ACCESS TO CAPITAL MARKETS FOR SMALL NEW ZEALAND EXPORTERS: IS THERE A MARKET FAILURE?

|

|

|

- Clarence Henry

- 8 years ago

- Views:

Transcription

1 ACCESS TO CAPITAL MARKETS FOR SMALL NEW ZEALAND EXPORTERS: IS THERE A MARKET FAILURE? Alex Sundakov and Ben Gerritsen Castalia Ben.gerritsen@castalia-advisors.com, ( ) Abstract This paper considers whether New Zealand s capital markets enable export businesses to grow effectively. We find that there are significant constraints facing smaller New Zealand exporters in raising capital for growth that are specific to the New Zealand environment, and are not faced by international firms. These constraints include thin domestic markets for venture capital and private equity, in the sense of a limited number of market participants, and high costs of accessing international capital markets, including the need to relocate their business to the investor s country of origin or the firm s target market. JEL Codes: G00, G20, G28 Keyword(s): Capital markets, finance, entrepreneurship Introduction and Background A common view held in the New Zealand business community is that our capital markets do not allow viable local businesses to access sufficient capital for growth. This paper examines the issue of access to capital for New Zealand firms looking to grow their business in overseas markets. We test whether the performance of New Zealand s capital markets is constraining business growth, and we suggest policy measures that might help to resolve any problems that are identified. We begin by setting out a framework for interpreting the results of this research. We examine what would constitute a failure of New Zealand s capital markets. We then describe the research methodology used to test whether New Zealand s capital markets are functioning well to enable viable New Zealand export businesses to grow. What constitutes a failure of New Zealand s capital markets? The first challenge in evaluating the performance of New Zealand s capital markets is to define what would constitute a market failure. Clearly, an inability to raise capital is not in itself conclusive evidence of a market failure. Difficulty in raising capital would also result from a well-functioning market if investment proposals were not well conceived, or if businesses had risks that were not adequately reflected in projected returns. In this report, we define market failure as being present when a New Zealand firm is unable to raise capital, or finds that the difficulties or delays in raising capital constrain growth where a similar venture would proceed unimpeded overseas. This establishes a benchmark for New Zealand s capital markets to operate as well as markets overseas. This benchmark can be linked with a sensible policy objective of providing local businesses with equal opportunities to expand compared to their foreign competitors, to ensure that New Zealand maintains a competitive and vibrant business environment. When evaluating the performance of New Zealand s capital markets, we also acknowledge that raising capital depends on expectations for returns held by business owners and prospective investors. For example, it is important not to discount the risk that Government programmes aimed at promoting access to finance may in fact distort capital markets by raising business expectations on the terms for providing capital. How do we assess the ability of New Zealand enterprises to access capital? In this research we have conducted a series of interviews with New Zealand businesses to obtain firsthand perspectives on the process of raising capital for export growth. A list of the questions asked in the interviews is provided as Attachment 1. These interviews do not provide a basis for quantitative analysis of capital access issues, but instead focus on obtaining unique insights into the most challenging aspects of raising capital, and how the process could be improved to unlock business potential. Interviewees were selected across a broad range of sectors to test whether firms operating in different sectors of the New Zealand economy face unique challenges in raising capital. Large exporters were excluded, with interviewees all employing less than 50 staff. Our sample includes recent start-ups as well as established local businesses, and deliberately includes both firms attempting to sell products overseas that are 1

