CFPB Part 2. Consumer Finance Protection Bureau. Preparing for CFPB: Best Practices for Realtors. Partnerships Built on Trust

|

|

|

- Gabriel Jordan

- 8 years ago

- Views:

Transcription

1 CFPB Part 2 Consumer Finance Protection Bureau Partnerships Built on Trust Preparing for CFPB: Best Practices for Realtors

2 Index Overview: Realtor s Guide to CFPB 1 Realtor s Best Practice #1: Understanding Privacy Issues for Consumers 3 Realtor s Best Practice #2: Delivering Final Figures and Numbers to Title 5 Realtor s Best Practice #3: Be Knowledgable About Importance of Contract Paragraphs and Proposed Coming Changes 6 Realtor s Best Practice #4: Understanding Timelines for Closing 9 Realtor s Best Practice #5: Ask Questions of the Lender 12 Realtor s Best Practice #6: Understanding the Forms 13 Realtor s Best Practice #7: Set Reasonable Expectations for the Principals 24 Disclosing the Title Premiums Under CFPB 26 Realtor FAQs: Understanding CFPB 27 Why do I Need Title Insurance and What do I get for the Premium 29 Notes 31 updated 9/21/2015

3 Partnerships Built on Trust Preparing for CFPB: Best Practices for Realtors TREC MCE Elective Course No The purpose of this course is to reinforce the training that MCE attendees learned regarding the upcoming changes to the federal law as well as build on the tasks that a realtor can do in each transaction to ensure a smooth transaction. This course will focus on a set of best practices for realtors to help get their clients to closing timely while honoring contractual requirements. Course highlights include: Best practices to have smooth and timely closings Planned changes to the TREC contracts TAR authorization forms Understanding new privacy restrictions How to help buyers and sellers understand the new processes

4 Page 1 of 32 Overview Realtor s Guide to CFPB Background and Purpose The CFPB was created under the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act). The purpose of the CFPB is to promote fairness and transparency for mortgages, credit cards, and other consumer financial products and services. For Mortgages, this means the CFPB will: Simplify the forms and process used for closing a loan Implement rules the prevent surprises Know before you owe Find ways to encourage consumers to shop for loans New disclosure timelines allow consumers more opportunity to ask questions and understand their transaction Penalties for non-compliance are heavy for lenders Lenders will only work with properly vetted companies Compliance is mandatory October 3rd, 2015 but lenders will start testing their systems and implementing procedures sooner CFPB rules apply to: Most closed-end consumer mortgage loans (purchase and refinance) CFPB rules do not apply to: Cash transactions Home Equity Lines of Credit Loans (HELOCs) Reverse Mortgages Manufactured Housing (MHU) Loans - unless the MHU is real property Creditors making five or fewer loans a year Other miscellaneous loans CFPB Terms Lender = creditor Borrower = consumer Closing = consummation P Consummation is the time that a consumer becomes contractually obligated on a credit transaction (signs the note) which could be different from the day the transaction closes and funds Loan Estimate Good Faith Estimate (GFE) and Truth in Lending (TIL) replaced Loan Estimate is the new form used to disclose loan terms

5 Page 2 of 32 Closing Disclosure HUD1 Settlement Statement replaced with the Closing Disclosure (CD) CD also replaces the final TIL and final GFE CD also referred to as the TRID (TILA-RESPA Integrated Disclosure) The Closing Disclosure ( CD ) can be provided to the consumer by the lender or settlement agent New Timelines The loan estimate ( LE ) must be provided to the consumer (by the creditor) three (3) business days after submission of the loan application LE must be delivered or placed in the mail not later than the 7th day BEFORE consummation If not provided in person, consumer is considered to have received the LE three (3) business days after it is delivered or placed in the mail The consumer must receive the CD three (3) business days before consummation If not provided in person, the consumer is considered to have received the CD three (3) business days after it is delivered or placed in the mail The seller must receive the CD no later than the day of consummation Who Produces the CD? Either the creditor OR the settlement agent can disclose the CD to the consumer The liability and penalties however will be on the lender for failure to provide so most lenders will produce and disclose the CD However, the Settlement Agent (Title Company) will produce and disclose the Seller s Closing Disclosure/Settlement Statement What is a Business Day? A business day for the initial LE disclosure is defined as a day on which the creditor s offices are open to the public to carry on substantially all functions. A business day for the waiting period between the LE and CD is defined as all calendar days except Sunday and federal holidays. For the CD disclosure Saturdays count as a business day. The lender ultimately makes the determination of what days are counted as a business day When will a last minute change require a new three (3) day disclosure? If the APR increase above the tolerance amount If there is a change in loan product If there is an addition of prepayment penalty Note that some changes may be corrected 1 day before consummation

business days after it is delivered or placed in the mail The consumer must receive the CD three (3) business days before consummation If not provided in")

6 Page 3 of 32 Realtor Best Practice #1 Understanding Privacy Issues for Consumers TAR Authorization Form In order for a lender or title company to release the Closing Disclosure to the realtors this form needs to be signed by all principals. It should include the brokerage information. If the realtor uses a separate contract to close company it should also include their name. Personal Non-Public Information (NPI) and Secure NPI is the type of information that requires the most protection of the consumer Examples: οο Names (maiden name, middle name, mother s maiden name included); οο Social Security or Tax ID οο Passport Number οο Date of Birth οο Account or Loan Number οο Biometric information οο Credit card number οο Employment history οο Driver s license number οο User names or passwords οο Phone numbers οο Addresses Suggestions to Secure NPI οο Realtors should always utilize a secure method οο Realtors should avoid placing NPI on any mobile devices (flash drives, CDs, etc); οο Realtors should secure paper files οο Realtors should not text any NPI information

; οο Social Security or Tax ID οο Passport Number οο Date of Birth οο Account or Loan Number οο Biometric information οο Credit card number οο Employment history οο Driver s license")

7 Page 4 of 32 AUTHORIZATION TO FURNISH TILA-RESPA INTEGRATED DISCLOSURES USE OF THIS FORM BY PERSONS WHO ARE NOT MEMBERS OF THE TEXAS ASSOCIATION OF REALTORS IS NOT AUTHORIZED. Texas Association of REALTORS, Inc To: Lender, Title Company, Escrow Agent, and/or their representatives RE: (Property) I, Seller Buyer, have entered into an exclusive listing/representation agreement with the following Broker: Name of Broker: TREC License Number: Address: City, State, Zip: Phone: Fax: Name of Broker s authorized agent, if applicable: TREC License Number of Broker s authorized agent, if applicable: I hereby authorize you to disclose and furnish a copy of any and all loan estimates, closing disclosures or other settlement statements provided in relation to the closing of the real estate transaction involving the Property, to the above-named Broker or Broker s authorized agent. Signature of Client Date Signature of Client Date (TAR-2516) Page 1 of 1

8 Page 5 of 32 Realtor Best Practice #2 Delivering Final Figures and Numbers to Title Lenders will be requiring final numbers from the title companies in advance of closing so they can prepare the Closing Disclosure. Each lender will have a different timeline 87 5 for needing this information but the earlier this information is available the more likely the closing will happen on time. To help avoid closing delays realtors should help get the following items delivered to title well in advance of closing: 1. Disbursement authorizations; 2. Home warranty selections; 3. Seller payoff information; 4. Buyer s homeowner s insurance invoice; 5. All contract amendments; 6. Notification to title if their principal will close via mail-out transaction; 7. Notification to title if their principal will use a power of attorney; and 8. All third party fees to be collected on the Closing Disclosure. 1 6 Many lenders are stating that this information must be provided to them days prior to closing in order to close on time. 0 3 Realtors should also consider when the walk-through is done. For most transactions the timeline can stay the same but for transactions that had difficult negotiations or a long list of repairs to be completed a realtor may need to do two walk-throughs to be sure the items are completed well before closing.

9 Page 6 of 32 Realtor Best Practice #3 Be Knowledgeable About Importance of Contract Paragraphs and Proposed Coming Changes Paragraph 4 has historically been the paragraph that discusses financing in the contract. That paragraph has been deleted entirely and replaced. Now all financing is addressed in Paragraph 3 and the appropriate addendum.

