Eric P. Wallace, CPA Boyer & Ritter CPAs and Consultants ewallace@cpabr.com

|

|

|

- Merry Bridges

- 8 years ago

- Views:

Transcription

1 Eric P. Wallace, CPA Boyer & Ritter CPAs and Consultants PRIMEGLOBAL 35th ANNUAL TAX CONFERENCE JANUARY 4-7, 2015 NEWPORT COAST, CA

2 TPRs as Finalized Rules and Theories Latest Updates and Evolutions of the TPRs TPR method change requirements Firm Logistics Best Practices, and a Comprehensive case study of an analysis of a taxpayer s depreciation schedule and its required method filings and 481(a) adjustments. 2

")

3 Applicable to you? Yes if you own fixed assets, have depreciation, buy fixed assets, improves or disposes of fixed assets, and/or have material and supplies That includes just about all for profit businesses (and 990Ts if they use federal depreciation rules) 3

4 Circular 230 Specifics Standards with respect to tax returns and documents, affidavits and other papers. (a) Tax returns. (1) A practitioner may not willfully, recklessly, or through gross incompetence (i) Sign a tax return or claim for refund that the practitioner knows or reasonably should know contains a position that (A) Lacks a reasonable basis; (B) Is an unreasonable position as described in section 6694(a)(2) ; or (C) Is a willful attempt by the practitioner to understate the liability for tax or a reckless or intentional disregard of rules or regulations by the practitioner 4

(2) ; or (C) Is a willful attempt by the practitioner to understate the liability for tax or a reckless or intentional disregard of rules or")

5 Regulation Requirements Final Regulations preamble, issued 9/2013 state: The final regulations provide that.. a change to comply with the final regulations is a change in method of accounting to which the provisions of sections 446 and 481 and the accompanying regulations apply. A taxpayer seeking to change to a method of accounting permitted in the final regulations must secure the consent of the Commissioner in accordance with (e) and follow the administrative procedures issued under (e)(3)(ii) for obtaining the Commissioner's consent to change its accounting method. In general, a taxpayer seeking a change in method of accounting to comply with these regulations must take into account a full adjustment under section 481(a). 5

and follow the administrative procedures issued under 1.446-1(e)(3)(ii) for obtaining the Commissioner's consent to change its accounting method.")

6 Regulation Required Dates: General statement for the applicable sections state the following: (e) Effective/applicability date (1) In general. This section applies to taxable years beginning on or after January 1,

7 Regulation Required Dates: Then if these are effective/applicable why do you say that certain sections in the TPRs have to be applied to transactions in prior, albeit even closed tax years? Eric s reading of the regs.: Because if a prior year transaction had or should have had a change, as a result of the TPR principals/rules, to an asset that is or should have been on the taxpayer s depreciation schedule, it must be changed under the rules of 446 and 481(a). 7

8 Regulation Required Dates: Certain TPR applicable sections, instead of as of saying the TPRs are effective , state the following: (j) Effective/applicability date (1) In general. This section generally applies to amounts paid or incurred in taxable years beginning on or after January 1,

9 Regulation Requirements Beyond certain parts of the requirements requiring method changes: Parts of the TPRs are elections (DMSH, PAD, SHST***) Parts of the TPRs are optional for prior, current or future year issues (Removal costs, PADs) *** de minimis safe harbor, partial asset dispositions, safe harbor for small taxpayers 9

10 The TPR Method Changes are 99.9% Automatic If the method change has a number assigned to it by the IRS, it is an automatic method change All TPR methods have automatic method #s (#21, 184 to 194, 175 to 180, 195 to 207) Automatic method changes do not require a filing fee to file Can be done by the due date of the tax return, including extensions Be careful, once the scope limitations are done (i.e. expire for tax years after 2014) advance consent method change may be required 10

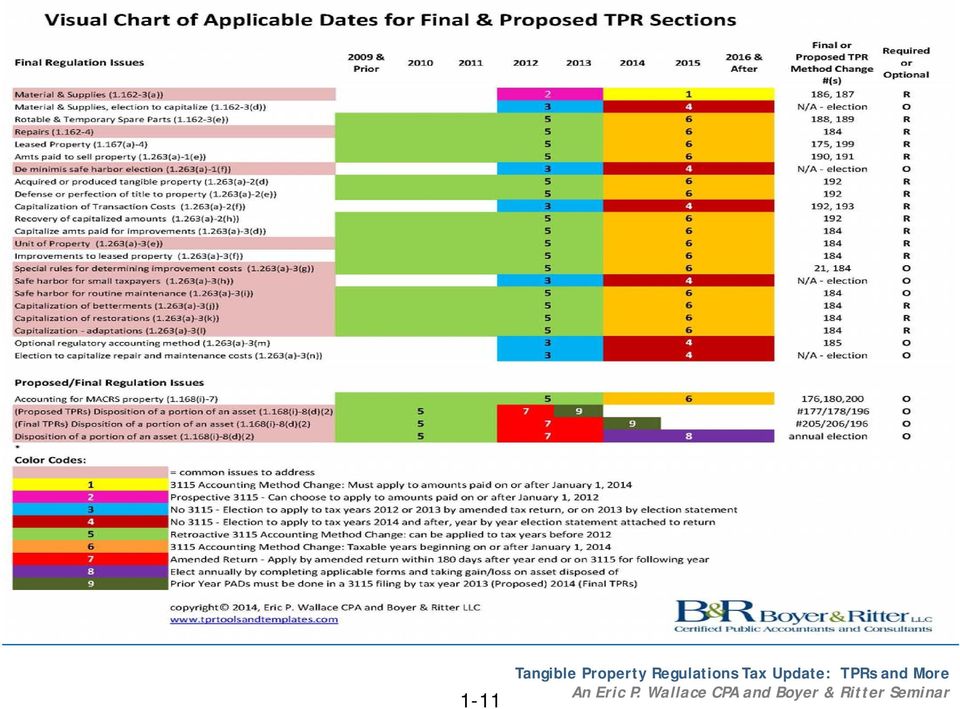

11 1-11

12 The Four Baskets of the Possible TPR Implementation The TPR Four Baskets of Implementation How to Apply Retroactive 1 Required Methods Current and Future Years 2 Required Methods Current and Future Years Retroactive 3 Optional Methods Some for Current and Future Years 4 Optional Elections Methods Current and Future Years 1-12

13 Use it or Lose It Rules (Applies to R & M and Depreciation)

14 New Regulation A taxpayer is not permitted to take advantage in a later year of the taxpayer's prior failure to take any such allowance or the taxpayer's taking an allowance plainly inadequate under the known facts in prior years. In the case of depreciation, if in prior years the taxpayer has consistently taken proper deductions under one method, the amount allowable for such prior years may not be increased, even though a greater amount would have been allowable under another proper method. 1-14

15 Repairs

16 Introduction Repairs = deductions Now can be: removal, demolition (but not 280B demolition types), moving and installation costs; Not: work performed prior to placing property into service (263A), or transaction costs, or costs that require capitalization under the regs (R.A.B.I. rules) 16

17 SUBJECT $$ TO THE R.A.B.I TEST 17

18 Amounts Paid to Improve Tangible Property i.e. the improvement standards, the R.A.B.I. rules

19 Amounts Paid to Improve Tangible Property Reg (a)-3(d) Requirement to capitalize amounts paid for improvements A TP generally must capitalize the related amounts paid to improve a unit of property owned by the TP For this purpose, a unit of property is improved if the amounts paid for activities performed after the property is placed in service by the TP Are for a betterment to the unit of property Restore the unit of property or Adapt the unit of property to a new or different use i.e. the new R.A.B.I. tests/criteria/rules 19

20 Unit of Property Note: This is a very important item in the TPRs

21 Important criteria to determine if expenditure can be written off Almost always considered early in TPR issues Unit of Property (U of P) Smaller the U of P likely required to be capitalized 21

22 Determining the U of P 1.263(a)-3(e) The unit of property determination is generally based upon the functional interdependence standard: Functionally interdependent if the placing in service of one component by the taxpayer is dependent on the placing in service of the other component by the taxpayer But there are. 22

23 Determining the UoP 1.263(a)-3(e) Special rules are provided for Buildings each building is a U of P Plant property Network assets Leased property Leased buildings and leased property other than buildings Improvements to property 23

24 Buildings 1.263(a)-3(e)(2) Building: each building and its structural components (as defined in (e)(2)) is a single unit of property An amount is paid to improve a building if the amount is paid for an improvement under (R.A.B.) to any of the following: Building structure. A building structure consists of the building and its structural components, or. 24

25 Buildings 1.263(a)-3(e)(2) Building Systems: HVAC, Plumbing, Electrical Escalators, Elevators Fire protection and alarm, Security Gas distribution Other as IRS provides in the future Or within the building systems or building structure, Or any item that performs a major and discrete function Or Any large physical portion of the building, 25

26 Unit of Property Issues One tangible personal property: no problem, all separate tangible personal property is a separate U of P: Example: TP buys 100 computers. Each computer is a separate U of P Apartment complex consisting of several buildings: each separate building must be separate U of P Large mall with buildings all connected together: must use facts and circumstances to determine if the U of P is one or separate buildings 26

27 Improvement Costs Criteria This is the I in the R.A.B.I. rules

28 What is Different with the R.A.B.I. Rules Prior criteria, elements, or fact patterns that we thought required the expenditure to be capitalized must be set aside. With the release of the final TPRs, if a criteria, element, or principal is not described, it is not to be considered in the determination of whether an expenditure should be capitalized For example. We will no longer consider if The TP spend a lot of money It made the property more valuable If the new criteria is not met, it is not considered in the R & M verses R.A.B.I. testing 28

