Financial Statements of Electricity Companies

|

|

|

- Briana Perkins

- 8 years ago

- Views:

Transcription

1 7 Financial Statements of Electricity Companies Unit 1: Relevant Legal and Administrative Provisions Learning Objectives After studying this unit, you will be able to: Know the legal framework applicable for electricity companies. Understand the composition and purposes of various statutory authorities. Know the Regulations applicable for electricity companies. Understand the policies applicable to the Power Sector. Understand how accounting is done in electricity companies 1.1 Introduction The electricity industry in India was guided by the Indian Electricity Act, 1910 and the Electricity (Supply) Act, The Indian Electricity Act, 1910 introduced a licensing system for the electricity industry and the Electricity (Supply) Act, 1948 introduced greater state involvement in the industry, facilitating regional coordination through state-owned, vertically integrated units called State Electricity Boards (SEBs) to develop a Grid System. The SEBs were responsible for generation, transmission and distribution of electricity within each state of the Indian Union. In the early 1990s, the power sector was liberalised by permitting private participation in the generation and transmission sectors and establishing regional load dispatch centres (RLDCs). In 1998, the Electricity Regulatory Commissions Act, 1998 (the ERC Act) established independent electricity regulatory commissions (ERC) at the central and state levels, with the objective of rationalising the electricity tariff regime and promoting and regulating the electricity industry. The ERC Act, which has been replaced by the Electricity Act, 2003 provided for the formation of state electricity regulatory commissions (SERCs) in the respective states for the rationalisation of energy tariffs.

Act, 1948.")

2 Financial Statements of Electricity Companies Historical Background of Legislative Initiatives The Indian Electricity Act, 1910 provided basic framework for electric supply industry in India. It made provisions for growth of the sector through licensees. The Act covered the provisions for licence by State Government, provision for licence for supply of electricity in a specified area, legal framework for lying down of wires and other works, provisions laying down relationship between licensee and consumer. The Electricity (Supply) Act, 1948 mandated creation of State Electricity Boards (SEBs) and need for the State to step in (through SEBs) to extend electrification (so far limited to cities) across the country. Later on this Act was amended to enable generation in Central sector and to bring in commercial viability in the functioning of SEBs -- especially section 59 was amended to make the earning of a minimum return of 3% on fixed assets a statutory requirement (w.e.f ). Further amendment was made in 1991 to open generation to private sector and establishment of RLDCs and another amendment in 1998 was made to provide for private sector participation in transmission, and also provision relating to Transmission Utilities. The Electricity Regulatory Commission Act, 1998 lays down the provision for setting up of Central / State Electricity Regulatory Commission with powers to determine tariffs. Further, it emphasized on the constitution of SERC optional for States and distancing of Government from tariff determination. 1.2 Electricity Act, 2003 The Electricity Act, 2003 (the Electricity Act) is a central legislation relating to generation, transmission, distribution, trading and use of electricity, that seeks to replace the multiple legislations that governs the Indian power sector. The most significant reform initiative under the Electricity Act was the move towards a multi-buyer, multi-seller system as opposed to the existing structure which permitted only a single buyer to purchase power from power generators. In addition, the Electricity Act grants the ERCs freedom in determining tariffs, without being constrained by rate-of-return regulations. Under the Electricity Act, no licence is required for generation of electricity if the generating station complies with the technical standards relating to connectivity with the grid. The Electricity Act was amended in 2007 to exempt captive power generation plants from licensing requirements for supply to any licensee or consumer. The Electricity Act was amended in 2010 by notification dated 3 March 2010 to provide that any developer of a special economic zone notified under the Special Economic Zones Act, 2005 shall be deemed to be a licensee under the Electricity Act Objectives The objectives of the Act are "to consolidate the laws relating to generation, transmission, distribution, trading and use of electricity and generally for taking measures conducive to development of electricity industry, promoting competition therein, protecting interest of consumers and supply of electricity to all areas, rationalization of electricity tariff, ensuring transparent policies regarding subsidies, promotion of efficient and environmentally benign

3 7.3 Advanced Accounting policies, constitution of Central Electricity Authority, Regulatory Commissions and establishment of Appellate Tribunal and for matters connected therewith or incidental thereto. The Electricity Act 2003 provides electricity market for private investments for increasing generation capacity and efficient network use in India. It encourages captive generation, nondiscriminatory open access to transmission and distribution system and de-licensing generation Under the Electricity Act 2003, activities like generation, transmission and distribution have been separately identified. Now, no person shall (a) transmit electricity; or (b) distribute electricity; or (c) undertake trading in electricity, unless he is authorised to do so by a license issued under section 14, or is exempt under section Licensing The Electricity Act stipulates that no person can transmit, distribute or undertake trading in electricity, unless he is authorised to do so by a licence issued under, or is exempt under, the Electricity Act. The Electricity Act provides for transmission licensees, distribution licensees and licensees for electricity trading. There can be a private distribution licensee as well Generation As per sec 2(29), "generate" means to produce electricity from a generating station for the purpose of giving supply to any premises or enabling a supply to be so given. Currently, any electricity generating company can establish, operate and maintain a generating station if it complies with the technical standards relating to connectivity with grid. Approvals from the Government, the state government and the techno-economic clearance from the Central Electricity Authority (CEA) are no longer required, except for hydroelectric projects. Generating companies are now permitted to sell electricity to any licensees and where permitted by State Electricity Regulatory Commissions (SERCs), to consumers. In addition, no restriction is placed on the setting up of captive power plants by any consumer or group of consumers for their own consumption. Under the Electricity Act, no surcharge is required to be paid on wheeling of power from the captive plant to the destination of the use by its owner. This provides financial incentive to large consumers to set up their own captive plants. Through an amendment in 2007, Section 9 was amended to state that no separate licence is required for the supply of electricity generated from the captive power plant to any licensee or the consumer. The ERCs determine the tariff for the supply of electricity from a generating company to any distribution licensee, transmission of electricity, wheeling of electricity and retail of electricity. The Central Electricity Regulatory Commission (CERC) has jurisdiction over generating companies owned or controlled by the Government and those generating companies who have entered into or otherwise have a composite scheme for generation and sale in more than one state. SERCs have jurisdiction over generating stations within the state boundaries, except those under the CERC s jurisdiction.

4 Financial Statements of Electricity Companies Transmission Transmission being a regulated activity involves the intervention of various players. The Government is responsible for facilitating the transmission and supply of electricity, particularly inter-state, regional and inter-regional transmission. The Electricity Act vests the responsibility of efficient, economical and integrated transmission and supply of electricity with the Government and empowers it to make regional demarcations of the country for the same. In addition, the Government will facilitate voluntary inter-connections and coordination of facilities for the inter-state, regional and inter-regional generation and transmission of electricity. The CEA is required to prescribe certain grid standards under the Electricity Act and every transmission licensee must comply with such technical standards of operation and maintenance of transmission lines. In addition, every transmission licensee is required to obtain a licence from the CERC and the SERCs, as the case may be. The Electricity Act requires the Government to designate one government company as the central transmission utility (CTU), which would be deemed as a transmission licensee. Similarly, each state government is required to designate one government company as state transmission utility (STU), which would also be deemed as a transmission licensee. The CTU and STUs are responsible for transmission of electricity, planning and co-ordination of the transmission system, providing non-discriminatory open access to any users and developing a coordinated, efficient and integrated inter-state and intra-state transmission system respectively. The Electricity Act prohibits the CTU and STUs from engaging in the business of generation or trading in electricity. Under the Electricity Act, a transmission licensee may with prior intimation to the appropriate ERC engage in any business for the optimum utilisation of its assets. Under the Electricity Act, the Government was empowered to establish the national load despatch centre (NLDC) and regional load despatch centre RLDCs for optimum scheduling and despatch of electricity among the RLDCs. The RLDCs are responsible for (a) optimum scheduling and despatch of electricity within the region, in accordance with the contracts entered into with the licensees or the generating companies operating in the region; (b) monitoring grid operations; (c) keeping accounts of the quantity of electricity transmitted through the regional grid; (d) exercising supervision and control over the inter-state transmission system; and (e) carrying out real time operations for grid control and despatch of electricity within the region through secure and economic operation of the regional grid in accordance with the grid standards and grid code. The transmission licensee is required to comply with the technical standards of operation and maintenance of transmission lines specified by the CEA. The Electricity Act allows IPPs open access to transmission lines. The provision of open access is subject to the availability of adequate transmission capacity as determined by the CTU or STU. The Electricity Act also

