Maryland Government Finance Officers Association. October 25, 2013

|

|

|

- Mitchell Spencer

- 8 years ago

- Views:

Transcription

1 Maryland Government Finance Officers Association October 25,

2 Payment Methods Receiving Payments Making Payments New Developments 2

3 Paper Plastic Bank Account Cyber Cash Digital Currency Cash Check Money Order Travelers Checks Debit Cards Credit Cards Stored Value Cards Online Bill Payment Bank Account Payments (ACH debits) Pay Pal, Google Wallet, Dwolla, et al BitCoin, BitMint 3

Pay Pal, Google Wallet, Dwolla, et al BitCoin,")

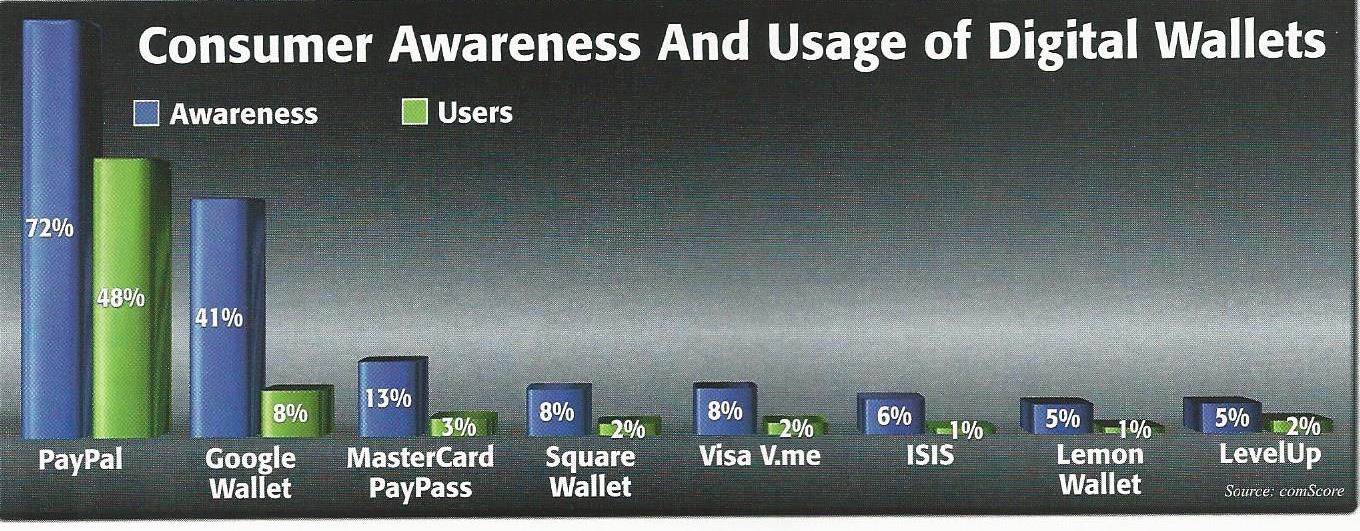

4 The average consumer held 5 of the nine payment instruments and used 3.8 of those in a typical month Movement is from paper to plastic and electronics 93.6% of consumers have at least one bank account 30% of consumers had a nonbank payment account (Pay Pal, Google Wallet, etc.) 80% of domestic consumer spending in 2011 was done without cash 4

5

6 Payment Card Industry (PCI) Data Security Standard Level 1 - Merchants processing 6 million or more transactions per year. Level 2 Merchants processing 1M to 6M Visa transactions per year. Level 3 - Merchants processing 20,000 to 1M e-commerce transactions per year. Level 4 - Merchants processing fewer than 20,000 e- commerce transactions per year, and all other merchants processing up to 1M transactions per year. 6

7 Reputational risk is worst case scenario for government entities where taxpayers are already sensitive about their privacy Many services charge a monthly fee for non compliance Fines for data breaches are substantial 7

8 Common challenge areas and drivers for change included: Lack of education and awareness Weak passwords, authentication Third-party security challenges Slow self-detection, malware 8

9 New guidelines version 3.0 of the PCI Data Security Standard (PCI DSS) to be released November 7 To be implemented by January 1, 2014 More emphasis on shared responsibility between acquirers and merchants who handle card transactions Protection of credit card terminals from physical tampering Compiling an inventory of system components, including servers. 9

10 10

11 Can reduce the scope of PCI compliance requirements Cardholder Data Environment (CDE) is any system that stores, processes or transmits cardholder data and is within the scope of PCIDDS To be considered outside the CDE, must show that a breach of the system would not breach the CDE and cardholder data 11

12 P2PE solutions need to comply with PCI Hardware Standards Cryptographic keys are secured inside the hardware terminal and terminal does not output clear text cardholder data Third party owns and manages security configuration, barring merchant access to keys Reduces the CDE to only the terminal itself 12

13

14 Rather than the magnetic stripe, these cards contain an embedded microchip that is authenticated using a PIN. To make a purchase, the card is placed into a PIN pad terminal which accesses the card s microchip and verifies its authenticity using algorithmic codes. The cardholder validates their identity by entering the PIN. 14

15 Chip &PIN authenticates by inserting the card in the POS device and entering PIN Chip & Signature authenticates by signature rather than PIN Near Field Communication (NFC) requires chip to be installed in phone No CVM (cardholder verification method) for small purchases 15

for small purchases 15")

16 Introduced in 1996, 22 countries, including China, India, Japan, Mexico, Canada and many in Western Europe and Latin America have migrated to EMV, encrypted microprocessor chip and PIN technology for credit and debit payments. Also referred to as the EMV (Europay- MasterCard-Visa) Chip-and-PIN card 40% of cards and 71% of payment terminals worldwide support EMV standards More than 1 billion EMV cards used at over 15.4 million EMV terminals throughout 80 countries 16

17 Once EMV cards and readers were introduced in the UK, overall credit card fraud dropped 32.5% between , with a 72.5% reduction in fraud from lost or stolen cards Most US merchants are not able to process the EMV cards presented by international travelers and must rely on cash sales for these customers. In 2012, only 1 million of Visa s 230 million US-issued cards were chip enabled 17

18 In 2001, it was estimated that it would cost $13.4 billion to convert the point of sale infrastructure in the US to accept these smart cards, and that 74% of the cost would have to be borne by the merchants. At that point, credit card fraud was only a $1 billion problem. Current estimate to implement is $12.7 billion Current credit card fraud is estimated at $8.6 billion PCI Compliance costs are substantial 18

19 An expensive solution to a small problem, says Sinclair Oil Corporation 80% of current transactions are PIN based, debit card purchases Cost per gas station to install EMV terminals? $20,000 per station $40 million for the company Wendy s says its actual fraud rate is so small it s hardly worth mentioning. It processes 300,000 card transactions day. 19

20 Master Card, Visa, American Express and Discover have issued an October 2015 deadline for POS terminals that can process EMV cards After that deadline, merchants not implementing EMV technology will absorb fraud losses Deadline extended to October 2017 for gas stations 20

21 21

22 EMV does not address the card not present transaction Some merchants may elect to absorb the cost of fraud losses rather than retrofit its terminal equipment Technology whose time has come and gone Mobile wallets Virtual cards are replacing plastic Digital cash 22

23

24 Participant Eligibility Elementary and secondary schools Colleges, universities, professional schools Local, state and federal courts Government entities Convenience fee can be: Flat fee per transaction Variable/tiered rate based on amount owed Fixed percentage of amount owed Different for debit and credit cards (cannot be assessed on PIN based debit cards) Must be the same fee structure for all credit card brands 24

25 Place and method of payment not restricted Whether in person, on the Internet, by phone, mail or at a kiosk Processing Requirements Notification of fee at the time of the transaction Customer service number must be transmitted to acquirer for the payment and the fee May not be advertised as an offset to the merchant discount rate Recommended, but not required, that the fee be charged as a separate and unique transaction 25

