Foreign Financial Account & Asset Reporting: FinCen (FBAR) v. FATCA

|

|

|

- Leonard Hardy

- 8 years ago

- Views:

Transcription

1 Foreign Financial Account & Asset Reporting: FinCen (FBAR) v. FATCA Presented by David J Lewis, Attorney, of Krugliak, Wilkins, Griffiths & Dougherty Co. LPA and Patricia L Gibbs, CPA, of CBIZ MHM September 2015

2 A. FinCen 114 (FBAR) AGENDA B. FATCA Form 8938 C. Offshore Voluntary Disclosure Program D. Other FATCA Considerations 2

3 . 3

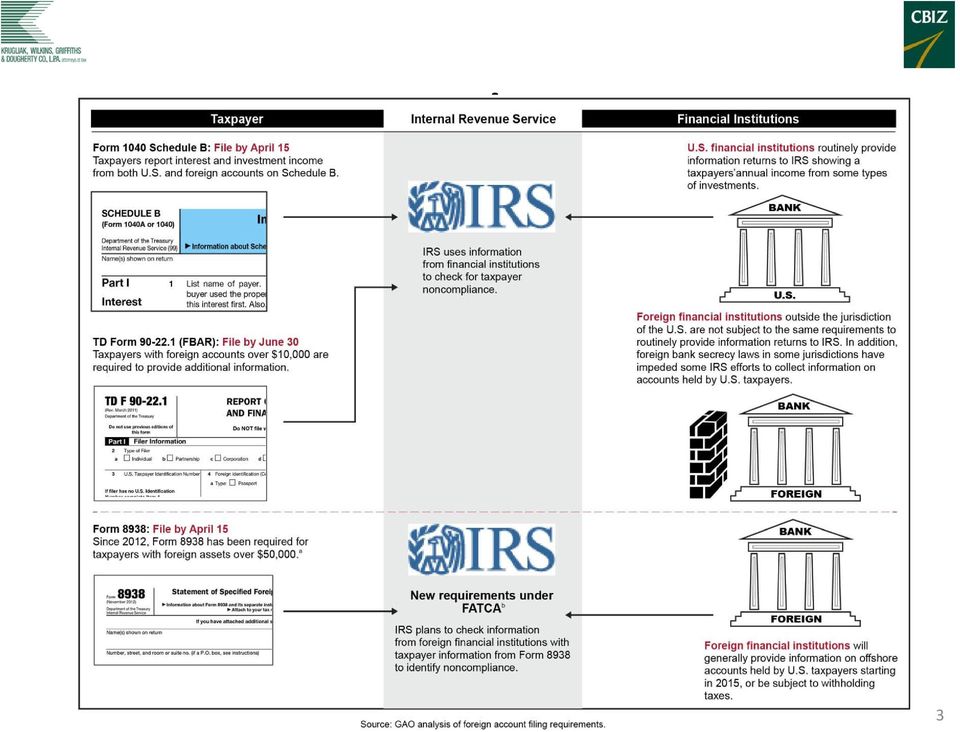

4 Report of Foreign Bank Accounts Form FinCEN 114 required under the Bank Secrecy Act which was enacted in 1970 Originally enforced by the US Treasury, since 2004, IRS has been delegated full investigatory and enforcement authority Purpose to assist IRS in identifying unreported income maintained or generated abroad and in identifying or tracing funds used for illicit purposes Filed on a calendar year basis regardless of fiscal year of U.S. person Due date is June 30 th of each year with no extensions Effective for the 2016 tax year, the due date will change to align with individual income tax returns due April 15, and to allow a six-month extension Penalties Failure to file penalty up to $10,000 If reasonable cause for failure and account is properly reported, no penalty will be imposed Willful failure to file penalty equal to greater of $100,000 or 50 percent of account balance Criminal penalties may also be assessed 4

5 Report of Foreign Bank Accounts Who must file: U.S. person with a financial interest in, or signature or other authority over one or more foreign accounts valued at more than $10,000 at any time during the calendar year In March 2011, the Treasury revised the FBAR and instructions; this included changes to the definition of signature authority US Person ( US includes US territories for FBAR purposes): A citizen or resident of the US, An entity created or organized in the United States or under the laws of the United States ( entity includes but is not limited to a corporation, partnership, and limited liability company), A trust formed under the laws of the US, or An estate formed under the laws of the US 5

6 Report of Foreign Bank Accounts Financial account: Securities, brokerage, savings, demand, checking, deposit or time deposit account maintained with a financial institution Commodities futures or options account Insurance or annuity policy with a cash value Shares in a mutual fund or similar pooled fund Any other accounts maintained in a foreign financial institution, such as foreign retirement accounts (for ex. Canadian RRSP & TFSA and Mexican individual retirement accounts) Foreign financial account: Located outside the U.S. Ownership of the financial institution is irrelevant 6

Foreign financial account: Located outside the U.S. Ownership of the financial institution is irrelevant 6")

7 Report of Foreign Bank Accounts Financial interest: Direct and indirect ownership is considered Owner of record or holder of legal title Owner of record is: An agent, nominee or attorney acting on behalf of a US person A corporation in which the U.S. person owns directly or indirectly more than 50% of the total value or voting power of all shares of stock A partnership in which the U.S. person owns directly or indirectly more than 50% of the partnership s profits or capital A trust in which the U.S. person has a greater than 50% present beneficial interest in the assets or income of the trust A trust in which the U.S. person is the grantor or has an ownership interest for Federal income tax purposes Any other greater than 50% entity 7

8 Report of Foreign Bank Accounts Exceptions to filing (FBAR instructions): Certain accounts jointly owned by spouses (see instructions for requirements) Consolidated FBARs (additional requirements in Part V) Foreign financial accounts of governmental entities International financial institutions (if the U.S. government is a member, for ex the World Bank and the IMF) IRA owners and beneficiaries Participants in and beneficiaries of tax-qualified retirement plans 8

IRA owners and beneficiaries Participants in and")

9 Report of Foreign Bank Accounts Signature Authority (including Other Authority): Authority, alone or in conjunction with another, to control the disposition of funds held in the financial account by direct communication, in writing or otherwise, with the person who maintains the account Exceptions: An officer or employee of a bank that is examined by the Office of the Comptroller of the Currency, the Board of Governors of the Federal Reserve System, the FDIC, the Office of Thrift Supervision, or the NCUA An officer or employee of a financial institution that is registered with and examined by the SEC or CFTC An officer or employee of an Authorized Service Provider (i.e., an entity that is registered with and examined by the SEC) An officer or employee of an entity that has a class of equity, securities or ADRs listed on any U.S. national securities exchange An officer or employee of a U.S. subsidiary if the US parent has a class of equity securities listed on any U.S. national securities exchange and the subsidiary is included in a consolidated FBAR of the US parent An officer or employee of an entity that has a class of equity securities or ADRs registered under section 12(g) of the Securities Exchange Act 9

An officer or employee of an entity that has a class of equity, securities or ADRs listed on any U.")

10 FATCA Overview Form

11 FATCA Form 8938 Filing Requirements For tax years beginning after March 18, 2010, specified individuals must file new Form 8938 with their income tax returns to report ownership of specified foreign financial assets if the total value of those assets exceeds an applicable threshold amount Determination of value-see form instructions and the regulations The threshold amount varies depending on the individual s residency and filing position IRS anticipates issuing regulations that will require domestic entities to file Form 8938, but to-date has only issued in proposed form Specified Individual: A US citizen A resident alien of the US for any part of the tax year A nonresident alien who makes an election to be treated as a resident alien for purposes of filing a joint income tax return A nonresident alien who is a bona fide resident of America Samoa or Puerto Rico 11

12 FATCA Form 8938 Filing Requirements (con t) Specified Foreign Financial Assets: Financial accounts maintained by a foreign financial institution The following foreign financial assets if they are held for investment and not held in an account maintained by a financial institution: Stock or securities issued by someone that is not a US person, Any interest in a foreign entity, and Any financial instrument or contract that has an issuer or counterparty that is not a US person Financial accounts maintained by a US payer are exempt. Financial accounts maintained by a dealer or trader in securities or commodities are exempt if all of the holdings in the account are subject to the mark-to-market accounting rules or an election under IRC 475(e) is made to treat the holdings as such. 12