5 7.5 Advanced Accounting lays down provisions for intra-state transmission, where the state commission facilitates and promotes transmission, wheeling and inter-connection arrangements within its territorial jurisdiction for the transmission and supply of electricity by economical and efficient utilisation of the electricity Trading The Electricity Act specifies trading in electricity as a licensed activity. Trading has been defined as the purchase of electricity for resale. This may involve wholesale supply (i.e. purchasing power from the generators and selling to the distribution licensees) or retail supply (i.e. purchasing from generators or distribution licensees for sale to end consumers). The licence to engage in electricity trading is required to be obtained from the appropriate ERC. The CERC, by notification dated 16 February 2009, issued the CERC (Procedure, Terms and Conditions for Grant of Trading License and Other Related Matters) Regulations, 2009 (the Trading Licence Regulations) to regulate the inter-state trading of electricity. The Trading Licence Regulations define inter-state trading as transfer of electricity from the territory of one state for resale to the territory of another state and includes electricity imported from any other country for resale in any state of India. Under the Trading Licence Regulations, any person desirous of undertaking inter-state trading in electricity shall apply to the CERC for the grant of a licence. The Trading Licence Regulations set out various qualifications for the grant of a licence for undertaking electricity trading, including certain technical and professional qualifications, and net worth requirements. An applicant is required to publish notice of his application in daily newspapers to receive objections, if any, to be filed before the CERC. Further, a licensee is subject to certain conditions including the extent of trading margin, maintenance of records and submission of auditors report. The existing licensees are required to meet the net worth, current ratio and liquidity ratio criteria and are required to pay the licence fee as specified by the CERC, from time to time. The eligibility criteria include norms relating to capital adequacy and technical parameters. However, the NLDC and RLDCs, CTUs, STUs and other transmission licensees are not allowed to trade in power, to prevent unfair competition. The relevant ERCs also have the right to fix a ceiling on trading margins in intra-state trading. The CERC has issued a draft amendment to the Trading Licence Regulations dated 7 May 2012 and entitled CERC (procedure, terms and conditions for grant of trading licence and other related matters) (First Amendment) Regulations, 2012 (the Draft TL Amendment Regulations) under which the number categories of trading licenses have been increased from three to four categories and the traders are additionally required to furnish information relating to the volume of electricity proposed to be traded during fiscal 2013 supported by special balance sheets so that the trader s risk may be viewed by the CERC in a more holistic manner. The Draft TL Amendment Regulations will also introduce a code of conduct for the trading licensees to encourage fair and transparent trading practices.

. The licence to engage in electricity trading is required to be obtained from the appropriate ERC.")

6 Financial Statements of Electricity Companies Distribution and Retail Supply The Electricity Act does not make any distinction between distribution and retail supply of electricity. Distribution is a licensed activity and distribution licensees are allowed to undertake trading without any separate licence. Under the Electricity Act, no licence is required for the purposes of the supply of electricity. Thus, a distribution licensee can undertake three activities: trading, distribution and supply, through one licence. The distribution licensee with prior permission of the appropriate commission may engage itself in any other activities for optimal utilisation of its assets Unregulated Rural Markets The licensing requirement does not apply in cases where a person intends to generate and distribute electricity in rural areas as notified by a state government. However, the supplier is required to comply with the requirements specified by the CEA such as protecting the public from dangers involved, eliminating or reducing the risks of injury and providing notifications of accidents and failures of transmission and supplies of electricity. It shall also be required to comply with system specifications for supply and transmission of electricity. The Electricity Act mandates formulation of national policies governing rural electrification and local distribution and rural off-grid supply including those based on renewable and other non-conventional energy sources. This policy initiative is expected to give impetus to rural electrification and also conceptualise rural power as a business opportunity. 1.3 Tariff Principles The Electricity Act, 2003 has introduced significant changes in terms of tariff principles applicable to the electricity industry. Under the Electricity Act, the appropriate ERCs are empowered to determine the tariff for: Supply of electricity by a generating company to a distribution licensee, provided that the appropriate commission may, in case of a shortage of supply of electricity, fix the minimum and maximum ceiling of tariff for sale or purchase of electricity in pursuance of an agreement, entered into between a generating company and a licensee or between licensees, for a period not exceeding one year to ensure reasonable prices of electricity; Transmission of electricity; Wheeling of electricity; and Retail of electricity, provided that in case of distribution of electricity in the same area by two or more distribution licensees, the appropriate commission may, for promoting competition among distribution licensees, fix only the maximum ceiling of tariff for retail of electricity. The appropriate ERC is required to be guided by the following while determining tariff: The principles and methodologies specified by the CERC for the determination of the tariff applicable to generating companies and licensees;

7 7.7 Advanced Accounting That the generation, transmission, distribution and supply of electricity are conducted on commercial principles; The factors which would encourage competition, efficiency, economical use of the resources, good performance and optimum investments; Safeguarding consumers interest and also ensure recovery of the cost of electricity in a reasonable manner; The principles rewarding efficiency in performance; Multi-year tariff principles; That the tariff progressively reflects the cost of supply of electricity, at an adequate and improving level of efficiency; That the tariff progressively reduces and eliminates cross-subsidies in the manner to be specified by the CERC; The promotion of co-generation and generation of electricity from renewable sources of energy; and The NEP and the Tariff Policy. The Electricity Act provides that the ERC shall adopt such tariff that has been determined through a transparent process of bidding in accordance with the guidelines issued by the Government. The MoP has issued detailed guidelines for competitive bidding as well as standard bidding documents for competitive bid projects. The determination of tariff for a particular power project would depend on the mode of participation in the project. Broadly, the tariffs can be determined in two ways: (i) based on the tariff principles prescribed by the CERC (cost plus basis consisting of a capacity charge, an energy charge, an unscheduled interchange charge and incentive payments); or (ii) competitive bidding route where the tariff is purely market based. 1.4 CERC (Terms and Conditions of Tariff) Regulations, 2009 The CERC (Terms and Conditions of Tariff) Regulations, 2009 (the CERC Tariff Regulations) apply where the tariff for a generating station or a unit (other than those based on nonconventional energy sources) and the transmission system is yet to be determined by the CERC. Tariff for the supply of electricity from a thermal generating station shall comprise two parts, namely, capacity charge (for recovery of annual fixed cost) and energy charge (for recovery of primary fuel cost and limestone cost (where applicable). Tariff for the supply of electricity from a hydro generating station shall comprise capacity charge and energy charge, for recovery of annual fixed cost through the two charges. Tariff for transmission of electricity on the inter-state transmission system shall comprise transmission charge for recovery of annual fixed cost.

8 Financial Statements of Electricity Companies 7.8 Tariff in respect of a generating station may be determined for the whole generating station or a stage, unit or block of the generating station, and tariff for the transmission system may be determined for the whole of the transmission system or the transmission line or sub-station. For determination of tariff, the capital cost of the project may be broken into stages and distinct units or blocks, transmission lines and sub-systems forming part of the project, if required, provided that where break-up of the capital cost of the project for different stages, units or blocks and transmission lines or sub-stations is not available and in case of on-going projects, the common facilities shall be apportioned on the basis of the installed capacity of the units, line length and number of bays and that in relation to multi-purpose hydro schemes with irrigation, flood control and power components, the capital cost chargeable to the power component of the scheme only shall be considered for determination of tariff. The generating company or the transmission licensee, as the case may be, may apply for determination of tariff in respect of units of the generating station or the transmission lines or sub-stations of the transmission system, completed or projected to be completed within six months from the date of the application. In the case of existing projects, the generating company or the transmission licensee, as the case may be, shall continue to provisionally bill the beneficiaries or the long-term customers with the tariff approved by the CERC and applicable as on 31 March 2009 for the period starting from 1 April, 2009 until approval of tariff by the CERC in accordance with the CERC Tariff Regulations. The CERC (Terms and Conditions of Tariff) (Second Amendment) Regulations, 2011 specify that, where the tariff provisionally billed exceeds or falls short of the final tariff approved by the CERC under the CERC Tariff Regulations, the generating company, or the transmission licensee, shall refund to (or recover from) the beneficiaries or the transmission customers within six months, together with simple interest, at the State Bank of India base rate during the previous year plus 350 basis points (for the years 2012 to 2013 and 2013 to 2014) for the period from the date of provisional billing to the date of issue of the final tariff order of the CERC monthly average. Where an application for the determination of the tariff of an existing or a new project has been filed before the CERC in accordance with clauses (1) and (2) of the CERC Tariff Regulations, the CERC may consider in its discretion to grant a provisional tariff of up to 95.0 per cent. of the annual fixed cost of the project claimed in the application, subject to adjustment as per the proviso to clause (3) of the CERC Tariff Regulations after the final tariff order has been issued, provided that the recovery of capacity charge and energy charge or transmission charge, as the case may be, in respect of the existing or new project for which provisional tariff has been granted, shall be made in accordance with the relevant provisions of the CERC Tariff Regulations.