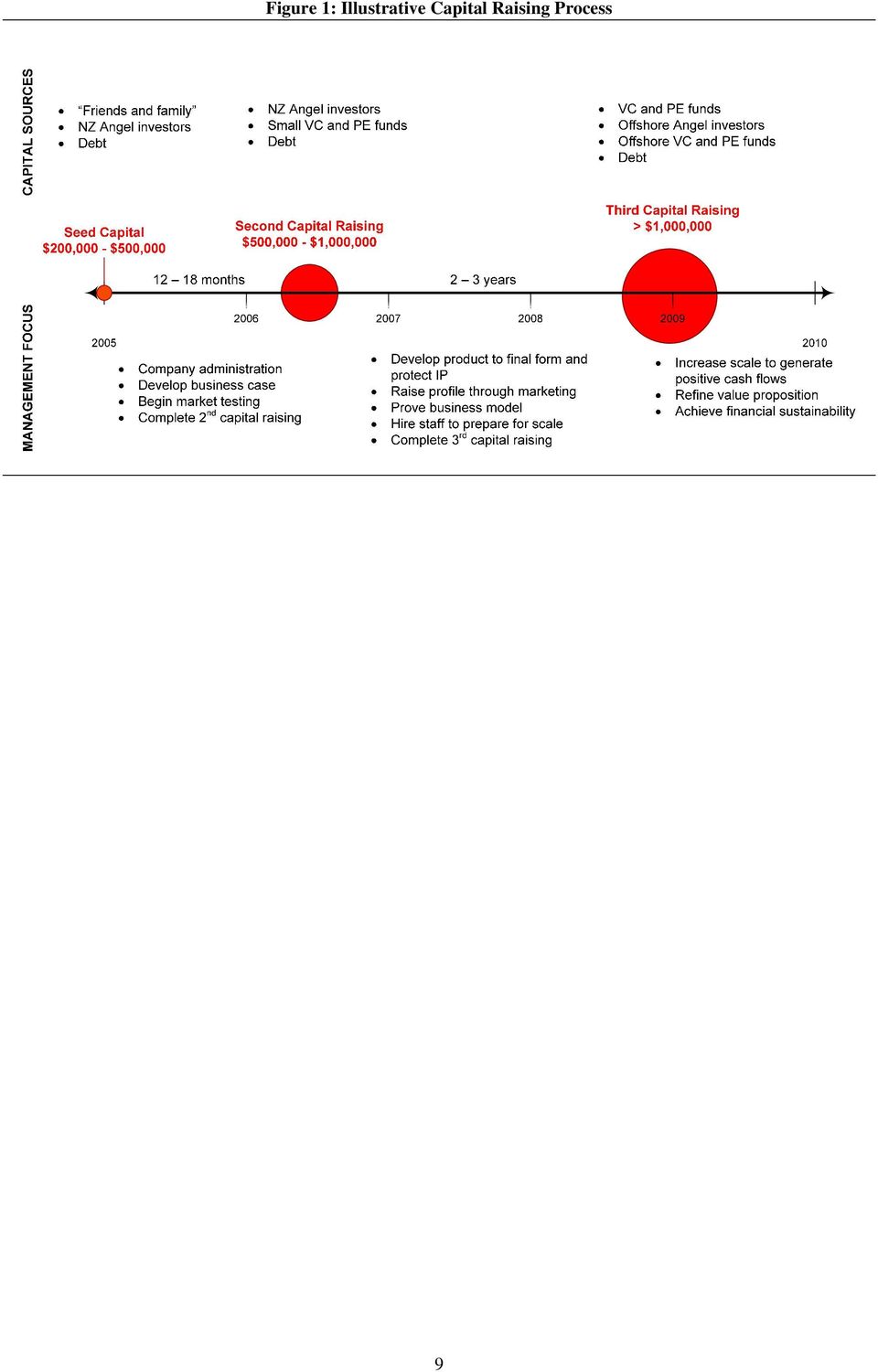

2 already successfully sold in New Zealand, and ventures involving new products for international markets. Specific examples from the interviews are used throughout this report to support the conclusions drawn. Where information provided in the interviews may be commercially sensitive, the interviewee is not named to protect commercial confidence. Different Capital Sources for Growth It is common to speak generally about capital as if all sources of capital are equal. In fact, different capital sources each have unique characteristics and challenges, which are described in this section. What different capital sources can be used to grow a business? Most firms initially rely on their retained earnings to fund organic growth. However, organic growth is usually tightly constrained, forcing firms to look for external sources of capital. Table 1 provides a brief description of the main sources of external capital, the risk appetite of the party providing the capital and a comment on perceived availability of each capital source. [Table 1 here] Which sources of capital are the most viable for growing an export business? We asked New Zealand businesses what their experience has been raising capital from the sources listed in Table 1. We specifically wanted to find out which capital sources are the most viable for funding expected export business growth, and which sources are not considered viable or attractive for this purpose. Relatively few export ventures reported an ability to raise debt for growth. Even businesses that have positive cash flows experience difficulties raising debt, with banks requiring ranking security on property (preferably real estate). Many firms had talked to commercial banks, but generally found no willingness to lend to the business without the security of personal guarantees or property mortgages. Several interviewees noted that venture capital was not a productive avenue for raising capital for their business. The reason is that the venture capital market in New Zealand is perceived as particularly thin and risk averse. Many businesses had heard of the Government initiative to match venture capital funding through the New Zealand Venture Investment Fund, although views on the effectiveness of NZVIF were mixed. Interviewees also noted that because of the fixed costs associated with due diligence, venture capital funds only seem to be interested in larger investments (more than $5 million). For most New Zealand start-up companies this investment is too large, meaning that venture capital funds tend to focus on more advanced (and possibly lower risk) companies. While angel investment has been used by many of the interviewees, perceptions on the value of angel capital are mixed. Some respondents value the corporate governance disciplines that angel investors introduce, and have appreciated an independent, objective opinion on their business. Other interviewees noted that the angel investor community in New Zealand is not effective in providing this independent voice because New Zealand angel investors are too busy with their own business endeavours. One respondent contrasted this to angel investment communities overseas, where the individuals involved are full time angels that contribute both their money and their smarts to maximise the value of their investment. For most businesses, angel investors are only useful in raising initial seed capital, and further growth calls for capital that exceeds the amount likely available from New Zealand angel investors. A few respondents noted that a public listing seemed less attractive as a way to raise capital or exit from an investment than other channels, such as trade sales and raising private capital. This reflects a perception that the fixed costs of listing (issuing a prospectus, complying with listing rules etc) may not be outweighed by the benefits, particularly in New Zealand where investors are seen as favouring traditional stocks to smaller, high-growth firms. Few firms had considered capital sources such as subordinated debt or more exotic financial instruments like debt factoring. This seems to reflect a lack of interest in fully investigating all capital sources which is perhaps not surprising, given the other management tasks undertaken in small New Zealand businesses with limited resources. Capital Raising Process Accessing capital is clearly only one aspect of growing a successful business. In this section, we consider how the process of raising capital fits in to the overall process of developing a successful business. How does the process of raising capital play out when developing a business? Every business is different, with different capital requirements and commercial strategies, and generalisations on a standard capital raising process are fraught with difficulty. Some ventures may only need to raise capital once, with future growth funded entirely from cash generated early in the company s life. Other firms may have several rounds of capital raising to keep management focused on proving a particular business model and to limit investor risks. Despite the unique process for raising capital followed by each business, many of the firms interviewed for this research recounted a capital raising process that shares several features. Figure 1 provides an illustrative example of capital raising requirements based on these shared experiences. This process includes three rounds of capital raising, with the amount raised growing on each occasion with the cost of the activities to be completed. The most likely capital sources for each round of capital raising are highlighted, although 2

3 there is scope to use any capital source at any time, provided that investors can be convinced of the value of the investment. [Figure 1 here] What are the main challenges in the process of raising capital? It is important not to be misled by the perceived formulaic and linear nature of the capital raising process shown in Figure 1. In fact, the process of raising capital is far from straightforward and several interviewees listed the ability to raise capital as the major constraint on their business growth. The first point to note is that the capital raising process can consume a significant amount of management and board time. Senior staff need to be involved in the process in order to present the company credibly to investors, and to develop the documentation that supports the funding pitch (including business plans, financial forecasts and investor presentations). Perversely, management time spent on capital raising can work against the probability of business success in the event that management effort is required in other areas to prove the business model. To overcome the imposition on management time, some businesses give responsibility for capital structure to a non-management representative, such a as non-executive director. This requires the current owners to trust the ability of the non-executive to effectively represent their interests, and may not be an option available to very small businesses. Other companies interviewed in this research received assistance from professional advisers in the capital raising process. This experience seems most valuable in presenting materials professionally and clearly, but requires the adviser to learn a great deal about the firm s value proposition and strategy to be most effective. A further challenge in the capital raising process is that delays are common. Investors will invariably recognise a value in waiting before committing their capital, while management will invariably need the capital as soon as possible. The effect of these non-aligned interests is that companies frequently need to alter their expenditure levels to avoid running out of cash prior to receiving a new injection of capital. This may not always be optimal from a business perspective, for example where a marketing campaign that relies on consistent brand visibility needs to be temporarily suspended. A third challenge in the capital raising process is to identify investors. Most businesses found that investors were not hard to identify in New Zealand, where the investor community is relatively small and professional networks commonly intersect. However, several businesses have found it difficult to identify the right investor that is, an investor with sector expertise, a shared passion for the business, a good strategic fit, and closely aligned values. Major Challenges to Accessing Capital In addition to questions of process, raising capital also involves a number of substantive challenges. In this section we discuss three challenges that featured prominently in the research interviews ensuring that the investment pitch is sound, that the right management team is in place, and that the business obtains the right mix of domestic and international capital. Establishing a Sound Business Model Most businesses interviewed for this research reported a good understanding of what goes into a good business plan senior personnel with business expertise and a track record of success, a strong value proposition, and an understanding of the target market. The challenge is to use the business plan to obtain firm investor commitments to provide capital. A winning business plan needs to address all those reasons an investor might say no, and present a compelling case that the capital will be used to add value over a given time horizon. In this environment, obtaining firm commitments from investors can take longer and require a more intensive effort from senior management than many businesses anticipate. Previous research identifies that small and medium sized enterprises in New Zealand lack investment ready capability, which is not surprising given the other demands on management time dealing with more day-to-day operational tasks. The businesses in this research that were most successful in raising capital identified that additional resources were needed to convince investors to participate in the company. One element of a sound business model that may not be well-understood by New Zealand businesses is investment exit. Several firms interviewed for this research had given little thought to how the business might be eventually sold. Exit possibilities should be presented to potential investors at the outset to highlight how the value of the investment (in addition to dividend payments) might be realised, including details on likely exit timeframes and potential buyers. Putting Effective Governance Arrangements in Place A second important challenge in raising capital is to put effective governance arrangements in place that ensure good decision-making. Many companies start out with very simple governance arrangements, with the Board of Directors consisting solely of the firm s management team. Independent governance is often introduced as a condition to raising capital from other investors, with new investors getting a seat on the Board. The presence of non-executive directors can help to inject some independent testing of management strategies, and provides an important monitoring capability for investors. A measure of independent governance also provides reassurance to potential new investors in the company that management is used to 3

4 having their ideas challenged, and can work effectively within a corporate decision-making framework. This can be challenging for entrepreneurs that have put significant sweat equity into developing the business concept and the strategy for growth. Investor-appointed Board members can also provide value by broadening the firm s understanding of market opportunities and facilitating beneficial relationships with other related companies. For example, one firm interviewed for this research noted that the independent directors appointed following a capital injection from a major venture capital fund provided additional channels to market and new supplier relationships that would not have otherwise been possible. The real challenge for New Zealand businesses is finding directors that are able to add value in this way. Most directors in New Zealand have professional backgrounds, and do not have experience with highrisk business ventures. Although these individuals understand financial issues and risk management, their skills may not be well-suited to maximising the value of dynamic, high growth companies. One interviewee noted that in his experience, most New Zealand directors are not able to perceive opportunity costs well, which leads to a counterproductive level of risk aversion. Choosing between Domestic and Offshore Capital Sources Several businesses interviewed for this research found that even with a sound business model and effective governance arrangements, they could not successfully raise the capital they needed for growth in New Zealand. Although not always their preferred course of action, these businesses have sought to raise required capital from off-shore investors. In this section we consider the reasons that New Zealand businesses are looking overseas for investors to support their growth ambitions, and the implications of bringing off-shore investors on board. We find that off-shore investors can add value to New Zealand business that may not be provided by investors based at home, but that a difficult condition attached to this value is that off-shore investors generally want the business relocated to their country of origin or the firm s main target market. Value created by bringing off-shore investors onboard The primary value in accessing capital from overseas sources is to ensure that businesses continue to operate despite a failure to raise funds in New Zealand. At least three of the firms interviewed for this research reported that overseas investment into their business was essential due to a failure to raise sufficient funding through New Zealand s capital markets. This suggests that New Zealand s capital markets are not reaching the benchmark of operating as well as capital markets overseas. Several businesses reported that they only started to look off-shore for investors once the opportunities in New Zealand had been largely exhausted. However, once their attention turned to the prospect of obtaining off-shore investment, several interviewees reported that the value of broadening their investment base became apparent. In particular, businesses noted that off-shore investment can add value through: Global connectivity Overseas equity providers also invest in other related firms, and can exploit these direct relationships for marketing purposes, supply channels and to tap into networks that will help the business succeed Sector expertise Particularly in areas that are not well established in New Zealand, such as the technology sector, overseas investors know the major issues facing the company and know the right questions to ask Opportunities for exit Off-shore investors have close ties within global investor networks that are much larger than the networks of New Zealand investors. Because all investors are interested in receiving the highest return possible on their investment, off-shore investors will use their networks to scope out the best opportunities for selling the business PR value and credibility Many large overseas investors have successfully grown businesses before, and therefore have a level of credibility in the marketplace that is not true of New Zealand investors. There can be an inherent value of having a well-regarded investor supporting the business. Trade-offs involved with off-shore ownership Given the benefits that can be unlocked by overseas investors, we might expect more New Zealand businesses to raise capital from off-shore sources. However, a major consideration for many New Zealand businesses is that off-shore investors generally want their target companies to relocate to their country of origin, particularly when the investor is based in the firm s target market. There are several reasons why off-shore investors insist on relocating the business. The first is so that management and sales teams are close to their target markets. Simply put, many offshore investors perceive no value in having a firm based in New Zealand if their customers are based in the United States or Europe. Investors may also want to be able to exercise a degree of control and monitoring that is not possible at a great distance. Perhaps the most significant reason for relocating New Zealand businesses in the eyes of off-shore investors is to maximise opportunities for exit. Selling a business is easier, and likely to generate higher returns, if the business is accessible to potential investors. This is not simply a matter of perception. There are substantial fixed costs in conducting buyer due diligence, and investors will be reluctant to expend additional money and effort to investigate a purchase based elsewhere. In 4