29 Special Rules for Determining Improvement Costs Reg (a)-3(g) Certain costs incurred during an improvement 2 General Rule 1 A TP must capitalize all the direct costs of an improvement and all the indirect costs (including, for example, otherwise deductible repair costs) that directly benefit or are incurred by reason of an improvement Indirect costs arising from activities that do not directly benefit and are not incurred by reason of an improvement are not required to be capitalized under Section 263(a), regardless of whether the activities are performed at the same time as an improvement 29

30 Special Rules for Determining Improvement Costs Reg (a)-3(g) Removal Costs 3 If a TP disposes of a depreciable asset, including a partial disposition under Prop. Reg (i)- 1(e)(2)(ix), and has taken into account the adjusted basis of the asset or component of the asset in realizing gain or loss, then the costs of removing the asset or component are not required to be capitalized 30

31 Special Rules for Determining Improvement Costs Reg (a)-3(g) 4 If a TP disposes of a component of a unit of property, but the disposal of the component is not a disposition, then the TP must deduct or capitalize the costs of removing the component based on whether the removal costs directly benefit or are incurred by reason of a repair to the unit of property or an improvement to the unit of property 31

32 Special Rules Compliance with Regulatory Requirements 1.263(a)-3(g)(4) A Federal, state, or local regulator's requirement that a taxpayer perform certain expenditures on a UoP to continue operating the property is not relevant in determining whether the amount paid improves the UoP 5 32

33 Special Rules Compliance with Regulatory Requirements 1.263(a)-3(g)(4) 6 A federal, state, or local regulator s requirement that a taxpayer perform certain expenditures on a U of P to continue operating the property is not relevant in determining whether the amount paid improves the U of P 33

34 Routine Maintenance (different rules for Buildings and tangible personal property)

35 Building Routine Maintenance 1.263(a)-3(i) RM = the recurring activities that a TP expects to perform as a result of the TP's use to keep the building structure or each building system in its ordinarily efficient operating condition. The replacement of damaged or worn parts with comparable and commercially available replacement parts. Routine maintenance may be performed any time during the useful life of the building structure or building systems. 35

36 Building RM However, the activities are routine only if the taxpayer reasonably expects to perform the activities more than once during the 10-year period beginning at the time the building structure or the building system upon which the routine maintenance is performed is placed in service by the taxpayer RM = recurring nature of the activity, industry practice, manufacturers' recommendations, and the taxpayer's experience with similar or identical property. 36

37 Routine Maintenance for Property o/t Buildings The activities are routine only if, at the time the unit of property is placed in service by the taxpayer, the taxpayer reasonably expects to perform the activities more than once during the ADS class life of the asset Want to be able to do the RMSH? Must file method #184 and cite 1.263(a)-3(i) 37

38 Betterments

39 Capitalization of Betterments 1.263(a)-3(j) Ameliorates a material condition or 7 material defect (that existed prior to placing the property in service) Material addition to the U of P 8 9 Material Increase (in productivity or output) 39

40 Betterments to Buildings and Refreshments or Remodels Analysis of whether costs incurred to refresh or remodel a building result in a betterment requires an examination of all the facts and circumstances including, but not limited to The purpose of the expenditure, The physical nature of the work performed, The effect of the expenditure on the UoP, and No longer - the TP s treatment of the expenditure on its AFS 40

41 If one can only replace with better parts, not a consideration in betterment Technological advancements 10 The F TPRs clarified this rule Other rules Comparing the condition 11 41

42 Biggest Issue that is Uncertain in Betterment Criteria? The biggest issue to consider in the betterment rules is what does the phrase material betterment mean? If a TP adds 2% to its warehouse space, is that a material betterment? If a TP adds 10% efficiency to its HVAC system is that a material betterment? There is no direction provided by the regulations 42

43 Restorations This is the part of the R.A.B.I. rules that deals with items such as roof replacements

44 Restorations 1.263(a)-3(k) It returns the U of P to its ordinarily efficient operating condition after it had deteriorated to a state of disrepair and no longer used It is rebuilding to like-new condition after the end of its ADS class life Replaces a major component or substantial structural part of the U of P or Comprises a large physical portion of the U of P

45 Capitalization of Restorations Reg (a)-3(k) A TP must capitalize as an improvement an amount paid to restore a unit of property, including an amount paid to make good the exhaustion for which an allowance is or has been made An amount restores a U of P if it is 16 A replacement where TP deducted a loss, taken into account the basis in a sale, casualty loss 45

46 Thirty % of the Wiring in a Building Written-Off Examples 46

47 40% Capitalized Examples 47

48 Adapt Property to a New or Different Use 1.263(a)-3(l)

49 Amounts to Adapt Property to a New or Different Use 1.263(a)-3(l) 17 Paid if the adaptation is not consistent with the intended ordinary use of the unit of property at the time originally placed in service In the case of a building, if it adapts to a new or different use, any of the properties designated in paragraphs building structure and systems, condominium, cooperative, lease building Temporary Final regulation section is -3(l) is -3T(j) 49

50 New Annual Elections Construction Tax Update: Tangible Property Regulations

51 The Final Main TPR New Annual Elections The final regulations have six potential annual elections Election to capitalize and depreciate certain materials and supplies, (d) De minimis safe harbor election, (f)(1) Election to capitalize amounts paid for employee compensation or overhead as amounts that facilitate the acquisition of property (1.263(a)-2(f)(iv)(B)) 4 Election to capitalize repair and maintenance costs (1.263(a)-2(n)(1) 5 Safe harbor for small taxpayers (1.263(a)-2(h)(1)) 6 Partial Asset Disposition (1.168(i)-8(d)(2)) 1-51 An Eric P. Wallace CPA Seminar Boyer & Ritter CPAs

52 What the Annual Elections Require to Implement The final regulations ways to implement the elections: Election to capitalize and depreciate M & S: just capitalize the M & S De minimis safe harbor election: must made the DMSH statement Election to capitalize amounts paid for employee compensation or overhead: just capitalize the expense 4 Election to capitalize R & M Costs: must make the R & M statement 5 Safe harbor for small taxpayers: must make the SHST statement 6 Partial Asset Disposition: just complete the tax forms in the current year, usually the 4797 form, section I 1-52 An Eric P. Wallace CPA Seminar Boyer & Ritter CPAs

53 TPR Method Changes Construction Tax Update: Tangible Property Regulations

54 Understand What Happens When a TP Files a 3115 The purpose of a 3115 filing is to First: Change a TP s particular tax method of accounting These are automatic if they have been assigned a method number by the IRS Second: Catch up for the accounting method change difference between the prior method and the proposed method that the TP is changing to (this is the 481(a) adjustment) You have to know which TPR method changes are mandatory and which ones are optional 54

55 The Potential Typical TPR Method Required Filings #184, 186, 192 combined, concurrent Form 3115 filing on R & M, R.A.B.I. test, RMSH, Unit of Property and proper cost capitalization (R) #7 for impermissible depreciation methods (R) #21 for removal costs (O) #205 for certain building asset dispositions (PADs) and #206 for certain dispositions or PADs o/t buildings (O); and/or #196 for the late PAD elections that are voluntary (O) 55

56 184, 186, 192 Combination #184, due by 2014, is the method that enables a taxpayer to adopt: R & M of and take a 481(a) adjustment for all prior R & M that should not have been capitalized, as now viewed under the final TPRs RMSH of 1.263(a)-3(i) Unit of Property of 1.263(a)-3(e) The R.A.B.I. rules of 1.263(a)-3 ((g), (j),(l), (k)) A #184 filing must cite the applicable regulation section(s) about 50 potential cites! 56 Construction Tax Update: Tangible Property Regulations

57 184, 186, 192 Combination #186 is the method that enables a taxpayer to adopt: The write off of units of property $200 and under The Non-incidental material and supplies method change This one is for transactions and after (or ), so typically will not have a section 481(a) adjustment #187 is the incidental M & S rule 57 Construction Tax Update: Tangible Property Regulations

58 184, 186, 192 Combination #192 is the method that enables a taxpayer to adopt: The proper capitalization of 1.263(a)-2 for assets purchased or produced Example: you must capitalize all facilitative and inherently facilitative costs Inherently facilitative costs are specifically defined in 1.263(a)-2(f)(ii) 58 Construction Tax Update: Tangible Property Regulations

59 Next Required Method = #7 Method #7 for any impermissible to permissible depreciation changes for: Class lives that are not correct Bonus that was done right Assets that were depreciated that should not have been and vice versa See RP for common class lives to assets employed in various Activities Risk of not filing? IRS use of the use it or lose it rule, as now authorized by Construction Tax Update: Tangible Property Regulations

60 First Optional is #21 A method #21 filing enables a taxpayer (TP) not to have to capitalize any prior or future removal costs associated with an improvement (i.e. a R.A.B.I.) why not file for all TPs? A TP must also have a PAD on the prior asset disposed of (whether current year or prior) can choose each time to employ not Not due by 2014 but if a TP wants not to have to capitalize removal costs, it must file this method change 60 Construction Tax Update: Tangible Property Regulations

61 PAD for Buildings for Prior Years The particular method will depend on what the TP situation is, but could be #196, #205/206 TP can use any reasonable method to calculate the basis of those assets including: PPI roll back method Factorial comparison Cost segregation 61 Construction Tax Update: Tangible Property Regulations

