BEST PRACTICES IN ACCOUNTS PAYABLE

|

|

|

- Godfrey Thornton

- 8 years ago

- Views:

Transcription

1 Financial Management Program BEST PRACTICES IN ACCOUNTS PAYABLE GASBO 2015 Tracy Arner, CPA 1

2 Objectives At the end of this session, the participant will be able to - Discuss the definition of accounts payable Recall components of internal control Recite best practices for accounts payable within a strong internal control framework 2

3 Accounts Payable Defined 3

4 What is Accounts Payable? The principle purpose of any accounts payable department is to pay the government s bills. Continued on next slide 4

5 What is Accounts Payable Unpaid bills are listed under Accounts Payable on the General Ledger. Any money owed as an account payable is a current liability. Money owed must be paid in a timely manner to avoid late penalties or fees. Some vendors offer discounts for paying within a certain number of days of the invoice date. 5

6 Accounts Payable Department An accounting department dedicated to verifying, tracking, and paying all accounts payable. Continued on next slide 6

7 Accounts Payable Department Handles all accounts payable in timely manner Follows a system of checks and balances. Uses many tools to assist with tracking accounts payable functions. Modern technology = paperless system; affordable scanners and computers; accounts payable software makes tracking and paying accounts a seamless process with little margin for error or duplication. 7

8 Accounts Payable The Liability The accounts payable account on the general ledger is classified as a liability something that is owed for Example: office supplies are bought on credit Continued on next slide 8

9 Accounts Payable The Liability Example: check issued for the office supplies 9

10 Accounts Payable and Internal Control 10

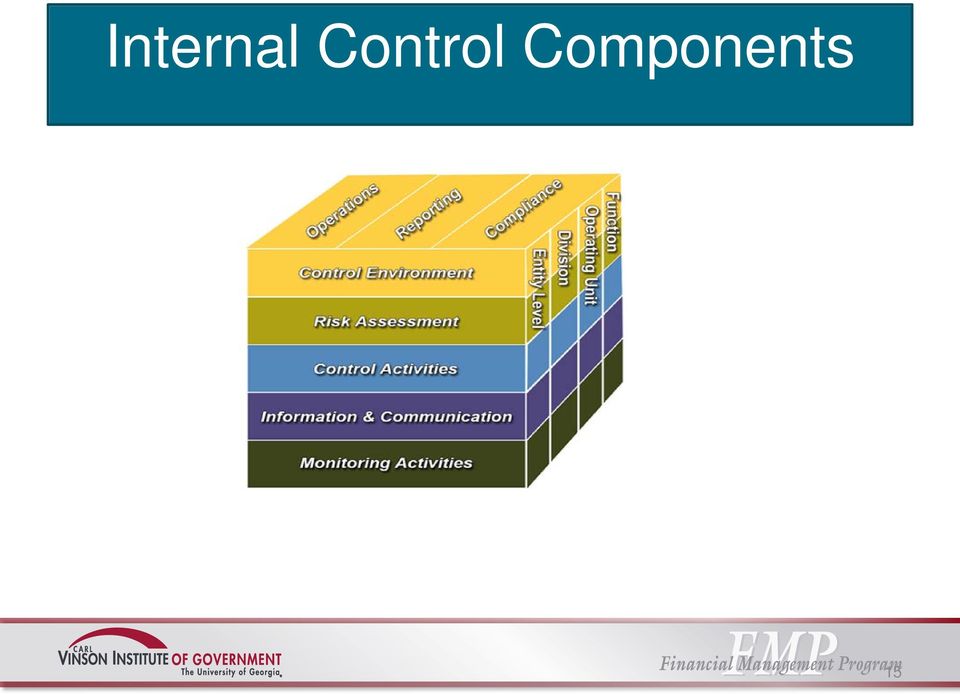

11 COSO Committee of Sponsoring Organizations 11

12 COSO s Internal Control Definition Internal control is a process, effected by an entity s board of directors, management and other personnel, designed to provide reasonable assurance regarding the achievement of objectives in the following categories: Continued on next slide 12

13 COSO s Internal Control Definition Effectiveness and efficiency of operations Reliability of Reporting Compliance with applicable laws and regulations 13

14 Objectives for Accounts Payable Preapproved A/P transactions A/P transactions recorded in proper period (cutoff) Transactions accurate and recorded in timely manner Recorded A/P transactions represent events that occurred and are in accordance with management s authorization A/P and vendor records are controlled and restricted to authorized personnel Duties are assigned so that no one individual can control recording and processing transactions 14

15 Internal Control Components 15

16 Control Environment and A/P Control environment affects accounts payable by establishing protocols: Published code of ethics communicated with employees. Personnel hired that possess the knowledge and skills to accomplish A/P tasks. Job descriptions that provide for proper segregation of duties for responsibility and authority. 16

17 Control Environment and A/P Control environment affects accounts payable by establishing protocols: Written procedures that cover all phases of accounts payable. Adequate training policies that communicate roles and responsibilities in the A/P area. Management should exhibit commitment for ongoing training of employees in the A/P area. 17

18 Risk Assessment and A/P Objective No. 1: All accounts payable transactions are preapproved. Written process for the establishment of a payable account, starting with a preapproved listing of vendors and the use of purchase orders. Continued on next slide 18

19 Risk Assessment and A/P Objective No. 2: All valid accounts payable transactions are included in the accounting records in the proper period. At the end of each accounting cycle, any vendor invoices should be recorded into the general ledger in the period in which the goods and/or services were received. Continued on next slide 19

20 Risk Assessment and A/P Objective No. 3: All valid transactions are accurate, consistent with the originating transaction data, and information is recorded in a timely manner. Establish a schedule daily, weekly or monthly recording of accounts payable transactions to ensure all information is recorded in a timely manner. Continued on next slide 20

21 Risk Assessment and A/P Objective No. 4: All recorded accounts payable transactions fairly represent the economic events that actually occurred, are lawful in nature, and have been executed in accordance with management s general authorization. Have written policies concerning the purchase of goods and services. Continued on next slide 21

22 Risk Assessment and A/P Objective No. 5: Access to accounts payable and vendor records are controlled and properly restricted to authorized personnel. Safeguard accounts payable records. Continued on next slide 22

23 Risk Assessment and A/P Objective No. 6: Duties are assigned to individuals in a manner that ensures that no one individual can control both the recording function and the procedures relative to processing a transaction. Segregation of duties. 23

24 Duties to be Segregated Authorization Custody (Access to Asset) Approval of POs and invoices Approval of access to vendor master files Signing of checks Access to accounts payable checks/bank accounts (EFT) Mailing accounts payable checks Record Keeping Preparing source documents Maintaining journals, ledgers, or other files Reconciliations (Accountability) Preparing reconciliations 24