10 Page 7 of 32 Third Party Financing Addendum Continued

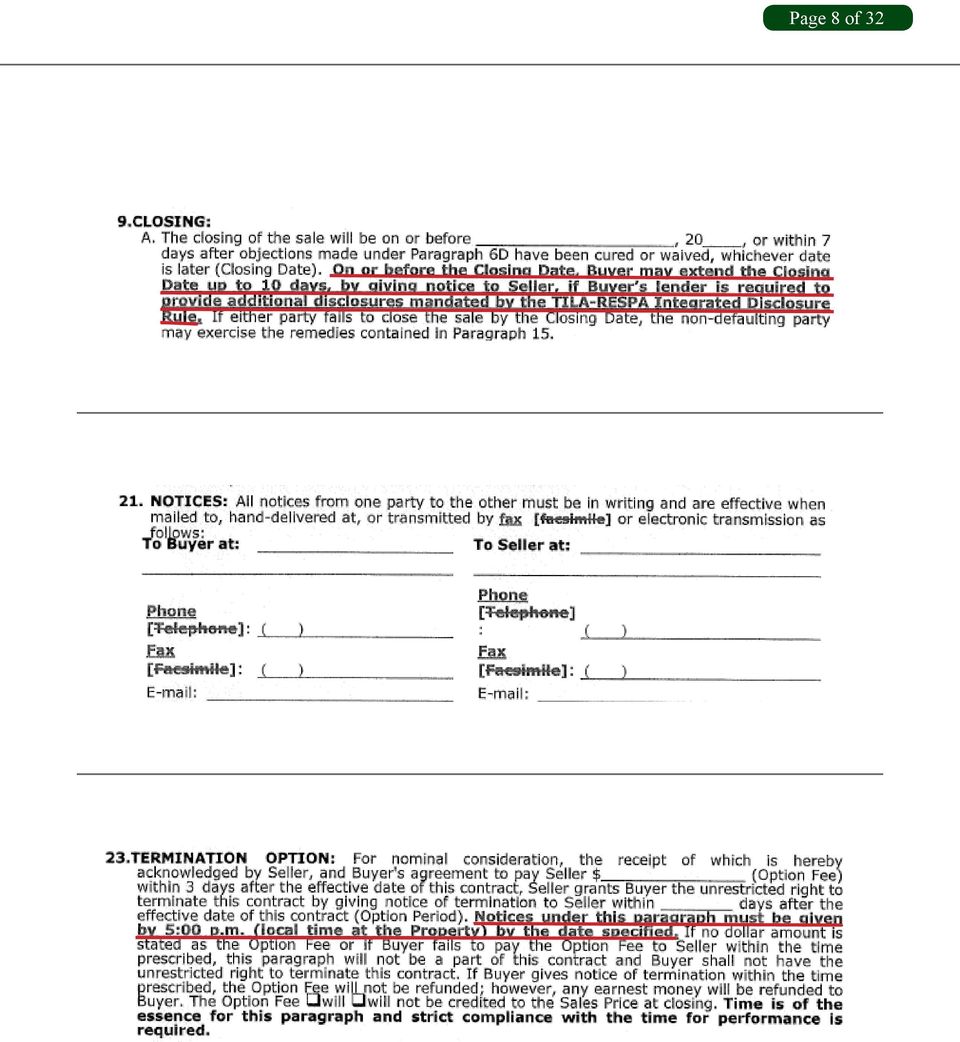

11 Page 8 of 32

12 Page 9 of 32 Realtor Best Practice #4 Understanding Timelines For Closing The Critical Dates List This is an important tool for realtors to use on their transactions to watch the critical timelines in the contract. "Back Up" Contract Sale of Other Property By Buyer Seller Financing Short Sale Critical Date List GF: Address: 123 Main Street Buyer: Bob Buyer Seller: Sam Seller Effective Date of Contract: 10/3/2015 Closing Date: 11/16/2015 Mon Earnest Money Received: 10/3/2015 Number of Days Deadline* Additional Earnest Money Commitment Delivery 20 Fri 10/23/2015 Survey Due Option 1: Existing with T47 8 Sun 10/11/2015 Option 2: New (Buyer) Option 3: New (Seller) Objections due either the closing date or: days after buyer receives the commitment, exception documents and Survey (whichever date is earlier.) 10 Seller's Disclosure Option 1: Buyer has received notice Option 2: Buyer has NOT received notice 5 Thu 10/8/2015 Option 3: Seller is not required to furnish Option Fee and Period Deadline for delivery of fee to agent or seller 3 Tue 10/6/2015 Deadline for expiration of option period 10 Tue 10/13/2015 Closing Disclosure Deadline If CD is delivered in person (3 days before closing) Thu 11/12/2015 If CD is mailed (7 days before closing) Mon 11/9/2015 Addendums Notice: Many lenders require all final figures from the title company business days prior to closing. This includes payoff statements, commission disbursement authorizations, home warranty selections, homeowner s insurance, etc. All items must be provided to us timely in order to avoid closing delays.

13 Option Fee and Period Deadline for delivery of fee to agent or seller 3 Tue 10/6/2015 Deadline for expiration of option period 10 Tue 10/13/2015 Page 10 of 32 Closing Disclosure Deadline If CD is delivered in person (3 days before closing) Thu 11/12/2015 If CD is mailed (7 days before closing) Mon 11/9/2015 The Critical Dates List - Continued Addendums Notice: Many lenders require all final figures from the title company business days prior to closing. This includes payoff statements, commission disbursement authorizations, home warranty selections, homeowner s insurance, etc. All items must be provided to us timely in order to avoid closing delays. Number of Days Deadline Third Party Financing 20 Fri 10/23/2015 Property Subjection to Mandatory Members in a POA Option 1: Seller to Provide 20 Fri 10/23/2015 Option 2: Buyer to Provide Include Any Additional Addendum Information Below, Noting the Dates Deadline *No representations or warranties are made with respect to the accuracy of the above dates. Such dates are provided merely as a convenience to the parties and the parties are encouraged to verify the dates.

14 Page 11 of 32 Sunday Monday Tuesday Wednesday Thursday Friday Saturday Four-days to prepare the Closing Disclosure First day signing / closing / funding may occur

15 Realtor Best Practice #5 Ask Questions of the Lender Page 12 of 32 Questions to ask your lenders:? Have you done a pre-qualification or a pre-approval for the borrower? Will you deliver the Closing Disclosure to the buyer In-person or via mail? What in-person methods will you allow? How many days prior to closing do you need all final figures? Will you send the Closing Disclosure to the title company to approve before sending it out to the buyers to be sure all fees are final? Will you communicate with the realtor once the Closing Disclosure has been sent? How will you handle contract amendments to add seller s credit for unfinished repairs once the Closing Disclosure has been disclosed? How confident are you that you can hit the disclosure timeline?

16 Page 13 of 32 Realtor Best Practice #6 Understand the Forms BEST BANK 1801 Oakway Boulevard Pleasant Town, TX Loan Estimate DATE ISSUED APPLICANTS PROPERTY SALE PRICE 8/01/2015 Mark Buyer 1525 Summer Lane Summertown, TX Bat Avenue Austin, TX $180, Save this Loan Estimate to compare with your Closing Disclosure. LOAN TERM PURPOSE PRODUCT LOAN TYPE LOAN ID # RATE LOCK 30 years Purchase ce Fixed Rate x Conventional FHA VA NO x YES, until 08/16/2015 at 5:00 p.m. EDT Before closing, your interest rate, points, and lender credits can change unless you lock the interest rate. All other estimated closing costs expire on 3/4/2013 at 5:00 p.m. EDT Loan Terms Loan Amount Interest Rate Monthly Principal & Interest See Projected Payments below for your Estimated Total Monthly Payment $162, % $ Can this amount increase after closing? NO NO NO Does the loan have these features? Prepayment Penalty Balloon Payment YES NO As high as $3,240 if you pay off the loan during the first 2 years Projected Payments Payment Calculation Years 1-7 Years 8-30 Principal & Interest $ $ Mortgage Insurance Estimated Escrow Amount can increase over time Estimated Total Monthly Payment $1,050 $968 Estimated Taxes, Insurance & Assessments Amount can increase over time $206 a month This estimate includes x Property Taxes x Homeowner s Insurance Other: In escrow? YES YES See Section G on page 2 for escrowed property costs. You must pay for other property costs separately. Costs at Closing Estimated Closing Costs $9,168 Includes $5,388 in Loan Costs + $3,780 in Other Costs $0 in Lender Credits. See page 2 for details. Estimated Cash to Close $29, Includes Closing Costs. See Calculating Cash to Close on page 2 for details. Visit for general information and tools. LOAN ESTIMATE PAGE 1 OF 3 LOAN ID #

17 Page 14 of 32 Closing Cost Details Loan Costs Other Costs A. Origination Charges 1 % of Loan Amount (Points) Application Fee Underwriting Fee $2,670 $1,620 $150 $900 E. Taxes and Other Government Fees Recording Fees and Other Taxes F. Prepaids Homeowner s Insurance Premium ( 6 months) Mortgage Insurance Premium ( months) Prepaid Interest ( $37.19 per day for %) Property Taxes ( months) $150 $150 $1,095 $537 $558 B. Services You Cannot Shop For Appraisal Fee Credit Report Fee Flood Determination Fee Flood Monitoring Fee Tax Monitoring Fee Tax Status Research Fee $667 $400 $30 $20 $32 $75 $110 G. Initial Escrow Payment at Closing $1,217 Homeowner s Insurance $89.50 per month for 2 mo. $179 Mortgage Insurance $ per month for 2 mo. $326 Property Taxes $ per month for 2 mo. $712 H. Other Title Owner s Title Policy (optional) $1,318 $1,318 I. TOTAL OTHER COSTS (E + F + G + H) $3,780 C. Services You Can Shop For Pest Inspection Fee Survey Fee Title Courier Fee Title Lender s Title Policy Title Settlement Agent Fee Title - Tax Certificate $2,051 $125 $365 $45 $1,218 $250 $48 J. TOTAL CLOSING COSTS D+I Lender Credits Calculating Cash to Close Total Closing Costs (J) Closing Costs Financed (Paid from your Loan Amount) Down Payment/Funds from Borrower Deposit Funds for Borrower Seller Credits Adjustments and Other Credits D. TOTAL LOAN COSTS (A + B + C) $5,388 Estimated Cash to Close $9,168 $9,168 $9,168 $0 $18,000 $2,000 $0 $0 $0 $29,168 LOAN ESTIMATE PAGE 2 OF 3 LOAN ID #