62 Final Typical TPR Method Is #196, and/or #205/206 A #196 filing is the late PAD election and 481(a) reporting where the TP is voluntarily filing, it has no asset definition change, and it is for a part (partial asset) of an asset If those definitions are not met, then the TP has to file a #205/#206 Without a #196 filing, a TP will be required to reverse the 481(a)s taken under previously filed #177 and/or # Construction Tax Update: Tangible Property Regulations

63 Identify critical TPR implementation steps CPA Firm Logistics Construction Tax Update: Tangible Property Regulations

64 The typical TPR method changes and associated automatic method numbers Goal: To understand what the typical 3115 TPR filings are and establish firm procedures to address the TPR filing requirements

65 Repairs and Maintenance (R & M) (R), #184 with a citation to regulation section Material and Supplies (M & S), #186 and/or #187, with a citation to (R) Unit of Property, #184, with a citation to 1.263(a)- 3(e) (R) Restoration, adaption, betterment and improvement (the R.A.B.I. rules), #184 with a citation to the particular part of 1.263(a)-3(g), -3(j), -3(l), -3(k), as applicable (R)

66 Routine Maintenance Safe Harbor, #184 with a citation to 1.263(a)-3(i) (R if you want to take) Removal Costs, #21 (1.263(a)-3(g) (O) Acquisition of property, #192, (1.263(a)-2) (R) Depreciation impermissible methods, #7 (R) Employment of wrong class lives Employment of incorrect bonus taken or not taken Partial asset dispositions, or asset dispositions (1.168(i)-8(d)) [depending on the situation, these may be #196, #205, #206](O but R if you want to take by 2014)

67 The due dates for filing of the 3115s Goal: Learn and comply with the TPR filing due dates TPR Implementation Due Dates: Generally by tax year 2014, up to and including the extended due date of the return Scope limitations waived for certain issues generally only through 2014

68 The allowed or allowable rules and how the use it or lose it rules are a great risk to taxpayers and their CPA firms Goal: Understand and embrace the fact that taxpayers will permanently lose tax deductions for (a) depreciation related issues, and/or (b) R & M related deductions if the corrections related to 3115 filings are not done by tax year 2014 (IRS regulation a new regulation added as part of the TPR issuance)

69 Recommendation: Implement proper procedures to ensure that all depreciation impermissible methods are corrected under a method #7 filing and that all previously capitalized R & M expenditures (as now measured under the principals of the final TPRs) remaining depreciable basis are written off by tax year 2014 in a method # filing

70 TPR Logistics is the study of, determination of the required action items, and employment of procedures that enable a CPA firm to address the TPR issues that a firm may not have considered, or not considered all of the facets that should be addressed

71 Goal: Eliminate or reduce the risks that your firm faces in the performance of client service in preparing for, advising, and executing the Issue Identification and its matching tax form preparation required for the TPRs, due in the proper time frame

72 Recommendation: Study the TPR rules and regulations, identify the resultant issues, develop a firm action plan or goals, assign the proper staff personnel at the appropriate levels, determine due dates for each assignment, and finally monitor compliance and achievement of the TPR assignments/goals

73 Goal and Recommendation: Determine and employ the most effective and efficient method of Form 3115 preparation, including the required attachment answers and power of attorney preparation whether that process is the use the current firm tax preparation software or outside software/forms Keep in mind we have a one time compliance issue with the need to file 3115s for one tax year left (i.e. by 2014)

74 Goal: Determine the procedures or steps necessary for each firm client to assure TPR compliance, monitor those steps, and to develop checklists or processes to assure that all business clients have all of the proper 3115s filed by tax year 2014 in the proper manner and current and future applicable annual elections are properly made

75 Goal and Recommendation: Create an IT process to pre-populate the typical or common forms (such as the 3115, its attachment, and Form 2848, IRS Power of Attorney) for all of your clients/taxpayers

76 The proper signatures have been obtained on the 3115s The 3115s copy with original signatures are mailed to the proper address(es) All of the required 3115 attachments are included The 481(a)s are properly calculated The 3115 package original is attached as a pdf to the electronically submitted income return in the proper tax year All of the proper 3115s are included and submitted in the proper time period The POAs are properly signed and included in the 3115 submissions as an attachment

77 The proper 3115 methods are prepared and submitted Concurrent 3115s are submitted when required and methods that cannot be concurrent are not improperly included on one 3115 submission Considerations for 263A, when applicable, are included Audit protection issues are considered in the 3115 filings The CPA firm has identified all of the relevant TPR client issues The tracking of future positive 481(a) adjustments, if any, resulting from the 3115 filings

78 Firm Policies on Employment of reasonable methods (factorial comparisons; cost segregations; /PPI rollbacks) as to when appropriate or not Signing the 3115 returns originals or e-signatures or not Section 754 issues And others

79 Goal: Treat R & M verses R.A.B.I. properly under the new rules and not a continuation of the old capitalization habits Recommendation: Meet with your clients in advance of the finalization of their accounting and depreciation schedules for tax year 2014 to avoid the duplication of work efforts that will have to be revised as a result of the employment of the new TPR criteria/rules/elections

80 Goal and Recommendations: Create, initiate and then communicate to taxpayers, related to the TPRs The requirements The annual elections, how to, their individual purpose, and applicability to the taxpayer The internal taxpayer processes and records that will need to be adapted/changed not limited to: (i) capitalization policies, (ii) record retention, (iii) removal costs, (iv) landlord/tenant negotiations and documents

81 The work effort involved in complying with the TPRs and the needs from the taxpayer The potential tax deductions (i.e. negative 481(a) adjustments) and/or positive or IRS favorable adjustments (such as the new non-incidental M & S rules) The narrow time parameters for the majority of TPR method changes These communications can consist of individual client letters or s, postings on the firm web page, to unique industry considerations

82 Recommendation: Assure that your client has the future instructions/ability to discern the differences between R & M and R.A.B.I. The primary way that is is going to occur is to meet with your clients and assist them in: Understanding the new TPR R.A.B.I. rules Documenting the R.A.B.I. decision process so that they can make the proper write off or capitalization decisions at the time expenditures are made

83 Goal and Recommendation: Establish appropriate internal taxpayer processes to enable the memorialization of the R.A.B.I. process for taxpayer expenditures where the disbursement is required to be subject to the R.A.B.I criteria Current depreciation software records of Description of the asset Date placed in service Amount or cost of the asset Depreciation method, convention Bonus or not 179 or not Current year and accumulated depreciation are no longer sufficient Taxpayer must be able to support its decision to capitalize or not to capitalize an expenditure as an asset

84 TPR Case Study Construction Tax Update: Tangible Property Regulations Eric P. Wallace CPA Boyer & Ritter CPAs 8 4

85 Case Study Facts Commercial Landlord, LLC, (CLLLC) a partnership, owns one building that is a strip mall in Anytown USA. The building was purchased in 1989 for $2.5M. The building has 10 tenant spaces that are leased for various periods. When the building was purchased it was fully leased. You have obtained their tax depreciation schedule as of

86 Commercial Landlord Rent and Royalty - Depreciation and Amortization 12/31/2013 A Asset Number Description Date in Service M L Cost or Other Basis Accum Depr Net Remaining Depreciable Basis 1LAND 04/01/89L 1,143,000 1,143,000 2BUILDING 04/01/89MSL ,249, , ,304 TENANT 3IMPROVEMENTS 09/01/91MSL ,951 41,285 17,731 4IMPROVEMENTS 06/15/92MSL ,715 3,076 1,489 5LAND IMPROVEMENTS 02/08/01MSL ,360 28,360-10NEW HVAC 03/25/03MSL ,026 5,451 16,010 11IMPROVEMENTS 09/22/03MSL ,951 1,180 3,644 17IMPROVEMENTS 02/22/08SL ,048 1,121 7,695 18ROOF AND WINDOWS 06/30/08SL ,490 30, ,670 20ALL AC UNITS 05/07/11MSL , ,668-21LEASE COMMISSION 02/01/11A , ,

87 Case Method Filings and 481(a)s You know that you have to file the required 3115s by tax year 2014, so you analyze their tax depreciation schedule as follows and have come up with the following method required filing changes and 481(a) adjustments: Method #184, 186, 192 for $(46,569) Method #7 for $+118,142 Method #196 for $(80,551) Method #21 for zero, but need data from client Let s discuss the why of each of these 87

88 Commercial Landlord Rent and Royalty - Depreciation and Amortization 12/31/2013 A B C Asset Number Description Date in Service M L Cost or Other Basis Accum Depr Net Remaining Depreciable Basis TPR Code 481 (a) adj. 1LAND 04/01/89L 1,143,000 1,143,000 2BUILDING 04/01/89MSL ,249, , ,304 TENANT 3IMPROVEMENTS 09/01/91MSL ,951 41,285 17,731 R (17,731) 4IMPROVEMENTS 06/15/92MSL ,715 3,076 1,489 R (1,489) 5LAND IMPROVEMENTS 02/08/01MSL ,360 28,360 - R - 10NEW HVAC 03/25/03MSL ,026 5,451 16,010 R (16,010) 11IMPROVEMENTS 09/22/03MSL ,951 1,180 3,644 R (3,644) 17IMPROVEMENTS 02/22/08SL ,048 1,121 7,695 R (7,695) 18ROOF AND WINDOWS 06/30/08SL ,490 30, ,670 P1 (55,486) 20ALL AC UNITS 05/07/11MSL , ,668 - CL 118,142 P1 (25,065) 21LEASE COMMISSION 02/01/11A , ,

89 PPI Calculation Details Roof and Windows PPI Rollback Calculations: $261,490 times PPI of June of 2008 divided by PPI of April of 1989 ($261,490*182.4/113.0)= $161, less AD from 1989 to of $106,512=$55,486 All AC Units PPI Rollback Calculations: $124,668 times PPI of May of 2011 divided by PPI of April of 1989 ($124,668*192.5/113.0)= $73,182 less AD from 1989 to of $48,116=$25,065 89