25 Control Activities Match invoice, receiving and purchase order information and follow up on missing or inconsistent information. Follow up on unmatched open purchase orders, receiving reports and invoices and resolve missing, duplicate or unmatched items, by individuals independent of purchasing and receiving functions. Use of control totals or one-for-one checking. Restrict access to accounts payable and files used in processing payables. Continued on next slide 25

26 Control Activities Reconcile vendor statements to accounts payable items. Resolve differences between the accounts payable subsidiary ledger and the accounts payable control account. Pay vendors only from original invoices supported by purchase and receiving documents. Continued on next slide 26

27 Control Activities Take discounts if appropriately approved. Purchases are authorized and in accordance with the school's approval levels. Record transaction accurately in the general ledger. Promptly perform Accounts Payable reconciliations for aging and clearing accounts and review reconciliations in a timely fashion. Continued on next slide 27

28 Control Activities Process invoices according to invoice payment terms. Route check requests to the appropriate personnel for review prior to input into accounts payable. Accurately record expenses in the accounting records during the period in which the liability was incurred. Continued on next slide 28

29 Control Activities Make payments made to preapproved vendors. That approval process should include identifying 1099 vendors in compliance with IRS regulations. Obtain affidavits for contractors providing services Research and resolve, if possible, old outstanding accounts payable checks including compliance with State laws and regulations regarding escheat property 29

30 Information and Communication Examples: and A/P Governing board/management: Aging of accounts payable. Internal customers: Discrepancies in vendor invoices. External customers: Discrepancies in vendor invoices. External auditors: Types of payables and amounts for financial statements. 30

31 Monitoring and A/P Supervisory activities: Initial and date face of reconciliation Review all changes to vendor information Supervisory approval for changes to invoice once entered into A/P system 31

32 Other Best Practices 32

33 P-Card Use Supporting documentation Policy Set limits Authorized users 33

34 NEW 1/1/2016 Purchasing card for elected officials New law effective 1/1/16 OCGA Governing authority must vote on issuance of card and create policy for use of the card 34

35 W-9 Set up vendors before any payments are made If not, vendor file incomplete 1099 s could be impossible to prepare and government could be assessed fines and penalties 35

36 OCGA (b)(1) All public employers in Georgia are required to collect a signed, notarized affidavit from any contractor who contracts with the local government for the physical performance of services Attorney General indicates a purchase order is a contract Affidavit must be maintained 5 years 36

37 Other Items Check vendors for debarred listing for federal grant expenditures Positive pay Set software controls to restrict access to authorized personnel 37

38 38

39 The Carl Vinson Institute of Government. All rights reserved.

CHAPTER 4 EFFECTIVE INTERNAL CONTROLS OVER PAYROLL

CHAPTER 4 EFFECTIVE INTERNAL CONTROLS OVER PAYROLL INTRODUCTION AND LEARNING OBJECTIVES Every organization, including governments, require employees to assist in meeting their goals and objectives. The

CHAPTER 4 EFFECTIVE INTERNAL CONTROLS OVER PAYROLL INTRODUCTION AND LEARNING OBJECTIVES Every organization, including governments, require employees to assist in meeting their goals and objectives. The

Chapter 15: Accounts Payable and Purchases

Accounting Research Manager - Audit Private Accounting Research Manager Miller Interpretations and Other Resources Knowledge-Based Audit Procedures Chapter 15: Accounts Payable and Purchases Chapter 15:

Accounting Research Manager - Audit Private Accounting Research Manager Miller Interpretations and Other Resources Knowledge-Based Audit Procedures Chapter 15: Accounts Payable and Purchases Chapter 15:

Guidelines for Congregations Internal Control Best Practices

Guidelines for Congregations Internal Control Best Practices A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America Congregations should establish and maintain

Guidelines for Congregations Internal Control Best Practices A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America Congregations should establish and maintain

Version Date: 10/16/2013

2004094 Accounting Documents (ADVANTAGE Financial System Input) This record series is used to input information into the ADVANTAGE Financial System. The files may contain, but are not limited to: copies

2004094 Accounting Documents (ADVANTAGE Financial System Input) This record series is used to input information into the ADVANTAGE Financial System. The files may contain, but are not limited to: copies

Stated below are the SCIRE activity level control objectives for purchasing and accounts payable.

SCIRE PURCHASING AND ACCOUNTS PAYABLE AND SUMMARY The goals of the purchasing function at SCIRE are to achieve open, competitive and costeffective buying, while adhering to external funding sources for

SCIRE PURCHASING AND ACCOUNTS PAYABLE AND SUMMARY The goals of the purchasing function at SCIRE are to achieve open, competitive and costeffective buying, while adhering to external funding sources for

Customer Credit and Accounts Receivable

Customer Credit and Accounts Receivable Gap Analysis: POS identifies the following Best Practices as efficient and effective control processes for the above risk. Listed for comparison are the controls

Customer Credit and Accounts Receivable Gap Analysis: POS identifies the following Best Practices as efficient and effective control processes for the above risk. Listed for comparison are the controls

Audit Program for Accounts Payable and Purchases

Form AP 50 Index Audit Program for Accounts Payable and Purchases Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding

Form AP 50 Index Audit Program for Accounts Payable and Purchases Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding

Review of Miscellaneous Income Reporting to the Internal Revenue Service

Review of Miscellaneous Income Reporting to the Internal Revenue Service July 19, 2010 Report No. 10-12 Office of the County Auditor Evan A. Lukic, CPA County Auditor Table of Contents Topic Page Executive

Review of Miscellaneous Income Reporting to the Internal Revenue Service July 19, 2010 Report No. 10-12 Office of the County Auditor Evan A. Lukic, CPA County Auditor Table of Contents Topic Page Executive

INTERNAL CONTROL QUESTIONNAIRE OFFICE OF INTERNAL AUDIT UNIVERSITY OF THE VIRGIN ISLANDS

Cabinet Member or Representative responsible for completing this form: INSTRUCTIONS FOR COMPLETING THIS FORM: Answer each question by placing an X in the either the Yes, No,, or Applicable () column. Provide

Cabinet Member or Representative responsible for completing this form: INSTRUCTIONS FOR COMPLETING THIS FORM: Answer each question by placing an X in the either the Yes, No,, or Applicable () column. Provide

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER Material Weaknesses (0) No material weaknesses were reported for FY 2013. Significant Deficiencies (1) Grant Receivable Accounting

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER Material Weaknesses (0) No material weaknesses were reported for FY 2013. Significant Deficiencies (1) Grant Receivable Accounting

Guidelines for Congregations Internal Control Best Practices

Guidelines for Congregations Internal Control Best Practices A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America In order to exercise good stewardship and care

Guidelines for Congregations Internal Control Best Practices A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America In order to exercise good stewardship and care

Chapter 15 Auditing the Expenditure Cycle

Chapter 15 Auditing the Expenditure Cycle Expenditure cycle consists of activities related to the acquisition of and payment for plant assets and goods and services. Two major transaction classes: 1 purchases

Chapter 15 Auditing the Expenditure Cycle Expenditure cycle consists of activities related to the acquisition of and payment for plant assets and goods and services. Two major transaction classes: 1 purchases

Florida A & M University

Florida A & M University AP PROCEDURES 3-8-2013 TABLE OF CONTENTS 1.0 OVERVIEW... 1 2.0 DEFINITIONS... 1 3.0 RESPONSIBILITIES... 2 4.0 GENERAL PROCEDURES... 3 4.1 DEPARTMENTAL FISCAL REPRESENTATIVES...

