Subcommittee on Courts and Competition Policy United States House of Representatives

|

|

|

- Pearl Grant

- 8 years ago

- Views:

Transcription

1 Subcommittee on Courts and Competition Policy United States House of Representatives Hearing on H.R. 3596, the Health Insurance Industry Antitrust Enforcement Act of 2009 Statement of James D. Hurley, ACAS, MAAA Medical Professional Liability Subcommittee American Academy of Actuaries October 8, 2009 The American Academy of Actuaries ( Academy ) is a 16,000-member professional association whose mission is to serve the public on behalf of the U.S. actuarial profession. The Academy assists public policymakers on all levels by providing leadership, objective expertise, and actuarial advice on risk and financial security issues. The Academy also sets qualification, practice, and professionalism standards for actuaries in the United States.

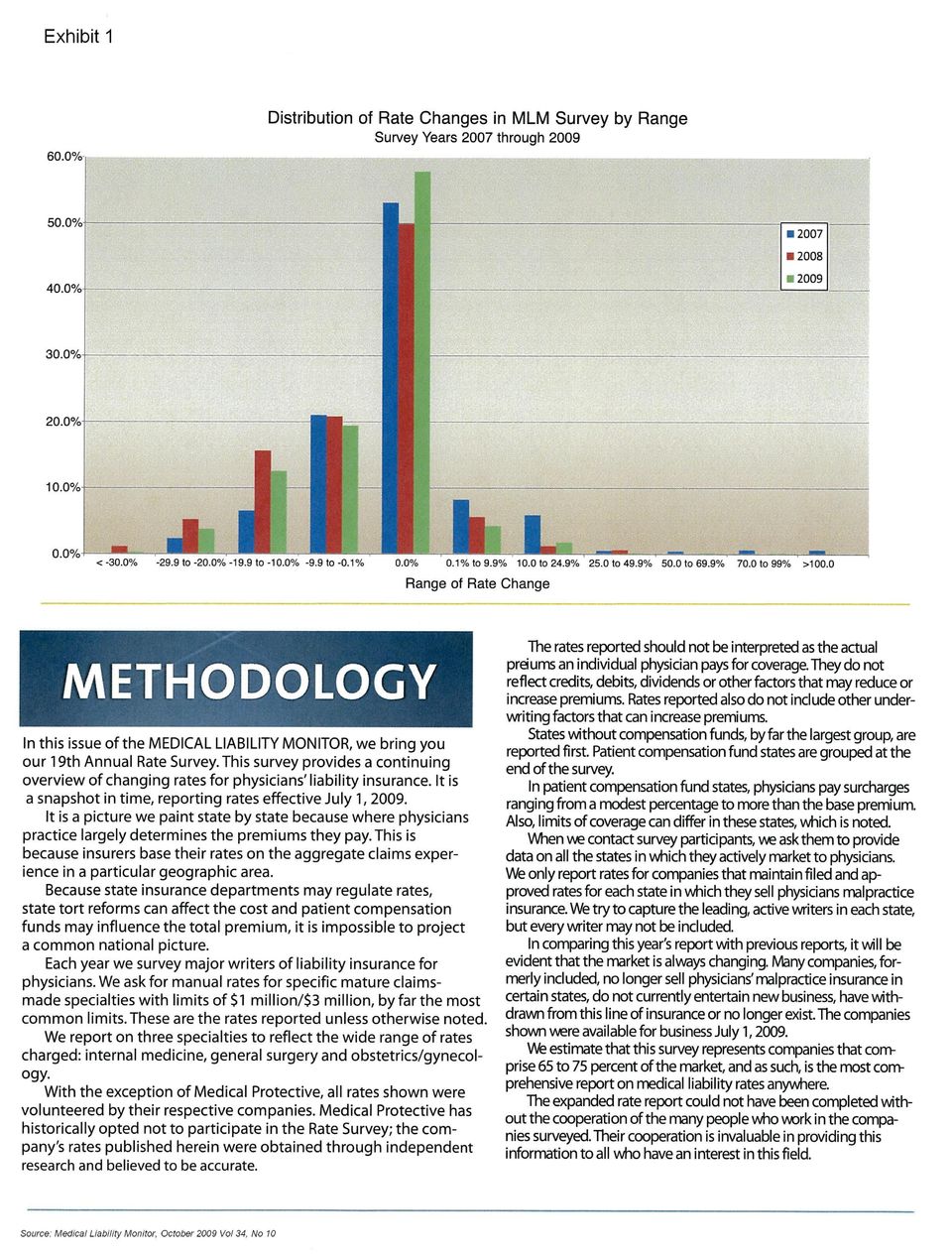

2 Chairman Conyers, Ranking Member Smith, and members of the Subcommittee. Thank you for inviting me to testify regarding H.R. 3596, the proposed Health Insurance Industry Antitrust Enforcement Act. My name is Jim Hurley. I am a consulting actuary with the firm Towers Perrin, working in the firm s Atlanta, GA office. I have worked for the Firm for approximately 25 years and am an Associate of the Casualty Actuarial Society and a Member of the American Academy of Actuaries. My work is primarily in the medical professional liability area and my comments will be from that perspective rather than from the health insurance perspective. Additionally, my comments will be from the perspective of someone who is frequently looking to estimate medical professional liability loss costs and, often, ultimately rates to be charged by insurance companies to insure such losses or for physicians and entities self-insuring their own medical professional liability exposure. In other words, my perspective is that of an actuarial practitioner actively working on medical professional liability problems daily. Before providing my comments, it is important to recognize the unique characteristics of medical professional liability coverage. In comparison to other lines of insurance, medical professional liability is a low-frequency, high-severity, long-tailed coverage (meaning, on average, there is an extended period of time between the occurrence of an event, the report of a claim related to the event, and the ultimate resolution of the claim). From a statistical standpoint, this makes the estimation of losses and premium rates more uncertain than for other lines of insurance, such as most types of health insurance. The low-frequency, high-severity, long-tailed nature of medical professional liability coverage contributes to the volatility in its coverage rates. This uncertainty is one of the reasons the coverage is often written on a claims-made basis rather than occurrence basis like most other property/casualty coverages. In the time allowed, I would like to comment on: 1. Concerns regarding the bill s language and possible misinterpretations; 2. Issues relating to data collection, aggregation and analysis of medical professional liability data; and 3. Some of the potential purposes and consequences of the proposed legislation. From a practitioner s perspective, the explicitly stated impact of the legislation would seem a non-event on its face. The proposal states, in part, that nothing in the McCarran- Ferguson Act (the Act ) shall be construed to permit.issuers of medical malpractice insurance to engage in any form of price fixing, bid rigging or market allocations. My understanding is that engaging in these acts in the context of the proposed legislation is illegal pursuant to state laws enacted after implementation of the McCarran-Ferguson Act. In my experience, companies do not engage in collusive price-fixing, bid-rigging, or market allocation. However, possible interpretations of the words in any form raise potential issues and consequences. In particular, it is possible that the words in any form as contained in the proposal, could preclude the collection, aggregation, and analysis of data across companies. 2