9 7.9 Advanced Accounting Learning Objectives Unit 2 : Preparation of Financial Statements After studying this unit, you will be able to: Understand relevant transaction of an electricity company such as security deposit, capital service line contribution, Accelerated Power Development and Reforms Program loan and grant and depreciation. Understand Reporting of financial statements of Electricity Company as per Schedule VI. Understand method of depreciation for replacement of asset i.e. the optimised depreciated replacement cost [ODRC] method. 2.1 Formats of Financial Statements Section 616 of the Companies Act, 1956 provides that the provisions of the Companies Act, 1956 shall not apply to companies engaged tn generation or supply of electricity except in so far as the said provisions are inconsistent with the provisions of the Indian Electricity Act 1910 or the Electricity (Supply) Act, The Indian Electricity Act 1910 or the Electricity (Supply) Act, 1948 have been repealed and Electricity Act, 2003 has been enacted in their place. Accordingly in section 616 of the Companies Act instead of the Indian Electricity Act 1910 or the Electricity (Supply) Act, 1948, the Electricity Act, 2003 can be read. Therefore it is clear that for the companies in the business of generation or supply of electricity, provisions of Companies Act, 1956 shall apply except in so far as the said provisions are inconsistent with the provisions of the Electricity Act, Electricity Act, 2003 does not prescribe any formats of financial statements to be followed by the electricity companies. Whereas, the Companies Act, 1956 provides that every company shall prepare its financial statements as per the Schedule VI to the Companies Act, Therefore, the electricity companies shall be required to prepare their accounts as per the Schedule VI to the Companies Act, Specific Transactions of Electricity Supply Company Security Deposit As provided in section 47 of the Act, the Distribution Licensee may require from any person, who requires a supply of electricity to his premises in pursuance of section 43 of the Act, to deposit sufficient security against the estimated payment which may become due to him - (1) In respect of electricity supplied to such person (including Energy Charges, Fixed / Demand Charges, Fuel Price and Power Purchase Adjustment (FPPPA) charges, Electricity Duty and any other charges as may be levied from time to time), or

![Understand Reporting of financial statements of Electricity Company as per Schedule VI. Understand method of depreciation for replacement of asset i.e. the optimised depreciated replacement cost [ODRC] method.](/docs-images/41/1485439/images/page_9.jpg "2.1 Formats of Financial Statements Section 616 of the Companies Act, 1956 provides that the provisions of the Companies Act, 1956 shall not apply to companies engaged tn generation or supply of")

10 Financial Statements of Electricity Companies 7.10 (2) Where any electric line or electric plant or electric meter is to be provided for supplying electricity to such person, in respect of the provision of such line or plant or meter. (3) The distribution licensee shall pay interest equivalent to the bank rate or more, as may be specified by the concerned State Commission, on the security referred to in sub-section (1) and refund such security on the request of the person who gave such security. (4) A distribution licensee shall not be entitled to require security in pursuance of clause (a) of sub-section (1) if the person requiring the supply is prepared to take the supply through a pre-payment meter. Interest on Security Deposit The Licensee shall pay interest to the consumer at the Reserve Bank of India bank rate prevailing on the I s1 of April for the year, payable annually on the consumer's security deposit with effect from date of such deposit in case of new connections energized after the date of this notification, or in other cases, from the date of notification of this Code. The interest accrued during the year shall be adjusted in the consumer's bill for the first quarter of the ensuing financial year. Accounting and Reporting of Security Deposit Journal Entry Amount to be debited / credited When security deposit is received 1. For amount received Bank A/c Dr. Actual amount received To Security Deposit A/c Note: Balance of Security Deposit A/c at the end of the accounting period should be disclosed as Non-current liability in the Balance Sheet since the same is, in substance, not repayable within a period of 12 months from the reporting date and hence does not satisfy any of the conditions for classifying a liability as current Journal Entry Amount to be debited / credited (a) Interest accrued on security deposit at the end of the accounting period 2. Interest on security deposit at bank rate or more, as may be specified by the concerned State Commission Interest Expense A/c Dr. To Interest Accrued on Security Deposit A/c Note: Balance of Interest Accrued on Security Deposit A/c at the end of the accounting period should be disclosed as Non-current liability in the Balance Sheet since the same is, in substance, not repayable within a period of 12 months from the reporting date and hence does not satisfy any of the conditions for classifying a liability as current

11 7.11 Advanced Accounting Journal Entry Amount to be debited / credited (b) Adjustment of accrued Interest on security deposit in the consumer's bill 3. The interest accrued during the year shall be adjusted in the consumer's bill for the first quarter of the ensuing financial year Interest Accrued on Security Deposit A/c To Sales Turnover Advance against Depreciation (AAD) Advance against depreciation (AAD) was an element of tariff provided under the Tariff Regulations for and to facilitate debt servicing by the generators since it was considered that depreciation recovered in the tariff considering a useful life of 25 years is not adequate for debt servicing. Though this amount is not repayable to the customers by the electricity companies, keeping in view the matching principle, and in line with the opinion of the Expert Advisory Committee (EAC) of the Institute of Chartered Accountants of India (ICAI), this is to be treated as deferred revenue to the extent depreciation chargeable in the accounts is considered to be higher than the depreciation recoverable in tariff in future years Accounting for Exchange Rate Variations on the Foreign Currency Borrowings Foreign exchange rate variation (FERV) on foreign currency loans and interest thereon is recoverable from/payable to the customers on actual payment in line with the Tariff Regulations. Keeping in view the opinion of the EAC of ICAI, the deferred foreign currency fluctuation asset is to be recognised by corresponding credit to deferred income from foreign currency fluctuation in respect of the FERV on foreign currency loans or interest thereon adjusted in the cost of fixed assets, which is recoverable from the customers in future years on actual repayment. This amount will be recognized as revenue corresponding to the depreciation charge in future years Assets under 5 KM scheme of the Government of India Ministry of Power has launched a scheme for electrification of villages within 5 km periphery of generation plants of Central Public Sector Undertakings (CPSUs) for providing reliable and quality power to the project affected people. The scheme provides free electricity connections to below poverty line (BPL) households. The scheme will cover all existing and upcoming power plants of CPSUs. The cost of the scheme will be borne by the CPSU to which the plant belongs. This cost will be booked by the CPSU under the project cost and will be considered by the CERC for determination of tariff Capital Service Line Contributions Different State Commissions prescribes such Service line cum Development (SLD) Charges norms as per section 47 of the Act. Norms of Delhi Electricity Supply Code Regulations, 2012 Chapter IV are given below for reference: Dr.

12 Financial Statements of Electricity Companies 7.12 Service line cum Development (SLD) Charges: ln case the area/colony is electrified by the Licensee, the SLD charges shall be payable by all consumers irrespective of whether it is electrified or un-electrified area. SLD charges, as given in Table-4, shall be leviable. Service Line cum Development Charge S.No. Sanctioned Load (kw) Amount (`) 1 Upto 5 3,000 2 More than 5 upto 10 7,000 3 More than 10 upto 20 11,000 4 More than 20 upto 50 16,000 5 More than 50 upto ,000 6 More than 100 kw (at 11 kv) 50% of the cost of HT cables/line/switchgear Accounting for this source of funds of Electricity Company requires special attention as the following different accounting and reporting practices are noticed in published Financial Statements of some companies. 1. Amount received from consumer towards capital/service line contributions is accounted as liability and subsequently recognized as income over the life of the asset; 2. Amount received from consumer towards capital / service line contributions is accounted as reserves as the amount is not refundable and reported under the head reserves and surplus without transferring any proportionate amount to the income statement over the life of asset; 3. Amount received from consumer towards capital / service line contributions is accounted as capital reserve as the amount is not refundable and subsequently proportionate amount is transferred to income statement during the expected life of the asset to match against depreciation on total cost of such asset; 4. Amount received from consumer towards capital/service line contributions is accounted as reduction in the cost of non-current asset and depreciation may be provided on such reduced cost. Accounting entry for the 3 rd option is as follows Journal Entry Amount to be debited / credited (c) When amount received from consumers towards capital / service line contributions 4. For amount received Bank A/c Dr. To Capital / service line contributions A/c Actual amount received

Amount (`) 1 Upto 5 3,000 2 More than 5 upto 10 7,000 3 More than 10 upto 20 11,000 4 More than 20 upto 50 16,000 5 More than 50 upto 100 31,000 6 More than 100 kw (at 11 kv) 50%")

13 7.13 Advanced Accounting Note: Balance of capital / service line contributions A/c at the end of the accounting period should be disclosed under Capital Reserve under Reserves and Surplus as in substance it is not redeemable to consumers. Journal Entry Amount to be debited / credited (d) When proportionate amount is transferred to income statement during the expected life of the asset from capital / service line contributions A/c 5. For amount received Capital / service line contributions A/c To Profit and Loss A/c Dr. Note: Balance of capital / service line contributions A/c at the end of the accounting period should be disclosed as Capital Reserve under Reserves and Surplus wherein this transfer is shown as deduction. The amount transferred matches proportionately against depreciation charged on total cost of such asset in the Statement of Profit and Loss. Return on equity shall be computed in rupee terms, on the equity base determined in accordance with regulation 12. Equity Base should not include the amount contributed by the consumers towards such capital investment. Consumer contribution for such capital investment is not brought out in the ARR. 2.3 Implementation of Accelerated Power Development and Reforms Program (APDRP) Government identified need for electricity distribution reforms in light of existing poor distribution network, huge transmission and distribution losses due to un-metered supply and theft, high LT/HT line ratio, overloaded DT/lines etc. For this Government introduced Accelerated Power Development Program (APDP) in February, The main objective of this program was to initiate a financial turnaround in the performance of the state owned power sector. Two years of working experience of APDP showed that it had several limitations. Therefore, in the Union Budget APDP was re-christened as Accelerated Power Development and Reforms Program (APDRP) with the stipulation that access of the States to the fund will be on the basis of agreed reform programmes the center piece of which would be narrowing and ultimate elimination of the gap between unit cost of supply and revenue realization within a specific time frame Objectives of APDRP APDRP has now been given much wider scope than APDP. It aims at strengthening and upgradation of the Sub-Transmission, and Distribution system in the country with the following objectives:

14 Financial Statements of Electricity Companies 7.14 i. Reducing Aggregate Technical and Commercial (AT&C) losses; ii. Improving quality of supply of power; iii. Increasing revenue collection; and iv. Improving consumer satisfaction. Union Government provide funds under the programme as additional central assistance over and above the normal Central Plan Allocation to those States who commit to a time bound programme of reforms as elaborated in the Memorandum of Understanding (MoU) and Memorandum of Agreement (MoA). The funds under the programme are provided under two components: i Investment component- Assistance for strengthening and upgradation of sub-transmission and distribution system. Focus is on high density urban areas to achieve quick result as losses in absolute term are very high in such areas. ii. Incentive component It is a grant for States/Utilities to encourage them to reduce their cash losses on yearly basis. Investment component Funds are provided through a combination of grant and loan. For this purpose States have been categorized as Special Category States and Non-Special Category States. 100% of the project cost in special category States (all North Eastern States, Sikkim, Uttaranchal, Himachal Pradesh and Jammu & Kashmir) in the ratio of 90% grant and 10% soft loan is financed. In respect of other States (Non-special category) Union Government finance 50% of the project cost and the ratio of grant and loan is 1:1. SEBs and Utilities have to arrange remaining 50% of the fund from Power Finance Corporation (PFC) and Rural Electrification Corporation (REC) or other financial institutions or from their own resources as counter-part funds. Incentive component: - This component has been introduced to motivate SEBs/Utilities to reduce their cash losses. State Governments are incentivised upto 50% of the actual cash loss reduction by SEBs/ Utilities as grant. The year is the base year for the calculation of loss reduction, in subsequent years. The losses are calculated net of subsidy and receivable. Funds under incentive components are provided as 100% grant to all the States (special category and nonspecial category) as Additional Plan Assistance. The following table will make the funding modalities more clear: S.No. Category of States % of Projects / Scheme Cost from APDRP as Grant Loan % of Projects Scheme Cost from PFC/REC/ Own/ Other Sources 1 Special Category States Non-special category States

and Memorandum of Agreement (MoA).")

15 7.15 Advanced Accounting Funding Pattern Funds under the Accelerated Power Development Reforms Programme (APDRP) are released to the State Government as below: i. Non-special category States: a. 25 percent of the APDRP amount after approval of project under APDRP and on tie up of counterpart funds from financial institutions and release of matching fund by financial institutions (FIs) b. On utilization of the 25 percent of sanctioned project cost, 50 percent of the APDRP amount is released. c. On utilization of 75 percent of the sanctioned project cost, balance 25 percent is released ii. Special Category States: (namely all North-Eastern States, Sikkim, Uttaranchal, Himachal Pradesh and Jammu & Kashmir): a. 25 percent of the APDRP amount after approval of project b. On utilization of 25 percent of the project cost, 50 percent of the APDRP amount is released c. On utilization of 75 percent of the project cost, balance 25 percent of the APDRP amount is released Accounting of Grant received under APDRP Grant received under the Accelerated Power Development and Reforms Programme (APDRP) of the Ministry of Power, Government of India towards capital expenditure, is treated as capital receipt and accounted as Capital Reserve and subsequently adjusted as income (by transfer to the Statement of Profit and Loss) in the same proportion as the depreciation written off on the assets acquired out of the grant. The depreciation for the year debited to the statement of Profit and Loss on asset acquired out of grant match against portion of grant transferred from Capital Reserve. The unadjusted balance of capital reserve is disclosed under Reserves and Surplus in balance sheet. In the Cash Flow Statement grant received under APDRP is reported under Financing Activity. At any time if the ownership of the assets acquired, out of the grants, vest with the Government, the grants (capital reserve) are adjusted in the carrying cost of such assets. The grant-in-aid assistance received by the utility under APDRP and its utilisation shown under the head capital expenditure made during the year is not considered for calculation of Annual Revenue Requirement (ARR) of the utility for the year. 2.4 Depreciation Depreciation requires special consideration for an electricity company for following reasons: 1. As already discussed, for the companies in the business of generation or supply of electricity, provisions of Companies Act, 1956 shall apply except in so far as the said provisions are inconsistent with the provisions of the Electricity Act, 2003.

: a. 25 percent of the APDRP amount after approval of project b.")

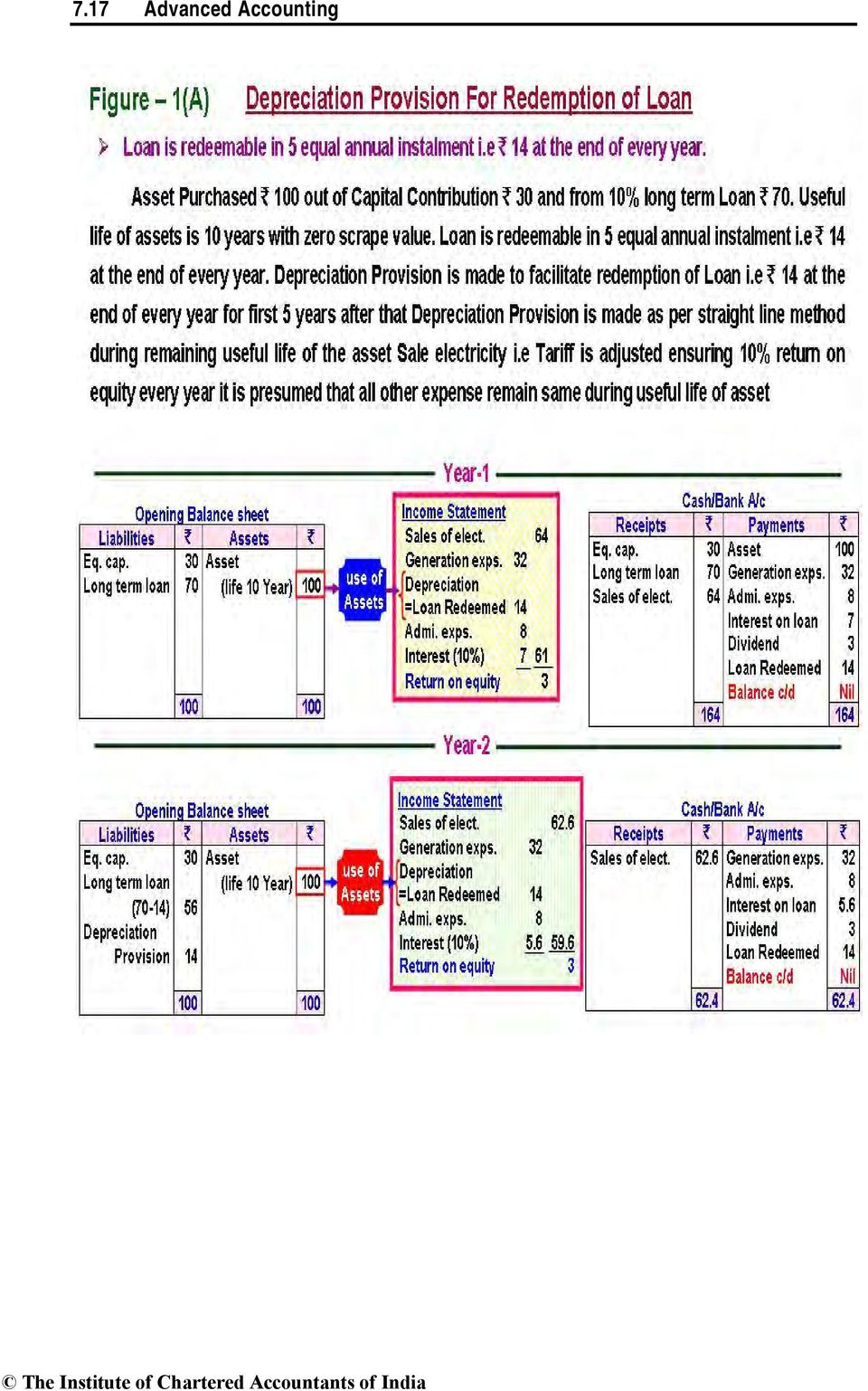

16 Financial Statements of Electricity Companies The rates of depreciation has been prescribed by the Central Electricity Regulatory Commission (CERC) under the tariff regulations, 2009 which has been notified under the powers given under the Electricity Act, The rates of depreciation as prescribed by CERC for the purpose of tariff are different from those prescribed under Schedule XIV to the Companies Act, 1956; 4. As per 2004 Regulations, the Central Electricity Regulatory Commission has observed that different rates of depreciation are already being allowed for the purpose of accounts and income-tax. This being so, following different depreciation rates for the purpose of tariff was considered fully justified. 5. As per 2009 Regulations, it has been stated in the Tariff Policy that the depreciation rates for the assets shall be specified by the Central Electricity Regulatory Commission and this rate of depreciation shall be applicable for the purpose of tariff as well as accounting. 6. The Office of the Comptroller & Auditor General of India has expressed an opinion that power sector companies shall be governed by the rates of depreciation notified by the CERC for providing depreciation in respect of generating assets in the accounts instead of the rates as per the Companies Act, Accordingly, a Company should revise its accounting policies relating to charging of depreciation w.e.f. 1 st April 2009 considering the rates and methodology notified by the CERC for determination of tariff through Regulations, 2009 (Ref. 35 th Annual Report for FY of NTPC Ltd page 59) Purpose of Depreciation For the treatment of depreciation, three views are generally expressed The first is that it represents a cash flow for repayment of loan; The second is that it represents a return of capital subscribed; and The third is that it represents a replacement of capital or a charge for the replacement of the assets consumed. As per 2004 Regulations, depreciation represents a cash flow for repayment of loan and allowed Advance Against Depreciation. (Explained in following paragraphs). As per 2009 Regulations, depreciation represents a cash flow for repayment of loan not by allowing Advance against Depreciation but by prescribing higher rates of depreciation for initial years of loan redemption explained in following paragraphs Philosophy of depreciation The philosophy of depreciation as adopted by the Commission in the existing norms as result of detailed study, prescribes following two methods of depreciation. (a) The Straight Line method by application of a fixed rate over the fair life of the asset; (b) Optimized Depreciated Replacement Cost (ODRC) based method under which the depreciation could be a method for replacement of the asset.