26

27 Mobile Payment Services accepting credit cards via cell phone or ipad Square ended 2012 with $10 billion in processing for 40,000 merchants Square s new pricing offers a flat $275/month fee with no swipe fee or no monthly fee and 2.75% swipe fee Three popular providers: Square Reader (2010) PayPal Here Reader (2012) Intuit Go Payment (2012) 27

28

29 Ability to capture account number information and create an electronic file to upload to receivable database ( mini inhouse lockbox ) Many banks now offer customers the ability to deposit checks using their Smartphone camera to capture an image of the front and back of the check. Remote Deposit Capture Duplicate Deposits Cross bank duplicate detection system is available and used by many big banks An increasing number of banks are applying availability schedules to all check deposits Holder in Due Course-check cashing organizations Secure scanned checks and shred timely! 29

30 Integrated Receivables services process checks, credit cards and electronic payments Data exchange of receivables file for lockbox provider to research account numbers and apply payments, reducing exception work MICR line and account number identification database to identify payments by MICR Service level agreements management is best practice 30

31

32 Fed Wire Extended Remittance Information (ERI) Originators of wire transfers can now include up to 9,000 characters of extended remittance information Identifying what the wire is intended to pay will be significantly easier Single Euro Payments Area (SEPA) Payment-integration of the European Union for bank transfers denominated in euros. SEPA consists of the 28 EU member states, Iceland, Liechtenstein, Norway and Switzerland and Monaco. Improve the efficiency of cross-border payments and turn the fragmented national markets for euro payments into a single domestic one, similar to our ACH network Transaction costs for SEPA payments are significantly less than wire transfers 32

33 On-line purchases using your on-line banking service Limited acceptance at PNC Bank, The Bank of Maine, US Bank Secure Vault Payments accepted at: Columbus State University, Columbus (GA) Water Works, University of Georgia, University of Wisconsin Stout, Wicked Whoopies 33

34 A Universal Payment Identification Code (UPIC) is a unique account identifier that looks and acts just like a real account number on ACH transactions Bank Agnostic 34

35

Weigh costs against daily armored pick up, immediate credit, improved internal controls")

36 Secure and accurate vault deposit system for cash-intensive businesses Tracks, stores and balances multiple cash sales Immediate credit Fee structure includes Purchase or lease of vault Provider fees for pickup and maintenance Bank related fees (per deposit, per volume) Weigh costs against daily armored pick up, immediate credit, improved internal controls 36

37 Reduction of coin collection and its related problems Register cell phone number, license plate and a credit card To use, call a toll free number, enter the location number of the meter and the number of minutes you wish to park You even get a text message when you meter time is running out! 45 transaction fee in DC; 35 in Montgomery County Use the Parkmobile mobile app or mobile website to enter in the location number listed on the sign. (reduced transaction fee of 30 37

38 38

39

40 Integrate with existing AP systems and workflows with bank via electronic data transfer of payment details, including payment method (check, purchasing card, ACH, Wire) Eliminates the risks associated with maintaining check stock Eliminates the need to transmit positive payee and account reconciliation data Many banks will assist in encouraging vendors to accept ACH and purchase card payments, reducing costs related to issuing checks (bank reconciliation, unclaimed property, reissuance of lost/stolen checks) Two models for purchasing card transactions Virtual Cards Buyer Initiated Payments BIP 40

41 41

42 Two models for purchasing card transactions Virtual Cards Buyer Initiated Payments BIP Virtual Cards Payment Instructions transmitted to bank Card number and dollar limits assigned to the vendor and securely remitted to vendor s Vendor places charge against card number Buyer Initiated Payments Payment Instructions transmitted to bank Bank initiates transaction into the card payment network Payment directly credited to Vendor s bank account as a credit card receipt Payment confirmation delivered to Vendor 42

43

44 New York Attorney General is inquiring about payroll card programs Consumer Financial Protection Bureau (CFPB) said employers can t mandate wages via payroll cards, but can offer option of Direct Deposit Class action lawsuit brought against a Pennsylvania McDonald s Largest complaint is the fees employees pay; un-banked employees pay between 2.4-3% in check cashing fees. Many payroll card programs do not cost employees for basic services 44

45

46 Short-range wireless communication Wave device at terminal to pay Merchants can upload coupons and promotional data and send text alerts of sales Driven by financial institutions to increase use of their credit cards 46

47 Able to handle multiple payment forms, various credit cards Primarily used for small-value payments; driven by financial institutions to increase use of their credit cards Smartphones must have NFC chip. Many smartphones, including Apple do not have NFC chips 47

48

49

50 Battery drain issues and interference from mobile cases used to protect phone Requires expensive POS terminal modification Security questions - 64% in a recent survey said they don t think mobile payments are secure 50 % of Smartphone users have not heard of mobile payments, and of the ones who had, only 8% said they are familiar with the technology Many smartphones, including Apple do not have NFC chips 50

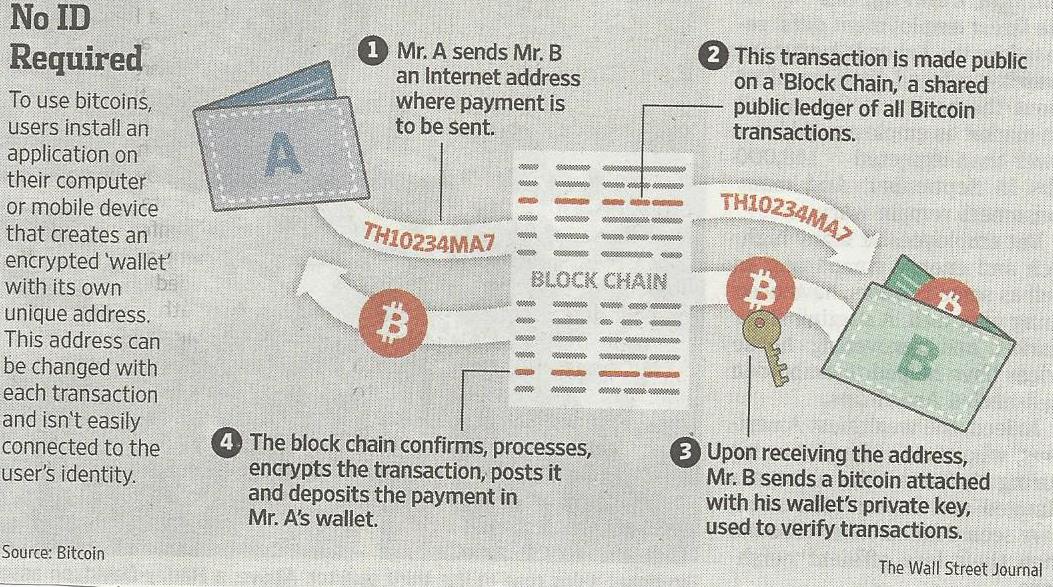

51 Clinkle offers high frequency sound waves to transmit data PayPal and Apple are using wireless signals via Bluetooth Low-Energy technology Cashtie Cloud Match Service replaces NFC hardware and software to accept mobile payments 51

52 52

53 Informational Account balances Transaction details Alerts Managerial Wires approvals ACH approvals Positive pay decisions Account transfers Source :Wells Fargo competitive analysis; data based on primary research using demos, press releases, third-party reviews 53

54 Source :Wells Fargo competitive analysis; data based on primary research using demos, press releases, third-party reviews 54

55 55

56 Person to person payment technology still not widely used in the US In May 2013, Google integrated its Google Wallet with Gmail for ing person to person payments Users must have a Google Wallet linked with a bank account for free transfers A flat 2.9% transaction fee for payments made from debit or credit card Receiving money is always free Barclays offers Pingit money sending service for smartphones Download app Ability to transfer money to anyone with a UK bank account

57

58

59 Merchants can accept; also enables person to person payments Dwolla accounts are free for consumers and merchants (Dwolla goes through the usual Know Your Customer procedures) Paying with Dwolla is like paying with cash or a check online Transactions under $10 are free; all others are 25 59

60 Magic Bands Walt Disney is testing a rubber bracelet that is tied to a credit card The bracelet can be waved in front of a credit card processing terminal to pay for items at Disney Parks The bracelets can also serve as hotel room keys Google Glass The Google Glass headset computer is still in development, but some advance releases are available for a premium MasterCard is actively developing applications that allow consumers to make payments at credit card processing stations Samsung s Galaxy Gear smartwatch MasterCard is also examining potential credit card payments applications 60

61 BitCoin (BTC) is the world s first completely decentralized digital currency The value of a BTC has grown and fluctuated greatly, from pennies in its early days to more than $260 at its peak in April 2013 Under close scrutiny by law enforcement for potential money laundering FinCEN maintains that Bitcoin exchanges operating in the U.S. must be registered as money transmitters. 61

62 62

63 ????????????? CJVolk Associates, Inc. Treasury and Cash Management Consulting Claudia Volk, CTP, AAP, CPA Principal 1300 South Washington Street Falls Church, VA T F claudia.volk@cjvolk.com????