90 PPI Discounting Table Determine the PPI differences Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

91 Case Study Conclusions/Thoughts on What CLLLC has to do: File (1) #184,186,192 concurrently, and cite 162-4, RMSH, make U of P statements, and the RABI citations of 1.263(a)-3, and report a $(46,569) 481(a); (2) a #7 separately and report a positive 481(a) of $118,142; (3) #21 and decide if it wants a 481(a) for prior removal costs or not; (4) a #196 with a negative 481(a) of $(80,551) Net or separately report its + and - 481(a)s but must make that decision when it files its 2014 return Calculate its AMT 481(a)s and will report those in its AMT schedules in its 2014 filings (and state differences in those returns) Mail the copy with original signatures 3115 and attachments to Ogden for all but #21 which goes to DC Attach the copied originals to its income tax filing for 2014 Include any elections it wants to in its 2014 return Report any related party filings on its 3115 attachments Decide if it wants to also complete and attach POAs 91

92 92

Quick Summary of Final Tangible Property Regulations

This summary is intended to provide a high-level overview only and should not be relied on for application to specific fact patterns and situations. Taxpayers should consult their tax advisors to determine

This summary is intended to provide a high-level overview only and should not be relied on for application to specific fact patterns and situations. Taxpayers should consult their tax advisors to determine

TANGIBLE PROPERTY REGULATIONS TROISIÈME PARTIE (Oh là là)

") TANGIBLE PROPERTY REGULATIONS TROISIÈME PARTIE (Oh là là) Jeff McGowan, CPA, CGMA Tax Partner Presented November 12, 2014 Kruggel Lawton CFO Summit 1. Cover Slide 2. Legislative History of Tangible Property

TANGIBLE PROPERTY REGULATIONS TROISIÈME PARTIE (Oh là là) Jeff McGowan, CPA, CGMA Tax Partner Presented November 12, 2014 Kruggel Lawton CFO Summit 1. Cover Slide 2. Legislative History of Tangible Property

KPM CPAs & Advisors Summary of IRS Tangible Property Rules

The IRS has issued long awaited regulations on the tax treatment of amounts paid to acquire, produce, or improve tangible property. These rules explain when those payments can be immediately expensed and

The IRS has issued long awaited regulations on the tax treatment of amounts paid to acquire, produce, or improve tangible property. These rules explain when those payments can be immediately expensed and

November 2014 WWW. E L L I N A N D T U C K E R. C O M

November 2014 They apply to all taxpayers who own depreciable real or personal property They affect all decisions regarding capitalization, depreciation, and disposition of tangible property Must capitalize

November 2014 They apply to all taxpayers who own depreciable real or personal property They affect all decisions regarding capitalization, depreciation, and disposition of tangible property Must capitalize

The final tangible asset and repair regulations - Part II

The final tangible asset and repair regulations - Part II Clarifications and taxpayer-friendly safe harbors and elections added for acquisition and improvement rules Prepared by: Kate Abdoo, Manager, RSM

The final tangible asset and repair regulations - Part II Clarifications and taxpayer-friendly safe harbors and elections added for acquisition and improvement rules Prepared by: Kate Abdoo, Manager, RSM

Eric P. Wallace CPA (1/18/2016)

") ERIC P WALLACE CPA Eric P. Wallace CPA () 1 TPR TOOLS AND TEMPLATES - TABLE OF CONTENTS Copyright Eric P. Wallace CPA, January 2016 TPR (Tangible Property Regulations) Tools and Templates (items highlighted

ERIC P WALLACE CPA Eric P. Wallace CPA () 1 TPR TOOLS AND TEMPLATES - TABLE OF CONTENTS Copyright Eric P. Wallace CPA, January 2016 TPR (Tangible Property Regulations) Tools and Templates (items highlighted

New Repair Regulations and the Impact on Owners of Investment Real Estate

Tom Scarpello Managing Partner 877.410.5040 New Repair Regulations and the Impact on Owners of Investment Real Estate On December 23, 2011, the IRS issued comprehensive guidance regarding amounts paid

Tom Scarpello Managing Partner 877.410.5040 New Repair Regulations and the Impact on Owners of Investment Real Estate On December 23, 2011, the IRS issued comprehensive guidance regarding amounts paid

Fix Your Fixed Assets. www.padgett-cpa.com

Fix Your Fixed Assets www.padgett-cpa.com 2014 Depreciation Update 2013 2014 Section 179 Expense Investment Limit $ 2,000,000 $ 200,000 Expense Limit $ 500,000 $ 25,000 Bonus Depreciation 50% 0% (Set to

Fix Your Fixed Assets www.padgett-cpa.com 2014 Depreciation Update 2013 2014 Section 179 Expense Investment Limit $ 2,000,000 $ 200,000 Expense Limit $ 500,000 $ 25,000 Bonus Depreciation 50% 0% (Set to

IRS CODE SECTION 263 FINAL REPAIR/CAPITALIZATION REGULATIONS

IRS CODE SECTION 263 FINAL REPAIR/CAPITALIZATION REGULATIONS Presenting the Top 10 Things You Must Know PRESENTED BY: JOHN MARTELLINI, CPA, MST LGC&D, LLP These seminar materials are intended to provide

IRS CODE SECTION 263 FINAL REPAIR/CAPITALIZATION REGULATIONS Presenting the Top 10 Things You Must Know PRESENTED BY: JOHN MARTELLINI, CPA, MST LGC&D, LLP These seminar materials are intended to provide

How the new repairs and maintenance capitalization standards will impact your next remodel Restaurant Finance Conference November 14, 2012

How the new repairs and maintenance capitalization standards will impact your next remodel Restaurant Finance Conference November 14, 2012 2012 Baker Tilly Virchow Krause, LLP Baker Tilly refers to Baker

How the new repairs and maintenance capitalization standards will impact your next remodel Restaurant Finance Conference November 14, 2012 2012 Baker Tilly Virchow Krause, LLP Baker Tilly refers to Baker

Overview. Tangible Property Regulations. Bader Martin, PS Certified Public Accountants + Business Advisors www.badermartin.com

Bader Martin, PS Certified Public Accountants + Business Advisors www.badermartin.com Contents Introduction 2 New Concept: Unit of Property 2 Capitalize Acquisitions and Improvements, Deduct Repairs 3

Bader Martin, PS Certified Public Accountants + Business Advisors www.badermartin.com Contents Introduction 2 New Concept: Unit of Property 2 Capitalize Acquisitions and Improvements, Deduct Repairs 3

WEBINAR FAQs IS THE PAPER FILED COPY DUE BY DATE THE TAX RETURN IS TIMELY E-FILED OR WHEN THE TAX RETURN IS DUE (INCLUDING EXTENSIONS)?

?") WEBINAR FAQs Filing Q1 IS THE PAPER FILED COPY DUE BY DATE THE TAX RETURN IS TIMELY E-FILED OR WHEN THE TAX RETURN IS DUE (INCLUDING EXTENSIONS)? Q33 What is the submission deadline of signed Form 3115

WEBINAR FAQs Filing Q1 IS THE PAPER FILED COPY DUE BY DATE THE TAX RETURN IS TIMELY E-FILED OR WHEN THE TAX RETURN IS DUE (INCLUDING EXTENSIONS)? Q33 What is the submission deadline of signed Form 3115

Commonly asked questions on the new tangible property regulations

Commonly asked questions on the new tangible property regulations A compilation of questions and answers from recent webcasts November 2013 Materials and supplies Question 1: How is a rotable defined?

Commonly asked questions on the new tangible property regulations A compilation of questions and answers from recent webcasts November 2013 Materials and supplies Question 1: How is a rotable defined?

Final tangible property repair regulations: Unit of property and acquisition or improvement of property

Final tangible property repair regulations: Unit of property and acquisition or improvement of property September 26, 2013 In brief This is the second WNTS Insight in a three-part series that discusses

Final tangible property repair regulations: Unit of property and acquisition or improvement of property September 26, 2013 In brief This is the second WNTS Insight in a three-part series that discusses

Anchin Real Estate Services Group

Anchin Real Estate Services Group What is a Capital Expenditure? Marc Wieder, CPA Partner Anchin, Block & Anchin LLP Accountants & Advisors What is a Capital Expenditure? Part 1 The IRS published important

Anchin Real Estate Services Group What is a Capital Expenditure? Marc Wieder, CPA Partner Anchin, Block & Anchin LLP Accountants & Advisors What is a Capital Expenditure? Part 1 The IRS published important

Tax Consequences of Selling Or Creating Real Estate

BUSINESS TAX & ACCOUNTING SEMINAR TURNING YOUR FIXED ASSET REVIEW INTO TANGIBLE TAX SAVINGS berrydunn.com GAIN CONTROL TODAY S OBJECTIVE Help taxpayers who acquire, produce, or improve tangible property

BUSINESS TAX & ACCOUNTING SEMINAR TURNING YOUR FIXED ASSET REVIEW INTO TANGIBLE TAX SAVINGS berrydunn.com GAIN CONTROL TODAY S OBJECTIVE Help taxpayers who acquire, produce, or improve tangible property

26 CFR 601.204: Changes in accounting periods and in methods of accounting. (Also Part I, 168, 446, 481; 1.168(i)-1, 1.168(i)-7, 1.168(i)-8, 1.446-1.