3 Currently, such analyses are permitted in accordance with the provisions of the McCarran-Ferguson Act and with the oversight of state regulators. Results of these analyses can be provided to companies that participate in the data collection or, perhaps, to other entities that may be given the opportunity to purchase the information. By way of background, in general, property/casualty insurance companies are required as a condition to being licensed to designate an entity to which they will report data. Probably the most well-known of these entities is Insurance Services Office (ISO). ISO is approved by the states to operate in this capacity as well as to analyze data and make results available to participants and others, subject to state regulations establishing the rules as to what types of analyses are permitted. These analyses of aggregated data, or data aggregation serve several purposes, which align with the original intent of the Act and assist state regulators charged with overseeing the pricing of insurance coverage. A few of these purposes are: 1. These analyses provide more credible data upon which to base loss estimates and premium rates. In the absence of this information, companies or self-insured entities would be forced to rely on their own, more limited data to make loss or rate determinations. Reduced access to data could increase the volatility of these determinations from year to year as companies are forced to establish rates using less credible data. 2. These analyses also serve to enhance competition. Without access to industry information, existing companies may be less willing to provide products in new markets or to different types of exposure because of the greater uncertainty associated with determining loss estimates and premium rates. 3. As further support to competition, industry information is of particular importance to newly formed companies or self-insurers looking to begin covering medical professional liability exposure. Absent the use of industry information, they may be reluctant to assume or retain this exposure. Their decision not to provide coverage reduces competitive alternatives in the marketplace. 4. Such industry analyses serve as guidance for companies, self-insurers, and regulators in reducing the likelihood of insolvencies, a long-term and recent concern. Through the review of industry data, companies, self-insurers, and regulators are better able to evaluate if too little is being charged or not enough is being set aside in reserves for a given exposure situation. These data aggregations serve the purposes outlined above, particularly for medical professional liability which, as suggested earlier, has characteristics that make it a statistically challenging exposure for companies and self-insurers. A few examples may help illustrate some of the challenges. For this coverage, any single company s own data, even for relatively large companies, is often not sufficiently credible to determine basic loss costs in multiple markets. Thus, a company writing a small amount of business in a given market may not have sufficiently credible data to estimate a stable and reliable loss cost for that jurisdiction. In another example, industry analyses can also provide guidance to companies and self-insurers regarding reasonable charges for higher limits of 3

.")

4 coverage. For instance, the experience of an individual company or self-insurer is probably not sufficient to estimate losses at $10 million or $20 million limits of coverage. Additionally, a single entity s data would rarely be sufficient to determine the appropriate differentials among types of exposure. For example, what would be an equitable loss cost differential among a family practice physician, a general surgeon, and an obstetrician? There are a number of possible consequences of not having credible information to assist in making loss cost determinations. Such entities, in the interest of preserving their viability, would be more cautious, if not unwilling, to assume exposure given the risk of the coverage. Remember, these industry analyses facilitate having such information available for new small companies, self-insurers, and large established entities looking to cover this exposure in new states. Thus, the end result relating to medical professional liability insurance companies is likely to be reduced availability with fewer willing insurers, less vigorous competition among those that do write the coverage, and higher costs to the consumer. Self-insurers are likely to be less willing to retain exposure, reducing their risk financing options and possibly increasing their costs as well. It is my understanding that one stated purpose of the proposed legislation is to reduce medical professional liability premiums. In my opinion, this change will not accomplish that purpose. In fact, it is more likely to have the opposite effect for the reasons I have outlined above. Additionally, medical professional liability losses and rates have been flat or declining in the last two to three years without the influence of this proposed change. Attached to the written version of this testimony is an exhibit containing a graph obtained from the Medical Liability Monitor, which summarizes the results of their annual survey for the last three years. The graph shows the distribution of the percentage change in filed rates implemented by physician insurers and that, in the last three years, approximately 30% of the observations reflect rate reductions. These trends occurred following the implementation of, and debate about, tort reforms in many states as well as the growing impact of risk management and patient safety initiatives. In summary, I note the following 1. the broad intent of the proposal is already being effectuated at the state level; 2. clarification of other implications (e.g., data collection and analysis) of the bill would help affected parties better understand the impact of the change; 3. collection, aggregation, and analyses of data is an important element of the current environment; it supports better decisions, promotes competition, and aids in protecting solvency; particularly for new and/or smaller competitors; 4. consumers benefit from a more competitive marketplace given the above; 5. implementation of this proposal will not assure lower medical professional liability premiums; it may, in fact, increase them; and 4

5 6. medical professional liability rates have been declining without this change, coincidental with the timing of tort reforms, and the growing impact of risk management and patient safety initiatives. Again, thank you for this opportunity to comment on the proposed legislation, and I will be happy to answer any questions you might have related to these comments. 5

6

H-232 U.S. Capitol 522 Hart Senate Office Building Washington, DC 20515 Washington, DC 20510

The Honorable Nancy Pelosi The Honorable Harry Reid Speaker, U.S. House of Representatives Majority Leader, U.S. Senate H-232 U.S. Capitol 522 Hart Senate Office Building Washington, DC 20515 Washington,

The Honorable Nancy Pelosi The Honorable Harry Reid Speaker, U.S. House of Representatives Majority Leader, U.S. Senate H-232 U.S. Capitol 522 Hart Senate Office Building Washington, DC 20515 Washington,

March 14, 2005. From: The Honorable Joe Barton

March 14, 2005 The Honorable Nathan Deal Chairman, Subcommittee on Health U.S. House Energy and Commerce Committee Washington, DC 20515 Dear Chairman Deal: This letter serves as a response to your request

March 14, 2005 The Honorable Nathan Deal Chairman, Subcommittee on Health U.S. House Energy and Commerce Committee Washington, DC 20515 Dear Chairman Deal: This letter serves as a response to your request

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21461 Medical Malpractice Liability Insurance and the McCarran-Ferguson Act Rawle O. King, Government and Finance Division

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21461 Medical Malpractice Liability Insurance and the McCarran-Ferguson Act Rawle O. King, Government and Finance Division

Ohio Medical Malpractice Commission. Statement of James Hurley, ACAS, MAAA Chairperson, Medical Malpractice Subcommittee American Academy of Actuaries

Ohio Medical Malpractice Commission Statement of James Hurley, ACAS, MAAA Chairperson, Medical Malpractice Subcommittee American Academy of Actuaries June 11, 2003 The American Academy of Actuaries is

Ohio Medical Malpractice Commission Statement of James Hurley, ACAS, MAAA Chairperson, Medical Malpractice Subcommittee American Academy of Actuaries June 11, 2003 The American Academy of Actuaries is

CRS Report for Congress

Order Code RS21461 March 19, 2003 CRS Report for Congress Received through the CRS Web Medical Malpractice Liability Insurance and the McCarran-Ferguson Act Summary Rawle O. King Analyst In Industry Economics

Order Code RS21461 March 19, 2003 CRS Report for Congress Received through the CRS Web Medical Malpractice Liability Insurance and the McCarran-Ferguson Act Summary Rawle O. King Analyst In Industry Economics

My name is Steven Lehmann. I am a Principal with Pinnacle Actuarial Resources, Inc., an actuarial consulting

Insurer Use of Education and Occupation Data National Conference of Insurance Legislators Special Property-Casualty Insurance Meeting February 28, 2009 My name is Steven Lehmann. I am a Principal with

Insurer Use of Education and Occupation Data National Conference of Insurance Legislators Special Property-Casualty Insurance Meeting February 28, 2009 My name is Steven Lehmann. I am a Principal with

Important Considerations When Analyzing Medical Malpractice Insurance Closed-Claim Databases

Important Considerations When Analyzing Medical Malpractice Insurance Closed-Claim Databases Medical Malpractice Subcommittee American Academy of Actuaries April 20, 2005 The American Academy of Actuaries

Important Considerations When Analyzing Medical Malpractice Insurance Closed-Claim Databases Medical Malpractice Subcommittee American Academy of Actuaries April 20, 2005 The American Academy of Actuaries

Minnesota Department of Commerce Medical Malpractice Insurance in Minnesota Data as of 12/31/2012

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Minnesota Department

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Minnesota Department

2007 Casualty Loss Reserve Seminar San Diego, CA

Practical Considerations in Medical Malpractice Reserving 2007 Casualty Loss Reserve Seminar San Diego, CA September 10, 2007 Jeremy Brigham, FCAS, MAAA 2005 Towers Perrin Towers Perrin Setting the Stage:

Practical Considerations in Medical Malpractice Reserving 2007 Casualty Loss Reserve Seminar San Diego, CA September 10, 2007 Jeremy Brigham, FCAS, MAAA 2005 Towers Perrin Towers Perrin Setting the Stage:

HEALTH CARE PRACTICE PROFESSIONAL LIABILITY MARKET UPDATE 2010

HEALTH CARE PRACTICE MARKET UPDATE 2010 May 2010 2009 was a good year for buyers of health care professional liability (HPL) insurance across the U.S., and 2010 is looking good as well. Many purchasers

HEALTH CARE PRACTICE MARKET UPDATE 2010 May 2010 2009 was a good year for buyers of health care professional liability (HPL) insurance across the U.S., and 2010 is looking good as well. Many purchasers

NEBRASKA HOSPITAL-MEDICAL LIABILITY ACT ANNUAL REPORT

NEBRASKA HOSPITAL-MEDICAL LIABILITY ACT ANNUAL REPORT as of December 31, 2009 THE EXCESS LIABILITY FUND (under the Nebraska Hospital-Medical Liability Act) The Nebraska Hospital-Medical Liability Act

NEBRASKA HOSPITAL-MEDICAL LIABILITY ACT ANNUAL REPORT as of December 31, 2009 THE EXCESS LIABILITY FUND (under the Nebraska Hospital-Medical Liability Act) The Nebraska Hospital-Medical Liability Act

DEPARTMENT OF JUSTICE

DEPARTMENT OF JUSTICE Statement of Christine A. Varney Assistant Attorney General Antitrust Division U.S. Department of Justice Before the Committee on the Judiciary United States Senate Hearing on Prohibiting

DEPARTMENT OF JUSTICE Statement of Christine A. Varney Assistant Attorney General Antitrust Division U.S. Department of Justice Before the Committee on the Judiciary United States Senate Hearing on Prohibiting

NEW YORK STATE WORKERS COMPENSATION BOARD ASSESSMENTS

Consulting Actuaries NEW YORK STATE WORKERS COMPENSATION BOARD ASSESSMENTS A DISCUSSION OF ASSESSMENTS AND RECENT INCREASES IMPACTING EMPLOYERS APRIL 2013 AUTHORS Scott J. Lefkowitz, FCAS, MAAA, FCA Steven

Consulting Actuaries NEW YORK STATE WORKERS COMPENSATION BOARD ASSESSMENTS A DISCUSSION OF ASSESSMENTS AND RECENT INCREASES IMPACTING EMPLOYERS APRIL 2013 AUTHORS Scott J. Lefkowitz, FCAS, MAAA, FCA Steven

Committee on Small Business U.S. House of Representatives

Committee on Small Business U.S. House of Representatives Hearing on Increasing Competition, Reducing Costs, and Expanding Small Business Health Insurance Coverage Using the Private Reinsurance Market

Committee on Small Business U.S. House of Representatives Hearing on Increasing Competition, Reducing Costs, and Expanding Small Business Health Insurance Coverage Using the Private Reinsurance Market

M&A in MPL: What Does It All Mean?

M&A in MPL: What Does It All Mean? Jeff Donaldson, FCAS, MAAA Overview Why are there acquisition opportunities in MPL? State of the market Underwriting cycle Loss cost trends Reserve evaluations Investment

M&A in MPL: What Does It All Mean? Jeff Donaldson, FCAS, MAAA Overview Why are there acquisition opportunities in MPL? State of the market Underwriting cycle Loss cost trends Reserve evaluations Investment

STATEMENT OF JULIE MIX MCPEAK COMMISSIONER, TENNESSEE DEPARTMENT OF COMMERCE AND INSURANCE

STATEMENT OF JULIE MIX MCPEAK COMMISSIONER, TENNESSEE DEPARTMENT OF COMMERCE AND INSURANCE BEFORE THE COMMITTEE ON WAYS AND MEANS SUBCOMMITTEE ON OVERSIGHT HEARING ON THE EFFECTS OF THE AFFORDABLE CARE

STATEMENT OF JULIE MIX MCPEAK COMMISSIONER, TENNESSEE DEPARTMENT OF COMMERCE AND INSURANCE BEFORE THE COMMITTEE ON WAYS AND MEANS SUBCOMMITTEE ON OVERSIGHT HEARING ON THE EFFECTS OF THE AFFORDABLE CARE

CONFERENCE COMMITTEE REPORT BRIEF HOUSE BILL NO. 2064. HB 2064 would make several amendments to the Insurance Code to:

SESSION OF 2015 CONFERENCE COMMITTEE REPORT BRIEF HOUSE BILL NO. 2064 As Agreed to March 31, 2015 Brief* HB 2064 would make several amendments to the Insurance Code to: Add insurance against the cost of

SESSION OF 2015 CONFERENCE COMMITTEE REPORT BRIEF HOUSE BILL NO. 2064 As Agreed to March 31, 2015 Brief* HB 2064 would make several amendments to the Insurance Code to: Add insurance against the cost of

ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE MARKET IN ARKANSAS

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE

Date: January 29, 2010. Commissioner Glenn Wilson. Nancy Myers, Property-Casualty Actuary. Medical Malpractice Report

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Minnesota Department

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Minnesota Department

Determining a reasonable range of loss reserves, required

C OVER S TORY By R USTY K UEHN Medical Malpractice Loss Reserves: Risk and Reasonability On March 1 of every calendar year, property/casualty insurance companies file a Statement of Actuarial Opinion (SAO),

C OVER S TORY By R USTY K UEHN Medical Malpractice Loss Reserves: Risk and Reasonability On March 1 of every calendar year, property/casualty insurance companies file a Statement of Actuarial Opinion (SAO),

I will start with a brief history and then briefly outline the ratemaking process. History of Property Insurance Legislation in NC

Thank Chairs My name is Rose Vaughn Williams. I am Legislative Counsel to the Department of Insurance. I ve been asked today to give the committee background on the rate making system for property insurance

Thank Chairs My name is Rose Vaughn Williams. I am Legislative Counsel to the Department of Insurance. I ve been asked today to give the committee background on the rate making system for property insurance

MEDICAL PROFESSIONAL LIABILITY INSURANCE MANDATORY REPORTING OF DETAILED CLAIM INFORMATION

MEDICAL PROFESSIONAL LIABILITY INSURANCE MANDATORY REPORTING OF DETAILED CLAIM INFORMATION GENERAL INSTRUCTIONS AND INFORMATION FREQUENTLY ASKED QUESTIONS Most Recent Update: January 6, 2014 Background:

MEDICAL PROFESSIONAL LIABILITY INSURANCE MANDATORY REPORTING OF DETAILED CLAIM INFORMATION GENERAL INSTRUCTIONS AND INFORMATION FREQUENTLY ASKED QUESTIONS Most Recent Update: January 6, 2014 Background:

Committee on Ways and Means Subcommittee on Health U.S. House of Representatives. Hearing on Examining Traditional Medicare s Benefit Design

Committee on Ways and Means Subcommittee on Health U.S. House of Representatives Hearing on Examining Traditional Medicare s Benefit Design February 26, 2013 Statement of Cori E. Uccello, MAAA, FSA, MPP

Committee on Ways and Means Subcommittee on Health U.S. House of Representatives Hearing on Examining Traditional Medicare s Benefit Design February 26, 2013 Statement of Cori E. Uccello, MAAA, FSA, MPP

Maryland Insurance Administration s 2006 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in

Maryland Insurance Administration s 2006 Report on the Availability and Affordability of Health Care Professional Liability Insurance in Maryland September 5, 2006 Maryland Insurance Administration's 2006

Maryland Insurance Administration s 2006 Report on the Availability and Affordability of Health Care Professional Liability Insurance in Maryland September 5, 2006 Maryland Insurance Administration's 2006