5 contrast, if the business is located near potential buyers then management can be on hand as required to resolve queries and showcase the firm s competencies and progress. Policy Proposals to Improve Access to Capital The difficulties experienced by New Zealand export businesses in raising domestic capital indicate that policy changes may be required to improve the conditions for enabling business growth. Policy proposals should be directed towards addressing specific problems which prevent local businesses from enjoying the same opportunities that overseas firms have to expand, while also allowing businesses to remain in New Zealand. In some cases, the barriers may be insurmountable, and an attempt to intervene in the market to offset such a barrier could work against the objective of ensuring that New Zealand maintains a competitive and vibrant business environment. Hence, any policy interventions need to be cautious and informed by market realities. In this section we consider three possible policy responses to the market failure identified in this paper. We first consider whether policy can facilitate a deeper capital market in New Zealand that would allow firms to raise needed capital domestically. We then consider ways that policy can respond to the problem of New Zealand firms moving overseas, while retaining the benefits of off-shore investment in our companies. Finally, we discuss other measures that have been proposed to tap into the New Zealand investor community living overseas. Measures to deepen New Zealand s capital markets This research has identified a concern for policy makers that New Zealand does not have enough domestic investors with specialised skills and the right risk appetite looking to place in capital in business opportunities. The New Zealand Government has recently considered how domestic capital markets might be improved as part of the Capital Markets Development Task Force. Many of the issues discussed in Task Force Report were raised in interviews with New Zealand businesses. In particular, one of the key recommendations of the Task Force was that tax and regulatory biases between different types of investment (for example, property versus financial assets) be eliminated. Interviewees confirmed that a bias exists towards property investment due to tax treatment and depreciation that has adverse impacts on the availability of capital for business growth. Removing tax advantages for property investors will at least indirectly help to deepen New Zealand s capital markets as more liquidity flows into other forms of investment the incentives to gear up skills and personnel and chase investment opportunities will become stronger. Several businesses also noted the potential for the New Zealand Superannuation Fund ( the Super Fund ) and managed Kiwisaver funds to deepen the availability of capital for New Zealand businesses. The Task Force report encourages continued Government support for initiatives of the Super Fund to investigate opportunities to invest in New Zealand companies to help build capability and scale in domestic capital markets. Measures to avoid the systematic relocation of New Zealand businesses The second area where policy changes could improve access to capital is through measures directed at the relocation of New Zealand businesses following capital contributions from off-shore investors. To overcome the desire of off-shore investors to relocate New Zealand companies, investors need to perceive some value in companies remaining in New Zealand. A small proportion of businesses are able to demonstrate an inherent value to remaining in New Zealand, for example due to a need to maintain close links with South East Asia or leveraging New Zealand s positive environmental reputation. However, the experience of businesses interviewed in this research suggests that something more is required to broaden the capacity of firms to credibly make a case for remaining in New Zealand (and enabling a greater share of the economic benefits of corporate success to remain in New Zealand). A further value to remaining in New Zealand is to stay within a sector cluster, where companies benefit from close proximity to each other through sharing of ideas, technologies and a pool of labour. Such clusters as in the case of the software sector in Israel or business process sector in India allow domestic businesses to attract international investors without relocating. For the most part, clusters are not deliberately created through policy. However, some interventions may facilitate the development of clusters when the right conditions are in place. One interviewee highlighted that the two conditions for an effective cluster may be strong domestic competition and demanding customers. An obvious possibility for a New Zealand business cluster exists in the agricultural sector where both of these conditions appear to hold. Policies to support and grow such clusters may help to overcome the conveyor belt effect of New Zealand companies moving overseas. A further view emerging from the interviews with New Zealand businesses is that policies to broaden partnerships with overseas investor communities would help to build international understanding and confidence in the value of New Zealand-based business. Conclusions The first conclusion from this research is that there are very real barriers to raising capital in New Zealand to grow an export business, and the capital that is 5

6 available tends to flow towards investments with a lower risk profile banks lend to businesses that provide personal guarantees and property as security, while venture capital funds generally seek businesses that already have positive cash flows. This appears to differ from the situation in other countries, such as United States or Australia, suggesting that New Zealand does not meet the benchmark of having capital markets that operate as well as markets overseas. The effect of our thin capital markets is that locally based export businesses may not have opportunities to expand that are comparable with their overseas competitors, which poses risks to maintaining a competitive and vibrant business environment in New Zealand. Our thin capital markets could lead to a conveyor belt effect where successful New Zealand firms are required to relocate off-shore particularly to the United States where investors and consumers reside. In reality, New Zealand firms will seek capital in overseas markets even if domestic capital is available. Off-shore investors can add significant value due to their highly specialise sector expertise and business networks, and ability to maximise the value of exit opportunities. The view emerging from this research suggests that sensible policies should therefore be directed a deepening New Zealand s capital markets, while at the same time giving off-shore investors good reasons for leaving the business in New Zealand. Proposed changes to tax and investment incentives could help to level the playing field between business and property investment, and initiatives such as the New Zealand Superannuation Fund could also help deepen our capital markets. There is also some evidence to suggest that off-shore investors can be convinced of the value of having businesses remain in New Zealand, where our country has an international reputation for excellence or a natural competitive advantage such as in the agribusiness and agritech sectors. 6

7 Attachment 1: List of Research Interview Questions Background Company name Relevant sector Business model Location of offices Location of affiliates Years in operation Staff numbers Annual turnover (revenue) Ownership Management structure and expertise Governance board composition, independence, expertise Export operations Proportion of the company s turnover relating to products or services provided outside New Zealand (i.e. size of the export business relative to the total business) Main export markets targeted Characterisation of underlying strategy for export business: Sell the same product internationally as is offered in New Zealand? Innovate for international markets based on competencies established in New Zealand market Record of export business growth: Over the history of the firm? Over the past 12 months? Expectations for growth in export markets: Over next 12 months? Over next 5 years? Most challenging issues facing export business Experiences with capital raising Firm s history of raising capital (debt and equity): Seed funding Capital for further growth / achieving scale Has the growth of the firm (and in particular the firm s export business) been constrained due to a lack of available capital? What are the most viable capital sources for funding expected growth in export business, and why? What methods of raising capital are not viable or attractive for funding expected growth in export business, and why? What are the most important features of your business and governance arrangements for raising additional capital from: Equity investors (angel investors, venture capital funds, overseas investors, private equity funds)? Debt providers (banks and providers of subordinated debt)? Grant funding providers? What options exist for making capital more readily available for New Zealand businesses looking to grow their business in overseas markets? 7

8 Table 1: Overview of Capital Sources Capital Source Description Risk Appetite in New Zealand Senior debt Subordinated debt Private equity (PE) Venture capital (VC) Angel investment (including friends and family ) Other Capital provided on basis of fixed return to lender Lender has priority in the event of business failure Debt with lower priority than senior debt in the event of business failure Examples include convertible notes and mezzanine debt Capital provided in exchange for shareholding in company Target mature investments that are able to generate positive cash flows Capital provided in exchange for shareholding in company Target start-up companies that are beginning to generate positive cash flows Capital provided in exchange for shareholding in company Target very early stage investments that may be cash flow negative Grant funding Public listing (IPO) Very Low Low Moderate Moderate (lower than for VC in other countries) High N/A Availability Generally not available without guarantee over real property Does not appear to be widely used by small export companies in New Zealand Some PE firms are active in New Zealand Most do not invest in cash flow negative, start-up companies Limited number of funds in New Zealand, large number overseas Can leverage Government NZVIF Small network in New Zealand that syndicates Huge network overseas, particularly in the United States NZTE grants are widely used IPOs are not common in New Zealand 8

9 Figure 1: Illustrative Capital Raising Process 9

for Analysing Listed Private Equity Companies

8 Steps for Analysing Listed Private Equity Companies Important Notice This document is for information only and does not constitute a recommendation or solicitation to subscribe or purchase any products.

