office in the exercise of the Commissioner s statutory functions in any way. Furthermore, it was stated that rather than relying on such views the reader is urged to exercise independent judgement on the interpretations of the data protection principles and where appropriate avail himself of professional advice. In conjunction with our Office of the General Counsel, I have considered the legal opinion of Senior Counsel obtained on this matter, which the industry has previously submitted to you, and agree with his detailed analysis based on a purposive construction of DPP3. In particular, we agree that all the DPPs should be read together and should be construed purposively to promote the objectives of the Personal Data (Privacy) Ordinance ( PDPO ). DPP3(a) refers to the purpose for which the data were to be used at the time of collection of data ( Original Purpose ), while DPP3(b) refers to a directly related purpose. In constructing what is the Original Purpose, the data user may have informed the data subject the Original Purpose explicitly, or in the absence of any explicit communication, the Original Purpose may be implied. 2 In determining the implied purpose for which the personal data were collected at the time of collection, all circumstances, including the reasonable expectation of the data subjects are relevant. Applying this to the industry proposal, it must have been within the reasonable expectation of the customer when applying for a loan that his personal data would be used for creating a credit profile to enable the proper assessment of credit risk. Therefore, we are of the view that the transfer of the data to the CRA to enable the creation of a credit profile for risk evaluation is within the Original Purpose albeit such purpose is an implied purpose. In this 2 DPP1(3) provides that data user must take all practical steps to explicitly inform a data subject of the purpose for which data are collected. Since this is not an absolute obligation, this shows that the Original Purpose may be implied in the absence of any explicit communication by the data user to the data subject.

6 - 6 - connection, please see paragraphs 19 to 24 of Senior Counsel s Opinion at Annex 2. Further or in the alternative, we rely on DPP3(b) which enables the use of personal data for a directly related purpose to enable the transfer of personal data to the CRA. This is because the transfer of data to the CRA to enable the creation of a credit profile of the customer is directly related to the Original Purpose of credit risk assessment. In contrast to DPP3(a), when determining the directly related purpose (which is not confined to the time of collection of data), the question is determined by whether it is directly related to the Original Purpose and is not dependent on whether the customer reasonably contemplated or expected that directly related purpose at the time of the mortgage loan application when the personal data were collected. In this connection, we refer you to paragraphs 25 to 31 of Senior Counsel s opinion at Annex 3. Apart from the MPF example cited in the Senior Counsel s opinion at paragraphs 28 to 30, the Senior Counsel s view is also supported by the Administrative Appeals Board ( AAB ) decision of 袁 碧 真 v Privacy Commissioner for Personal Data, AAB No. 41/2006. In this case, the appellant provided her personal data, including her name, address, and telephone number to the management company when she complained about the foul smell in the corridor outside her flat. The appellant had expressly told the representative of the management company that if it decided to make a report to the police, the management should preserve her anonymity. The AAB upheld the views of the then Privacy Commissioner and ruled that although the management company had promised the appellant that it would not disclose her personal data to the police, when the management company provided the appellant s personal data to the police, it was using the personal data for a purpose which was directly related to a purpose for which her data were collected in the first place 3. It is worth pointing out that in this case the ruling was made even though the transfer of information to the Police was not within the appellant s reasonable contemplation at the time the data was collected nor had the appellant given her prescribed consent for the transfer. Applying this case to the industry proposal, it would seem even if the uploading of such data to CRA was not within the applicant s reasonable contemplation, the data can still be uploaded to CRA as this serves a directly related purpose. 3 On the facts of this case, section 58(2)(a)of the PDPO provides that personal data are exempt from the provisions of DPP3 anyway. However, the decision contains detailed analysis on how DPP3 is to be applied and why the agreement between the data subject and the data user was irrelevant in considering whether DPP3 has been contravened.

, when determining the directly related purpose (which is not confined to the time of collection of data), the question is determined by whether it is directly related to the")

7 - 7 - Paragraphs 51 to 55 The HKBA states in paragraph 52 of its submission that the requirement of the written consent of data subjects prior to access by credit providers to the proposed additional mortgage data does not help to address the issue discussed above in paragraphs 39 to 50 in relation to Issue 3. However, the HKBA supports and welcomes the requirement for consent as a further level of privacy protection for sharing of mortgage data by CRA. We would just emphasize that the requirement for written consent of data subjects is indeed an important level of privacy protection. As the transfer of data to the CRA is only a preparatory step, no true sharing of data will occur without the customer s written consent. Paragraphs 56 to 60 On the benefits of the transitional period, the HKBA should perhaps refer to paragraphs 5.41 and 5.42 of the Consultation Document which explain the transitional period in greater detail. The purpose of the transitional period is to ensure any positive mortgage data collected by the CRA could not be accessed and used during the transitional period other than new applications for credit facilities and certain prescribed exceptional circumstances, such as financial difficulties of the customer, or when there is a need for debt restructuring. This may be beneficial to those who have over-borrowed in that it would offer a longer period of time in which they would be able to reassess and revise a realistic repayment schedule with their lending institutions. It is also useful to point out that under the industry proposal, a credit provider will have to obtain an individual's written consent to access his mortgage count whether before or after expiry of the transitional period. If an individual applies for any consumer credit from a credit provider on or after the proposal implementation date, that credit provider will obtain his written consent to access his mortgage count at the CRA. The credit provider will then access his mortgage count for processing that application or if the other specified circumstances (e.g. debt restructuring etc.) occurs during the transitional period, and will not otherwise access his mortgage count until expiry of the transitional period. There is no need to obtain the individual's written consent again for accessing his mortgage count after expiry of the transitional period because the initial written consent already covers it. On the other hand, if an individual does not apply for any consumer credit from any credit provider after the implementation date (i.e. there is no opportunity for any credit provider to obtain his written consent to access his mortgage

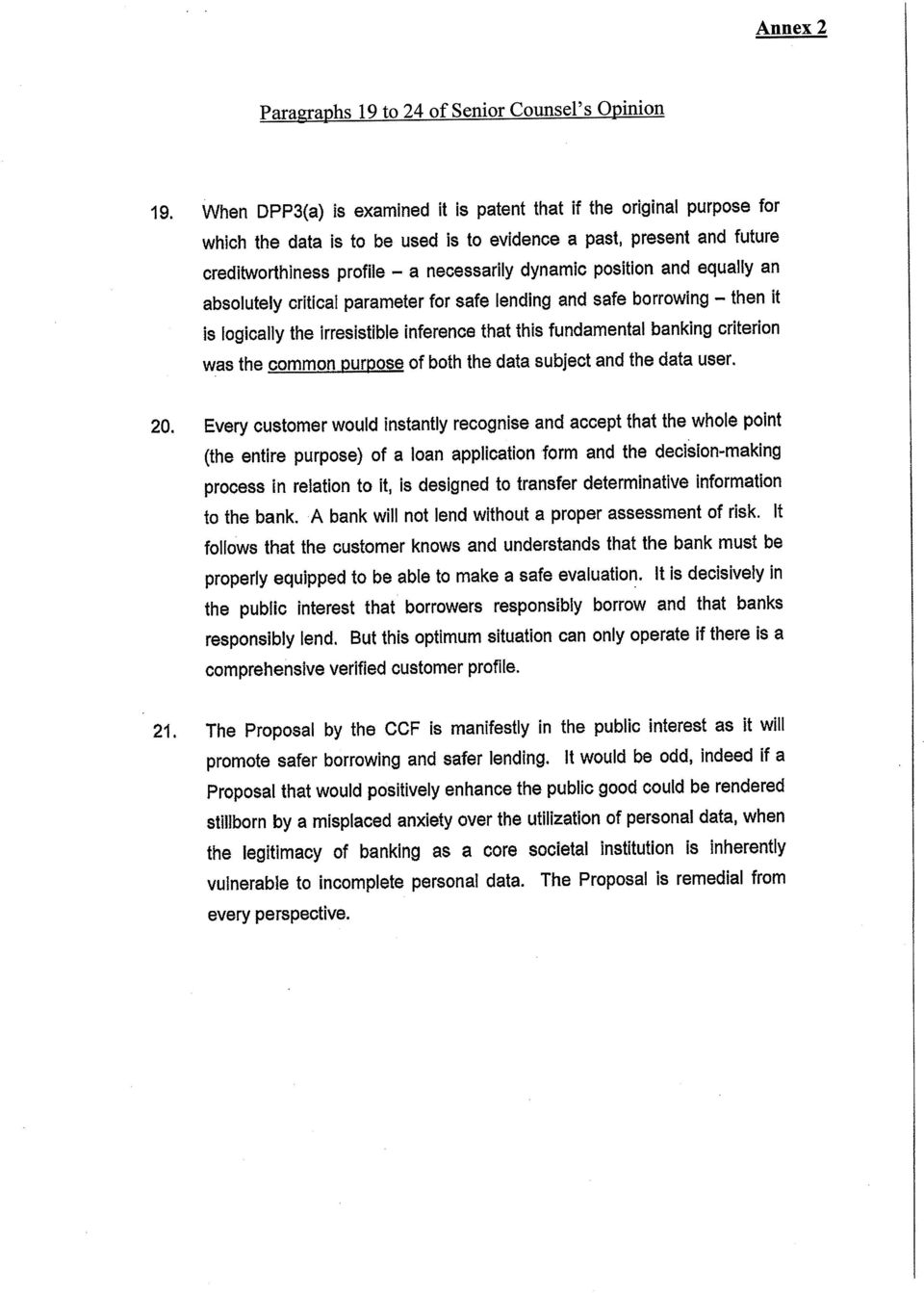

8 - 8 - count at the CRA), no credit provider will access his mortgage count at the CRA for any purpose whether during or after the transitional period. In line with the treatment of the HKMA s submissions to you in response to the Consultation exercise, we will be posting this letter on the HKMA website. Yours sincerely, Arthur Yuen Deputy Chief Executive c.c. Policy 21 Limited The Chairman, Consumer Credit Forum The Chairman, HKAB The Chairman, DTCA FSTB (Attn: Miss Natalie Li) Encl.