18 Page 15 of 32 Additional Information About This Loan LENDER NMLS/ LICENSE ID LOAN OFFICER NMLS/ LICENSE ID PHONE Best Bank Joe West MORTGAGE BROKER NMLS/ LICENSE ID LOAN OFFICER NMLS/ LICENSE ID PHONE Comparisons In 5 Years Use these measures to compare this loan with other loans. $112,294 $28,956 Total you will have paid in principal, interest, mortgage insurance, and loan costs. Principal you will have paid off. Annual Percentage Rate (APR) Total Interest Percentage (TIP) 4.713% 77.28% Your costs over the loan term expressed as a rate. This is not your interest rate. The total amount of interest that you will pay over the loan term as a percentage of your loan amount. Other Considerations Appraisal Assumption Homeowner s Insurance Late Payment Refinance Servicing We may order an appraisal to determine the property s value and charge you for this appraisal. We will promptly give you a copy of any appraisal, even if your loan does not close. You can pay for an additional appraisal for your own use at your own cost. If you sell or transfer this property to another person, we will allow, under certain conditions, this person to assume this loan on the original terms. x will not allow assumption of this loan on the original terms. This loan requires homeowner s insurance on the property, which you may obtain from a company of your choice that we find acceptable. If your payment is more than 15 days late, we will charge a late fee of 5% of the monthly principal and interest payment. Refinancing this loan will depend on your future financial situation, the property value, and market conditions. You may not be able to refinance this loan. We intend to service your loan. If so, you will make your payments to us. x to transfer servicing of your loan. Confirm Receipt By signing, you are only confirming that you have received this form. You do not have to accept this loan because you have signed or received this form. Applicant Signature Date Co-Applicant Signature Date LOAN ESTIMATE PAGE 3 OF 3 LOAN ID #

19 Page 16 of 32 Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 8/01/2015 Closing Date 8/03/2015 Disbursement Date 8/03/2015 Settlement Agent Gracy Title, a stewart File # company GracyTest1 Property 1501 Bat Ave. Austin, TX Sale Price $180, See attached page for additional information Loan Terms Loan Amount Interest Rate Transaction Information Borrower Mark Buyer 1525 Summer Lane $162, NO 3.875% NO Loan Information Loan Term Purpose Product Summertown, TX Seller John Seller 1501 Bat Ave. Loan Type Austin, TX Lender Best Bank Loan ID # MIC # Can this amount increase after closing? 30 Years Purchase Fixed Rate x Conventional VA FHA Monthly Principal & Interest See Projected Payments below for your Estimated Total Monthly Payment Prepayment Penalty Balloon Payment $ NO Does the loan have these features? As high as $3, if you pay off the YES loan during the first 2 years NO Projected Payments Payment Calculation Years 1-7 Years 8-30 $ $ Principal & Interest Mortgage Insurance + $ $0.00 Estimated Escrow Amount Can Increase Over Time + $ $ Estimated Total Monthly Payment $1, $ Estimated Taxes, Insurance & Assessments Amount Can Increase Over Time See Details on Page 4 This estimate includes X Property Taxes $ X Homeowner s Insurance YES In escrow? YES Monthly x Other: HOA $150 NO See Escrow Account on page 4 for details. You must pay for other property costs separately Costs at Closing Closing Costs Cash to Close $6, Includes $3, in Loan Costs + $2, in Other Costs $0.00 in Lender Credits. See page 2 for details. $21, Includes Closing Costs. See Calculating Cash to Close on page 3 for details. CLOSING DISCLOSURE PAGE 1 OF 5 LOAN ID #

20 Page 17 of 32 Closing Cost Details Loan Costs Borrower-Paid At Closing Before Closing A. Origination Charges $1, % of Loan Amount (Points) 02 Application Fee to Best Bank $ Loan Origination Fee to Best Bank $1, B. Services Borrower Did Not Shop For $ Appraisal to Best Bank $ Credit Report Fee to Best Bank $ Document Preparation Fee to Best Bank $ Tax Service to Best Bank $ C. Services Borrower Did Shop For $1, Title - Courier Fee to Gracy Title, a stewart company $45.00 $ Title - Escrow Fee to Gracy Title, a stewart company $ $ Title - Tax Certificate Fee to Tejas Tax Data $ Title - Lender's Policy to Gracy Title, a stewart company $1, Title LP Endorsement - NYDP to Gracy Title, a stewart company $ Title LP Endorsement - T19 to Gracy Title, a stewart company $ Title LP Endorsement - T30 to Gracy Title, a stewart company $ Title - LP Endorsement - T-36 to Gracy Title, a stewart company $25.00 D. TOTAL LOAN COSTS (Borrower-Paid) $3, Loan Costs Subtotals (A + B + C) $3, $0.00 Seller-Paid At Closing Before Closing Paid by Others Other Costs E. Taxes and Other Government Fees $ Recording Fees Deed: $34.00 Mortgage: $ $ e-recording Fee to Gracy Title, a stewart company $4.00 $4.00 F. Prepaids $1, Homeowner s Insurance Premium (12 mo.) to HOI $ Mortgage Insurance Premium ( mo.) 03 Prepaid Interest ($11.34 per day from 8/03/15 to 9/01/15 ) m $ Property Taxes ( o.) mo.) 05 G. Initial Escrow Payment at Closing $1, Homeowner s Insurance $75.00 per month for 2 mo. $ Mortgage Insurance per month for mo. 03 Property Taxes $ per month for 6 mo. $1, Aggregate Adjustment -$ H. Other $ HOA - Resale Certificate Fee to HOA $ HOA Transfer Fee to HOA $50.00 $ Home Warranty Fee to HWA $ Real Estate Commission Buyer s to Selling Broker $5, Broker Real Estate Commission Seller's to Listing Broker $5, Broker Title - Endorsement - A&B (optional) to Gracy Title $ onal) Title - Endorsement T19.1 (optional) to Gracy Title $ onal) Title - Owner's Policy (optional) to Gracy Title $ I. TOTAL OTHER COSTS (Borrower-Paid) $2, Other Costs Subtotals (E + F + G + H) $2, $0.00 J. TOTAL CLOSING COSTS (Borrower-Paid) $6, Closing Costs Subtotals (D + I) $6, $0.00 $12, $0.00 $0.00 Lender Credits CLOSING DISCLOSURE PAGE 2 OF 5 LOAN ID #

21 Page 18 of 32 Calculating Cash to Close Use this table to see what has changed from your Loan Estimate Loan Estimate Final Did this change? See Total Loan Costs (D) and Total Other Costs (I) Total Closing Costs (J) $9, $6, YES Closing Costs Paid Before Closing $0.00 $0.00 Closing Costs Financed (Paid from your Loan Amount) $0.00 $0.00 NO NO Down Payment/Funds from Borrower $18, $18, NO You increased this payment. See details in Sections K and L. Deposit $2, $2, NO You decreased this payment. See details in Section L. Funds for Borrower $0.00 $0.00 Seller Credits $0.00 $0.00 NO The amount the seller will pay for the loan costs has increased. See details in Section L. Adjustments and Other Credits $0.00 -$1, YES See details in Sections K and L Cash to Close $29, $21, NO Summaries of Transactions Use this table to see a summary of your transaction. BORROWER S TRANSACTION K. Due from Borrower at Closing $186, Sale Price of Property $180, Sale Price of Any Personal Property Included in Sale 03 Closing Costs Paid at Closing (J) $6, Adjustments Adjustments for Items Paid by Seller in Advance 08 City/Town Taxes 09 County Taxes 10 Assessments 11 HOA Dues 8/3/15 to 9/1/15 $ L. Paid Already by or on Behalf of Borrower at Closing $165, Deposit $2, Loan Amount $162, Existing Loan(s) Assumed or Taken Subject to Seller Credit Other Credits Adjustments 09 Adjustment for Title Insurance Premium $1, Credit for Option Fee Adjustments for Items Unpaid by Seller 13 City/Town Taxes 14 County Taxes 15 Assessments $ $3, CALCULATION Total Due from Borrower at Closing (K) $186, Total Paid Already by or on Behalf of Borrower at Closing (L) -$165, Cash to Close From To Borrower $21, SELLER S TRANSACTION M. Due to Seller at Closing $180, Sale Price of Property $180, Sale Price of Any Personal Property Included in Sale Adjustments for Items Paid by Seller in Advance 09 City/Town Taxes 10 County Taxes 11 Assessments 12 HOA Dues 8/3/15 to 9/1/15 $ N. Due from Seller at Closing $113, Excess Deposit 02 Closing Costs Paid at Closing (J) $12, Existing Loan(s) Assumed or Taken Subject to 04 Payoff of First Mortgage Loan $100, Payoff of Second Mortgage Loan Adjustment for Title Insurance Premium $1, Credit for Option Fee $ Adjustments for Items Unpaid by Seller 15 City/Town Taxes 16 County Taxes 01/01/15 to 08/03/15 17 Assessments /01/15 to 08/03/15 $3, CALCULATION Total Due to Seller at Closing (M) $180, Total Due from Seller at Closing (N) -$113, Cash From To Seller $66, CLOSING DISCLOSURE PAGE 3 OF 5 LOAN ID #

