Capital requirements for health insurance under Solvency II

|

|

|

- Bernadette Henderson

- 8 years ago

- Views:

Transcription

1 Capital requirements for health insurance under Solvency II Medical Expense Insurance: Actuarial Aspects and Solvency Afternoon Seminar at the AG Insurance Chair in Health Insurance, KU Leuven 25 April 2013

2 Solvency II Group supervision & cross-sectoral convergence Groups are recognised as an economic entity => supervision on a consolidated basis (diversification benefits, group risks) Pillar 1: quantitative requirements 1. Harmonised calculation of technical provisions 2. "Prudent person" approach to investments instead of current quantitative restrictions 3. Two capital requirements: the Solvency Capital Requirement (SCR) and the Minimum Capital Requirement (MCR) Pillar 2: qualitative requirements and supervision 1. Enhanced governance, internal control, risk management and own risk and solvency assessment (ORSA) 2. Strengthened supervisory review, harmonised supervisory standards and practices Pillar 3: prudential reporting and public disclosure 1. Common supervisory reporting 2. Public disclosure of the financial condition and solvency report (market discipline through transparency)

2.")

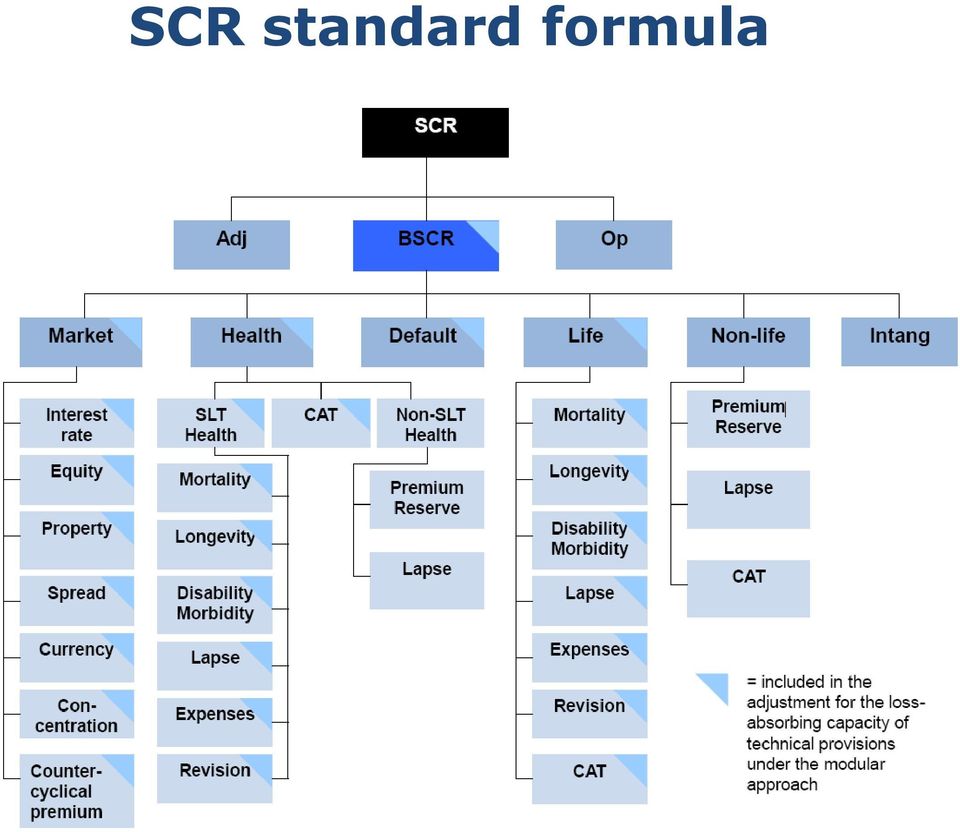

3 SCR standard formula Modules of the SCR standard formula Non-life underwriting risk Life underwriting risk Health underwriting risk Market risk Counterparty default risk "The health underwriting risk module shall reflect the risk arising from the underwriting of health insurance obligations, whether it is pursued on a similar basis to that of life insurance or not, following both from the perils covered and the process used in the conduct of business."

4 Definition and segmentation of health insurance Heterogeneity of the European health insurance market 27 different social systems and insurance traditions substitutive, supplementary or complementary large variety of medical services covered long-term or short term covering expenses or paying lump sums special features like premiums adjustments, risk equalisation Health Task Force in 2010 Members: supervisors, industry representatives, actuaries Worked on definition segmentation health risk equalisation systems

5 Definition and segmentation of health insurance Health insurance covers one or both of the following: The provision of medical treatment or care including preventive or curative medical treatment or care due to illness, accident, disability or infirmity, or financial compensation for such treatment or care Financial compensation for illness, accident, disability or infirmity Medical expense insurance (ME) Income protection insurance (IP) Workers' compensation insurance (WC) = health insurance relating to accidents at work, industrial injury and occupational disease.

Workers' compensation insurance (WC) = health insurance relating to accidents at work, industrial injury and")

6 Definition and segmentation of health insurance Non-life insurance obligations (NSLT Health) ME insurance * IP insurance * WC insurance ME prop. reinsurance * IP prop. reinsurance * WC prop. reinsurance Health nprop. reinsurance * excluding WC Life insurance obligations (SLT Health) Health insurance Annuities Health reinsurance

Health")

7 SCR standard formula

8 Health underwriting risk module Health NSLT Health SLT Health CAT Premium & Reserve Mortality Lapse Mass accident Lapse Longevity Expense Accident concentration Morbidity/ Disability Revision Pandemic

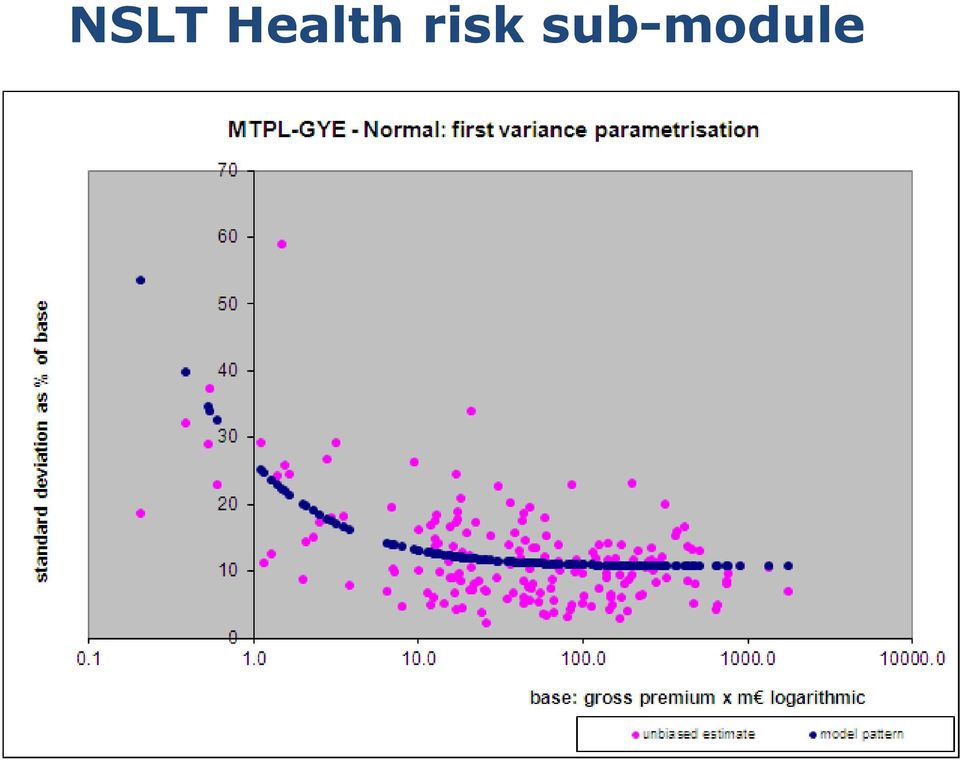

9 Premium and reserve risk SCR pr = 3 σ V multiplication by 3 corresponds to slightly skewed distribution of annual losses standard deviation of annual losses, normalised by volume measure volume measure V = V prem +V res