RE: Disclosure Requirements for Short Duration Insurance Contracts

INS-14 November 21, 2014 Mr. Russell G. Golden Chairman Financial Accounting Standards Board 401 Merritt 7 P.O. Box 5116 Norwalk, Connecticut 06856-5116 RE: Disclosure Requirements for Short Duration Insurance

INS-14 November 21, 2014 Mr. Russell G. Golden Chairman Financial Accounting Standards Board 401 Merritt 7 P.O. Box 5116 Norwalk, Connecticut 06856-5116 RE: Disclosure Requirements for Short Duration Insurance

Don t Make Main Street Insurance Consumers Subsidize Wall Street

Don t Make Main Street Insurance Consumers Subsidize Wall Street To address the economic turmoil caused by the collapse of several major Wall Street firms, Congress now faces the difficult charge of crafting

Don t Make Main Street Insurance Consumers Subsidize Wall Street To address the economic turmoil caused by the collapse of several major Wall Street firms, Congress now faces the difficult charge of crafting

ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE MARKET IN ARKANSAS

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE MARKET IN ARKANSAS

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE MARKET IN ARKANSAS

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

Bracing for change Medical professional liability (MPL) insurance costs at a crossroads

insurance costs at a crossroads") February 2011 Bracing for change Medical professional liability (MPL) insurance costs at a crossroads At a glance The effects of the healthcare reform law, changing market conditions, emerging societal

February 2011 Bracing for change Medical professional liability (MPL) insurance costs at a crossroads At a glance The effects of the healthcare reform law, changing market conditions, emerging societal

Risk Retention Groups: Market Influences

Risk Retention Groups: Market Influences Prepared for the Professional Liability Underwriting Society Ben Permut MBA, May 2008 Risk Management and Insurance Wisconsin School of Business University of Wisconsin,

Risk Retention Groups: Market Influences Prepared for the Professional Liability Underwriting Society Ben Permut MBA, May 2008 Risk Management and Insurance Wisconsin School of Business University of Wisconsin,

2011 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland

2011 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland August 2011 Table of Contents Executive Summary.1 Introduction..2 Malpractice Insurance

2011 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland August 2011 Table of Contents Executive Summary.1 Introduction..2 Malpractice Insurance

Medical Malpractice Reform

Medical Malpractice Reform 49 This Act to contains a clause wherein the state legislature asks the state Supreme Court to require a plaintiff filing a medical liability claim to include a certificate of

Medical Malpractice Reform 49 This Act to contains a clause wherein the state legislature asks the state Supreme Court to require a plaintiff filing a medical liability claim to include a certificate of

N e w Y o r k S t a t e S e n a t e

N e w Y o r k S t a t e S e n a t e Notice of Public Hearing SUBJECT: Medical Malpractice Reform Senate Standing Committee on Insurance Neil D. Breslin, Chair Senate Standing Committee on Health Thomas

N e w Y o r k S t a t e S e n a t e Notice of Public Hearing SUBJECT: Medical Malpractice Reform Senate Standing Committee on Insurance Neil D. Breslin, Chair Senate Standing Committee on Health Thomas

Wednesday, May 18, 2011

I tem: A F: A -3 Wednesday, May 18, 2011 SUBJECT: REQUEST FOR APPROVAL OF THE SCHMIDT COLLEGE OF MEDICINE SELF- INSURANCE PROGRAM. PROPOSED BOARD ACTION 1. Provide approval to obtain general and professional

I tem: A F: A -3 Wednesday, May 18, 2011 SUBJECT: REQUEST FOR APPROVAL OF THE SCHMIDT COLLEGE OF MEDICINE SELF- INSURANCE PROGRAM. PROPOSED BOARD ACTION 1. Provide approval to obtain general and professional

Summary of the Key Provisions of Florida Medical Malpractice Statutes d. Expert Witness Rules

Summary of the Key Provisions of Florida Medical Malpractice Statutes 766.102. Medical negligence; standards of recovery; expert witness (5) A person may not give expert testimony concerning the prevailing

Summary of the Key Provisions of Florida Medical Malpractice Statutes 766.102. Medical negligence; standards of recovery; expert witness (5) A person may not give expert testimony concerning the prevailing

Maryland Insurance Administration s 2005 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in

Maryland Insurance Administration s 2005 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland November, 2005 Maryland Insurance Administration's

Maryland Insurance Administration s 2005 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland November, 2005 Maryland Insurance Administration's

Medical Malpractice Liability Insurers - Biennial Reporting of Rate Modifiers

INSURANCE DEPARTMENT OF BANKING AND INSURANCE OFFICE OF PROPERTY AND CASUALTY Medical Malpractice Liability Insurers - Biennial Reporting of Rate Modifiers Proposed New Rules: N.J.A.C. 11:27-13 Authorized

INSURANCE DEPARTMENT OF BANKING AND INSURANCE OFFICE OF PROPERTY AND CASUALTY Medical Malpractice Liability Insurers - Biennial Reporting of Rate Modifiers Proposed New Rules: N.J.A.C. 11:27-13 Authorized

RESOLUTION FAVORING CONTINUED STATE-BASED INSURANCE CONSUMER PROTECTION

RESOLUTION FAVORING CONTINUED STATE-BASED INSURANCE CONSUMER PROTECTION NCSL STANDING COMMITTEE ON COMMUNICATIONS, FINANCIAL SERVICES & INTERSTATE COMMERCE WHEREAS, the states have sole regulatory authority

RESOLUTION FAVORING CONTINUED STATE-BASED INSURANCE CONSUMER PROTECTION NCSL STANDING COMMITTEE ON COMMUNICATIONS, FINANCIAL SERVICES & INTERSTATE COMMERCE WHEREAS, the states have sole regulatory authority

Florida Workers Compensation and Attorney Fees April 28, 2016 April 28, 2016 Florida Supreme Court Ruling. Introduction... 1

Consulting Actuaries Implications of the April 28, 2016 Florida Supreme Court Ruling on the Unconstitutionality of Florida s Workers Compensation Attorney Fee Schedule Jennifer K. Price, FCAS, MAAA Scott

Consulting Actuaries Implications of the April 28, 2016 Florida Supreme Court Ruling on the Unconstitutionality of Florida s Workers Compensation Attorney Fee Schedule Jennifer K. Price, FCAS, MAAA Scott

SUPPLEMENTAL NOTE ON HOUSE BILL NO. 2516

SESSION OF 2014 SUPPLEMENTAL NOTE ON HOUSE BILL NO. 2516 As Amended by House Committee on Insurance Brief* HB 2516 would amend provisions relating to the operation of mutual insurance companies organized

SESSION OF 2014 SUPPLEMENTAL NOTE ON HOUSE BILL NO. 2516 As Amended by House Committee on Insurance Brief* HB 2516 would amend provisions relating to the operation of mutual insurance companies organized

This briefing paper summarizes the measures the Montana Legislature has put into place to improve the state's medical liability climate.