Preparing for EMV chip card acceptance

Preparing for EMV chip card acceptance Ben Brown Vice President, Regional Sales Manager, Wells Fargo Merchant Services Lily Page Vice President, Wholesale ereceivables, Wells Fargo Merchant Services June

Preparing for EMV chip card acceptance Ben Brown Vice President, Regional Sales Manager, Wells Fargo Merchant Services Lily Page Vice President, Wholesale ereceivables, Wells Fargo Merchant Services June

EMV and Small Merchants:

September 2014 EMV and Small Merchants: What you need to know Mike English Executive Director, Product Development Heartland Payment Systems 2014 Heartland Payment Systems, Inc. All trademarks, service

September 2014 EMV and Small Merchants: What you need to know Mike English Executive Director, Product Development Heartland Payment Systems 2014 Heartland Payment Systems, Inc. All trademarks, service

EMV and Restaurants: What you need to know. Mike English. October 2014. Executive Director, Product Development Heartland Payment Systems

October 2014 EMV and Restaurants: What you need to know Mike English Executive Director, Product Development Heartland Payment Systems 2014 Heartland Payment Systems, Inc. All trademarks, service marks

October 2014 EMV and Restaurants: What you need to know Mike English Executive Director, Product Development Heartland Payment Systems 2014 Heartland Payment Systems, Inc. All trademarks, service marks

EMV in Hotels Observations and Considerations

EMV in Hotels Observations and Considerations Just in: EMV in the Mail Customer Education: Credit Card companies have already started customer training for the new smart cards. 1 Questions to be Answered

EMV in Hotels Observations and Considerations Just in: EMV in the Mail Customer Education: Credit Card companies have already started customer training for the new smart cards. 1 Questions to be Answered

OpenEdge Research & Development Group April 2015

2015: Security, Merchant Readiness & the Coming Liability Shift OpenEdge Research & Development Group April 2015 solutions@openedgepay.com openedgepay.com 2015: Security, Merchant Table of Contents The

2015: Security, Merchant Readiness & the Coming Liability Shift OpenEdge Research & Development Group April 2015 solutions@openedgepay.com openedgepay.com 2015: Security, Merchant Table of Contents The

toast EMV in 2015: How Restaurants Can Prepare for the New Chip-and-Pin Standard

toast EMV in 2015: How Restaurants Can Prepare for the New Chip-and-Pin Standard Table of Contents For more than 40 years, merchants and consumers have used magnetic stripe credit cards and compatible

toast EMV in 2015: How Restaurants Can Prepare for the New Chip-and-Pin Standard Table of Contents For more than 40 years, merchants and consumers have used magnetic stripe credit cards and compatible

welcome to liber8:payment

liber8:payment welcome to liber8:payment Our self-service kiosks free up staff time and improve the overall patron experience. liber8:payment further enhances these benefits by providing the convenience

liber8:payment welcome to liber8:payment Our self-service kiosks free up staff time and improve the overall patron experience. liber8:payment further enhances these benefits by providing the convenience

Evolving Mobile Payments Industry Landscape

Evolving Mobile Payments Industry Landscape Mobile Banking: Can the Unbanked Bank on It? Sargent Shriver National Center on Poverty Law webinar August 16, 2012 Marianne Crowe Federal Reserve Bank of Boston

Evolving Mobile Payments Industry Landscape Mobile Banking: Can the Unbanked Bank on It? Sargent Shriver National Center on Poverty Law webinar August 16, 2012 Marianne Crowe Federal Reserve Bank of Boston

THE FIVE Ws OF EMV BY DAVE EWALD GLOBAL EMV CONSULTANT AND MANAGER DATACARD GROUP

THE FIVE Ws OF EMV BY DAVE EWALD GLOBAL EMV CONSULTANT AND MANAGER DATACARD GROUP WHERE IS THE U.S. PAYMENT CARD INDUSTRY NOW? WHERE IS IT GOING? Today, payment and identification cards of all types (credit

THE FIVE Ws OF EMV BY DAVE EWALD GLOBAL EMV CONSULTANT AND MANAGER DATACARD GROUP WHERE IS THE U.S. PAYMENT CARD INDUSTRY NOW? WHERE IS IT GOING? Today, payment and identification cards of all types (credit

EMV's Role in reducing Payment Risks: a Multi-Layered Approach

EMV's Role in reducing Payment Risks: a Multi-Layered Approach April 24, 2013 Agenda EMV Rationale Why is this worth the effort? Guides how we implement it EMV Vulnerability at the POS EMV Impact on CNP

EMV's Role in reducing Payment Risks: a Multi-Layered Approach April 24, 2013 Agenda EMV Rationale Why is this worth the effort? Guides how we implement it EMV Vulnerability at the POS EMV Impact on CNP

We believe First Data is well positioned to take advantage of all of these trends given the breadth of our solutions and our global operating

Given recent payment data breaches, clients are increasingly demanding robust security and fraud solutions; and Financial institutions continue to outsource and leverage technology providers given their

Given recent payment data breaches, clients are increasingly demanding robust security and fraud solutions; and Financial institutions continue to outsource and leverage technology providers given their

Credit card: permits consumers to purchase items while deferring payment

General Payment Systems Cash: portable, no authentication, instant purchasing power, allows for micropayments, no transaction fee for using it, anonymous But Easily stolen, no float time, can t easily

General Payment Systems Cash: portable, no authentication, instant purchasing power, allows for micropayments, no transaction fee for using it, anonymous But Easily stolen, no float time, can t easily

Changing Consumer Purchasing Patterns. John Mayleben, CPP SVP, Technology and Product Development Michigan Retailers Association

Changing Consumer Purchasing Patterns John Mayleben, CPP SVP, Technology and Product Development Michigan Retailers Association Michigan Retailers Association! Michigan Retailers Association is trade

Changing Consumer Purchasing Patterns John Mayleben, CPP SVP, Technology and Product Development Michigan Retailers Association Michigan Retailers Association! Michigan Retailers Association is trade

Payments Transformation - EMV comes to the US

Accenture Payment Services Payments Transformation - EMV comes to the US In 1993 Visa, MasterCard and Europay (EMV) came together and formed EMVCo 1 to tackle the global challenge of combatting fraudulent

Accenture Payment Services Payments Transformation - EMV comes to the US In 1993 Visa, MasterCard and Europay (EMV) came together and formed EMVCo 1 to tackle the global challenge of combatting fraudulent

Are You Ready For PCI v 3.0. Speaker: Corbin DelCarlo Institution: McGladrey LLP Date: October 6, 2014

Are You Ready For PCI v 3.0 Speaker: Corbin DelCarlo Institution: McGladrey LLP Date: October 6, 2014 Today s Presenter Corbin Del Carlo QSA, PA QSA Director, National Leader PCI Services Practice 847.413.6319

Are You Ready For PCI v 3.0 Speaker: Corbin DelCarlo Institution: McGladrey LLP Date: October 6, 2014 Today s Presenter Corbin Del Carlo QSA, PA QSA Director, National Leader PCI Services Practice 847.413.6319