17 7.17 Advanced Accounting

18 Financial Statements of Electricity Companies 7.18

19 7.19 Advanced Accounting

20 Financial Statements of Electricity Companies 7.20

DRAFT KERALA STATE ELECTRICITY REGULATORY COMMISSION, NOTICE. No. 442/CT/2014/KSERC Dated, Thiruvananthapuram 31 st March, 2015

DRAFT 31.3.2015 KERALA STATE ELECTRICITY REGULATORY COMMISSION, NOTICE 442/CT/2014/KSERC Dated, Thiruvananthapuram 31 st March, 2015 The Kerala State Electricity Regulatory Commission hereby publishes

DRAFT 31.3.2015 KERALA STATE ELECTRICITY REGULATORY COMMISSION, NOTICE 442/CT/2014/KSERC Dated, Thiruvananthapuram 31 st March, 2015 The Kerala State Electricity Regulatory Commission hereby publishes

DELHI ELECTRICITY REGULATORY COMMISSION

DELHI ELECTRICITY REGULATORY COMMISSION DELHI ELECTRICITY REGULATORY COMMISSION (RENEWABLE PURCHASE OBLIGATION AND RENEWABLE ENERGY CERTIFICATE FRAMEWORK IMPLEMENTATION) REGULATIONS, 2011 No. Dated:. NOTIFICATION

DELHI ELECTRICITY REGULATORY COMMISSION DELHI ELECTRICITY REGULATORY COMMISSION (RENEWABLE PURCHASE OBLIGATION AND RENEWABLE ENERGY CERTIFICATE FRAMEWORK IMPLEMENTATION) REGULATIONS, 2011 No. Dated:. NOTIFICATION

Renewable Energy Certificate Mechanism for India. ABPS Infrastructure Advisory. Background

Renewable Energy Certificate Mechanism for India Background ABPS Infrastructure Advisory India is abundantly gifted with a variety of renewable energy (RE) sources. However, not all states are endowed

Renewable Energy Certificate Mechanism for India Background ABPS Infrastructure Advisory India is abundantly gifted with a variety of renewable energy (RE) sources. However, not all states are endowed

National Electricity Policy 03-Feb-2005

National Electricity Policy 03-Feb-2005 Under the provisions of section 3(1) of the Electricity Act, 2003, the Central Government is required to prepare the National Electricity Policy for development

National Electricity Policy 03-Feb-2005 Under the provisions of section 3(1) of the Electricity Act, 2003, the Central Government is required to prepare the National Electricity Policy for development

THE ELECTRICITY ACT, 2003. [No. 36 OF 2003]

![THE ELECTRICITY ACT, 2003. [No. 36 OF 2003]](/thumbs/24/2664732.jpg "THE ELECTRICITY ACT, 2003. [No. 36 OF 2003]") THE ELECTRICITY ACT, 2003 [No. 36 OF 2003] An Act to consolidate the laws relating to generation, transmission, distribution, trading and use of electricity and generally for taking measures conducive

THE ELECTRICITY ACT, 2003 [No. 36 OF 2003] An Act to consolidate the laws relating to generation, transmission, distribution, trading and use of electricity and generally for taking measures conducive

CENTRAL ELECTRICITY REGULATORY COMMISSION NEW DELHI NOTIFICATION. No. L-1/(3)/2009-CERC Dated the 7 th August 2009

/2009-CERC Dated the 7 th August 2009") CENTRAL ELECTRICITY REGULATORY COMMISSION NEW DELHI NOTIFICATION No. L-1/(3)/2009-CERC Dated the 7 th August 2009 In exercise of powers conferred by section 178 of the Electricity Act, 2003 and all other

CENTRAL ELECTRICITY REGULATORY COMMISSION NEW DELHI NOTIFICATION No. L-1/(3)/2009-CERC Dated the 7 th August 2009 In exercise of powers conferred by section 178 of the Electricity Act, 2003 and all other

KERALA STATE ELECTRICITY REGULATORY COMMISSION

KERALA STATE ELECTRICITY REGULATORY COMMISSION Notification No. 2096/KSERC/CT/2014 Dated, Thiruvananthapuram 10 th June 2014. In exercise of the powers conferred under sections 66, 86 (1) (e) and 181 of

KERALA STATE ELECTRICITY REGULATORY COMMISSION Notification No. 2096/KSERC/CT/2014 Dated, Thiruvananthapuram 10 th June 2014. In exercise of the powers conferred under sections 66, 86 (1) (e) and 181 of

Solar Power Policy Uttar Pradesh 2012 Suggestions to be sent to : dirupneda@rediffmail.com ho_nmk@rediffmail.com

Draft ver2 Solar Power Policy Uttar Pradesh 2012 Suggestions to be sent to : dirupneda@rediffmail.com ho_nmk@rediffmail.com 1 TABLE OF CONTENTS S.No Contents Page No 1. PREAMBLE 3 2. OBJECTIVES 3 3. OPERATIVE

Draft ver2 Solar Power Policy Uttar Pradesh 2012 Suggestions to be sent to : dirupneda@rediffmail.com ho_nmk@rediffmail.com 1 TABLE OF CONTENTS S.No Contents Page No 1. PREAMBLE 3 2. OBJECTIVES 3 3. OPERATIVE

MINISTRY OF LAW AND JUSTICE (Legislative Department) New Delhi, the 2 nd June, 2003.Jyaistha 12, 1925 (Saka)

New Delhi, the 2 nd June, 2003.Jyaistha 12, 1925 (Saka)") MINISTRY OF LAW AND JUSTICE (Legislative Department) New Delhi, the 2 nd June, 2003.Jyaistha 12, 1925 (Saka) The following Act of Parliament received the assent of the President on the 26 th May, 2003,

MINISTRY OF LAW AND JUSTICE (Legislative Department) New Delhi, the 2 nd June, 2003.Jyaistha 12, 1925 (Saka) The following Act of Parliament received the assent of the President on the 26 th May, 2003,

Model Renewable Energy Wheeling Agreement under Renewable Energy Certificate (REC) scheme

scheme") Model Renewable Energy Wheeling Agreement under Renewable Energy Certificate (REC) scheme This agreement made at on this day of two thousand between M/s. (Renewable Energy Generator name and address) hereinafter

Model Renewable Energy Wheeling Agreement under Renewable Energy Certificate (REC) scheme This agreement made at on this day of two thousand between M/s. (Renewable Energy Generator name and address) hereinafter

THE ELECTRICITY ACT, 2003. [No. 36 OF 2003]

![THE ELECTRICITY ACT, 2003. [No. 36 OF 2003]](/thumbs/29/13496763.jpg "THE ELECTRICITY ACT, 2003. [No. 36 OF 2003]") THE ELECTRICITY ACT, 2003 [No. 36 OF 2003] An Act to consolidate the laws relating to generation, transmission, distribution, trading and use of electricity and generally for taking measures conducive

THE ELECTRICITY ACT, 2003 [No. 36 OF 2003] An Act to consolidate the laws relating to generation, transmission, distribution, trading and use of electricity and generally for taking measures conducive

Report on Significant Accounting Policies

Report on Significant Accounting Policies After the unbundling from the State Government s Electricity Department, PETCO ( Puducherry Electricity Transmission Company ) and PESCO ( Puducherry Electricity

Report on Significant Accounting Policies After the unbundling from the State Government s Electricity Department, PETCO ( Puducherry Electricity Transmission Company ) and PESCO ( Puducherry Electricity

IREDA-NCEF REFINANCE SCHEME

IREDA-NCEF REFINANCE SCHEME REVIVAL OF THE OPERATIONS OF EXISTING BIOMASS POWER & SMALL HYDRO POWER PROJECTS AFFECTED DUE TO UNFORSEEN CIRCUMSTANCES SUPPORTED BY THE NATIONAL CLEAN ENERGY FUND IREDA NCEF

IREDA-NCEF REFINANCE SCHEME REVIVAL OF THE OPERATIONS OF EXISTING BIOMASS POWER & SMALL HYDRO POWER PROJECTS AFFECTED DUE TO UNFORSEEN CIRCUMSTANCES SUPPORTED BY THE NATIONAL CLEAN ENERGY FUND IREDA NCEF

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

CENTRAL ELECTRICITY REGULATORY COMMISSION NEW DELHI. No. L-1/12/2010-CERC Dated: 14 th January, 2010 NOTIFICATION

CENTRAL ELECTRICITY REGULATORY COMMISSION NEW DELHI No. L-1/12/2010-CERC Dated: 14 th January, 2010 NOTIFICATION In exercise of powers conferred under sub-section (1) of Section 178 and Section 66 read

CENTRAL ELECTRICITY REGULATORY COMMISSION NEW DELHI No. L-1/12/2010-CERC Dated: 14 th January, 2010 NOTIFICATION In exercise of powers conferred under sub-section (1) of Section 178 and Section 66 read

The levy of VAT is administered by the Goa Value Added Tax Act, 2005 and the rules made thereunder.