22 Page 19 of 32 Additional Information About This Loan Loan Disclosures Assumption If you sell or transfer this property to another person, your lender will allow, under certain conditions, this person to assume this loan on the original terms. X will not allow assumption of this loan on the original terms. Demand Feature Your loan has a demand feature, which permits your lender to require early repayment of the loan. You should review your note for details. X does not have a demand feature. Late Payment If your payment is more than 15 days late, your lender will charge a late fee of 5% of the monthly principal and interest payment. Negative Amortization (Increase in Loan Amount) Under your loan terms, you are scheduled to make monthly payments that do not pay all of the interest due that month. As a result, your loan amount will increase (negatively amortize), and your loan amount will likely become larger than your original loan amount. Increases in your loan amount lower the equity you have in this property. may have monthly payments that do not pay all of the interest due that month. If you do, your loan amount will increase (negatively amortize), and, as a result, your loan amount may become larger than your original loan amount. Increases in your loan amount lower the equity you have in this property. X do not have a negative amortization feature. Partial Payments Your lender may accept payments that are less than the full amount due (partial payments) and apply them to your loan. may hold them in a separate account until you pay the rest of the payment, and then apply the full payment to your loan. X does not accept any partial payments. If this loan is sold, your new lender may have a different policy. Security Interest You are granting a security interest in 1501 Bat Ave., Austin, TX Property Address You may lose this property if you do not make your payments or satisfy other obligations for this loan. Escrow Account For now, your loan X will have an escrow account (also called an impound or trust account) to pay the property costs listed below. Without an escrow account, you would pay them directly, possibly in one or two large payments a year. Your lender may be liable for penalties and interest for failing to make a payment. Escrow Escrowed Property Costs over Year 1 Non-Escrowed Property Costs over Year 1 Initial Escrow Payment Monthly Escrow Payment will not have an escrow account because you declined it your lender does not offer one. You must directly pay your property costs, such as taxes and homeowner s insurance. Contact your lender to ask if your loan can have an escrow account. No Escrow Estimated Property Costs over Year 1 Escrow Waiver Fee $2, Estimated total amount over year 1 for your escrowed property costs: Homeowner s Insurance, Property Taxes $1, Estimated total amount over year 1 for your non-escrowed property costs: HOA You may have other property costs. $1, A cushion for the escrow account you pay at closing. See Section G on page 2. $ The amount included in your total monthly payment. Estimated total amount over year 1. You must pay these costs directly, possibly in one or two large payments a year. In the future, Your property costs may change and, as a result, your escrow payment may change. You may be able to cancel your escrow account, but if you do, you must pay your property costs directly. If you fail to pay your property taxes, your state or local government may (1) impose fines and penalties or (2) place a tax lien on this property. If you fail to pay any of your property costs, your lender may (1) add the amounts to your loan balance, (2) add an escrow account to your loan, or (3) require you to pay for property insurance that the lender buys on your behalf, which likely would cost more and provide fewer benefits than what you could buy on your own. Adjustable Payment (AP) Table Adjustable Interest Rate (AIR) Table CLOSING DISCLOSURE PAGE 4 OF 5 LOAN ID #

23 Page 20 of 32 Loan Calculations Total of Payments. Total you will have paid after you make all payments of principal, interest, mortgage insurance, and loan costs, as scheduled. $285, Finance Charge. The dollar amount the loan will cost you. $118, Amount Financed. The loan amount available after paying your upfront finance charge. $162, Annual Percentage Rate (APR). Your costs over the loan term expressed as a rate. This is not your interest rate. Total Interest Percentage (TIP). The total amount of interest that you will pay over the loan term as a percentage of your loan amount % 69.46% Other Disclosures Appraisal If the property was appraised for your loan, your lender is required to give you a copy at no additional cost at least 3 days before closing. If you have not yet received it, please contact your lender at the information listed below. Contract Details See your note and security instrument for information about what happens if you fail to make your payments, what is a default on the loan, situations in which your lender can require early repayment of the loan, and the rules for making payments before they are due. Liability after Foreclosure If your lender forecloses on this property and the foreclosure does not cover the amount of unpaid balance on this loan, X state law may protect you from liability for the unpaid balance. If you refinance or take on any additional debt on this property, you may lose this protection and have to pay any debt remaining even after foreclosure. You may want to consult a lawyer for more information. state law does not protect you from liability for the unpaid balance.? Questions? If you have questions about the loan terms or costs on this form, use the contact information below. To get more information or make a complaint, contact the Consumer Financial Protection Bureau at Refinance Refinancing this loan will depend on your future financial situation, the property value, and market conditions. You may not be able to refinance this loan. Tax Deductions If you borrow more than this property is worth, the interest on the loan amount above this property s fair market value is not deductible from your federal income taxes. You should consult a tax advisor for more information. Contact Information Lender Mortgage Broker Real Estate Broker (B) Real Estate Broker (S) Omega Real Estate Broker, Inc 135 S Main Street Austin, TX Name Best Bank Alpha Real Estate Broker Company Address 1801 Oakway Blvd. 246 West Avenue Pleasant Town, TX Austin, TX NMLS ID TX License ID Contact Joe West Michael Smith Fred Jones Contact NMLS ID Contact A78626 P13415 TX License ID joewest@bestbank.fake msmith@alpha.biz fred@omegare.biz Phone Settlement Agent Gracy Title, a stewart company 100 Congress Ave Austin, TX Jane Closer Z closer@gracytitle.com Confirm Receipt By signing, you are only confirming that you have received this form. You do not have to accept this loan because you have signed or received this form. Applicant Signature Date Co-Applicant Signature Date CLOSING DISCLOSURE PAGE 5 OF 5 LOAN ID #

24 Page 21 of 32 Texas Disclosure Form T-64 This form provides additional disclosures and acknowledgements required in Texas. It is used with the federal Closing Disclosure form. Closing Information Transaction Information Closing Disclosure Issued Property Address: 1501 Bat Ave., Austin, TX Date: 8/01/2015 Closing Date: 8/03/2015 Borrower(s): Mark Buyer GF #: GracyTest1 Address(es): 1525 Summer Lane, Summertown, TX Sales Price: $180, Seller(s): John Seller Loan Amount: $162, Address(es): 1501 Bat Ave., Austin, Texas Lender: Best Bank Address: 1801 Oakway Blvd. Pleasant Town, TX Lender and Settlement Agent Settlement Agent: Gracy Title, a stewart company Address: 901 S. MoPac, Bldg III, Suite 100 Austin, TX Title Insurance Premiums If you are buying both an owner s policy and a loan policy, the title insurance premiums on this form might be different than the premiums on the Closing Disclosure. The owner s policy premium listed on the Closing Disclosure will probably be lower than on this form, and the loan policy premium will probably be higher. If you add the two policies premiums on the Closing Disclosure together, however, the total should be the same as the total of the two premiums on this form. The premiums are different on the two forms because the Closing Disclosure is governed by federal law, while this form is governed by Texas law. The owner s policy and loan policy premiums are set by the Texas commissioner of insurance. When you buy both an owner s policy and a loan policy in the same transaction, you are charged the full premium for the owner s policy but receive a discount on the loan policy premium. Federal and Texas law differ on where the discount is shown. Texas law requires the discount to be reflected in the loan policy premium, while federal law requires the discount to be reflected in the owner s policy premium. Title Agent: Gracy Title, a stewart company Owner s Policy Premium $200 Loan Policy Premium $1218 Underwriter: Stewart Title Guaranty Company Endorsements $ Other $ TOTAL $1, Of this total amount: $ (or 15%) will be paid to the Underwriter; the Title Agent will retain $1, (or 85%); and the remainder of the premium will be paid to other parties as follows: Amount ($ or %) To Whom For Services Fees Paid to Settlement Agent Fees Paid to Settlement Agent on the Closing Disclosure include: Title - Courier Fee $70.00 Title - Tax Certificate Fee $48.00 GF # Page 1 of 2

25 Page 22 of 32 Texas Disclosure Form T-64 This form provides additional disclosures and acknowledgements required in Texas. It is used with the federal Closing Disclosure form. Real Estate Commission Disbursement Portions of the Real Estate Commissions disclosed on the Closing Disclosure will be disbursed to: Michael Smith Fred Jones Other Disclosures Although not required, this section may be used to disclose individual recording charges included on Line 01 of Section E of the Closing Disclosure, or to disclose a breakdown of other charges that were combined on the Closing Disclosure: Document Name Recording Fee Document Name Recording Fee Power of Attorney $37.00 Closing Disclosure Charge Name Included in Closing Disclosure Charge The Closing Disclosure was assembled from the best information available from other sources. The Settlement Agent cannot guarantee the accuracy of that information. Tax and insurance prorations and reserves were based on figures for the preceding year or supplied by others, or are estimates for current year. If there is any change for the current year, all necessary adjustments must be made directly between Seller and Borrower, if applicable. I (We) acknowledge receiving this Texas Disclosure and the Closing Disclosure. I (We) authorize the Settlement Agent to make the expenditures and disbursements on the Closing Disclosure and I (we) approve those payments. If I am (we are) the Borrower(s), I (we) acknowledge receiving the Loan Funds, if applicable, in the amount on the Closing Disclosure. Borrower: Seller: Borrower: Seller: Settlement Agent: By: Escrow Officer GF # GracyTest1 Page 2 of 2

