HOUSEHOLD DEBT AND CREDIT

|

|

|

- Andra Moore

- 8 years ago

- Views:

Transcription

1 QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES

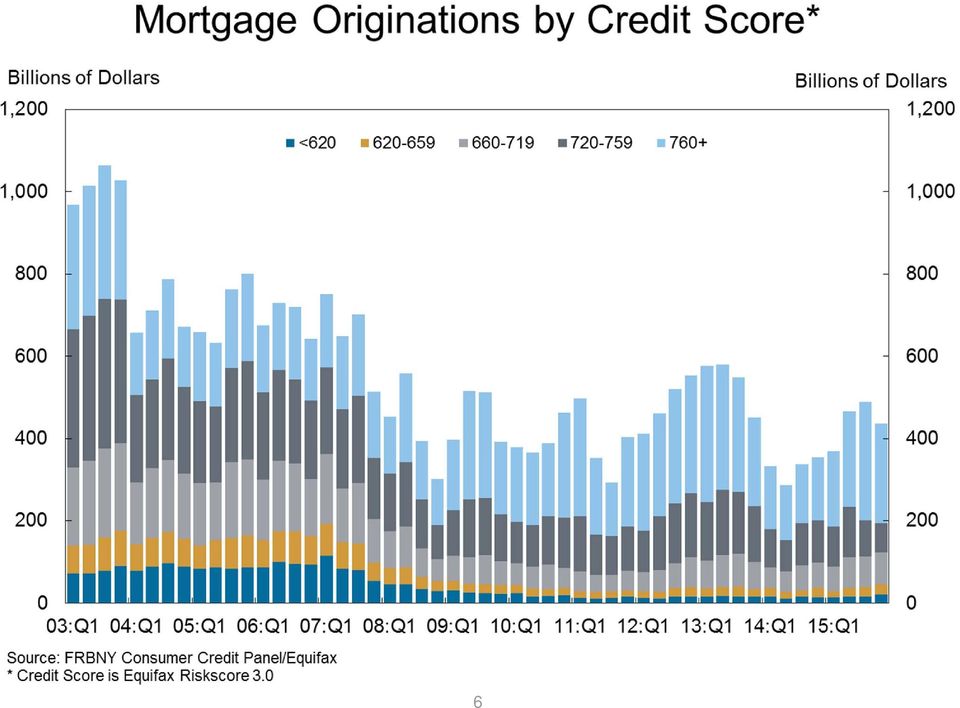

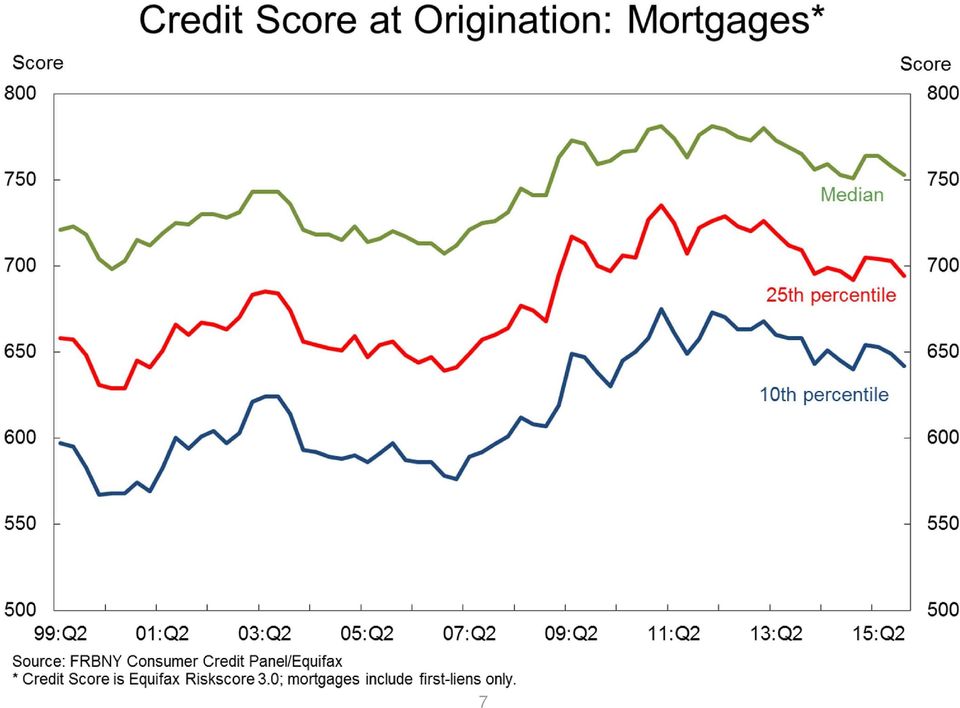

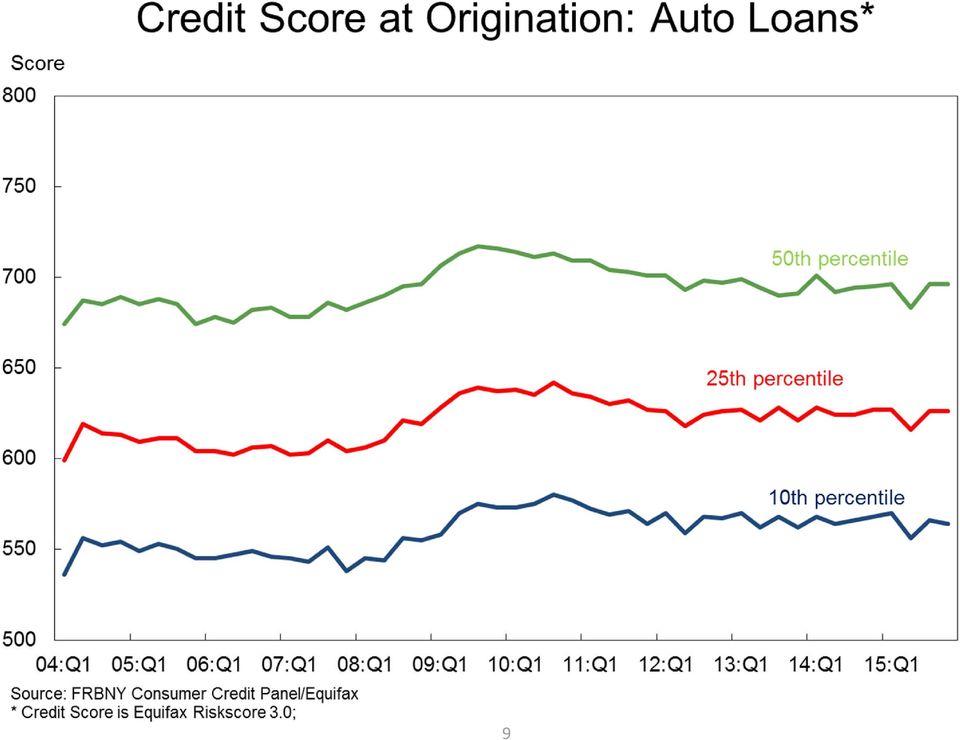

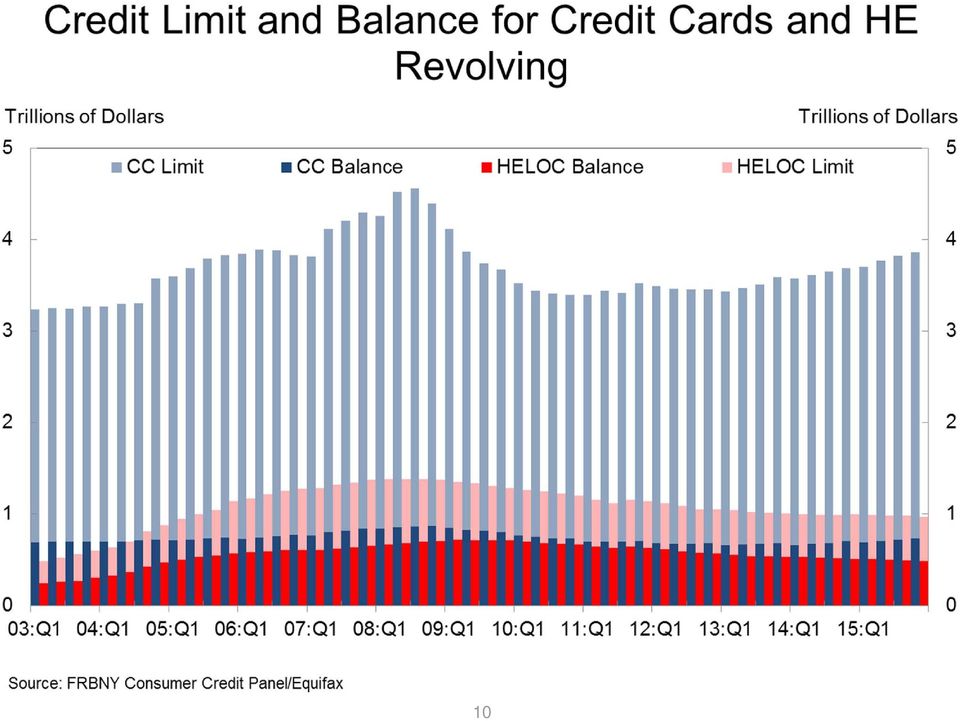

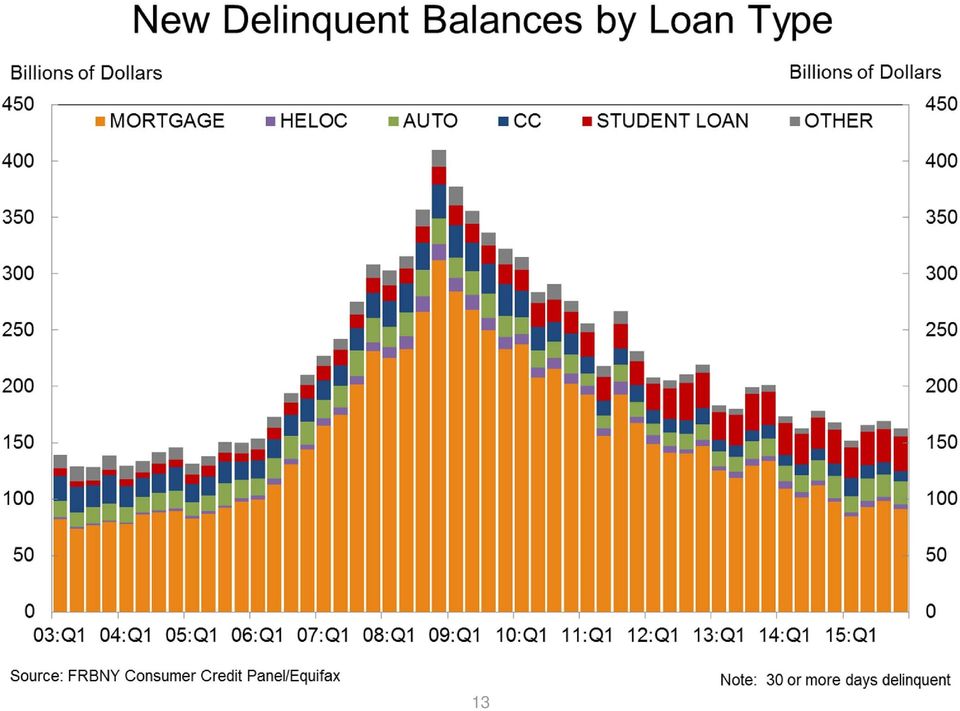

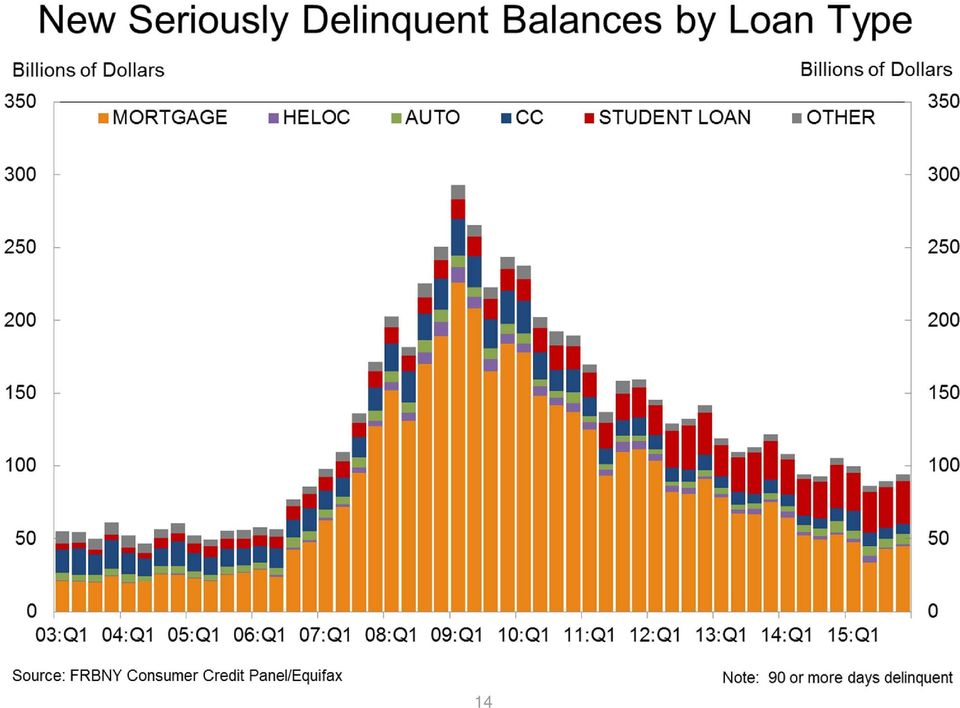

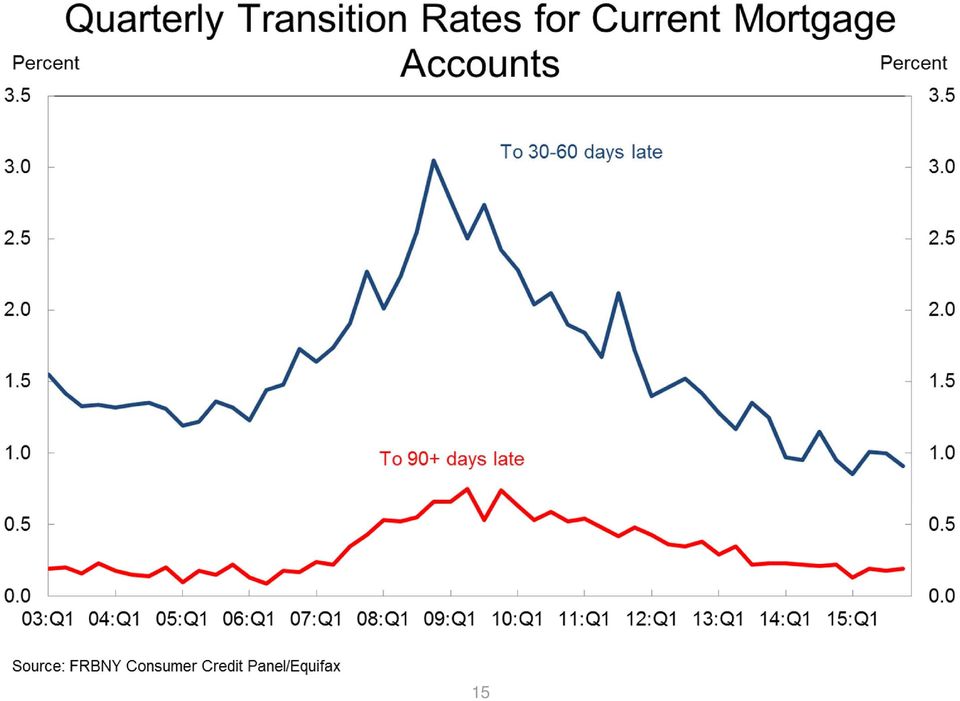

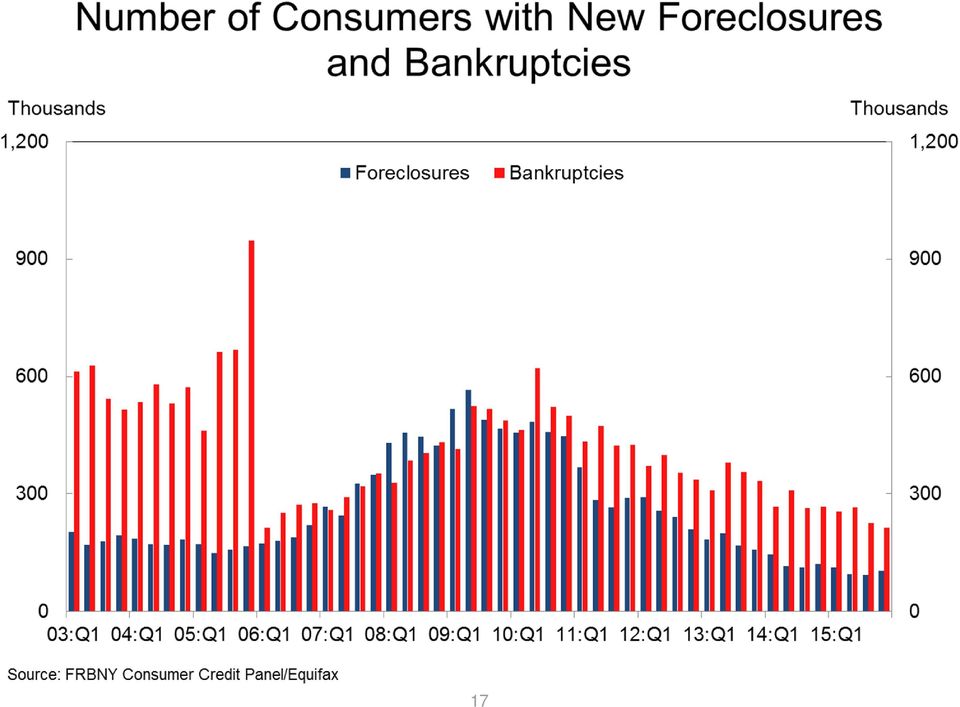

2 Household Debt and Credit Developments in 2015Q4 1 Aggregate household debt balances increased slightly in the fourth quarter of As of December 31, 2015, total household indebtedness was $12.12 trillion, a $51 billion (0.4%) increase from the third quarter of Overall household debt remains 4.4% below its 2008Q3 peak of $12.68 trillion. Mortgage balances, the largest component of household debt, were roughly flat in the fourth quarter. Mortgage balances shown on consumer credit reports stood at $8.25 trillion, an $11 billion drop from the third quarter of Balances on home equity lines of credit (HELOC) dropped by $5 billion, to $487 billion. Non-housing debt balances continued to increase in the fourth quarter, with a $19 billion increases each in auto loan and credit card balances respectively. Student loan balances increased by $29 billion. New originations continued at a moderately strong pace in the 4 th quarter. Mortgage originations, which we measure as appearances of new mortgage balances on consumer credit reports and which include refinanced mortgages, were at $437 billion, a slight decrease from the third quarter. Auto loan originations were $132 billion. The aggregate credit card limit increased for the 12 th consecutive quarter, and was up by 1% from the previous quarter. HELOC limits declined by 1%. The distribution of the credit scores of new mortgage borrowers changed slightly, although 56% of all new mortgage balances were to borrowers with credit scores above 780. Auto loan originations, though lower than last quarter, were robust across the board, with high levels of originations across the credit score distribution. Overall delinquency rates improved modestly in 2015Q4. As of December 31, 5.4% of outstanding debt was in some stage of delinquency. Of the $652 billion of debt that is delinquent, $442 billion is seriously delinquent (at least 90 days late or severely derogatory ). About 213,000 consumers had a bankruptcy notation added to their credit reports in 2015Q4, 20% fewer than in the same quarter last year. Housing Debt Mortgage originations declined slightly, to $437 billion. About 104,000 individuals had a new foreclosure notation added to their credit reports between October 1 and December 31, slightly higher than last quarter s 16-year low. Mortgage delinquencies continued the improving trend seen in the past 5 years. 2.2% of mortgage balances were 90 days delinquent during 2015Q4, compared to 2.3% in the previous quarter. Delinquency transition rates for current mortgage accounts were somewhat improved, with 1.1% of current balances transitioning to delinquency, while 17.7% of mortgage balances in early delinquency transitioned to 90+ days delinquent and 32.9% became current. Student Loans, Credit Cards, and Auto Loans Outstanding student loan balances increased by $29 billion, to $1.23 trillion as of December 31, % of aggregate student loan debt was 90+ days delinquent or in default in 2015Q4. 