Frequently Asked Questions 1. What is VAT? VAT is the short form of Value Added Tax. VAT is the tax that has replaced the earlier levy of Sales Tax. Under the earlier first point system of levy of tax,

Frequently Asked Questions 1. What is VAT? VAT is the short form of Value Added Tax. VAT is the tax that has replaced the earlier levy of Sales Tax. Under the earlier first point system of levy of tax,

FIXED CHARGE: This is a cost that goes towards making the service available, including

ELECTRICITY BILL COMPONENTS FIXED CHARGE: This is a cost that goes towards making the service available, including installation and maintenance of poles, power lines and equipment, and 24-hour customer

ELECTRICITY BILL COMPONENTS FIXED CHARGE: This is a cost that goes towards making the service available, including installation and maintenance of poles, power lines and equipment, and 24-hour customer

TARIFF DETERMINATION METHODOLOGY FOR THERMAL POWER PLANT

TARIFF DETERMINATION METHODOLOGY FOR THERMAL POWER PLANT 1. Background The Electricity Act 2003 has empowered the Central Electricity Regulatory Commission (CERC) to specify the terms and conditions for

TARIFF DETERMINATION METHODOLOGY FOR THERMAL POWER PLANT 1. Background The Electricity Act 2003 has empowered the Central Electricity Regulatory Commission (CERC) to specify the terms and conditions for

Analysis of state-wise RPO Regulation across India

The Renewable Purchase Obligations (RPO) has been the major driving force in India to promote the renewable energy sector. But the State Electricity Regulatory Commissions (SERCs) have defined their respective

The Renewable Purchase Obligations (RPO) has been the major driving force in India to promote the renewable energy sector. But the State Electricity Regulatory Commissions (SERCs) have defined their respective

ANDHRA PRADESH ELECTRICITY REGULATORY COMMISSION

ANDHRA PRADESH ELECTRICITY REGULATORY COMMISSION RENEWABLE POWER PURCHASE OBLIGATION (COMPLIANCE BY PURCHASE OF RENEWABLE ENERGY / RENEWABLE ENERGY CERTIFICATES) REGULATIONS, 2012 Regulation No. 1 of 2012

ANDHRA PRADESH ELECTRICITY REGULATORY COMMISSION RENEWABLE POWER PURCHASE OBLIGATION (COMPLIANCE BY PURCHASE OF RENEWABLE ENERGY / RENEWABLE ENERGY CERTIFICATES) REGULATIONS, 2012 Regulation No. 1 of 2012

CHAPTER 13 COMPLIANCE

CHAPTER 13 COMPLIANCE By a Trading Member / Clearing Member 13.1 Annual Accounts and Audit 13.1.1 Every trading member / clearing member shall prepare annual accounts for each financial year ending on

CHAPTER 13 COMPLIANCE By a Trading Member / Clearing Member 13.1 Annual Accounts and Audit 13.1.1 Every trading member / clearing member shall prepare annual accounts for each financial year ending on

Fixed Assets. Name: SudhirJain M. No.: 213157

Fixed Assets Name: SudhirJain M. No.: 213157 Agenda AS- 10 Accounting for Fixed Assets Introduction & Scope Definitions and other relevant provisions Relevant provisions of other Accounting Standards applicable

Fixed Assets Name: SudhirJain M. No.: 213157 Agenda AS- 10 Accounting for Fixed Assets Introduction & Scope Definitions and other relevant provisions Relevant provisions of other Accounting Standards applicable

NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

IREDA-NCEF REFINANCE SCHEME REFINANCE SCHEME FOR PROMOTION OF RENEWABLE ENERGY SUPPORTED BY THE NATIONAL CLEAN ENERGY FUND

IREDA-NCEF REFINANCE SCHEME REFINANCE SCHEME FOR PROMOTION OF RENEWABLE ENERGY SUPPORTED BY THE NATIONAL CLEAN ENERGY FUND IREDA NCEF REFINANCE SCHEME REFINANCE SCHEME FOR PROMOTION OF RENEWABLE ENERGY

IREDA-NCEF REFINANCE SCHEME REFINANCE SCHEME FOR PROMOTION OF RENEWABLE ENERGY SUPPORTED BY THE NATIONAL CLEAN ENERGY FUND IREDA NCEF REFINANCE SCHEME REFINANCE SCHEME FOR PROMOTION OF RENEWABLE ENERGY

KERALA STATE ELECTRICITY REGULATORY COMMISSION THIRUVANANTHAPURAM IN THE MATTER OF

KERALA STATE ELECTRICITY REGULATORY COMMISSION THIRUVANANTHAPURAM PRESENT: Shri. K.J.Mathew, Chairman Shri. C. Abdulla, Member Shri. M.P.Aiyappan, Member Petition No. CT/SOLAR JNNSM/KSERC/2010 August 4,

KERALA STATE ELECTRICITY REGULATORY COMMISSION THIRUVANANTHAPURAM PRESENT: Shri. K.J.Mathew, Chairman Shri. C. Abdulla, Member Shri. M.P.Aiyappan, Member Petition No. CT/SOLAR JNNSM/KSERC/2010 August 4,

Japan. Nagahide Sato and Sadayuki Matsudaira. Nishimura & Asahi

Nagahide Sato and Sadayuki Matsudaira Nishimura & Asahi 1 Policy and law What is the government policy and legislative framework for the electricity sector? The electricity sector in is governed by the

Nagahide Sato and Sadayuki Matsudaira Nishimura & Asahi 1 Policy and law What is the government policy and legislative framework for the electricity sector? The electricity sector in is governed by the

Statement of Cash Flows

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 7 Statement of Cash Flows This version of SB-FRS 7 does not include amendments that are effective for annual periods beginning after 1 January 2014.

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 7 Statement of Cash Flows This version of SB-FRS 7 does not include amendments that are effective for annual periods beginning after 1 January 2014.

Japan. Nagahide Sato and Sadayuki Matsudaira Nishimura & Asahi

Nagahide Sato and Sadayuki Matsudaira Nishimura & Asahi 1 Policy and law What is the government policy and legislative framework for the electricity sector? The electricity sector in is governed by the

Nagahide Sato and Sadayuki Matsudaira Nishimura & Asahi 1 Policy and law What is the government policy and legislative framework for the electricity sector? The electricity sector in is governed by the

PUBLIC FINANCE MANAGEMENT ACT NO. 1 OF 1999

PUBLIC FINANCE MANAGEMENT ACT NO. 1 OF 1999 [ASSENTED TO 2 MARCH, 1999] [DATE OF COMMENCEMENT: 1 APRIL, 2000] (Unless otherwise indicated) (English text signed by the President) NATIONAL TREASURY This

PUBLIC FINANCE MANAGEMENT ACT NO. 1 OF 1999 [ASSENTED TO 2 MARCH, 1999] [DATE OF COMMENCEMENT: 1 APRIL, 2000] (Unless otherwise indicated) (English text signed by the President) NATIONAL TREASURY This

PROCEDURE FOR ISSUANCE OF RENEWABLE ENERGY CERTIFICATE TO THE ELIGIBLE ENTITY BY CENTRAL AGENCY

PROCEDURE FOR ISSUANCE OF RENEWABLE ENERGY CERTIFICATE TO THE ELIGIBLE ENTITY BY CENTRAL AGENCY 1. OBJECTIVE 1.1. This procedure shall provide guidance to the entities to implement Renewable Energy Certificate

PROCEDURE FOR ISSUANCE OF RENEWABLE ENERGY CERTIFICATE TO THE ELIGIBLE ENTITY BY CENTRAL AGENCY 1. OBJECTIVE 1.1. This procedure shall provide guidance to the entities to implement Renewable Energy Certificate

INFORMATION BROCHURE. Refinance Scheme for Scheduled Banks for their lending for Housing, 2003

INFORMATION BROCHURE Refinance Scheme for Scheduled Banks for their lending for Housing, 2003 1. Introduction The objective of the scheme is to provide refinance assistance to Scheduled Banks (SBs) in

INFORMATION BROCHURE Refinance Scheme for Scheduled Banks for their lending for Housing, 2003 1. Introduction The objective of the scheme is to provide refinance assistance to Scheduled Banks (SBs) in

PUBLIC FINANCE MANAGEMENT ACT NO. 1 OF 1999

PUBLIC FINANCE MANAGEMENT ACT NO. 1 OF 1999 as amended by Public Finance Management Amendment Act, No. 29 of 1999 ACT To regulate financial management in the national government and provincial governments;

PUBLIC FINANCE MANAGEMENT ACT NO. 1 OF 1999 as amended by Public Finance Management Amendment Act, No. 29 of 1999 ACT To regulate financial management in the national government and provincial governments;

Consolidated financial statements

Summary of significant accounting policies Basis of preparation DSM s consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted

Summary of significant accounting policies Basis of preparation DSM s consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted

The following Accounting Standards Interpretation (ASI) relates to AS 7. ASI 29 Turnover in case of Contractors

relates to AS 7. ASI 29 Turnover in case of Contractors") 108 Accounting Standard (AS) 7 (revised 2002) Construction Contracts Contents OBJECTIVE SCOPE Paragraph 1 DEFINITIONS 2-5 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 6-9 CONTRACT REVENUE 10-14 CONTRACT

108 Accounting Standard (AS) 7 (revised 2002) Construction Contracts Contents OBJECTIVE SCOPE Paragraph 1 DEFINITIONS 2-5 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 6-9 CONTRACT REVENUE 10-14 CONTRACT

RAJASTHAN ELECTRICITY REGULATORY COMMISSION JAIPUR

RAJASTHAN ELECTRICITY REGULATORY COMMISSION JAIPUR NOTIFICATION 23 rd December, 2010 No.RERC/Secy/Reg. 82 : In exercise of powers conferred under sections 61, 66, 86(1)(e) and 181 of the Electricity Act,

RAJASTHAN ELECTRICITY REGULATORY COMMISSION JAIPUR NOTIFICATION 23 rd December, 2010 No.RERC/Secy/Reg. 82 : In exercise of powers conferred under sections 61, 66, 86(1)(e) and 181 of the Electricity Act,

International Accounting Standard 7 Statement of cash flows *

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

Sri Lanka Accounting Standard-LKAS 7. Statement of Cash Flows

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

DRAFT REGULATIONS FOR ANDHRA PRADESH ELECTRICITY REGULATORY COMMISSION UNDER SECTION 86(1)(e) OF THE ACT NOTIFICATION

(e) OF THE ACT NOTIFICATION") DRAFT REGULATIONS FOR ANDHRA PRADESH ELECTRICITY REGULATORY COMMISSION UNDER SECTION 86(1)(e) OF THE ACT No. Dated: -12-2011 NOTIFICATION In exercise of powers conferred under sections 61, 66, 86(1)(e)

DRAFT REGULATIONS FOR ANDHRA PRADESH ELECTRICITY REGULATORY COMMISSION UNDER SECTION 86(1)(e) OF THE ACT No. Dated: -12-2011 NOTIFICATION In exercise of powers conferred under sections 61, 66, 86(1)(e)

Statement of Cash Flows

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

Renewable Energy. and Renewal Energy Certificates in Indian Context

Renewable Energy and Renewal Energy Certificates in Indian Context With the increasing demand of energy and growing depletion of resources for energy generation, a global movement towards production of

Renewable Energy and Renewal Energy Certificates in Indian Context With the increasing demand of energy and growing depletion of resources for energy generation, a global movement towards production of

Welcome to workshop on revised schedule VI. K. Chandra Sekhar Company Secretary Ace Designers Limited, Bangalore

Welcome to workshop on revised schedule VI K. Chandra Sekhar Company Secretary Ace Designers Limited, Bangalore 1 Relevant provisions Indian Companies Act, 1956 Rules Notifications Circulars Accounting

Welcome to workshop on revised schedule VI K. Chandra Sekhar Company Secretary Ace Designers Limited, Bangalore 1 Relevant provisions Indian Companies Act, 1956 Rules Notifications Circulars Accounting

Companies (Acceptance of Deposits) Rules, 1975

Rules, 1975") Companies (Acceptance of Deposits) Rules, 1975 In exercise of the powers conferred by section 58A, read with section 642 of the Companies Act, 1956(1 of 1956), the Central Government, in consultation with

Companies (Acceptance of Deposits) Rules, 1975 In exercise of the powers conferred by section 58A, read with section 642 of the Companies Act, 1956(1 of 1956), the Central Government, in consultation with

Schedule 22: Significant Accounting Policies

Schedule 22: Significant Accounting Policies 1. Accounting Concepts : - The accounts are prepared on historical cost concept based on accrual method of accounting as going concern, and consistent with

Schedule 22: Significant Accounting Policies 1. Accounting Concepts : - The accounts are prepared on historical cost concept based on accrual method of accounting as going concern, and consistent with

DRAFT MODEL REGULATIONS for STATE ELECTRICITY REGULATORY COMMISSION UNDER SETION 86 (1) (e) OF THE ACT. No. Dated: October, 2009 NOTIFICATION (DRAFT)

(e) OF THE ACT. No. Dated: October, 2009 NOTIFICATION (DRAFT)") DRAFT MODEL REGULATIONS for STATE ELECTRICITY REGULATORY COMMISSION UNDER SETION 86 (1) (e) OF THE ACT No. Dated: October, 2009 NOTIFICATION (DRAFT) In exercise of powers conferred under sections 61, 66,

DRAFT MODEL REGULATIONS for STATE ELECTRICITY REGULATORY COMMISSION UNDER SETION 86 (1) (e) OF THE ACT No. Dated: October, 2009 NOTIFICATION (DRAFT) In exercise of powers conferred under sections 61, 66,

Cash Flow Statements

Compiled Accounting Standard AASB 107 Cash Flow Statements This compiled Standard applies to annual reporting periods beginning on or after 1 July 2007. Early application is permitted. It incorporates

Compiled Accounting Standard AASB 107 Cash Flow Statements This compiled Standard applies to annual reporting periods beginning on or after 1 July 2007. Early application is permitted. It incorporates

Roche Capital Market Ltd Financial Statements 2009

R Roche Capital Market Ltd Financial Statements 2009 1 Roche Capital Market Ltd, Financial Statements Reference numbers indicate corresponding Notes to the Financial Statements. Roche Capital Market Ltd,

R Roche Capital Market Ltd Financial Statements 2009 1 Roche Capital Market Ltd, Financial Statements Reference numbers indicate corresponding Notes to the Financial Statements. Roche Capital Market Ltd,

How To Account For Construction Contracts In Indian Accounting Standard (Indas)

") Contents Indian Accounting Standard (Ind AS) 11 Construction Contracts Paragraphs OBJECTIVE SCOPE 1 2 DEFINITIONS 3 6 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 7 10 CONTRACT REVENUE 11 15 CONTRACT

Contents Indian Accounting Standard (Ind AS) 11 Construction Contracts Paragraphs OBJECTIVE SCOPE 1 2 DEFINITIONS 3 6 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 7 10 CONTRACT REVENUE 11 15 CONTRACT

Standard conditions of the Electricity Distribution Licence

Gas and Electricity Markets Authority ELECTRICITY ACT 1989 Standard conditions of the Electricity Distribution Licence Standard conditions of the Electricity Distribution Licence 30 October 2015 SECTION

Gas and Electricity Markets Authority ELECTRICITY ACT 1989 Standard conditions of the Electricity Distribution Licence Standard conditions of the Electricity Distribution Licence 30 October 2015 SECTION

IGAS 3. Cash Flow Statements. Government Accounting Standards Advisory Board. Contents

Cash Flow Statements Government Accounting Standards Advisory Board Contents Description Page Number 1. Introduction 3 2. Objective 3 3. Scope 3 4. Benefits of Cash Flow Information 4 5. Definitions 4

Cash Flow Statements Government Accounting Standards Advisory Board Contents Description Page Number 1. Introduction 3 2. Objective 3 3. Scope 3 4. Benefits of Cash Flow Information 4 5. Definitions 4

INDEX S. No. PARTICULARS Note:

INDEX S. No. PARTICULARS T1 Profit & Loss Account - Transmission Business T2 Profit & Loss Account - SLDC Business T3 Annual Revenue Requirement - Transmission Business T4 Annual Revenue Requirement -

INDEX S. No. PARTICULARS T1 Profit & Loss Account - Transmission Business T2 Profit & Loss Account - SLDC Business T3 Annual Revenue Requirement - Transmission Business T4 Annual Revenue Requirement -

Preliminary Results for the year ended 31 march 2010

Preliminary Results for the year ended 31 march 2010 Portsmouth Water Limited, a supplier of water to Hampshire and West Sussex, announced its results for the year to 31 March 2010. Highlights During the

Preliminary Results for the year ended 31 march 2010 Portsmouth Water Limited, a supplier of water to Hampshire and West Sussex, announced its results for the year to 31 March 2010. Highlights During the

CHAPTER 16 INVESTMENT ENTITIES

CHAPTER 16 INVESTMENT ENTITIES Introduction 16.1 This Chapter sets out the requirements for the listing of the securities of investment entities, which include investment companies, unit trusts, closed-end

CHAPTER 16 INVESTMENT ENTITIES Introduction 16.1 This Chapter sets out the requirements for the listing of the securities of investment entities, which include investment companies, unit trusts, closed-end

INDIRECT TAXES. Some of the indirect taxes are:

INDIRECT TAXES Indirect Taxes are the charges levied by the State on consumption, expenditure, privilege, or right but not on income or property. Customs duties levied on imports, excise duties on production,

INDIRECT TAXES Indirect Taxes are the charges levied by the State on consumption, expenditure, privilege, or right but not on income or property. Customs duties levied on imports, excise duties on production,

a) Whether there is a need to revisit the existing approach for debt: equity ratio or to continue with the existing composition?