SRJ 35: Study of Health Care Medical Malpractice: Montana's Approach to Limiting Liability by Sue O'Connell, Research Analyst Prepared for the Children, Families, Health, and Human Services Interim Committee

SRJ 35: Study of Health Care Medical Malpractice: Montana's Approach to Limiting Liability by Sue O'Connell, Research Analyst Prepared for the Children, Families, Health, and Human Services Interim Committee

Five Best Practice Strategies for Maintaining Excellence in Workers Compensation Self-Insured Groups

Five Best Practice Strategies for Maintaining Excellence in Workers Compensation Self-Insured Groups Safety National is the market leader for providing excess workers compensation coverage for self-insured

Five Best Practice Strategies for Maintaining Excellence in Workers Compensation Self-Insured Groups Safety National is the market leader for providing excess workers compensation coverage for self-insured

LOSS COSTS, RATING BUREAUS AND THE WORKERS COMPENSATION CRISIS (CAS CONVENTION, ll/go) Richard A. Hofmann

Richard A. Hofmann") LOSS COSTS, RATING BUREAUS AND THE WORKERS COMPENSATION CRISIS (CAS CONVENTION, ll/go) Richard A. Hofmann 125 "Loss Costs. Rating Bureaus and the Workers COmnenSatiOn Crisis11 By Richard A. Hofmann, ACAS,

LOSS COSTS, RATING BUREAUS AND THE WORKERS COMPENSATION CRISIS (CAS CONVENTION, ll/go) Richard A. Hofmann 125 "Loss Costs. Rating Bureaus and the Workers COmnenSatiOn Crisis11 By Richard A. Hofmann, ACAS,

1 3 0 0 I S t r e e t, N.W. WASHINGTON, D. C. 2 0 0 0 5 WRITER S DIRECT NUM BER: (202) 962-7225. R e q u e s t for Business Review

962-7225. R e q u e s t for Business Review") D a v is P o l k & Wa r d w e l l LEXINGTONAVENUE N E W Y O R K, N. Y. 10 0 1 7 1 C H A S E M A N H A T T A N P L A Z A N E W Y O R K, N.Y. 10 0 0 5 P L A C E D E L A C O M C O R D E 7 8 0 0 6 P A R I

D a v is P o l k & Wa r d w e l l LEXINGTONAVENUE N E W Y O R K, N. Y. 10 0 1 7 1 C H A S E M A N H A T T A N P L A Z A N E W Y O R K, N.Y. 10 0 0 5 P L A C E D E L A C O M C O R D E 7 8 0 0 6 P A R I

Arkansas Insurance Department

Arkansas Insurance Department Mike Beebe Governor Jay Bradford Commissioner August 15, 2011 Via E-Mail and Messenger Mr. David Ferguson Director Bureau of Legislative Research State Capitol, Room 315 Little

Arkansas Insurance Department Mike Beebe Governor Jay Bradford Commissioner August 15, 2011 Via E-Mail and Messenger Mr. David Ferguson Director Bureau of Legislative Research State Capitol, Room 315 Little

11 NYCRR 73.0. Text is current through February 15, 2002, and annotations are current through August 1, 2001.

11 NYCRR 73.0 OFFICIAL COMPILATION OF CODES, RULES AND REGULATIONS OF THE STATE OF NEW YORK TITLE 11. INSURANCE DEPARTMENT CHAPTER III. POLICY AND CERTIFICATE PROVISIONS [FN1] SUBCHAPTER B. PROPERTY AND

11 NYCRR 73.0 OFFICIAL COMPILATION OF CODES, RULES AND REGULATIONS OF THE STATE OF NEW YORK TITLE 11. INSURANCE DEPARTMENT CHAPTER III. POLICY AND CERTIFICATE PROVISIONS [FN1] SUBCHAPTER B. PROPERTY AND

76th OREGON LEGISLATIVE ASSEMBLY--2011 Regular Session. Enrolled. Senate Bill 91

76th OREGON LEGISLATIVE ASSEMBLY--2011 Regular Session Enrolled Senate Bill 91 Printed pursuant to Senate Interim Rule 213.28 by order of the President of the Senate in conformance with presession filing

76th OREGON LEGISLATIVE ASSEMBLY--2011 Regular Session Enrolled Senate Bill 91 Printed pursuant to Senate Interim Rule 213.28 by order of the President of the Senate in conformance with presession filing

ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE MARKET IN ARKANSAS

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

RESOLUTION 108-2011. Injured Patients and Families Compensation Fund. Health Insurance Coverage and Access

RESOLUTION 108-2011 Albert L. Fisher, MD 1 2 3 4 5 6 7 Whereas, Wisconsin physicians have paid billions of dollars into the Injured Patients and Families Compensation Fund over the last 35 years, for which

RESOLUTION 108-2011 Albert L. Fisher, MD 1 2 3 4 5 6 7 Whereas, Wisconsin physicians have paid billions of dollars into the Injured Patients and Families Compensation Fund over the last 35 years, for which

Kansas Health Care Stabilization Fund General Information (As of July 1, 2014)

") Kansas Health Care Stabilization Fund General Information (As of July 1, 2014) The HCSF Board of Governors The Health Care Stabilization Fund Board of Governors is a state agency governed by an eleven

Kansas Health Care Stabilization Fund General Information (As of July 1, 2014) The HCSF Board of Governors The Health Care Stabilization Fund Board of Governors is a state agency governed by an eleven

2014 Statutory Combined Annual Statement Schedule P Disclosure

2014 Statutory Combined Annual Statement Schedule P Disclosure This disclosure provides supplemental facts and methodologies intended to enhance understanding of Schedule P reserve data. It provides additional

2014 Statutory Combined Annual Statement Schedule P Disclosure This disclosure provides supplemental facts and methodologies intended to enhance understanding of Schedule P reserve data. It provides additional

EXAMINING COSTS AND TRENDS OF WORKERS COMPENSATION CLAIMS IN NEW YORK STATE

Consulting Actuaries EXAMINING COSTS AND TRENDS OF WORKERS COMPENSATION CLAIMS IN NEW YORK STATE MARCH 2013 AUTHORS Scott J. Lefkowitz, FCAS, MAAA, FCA Steven G. McKinnon, FCAS, MAAA, FCA Eric J. Hornick,

Consulting Actuaries EXAMINING COSTS AND TRENDS OF WORKERS COMPENSATION CLAIMS IN NEW YORK STATE MARCH 2013 AUTHORS Scott J. Lefkowitz, FCAS, MAAA, FCA Steven G. McKinnon, FCAS, MAAA, FCA Eric J. Hornick,

TESTIMONY ALLAN E. O BRYANT EXECUTIVE VICE PRESIDENT HEAD OF INTERNATIONAL MARKETS AND OPERATIONS REINSURANCE GROUP OF AMERICA, INCORPORATED

TESTIMONY OF ALLAN E. O BRYANT EXECUTIVE VICE PRESIDENT HEAD OF INTERNATIONAL MARKETS AND OPERATIONS REINSURANCE GROUP OF AMERICA, INCORPORATED HEARING ON U.S. INSURANCE SECTOR: INTERNATIONAL COMPETITIVENESS

TESTIMONY OF ALLAN E. O BRYANT EXECUTIVE VICE PRESIDENT HEAD OF INTERNATIONAL MARKETS AND OPERATIONS REINSURANCE GROUP OF AMERICA, INCORPORATED HEARING ON U.S. INSURANCE SECTOR: INTERNATIONAL COMPETITIVENESS

Introduction to General Insurance FEBRUARY 2015

Important Exam Information: Exam Registration Candidates may register online or with an application. Order Study Notes There is no study note package for this examination. Introductory Study Note The Introductory

Important Exam Information: Exam Registration Candidates may register online or with an application. Order Study Notes There is no study note package for this examination. Introductory Study Note The Introductory

A.M. Best - Congressional Testimony Committee on Financial Services America s Insurance Industry: Keeping the Promise

A.M. Best - Congressional Testimony Committee on Financial Services America s Insurance Industry: Keeping the Promise The horrible events of September 11 th caused shocks throughout the world s financial

A.M. Best - Congressional Testimony Committee on Financial Services America s Insurance Industry: Keeping the Promise The horrible events of September 11 th caused shocks throughout the world s financial

The current marketplace for medical

MEDICAL MALPRACTICE INSURANCE: A MARKET IN TRANSITION By Chad C. Karls, FCAS, MAAA and Kevin J. Atinsky, ACAS, MAAA Milliman USA The current marketplace for medical malpractice coverage in the United States

MEDICAL MALPRACTICE INSURANCE: A MARKET IN TRANSITION By Chad C. Karls, FCAS, MAAA and Kevin J. Atinsky, ACAS, MAAA Milliman USA The current marketplace for medical malpractice coverage in the United States

42 NJR 7(2) July 19, 2010 Filed June 30, 2010. Authorized By: Thomas B. Considine, Commissioner, Department of Banking and Insurance.