Florida A & M University AP PROCEDURES 3-8-2013 TABLE OF CONTENTS 1.0 OVERVIEW... 1 2.0 DEFINITIONS... 1 3.0 RESPONSIBILITIES... 2 4.0 GENERAL PROCEDURES... 3 4.1 DEPARTMENTAL FISCAL REPRESENTATIVES...

QuickBooks. Reports List 2013. Enterprise Solutions 14.0

QuickBooks Reports List 2013 Enterprise Solutions 14.0 Table of Contents Complete List of Reports... 5 Company & Financial Reports... 6 Profit & Loss... 6 Income & Expenses... 7 Balance Sheet & Net Worth...

QuickBooks Reports List 2013 Enterprise Solutions 14.0 Table of Contents Complete List of Reports... 5 Company & Financial Reports... 6 Profit & Loss... 6 Income & Expenses... 7 Balance Sheet & Net Worth...

Intuit QuickBooks Enterprise Solutions 10.0 Complete List of Reports

Intuit QuickBooks Enterprise Solutions 10.0 Complete List of Reports Intuit QuickBooks Enterprise Solutions, for growing businesses, is the most powerful QuickBooks product. It has the capabilities and

Intuit QuickBooks Enterprise Solutions 10.0 Complete List of Reports Intuit QuickBooks Enterprise Solutions, for growing businesses, is the most powerful QuickBooks product. It has the capabilities and

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY 1. Purpose The Dixon Montessori Charter School Board of Directors ( Board ) has reviewed and adopted the following policies and procedures to ensure

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY 1. Purpose The Dixon Montessori Charter School Board of Directors ( Board ) has reviewed and adopted the following policies and procedures to ensure

Internal Controls over Cash for Small Nonprofits

Internal Controls over Cash for Small Nonprofits Internal controls may be a sensitive issue in small nonprofit organizations. These organizations are built on the concepts of honesty, truthfulness, and

Internal Controls over Cash for Small Nonprofits Internal controls may be a sensitive issue in small nonprofit organizations. These organizations are built on the concepts of honesty, truthfulness, and

ACCOUNTING RECORDS AND SOURCE DOCUMENTATION

ACCOUNTING RECORDS AND SOURCE DOCUMENTATION May 1994 Introduction Criteria for Accounting Documents and Records Accounting Procedures Manual Chart of Accounts Nine Principles Governing Accounting Records

ACCOUNTING RECORDS AND SOURCE DOCUMENTATION May 1994 Introduction Criteria for Accounting Documents and Records Accounting Procedures Manual Chart of Accounts Nine Principles Governing Accounting Records

Accounts Payable. Best Practices: Existing Control: Control Gap: Controls Evaluation and Gap Analysis. Purchasing

Accounts Payable Gap Analysis: POS identifies the following Best Practices as efficient and effective control processes for the above risk. Listed for comparison are the controls currently in place, if

Accounts Payable Gap Analysis: POS identifies the following Best Practices as efficient and effective control processes for the above risk. Listed for comparison are the controls currently in place, if

Class Specification Accounts Payable/ Receivable Supervisor

Class Specification Accounts Payable/ Receivable Supervisor Summary Statement: The purpose of this position is to Supervise the Accounts Payable Division or Accounts Receivable Division of the Finance

Class Specification Accounts Payable/ Receivable Supervisor Summary Statement: The purpose of this position is to Supervise the Accounts Payable Division or Accounts Receivable Division of the Finance

MANAGEMENT AUDIT REPORT ACCOUNTS PAYABLE

MANAGEMENT AUDIT REPORT OF ACCOUNTS PAYABLE REPORT NO. 04-108 CITY OF ALBUQUERQUE OFFICE OF INTERNAL AUDIT AND INVESTIGATIONS of Accounts Payable Report No. 04-108 Executive Summary Background The Department

MANAGEMENT AUDIT REPORT OF ACCOUNTS PAYABLE REPORT NO. 04-108 CITY OF ALBUQUERQUE OFFICE OF INTERNAL AUDIT AND INVESTIGATIONS of Accounts Payable Report No. 04-108 Executive Summary Background The Department

C A R L E T O N U N I V E R S I T Y POSITION DESCRIPTION

C A R L E T O N U N I V E R S I T Y POSITION DESCRIPTION PART A OFFICER USE ONLY Employee Name: Title of Immediate Supervisor: Supervisor, Accounts Payable Position Title: Accounts Payable Administrator

C A R L E T O N U N I V E R S I T Y POSITION DESCRIPTION PART A OFFICER USE ONLY Employee Name: Title of Immediate Supervisor: Supervisor, Accounts Payable Position Title: Accounts Payable Administrator

UCLA Policy 360: Internal Control Guidelines for Campus Departments

UCLA Policy 360: Internal Control Guidelines for Campus Departments Issuing Officer: Assistant Vice Chancellor, Corporate Financial Services Responsible Dept: Financial Management Programs Effective Date:

UCLA Policy 360: Internal Control Guidelines for Campus Departments Issuing Officer: Assistant Vice Chancellor, Corporate Financial Services Responsible Dept: Financial Management Programs Effective Date:

Weaknesses in the Smithsonian Tropical Research Institute s Financial Management Require Prompt Attention

Weaknesses in the Smithsonian Tropical Research Institute s Financial Management Require Prompt Attention Office of the Inspector General Report Number A-13-01 October 29, 2013 INTRODUCTION This report

Weaknesses in the Smithsonian Tropical Research Institute s Financial Management Require Prompt Attention Office of the Inspector General Report Number A-13-01 October 29, 2013 INTRODUCTION This report

PROCEDURE. Accounts Payable

THE RICHARD STOCKTON COLLEGE OF NEW JERSEY PROCEDURE Accounts Payable Procedure Administrator: Associate Vice President for Administration and Finance Authority: N.J.S.A. 18A:64-6 Effective Date: January

THE RICHARD STOCKTON COLLEGE OF NEW JERSEY PROCEDURE Accounts Payable Procedure Administrator: Associate Vice President for Administration and Finance Authority: N.J.S.A. 18A:64-6 Effective Date: January