10 Calibration of standard deviations Non-life and NSLT health calibration controversial since QIS2 poor empirical justification For QIS5 larger calibration exercise of CEIOPS But data base and calibration methodology remain controversial 2010/2011 EIOPA Joint Working Group on Calibration Chaired by Peter ter Berg (Dutch National Bank) Involves supervisors, industry representatives and actuaries Mid-2011: new calibration proposal for non-life and NSLT health

11 Data basis Content of data sets: Earned premiums Claims triangles Ultimate loss estimates Expenses Gross/net of reinsurance; including/excluding CAT losses About 2700 data sets from insurers of 26 EEA member states

12 Insurers BE Insurers Countries Medical expenses Income protection Workers' compensation NP reinsurance 8-6

13 Data limitations and data cleaning Automatic filters for data anomalies manual correction or exclusion of data Length of data series: min 3 years, confirmed by sensitivity analysis Insurers' data excluding CAT only usable for property insurance for other LoB manual removal of isolated peaks Data with outlying residuals removed Mainly use of data gross of reinsurance because sample of net data significantly smaller

14 Estimation process Step 1: Estimation of standard deviation per insurer Step 2: Modelling of size-dependent standard deviation Step 3: Derive calibration from the model

15 Step 1: Estimation of standard derivation per insurer Premium risk: Standard estimator applied to time series of combined ratios Reserve risk: Standard estimator applied to time series of run-off ratios Mean squared error of prediction (MSEP) Merz/Wüthrich: "Modelling The Claims Developement Result For Solvency Purposes"

Merz/Wüthrich: \"Modelling The Claims Developement Result For")

16

17 Step 2: Modelling of size-dependent standard deviation Premium risk: Variance proportional to premiums or squared premiums or a mixture of both Lognormal distribution of annual loss Maximum likelihood estimation Reserve risk: Run-off ratios same model as for premium risk with best estimate as volume measure MSEP two approaches: Variance proportional to squared best estimate; least squares fitting Similar model as for premium risk with best estimate as volume measure

18 Step 3: Correction for sample bias Size bias of sample Larger insurers may be overrepresented in the sample Use of size distribution of QIS5 participants plus correction for missing small participants National market bias Some national markets may be better represented in the sample than others Average of country standard deviations, weighted with country market size

19 Example: Medical expense insurance premium risk

20 Step 3: Choice of relevant insurer size for calibration How many insurers should be below/above the relevant size? How many policyholders should belong to insurers below/above the relevant size? Median insurer size, but not more than 95% of policyholders should belong to insurers larger than the relevant size.

21 Results Medical expenses Income protection Workers' compensation NP reinsurance Premium risk Reserve risk QIS5 new QIS5 new 4% 5% 10% 5% 8.5% 9% 14% 14% 5.5% 8% 11% 11% 17% 17% 20% 20%

22 Impact assessment Change in SCR Medical expenses +5% Income protection ±0% Workers' compensation +15% NP reinsurance ±0% Premium and reserve risk +4% More details about the calibration on EIOPA's website: "Calibration of the Premium and Reserve Risk Factors in the Standard Formula of Solvency II"

23 Solvency Capital Requirement The SCR standard formula is not the last word! Recognition of health risk equalisation systems Undertaking-specific parameters Premium and reserve risk Revision risk Partial and full internal models Capital add-ons

Fifth Quantitative Impact Study of Solvency II (QIS5)

") Fifth Quantitative Impact Study of Solvency II (QIS5) Guidance on the treatment of German accident insurance with guaranteed premium repayment in the solvency balance sheet of QIS5 Introduction The UBR

Fifth Quantitative Impact Study of Solvency II (QIS5) Guidance on the treatment of German accident insurance with guaranteed premium repayment in the solvency balance sheet of QIS5 Introduction The UBR

An update on QIS5. Agenda 4/27/2010. Context, scope and timelines The draft Technical Specification Getting into gear Questions

A Closer Look at Solvency II Eleanor Beamond-Pepler, FSA An update on QIS5 2010 The Actuarial Profession www.actuaries.org.uk Agenda Context, scope and timelines The draft Technical Specification Getting

A Closer Look at Solvency II Eleanor Beamond-Pepler, FSA An update on QIS5 2010 The Actuarial Profession www.actuaries.org.uk Agenda Context, scope and timelines The draft Technical Specification Getting

Solvency II Standard Model for Health Insurance Business

Solvency II Standard Model for Health Insurance Business Hanno Reich KPMG AG, Germany kpmg Agenda 1. Solvency II Project 2. Future regulatory framework (Solvency II) 3. Calculation of Solvency Capital

Solvency II Standard Model for Health Insurance Business Hanno Reich KPMG AG, Germany kpmg Agenda 1. Solvency II Project 2. Future regulatory framework (Solvency II) 3. Calculation of Solvency Capital

CEIOPS-DOC-43/09. (former CP 50) October 2009

October 2009") CEIOPS-DOC-43/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: SCR standard formula - underwriting risk module (former CP 50) October 2009 CEIOPS e.v. Westhafenplatz 1-60327 Frankfurt

CEIOPS-DOC-43/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: SCR standard formula - underwriting risk module (former CP 50) October 2009 CEIOPS e.v. Westhafenplatz 1-60327 Frankfurt

SOLVENCY II HEALTH INSURANCE

2014 Solvency II Health SOLVENCY II HEALTH INSURANCE 1 Overview 1.1 Background and scope The current UK regulatory reporting regime is based on the EU Solvency I Directives. Although the latest of those

2014 Solvency II Health SOLVENCY II HEALTH INSURANCE 1 Overview 1.1 Background and scope The current UK regulatory reporting regime is based on the EU Solvency I Directives. Although the latest of those

FRAMEWORK FOR CONSULTATION OF CEIOPS AND OTHER STAKEHOLDERS ON SOLVENCY II

Annex 1 to MARKT/2506/04-EN FRAMEWORK FOR CONSULTATION OF CEIOPS AND OTHER STAKEHOLDERS ON SOLVENCY II Purpose of this document The purpose of this paper is to consult the Insurance Committee on a framework

Annex 1 to MARKT/2506/04-EN FRAMEWORK FOR CONSULTATION OF CEIOPS AND OTHER STAKEHOLDERS ON SOLVENCY II Purpose of this document The purpose of this paper is to consult the Insurance Committee on a framework

CEIOPS-DOC-47/09. (former CP 55) October 2009

October 2009") CEIOPS-DOC-47/09 Final CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Article 130 Calculation of the MCR (former CP 55) October 2009 CEIOPS e.v. Westhafenplatz 1-60327 Frankfurt Germany

CEIOPS-DOC-47/09 Final CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Article 130 Calculation of the MCR (former CP 55) October 2009 CEIOPS e.v. Westhafenplatz 1-60327 Frankfurt Germany

Solvency 2 Preparatory Phase. Comparison with LTGA specifications. June 2014

Solvency 2 Preparatory Phase Comparison with LTGA specifications June 2014 Summary This document presents: An analysis of the main changes between the Technical Specifications of the Long Term Guarantee