8 Steps for Analysing Listed Private Equity Companies Important Notice This document is for information only and does not constitute a recommendation or solicitation to subscribe or purchase any products.

Financing a New Venture

Financing a New Venture A Canadian Innovation Centre How-To Guide 1 Financing a new venture New ventures require financing to fund growth Forms of financing include equity (personal, family & friends,

Financing a New Venture A Canadian Innovation Centre How-To Guide 1 Financing a new venture New ventures require financing to fund growth Forms of financing include equity (personal, family & friends,

VENTURE CAPITAL 101 I. WHAT IS VENTURE CAPITAL?

VENTURE CAPITAL 101 I. WHAT IS VENTURE CAPITAL? Venture capital is money provided by an outside investor to finance a new, growing, or troubled business. The venture capitalist provides the funding knowing

VENTURE CAPITAL 101 I. WHAT IS VENTURE CAPITAL? Venture capital is money provided by an outside investor to finance a new, growing, or troubled business. The venture capitalist provides the funding knowing

The benefits of private equity investment

The benefits of private equity investment David Wilton, Chief Investment Officer, International Finance Corporation (IFC), looks at how private equity can be beneficial; the different investment strategies

The benefits of private equity investment David Wilton, Chief Investment Officer, International Finance Corporation (IFC), looks at how private equity can be beneficial; the different investment strategies

A PRACTICAL GUIDE TO VENTURE CAPITAL FUNDING FOR EARLY STAGE COMPANIES

A PRACTICAL GUIDE TO VENTURE CAPITAL FUNDING FOR EARLY STAGE COMPANIES A COURTESY GUIDE PREPARED BY SWAAB ATTORNEYS 2014 Introduction to venture capital investment Venture capital is money provided by

A PRACTICAL GUIDE TO VENTURE CAPITAL FUNDING FOR EARLY STAGE COMPANIES A COURTESY GUIDE PREPARED BY SWAAB ATTORNEYS 2014 Introduction to venture capital investment Venture capital is money provided by

Why Managed Funds Are One of Your Best Investment Options

Why Managed Funds Are One of Your Best Investment Options What Is A Managed Investment Fund and What are its Advantages? Managed funds are collective investments where a number of investors pool their

Why Managed Funds Are One of Your Best Investment Options What Is A Managed Investment Fund and What are its Advantages? Managed funds are collective investments where a number of investors pool their

To License a Patent or, to Assign it: Factors Influencing the Choice

To License a Patent or, to Assign it: Factors Influencing the Choice Philip Mendes Partner Innovation Law Level 3, 380 Queen Street Brisbane, QLD, Australia philip@innovatiuonlaw.com.au Introduction Other

To License a Patent or, to Assign it: Factors Influencing the Choice Philip Mendes Partner Innovation Law Level 3, 380 Queen Street Brisbane, QLD, Australia philip@innovatiuonlaw.com.au Introduction Other

Understanding a Firm s Different Financing Options. A Closer Look at Equity vs. Debt

Understanding a Firm s Different Financing Options A Closer Look at Equity vs. Debt Financing Options: A Closer Look at Equity vs. Debt Business owners who seek financing face a fundamental choice: should

Understanding a Firm s Different Financing Options A Closer Look at Equity vs. Debt Financing Options: A Closer Look at Equity vs. Debt Business owners who seek financing face a fundamental choice: should

Report of the Alternative Investment Expert Group: Developing European Private Equity

Report of the Alternative Investment Expert Group: Developing European Private Equity Response from The Association of Investment Trust Companies The Association of Investment Trust Companies (AITC) welcomes

Report of the Alternative Investment Expert Group: Developing European Private Equity Response from The Association of Investment Trust Companies The Association of Investment Trust Companies (AITC) welcomes

Section A Introduction This section asks for information that aims to identify the independence and ownership situation of your business.

Access to Finance Purpose of this survey Access to finance is crucial to business success and an important factor for economic growth in Europe following the economic crisis in 2007. The purpose of this

Access to Finance Purpose of this survey Access to finance is crucial to business success and an important factor for economic growth in Europe following the economic crisis in 2007. The purpose of this

1. Introduction. For further information contact; Donnchadh Cullinan Manager, Banking Relationships & Growth Capital Department +353 1 727 2162

Enterprise Ireland is the Government agency responsible for the development and growth of Irish enterprises in world markets. We work in partnership with Irish enterprises to help them start, grow, innovate

Enterprise Ireland is the Government agency responsible for the development and growth of Irish enterprises in world markets. We work in partnership with Irish enterprises to help them start, grow, innovate

Early Stage Funding. Dragon Law. This book is for sale at http://leanpub.com/earlystagefunding. This version was published on 2015-12-09

Early Stage Funding Dragon Law This book is for sale at http://leanpub.com/earlystagefunding This version was published on 2015-12-09 This is a Leanpub book. Leanpub empowers authors and publishers with

Early Stage Funding Dragon Law This book is for sale at http://leanpub.com/earlystagefunding This version was published on 2015-12-09 This is a Leanpub book. Leanpub empowers authors and publishers with

Self Managed Super Funds Take charge

Self Managed Super Funds Take charge Gain control of your financial future with a Self-Managed Super Fund (SMSF) About Markiewicz & Co. Markiewicz & Co. is one of Australia s leading full service investment

Self Managed Super Funds Take charge Gain control of your financial future with a Self-Managed Super Fund (SMSF) About Markiewicz & Co. Markiewicz & Co. is one of Australia s leading full service investment

ELEFTHO : Supporting Business Incubators & technology parks.

ELEFTHO : Supporting Business Incubators & technology parks. Region of Central Macedonia Task Page 1 of 14 Contents Description of policy... 3 Name of the policy... 3 Responsible body... 3 Implementation

ELEFTHO : Supporting Business Incubators & technology parks. Region of Central Macedonia Task Page 1 of 14 Contents Description of policy... 3 Name of the policy... 3 Responsible body... 3 Implementation

Hon Dr Michael Cullen Minister of Finance

Hon Dr Michael Cullen Minister of Finance Pro-business tax cuts: background information Fairer rules on taxing investment income New rules will make the taxation of income from investment through managed

Hon Dr Michael Cullen Minister of Finance Pro-business tax cuts: background information Fairer rules on taxing investment income New rules will make the taxation of income from investment through managed

Note on Private Equity Deal Structures

Case # 5-0006 Updated January 12, 2005 Note on Private Equity Deal Structures Introduction Term Sheets are brief preliminary documents designed to facilitate and provide a framework for negotiations between

Case # 5-0006 Updated January 12, 2005 Note on Private Equity Deal Structures Introduction Term Sheets are brief preliminary documents designed to facilitate and provide a framework for negotiations between

Raise Venture Capital

Raise Venture Capital How can we help? Our mission is to transform equity raising businesses into first class investor ready companies. Venture funded companies outperform non-venture backed firms by more

Raise Venture Capital How can we help? Our mission is to transform equity raising businesses into first class investor ready companies. Venture funded companies outperform non-venture backed firms by more

Financing your business. Dr. T. R. Heidrick Poole Professor in Technology Management Faculty of Engineering/School of Business U of A

Financing your business Dr. T. R. Heidrick Poole Professor in Technology Management Faculty of Engineering/School of Business U of A Risk Capital ct. d Earns returns through participation in the future

Financing your business Dr. T. R. Heidrick Poole Professor in Technology Management Faculty of Engineering/School of Business U of A Risk Capital ct. d Earns returns through participation in the future

Overseas Direct Investment ANALYSIS & INSIGHTS

Overseas Direct Investment ANALYSIS & INSIGHTS What is overseas direct investment (ODI)? ODI refers to investment by Australian companies in business operations overseas. This can take the form of a new

Overseas Direct Investment ANALYSIS & INSIGHTS What is overseas direct investment (ODI)? ODI refers to investment by Australian companies in business operations overseas. This can take the form of a new