Office of Business and Finance

OBJECTIVE To establish procedures for review and payment of invoices for goods and services purchased by the university. POLICY Applies to: Faculty, staff, students, visitors, vendors Issued: 08/2000 Revised:

OBJECTIVE To establish procedures for review and payment of invoices for goods and services purchased by the university. POLICY Applies to: Faculty, staff, students, visitors, vendors Issued: 08/2000 Revised:

MEMORANDUM. Municipal Officials. From: Karen Horn, Director, Public Policy and Advocacy; and Abby Friedman, Director, Municipal Assistance Center

MEMORANDUM To: Municipal Officials From: Karen Horn, Director, Public Policy and Advocacy; and Abby Friedman, Director, Municipal Assistance Center 89 Main Street, Suite 4 Montpelier, Vermont 05602-2948

MEMORANDUM To: Municipal Officials From: Karen Horn, Director, Public Policy and Advocacy; and Abby Friedman, Director, Municipal Assistance Center 89 Main Street, Suite 4 Montpelier, Vermont 05602-2948

Environment. Main points...226. Introduction...227. Our audit conclusions and findings...228. Internal reporting needs improvement...

Environment 9 Main points...226 Introduction...227 Our audit conclusions and findings...228 Internal reporting needs improvement...229 Control over capital assets needed...229 Recording and collection

Environment 9 Main points...226 Introduction...227 Our audit conclusions and findings...228 Internal reporting needs improvement...229 Control over capital assets needed...229 Recording and collection

BUSINESS PROCESS (SAS 112 Compliance)

") Functional Area: Accounts Payable Name of Process: Travel Cash Advance Processing Purpose of Process: The purpose of travel advances is to minimize the financial burden on employees while traveling on

Functional Area: Accounts Payable Name of Process: Travel Cash Advance Processing Purpose of Process: The purpose of travel advances is to minimize the financial burden on employees while traveling on

The policy and procedural guidelines contained in this handbook are designed to:

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

AUDITOR GENERAL WILLIAM O. MONROE, CPA

AUDITOR GENERAL WILLIAM O. MONROE, CPA CITY OF WEEKI WACHEE, FLORIDA Follow-up on Operational Audit Report No. 2005-178 SUMMARY This report provides the results of our follow-up procedures for each of

AUDITOR GENERAL WILLIAM O. MONROE, CPA CITY OF WEEKI WACHEE, FLORIDA Follow-up on Operational Audit Report No. 2005-178 SUMMARY This report provides the results of our follow-up procedures for each of

AUDITOR GENERAL DAVID W. MARTIN, CPA

AUDITOR GENERAL DAVID W. MARTIN, CPA AGENCY FOR HEALTH CARE ADMINISTRATION ADMINISTRATIVE ACTIVITIES Operational Audit SUMMARY This operational audit of the Agency for Health Care Administration (Agency)

AUDITOR GENERAL DAVID W. MARTIN, CPA AGENCY FOR HEALTH CARE ADMINISTRATION ADMINISTRATIVE ACTIVITIES Operational Audit SUMMARY This operational audit of the Agency for Health Care Administration (Agency)

B Resource Guide: Implementing Financial Controls

What s in this Guide: I. Definition: What are Financial Controls? II. Why Do You Need Financial Controls? III. Best Practices: Financial Controls to Consider I. Definition: What are Financial Controls?

What s in this Guide: I. Definition: What are Financial Controls? II. Why Do You Need Financial Controls? III. Best Practices: Financial Controls to Consider I. Definition: What are Financial Controls?

August 2014 Report No. 14-043

John Keel, CPA State Auditor A Report on On-site Audits of Residential Child Care Providers Report No. 14-043 A Report on On-site Audits of Residential Child Care Providers Overall Conclusion Three of

John Keel, CPA State Auditor A Report on On-site Audits of Residential Child Care Providers Report No. 14-043 A Report on On-site Audits of Residential Child Care Providers Overall Conclusion Three of

P-Card Fraud Controls. Introduction

Introduction According to 2013 Association of Financial Professionals (AFP) Payments Fraud and Survey, the second most targeted payment type for fraud was corporate/commercial purchasing cards. 29% of

Introduction According to 2013 Association of Financial Professionals (AFP) Payments Fraud and Survey, the second most targeted payment type for fraud was corporate/commercial purchasing cards. 29% of

Office of the State Controller. Self-Assessment of Internal Controls. Purchasing/Accounts Payable Cycle. Objectives and Risks

Office of the State Controller Self-Assessment of Internal Controls Purchasing/Accounts Payable Cycle Objectives and Risks Agency Year-End Objectives All requests for goods and services are initiated and

Office of the State Controller Self-Assessment of Internal Controls Purchasing/Accounts Payable Cycle Objectives and Risks Agency Year-End Objectives All requests for goods and services are initiated and

Environmental Services Solid Waste Management Division Follow-Up Audit

Environmental Services Solid Waste Management Division Follow-Up Audit Issued by the February 26, 2007 EXECUTIVE SUMMARY The Internal Audit Department conducted a follow-up audit on the Environmental Services

Environmental Services Solid Waste Management Division Follow-Up Audit Issued by the February 26, 2007 EXECUTIVE SUMMARY The Internal Audit Department conducted a follow-up audit on the Environmental Services

MEMORANDUM INTERNAL CONTROL REQUIREMENTS FOR NON-PROFITS

DIVISION OF CHILD CARE AND EARLY CHILDHOOD EDUCATION HEALTH AND NUTRITION UNIT P O BOX 1437, SLOT S 155 501-320-8982 FAX: 501-682-2334 TDD: 501-682-1550 TO: NON-PROFIT INSTITUTIONS FROM: HEALTH AND NUTRITION

DIVISION OF CHILD CARE AND EARLY CHILDHOOD EDUCATION HEALTH AND NUTRITION UNIT P O BOX 1437, SLOT S 155 501-320-8982 FAX: 501-682-2334 TDD: 501-682-1550 TO: NON-PROFIT INSTITUTIONS FROM: HEALTH AND NUTRITION

June 2008 Report No. 08-038. An Audit Report on The Department of Information Resources and the Consolidation of the State s Data Centers

John Keel, CPA State Auditor An Audit Report on The Department of Information Resources and the Consolidation of the State s Data Centers Report No. 08-038 An Audit Report on The Department of Information

John Keel, CPA State Auditor An Audit Report on The Department of Information Resources and the Consolidation of the State s Data Centers Report No. 08-038 An Audit Report on The Department of Information

Environmental Services Solid Waste Management Division Audit Report

Solid Waste Management Division Audit Report Issued by the March 10, 2006 EXECUTIVE SUMMARY The has concluded its audit of the Solid Waste Management (SWM) Division. Based on the results of the audit,