9

10

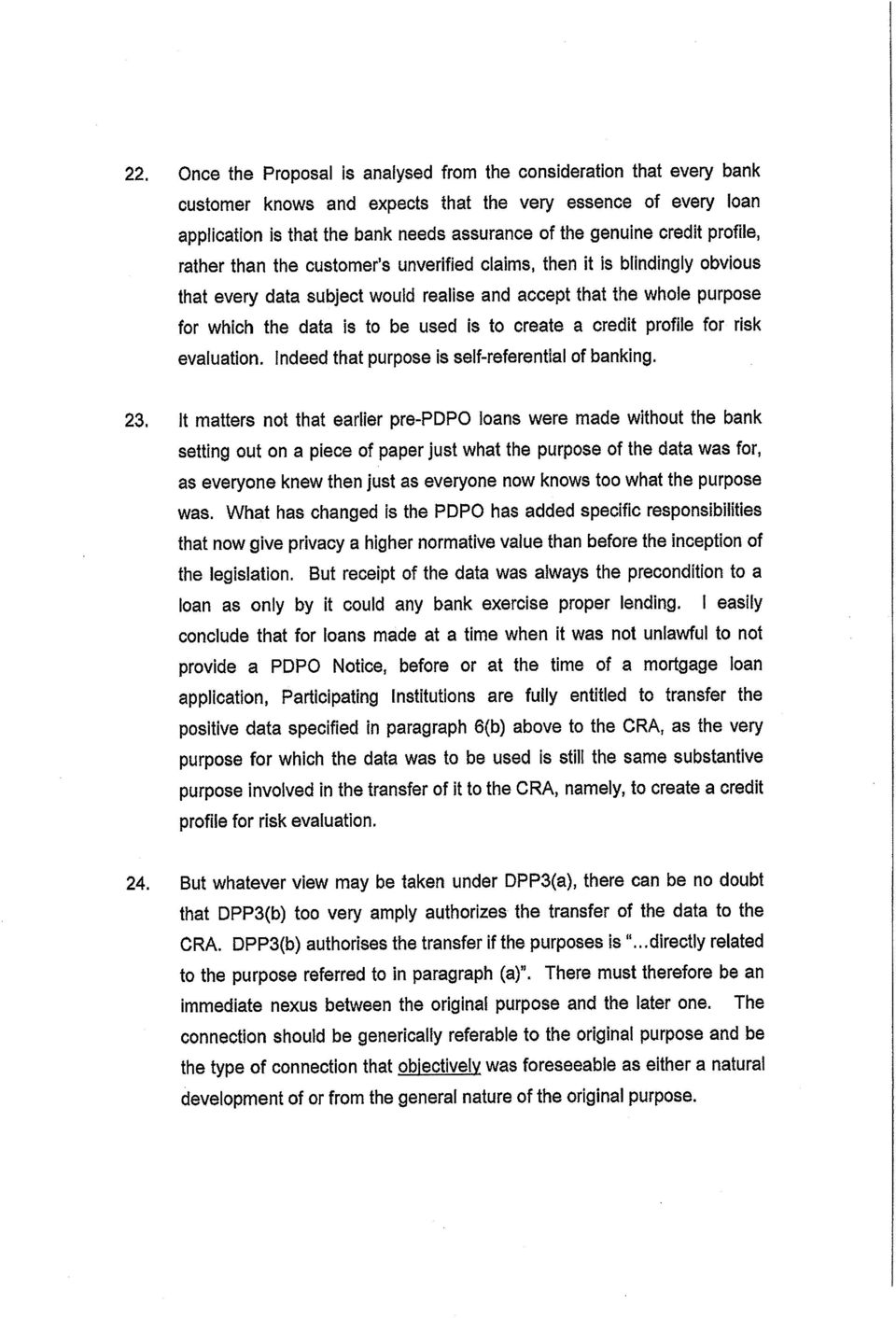

11

12

13

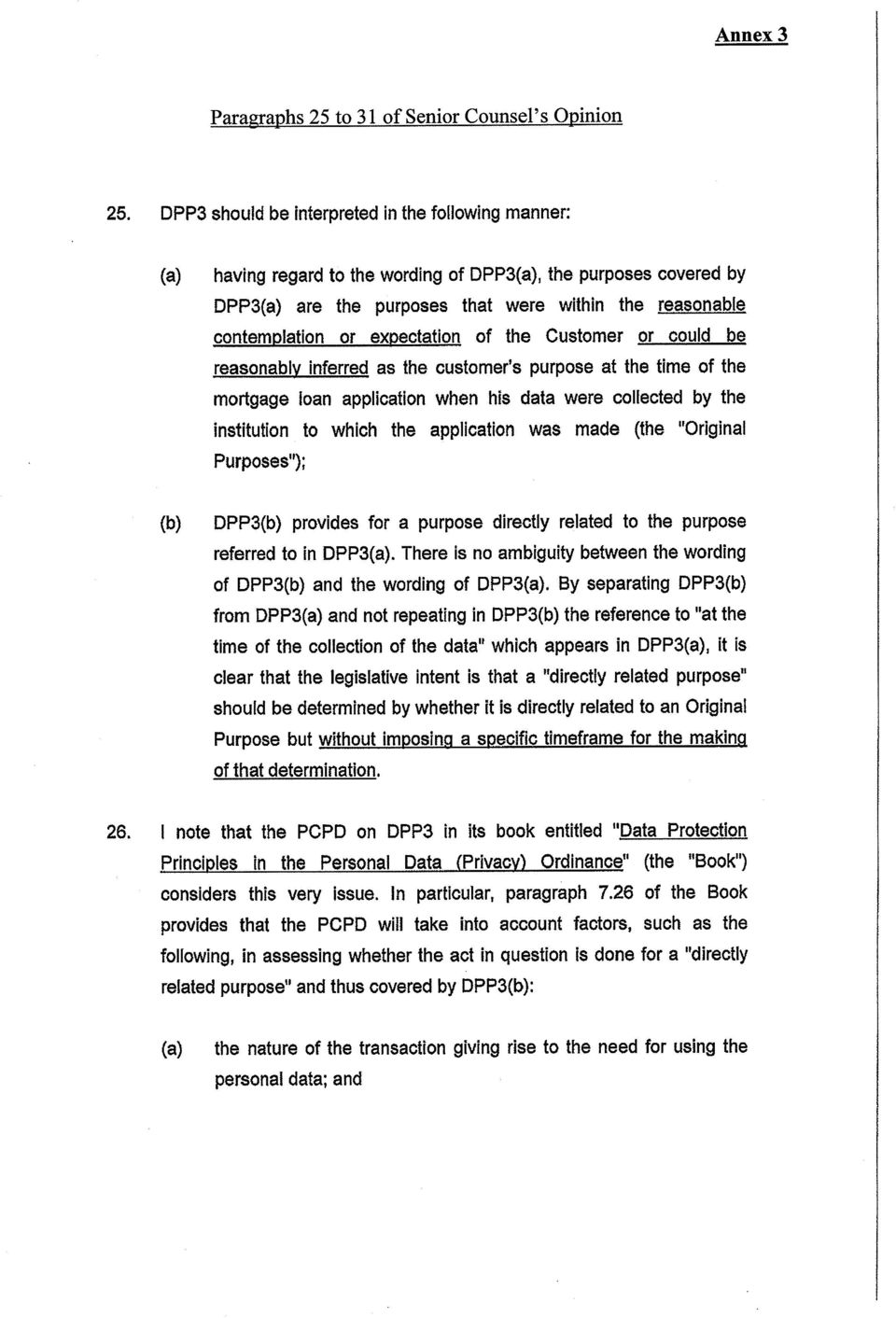

Report Published under Section 48(2) of the Personal Data (Privacy) Ordinance (Cap. 486) Report Number: R10-11568

of the Personal Data (Privacy) Ordinance (Cap. 486) Report Number: R10-11568") Report Published under Section 48(2) of the Personal Data (Privacy) Ordinance (Cap. 486) Report Number: R10-11568 Date issued: 24 February 2010 Debt Collection Agency authorized by a Finance Company Disclosed

Report Published under Section 48(2) of the Personal Data (Privacy) Ordinance (Cap. 486) Report Number: R10-11568 Date issued: 24 February 2010 Debt Collection Agency authorized by a Finance Company Disclosed

Report Published under Section 48(2) of the Personal Data (Privacy) Ordinance (Cap. 486) Report Number: R11-1696

of the Personal Data (Privacy) Ordinance (Cap. 486) Report Number: R11-1696") Report Published under Section 48(2) of the Personal Data (Privacy) Ordinance (Cap. 486) Report Number: R11-1696 Date issued: 20 June 2011 Transfer of Customers Personal Data by Fubon Bank (Hong Kong)