26 Page 23 of 32 File Number: Gracytest1 Closing Information SELLER S SETTLEMENT STATEMENT Transaction Information Date Issued Closing Date 8/03/2015 Disbursement Date 8/03/2015 File # Gracytest1 Property Location 1501 Bat Ave. Austin, TX Buyer/Borrower Seller Mark Buyer 1525 Summer Lane Summertown, TX John Seller 1501 Bat Ave. Austin, TX Gracy Title 901 S Mopac, Building III, Suite 100, Austin, TX Debit Credit Sales Price Sales Price of Property $180, Payoffs Payoff of First Mortgage Loan to First Mortgage $100, New Loan Charges Services Borrower Did Not Shop For Document Preparation Fee to Best Bank $ Taxes and Other Government Fees e-recording Fee to Gracy Title $4.00 Other HOA - Resale Certificate to Hoa $ HOA Transfer Fee to HOA $ Home Warranty Fee to HWA $ Real Estate Commission Buyer s Broker $5, to Selling Broker $5, Real Estate Commission Seller's Broker $5, to Lising Broker $5, Title Charges Title - Courier Fee to Gracy Title $25.00 Title - Escrow Fee to Gracy Title $ Title - Tax Certificate Fee to Gracy Title $48.00 Title Insurance Premiums and Endorsement Fees The title insurance premiums represent the rates filed with the Texas Department of Insurance. The title insurance premiums shown on the Closing Disclosure were calculated and disclosed in the manner required by Federal regulation. Despite the difference in the breakdown of premiums disclosed, the total combined premiums are equal to the total combined premiums shown on the Closing Disclosure. Title - Owner's Policy (optional) $180, Premium - $1, to Gracy Title A B OTP RESIDENTIAL $65.90 Title Premium Total: $1, Underwriter Remittance Title Agent: Gracy Title Underwriter: Stewart Title Guaranty Company Of this total amount: $ (or 20%) will be paid to the Underwriter; $1, (or 80%) will be retained by the Title Agent Adjustments for Items Paid By Seller In Advance HOA Dues 8/3/2015 to 9/1/2015 $33.37 Adjustments for Items Unpaid By Seller County Taxes 1/1/2015 to 8/3/2015 $3, Subtotal: $116, $180, Balance due to Seller: $63, Totals: $180, $180,033.37

27 Realtor Best Practice #7 Set Reasonable Expectations for the Principals Page 24 of 32 Steps to help your buyer clients get to closing: 1. Encourage your clients to think through mortgage choices first. The pre-application timeframe is critical and gives clients a chance to decide on a loan type and down payment amount before they are focused on a closing date. Once your clients go under contract the timeline to get to closing can be shorter than they really understand. Make sure your clients feel comfortable they can afford the home and feel confident in their ability to receive a mortgage loan approval for the required amount. Encourage prospective homebuyers to review their credit reports early in the process. Through early review, they can find and correct errors to potentially raise their credit score and reduce their cost of borrowing. If the client is going to shop lenders now is the time to do so before they go under contract. 2. Once a property has been identified, encourage your clients to request the initial Loan Estimates from their lender. Loan Estimates show rates and loan terms in an easy-to-compare format, customized based on your clients credit and the details of their request. Clients who understand market rates are more likely to feel confident about their choices and work proactively and collaboratively with their lender. Loan Estimates are most useful when your clients define the requested mortgage type and compare apples-to-apples Loan Estimates. This is also the time to talk to your clients about the importance of providing all documentation needed to the lender as soon as possible. Your clients should also be shopping for and selecting their homeowner s insurance at this time now too. 3. Make sure your clients indicate their intent to proceed to their loan officers. Loan Estimates expire after ten business days. If your clients do not complete the steps required by the lender to express their intent to proceed your clients may have to start over with a new application and the lender would not be obligated to honor the initial Loan Estimate terms as provided.

28 Page 25 of Be the source of accurate and timely information about the property and transaction. Make sure your clients have detailed information they can share with their lender about property taxes, homeowner s association fees, condominium association fees, and the estimated cost for homeowners insurance. Although the lender likely needs to verify these costs later, accurate numbers now can prevent revised Loan Estimates later. If anything about the transaction changes, communicate those changes promptly to everyone involved and confirm the information has been received. The lender determines whether the change requires a revised Loan Estimate. Your best strategy is to communicate any changes to your client and to confirm that the lender has received the information as well. Confirm the lender and the closing company have the buyer s and the seller s real estate broker information. Because this information appears on the Closing Disclosure, they both need correct and complete information. 5. Get all paperwork and final figures to title at least two weeks prior to closing. This would include home warranty selection, HOI binders, commission disbursements, etc. 6. Find out who provides the Closing Disclosure for your transaction. Some lenders may only send the CD to the buyers and you will need to talk to your buyers about the importance of sharing the form with you and the title company. Tips for listing agents: 1. Encourage your sellers to complete any required repairs timely; 2. Discuss the importance of replying to title company questionnaires timely; 3. Have your seller provide their payoff information and marital status at the time of signing the listing agreement; 4. Prepare your sellers for potential delays in closing. Make sure you are discussing the closing paragraph of the contract with them and the potential that closing will be pushed back. For more information from this article visit the CFPB website:

29 Disclosing the Title Premiums Disclosing the Under Title Premiums CFPB Under CFPB Page 26 of 32 Rule: We are required to disclose the full cost of the lender s title policy as a charge to the buyer. EXAMPLE: You have a sales price of $180,000 and a loan amount of $162,000. The buyer wants A&B and T19.1. The lender requires T 36, T 19 and full tax deletion. How It Looks On Page 2: Borrower Paid Seller Paid Paid by Others At Closing Before Closing At Closing Before Closing C. Services Borrower Did Shop For Title Lender s Title Insurance Title Lender s Title Insurance Endorsements $ Per lender H. Other Title Owners Title Insurance (optional) $ Title Owners Title Insurance Endorsements The total premium collected is $1418. *Mathematical Breakdown: OTP cost $1318 LP cost ($1218) Difference: $100 Per Buyer Plus: Total $100 (simultaneous issue cost) $200 additional required from buyer under Other In order to follow the contract terms, we will still have an adjustment from the seller to the buyer for their OTP amount. Page 3: Paid Already by or on Behalf of Borrower at Closing Adjustments: Adjustment for Title Insurance Premium Due from Seller at Closing Adjustments: $ ** Adjustment for Title Insurance Premium $

30 Page 27 of 32 Q: What is changing? Realtor s Guide Understanding to Understanding CFPB CFPB FAQ A: There are lots of things changing. Buyers, Seller, Realtors, Lenders and Title Companies will all see new forms, new terminology and new timelines for closing. Q; Where are these changes coming from and why are things changing? A: The changes coming soon originated from the Dodd-Frank Wall Street Reform and Consumer Protection Act that was created in From this Act the Consumer Finance Protection Bureau was created (herein after known as CFPB). The CFPB made the changes discussed below to help consumers understand their mortgages and the pre-closing disclosures to help them better shop their loan options. These rules and new forms also help prevent surprises at closing and should serve to have more informed buyers at the closing table. Q: When do these changes go into effect? A: The rules change for all loan applications that are taken on October 1, 2015 and after. Q: What lender forms are changing? A: Under today s loan application process each potential lender provides the buyer with a Good Faith Estimate and a Truthin-Lending disclosure. A borrower is expected to (1) understand these forms and (2) be able to comparison shop between each lender. Since your average buyer does not purchase property very often these forms can be confusing for them. Each lender uses different terminology for the fees that are charged and these forms often make reference to industry specific concepts that a borrower may not be familiar with. An example of this would be a Good Faith Estimate that refers to the payment as PITI instead of specifying to the buyer that they mean the payment includes principal, interest, taxes and insurance. The Good Faith Estimate and Truth-in-Lending are being replaced with the Loan Estimate. The Loan Estimate must be provided within 3 days of application and will itemize the loan terms, cash-to-close, closing fees and loan characteristics using a plain-language explanation. Q: What closing forms are changing? A: When a buyer goes to closing today they are presented with a Settlement Statement (HUD-1), Final Good Faith Estimate and Final Truth-in-Lending form. These three forms are being replaced by the Closing Disclosure. This disclosure includes all loan terms, the fees associated with closing and also a list of the loan features. Q: Who will prepare these forms? A: Under the rules either the lender or the closing agent may prepare these forms. The lender, however, is responsible and liable for any mistakes in the disclosures so for that reason most lenders are choosing to prepare both the Loan Estimate and the Closing Disclosure. These same lenders are also taking responsibility for delivering the Closing Disclosure to the buyer. Q: What about the sellers? What forms will they see? A: The sellers will receive a separate closing statement. Production and delivery of their statement is not mandated by CFPB and the seller may receive their documents up until the day of closing. These forms will be sent to the seller from the title company. Q: What timelines are changing? Realtor FAQs A: The law now imposes a mandatory waiting period to permit the buyer time to review their final loan terms prior to closing. A distinction is made with respect to the timeline on the delivery of the Closing Disclosure. If the Closing Disclosure is