Solid Waste Management Division Audit Report Issued by the March 10, 2006 EXECUTIVE SUMMARY The has concluded its audit of the Solid Waste Management (SWM) Division. Based on the results of the audit,

Lewis County Collector and Property Tax System

Nicole R. Galloway, CPA Missouri State Auditor FOLLOW-UP REPORT ON AUDIT FINDINGS Lewis County Collector and Property Tax System June 2015 http://auditor.mo.gov Report No. 2015-040 Follow-Up Report on

Nicole R. Galloway, CPA Missouri State Auditor FOLLOW-UP REPORT ON AUDIT FINDINGS Lewis County Collector and Property Tax System June 2015 http://auditor.mo.gov Report No. 2015-040 Follow-Up Report on

Product Brief. Intacct Financials & Accounting. Intacct General Ledger

Product Brief Intacct Financials & Accounting Intacct Financials and Accounting includes Intacct General Ledger, Intacct Accounts Receivable, Intacct Accounts Payable, Intacct Cash Management and Intacct

Product Brief Intacct Financials & Accounting Intacct Financials and Accounting includes Intacct General Ledger, Intacct Accounts Receivable, Intacct Accounts Payable, Intacct Cash Management and Intacct

Student Accounts Receivable

Student Accounts Receivable Original Implementation: July 15, 2008 Last Revision: April 14, 2015 PURPOSE This document establishes guidelines for the prudent collection of student accounts receivable in

Student Accounts Receivable Original Implementation: July 15, 2008 Last Revision: April 14, 2015 PURPOSE This document establishes guidelines for the prudent collection of student accounts receivable in

SAO Cash Management Group To Be Process Flow

Centralized Accounts Payable (AP) Disbursement Generate Checks and Positive Pay file Distribute Checks Review AP Reports Exception Processing Create Control Group in Peoplesoft Accounts Payable (HIGHLY

Centralized Accounts Payable (AP) Disbursement Generate Checks and Positive Pay file Distribute Checks Review AP Reports Exception Processing Create Control Group in Peoplesoft Accounts Payable (HIGHLY

Internal Control Guidelines

Internal Control Guidelines The four basic functions of management are usually described as planning, organizing, directing, and controlling. Internal control is what we mean when we discuss the fourth

Internal Control Guidelines The four basic functions of management are usually described as planning, organizing, directing, and controlling. Internal control is what we mean when we discuss the fourth

City of Berkeley. Prepared by:

City of Berkeley Berkeley Public Library Purchasing and Accounts Payable Audit Prepared by: Ann-Marie Hogan, City Auditor, CIA, CGAP Teresa Berkeley-Simmons, Audit Manager, CIA, CGAP Frank Marietti, Senior

City of Berkeley Berkeley Public Library Purchasing and Accounts Payable Audit Prepared by: Ann-Marie Hogan, City Auditor, CIA, CGAP Teresa Berkeley-Simmons, Audit Manager, CIA, CGAP Frank Marietti, Senior

Accounts Payable Workshop. Boston University Office of the Comptroller

Accounts Payable Workshop Boston University Office of the Comptroller Accounts Payable Workshop Topics of Discussion Accounts Payable Organization Purchases Covered by University Purchasing Policy Receipt

Accounts Payable Workshop Boston University Office of the Comptroller Accounts Payable Workshop Topics of Discussion Accounts Payable Organization Purchases Covered by University Purchasing Policy Receipt

Appendix C: Examples of Common Accounting and Bookkeeping Procedures

Appendix C: Examples of Common Accounting and Bookkeeping Procedures In this Appendix the use of the term monthly means on a regular cycle, based on the needs of your district. Some of the sample accounting

Appendix C: Examples of Common Accounting and Bookkeeping Procedures In this Appendix the use of the term monthly means on a regular cycle, based on the needs of your district. Some of the sample accounting

Standard Procedures and Controls for the Title Industry. Prepared by the ALTA Internal Auditing Committee ALTA

Standard Procedures and Controls for the Title Industry Prepared by the ALTA Internal Auditing Committee ALTA The American Land Title Association, founded in 1907, is the national trade association and

Standard Procedures and Controls for the Title Industry Prepared by the ALTA Internal Auditing Committee ALTA The American Land Title Association, founded in 1907, is the national trade association and

BDO Consulting. Segregation of Duties Checklist

BDO Consulting Segregation of Duties Checklist August 2009 BDO Consulting s Fraud Prevention practice is pleased to present the 2009 Segregation of Duties Checklist. We have developed this tool to assist

BDO Consulting Segregation of Duties Checklist August 2009 BDO Consulting s Fraud Prevention practice is pleased to present the 2009 Segregation of Duties Checklist. We have developed this tool to assist

USE OF BUSINESS CARDS FOR PURCHASING

POLICY STATEMENT USE OF BUSINESS CARDS FOR PURCHASING POLICY ADOPTED: 8 MARCH 2000 RATIONALE Considerable time and effort is expended in the processing of requisitions, purchase orders and invoices that

POLICY STATEMENT USE OF BUSINESS CARDS FOR PURCHASING POLICY ADOPTED: 8 MARCH 2000 RATIONALE Considerable time and effort is expended in the processing of requisitions, purchase orders and invoices that

Part of the Deloitte working capital series. Make your working capital work for you. Strategies for optimizing your accounts payable

Part of the Deloitte working capital series Make your working capital work for you Strategies for optimizing your accounts payable The Deloitte working capital series Strategies for optimizing your accounts

Part of the Deloitte working capital series Make your working capital work for you Strategies for optimizing your accounts payable The Deloitte working capital series Strategies for optimizing your accounts

Internal Controls Best Practices

Internal Controls Best Practices This list includes the most common internal controls applied by small to medium sized businesses to their operations. It includes controls that apply to the processes most

Internal Controls Best Practices This list includes the most common internal controls applied by small to medium sized businesses to their operations. It includes controls that apply to the processes most

Year-end Prep Webinar December 11, 2014

Webinar December 11, 2014 Denise Austin Professional Services Consultant Tom Lane Vice President of Sales and Marketing Agenda Is a 13 th Period Right for You Month End vs Year End Period End / Year End

Webinar December 11, 2014 Denise Austin Professional Services Consultant Tom Lane Vice President of Sales and Marketing Agenda Is a 13 th Period Right for You Month End vs Year End Period End / Year End

LOSS CONTROL SUPPLEMENTAL APPLICATION FOR INSURANCE COMPANIES

Name of Insurance Company to which application is made LOSS CONTROL SUPPLEMENTAL APPLICATION FOR INSURANCE COMPANIES NAME OF INSURED: ADDRESS: DATE: A. EMPLOYMENT PRACTICES 1. Do you require that each