Managing Cash Flow & Accessing Finance

Managing Cash Flow & Accessing Finance A Presentation by Clive Lewis, Head of Enterprise, Institute of Chartered Accountants in England & Wales (ICAEW) Managing Cash Flow & Accessing Finance Presentation

Managing Cash Flow & Accessing Finance A Presentation by Clive Lewis, Head of Enterprise, Institute of Chartered Accountants in England & Wales (ICAEW) Managing Cash Flow & Accessing Finance Presentation

5. Funding Available for IP-Rich Businesses

20 IP Finance Toolkit 5. Funding Available for IP-Rich Businesses Introduction As the Banking on IP? report notes; SMEs first port of call for finance is often a bank. Figures quoted in the report show

20 IP Finance Toolkit 5. Funding Available for IP-Rich Businesses Introduction As the Banking on IP? report notes; SMEs first port of call for finance is often a bank. Figures quoted in the report show

Insufficient Cash On Hand A Frequent Reason For Needing A Business Loan

Insufficient Cash On Hand A Frequent Reason For Needing A Business Loan 2 Cash flow is cash into or out of a business When cash inflows exceed cash outflows, it is generally indicative of good financial

Insufficient Cash On Hand A Frequent Reason For Needing A Business Loan 2 Cash flow is cash into or out of a business When cash inflows exceed cash outflows, it is generally indicative of good financial

INVESTMENT POLICY April 2013

Policy approved at 22 April 2013 meeting of the Board of Governors (Minute 133:4:13) INVESTMENT POLICY April 2013 Contents SECTION 1. OVERVIEW SECTION 2. INVESTMENT PHILOSOPHY- MAXIMISING RETURN SECTION

Policy approved at 22 April 2013 meeting of the Board of Governors (Minute 133:4:13) INVESTMENT POLICY April 2013 Contents SECTION 1. OVERVIEW SECTION 2. INVESTMENT PHILOSOPHY- MAXIMISING RETURN SECTION

Your bid for growth funds. Supporting your business with financing decisions

Your bid for growth funds Supporting your business with financing decisions Contents 3 Introduction 4 Preparing your application 6 Assessing applications 8 What Barclays considers 9 Funding solutions 10

Your bid for growth funds Supporting your business with financing decisions Contents 3 Introduction 4 Preparing your application 6 Assessing applications 8 What Barclays considers 9 Funding solutions 10

Chapter 7: Capital Structure: An Overview of the Financing Decision

Chapter 7: Capital Structure: An Overview of the Financing Decision 1. Income bonds are similar to preferred stock in several ways. Payment of interest on income bonds depends on the availability of sufficient

Chapter 7: Capital Structure: An Overview of the Financing Decision 1. Income bonds are similar to preferred stock in several ways. Payment of interest on income bonds depends on the availability of sufficient

Know o ing Y o Y ur r Options s & How to Access Them

Knowing Your Options & How to Access Them Funding Choices in Edinburgh & Scotland Type of Finance Investment Grants Loans Type of Finance Invoice Financing Owners Capital Cash From Profits Asset Finance

Knowing Your Options & How to Access Them Funding Choices in Edinburgh & Scotland Type of Finance Investment Grants Loans Type of Finance Invoice Financing Owners Capital Cash From Profits Asset Finance

The real value of corporate governance

Volume 9 No. 1 The real value of corporate governance (c) Copyright 2007, The University of Auckland. Permission to make digital or hard copies of all or part of this work for personal or classroom use

Volume 9 No. 1 The real value of corporate governance (c) Copyright 2007, The University of Auckland. Permission to make digital or hard copies of all or part of this work for personal or classroom use

MLC MasterKey Unit Trust Product Disclosure Statement (PDS)

") MLC MasterKey Unit Trust Product Disclosure Statement (PDS) Preparation date 1 July 2014 Issued by MLC Investments Limited (MLC) ABN 30 002 641 661 AFSL 230705 This information is general and doesn t take

MLC MasterKey Unit Trust Product Disclosure Statement (PDS) Preparation date 1 July 2014 Issued by MLC Investments Limited (MLC) ABN 30 002 641 661 AFSL 230705 This information is general and doesn t take

HMT Discussion paper on non-bank lending

17 February 2010 By e-mail to: non-banklending@hmtreasury.gsi.gov.uk Dear Sirs HMT Discussion paper on non-bank lending The IMA represents the UK-based investment management industry. Our members include

17 February 2010 By e-mail to: non-banklending@hmtreasury.gsi.gov.uk Dear Sirs HMT Discussion paper on non-bank lending The IMA represents the UK-based investment management industry. Our members include

RELEVANT TO ACCA QUALIFICATION PAPER F9. Studying Paper F9? Performance objectives 15 and 16 are relevant to this exam

RELEVANT TO ACCA QUALIFICATION PAPER F9 Studying Paper F9? Performance objectives 15 and 16 are relevant to this exam Business finance Section E of the Paper F9, Financial Management syllabus deals with

RELEVANT TO ACCA QUALIFICATION PAPER F9 Studying Paper F9? Performance objectives 15 and 16 are relevant to this exam Business finance Section E of the Paper F9, Financial Management syllabus deals with

Accessing Finance: A Guide for Food and Drink Companies

Accessing Finance: A Guide for Food and Drink Companies 2 1 loan bank equity FINANCE GROWTH Contents Page 1 Introduction 2 2 Types of Finance 4 2.1 Founder, Friends and Family 4 2.2 Equity Investors 5

Accessing Finance: A Guide for Food and Drink Companies 2 1 loan bank equity FINANCE GROWTH Contents Page 1 Introduction 2 2 Types of Finance 4 2.1 Founder, Friends and Family 4 2.2 Equity Investors 5

Finding sources of capital. Secured and unsecured borrowing Selling equity Government programs Frequently overlooked sources

Finding sources of capital BusineSS Coach series Secured and unsecured borrowing Selling equity Government programs Frequently overlooked sources Business Coach series The fundamentals of finance The situation

Finding sources of capital BusineSS Coach series Secured and unsecured borrowing Selling equity Government programs Frequently overlooked sources Business Coach series The fundamentals of finance The situation

Sources of finance (Or where can we get money from?)

") Sources of finance (Or where can we get money from?) Why do we need finance? 1. Setting up a business 2. Need to finance our day-to-day activities 3. Expansion 4. Research into new products 5. Special

Sources of finance (Or where can we get money from?) Why do we need finance? 1. Setting up a business 2. Need to finance our day-to-day activities 3. Expansion 4. Research into new products 5. Special

Kea Influencer Relations and Marketing for High-Tech & Technology Providers

Kea Analyst Relations Industry analysts play a key role in defining markets and educating buyers. We work with clients to identify and track the most influential and relevant industry analysts, and advise

Kea Analyst Relations Industry analysts play a key role in defining markets and educating buyers. We work with clients to identify and track the most influential and relevant industry analysts, and advise

Advanced Financial Management

Progress Test 2 Advanced Financial Management P4AFM-PT2-Z14-A Answers & Marking Scheme 2014 DeVry/Becker Educational Development Corp. Tutorial note: the answers below are more comprehensive than would

Progress Test 2 Advanced Financial Management P4AFM-PT2-Z14-A Answers & Marking Scheme 2014 DeVry/Becker Educational Development Corp. Tutorial note: the answers below are more comprehensive than would

Eurostat's 2010 Survey Questionnaire on Access to Finance

From: Entrepreneurship at a Glance 2012 Access the complete publication at: http://dx.doi.org/10.1787/entrepreneur_aag-2012-en Eurostat's 2010 Survey Questionnaire on Access to Finance Please cite this

From: Entrepreneurship at a Glance 2012 Access the complete publication at: http://dx.doi.org/10.1787/entrepreneur_aag-2012-en Eurostat's 2010 Survey Questionnaire on Access to Finance Please cite this

Secondary research into the availability of business finance

Secondary research into the availability of business finance NESTA The National Endowment for Science, Technology and the Arts (NESTA) is an independent body with a mission to make the UK more innovative.

Secondary research into the availability of business finance NESTA The National Endowment for Science, Technology and the Arts (NESTA) is an independent body with a mission to make the UK more innovative.

Initial Public Offering. Are you ready to float?