Solvency 2 Preparatory Phase Comparison with LTGA specifications June 2014 Summary This document presents: An analysis of the main changes between the Technical Specifications of the Long Term Guarantee

Fourth study of the Solvency II standard approach

Solvency Consulting Knowledge Series Your contacts Kathleen Ehrlich Tel.: +49 (89) 38 91-27 77 E-mail: kehrlich@munichre.com Dr. Rolf Stölting Tel.: +49 (89) 38 91-52 28 E-mail: rstoelting@munichre.com

Solvency Consulting Knowledge Series Your contacts Kathleen Ehrlich Tel.: +49 (89) 38 91-27 77 E-mail: kehrlich@munichre.com Dr. Rolf Stölting Tel.: +49 (89) 38 91-52 28 E-mail: rstoelting@munichre.com

CEIOPS-DOC-22/09. (former CP27) October 2009. CEIOPS e.v. Westhafenplatz 1-60327 Frankfurt Germany Tel. + 49 69-951119-20

October 2009. CEIOPS e.v. Westhafenplatz 1-60327 Frankfurt Germany Tel. + 49 69-951119-20") CEIOPS-DOC-22/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Technical Provisions - Lines of business on the basis of which (re)insurance obligations are to be segmented (former CP27)

CEIOPS-DOC-22/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Technical Provisions - Lines of business on the basis of which (re)insurance obligations are to be segmented (former CP27)

SOLVENCY II LIFE INSURANCE

SOLVENCY II LIFE INSURANCE 1 Overview 1.1 Background and scope The current UK regulatory reporting regime is based on the EU Solvency I Directives. Although the latest of those Directives was implemented

SOLVENCY II LIFE INSURANCE 1 Overview 1.1 Background and scope The current UK regulatory reporting regime is based on the EU Solvency I Directives. Although the latest of those Directives was implemented

Solvency II and catastrophe

Solvency II and catastrophe risks: Measurement approaches for propertycasualty insurers Country-specific requirements or standard formula? Authors: Dr. Kathleen Ehrlich Dr. Norbert Kuschel Contact solvency-solutions@munichre.com

Solvency II and catastrophe risks: Measurement approaches for propertycasualty insurers Country-specific requirements or standard formula? Authors: Dr. Kathleen Ehrlich Dr. Norbert Kuschel Contact solvency-solutions@munichre.com

Solvency II Introduction to Pillar 3. Friday 20 th May 2016

Solvency II Introduction to Pillar 3 Friday 20 th May 2016 Disclaimer The views expressed in this presentation are those of the presenter(s) and not necessarily of the Society of Actuaries in Ireland Introduction

Solvency II Introduction to Pillar 3 Friday 20 th May 2016 Disclaimer The views expressed in this presentation are those of the presenter(s) and not necessarily of the Society of Actuaries in Ireland Introduction

Solvency II Pillar III Quantitative Reporting Templates (QRTs) Sinead Clarke, Eoin King 11 th December 2012

Sinead Clarke, Eoin King 11 th December 2012") Solvency II Pillar III Quantitative Reporting Templates (QRTs) Sinead Clarke, Eoin King 11 th December 2012 Agenda Introduction and Background Summary of QRTs Reporting Timelines and Next Steps Questions

Solvency II Pillar III Quantitative Reporting Templates (QRTs) Sinead Clarke, Eoin King 11 th December 2012 Agenda Introduction and Background Summary of QRTs Reporting Timelines and Next Steps Questions

Texts passed by the European Council and Parliament Adapted by Member States

Introduction A few words about European Directives Texts passed by the European Council and Parliament Adapted by Member States Insurance law: What is going on? A draft directive under discussion = SOLVENCY

Introduction A few words about European Directives Texts passed by the European Council and Parliament Adapted by Member States Insurance law: What is going on? A draft directive under discussion = SOLVENCY

Quantitative Impact Study 1 (QIS1) Summary Report for Belgium. 21 March 2006

Summary Report for Belgium. 21 March 2006") Quantitative Impact Study 1 (QIS1) Summary Report for Belgium 21 March 2006 1 Quantitative Impact Study 1 (QIS1) Summary Report for Belgium INTRODUCTORY REMARKS...4 1. GENERAL OBSERVATIONS...4 1.1. Market

Quantitative Impact Study 1 (QIS1) Summary Report for Belgium 21 March 2006 1 Quantitative Impact Study 1 (QIS1) Summary Report for Belgium INTRODUCTORY REMARKS...4 1. GENERAL OBSERVATIONS...4 1.1. Market

Solvency ii: an overview. Lloyd s July 2010

Solvency ii: an overview Lloyd s July 2010 Contents Solvency II: key features Legislative process Solvency II implementation Conclusions 2 Solvency II: key features 3 Solvency II the basics Introduces

Solvency ii: an overview Lloyd s July 2010 Contents Solvency II: key features Legislative process Solvency II implementation Conclusions 2 Solvency II: key features 3 Solvency II the basics Introduces

SCOR inform - April 2012. Life (re)insurance under Solvency II

insurance under Solvency II") SCOR inform - April 2012 Life (re)insurance under Solvency II Life (re)insurance under Solvency II Author Thorsten Keil SCOR Global Life Cologne Editor Bérangère Mainguy Tel: +33 (0)1 58 44 70 00 Fax:

SCOR inform - April 2012 Life (re)insurance under Solvency II Life (re)insurance under Solvency II Author Thorsten Keil SCOR Global Life Cologne Editor Bérangère Mainguy Tel: +33 (0)1 58 44 70 00 Fax:

SOLVENCY II LIFE INSURANCE

2016 Solvency II Life SOLVENCY II LIFE INSURANCE 1 Overview 1.1 Background and scope The key objectives of Solvency II were to increase the level of harmonisation of solvency regulation across Europe,

2016 Solvency II Life SOLVENCY II LIFE INSURANCE 1 Overview 1.1 Background and scope The key objectives of Solvency II were to increase the level of harmonisation of solvency regulation across Europe,

SOLVENCY II HEALTH INSURANCE

2016 Solvency II Health SOLVENCY II HEALTH INSURANCE 1 Overview 1.1 Background and scope The key objectives of Solvency II were to increase the level of harmonisation of solvency regulation across Europe,

2016 Solvency II Health SOLVENCY II HEALTH INSURANCE 1 Overview 1.1 Background and scope The key objectives of Solvency II were to increase the level of harmonisation of solvency regulation across Europe,

The standard formula requires further adjustments

EIOPA publishes the results of the fifth quantitative impact study (QIS5) The standard formula requires further adjustments Authors Martin Brosemer Dr. Kathleen Ehrlich Dr. Norbert Kuschel Lars Moormann

EIOPA publishes the results of the fifth quantitative impact study (QIS5) The standard formula requires further adjustments Authors Martin Brosemer Dr. Kathleen Ehrlich Dr. Norbert Kuschel Lars Moormann

Implementation of Solvency II

undertaking-specific parameters Are there alternatives to an internal model? Authors Dr. Kathleen Ehrlich Dr. Manijeh Schwindt Dr. Norbert Kuschel Contact solvency-solutions@munichre.com June 2012 The

undertaking-specific parameters Are there alternatives to an internal model? Authors Dr. Kathleen Ehrlich Dr. Manijeh Schwindt Dr. Norbert Kuschel Contact solvency-solutions@munichre.com June 2012 The

Guidelines on undertaking-specific parameters

EIOPA-BoS-14/178 EN Guidelines on undertaking-specific parameters EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20; Fax. + 49 69-951119-19; email: info@eiopa.europa.eu