Name of Insurance Company to which application is made LOSS CONTROL SUPPLEMENTAL APPLICATION FOR INSURANCE COMPANIES NAME OF INSURED: ADDRESS: DATE: A. EMPLOYMENT PRACTICES 1. Do you require that each

INTERNAL CONTROL OVER PURCHASE INTERNAL CONTROL OVER INVENTORY INTERNAL CONTROL OVER CASH PAYMENTS INTERNAL CONTROL OVER CASH RECEIPTS

Internal Control over the followings is included in the syllabus: INTERNAL CONTROL OVER SALES INTERNAL CONTROL OVER PURCHASE INTERNAL CONTROL OVER INVENTORY INTERNAL CONTROL OVER CASH PAYMENTS INTERNAL

Internal Control over the followings is included in the syllabus: INTERNAL CONTROL OVER SALES INTERNAL CONTROL OVER PURCHASE INTERNAL CONTROL OVER INVENTORY INTERNAL CONTROL OVER CASH PAYMENTS INTERNAL

CLASSIFICATION SPECIFICATION FINANCIAL ANALYST

0729 CLASSIFICATION SPECIFICATION FINANCIAL ANALYST GENERAL DESCRIPTION Provides complex technical support to the organization in the area of governmental accounting, grants and contracts with sub-recipient

0729 CLASSIFICATION SPECIFICATION FINANCIAL ANALYST GENERAL DESCRIPTION Provides complex technical support to the organization in the area of governmental accounting, grants and contracts with sub-recipient

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES CASH MANAGEMENT I. Checks a. All checks are restrictively endorsed, using the endorsement stamp maintained by the building secretary.

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES CASH MANAGEMENT I. Checks a. All checks are restrictively endorsed, using the endorsement stamp maintained by the building secretary.

Accounts Payable and Short Term Liabilities

Chapter 9 Accounts Payable and Short Term Liabilities Accounts payable represent short term obligations to be paid to parish and school vendors/creditors for goods purchased or services provided. Generally,

Chapter 9 Accounts Payable and Short Term Liabilities Accounts payable represent short term obligations to be paid to parish and school vendors/creditors for goods purchased or services provided. Generally,

Solutions for Accounts Payable Process Optimization

Solutions for Accounts Payable Process Optimization ScerIS is your resource for Accounts Payable Process Optimization (APPO). We help clients do more at lower cost, in less time and with fewer people.

Solutions for Accounts Payable Process Optimization ScerIS is your resource for Accounts Payable Process Optimization (APPO). We help clients do more at lower cost, in less time and with fewer people.

Class Specification Accounts Payable Supervisor

Class Specification Accounts Payable Supervisor Summary Statement: The purpose of this position is to manage the Accounts Payable and Disbursements Division of the Finance Department and administer the

Class Specification Accounts Payable Supervisor Summary Statement: The purpose of this position is to manage the Accounts Payable and Disbursements Division of the Finance Department and administer the

Assertion Control objectives Controls Tests of controls Occurrence and existence

Internal Control over Payroll Assertion Control objectives Controls Tests of controls Occurrence and existence Payment is made only to bona fide employees of the entity. Segregation of duties between HR

Internal Control over Payroll Assertion Control objectives Controls Tests of controls Occurrence and existence Payment is made only to bona fide employees of the entity. Segregation of duties between HR

To the Rector, Wardens and Vestry of (Church Name; Church Address; City and Zip)

") Section B. Sample Audit Committee Certificate Date To the Rector, Wardens and Vestry of (Church Name; Church Address; City and Zip) Subject: (Audit Year) Audit of (Church Name) We have inspected the statement

Section B. Sample Audit Committee Certificate Date To the Rector, Wardens and Vestry of (Church Name; Church Address; City and Zip) Subject: (Audit Year) Audit of (Church Name) We have inspected the statement

August 2012 Report No. 12-048

John Keel, CPA State Auditor An Audit Report on The Texas Windstorm Insurance Association Report No. 12-048 An Audit Report on The Texas Windstorm Insurance Association Overall Conclusion The Texas Windstorm

John Keel, CPA State Auditor An Audit Report on The Texas Windstorm Insurance Association Report No. 12-048 An Audit Report on The Texas Windstorm Insurance Association Overall Conclusion The Texas Windstorm

Business Plan: Finance

Business Plan: Finance How does this service contribute to the results identified in the City of London Strategic Plan? A Strong Economy A Vibrant and Diverse Community A Green and Growing City A Sustainable

Business Plan: Finance How does this service contribute to the results identified in the City of London Strategic Plan? A Strong Economy A Vibrant and Diverse Community A Green and Growing City A Sustainable

Audit of Cash Balances

Audit of Cash Balances Chapter 23 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 23-1 Learning Objective 1 Show the relationship of cash in the bank to the various transaction

Audit of Cash Balances Chapter 23 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 23-1 Learning Objective 1 Show the relationship of cash in the bank to the various transaction

FIVE MANAGEMENT SYSTEM Policies and Procedures Checklist

FIVE MANAGEMENT SYSTEM Procedures Checklist Provided by: Navajo Nation Office of the Auditor General TABLE OF CONTENTS Introduction.........................................1 General Administrative Procedures...............................1

FIVE MANAGEMENT SYSTEM Procedures Checklist Provided by: Navajo Nation Office of the Auditor General TABLE OF CONTENTS Introduction.........................................1 General Administrative Procedures...............................1

FINANCIAL CONTROLS POLICIES AND PROCEDURES FOR SMALL NONPROFIT ORGANIZATIONS

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

Accounts Payable Manual

Accounts Payable Manual P a g e 2 January 2015 P a g e 3 Table of Contents Introduction... 4 Accounts Payable... 5 Vendor Payments... 7 Paperless Invoice Process... 13 Imprest Accounts and Petty Cash Funds...

Accounts Payable Manual P a g e 2 January 2015 P a g e 3 Table of Contents Introduction... 4 Accounts Payable... 5 Vendor Payments... 7 Paperless Invoice Process... 13 Imprest Accounts and Petty Cash Funds...