13 FATCA Form 8938 Reporting Duplicate Information Individuals do not have to report a specified foreign financial asset on Form 8938 if they report it on one or more forms timely filed with the IRS for the same tax year. For example: Form 5471 Form 8621 Form 8865 Form 3520 The individual is still required to file Form however they only need to list the form(s) on which the specified foreign financial asset was reported. 13

14 FATCA Form 8938 Filing Requirements (con t) Interest in Specified Foreign Financial Assets Individuals have an interest in a specified foreign financial asset if any income, gains, losses, deductions, credits, gross proceeds, or distribution from holding or disposing of the asset are or would be required to be reported, included or otherwise reflected on their income tax return. Interests held by disregarded entities if the individual is the owner of a disregarded entity, they have an interest in any specified foreign financial asset owned by the disregarded entity. Interests in assets held in financial accounts if the individual has an interest in a financial account that holds specified foreign financial assets, they do not have to report the assets held in the account. 14

15 FATCA Form 8938 Individual Filing Thresholds The filing threshold is based on the taxpayers filing status: Filing Status Value* on the last day of the tax year is at least: Or, at any time during the year, the value is greater than: Unmarried taxpayers, living in the US 50,000 75,000 Married taxpayers filing jointly, living in the US Married taxpayers filing separately, living in the US Taxpayers not filing a joint return, living abroad** 100, ,000 50,000 75, , ,000 Taxpayers filing jointly, living abroad 400, ,000 * Fair market value translated using US Treasury Financial Management Service rate for December 31 **Living abroad means bona fide residents of a foreign country or individuals present in foreign countries for 330 full days during a 12 month time period 15

16 FATCA Form 8938 Penalties Failure to File Penalty $10,000 penalty for not filing a correct Form 8938 by due date (including extensions) Additional penalties (up to maximum of $50,000) may be assessed if the individual receives a notice of failure to file and does not comply Reasonable cause exception applies Accuracy-Related Penalty Fraud Criminal Penalties could also be assessed 16

17 Comparison Chart Form 8938 v FBAR and-fbar-requirements 17

18 Form 8938 and Offshore Voluntary Disclosure Program FATCA s efforts are aimed at foreign financial institutions, requesting cooperation to prevent tax evasion by U.S. taxpayers Alternatively, the Offshore Voluntary Disclosure Program (OVDP) focuses its efforts on taxpayers, allowing them to come forward and report undeclared foreign income and assets Participation in the OVDP requires taxpayers to produce relevant foreign financial documentation and forms, including Form OVDP FAQ 7, 25 IGAs (Intergovernmental Government Agreements) will cause disclosure of foreign financial information to the IRS, with or without taxpayer cooperation. Thus, taxpayers may be encouraged to participate in the OVDP, in an effort to avoid foreign reporting penalties. 18

will cause disclosure of foreign financial information to the IRS, with or without taxpayer cooperation.")

19 Offshore Voluntary Disclosure Program What is OVDP? Amended Forms 1040 for the prior eight years for which non-compliance has occurred. FinCEN Form 114 Pay additional tax on amended Forms 1040, interest, 20 percent accuracy penalty on understated tax, and high-water mark on value of previously unreported foreign accounts and other assets that generated income for which there was no compliance at 27.5 percent. Closing agreement and complete taxpayer cooperation. Closing agreement expresses government s agreement not to prosecute for related non-compliance Only available for legal income cases No prior IRS contact nor investigation regarding taxpayer s non-compliance IRS reserves the right to close program at any time For additional information see the OVDP FAQs at Voluntary-Disclosure-Program-Frequently-Asked-Questions-and-Answers 19

20 Streamlined Filing Compliance Procedure On September 1, 2012, the IRS launched its Streamlined Procedure to allow non-u.s. taxpayers who failed to report foreign financial assets, not a result of willful conduct, to file/amend delinquent reports and resolve tax and penalty obligations. On July 1, 2014 changes occurred to the program including: Extension of eligibility to U.S. taxpayers residing in the United States; Elimination of the $1,500 tax threshold; and Elimination of the risk assessment processes associated with the streamlined filing compliance announced in

21 Streamlined Filing Compliance Procedure Requirements: Taxpayers wanting to participate in the Streamlined Program must sign statements, under penalties of perjury, stating in part that:» My failure to report all income, pay all tax, and submit all required information returns, including FBARs, was due to non-willful conduct.» I understand that non-willful conduct is conduct that is due to negligence, inadvertence, or mistake or conduct that is the result of a good faith misunderstanding of the requirements of the law. I recognize that if the Internal Revenue Service receives or discovers evidence of willfulness, fraud, or criminal conduct, it may open an examination or investigation that could lead to civil fraud penalties, FBAR penalties, information return penalties, or even referral to Criminal Investigation. In addition to this statement, taxpayers must provide specific reasons for their failure to report all income, pay all tax, and submit all required information returns, including FBARs. Streamlined Program requires the filing of amended tax returns for the past 3 years reporting all foreign sourced and domestic sourced income and required information returns including Form 8938 for years 2010 through 2012; Additionally, participants must submit FBARs for the past 6 years; The only penalty under the Streamlined Program is the miscellaneous offshore penalty equal to 5 percent of the foreign financial assets that gave rise to the tax compliance issue all income tax related penalties associated with the foreign source income will be waived; But, the Streamlined Program does not limit the civil penalties otherwise associated with the reporting of U.S. source income. The 5 percent offshore penalty only resolves liabilities and penalties related to foreign noncompliance domestic portions of a voluntary disclosure are subject to examination; and The Streamlined Program does not provide protection against a possible criminal investigation and its resulting consequences including possible imprisonment, payment of back taxes and interest, and civil penalties. 21

22 Voluntary Disclosure Summary With rapidly expanding lists of IGA countries, IRS access to foreign account information is the new reality As a return preparer or tax adviser, have your firm s standards expanded to ask enough information and proactively raise the issue of reporting foreign assets? Going forward, tax preparers need to be aware of the possible preparer liability in connection to foreign financial reporting (Treasury Circular 230) 22

23 Miscellaneous: Trusts as FFIs In the current Regulations, financial institutions are defined to include, among other entities, any non-u.s. entity that acts as an investment entity. An investment entity is defined as an entity: that trades in financial instruments, manages individual or collective portfolios, or otherwise invests, administers, or manages financial assets on behalf of others; that invests or trades in financial assets and is managed by an investment adviser, depository institution, custodial institution or insurance company; and that functions as a collective investment vehicle, mutual fund, exchange traded fund, private equity fund, hedge fund, venture capital fund, leveraged buyout fund or any similar investment vehicle. Treas. Reg (e)(1) and (4) 23

24 Miscellaneous: Trusts as FFIs Based on this broad concept of investment entity, many tax advisers are warning that trusts and private investment companies could be considered financial institutions under FATCA Consequently, taxpayers who are service providers or managers of foreign trusts or private investment companies need to be aware of the FATCA registration and reporting requirements 24

25 Contact Information Patricia L. Gibbs, CPA CBIZ MHM 4040 Embassy Parkway, Suite 100 Akron, OH Direct Dial: David J. Lewis, Esq. Krugliak, Wilkins, Griffiths & Dougherty Co., LPA 50 South Main Street, Suite 501 Akron, OH Direct Dial:

26 The End! Questions??? Comments??? Thunderous Applause??? 26

Are You Ready For New Form 8938 to Report Specified Foreign Financial Assets?