EIOPA-BoS-14/178 EN Guidelines on undertaking-specific parameters EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20; Fax. + 49 69-951119-19; email: info@eiopa.europa.eu

Solvency II for Beginners 16.05.2013

Solvency II for Beginners 16.05.2013 Agenda Why has Solvency II been created? Structure of Solvency II The Solvency II Balance Sheet Pillar II & III Aspects Where are we now? Solvency II & Actuaries Why

Solvency II for Beginners 16.05.2013 Agenda Why has Solvency II been created? Structure of Solvency II The Solvency II Balance Sheet Pillar II & III Aspects Where are we now? Solvency II & Actuaries Why

FSA UK Country Report

Financial Services Authority FSA UK Country Report The fifth Quantitative Impact Study (QIS5) for Solvency II March 2011 Contents 1 Introduction 3 2 Participation 6 3 Quality 8 4 Preparedness and resourcing

Financial Services Authority FSA UK Country Report The fifth Quantitative Impact Study (QIS5) for Solvency II March 2011 Contents 1 Introduction 3 2 Participation 6 3 Quality 8 4 Preparedness and resourcing

International Financial Reporting for Insurers: IFRS and U.S. GAAP September 2009 Session 25: Solvency II vs. IFRS

International Financial Reporting for Insurers: IFRS and U.S. GAAP September 2009 Session 25: Solvency II vs. IFRS Simon Walpole Solvency II Simon Walpole Solvency II Agenda Introduction to Solvency II

International Financial Reporting for Insurers: IFRS and U.S. GAAP September 2009 Session 25: Solvency II vs. IFRS Simon Walpole Solvency II Simon Walpole Solvency II Agenda Introduction to Solvency II

CEIOPS-DOC-33/09. (former CP 39) October 2009

October 2009") CEIOPS-DOC-33/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Technical provisions Article 86 a Actuarial and statistical methodologies to calculate the best estimate (former CP 39)

CEIOPS-DOC-33/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Technical provisions Article 86 a Actuarial and statistical methodologies to calculate the best estimate (former CP 39)

CEIOPS-DOC-45/09. (former CP 53) October 2009

October 2009") CEIOPS-DOC-45/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: SCR standard formula - Article 111 (f) Operational Risk (former CP 53) October 2009 CEIOPS e.v. Westhafenplatz 1-60327 Frankfurt

CEIOPS-DOC-45/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: SCR standard formula - Article 111 (f) Operational Risk (former CP 53) October 2009 CEIOPS e.v. Westhafenplatz 1-60327 Frankfurt

Insurance Groups under Solvency II

Insurance Groups under Solvency II November 2013 Table of Contents 1. Introduction... 2 2. Defining an insurance group... 2 3. Cases of application of group supervision... 6 4. The scope of group supervision...

Insurance Groups under Solvency II November 2013 Table of Contents 1. Introduction... 2 2. Defining an insurance group... 2 3. Cases of application of group supervision... 6 4. The scope of group supervision...

Treatment of technical provisions under Solvency II

Treatment of technical provisions under Solvency II Quantitative methods, qualitative requirements and disclosure obligations Authors Martin Brosemer Dr. Susanne Lepschi Dr. Katja Lord Contact solvency-solutions@munichre.com

Treatment of technical provisions under Solvency II Quantitative methods, qualitative requirements and disclosure obligations Authors Martin Brosemer Dr. Susanne Lepschi Dr. Katja Lord Contact solvency-solutions@munichre.com

Solvency II overview

David Payne, FIA Casualty Loss Reserve Seminar 15 September 2011 INTNL-2: Solvency II Update Antitrust Notice The Casualty Actuarial Society is committed to adhering strictly to the letter and spirit of

David Payne, FIA Casualty Loss Reserve Seminar 15 September 2011 INTNL-2: Solvency II Update Antitrust Notice The Casualty Actuarial Society is committed to adhering strictly to the letter and spirit of

THE INSURANCE BUSINESS (SOLVENCY) RULES 2015

RULES 2015") THE INSURANCE BUSINESS (SOLVENCY) RULES 2015 Table of Contents Part 1 Introduction... 2 Part 2 Capital Adequacy... 4 Part 3 MCR... 7 Part 4 PCR... 10 Part 5 - Internal Model... 23 Part 6 Valuation... 34

THE INSURANCE BUSINESS (SOLVENCY) RULES 2015 Table of Contents Part 1 Introduction... 2 Part 2 Capital Adequacy... 4 Part 3 MCR... 7 Part 4 PCR... 10 Part 5 - Internal Model... 23 Part 6 Valuation... 34

INVESTMENT FUNDS: Funds investments. KPMG Business DialogueS November 4 th 2011

INVESTMENT FUNDS: Impact of Solvency II Directive on Funds investments KPMG Business DialogueS November 4 th 2011 Map of the presentation Introduction The first consequences for asset managers and investors

INVESTMENT FUNDS: Impact of Solvency II Directive on Funds investments KPMG Business DialogueS November 4 th 2011 Map of the presentation Introduction The first consequences for asset managers and investors

Solvency II: Implications for Loss Reserving

Solvency II: Implications for Loss Reserving John Charles Doug Collins CLRS: 12 September 2006 Agenda Solvency II Introduction Pre-emptive adopters Solvency II concepts Quantitative Impact Studies Internal

Solvency II: Implications for Loss Reserving John Charles Doug Collins CLRS: 12 September 2006 Agenda Solvency II Introduction Pre-emptive adopters Solvency II concepts Quantitative Impact Studies Internal

Solvency II. Solvency II implemented on 1 January 2016. Why replace Solvency I? To which insurance companies does the new framework apply?

Solvency II A new framework for prudential supervision of insurance companies 1 Solvency II implemented on 1 January 2016. 1 January 2016 marks the introduction of Solvency II, a new framework for the

Solvency II A new framework for prudential supervision of insurance companies 1 Solvency II implemented on 1 January 2016. 1 January 2016 marks the introduction of Solvency II, a new framework for the

Insurance Roadshow London, October 2008. Solvency 2 Update

Insurance Roadshow London, October 2008 Solvency 2 Update Agenda Progress to date Overview of key component of Solvency 2 Further issues for discussion Impact on ratings Solvency 2 - What s new? Progress

Insurance Roadshow London, October 2008 Solvency 2 Update Agenda Progress to date Overview of key component of Solvency 2 Further issues for discussion Impact on ratings Solvency 2 - What s new? Progress

Introduction to Solvency II

Introduction to Solvency II Tim Edwards Gavin Dunkerley 24 th September 2008 Introduction The primary purpose of this presentation is to explain what Solvency II is and why it is important We also hope

Introduction to Solvency II Tim Edwards Gavin Dunkerley 24 th September 2008 Introduction The primary purpose of this presentation is to explain what Solvency II is and why it is important We also hope

Solvency II Technical Provisions valuation as at 31st december 2010. submission template instructions

Solvency II Technical Provisions valuation as at 31st december 2010 submission template instructions Introduction As set out in the Guidance Notes for the 2011 Dry Run Review Process, calculation of Technical

Solvency II Technical Provisions valuation as at 31st december 2010 submission template instructions Introduction As set out in the Guidance Notes for the 2011 Dry Run Review Process, calculation of Technical

CEIOPS-QIS5-06/10 6 September 2010

CEIOPS-QIS5-06/10 6 September 2010 Manual for the completion of the QIS5 spreadsheet (for solo undertakings) Please note that this manual is not part of the formal QIS5 documentation as issued by the European

CEIOPS-QIS5-06/10 6 September 2010 Manual for the completion of the QIS5 spreadsheet (for solo undertakings) Please note that this manual is not part of the formal QIS5 documentation as issued by the European