July 19, 2010 Filed June 30, 2010. Authorized By: Thomas B. Considine, Commissioner, Department of Banking and Insurance.") INSURANCE 42 NJR 7(2) July 19, 2010 Filed June 30, 2010 DEPARTMENT OF BANKING AND INSURANCE OFFICE OF PROPERTY AND CASUALTY Changes to Medical Malpractice Liability Insurance Rates Proposed New Rules:

INSURANCE 42 NJR 7(2) July 19, 2010 Filed June 30, 2010 DEPARTMENT OF BANKING AND INSURANCE OFFICE OF PROPERTY AND CASUALTY Changes to Medical Malpractice Liability Insurance Rates Proposed New Rules:

STATE OF NEW HAMPSHIRE INSURANCE DEPARTMENT. REPORT on AVAILABILITY of MEDICAL MALPRACTICE INSURANCE

STATE OF NEW HAMPSHIRE INSURANCE DEPARTMENT REPORT on AVAILABILITY of MEDICAL MALPRACTICE INSURANCE New Hampshire Medical Malpractice Joint Underwriting Association (JUA) February 19, 2015 Table of Contents

STATE OF NEW HAMPSHIRE INSURANCE DEPARTMENT REPORT on AVAILABILITY of MEDICAL MALPRACTICE INSURANCE New Hampshire Medical Malpractice Joint Underwriting Association (JUA) February 19, 2015 Table of Contents

SUPPLEMENTAL NOTE ON SUBSTITUTE FOR SENATE BILL NO. 11

Corrected SESSION OF 2007 SUPPLEMENTAL NOTE ON SUBSTITUTE FOR SENATE BILL NO. 11 As Amended by House Committee of the W hole Brief* Sub. for SB 11, as amended by the House Committee of the Whole, would

Corrected SESSION OF 2007 SUPPLEMENTAL NOTE ON SUBSTITUTE FOR SENATE BILL NO. 11 As Amended by House Committee of the W hole Brief* Sub. for SB 11, as amended by the House Committee of the Whole, would

Drug and Alcohol Testing of Doctors. Medical Negligence Lawsuits. Initiative Statute.

osition Official Title and Summary Prepared by the Attorney General Requires drug and alcohol testing of doctors and reporting of positive test to the California Medical Board. Requires Board to suspend

osition Official Title and Summary Prepared by the Attorney General Requires drug and alcohol testing of doctors and reporting of positive test to the California Medical Board. Requires Board to suspend

WCIRB REPORT ON THE STATE OF THE CALIFORNIA WORKERS COMPENSATION INSURANCE SYSTEM

STATE OF THE SYSTEM WCIRB REPORT ON THE STATE OF THE CALIFORNIA WORKERS COMPENSATION INSURANCE SYSTEM Introduction The workers compensation insurance system in California is over 100 years old. It provides

STATE OF THE SYSTEM WCIRB REPORT ON THE STATE OF THE CALIFORNIA WORKERS COMPENSATION INSURANCE SYSTEM Introduction The workers compensation insurance system in California is over 100 years old. It provides

Senator Roger F. Wicker Testimony on the Reauthorization of the National Flood Insurance Program Senate Banking Committee June 9, 2011

Senator Roger F. Wicker Testimony on the Reauthorization of the National Flood Insurance Program Senate Banking Committee June 9, 2011 Thank you, Chairman Johnson and Ranking Member Shelby, for holding

Senator Roger F. Wicker Testimony on the Reauthorization of the National Flood Insurance Program Senate Banking Committee June 9, 2011 Thank you, Chairman Johnson and Ranking Member Shelby, for holding

May 4, 2006. Capitol Building, S-230 Capitol Building, S-221 Washington, DC 20510 Washington, DC 20510

The Honorable William Frist Majority Leader Minority Leader United States Senate United States Senate Capitol Building, S-230 Capitol Building, S-221 Washington, DC 20510 Washington, DC 20510 Dear Majority

The Honorable William Frist Majority Leader Minority Leader United States Senate United States Senate Capitol Building, S-230 Capitol Building, S-221 Washington, DC 20510 Washington, DC 20510 Dear Majority

ADDENDUM NO. 1 TO RFP 9600-61: Locum Tenens Referrals

ADDENDUM NO. 1 TO RFP 9600-61: Locum Tenens Referrals Date: March 18, 2015 To: All Vendors Interested in RFP # 9600-61 From: Kristen Aldrich, Deputy Purchasing Agent, NMC Contracts Division Subject: Addendum

ADDENDUM NO. 1 TO RFP 9600-61: Locum Tenens Referrals Date: March 18, 2015 To: All Vendors Interested in RFP # 9600-61 From: Kristen Aldrich, Deputy Purchasing Agent, NMC Contracts Division Subject: Addendum

Compliance Issues for Captives

Compliance Issues for Captives State Taxation and Regulation in the Wake of the Nonadmitted and Reinsurance Reform Act of 2010 Kathy Davis Kevin Moriarty Downs Rachlin Martin PLLC Downs Rachlin Martin

Compliance Issues for Captives State Taxation and Regulation in the Wake of the Nonadmitted and Reinsurance Reform Act of 2010 Kathy Davis Kevin Moriarty Downs Rachlin Martin PLLC Downs Rachlin Martin

Department of Labor Hearing on the Definition of Fiduciary Proposed Regulation. Testimony on behalf of. America s Health Insurance Plans and

August 10, 2015 Department of Labor Hearing on the Definition of Fiduciary Proposed Regulation Testimony on behalf of America s Health Insurance Plans and Blue Cross Blue Shield Association By Jon Breyfogle

August 10, 2015 Department of Labor Hearing on the Definition of Fiduciary Proposed Regulation Testimony on behalf of America s Health Insurance Plans and Blue Cross Blue Shield Association By Jon Breyfogle

CONTEMPORARY TRENDS IN GENERAL INSURANCE - U. S. A. by C. K. Khury

CONTEMPORARY TRENDS IN GENERAL INSURANCE - U. S. A. by C. K. Khury Overview The general insurance industry in the United States has never lacked for issues or challenges. Scholars of the business can point

CONTEMPORARY TRENDS IN GENERAL INSURANCE - U. S. A. by C. K. Khury Overview The general insurance industry in the United States has never lacked for issues or challenges. Scholars of the business can point

ON: Examining Legislative Proposals to Modernize Business Development Companies and Expand Investment Opportunities

ON: Examining Legislative Proposals to Modernize Business Development Companies and Expand Investment Opportunities TO: House Committee on Financial Services, Subcommittee on Capital Markets and Government

ON: Examining Legislative Proposals to Modernize Business Development Companies and Expand Investment Opportunities TO: House Committee on Financial Services, Subcommittee on Capital Markets and Government

2007 Medical Malpractice Claims Report

2007 Medical Malpractice Claims Report Department of Commerce & Insurance November 1, 2007 2007 Tennessee Medical Malpractice Report INTRODUCTION In 2004, the Tennessee General Assembly enacted 2004 Tenn.

2007 Medical Malpractice Claims Report Department of Commerce & Insurance November 1, 2007 2007 Tennessee Medical Malpractice Report INTRODUCTION In 2004, the Tennessee General Assembly enacted 2004 Tenn.