2 Auto loan balances reached $1.06 trillion, a $19 billion increase. 3.4% of auto loan balances are 90 or more days delinquent, unchanged since the third quarter. Credit card balances increased by $19 billion, to $733 billion. Credit Inquiries The number of credit inquiries within six months an indicator of consumer credit demand declined by 7 million from the previous quarter, to 175 million. 1 This report is based on the New York Fed Consumer Credit Panel, which is constructed from a nationally representative random sample drawn from Equifax credit report data. For details on the data set and the measures reported here, see the data dictionary available at the end of this report. Please contact Joelle Scally with questions. 2 As explained in a recent report, delinquency rates for student loans are likely to understate effective delinquency rates because about half of these loans are currently in deferment, in grace periods or in forbearance and therefore temporarily not in the repayment cycle. This implies that among loans in the repayment cycle delinquency rates are roughly twice as high.

dropped by $5 billion, to $487 billion.")

3 Page Left Blank Intentionally 1

4 NATIONAL CHARTS 2

5 3

6 4

7 5

8 6

9 7

10 8

11 9

12 10

13 11

14 12

15 13

16 14

17 15

18 16

19 17

20 18

21 CHARTS FOR SELECT STATES 19

22 20

23 21

24 22

25 23

26 24

27 25

28 26

29 27

30 28

31 Data Dictionary The FRBNY Consumer Credit Panel consists of detailed Equifax credit-report data for a unique longitudinal quarterly panel of individuals and households from 1999 to The panel is a nationally representative 5% random sample of all individuals with a social security number and a credit report (usually aged 19 and over). We also sampled all other individuals living at the same address as the primary sample members, allowing us to track household-level credit and debt for a random sample of US households. The resulting database includes approximately 44 million individuals in each quarter. More details regarding the sample design can be found in Lee and van der Klaauw (2010). 2 A comprehensive overview of the specific content of consumer credit reports is provided in Avery, Calem, Canner and Bostic (2003). 3 The credit report data in our panel primarily includes information on accounts that have been reported by the creditor within 3 months of the date that the credit records were drawn each quarter. Thus, accounts that are not currently reported on are excluded. Such accounts may be closed accounts with zero balances, dormant or inactive accounts with no balance, or accounts that when last reported had a positive balance. The latter accounts include accounts that were either subsequently sold, transferred, or paid off as well as accounts, particularly derogatory accounts, that are still outstanding but on which the lender has ceased reporting. According to Avery et al (2003), the latter group of noncurrently reporting accounts, with positive balances when last reported, accounted for approximately 8% of all credit accounts in their sample. For the vast majority of these accounts, and particularly for mortgage and installment loans, additional analysis suggested they had been closed (with zero balance) or transferred. 