31 Page 28 of 32 provided in-person to the consumer then there is a three day waiting period between disclosure and closing. If the Closing Disclosure is not provided in-person then the client is deemed to have received the Closing Disclosure three days from it being sent and then the three day waiting period starts. Q: Does the closing date count as part of the three days? A: No. The day of closing does not count as part of the three days. For example if your file is to close on Friday the Closing Disclosure must be sent by the Tuesday before closing. The three day review period would include Tuesday, Wednesday and Thursday to review and then the closing could occur on Friday. Note that this is the rule for an inperson delivery. If the Closing Disclosure was not delivered via an in-person method then the Closing Disclosure is received three days from it being sent and then the three day waiting period starts. Under this example if closing was Friday the Closing Disclosure would need to be sent the previous Friday. In this example the Closing Disclosure is sent on Friday and received by the customer Tuesday to start the three day review period. Q: How are the days counted? A: For the Closing Disclosure, business days are counted as all days except Sundays and Federal holidays. Q: What happens if something changes in the transaction after the Closing Disclosure has been sent? A: Not all changes to the Closing Disclosure will require a new three-day waiting period. Changes that will require another mandatory waiting period are: (1) a change to the annual percentage rate of 0.125% or more (can be 0.25% on smaller loans); (2) a change in the loan product, or (3) the addition of a pre-payment to the loan. Other changes will have to be reviewed by the lender and the lender will decide if another waiting period is necessary. Q: What if my client went under contract in September for an October closing but decides to switch lenders after October 1 st? A: The new lender would be subject to all requirements under CFPB for forms and timelines. Q: Are there any transactions that do not fall under these new rules? A: Yes. Cash transactions are not subject to CFPB. Also CFPB does not apply to home equity line of credit loans, reverse mortgages, manufactured home loans, and loans given by lenders that issue five or fewer loans per year. Q: If the lender is sending the Closing Disclosure who is handling the closing now? A: Your title company is still handling the actual closing. The title company still opens escrow for the earnest money contract and processes your transaction through funding and title policy production. The title company will still be working up the figures in their systems since they have to do the actual disbursements of all funds through the transaction. Q: Since the lenders are now completing the Closing Disclosure how will they know what non-loan fees to use for closing? A: The title company will be supplying all non-loan fee information to the lender for completion of the Closing Disclosure. The title company will supply the lender with the figures for the title premiums, tax and homeowners association prorations, realtor commissions, third-party fees and seller payoffs. Many lenders are stating they will require final figures from the title company 10 days to two weeks prior to closing. Q: What are the things I can do to help my closings go smoothly? A: To avoid a delay in your closings it will be important that you have everything ready for closing no less than 15 days prior to closing. The title company will have to provide all transaction details to the lender days prior to closing. Things to consider would be disbursement authorizations, home warranty selections, all amendments, and any figures that affect closing. Also, when the law first goes into effect consider adding a cushion to the closing date. In the beginning if you re typically writing 30 day contracts you may want to consider 45 days unless you are confident your buyer s lender can hit the closing timeline.

Important Information Regarding TILA-RESPA Integrated Disclosure (TRID) Rule

Rule") Important Information Regarding TILA-RESPA Integrated Disclosure (TRID) Rule Notice to students: If your course contains information on the Truth in Lending Act (TILA) and the Real Estate Settlement Procedure

Important Information Regarding TILA-RESPA Integrated Disclosure (TRID) Rule Notice to students: If your course contains information on the Truth in Lending Act (TILA) and the Real Estate Settlement Procedure

HERE ARE FIVE THINGS YOU WILL NEED TO KNOW BEFORE THE NEW RULES TAKE EFFECT OCTOBER 3, 2015

5 THINGS TO KNOW BEFORE OCTOBER 3RD, 2015 As a result of the 20 financial meltdown, the Consumer Financial Protection Bureau (CFPB) has published a new set of game changing rules and forms that will impact

5 THINGS TO KNOW BEFORE OCTOBER 3RD, 2015 As a result of the 20 financial meltdown, the Consumer Financial Protection Bureau (CFPB) has published a new set of game changing rules and forms that will impact

Presented by TREC Instructor: Laura Perry, Attorney TREC course: 7748

Presented by TREC Instructor: Laura Perry, Attorney TREC course: 7748 Comprehensive Outline Say Goodbye to the HUD1 and GFE on October 1 st, 2015 (or Hello Loan Estimate and Closing Disclosure) Opening

Presented by TREC Instructor: Laura Perry, Attorney TREC course: 7748 Comprehensive Outline Say Goodbye to the HUD1 and GFE on October 1 st, 2015 (or Hello Loan Estimate and Closing Disclosure) Opening

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures Agenda Basics: Why We re Here Final Rule The New Forms Evaluating the Rule Cost to Implement What s Next Questions Basics Dodd-Frank

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures Agenda Basics: Why We re Here Final Rule The New Forms Evaluating the Rule Cost to Implement What s Next Questions Basics Dodd-Frank

Transaction Information. Michael Jones and Mary Stone 123 Anywhere Street. Anytown, ST 12345. Steve Cole and Amy Doe 321 Somewhere Drive

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 4//20 Closing Date 4//20 Disbursement Date

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 4//20 Closing Date 4//20 Disbursement Date

TILA RESPA Integrated Disclosure

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-25(E) Mortgage Loan Transaction Closing Disclosure Refinance Transaction Sample This is a sample of a completed Closing Disclosure for the refinance

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-25(E) Mortgage Loan Transaction Closing Disclosure Refinance Transaction Sample This is a sample of a completed Closing Disclosure for the refinance

TABLE OF CONTENTS. Form Number Title / Description Page

TABLE OF CONTENTS Form Number Title / Description Page TIME CHART / ROUNDING FORMS LOAN ESTIMATE Loan Estimate and Closing Disclosure Time Chart 1 TILA RESPA Time Chart 3 Loan Estimate Rounding Chart 5

TABLE OF CONTENTS Form Number Title / Description Page TIME CHART / ROUNDING FORMS LOAN ESTIMATE Loan Estimate and Closing Disclosure Time Chart 1 TILA RESPA Time Chart 3 Loan Estimate Rounding Chart 5

CFPB s RESPA TILA Integrated Disclosure. Finley P. Maxson NAR Senior Counsel fmaxson@realtors.org (312) 329-8381

329-8381") CFPB s RESPA TILA Integrated Disclosure Finley P. Maxson NAR Senior Counsel fmaxson@realtors.org (312) 329-8381 RESPA-TILA Integrated Disclosure A. Background I. Impetus for change a. Dodd-Frank directed

CFPB s RESPA TILA Integrated Disclosure Finley P. Maxson NAR Senior Counsel fmaxson@realtors.org (312) 329-8381 RESPA-TILA Integrated Disclosure A. Background I. Impetus for change a. Dodd-Frank directed

Understanding TRID Forms

YOUR GUIDE TO Understanding TRID Forms Learn more about the Loan Estimate, Closing Disclosure and Settlement Statement. This book includes details such as tolerance/variance levels, form changes based

YOUR GUIDE TO Understanding TRID Forms Learn more about the Loan Estimate, Closing Disclosure and Settlement Statement. This book includes details such as tolerance/variance levels, form changes based

Settlement Disclosure

Settlement Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Settlement information Date 2/21/2012 Agent ABC Settlement File # 01234

Settlement Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Settlement information Date 2/21/2012 Agent ABC Settlement File # 01234

TRID. Loan Estimate and Closing Disclosure Cross-reference Guide 07.01.2015. 2015 Temenos USA. All rights reserved

TRID T I L A-RESPA INTEGRAT E D D I S C L O S U R E S Loan Estimate and Closing Disclosure Cross-reference Guide 07.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636

TRID T I L A-RESPA INTEGRAT E D D I S C L O S U R E S Loan Estimate and Closing Disclosure Cross-reference Guide 07.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636

Closing Disclosure. Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

KNOW BEFORE YOU CLOSE THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE EXPLAINED

I. What is the CFPB? KNOW BEFORE YOU CLOSE THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE EXPLAINED For more than 30 years, federal law has required all lenders to provide two disclosure forms to consumers

I. What is the CFPB? KNOW BEFORE YOU CLOSE THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE EXPLAINED For more than 30 years, federal law has required all lenders to provide two disclosure forms to consumers

TILA/RESPA INTEGRATED DISCLOSURE RULE

TILA/RESPA INTEGRATED DISCLOSURE RULE Effective August 1, 2015 TRID Terms Explained 1. CFPB Consumer Financial Protection Bureau Agency tasked with protecting consumers related to financial transactions.

TILA/RESPA INTEGRATED DISCLOSURE RULE Effective August 1, 2015 TRID Terms Explained 1. CFPB Consumer Financial Protection Bureau Agency tasked with protecting consumers related to financial transactions.