Holly C. Bakke, Commissioner, Department of Banking and Insurance. Authority: N.J.S.A.17:30D-17(a) and (b) and P.L. 2004 c. 17

and (b) and P.L. 2004 c. 17") INSURANCE DEPARTMENT OF BANKING AND INSURANCE DIVISION OF INSURANCE Medical Malpractice Reporting Requirements Proposed Amendments: N.J.A.C. 11:1-7.1 and 7.3 Authorized By: Holly C. Bakke, Commissioner,

INSURANCE DEPARTMENT OF BANKING AND INSURANCE DIVISION OF INSURANCE Medical Malpractice Reporting Requirements Proposed Amendments: N.J.A.C. 11:1-7.1 and 7.3 Authorized By: Holly C. Bakke, Commissioner,

UNITED STATES OFFICE OF PERSONNEL MANAGEMENT

UNITED STATES OFFICE OF PERSONNEL MANAGEMENT STATEMENT OF JONATHAN FOLEY DIRECTOR, PLANNING AND POLICY ANALYSIS U.S. OFFICE OF PERSONNEL MANAGEMENT before the SUBCOMMITTEE ON FEDERAL WORKFORCE, U.S. POSTAL

UNITED STATES OFFICE OF PERSONNEL MANAGEMENT STATEMENT OF JONATHAN FOLEY DIRECTOR, PLANNING AND POLICY ANALYSIS U.S. OFFICE OF PERSONNEL MANAGEMENT before the SUBCOMMITTEE ON FEDERAL WORKFORCE, U.S. POSTAL

AN OVERVIEW OF THE WISCONSIN HEALTH CARE LIABILITY AND PATIENTS COMPENSATION ACT

AN OVERVIEW OF THE WISCONSIN HEALTH CARE LIABILITY AND PATIENTS COMPENSATION ACT A REPORT TO THE SJR 32 SUBCOMMITTEE ON MEDICAL LIABILITY INSURANCE Prepared by David D. Bohyer, Research Director March

AN OVERVIEW OF THE WISCONSIN HEALTH CARE LIABILITY AND PATIENTS COMPENSATION ACT A REPORT TO THE SJR 32 SUBCOMMITTEE ON MEDICAL LIABILITY INSURANCE Prepared by David D. Bohyer, Research Director March

AHIP Comments to House Ways and Means Committee Work Groups Urging Repeal of the ACA Health Insurance Tax

AHIP Comments to House Ways and Means Committee Work Groups Urging Repeal of the ACA Health Insurance Tax April 12, 2013 I. Introduction America s Health Insurance Plans (AHIP) is the national trade association

AHIP Comments to House Ways and Means Committee Work Groups Urging Repeal of the ACA Health Insurance Tax April 12, 2013 I. Introduction America s Health Insurance Plans (AHIP) is the national trade association

AN ACT IN THE COUNCIL OF THE DISTRICT OF COLUMBIA

AN ACT IN THE COUNCIL OF THE DISTRICT OF COLUMBIA Codification District of Columbia Official Code 2001 Edition 2007 Winter Supp. West Group Publisher To amend AN ACT To provide for regulation of certain

AN ACT IN THE COUNCIL OF THE DISTRICT OF COLUMBIA Codification District of Columbia Official Code 2001 Edition 2007 Winter Supp. West Group Publisher To amend AN ACT To provide for regulation of certain

The Surplus Lines Insurance Market

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS22506 Surplus Lines Insurance: Background and Current Legislation Baird Webel, Government and Finance Division June 27,

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS22506 Surplus Lines Insurance: Background and Current Legislation Baird Webel, Government and Finance Division June 27,

New Hanover County. Request for Qualifications. Crime Scene Investigation (CSI) Building Expansion

Building Expansion") New Hanover County Request for Qualifications Crime Scene Investigation (CSI) Building Expansion General Information The purpose of this Request for Qualifications is to solicit qualifications from qualified

New Hanover County Request for Qualifications Crime Scene Investigation (CSI) Building Expansion General Information The purpose of this Request for Qualifications is to solicit qualifications from qualified

Written Testimony of William Brewer. President, National Association of Consumer Bankruptcy Attorneys

Written Testimony of William Brewer President, National Association of Consumer Bankruptcy Attorneys Before the Subcommittee on Courts, Commercial and Administrative Law Judiciary Committee U.S. House

Written Testimony of William Brewer President, National Association of Consumer Bankruptcy Attorneys Before the Subcommittee on Courts, Commercial and Administrative Law Judiciary Committee U.S. House

Professional Liability Insurance Issues for CRNAs

Professional Liability Insurance Issues for CRNAs Louise E. Hershkowitz, CRNA, MSHA Pennsylvania Association of Nurse Anesthetists Hershey, Pennsylvania April 4, 2004 What is It? A Contract for Service

Professional Liability Insurance Issues for CRNAs Louise E. Hershkowitz, CRNA, MSHA Pennsylvania Association of Nurse Anesthetists Hershey, Pennsylvania April 4, 2004 What is It? A Contract for Service

DELAWARE RIVER JOINT TOLL BRIDGE COMMISSION REQUEST FOR QUALIFICATIONS

Preserving Our Past, Enhancing Our Future DELAWARE RIVER JOINT TOLL BRIDGE COMMISSION REQUEST FOR QUALIFICATIONS NEW JERSEY-BASED PROPERTY & CASUALTY INSURANCE / RISK MANAGEMENT PROFESSIONAL SERVICES March

Preserving Our Past, Enhancing Our Future DELAWARE RIVER JOINT TOLL BRIDGE COMMISSION REQUEST FOR QUALIFICATIONS NEW JERSEY-BASED PROPERTY & CASUALTY INSURANCE / RISK MANAGEMENT PROFESSIONAL SERVICES March

1. A. Should the Colorado Health Benefit Exchange operate as one or two entities and

1. A. Should the Colorado Health Benefit Exchange operate as one or two entities and Goal/Objective Create a successful individual and SHOP Exchange as defined by SB11 200 Create a self sustaining COHBE

1. A. Should the Colorado Health Benefit Exchange operate as one or two entities and Goal/Objective Create a successful individual and SHOP Exchange as defined by SB11 200 Create a self sustaining COHBE

Drug and Alcohol Testing of Doctors. Medical Negligence Lawsuits. Initiative Statute.

Proposition 46 Drug and Alcohol Testing of Doctors. Medical Negligence Lawsuits. Initiative Statute. Yes/No Statement A YES vote on this measure means: The cap on medical malpractice damages for such things

Proposition 46 Drug and Alcohol Testing of Doctors. Medical Negligence Lawsuits. Initiative Statute. Yes/No Statement A YES vote on this measure means: The cap on medical malpractice damages for such things

How To Calculate Workers Compensation Claim Costs In New York

Consulting Actuaries Examining Costs and Trends of Workers Compensation Claims in New York State Authors Scott J. Lefkowitz, FCAS, MAAA, FCA Steven G. McKinnon, FCAS, MAAA Contents 1. Introduction 1 2.

Consulting Actuaries Examining Costs and Trends of Workers Compensation Claims in New York State Authors Scott J. Lefkowitz, FCAS, MAAA, FCA Steven G. McKinnon, FCAS, MAAA Contents 1. Introduction 1 2.

Examining Costs and Trends of Workers Compensation Claims

Consulting Actuaries Examining Costs and Trends of Workers Compensation Claims in Connecticut Authors Scott J. Lefkowitz, FCAS, MAAA, FCA Eric. J. Hornick, FCAS, MAAA, FCA Contents 1. Introduction 1 2.

Consulting Actuaries Examining Costs and Trends of Workers Compensation Claims in Connecticut Authors Scott J. Lefkowitz, FCAS, MAAA, FCA Eric. J. Hornick, FCAS, MAAA, FCA Contents 1. Introduction 1 2.