Are You Ready For New Form 8938 to Report Specified Foreign Financial Assets? The Hiring Incentives to Restore Employment ( HIRE ) Act, signed into law in 2010, included modified provisions of the previously

Are You Ready For New Form 8938 to Report Specified Foreign Financial Assets? The Hiring Incentives to Restore Employment ( HIRE ) Act, signed into law in 2010, included modified provisions of the previously

Instructions for Form 8938

2015 Instructions for Form 8938 Statement of Specified Foreign Financial Assets Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise

2015 Instructions for Form 8938 Statement of Specified Foreign Financial Assets Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise

Instructions for Form 8938 (Rev. December 2014)

") Instructions for Form 8938 (Rev. December 2014) Statement of Specified Foreign Financial Assets Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

Instructions for Form 8938 (Rev. December 2014) Statement of Specified Foreign Financial Assets Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

Long Awaited Guidance Concerning Foreign Bank Account ( FBAR ) Filing Requirements Released

Filing Requirements Released") Long Awaited Guidance Concerning Foreign Bank Account ( FBAR ) Filing Requirements Released This past week, the Treasury Department s Financial Crimes Enforcement Network (FinCEN) released proposed changes

Long Awaited Guidance Concerning Foreign Bank Account ( FBAR ) Filing Requirements Released This past week, the Treasury Department s Financial Crimes Enforcement Network (FinCEN) released proposed changes

Radio X June 19 Broadcast Foreign Asset Reporting Questions & Answers

Radio X June 19 Broadcast Foreign Asset Reporting Questions & Answers 1. What is the FBAR filing? FBAR is the acronym for the Foreign Bank Account Report that must be filed annually with the IRS to report

Radio X June 19 Broadcast Foreign Asset Reporting Questions & Answers 1. What is the FBAR filing? FBAR is the acronym for the Foreign Bank Account Report that must be filed annually with the IRS to report

Foreign Bank Account Reports (FBAR)

") Foreign Bank Account Reports (FBAR) Peter Trieu, Esq., LLM and Company 101 Second Street, Ste. 1200 San Francisco, CA 94105 415-433-1177 ptrieu@rowbotham.com Reporting Requirement U.S. persons holding

Foreign Bank Account Reports (FBAR) Peter Trieu, Esq., LLM and Company 101 Second Street, Ste. 1200 San Francisco, CA 94105 415-433-1177 ptrieu@rowbotham.com Reporting Requirement U.S. persons holding

TD F 90-22.1 (Rev. January 2012) Department of the Treasury

Department of the Treasury") TD F 90-22.1 (Rev. January 2012) Department of the Treasury REPORT OF FOREIGN BANK AND FINANCIAL ACCOUNTS OMB No. 1545-2038 1 This Report is for Calendar Year Ended 12/31 Do not use previous editions of

TD F 90-22.1 (Rev. January 2012) Department of the Treasury REPORT OF FOREIGN BANK AND FINANCIAL ACCOUNTS OMB No. 1545-2038 1 This Report is for Calendar Year Ended 12/31 Do not use previous editions of

US Taxpayers Participating in Non US Retirement Plans: When is There an FBAR or FATCA Reporting Obligation?

February 29, 2012 Authors: Anubhav Gogna and David W. Powell If you have questions, please contact your regular Groom attorney or any of the attorneys listed below: Anubhav Gogna agogna@groom.com (202)

February 29, 2012 Authors: Anubhav Gogna and David W. Powell If you have questions, please contact your regular Groom attorney or any of the attorneys listed below: Anubhav Gogna agogna@groom.com (202)

INTERNATIONAL TIDBIT: Reporting Foreign Investments New Requirements for the 2013 Tax Year

INTERNATIONAL TIDBIT: Reporting Foreign Investments New Requirements for the 2013 Tax Year The last few years have seen increased emphasis on individuals reporting about their foreign investments and penalizing

INTERNATIONAL TIDBIT: Reporting Foreign Investments New Requirements for the 2013 Tax Year The last few years have seen increased emphasis on individuals reporting about their foreign investments and penalizing

Report of Foreign Bank and Financial Accounts (FBAR)

") Report of Foreign Bank and Financial Accounts (FBAR) Presenter s name Date Objectives FBAR purpose FBAR reporting / recordkeeping FBAR penalties Compliance initiatives 2 FBAR Purpose Combat the use of

Report of Foreign Bank and Financial Accounts (FBAR) Presenter s name Date Objectives FBAR purpose FBAR reporting / recordkeeping FBAR penalties Compliance initiatives 2 FBAR Purpose Combat the use of

FOREIGN INCOME, ASSETS, AND IRS AMNESTY PROGRAMS

FOREIGN INCOME, ASSETS, AND IRS AMNESTY PROGRAMS Ahuja & Clark, PLLC By: Madhu Ahuja, CPA, CVA, CFE Ravi Modi, CPA www.ahujaclark.com WHO IS SUBJECT TO TAX FILING REQUIREMENTS? U.S. Citizen and Green Card

FOREIGN INCOME, ASSETS, AND IRS AMNESTY PROGRAMS Ahuja & Clark, PLLC By: Madhu Ahuja, CPA, CVA, CFE Ravi Modi, CPA www.ahujaclark.com WHO IS SUBJECT TO TAX FILING REQUIREMENTS? U.S. Citizen and Green Card

FBAR Background. Reporting Foreign Financial Accounts on the Electronic FBAR

FBAR Background Reporting Foreign Financial Accounts on the Electronic FBAR ROD LUNDQUIST, SENIOR POLICY ANALYST SMALL BUSINESS/SELF-EMPLOYED June 4, 2014 Bank Secrecy Act enacted in 1970 Codified primarily

FBAR Background Reporting Foreign Financial Accounts on the Electronic FBAR ROD LUNDQUIST, SENIOR POLICY ANALYST SMALL BUSINESS/SELF-EMPLOYED June 4, 2014 Bank Secrecy Act enacted in 1970 Codified primarily

compensatory partnership and LLC interests in a non-u.s. entity.

FATCA COMPENSATION REPORTING: NEW RULES MAY REQUIRE REPORTING OF NON-U.S. SOURCED COMPENSATION TO THE IRS March 22, 2012 To Our Clients and Friends: In an effort to shake out hidden assets and prevent

FATCA COMPENSATION REPORTING: NEW RULES MAY REQUIRE REPORTING OF NON-U.S. SOURCED COMPENSATION TO THE IRS March 22, 2012 To Our Clients and Friends: In an effort to shake out hidden assets and prevent

Foreign Account Tax Compliance Act ("FATCA")

") Required Form Who Must File? Does the United States include U.S. territories? Reporting Threshold (Total Value of Assets) When do you have an interest in an account or asset? Foreign Account Tax Compliance

Required Form Who Must File? Does the United States include U.S. territories? Reporting Threshold (Total Value of Assets) When do you have an interest in an account or asset? Foreign Account Tax Compliance

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA

March 2015 CONTENTS U.S. income tax filing requirements Non-filers U.S. foreign reporting requirements Foreign trusts Foreign corporations Foreign partnerships U.S. Social Security U.S. estate tax U.S.

March 2015 CONTENTS U.S. income tax filing requirements Non-filers U.S. foreign reporting requirements Foreign trusts Foreign corporations Foreign partnerships U.S. Social Security U.S. estate tax U.S.

New Year brings new US Reporting requirement introducing Form 8938 Statement of Specified Foreign Financial Assets

New Year brings new US Reporting requirement introducing Form 8938 Statement of Specified Foreign Financial Assets Arthur J. Dichter Cantor & Webb P.A., Miami FL The following article gives an overview

New Year brings new US Reporting requirement introducing Form 8938 Statement of Specified Foreign Financial Assets Arthur J. Dichter Cantor & Webb P.A., Miami FL The following article gives an overview

What s News in Tax Analysis That Matters from Washington National Tax

What s News in Tax Analysis That Matters from Washington National Tax Have Undisclosed Foreign Assets? IRS Offers Options There is good news for individuals who inadvertently failed to fulfill tax and

What s News in Tax Analysis That Matters from Washington National Tax Have Undisclosed Foreign Assets? IRS Offers Options There is good news for individuals who inadvertently failed to fulfill tax and

Daily Tax Report. N ew rules requiring reporting of specified foreign. FBAR and FATCA Foreign Financial Assets Reporting: Seeing Double?