Initial Public Offering Are you ready to float? What is an IPO? Are you considering listing your company on a stock exchange? In recent times, the phrases listing and floating have been replaced with an

Initial Public Offering Are you ready to float? What is an IPO? Are you considering listing your company on a stock exchange? In recent times, the phrases listing and floating have been replaced with an

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute Other free books by BizMove that may interest you: Free starting a business books Free management skills

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute Other free books by BizMove that may interest you: Free starting a business books Free management skills

Key Steps Before Talking to Venture Capitalists

Key Steps Before Talking to Venture Capitalists Some entrepreneurs may not be familiar with raising institutional capital to grow their businesses. Expansion plans beyond common organic growth are typically

Key Steps Before Talking to Venture Capitalists Some entrepreneurs may not be familiar with raising institutional capital to grow their businesses. Expansion plans beyond common organic growth are typically

Meeting the Needs of Private Equity in the Finance Organization

Meeting the Needs of Private Equity in the Finance Organization When there is a change in a company s ownership, significant changes are generally required in its finance organization. This is especially

Meeting the Needs of Private Equity in the Finance Organization When there is a change in a company s ownership, significant changes are generally required in its finance organization. This is especially

The risks and benefits of shares

Course 3 The risks and benefits of shares Topic 1: The risks of shares... 3 The risks of shares... 3 The risk of capital loss... 3 Volatility risk... 4 The risk of poor quality advice... 4 Time for your

Course 3 The risks and benefits of shares Topic 1: The risks of shares... 3 The risks of shares... 3 The risk of capital loss... 3 Volatility risk... 4 The risk of poor quality advice... 4 Time for your

Morningstar Core Equities Portfolio

Morningstar Core Equities Portfolio Managed Portfolio Disclosure Document for members dated 29/02/2016. The Portfolio Manager is Morningstar Australasia Pty Limited (ABN 95 090 665 544, AFSL 240892). Issued

Morningstar Core Equities Portfolio Managed Portfolio Disclosure Document for members dated 29/02/2016. The Portfolio Manager is Morningstar Australasia Pty Limited (ABN 95 090 665 544, AFSL 240892). Issued

Privately held business: helping start-ups start up

Privately held business: helping start-ups start up Contents Introduction 3 Strategic planning: what s the big idea? 4 The business life cycle: where do you fit in? 6 Structure: start as you mean to go

Privately held business: helping start-ups start up Contents Introduction 3 Strategic planning: what s the big idea? 4 The business life cycle: where do you fit in? 6 Structure: start as you mean to go

Demand Dividend: Creating Reliable Returns in Impact Investing

Demand Dividend: Creating Reliable Returns in Impact Investing Demand Dividend is a debt vehicle designed to improve the repayment cycle for impact investors and ease capital access for social enterprises.

Demand Dividend: Creating Reliable Returns in Impact Investing Demand Dividend is a debt vehicle designed to improve the repayment cycle for impact investors and ease capital access for social enterprises.

Measures to support access to finance for SMEs. Funding for Lending... 2. The National Loan Guarantee Scheme (NLGS)... 2

... 2") Measures to support access to finance for SMEs Contents Funding for Lending... 2 The National Loan Guarantee Scheme (NLGS)... 2 Enterprise Finance Guarantee (EFG)... 3 Business Finance Partnership (BFP)...

Measures to support access to finance for SMEs Contents Funding for Lending... 2 The National Loan Guarantee Scheme (NLGS)... 2 Enterprise Finance Guarantee (EFG)... 3 Business Finance Partnership (BFP)...

INTEREST FREE NON REPAYABLE BUSINESS FUNDING. Charles Brooks Comprehensive BusinessManagement Ltd www.cbmgroup.co.uk

INTEREST FREE NON REPAYABLE BUSINESS FUNDING Charles Brooks Comprehensive BusinessManagement Ltd www.cbmgroup.co.uk 1 INTRODUCTION If you ve ever been involved in a start up venture you can probably remember

INTEREST FREE NON REPAYABLE BUSINESS FUNDING Charles Brooks Comprehensive BusinessManagement Ltd www.cbmgroup.co.uk 1 INTRODUCTION If you ve ever been involved in a start up venture you can probably remember

BUSINESS PLAN QUESTIONNAIRE

BUSINESS PLAN QUESTIONNAIRE Company Name: Business Owner Name(s): Address: Phone: E-mail: Fax: Web Site: Who is the primary audience for your business plan? Lenders Investors Internal Use MISSION/VISION/OBJECTIVES

BUSINESS PLAN QUESTIONNAIRE Company Name: Business Owner Name(s): Address: Phone: E-mail: Fax: Web Site: Who is the primary audience for your business plan? Lenders Investors Internal Use MISSION/VISION/OBJECTIVES

Frontier International

International research insights from Frontier Advisors Real Assets Research Team Issue 15, June 2015 Frontier regularly conducts international research trips to observe and understand more about international

International research insights from Frontier Advisors Real Assets Research Team Issue 15, June 2015 Frontier regularly conducts international research trips to observe and understand more about international

Funding Options In a commercial a few years ago, baseball legend and philosopher Yogi Berra said they give you cash, which is just as good as money. In typical Yogi fashion, there is some wisdom behind

Funding Options In a commercial a few years ago, baseball legend and philosopher Yogi Berra said they give you cash, which is just as good as money. In typical Yogi fashion, there is some wisdom behind

Business Studies - Financial Planning and Management Study Notes. Financial Planning and Management Study Notes:

Business Studies - Financial Planning and Management Study Notes Financial Planning and Management Study Notes: The Role of Financial Planning: The strategic role of financial management: Organisational

Business Studies - Financial Planning and Management Study Notes Financial Planning and Management Study Notes: The Role of Financial Planning: The strategic role of financial management: Organisational

R A I S I N G F U N D S I N SWEDEN

R A I S I N G F U N D S I N SWEDEN Raising funds in Sweden Sweden can offer good opportunities and many ways to raise finance for businesses. The costs of establishing a Swedish limited company are low

R A I S I N G F U N D S I N SWEDEN Raising funds in Sweden Sweden can offer good opportunities and many ways to raise finance for businesses. The costs of establishing a Swedish limited company are low

Guide to Public and Private Funding

Guide to Public and Private Funding Introduction to public and private funding Key Public Funding Opportunities Key Private Funding Opportunities Which funding opportunity is right for my business? Do

Guide to Public and Private Funding Introduction to public and private funding Key Public Funding Opportunities Key Private Funding Opportunities Which funding opportunity is right for my business? Do

Lecture 18 SOURCES OF FINANCE AND GOVERNMENT POLICIES

Lecture 18 SOURCES OF FINANCE AND GOVERNMENT POLICIES Learning Objectives Sources of finance for small and medium-sized businesses. Types of financial assistance Finance is needed throughout a company

Lecture 18 SOURCES OF FINANCE AND GOVERNMENT POLICIES Learning Objectives Sources of finance for small and medium-sized businesses. Types of financial assistance Finance is needed throughout a company

Public Debt and Cash Management

Federation of European Accountants Federation of European Accountants Fédération Fédération des Experts des Experts comptables comptables Européens Européens Public Sector Public Debt and Cash Management

Federation of European Accountants Federation of European Accountants Fédération Fédération des Experts des Experts comptables comptables Européens Européens Public Sector Public Debt and Cash Management

Accounting & Tax Services for Small Businesses

Accounting & Tax Services for Small Businesses Taxation Solutions Too many business owners fail to manage their tax position which often means they pay too much tax or unnecessarily incur fines and interest

Accounting & Tax Services for Small Businesses Taxation Solutions Too many business owners fail to manage their tax position which often means they pay too much tax or unnecessarily incur fines and interest

RISK DISCLOSURE STATEMENT

RISK DISCLOSURE STATEMENT You should note that there are significant risks inherent in investing in certain financial instruments and in certain markets. Investment in derivatives, futures, options and

RISK DISCLOSURE STATEMENT You should note that there are significant risks inherent in investing in certain financial instruments and in certain markets. Investment in derivatives, futures, options and

Raising Business Angel Investment. EBAN Institute Bootcamp Moscow 2 nd October 2013

Raising Business Angel Investment EBAN Institute Bootcamp Moscow 2 nd October 2013 Executive summary 1 2 3 Equity raising process Top three investment criteria Company executive summary Business plant

Raising Business Angel Investment EBAN Institute Bootcamp Moscow 2 nd October 2013 Executive summary 1 2 3 Equity raising process Top three investment criteria Company executive summary Business plant

Valuations. The Effect of the Credit Crunch, US Healthcare Reform and the Shortage of New Innovative Products. Medius Associates.

Licensing Valuations Deal The Effect of the Credit Crunch, US Healthcare Reform and the Shortage of New Innovative Products Medius Associates Roger Davies This article was borne from personal experience

Licensing Valuations Deal The Effect of the Credit Crunch, US Healthcare Reform and the Shortage of New Innovative Products Medius Associates Roger Davies This article was borne from personal experience

Investing in innovative companies How Private Equity think

Investing in innovative companies How Private Equity think Christer Nilsson Director 3i Nordic Date: 2010-11-25 www.3i.com (see also Nordic section) 1 2 I will cover Innovations? What is Private Equity?