4 Our exclusion of the latter accounts is comparable to some stale account rules used by credit reporting companies, which treat noncurrently reporting revolving and nonrevolving accounts with positive balances as closed and with zero balance. All figures shown in the tables and graphs are based on the 5% random sample of individuals. To reduce processing costs, we drew a 2% random subsample of these individuals, meaning that the results presented here are for a 0.1% random sample of individuals with credit reports, or approximately 259,000 individuals as of Q In computing several of these statistics, account was taken of the joint or individual nature of various loan accounts. For example, to minimize biases due to double counting, in computing individual-level total balances, 50% of the balance associated with each joint account was attributed to that individual. Per-capita figures are computed by dividing totals for our sample by the total number of people in our sample, so these figures apply to the population of individuals who have a credit report. In comparing aggregate measures of household debt presented in this report to those included in the Board of Governor s Flow Of Funds (FoF) Accounts, there are several important considerations. First, among the different components included in the FoF household debt measure (which also includes debt of nonprofit organizations), our measures are directly comparable to two of its components: home mortgage debt and consumer credit. Total mortgage debt and non-mortgage debt in the third quarter of 2009 were respectively $9.7 and $2.6 trillion, while the comparable amounts in the FoF for the same quarter were 1 As of the Q report, the Quarterly Report will provide data and charts over a ten year period. Note that reported aggregates, especially in , may reflect some delays in the reporting of student loans by servicers to credit bureaus which could lead to some undercounting of student loan balances. Quarterly data prior to Q1 2003, excluding student loans, will remain available on the Household Credit webpage. 2 Lee, D. and W. van der Klaauw, An introduction to the FRBNY Consumer Credit Panel, [2010]. 3 Avery, R.B., P.S. Calem, G.B. Canner and R.W. Bostic, An Overview of Consumer Data and Credit Reporting, Federal Reserve Bulletin, Feb. 2003, pp Avery et al (2003) found that for many nonreported mortgage accounts a new mortgage account appeared around the time the account stopped being reported, suggesting a refinance or that the servicing was sold. Most revolving and open non-revolving accounts with a positive balance require monthly payments if they remain open, suggesting the accounts had been closed. Noncurrently reporting derogatory accounts can remain unchanged and not requiring updating for a long time when the borrower has stopped paying and the creditor may have stopped trying to collect on the account. Avery et al report that some of these accounts appeared to have been paid off. 5 Due to relatively low occurrence rates we used the full 5% sample for the computation of new foreclosure and bankruptcy rates. Additionally, to capture and account for servicer discrepancies, we used the 1% sample for student loan data. For all other graphs, we found the 0.1% sample to provide a very close representation of the 5% sample. 29