Daily Tax Report NUMBER 246 DECEMBER 22, 2011 FBAR and : Seeing Double? Not Really BY CHARLES M. BRUCE N ew rules requiring reporting of specified foreign financial assets were enacted in March 2010 and

Daily Tax Report NUMBER 246 DECEMBER 22, 2011 FBAR and : Seeing Double? Not Really BY CHARLES M. BRUCE N ew rules requiring reporting of specified foreign financial assets were enacted in March 2010 and

Handling IRS Targeted Audits, Voluntary Disclosures and Reporting Foreign Assets. Presentation Roadmap

Handling IRS Targeted Audits, Voluntary Disclosures and Reporting Foreign Assets Elizabeth Copeland 210.250.6121 elizabeth.copeland@strasburger.com Farley Katz 210.250.6007 farley.katz@strasburger.com

Handling IRS Targeted Audits, Voluntary Disclosures and Reporting Foreign Assets Elizabeth Copeland 210.250.6121 elizabeth.copeland@strasburger.com Farley Katz 210.250.6007 farley.katz@strasburger.com

The I.R.S. Amnesty Program & The New Streamlined Filing Compliance Procedures

TOPICS IN THE SEMINAR INCLUDE: The I.R.S. Amnesty Program & The New Streamlined Filing Compliance Procedures By Richard S. Lehman, Esq. TAX ATTORNEY www.lehmantaxlaw.com SEMINAR INTRODUCTION by Richard

TOPICS IN THE SEMINAR INCLUDE: The I.R.S. Amnesty Program & The New Streamlined Filing Compliance Procedures By Richard S. Lehman, Esq. TAX ATTORNEY www.lehmantaxlaw.com SEMINAR INTRODUCTION by Richard

Top 10 Foreign Bank Account Reporting (FBAR) Mistakes (And How to Fix Them)

Mistakes (And How to Fix Them)") Latham & Watkins Tax Controversy Practice June 2, 2015 Number 1839 Top 10 Foreign Bank Account Reporting (FBAR) Mistakes (And How to Fix Them) While FBAR reporting rules are frequently misunderstood, US

Latham & Watkins Tax Controversy Practice June 2, 2015 Number 1839 Top 10 Foreign Bank Account Reporting (FBAR) Mistakes (And How to Fix Them) While FBAR reporting rules are frequently misunderstood, US

US Tax Issues for Canadian Residents

US Tax Issues for Canadian Residents SPECIAL REPORT US Tax Issues for Canadian Residents The IRS has recently declared new catch up filing procedures for non-resident US taxpayers who are considered innocent

US Tax Issues for Canadian Residents SPECIAL REPORT US Tax Issues for Canadian Residents The IRS has recently declared new catch up filing procedures for non-resident US taxpayers who are considered innocent

Reporting Cash Transactions and Foreign Financial Accounts (Foreign Bank Account Reports "FBAR")

") Reporting Cash Transactions and Foreign Financial Accounts (Foreign Bank Account Reports "FBAR") Form 8300 - Reporting Cash Payments Over $10,000 in a Trade or Business Reportable transactions include,

Reporting Cash Transactions and Foreign Financial Accounts (Foreign Bank Account Reports "FBAR") Form 8300 - Reporting Cash Payments Over $10,000 in a Trade or Business Reportable transactions include,

Offshore#Banking#and#Foreign#Bank#Accounts: Keeping#your#Clients#out#of#Trouble#with#the#IRS

Moving#Your#Practice#in#the#Right#Direction# TM Offshore#Banking#and#Foreign#Bank#Accounts: Keeping#your#Clients#out#of#Trouble#with#the#IRS A"Practice"Essentials"Presentation #2011#OnePath#Practice#Management#Advisors,#LLC.#All#Rights#Reserved.

Moving#Your#Practice#in#the#Right#Direction# TM Offshore#Banking#and#Foreign#Bank#Accounts: Keeping#your#Clients#out#of#Trouble#with#the#IRS A"Practice"Essentials"Presentation #2011#OnePath#Practice#Management#Advisors,#LLC.#All#Rights#Reserved.

US Voluntary Disclosure

what you need to know, and how we can help www.withersworldwide.com Introduction Countries throughout the world have committed to redefining banking secrecy laws so as to no longer protect any form of

what you need to know, and how we can help www.withersworldwide.com Introduction Countries throughout the world have committed to redefining banking secrecy laws so as to no longer protect any form of

Reporting Foreign Assets and Offshore Accounts

Reporting Foreign Assets and Offshore Accounts ( and Form 8938) Commissioner Shulman (June 2009) For individuals with overseas income and assets, it s much more straightforward. If you are a U.S. taxpayer

Reporting Foreign Assets and Offshore Accounts ( and Form 8938) Commissioner Shulman (June 2009) For individuals with overseas income and assets, it s much more straightforward. If you are a U.S. taxpayer

Overview of 2011 IRS Offshore Voluntary Disclosure Initiative

Overview of 2011 IRS Offshore Voluntary Disclosure Initiative Attorney Morris N. Robinson, CPA, LLM M. Robinson & Company MassTaxLawyers.com 160 Federal Street Boston, MA 02110 617/ 428-6900 1 M. Robinson

Overview of 2011 IRS Offshore Voluntary Disclosure Initiative Attorney Morris N. Robinson, CPA, LLM M. Robinson & Company MassTaxLawyers.com 160 Federal Street Boston, MA 02110 617/ 428-6900 1 M. Robinson

FBAR Foreign Bank Account Reporting

FBAR Foreign Bank Account Reporting ------------------------------------------------------------------------------------------------------------ Form TD F 90-22.1 is required when a U.S. Person has a financial

FBAR Foreign Bank Account Reporting ------------------------------------------------------------------------------------------------------------ Form TD F 90-22.1 is required when a U.S. Person has a financial

Reporting Requirements for Foreign Financial Accounts

Reporting Requirements for Foreign Financial Accounts Proposed FinCEN Regulations and IRS Guidance On Foreign Bank and Financial Account Reporting SUMMARY On February 26, the IRS issued Notice 2010-23

Reporting Requirements for Foreign Financial Accounts Proposed FinCEN Regulations and IRS Guidance On Foreign Bank and Financial Account Reporting SUMMARY On February 26, the IRS issued Notice 2010-23

Increased IRS Tax Compliance Involving U.S. Citizens/Green Card Holders in Israel

Increased IRS Tax Compliance Involving U.S. Citizens/Green Card Holders in Israel October 2012 Tax Seminar Stuart M. Schabes, Esquire Ober, Kaler, Grimes & Shriver smschabes@ober.com 410-347-7696 (U.S.)

Increased IRS Tax Compliance Involving U.S. Citizens/Green Card Holders in Israel October 2012 Tax Seminar Stuart M. Schabes, Esquire Ober, Kaler, Grimes & Shriver smschabes@ober.com 410-347-7696 (U.S.)

US FATCA FAQ and Glossary of FATCA terms

US FATCA FAQ and Glossary of FATCA terms These FAQs are intended to aid you in your understanding how FATCA affects your relationship with UBS. This is not intended as tax advice. If you are uncertain

US FATCA FAQ and Glossary of FATCA terms These FAQs are intended to aid you in your understanding how FATCA affects your relationship with UBS. This is not intended as tax advice. If you are uncertain

Presentation by Jennifer Coates for the American Immigration Lawyers Association

Tax Issues for Non- Citizens What Immigration Lawyers Need to Know Presentation by Jennifer Coates for the American Immigration Lawyers Association Principal, Jenny Coates Law, PLLC Seattle and Bainbridge,

Tax Issues for Non- Citizens What Immigration Lawyers Need to Know Presentation by Jennifer Coates for the American Immigration Lawyers Association Principal, Jenny Coates Law, PLLC Seattle and Bainbridge,

FBAR s: 2011 Final (BSA) Regulations and How they apply to Protectors, Directors and other Powerholders

Regulations and How they apply to Protectors, Directors and other Powerholders") FBAR s: 2011 Final (BSA) Regulations and How they apply to Protectors, Directors and other Powerholders STEP Miami Branch One Day Conference Friday, June 10, 2011 Conrad Hotel, Miami, FL Stewart L. Kasner

FBAR s: 2011 Final (BSA) Regulations and How they apply to Protectors, Directors and other Powerholders STEP Miami Branch One Day Conference Friday, June 10, 2011 Conrad Hotel, Miami, FL Stewart L. Kasner

FATCA FAQs: Frequently asked questions on the Foreign Account Tax Compliance

www.pwc.com/us/fatca July 2011 FATCA FAQs: Frequently asked questions on the Foreign Account Tax Compliance Act 1. What is FATCA? FATCA is an acronym for The Foreign Account Tax Compliance Act (FATCA)

www.pwc.com/us/fatca July 2011 FATCA FAQs: Frequently asked questions on the Foreign Account Tax Compliance Act 1. What is FATCA? FATCA is an acronym for The Foreign Account Tax Compliance Act (FATCA)

INTERNATIONAL TAX COMPLIANCE FOR GOVERNMENT CONTRACTORS

INTERNATIONAL TAX COMPLIANCE FOR GOVERNMENT CONTRACTORS Mark T. Gossart Alison N. Dougherty September 26, 2012 2012 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland 20850 301.231.6200

INTERNATIONAL TAX COMPLIANCE FOR GOVERNMENT CONTRACTORS Mark T. Gossart Alison N. Dougherty September 26, 2012 2012 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland 20850 301.231.6200

Farmers and Foreign Accounts

Farmers and Foreign Accounts Marc Lovell Tax School and Department of Agricultural and Consumer Economics University of Illinois August 9, 04 farmdoc daily (4):65 Recommended citation format: Lovell, M.