-1, 1.168(i)-7, 1.168(i)-8, 1.446-1.") 26 CFR 601.204: Changes in accounting periods and in methods of accounting. (Also Part I, 168, 446, 481; 1.168(i)-1, 1.168(i)-7, 1.168(i)-8, 1.446-1.) Rev. Proc. 2014-54 SECTION 1. PURPOSE This revenue

26 CFR 601.204: Changes in accounting periods and in methods of accounting. (Also Part I, 168, 446, 481; 1.168(i)-1, 1.168(i)-7, 1.168(i)-8, 1.446-1.) Rev. Proc. 2014-54 SECTION 1. PURPOSE This revenue

Final IRC 263(a) Tangible Property Regulations

Tangible Property Regulations") Final IRC 263(a) Tangible Property Regulations Technical Update Nathan Clark, CPA Senior Director, Fixed Asset Advisory Services Marla Miller, CPA Senior Director, Fixed Asset Advisory Services November

Final IRC 263(a) Tangible Property Regulations Technical Update Nathan Clark, CPA Senior Director, Fixed Asset Advisory Services Marla Miller, CPA Senior Director, Fixed Asset Advisory Services November

Manage Risk with Fixed Assets

Manage Risk with Fixed Assets Presented by: V. Lynn Lambert, CPA Lambert Lanoue & Smoker LLC www.lambertcpas.com Outline Analysis of Lease vs Purchase of Fixed Assets New IRS Repair Regulations Capital

Manage Risk with Fixed Assets Presented by: V. Lynn Lambert, CPA Lambert Lanoue & Smoker LLC www.lambertcpas.com Outline Analysis of Lease vs Purchase of Fixed Assets New IRS Repair Regulations Capital

26 CFR 601.204 Changes in accounting periods and in methods of accounting. (Also Part I, 162, 263(a), 263A, 446, 481; 1.446-1.)

, 263A, 446, 481; 1.446-1.)") 26 CFR 601.204 Changes in accounting periods and in methods of accounting. (Also Part I, 162, 263(a), 263A, 446, 481; 1.446-1.) Rev. Proc. 2015-20 SECTION 1. PURPOSE This revenue procedure modifies Rev.

26 CFR 601.204 Changes in accounting periods and in methods of accounting. (Also Part I, 162, 263(a), 263A, 446, 481; 1.446-1.) Rev. Proc. 2015-20 SECTION 1. PURPOSE This revenue procedure modifies Rev.

Updated: Analysis of Comprehensive Repair/Capitalization Regulations

November 2012 taxalerts.plantemoran.com Updated: Analysis of Comprehensive Repair/Capitalization Regulations Repair Regulations Have Sweeping Impact; Will Require Accounting Method Changes; 2014 Effective

November 2012 taxalerts.plantemoran.com Updated: Analysis of Comprehensive Repair/Capitalization Regulations Repair Regulations Have Sweeping Impact; Will Require Accounting Method Changes; 2014 Effective

2014-2015 Tax Update: Another Year For Tax Breaks By Kurt J. Kilwein, CPA, CFP, Partner and Olga Zarney, CPA, MBT, Manager

WINTER 2014-2015 2014-2015 Tax Update: Another Year For Tax Breaks By Kurt J. Kilwein, CPA, CFP, Partner and Olga Zarney, CPA, MBT, Manager Individual Taxation Many of the tax breaks which expired at the

WINTER 2014-2015 2014-2015 Tax Update: Another Year For Tax Breaks By Kurt J. Kilwein, CPA, CFP, Partner and Olga Zarney, CPA, MBT, Manager Individual Taxation Many of the tax breaks which expired at the

What s News in Tax Analysis That Matters from Washington National Tax

What s News in Tax Analysis That Matters from Washington National Tax The Final Disposition Regulations : The Last Installment of the Repair Regs Saga The government issued final regulations and transitional

What s News in Tax Analysis That Matters from Washington National Tax The Final Disposition Regulations : The Last Installment of the Repair Regs Saga The government issued final regulations and transitional

SUBJECT Income Tax Accounting Question & Answer Series #3 ACCOUNTING IMPLICATIONS FROM THE TANGIBLE PROPERTY REPAIR REGULATIONS CONTACT: BACKGROUND

BDO STATE AND LOCAL TAX ALERT 1 DECEMBER 2014 www.bdo.com SUBJECT Income Tax Accounting Question & Answer Series #3 ACCOUNTING IMPLICATIONS FROM THE TANGIBLE PROPERTY REPAIR REGULATIONS PREFACE: There

BDO STATE AND LOCAL TAX ALERT 1 DECEMBER 2014 www.bdo.com SUBJECT Income Tax Accounting Question & Answer Series #3 ACCOUNTING IMPLICATIONS FROM THE TANGIBLE PROPERTY REPAIR REGULATIONS PREFACE: There

Taxation: Deductions, Credits, and Strategies You May Be Missing By Glenn Scharf, CPA, CVA and John Mascaro, CPA

Taxation: Deductions, Credits, and Strategies You May Be Missing By Glenn Scharf, CPA, CVA and John Mascaro, CPA Many manufacturers continue to miss the boat on taking advantage of all aspects of the tax

Taxation: Deductions, Credits, and Strategies You May Be Missing By Glenn Scharf, CPA, CVA and John Mascaro, CPA Many manufacturers continue to miss the boat on taking advantage of all aspects of the tax

Final regulations on disposition of tangible depreciable property: Indepth discussion of key issues

from Washington National Tax Services Final regulations on disposition of tangible depreciable property: Indepth discussion of key issues September 12, 2014 In brief The IRS on August 14 released final

from Washington National Tax Services Final regulations on disposition of tangible depreciable property: Indepth discussion of key issues September 12, 2014 In brief The IRS on August 14 released final

WNTS Insight. In brief. October 7, 2013

Final tangible property repair regulations and proposed regulations: Dispositions, general asset accounts, recovery of certain capital improvements, and removal costs October 7, 2013 In brief This is the

Final tangible property repair regulations and proposed regulations: Dispositions, general asset accounts, recovery of certain capital improvements, and removal costs October 7, 2013 In brief This is the

MANUFACTURING INSIDER

MANUFACTURING INSIDER VOLUME 6 :: ISSUE 4 In This Issue: On The Road Again: Using Project Management As A GPS In Manufacturing Final IRC Regulations On Deducting Manufacturing Expenses: How Will They Affect

MANUFACTURING INSIDER VOLUME 6 :: ISSUE 4 In This Issue: On The Road Again: Using Project Management As A GPS In Manufacturing Final IRC Regulations On Deducting Manufacturing Expenses: How Will They Affect

AT&T Global Network Client for Windows Product Support Matrix January 29, 2015

AT&T Global Network Client for Windows Product Support Matrix January 29, 2015 Product Support Matrix Following is the Product Support Matrix for the AT&T Global Network Client. See the AT&T Global Network

AT&T Global Network Client for Windows Product Support Matrix January 29, 2015 Product Support Matrix Following is the Product Support Matrix for the AT&T Global Network Client. See the AT&T Global Network

REAL ESTATE REVIEW. October 2014 O C TO B E R 2 0 14 R EAL ESTATE REVIEW

O C TO B E R 2 0 14 R EAL ESTATE REVIEW REAL ESTATE REVIEW October 2014 FREIGHT DEPOT 1200 MARKET STREET CHATTANOOGA, TN 37402 423.756.7771 HHMCPAS.COM REAL ESTATE REVIEW / October 14 THE TANGIBLE PROPERTY

O C TO B E R 2 0 14 R EAL ESTATE REVIEW REAL ESTATE REVIEW October 2014 FREIGHT DEPOT 1200 MARKET STREET CHATTANOOGA, TN 37402 423.756.7771 HHMCPAS.COM REAL ESTATE REVIEW / October 14 THE TANGIBLE PROPERTY

Guide to Starting Self Employment or Business. Guide No.6 in the Tax Guide Series

Guide to Starting Self Employment or Business Guide No.6 in the Tax Guide Series About This Guide This Guide has been prepared to help someone starting out in a new business or self employment venture

Guide to Starting Self Employment or Business Guide No.6 in the Tax Guide Series About This Guide This Guide has been prepared to help someone starting out in a new business or self employment venture

1. Equipment and supplies presently being expensed under a minimum capitalization policy:

The IRS Has Changed How Business Assets, Repairs, and Supplies Will Be Handled Beginning New Year s Day. There Are Important Steps To Take Before Year End That Will Soften The Blow. By: Tom Zoebelein,

The IRS Has Changed How Business Assets, Repairs, and Supplies Will Be Handled Beginning New Year s Day. There Are Important Steps To Take Before Year End That Will Soften The Blow. By: Tom Zoebelein,

CHAPTER 10. Acquisition and Disposition of Property, Plant, and Equipment 1, 2, 3, 5, 6, 11, 12, 21 11, 15, 16 8, 9, 10, 11, 12

CHAPTER 10 Acquisition and Disposition of Property, Plant, and Equipment ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Valuation

CHAPTER 10 Acquisition and Disposition of Property, Plant, and Equipment ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Valuation

June 8, 2015. Dear Mr. Keyso:

June 8, 2015 Mr. Andrew Keyso, Jr. Associate Chief Counsel Income Tax & Accounting Internal Revenue Service 1111 Constitution Avenue, N.W. Washington, D.C. 20224 Re: Recommendation that Taxpayers Making

June 8, 2015 Mr. Andrew Keyso, Jr. Associate Chief Counsel Income Tax & Accounting Internal Revenue Service 1111 Constitution Avenue, N.W. Washington, D.C. 20224 Re: Recommendation that Taxpayers Making

Increase in De Minimis Safe Harbor Limit for Taxpayers Without an Applicable Financial Statement