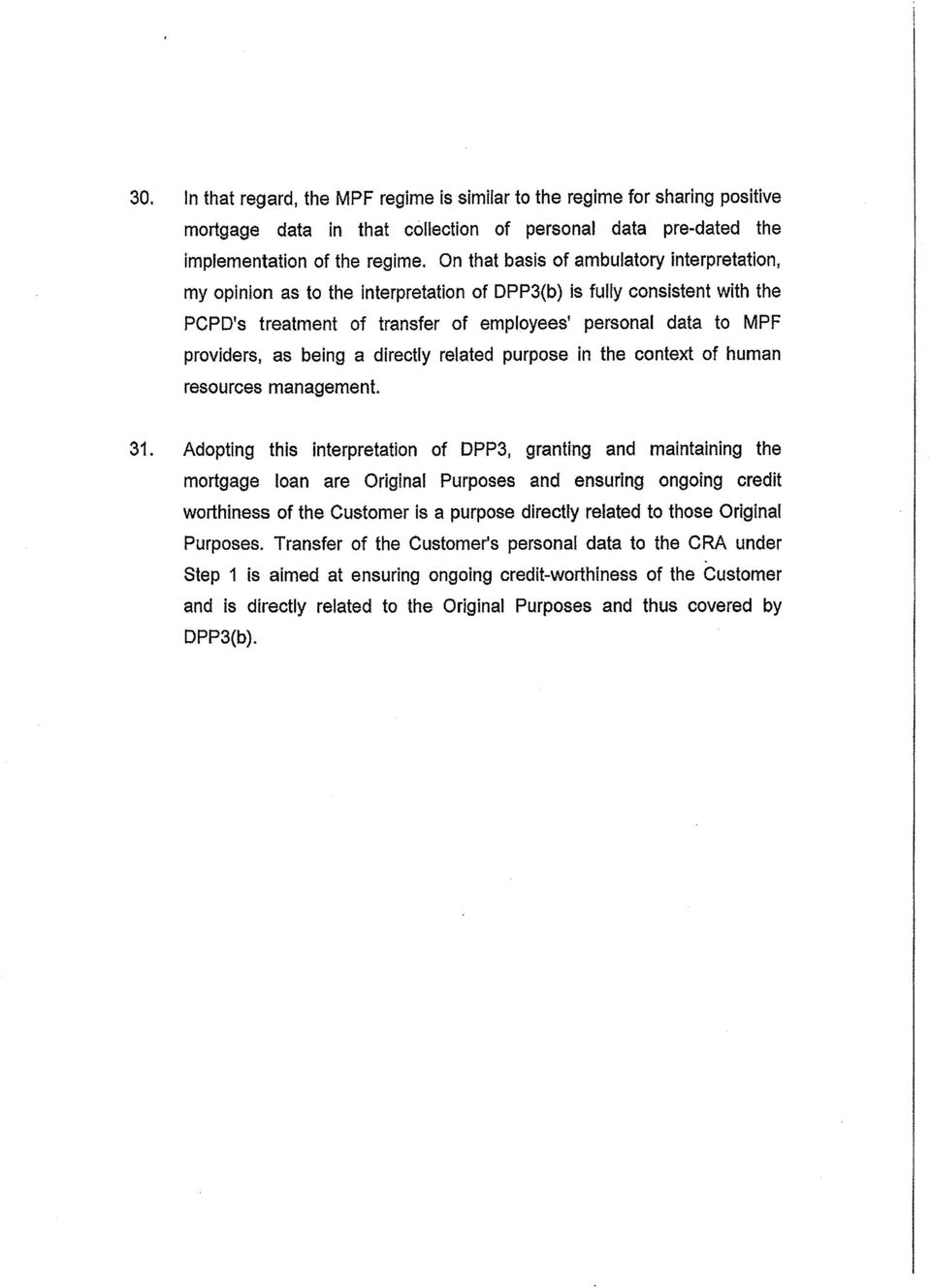

Report Published under Section 48(2) of the Personal Data (Privacy) Ordinance (Cap. 486) Report Number: R11-1696 Date issued: 20 June 2011 Transfer of Customers Personal Data by Fubon Bank (Hong Kong)

Supervisory Policy Manual

This module should be read in conjunction with the Introduction and with the Glossary, which contains an explanation of abbreviations and other terms used in this Manual. If reading on-line, click on blue

This module should be read in conjunction with the Introduction and with the Glossary, which contains an explanation of abbreviations and other terms used in this Manual. If reading on-line, click on blue

Code of Practice on Human Resource Management Office of the Privacy Commissioner for Personal Data 12/F, 248 Queen s Road East, Wanchai, Hong Kong Tel: 2827 2827 Fax: 2877 7026 Internet: http://www.pcpd.org.hk

Code of Practice on Human Resource Management Office of the Privacy Commissioner for Personal Data 12/F, 248 Queen s Road East, Wanchai, Hong Kong Tel: 2827 2827 Fax: 2877 7026 Internet: http://www.pcpd.org.hk

Decision Notice. Decision 136/2015: Mr Patrick Kelly and NHS Tayside. Information relating to Professor Muftah Salem Eljamel

Decision Notice Decision 136/2015: Mr Patrick Kelly and NHS Tayside Information relating to Professor Muftah Salem Eljamel Reference No: 201500390 Decision Date: 24 August 2015 Summary On 2 December 2014,

Decision Notice Decision 136/2015: Mr Patrick Kelly and NHS Tayside Information relating to Professor Muftah Salem Eljamel Reference No: 201500390 Decision Date: 24 August 2015 Summary On 2 December 2014,

Information Paper for the Legislative Council Panel on Financial Affairs. Protection of Consumer Credit Data

LC Paper No. CB(1)691/03-04(01) Information Paper for the Legislative Council Panel on Financial Affairs Protection of Consumer Credit Data Purpose Pursuant to the request by the Panel vide the Clerk to

LC Paper No. CB(1)691/03-04(01) Information Paper for the Legislative Council Panel on Financial Affairs Protection of Consumer Credit Data Purpose Pursuant to the request by the Panel vide the Clerk to

Our Ref.: B4/1C. 14 September 2012. The Chief Executive All Authorized Institutions. Dear Sir/Madam, Prudential Measures for Property Mortgage Loans

Our Ref.: B4/1C 14 September 2012 The Chief Executive All Authorized Institutions Dear Sir/Madam, Prudential Measures for Property Mortgage Loans The Hong Kong Monetary Authority (HKMA) notices that there

Our Ref.: B4/1C 14 September 2012 The Chief Executive All Authorized Institutions Dear Sir/Madam, Prudential Measures for Property Mortgage Loans The Hong Kong Monetary Authority (HKMA) notices that there

Our Ref.: B4/1C. 22 February 2013. The Chief Executive All Authorized Institutions. Dear Sir/Madam, Prudential Measures for Property Mortgage Loans

Our Ref.: B4/1C 22 February 2013 The Chief Executive All Authorized Institutions Dear Sir/Madam, Prudential Measures for Property Mortgage Loans The Hong Kong Monetary Authority (HKMA) has been closely

Our Ref.: B4/1C 22 February 2013 The Chief Executive All Authorized Institutions Dear Sir/Madam, Prudential Measures for Property Mortgage Loans The Hong Kong Monetary Authority (HKMA) has been closely

CODE OF MONEY LENDING PRACTICE. 1. Status of the Code of Money Lending Practice 1 2. Objectives 1 3. Principles 2 4. Enquiries 2

CODE OF MONEY LENDING PRACTICE PART I - INTRODUCTION TABLE OF CONTENTS Page 1. Status of the Code of Money Lending Practice 1 2. Objectives 1 3. Principles 2 4. Enquiries 2 PART II RECOMMENDATIONS OF MONEY

CODE OF MONEY LENDING PRACTICE PART I - INTRODUCTION TABLE OF CONTENTS Page 1. Status of the Code of Money Lending Practice 1 2. Objectives 1 3. Principles 2 4. Enquiries 2 PART II RECOMMENDATIONS OF MONEY

Prudential Measures for Property Mortgage Loans

Our Ref.: B1/15C B9/25C 27 February 2015 The Chief Executive All Authorized Institutions Dear Sir/Madam, Prudential Measures for Property Mortgage Loans With the HKMA s introduction of the sixth round

Our Ref.: B1/15C B9/25C 27 February 2015 The Chief Executive All Authorized Institutions Dear Sir/Madam, Prudential Measures for Property Mortgage Loans With the HKMA s introduction of the sixth round

The aim and benefits of a CCRA. The operation of the CCRA scheme

Increasing public attention has been given to the need of small and medium-sized enterprises (SMEs) for greater access to credit. At the same time it is recognised that lending institutions need access

Increasing public attention has been given to the need of small and medium-sized enterprises (SMEs) for greater access to credit. At the same time it is recognised that lending institutions need access

Consideration of Laws and Regulations in an Audit of Financial Statements

HKSA 250 Issued July 2009; revised July 2010 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard on Auditing 250 Consideration of Laws and

HKSA 250 Issued July 2009; revised July 2010 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard on Auditing 250 Consideration of Laws and