Farmers and Foreign Accounts Marc Lovell Tax School and Department of Agricultural and Consumer Economics University of Illinois August 9, 04 farmdoc daily (4):65 Recommended citation format: Lovell, M.

FATCA AND NEW ZEALAND LAW FIRMS

This Practice Briefing does not constitute legal advice INTRODUCTION The FATCA agreement between New Zealand and United States is directed at reducing tax evasion by US taxpayers. New Zealand law firms

This Practice Briefing does not constitute legal advice INTRODUCTION The FATCA agreement between New Zealand and United States is directed at reducing tax evasion by US taxpayers. New Zealand law firms

Nuts & Bolts of Cross Border Tax Issues

Nuts & Bolts of Cross Border Tax Issues Central Arizona Estate Planning Council November 2, 2015 Presented by: Certified Public Accountant Attorney at Law 1 Overview What is an International Tax Practice?

Nuts & Bolts of Cross Border Tax Issues Central Arizona Estate Planning Council November 2, 2015 Presented by: Certified Public Accountant Attorney at Law 1 Overview What is an International Tax Practice?

Your Taxes: IRS grants 3-week extension for its tax-amnesty program

Your Taxes: IRS grants 3-week extension for its tax-amnesty program Sep. 22, 2009 KEVIN E. PACKMAN and LEON HARRIS, THE JERUSALEM POST This article is an urgent update for US taxpayers... and it comes

Your Taxes: IRS grants 3-week extension for its tax-amnesty program Sep. 22, 2009 KEVIN E. PACKMAN and LEON HARRIS, THE JERUSALEM POST This article is an urgent update for US taxpayers... and it comes

INTERNATIONAL TAX CONTROVERSY

INTERNATIONAL TAX CONTROVERSY BY MISHKIN SANTA PETER MITCHELL About Us Who we are What we do Why we re here Part I: International Tax Controversy Voluntary Disclosure Attorney-client privilege IRM 9.5.11.9

INTERNATIONAL TAX CONTROVERSY BY MISHKIN SANTA PETER MITCHELL About Us Who we are What we do Why we re here Part I: International Tax Controversy Voluntary Disclosure Attorney-client privilege IRM 9.5.11.9

Dispelling Fear! What are your fears?! - Criminal implications! - Cost of penalties! - Cost of getting compliant with advisors!

Dispelling Fear! What are your fears?! - Criminal implications! - Cost of penalties! - Cost of getting compliant with advisors! Do not fear the consequences, get the facts:! Each Individual is unique!

Dispelling Fear! What are your fears?! - Criminal implications! - Cost of penalties! - Cost of getting compliant with advisors! Do not fear the consequences, get the facts:! Each Individual is unique!

8 THINGS YOU MUST KNOW BEFORE THE IRS CALLS YOU

8 THINGS YOU MUST KNOW BEFORE THE IRS CALLS YOU Contact Us Today to Schedule a Free Consultation. Call 866-784-0023 or visit www.mlhorwitzlaw.com 8 Things You Must Know Before the IRS Calls You What is

8 THINGS YOU MUST KNOW BEFORE THE IRS CALLS YOU Contact Us Today to Schedule a Free Consultation. Call 866-784-0023 or visit www.mlhorwitzlaw.com 8 Things You Must Know Before the IRS Calls You What is

FOREIGN BANK ACCOUNT REPORTING (FBAR) UPDATE CORE LAWYER WORKING GROUP SUMMER 2010. Caring For Those Who Serve

UPDATE CORE LAWYER WORKING GROUP SUMMER 2010. Caring For Those Who Serve") FOREIGN BANK ACCOUNT REPORTING (FBAR) UPDATE CORE LAWYER WORKING GROUP SUMMER 2010 Caring For Those Who Serve Reminder: What is FBAR? The Report of Foreign Bank and Financial Accounts ( FBAR ), Treasury

FOREIGN BANK ACCOUNT REPORTING (FBAR) UPDATE CORE LAWYER WORKING GROUP SUMMER 2010 Caring For Those Who Serve Reminder: What is FBAR? The Report of Foreign Bank and Financial Accounts ( FBAR ), Treasury

Simplified Instructions for Completing a Form W-8BEN-E

Simplified Instructions for Completing a Form W-8BEN-E For Non-Financial Institutions Only Updated April 2015 Circular 230 Disclaimer: Any tax advice contained in this communication is not intended or

Simplified Instructions for Completing a Form W-8BEN-E For Non-Financial Institutions Only Updated April 2015 Circular 230 Disclaimer: Any tax advice contained in this communication is not intended or

1 of 14 9/18/2014 2:20 PM

Internal Revenue Manual - 4.26.16 Report of Foreign Bank and Financia... Part 4. Examining Process Chapter 26. Bank Secrecy Act Section 16. Report of Foreign Bank and Financial Accounts (FBAR) 4.26.16

Internal Revenue Manual - 4.26.16 Report of Foreign Bank and Financia... Part 4. Examining Process Chapter 26. Bank Secrecy Act Section 16. Report of Foreign Bank and Financial Accounts (FBAR) 4.26.16

Human Resource Services Webcast

Human Resource Services Webcast Foreign reporting requirements in Canada and the US: What s new and why you need to comply Administrative information 60 minute webcast Audio with slides For a better viewing

Human Resource Services Webcast Foreign reporting requirements in Canada and the US: What s new and why you need to comply Administrative information 60 minute webcast Audio with slides For a better viewing

Correcting IRS Income Tax and Foreign Asset Reporting Problems

Correcting IRS Income Tax and Foreign Asset Reporting Problems D. Sean McMahon, JD, LLM Boston, Massachusetts www.mcmahontaxlaw.com D. Sean McMahon Former Senior Attorney with the IRS Office of Chief Counsel

Correcting IRS Income Tax and Foreign Asset Reporting Problems D. Sean McMahon, JD, LLM Boston, Massachusetts www.mcmahontaxlaw.com D. Sean McMahon Former Senior Attorney with the IRS Office of Chief Counsel

US Citizens Living in Canada

US Citizens Living in Canada Income Tax Considerations 1) I am a US citizen living in Canada. What are my income tax filing and reporting requirements? US Income Tax Returns A US citizen residing in Canada

US Citizens Living in Canada Income Tax Considerations 1) I am a US citizen living in Canada. What are my income tax filing and reporting requirements? US Income Tax Returns A US citizen residing in Canada

The Foreign Account Tax Compliance Act (FATCA)

") The Foreign Account Tax Compliance Act (FATCA) I. OVERVIEW A. What is FATCA? FATCA, as it is colloquially known, refers to Chapter 4 of the US Internal Revenue Code, which was enacted by the Hiring Incentives

The Foreign Account Tax Compliance Act (FATCA) I. OVERVIEW A. What is FATCA? FATCA, as it is colloquially known, refers to Chapter 4 of the US Internal Revenue Code, which was enacted by the Hiring Incentives

The New Duty to Report Foreign Financial Assets on Form 8938: Demystifying the Complex Rules and Severe Consequences of Noncompliance

The New Duty to Report Foreign Financial Assets on Form 8938: Demystifying the Complex Rules and Severe Consequences of ncompliance May June 2012 By Hale E. Sheppard Hale E. Sheppard, J.D., LL.M., LL.M.T.,

The New Duty to Report Foreign Financial Assets on Form 8938: Demystifying the Complex Rules and Severe Consequences of ncompliance May June 2012 By Hale E. Sheppard Hale E. Sheppard, J.D., LL.M., LL.M.T.,

Foreign Account Tax Compliance Act (FATCA)

") Foreign Account Tax Compliance Act (FATCA) Introduction As a global financial services organisation, it is necessary for Standard Bank to comply with the laws and regulations of many different authorities,

Foreign Account Tax Compliance Act (FATCA) Introduction As a global financial services organisation, it is necessary for Standard Bank to comply with the laws and regulations of many different authorities,

international tax issues and reporting requirements

international tax issues and reporting requirements Foreign income exclusions and foreign tax credits can significantly reduce the taxes you pay on foreign sourced income and help you avoid double taxation.

international tax issues and reporting requirements Foreign income exclusions and foreign tax credits can significantly reduce the taxes you pay on foreign sourced income and help you avoid double taxation.