Increase in De Minimis Safe Harbor Limit for Taxpayers Without an Applicable Financial Statement Notice 2015-82 PURPOSE This notice provides an increase in the de minimis safe harbor limit provided in

Increase in De Minimis Safe Harbor Limit for Taxpayers Without an Applicable Financial Statement Notice 2015-82 PURPOSE This notice provides an increase in the de minimis safe harbor limit provided in

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*

CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*") COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) 2 Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) 2 Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*

CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*") COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) 2 Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) 2 Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun

Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 1 of 138. Exhibit 8

Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 1 of 138 Exhibit 8 Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 2 of 138 Domain Name: CELLULARVERISON.COM Updated Date: 12-dec-2007

Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 1 of 138 Exhibit 8 Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 2 of 138 Domain Name: CELLULARVERISON.COM Updated Date: 12-dec-2007

Tax Update. Rod Mauszycki, CliftonLarsonAllen

Tax Update Rod Mauszycki, CliftonLarsonAllen Government s view of the economy could be summed up in a few short phrases: If it moves, tax it. If it keeps moving, regulate it. And if it stops moving, subside

Tax Update Rod Mauszycki, CliftonLarsonAllen Government s view of the economy could be summed up in a few short phrases: If it moves, tax it. If it keeps moving, regulate it. And if it stops moving, subside

REPAIR V. CAPITALIZATION REGS

REPAIR V. CAPITALIZATION REGS Copyright Tax Educators' Network, Inc.. 2014 1 INTRODUCTION & COMMENTS Copyright Tax Educators' Network, Inc.. 2014 2 Workshop Objectives Knowledge Issue awareness Ability

REPAIR V. CAPITALIZATION REGS Copyright Tax Educators' Network, Inc.. 2014 1 INTRODUCTION & COMMENTS Copyright Tax Educators' Network, Inc.. 2014 2 Workshop Objectives Knowledge Issue awareness Ability

Instructions for Form 8582 Passive Activity Loss Limitations

2007 Instructions for Form 8582 Passive Activity Loss Limitations Department of the Treasury Internal Revenue Service Section references are to the Internal rental passive activities. Overall loss is limited,

2007 Instructions for Form 8582 Passive Activity Loss Limitations Department of the Treasury Internal Revenue Service Section references are to the Internal rental passive activities. Overall loss is limited,

What s News in Tax Analysis That Matters from Washington National Tax

What s News in Tax Analysis That Matters from Washington National Tax Foreign Corporations: Use of Accounting Methods in E&P Planning and Compliance This article addresses the importance of using proper

What s News in Tax Analysis That Matters from Washington National Tax Foreign Corporations: Use of Accounting Methods in E&P Planning and Compliance This article addresses the importance of using proper

Property, Plant and Equipment

Compiled AASB Standard AASB 116 Property, Plant and Equipment This compiled Standard applies to annual reporting periods beginning on or after 1 July 2009. Early application is permitted. It incorporates

Compiled AASB Standard AASB 116 Property, Plant and Equipment This compiled Standard applies to annual reporting periods beginning on or after 1 July 2009. Early application is permitted. It incorporates

GAIN CLARITY CRITICAL TAX ISSUES. Impacting Your Business GAIN CONTROL. berrydunn.com

GAIN CLARITY CRITICAL TAX ISSUES Impacting Your Business berrydunn.com ON TRACK WITH YOUR AGENDA Health Care Reform Cost Recovery Form 1099-K Reporting Foreign Bank Account Reporting Changes for 2013 2013

GAIN CLARITY CRITICAL TAX ISSUES Impacting Your Business berrydunn.com ON TRACK WITH YOUR AGENDA Health Care Reform Cost Recovery Form 1099-K Reporting Foreign Bank Account Reporting Changes for 2013 2013

2014 S CORPORATION INCOME TAX RETURN CHECKLIST (FORM 1120) (MINI)

(MINI)") (FORM 1120) (MINI) Client name and number Prepared by Date Reviewed by Date GENERAL INFORMATION DONE N/A 1) Consider if any conflict(s) of interest exist(s) between the entity and its shareholders and/or

(FORM 1120) (MINI) Client name and number Prepared by Date Reviewed by Date GENERAL INFORMATION DONE N/A 1) Consider if any conflict(s) of interest exist(s) between the entity and its shareholders and/or

2015 S CORPORATION INCOME TAX RETURN CHECKLIST (FORM 1120S) (MINI)

(MINI)") Client name and number Prepared by Date Reviewed by Date GENERAL INFORMATION DONE N/A 1) Identify authorized officer who will sign the return. 2) Consider if any conflict(s) of interest exist(s) between

Client name and number Prepared by Date Reviewed by Date GENERAL INFORMATION DONE N/A 1) Identify authorized officer who will sign the return. 2) Consider if any conflict(s) of interest exist(s) between

Updates to the U.S. Master Depreciation Guide 2014

Updates to the U.S. Master Depreciation Guide 2014 The IRS issued Rev. Proc. 2014-17, 2014 IRB 661 on February 28, 2014 to provide automatic accounting method change procedures to change to a method described

Updates to the U.S. Master Depreciation Guide 2014 The IRS issued Rev. Proc. 2014-17, 2014 IRB 661 on February 28, 2014 to provide automatic accounting method change procedures to change to a method described

Tax Return Questionnaire - 2014 Tax Year

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Internal Revenue Service

Internal Revenue Service Number: 201037005 Release Date: 9/17/2010 Index Number: 856.04-00 ----------------------- ------------------------- -------------------------------- --------------------------------------------------

Internal Revenue Service Number: 201037005 Release Date: 9/17/2010 Index Number: 856.04-00 ----------------------- ------------------------- -------------------------------- --------------------------------------------------

2013-2014 Tax Update Lead Story Headline

December Daniel, Ratliff & Company 704-371-5000 2013-2014 Tax Updates 2013-2014 Tax Update Lead Story Headline Contents 50% Bonus Depreciation Scheduled to Expire After 2013 2 Expanded Section 179 Deduction

December Daniel, Ratliff & Company 704-371-5000 2013-2014 Tax Updates 2013-2014 Tax Update Lead Story Headline Contents 50% Bonus Depreciation Scheduled to Expire After 2013 2 Expanded Section 179 Deduction

Term Sheet for Lease in Cambridge, Massachusetts

1/22/15 Term Sheet for Lease in Cambridge, Massachusetts D A T E D A S O F : J A N U A R Y X X, 2015 PREAMBLE: Landlord and Tenant (each as defined below) hereby enter this Term Sheet (this Term Sheet

1/22/15 Term Sheet for Lease in Cambridge, Massachusetts D A T E D A S O F : J A N U A R Y X X, 2015 PREAMBLE: Landlord and Tenant (each as defined below) hereby enter this Term Sheet (this Term Sheet

Agreement for 2015 S Corporation Income Tax Preparation

Agreement for 2015 S Corporation Income Tax Preparation Dear Client: We will prepare the federal, resident state and city S-corporation income tax returns for for the year ended December 31, 2015 and we

Agreement for 2015 S Corporation Income Tax Preparation Dear Client: We will prepare the federal, resident state and city S-corporation income tax returns for for the year ended December 31, 2015 and we

Tax Law Snapshot for Small Businesses 2014 Filing Season

Tax Law Snapshot for Small Businesses 2014 Filing Season As the economy recovers, you want to position your business for growth. By combining unrivaled education, training and experience and adherence

Tax Law Snapshot for Small Businesses 2014 Filing Season As the economy recovers, you want to position your business for growth. By combining unrivaled education, training and experience and adherence

Accounting Policies. 4.02 Land and Land Improvements. 4.03 Buildings and Building Service Equipment. 4.04 Leasehold Improvements

Page 1 of 14 Accounting Policies Section 4.0 Capital Assets 4.01 Capital Assets Defined 4.02 Land and Land Improvements 4.03 Buildings and Building Service Equipment 4.04 Leasehold Improvements 4.05 Equipment

Page 1 of 14 Accounting Policies Section 4.0 Capital Assets 4.01 Capital Assets Defined 4.02 Land and Land Improvements 4.03 Buildings and Building Service Equipment 4.04 Leasehold Improvements 4.05 Equipment

Construction. Industry Advisor. Winter 2014. Expense or capitalize? How your contracts can help strengthen cash flow

Construction Industry Advisor Winter 2014 Expense or capitalize? New repair regulations offer guidance for contractors How your contracts can help strengthen cash flow Sales and use taxes Evaluate your

Construction Industry Advisor Winter 2014 Expense or capitalize? New repair regulations offer guidance for contractors How your contracts can help strengthen cash flow Sales and use taxes Evaluate your

Instructions for Form 8582-CR (Rev. January 2012)

") Instructions for Form 8582-CR (Rev. January 2012) For use with Form 8582-CR (Rev. January 2012) Passive Activity Credit Limitations Department of the Treasury Internal Revenue Service Section references

Instructions for Form 8582-CR (Rev. January 2012) For use with Form 8582-CR (Rev. January 2012) Passive Activity Credit Limitations Department of the Treasury Internal Revenue Service Section references

What s News in Tax Analysis That Matters from Washington National Tax

What s News in Tax Analysis That Matters from Washington National Tax Cable System Operators: New Safe Harbors for Applying the Tangible Property Regulations The IRS issued industry-specific guidance that

What s News in Tax Analysis That Matters from Washington National Tax Cable System Operators: New Safe Harbors for Applying the Tangible Property Regulations The IRS issued industry-specific guidance that

Instructions for Form 3115 (Rev. March 2012) (Use with the December 2009 revision of Form 3115) Application for Change in Accounting Method