SA QIS3 Key changes and challenges The end is in sight

SA QIS3 Key changes and challenges The end is in sight December 2013 Contents Introduction 1 Balance sheet 2 Assets and liabilities other than technical provisions 3 Technical provisions 4 Segmentation

SA QIS3 Key changes and challenges The end is in sight December 2013 Contents Introduction 1 Balance sheet 2 Assets and liabilities other than technical provisions 3 Technical provisions 4 Segmentation

ORSA - The heart of Solvency II

ORSA - The heart of Solvency II Groupe Consultatif Summer School Gabriel Bernardino, EIOPA Lisbon, 25 May 2011 ORSA - The heart of Solvency II Developing the regulatory framework for Solvency II ORSA it

ORSA - The heart of Solvency II Groupe Consultatif Summer School Gabriel Bernardino, EIOPA Lisbon, 25 May 2011 ORSA - The heart of Solvency II Developing the regulatory framework for Solvency II ORSA it

Summary of Comments on CEIOPS-CP-50/09 Consultation Paper on the Draft L2 Advice on SCR Standard Formula - Health underwriting risk

CEIOPS would like to thank AAS BALTA, AB Lietuvos draudimas, AMICE, Association of British Insurers, Belgian Coordination Group Solvency II (Assuralia/, Bupa, CEA,, Centre Technique des Institutions de

CEIOPS would like to thank AAS BALTA, AB Lietuvos draudimas, AMICE, Association of British Insurers, Belgian Coordination Group Solvency II (Assuralia/, Bupa, CEA,, Centre Technique des Institutions de

Guidelines on the valuation of technical provisions

EIOPA-BoS-14/166 EN Guidelines on the valuation of technical provisions EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20; Fax. + 49 69-951119-19; email: info@eiopa.europa.eu

EIOPA-BoS-14/166 EN Guidelines on the valuation of technical provisions EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20; Fax. + 49 69-951119-19; email: info@eiopa.europa.eu

Guidelines on ring-fenced funds

EIOPA-BoS-14/169 EN Guidelines on ring-fenced funds EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20; Fax. + 49 69-951119-19; email: info@eiopa.europa.eu site: https://eiopa.europa.eu/

EIOPA-BoS-14/169 EN Guidelines on ring-fenced funds EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20; Fax. + 49 69-951119-19; email: info@eiopa.europa.eu site: https://eiopa.europa.eu/

Solvency II Standard Formula and NAIC Risk-Based Capital (RBC)

") Solvency II Standard Formula and NAIC Risk-Based Capital (RBC) Report 3 of the CAS Risk-Based Capital (RBC) Research Working Parties Issued by the RBC Dependencies and Calibration Working Party (DCWP)

Solvency II Standard Formula and NAIC Risk-Based Capital (RBC) Report 3 of the CAS Risk-Based Capital (RBC) Research Working Parties Issued by the RBC Dependencies and Calibration Working Party (DCWP)

SOLVENCY II GENERAL INSURANCE

SOLVENCY II GENERAL INSURANCE 1 Solvency II 1.1 Background to development of Solvency II During the development of Solvency II key objectives were maintained: to increase the level of harmonisation of

SOLVENCY II GENERAL INSURANCE 1 Solvency II 1.1 Background to development of Solvency II During the development of Solvency II key objectives were maintained: to increase the level of harmonisation of

KPMG Business DialogueS

KPMG Business DialogueS KPMG Luxembourg May 30, 2012 Solvency II, Pillar 3 Chrystelle Veeckmans, Director, Audit services Geoffroy Gailly, Director, Management Consulting Pascal Föhr, Senior Manager, Audit

KPMG Business DialogueS KPMG Luxembourg May 30, 2012 Solvency II, Pillar 3 Chrystelle Veeckmans, Director, Audit services Geoffroy Gailly, Director, Management Consulting Pascal Föhr, Senior Manager, Audit

CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Articles 120 to 126. Tests and Standards for Internal Model Approval

CEIOPS-DOC-48/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Articles 120 to 126 Tests and Standards for Internal Model Approval (former Consultation Paper 56) October 2009 CEIOPS e.v.

CEIOPS-DOC-48/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Articles 120 to 126 Tests and Standards for Internal Model Approval (former Consultation Paper 56) October 2009 CEIOPS e.v.

Preparing for ORSA - Some practical issues Speaker:

2013 Seminar for the Appointed Actuary Colloque pour l actuaire désigné 2013 Session 13: Preparing for ORSA - Some practical issues Speaker: André Racine, Principal Eckler Ltd. Context of ORSA Agenda Place

2013 Seminar for the Appointed Actuary Colloque pour l actuaire désigné 2013 Session 13: Preparing for ORSA - Some practical issues Speaker: André Racine, Principal Eckler Ltd. Context of ORSA Agenda Place

Revised Annexes to the Technical Specifications for the Solvency II valuation and Solvency Capital Requirements calculations (Part I)

") EIOPA-DOC-12/467 21 December 2012 Revised Annexes to the Technical Specifications for the Solvency II valuation and Solvency Capital Requirements calculations (Part I) 1 TABLE OF CONTENT ANNEX A - DEFINITION

EIOPA-DOC-12/467 21 December 2012 Revised Annexes to the Technical Specifications for the Solvency II valuation and Solvency Capital Requirements calculations (Part I) 1 TABLE OF CONTENT ANNEX A - DEFINITION

Regulatory Solvency Assessment of Property/Casualty Insurance Companies in the United States

Regulatory Solvency Assessment of Property/Casualty Insurance Companies in the United States A presentation by Robert F. Conger Past-President, Casualty Actuarial Society September 2013 Regulatory Solvency

Regulatory Solvency Assessment of Property/Casualty Insurance Companies in the United States A presentation by Robert F. Conger Past-President, Casualty Actuarial Society September 2013 Regulatory Solvency

Solvency Assessment and Management Third South African Quantitative Impact Study (SA QIS3)

") CONTACT DETAILS Physical Address: Riverwalk Solvency Assessment and Management Third South African Quantitative Impact Study (SA QIS3) Draft Technical Specifications Part 4 of 6: SCR Life Underwriting

CONTACT DETAILS Physical Address: Riverwalk Solvency Assessment and Management Third South African Quantitative Impact Study (SA QIS3) Draft Technical Specifications Part 4 of 6: SCR Life Underwriting

Solvency 2 and captives a SWERMA perspective

Solvency 2 and captives a SWERMA perspective Some especially important Pillar 1 issues: By way of introduction it s noted that CEIOPS (see footnote 2) in reference to Article 111 (j) makes certain proposals

Solvency 2 and captives a SWERMA perspective Some especially important Pillar 1 issues: By way of introduction it s noted that CEIOPS (see footnote 2) in reference to Article 111 (j) makes certain proposals

Consultation Paper on the Proposal for Guidelines on submission of information to national competent authorities

EIOPA-CP-13/010 27 March 2013 Consultation Paper on the Proposal for Guidelines on submission of information to national competent authorities Page 1 of 268 Table of Contents Responding to this paper...

EIOPA-CP-13/010 27 March 2013 Consultation Paper on the Proposal for Guidelines on submission of information to national competent authorities Page 1 of 268 Table of Contents Responding to this paper...

Actuarial Discipline: Threat or Opportunity?