The Comprehensive, Yet Concise Guide to Credit Card Processing

The Comprehensive, Yet Concise Guide to Credit Card Processing Written by David Rodwell CreditCardProcessing.net Terms of Use This ebook was created to provide educational information regarding payment

The Comprehensive, Yet Concise Guide to Credit Card Processing Written by David Rodwell CreditCardProcessing.net Terms of Use This ebook was created to provide educational information regarding payment

PCI DSS FAQ. The twelve requirements of the PCI DSS are defined as follows:

What is PCI DSS? PCI DSS is an acronym for Payment Card Industry Data Security Standards. PCI DSS is a global initiative intent on securing credit and banking transactions by merchants & service providers

What is PCI DSS? PCI DSS is an acronym for Payment Card Industry Data Security Standards. PCI DSS is a global initiative intent on securing credit and banking transactions by merchants & service providers

EMV Chip and PIN. Improving the Security of Federal Financial Transactions. Ian W. Macoy, AAP August 17, 2015

EMV Chip and PIN Improving the Security of Federal Financial Transactions Ian W. Macoy, AAP August 17, 2015 Agenda 1. Executive Order 13681 2. What Is EMV? 3. Federal Agency Payment Card Acceptance Environment

EMV Chip and PIN Improving the Security of Federal Financial Transactions Ian W. Macoy, AAP August 17, 2015 Agenda 1. Executive Order 13681 2. What Is EMV? 3. Federal Agency Payment Card Acceptance Environment

Office of Finance and Treasury

Office of Finance and Treasury How to Accept & Process Credit and Debit Card Transactions Procedure Related Policy Title Credit Card Processing Policy For University Merchant Locations Responsible Executive

Office of Finance and Treasury How to Accept & Process Credit and Debit Card Transactions Procedure Related Policy Title Credit Card Processing Policy For University Merchant Locations Responsible Executive

How To Protect Your Restaurant From A Data Security Breach

NAVIGATING THE PAYMENTS AND SECURITY LANDSCAPE Payment disruptions impacting restaurant owners today An NCR Hospitality white paper Almost every month we hear a news story about another data breach that

NAVIGATING THE PAYMENTS AND SECURITY LANDSCAPE Payment disruptions impacting restaurant owners today An NCR Hospitality white paper Almost every month we hear a news story about another data breach that

Understand the Business Impact of EMV Chip Cards

Understand the Business Impact of EMV Chip Cards 3 What About Mail/Telephone Order and ecommerce? 3 What Is EMV 3 How Chip Cards Work 3 Contactless Technology 4 Background: Behind the Curve 4 Liability

Understand the Business Impact of EMV Chip Cards 3 What About Mail/Telephone Order and ecommerce? 3 What Is EMV 3 How Chip Cards Work 3 Contactless Technology 4 Background: Behind the Curve 4 Liability

The Adoption of EMV Technology in the U.S. By Dave Ewald Global Industry Sales Consultant Datacard Group

The Adoption of EMV Technology in the U.S. By Dave Ewald Global Industry Sales Consultant Datacard Group Abstract: Visa Inc. and MasterCard recently announced plans to accelerate chip migration in the

The Adoption of EMV Technology in the U.S. By Dave Ewald Global Industry Sales Consultant Datacard Group Abstract: Visa Inc. and MasterCard recently announced plans to accelerate chip migration in the

PCI and EMV Compliance Checkup

PCI and EMV Compliance Checkup ATM Security Jim Pettitt Director, ATM Security Diebold Incorporated Agenda ATM threats today Top of mind risk PCI Impact on Security U.S. EMV Migration Conclusions / recommendations

PCI and EMV Compliance Checkup ATM Security Jim Pettitt Director, ATM Security Diebold Incorporated Agenda ATM threats today Top of mind risk PCI Impact on Security U.S. EMV Migration Conclusions / recommendations

A Brand New Checkout Experience

A Brand New Checkout Experience EMV Transformation EMV technology is transforming the U.S. payment industry, bringing a whole new experience to the checkout counter. Introduction What is EMV? It s 3 small

A Brand New Checkout Experience EMV Transformation EMV technology is transforming the U.S. payment industry, bringing a whole new experience to the checkout counter. Introduction What is EMV? It s 3 small

A Brand New Checkout Experience

A Brand New Checkout Experience EMV Transformation EMV technology is transforming the U.S. payment industry, bringing a whole new experience to the checkout counter. Introduction What is EMV? It s 3 small

A Brand New Checkout Experience EMV Transformation EMV technology is transforming the U.S. payment industry, bringing a whole new experience to the checkout counter. Introduction What is EMV? It s 3 small

EMV : Frequently Asked Questions for Merchants

EMV : Frequently Asked Questions for Merchants The information in this document is offered on an as is basis, without warranty of any kind, either expressed, implied or statutory, including but not limited

EMV : Frequently Asked Questions for Merchants The information in this document is offered on an as is basis, without warranty of any kind, either expressed, implied or statutory, including but not limited

Emerging Trends in the Payment Ecosystem: The Good, the Bad and the Ugly DAN KRAMER

Emerging Trends in the Payment Ecosystem: The Good, the Bad and the Ugly DAN KRAMER SHAZAM, Senior Vice President Agenda The Ugly Fraud The Bad EMV? The Good Tokenization and Other Emerging Payment Options

Emerging Trends in the Payment Ecosystem: The Good, the Bad and the Ugly DAN KRAMER SHAZAM, Senior Vice President Agenda The Ugly Fraud The Bad EMV? The Good Tokenization and Other Emerging Payment Options

Flexible and secure. acceo tender retail. payment solution. tender-retail.acceo.com

Flexible and secure payment solution acceo tender retail payment solution tender-retail.acceo.com Take control of your payment transactions ACCEO Tender Retail is a specialized middleware that handles

Flexible and secure payment solution acceo tender retail payment solution tender-retail.acceo.com Take control of your payment transactions ACCEO Tender Retail is a specialized middleware that handles

COLUMBUS STATE COMMUNITY COLLEGE POLICY AND PROCEDURES MANUAL

PAYMENT CARD INDUSTRY COMPLIANCE (PCI) Effective June 1, 2011 Page 1 of 6 (1) Definitions a. Payment Card Industry Data Security Standards (PCI-DSS): A set of standards established by the Payment Card

PAYMENT CARD INDUSTRY COMPLIANCE (PCI) Effective June 1, 2011 Page 1 of 6 (1) Definitions a. Payment Card Industry Data Security Standards (PCI-DSS): A set of standards established by the Payment Card

Merchant Processing. Trends and Truths. Roger Raney TransFirst Regional Sales Manager rraney@transfirst.com 941.704.5858

Merchant Processing Trends and Truths Karen Miles US Rice Producers Association Financial Director karen@usriceproducers.com 713.974.7423 Roger Raney TransFirst Regional Sales Manager rraney@transfirst.com

Merchant Processing Trends and Truths Karen Miles US Rice Producers Association Financial Director karen@usriceproducers.com 713.974.7423 Roger Raney TransFirst Regional Sales Manager rraney@transfirst.com

EMV Frequently Asked Questions for Merchants May, 2014

EMV Frequently Asked Questions for Merchants May, 2014 Copyright 2014 Vantiv All rights reserved. Disclaimer The information in this document is offered on an as is basis, without warranty of any kind,

EMV Frequently Asked Questions for Merchants May, 2014 Copyright 2014 Vantiv All rights reserved. Disclaimer The information in this document is offered on an as is basis, without warranty of any kind,

What Merchants Need to Know About EMV

Effective November 1, 2014 1. What is EMV? EMV is the global standard for card present payment processing technology and it s coming to the U.S. EMV uses an embedded chip in the card that holds all the

Effective November 1, 2014 1. What is EMV? EMV is the global standard for card present payment processing technology and it s coming to the U.S. EMV uses an embedded chip in the card that holds all the

Saint Louis University Merchant Card Processing Policy & Procedures

Saint Louis University Merchant Card Processing Policy & Procedures Overview: Policies and procedures for processing credit card transactions and properly storing credit card data physically and electronically.