FINANCIAL POLICIES INDEX

FINANCIAL POLICIES INDEX Page Accounts Payable 2 Cash Receipts 6 Credit Cards 9 General Ledger Adjustments 10 Fixed Asset 11 Payroll Tax Reporting 13 Travel Reimbursement 14 Handling Mail 15 1 Accounts

FINANCIAL POLICIES INDEX Page Accounts Payable 2 Cash Receipts 6 Credit Cards 9 General Ledger Adjustments 10 Fixed Asset 11 Payroll Tax Reporting 13 Travel Reimbursement 14 Handling Mail 15 1 Accounts

Accounts Payable Business Case. The Benefits of Accounts Payable Integration with PayCargo

Accounts Payable Business Case The Benefits of Accounts Payable Integration with PayCargo How to Use this Presentation This presentation will be invaluable to those who seek to articulate the benefits

Accounts Payable Business Case The Benefits of Accounts Payable Integration with PayCargo How to Use this Presentation This presentation will be invaluable to those who seek to articulate the benefits

The Finance Function. Investment Real Estate: Finance and Asset Management

The Finance Function CHAPTER 3 Today, one cannot try to identify a single business model for a real estate management office and its finance function. Rather, three or four general business models are

The Finance Function CHAPTER 3 Today, one cannot try to identify a single business model for a real estate management office and its finance function. Rather, three or four general business models are

P L A N A D V I S O R Y. The Importance of Internal Controls in Financial Reporting and Safeguarding Plan Assets

P L A N A D V I S O R Y The Importance of Internal Controls in Financial Reporting and Safeguarding Plan Assets P L A N A D V I S O R Y Table of Contents Introduction 3 Why Internal Control Is Important

P L A N A D V I S O R Y The Importance of Internal Controls in Financial Reporting and Safeguarding Plan Assets P L A N A D V I S O R Y Table of Contents Introduction 3 Why Internal Control Is Important

10-1. Auditing Business Process. Objectives Understand the Auditing of the Enteties Business. Process

10-1 Auditing Business Process Auditing Business Process Objectives Understand the Auditing of the Enteties Business Process Identify the types of transactions in different Business Process Asses Control

10-1 Auditing Business Process Auditing Business Process Objectives Understand the Auditing of the Enteties Business Process Identify the types of transactions in different Business Process Asses Control

Wells Fargo Bank WellsOne Commercial Card Program REED COLLEGE. Policy and Procedures Manual Date: 7/21/09

Wells Fargo Bank WellsOne Commercial Card Program REED COLLEGE Policy and Procedures Manual Date: 7/21/09 Table of Contents Introduction... 3 General Guidelines - Card Issuance... 4 - Card Usage... 4 -

Wells Fargo Bank WellsOne Commercial Card Program REED COLLEGE Policy and Procedures Manual Date: 7/21/09 Table of Contents Introduction... 3 General Guidelines - Card Issuance... 4 - Card Usage... 4 -

New Jersey Commerce and Economic Growth Commission

New Jersey State Legislature Office of Legislative Services Office of the State Auditor New Jersey Commerce and Economic Growth Commission Fiscal Year 2004 Richard L. Fair State Auditor LEGISLATIVE SERVICES

New Jersey State Legislature Office of Legislative Services Office of the State Auditor New Jersey Commerce and Economic Growth Commission Fiscal Year 2004 Richard L. Fair State Auditor LEGISLATIVE SERVICES

Table of Contents. Transmittal Letter... 1. Executive Summary... 2-3. Background... 4-5. Objectives and Approach... 6. Issues Matrix...

Internal Audit Committee of Brevard County, Florida Internal Audit Review of Accounts Payable Prepared By: Internal Auditors of Brevard County September 22, 2010 Table of Contents Transmittal Letter...

Internal Audit Committee of Brevard County, Florida Internal Audit Review of Accounts Payable Prepared By: Internal Auditors of Brevard County September 22, 2010 Table of Contents Transmittal Letter...

Audit Guidelines. The Annual Church Audit. by Dan Busby. Key Concepts. Idea! Use this document as a checklist for your annual audit.

The Annual Church Audit by Dan Busby Audit Guidelines Church board members have a long list of responsibilities. Among these is the responsibility for the money that flows through the church. Included

The Annual Church Audit by Dan Busby Audit Guidelines Church board members have a long list of responsibilities. Among these is the responsibility for the money that flows through the church. Included

GJW Accounting & Tax Service, LLC s (GJWATS) Responsibility

Responsibility") Dear: 402 Kames Cove Slinger, WI 53086 Phone: 262-257-9776 Fax: 877-785-0374 www.gjwaccounting.com gjwilson@gjwaccounting.com We appreciate the opportunity to offer s to. To ensure a clear understanding

Dear: 402 Kames Cove Slinger, WI 53086 Phone: 262-257-9776 Fax: 877-785-0374 www.gjwaccounting.com gjwilson@gjwaccounting.com We appreciate the opportunity to offer s to. To ensure a clear understanding

HOWARD UNIVERSITY POLICY

HOWARD UNIVERSITY POLICY Policy Number: 300-001 Policy Title: ACCOUNTS PAYABLE: PAYMENTS TO VENDORS Responsible Officer: Chief Financial Officer Responsible Office: Office of the Chief Financial Officer

HOWARD UNIVERSITY POLICY Policy Number: 300-001 Policy Title: ACCOUNTS PAYABLE: PAYMENTS TO VENDORS Responsible Officer: Chief Financial Officer Responsible Office: Office of the Chief Financial Officer

City of Berkeley. Accounts Payable Audit

City of Berkeley Accounts Payable Audit Prepared by: Ann-Marie Hogan, City Auditor, CIA, CGAP Teresa Berkeley-Simmons, Audit Manager, CIA, CGAP Frank Marietti, Senior Auditor, CIA, CGAP Presented to Council

City of Berkeley Accounts Payable Audit Prepared by: Ann-Marie Hogan, City Auditor, CIA, CGAP Teresa Berkeley-Simmons, Audit Manager, CIA, CGAP Frank Marietti, Senior Auditor, CIA, CGAP Presented to Council

Office of the City Auditor. Audit Report. AUDIT OF MONTHLY BANK RECONCILIATIONS (Report No. A08-014) May 16, 2008. City Auditor. Craig D.

May 16, 2008. City Auditor. Craig D.") CITY OF DALLAS Dallas City Council Office of the City Auditor Audit Report Mayor Tom Leppert Mayor Pro Tem Dr. Elba Garcia AUDIT OF MONTHLY BANK RECONCILIATIONS (Report No. A08-014) Deputy Mayor Pro Tem

CITY OF DALLAS Dallas City Council Office of the City Auditor Audit Report Mayor Tom Leppert Mayor Pro Tem Dr. Elba Garcia AUDIT OF MONTHLY BANK RECONCILIATIONS (Report No. A08-014) Deputy Mayor Pro Tem

Patrice Randle, City Auditor Craig Terrell, Assistant City Auditor. Group Health Fund Follow-Up Audit April 2012

Patrice Randle, City Auditor Craig Terrell, Assistant City Auditor Group Health Fund Follow-Up Audit April 2012 Group Health Fund Follow-Up Audit Table of Contents Page Executive Summary...1 Audit Scope

Patrice Randle, City Auditor Craig Terrell, Assistant City Auditor Group Health Fund Follow-Up Audit April 2012 Group Health Fund Follow-Up Audit Table of Contents Page Executive Summary...1 Audit Scope