Decision 147/2011 Dr X and Fife NHS Board. Details of complaints. Reference No: 201100681, 201100688, 201100795 Decision Date: 5 August 2011

and Fife NHS Board Details of complaints Reference No: 201100681, 201100688, 201100795 Decision Date: 5 August 2011 Kevin Dunion Scottish Information Commissioner Kinburn Castle Doubledykes Road St Andrews

and Fife NHS Board Details of complaints Reference No: 201100681, 201100688, 201100795 Decision Date: 5 August 2011 Kevin Dunion Scottish Information Commissioner Kinburn Castle Doubledykes Road St Andrews

Personal Data (Privacy) Ordinance and Electronic Health Record Sharing System (Points to Note for Healthcare Providers and Healthcare Professionals)

Ordinance and Electronic Health Record Sharing System (Points to Note for Healthcare Providers and Healthcare Professionals)") Personal Data (Privacy) Ordinance and Electronic Health Record Sharing System (Points to Note for Healthcare Providers and Healthcare Professionals) The Electronic Health Record Sharing System Ordinance

Personal Data (Privacy) Ordinance and Electronic Health Record Sharing System (Points to Note for Healthcare Providers and Healthcare Professionals) The Electronic Health Record Sharing System Ordinance

LC Paper No. CB(2)1515/13-14(01)

1515/13-14(01)") LC Paper No. CB(2)1515/13-14(01) Annex I Comments on the legal and drafting issues on Electronic Health Record Sharing System Bill Clause 1 (Short title and commencement) 1. Please advise the expected

LC Paper No. CB(2)1515/13-14(01) Annex I Comments on the legal and drafting issues on Electronic Health Record Sharing System Bill Clause 1 (Short title and commencement) 1. Please advise the expected

Frequently Asked Questions About Recruitment Advertisements

Understanding the Code of Practice on Human Resource Management Frequently Asked Questions About Recruitment Advertisements The Code of Practice on Human Resource Management ( the Code ) was issued pursuant

Understanding the Code of Practice on Human Resource Management Frequently Asked Questions About Recruitment Advertisements The Code of Practice on Human Resource Management ( the Code ) was issued pursuant

Control measures for guarding against some recent fraud cases

Our Ref.: B1/15C B9/81C 5 June 2014 The Chief Executive All Authorized Institutions Dear Sir/Madam, Control measures for guarding against some recent fraud cases I am writing to draw the attention of your

Our Ref.: B1/15C B9/81C 5 June 2014 The Chief Executive All Authorized Institutions Dear Sir/Madam, Control measures for guarding against some recent fraud cases I am writing to draw the attention of your

CIS/3066/1998 OF THE COMMISSIONER

..... - CIS/3066/1998 DECISION OF THE COMMISSIONER 1. This is an appeal, brought by the claimant with the leave of a Commissioner, against a decision of the Plymouth social security appeal tribunal dated

..... - CIS/3066/1998 DECISION OF THE COMMISSIONER 1. This is an appeal, brought by the claimant with the leave of a Commissioner, against a decision of the Plymouth social security appeal tribunal dated

How To Calculate Asset Concentration In An Accumulator

Our Ref: B1/15C G16/1C 7 March 2014 The Chief Executive All Authorized Institutions Dear Sir / Madam, Foreign Exchange Accumulators 1 ( FX accumulators ) and Non-leveraged Renminbi ( RMB )-Linked Deposits

Our Ref: B1/15C G16/1C 7 March 2014 The Chief Executive All Authorized Institutions Dear Sir / Madam, Foreign Exchange Accumulators 1 ( FX accumulators ) and Non-leveraged Renminbi ( RMB )-Linked Deposits

Complaint about Advertising Claims and Sales Conduct of China Mobile Hong Kong Company Limited

CDN:0226 Complaint about Advertising Claims and Sales Conduct of China Mobile Hong Kong Company Limited s Salesperson Complaint against: Issue: Relevant Instruments: China Mobile Hong Kong Company Limited

CDN:0226 Complaint about Advertising Claims and Sales Conduct of China Mobile Hong Kong Company Limited s Salesperson Complaint against: Issue: Relevant Instruments: China Mobile Hong Kong Company Limited

Communication between the Auditor and the Insurance Authority

PN 620.2 Revised February 2013 Practice Note 620.2 Communication between the Auditor and the Insurance Authority PRACTICE NOTE 620.2 COMMUNICATION BETWEEN THE AUDITOR AND THE INSURANCE AUTHORITY (Issued

PN 620.2 Revised February 2013 Practice Note 620.2 Communication between the Auditor and the Insurance Authority PRACTICE NOTE 620.2 COMMUNICATION BETWEEN THE AUDITOR AND THE INSURANCE AUTHORITY (Issued

Disclosure of Loans to Officers

AB 1 Issued August 1985 Accounting Bulletin 1 Disclosure of Loans to Officers AB 1 COPYRIGHT Copyright 2008 Hong Kong Institute of Certified Public Accountants This Accounting Bulletin contains Hong Kong

AB 1 Issued August 1985 Accounting Bulletin 1 Disclosure of Loans to Officers AB 1 COPYRIGHT Copyright 2008 Hong Kong Institute of Certified Public Accountants This Accounting Bulletin contains Hong Kong

CLEARING AND SETTLEMENT SYSTEMS BILL

C1881 CLEARING AND SETTLEMENT SYSTEMS BILL CONTENTS Clause Page PART 1 PRELIMINARY 1. Short title and commencement... C1887 2. Interpretation... C1887 PART 2 DESIGNATION AND OVERSIGHT Division 1 Designation

C1881 CLEARING AND SETTLEMENT SYSTEMS BILL CONTENTS Clause Page PART 1 PRELIMINARY 1. Short title and commencement... C1887 2. Interpretation... C1887 PART 2 DESIGNATION AND OVERSIGHT Division 1 Designation

INLAND REVENUE BOARD OF REVIEW DECISIONS. Case No. D22/01

Case No. D22/01 Salaries tax deduction home loan interest refinance of mortgage section 26E of the Inland Revenue Ordinance ( IRO ). Panel: Andrew Halkyard (chairman), Patrick Ho Pak Tai and Paul Mok Yun

Case No. D22/01 Salaries tax deduction home loan interest refinance of mortgage section 26E of the Inland Revenue Ordinance ( IRO ). Panel: Andrew Halkyard (chairman), Patrick Ho Pak Tai and Paul Mok Yun

Investigation Report: The Hong Kong Police Force. Leaked Internal Documents Containing Personal Data. via Foxy

Published under Section 48(2) of the Personal Data (Privacy) Ordinance (Cap. 486) Investigation Report: The Hong Kong Police Force Leaked Internal Documents Containing Personal Data via Foxy (English translation)

Published under Section 48(2) of the Personal Data (Privacy) Ordinance (Cap. 486) Investigation Report: The Hong Kong Police Force Leaked Internal Documents Containing Personal Data via Foxy (English translation)

CHAPTER 11 MONEY BROKERS

CHAPTER 11 MONEY BROKERS Introduction 11.1 The MA, pursuant to section 118C(7) of the Ordinance, has issued a Guideline on Approval and Revocation of Approval of Money Brokers (the Guideline) which describes

CHAPTER 11 MONEY BROKERS Introduction 11.1 The MA, pursuant to section 118C(7) of the Ordinance, has issued a Guideline on Approval and Revocation of Approval of Money Brokers (the Guideline) which describes

Disclosure of Interests in Other Entities

HKFRS 12 Revised November 2014January 2015 Effective for annual periods beginning on or after 1 January 2013 Hong Kong Financial Reporting Standard 12 Disclosure of Interests in Other Entities COPYRIGHT

HKFRS 12 Revised November 2014January 2015 Effective for annual periods beginning on or after 1 January 2013 Hong Kong Financial Reporting Standard 12 Disclosure of Interests in Other Entities COPYRIGHT

Overview of the Impact of the Privacy Reforms on Credit Reporting

Overview of the Impact of the Privacy Reforms on Credit Reporting June 2012 Andrew Galvin, Partner 1 OVERVIEW 1.1 Credit Reporting Reform - Background When initially passed, the Privacy Act 1988 essentially

Overview of the Impact of the Privacy Reforms on Credit Reporting June 2012 Andrew Galvin, Partner 1 OVERVIEW 1.1 Credit Reporting Reform - Background When initially passed, the Privacy Act 1988 essentially

CLSA ASIA-PACIFIC SECURITIES DEALING SERVICES: AUSTRALIA MARKET ANNEX

CLSA ASIA-PACIFIC SECURITIES DEALING SERVICES: AUSTRALIA MARKET ANNEX IMPORTANT NOTICE CLSA Singapore Pte Ltd (ARBN 125 288 271, a company incorporated in Singapore) is permitted to provide certain financial

CLSA ASIA-PACIFIC SECURITIES DEALING SERVICES: AUSTRALIA MARKET ANNEX IMPORTANT NOTICE CLSA Singapore Pte Ltd (ARBN 125 288 271, a company incorporated in Singapore) is permitted to provide certain financial

Mortgage Brokerages, Lenders and Administrators Act, 2006. Additional Draft Regulations for Consultation

Mortgage Brokerages, Lenders and Administrators Act, 2006 Additional Draft Regulations for Consultation Proposed by the Ministry of Finance January, 2008 Mortgage Brokerages, Lenders and Administrators

Mortgage Brokerages, Lenders and Administrators Act, 2006 Additional Draft Regulations for Consultation Proposed by the Ministry of Finance January, 2008 Mortgage Brokerages, Lenders and Administrators