32 $10.3 and $2.5 trillion, respectively. 6 Second, a detailed accounting for the remaining differences between the debt measures from both data sources will require a more detailed breakdown and documentation of the computation of the FoF measures. 7 Loan types. In our analysis we distinguish between the following types of accounts: mortgage accounts, home equity revolving accounts, auto loans, bank card accounts, student loans and other loan accounts. Mortgage accounts include all mortgage installment loans, including first mortgages and home equity installment loans (HEL), both of which are closed-end loans. Home Equity Revolving accounts (aka Home Equity Line of Credit or HELOC), unlike home equity installment loans, are home equity loans with a revolving line of credit where the borrower can choose when and how often to borrow up to an updated credit limit. Auto Loans are loans taken out to purchase a car, including Auto Bank loans provided by banking institutions (banks, credit unions, savings and loan associations), and Auto Finance loans, provided by automobile dealers and automobile financing companies. Bankcard accounts (or credit card accounts) are revolving accounts for banks, bankcard companies, national credit card companies, credit unions and savings & loan associations. Student Loans include loans to finance educational expenses provided by banks, credit unions and other financial institutions as well as federal and state governments. The Other category includes Consumer Finance (sales financing, personal loans) and Retail (clothing, grocery, department stores, home furnishings, gas etc) loans. Our analysis excludes authorized user trades, disputed trades, lost/stolen trades, medical trades, child/family support trades, commercial trades and, as discussed above, inactive trades (accounts not reported on within the last 3 months). Total debt balance. Total balance across all accounts, excluding those in bankruptcy. Number of open, new and closed accounts. Total number of open accounts, number of accounts opened within the last 12 months. Number of closed accounts is defined as the difference between the number of open accounts 12 months ago plus the number of accounts opened within the last 12 months, minus the total number of open accounts at the current date. Inquiries. Number of credit-related consumer-initiated inquiries reported to the credit reporting agency in the past 6 months. Only hard pulls are included, which are voluntary inquiries generated when a consumer authorizes lenders to request a copy of their credit report. It excludes inquiries made by creditors about existing accounts (for example to determine whether they want to send the customer pre-approved credit applications or to verify the accuracy of customer-provided information) and inquiries made by consumers themselves. Note that inquiries are credit reporting company specific and not all inquiries associated with credit activities are reported to each credit reporting agency. Moreover, the reporting practices for the credit reporting companies may have changed during the period of analysis. High credit and balance for credit cards. Total amount of high credit on all credit cards held by the consumer. High credit is either the credit limit, or highest balance ever reported during history of this loan. As reported by Avery et al (2003) the use of the highest-balance measure for credit limits on accounts in which limits are not reported likely understates the actual credit limits available on those accounts. High credit and balance for HE Revolving. Same as for credit cards, but now applied to HELOCs. Credit utilization rates (for revolving accounts). Computed as proportion of available credit in use (outstanding balance divided by credit limit), and for reasons discussed above are likely to overestimate actual credit utilization. 6 Flow of Funds Accounts of the United States, Flows and Outstandings, Third Quarter 2009, Board of Governors, Table L Our debt totals exclude debt held by individuals without social security numbers. Additional information suggests that total debt held by such individuals is relatively small and accounts for little of the difference. 30

33 Delinquency status. Varies between current (paid as agreed), 30-day late (between 30 and 59 day late; not more than 2 payments past due), 60-day late (between 60 and 89 days late; not more than 3 payments past due), 90-day late (between 90 and 119 days late; not more than 4 payments past due), 120-day late (at least 120 days past due; 5 or more payments past due) or collections, and severely derogatory (any of the previous states combined with reports of a repossession, charge off to bad debt or foreclosure). Not all creditors provide updated information on payment status, especially after accounts have been derogatory for a longer period of time. Thus the payment performance profiles obtained from our data may to some extent reflect reporting practices of creditors. Percent of balance 90+ days late. Percent of balance that is either 90-day late, 120-day late or severely derogatory. 90+ days late is synonymous to seriously delinquent. New foreclosures. Number of individuals with foreclosures first appearing on their credit report during the past 3 months. Based on foreclosure information provided by lenders (account level foreclosure information) as well as through public records. Note that since borrowers may have multiple real estate loans, this measure is conceptually different from foreclosure rates often reported in the press. For example, a borrower with a mortgage currently in foreclosure would not be counted here if he receives a foreclosure notice on an additional mortgage account. In the case of joint mortgages, both borrowers reports indicate the presence of a foreclosure notice in the last 3 months, and both are counted here. New bankruptcies. New bankruptcies first reported during the past 3 months. Based on bankruptcy information provided by lenders (account level bankruptcy information) as well as through public records. Collections. Number and amount of 3 rd party collections (i.e. collections not being handled by original creditor) on file within the last 12 months. Includes both public record and account level 3 rd party collections information. As reported by Avery et al (2003), only a small proportion of collections are related to credit accounts with the majority of collection actions being associated with medical bills and utility bills. Consumer Credit Score. Credit score is the Equifax Risk Score 3.0. It was developed by Equifax and predicts the likelihood of a consumer becoming seriously delinquent (90+ days past due). The score ranges from , with a higher score being viewed as a better risk than someone with a lower score. New (seriously) delinquent balances and transition rates. New (seriously) delinquent balance reported in each loan category. For mortgages, this is based on the balance of each account at the time it enters (serious) delinquency, while for other loan types it is based on the net increase in the aggregate (seriously) delinquent balance for all accounts of that loan type belonging to an individual. Transition rates. The transition rate is the new (seriously) delinquent balance, expressed as a percent of the previous quarter s balance that was not (seriously) delinquent. Newly originated installment loan balances. We calculate the balance on newly originated mortgage loans as they first appear on an individual s credit report. For auto loans we compare the total balance and number of accounts on an individual credit report in consecutive quarters. New auto loan originations are then defined as increases in the balance accompanied by increases in the number of accounts reported. Cover photo credits clockwise from top right: Andrew Love/flickr.com, The Truth About /flickr.com, Casey Serin/flickr.com, Microsoft.com Federal Reserve Bank of New York. Equifax is a registered trademark of Equifax Inc. All rights reserved. 31

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 2015Q1 1 Aggregate household

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 2015Q1 1 Aggregate household

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 2014 Q2 1 Aggregate consumer

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 2014 Q2 1 Aggregate consumer

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 2015Q3 1 Aggregate household

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 2015Q3 1 Aggregate household

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 2013 Q3 1 Aggregate consumer

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 2013 Q3 1 Aggregate consumer

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 2016Q2 1 Aggregate household

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 2016Q2 1 Aggregate household

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 2014 Q4 1 Aggregate household

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 2014 Q4 1 Aggregate household

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 212 Q2 1 Aggregate consumer

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 212 Q2 1 Aggregate consumer

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT May 211 FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 211Q1 1 Aggregate consumer

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT May 211 FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 211Q1 1 Aggregate consumer

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 216Q1 1 Aggregate household

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 216Q1 1 Aggregate household

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT November 21 FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS MICROECONOMIC AND REGIONAL STUDIES Household Debt and Credit Developments in 21Q3 1 Aggregate

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT November 21 FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS MICROECONOMIC AND REGIONAL STUDIES Household Debt and Credit Developments in 21Q3 1 Aggregate

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 211Q3 1 Aggregate consumer debt

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 211Q3 1 Aggregate consumer debt

Federal Reserve Bank of New York Staff Reports

Federal Reserve Bank of New York Staff Reports An Introduction to the FRBNY Consumer Credit Panel Donghoon Lee Wilbert van der Klaauw Staff Report no. 479 November 2010 This paper presents preliminary

Federal Reserve Bank of New York Staff Reports An Introduction to the FRBNY Consumer Credit Panel Donghoon Lee Wilbert van der Klaauw Staff Report no. 479 November 2010 This paper presents preliminary

Measuring Student Debt and Its Performance

Federal Reserve Bank of New York Staff Reports Measuring Student Debt and Its Performance Meta Brown Andrew Haughwout Donghoon Lee Joelle Scally Wilbert van der Klaauw Staff Report No. 668 April 2014 This

Federal Reserve Bank of New York Staff Reports Measuring Student Debt and Its Performance Meta Brown Andrew Haughwout Donghoon Lee Joelle Scally Wilbert van der Klaauw Staff Report No. 668 April 2014 This

Student Loan Borrowing and Repayment Trends, 2015

Student Loan Borrowing and Repayment Trends, 2015 April 16, 2015 Andrew Haughwout, Donghoon Lee, Joelle Scally, Wilbert van der Klaauw The views presented here are those of the authors and do not necessarily

Student Loan Borrowing and Repayment Trends, 2015 April 16, 2015 Andrew Haughwout, Donghoon Lee, Joelle Scally, Wilbert van der Klaauw The views presented here are those of the authors and do not necessarily

Student Loan Balance & Repayment Trends in the FRBNY Consumer Credit Panel

PRELIMINARY, PLEASE ASK US BEFORE CITING Student Loan Balance & Repayment Trends in the FRBNY Consumer Credit Panel Donghoon Lee and Meta Brown June 6 th 2012 The views expressed are those of the authors

PRELIMINARY, PLEASE ASK US BEFORE CITING Student Loan Balance & Repayment Trends in the FRBNY Consumer Credit Panel Donghoon Lee and Meta Brown June 6 th 2012 The views expressed are those of the authors