Actuarial Discipline: Threat or Opportunity? Risk and Investment Conference Brighton, 17 June 2013 Prof. Karel Van Hulle KU Leuven and Goethe University Frankfurt Actuarial Discipline The importance of

Actuarial Discipline: Threat or Opportunity? Risk and Investment Conference Brighton, 17 June 2013 Prof. Karel Van Hulle KU Leuven and Goethe University Frankfurt Actuarial Discipline The importance of

Health SLT risks for income protection insurance under Solvency II

riss for income protection insurance under Solvency II Nataliya Boyo 5640229 28 Mei, 2011 Master thesis Drs. R. Bruning AAG Faculty of Economics and Business University of Amsterdam Content 1 Introduction

riss for income protection insurance under Solvency II Nataliya Boyo 5640229 28 Mei, 2011 Master thesis Drs. R. Bruning AAG Faculty of Economics and Business University of Amsterdam Content 1 Introduction

Solvency II. 2014 Standard Formula Exercise Guidance Notes. February 2014

Solvency II 2014 Standard Formula Exercise Guidance Notes February 2014 Disclaimer No responsibility of liability is accepted by the Society of Lloyd s, the Council, or any Committee of Board constituted

Solvency II 2014 Standard Formula Exercise Guidance Notes February 2014 Disclaimer No responsibility of liability is accepted by the Society of Lloyd s, the Council, or any Committee of Board constituted

Impacts of the Solvency II Standard Formula on health insurance business in Germany

Impacts of the Solvency II Standard Formula on health insurance business in Germany Sascha Raithel Association of German private healthcare insurers Agenda 1. Private health insurance business in Germany

Impacts of the Solvency II Standard Formula on health insurance business in Germany Sascha Raithel Association of German private healthcare insurers Agenda 1. Private health insurance business in Germany

Regulations in General Insurance. Solvency II

Regulations in General Insurance Solvency II Solvency II What is it? Solvency II is a new risk-based regulatory requirement for insurance, reinsurance and bancassurance (insurance) organisations that operate

Regulations in General Insurance Solvency II Solvency II What is it? Solvency II is a new risk-based regulatory requirement for insurance, reinsurance and bancassurance (insurance) organisations that operate

NST.06 - Non-life Insurance Claims Information - Detailed split by Distribution Channel and Claims Type.

NST.06 - Non-life Insurance Claims Information - Detailed split by Distribution Channel and Claims Type. The first column of the next table identifies the items to be reported by identifying the columns

NST.06 - Non-life Insurance Claims Information - Detailed split by Distribution Channel and Claims Type. The first column of the next table identifies the items to be reported by identifying the columns

EIOPACP 13/011. Guidelines on PreApplication of Internal Models

EIOPACP 13/011 Guidelines on PreApplication of Internal Models EIOPA Westhafen Tower, Westhafenplatz 1 60327 Frankfurt Germany Tel. + 49 6995111920; Fax. + 49 6995111919; site: www.eiopa.europa.eu Guidelines

EIOPACP 13/011 Guidelines on PreApplication of Internal Models EIOPA Westhafen Tower, Westhafenplatz 1 60327 Frankfurt Germany Tel. + 49 6995111920; Fax. + 49 6995111919; site: www.eiopa.europa.eu Guidelines

'SOLVENCY II': Frequently Asked Questions (FAQs)

") EUROPEAN COMMISSION Internal Market and Services DG FINANCIAL INSTITUTIONS Insurance and pensions 'SOLVENCY II': Frequently Asked Questions (FAQs) 1. Why does the EU need harmonised solvency rules? The

EUROPEAN COMMISSION Internal Market and Services DG FINANCIAL INSTITUTIONS Insurance and pensions 'SOLVENCY II': Frequently Asked Questions (FAQs) 1. Why does the EU need harmonised solvency rules? The

Solvency II New Framework for Risk Management Organisation. Dr. Maciej Sterzynski (Triglav Insurance, Ltd.) Matija Bitenc (Triglav Insurance, Ltd.

Matija Bitenc (Triglav Insurance, Ltd.") Solvency II New Framework for Risk Management Organisation Dr. Maciej Sterzynski (Triglav Insurance, Ltd.) Matija Bitenc (Triglav Insurance, Ltd.) 1 AGENDA ð Understanding Solvency II ð Setting up Integrated

Solvency II New Framework for Risk Management Organisation Dr. Maciej Sterzynski (Triglav Insurance, Ltd.) Matija Bitenc (Triglav Insurance, Ltd.) 1 AGENDA ð Understanding Solvency II ð Setting up Integrated

ORSA for Insurers A Global Concept

ORSA for Insurers A Global Concept Stuart Wason, FSA, FCIA, MAAA, CERA Senior Director, Actuarial Division Office of the Superintendent of Financial Institutions Canada (OSFI) Table of Contents Early developments

ORSA for Insurers A Global Concept Stuart Wason, FSA, FCIA, MAAA, CERA Senior Director, Actuarial Division Office of the Superintendent of Financial Institutions Canada (OSFI) Table of Contents Early developments

Embedded Value Report

Embedded Value Report 2012 ACHMEA EMBEDDED VALUE REPORT 2012 Contents Management summary 3 Introduction 4 Embedded Value Results 5 Value Added by New Business 6 Analysis of Change 7 Sensitivities 9 Impact

Embedded Value Report 2012 ACHMEA EMBEDDED VALUE REPORT 2012 Contents Management summary 3 Introduction 4 Embedded Value Results 5 Value Added by New Business 6 Analysis of Change 7 Sensitivities 9 Impact

COMMISSION DELEGATED DECISION (EU) / of 5.6.2015

/ of 5.6.2015") EUROPEAN COMMISSION Brussels, 5.6.2015 C(2015) 3740 final COMMISSION DELEGATED DECISION (EU) / of 5.6.2015 on the provisional equivalence of the solvency regimes in force in Australia, Bermuda, Brazil,

EUROPEAN COMMISSION Brussels, 5.6.2015 C(2015) 3740 final COMMISSION DELEGATED DECISION (EU) / of 5.6.2015 on the provisional equivalence of the solvency regimes in force in Australia, Bermuda, Brazil,

Central Bank of Ireland Guidelines on Preparing for Solvency II Pre-application for Internal Models

2013 Central Bank of Ireland Guidelines on Preparing for Solvency II Pre-application for Internal Models 1 Contents 1 Context... 1 2 General... 2 3 Guidelines on Pre-application for Internal Models...

2013 Central Bank of Ireland Guidelines on Preparing for Solvency II Pre-application for Internal Models 1 Contents 1 Context... 1 2 General... 2 3 Guidelines on Pre-application for Internal Models...

Public Report. November 2007

CEIOPS-DOC-19/07 CEIOPS Report on its third Quantitative Impact Study (QIS3) for Solvency II Public Report November 2007 CEIOPS e.v. - Westhafenplatz 1 60327 Frankfurt am Main Germany Tel. + 49 69-951119-20

CEIOPS-DOC-19/07 CEIOPS Report on its third Quantitative Impact Study (QIS3) for Solvency II Public Report November 2007 CEIOPS e.v. - Westhafenplatz 1 60327 Frankfurt am Main Germany Tel. + 49 69-951119-20

EIOPA technical specifications for Long-Term Guarantee Assessment. January 2013. Milliman Solvency II Update

EIOPA technical specifications for Long-Term Guarantee Assessment January 2013 The Long-Term Guarantee Assessment requires participating firms to test the application of the proposed package of measures

EIOPA technical specifications for Long-Term Guarantee Assessment January 2013 The Long-Term Guarantee Assessment requires participating firms to test the application of the proposed package of measures

2015 No. 575 FINANCIAL SERVICES AND MARKETS. The Solvency 2 Regulations 2015

S T A T U T O R Y I N S T R U M E N T S 2015 No. 575 FINANCIAL SERVICES AND MARKETS The Solvency 2 Regulations 2015 Made - - - - 6th March 2015 Laid before Parliament 9th March 2015 Coming into force in