Saint Louis University Merchant Card Processing Policy & Procedures Overview: Policies and procedures for processing credit card transactions and properly storing credit card data physically and electronically.

Cash 257 Merchant Services and Revenue Collection

CPIM Academy Cash 257 Merchant Services and Revenue Collection 2015 Objectives Feel prepared to discuss/understand basics of merchant processing Understand Service Fees Difference between credit and debit

CPIM Academy Cash 257 Merchant Services and Revenue Collection 2015 Objectives Feel prepared to discuss/understand basics of merchant processing Understand Service Fees Difference between credit and debit

Payment Methods. The cost of doing business. Michelle Powell - BASYS Processing, Inc.

Payment Methods The cost of doing business Michelle Powell - BASYS Processing, Inc. You ve got to spend money, to make money Major Industry Topics Industry Process Flow PCI DSS Compliance Risks of Non-Compliance

Payment Methods The cost of doing business Michelle Powell - BASYS Processing, Inc. You ve got to spend money, to make money Major Industry Topics Industry Process Flow PCI DSS Compliance Risks of Non-Compliance

Fiscal Service EMV Education Series EMV-Compliant Point-of-Sale Card Acceptance for Federal Agencies. Fiscal Service / Vantiv July 27, 2015

Fiscal Service EMV Education Series EMV-Compliant Point-of-Sale Card Acceptance for Federal Agencies Fiscal Service / Vantiv July 27, 2015 Disclaimer: This communication, including any content herein and/or

Fiscal Service EMV Education Series EMV-Compliant Point-of-Sale Card Acceptance for Federal Agencies Fiscal Service / Vantiv July 27, 2015 Disclaimer: This communication, including any content herein and/or

U.S. Bank. U.S. Bank Chip Card FAQs for Program Administrators. In this guide you will find: Explaining Chip Card Technology (EMV)

") U.S. Bank U.S. Bank Chip Card FAQs for Program Administrators Here are some frequently asked questions Program Administrators have about the replacement of U.S. Bank commercial cards with new chip-enabled

U.S. Bank U.S. Bank Chip Card FAQs for Program Administrators Here are some frequently asked questions Program Administrators have about the replacement of U.S. Bank commercial cards with new chip-enabled

EMV FAQs. Contact us at: CS@VancoPayments.com. Visit us online: VancoPayments.com

EMV FAQs Contact us at: CS@VancoPayments.com Visit us online: VancoPayments.com What are the benefits of EMV cards to merchants and consumers? What is EMV? The acronym EMV stands for an organization formed

EMV FAQs Contact us at: CS@VancoPayments.com Visit us online: VancoPayments.com What are the benefits of EMV cards to merchants and consumers? What is EMV? The acronym EMV stands for an organization formed

6-8065 Payment Card Industry Compliance

0 0 0 Yosemite Community College District Policies and Administrative Procedures No. -0 Policy -0 Payment Card Industry Compliance Yosemite Community College District will comply with the Payment Card

0 0 0 Yosemite Community College District Policies and Administrative Procedures No. -0 Policy -0 Payment Card Industry Compliance Yosemite Community College District will comply with the Payment Card

Platinum and Platinum Rewards Visa EMV Credit Cards Frequently Asked Questions (FAQ s)

") Platinum and Platinum Rewards Visa EMV Credit Cards Frequently Asked Questions (FAQ s) What is EMV? EMV stands for Europay, MasterCard and Visa. EMV or chip cards have been in use in Europe for over 20

Platinum and Platinum Rewards Visa EMV Credit Cards Frequently Asked Questions (FAQ s) What is EMV? EMV stands for Europay, MasterCard and Visa. EMV or chip cards have been in use in Europe for over 20

Practically Thinking: What Small Merchants Should Know about EMV

Practically Thinking: What Small Merchants Should Know about EMV 1 Practically Thinking: What Small Merchants Should Know About EMV Overview Savvy business owners know that payments are about more than

Practically Thinking: What Small Merchants Should Know about EMV 1 Practically Thinking: What Small Merchants Should Know About EMV Overview Savvy business owners know that payments are about more than

Phone: (541)447-5627 FAX: (541) 447-5628 Web Site: www.cityofprineville.com

447-5627 FAX: (541) 447-5628 Web Site: www.cityofprineville.com") City of Prineville 387 NE THIRD STREET PRINEVILLE, OREGON 97754 Phone: (541)447-5627 FAX: (541) 447-5628 Web Site: www.cityofprineville.com January 26, 2015 ADDENDUM # 3 - RFP# 1002-13-14 TITLE: Banking

City of Prineville 387 NE THIRD STREET PRINEVILLE, OREGON 97754 Phone: (541)447-5627 FAX: (541) 447-5628 Web Site: www.cityofprineville.com January 26, 2015 ADDENDUM # 3 - RFP# 1002-13-14 TITLE: Banking

International Remittances

December 2008 International Remittances by Terri Bradford, Payments System Research Specialist oney may or may not make the world go around, but it certainly makes its way around the world. The World Bank

December 2008 International Remittances by Terri Bradford, Payments System Research Specialist oney may or may not make the world go around, but it certainly makes its way around the world. The World Bank

The Impact of Emerging Payment Technologies on Retail and Hospitality Businesses. National Computer Corporation www.nccusa.com

The Impact of Emerging Payment Technologies on Retail and Hospitality Businesses The Impact of Emerging Payment Technologies on Retail and Hospitality Businesses Making the customer payment process convenient,

The Impact of Emerging Payment Technologies on Retail and Hospitality Businesses The Impact of Emerging Payment Technologies on Retail and Hospitality Businesses Making the customer payment process convenient,

PCI 3.1 Changes. Jon Bonham, CISA Coalfire System, Inc.

PCI 3.1 Changes Jon Bonham, CISA Coalfire System, Inc. Agenda Introduction of Coalfire What does this have to do with the business office Changes to version 3.1 EMV P2PE Questions and Answers Contact Information

PCI 3.1 Changes Jon Bonham, CISA Coalfire System, Inc. Agenda Introduction of Coalfire What does this have to do with the business office Changes to version 3.1 EMV P2PE Questions and Answers Contact Information

TREASURER S OFFICE ADMINISTRATIVE STANDARDS FOR THE TREASURER S FISCAL PROCEDURE No. 08-01 MERCHANT DEBIT AND CREDIT CARD RECEIPTS

TREASURER S OFFICE ADMINISTRATIVE STANDARDS FOR THE TREASURER S FISCAL PROCEDURE No. 08-01 MERCHANT DEBIT AND CREDIT CARD RECEIPTS 1. Introduction Debit and Credit Card Receipt Standards apply to the administration

TREASURER S OFFICE ADMINISTRATIVE STANDARDS FOR THE TREASURER S FISCAL PROCEDURE No. 08-01 MERCHANT DEBIT AND CREDIT CARD RECEIPTS 1. Introduction Debit and Credit Card Receipt Standards apply to the administration

Secure Payments Framework Workgroup

Secure Payments Framework Workgroup EMV for the US Hospitality Industry Version 1.0 About HTNG Hotel Technology Next Generation (HTNG) is a non-profit association with a mission to foster, through collaboration

Secure Payments Framework Workgroup EMV for the US Hospitality Industry Version 1.0 About HTNG Hotel Technology Next Generation (HTNG) is a non-profit association with a mission to foster, through collaboration

CPIM Academy. Cash 257 Merchant Services and Revenue Collection

CPIM Academy Cash 257 Merchant Services and Revenue Collection 2015 Objectives Feel prepared to discuss/understand basics of merchant processing Understand Service Fees Difference between credit and debit

CPIM Academy Cash 257 Merchant Services and Revenue Collection 2015 Objectives Feel prepared to discuss/understand basics of merchant processing Understand Service Fees Difference between credit and debit

Apple Pay. Frequently Asked Questions UK Launch

Apple Pay Frequently Asked Questions UK Launch Version 1.0 2015 First Data Corporation. All Rights Reserved. All trademarks, service marks and trade names referenced in this material are the property of

Apple Pay Frequently Asked Questions UK Launch Version 1.0 2015 First Data Corporation. All Rights Reserved. All trademarks, service marks and trade names referenced in this material are the property of

Mobile Payment Solutions: Best Practices and Guidelines

Presented by the Mobile Payments Committee of the Electronic Transactions Association Mobile Payment Solutions: Best Practices and Guidelines ETA s Best Practices and Guidelines for Mobile Payment Solutions

Presented by the Mobile Payments Committee of the Electronic Transactions Association Mobile Payment Solutions: Best Practices and Guidelines ETA s Best Practices and Guidelines for Mobile Payment Solutions

How To Comply With The New Credit Card Chip And Pin Card Standards

My main responsibility as a Regional Account Manager for IMD is obtain the absolute lowest possible merchant fees for you as a business. Why? The more customers we can save money, the more volume of business

My main responsibility as a Regional Account Manager for IMD is obtain the absolute lowest possible merchant fees for you as a business. Why? The more customers we can save money, the more volume of business

Friday, June 5, 2015 3:15 p.m.