Investing in innovative companies How Private Equity think Christer Nilsson Director 3i Nordic Date: 2010-11-25 www.3i.com (see also Nordic section) 1 2 I will cover Innovations? What is Private Equity?

Good Practice Checklist

Investment Governance Good Practice Checklist Governance Structure 1. Existence of critical decision-making bodies e.g. Board of Directors, Investment Committee, In-House Investment Team, External Investment

Investment Governance Good Practice Checklist Governance Structure 1. Existence of critical decision-making bodies e.g. Board of Directors, Investment Committee, In-House Investment Team, External Investment

Access to Finance Guide: 1. Bank Finance Options

Access to Finance Guide: 1. Bank Finance Options Overdrafts An overdraft is a flexible way for you to manage short-term borrowing requirements. Business overdrafts are traditionally easy to arrange and

Access to Finance Guide: 1. Bank Finance Options Overdrafts An overdraft is a flexible way for you to manage short-term borrowing requirements. Business overdrafts are traditionally easy to arrange and

BANKERS GUIDE TO SECURE LENDING

BANKERS GUIDE TO SECURE LENDING WAREHOUSE RECEIPTS, ORDER OR STRAIGHT BILLS OF LADING, OTHER NEGOTIABLE AND NON-NEGOTIABLE DOCUMENTS OF TITLE, INCLUDING WAREHOUSE AND BAILEE OR DOCK RECEIPTS Lending Rationale

BANKERS GUIDE TO SECURE LENDING WAREHOUSE RECEIPTS, ORDER OR STRAIGHT BILLS OF LADING, OTHER NEGOTIABLE AND NON-NEGOTIABLE DOCUMENTS OF TITLE, INCLUDING WAREHOUSE AND BAILEE OR DOCK RECEIPTS Lending Rationale

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

. Board Charter - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 1. Interpretation 1.1 In this Charter: Act means the Companies

. Board Charter - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 1. Interpretation 1.1 In this Charter: Act means the Companies

Creating growth Improving access to finance for UK creative industries

Brief March 2011 Creating growth Improving access to finance for UK creative industries Emma Wild knowledge economy group CBI email: emma.wild@cbi.org.uk Access to finance is essential for business growth.

Brief March 2011 Creating growth Improving access to finance for UK creative industries Emma Wild knowledge economy group CBI email: emma.wild@cbi.org.uk Access to finance is essential for business growth.

Support to business during a recession. Scheme outlines

Support to business during a recession Scheme outlines MARCH 2010 Contents Working Capital Scheme 1 Trade Credit Insurance Scheme 3 Enterprise Finance Guarantee Scheme 6 Capital for Enterprise Fund 9 Automotive

Support to business during a recession Scheme outlines MARCH 2010 Contents Working Capital Scheme 1 Trade Credit Insurance Scheme 3 Enterprise Finance Guarantee Scheme 6 Capital for Enterprise Fund 9 Automotive

By Alister Steele September 2012

A New Role for Housing Associations By Alister Steele September 2012 Introduction Housing association s core role is providing housing for those in greatest need underpinned by traditionally high levels

A New Role for Housing Associations By Alister Steele September 2012 Introduction Housing association s core role is providing housing for those in greatest need underpinned by traditionally high levels

Small/Mid-Cap Quality Strategy (including FPA Paramount Fund, Inc. and FPA Perennial Fund, Inc.)

") Small/Mid-Cap Quality Strategy (including FPA Paramount Fund, Inc. and FPA Perennial Fund, Inc.) Investment Policy Statement OVERVIEW Investment Objective and Strategy The primary objective of the FPA

Small/Mid-Cap Quality Strategy (including FPA Paramount Fund, Inc. and FPA Perennial Fund, Inc.) Investment Policy Statement OVERVIEW Investment Objective and Strategy The primary objective of the FPA

B R I E F I N G N O T E

B R I E F I N G N O T E FINANCING A BUSINESS CHOOSING THE RIGHT OPTION Background A small number of businesses are in the fortunate position of operating in a cash surplus with money in the bank. For the

B R I E F I N G N O T E FINANCING A BUSINESS CHOOSING THE RIGHT OPTION Background A small number of businesses are in the fortunate position of operating in a cash surplus with money in the bank. For the

An Introduction to Startup Financing and a New Approach to Attracting Capital Resources. Robert T. Goldberg, President StartupFactory, LLC

An Introduction to Startup Financing and a New Approach to Attracting Capital Resources. Robert T. Goldberg, President StartupFactory, LLC Quick Tips: When seeking startup funding it is critical to understand

An Introduction to Startup Financing and a New Approach to Attracting Capital Resources. Robert T. Goldberg, President StartupFactory, LLC Quick Tips: When seeking startup funding it is critical to understand

Study on Financing Growth Capital for SMEs

Study on Financing Growth Capital for SMEs Remarks by Marion G. Wrobel Vice-President, Policy and Operations Canadian Bankers Association for The Standing Senate Committee on Banking Trade and Commerce

Study on Financing Growth Capital for SMEs Remarks by Marion G. Wrobel Vice-President, Policy and Operations Canadian Bankers Association for The Standing Senate Committee on Banking Trade and Commerce

About Hedge Funds. What is a Hedge Fund?

About Hedge Funds What is a Hedge Fund? A hedge fund is a fund that can take both long and short positions, use arbitrage, buy and sell undervalued securities, trade options or bonds, and invest in almost

About Hedge Funds What is a Hedge Fund? A hedge fund is a fund that can take both long and short positions, use arbitrage, buy and sell undervalued securities, trade options or bonds, and invest in almost

Diploma in Financial Management Examination Module B Paper DB1 incorporating subject areas: Financial Strategy; Risk Management

Answers Diploma in Financial Management Examination Module B Paper DB1 incorporating subject areas: Financial Strategy; Risk Management June 2005 Answers 1 D Items 2, 3 and 4 are correct. Item 1 relates

Answers Diploma in Financial Management Examination Module B Paper DB1 incorporating subject areas: Financial Strategy; Risk Management June 2005 Answers 1 D Items 2, 3 and 4 are correct. Item 1 relates

Loan financing for service providers

Loan financing for service providers May 2014 Disclaimer The materials presented in this document are for general information only and should not be taken as constituting professional advice. Users should

Loan financing for service providers May 2014 Disclaimer The materials presented in this document are for general information only and should not be taken as constituting professional advice. Users should

A primer in Entrepreneurship

Prof. Dr. Institutefor Strategy and Business Economics Chapter 10: Getting Financing or Funding Table of Contents I. The Importance of Getting Financing or Funding II. III. Sources of Equity Funding Sources

Prof. Dr. Institutefor Strategy and Business Economics Chapter 10: Getting Financing or Funding Table of Contents I. The Importance of Getting Financing or Funding II. III. Sources of Equity Funding Sources

Investing in infrastructure?

Investing in infrastructure? Independent guide for investors about infrastructure investments This guide is for you, whether you re an experienced investor or just starting out. Key tips from ASIC about

Investing in infrastructure? Independent guide for investors about infrastructure investments This guide is for you, whether you re an experienced investor or just starting out. Key tips from ASIC about

Contents Foreword 1 Introduction by Patrick Reeve Executive summary 1. Business confidence and growth ambitions 2. Availability of finance

2014 Contents Foreword 1 Introduction by Patrick Reeve 3 Executive summary 4 1. Business confidence and growth ambitions 4 2. Availability of finance 6 3. Management skills 8 4. Apprenticeships 9 5. Optimists

2014 Contents Foreword 1 Introduction by Patrick Reeve 3 Executive summary 4 1. Business confidence and growth ambitions 4 2. Availability of finance 6 3. Management skills 8 4. Apprenticeships 9 5. Optimists

Success in Renewables. Glossary of Terms Investment and Renewables

Success in Renewables Glossary of Terms Investment and Renewables If you re new to renewable energy or investment, then it can be a minefield of new language and terminology. What seems totally normal

Success in Renewables Glossary of Terms Investment and Renewables If you re new to renewable energy or investment, then it can be a minefield of new language and terminology. What seems totally normal

Why Stapled Securities?