S T A T U T O R Y I N S T R U M E N T S 2015 No. 575 FINANCIAL SERVICES AND MARKETS The Solvency 2 Regulations 2015 Made - - - - 6th March 2015 Laid before Parliament 9th March 2015 Coming into force in

1. INTRODUCTION AND PURPOSE

Solvency Assessment and Management: Pillar 1 - Sub Committee Capital Requirements Task Group Discussion Document 73 (v 2) Treatment of new business in SCR EXECUTIVE SUMMARY As for the Solvency II Framework

Solvency Assessment and Management: Pillar 1 - Sub Committee Capital Requirements Task Group Discussion Document 73 (v 2) Treatment of new business in SCR EXECUTIVE SUMMARY As for the Solvency II Framework

CEIOPS-DOC-36/09. (former CP 42) October 2009

October 2009") CEIOPS-DOC-36/09 Final CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Technical Provisions Article 86 (d) Calculation of the Risk Margin (former CP 42) October 2009 CEIOPS e.v. Westhafenplatz

CEIOPS-DOC-36/09 Final CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Technical Provisions Article 86 (d) Calculation of the Risk Margin (former CP 42) October 2009 CEIOPS e.v. Westhafenplatz

Méthode de provisionnement en assurance non-vie Solvency II & IFRS

Méthode de provisionnement en assurance non-vie Solvency II & IFRS A Revolution of the Insurance Business Model Journées d économétrie et d économie de l'assurance 22 octobre 2009 1 Yannick APPERT-RAULLIN

Méthode de provisionnement en assurance non-vie Solvency II & IFRS A Revolution of the Insurance Business Model Journées d économétrie et d économie de l'assurance 22 octobre 2009 1 Yannick APPERT-RAULLIN

Consequences. Modelling. Starting Points. Timetable. Solvency II. Solvency I vs Solvency II. Solvency I

Consequences Modelling Starting Points Timetable Pillar I Minimum Capital Requirements Pillar II Supervisory Review Pillar III Market Discipline Solvency II Solvency I vs Solvency II Solvency I Solvency

Consequences Modelling Starting Points Timetable Pillar I Minimum Capital Requirements Pillar II Supervisory Review Pillar III Market Discipline Solvency II Solvency I vs Solvency II Solvency I Solvency

Solvency II in practice. Speaker: Tim O Hanrahan Deputy Head, Insurance, Central Bank of Ireland 16 March 2016

1 Solvency II in practice Speaker: Tim O Hanrahan Deputy Head, Insurance, Central Bank of Ireland 16 March 2016 1 Recap on Solvency II Regulatory Framework under Solvency II Pillar I - Capital Pillar II

1 Solvency II in practice Speaker: Tim O Hanrahan Deputy Head, Insurance, Central Bank of Ireland 16 March 2016 1 Recap on Solvency II Regulatory Framework under Solvency II Pillar I - Capital Pillar II

Biljana Petrevska 1, PhD SOLVENCY II SUPERVISION OF THE INSURANCE UNDERTAKINGS RISK MANAGEMENT SYSTEMS. Abstract

Biljana Petrevska 1, PhD SOLVENCY II SUPERVISION OF THE INSURANCE UNDERTAKINGS RISK MANAGEMENT SYSTEMS Abstract The main purpose of this paper is to analyze Solvency II which is a new supranational insurance

Biljana Petrevska 1, PhD SOLVENCY II SUPERVISION OF THE INSURANCE UNDERTAKINGS RISK MANAGEMENT SYSTEMS Abstract The main purpose of this paper is to analyze Solvency II which is a new supranational insurance

The European solvency margin: an update for Italian non-life insurance companies

The European solvency margin: an update for Italian non-life insurance companies Alberto Dreassi* and Stefano Miani** This paper analyses the main underlying quantitative approach of the European Solvency

The European solvency margin: an update for Italian non-life insurance companies Alberto Dreassi* and Stefano Miani** This paper analyses the main underlying quantitative approach of the European Solvency

SAS AND CRYSTAL SYSTEM EMPOWERING SOLVENCY II FIAR - THE INTERNATIONAL INSURANCE-REINSURANCE FORUM 2014, BRASOV

SAS AND CRYSTAL SYSTEM EMPOWERING SOLVENCY II FIAR - THE INTERNATIONAL INSURANCE-REINSURANCE FORUM 2014, BRASOV HIGH PERFORMANCE ANALYTICS CRYSTAL SYSTEM 2001 Crystal System Bucharest Near-Shore factory

SAS AND CRYSTAL SYSTEM EMPOWERING SOLVENCY II FIAR - THE INTERNATIONAL INSURANCE-REINSURANCE FORUM 2014, BRASOV HIGH PERFORMANCE ANALYTICS CRYSTAL SYSTEM 2001 Crystal System Bucharest Near-Shore factory

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014

Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014") Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial year from 1 January 2014 to 31 December 2014

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial year from 1 January 2014 to 31 December 2014

SOLVENCY II Level 2 Implementing Measures

SOLVENCY II Level 2 Implementing Measures Executive Summary Position After the Three Waves of Consultation Papers and the Quantitative Impact Study 5 Technical Specifications August 2010 The data and information

SOLVENCY II Level 2 Implementing Measures Executive Summary Position After the Three Waves of Consultation Papers and the Quantitative Impact Study 5 Technical Specifications August 2010 The data and information

CEA Working Paper on the risk measures VaR and TailVaR

CEA Working Paper on the risk measures VaR and TailVaR CEA reference: ECO 6294 Date: 7 November 2006 Referring to: Solvency II Related CEA documents: See Appendix Contact person: Patricia Plas, ECOFIN

CEA Working Paper on the risk measures VaR and TailVaR CEA reference: ECO 6294 Date: 7 November 2006 Referring to: Solvency II Related CEA documents: See Appendix Contact person: Patricia Plas, ECOFIN

STATUTORY INSTRUMENTS. S.I. No. 485 of 2015 EUROPEAN UNION (INSURANCE AND REINSURANCE) REGULATIONS 2015

REGULATIONS 2015") STATUTORY INSTRUMENTS. S.I. No. 485 of 2015 EUROPEAN UNION (INSURANCE AND REINSURANCE) REGULATIONS 2015 2 [485] S.I. No. 485 of 2015 EUROPEAN UNION (INSURANCE AND REINSURANCE) REGULATIONS 2015 1. Citation

STATUTORY INSTRUMENTS. S.I. No. 485 of 2015 EUROPEAN UNION (INSURANCE AND REINSURANCE) REGULATIONS 2015 2 [485] S.I. No. 485 of 2015 EUROPEAN UNION (INSURANCE AND REINSURANCE) REGULATIONS 2015 1. Citation

Solvency II. PwC. *connected thinking. Internal models requirements and an example

Solvency II Internal models requirements and an example *connected thinking PwC Solvency II introduced the possibility to use an internal model to estimate solvency capital requirements (SCR) No cherry-picking

Solvency II Internal models requirements and an example *connected thinking PwC Solvency II introduced the possibility to use an internal model to estimate solvency capital requirements (SCR) No cherry-picking

2. The European insurance sector

2. The European insurance sector Insurance companies are still exposed to the low interest rate environment. Long-term interest rates are especially of importance to life insurers, since these institutions

2. The European insurance sector Insurance companies are still exposed to the low interest rate environment. Long-term interest rates are especially of importance to life insurers, since these institutions

Implementation of Solvency II: The dos and the don ts

KEYNOTE SPEECH Gabriel Bernardino Chairman of EIOPA Implementation of Solvency II: The dos and the don ts International conference Solvency II: What Can Go Wrong? Ljubljana, 2 September 2015 Page 2 of