Online Behavioural Tracking / April 2014

Online Behavioural Tracking This information leaflet aims to highlight to organisations what they should consider before deployment of online tracking on their websites. It explains the relationship between

Online Behavioural Tracking This information leaflet aims to highlight to organisations what they should consider before deployment of online tracking on their websites. It explains the relationship between

Draft Operational Statement ED 0152: The Commissioner of Inland Revenue's Search Powers

24 June 2013 Team Manager, Technical Services Office of the Chief Tax Counsel National Office Inland Revenue PO Box 2198 WELLINGTON Draft Operational Statement ED 0152: The Commissioner of Inland Revenue's

24 June 2013 Team Manager, Technical Services Office of the Chief Tax Counsel National Office Inland Revenue PO Box 2198 WELLINGTON Draft Operational Statement ED 0152: The Commissioner of Inland Revenue's

Requests where the cost of compliance with a request exceeds the appropriate

ICO lo Requests where the cost of compliance with a request exceeds the appropriate Freedom of Information Act Contents Overview... 2 What FOIA says about section 12... 3 The appropriate... 4 Estimating

ICO lo Requests where the cost of compliance with a request exceeds the appropriate Freedom of Information Act Contents Overview... 2 What FOIA says about section 12... 3 The appropriate... 4 Estimating

Debt Managers Standards Association Limited (DEMSA) Code of Conduct (the Code)

Code of Conduct (the Code)") Debt Managers Standards Association Limited (DEMSA) Code of Conduct (the Code) CONTENTS 1. Introduction 2. Availability of the Code 3. Membership of DEMSA 4. Compliance with Statutory Regulations 5. Compliance

Debt Managers Standards Association Limited (DEMSA) Code of Conduct (the Code) CONTENTS 1. Introduction 2. Availability of the Code 3. Membership of DEMSA 4. Compliance with Statutory Regulations 5. Compliance

Hong Kong is increasingly seen as a necessary operations

1 TIMOTHY LOH Financial Services & Law Review Setting Up In Hong Kong: A Guide for the Finance Industry Hong Kong is increasingly seen as a necessary operations center for the financial industry. It is

1 TIMOTHY LOH Financial Services & Law Review Setting Up In Hong Kong: A Guide for the Finance Industry Hong Kong is increasingly seen as a necessary operations center for the financial industry. It is

Thursday, October 10, 2013 POTENTIAL BARRIERS TO HOSPITAL SUBSIDIES FOR HEALTH INSURANCE FOR THOSE IN NEED

Thursday, October 10, 2013 POTENTIAL BARRIERS TO HOSPITAL SUBSIDIES FOR HEALTH INSURANCE FOR THOSE IN NEED AT A GLANCE The Issue: A number of hospitals and health systems have inquired about whether it

Thursday, October 10, 2013 POTENTIAL BARRIERS TO HOSPITAL SUBSIDIES FOR HEALTH INSURANCE FOR THOSE IN NEED AT A GLANCE The Issue: A number of hospitals and health systems have inquired about whether it

DEPARTMENT OF HEALTH AND SOCIAL SECURITY

SOCIAL SECURITY COMMISSIONER S DECISION ISLE OF MAN COURTS OF JUSTICE DEEMSTERS WALK, BUCKS ROAD, DOUGLAS DEPARTMENT OF HEALTH AND SOCIAL SECURITY Appellant -v- MR. A Respondent At the Appeal hearing before

SOCIAL SECURITY COMMISSIONER S DECISION ISLE OF MAN COURTS OF JUSTICE DEEMSTERS WALK, BUCKS ROAD, DOUGLAS DEPARTMENT OF HEALTH AND SOCIAL SECURITY Appellant -v- MR. A Respondent At the Appeal hearing before

Annex I. SME Loan Guarantee Scheme for Accounts Receivable Loans: Questionnaire on Default Claim. For Application(s) : (please insert application no.

: (please insert application no.") 香 港 特 別 行 政 區 政 府 工 業 貿 易 署 Trade and Industry Department The Government of the Hong Kong Special Administrative Region Annex I SME Loan Guarantee Scheme for Accounts Receivable Loans: Questionnaire on

香 港 特 別 行 政 區 政 府 工 業 貿 易 署 Trade and Industry Department The Government of the Hong Kong Special Administrative Region Annex I SME Loan Guarantee Scheme for Accounts Receivable Loans: Questionnaire on

Legislative Council Panel on Housing. Refinancing of Home Ownership Scheme flats with premium unpaid

Legislative Council Panel on Housing Refinancing of Home Ownership Scheme flats with premium unpaid CB(1)1037/14-15(03) PURPOSE This paper briefs Members on matters relating to refinancing of Home Ownership

Legislative Council Panel on Housing Refinancing of Home Ownership Scheme flats with premium unpaid CB(1)1037/14-15(03) PURPOSE This paper briefs Members on matters relating to refinancing of Home Ownership

Land Acquisition (Just Terms Compensation) Act 1991 No 22

Act 1991 No 22") New South Wales Land Acquisition (Just Terms Compensation) Act 1991 No 22 Status information Currency of version Current version for 31 January 2011 to date (generated 21 February 2011 at 10:02). Legislation

New South Wales Land Acquisition (Just Terms Compensation) Act 1991 No 22 Status information Currency of version Current version for 31 January 2011 to date (generated 21 February 2011 at 10:02). Legislation

Consultation Paper on the Evidential Requirements under the Securities and Futures (Professional Investor) Rules. October 2010

Rules. October 2010") Consultation Paper on the Evidential Requirements under the Securities and Futures (Professional Investor) Rules October 2010 Table of Contents Foreword 1 Personal Information Collection Statement 2 Introduction

Consultation Paper on the Evidential Requirements under the Securities and Futures (Professional Investor) Rules October 2010 Table of Contents Foreword 1 Personal Information Collection Statement 2 Introduction

BELIZE LIMITED LIABILITY PARTNERSHIP ACT CHAPTER 258 REVISED EDITION 2003 SHOWING THE SUBSTANTIVE LAWS AS AT 31ST MAY, 2003

BELIZE LIMITED LIABILITY PARTNERSHIP ACT CHAPTER 258 REVISED EDITION 2003 SHOWING THE SUBSTANTIVE LAWS AS AT 31ST MAY, 2003 This is a revised edition of the Substantive Laws, prepared by the Law Revision

BELIZE LIMITED LIABILITY PARTNERSHIP ACT CHAPTER 258 REVISED EDITION 2003 SHOWING THE SUBSTANTIVE LAWS AS AT 31ST MAY, 2003 This is a revised edition of the Substantive Laws, prepared by the Law Revision

COMMENTARY. Hong Kong Strengthens Its Personal Data. on Direct Marketing JONES DAY

May 2013 JONES DAY COMMENTARY Hong Kong Strengthens Its Personal Data Privacy Laws and Imposes Criminal Penalties on Direct Marketing In 2012 Hong Kong introduced the Personal Data (Privacy) (Amendment)

May 2013 JONES DAY COMMENTARY Hong Kong Strengthens Its Personal Data Privacy Laws and Imposes Criminal Penalties on Direct Marketing In 2012 Hong Kong introduced the Personal Data (Privacy) (Amendment)

The Mortgage Brokerages and Mortgage Administrators Act

MORTGAGE BROKERAGES AND 1 The Mortgage Brokerages and Mortgage Administrators Act being Chapter M-20.1* of The Statutes of Saskatchewan, 2007 (effective October 1, 2010), as amended by the Statutes of

MORTGAGE BROKERAGES AND 1 The Mortgage Brokerages and Mortgage Administrators Act being Chapter M-20.1* of The Statutes of Saskatchewan, 2007 (effective October 1, 2010), as amended by the Statutes of

REGULATORY OVERVIEW THE REGULATORY AUTHORITIES IN HONG KONG REGARDING MONEY LENDING BUSINESS, AND THE RELEVANT LAWS AND REGULATIONS

THE REGULATORY AUTHORITIES IN HONG KONG REGARDING MONEY LENDING BUSINESS, AND THE RELEVANT LAWS AND REGULATIONS The Money Lenders Ordinance and the Money Lenders Regulations (the Relevant Statutes ) are

THE REGULATORY AUTHORITIES IN HONG KONG REGARDING MONEY LENDING BUSINESS, AND THE RELEVANT LAWS AND REGULATIONS The Money Lenders Ordinance and the Money Lenders Regulations (the Relevant Statutes ) are

SECURITIES AND FUTURES (INVESTOR COMPENSATION CLAIMS) RULES

RULES") L. S. NO. 2 TO GAZETTE NO. 50/2002 L.N. 215 of 2002 B1735 L.N. 215 of 2002 SECURITIES AND FUTURES (INVESTOR COMPENSATION CLAIMS) RULES CONTENTS Section Page PART 1 PRELIMINARY 1. Commencement... B1737

L. S. NO. 2 TO GAZETTE NO. 50/2002 L.N. 215 of 2002 B1735 L.N. 215 of 2002 SECURITIES AND FUTURES (INVESTOR COMPENSATION CLAIMS) RULES CONTENTS Section Page PART 1 PRELIMINARY 1. Commencement... B1737

Sample Letters. Sample Letters And Optional Paragraphs

Sample Letters Disclaimer The following sample letters are to be used as a guide or example, and must be adjusted to suit your client's needs. Lawyers Mutual Insurance Company of Kentucky hereby disclaims

Sample Letters Disclaimer The following sample letters are to be used as a guide or example, and must be adjusted to suit your client's needs. Lawyers Mutual Insurance Company of Kentucky hereby disclaims

OUT-OF-COURT RESTRUCTURING GUIDELINES FOR MAURITIUS

These Guidelines have been issued by the Insolvency Service and endorsed by the Bank of Mauritius. OUT-OF-COURT RESTRUCTURING GUIDELINES FOR MAURITIUS 1. INTRODUCTION It is a generally accepted global

These Guidelines have been issued by the Insolvency Service and endorsed by the Bank of Mauritius. OUT-OF-COURT RESTRUCTURING GUIDELINES FOR MAURITIUS 1. INTRODUCTION It is a generally accepted global

Yes No. If the answer is yes, please provide the following information:

香 港 特 別 行 政 區 政 府 工 業 貿 易 署 Trade and Industry Department The Government of the Hong Kong Special Administrative Region Annex I SME Loan Guarantee Scheme for Business Installations and Equipment Loans:

香 港 特 別 行 政 區 政 府 工 業 貿 易 署 Trade and Industry Department The Government of the Hong Kong Special Administrative Region Annex I SME Loan Guarantee Scheme for Business Installations and Equipment Loans:

CHAIRMAN ANDREW BARTLETT QC. and LAY MEMBERS PAUL TAYLOR IVAN WILSON. and

Information Tribunal Appeal Number: EA/2008/0092 Information Commissioner s Ref: FS50126264 Determined on documents only Decision Promulgated 17 July 2009 BEFORE CHAIRMAN ANDREW BARTLETT QC and LAY MEMBERS

Information Tribunal Appeal Number: EA/2008/0092 Information Commissioner s Ref: FS50126264 Determined on documents only Decision Promulgated 17 July 2009 BEFORE CHAIRMAN ANDREW BARTLETT QC and LAY MEMBERS

Report Published under Section 48(1) of the Personal Data (Privacy) Ordinance (Cap. 486) Report Number: R11-3803

of the Personal Data (Privacy) Ordinance (Cap. 486) Report Number: R11-3803") Report Published under Section 48(1) of the Personal Data (Privacy) Ordinance (Cap. 486) Report Number: R11-3803 Date issued: 15 March 2011 This page is intentionally left blank to facilitate double-side

Report Published under Section 48(1) of the Personal Data (Privacy) Ordinance (Cap. 486) Report Number: R11-3803 Date issued: 15 March 2011 This page is intentionally left blank to facilitate double-side

Project on Standardization of Mortgage Origination Documents in Hong Kong (the Project )

") Project on Standardization of Mortgage Origination Documents in Hong Kong (the Project ) Guidance Notes to the Recommended Core Provisions for Mortgage Loan Application Form 1. The Steering Committee of

Project on Standardization of Mortgage Origination Documents in Hong Kong (the Project ) Guidance Notes to the Recommended Core Provisions for Mortgage Loan Application Form 1. The Steering Committee of

Banking & Finance - Bulletin 60 December 2008

Banking & Finance - Bulletin 60 December 2008 In this issue: Breaking a Fixed Rate Loan our approach to break costs Direct Debits on Transaction Accounts Maladministration and Secured Lending Dealing with

Banking & Finance - Bulletin 60 December 2008 In this issue: Breaking a Fixed Rate Loan our approach to break costs Direct Debits on Transaction Accounts Maladministration and Secured Lending Dealing with

Cases referred to: ZAMBIA PRIVATISATION AGENCY v JAMES MATALE (1996) S.J.

S.J.") ZAMBIA PRIVATISATION AGENCY v JAMES MATALE (1996) S.J. SUPREME COURT E.L SAKALA, ACTING DEPUTY CHIEF JUSTICE, CHAILA AND CHIRWA, JJ.S. 1ST FEBRUARY AND 15 MARCH, 1996. Flynote Labour law - Employment -

ZAMBIA PRIVATISATION AGENCY v JAMES MATALE (1996) S.J. SUPREME COURT E.L SAKALA, ACTING DEPUTY CHIEF JUSTICE, CHAILA AND CHIRWA, JJ.S. 1ST FEBRUARY AND 15 MARCH, 1996. Flynote Labour law - Employment -

Supervisory Policy Manual

This module should be read in conjunction with the Introduction and with the Glossary, which contains an explanation of abbreviations and other terms used in this Manual. If reading on-line, click on blue

This module should be read in conjunction with the Introduction and with the Glossary, which contains an explanation of abbreviations and other terms used in this Manual. If reading on-line, click on blue

BELIZE LIMITED LIABILITY PARTNERSHIP ACT CHAPTER 258 REVISED EDITION 2000 SHOWING THE LAW AS AT 31ST DECEMBER, 2000

BELIZE LIMITED LIABILITY PARTNERSHIP ACT CHAPTER 258 REVISED EDITION 2000 SHOWING THE LAW AS AT 31ST DECEMBER, 2000 This is a revised edition of the law, prepared by the Law Revision Commissioner under

BELIZE LIMITED LIABILITY PARTNERSHIP ACT CHAPTER 258 REVISED EDITION 2000 SHOWING THE LAW AS AT 31ST DECEMBER, 2000 This is a revised edition of the law, prepared by the Law Revision Commissioner under

Order F15-55 MINISTRY OF JUSTICE. Celia Francis, Adjudicator. September 30, 2015

Order F15-55 MINISTRY OF JUSTICE Celia Francis, Adjudicator September 30, 2015 CanLII Cite: 2015 BCIPC 58 Quicklaw Cite: [2015] B.C.I.P.C.D. No. 58 Summary: The applicant requested a copy of the report

Order F15-55 MINISTRY OF JUSTICE Celia Francis, Adjudicator September 30, 2015 CanLII Cite: 2015 BCIPC 58 Quicklaw Cite: [2015] B.C.I.P.C.D. No. 58 Summary: The applicant requested a copy of the report

Insolvency and. Business Recovery. Procedures. A Brief Guide. Compiled by Compass Financial Recovery and Insolvency Ltd

Insolvency and Business Recovery Procedures A Brief Guide Compiled by Compass Financial Recovery and Insolvency Ltd I What is Insolvency? Insolvency is legally defined as: A company is insolvent (unable

Insolvency and Business Recovery Procedures A Brief Guide Compiled by Compass Financial Recovery and Insolvency Ltd I What is Insolvency? Insolvency is legally defined as: A company is insolvent (unable

Audit issues when financial market conditions are difficult and credit facilities may be restricted

Bulletin 2008/01 Audit issues when financial market conditions are difficult and credit facilities may be restricted THE AUDITING PRACTICES BOARD The Auditing Practices Board Limited, which is part of

Bulletin 2008/01 Audit issues when financial market conditions are difficult and credit facilities may be restricted THE AUDITING PRACTICES BOARD The Auditing Practices Board Limited, which is part of

Supervisory Policy Manual

This module should be read in conjunction with the Introduction and with the Glossary, which contains an explanation of abbreviations and other terms used in this Manual. If reading on-line, click on blue

This module should be read in conjunction with the Introduction and with the Glossary, which contains an explanation of abbreviations and other terms used in this Manual. If reading on-line, click on blue

THE LAND REGISTRY E-ALERT SERVICE - APPLICATION FOR CHANGE OF PARTICULARS

THE LAND REGISTRY E-ALERT SERVICE - APPLICATION FOR CHANGE OF PARTICULARS Part A Particulars of Subscriber s Account Account No. - - EAL Account Name Verification Code [Note (i)] *HKID Card No./Company

THE LAND REGISTRY E-ALERT SERVICE - APPLICATION FOR CHANGE OF PARTICULARS Part A Particulars of Subscriber s Account Account No. - - EAL Account Name Verification Code [Note (i)] *HKID Card No./Company

Guidance for Data Users on the Collection and Use of Personal Data through the Internet 1

Guidance for Data Users on the Collection and Use of Personal Data through the Internet Introduction Operating online businesses or services, whether by commercial enterprises, non-government organisations

Guidance for Data Users on the Collection and Use of Personal Data through the Internet Introduction Operating online businesses or services, whether by commercial enterprises, non-government organisations

mayor during city council meetings and study sessions since ( and including) May 3." Mr. Wade

May 3. Mr. Wade") y. ; 1 OFFICE OF THE ATTORNEY GENERAL STATE OF ILLINOIS Lisa Madigan ATTORNEY GENERAL Public Access Opinion No. 11-006 Request for Review 2011 PAC 15916) FREEDOM OF INFORMATION ACT: Public Records -- Electronic

y. ; 1 OFFICE OF THE ATTORNEY GENERAL STATE OF ILLINOIS Lisa Madigan ATTORNEY GENERAL Public Access Opinion No. 11-006 Request for Review 2011 PAC 15916) FREEDOM OF INFORMATION ACT: Public Records -- Electronic

Department of Justice Revises Policies Regarding Waiver of Privilege. Gabriel L. Imperato, Esq.*

Department of Justice Revises Policies Regarding Waiver of Privilege Gabriel L. Imperato, Esq.* The Department of Justice recently modified its Principles for Federal Prosecution of Business Organizations,

Department of Justice Revises Policies Regarding Waiver of Privilege Gabriel L. Imperato, Esq.* The Department of Justice recently modified its Principles for Federal Prosecution of Business Organizations,

LEVEL 3 - UNIT 15 - THE PRACTICE OF LAW FOR THE ELDERLY CLIENT SUGGESTED ANSWERS JANUARY 2011

LEVEL 3 - UNIT 15 - THE PRACTICE OF LAW FOR THE ELDERLY CLIENT SUGGESTED ANSWERS JANUARY 2011 Note to Candidates and Tutors: The purpose of the suggested answers is to provide students and tutors with

LEVEL 3 - UNIT 15 - THE PRACTICE OF LAW FOR THE ELDERLY CLIENT SUGGESTED ANSWERS JANUARY 2011 Note to Candidates and Tutors: The purpose of the suggested answers is to provide students and tutors with

Electronic Health Record Sharing System Bill. Contents. Part 1. Preliminary. 1. Short title and commencement... C1203. 2. Interpretation...