BSA Electronic Filing Requirements For Report of Foreign Bank and Financial Accounts (FinCEN Form 114)

") Financial Crimes Enforcement Network BSA Electronic Filing Requirements For Report of Foreign Bank and Financial Accounts (FinCEN Form 114) Release Date June 2014 (v1.3) Effective October 2013 for the

Financial Crimes Enforcement Network BSA Electronic Filing Requirements For Report of Foreign Bank and Financial Accounts (FinCEN Form 114) Release Date June 2014 (v1.3) Effective October 2013 for the

American Bar Association Section of Family Law 2014 Spring CLE Conference PLENARY:

American Bar Association Section of Family Law 2014 Spring CLE Conference PLENARY: How to Find Your Spouse s Secret Offshore Bank Account: Using U.S. Tax Reporting Requirements as a Discovery Tool for

American Bar Association Section of Family Law 2014 Spring CLE Conference PLENARY: How to Find Your Spouse s Secret Offshore Bank Account: Using U.S. Tax Reporting Requirements as a Discovery Tool for

Tax Management International Journal

Tax Management International Journal Reproduced with permission from Tax Management International Journal, 43 TMIJ 604, 10/10/2014. Copyright 2014 by The Bureau of National Affairs, Inc. (800-372- 1033)

Tax Management International Journal Reproduced with permission from Tax Management International Journal, 43 TMIJ 604, 10/10/2014. Copyright 2014 by The Bureau of National Affairs, Inc. (800-372- 1033)

Corrective U.S. Tax Compliance for Dual Status and Foreign Taxpayers Andrew Bernknopf, Esq., Member:

Corrective U.S. Tax Compliance for Dual Status and Foreign Taxpayers Andrew Bernknopf, Esq., Member: This article provides an overview of corrective United States tax compliance measures for individuals

Corrective U.S. Tax Compliance for Dual Status and Foreign Taxpayers Andrew Bernknopf, Esq., Member: This article provides an overview of corrective United States tax compliance measures for individuals

Foreign Account Tax Compliance Act ( FATCA ) How Does It Affect NFFEs and Individuals

How Does It Affect NFFEs and Individuals") Foreign Account Tax Compliance Act ( FATCA ) How Does It Affect NFFEs and Individuals May, 2012 2008 Venable LLP 1 agenda Overview FATCA and NFFEs FATCA and Individuals US Information Reporting for US

Foreign Account Tax Compliance Act ( FATCA ) How Does It Affect NFFEs and Individuals May, 2012 2008 Venable LLP 1 agenda Overview FATCA and NFFEs FATCA and Individuals US Information Reporting for US

The Foreign Bank Account Bomb How to Defuse It

THE LAW FIRM OF BOVE & LANGA A PROFESSIONAL CORPORATION TEN TREMONT STREET, SUITE 600 BOSTON, MASSACHUSETTS 02108 Telephone: 617.720.6040 Facsimile: 617.720.1919 www.bovelanga.com The Foreign Bank Account

THE LAW FIRM OF BOVE & LANGA A PROFESSIONAL CORPORATION TEN TREMONT STREET, SUITE 600 BOSTON, MASSACHUSETTS 02108 Telephone: 617.720.6040 Facsimile: 617.720.1919 www.bovelanga.com The Foreign Bank Account

U.S. / ISRAELI INCOME TAX UPDATE FOR YEAR 2015 (2014 Tax Year)

") 02-999-2104, 03-527-3254, 09-746-0623 Cellular: 052-274-9999 Fax: 02-991-0195 Email: alan@ardcpa.com Website: www.ardcpa.com U.S. / ISRAELI INCOME TAX UPDATE FOR YEAR 2015 (2014 Tax Year) The 2014 U.S.

02-999-2104, 03-527-3254, 09-746-0623 Cellular: 052-274-9999 Fax: 02-991-0195 Email: alan@ardcpa.com Website: www.ardcpa.com U.S. / ISRAELI INCOME TAX UPDATE FOR YEAR 2015 (2014 Tax Year) The 2014 U.S.

Top 10 Tax Considerations for U.S. Citizens Living in Canada

Top 10 Tax Considerations for U.S. Citizens Living in Canada Recent Canadian media reports have estimated that there are approximately one million U.S. citizens living in Canada and that a relatively low

Top 10 Tax Considerations for U.S. Citizens Living in Canada Recent Canadian media reports have estimated that there are approximately one million U.S. citizens living in Canada and that a relatively low

You may have US tax filing obligations even if some or all of your income was already taxed at source or is going to be taxed by a foreign country.

Dummies Guide -- US Taxes Abroad Introduction and Overview You're a US citizen or a green card holder and you live somewhere outside the USA (i.e., in a "foreign" country). You may have US tax filing obligations

Dummies Guide -- US Taxes Abroad Introduction and Overview You're a US citizen or a green card holder and you live somewhere outside the USA (i.e., in a "foreign" country). You may have US tax filing obligations

Tax Implications for US Citizens/Residents Moving to & Living in Canada

Tax Implications for US Citizens/Residents Moving to & Living in Canada TAX Julia Klann & Domeny Wu March 20, 2014 Topics to Discuss Moving to Canada & Overview of Canadian & US Tax Systems US Filing Requirements

Tax Implications for US Citizens/Residents Moving to & Living in Canada TAX Julia Klann & Domeny Wu March 20, 2014 Topics to Discuss Moving to Canada & Overview of Canadian & US Tax Systems US Filing Requirements

Guidance for companies, trusts and partnerships on completing a self-certification form

Guidance for companies, trusts and partnerships on completing a self-certification form In order to combat tax evasion by both individuals and businesses, the UK and many other countries have entered into

Guidance for companies, trusts and partnerships on completing a self-certification form In order to combat tax evasion by both individuals and businesses, the UK and many other countries have entered into

Residency for U.S. Income Tax Purposes by Jo Anne C. Adlerstein

Copyright 2014, American Immigration Lawyers Association. Reprinted, with permission, from AILA s Immigration Practice Pointers (2014 15 Ed.), AILA Publications, http://agora.aila.org. Residency for U.S.

Copyright 2014, American Immigration Lawyers Association. Reprinted, with permission, from AILA s Immigration Practice Pointers (2014 15 Ed.), AILA Publications, http://agora.aila.org. Residency for U.S.

Tax Aspects of Consulting The Exit Tax Roth IRA Conversions Other. Foreign Bank Account Reporting Update Social Security

The Wolf Group, PC Tax Aspects of Consulting The Exit Tax Roth IRA Conversions Other Foreign Bank Account Reporting Update Social Security U.S. citizen Green card holder G-4 visa holder Based on common

The Wolf Group, PC Tax Aspects of Consulting The Exit Tax Roth IRA Conversions Other Foreign Bank Account Reporting Update Social Security U.S. citizen Green card holder G-4 visa holder Based on common

Foreign Account Tax Compliance Act FATCA Onboarding Requirements for Payees U.S. Financial Institutions

Paris New York London Rome Milan Casablanca Dubai Amsterdam Brussels Hong Kong Singapore Foreign Account Tax Compliance Act FATCA Onboarding Requirements for Payees U.S. Financial Institutions June 13,

Paris New York London Rome Milan Casablanca Dubai Amsterdam Brussels Hong Kong Singapore Foreign Account Tax Compliance Act FATCA Onboarding Requirements for Payees U.S. Financial Institutions June 13,

US Voluntary Disclosure

what you need to know, and how we can help US Voluntary Disclosure what you need to know, and how we can help www.withersworldwide.com www.withersworldwide.com Introduction Countries throughout the world

what you need to know, and how we can help US Voluntary Disclosure what you need to know, and how we can help www.withersworldwide.com www.withersworldwide.com Introduction Countries throughout the world

How To Disclose Your Foreign Bank Accounts And Avoid Criminal Prosecution! FIVE STONE. tax advisers

How To Disclose Your Foreign Bank Accounts And Avoid Criminal Prosecution! Do you have or think you may have a foreign bank account that should be disclosed to the United States Government? Have you received

How To Disclose Your Foreign Bank Accounts And Avoid Criminal Prosecution! Do you have or think you may have a foreign bank account that should be disclosed to the United States Government? Have you received

The IRS Is Looking For Non-Compliant Taxpayers With Foreign Interests: Is Your Taxpayer One Of Them?