Household Debt and Credit: Student Debt

Household Debt and Credit: Student Debt February 28, 2013 Donghoon Lee The views presented here are those of the author and do not necessarily reflect those of the Federal Reserve Bank of New York, or

Household Debt and Credit: Student Debt February 28, 2013 Donghoon Lee The views presented here are those of the author and do not necessarily reflect those of the Federal Reserve Bank of New York, or

Reason Statement Full Description Actions You Can Take or Keep this in mind

Factors Guide - Experian The consumer-friendly reason descriptions and actions a consumer can take (or things to keep ) below are provided for use within your FICO Open Access customer displays. The table

Factors Guide - Experian The consumer-friendly reason descriptions and actions a consumer can take (or things to keep ) below are provided for use within your FICO Open Access customer displays. The table

FICO Score Factors Guide - TransUnion

Factors Guide - TransUnion The consumer-friendly reason descriptions and things to keep in mind below are provided for use within FICO Open Access customer displays. The table includes a reason description

Factors Guide - TransUnion The consumer-friendly reason descriptions and things to keep in mind below are provided for use within FICO Open Access customer displays. The table includes a reason description

Week 2: Personal Guarantor

Week 2: Personal Guarantor Before you begin the credit building process, you need to identify who will personally guarantee the business credit lines. Your choices are as follows: yourself, someone you

Week 2: Personal Guarantor Before you begin the credit building process, you need to identify who will personally guarantee the business credit lines. Your choices are as follows: yourself, someone you

How To Get Credit Records From A Credit Card To A Bank Account

An Overview of Consumer Data and Credit Reporting. Robert B. Avery, Paul S. Calem, and Glenn B. Canner, of the Board's Division of Research and Statistics, and Raphael W. Bostic, of the University of Southern

An Overview of Consumer Data and Credit Reporting. Robert B. Avery, Paul S. Calem, and Glenn B. Canner, of the Board's Division of Research and Statistics, and Raphael W. Bostic, of the University of Southern

Insurance Score Models

Insurance Score Models Prepared by State of Alaska Division of Insurance Department of Community and Economic Development www.dced.state.ak.us/insurance (907) 465-2020 Insurance Score Models Some insurers

Insurance Score Models Prepared by State of Alaska Division of Insurance Department of Community and Economic Development www.dced.state.ak.us/insurance (907) 465-2020 Insurance Score Models Some insurers

FICO Score Factors Guide

Key score factors explain the top factors that affected your FICO Score. The order in which your FICO Score factors are listed is important. The first indicates the area that most affected your FICO Score

Key score factors explain the top factors that affected your FICO Score. The order in which your FICO Score factors are listed is important. The first indicates the area that most affected your FICO Score

Your Credit Score. 800-491-2328 www.congressionalfcu.org. score of at least 620 for approval and 760 for the best interest rate.

800-491-2328 www.congressionalfcu.org Your Credit Score Your credit score can have a major impact on your life. Not only do creditors typically check your score when deciding whether or not to approve

800-491-2328 www.congressionalfcu.org Your Credit Score Your credit score can have a major impact on your life. Not only do creditors typically check your score when deciding whether or not to approve

Consumer Credit Report

Page 1 of 5 Consumer Credit Report Tenth District Consumer Credit Report December 2, 2015 By Kelly Edmiston, Senior Economist Average debt for Tenth District consumers, defined for this report as all outstanding

Page 1 of 5 Consumer Credit Report Tenth District Consumer Credit Report December 2, 2015 By Kelly Edmiston, Senior Economist Average debt for Tenth District consumers, defined for this report as all outstanding

How To Know Your Credit Risk

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Your Credit Score and How You Can Improve It

Understanding Your Credit Score and How You Can Improve It How is your score calculated? The exact formula is a mystery and protected by the Federal Trade Commission Think of it as a secret recipe. Credit

Understanding Your Credit Score and How You Can Improve It How is your score calculated? The exact formula is a mystery and protected by the Federal Trade Commission Think of it as a secret recipe. Credit

About your credit score. About FICO Score. Other names for FICO Score. http://www.myfico.com/crediteducation/creditscores.aspx

http://www.myfico.com/crediteducation/creditscores.aspx About your credit score Your credit score influences the credit that s available to you and the terms (interest rate, etc.) that lenders offer you.

http://www.myfico.com/crediteducation/creditscores.aspx About your credit score Your credit score influences the credit that s available to you and the terms (interest rate, etc.) that lenders offer you.

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 2012-25 August 20, 2012 Consumer Debt and the Economic Recovery BY JOHN KRAINER A key ingredient of an economic recovery is a pickup in household spending supported by increased consumer

FRBSF ECONOMIC LETTER 2012-25 August 20, 2012 Consumer Debt and the Economic Recovery BY JOHN KRAINER A key ingredient of an economic recovery is a pickup in household spending supported by increased consumer

Understanding Your FICO Score

Understanding Your FICO Score 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Report 1 Checking Your Credit Report

Understanding Your FICO Score 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Report 1 Checking Your Credit Report

IMPROVING YOUR CREDIT AND DEBT

IMPROVING YOUR CREDIT AND DEBT The Credit & Debt Problem Americans are loaded with credit-card debt. The average American household with at least one credit card has nearly $15,950 in credit-card debt

IMPROVING YOUR CREDIT AND DEBT The Credit & Debt Problem Americans are loaded with credit-card debt. The average American household with at least one credit card has nearly $15,950 in credit-card debt

SCORES OVERVIEW. TransUnion Scores

S OVERVIEW Scores 1 Table of Contents CreditVision Scores CreditVision Account Management Score.... 2 CreditVision Auto Score....3 CreditVision Bankruptcy Score....3 CreditVision HELOC Score....4 CreditVision

S OVERVIEW Scores 1 Table of Contents CreditVision Scores CreditVision Account Management Score.... 2 CreditVision Auto Score....3 CreditVision Bankruptcy Score....3 CreditVision HELOC Score....4 CreditVision

Federal Reserve Bank of Kansas City: Consumer Credit Report

Federal Reserve Bank of Kansas City: Consumer Credit Report Tenth District Consumer Credit Report May 29, 2015 By Kelly Edmiston, Senior Economist and Mwai Malindi, Research Associate FIRST QUARTER 2015

Federal Reserve Bank of Kansas City: Consumer Credit Report Tenth District Consumer Credit Report May 29, 2015 By Kelly Edmiston, Senior Economist and Mwai Malindi, Research Associate FIRST QUARTER 2015

Credit Analyzer. Potential score change: +19 12/10/2009. CreditXpert Credit Score Summary. Actions

Page 1 of 8 Credit Analyzer Reports available for: TransUnion Experian Equifax Results for TransUnion For: Provided By: Mode: Rapid Rescore (Timeframe: Immediate) Credit Report Date: 12/03/2009 Disposable

Page 1 of 8 Credit Analyzer Reports available for: TransUnion Experian Equifax Results for TransUnion For: Provided By: Mode: Rapid Rescore (Timeframe: Immediate) Credit Report Date: 12/03/2009 Disposable

The Truth About Credit Repair

The Truth About Credit Repair Discover The Insider Secrets Of How The Credit System Really Works and How To Beat The Credit Bureaus At Their Own Game. David Shapiro Esq. Applied Credit Repair Solutions

The Truth About Credit Repair Discover The Insider Secrets Of How The Credit System Really Works and How To Beat The Credit Bureaus At Their Own Game. David Shapiro Esq. Applied Credit Repair Solutions

Overview of Credit Scoring

Overview of Credit Scoring Page 19 of 134 Overview of Credit Scoring This session will focus on providing you with both information about this topic as well as new ideas and activities for making this

Overview of Credit Scoring Page 19 of 134 Overview of Credit Scoring This session will focus on providing you with both information about this topic as well as new ideas and activities for making this

Understanding your Credit Score

Understanding your Credit Score Understanding Your Credit Score Fair, Isaac and Co. is the San Rafael, California Company founded in 1956 by Bill Fair and Earl Isaac. They pioneered the field of credit

Understanding your Credit Score Understanding Your Credit Score Fair, Isaac and Co. is the San Rafael, California Company founded in 1956 by Bill Fair and Earl Isaac. They pioneered the field of credit

Solving the Credit Puzzle. L G & W Federal Credit Union

Solving the Credit Puzzle L G & W Federal Credit Union Knowledge Check How much do you already know about credit scoring? Sample Credit Report Credit Bureaus Equifax TransUnion Experian Who Can Pull Your

Solving the Credit Puzzle L G & W Federal Credit Union Knowledge Check How much do you already know about credit scoring? Sample Credit Report Credit Bureaus Equifax TransUnion Experian Who Can Pull Your

Financial Empowerment Curriculum Moving Ahead Through Financial Management. Workshop Credit Overview

Financial Empowerment Curriculum Moving Ahead Through Financial Management Workshop Credit Overview 1 Workshop Objectives Explain why credit is important. Access and read a copy of your credit report.