FINANCIAL REGULATION DISCUSSION PAPER SERIES Why Stapled Securities? FRDP 2012 3 June 4, 2012 Australia is relatively unique internationally in permitting business entities to issue stapled securities,

FINANCIAL REGULATION DISCUSSION PAPER SERIES Why Stapled Securities? FRDP 2012 3 June 4, 2012 Australia is relatively unique internationally in permitting business entities to issue stapled securities,

Outsource, Insource, Shared Services or Plan D?

Outsource, Insource, Shared Services or Plan D? The Question Every CEO & CFO Will Need to Answer may hamper business growth or worse make it difficult for the business to remain a going concern. The image

Outsource, Insource, Shared Services or Plan D? The Question Every CEO & CFO Will Need to Answer may hamper business growth or worse make it difficult for the business to remain a going concern. The image

place-based asset management

place-based asset management Managing public sector property to support aligned local public services TOWN HALL CIPFA, the Chartered Institute of Public Finance and Accountancy, is the professional body

place-based asset management Managing public sector property to support aligned local public services TOWN HALL CIPFA, the Chartered Institute of Public Finance and Accountancy, is the professional body

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased.

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

A Pi Primer in Entrepreneurship

A Pi Primer in Entrepreneurship Prof. Dr. Ulrich Kaiser Chairof Entrepreneurship Universität Zürich Fall 2012 Content 2008 Prentice Hall Seite 2 A Pi Primer in Entrepreneurship Part III Movingfroman Ideato

A Pi Primer in Entrepreneurship Prof. Dr. Ulrich Kaiser Chairof Entrepreneurship Universität Zürich Fall 2012 Content 2008 Prentice Hall Seite 2 A Pi Primer in Entrepreneurship Part III Movingfroman Ideato

A primer in Entrepreneurship

Prof. Dr. Institutefor Strategy and Business Economics Chapter 10: Getting or Financing Table of Contents I. The Importance of Getting Financing or II. III. IV. Sources of Equity Sources of Debt Financing

Prof. Dr. Institutefor Strategy and Business Economics Chapter 10: Getting or Financing Table of Contents I. The Importance of Getting Financing or II. III. IV. Sources of Equity Sources of Debt Financing

CLUB RATIO PRIVATE ANALYSIS AND FINANCIAL OPERATIONS HEALTH OF THE CLUB TRACKING THE FINANCIAL WHY CLUBS MONITOR RATIOS LIQUIDITY RATIOS

FINANCIAL RATIO ANALYSIS AND PRIVATE CLUB OPERATIONS TRACKING THE FINANCIAL HEALTH OF THE CLUB B Y P H I L I P N E W M A N Private clubs are mission driven serving members is the primary goal. Accordingly,

FINANCIAL RATIO ANALYSIS AND PRIVATE CLUB OPERATIONS TRACKING THE FINANCIAL HEALTH OF THE CLUB B Y P H I L I P N E W M A N Private clubs are mission driven serving members is the primary goal. Accordingly,

Understanding Fixed Income

Understanding Fixed Income 2014 AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 Understanding Fixed Income About fixed income at AMP Capital Our global presence helps us deliver outstanding

Understanding Fixed Income 2014 AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 Understanding Fixed Income About fixed income at AMP Capital Our global presence helps us deliver outstanding

Financing Profiles SMALL BUSINESS. SME Financing Data Initiative May 2006. Definitions. Summary of Key Findings

SMALL BUSINESS Financing Profiles SME Financing Data Initiative May 2006 High-Growth SMEs Small businesses are key to economic growth. Recent studies by Industry Canada (Parsley and Dreessen, 2004) and

SMALL BUSINESS Financing Profiles SME Financing Data Initiative May 2006 High-Growth SMEs Small businesses are key to economic growth. Recent studies by Industry Canada (Parsley and Dreessen, 2004) and

Cooper Energy and the East Coast Gas Market

Cooper Energy and the East Coast Gas Market Cooper Energy is an ASX-listed oil and gas company that is engaged in: developing new gas supply projects; marketing gas directly to eastern Australian gas users;

Cooper Energy and the East Coast Gas Market Cooper Energy is an ASX-listed oil and gas company that is engaged in: developing new gas supply projects; marketing gas directly to eastern Australian gas users;

The Issue: Building a Strong Venture Capital Climate in Canada

The Issue: Building a Strong Venture Capital Climate in Canada Capital is one of the vital ingredients in the formation of robustly competitive information and communications technology companies. Canada

The Issue: Building a Strong Venture Capital Climate in Canada Capital is one of the vital ingredients in the formation of robustly competitive information and communications technology companies. Canada

Private Equity in Asia

Private Equity in Asia October 21 Asia private equity, in particular China, has increasingly attracted attention from institutional investors due to the region s faster economic recovery, greater growth

Private Equity in Asia October 21 Asia private equity, in particular China, has increasingly attracted attention from institutional investors due to the region s faster economic recovery, greater growth

PRINCIPLES FOR PERIODIC DISCLOSURE BY LISTED ENTITIES

PRINCIPLES FOR PERIODIC DISCLOSURE BY LISTED ENTITIES Final Report TECHNICAL COMMITTEE OF THE INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS FEBRUARY 2010 CONTENTS Chapter Page 1 Introduction 3 Uses

PRINCIPLES FOR PERIODIC DISCLOSURE BY LISTED ENTITIES Final Report TECHNICAL COMMITTEE OF THE INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS FEBRUARY 2010 CONTENTS Chapter Page 1 Introduction 3 Uses

Business Plan Helpsheet

NORTHERN IRELAND Business Plan Helpsheet Published by Chartered Accountants Ulster Society with content from CCAB-I and the Irish Banking Federation Business Plan Helpsheet 01 Contents This helpsheet has

NORTHERN IRELAND Business Plan Helpsheet Published by Chartered Accountants Ulster Society with content from CCAB-I and the Irish Banking Federation Business Plan Helpsheet 01 Contents This helpsheet has

FIDUCIAN AUSTRALIAN SHARES FUND

PRODUCT DISCLOSURE STATEMENT FIDUCIAN AUSTRALIAN SHARES FUND ARSN 093 542 271 2 MARCH 2015 This Product Disclosure Statement (PDS) provides a summary of significant information about the Fiducian Australian

PRODUCT DISCLOSURE STATEMENT FIDUCIAN AUSTRALIAN SHARES FUND ARSN 093 542 271 2 MARCH 2015 This Product Disclosure Statement (PDS) provides a summary of significant information about the Fiducian Australian

Investing in mortgage schemes?

Investing in mortgage schemes? Independent guide for investors about unlisted mortgage schemes This guide is for you, whether you re an experienced investor or just starting out. Key tips from ASIC about

Investing in mortgage schemes? Independent guide for investors about unlisted mortgage schemes This guide is for you, whether you re an experienced investor or just starting out. Key tips from ASIC about

CORPORATE MEMBERS OF LIMITED LIABILITY PARTNERSHIPS

1. INTRODUCTION CORPORATE MEMBERS OF LIMITED LIABILITY PARTNERSHIPS 1.1 This note, prepared on behalf of the Company Law Committee of the City of London Law Society ( CLLS ), relates to BIS request for

1. INTRODUCTION CORPORATE MEMBERS OF LIMITED LIABILITY PARTNERSHIPS 1.1 This note, prepared on behalf of the Company Law Committee of the City of London Law Society ( CLLS ), relates to BIS request for

Helpsheet Business Plan Guidance

Helpsheet Business Plan Guidance Published jointly by CCAB-I and the Irish Banking Federation This helpsheet has been prepared by the Consultative Committee of Accountancy Bodies - Ireland (CCAB-I) and

Helpsheet Business Plan Guidance Published jointly by CCAB-I and the Irish Banking Federation This helpsheet has been prepared by the Consultative Committee of Accountancy Bodies - Ireland (CCAB-I) and

Debt: Do MFIs calculate the fully loaded cost of all debt instruments? August 2007

CGAP Brief August 2007 MFI Capital Structure Decision Making: A Call for Greater Awareness Microfinance institutions (MFIs) today have an increasingly broad range of financing sources at their disposal.

CGAP Brief August 2007 MFI Capital Structure Decision Making: A Call for Greater Awareness Microfinance institutions (MFIs) today have an increasingly broad range of financing sources at their disposal.

1. INTRODUCTION 2. EXECUTIVE SUMMARY 3. SUBMISSIONS. Loretta DeSourdy Head of Regulatory Affairs Westpac New Zealand Limited PO Box 691 Wellington

BT FUNDS MANAGEMENT (NZ) LIMITED AND WESTPAC NEW ZEALAND LIMITED Submission to the Commission for Financial Literacy and Retirement Income on the 2013 Review of Retirement Income Policy 10 June 2013 Mariëtte