KEYNOTE SPEECH Gabriel Bernardino Chairman of EIOPA Implementation of Solvency II: The dos and the don ts International conference Solvency II: What Can Go Wrong? Ljubljana, 2 September 2015 Page 2 of

02/06/2014. Solvency II update. Agenda. Recap: Solvency II three pillar approach. Nick Ford

Solvency II update Nick Ford 02 June 2014 Agenda Intro and brief recap Pillar 1 Main issues Impacts on products Pillar 2 Main issues Internal Model Approval Pillar 3 Actuarial forms and concerns Timelines

Solvency II update Nick Ford 02 June 2014 Agenda Intro and brief recap Pillar 1 Main issues Impacts on products Pillar 2 Main issues Internal Model Approval Pillar 3 Actuarial forms and concerns Timelines

ANALYSTS' DINNER UPDATE ON SOLVENCY II. London, 14 December 2011. Jörg Schneider Joachim Oechslin Jürgen Dümont

ANALYSTS' DINNER UPDATE ON SOLVENCY II London, 14 December 2011 Jörg Schneider Joachim Oechslin Jürgen Dümont Solvency II Fuelling a global trend towards risk-based supervision(?) Influence of Solvency

ANALYSTS' DINNER UPDATE ON SOLVENCY II London, 14 December 2011 Jörg Schneider Joachim Oechslin Jürgen Dümont Solvency II Fuelling a global trend towards risk-based supervision(?) Influence of Solvency

Report on the findings

Parallel Run on the Valuation of Long Term Insurance Business, Risk Based Capital Requirements for Insurers and Non-Life Outstanding Claims Reserves. Report on the findings TABLE OF CONTENTS EXECUTIVE

Parallel Run on the Valuation of Long Term Insurance Business, Risk Based Capital Requirements for Insurers and Non-Life Outstanding Claims Reserves. Report on the findings TABLE OF CONTENTS EXECUTIVE

Feedback on the 2012 thematic review of technical provisions

Feedback on the 2012 thematic review of technical provisions Introduction Background In late 2012 the FSA published a question bank 1 on Solvency II (SII) technical provisions for completion by general

Feedback on the 2012 thematic review of technical provisions Introduction Background In late 2012 the FSA published a question bank 1 on Solvency II (SII) technical provisions for completion by general

15 April 2015 Kurt Svoboda, CFRO. UNIQA Insurance Group AG Economic Capital and Embedded Value 2014

15 April 2015 Kurt Svoboda, CFRO UNIQA Insurance Group AG Economic Capital and Embedded Value 2014 Economic Capital Embedded Value Sensitivities and other analysis Appendix Assumptions Glossary & Disclaimer

15 April 2015 Kurt Svoboda, CFRO UNIQA Insurance Group AG Economic Capital and Embedded Value 2014 Economic Capital Embedded Value Sensitivities and other analysis Appendix Assumptions Glossary & Disclaimer

Important note: This document is a working document of the Commission services for discussion. It does not purport to represent or pre-judge the

DRAFT Technical specifications for QIS 5 Important note: This document is a working document of the Commission services for discussion. It does not purport to represent or pre-judge the formal proposals

DRAFT Technical specifications for QIS 5 Important note: This document is a working document of the Commission services for discussion. It does not purport to represent or pre-judge the formal proposals

Gabriel Bernardino Chairman of EIOPA

Solvency II status update Gabriel Bernardino Chairman of EIOPA KPMG Czech Republic Solvency Conference KPMG Czech Republic Solvency Conference Prague, 12 April 2012 Where is Solvency II? Directive (O.J.

Solvency II status update Gabriel Bernardino Chairman of EIOPA KPMG Czech Republic Solvency Conference KPMG Czech Republic Solvency Conference Prague, 12 April 2012 Where is Solvency II? Directive (O.J.

Final Report. Public Consultation No. 14/036 on. Guidelines on application of outwards reinsurance. arrangements to the non-life

EIOPA-BoS-14/173 27 November 2014 Final Report on Public Consultation No. 14/036 on Guidelines on application of outwards reinsurance arrangements to the non-life underwriting risk sub-module EIOPA Westhafen

EIOPA-BoS-14/173 27 November 2014 Final Report on Public Consultation No. 14/036 on Guidelines on application of outwards reinsurance arrangements to the non-life underwriting risk sub-module EIOPA Westhafen

Consultation Paper CP22/16 Solvency II: Monitoring model drift and standard formula SCR reporting for firms with an approved internal model

Consultation Paper CP22/16 Solvency II: Monitoring model drift and standard formula SCR reporting for firms with an approved internal model May 2016 Prudential Regulation Authority 20 Moorgate London EC2R

Consultation Paper CP22/16 Solvency II: Monitoring model drift and standard formula SCR reporting for firms with an approved internal model May 2016 Prudential Regulation Authority 20 Moorgate London EC2R

Non Life Insurance risk management in the Insurance company : CSOB case studies

Non Life Insurance risk management in the Insurance company : CSOB case studies Content Topics : case study Non Life Insurance risk management, 1. Non Life Insurance 2. Case study Example of non life insurance

Non Life Insurance risk management in the Insurance company : CSOB case studies Content Topics : case study Non Life Insurance risk management, 1. Non Life Insurance 2. Case study Example of non life insurance

Making it clear Reporting and disclosure in the Solvency II world

Making it clear Reporting and disclosure in the Solvency II world The Solvency II Directive is built around the 3 pillars of quantitative requirements (Pillar 1), supervisory review (Pillar 2) and disclosure

Making it clear Reporting and disclosure in the Solvency II world The Solvency II Directive is built around the 3 pillars of quantitative requirements (Pillar 1), supervisory review (Pillar 2) and disclosure

ORSA for Dummies. Institute of Risk Management Solvency II Group April 17th 2012. Peter Taylor

ORSA for Dummies Institute of Risk Management Solvency II Group April 17th 2012 Peter Taylor ORSA for - the Dummies heart of Solvency II Institute of Risk Management Solvency II Group April 17th 2012 Peter

ORSA for Dummies Institute of Risk Management Solvency II Group April 17th 2012 Peter Taylor ORSA for - the Dummies heart of Solvency II Institute of Risk Management Solvency II Group April 17th 2012 Peter

EIOPA-CP-11/008 7 November 2011. Consultation Paper On the Proposal for Guidelines on Own Risk and Solvency Assessment

EIOPA-CP-11/008 7 November 2011 Consultation Paper On the Proposal for Guidelines on Own Risk and Solvency Assessment EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20;

EIOPA-CP-11/008 7 November 2011 Consultation Paper On the Proposal for Guidelines on Own Risk and Solvency Assessment EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20;

Solvency II. Impacts on asset managers and servicers. Financial Services Asset Management. www.pwc.com/it

Financial Services Asset Management Solvency II Impacts on asset managers and servicers The Omnibus II proposal will amend the Solvency II Directive voted in 2009. It would probably defer full Solvency

Financial Services Asset Management Solvency II Impacts on asset managers and servicers The Omnibus II proposal will amend the Solvency II Directive voted in 2009. It would probably defer full Solvency

The package of measures to avoid artificial volatility and pro-cyclicality

The package of measures to avoid artificial volatility and pro-cyclicality Explanation of the measures and the need to include them in the Solvency II framework Contents 1. Key messages 2. Why the package

The package of measures to avoid artificial volatility and pro-cyclicality Explanation of the measures and the need to include them in the Solvency II framework Contents 1. Key messages 2. Why the package