MCUL & Affiliates 2015 Annual Convention and Exposition Mobile Payments Greatest Opportunity or Biggest Threat? Amy Smith, AAP, CAE President & CEO The Payments Authority Friday, June 5, 2015 3:15 p.m.

MCUL & Affiliates 2015 Annual Convention and Exposition Mobile Payments Greatest Opportunity or Biggest Threat? Amy Smith, AAP, CAE President & CEO The Payments Authority Friday, June 5, 2015 3:15 p.m.

How To Control Credit Card And Debit Card Payments In Wisconsin

BACKGROUND State of Wisconsin agencies accepted more than 6 million credit/debit card payments annually through the following payment channels: Point of Sale (State agency location) Point of Sale (Retail-agent

BACKGROUND State of Wisconsin agencies accepted more than 6 million credit/debit card payments annually through the following payment channels: Point of Sale (State agency location) Point of Sale (Retail-agent

Policies and Procedures. Merchant Card Services Office of Treasury Operations

Policies and Procedures Merchant Card Services Office of Treasury Operations 1 Welcome! Table of Contents: Introduction Establishing Payment Card Services Payment Card Acceptance Procedures Payment Card

Policies and Procedures Merchant Card Services Office of Treasury Operations 1 Welcome! Table of Contents: Introduction Establishing Payment Card Services Payment Card Acceptance Procedures Payment Card

Merchant Services Payment Solutions for Your Business

Merchant Services Payment Solutions for Your Business Products & Services Highlights Processing Solutions VISA, MC, Discover, JCB, Diners, American Express, China UnionPay Multi Currency Cross Border Dynamic

Merchant Services Payment Solutions for Your Business Products & Services Highlights Processing Solutions VISA, MC, Discover, JCB, Diners, American Express, China UnionPay Multi Currency Cross Border Dynamic

NEWS BULLETIN 2015-16

NEWS BULLETIN Maine Automobile Dealers Association 180 Civic Center Drive P. O. Box 2667 Augusta, Maine 04338-2667 DIAL 623-3882 e-mail:info@maineautodealers.com FAX 623-2318 DISTRIBUTION General Manager

NEWS BULLETIN Maine Automobile Dealers Association 180 Civic Center Drive P. O. Box 2667 Augusta, Maine 04338-2667 DIAL 623-3882 e-mail:info@maineautodealers.com FAX 623-2318 DISTRIBUTION General Manager

Target Security Breach

Target Security Breach Lessons Learned for Retailers and Consumers 2014 Pointe Solutions, Inc. PO Box 41, Exton, PA 19341 USA +1 610 524 1230 Background In the aftermath of the Target breach that affected

Target Security Breach Lessons Learned for Retailers and Consumers 2014 Pointe Solutions, Inc. PO Box 41, Exton, PA 19341 USA +1 610 524 1230 Background In the aftermath of the Target breach that affected

FOR A BARRIER-FREE PAYMENT PROCESSING SOLUTION

FOR A BARRIER-FREE PAYMENT PROCESSING SOLUTION MAKE THE SWITCH TO MONEXgroup ecommerce I Mobile I Wireless I Integrated I Countertop Solutions PAYMENTS IN-STORE PAYMENTS ON-THE-GO PAYMENTS ONLINE Accept

FOR A BARRIER-FREE PAYMENT PROCESSING SOLUTION MAKE THE SWITCH TO MONEXgroup ecommerce I Mobile I Wireless I Integrated I Countertop Solutions PAYMENTS IN-STORE PAYMENTS ON-THE-GO PAYMENTS ONLINE Accept

How To Get A Checking Account In The United States

Date Here Welcome University of Michigan International Students U.S. Banking System Overview Banking is regulated by federal and state governments Privacy Disclosure Fraud protection Protection against

Date Here Welcome University of Michigan International Students U.S. Banking System Overview Banking is regulated by federal and state governments Privacy Disclosure Fraud protection Protection against

Beginner s Guide to Point of Sale

Beginner s Guide to Point of Sale Are you looking to purchase your first restaurant POS system? Interested in switching to a new restaurant POS? Enjoy reading online guides with informative graphics? Our

Beginner s Guide to Point of Sale Are you looking to purchase your first restaurant POS system? Interested in switching to a new restaurant POS? Enjoy reading online guides with informative graphics? Our

SELLING PAYMENT SYSTEMS SERVICES & SOLUTIONS

SELLING PAYMENT SYSTEMS SERVICES & SOLUTIONS A RESELLER S GUIDE CONTENTS New Sales Opportunities : EMV Mandate Means New Business... 3 New POS Will Need Both EMV and PCI... 3 Growing Demand for NFC Transactions...

SELLING PAYMENT SYSTEMS SERVICES & SOLUTIONS A RESELLER S GUIDE CONTENTS New Sales Opportunities : EMV Mandate Means New Business... 3 New POS Will Need Both EMV and PCI... 3 Growing Demand for NFC Transactions...

Mobile Near-Field Communications (NFC) Payments

Payments") Mobile Near-Field Communications (NFC) Payments OCTOBER 2013 GENERAL INFORMATION American Express continues to develop its infrastructure and capabilities to support growing market interest in mobile payments

Mobile Near-Field Communications (NFC) Payments OCTOBER 2013 GENERAL INFORMATION American Express continues to develop its infrastructure and capabilities to support growing market interest in mobile payments

What is EMV? What is different?

U.S. consumers are receiving new debit and credit cards with embedded chip technology that better stores and protects cardholder information. These new chip cards are part of the new card standard, Europay,

U.S. consumers are receiving new debit and credit cards with embedded chip technology that better stores and protects cardholder information. These new chip cards are part of the new card standard, Europay,

EMV and Chip Cards Key Information On What This Is, How It Works and What It Means

EMV and Chip Cards Key Information On What This Is, How It Works and What It Means Document Purpose This document is intended to provide information about the concepts behind and the processes involved

EMV and Chip Cards Key Information On What This Is, How It Works and What It Means Document Purpose This document is intended to provide information about the concepts behind and the processes involved

Planning For EMV Technology. Your Guide to Making the Transition

Planning For EMV Technology Your Guide to Making the Transition Table of Contents What is EMV? How does it work? Why is it happening? Who will be affected? Is POS terminal replacement necessary? Is this

Planning For EMV Technology Your Guide to Making the Transition Table of Contents What is EMV? How does it work? Why is it happening? Who will be affected? Is POS terminal replacement necessary? Is this

Merchant Payment Card Processing Guidelines

Merchant Payment Card Processing Guidelines The following is intended to provide guidance that departments or units can use to help develop specific procedures for their department or unit. If you have

Merchant Payment Card Processing Guidelines The following is intended to provide guidance that departments or units can use to help develop specific procedures for their department or unit. If you have

Visa Reloadable Frequently Asked Questions. EMV Travel Card

Visa Reloadable Frequently Asked Questions EMV Travel Card How does the International Prepaid Card work? The International Prepaid Card is a reloadable prepaid Visa debit card, which means you can spend

Visa Reloadable Frequently Asked Questions EMV Travel Card How does the International Prepaid Card work? The International Prepaid Card is a reloadable prepaid Visa debit card, which means you can spend

Fraud Protection, You and Your Bank

Fraud Protection, You and Your Bank Maximize your chances to minimize your losses Presentation for Missouri GFOA April 2011 By: Terry Endres, VP, Government Treasury Solutions Phone: 314-466-6774 Terry.m.endres@baml.com

Fraud Protection, You and Your Bank Maximize your chances to minimize your losses Presentation for Missouri GFOA April 2011 By: Terry Endres, VP, Government Treasury Solutions Phone: 314-466-6774 Terry.m.endres@baml.com

EMV EMV TABLE OF CONTENTS

2 TABLE OF CONTENTS Intro... 2 Are You Ready?... 3 What Is?... 4 Why?... 5 What Does Mean To Your Business?... 6 Checklist... 8 3 U.S. Merchants 60% are expected to convert to -enabled devices by 2015.