The IRS Is Looking For Non-Compliant Taxpayers With Foreign Interests: Is Your Taxpayer One Of Them? Josh O. Ungerman and Anthony P. Daddino Each year, in the United States alone, offshore tax evasion

The IRS Is Looking For Non-Compliant Taxpayers With Foreign Interests: Is Your Taxpayer One Of Them? Josh O. Ungerman and Anthony P. Daddino Each year, in the United States alone, offshore tax evasion

Frequently Asked Questions: US Foreign Account Tax Compliance Act & the World Bank s Staff Retirement Plan

Frequently Asked Questions: US Foreign Account Tax Compliance Act & the World Bank s Staff Retirement Plan The purpose of this FAQ is to provide the World Bank staff and Staff Retirement Plan beneficiaries

Frequently Asked Questions: US Foreign Account Tax Compliance Act & the World Bank s Staff Retirement Plan The purpose of this FAQ is to provide the World Bank staff and Staff Retirement Plan beneficiaries

Offshore Tax Evasion: US Initiatives

Scott D. Michel, Caplin & Drysdale This Article discusses the US reporting rules for US taxpayers with foreign accounts and assets (including FBAR and FATCA), the civil penalties for non-compliance with

Scott D. Michel, Caplin & Drysdale This Article discusses the US reporting rules for US taxpayers with foreign accounts and assets (including FBAR and FATCA), the civil penalties for non-compliance with

CALIFORNIA STATE BAR TAXATION SECTION TAX PROCEDURE AND LITIGATION COMMITTEE AND INTERNATIONAL TAX COMMITTEE

CALIFORNIA STATE BAR TAXATION SECTION TAX PROCEDURE AND LITIGATION COMMITTEE AND INTERNATIONAL TAX COMMITTEE A SIMPLIFIED PROCEDURE TO ALLOW LATE FILED FORMS 8891 FOR INDIVIDUALS WITH CANADIAN RETIREMENT

CALIFORNIA STATE BAR TAXATION SECTION TAX PROCEDURE AND LITIGATION COMMITTEE AND INTERNATIONAL TAX COMMITTEE A SIMPLIFIED PROCEDURE TO ALLOW LATE FILED FORMS 8891 FOR INDIVIDUALS WITH CANADIAN RETIREMENT

Withholding of Tax on Nonresident Aliens and Foreign Entities

Department of the Treasury Internal Revenue Service Publication 515 Cat. No. 15019L Withholding of Tax on Nonresident Aliens and Foreign Entities For use in 2013 Contents What's New... 1 Reminders... 2

Department of the Treasury Internal Revenue Service Publication 515 Cat. No. 15019L Withholding of Tax on Nonresident Aliens and Foreign Entities For use in 2013 Contents What's New... 1 Reminders... 2

May 7, 2012 California Bar Suggests Guidance, Safe Harbor to Aid Foreign Pension Beneficiaries

May 7, 2012 California Bar Suggests Guidance, Safe Harbor to Aid Foreign Pension Beneficiaries Philip D.W. Hodgen and Steven L. Walker of the California State Bar Taxation Section proposed that the IRS

May 7, 2012 California Bar Suggests Guidance, Safe Harbor to Aid Foreign Pension Beneficiaries Philip D.W. Hodgen and Steven L. Walker of the California State Bar Taxation Section proposed that the IRS

GUIDE TO U.S. INCOME TAXATION FOR IDB-IIC FCU MEMBERS

GUIDE TO U.S. INCOME TAXATION FOR IDB-IIC FCU MEMBERS Prepared Exclusively for IDB-IIC FCU Members by The Wolf Group, P.C. January, 2013 Copyright 2013 - The Wolf Group, P.C. January 2013 1 Copyright 2013

GUIDE TO U.S. INCOME TAXATION FOR IDB-IIC FCU MEMBERS Prepared Exclusively for IDB-IIC FCU Members by The Wolf Group, P.C. January, 2013 Copyright 2013 - The Wolf Group, P.C. January 2013 1 Copyright 2013

FATCA Frequently Asked Questions

FATCA Frequently Asked Questions FATCA overview 1. What is FATCA? 2. What is the impact of FATCA? 3. How do I know if I am affected? 4. When will the FATCA legislation become effective? 5. Is HSBC the

FATCA Frequently Asked Questions FATCA overview 1. What is FATCA? 2. What is the impact of FATCA? 3. How do I know if I am affected? 4. When will the FATCA legislation become effective? 5. Is HSBC the

New York Law School April 24, 2015. Professor Alan I. Appel New York Law School

Undisclosed Foreign Accounts: IRS Investigations, Audits, OVDP and Streamlined Disclosures The Lawyer s Role in Guiding the Taxpayer through Perilous Waters New York Law School April 24, 2015 Professor

Undisclosed Foreign Accounts: IRS Investigations, Audits, OVDP and Streamlined Disclosures The Lawyer s Role in Guiding the Taxpayer through Perilous Waters New York Law School April 24, 2015 Professor

22.16: IRS Provides Targeted Relief for FBAR Filers, Including Investors in Foreign Investment Funds

22.16: IRS Provides Targeted Relief for FBAR Filers, Including Investors in Foreign Investment Funds By Babak Nikravesh of Jones Day and Justin MacCarthy (formerly of Jones Day) In early 2010, the Internal

22.16: IRS Provides Targeted Relief for FBAR Filers, Including Investors in Foreign Investment Funds By Babak Nikravesh of Jones Day and Justin MacCarthy (formerly of Jones Day) In early 2010, the Internal

U.S. Taxation and information reporting for foreign trusts and their U.S. owners and U.S. beneficiaries

Private Company Services U.S. Taxation and information reporting for foreign trusts and their U.S. owners and U.S. beneficiaries United States (U.S.) owners and beneficiaries of foreign trusts (i.e., non-u.s.

Private Company Services U.S. Taxation and information reporting for foreign trusts and their U.S. owners and U.S. beneficiaries United States (U.S.) owners and beneficiaries of foreign trusts (i.e., non-u.s.

The Bank of Nova Scotia Shareholder Dividend and Share Purchase Plan

The Bank of Nova Scotia Shareholder Dividend and Share Purchase Plan Offering Circular Effective November 6, 2013 The description contained in this Offering Circular of the Canadian and U.S. income tax

The Bank of Nova Scotia Shareholder Dividend and Share Purchase Plan Offering Circular Effective November 6, 2013 The description contained in this Offering Circular of the Canadian and U.S. income tax

NewsLetter Asesoría Financiera, S.A.

NewsLetter Asesoría Financiera, S.A. NEWSLETTER Nº 9/2015 (28 January 2015) Gal.la Sánchez Vendrell. Partner. Lawyer. CEO Tax amnesty for American citizens resident in Spain The US is one of the few countries

NewsLetter Asesoría Financiera, S.A. NEWSLETTER Nº 9/2015 (28 January 2015) Gal.la Sánchez Vendrell. Partner. Lawyer. CEO Tax amnesty for American citizens resident in Spain The US is one of the few countries

Foreign Account Tax Compliance Act (FATCA) Frequently Asked Questions

Frequently Asked Questions") Foreign Account Tax Compliance Act (FATCA) Frequently Asked Questions For Momentum Retail (excluding Momentum Wealth International) General FATCA questions 1. What is FATCA? FATCA is the acronym for the

Foreign Account Tax Compliance Act (FATCA) Frequently Asked Questions For Momentum Retail (excluding Momentum Wealth International) General FATCA questions 1. What is FATCA? FATCA is the acronym for the

FAQs on Cost-Basis Reporting for Brokers

FAQs on Cost-Basis Reporting for Brokers The IRS published a list of Frequently Asked Questions on the new expanded tax reporting requirement for brokers which include reporting their customer s tax basis

FAQs on Cost-Basis Reporting for Brokers The IRS published a list of Frequently Asked Questions on the new expanded tax reporting requirement for brokers which include reporting their customer s tax basis

gyb Growing your business TM Volume 63 2011 Personal investments abroad The IRS is taking a closer look

gyb Growing your business TM Volume 63 2011 Personal investments abroad The IRS is taking a closer look Personal investments abroad: The IRS is taking a closer look For all that the complexity of new global-reporting

gyb Growing your business TM Volume 63 2011 Personal investments abroad The IRS is taking a closer look Personal investments abroad: The IRS is taking a closer look For all that the complexity of new global-reporting