Settlement Disclosure

Settlement Disclosure This form is a statement of final loan terms and actual closing costs. Settlement information Date 12/13/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd, Ste 405

Settlement Disclosure This form is a statement of final loan terms and actual closing costs. Settlement information Date 12/13/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd, Ste 405

Settlement Disclosure

Settlement Disclosure This form is a statement of final loan terms and actual closing costs. Settlement information Date 12/13/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd, Ste 405

Settlement Disclosure This form is a statement of final loan terms and actual closing costs. Settlement information Date 12/13/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd, Ste 405

MVB MORTGAGE presents A Guide to TRID: the New Loan Estimate & Closing Disclosure

MVB MORTGAGE presents A Guide to TRID: the New Loan Estimate & Closing Disclosure We re the piece of the puzzle bringing the home ownership picture together for your clients! The McCoy Team Danny McCoy

MVB MORTGAGE presents A Guide to TRID: the New Loan Estimate & Closing Disclosure We re the piece of the puzzle bringing the home ownership picture together for your clients! The McCoy Team Danny McCoy

Closing Information Transaction Information Loan Information

Credir, NMLS# Credir NMLS # Originar: Loan Originar, NMLS# Originar NMLS # Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate.

Credir, NMLS# Credir NMLS # Originar: Loan Originar, NMLS# Originar NMLS # Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate.

Settlement Disclosure Form

Settlement Disclosure Form This form is a statement of final loan terms and actual settlement costs. SETTLEMENT INFORMATION Date 11/9/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd,

Settlement Disclosure Form This form is a statement of final loan terms and actual settlement costs. SETTLEMENT INFORMATION Date 11/9/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd,

TRID Consolidated Resources

TRID Consolidated Resources Annotated Forms for TILA RESPA Integrated Disclosure Closing Disclosure. 1 Annotated Forms for TILA RESPA Integrated Disclosure Loan Estimate.2 Closing Disclosure Form.. 3 Loan

TRID Consolidated Resources Annotated Forms for TILA RESPA Integrated Disclosure Closing Disclosure. 1 Annotated Forms for TILA RESPA Integrated Disclosure Loan Estimate.2 Closing Disclosure Form.. 3 Loan

Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD).

.") Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD). Page 1 Closing Information Date Issued Date the CD

Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD). Page 1 Closing Information Date Issued Date the CD

Upon completion you will be able to:

Agenda This training manual consists of three parts that will provide you with step-bystep instructions about how to complete the Closing Disclosure form required by the Integrated Disclosures Rule Upon

Agenda This training manual consists of three parts that will provide you with step-bystep instructions about how to complete the Closing Disclosure form required by the Integrated Disclosures Rule Upon

Loan Estimate. Loan Terms. Projected Payments. Costs at Closing. Save this Loan Estimate to compare with your Closing Disclosure.

Loan Estimate DATE ISSUED APPLICANTS PROPERTY SALE PRICE Loan Terms Save this Loan Estimate to compare with your Closing Disclosure. LOAN TERM 30 years PURPOSE Purchase PRODUCT 5 Year Interest Only, 5/3

Loan Estimate DATE ISSUED APPLICANTS PROPERTY SALE PRICE Loan Terms Save this Loan Estimate to compare with your Closing Disclosure. LOAN TERM 30 years PURPOSE Purchase PRODUCT 5 Year Interest Only, 5/3

UNDERSTANDING THE LOAN ESTIMATE

The following breaks down the Loan Estimate by section with examples from Encompass followed by official commentary. Also attached, is a copy of a completed Loan Estimate form provided by the Encompass..

The following breaks down the Loan Estimate by section with examples from Encompass followed by official commentary. Also attached, is a copy of a completed Loan Estimate form provided by the Encompass..

CFPB Loan Disclosure Rules: Know Before You Owe Mortgage Forms The New Requirements and Their Impact on Financial Institutions

CFPB Loan Disclosure Rules: Know Before You Owe Mortgage Forms The New Requirements and Their Impact on Financial Institutions David A. Elliott Partner Richard C. Keller Partner OUTLINE Section 1032(f)

CFPB Loan Disclosure Rules: Know Before You Owe Mortgage Forms The New Requirements and Their Impact on Financial Institutions David A. Elliott Partner Richard C. Keller Partner OUTLINE Section 1032(f)

Know Before You Owe. TILA-RESPA Integrated Disclosure (TRID) Rule

Rule") Know Before You Owe TILA-RESPA Integrated Disclosure (TRID) Rule Background of CFPB The Consumer Financial Protection Bureau (CFPB) was established in 2010 under the Dodd-Frank Act Directed to publish

Know Before You Owe TILA-RESPA Integrated Disclosure (TRID) Rule Background of CFPB The Consumer Financial Protection Bureau (CFPB) was established in 2010 under the Dodd-Frank Act Directed to publish

TRID Survival Guide: Consumer Edition

TRID Survival Guide: Consumer Edition What you need to know about the TILA-RESPA Integrated Closing Disclosures. NFM Lending NMLS # 2893 Toll-Free: 1-888-233-0092 www.nfmlending.com Introduction NFM Lending

TRID Survival Guide: Consumer Edition What you need to know about the TILA-RESPA Integrated Closing Disclosures. NFM Lending NMLS # 2893 Toll-Free: 1-888-233-0092 www.nfmlending.com Introduction NFM Lending

General Resources CFPB Resources ALTA Best Practices Closing Insight Notaries Business & Commercial Loans Foreign Consumers

Remember, a knowing or reckless violation of TRID, even if done under instructions from the lender, may result in penalties of up to $1 million a day per violation against the individual settlement agent.

Remember, a knowing or reckless violation of TRID, even if done under instructions from the lender, may result in penalties of up to $1 million a day per violation against the individual settlement agent.

Changes to Mortgage Loan Closing Process

Changes to Mortgage Loan Closing Process 2015 Iowa Title Guaranty Settlement Conference Presented by: Ronette Schlatter, CRCM 1 Background Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA)

Changes to Mortgage Loan Closing Process 2015 Iowa Title Guaranty Settlement Conference Presented by: Ronette Schlatter, CRCM 1 Background Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA)

TILA-RESPA INTEGRATED MORTGAGE DISCLOSURES

TILA-RESPA INTEGRATED MORTGAGE DISCLOSURES Explaining the New Rule History Timing Purpose Coverage? Changes Definition of an Application Loan Estimate Closing Disclosure Variations/Tolerances 5 Things

TILA-RESPA INTEGRATED MORTGAGE DISCLOSURES Explaining the New Rule History Timing Purpose Coverage? Changes Definition of an Application Loan Estimate Closing Disclosure Variations/Tolerances 5 Things

Lender Company Name 2.3 Street Address, City, State, ZIP 23.2.1 Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate 0.1 DATE ISSUED 1.1 APPLICANTS 2.1 123 Anywhere Street Anytown,

Lender Company Name 2.3 Street Address, City, State, ZIP 23.2.1 Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate 0.1 DATE ISSUED 1.1 APPLICANTS 2.1 123 Anywhere Street Anytown,

Update on CFPB s TILA- RESPA Integrated Disclosure Rule

Update on CFPB s TILA- RESPA Integrated Disclosure Rule Mortgage Bankers Ruth A. Dillingham, Special Counsel First American Title Insurance Company This presentation is for informational purposes only

Update on CFPB s TILA- RESPA Integrated Disclosure Rule Mortgage Bankers Ruth A. Dillingham, Special Counsel First American Title Insurance Company This presentation is for informational purposes only

A Primer on the New CFPB Regulations Governing Residential Closings. Navigating the New Forms (Loan Estimate and Closing Disclosure.

A Primer on the New CFPB Regulations Governing Residential Closings. Navigating the New Forms (Loan Estimate and Closing Disclosure.) For loan applications received beginning October 3, 2015. Disclaimer:

A Primer on the New CFPB Regulations Governing Residential Closings. Navigating the New Forms (Loan Estimate and Closing Disclosure.) For loan applications received beginning October 3, 2015. Disclaimer:

Category: Before & After (Revised Documents)

") Category: Before & After (Revised Documents) Entry title: CFPB Loan Estimate Form Owner's organization: Consumer Financial Protection Bureau Organization type: Public sector / government Publication date:

Category: Before & After (Revised Documents) Entry title: CFPB Loan Estimate Form Owner's organization: Consumer Financial Protection Bureau Organization type: Public sector / government Publication date:

TILA-RESPA Integrated Disclosures

Outlook Live Webinar- June 17, 2014 TILA-RESPA Integrated Disclosures Presented by the Consumer Financial Protection Bureau Visit us at www.consumercomplianceoutlook.org Disclaimer The Bureau issued the

Outlook Live Webinar- June 17, 2014 TILA-RESPA Integrated Disclosures Presented by the Consumer Financial Protection Bureau Visit us at www.consumercomplianceoutlook.org Disclaimer The Bureau issued the

TABLE OF CONTENTS. SCENARIO #1 FIXED PURCHASE. Page 2. Loan Estimate.. Page 3. Closing Disclosure. Page 12. SCENARIO #2 TOLERANCE CURE Page 22

TRID CASE BOOK TABLE OF CONTENTS SCENARIO #1 FIXED PURCHASE. Page 2 Loan Estimate.. Page 3 Closing Disclosure. Page 12 SCENARIO #2 TOLERANCE CURE Page 22 SCENARIO #3 FIXED REFINANCE Page 25 Loan Estimate...

TRID CASE BOOK TABLE OF CONTENTS SCENARIO #1 FIXED PURCHASE. Page 2 Loan Estimate.. Page 3 Closing Disclosure. Page 12 SCENARIO #2 TOLERANCE CURE Page 22 SCENARIO #3 FIXED REFINANCE Page 25 Loan Estimate...