Financial Empowerment Curriculum Moving Ahead Through Financial Management Workshop Credit Overview 1 Workshop Objectives Explain why credit is important. Access and read a copy of your credit report.

Medical School Loan Repayment & Building Credit

Medical School Loan Repayment & Building Credit Presented by: Thomas Murphy Harvard University Employees Credit Union Presentation Objectives Medical School Loan Overview Forbearance or Repayment Understanding

Medical School Loan Repayment & Building Credit Presented by: Thomas Murphy Harvard University Employees Credit Union Presentation Objectives Medical School Loan Overview Forbearance or Repayment Understanding

Taking Charge of Your Financial Future

Taking Charge of Your Financial Future Why is Your Credit Score Important? Understanding credit scoring can help you manage your credit. By knowing how credit risk is evaluated, you can take actions that

Taking Charge of Your Financial Future Why is Your Credit Score Important? Understanding credit scoring can help you manage your credit. By knowing how credit risk is evaluated, you can take actions that

Credit Score Secrets Revealed

Credit Score Secrets Revealed This Complementary Special Report was prepared by: 2 The Secrets Behind Your Credit Scores Your life is your credit. And your Credit Score is the key to everything. As important

Credit Score Secrets Revealed This Complementary Special Report was prepared by: 2 The Secrets Behind Your Credit Scores Your life is your credit. And your Credit Score is the key to everything. As important

Your credit score. What it is. What it means.

Your credit score. What it is. What it means. Y ou may have heard of credit scores and wonder what they are. How do they affect your ability to get a loan? How do they affect the interest rate and points

Your credit score. What it is. What it means. Y ou may have heard of credit scores and wonder what they are. How do they affect your ability to get a loan? How do they affect the interest rate and points

CREDIT REPORTS WHAT EVERY CONSUMER SHOULD KNOW ABOUT MORTGAGE EQUITY P A R T N E R S

F WHAT EVERY CONSUMER SHOULD KNOW ABOUT CREDIT REPORTS MORTGAGE EQUITY P A R T N E R S Your Leaders in Lending B The information contained herein is for informational purposes only. The algorithymes and

F WHAT EVERY CONSUMER SHOULD KNOW ABOUT CREDIT REPORTS MORTGAGE EQUITY P A R T N E R S Your Leaders in Lending B The information contained herein is for informational purposes only. The algorithymes and

About credit reports. Credit Reporting Agencies. Creating Your Credit Report

About credit reports Credit Reporting Agencies Credit reporting agencies maintain files on millions of borrowers. Lenders making credit decisions buy credit reports on their prospects, applicants and customers

About credit reports Credit Reporting Agencies Credit reporting agencies maintain files on millions of borrowers. Lenders making credit decisions buy credit reports on their prospects, applicants and customers

Understanding Your Credit Score

Understanding Your Credit Score Contents An Introduction to Credit Scores...... 1 How Credit Scoring Helps You........ 2 Your Credit Report The Basis of Your Credit Score........ 4 How Scoring Works................

Understanding Your Credit Score Contents An Introduction to Credit Scores...... 1 How Credit Scoring Helps You........ 2 Your Credit Report The Basis of Your Credit Score........ 4 How Scoring Works................

Understanding Your Credit Score

Understanding Your Credit Score Contents Your Credit Score A Vital Part of Your Credit Health...... 1 How Credit Scoring Helps You........ 2 Your Credit Report The Basis of Your Score............. 4 How

Understanding Your Credit Score Contents Your Credit Score A Vital Part of Your Credit Health...... 1 How Credit Scoring Helps You........ 2 Your Credit Report The Basis of Your Score............. 4 How

Understanding Credit. Megan Stearns, Credit Counselor

Understanding Credit Megan Stearns, Credit Counselor Obtaining your free credit report will lower your credit score. Closing old accounts can help your credit score. Paying off the balances on your credit

Understanding Credit Megan Stearns, Credit Counselor Obtaining your free credit report will lower your credit score. Closing old accounts can help your credit score. Paying off the balances on your credit

CBCInnovis Infile Credit Report Reference Guide

1 2 3 4 5 6 6 7 7 8 A A A B C C C 9 D E F G H I J K 10 11 1 1 2 3 4 5 6 7 8 9 PROCESSING CENTER CONTACT INFORMATION: Please contact the Processing Center if you have any questions regarding a CBCInnovis

1 2 3 4 5 6 6 7 7 8 A A A B C C C 9 D E F G H I J K 10 11 1 1 2 3 4 5 6 7 8 9 PROCESSING CENTER CONTACT INFORMATION: Please contact the Processing Center if you have any questions regarding a CBCInnovis

Topic 3 Credit Report

Topic 3 Credit Report Questions to Think About: What are the different types of credit and why is credit important? What are its advantages and disadvantages? What is a credit report? How do you read it

Topic 3 Credit Report Questions to Think About: What are the different types of credit and why is credit important? What are its advantages and disadvantages? What is a credit report? How do you read it

Reviewing C Your Credit Report

chapter 2 Reviewing C Your Credit Report What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

chapter 2 Reviewing C Your Credit Report What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

A.MORTGAGE LENDER B. CREDIT CARD ISSUER C.HOME INSURER E. ELECTRIC COMPANY F. LANDLORD G.ALL OF THE ABOVE D.CELL PHONE COMPANY

1. WHICH OF THE FOLLOWING MIGHT USE CREDIT SCORES? A.MORTGAGE LENDER B. CREDIT CARD ISSUER C.HOME INSURER E. ELECTRIC COMPANY F. LANDLORD G.ALL OF THE ABOVE D.CELL PHONE COMPANY 1. WHICH OF THE FOLLOWING

1. WHICH OF THE FOLLOWING MIGHT USE CREDIT SCORES? A.MORTGAGE LENDER B. CREDIT CARD ISSUER C.HOME INSURER E. ELECTRIC COMPANY F. LANDLORD G.ALL OF THE ABOVE D.CELL PHONE COMPANY 1. WHICH OF THE FOLLOWING

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Through financial knowledge and expertise, we provide high-quality products and services that enable people to enjoy a better

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Through financial knowledge and expertise, we provide high-quality products and services that enable people to enjoy a better

Credit Scoring and Its Role In Lending A Guide for the Mortgage Professional

Credit Scoring and Its Role In Lending A Guide for the Mortgage Professional How To Improve an Applicant's Credit Score There is no magic to improving an applicant's credit score. Credit scores automatically

Credit Scoring and Its Role In Lending A Guide for the Mortgage Professional How To Improve an Applicant's Credit Score There is no magic to improving an applicant's credit score. Credit scores automatically

Understanding Your Credit Score Contents Your Credit Score A Vital Part of Your Credit Health...... 1 How Credit Scoring Helps You........ 2 Your Credit Report The Basis of Your Score............. 4 How

Understanding Your Credit Score Contents Your Credit Score A Vital Part of Your Credit Health...... 1 How Credit Scoring Helps You........ 2 Your Credit Report The Basis of Your Score............. 4 How

IMPROVE YOUR CREDIT SCORE. Effective Credit Management At Your Fingertips

IMPROVE YOUR CREDIT SCORE Effective Credit Management At Your Fingertips Introduction In this ebook, you will get valuable information including: What is a credit score The score breakdown Managing your

IMPROVE YOUR CREDIT SCORE Effective Credit Management At Your Fingertips Introduction In this ebook, you will get valuable information including: What is a credit score The score breakdown Managing your

Understanding Your Credit Score

Understanding Your Credit Score Prof. Michael Staten Director, Take Charge America Institute Norton School of Family and Consumer Sciences FEFE Conference, Baltimore, MD April 30, 2010 A Good Credit Score

Understanding Your Credit Score Prof. Michael Staten Director, Take Charge America Institute Norton School of Family and Consumer Sciences FEFE Conference, Baltimore, MD April 30, 2010 A Good Credit Score

Lending 101 The Basics

Lending 101 The Basics Overview Loan categories Credit types Different loan types Interest rate Applying for a loan Credit & credit reports Simple loan tips Test Loan Categories Secured loan - a loan that

Lending 101 The Basics Overview Loan categories Credit types Different loan types Interest rate Applying for a loan Credit & credit reports Simple loan tips Test Loan Categories Secured loan - a loan that

Credit Scoring. 1-800-444-RATE www.gogsf.com

Credit Scoring 1-800-444-RATE www.gogsf.com Your credit score is a major factor that will be considered by the lender when they review your loan application. They want to know what your credit history

Credit Scoring 1-800-444-RATE www.gogsf.com Your credit score is a major factor that will be considered by the lender when they review your loan application. They want to know what your credit history

UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor

By Bill Taylor") UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor Most studies about consumer debt have only focused on credit cards and mortgages. However, personal debt also may include medical expenses, school

UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor Most studies about consumer debt have only focused on credit cards and mortgages. However, personal debt also may include medical expenses, school

Understanding a Credit Report! April 21, 2011. New York City Department of Consumer Affairs. All rights reserved.