Whether there is a need to revisit the existing approach for debt: equity ratio or to continue with the existing composition?") Summary of the comments and suggestions received on Approach Paper on Terms and Conditions of Tariff Regulations for the tariff period 1.4.2014 to 31.3.2019 ( Ref No. 20/2013/CERC/Fin(Vol-I)/Tariff Reg/CERC

Summary of the comments and suggestions received on Approach Paper on Terms and Conditions of Tariff Regulations for the tariff period 1.4.2014 to 31.3.2019 ( Ref No. 20/2013/CERC/Fin(Vol-I)/Tariff Reg/CERC

Indian Accounting Standard (Ind AS) 12. Income Taxes

12. Income Taxes") Indian Accounting Standard (Ind AS) 12 Contents Income Taxes Paragraphs Objective Scope 1 4 Definitions 5 11 Tax base 7 11 Recognition of current tax liabilities and current tax assets 12 14 Recognition

Indian Accounting Standard (Ind AS) 12 Contents Income Taxes Paragraphs Objective Scope 1 4 Definitions 5 11 Tax base 7 11 Recognition of current tax liabilities and current tax assets 12 14 Recognition

A CONSOLIDATED VERSION OF THE PUBLIC DEBT MANAGEMENT ACT

M. OOZEER A CONSOLIDATED VERSION OF THE PUBLIC DEBT MANAGEMENT ACT 14 May 2015 2 A CONSOLIDATED VERSION OF THE PUBLIC DEBT MANAGEMENT ACT Act No. 5 of 2008 [Amended 14/2009, 10/2010, 36/2011, 38/2011,

M. OOZEER A CONSOLIDATED VERSION OF THE PUBLIC DEBT MANAGEMENT ACT 14 May 2015 2 A CONSOLIDATED VERSION OF THE PUBLIC DEBT MANAGEMENT ACT Act No. 5 of 2008 [Amended 14/2009, 10/2010, 36/2011, 38/2011,

Namibia. Koep & Partners. Introduction

Koep & Partners Introduction Key legislation and regulatory structure Once largely ignored by international oil and gas companies, has in recent times been called one of the last frontiers of oil and gas

Koep & Partners Introduction Key legislation and regulatory structure Once largely ignored by international oil and gas companies, has in recent times been called one of the last frontiers of oil and gas

Part 1 National Treasury

PUBLIC FINANCE MANAGEMENT ACT 1 OF 1999 [ASSENTED TO 2 MARCH 1999] [DATE OF COMMENCEMENT: 1 APRIL 2000] (Unless otherwise indicated) (English text signed by the President) as amended by Public Finance

PUBLIC FINANCE MANAGEMENT ACT 1 OF 1999 [ASSENTED TO 2 MARCH 1999] [DATE OF COMMENCEMENT: 1 APRIL 2000] (Unless otherwise indicated) (English text signed by the President) as amended by Public Finance

Exposure Draft. Guidance Note on Accounting for Derivative Contracts

Exposure Draft Guidance Note on Accounting for Derivative Contracts (Last date of comments: January 21, 2015) Issued by Research Committee The Institute of Chartered Accountants of India (Set up by an

Exposure Draft Guidance Note on Accounting for Derivative Contracts (Last date of comments: January 21, 2015) Issued by Research Committee The Institute of Chartered Accountants of India (Set up by an

Accounting and Reporting Policy FRS 102. Staff Education Note 14 Credit unions - Illustrative financial statements

Accounting and Reporting Policy FRS 102 Staff Education Note 14 Credit unions - Illustrative financial statements Disclaimer This Education Note has been prepared by FRC staff for the convenience of users

Accounting and Reporting Policy FRS 102 Staff Education Note 14 Credit unions - Illustrative financial statements Disclaimer This Education Note has been prepared by FRC staff for the convenience of users

Water Supply Authority. Regulatory Accounting Guidelines

Water Supply Authority Regulatory Accounting Guidelines Edition 2 February 2004 Regulatory Accounting Guidelines Edition 2 February 2004 Contents 1 General... 1 1.1 Background and introduction... 1 1.2

Water Supply Authority Regulatory Accounting Guidelines Edition 2 February 2004 Regulatory Accounting Guidelines Edition 2 February 2004 Contents 1 General... 1 1.1 Background and introduction... 1 1.2

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES (Issued April 1999) The standards, which have been set in bold italic type, should be read in the context of

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES (Issued April 1999) The standards, which have been set in bold italic type, should be read in the context of

EXCHANGE CONTROL IN FIJI

[A] EXCHANGE CONTROL IN FIJI INTRODUCTION Exchange Control encompasses Government s regulations with regard to the buying and selling of foreign currency and related transactions between Fiji and the rest

[A] EXCHANGE CONTROL IN FIJI INTRODUCTION Exchange Control encompasses Government s regulations with regard to the buying and selling of foreign currency and related transactions between Fiji and the rest

Generation Cost Calculation for 660 MW Thermal Power Plants

P P IJISET - International Journal of Innovative Science, Engineering & Technology, Vol. 1 Issue 10, December 2014. Generation Cost Calculation for 660 Thermal Power Plants 1 1* 2 Vilas S. MotghareP P,

P P IJISET - International Journal of Innovative Science, Engineering & Technology, Vol. 1 Issue 10, December 2014. Generation Cost Calculation for 660 Thermal Power Plants 1 1* 2 Vilas S. MotghareP P,

LONG TERM FINANCIAL PLAN (INTERIM) 2012/13 to 2022/23

2012/13 to 2022/23") LONG TERM FINANCIAL PLAN (INTERIM) 2012/13 to 2022/23 INTRODUCTION Long term financial planning is a key element of the Integrated Planning and Reporting Framework. It is the mechanism that enables local

LONG TERM FINANCIAL PLAN (INTERIM) 2012/13 to 2022/23 INTRODUCTION Long term financial planning is a key element of the Integrated Planning and Reporting Framework. It is the mechanism that enables local

RATLOU LOCAL MUNICIPALITY

RATLOU LOCAL MUNICIPALITY CREDIT CONTROL AND DEBT COLLECTION POLICY Original Council Approval Date of Council Approval Resolution Number Effective Date Amended CONTENTS CREDIT CONTROL AND DEBT COLLECTION

RATLOU LOCAL MUNICIPALITY CREDIT CONTROL AND DEBT COLLECTION POLICY Original Council Approval Date of Council Approval Resolution Number Effective Date Amended CONTENTS CREDIT CONTROL AND DEBT COLLECTION

International Accounting Standard 12 Income Taxes. Objective. Scope. Definitions IAS 12

International Accounting Standard 12 Income Taxes Objective The objective of this Standard is to prescribe the accounting treatment for income taxes. The principal issue in accounting for income taxes

International Accounting Standard 12 Income Taxes Objective The objective of this Standard is to prescribe the accounting treatment for income taxes. The principal issue in accounting for income taxes

Information Paper 16. Long-term Financial Plan (A Model Format for Financial Information)

") Information Paper 16 Long-term Financial (A Model Format for Financial Information) February 2008 LGA Long-term Financial (A Model Format for Financial Information) Information Paper Introduction The LGA

Information Paper 16 Long-term Financial (A Model Format for Financial Information) February 2008 LGA Long-term Financial (A Model Format for Financial Information) Information Paper Introduction The LGA

SAMPLE TERMS OF REFERENCE FOR ELECTRICITY SECTOR PRIVATIZATION TRANSACTION ADVISORY SERVICES

SAMPLE TERMS OF REFERENCE FOR ELECTRICITY SECTOR PRIVATIZATION TRANSACTION ADVISORY SERVICES Table of Contents 1st. INTRODUCTION... 3 2nd. ELECTRICITY SECTOR BACKGROUND. 4 3rd. SCOPE OF WORK. 6 PHASE :

SAMPLE TERMS OF REFERENCE FOR ELECTRICITY SECTOR PRIVATIZATION TRANSACTION ADVISORY SERVICES Table of Contents 1st. INTRODUCTION... 3 2nd. ELECTRICITY SECTOR BACKGROUND. 4 3rd. SCOPE OF WORK. 6 PHASE :

DRAFT ORDER (SUO-MOTU)

") Before the MAHARASHTRA ELECTRICITY REGULATORY COMMISSION 13 th Floor, Centre No.1, World Trade Centre, Cuffe Parade, Mumbai- 400 005 Tel: 22163964/65/69 Fax: 22163976 E-mail: mercindia@mercindia.org.in

Before the MAHARASHTRA ELECTRICITY REGULATORY COMMISSION 13 th Floor, Centre No.1, World Trade Centre, Cuffe Parade, Mumbai- 400 005 Tel: 22163964/65/69 Fax: 22163976 E-mail: mercindia@mercindia.org.in

AGANANG LOCAL MUNICIPALITY. Credit Control and Debt Collection Policy. Credit control and debt collection policy

AGANANG LOCAL MUNICIPALITY Credit Control and Debt Collection Policy 1 1. PREAMBLE Whereas Section 96(a) of the Local Government: Municipal Systems Act, No 32 of 2000 (hereinafter referred to as the Systems

AGANANG LOCAL MUNICIPALITY Credit Control and Debt Collection Policy 1 1. PREAMBLE Whereas Section 96(a) of the Local Government: Municipal Systems Act, No 32 of 2000 (hereinafter referred to as the Systems

International Accounting Standard 12 Income Taxes