ANNUAL REPORT Per SCR 111 of 2007

ANNUAL REPORT Per SCR 111 of 2007 BY LOUISIANA PATIENT S COMPENSATION FUND October 1, 2008 A BRIEF HISTORY OF THE LOUISIANA PATIENT S COMPENSATION FUND In the early 1970 s, a problem of crisis proportions

ANNUAL REPORT Per SCR 111 of 2007 BY LOUISIANA PATIENT S COMPENSATION FUND October 1, 2008 A BRIEF HISTORY OF THE LOUISIANA PATIENT S COMPENSATION FUND In the early 1970 s, a problem of crisis proportions

Testimony before the House Insurance Committee

Testimony before the House Insurance Committee Public hearing on HB 717 Creating an Office of Consumer Advocate for Health Insurance Presented by Carolyn Morris Director, Bureau of Consumer Services February

Testimony before the House Insurance Committee Public hearing on HB 717 Creating an Office of Consumer Advocate for Health Insurance Presented by Carolyn Morris Director, Bureau of Consumer Services February

Actuarial Roundtable Presented by Milliman

Actuarial Roundtable Presented by Milliman Chicago RIMS Chapter October 21, 2014 Richard Frese, FCAS, MAAA Elizabeth Bart, FCAS, MAAA Mike Paczolt, FCAS, MAAA Tony Bloemer, FCAS, MAAA Doug Nishimura, ARM

Actuarial Roundtable Presented by Milliman Chicago RIMS Chapter October 21, 2014 Richard Frese, FCAS, MAAA Elizabeth Bart, FCAS, MAAA Mike Paczolt, FCAS, MAAA Tony Bloemer, FCAS, MAAA Doug Nishimura, ARM

Introduction to Medical Malpractice Insurance

William Gallagher Associates Introduction to Medical Malpractice Insurance What is Medical Malpractice Insurance? Insurance, in general, is the practice of sharing your risk with a large number of individuals

William Gallagher Associates Introduction to Medical Malpractice Insurance What is Medical Malpractice Insurance? Insurance, in general, is the practice of sharing your risk with a large number of individuals

Indemnity Payment at 30 Months Maturity

2013 Workers Compensation Insurance Oversight Report INTRODUCTION: Revisions to the Illinois Workers Compensation Act (820 ILCS 305/29) in the summer of 2011 require the Department of Insurance (Department)

2013 Workers Compensation Insurance Oversight Report INTRODUCTION: Revisions to the Illinois Workers Compensation Act (820 ILCS 305/29) in the summer of 2011 require the Department of Insurance (Department)

GAO. FEDERAL EMPLOYEES HEALTH BENEFITS PROGRAM Premiums Continue to Rise, but Rate of Growth Has Recently Slowed. Testimony

GAO For Release on Delivery Expected at 10:30 a.m. EDT Friday, May 18, 2007 United States Government Accountability Office Testimony Before the Subcommittee on Oversight of Government Management, the Federal

GAO For Release on Delivery Expected at 10:30 a.m. EDT Friday, May 18, 2007 United States Government Accountability Office Testimony Before the Subcommittee on Oversight of Government Management, the Federal

HOUSE BILL NO. HB0106. Medical malpractice-use of expert witnesses. A BILL. for. AN ACT relating to medical malpractice actions; providing

00 STATE OF WYOMING 0LSO-0 HOUSE BILL NO. HB0 Medical malpractice-use of expert witnesses. Sponsored by: Representative(s) Gingery A BILL for AN ACT relating to medical malpractice actions; providing for

00 STATE OF WYOMING 0LSO-0 HOUSE BILL NO. HB0 Medical malpractice-use of expert witnesses. Sponsored by: Representative(s) Gingery A BILL for AN ACT relating to medical malpractice actions; providing for

Medical Malpractice, the Affordable Care Act and State Provider Shield Laws: More Myth than Necessity?

Boston College Law School Digital Commons @ Boston College Law School Boston College Law School Faculty Papers 5-14-2013 Medical Malpractice, the Affordable Care Act and State Provider Shield Laws: More

Boston College Law School Digital Commons @ Boston College Law School Boston College Law School Faculty Papers 5-14-2013 Medical Malpractice, the Affordable Care Act and State Provider Shield Laws: More

Current Issues and Trends in Medical Malpractice

Current Issues and Trends in Medical Malpractice Casualty Loss Reserve Seminar September 20, 2010 Chris Coleianne Aon Global Risk Consulting Columbia, Maryland Current Issues and Trends in Medical Malpractice

Current Issues and Trends in Medical Malpractice Casualty Loss Reserve Seminar September 20, 2010 Chris Coleianne Aon Global Risk Consulting Columbia, Maryland Current Issues and Trends in Medical Malpractice

A REVIEW OF CURRENT WORKERS COMPENSATION COSTS IN NEW YORK

Consulting Actuaries A REVIEW OF CURRENT WORKERS COMPENSATION COSTS IN NEW YORK Scott J. Lefkowitz, FCAS, MAAA, FCA CONTENTS Introduction... 1 Summary of the 2007 Legislation... 3 Consequences of the 2007

Consulting Actuaries A REVIEW OF CURRENT WORKERS COMPENSATION COSTS IN NEW YORK Scott J. Lefkowitz, FCAS, MAAA, FCA CONTENTS Introduction... 1 Summary of the 2007 Legislation... 3 Consequences of the 2007

Pitfalls in Evaluating Proposed Tort Reforms

Gail E. Tverberg, FCAS, MAAA Abstract Motivation. To provide the ratemaking actuary with a description of typical medical malpractice tort reforms and issues involved in pricing these reforms. Method.

Gail E. Tverberg, FCAS, MAAA Abstract Motivation. To provide the ratemaking actuary with a description of typical medical malpractice tort reforms and issues involved in pricing these reforms. Method.

The Role of the Board in Enterprise Risk Management

Enterprise Risk The Role of the Board in Enterprise Risk Management The board of directors plays an essential role in ensuring that an effective ERM program is in place. Governance, policy, and assurance

Enterprise Risk The Role of the Board in Enterprise Risk Management The board of directors plays an essential role in ensuring that an effective ERM program is in place. Governance, policy, and assurance

PROFESSIONAL LIABILITY INSURANCE COVERAGE

Management Advisory 2002,Victor O. Schinnerer & Company, Inc. The information presented here is for risk management guidance. It is not legal advice nor should it be construed to be a determination on

Management Advisory 2002,Victor O. Schinnerer & Company, Inc. The information presented here is for risk management guidance. It is not legal advice nor should it be construed to be a determination on

All insured's must be owners and likewise all owners must be insured's. Under the LRRA, the membership of the RRG must be relatively homogeneous

What is a Risk Retention Group? A risk retention group (RRG) is a policy issuing liability insurance company that is owned by its member insured's and formed under the Liability Risk Retention Act of 1981,

What is a Risk Retention Group? A risk retention group (RRG) is a policy issuing liability insurance company that is owned by its member insured's and formed under the Liability Risk Retention Act of 1981,

FEDERAL LIABILITY RISK RETENTION ACT OF 1986. 15 USC 3901-3906 (1981, as amended 1986)

") FEDERAL LIABILITY RISK RETENTION ACT OF 1986 15 USC 3901-3906 (1981, as amended 1986) Sec. 3901 DEFINITIONS [Section 2]* Sec. 3902 RISK RETENTION GROUPS [Section 3] (a) EXEMPTION FROM STATE LAWS, REGULATIONS

FEDERAL LIABILITY RISK RETENTION ACT OF 1986 15 USC 3901-3906 (1981, as amended 1986) Sec. 3901 DEFINITIONS [Section 2]* Sec. 3902 RISK RETENTION GROUPS [Section 3] (a) EXEMPTION FROM STATE LAWS, REGULATIONS

Legislation-in-Brief The Standard Valuation Law and Principle-based Reserves

1 Legislation-in-Brief The Standard Valuation Law and Principle-based Reserves The American Academy of Actuaries is an 18,000+ member professional association whose mission is to serve the public and the

1 Legislation-in-Brief The Standard Valuation Law and Principle-based Reserves The American Academy of Actuaries is an 18,000+ member professional association whose mission is to serve the public and the