(Use with the December 2009 revision of Form 3115) Application for Change in Accounting Method") Instructions for Form 3115 (Rev. March 2012) (Use with the December 2009 revision of Form 3115) Application for Change in Accounting Method Department of the Treasury Internal Revenue Service Section references

Instructions for Form 3115 (Rev. March 2012) (Use with the December 2009 revision of Form 3115) Application for Change in Accounting Method Department of the Treasury Internal Revenue Service Section references

ASSISTED LIVING FACILITY EXECUTIVE SUMMARY

ASSISTED LIVING FACILITY EXECUTIVE SUMMARY The following case study assumptions provide the basis for the feasibility of developing a heavy care assisted living facility as part of the Anytown Medical

ASSISTED LIVING FACILITY EXECUTIVE SUMMARY The following case study assumptions provide the basis for the feasibility of developing a heavy care assisted living facility as part of the Anytown Medical

S Corporation Mergers and Acquisitions: Tax Planning Strategies for Favorable Outcomes

60TH ANNUAL MNCPA TAX CONFERENCE November 17-18, 2014 Minneapolis Convention Center ONLINE RESOURCES Session Handouts Most session handouts are available on the MNCPA website. To access: Go to www.mncpa.org/materials

60TH ANNUAL MNCPA TAX CONFERENCE November 17-18, 2014 Minneapolis Convention Center ONLINE RESOURCES Session Handouts Most session handouts are available on the MNCPA website. To access: Go to www.mncpa.org/materials

Cost Segregation Studies, Depreciation Updates, and Repair vs. Capitalization. By David A. Fabian & Jeffrey D. Hiatt MS Consultants, LLC 2013

Cost Segregation Studies, Depreciation Updates, and Repair vs. Capitalization By David A. Fabian & Jeffrey D. Hiatt MS Consultants, LLC Today s Topics 1. Cost Segregation 2. Depreciation Updates 3. Repair

Cost Segregation Studies, Depreciation Updates, and Repair vs. Capitalization By David A. Fabian & Jeffrey D. Hiatt MS Consultants, LLC Today s Topics 1. Cost Segregation 2. Depreciation Updates 3. Repair

Part III. Administrative, Procedural, and Miscellaneous

Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.204: Changes in accounting periods and methods of accounting. (Also Part 1, 162, 263A, 446, 447, 448, 460, 471, 481, 1001; 1.162-3, 1.263A-1,

Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.204: Changes in accounting periods and methods of accounting. (Also Part 1, 162, 263A, 446, 447, 448, 460, 471, 481, 1001; 1.162-3, 1.263A-1,

Unrelated Business Income Taxes (UBIT), Weill Cornell Medical College - Qatar

, Weill Cornell Medical College - Qatar") INTERIM Issued: June 4, 2004 CORNELL UNIVERSITY POLICY LIBRARY Unrelated Business Income Taxes (UBIT), Weill Cornell Medical College - Qatar POLICY 3.15.2 Responsible Executive: Dean, POLICY STATEMENT

INTERIM Issued: June 4, 2004 CORNELL UNIVERSITY POLICY LIBRARY Unrelated Business Income Taxes (UBIT), Weill Cornell Medical College - Qatar POLICY 3.15.2 Responsible Executive: Dean, POLICY STATEMENT

Reg. 1.5833-1 (Effective for tax years beginning on and after January 1, 1998) Allocation and apportionment of Vermont net income by corporations

Allocation and apportionment of Vermont net income by corporations") Reg. 1.5833 ALLOCATION AND APPORTIONMENT OF INCOME Reg. 1.5833-1 (Effective for tax years beginning on and after January 1, 1998) Allocation and apportionment of Vermont net income by corporations (a)

Reg. 1.5833 ALLOCATION AND APPORTIONMENT OF INCOME Reg. 1.5833-1 (Effective for tax years beginning on and after January 1, 1998) Allocation and apportionment of Vermont net income by corporations (a)

AGATE FIRE PROTECTION DISTRICT RESOLUTION NO. 11-0908 A RESOLUTION OF THE AGATE FIRE PROTECTION DISTRICT BOARD OF

RESOLUTION NO. 11-0908 A RESOLUTION OF THE AGATE FIRE PROTECTION DISTRICT BOARD OF DIRECTORS ADOPTING A CAPITALIZATION POLICY WHEREAS, the Governmental Accounting Standards Board issued Pronouncement #34

RESOLUTION NO. 11-0908 A RESOLUTION OF THE AGATE FIRE PROTECTION DISTRICT BOARD OF DIRECTORS ADOPTING A CAPITALIZATION POLICY WHEREAS, the Governmental Accounting Standards Board issued Pronouncement #34

Construction Contracts

Compiled Accounting Standard AASB 111 Construction Contracts This compiled Standard applies to annual reporting periods beginning on or after 1 January 2009 that end on or after 30 June 2009. Early application

Compiled Accounting Standard AASB 111 Construction Contracts This compiled Standard applies to annual reporting periods beginning on or after 1 January 2009 that end on or after 30 June 2009. Early application

PHADA s 2009 Commissioners Conference. San Diego, CA Monday, January 26, 2009

PHADA s 2009 Commissioners Conference San Diego, CA Monday, January 26, 2009 Low-Income Housing Tax Credit Advanced Issues George F. Littlejohn, CPA george.littlejohn@novoco.com Robert S. Thesman, CPA

PHADA s 2009 Commissioners Conference San Diego, CA Monday, January 26, 2009 Low-Income Housing Tax Credit Advanced Issues George F. Littlejohn, CPA george.littlejohn@novoco.com Robert S. Thesman, CPA

The Town of Fort Frances POLICY SECTION ACCOUNTING FOR TANGIBLE CAPITAL ASSETS. ADMINISTRATION AND FINANCE NEW: May 2009 1. PURPOSE: 2.

The Town of Fort Frances ACCOUNTING FOR TANGIBLE CAPITAL ASSETS SECTION ADMINISTRATION AND FINANCE NEW: May 2009 REVISED: POLICY Resolution Number: 05/09 Consent 156 Policy Number: 1.18 PAGE 1 of 11 Supercedes

The Town of Fort Frances ACCOUNTING FOR TANGIBLE CAPITAL ASSETS SECTION ADMINISTRATION AND FINANCE NEW: May 2009 REVISED: POLICY Resolution Number: 05/09 Consent 156 Policy Number: 1.18 PAGE 1 of 11 Supercedes

OPERATING FUND. PRELIMINARY & UNAUDITED FINANCIAL HIGHLIGHTS September 30, 2015 RENDELL L. JONES CHIEF FINANCIAL OFFICER

PRELIMINARY & UNAUDITED FINANCIAL HIGHLIGHTS September 30, 2015 RENDELL L. JONES CHIEF FINANCIAL OFFICER MANAGEMENT OVERVIEW September 30, 2015 Balance Sheet Cash and cash equivalents had a month-end balance

PRELIMINARY & UNAUDITED FINANCIAL HIGHLIGHTS September 30, 2015 RENDELL L. JONES CHIEF FINANCIAL OFFICER MANAGEMENT OVERVIEW September 30, 2015 Balance Sheet Cash and cash equivalents had a month-end balance

Analysis One Code Desc. Transaction Amount. Fiscal Period

Analysis One Code Desc Transaction Amount Fiscal Period 57.63 Oct-12 12.13 Oct-12-38.90 Oct-12-773.00 Oct-12-800.00 Oct-12-187.00 Oct-12-82.00 Oct-12-82.00 Oct-12-110.00 Oct-12-1115.25 Oct-12-71.00 Oct-12-41.00

Analysis One Code Desc Transaction Amount Fiscal Period 57.63 Oct-12 12.13 Oct-12-38.90 Oct-12-773.00 Oct-12-800.00 Oct-12-187.00 Oct-12-82.00 Oct-12-82.00 Oct-12-110.00 Oct-12-1115.25 Oct-12-71.00 Oct-12-41.00

Benefits of Cost Segregation on Cancer Treatment Facilities

WHITE PAPER: Benefits of Cost Segregation on Cancer Treatment Facilities Executive Summary Appropriately conceived and implemented tax strategies create direct measurable financial benefits on the total

WHITE PAPER: Benefits of Cost Segregation on Cancer Treatment Facilities Executive Summary Appropriately conceived and implemented tax strategies create direct measurable financial benefits on the total

FORM FILLING INSTRUCTIONS GENERAL COMMERCIAL SURVEY

Craven County Assessor s Office Commercial Property 2016 Income & Expense Survey Instructions PURPOSE OF GENERAL COMMERCIAL PROPERTY INCOME & EXPENSE SURVEY: This survey is intended to provide the Craven

Craven County Assessor s Office Commercial Property 2016 Income & Expense Survey Instructions PURPOSE OF GENERAL COMMERCIAL PROPERTY INCOME & EXPENSE SURVEY: This survey is intended to provide the Craven

Guidance under Section 1032 Relating to the Treatment of a Disposition by One Corporation of the Stock of Another Corporation in a Taxable Transaction

[4830-01-U] DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 1 [REG-106221-98] RIN 1545-AW53 Guidance under Section 1032 Relating to the Treatment of a Disposition by One Corporation of

[4830-01-U] DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 1 [REG-106221-98] RIN 1545-AW53 Guidance under Section 1032 Relating to the Treatment of a Disposition by One Corporation of

Mortgage Forgiveness Debt Relief Act of 2007

2007 California Wildfires Disaster Tax Issues Presidentially Declared Disaster Areas Anna Maria Galdieri is a CPA in Oakland, California. She developed her expertise in the area of disaster tax law working