2 TABLE OF CONTENTS Intro... 2 Are You Ready?... 3 What Is?... 4 Why?... 5 What Does Mean To Your Business?... 6 Checklist... 8 3 U.S. Merchants 60% are expected to convert to -enabled devices by 2015.

PCI Risks and Compliance Considerations

PCI Risks and Compliance Considerations July 21, 2015 Stephen Ramminger, Senior Business Operations Manager, ControlScan Jon Uyterlinde, Product Manager, Merchant Services, SVB Agenda 1 2 3 4 5 6 7 8 Introduction

PCI Risks and Compliance Considerations July 21, 2015 Stephen Ramminger, Senior Business Operations Manager, ControlScan Jon Uyterlinde, Product Manager, Merchant Services, SVB Agenda 1 2 3 4 5 6 7 8 Introduction

University Policy Accepting Credit Cards to Conduct University Business

BROWN UNIVERSITY University Policy Accepting Credit Cards to Conduct University Business Purpose Brown University requires all departments that are involved with credit card handling to do so in compliance

BROWN UNIVERSITY University Policy Accepting Credit Cards to Conduct University Business Purpose Brown University requires all departments that are involved with credit card handling to do so in compliance

SETUP GUIDE. Thank you for your purchase of Hamilton products! In this handy guide, you will discover: ADDITIONAL REQUIREMENTS SETUP HOW IT WORKS

SETUP GUIDE High Speed Secure Credit Card Processing Thank you for your purchase of Hamilton products! In this handy guide, you will discover: WHAT IS INCLUDED ADDITIONAL REQUIREMENTS HOW IT WORKS SETUP

SETUP GUIDE High Speed Secure Credit Card Processing Thank you for your purchase of Hamilton products! In this handy guide, you will discover: WHAT IS INCLUDED ADDITIONAL REQUIREMENTS HOW IT WORKS SETUP

FUTURE PROOF TERMINAL QUICK REFERENCE GUIDE. Review this Quick Reference Guide to. learn how to run a sale, settle your batch

QUICK REFERENCE GUIDE FUTURE PROOF TERMINAL Review this Quick Reference Guide to learn how to run a sale, settle your batch and troubleshoot terminal responses. INDUSTRY Retail and Restaurant APPLICATION

QUICK REFERENCE GUIDE FUTURE PROOF TERMINAL Review this Quick Reference Guide to learn how to run a sale, settle your batch and troubleshoot terminal responses. INDUSTRY Retail and Restaurant APPLICATION

Payment Processing considerations to comply with IRS and PCI-DSS regulations and policies

itransact Presents Payment Processing considerations to comply with IRS and PCI-DSS regulations and policies Learning Objectives At the end of this course you will be able to: Prepare for IRS 6050w and

itransact Presents Payment Processing considerations to comply with IRS and PCI-DSS regulations and policies Learning Objectives At the end of this course you will be able to: Prepare for IRS 6050w and

Sending money abroad. Plain text guide

Sending money abroad Plain text guide Contents Introduction 2 Ways to make international payments 3 Commonly asked questions 5 What is the cost to me of sending money abroad? 5 What is the cost to the

Sending money abroad Plain text guide Contents Introduction 2 Ways to make international payments 3 Commonly asked questions 5 What is the cost to me of sending money abroad? 5 What is the cost to the

OpenEdge Research & Development Group April 2015

2015: Development, Merchant Readiness & the Coming Liability Shift OpenEdge Research & Development Group April 2015 developers@openedgepay.com openedgepay.com 2015: Development, Merchant Table of Contents

2015: Development, Merchant Readiness & the Coming Liability Shift OpenEdge Research & Development Group April 2015 developers@openedgepay.com openedgepay.com 2015: Development, Merchant Table of Contents

Apple Pay. Frequently Asked Questions UK

Apple Pay Frequently Asked Questions UK Version 1.0 (July 2015) First Data Merchant Solutions is a trading name of First Data Europe Limited, a private limited company incorporated in England (company

Apple Pay Frequently Asked Questions UK Version 1.0 (July 2015) First Data Merchant Solutions is a trading name of First Data Europe Limited, a private limited company incorporated in England (company

Introductions 1 min 4

1 2 1 Minute 3 Introductions 1 min 4 5 2 Minutes Briefly Introduce the topics for discussion. We will have time for Q and A following the webinar. 6 Randy - EMV History / Chip Cards /Terminals 5 Minutes

1 2 1 Minute 3 Introductions 1 min 4 5 2 Minutes Briefly Introduce the topics for discussion. We will have time for Q and A following the webinar. 6 Randy - EMV History / Chip Cards /Terminals 5 Minutes

GLOSSARY OF MOST COMMONLY USED TERMS IN THE MERCHANT SERVICES INDUSTRY

GLOSSARY OF MOST COMMONLY USED TERMS IN THE MERCHANT SERVICES INDUSTRY Acquiring Bank The bank or financial institution that accepts credit and/or debit card payments for products or services on behalf

GLOSSARY OF MOST COMMONLY USED TERMS IN THE MERCHANT SERVICES INDUSTRY Acquiring Bank The bank or financial institution that accepts credit and/or debit card payments for products or services on behalf

PCI DSS Compliance Services January 2016

PCI DSS Compliance Services January 2016 20160104-Galitt-PCI DSS Compliance Services.pptx Agenda 1. Introduction 2. Overview of the PCI DSS standard 3. PCI DSS compliance approach Copyright Galitt 2 Introduction

PCI DSS Compliance Services January 2016 20160104-Galitt-PCI DSS Compliance Services.pptx Agenda 1. Introduction 2. Overview of the PCI DSS standard 3. PCI DSS compliance approach Copyright Galitt 2 Introduction

FOR A BARRIER-FREE PAYMENT PROCESSING SOLUTION

FOR A BARRIER-FREE PAYMENT PROCESSING SOLUTION MAKE THE SWITCH TO MONEXgroup ecommerce I Mobile I Wireless I Integrated I Countertop Solutions IN-STORE ON-THE-GO ONLINE Accept secure debit and credit card

FOR A BARRIER-FREE PAYMENT PROCESSING SOLUTION MAKE THE SWITCH TO MONEXgroup ecommerce I Mobile I Wireless I Integrated I Countertop Solutions IN-STORE ON-THE-GO ONLINE Accept secure debit and credit card

U.S. Mobile Payments Landscape NCSL Legislative Summit 2013

U.S. Mobile Payments Landscape NCSL Legislative Summit 2013 Marianne Crowe Vice President, Payment Strategies Federal Reserve Bank of Boston August 13, 2013 2 Agenda Overview of Mobile Payments Landscape

U.S. Mobile Payments Landscape NCSL Legislative Summit 2013 Marianne Crowe Vice President, Payment Strategies Federal Reserve Bank of Boston August 13, 2013 2 Agenda Overview of Mobile Payments Landscape