C1193 Electronic Health Record Sharing System Bill Contents Clause Page Part 1 Preliminary 1. Short title and commencement... C1203 2. Interpretation... C1203 3. Substitute decision maker... C1213 4. Ordinance

C1193 Electronic Health Record Sharing System Bill Contents Clause Page Part 1 Preliminary 1. Short title and commencement... C1203 2. Interpretation... C1203 3. Substitute decision maker... C1213 4. Ordinance

Freedom of information guidance Exemptions guidance Section 41 Information provided in confidence

Freedom of information guidance Exemptions guidance Section 41 Information provided in confidence 14 May 2008 Contents Introduction 2 What information may be covered by this exemption? 3 Was the information

Freedom of information guidance Exemptions guidance Section 41 Information provided in confidence 14 May 2008 Contents Introduction 2 What information may be covered by this exemption? 3 Was the information

STATUTORY INSTRUMENTS. S.I. No. 336 of 2011

STATUTORY INSTRUMENTS. S.I. No. 336 of 2011 EUROPEAN COMMUNITIES (ELECTRONIC COMMUNICATIONS NETWORKS AND SERVICES) (PRIVACY AND ELECTRONIC COMMUNICATIONS) REGULATIONS 2011 (Prn. A11/1165) 2 [336] S.I.

STATUTORY INSTRUMENTS. S.I. No. 336 of 2011 EUROPEAN COMMUNITIES (ELECTRONIC COMMUNICATIONS NETWORKS AND SERVICES) (PRIVACY AND ELECTRONIC COMMUNICATIONS) REGULATIONS 2011 (Prn. A11/1165) 2 [336] S.I.

SME Loan Guarantee Scheme for Business Installations and Equipment Loans / Associated Working Capital Loans: Questionnaire on Default Claim

香 港 特 別 行 政 區 政 府 工 業 貿 易 署 Trade and Industry Department The Government of the Hong Kong Special Administrative Region Annex I SME Loan Guarantee Scheme for Business Installations and Equipment Loans

香 港 特 別 行 政 區 政 府 工 業 貿 易 署 Trade and Industry Department The Government of the Hong Kong Special Administrative Region Annex I SME Loan Guarantee Scheme for Business Installations and Equipment Loans

SUBJECT ACCESS REQUEST

DATA PROTECTION ACT 1998 SUBJECT ACCESS REQUEST Procedure Manual 1 Invest NI Subject Access Request Procedure Manual 1. Introduction 1.1 What is a Subject Access Request? 1.2 Routine Requests 1.3 What

DATA PROTECTION ACT 1998 SUBJECT ACCESS REQUEST Procedure Manual 1 Invest NI Subject Access Request Procedure Manual 1. Introduction 1.1 What is a Subject Access Request? 1.2 Routine Requests 1.3 What

The Limited Partnership Bill, 2010 THE LIMITED LIABILITY PARTNERSHIP BILL 2010 ARRANGEMENT OF CLAUSES PART I PRELIMINARY. Clause

THE LIMITED LIABILITY PARTNERSHIP BILL 2010 ARRANGEMENT OF CLAUSES 1 Short title and commencement. 2 Interpretation. PART I PRELIMINARY Clause PART II REGISTRAR AND REGISTRAR OF LIMITED LIABILITY PARTNERSHIPS

THE LIMITED LIABILITY PARTNERSHIP BILL 2010 ARRANGEMENT OF CLAUSES 1 Short title and commencement. 2 Interpretation. PART I PRELIMINARY Clause PART II REGISTRAR AND REGISTRAR OF LIMITED LIABILITY PARTNERSHIPS

ORDER MO-3277. Appeal MA14-573. Town of the Blue Mountains. January 8, 2016

ORDER MO-3277 Appeal MA14-573 Town of the Blue Mountains January 8, 2016 Summary: The Town of Blue Mountains (the town) received a request under the Municipal Freedom of Information and Protection of Privacy

ORDER MO-3277 Appeal MA14-573 Town of the Blue Mountains January 8, 2016 Summary: The Town of Blue Mountains (the town) received a request under the Municipal Freedom of Information and Protection of Privacy

The Finance Commission of Texas adopts new rule 7 TAC 5.1, concerning required disclosures in connection with certain home loans.

Title 7. Banking and Securities Part I. Finance Commission of Texas Chapter 5. Home Loans 7 TAC 5.1. Required Disclosures in Connection with Certain Home Loans The Finance Commission of Texas adopts new

Title 7. Banking and Securities Part I. Finance Commission of Texas Chapter 5. Home Loans 7 TAC 5.1. Required Disclosures in Connection with Certain Home Loans The Finance Commission of Texas adopts new

Press release. LCQ13: Regulation of mortgage loan business of finance companies and mortgage intermediaries. Wednesday, March 25, 2015

Press release LCQ13: Regulation of mortgage loan business of finance companies and mortgage intermediaries Wednesday, March 25, 2015 Following is a question by the Hon Paul Tse and a written reply by the

Press release LCQ13: Regulation of mortgage loan business of finance companies and mortgage intermediaries Wednesday, March 25, 2015 Following is a question by the Hon Paul Tse and a written reply by the

Chapter 14:14 MONEYLENDING AND RATES OF INTEREST ACT. Acts 9/1930, 25/1948,59/1961,6/1967, 7/1972, 5/1981, 30/1984, 22/2001; 16/2004. R.G.N. 554/1962.

Section Chapter 14:14 MONEYLENDING AND RATES OF INTEREST ACT Acts 9/1930, 25/1948,59/1961,6/1967, 7/1972, 5/1981, 30/1984, 22/2001; 16/2004. R.G.N. 554/1962. ARRANGEMENT OF SECTIONS 1. Short title. 2.

Section Chapter 14:14 MONEYLENDING AND RATES OF INTEREST ACT Acts 9/1930, 25/1948,59/1961,6/1967, 7/1972, 5/1981, 30/1984, 22/2001; 16/2004. R.G.N. 554/1962. ARRANGEMENT OF SECTIONS 1. Short title. 2.

National Consumer Credit Protection Amendment (Credit Reform Phase 2) Bill 2012

Bill 2012") Mr Christian Mikula Manager, Disclosure and International Unit Retail Investor Division The Treasury Langton Crescent PARKES ACT 2600 By email: creditphase2bill@treasury.gov.au 1 March 2013 National Consumer

Mr Christian Mikula Manager, Disclosure and International Unit Retail Investor Division The Treasury Langton Crescent PARKES ACT 2600 By email: creditphase2bill@treasury.gov.au 1 March 2013 National Consumer

The Debt Arrangement Scheme Improving Access

Consultation by the Scottish Government Submission from the Association of British Credit Unions Limited (ABCUL) Details Name Frank McKillop Job Title Policy Officer (Scotland) Organisation Association

Consultation by the Scottish Government Submission from the Association of British Credit Unions Limited (ABCUL) Details Name Frank McKillop Job Title Policy Officer (Scotland) Organisation Association

IN THE MATTER OF THE HOMEOWNER PROTECTION ACT, S.B.C. 1998, C.31. AND IN THE MATTER OF an appeal to the BRITISH COLUMBIA SAFETY STANDARDS APPEAL BOARD

Indexed as: BCSSAB 10 (1) 2013 Date Issued: February 19, 2014 Appeal No. SSAB 10-2013 IN THE MATTER OF THE HOMEOWNER PROTECTION ACT, S.B.C. 1998, C.31 AND IN THE MATTER OF an appeal to the BRITISH COLUMBIA

Indexed as: BCSSAB 10 (1) 2013 Date Issued: February 19, 2014 Appeal No. SSAB 10-2013 IN THE MATTER OF THE HOMEOWNER PROTECTION ACT, S.B.C. 1998, C.31 AND IN THE MATTER OF an appeal to the BRITISH COLUMBIA

The Credit Reporting Act

1 CREDIT REPORTING c. C-43.2 The Credit Reporting Act being Chapter C-43.2 of The Statutes of Saskatchewan, 2004 (effective March 1, 2005). NOTE: This consolidation is not official. Amendments have been

1 CREDIT REPORTING c. C-43.2 The Credit Reporting Act being Chapter C-43.2 of The Statutes of Saskatchewan, 2004 (effective March 1, 2005). NOTE: This consolidation is not official. Amendments have been

Practice note on credit risk management for loans to the corporate sector

Banking Supervision Department 銀 行 監 理 部 Our Ref.: B10/1C 27 March 2015 The Chief Executive All Authorized Institutions Dear Sir/Madam, Practice note on credit risk management for loans to the corporate