Understanding a Credit Report! Questions to Think About What are the different types of credit and why is credit important? What is a credit report? How does credit impact future financial goals? 3 What

Understanding a Credit Report! Questions to Think About What are the different types of credit and why is credit important? What is a credit report? How does credit impact future financial goals? 3 What

Credit Score Management Seminar. Manage, protect and improve your Credit Score!

Credit Score Management Seminar Manage, protect and improve your Credit Score! Overview What is a Credit Score How Lenders Use Your Credit Score How Your Credit Score Impacts You What Makes Up Your Credit

Credit Score Management Seminar Manage, protect and improve your Credit Score! Overview What is a Credit Score How Lenders Use Your Credit Score How Your Credit Score Impacts You What Makes Up Your Credit

Report to the Congress on the Profitability of Credit Card Operations of Depository Institutions

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM Report to the Congress on the Profitability of Credit Card Operations of Depository Institutions Submitted to the Congress pursuant to section 8 of the

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM Report to the Congress on the Profitability of Credit Card Operations of Depository Institutions Submitted to the Congress pursuant to section 8 of the

YOUR CREDIT SCORE. Payment History - 35%

YOUR REDIT SORE Many of our clients are concerned about their ability to obtain credit in the future. There are several issues related to those concerns. redit reporting agencies (Experian, Equifax, and

YOUR REDIT SORE Many of our clients are concerned about their ability to obtain credit in the future. There are several issues related to those concerns. redit reporting agencies (Experian, Equifax, and

Secrets of the Credit Score UCCS Employee Seminar 10/21/2014

Secrets of the Credit Score UCCS Employee Seminar 10/21/2014 Schuyler (Skip) Wells, Ent Federal Credit Union Question!! What do credit reports, the number of and use of credit cards, inquiries, credit

Secrets of the Credit Score UCCS Employee Seminar 10/21/2014 Schuyler (Skip) Wells, Ent Federal Credit Union Question!! What do credit reports, the number of and use of credit cards, inquiries, credit

Credit 101. Learn how to get and keep your credit in shape! From Silverton Mortgage

Credit 101 Learn how to get and keep your credit in shape! From Silverton Mortgage Table of Contents What is a credit score? 2 Why is it important? 2 How is a credit score determined? 3 How can I see my

Credit 101 Learn how to get and keep your credit in shape! From Silverton Mortgage Table of Contents What is a credit score? 2 Why is it important? 2 How is a credit score determined? 3 How can I see my

Mortgage Lending: The Bubble, the Burst and Now What?

Mortgage Lending: The Bubble, the Burst and Now What? How did the financial crisis affect members and how have they fared since? 1 2 3 In the Bubble... What did the credit health of the population look

Mortgage Lending: The Bubble, the Burst and Now What? How did the financial crisis affect members and how have they fared since? 1 2 3 In the Bubble... What did the credit health of the population look

Credit Scores. www.howtogainwealth.com. Copyright 2009 How to Gain Wealth. All rights reserved.

Credit Scores Why is my Credit Score important? Lenders, such as banks and credit card companies, use credit scores to evaluate the potential risk posed by lending money to consumers and to mitigate losses

Credit Scores Why is my Credit Score important? Lenders, such as banks and credit card companies, use credit scores to evaluate the potential risk posed by lending money to consumers and to mitigate losses

Improving Your Credit

Teacher Homebuyer Guide to: Improving Your Credit By John Godbey, Founder and Broker of Teacher Homebuyer Real Estate Introduction Thank you for signing up for our Ebook "Improving Your Credit." We find

Teacher Homebuyer Guide to: Improving Your Credit By John Godbey, Founder and Broker of Teacher Homebuyer Real Estate Introduction Thank you for signing up for our Ebook "Improving Your Credit." We find

How To Determine Credit History

297 Credit Report Accuracy and Access to Credit Robert B. Avery, Paul S. Calem, and Glenn B. Canner, of the Board s Division of Research and Statistics, prepared this article. Shannon C. Mok provided research

297 Credit Report Accuracy and Access to Credit Robert B. Avery, Paul S. Calem, and Glenn B. Canner, of the Board s Division of Research and Statistics, prepared this article. Shannon C. Mok provided research

CREDIT BASICS About your credit score

CREDIT BASICS About your credit score Your credit score influences the credit that s available to you and the terms (interest rate, etc.) that lenders offer you. It s a vital part of your credit health.

CREDIT BASICS About your credit score Your credit score influences the credit that s available to you and the terms (interest rate, etc.) that lenders offer you. It s a vital part of your credit health.

Data point: Medical debt and credit scores

Data point: Medical debt and credit scores May 2014 Kenneth P. Brevoort Michelle Kambara This is another in an occasional series of publications from the Consumer Financial Protection Bureau s Office of

Data point: Medical debt and credit scores May 2014 Kenneth P. Brevoort Michelle Kambara This is another in an occasional series of publications from the Consumer Financial Protection Bureau s Office of

CREDIT REPORTS & SCORES:

CREDIT REPORTS & SCORES: A Guide to Understanding and Improving Your Credit NYLAG Financial Counseling Division Workshop Financial Counseling Division New York Legal Assistance Group (212) 613-5000 NYLAG

CREDIT REPORTS & SCORES: A Guide to Understanding and Improving Your Credit NYLAG Financial Counseling Division Workshop Financial Counseling Division New York Legal Assistance Group (212) 613-5000 NYLAG

FEDERAL RESERVE BULLETIN

FEDERAL RESERVE BULLETIN VOLUME 38 May 1952 NUMBER 5 Business expenditures for new plant and equipment and for inventory reached a new record level in 1951 together, they exceeded the previous year's total

FEDERAL RESERVE BULLETIN VOLUME 38 May 1952 NUMBER 5 Business expenditures for new plant and equipment and for inventory reached a new record level in 1951 together, they exceeded the previous year's total

Student Loans and Credit Reports

Student Loans and Credit Reports We Will Discuss The role of credit in personal finance Review of credit terms and factors Impact of student loans on reports and scores Next steps you can take to encourage

Student Loans and Credit Reports We Will Discuss The role of credit in personal finance Review of credit terms and factors Impact of student loans on reports and scores Next steps you can take to encourage

What We Need to Know About. Credit Management & Credit Repair for Entrepreneurs

What We Need to Know About. Credit Management & Credit Repair for Entrepreneurs What is Credit? When someone lends you money, and you pay them back with interest, they have extended you credit. Credit

What We Need to Know About. Credit Management & Credit Repair for Entrepreneurs What is Credit? When someone lends you money, and you pay them back with interest, they have extended you credit. Credit

How to improve your FICO Score in perilous times By Blair Ball. National Distribution of FICO Scores

How to improve your FICO Score in perilous times By Blair Ball When you re applying for credit whether it s a credit card, a car loan, a personal loan or a mortgage lenders want to know your credit risk

How to improve your FICO Score in perilous times By Blair Ball When you re applying for credit whether it s a credit card, a car loan, a personal loan or a mortgage lenders want to know your credit risk

PA HealthCare Credit Union. The Credit Clinic. The PA HealthCare Credit Union contributes to the financial success of our members.

PA HealthCare Credit Union The Credit Clinic The PA HealthCare Credit Union contributes to the financial success of our members. 1 Copyright 2006 Agenda Welcome & Introduction Overview Product Rate Credit

PA HealthCare Credit Union The Credit Clinic The PA HealthCare Credit Union contributes to the financial success of our members. 1 Copyright 2006 Agenda Welcome & Introduction Overview Product Rate Credit

Early Delinquency Intervention: Saving Your Home From Foreclosure

Early Delinquency Intervention: Saving Your Home From Foreclosure There are many circumstances in a homeowner s life that could result in missed mortgage payments: unexpected expenses, loss of overtime,

Early Delinquency Intervention: Saving Your Home From Foreclosure There are many circumstances in a homeowner s life that could result in missed mortgage payments: unexpected expenses, loss of overtime,

FICO Credit-Based Insurance Scores

1. Most consumers benefit from the use of insurance scores Lower premiums In its July 2007 report, Credit-Based Insurance Scores: Impacts on Consumers of Automobile Insurance, the Federal Trade Commission

1. Most consumers benefit from the use of insurance scores Lower premiums In its July 2007 report, Credit-Based Insurance Scores: Impacts on Consumers of Automobile Insurance, the Federal Trade Commission

Assume the Role of Managing Your Credit Prudently and Watch Your Credit Score Improve July 2012

Assume the Role of Managing Your Credit Prudently and Watch Your Credit Score Improve July 2012 OVERVIEW The three numbers that make up a credit score have become an obsession to some people. But what

Assume the Role of Managing Your Credit Prudently and Watch Your Credit Score Improve July 2012 OVERVIEW The three numbers that make up a credit score have become an obsession to some people. But what

Improving a Credit Profile

Improving a Credit Profile Steps to improving a credit profile STEP 1. Order your credit Report STEP 2. Evaluate & develop a plan STEP 3. Is the personal information accurate? STEP 4. Are the tradelines

Improving a Credit Profile Steps to improving a credit profile STEP 1. Order your credit Report STEP 2. Evaluate & develop a plan STEP 3. Is the personal information accurate? STEP 4. Are the tradelines

Definitions. In some cases a survey rather than an ILC is required.