Card Technology Choices for U.S. Issuers An EMV White Paper

Card Technology Choices for U.S. Issuers An EMV White Paper This white paper is written with the aim of educating Issuers in the United States on the various technology choices that they have to consider

Card Technology Choices for U.S. Issuers An EMV White Paper This white paper is written with the aim of educating Issuers in the United States on the various technology choices that they have to consider

Security. Tiffany Trent-Abram VP, Global Product Management. November 6 th, 2015. One Connection - A World of Opportunities

One Connection - A World of Opportunities Security Tiffany Trent-Abram VP, Global Product Management November 6 th, 2015 2015 TNS Inc. All Rights Reserved. Bringing Global Credibility and History TNS Specializes

One Connection - A World of Opportunities Security Tiffany Trent-Abram VP, Global Product Management November 6 th, 2015 2015 TNS Inc. All Rights Reserved. Bringing Global Credibility and History TNS Specializes

Best practices for choosing and integrating a mobile payments platform. A GlobalOnePay White Paper

Best practices for choosing and integrating a mobile payments platform A GlobalOnePay White Paper Mobile commerce (mcommerce) purchases and in-app payments made on mobile devices are rapidly becoming just

Best practices for choosing and integrating a mobile payments platform A GlobalOnePay White Paper Mobile commerce (mcommerce) purchases and in-app payments made on mobile devices are rapidly becoming just

American Express Contactless Payments

PRODUCT CAPABILITY GUIDE American Express Contactless Payments American Express Contactless Payments Help Enable Increased Convenience For Card Members At The Point Of Sale American Express contactless

PRODUCT CAPABILITY GUIDE American Express Contactless Payments American Express Contactless Payments Help Enable Increased Convenience For Card Members At The Point Of Sale American Express contactless

Corbin Del Carlo Director, National Leader PCI Services. October 5, 2015

PCI compliance: v3.1 Key Considerations Corbin Del Carlo Director, National Leader PCI Services October 5, 2015 Today s Presenter Corbin Del Carlo QSA, PA QSA Director, National Leader PCI Services Practice

PCI compliance: v3.1 Key Considerations Corbin Del Carlo Director, National Leader PCI Services October 5, 2015 Today s Presenter Corbin Del Carlo QSA, PA QSA Director, National Leader PCI Services Practice

bi on Solution white paper

bi on Solution white paper Billon Solution Overview Despite concerted efforts for years, cash has not yet been eliminated. Mostly because not everyone has a bank account and debit card - an estimated 2.5

bi on Solution white paper Billon Solution Overview Despite concerted efforts for years, cash has not yet been eliminated. Mostly because not everyone has a bank account and debit card - an estimated 2.5

Guideline on Debit or Credit Cards Usage

CMSGu2012-04 Mauritian Computer Emergency Response Team CERT-MU SECURITY GUIDELINE 2011-02 Enhancing Cyber Security in Mauritius Guideline on Debit or Credit Cards Usage National Computer Board Mauritius

CMSGu2012-04 Mauritian Computer Emergency Response Team CERT-MU SECURITY GUIDELINE 2011-02 Enhancing Cyber Security in Mauritius Guideline on Debit or Credit Cards Usage National Computer Board Mauritius

Credit vs. Debit: The Network Perspective

July 25, 2010 Credit vs. Debit: The Network Perspective Richard Santoro, Vice President, Government Affairs MasterCard Worldwide 1 Overview Origins of Payment Cards Four-Party Payment System Model Anatomy

July 25, 2010 Credit vs. Debit: The Network Perspective Richard Santoro, Vice President, Government Affairs MasterCard Worldwide 1 Overview Origins of Payment Cards Four-Party Payment System Model Anatomy

Chip Card (EMV ) CAL-Card FAQs

CAL-Card FAQs") U.S. Bank Chip Card (EMV ) CAL-Card FAQs Below are answers to some frequently asked questions about the migration to U.S. Bank chipenabled CAL-Cards. This guide can help ensure that you are prepared for

U.S. Bank Chip Card (EMV ) CAL-Card FAQs Below are answers to some frequently asked questions about the migration to U.S. Bank chipenabled CAL-Cards. This guide can help ensure that you are prepared for

The 12 Essentials of PCI Compliance How it Differs from HIPPA Compliance Understand & Implement Effective PCI Data Security Standard Compliance

Date: 07/19/2011 The 12 Essentials of PCI Compliance How it Differs from HIPPA Compliance Understand & Implement Effective PCI Data Security Standard Compliance PCI and HIPAA Compliance Defined Understand

Date: 07/19/2011 The 12 Essentials of PCI Compliance How it Differs from HIPPA Compliance Understand & Implement Effective PCI Data Security Standard Compliance PCI and HIPAA Compliance Defined Understand

Pima Federal Visa Credit Cards Frequently Asked Questions (FAQs)

") Pima Federal Visa Credit Cards Frequently Asked Questions (FAQs) (Effective May 2013) APPLICATION PROCESS Q: Who can apply for a Pima Federal Visa Credit Card? A: Any member of Pima Federal is eligible

Pima Federal Visa Credit Cards Frequently Asked Questions (FAQs) (Effective May 2013) APPLICATION PROCESS Q: Who can apply for a Pima Federal Visa Credit Card? A: Any member of Pima Federal is eligible

The need for a secure & trusted payment instrument in e-commerce. Ali AlMeshal

The need for a secure & trusted payment instrument in e-commerce Ali AlMeshal In Physical/Real World Hand over card Visual check Swipe in POS Online authorization Receipt with signature panel Sign or Pin

The need for a secure & trusted payment instrument in e-commerce Ali AlMeshal In Physical/Real World Hand over card Visual check Swipe in POS Online authorization Receipt with signature panel Sign or Pin

Credit Card Processing Overview

CardControl 3.0 Credit Card Processing Overview Overview Credit card processing is a very complex and important system for anyone that sells goods. This guide will hopefully help educate and inform new

CardControl 3.0 Credit Card Processing Overview Overview Credit card processing is a very complex and important system for anyone that sells goods. This guide will hopefully help educate and inform new

U.S. House Small Business Committee. On Behalf of the National Grocers Association. October 6, 2015

U.S. House Small Business Committee On Behalf of the National Grocers Association October 6, 2015 The National Grocers Association (NGA) appreciates the opportunity to submit comments for the record to

U.S. House Small Business Committee On Behalf of the National Grocers Association October 6, 2015 The National Grocers Association (NGA) appreciates the opportunity to submit comments for the record to

QUICK REFERENCE CHIP CARD TRANSACTION

QUICK REFERENCE CHIP CARD TRANSACTION Hypercom/Verifone T-42 POS Point of Sale Terminal Ver. 0413.1 PROCESS A WITH CHIP CARD The terminal screen will display The terminal is ready to process a different

QUICK REFERENCE CHIP CARD TRANSACTION Hypercom/Verifone T-42 POS Point of Sale Terminal Ver. 0413.1 PROCESS A WITH CHIP CARD The terminal screen will display The terminal is ready to process a different

Solutions For Higher Education: Reducing Compliance Scope Across Campus With PCI Validated P2PE

Solutions For Higher Education: Reducing Compliance Scope Across Campus With PCI Validated P2PE Complete Campus Coverage With the complexity of a college campus ecosystem as varied as the development office

Solutions For Higher Education: Reducing Compliance Scope Across Campus With PCI Validated P2PE Complete Campus Coverage With the complexity of a college campus ecosystem as varied as the development office

GRINNELL COLLEGE CREDIT CARD PROCESSING AND SECURITY POLICY

GRINNELL COLLEGE CREDIT CARD PROCESSING AND SECURITY POLICY PURPOSE The Payment Card Industry Data Security Standard was established by the credit card industry in response to an increase in identify theft

GRINNELL COLLEGE CREDIT CARD PROCESSING AND SECURITY POLICY PURPOSE The Payment Card Industry Data Security Standard was established by the credit card industry in response to an increase in identify theft