Banking Supervision Department 銀 行 監 理 部 Our Ref.: B10/1C 27 March 2015 The Chief Executive All Authorized Institutions Dear Sir/Madam, Practice note on credit risk management for loans to the corporate

This is an appeal against an assessment for income tax raised in respect of a

REPORTABLE IN THE TAX COURT CAPE TOWN Case No. 11986 Appellant and THE COMMISSIONER FOR THE SOUTH AFRICAN REVENUE SERVICE Respondent JUDGMENT: 11 DECEMBER 2006 DAVIS P Introduction: This is an appeal against

REPORTABLE IN THE TAX COURT CAPE TOWN Case No. 11986 Appellant and THE COMMISSIONER FOR THE SOUTH AFRICAN REVENUE SERVICE Respondent JUDGMENT: 11 DECEMBER 2006 DAVIS P Introduction: This is an appeal against

Consumer Credit sourcebook. Chapter 8. Debt advice

Consumer Credit sourcebook Chapter Debt advice CONC : Debt advice Section.1 : Application.1 Application.1.1 This chapter applies, unless otherwise stated in or in relation to a rule to every firm with

Consumer Credit sourcebook Chapter Debt advice CONC : Debt advice Section.1 : Application.1 Application.1.1 This chapter applies, unless otherwise stated in or in relation to a rule to every firm with

Guidelines for Application for Accreditation by the Communications Authority as Local Certification Bodies

OFCA I 425(14) Issue 5 Guidelines for Application for Accreditation by the Communications Authority as Local Certification Bodies Introduction Under section 32E(g) of the Telecommunications Ordinance (Cap.

OFCA I 425(14) Issue 5 Guidelines for Application for Accreditation by the Communications Authority as Local Certification Bodies Introduction Under section 32E(g) of the Telecommunications Ordinance (Cap.

BBA submission on the HM Treasury (HMT) Consultation Competition in banking: improving access to SME credit data

Consultation Competition in banking: improving access to SME credit data") BBA submission on the HM Treasury (HMT) Consultation Competition in banking: improving access to SME credit data The British Bankers Association (BBA) is the leading association for the United Kingdom

BBA submission on the HM Treasury (HMT) Consultation Competition in banking: improving access to SME credit data The British Bankers Association (BBA) is the leading association for the United Kingdom

Chapter: 32 COMPANIES ORDINANCE Gazette Number Version Date. Long title 30/06/1997. To consolidate and amend the law relating to companies.

Chapter: 32 COMPANIES ORDINANCE Gazette Number Version Date Long title 30/06/1997 To consolidate and amend the law relating to companies. [1 July 1933] (Originally 39 of 1932 (Cap 32, 1950)) Section: 1

Chapter: 32 COMPANIES ORDINANCE Gazette Number Version Date Long title 30/06/1997 To consolidate and amend the law relating to companies. [1 July 1933] (Originally 39 of 1932 (Cap 32, 1950)) Section: 1

Consolidated Financial Statements

HKFRS 10 Revised October 2014January 2015 Effective for annual periods beginning on or after 1 January 2013 Hong Kong Financial Reporting Standard 10 Consolidated Financial Statements COPYRIGHT Copyright

HKFRS 10 Revised October 2014January 2015 Effective for annual periods beginning on or after 1 January 2013 Hong Kong Financial Reporting Standard 10 Consolidated Financial Statements COPYRIGHT Copyright

BE IT ENACTED by the Queen s Most Excellent Majesty, by

At a Tynwald held in Douglas, Isle of Man, the 21st day of October in the fifty-seventh year of the reign of our Sovereign Lady ELIZABETH THE SECOND by the Grace of God of the United Kingdom of Great Britain

At a Tynwald held in Douglas, Isle of Man, the 21st day of October in the fifty-seventh year of the reign of our Sovereign Lady ELIZABETH THE SECOND by the Grace of God of the United Kingdom of Great Britain

Personal data privacy protection: what mobile apps developers and their clients should know

Personal data privacy protection: what mobile Introduction This technical information leaflet aims to highlight the privacy implications that mobile applications ( mobile apps ) developers (including organisations

Personal data privacy protection: what mobile Introduction This technical information leaflet aims to highlight the privacy implications that mobile applications ( mobile apps ) developers (including organisations

2015 No. 0000 FINANCIAL SERVICES AND MARKETS. The Small and Medium Sized Businesses (Credit Information) Regulations 2015

Regulations 2015") Draft Regulations to illustrate the Treasury s current intention as to the exercise of powers under clause 4 of the the Small Business, Enterprise and Employment Bill. D R A F T S T A T U T O R Y I N S

Draft Regulations to illustrate the Treasury s current intention as to the exercise of powers under clause 4 of the the Small Business, Enterprise and Employment Bill. D R A F T S T A T U T O R Y I N S

2015 No. 0000 FINANCIAL SERVICES AND MARKETS. The Small and Medium Sized Business (Finance Platforms) Regulations 2015

Regulations 2015") Draft Regulations to illustrate the Treasury s current intention as to the exercise of powers under clause 5 of the Small Business, Enterprise and Employment Bill. D R A F T S T A T U T O R Y I N S T R

Draft Regulations to illustrate the Treasury s current intention as to the exercise of powers under clause 5 of the Small Business, Enterprise and Employment Bill. D R A F T S T A T U T O R Y I N S T R

THE LAW REFORM COMMISSION OF WESTERN AUSTRALIA

THE LAW REFORM COMMISSION OF WESTERN AUSTRALIA Project No 45 Mortgage Brokers REPORT SEPTEMBER 1974 The Law Reform Commission of Western Australia was established by the Law Reform Commission Act 1972.

THE LAW REFORM COMMISSION OF WESTERN AUSTRALIA Project No 45 Mortgage Brokers REPORT SEPTEMBER 1974 The Law Reform Commission of Western Australia was established by the Law Reform Commission Act 1972.

Clearing and Settlement Systems Bill

Summary of and Hong Kong Society of Accountants ( HKSA ) in letter dated 6 February 2004 as discussed at Meeting with the Administration on 4 March 2004 Purpose HKSA agrees that the should preserve the

Summary of and Hong Kong Society of Accountants ( HKSA ) in letter dated 6 February 2004 as discussed at Meeting with the Administration on 4 March 2004 Purpose HKSA agrees that the should preserve the

Legislative Council Panel on Financial Affairs. Matters Related to the Charging of Fees and Advertising Practices of Financial Intermediaries

CB(1)955/14-15(02) For Information Legislative Council Panel on Financial Affairs Matters Related to the Charging of Fees and Advertising Practices of Financial Intermediaries This information note sets

CB(1)955/14-15(02) For Information Legislative Council Panel on Financial Affairs Matters Related to the Charging of Fees and Advertising Practices of Financial Intermediaries This information note sets

BEREC Monitoring quality of Internet access services in the context of Net Neutrality

BEREC Monitoring quality of Internet access services in the context of Net Neutrality BEUC statement Contact: Guillermo Beltrà - digital@beuc.eu Ref.: BEUC-X-2014-029 28/04/2014 BUREAU EUROPÉEN DES UNIONS

BEREC Monitoring quality of Internet access services in the context of Net Neutrality BEUC statement Contact: Guillermo Beltrà - digital@beuc.eu Ref.: BEUC-X-2014-029 28/04/2014 BUREAU EUROPÉEN DES UNIONS

INLAND REVENUE BOARD OF REVIEW DECISIONS. Case No. D51/04

Case No. D51/04 Property tax section 42(1) of the Inland Revenue Ordinance whether a global deduction of interest payable against the total taxable property income. Panel: Anna Chow Suk Han (chairman),

Case No. D51/04 Property tax section 42(1) of the Inland Revenue Ordinance whether a global deduction of interest payable against the total taxable property income. Panel: Anna Chow Suk Han (chairman),

Queensland WHISTLEBLOWERS PROTECTION ACT 1994

Queensland WHISTLEBLOWERS PROTECTION ACT 1994 Act No. 68 of 1994 Queensland WHISTLEBLOWERS PROTECTION ACT 1994 Section PART 1 PRELIMINARY TABLE OF PROVISIONS Division 1 Title and commencement Page 1 Short

Queensland WHISTLEBLOWERS PROTECTION ACT 1994 Act No. 68 of 1994 Queensland WHISTLEBLOWERS PROTECTION ACT 1994 Section PART 1 PRELIMINARY TABLE OF PROVISIONS Division 1 Title and commencement Page 1 Short

Sixth Statutory Managers Report

Sixth Statutory Managers Report Aorangi Securities Limited 4 March 2011 Sixth Statutory Managers Report for Aorangi Securities Limited March 2011 2 Introduction History On 20 June 2010, Richard Grant Simpson

Sixth Statutory Managers Report Aorangi Securities Limited 4 March 2011 Sixth Statutory Managers Report for Aorangi Securities Limited March 2011 2 Introduction History On 20 June 2010, Richard Grant Simpson

ORDER MO-2114 Appeal MA-060192-1 York Regional Police Services Board

ORDER MO-2114 Appeal MA-060192-1 York Regional Police Services Board Tribunal Services Department Services de tribunal administratif 2 Bloor Street East 2, rue Bloor Est Suite 1400 Bureau 1400 Toronto,

ORDER MO-2114 Appeal MA-060192-1 York Regional Police Services Board Tribunal Services Department Services de tribunal administratif 2 Bloor Street East 2, rue Bloor Est Suite 1400 Bureau 1400 Toronto,