How To Comply With The Foreign Account Tax Compliance Act

PRESENTATION ON THE FOREIGN ACCOUNT TAX COMPLIANCE ACT (FATCA) FOR CONSULTATIONS WITH THE INDUSTRY Prepared for the Meeting with ECCU Non-Bank Financial Institutions February 2014 EASTERN CARIBBEAN CENTRAL

PRESENTATION ON THE FOREIGN ACCOUNT TAX COMPLIANCE ACT (FATCA) FOR CONSULTATIONS WITH THE INDUSTRY Prepared for the Meeting with ECCU Non-Bank Financial Institutions February 2014 EASTERN CARIBBEAN CENTRAL

Procedures for Opt Out and Removal of Taxpayers from IRS FBAR Voluntary Disclosure Program

Procedures for Opt Out and Removal of Taxpayers from IRS FBAR Voluntary Disclosure Program Guidance for Opt Out and Removal of Taxpayers from the Civil Settlement Structure of the 2009 Offshore Voluntary

Procedures for Opt Out and Removal of Taxpayers from IRS FBAR Voluntary Disclosure Program Guidance for Opt Out and Removal of Taxpayers from the Civil Settlement Structure of the 2009 Offshore Voluntary

New Reporting Requirement for Foreign Bank Accounts and Assets

TAX & BUSINESS PLANNING IN THE NEWS February 2012 New Reporting Requirement for Foreign Bank Accounts and Assets A Polsinelli Shughart Update What is a Foreign Financial Asset Who Must File... 2 Filing

TAX & BUSINESS PLANNING IN THE NEWS February 2012 New Reporting Requirement for Foreign Bank Accounts and Assets A Polsinelli Shughart Update What is a Foreign Financial Asset Who Must File... 2 Filing

Since the 1970s, the Department of Treasury

Foreign Account Reporting for Retirement Plans By Jennifer E. Eller and Michael P. Kreps The authors discuss the filing requirements of the Bank Secrecy Act that may apply to retirement plans if funds

Foreign Account Reporting for Retirement Plans By Jennifer E. Eller and Michael P. Kreps The authors discuss the filing requirements of the Bank Secrecy Act that may apply to retirement plans if funds

IRS Issues Final FATCA Regulations

IRS Issues Final FATCA Regulations The United States Internal Revenue Service (IRS) has issued long-awaited final regulations (the Final Regulations) under the Foreign Account Tax Compliance Act (FATCA).

IRS Issues Final FATCA Regulations The United States Internal Revenue Service (IRS) has issued long-awaited final regulations (the Final Regulations) under the Foreign Account Tax Compliance Act (FATCA).

Whereas, the Government of the Republic of Poland is supportive of the underlying policy goal of FATCA to improve tax compliance;

Agreement between the Government of the Republic of Poland and the Government of the United States of America to Improve International Tax Compliance and to Implement FATCA Whereas, the Government of the

Agreement between the Government of the Republic of Poland and the Government of the United States of America to Improve International Tax Compliance and to Implement FATCA Whereas, the Government of the

The Impact of FATCA on U.S. and Non-U.S. Private Equity & Hedge Funds Closing the distance

The Impact of FATCA on U.S. and Non-U.S. Private Equity & Hedge Funds Closing the distance Global Financial Services Industry Overview The Foreign Account Tax Compliance Act ( FATCA ) regime signifies

The Impact of FATCA on U.S. and Non-U.S. Private Equity & Hedge Funds Closing the distance Global Financial Services Industry Overview The Foreign Account Tax Compliance Act ( FATCA ) regime signifies

10234 Federal Register / Vol. 76, No. 37 / Thursday, February 24, 2011 / Rules and Regulations

10234 Federal Register / Vol. 76, No. 37 / Thursday, February 24, 2011 / Rules and Regulations 1201). The February-March 2010 proposal called for a two-stage increase. The consumptive use rate was proposed

10234 Federal Register / Vol. 76, No. 37 / Thursday, February 24, 2011 / Rules and Regulations 1201). The February-March 2010 proposal called for a two-stage increase. The consumptive use rate was proposed

Panel. U.S. and Mexican Taxation of Individuals Residing Abroad

Panel U.S. and Mexican Taxation of Individuals Residing Abroad Diana S. Davis, Esq., Of Counsel, Greenberg Traurig, LLP Kenneth Guilfoyle, CPA, Expatriate Services Practice Leader, BDO Seidman, LLP U.S.

Panel U.S. and Mexican Taxation of Individuals Residing Abroad Diana S. Davis, Esq., Of Counsel, Greenberg Traurig, LLP Kenneth Guilfoyle, CPA, Expatriate Services Practice Leader, BDO Seidman, LLP U.S.

TAX ASPECTS OF MUTUAL FUND INVESTING

Tax Guide for 2015 TAX ASPECTS OF MUTUAL FUND INVESTING INTRODUCTION I. Mutual Fund Distributions A. Distributions From All Mutual Funds 1. Net Investment Income and Short-Term Capital Gain Distributions

Tax Guide for 2015 TAX ASPECTS OF MUTUAL FUND INVESTING INTRODUCTION I. Mutual Fund Distributions A. Distributions From All Mutual Funds 1. Net Investment Income and Short-Term Capital Gain Distributions

Overview of Common Civil Penalties Asserted by the IRS

Overview of Common Civil Penalties Asserted by the IRS December, 2008 Bob Kane Rob McCallum LeSourd & Patten, P.S. INTRODUCTION In 1989, Congress enacted legislation substantially revising the civil penalty

Overview of Common Civil Penalties Asserted by the IRS December, 2008 Bob Kane Rob McCallum LeSourd & Patten, P.S. INTRODUCTION In 1989, Congress enacted legislation substantially revising the civil penalty

ELECTRONIC COMMUNICATION:

TAX FILING YEAR 2015 DISCLAIMER: and (SPOUSE/if filing Jointly) the undersigned taxpayer (s) hereby engage the services of American Expat Tax Services, Pte Limited (referred to hereinafter as AETS) as

TAX FILING YEAR 2015 DISCLAIMER: and (SPOUSE/if filing Jointly) the undersigned taxpayer (s) hereby engage the services of American Expat Tax Services, Pte Limited (referred to hereinafter as AETS) as

Professional Tax Preparation and Consulting Engagement Agreement American Expat Tax Services Pte Ltd (Singapore Reg. No.

DISCLAIMER: and (SPOUSE/if filing Jointly) the undersigned taxpayer (s) hereby engage the services of American Expat Tax Services, Pte Limited (referred to hereinafter as AETS) as a U.S. tax preparation

DISCLAIMER: and (SPOUSE/if filing Jointly) the undersigned taxpayer (s) hereby engage the services of American Expat Tax Services, Pte Limited (referred to hereinafter as AETS) as a U.S. tax preparation

Certification of Non-Willfulness Streamlined Filing Compliance Procedure

Certification of Non-Willfulness Streamlined Filing Compliance Procedure Article by: Mishkin Santa, LL.M, J.D. - Director of International Advisory & Legal Services The eligibility requirements for expanded

Certification of Non-Willfulness Streamlined Filing Compliance Procedure Article by: Mishkin Santa, LL.M, J.D. - Director of International Advisory & Legal Services The eligibility requirements for expanded

Investment Adviser Annual and Other Compliance Matters

2013 Investment Adviser Annual and Other Compliance Matters This annual memorandum provides clients and friends of Finn Dixon & Herling with brief summaries of selected compliance matters relevant to investment

2013 Investment Adviser Annual and Other Compliance Matters This annual memorandum provides clients and friends of Finn Dixon & Herling with brief summaries of selected compliance matters relevant to investment

University of Illinois Tax School 2014 Federal Tax Workbook Chapter 6: IRS Representation and Procedures

University of Illinois Tax School 2014 Federal Tax Workbook Chapter 6: IRS Representation and Procedures Presenter s Name: Shawn Savage IRS Sr. Stakeholder Liaison Date: October 21, 23, 29 2014 Topic 1:

University of Illinois Tax School 2014 Federal Tax Workbook Chapter 6: IRS Representation and Procedures Presenter s Name: Shawn Savage IRS Sr. Stakeholder Liaison Date: October 21, 23, 29 2014 Topic 1: