TILA RESPA Integrated Disclosures. On October 3 rd, life as we know it will change forever. One of the new forms is.

|

|

|

- Amberly Henderson

- 8 years ago

- Views:

Transcription

1 TILA RESPA Integrated Disclosures The Loan Estimate and Miscellaneous Requirements Lynne Murphy Breen, Esquire Sue Ellen Rogal, Esquire September 16, 2015 On October 3 rd, life as we know it will change forever Just kidding! On October 3 rd, the final rule from the Consumer Financial Protection Bureau will go into effect and the TILA RESPA Integrated Disclosure forms will be used for most residential transactions applied for on or after that date. One of the new forms is the Loan Estimate A three page form which looks like a combination TIL/GFE Designed to provide consumers with information which may be helpful in understanding the features, costsandrisksassociatedwiththemortgageloanfor which they are applying. Must be provided to consumers no later than three (3) business days after they submit a loan application. 1

2 Defined Terms Applicants The Borrowers/Consumers Business Day A day on which the creditor s offices are open to the public for carrying on substantially all of its business functions. For purposes of rescission and delivery, the term means all calendar days except Sundays and legal public holidays. Consummation The day the Consumer becomes contractually obligated to the Creditor on the loan. Both lenders and the CFPB seem to be suggesting that this is the date the borrower signs the note, regardless of escrow rules. In Massachusetts, consummation date will equal closing date for both purchases and refinances. Consumer A borrower in a residential loan transaction Creditor A loan originator, lender or bank ( Lender ) Variances The new rule contains 3 tolerance levels, but describes them as variances and expands the charges that cannot increase at closing to include charges for any service the borrower cannot shop for, as well as charges for any service provided by a subsidiary or affiliate of the creditor. Affected Transactions Both the Loan Estimate and Closing Disclosure must be used for most closed end consumer mortgages for which application is made on or after October 3, Transactions which are not affected Home equity lines of credit, reverse mortgages, mortgages secured by a mobile home (or other dwelling not attached to real property), no interest second mortgages made for down payment assistance, and energy efficiency or foreclosure avoidance loans are not subject to the new rule, and will continue to use the separate TIL and HUD forms now in use. The rule does not apply to commercial transaction. The rule does not apply to mortgage loans made by individuals who are not considered creditors because they make 5 or fewer mortgages per year (i.e. mortgages given by family members). 2

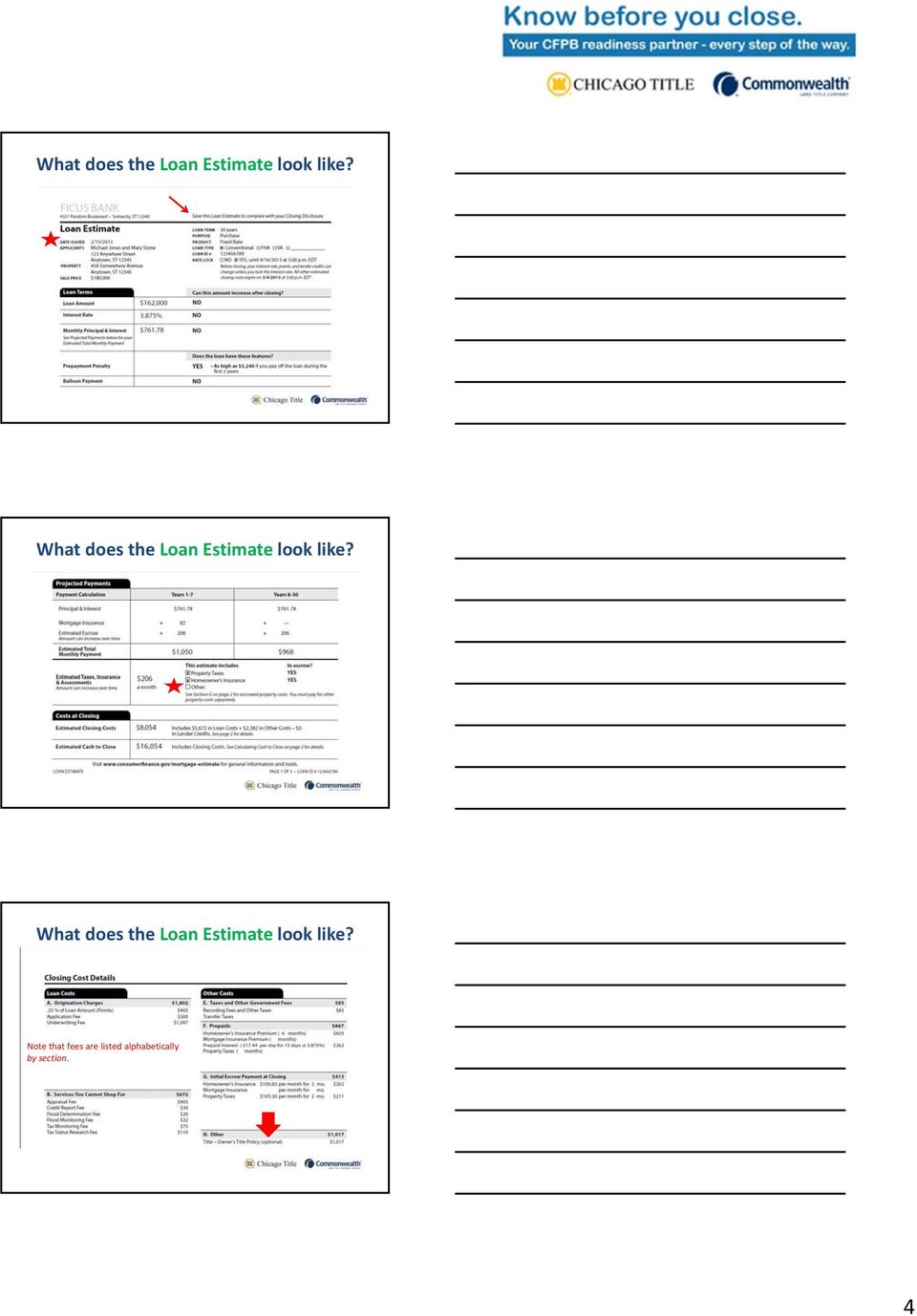

3 Transactions which are not affected Residential consumer loans not affected by the Rule will continue to use the separate TIL and HUD forms now in use. Commercial and non creditor loans may use the original HUD 1 SettlementStatement,if they so choose. Note: A home equity loan is subject to the new rule. The distinction is between line (open ended, consumer writes checks in amounts that vary) and loan (closed ended, one time payment to consumer). But before we go any further, take a deep breath and repeat after me: The Loan Estimate and the Closing Disclosure are just two more consumer disclosure forms, like the TIL and the GFE, and the HUD 1 Settlement Statement. I will learn to use the new forms, and, yes, even grow to like them. (And hopefully retire before they change again). I am not going to panic. What does it look like? The Loan Estimate is a 3 page document which contains information about Loan Terms, Projected Payments, Costs at Closing (broken down into Loan Costs, Other Costs and Calculating Cash to Close), and provides sections which allow the consumer to see the full impact of the mortgage loan (Comparison and Other Considerations). Each consumer must sign to acknowledge receipt of the Loan Estimate. 3

4 What does the Loan Estimate look like? What does the Loan Estimate look like? What does the Loan Estimate look like? Note that fees are listed alphabetically by section. 4

5 What does the Loan Estimate look like? Note that the names of all title related charges must begin with the word Title, and then listed alphabetically by the actual fee name What does the Loan Estimate look like? What does the Loan Estimate look like? 5

6 What does the Loan Estimate look like? About the Loan Estimate The Loan Estimate must contain a good faith estimate of credit costs and transaction terms It must be in writing and contain only the specific information set forth in the rule and as set forth in the CFPB s form Lenders may only use revised or correct Loan Estimates when specific requirements are met, such as when changed circumstances result in increased charges; technical errors, miscalculations or underestimates are NOT permissible reasons to revise a Loan Estimate About the Loan Estimate An application means the submission of a consumer s financial information for purposes of obtaining an extension of credit. Under the rule, an application consists of the submission of these six (6) pieces of information: The consumer s name; The consumer s income; The consumer s social security number to obtain a credit report; The property address; An estimate of the value of the property; and The mortgage loan amount sought. An application may be submitted in written or electronic format, which includes a written record of an oral application. 6

7 Who will prepare the Loan Estimate? The rule states that the Lender is responsible for the preparationof the Loan Estimate; creditors are required to act in good faith and exercise due diligence in obtain information necessary to complete the Loan Estimate. This requires communication and collaboration between Lender and service providers. If the Lender prepares the Loan Estimate, why should I care about it? The Lender is required to make sure that the data obtained is the best information available you can assist your Lender by providing detailed and accurate fees for your office and services obtained through your office (i.e. MLC, plot plan, title, recording fees, deed stamps). Be sure that all communications regarding fees contain a date and the name of your office, because the Lender must track what data was obtained when and from whom in order to document information disclosed on the Loan Estimate! If the Lender prepares the Loan Estimate, why should I care about it? One word: Tolerances. WhetherornotaLoan Estimate was made in good faith is determined by calculating the difference between the estimated charge originally provided in the Loan Estimate and the actual charges paid by or imposed on the consumer in the Closing Disclosure. Tolerance requirements vary depending upon the circumstances: If the borrower shopped for closing services (and the CFPB really means shopped picking your name off of a list from the lender isn t shopping), there is an open tolerance for related charges If the lender picked you, the tolerance is 10% However, if you are an affiliated provider for the lender, the tolerance is 0%. Being on the lender s list of closing attorneys is different than being an affiliated provider, so be sure to check with your lender! Charging a consumer less that the amount disclosed is considered to be in good faith, with out regard to any tolerance limitations, so if you don t provide accurate fees upfront, you may end up eating those costs at closing! 7

8 If the Lender prepares the Loan Estimate, why should I care about it? Because you want to be sure that the Lender is accurately quoting the Loan and Owner s Title Insurance premiums, in light of: The new tolerance requirements Thefactthatmanyout of state lenders are not used to quoting premium the way the CFPB requires (which, happily, is how we ve always done it in Massachusetts) If the Lender prepares the Loan Estimate, why should I care about it? Calculating premium under the rule: The rule requires that the Loan premium be disclosed in the Services You Can Shop For category. To calculate, multiply the loan amount (in thousands, rounded up to the nearest thousand) times $2.50 (up to $1,000,000). Ex. $265,500 Loan Amount: 2.50 x 266 = $ The rule requires that the Owner s premium be disclosed in the Other category (with the optional designation). To calculate, multiply the purchase price (in thousands, rounded up to the nearest thousand) times $4 (up to $1,000,000), plus the simultaneous fee, less the Loan premium. Ex. $409,900 Purchase Price: (4 x 410) = $1, If the Lender prepares the Loan Estimate, why should I care about it? It is also important that the fee names listed on the Loan Estimate match those listed on the Closing Disclosure, so either make a list of all possible fee names and send them to your lender or ask your lender for their list. All fees associated with title must be preceded by the word Title, as in Title Deed Preparation, Title Document Preparation, Title Settlement Agent Fee, Title Title Examination. 8

times $2.50 (up to $1,000,000). Ex.")

9 Who will be responsible for delivery of the Loan Estimate? The Lender is responsible for delivering the Loan Estimate (or placing it in the mail) no later than the third business day after receipt of the consumer s loan application. For purposes of providing the Loan Estimate,abusiness day is a day on which the lender s offices are open to the public for carrying out substantially all of its business functions. (Note that this is different than the definition of business day used when counting the days to ensure that the consumer receives the Closing Disclosure on time.) What will be the impact of the (optional) designation for the owner s title insurance premium on the Loan Estimate and Closing Disclosure? Optional? If title insurance is optional, why is it required by the lender and considered a Loan Cost? Spread the word: An owner s policy isn t (optional), it s necessary! What are the lenders saying about the Loan Estimate? Two words: Collaboration and Communication Old school , fax, overnight delivery, mail (yikes!) not so much Use of a third party portal where information will be exchanged between the lender s software and the attorney s closing software yup! (Have you heard about platforms like RealEC, DocMagic, ELinks and Bee s Path?) 9

10 What questions should you be asking your lenders with regard to the production of the Loan Estimate? Do they have your complete fee schedule, including fees for MLCs, plot plans, recording fees/deed stamps, and title insurance rates? Do they have a list of fee names that will be used on the Loan Estimate and Closing Disclosure or would they like one from you? Ask for a copy of their revised Closing Instructions which will be used for all TRID impacted closings How will you and they exchange data? Miscellaneous Requirements Timeshares: Loans secured by interests in timeshare plans are still subject to the TILA RESPA rule, but because these loans may be consummated within a few days, the CFPB adopted abbreviated timing, delivery, and disclosure obligations for these loans when consummation occurs within 3 business days of the application. For these loans, creditors may forego a Loan Estimate and provide only the Closing Disclosure. In addition, the waiting periods and timing requirements applicable to most TRID loans are inapplicable to loans secured by timeshare interests. Instead, creditors are required to ensure only that the consumer received the Closing Disclosure no later than consummation. For details on timeshare transactions, see Comment 19(f)(1)(iii) 3. Miscellaneous Requirements Imposing a Fee: A creditor or other person may not impose any fee on a consumer in connection with a mortgage application until the consumer has received the Loan Estimate and has indicated intent to proceed with the transaction. This restriction includes limits on imposing: Application fees; Appraisal fees; Underwriting fees; and Other fees imposed on the consumer. The only exception is for a bona fide and reasonable fee for obtaining a consumer s credit report. 10

11 Miscellaneous Requirements Imposing a Fee: A fee is imposed by a person if the person requires a consumer to provide a method for payment, even if the payment is not made at that time. This would include, for example: A creditor or mortgage broker requiring the consumer to provide a check to pay for a processing fee before the consumer receives the Loan Estimate, even if the check is not to be cashed until after the Loan Estimate is received and the consumer has indicated an intent to proceed A creditor or mortgage broker requiring the consumer to provide a credit card number for a processing fee before the consumer receives the Loan Estimate, even if the credit card will not be charge until after the Loan Estimate is received and the consumer has indicated an intent to proceed Miscellaneous Requirements Intent to Proceed: A consumer indicates intent to proceed with the transaction when the consumer communicates, in any manner, that the consumer chooses to proceed after the Loan Estimate has been delivered. This may include: Oral communication in person immediately upon deliver of the Loan Estimate; Oral communication over the phone, written communication via , or signing a pre printed form after receipt of the Loan Estimate A consumer s silence is not indicative of intent to proceed. The creditor must document the communication of intent to proceed in order to satisfy the record retention requirements of the rule. Miscellaneous Requirements Estimates of costs and terms given prior to the Loan Estimate: The rule does not prohibit a creditor or other person from providing a consumer with estimated terms or costs prior to the consumer receiving the Loan Estimate. However, if a person provides a consumer with a written estimate of terms or costs specific to that consumer before the consumer receives the Loan Estimate, theformmaynot have headings, content, and format substantially similar to the Loan Estimate or Closing Disclosure, and it must clearly and conspicuously stateatthetopofthefrontofthefirstpageofthewrittenestimate the following statement in font size no small than 12 point font: Your actual rate, payment, and costs could be higher. Get an official Loan Estimate before choosing the loan. The CFPB has provided a model form see Form H 26 of appendix H to Regulation Z. 11

12 Miscellaneous Requirements Additional verifying information other than the 6 pieces before providing a Loan Estimate: A creditor or other person may not condition providing the Loan Estimate on a consumer submitting document verifying information related to the consumer s mortgage loan application before providing the Loan Estimate. For example: A creditor may ask for the sale price and address of the property, but may not require the consumer to provide a purchase and sale agreement to support the information the consumer provides orally before the creditor provided the Loan Estimate. A mortgage broker may ask for the names, account numbers, and balances of the consumer s checking and savings accounts, but the mortgage broker may not require the consumer to provide bank statements or similar documentation to support the information orally provided by the consumer before the creditor provides the Loan Estimate. Miscellaneous Requirements Special Information Booklet (RESPA Settlement Costs Booklet) Creditors must provide a copy of the special information booklet to consumer who apply for a consumer credit transaction secured by real property, except: If the consumer is applying for a HELOC, the creditor, or mortgage broker, can provide a copy of the brochure entitled When Your Home is On the Line: What You Should Know About Home Equity Lines of Credit instead of the special information booklet The creditor need not provide the special information booklet if the consumer is applying for a real property secured consumer credit transaction that does not have the purpose of purchasing a one to four family residential property, such as a refinancing, a closed end loan secured by a subordinate lien, or a reverse mortgage. Creditors must deliver, or place in the mail, the special information booklet not later than three (3) business days after receiving the consumer s loan application. Miscellaneous Requirements Other Disclosures: Escrow Closing Notice The Escrow Closing Notice must be provided prior to cancelling an escrow account to any consumers for whom an escrow account was established in connection with a closed end consumer credit transaction secured by a first lien on real property or a dwelling, except for reverse mortgages. The creditor or servicer must provide consumers with the notice no later than three (3) business days before the consumer s escrow account is cancelled. (See (e)(1) for details about the Notice.) Partial Payment Disclosure If a lender or servicer is required by the existing Regulation Z to provide mortgage transfer notices when the ownership of a mortgage loan is being transferred, that notice must include information related to the partial payment policy that will apply to the mortgage loan. This post consummation partial payment disclosure is required for a closed end consumer credit transaction secured by a dwelling or real property, other than a reverse mortgage. (See (d)(5) for details about the Disclosure.) 12

13 Miscellaneous Requirements Practical Implementation and Compliance Issues: Identify all affected staff and determine training needs closing and post closing staff and processes are likely to be most broadly impacted by the rule changes Review your technology platforms hardware and software may need to be updated Educate your buyers, sellers and realtors by walking them through the transaction timeline (see chart on next slide) encourage them to review the P&S to be sure that amendments and extensions comply and to obtain payoffs and final readings as early in the transaction as possible Miscellaneous Requirements Questions to Ask Your Lenders: Who is preparing the Closing Disclosure? If they are, how do they want you to provide data through a portal, by , by mail or hand delivery? If you are preparing it, how will they get their information to you? How will they send the completed Closing Disclosure to you for approval before delivery to the consumer? How will the Closing Disclosure be delivered to the consumer? How will changes be made to the Closing Disclosure after it is provided to the borrower? 13

14 Questions? About our Companies Fidelity National Financial, Inc. (FNF), is a leading provider of title insurance, technology and transaction services to the real estate and mortgage industries. It is a Fortune 500 company, currently listed at #314. Fidelity National Title Group (FNTG), a subsidiary of FNF, provides title insurance and escrow services. Its underwriters, which include Chicago Title Insurance Company and Commonwealth Land Title Insurance Company, issue approximately half of the title insurance policies in the United States. 14

, a subsidiary of FNF, provides title insurance and escrow services.")

When do I have to start following the TILA-RESPA rule and using the new Integrated Disclosures?

............................................................................................. Overview of the TILA-RESPA Rule.............................................................................................

............................................................................................. Overview of the TILA-RESPA Rule.............................................................................................

FRESH. Agenda. Credit Union Integrated Mortgage Disclosures Are you Prepared?

MCUL & Affiliates 2015 Annual Convention and Exposition Credit Union Integrated Mortgage Disclosures Are you Prepared? Glory LeDu Thursday, June 4, 2015 2:00 p.m. Sponsored by: FRESH Ideas to Reinvent

MCUL & Affiliates 2015 Annual Convention and Exposition Credit Union Integrated Mortgage Disclosures Are you Prepared? Glory LeDu Thursday, June 4, 2015 2:00 p.m. Sponsored by: FRESH Ideas to Reinvent

TILA-RESPA Integrated Disclosures

Outlook Live Webinar- June 17, 2014 TILA-RESPA Integrated Disclosures Presented by the Consumer Financial Protection Bureau Visit us at www.consumercomplianceoutlook.org Disclaimer The Bureau issued the

Outlook Live Webinar- June 17, 2014 TILA-RESPA Integrated Disclosures Presented by the Consumer Financial Protection Bureau Visit us at www.consumercomplianceoutlook.org Disclaimer The Bureau issued the

TILA-RESPA Integrated Disclosure Rule * January 21, 2015

TILA-RESPA Integrated Disclosure Rule * January 21, 2015 Presented by David Kantor Stinson Leonard Street LLP David.kantor@stinsonleonard.com 612-335-1620 1. Effective Date. The new Integrated Disclosures

TILA-RESPA Integrated Disclosure Rule * January 21, 2015 Presented by David Kantor Stinson Leonard Street LLP David.kantor@stinsonleonard.com 612-335-1620 1. Effective Date. The new Integrated Disclosures

TILA/RESPA Integrated Disclosures. BRIAN A. NETTLEINGHAM Attorney/Shareholder Regulatory Compliance Group

TILA/RESPA Integrated Disclosures BRIAN A. NETTLEINGHAM Attorney/Shareholder Regulatory Compliance Group BACKGROUND Dodd-Frank Wall Street Reform Act Created the Consumer Financial Protection Bureau National

TILA/RESPA Integrated Disclosures BRIAN A. NETTLEINGHAM Attorney/Shareholder Regulatory Compliance Group BACKGROUND Dodd-Frank Wall Street Reform Act Created the Consumer Financial Protection Bureau National

CFPB Integrated Mortgage Disclosures

CFPB Integrated Mortgage Disclosures Today s Goal To help you not only understand the rule changes, but make sure you have the tools, resources and support to take action to implement in your credit union

CFPB Integrated Mortgage Disclosures Today s Goal To help you not only understand the rule changes, but make sure you have the tools, resources and support to take action to implement in your credit union

General Resources CFPB Resources ALTA Best Practices Closing Insight Notaries Business & Commercial Loans Foreign Consumers

Remember, a knowing or reckless violation of TRID, even if done under instructions from the lender, may result in penalties of up to $1 million a day per violation against the individual settlement agent.

Remember, a knowing or reckless violation of TRID, even if done under instructions from the lender, may result in penalties of up to $1 million a day per violation against the individual settlement agent.

2015 Fidelity National Title Group

Five Things You Need to Know Before August 2015 WHAT IS THE CFPB? THE NEW LINGO Dodd-Frank Act --Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 CFPB Consumer Financial Protection Bureau

Five Things You Need to Know Before August 2015 WHAT IS THE CFPB? THE NEW LINGO Dodd-Frank Act --Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 CFPB Consumer Financial Protection Bureau

January 20, 2015 Updated Changes:

Get Ready! Get Set! August 1, 2015 is Around the Corner THE COMBINED TILA AND RESPA MORTGAGE DISCLOSURES (Memo Updated on 1/27/15 to include the changes below) As most of you are probably aware, a major

Get Ready! Get Set! August 1, 2015 is Around the Corner THE COMBINED TILA AND RESPA MORTGAGE DISCLOSURES (Memo Updated on 1/27/15 to include the changes below) As most of you are probably aware, a major

Home Mortgage Loan Tips: TILA-RESPA Integrated Disclosures

PLEASE STAND BY Your webinar is about to begin. pncmortgage.com/agentalliance 1 2015 Home Lending Changes New Mortgage Rules Demystified: TILA RESPA Integrated Disclosures (TRID) Welcome to the webinar!

PLEASE STAND BY Your webinar is about to begin. pncmortgage.com/agentalliance 1 2015 Home Lending Changes New Mortgage Rules Demystified: TILA RESPA Integrated Disclosures (TRID) Welcome to the webinar!

TRID. What are the Timing Requirements for Revisions to a Loan Estimate?

TRID What is TRID? TRID is an acronym for TILA- RESPA Integrated Disclosure (also referred to as the TILA-RESPA Rule) and applies to most closed-end Borrower credit transactions secured by real property.

TRID What is TRID? TRID is an acronym for TILA- RESPA Integrated Disclosure (also referred to as the TILA-RESPA Rule) and applies to most closed-end Borrower credit transactions secured by real property.

Loan Estimate (LE) TILA-RESPA Integrated Disclosure (TRID) Rule Requirements

TILA-RESPA Integrated Disclosure (TRID) Rule Requirements") Loan Estimate (LE) TILA-RESPA Integrated Disclosure (TRID) Rule Requirements New Definitions; New Forms New Work Flow New Rule creates new definition of Covered Loan Loan Application Consummation (Closing)

Loan Estimate (LE) TILA-RESPA Integrated Disclosure (TRID) Rule Requirements New Definitions; New Forms New Work Flow New Rule creates new definition of Covered Loan Loan Application Consummation (Closing)

bankerstitleshenandoah.com 1.888.259.7184

Delivered in partnership with your local title and settlement agency bankerstitleshenandoah.com 1.888.259.7184 About this Manual In an effort to provide a thorough condensed training reference, this manual

Delivered in partnership with your local title and settlement agency bankerstitleshenandoah.com 1.888.259.7184 About this Manual In an effort to provide a thorough condensed training reference, this manual

TILA RESPA Procedural Impacts Are You Ready? Presenters. CUNA Mutual Group 2015 All rights reserved. 1. July 7, 2015

Presented by: TILA RESPA Procedural Impacts Presenters Jon Bundy Regulatory Compliance Manager CUNA Mutual Group 608-665-7101 jonathan.bundy@cunamutual.com Theresa Reinke LOANLINER Compliance Consultant

Presented by: TILA RESPA Procedural Impacts Presenters Jon Bundy Regulatory Compliance Manager CUNA Mutual Group 608-665-7101 jonathan.bundy@cunamutual.com Theresa Reinke LOANLINER Compliance Consultant

INTEGRATED MORTGAGE DISCLOSURES CLOSING DISCLOSURE

INTEGRATED MORTGAGE DISCLOSURES TILA RESPA RULE CLOSING DISCLOSURE Financial Solutions Patti Blenden October 2014 1 September 2014 Guide The Loan Estimate and Closing Disclosure must be used for most closed

INTEGRATED MORTGAGE DISCLOSURES TILA RESPA RULE CLOSING DISCLOSURE Financial Solutions Patti Blenden October 2014 1 September 2014 Guide The Loan Estimate and Closing Disclosure must be used for most closed

Overview The Regulation The Loan Estimate (LE) The Closing Disclosure (CD) Loan Estimate (LE) Application Date LE Responsibility

The Closing Disclosure (CD) Loan Estimate (LE) Application Date LE Responsibility") To support your preparation efforts when implementing the TILA-RESPA Integrated Disclosure (TRID) rule effective for applications dated on or after October 3, 2015, we have created this Helpful Tips for

To support your preparation efforts when implementing the TILA-RESPA Integrated Disclosure (TRID) rule effective for applications dated on or after October 3, 2015, we have created this Helpful Tips for

Know Before You Owe. TILA-RESPA Integrated Disclosure (TRID) Rule

Rule") Know Before You Owe TILA-RESPA Integrated Disclosure (TRID) Rule Background of CFPB The Consumer Financial Protection Bureau (CFPB) was established in 2010 under the Dodd-Frank Act Directed to publish

Know Before You Owe TILA-RESPA Integrated Disclosure (TRID) Rule Background of CFPB The Consumer Financial Protection Bureau (CFPB) was established in 2010 under the Dodd-Frank Act Directed to publish

A Primer on the New CFPB Regulations Governing Residential Closings. Navigating the New Forms (Loan Estimate and Closing Disclosure.

A Primer on the New CFPB Regulations Governing Residential Closings. Navigating the New Forms (Loan Estimate and Closing Disclosure.) For loan applications received beginning October 3, 2015. Disclaimer:

A Primer on the New CFPB Regulations Governing Residential Closings. Navigating the New Forms (Loan Estimate and Closing Disclosure.) For loan applications received beginning October 3, 2015. Disclaimer:

PRMG is Ramping Up for the TILA RESPA Rule

PRMG is Ramping Up for the TILA RESPA Rule Paramount Residential Mortgage Group, Inc. (PRMG) is ramping up for the new TILA RESPA rule. Effective with applications taken on or after August 1, 2015, lenders

PRMG is Ramping Up for the TILA RESPA Rule Paramount Residential Mortgage Group, Inc. (PRMG) is ramping up for the new TILA RESPA rule. Effective with applications taken on or after August 1, 2015, lenders

CLARIFICATION OF MAJOR CHANGES. Integrated Mortgage Disclosures

CLARIFICATION OF MAJOR CHANGES Integrated Mortgage Disclosures One of the mortgage industry s most anticipated provisions of the Dodd-Frank Act has been the integration of the Truth-in-Lending Act (TILA)

CLARIFICATION OF MAJOR CHANGES Integrated Mortgage Disclosures One of the mortgage industry s most anticipated provisions of the Dodd-Frank Act has been the integration of the Truth-in-Lending Act (TILA)

PART 2: THE LOAN ESTIMATE. Integrated Disclosures Rule Effective August 1, 2015

PART 2: THE LOAN ESTIMATE Integrated Disclosures Rule Effective August 1, 2015 1 Thank you for your time today! Integrated Disclosures Webinar Series brought to you by HomeBridge Wholesale Visit: www.homebridgewholesale.com

PART 2: THE LOAN ESTIMATE Integrated Disclosures Rule Effective August 1, 2015 1 Thank you for your time today! Integrated Disclosures Webinar Series brought to you by HomeBridge Wholesale Visit: www.homebridgewholesale.com

Answer: ppddocs.com we don t endorse this site or this product, it is just a site we used to input examples for the webinar

BAI Learning & Development Webinar Q&A TILA-RESPA Integration Part 1 A New Way to Disclose 1. How should we handle Lender Paid Fees? Since we have to send the Loan Estimate 3 days after application, we

BAI Learning & Development Webinar Q&A TILA-RESPA Integration Part 1 A New Way to Disclose 1. How should we handle Lender Paid Fees? Since we have to send the Loan Estimate 3 days after application, we

TILA-RESPA INTEGRATED DISCLOSURE (TRID) AT A GLANCE COPYRIGHT 2015 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

AT A GLANCE COPYRIGHT 2015 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED") TILA-RESPA INTEGRATED DISCLOSURE (TRID) AT A GLANCE Last Revised: 8/28/2015 TABLE OF CONTENTS What is TRID?...3 Forms...4-7 - Loan Estimate - Closing Disclosure - Change of Circumstance Delivery Methods

TILA-RESPA INTEGRATED DISCLOSURE (TRID) AT A GLANCE Last Revised: 8/28/2015 TABLE OF CONTENTS What is TRID?...3 Forms...4-7 - Loan Estimate - Closing Disclosure - Change of Circumstance Delivery Methods

CFPB THE NEW DISCLOSURE FORMS AND REQUIREMENTS BE READY!!

CFPB THE NEW DISCLOSURE FORMS AND REQUIREMENTS BE READY!! CELIA C. FLOWERS FLOWERS DAVIS, P.L.L.C. and EAST TEXAS TITLE COMPANY Tyler, Texas 75701 TILA and RESPA History 2012 TEXAS LAND TITLE INSTITUTE

CFPB THE NEW DISCLOSURE FORMS AND REQUIREMENTS BE READY!! CELIA C. FLOWERS FLOWERS DAVIS, P.L.L.C. and EAST TEXAS TITLE COMPANY Tyler, Texas 75701 TILA and RESPA History 2012 TEXAS LAND TITLE INSTITUTE

TRID Quick Reference Guide

TRID General Rules and Definitions New Required Disclosures Loan Estimate (LE) replaces the GFE and Initial TIL Closing Disclosure (CD) replaces the Final TIL and HUD-1 Home Loan Toolkit replaces the HUD

TRID General Rules and Definitions New Required Disclosures Loan Estimate (LE) replaces the GFE and Initial TIL Closing Disclosure (CD) replaces the Final TIL and HUD-1 Home Loan Toolkit replaces the HUD

Chapter 5: Completing Pages Four and Five of the Closing Disclosure... 35 Summary... 42

Table of Contents The Integrated Disclosure Rule... 4 Chapter 1: Introduction to the Integrated Disclosure Rule... 5 Consolidated Disclosures... 5 Chapter 2: Delivery of the Loan Estimate and Closing Disclosure...

Table of Contents The Integrated Disclosure Rule... 4 Chapter 1: Introduction to the Integrated Disclosure Rule... 5 Consolidated Disclosures... 5 Chapter 2: Delivery of the Loan Estimate and Closing Disclosure...

TILA-RESPA Integrated Disclosure rule. Small entity compliance guide

TILA-RESPA Integrated Disclosure rule Small entity compliance guide September 2014 Version Log The Bureau updates this guide on a periodic basis to reflect finalized clarifications to the rule which impacts

TILA-RESPA Integrated Disclosure rule Small entity compliance guide September 2014 Version Log The Bureau updates this guide on a periodic basis to reflect finalized clarifications to the rule which impacts

TILA-RESPA Integrated Disclosure rule. Small entity compliance guide

TILA-RESPA Integrated Disclosure rule Small entity compliance guide March 2014 Table of contents Table of contents... 2 1. Introduction... 10 1.1 What is the purpose of this guide?... 11 1.2 Who should

TILA-RESPA Integrated Disclosure rule Small entity compliance guide March 2014 Table of contents Table of contents... 2 1. Introduction... 10 1.1 What is the purpose of this guide?... 11 1.2 Who should

QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS)

(CLOSED-END HOME MORTGAGE TRANSACTIONS)") QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS) Type of (2) Contents of Truth in Lending Statements 226.17 226.36 Early s 226.19(a)(1)

QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS) Type of (2) Contents of Truth in Lending Statements 226.17 226.36 Early s 226.19(a)(1)

Brief Walk Through of TRID. Presented by: Scott Meerstein MGIC Inside Sales

Brief Walk Through of TRID Presented by: Scott Meerstein MGIC Inside Sales The information presented in this presentation is for general information only, and is based on guidelines and practices generally

Brief Walk Through of TRID Presented by: Scott Meerstein MGIC Inside Sales The information presented in this presentation is for general information only, and is based on guidelines and practices generally

CFPB s RESPA TILA Integrated Disclosure. Finley P. Maxson NAR Senior Counsel fmaxson@realtors.org (312) 329-8381

329-8381") CFPB s RESPA TILA Integrated Disclosure Finley P. Maxson NAR Senior Counsel fmaxson@realtors.org (312) 329-8381 RESPA-TILA Integrated Disclosure A. Background I. Impetus for change a. Dodd-Frank directed

CFPB s RESPA TILA Integrated Disclosure Finley P. Maxson NAR Senior Counsel fmaxson@realtors.org (312) 329-8381 RESPA-TILA Integrated Disclosure A. Background I. Impetus for change a. Dodd-Frank directed

NORTH AMERICAN TITLE COMPANY Like Clockwork. www.nat.com/cfpb

NORTH AMERICAN TITLE COMPANY Like Clockwork www.nat.com/cfpb UNDERSTANDING THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE FORMS American Title, we want to make sure all of our customers have the information

NORTH AMERICAN TITLE COMPANY Like Clockwork www.nat.com/cfpb UNDERSTANDING THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE FORMS American Title, we want to make sure all of our customers have the information

CUNA s COMPLIANCE HIGHLIGHTS

CUNA s COMPLIANCE HIGHLIGHTS TILA/RESPA INTEGRATED MORTGAGE DISCLOSURES For more than 30 years, Federal law has required lenders to provide two different disclosure forms to consumers applying for a mortgage.

CUNA s COMPLIANCE HIGHLIGHTS TILA/RESPA INTEGRATED MORTGAGE DISCLOSURES For more than 30 years, Federal law has required lenders to provide two different disclosure forms to consumers applying for a mortgage.

Update on CFPB s TILA- RESPA Integrated Disclosure Rule

Update on CFPB s TILA- RESPA Integrated Disclosure Rule Mortgage Bankers Ruth A. Dillingham, Special Counsel First American Title Insurance Company This presentation is for informational purposes only

Update on CFPB s TILA- RESPA Integrated Disclosure Rule Mortgage Bankers Ruth A. Dillingham, Special Counsel First American Title Insurance Company This presentation is for informational purposes only

TILA-RESPA Integrated Disclosure (TRID) Correspondent Division. Overview. Loan Estimate (LE) Key points. Topic The Regulation

Correspondent Division. Overview. Loan Estimate (LE) Key points. Topic The Regulation") Overview The Regulation The Consumer Financial Protection Bureau (CFPB) issued a final rule amending Regulation Z (Truth in Lending Act) and Regulation X (Real Estate Settlement Procedures Act) to integrate

Overview The Regulation The Consumer Financial Protection Bureau (CFPB) issued a final rule amending Regulation Z (Truth in Lending Act) and Regulation X (Real Estate Settlement Procedures Act) to integrate

INTEGRATED MORTGAGE DISCLOSURES

INTEGRATED MORTGAGE DISCLOSURES (TILA RESPA RULE) Financial Solutions Patti Blenden April 2015 1 CFPB Accomplishes Integration of GFE/eTILA After 30 years of encouraging HUD and the FRB to cooperate Dodd

INTEGRATED MORTGAGE DISCLOSURES (TILA RESPA RULE) Financial Solutions Patti Blenden April 2015 1 CFPB Accomplishes Integration of GFE/eTILA After 30 years of encouraging HUD and the FRB to cooperate Dodd

TILA RESPA An Overview

TILA RESPA An Overview March 13, 2014 E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. and Michael J. Coleman, Esq. NAFCU Director of Regulatory Affairs E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. 150

TILA RESPA An Overview March 13, 2014 E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. and Michael J. Coleman, Esq. NAFCU Director of Regulatory Affairs E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. 150

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures. Michelle L. Korsmo Chief Executive Officer Steven Gottheim Counsel

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures Michelle L. Korsmo Chief Executive Officer Steven Gottheim Counsel Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures Michelle L. Korsmo Chief Executive Officer Steven Gottheim Counsel Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

Tony Hernandez /s/ Tony Hernandez Administrator Housing and Community Facilities Programs

October 6, 2016 TO: State Directors Rural Development ATTN: Program Directors Single Family Housing FROM: Tony Hernandez /s/ Tony Hernandez Administrator Housing and Community Facilities Programs SUBJECT:

October 6, 2016 TO: State Directors Rural Development ATTN: Program Directors Single Family Housing FROM: Tony Hernandez /s/ Tony Hernandez Administrator Housing and Community Facilities Programs SUBJECT:

TILA-RESPA Integrated Disclosure Rule

TILA-RESPA Integrated Disclosure Rule May 13, 2015 Joseph J. Reilly Partner Benjamin K. Olson Partner 1 Key Changes Effective for applications received by the creditor or mortgage broker on or after August

TILA-RESPA Integrated Disclosure Rule May 13, 2015 Joseph J. Reilly Partner Benjamin K. Olson Partner 1 Key Changes Effective for applications received by the creditor or mortgage broker on or after August

How To Write A Disclosure Form

Office of Consumer Protection Truth-In-Lending Real Estate Settlement Procedures Act Integrated Disclosures Webinar February 11, 2015 The information contained in this presentation is for informational

Office of Consumer Protection Truth-In-Lending Real Estate Settlement Procedures Act Integrated Disclosures Webinar February 11, 2015 The information contained in this presentation is for informational

TRID FAQ TILA/RESPA Integrated Disclosure Frequently Asked Questions

TRID FAQ TILA/RESPA Integrated Disclosure Frequently Asked Questions 242 W. SUNSET, STE.201 SAN ANTONIO, TX 78209 210-828-5844 DOCS@BAIRDLAW.COM Table of Contents GENERAL QUESTIONS... 3 1. What is TRID?...

TRID FAQ TILA/RESPA Integrated Disclosure Frequently Asked Questions 242 W. SUNSET, STE.201 SAN ANTONIO, TX 78209 210-828-5844 DOCS@BAIRDLAW.COM Table of Contents GENERAL QUESTIONS... 3 1. What is TRID?...

THE NEW TILA/RESPA INTEGRATED DISCLOSURES

THE NEW TILA/RESPA INTEGRATED DISCLOSURES IN PLAIN ENGLISH TRID Workshop Finals E F F E C T I V E A U G U S T 1, 2 0 1 5 *PROPOSAL PENDING TO DELAY EFFECTIVE DATE UNTIL OCTOBER 3RD, 2015 WHAT YOU WILL

THE NEW TILA/RESPA INTEGRATED DISCLOSURES IN PLAIN ENGLISH TRID Workshop Finals E F F E C T I V E A U G U S T 1, 2 0 1 5 *PROPOSAL PENDING TO DELAY EFFECTIVE DATE UNTIL OCTOBER 3RD, 2015 WHAT YOU WILL

Welcome! Thank you for joining the NYCB Gemstone Loan Estimate Process training presentation.

Welcome! Hello, Thank you for joining the NYCB Gemstone Loan Estimate Process training presentation. We will start the session shortly. Please note that all participants will be muted upon entry of the

Welcome! Hello, Thank you for joining the NYCB Gemstone Loan Estimate Process training presentation. We will start the session shortly. Please note that all participants will be muted upon entry of the

Regulation X Real Estate Settlement Procedures Act

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the act) became effective on June 20, 1975. The act requires lenders,

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the act) became effective on June 20, 1975. The act requires lenders,

How To Serve A Mortgage In The United States

Break Out Session: Mortgage Loan Servicing and Administration 2 Agenda Mortgage Servicing Rules (Real Estate Settlement Procedures Act [RESPA] and Truth in Lending Act [TILA]) Effective Date: Applications

Break Out Session: Mortgage Loan Servicing and Administration 2 Agenda Mortgage Servicing Rules (Real Estate Settlement Procedures Act [RESPA] and Truth in Lending Act [TILA]) Effective Date: Applications

The Closing Disclosure

The Closing Disclosure Overview: The new TRID Regulation is effective for applications taken on October 3, 2015 and after. As a result, the GFE, TIL, and HUD-1 will no longer be issued. The Loan Estimate

The Closing Disclosure Overview: The new TRID Regulation is effective for applications taken on October 3, 2015 and after. As a result, the GFE, TIL, and HUD-1 will no longer be issued. The Loan Estimate

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015. Presenter: Bonnie S. Nachamie

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015 Presenter: Bonnie S. Nachamie The Closing Disclosure ( CD ) is the new form that amends, enhances and replaces the Final TIL and HUD-1 The

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015 Presenter: Bonnie S. Nachamie The Closing Disclosure ( CD ) is the new form that amends, enhances and replaces the Final TIL and HUD-1 The

TILA RESPA One of the Most Expensive Changes in Decades

Veronese 2405 Wednesday, July 23, 2014 1:00 2:00 p.m.; 2:15 3:15 p.m. TILA RESPA One of the Most Expensive Changes in Decades E. Andrew Keeney, Esq., Partner, Kaufman & Canoles, P.C. 1 TILA RESPA One of

Veronese 2405 Wednesday, July 23, 2014 1:00 2:00 p.m.; 2:15 3:15 p.m. TILA RESPA One of the Most Expensive Changes in Decades E. Andrew Keeney, Esq., Partner, Kaufman & Canoles, P.C. 1 TILA RESPA One of

TILA-RESPA INTEGRATED MORTGAGE DISCLOSURES

TILA-RESPA INTEGRATED MORTGAGE DISCLOSURES Explaining the New Rule History Timing Purpose Coverage? Changes Definition of an Application Loan Estimate Closing Disclosure Variations/Tolerances 5 Things

TILA-RESPA INTEGRATED MORTGAGE DISCLOSURES Explaining the New Rule History Timing Purpose Coverage? Changes Definition of an Application Loan Estimate Closing Disclosure Variations/Tolerances 5 Things

Changes to Mortgage Loan Closing Process

Changes to Mortgage Loan Closing Process 2015 Iowa Title Guaranty Settlement Conference Presented by: Ronette Schlatter, CRCM 1 Background Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA)

Changes to Mortgage Loan Closing Process 2015 Iowa Title Guaranty Settlement Conference Presented by: Ronette Schlatter, CRCM 1 Background Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA)

A Primer for a New Era in Closings: For loan applications received beginning August 1, 2015 some info courtesy of ALTA

A Primer for a New Era in Closings: For loan applications received beginning August 1, 2015 some info courtesy of ALTA A New Era in Closings Applicable Loans Final rule applies to most consumer mortgages,

A Primer for a New Era in Closings: For loan applications received beginning August 1, 2015 some info courtesy of ALTA A New Era in Closings Applicable Loans Final rule applies to most consumer mortgages,

Wells Fargo Settlement Agent Communications

Wells Fargo Settlement Agent Communications News for Wells Fargo Settlement Agents September 14, 2015 Wells Fargo says thank you! When the Consumer Financial Protection Bureau (CFPB) announced the TILA

Wells Fargo Settlement Agent Communications News for Wells Fargo Settlement Agents September 14, 2015 Wells Fargo says thank you! When the Consumer Financial Protection Bureau (CFPB) announced the TILA

CFPB Proposes New Mortgage Disclosure Rules

A DV I S O RY July 2012 On July 9, 2012, the Bureau of Consumer Financial Protection (CFPB) issued a proposed rule on mortgage disclosures (Proposed Rule) implementing requirements of the Dodd-Frank Wall

A DV I S O RY July 2012 On July 9, 2012, the Bureau of Consumer Financial Protection (CFPB) issued a proposed rule on mortgage disclosures (Proposed Rule) implementing requirements of the Dodd-Frank Wall

TILA/RESPA Integrated Disclosure (TRID) Rule

Rule") TILA/RESPA Integrated Disclosure (TRID) Rule Ken Markison, Vice President, Regulatory Counsel, MBA Jerra H. Ryan, Vice President of Compliance, Cherry Creek Mortgage Alex Karram, Attorney, Weiner Brodsky

TILA/RESPA Integrated Disclosure (TRID) Rule Ken Markison, Vice President, Regulatory Counsel, MBA Jerra H. Ryan, Vice President of Compliance, Cherry Creek Mortgage Alex Karram, Attorney, Weiner Brodsky

CFPB Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

FAQs About RESPA for Industry

FAQs About RESPA for Industry 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien (first or subordinate

FAQs About RESPA for Industry 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien (first or subordinate

YOUR NEW MORTGAGE DISCLOSURE FORMS - AN IN-DEPTH LOOK FIS REGULATORY ADVISORY SERVICES

YOUR NEW MORTGAGE DISCLOSURE FORMS - AN IN-DEPTH LOOK BY FIS REGULATORY ADVISORY SERVICES 92012 Your New Mortgage Disclosure Forms An In Depth Look www.fisregulatoryservices.com i 1 Agenda Introduction

YOUR NEW MORTGAGE DISCLOSURE FORMS - AN IN-DEPTH LOOK BY FIS REGULATORY ADVISORY SERVICES 92012 Your New Mortgage Disclosure Forms An In Depth Look www.fisregulatoryservices.com i 1 Agenda Introduction

Upon completion you will be able to:

Agenda This training manual consists of three parts that will provide you with step-bystep instructions about how to complete the Closing Disclosure form required by the Integrated Disclosures Rule Upon

Agenda This training manual consists of three parts that will provide you with step-bystep instructions about how to complete the Closing Disclosure form required by the Integrated Disclosures Rule Upon

UNDERSTANDING THE LOAN ESTIMATE

The following breaks down the Loan Estimate by section with examples from Encompass followed by official commentary. Also attached, is a copy of a completed Loan Estimate form provided by the Encompass..

The following breaks down the Loan Estimate by section with examples from Encompass followed by official commentary. Also attached, is a copy of a completed Loan Estimate form provided by the Encompass..

Understanding the CFPB s TILA-RESPA Integrated Disclosures. Marvin Stone SVP, Business Integration CFPB Program Manager Stewart Title Guaranty Corp.

Understanding the CFPB s TILA-RESPA Integrated Disclosures Marvin Stone SVP, Business Integration CFPB Program Manager Stewart Title Guaranty Corp. A Brief History. Truth-in-Lending Act (TILA) of 1968

Understanding the CFPB s TILA-RESPA Integrated Disclosures Marvin Stone SVP, Business Integration CFPB Program Manager Stewart Title Guaranty Corp. A Brief History. Truth-in-Lending Act (TILA) of 1968

Important Information Regarding TILA-RESPA Integrated Disclosure (TRID) Rule

Rule") Important Information Regarding TILA-RESPA Integrated Disclosure (TRID) Rule Notice to students: If your course contains information on the Truth in Lending Act (TILA) and the Real Estate Settlement Procedure

Important Information Regarding TILA-RESPA Integrated Disclosure (TRID) Rule Notice to students: If your course contains information on the Truth in Lending Act (TILA) and the Real Estate Settlement Procedure

TRID In the Weeds. Article by Alice Alvey January 2015

TRID In the Weeds Article by Alice Alvey January 2015 TRID BY ALICE ALVEY Alice Alvey It s not easy to see into the weeds of this regulation by attending a few webinars. It takes hundreds of man-hours

TRID In the Weeds Article by Alice Alvey January 2015 TRID BY ALICE ALVEY Alice Alvey It s not easy to see into the weeds of this regulation by attending a few webinars. It takes hundreds of man-hours

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS The following are instructions for completing the HUD-1 settlement statement,

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS The following are instructions for completing the HUD-1 settlement statement,

Overview. General Requirements

Truth in Lending Act Overview Congress passed legislation increasing the amount and type of credit information disclosed to the consumer through Title I of the Consumer Credit Protection Act of 1968, known

Truth in Lending Act Overview Congress passed legislation increasing the amount and type of credit information disclosed to the consumer through Title I of the Consumer Credit Protection Act of 1968, known

CFPB and Lenders. A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry

CFPB and Lenders A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry What is the Consumer Financial Protection Bureau (CFPB)? Independent agency of the United

CFPB and Lenders A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry What is the Consumer Financial Protection Bureau (CFPB)? Independent agency of the United

7 business days after loan estimate delivery is the waiting period for consummation (loan closing) after the Loan Estimate Delivery

after the Loan Estimate Delivery") TRID INFORMATION Delivery of the Loan Estimate The Loan Estimate must be placed in the mail or delivered no later than 3 business days after TRID application is submitted. Helpful Hint: Business days for

TRID INFORMATION Delivery of the Loan Estimate The Loan Estimate must be placed in the mail or delivered no later than 3 business days after TRID application is submitted. Helpful Hint: Business days for

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate.