Definitions 1. What is the closing? The closing is a formal meeting at which both the buyer and seller meet to sign all the final documentation required for the buyer's mortgage loan. Once the closing

Definitions 1. What is the closing? The closing is a formal meeting at which both the buyer and seller meet to sign all the final documentation required for the buyer's mortgage loan. Once the closing

Mortgage & Home Equity Reporting Guidelines In Response to Current Financial Conditions

Mortgage & Home Equity Reporting Guidelines In Response to Current Financial Conditions General Reporting Guidelines Report accounts in the standard Metro 2 Format. Refer to the Credit Reporting Resource

Mortgage & Home Equity Reporting Guidelines In Response to Current Financial Conditions General Reporting Guidelines Report accounts in the standard Metro 2 Format. Refer to the Credit Reporting Resource

Use of Consumer Credit Data for Statistical Purposes: Korean Experience

Use of Consumer Credit Data for Statistical Purposes: Korean Experience Byong-ki Min October 2014 Abstract For some time, the Bank of Korea has sought to obtain micro data that can help us to analyze our

Use of Consumer Credit Data for Statistical Purposes: Korean Experience Byong-ki Min October 2014 Abstract For some time, the Bank of Korea has sought to obtain micro data that can help us to analyze our

Your Credit Score. It s Not As Bad Or As Permanent As You May Think. Presented by Jennifer Matthews, MBA President and CEO

Your Credit Score It s Not As Bad Or As Permanent As You May Think Presented by Jennifer Matthews, MBA Things to Know What a credit score is Where to get a free credit report What goes into your credit

Your Credit Score It s Not As Bad Or As Permanent As You May Think Presented by Jennifer Matthews, MBA Things to Know What a credit score is Where to get a free credit report What goes into your credit

The nuts and bolts of consumer and business credit reporting

The nuts and bolts of consumer and business credit reporting Making sure your personal credit report doesn t cause a credit breakdown for your small business 2014 Experian Information Solutions, Inc. All

The nuts and bolts of consumer and business credit reporting Making sure your personal credit report doesn t cause a credit breakdown for your small business 2014 Experian Information Solutions, Inc. All

OCC and OTS Mortgage Metrics Report

Impact on Consumer VantageScore Credit Scores Due To Various Mortgage Loan Restructuring Options January 2010 OVERVIEW The recent economic downturn and the credit market crisis combined to produce immense

Impact on Consumer VantageScore Credit Scores Due To Various Mortgage Loan Restructuring Options January 2010 OVERVIEW The recent economic downturn and the credit market crisis combined to produce immense

ALERTS NOTIFICATION USER GUIDE

Page 1 of 10 ABOUT EQUIFAX ALERTS NOTIFICATION USER GUIDE Equifax Canada Inc. Box 190 Jean Talon Station Montreal, Quebec H1S 2Z2 Equifax empowers businesses and consumers with information they can trust.

Page 1 of 10 ABOUT EQUIFAX ALERTS NOTIFICATION USER GUIDE Equifax Canada Inc. Box 190 Jean Talon Station Montreal, Quebec H1S 2Z2 Equifax empowers businesses and consumers with information they can trust.

Managing Your Credit Report and Scores. Apprisen. 800.355.2227 www.apprisen.com

Managing Your Credit Report and Scores Apprisen 800.355.2227 www.apprisen.com Managing Your Credit Report and Scores Your credit score is one of the most important aspects of your personal finances. From

Managing Your Credit Report and Scores Apprisen 800.355.2227 www.apprisen.com Managing Your Credit Report and Scores Your credit score is one of the most important aspects of your personal finances. From

Student Loans and Credit Reports

Student Loans and Credit Reports Presented by: Debbie Murphy We Will Discuss: The role of credit in personal finance Review of credit terms and factors Impact of student loans on reports and scores Next

Student Loans and Credit Reports Presented by: Debbie Murphy We Will Discuss: The role of credit in personal finance Review of credit terms and factors Impact of student loans on reports and scores Next

Client Alert. Compliance with the New Risk-Based Pricing Rule. March 2010. By Andrew Smith and Joe Gabai. Background. Enforcement

March 2010 Compliance with the New Risk-Based Pricing Rule By Andrew Smith and Joe Gabai A new rule, issued by the Federal Reserve Board and the Federal Trade Commission, requires any company that uses

March 2010 Compliance with the New Risk-Based Pricing Rule By Andrew Smith and Joe Gabai A new rule, issued by the Federal Reserve Board and the Federal Trade Commission, requires any company that uses

How to Improve and Maintain your Credit Score

How to Improve and Maintain your Credit Score Special points of interest: Factors that influence your credit score How your credit score is calculated Improving your credit score How to fix flawed credit

How to Improve and Maintain your Credit Score Special points of interest: Factors that influence your credit score How your credit score is calculated Improving your credit score How to fix flawed credit

The Advantages and Disadvantages of Credit History Scoring

BIS Working Papers No 146 Consumer credit scoring: do situational circumstances matter? by Robert B Avery*, Paul S Calem* and Glenn B Canner* Monetary and Economic Department January 2004 * Board of Governors

BIS Working Papers No 146 Consumer credit scoring: do situational circumstances matter? by Robert B Avery*, Paul S Calem* and Glenn B Canner* Monetary and Economic Department January 2004 * Board of Governors

Establishing and maintaining good credit is an important part of financial planning. Typically most individuals do not have enough cash on hand for

Basics of Credit Establishing and maintaining good credit is an important part of financial planning. Typically most individuals do not have enough cash on hand for emergencies, or to make major purchases

Basics of Credit Establishing and maintaining good credit is an important part of financial planning. Typically most individuals do not have enough cash on hand for emergencies, or to make major purchases

How To Check Your Credit Report For Not Credit History

Your Credit Report P.O. Box 15128 Spokane Valley, WA 99215 800.852.5316 www.hzcu.org You may not think about them every day, but your credit report and the three little digits that make up your credit

Your Credit Report P.O. Box 15128 Spokane Valley, WA 99215 800.852.5316 www.hzcu.org You may not think about them every day, but your credit report and the three little digits that make up your credit

Loan Processing Credit Reports

Loan Processing Credit Reports Alternative Financing and Telework Loan Programs Annual Meeting Washington, DC December 13, 2004 By Brett Christensen Executive Vice President Lending Solutions Consulting,

Loan Processing Credit Reports Alternative Financing and Telework Loan Programs Annual Meeting Washington, DC December 13, 2004 By Brett Christensen Executive Vice President Lending Solutions Consulting,

Credit ~ The Basics Participant s Guide

1 Credit ~ The Basics Participant s Guide Table of Contents Welcome Pre-Test What is Credit & Why is it Important? Types of Loans The Cost of Credit The Four C s of Credit Credit Reports Credit Scores

1 Credit ~ The Basics Participant s Guide Table of Contents Welcome Pre-Test What is Credit & Why is it Important? Types of Loans The Cost of Credit The Four C s of Credit Credit Reports Credit Scores

Employment declined dramatically Nonfarm payroll employment (index=100 at peak of business cycle)

") Employment declined dramatically Nonfarm payroll employment (index=1 at peak of business cycle) 27 1981 1973 199 21 198 Index 14 13 12 11 1 99 98 97 96 95 94-5 5 1 15 2 25 3 35 4 Months since peak of business

Employment declined dramatically Nonfarm payroll employment (index=1 at peak of business cycle) 27 1981 1973 199 21 198 Index 14 13 12 11 1 99 98 97 96 95 94-5 5 1 15 2 25 3 35 4 Months since peak of business

Know the Score. May 20, 2015

Know the Score May 20, 2015 2014 Credit Builders Alliance, Inc. Some rights reserved. CREDIT BUILDERS ALLIANCE and the accompanying Logo are trademarks of CreditBuilders Alliance, Inc. This document is

Know the Score May 20, 2015 2014 Credit Builders Alliance, Inc. Some rights reserved. CREDIT BUILDERS ALLIANCE and the accompanying Logo are trademarks of CreditBuilders Alliance, Inc. This document is

Page 1 of 5 http://nyti.ms/mfa3y0 ECONOMY The Hefty Yoke of Student Loan Debt FEB. 20, 2014 High & Low Finance By FLOYD NORRIS More than five years after the binge of irresponsible lending led to the credit

Page 1 of 5 http://nyti.ms/mfa3y0 ECONOMY The Hefty Yoke of Student Loan Debt FEB. 20, 2014 High & Low Finance By FLOYD NORRIS More than five years after the binge of irresponsible lending led to the credit