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015. Presenter: Bonnie S. Nachamie

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015 Presenter: Bonnie S. Nachamie The Closing Disclosure ( CD ) is the new form that amends, enhances and replaces the Final TIL and HUD-1 The

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015 Presenter: Bonnie S. Nachamie The Closing Disclosure ( CD ) is the new form that amends, enhances and replaces the Final TIL and HUD-1 The

CFPB Proposes New Mortgage Disclosure Rules

A DV I S O RY July 2012 On July 9, 2012, the Bureau of Consumer Financial Protection (CFPB) issued a proposed rule on mortgage disclosures (Proposed Rule) implementing requirements of the Dodd-Frank Wall

A DV I S O RY July 2012 On July 9, 2012, the Bureau of Consumer Financial Protection (CFPB) issued a proposed rule on mortgage disclosures (Proposed Rule) implementing requirements of the Dodd-Frank Wall

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate.

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate. General Information Page 1 Date Issued Date the LE is mailed or delivered

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate. General Information Page 1 Date Issued Date the LE is mailed or delivered

TRID FAQ TILA/RESPA Integrated Disclosure Frequently Asked Questions

TRID FAQ TILA/RESPA Integrated Disclosure Frequently Asked Questions 242 W. SUNSET, STE.201 SAN ANTONIO, TX 78209 210-828-5844 DOCS@BAIRDLAW.COM Table of Contents GENERAL QUESTIONS... 3 1. What is TRID?...

TRID FAQ TILA/RESPA Integrated Disclosure Frequently Asked Questions 242 W. SUNSET, STE.201 SAN ANTONIO, TX 78209 210-828-5844 DOCS@BAIRDLAW.COM Table of Contents GENERAL QUESTIONS... 3 1. What is TRID?...

Brief Walk Through of TRID. Presented by: Scott Meerstein MGIC Inside Sales

Brief Walk Through of TRID Presented by: Scott Meerstein MGIC Inside Sales The information presented in this presentation is for general information only, and is based on guidelines and practices generally

Brief Walk Through of TRID Presented by: Scott Meerstein MGIC Inside Sales The information presented in this presentation is for general information only, and is based on guidelines and practices generally

TILA/RESPA Integrated Disclosures. BRIAN A. NETTLEINGHAM Attorney/Shareholder Regulatory Compliance Group

TILA/RESPA Integrated Disclosures BRIAN A. NETTLEINGHAM Attorney/Shareholder Regulatory Compliance Group BACKGROUND Dodd-Frank Wall Street Reform Act Created the Consumer Financial Protection Bureau National

TILA/RESPA Integrated Disclosures BRIAN A. NETTLEINGHAM Attorney/Shareholder Regulatory Compliance Group BACKGROUND Dodd-Frank Wall Street Reform Act Created the Consumer Financial Protection Bureau National

Mission: to make markets for consumer financial products and services work for Americans.

TRID with Norman Roos, Robinson and Cole LLP William McCue, McCue Mortgage Company Lawrence Garfinkel, Hunt Leibert Jacobson P.C. Jeremy Potter, Norcom Mortgage Agenda Introduction Overview and Framework

TRID with Norman Roos, Robinson and Cole LLP William McCue, McCue Mortgage Company Lawrence Garfinkel, Hunt Leibert Jacobson P.C. Jeremy Potter, Norcom Mortgage Agenda Introduction Overview and Framework

Your home loan toolkit

Your home loan toolkit A step-by-step guide Consumer Financial Protection Bureau Page 1 How can this toolkit help you? Buying a home is exciting and, let s face it, complicated. This booklet is a toolkit

Your home loan toolkit A step-by-step guide Consumer Financial Protection Bureau Page 1 How can this toolkit help you? Buying a home is exciting and, let s face it, complicated. This booklet is a toolkit

MORTGAGE TERMS. Assignment of Mortgage A document used to transfer ownership of a mortgage from one party to another.

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

Loan Estimate (LE) TILA-RESPA Integrated Disclosure (TRID) Rule Requirements

TILA-RESPA Integrated Disclosure (TRID) Rule Requirements") Loan Estimate (LE) TILA-RESPA Integrated Disclosure (TRID) Rule Requirements New Definitions; New Forms New Work Flow New Rule creates new definition of Covered Loan Loan Application Consummation (Closing)

Loan Estimate (LE) TILA-RESPA Integrated Disclosure (TRID) Rule Requirements New Definitions; New Forms New Work Flow New Rule creates new definition of Covered Loan Loan Application Consummation (Closing)

January 20, 2015 Updated Changes:

Get Ready! Get Set! August 1, 2015 is Around the Corner THE COMBINED TILA AND RESPA MORTGAGE DISCLOSURES (Memo Updated on 1/27/15 to include the changes below) As most of you are probably aware, a major

Get Ready! Get Set! August 1, 2015 is Around the Corner THE COMBINED TILA AND RESPA MORTGAGE DISCLOSURES (Memo Updated on 1/27/15 to include the changes below) As most of you are probably aware, a major

TRID. What are the Timing Requirements for Revisions to a Loan Estimate?

TRID What is TRID? TRID is an acronym for TILA- RESPA Integrated Disclosure (also referred to as the TILA-RESPA Rule) and applies to most closed-end Borrower credit transactions secured by real property.

TRID What is TRID? TRID is an acronym for TILA- RESPA Integrated Disclosure (also referred to as the TILA-RESPA Rule) and applies to most closed-end Borrower credit transactions secured by real property.

The New RESPA Closing Process

The New RESPA Closing Process Presented by Thomas G. Cullen Managing Attorney Wisconsin Operations Attorneys Title Guaranty Fund, Inc. Roman Reynolds Member Services Representative Member Sales and Support

The New RESPA Closing Process Presented by Thomas G. Cullen Managing Attorney Wisconsin Operations Attorneys Title Guaranty Fund, Inc. Roman Reynolds Member Services Representative Member Sales and Support

CORRESPONDENT Compliance Manual. Instructions to Complete the TRID Loan Estimate

CORRESPONDENT Compliance Manual Instructions to Complete the TRID Loan Estimate Compliance Department 9/14/2015 2015 Impac Mortgage Corp. NMLS #128231. www.nmlsconsumeraccess.org. Rates, fees and programs

CORRESPONDENT Compliance Manual Instructions to Complete the TRID Loan Estimate Compliance Department 9/14/2015 2015 Impac Mortgage Corp. NMLS #128231. www.nmlsconsumeraccess.org. Rates, fees and programs

First Mortgage Documents User Guide 139

HUD 1 Settlement Statement Line instructions General Instructions Information and amounts may be filled in by typewriter, hand printing, computer printing, or any other method producing clear and legible

HUD 1 Settlement Statement Line instructions General Instructions Information and amounts may be filled in by typewriter, hand printing, computer printing, or any other method producing clear and legible

DISCLAIMER. Page - 1 - of 17

DISCLAIMER The information provided in this presentation and any printed material is for informational purposes only. None of the forms, materials or opinions is offered, or should be construed, as legal

DISCLAIMER The information provided in this presentation and any printed material is for informational purposes only. None of the forms, materials or opinions is offered, or should be construed, as legal

EXPLANATION OF THE HUD-1 Settlement Statement

EXPLANATION OF THE HUD-1 Settlement Statement The Settlement Statement is the financial picture of the closing. All money deposited into the escrow account and the disbursals out of the escrow account

EXPLANATION OF THE HUD-1 Settlement Statement The Settlement Statement is the financial picture of the closing. All money deposited into the escrow account and the disbursals out of the escrow account

TRID In the Weeds. Article by Alice Alvey January 2015

TRID In the Weeds Article by Alice Alvey January 2015 TRID BY ALICE ALVEY Alice Alvey It s not easy to see into the weeds of this regulation by attending a few webinars. It takes hundreds of man-hours

TRID In the Weeds Article by Alice Alvey January 2015 TRID BY ALICE ALVEY Alice Alvey It s not easy to see into the weeds of this regulation by attending a few webinars. It takes hundreds of man-hours

The Closing Disclosure

The Closing Disclosure Overview: The new TRID Regulation is effective for applications taken on October 3, 2015 and after. As a result, the GFE, TIL, and HUD-1 will no longer be issued. The Loan Estimate

The Closing Disclosure Overview: The new TRID Regulation is effective for applications taken on October 3, 2015 and after. As a result, the GFE, TIL, and HUD-1 will no longer be issued. The Loan Estimate

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS The following are instructions for completing the HUD-1 settlement statement,

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS The following are instructions for completing the HUD-1 settlement statement,

NORTH AMERICAN TITLE COMPANY Like Clockwork. www.nat.com/cfpb

NORTH AMERICAN TITLE COMPANY Like Clockwork www.nat.com/cfpb UNDERSTANDING THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE FORMS American Title, we want to make sure all of our customers have the information

NORTH AMERICAN TITLE COMPANY Like Clockwork www.nat.com/cfpb UNDERSTANDING THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE FORMS American Title, we want to make sure all of our customers have the information

TILA-RESPA Integrated Disclosure (TRID) Correspondent Division. Overview. Loan Estimate (LE) Key points. Topic The Regulation