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate. General Information Page 1 Date Issued Date the LE is mailed or delivered

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate. General Information Page 1 Date Issued Date the LE is mailed or delivered

Key Components of TRID. Presented by: Benjamin K. Olson

Key Components of TRID Presented by: Benjamin K. Olson 1 TRID Effective Date and Enforcement June 17, 2015: CFPB Press Release CFPB Director announces proposal to delay effective date until October 1:

Key Components of TRID Presented by: Benjamin K. Olson 1 TRID Effective Date and Enforcement June 17, 2015: CFPB Press Release CFPB Director announces proposal to delay effective date until October 1:

Provident Bank Mortgage Wholesale Operations FAQ s on TRID

Provident Bank Mortgage Wholesale Operations FAQ s on TRID General 1) Q: Can an email or other communication to the borrower provide a list of standard items that will be needed for the application (income/asset

Provident Bank Mortgage Wholesale Operations FAQ s on TRID General 1) Q: Can an email or other communication to the borrower provide a list of standard items that will be needed for the application (income/asset

Mission: to make markets for consumer financial products and services work for Americans.

TRID with Norman Roos, Robinson and Cole LLP William McCue, McCue Mortgage Company Lawrence Garfinkel, Hunt Leibert Jacobson P.C. Jeremy Potter, Norcom Mortgage Agenda Introduction Overview and Framework

TRID with Norman Roos, Robinson and Cole LLP William McCue, McCue Mortgage Company Lawrence Garfinkel, Hunt Leibert Jacobson P.C. Jeremy Potter, Norcom Mortgage Agenda Introduction Overview and Framework

ADVISORY MEMORANDUM KATHY BURNS, DIRECTOR OF HOMEOWNERSHIP COMPLIANCE DOCUMENTATION REQUIREMENTS

ADVISORY MEMORANDUM TO: FROM: ALL MASSHOUSING LENDERS KATHY BURNS, DIRECTOR OF HOMEOWNERSHIP DATE: NOVEMBER 15, 2010 RE: COMPLIANCE DOCUMENTATION REQUIREMENTS The purpose of this Advisory is to provide

ADVISORY MEMORANDUM TO: FROM: ALL MASSHOUSING LENDERS KATHY BURNS, DIRECTOR OF HOMEOWNERSHIP DATE: NOVEMBER 15, 2010 RE: COMPLIANCE DOCUMENTATION REQUIREMENTS The purpose of this Advisory is to provide

standard mandated forms, and the font size, labels and other text on the blank forms cannot be changed. Comment 1 to Section 1026.

TILA-RESPA Integrated Disclosures Frequently Asked Questions Outlook Live Webinar May 26, 2015 Presented by the Consumer Financial Protection Bureau (CFPB) Transcribed and Edited by the American Bankers

TILA-RESPA Integrated Disclosures Frequently Asked Questions Outlook Live Webinar May 26, 2015 Presented by the Consumer Financial Protection Bureau (CFPB) Transcribed and Edited by the American Bankers

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

Reference for Closing Agents To Provide to Lender Customers. Excerpts from RESPA Rules and FAQ s

Reference for Closing Agents To Provide to Lender Customers Excerpts from RESPA Rules and FAQ s This Reference document may assist closing agents as it includes frequently asked questions related to compliant

Reference for Closing Agents To Provide to Lender Customers Excerpts from RESPA Rules and FAQ s This Reference document may assist closing agents as it includes frequently asked questions related to compliant

CFPB Mortgage Amendments. Get Caught Up!

CFPB Mortgage Amendments Get Caught Up! Agenda HPML Appraisal Requirements High Cost Mortgage QM Points and Fees QM Cure Provision HPML Escrow Requirements HMDA Revisions Loan Estimate Form Closing Disclosure

CFPB Mortgage Amendments Get Caught Up! Agenda HPML Appraisal Requirements High Cost Mortgage QM Points and Fees QM Cure Provision HPML Escrow Requirements HMDA Revisions Loan Estimate Form Closing Disclosure

TILA-RESPA Integrated Mortgage Disclosures

TILA-RESPA Integrated Mortgage Disclosures Supreme Lending 2015 Distribution to the general public is prohibited. This is not considered an advertisement as defined by 12 CFR 226.2(a)(2). Supreme Lending

TILA-RESPA Integrated Mortgage Disclosures Supreme Lending 2015 Distribution to the general public is prohibited. This is not considered an advertisement as defined by 12 CFR 226.2(a)(2). Supreme Lending

The CFPB Finalizes New Mortgage Servicing Rules

A DV I S O RY April 2013 The CFPB Finalizes New Mortgage Servicing Rules On January 17, 2013, the Consumer Financial Protection Bureau (CFPB) finalized rules implementing the mortgage loan servicing requirements

A DV I S O RY April 2013 The CFPB Finalizes New Mortgage Servicing Rules On January 17, 2013, the Consumer Financial Protection Bureau (CFPB) finalized rules implementing the mortgage loan servicing requirements

TRID Overview. Provided by Primary Capital Mortgage. Presented by Stacie Weider, Training Manager

Provided by Primary Capital Mortgage Presented by Stacie Weider, Training Manager What is TRID? TILA RESPA Integrated Disclosure Rule, which is effective October, 3, 2015. History Notes The Goal To provide

Provided by Primary Capital Mortgage Presented by Stacie Weider, Training Manager What is TRID? TILA RESPA Integrated Disclosure Rule, which is effective October, 3, 2015. History Notes The Goal To provide

TRID Settlement Service Provider List (SSP List)

") TRID Settlement Service Provider List (SSP List) Overview The rule permits lenders/mortgage brokers to provide borrowers the ability to select third party service providers. By doing so could favorably

TRID Settlement Service Provider List (SSP List) Overview The rule permits lenders/mortgage brokers to provide borrowers the ability to select third party service providers. By doing so could favorably

Financial Regulatory Reform: The New Rules on Loan Originator Compensation

Financial Regulatory Reform: The New Rules on Loan Originator Compensation 1 Introduction NOTICE: This information is not intended to be used as legal advice to any person or entity. The information contained

Financial Regulatory Reform: The New Rules on Loan Originator Compensation 1 Introduction NOTICE: This information is not intended to be used as legal advice to any person or entity. The information contained

Introduction. The new rules and forms take effect October 3 rd, 2015 for all loan applications submitted on or after that date.