2007 California Wildfires Disaster Tax Issues Presidentially Declared Disaster Areas Anna Maria Galdieri is a CPA in Oakland, California. She developed her expertise in the area of disaster tax law working

Many real property owners lease out a portion

March April 2012 Like-Kind Exchange Corner By Mary B. Foster Exchanging Out of an Income Stream: New Ruling May Be Useful for Code Sec. 1031 Exchanges of Cell Phone Tower Leases Mary B. Foster is President

March April 2012 Like-Kind Exchange Corner By Mary B. Foster Exchanging Out of an Income Stream: New Ruling May Be Useful for Code Sec. 1031 Exchanges of Cell Phone Tower Leases Mary B. Foster is President

Annual Banking Workshop Tax Update

Jeffrey A. Ring, CPA, MST Annual Banking Workshop Tax Update berrydunn.com ON TRACK WITH YOUR AGENDA Review of recent guidance, tax credits, BASEL III tax computations and state nexus matters Bad Debt

Jeffrey A. Ring, CPA, MST Annual Banking Workshop Tax Update berrydunn.com ON TRACK WITH YOUR AGENDA Review of recent guidance, tax credits, BASEL III tax computations and state nexus matters Bad Debt

Tax rules for bond investors

Tax rules for bond investors Understand the treatment of different bonds Paying taxes is an inevitable part of investing for most bondholders, and understanding the tax rules, and procedures can be difficult

Tax rules for bond investors Understand the treatment of different bonds Paying taxes is an inevitable part of investing for most bondholders, and understanding the tax rules, and procedures can be difficult

Private Activity Bond Authority Manufacturing Facility Application Guidelines Utah Governor's Office of Economic Development

Private Activity Bond Authority Manufacturing Facility Application Guidelines Utah Governor's Office of Economic Development Introduction of Private Activity Bond Review Board The State of Utah created

Private Activity Bond Authority Manufacturing Facility Application Guidelines Utah Governor's Office of Economic Development Introduction of Private Activity Bond Review Board The State of Utah created

FULLER LANDAU LLP. Tax Return Questionnaire - 2014 Tax Year. Name and Address: Social Security Occupation Number:

FULLER LANDAU LLP Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return

FULLER LANDAU LLP Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return

Jon Buschke 3059 Austin Ave Simi Valley, CA 93063 (805) 813-1647 jbuschke@hotmail.com

813-1647 jbuschke@hotmail.com") PDF Raw Data < B Na ec Solar Lease Quote Prepared For: Jon Buschke 3059 Austin Ave Simi Valley, CA 93063 (805) 813-1647 jbuschke@hotmail.com Prepared By: Michael Garcia Solarology 2524 Townsgate rd unit

PDF Raw Data < B Na ec Solar Lease Quote Prepared For: Jon Buschke 3059 Austin Ave Simi Valley, CA 93063 (805) 813-1647 jbuschke@hotmail.com Prepared By: Michael Garcia Solarology 2524 Townsgate rd unit

Home Mortgage Interest Deduction

Department of the Treasury Internal Revenue Service Publication 936 Cat.. 10426G Home Mortgage Interest Deduction For use in preparing 1998 Returns Contents Introduction... 1 Part I: Home Mortgage Interest...

Department of the Treasury Internal Revenue Service Publication 936 Cat.. 10426G Home Mortgage Interest Deduction For use in preparing 1998 Returns Contents Introduction... 1 Part I: Home Mortgage Interest...

CASTLE ROCK TAX INFO & LINKS

CASTLE ROCK TAX INFO & LINKS Colorado Sales Tax Information (See attached below) (Business & Tax Licensing Information below was condensed for your convenience from this link: http://crgov.com/index.aspx?nid=1513

CASTLE ROCK TAX INFO & LINKS Colorado Sales Tax Information (See attached below) (Business & Tax Licensing Information below was condensed for your convenience from this link: http://crgov.com/index.aspx?nid=1513

BY ERIC P. WALLACE. Numerous Choices? Maybe!

BY ERIC P. WALLACE Construction is one of the most difficult industries to understand from a tax perspective. Here s why: 1) The number of available tax methods, each with revenue and cost recognition

BY ERIC P. WALLACE Construction is one of the most difficult industries to understand from a tax perspective. Here s why: 1) The number of available tax methods, each with revenue and cost recognition

Instructions for Form 8582-CR (Rev. December 2010)

") Instructions for Form 8582-CR (Rev. December 2010) For use with Form 8582 CR (Rev. December 2009) Passive Activity Credit Limitations Department of the Treasury Internal Revenue Service Section references

Instructions for Form 8582-CR (Rev. December 2010) For use with Form 8582 CR (Rev. December 2009) Passive Activity Credit Limitations Department of the Treasury Internal Revenue Service Section references

DESCRIPTION OF THE PLAN

DESCRIPTION OF THE PLAN PURPOSE 1. What is the purpose of the Plan? The purpose of the Plan is to provide eligible record owners of common stock of the Company with a simple and convenient means of investing

DESCRIPTION OF THE PLAN PURPOSE 1. What is the purpose of the Plan? The purpose of the Plan is to provide eligible record owners of common stock of the Company with a simple and convenient means of investing

26 CFR 1.263(a)-1: Capital expenditures; in general. (Also 162, 165, 167, 263A; 1.165-3, 1.167(a)-8, 1.167(a)-11, 1.263A-1)

-1: Capital expenditures; in general. (Also 162, 165, 167, 263A; 1.165-3, 1.167(a)-8, 1.167(a)-11, 1.263A-1)") Part I Section 263. Capital Expenditures 26 CFR 1.263(a)-1: Capital expenditures; in general. (Also 162, 165, 167, 263A; 1.165-3, 1.167(a)-8, 1.167(a)-11, 1.263A-1) Rev. Rul. 2000-7 ISSUE If the retirement

Part I Section 263. Capital Expenditures 26 CFR 1.263(a)-1: Capital expenditures; in general. (Also 162, 165, 167, 263A; 1.165-3, 1.167(a)-8, 1.167(a)-11, 1.263A-1) Rev. Rul. 2000-7 ISSUE If the retirement

Financial Accounting and Reporting Exam Review. Fixed Assets. Chapter Five. Black CPA Review www.blackcpareview.com Chapter 5

Fixed Assets Chapter Five Black CPA Review www.blackcpareview.com Chapter 5 Objectives: Objective 1: Know which costs associated with the purchase of fixed assets are capitalized Objective 2: Understand

Fixed Assets Chapter Five Black CPA Review www.blackcpareview.com Chapter 5 Objectives: Objective 1: Know which costs associated with the purchase of fixed assets are capitalized Objective 2: Understand

New FASB guidance, IRS and Court rulings address tax accounting method issues

Accounting Methods Spotlight / Issue 8 / August 2014 Did you know? p1 / Other guidance p2/ Cases p5 New FASB guidance, IRS and Court rulings address tax accounting method issues In this month s issue,

Accounting Methods Spotlight / Issue 8 / August 2014 Did you know? p1 / Other guidance p2/ Cases p5 New FASB guidance, IRS and Court rulings address tax accounting method issues In this month s issue,

Small Business Tax Saving Strategies for the 2012 Filing Season

Small Business Tax Saving Strategies for the 2012 Filing Season Few business sectors embody today s entrepreneurial spirit, drive for innovation and unwavering perseverance more than the small business

Small Business Tax Saving Strategies for the 2012 Filing Season Few business sectors embody today s entrepreneurial spirit, drive for innovation and unwavering perseverance more than the small business

Pre-Existing Structures at the Site Project Duration Type of Structure Under Construction Any Other Entities with Interests in the Property

Speakers: Vice President, Global Risk Management & Insurance Starwood Hotels & Resorts Worldwide Senior Vice President - National Director National Property Claims - Strategic Outcomes Practice Willis

Speakers: Vice President, Global Risk Management & Insurance Starwood Hotels & Resorts Worldwide Senior Vice President - National Director National Property Claims - Strategic Outcomes Practice Willis

Assuming office supplies are charged to the Office Supplies inventory account when purchased:

Adjusting Entries Prepaid Expenses Second Bullet Example - Assuming office supplies are charged to the Office Supplies inventory account when purchased: Office supplies expense 7,800 Office supplies 7,800

Adjusting Entries Prepaid Expenses Second Bullet Example - Assuming office supplies are charged to the Office Supplies inventory account when purchased: Office supplies expense 7,800 Office supplies 7,800

2013 Ohio Small Business Investor Income Deduction

2013 Ohio Small Business Investor Income Deduction Instructions for Apportioning Business Income Solely for Purposes of Computing the Small Business Investor Income Deduction hio Department of Taxation

2013 Ohio Small Business Investor Income Deduction Instructions for Apportioning Business Income Solely for Purposes of Computing the Small Business Investor Income Deduction hio Department of Taxation

U.S. Income Tax Return for an S Corporation

Form 1120S U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is attaching Form 2553 to elect to be an S corporation. Information about Form 1120S and

Form 1120S U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is attaching Form 2553 to elect to be an S corporation. Information about Form 1120S and

1999 Instructions for Schedule E, Supplemental Income and Loss

1999 Instructions for Schedule E, Supplemental Income Loss Use Schedule E (Form 1040) to report income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, residual

1999 Instructions for Schedule E, Supplemental Income Loss Use Schedule E (Form 1040) to report income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, residual

How To Determine If A Computer Program Is A Copyright Right Or A Copyright Article

IRS Software Regulations for Purchasing Software from Foreign Vendors Reg 251520-96 - Sec. 1.861-18 Classification of transactions involving computer programs. (a) General -- (1) Scope. This section provides