Introduction The new rules and forms take effect October 3 rd, 2015 for all loan applications submitted on or after that date. Phased-in approach: Continue to close out loans in the lender s pipeline using

Introduction The new rules and forms take effect October 3 rd, 2015 for all loan applications submitted on or after that date. Phased-in approach: Continue to close out loans in the lender s pipeline using

TILA-RESPA INTEGRATED DISCLOSURE RULE

TILA-RESPA INTEGRATED DISCLOSURE RULE Speakers: David Baghdady, Assoc. State Counsel/AVP, First American Title Ins. Co. Richard Hogan, Vice President and Associate General Counsel, CATIC Jeremy Potter,

TILA-RESPA INTEGRATED DISCLOSURE RULE Speakers: David Baghdady, Assoc. State Counsel/AVP, First American Title Ins. Co. Richard Hogan, Vice President and Associate General Counsel, CATIC Jeremy Potter,

TRID Consolidated Resources

TRID Consolidated Resources Annotated Forms for TILA RESPA Integrated Disclosure Closing Disclosure. 1 Annotated Forms for TILA RESPA Integrated Disclosure Loan Estimate.2 Closing Disclosure Form.. 3 Loan

TRID Consolidated Resources Annotated Forms for TILA RESPA Integrated Disclosure Closing Disclosure. 1 Annotated Forms for TILA RESPA Integrated Disclosure Loan Estimate.2 Closing Disclosure Form.. 3 Loan

Completing the New HUD-1 Settlement Statement

Completing the New HUD-1 Settlement Statement The new HUD-1 Settlement Statement ( HUD ) is designed to correlate closely to the new GFE, allowing borrowers to see how the estimate settlement costs disclosed

Completing the New HUD-1 Settlement Statement The new HUD-1 Settlement Statement ( HUD ) is designed to correlate closely to the new GFE, allowing borrowers to see how the estimate settlement costs disclosed

The New Mortgage Lending Process: A 2014 Check-Up and 2015 Planning

The New Mortgage Lending Process: A 2014 Check-Up and 2015 Planning Copyright 2012 Tata Consultancy Services Limited No Legal Advice, Opinions, or Services Provided This presentation does not constitute

The New Mortgage Lending Process: A 2014 Check-Up and 2015 Planning Copyright 2012 Tata Consultancy Services Limited No Legal Advice, Opinions, or Services Provided This presentation does not constitute

TILA-RESPA Integrated Mortgage Disclosures

TILA-RESPA Integrated Mortgage Disclosures Supreme Lending NMLS #2129 2015 Distribution to the general public is prohibited. This is not considered an advertisement as defined by 12 CFR 226.2(a)(2). Supreme

TILA-RESPA Integrated Mortgage Disclosures Supreme Lending NMLS #2129 2015 Distribution to the general public is prohibited. This is not considered an advertisement as defined by 12 CFR 226.2(a)(2). Supreme

Webinar Thursday, January 16, 2014 2:00 3:30 pm ET

Webinar Thursday, January 16, 2014 2:00 3:30 pm ET Webinar Thursday, January 16, 2014 2:00 3:30 pm ET Moderator Roger Blauvelt Vice President & National Agency Counsel WFG National Title Insurance Company

Webinar Thursday, January 16, 2014 2:00 3:30 pm ET Webinar Thursday, January 16, 2014 2:00 3:30 pm ET Moderator Roger Blauvelt Vice President & National Agency Counsel WFG National Title Insurance Company

HERE ARE FIVE THINGS YOU WILL NEED TO KNOW BEFORE THE NEW RULES TAKE EFFECT OCTOBER 3, 2015

5 THINGS TO KNOW BEFORE OCTOBER 3RD, 2015 As a result of the 20 financial meltdown, the Consumer Financial Protection Bureau (CFPB) has published a new set of game changing rules and forms that will impact

5 THINGS TO KNOW BEFORE OCTOBER 3RD, 2015 As a result of the 20 financial meltdown, the Consumer Financial Protection Bureau (CFPB) has published a new set of game changing rules and forms that will impact

TRID. Loan Estimate and Closing Disclosure Cross-reference Guide 07.01.2015. 2015 Temenos USA. All rights reserved

TRID T I L A-RESPA INTEGRAT E D D I S C L O S U R E S Loan Estimate and Closing Disclosure Cross-reference Guide 07.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636

TRID T I L A-RESPA INTEGRAT E D D I S C L O S U R E S Loan Estimate and Closing Disclosure Cross-reference Guide 07.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636

The Federal Register published the proposed rule on August 23, 2012.

CFPB Issues Draft RESPA-TILA Proposed Rules On July 9, the Consumer Financial Protection Bureau ( Bureau or CFPB ) released draft proposed rules and model forms that combine the required disclosures under

CFPB Issues Draft RESPA-TILA Proposed Rules On July 9, the Consumer Financial Protection Bureau ( Bureau or CFPB ) released draft proposed rules and model forms that combine the required disclosures under

CUNA s SUMMARY OF THE CFPB s MORTGAGE LENDING RULES Spring 2013

MANDATORY ESCROW ACCOUNTS Effective: June 1, 2013 REGULATION Requires escrow accounts be maintained for five years (rather than the current one year) for higher-priced mortgage loans. A higher-priced mortgage

MANDATORY ESCROW ACCOUNTS Effective: June 1, 2013 REGULATION Requires escrow accounts be maintained for five years (rather than the current one year) for higher-priced mortgage loans. A higher-priced mortgage

Line 1101 is used to record the total for the category of Title services and lender s title insurance. This amount must be listed in the columns.

Lines 1100-1108. This series covers title charges and charges by attorneys and closing or settlement agents. The title charges include a variety of services performed by title companies or others, and

Lines 1100-1108. This series covers title charges and charges by attorneys and closing or settlement agents. The title charges include a variety of services performed by title companies or others, and

CFPB Issues Much Anticipated Final Rules: Ability to Repay, Qualified Mortgages, Escrow Requirements and Homeownership Counseling

CFPB Issues Much Anticipated Final Rules: Ability to Repay, Qualified Mortgages, Escrow Requirements and Homeownership Counseling The Consumer Financial Protection Bureau ( CFPB ) issued their much anticipated

CFPB Issues Much Anticipated Final Rules: Ability to Repay, Qualified Mortgages, Escrow Requirements and Homeownership Counseling The Consumer Financial Protection Bureau ( CFPB ) issued their much anticipated

LOAN ESTIMATE TABLE. Definition of an application that triggers a Loan Estimate

LOAN ESTIMATE TABLE CATEGORY SYNOPSIS TIMING AND DELIVERY Timing & Delivery No later than the third-business-day after receiving the consumer s application. Must also be delivered or placed in the mail

LOAN ESTIMATE TABLE CATEGORY SYNOPSIS TIMING AND DELIVERY Timing & Delivery No later than the third-business-day after receiving the consumer s application. Must also be delivered or placed in the mail

TABLE OF CONTENTS. Form Number Title / Description Page

TABLE OF CONTENTS Form Number Title / Description Page TIME CHART / ROUNDING FORMS LOAN ESTIMATE Loan Estimate and Closing Disclosure Time Chart 1 TILA RESPA Time Chart 3 Loan Estimate Rounding Chart 5

TABLE OF CONTENTS Form Number Title / Description Page TIME CHART / ROUNDING FORMS LOAN ESTIMATE Loan Estimate and Closing Disclosure Time Chart 1 TILA RESPA Time Chart 3 Loan Estimate Rounding Chart 5

Summary of RESPA Rules... 1 Summary of Changes... 2 Required Use... 2 Average Cost Pricing... 3 Calculating the Average Charge...

Summary of RESPA Rules... 1 Summary of Changes... 2 Required Use... 2 Average Cost Pricing... 3 Calculating the Average Charge... 4 Good Faith Estimate... 5 Curing Tolerance Violations... 9 Lenders Disclosure

Summary of RESPA Rules... 1 Summary of Changes... 2 Required Use... 2 Average Cost Pricing... 3 Calculating the Average Charge... 4 Good Faith Estimate... 5 Curing Tolerance Violations... 9 Lenders Disclosure

2015 TILA-RESPA Compliance: Is Your Business Ready?

2015 TILA-RESPA Compliance: Is Your Business Ready? The long-anticipated Truth-in-Lending (TILA), and Real Estate Settlement Procedures Act (RESPA) changes that were finalized in 2013 go into effect this

2015 TILA-RESPA Compliance: Is Your Business Ready? The long-anticipated Truth-in-Lending (TILA), and Real Estate Settlement Procedures Act (RESPA) changes that were finalized in 2013 go into effect this

Are You Ready for TRID? Dodd Frank the CFPB & You Featuring TRID

WELCOME! www.grantsimon.com Are You Ready for TRID? Dodd Frank the CFPB & You Featuring TRID 1 TRID TILA-RESPA INTEGRATED DISCLOSURE Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1 & TIL

WELCOME! www.grantsimon.com Are You Ready for TRID? Dodd Frank the CFPB & You Featuring TRID 1 TRID TILA-RESPA INTEGRATED DISCLOSURE Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1 & TIL

Appendix B: Good Faith Estimate

Appendix B: Good Faith Estimate Good Faith Estimate The Real Estate Settlement Procedures Act, commonly referred to as RESPA, requires that within three business days of receipt of the loan application,

Appendix B: Good Faith Estimate Good Faith Estimate The Real Estate Settlement Procedures Act, commonly referred to as RESPA, requires that within three business days of receipt of the loan application,