Table of Contents: Chapter 2 Internal Control

Table of Contents: Chapter 2 Chapter 2... 2 2.1 Establishing an Effective System... 2 2.1.1 Sample Plan Elements... 5 2.1.2 Limitations of... 7 2.2 Approvals... 7 2.3 PCard... 7 2.4 Payroll... 7 2.5 Reconciliation

Table of Contents: Chapter 2 Chapter 2... 2 2.1 Establishing an Effective System... 2 2.1.1 Sample Plan Elements... 5 2.1.2 Limitations of... 7 2.2 Approvals... 7 2.3 PCard... 7 2.4 Payroll... 7 2.5 Reconciliation

A Municipal Checklist for Internal Control-Part I, Cash Controls

A Municipal Checklist for Internal Control-Part I, Cash Controls I. General Internal Control & Banking 1 Is a professional (independent) audit done annually? 2 If you have an annual audit was the most

A Municipal Checklist for Internal Control-Part I, Cash Controls I. General Internal Control & Banking 1 Is a professional (independent) audit done annually? 2 If you have an annual audit was the most

SUGGESTED CONTROLS TO MITIGATE THE POTENTIAL RISK (Internal Audit)

") Unit: Subject: Sarbanes-Oxley Act Review - Inventory Management Title: Risk & Control Identification Year end: MILL RAW MATERIALS Receiving of Raw Materials Raw materials are received and accepted only

Unit: Subject: Sarbanes-Oxley Act Review - Inventory Management Title: Risk & Control Identification Year end: MILL RAW MATERIALS Receiving of Raw Materials Raw materials are received and accepted only

Navy s Contract/Vendor Pay Process Was Not Auditable

Inspector General U.S. Department of Defense Report No. DODIG-2015-142 JULY 1, 2015 Navy s Contract/Vendor Pay Process Was Not Auditable INTEGRITY EFFICIENCY ACCOUNTABILITY EXCELLENCE INTEGRITY EFFICIENCY

Inspector General U.S. Department of Defense Report No. DODIG-2015-142 JULY 1, 2015 Navy s Contract/Vendor Pay Process Was Not Auditable INTEGRITY EFFICIENCY ACCOUNTABILITY EXCELLENCE INTEGRITY EFFICIENCY

Senior Accountant Position Description Housing Resources Group (HRG)

") Senior Accountant Position Description Housing Resources Group (HRG) Position Type: 40 hours per week, exempt Reports to: Controller Basic Responsibilities: Initiate, manage and assist with and complete

Senior Accountant Position Description Housing Resources Group (HRG) Position Type: 40 hours per week, exempt Reports to: Controller Basic Responsibilities: Initiate, manage and assist with and complete

WEEK 6. Objective 1: Sales Transaction Cycle Risks

WEEK 6 CSA ch4 & GS ch10: pp457-488 Objective 1: Sales Transaction Cycle Risks The major assertions of interest to the auditor in ST of balances for account receivable are existence and valuation and allocation.

WEEK 6 CSA ch4 & GS ch10: pp457-488 Objective 1: Sales Transaction Cycle Risks The major assertions of interest to the auditor in ST of balances for account receivable are existence and valuation and allocation.

Internal Control Systems

D. INTERNAL CONTROL 1. Internal Control Systems 2. The Use of Internal Control Systems by Auditors 3. Transaction Cycles 4. Tests of Control 5. The Evaluation of Internal Control Component 6. Communication

D. INTERNAL CONTROL 1. Internal Control Systems 2. The Use of Internal Control Systems by Auditors 3. Transaction Cycles 4. Tests of Control 5. The Evaluation of Internal Control Component 6. Communication

FINANCIAL RELATED AUDIT OF BOYKIN CONTINUING EDUCATION CENTER School Year 2008-09

Detroit Public Schools Office of the Auditor General OF BOYKIN CONTINUING EDUCATION CENTER School Year 2008-09 REPORT NO: 09-015 REPORT DATE: June, 2009 Fisher Building 3011 West Grand Boulevard Suite

Detroit Public Schools Office of the Auditor General OF BOYKIN CONTINUING EDUCATION CENTER School Year 2008-09 REPORT NO: 09-015 REPORT DATE: June, 2009 Fisher Building 3011 West Grand Boulevard Suite

Accounts Payable. Summary

Accounts Payable Summary EFT is HCR ManorCare s expected method of payment. EDI is HCR ManorCare s preferred method of invoicing. All new vendors must be approved by Corporate Purchasing prior to purchase

Accounts Payable Summary EFT is HCR ManorCare s expected method of payment. EDI is HCR ManorCare s preferred method of invoicing. All new vendors must be approved by Corporate Purchasing prior to purchase

Otsego Northern Catskills BOCES Payment Card Program

Otsego Northern Catskills BOCES Payment Card Program (p-card Program) Cardholder Procedure Manual Table of Contents Page A. Introduction 1 B. p-card Overview 1 C. Personal Liability and Your Credit Rating

Otsego Northern Catskills BOCES Payment Card Program (p-card Program) Cardholder Procedure Manual Table of Contents Page A. Introduction 1 B. p-card Overview 1 C. Personal Liability and Your Credit Rating

GAO. Standards for Internal Control in the Federal Government. Internal Control. United States General Accounting Office.

GAO United States General Accounting Office Internal Control November 1999 Standards for Internal Control in the Federal Government GAO/AIMD-00-21.3.1 Foreword Federal policymakers and program managers

GAO United States General Accounting Office Internal Control November 1999 Standards for Internal Control in the Federal Government GAO/AIMD-00-21.3.1 Foreword Federal policymakers and program managers

Wheaton College. Updated November 2012. Park Hall, Room 205 Park Hall, Room 202 Phone: 3433/3438 Phone: 3439

Wheaton College Corporate Credit Card User Guide Updated November 2012 For General Information Contact: For Accounting/Reconciliation Info Contact: Business Services Office Accounts Payable Office Park

Wheaton College Corporate Credit Card User Guide Updated November 2012 For General Information Contact: For Accounting/Reconciliation Info Contact: Business Services Office Accounts Payable Office Park

Accounts Payable Services. A strong foundation for sustained benefits. Accounts Payable

Services A strong foundation for sustained benefits 2 Introduction The accounts payable (AP) function is changing. For the past decade, finance departments have focused on driving cost, complexity, risk

Services A strong foundation for sustained benefits 2 Introduction The accounts payable (AP) function is changing. For the past decade, finance departments have focused on driving cost, complexity, risk

SUGGESTED CONTROLS TO MITIGATE THE POTENTIAL RISK (Internal Audit)

") Unit: Subject: Sarbanes-Oxley Act Review - Fixed Assets Cycle Title: Risk and Control Identification Year end: Acquisition of Fixed Assets Recorded fixed asset acquisitions represent fixed assets acquired

Unit: Subject: Sarbanes-Oxley Act Review - Fixed Assets Cycle Title: Risk and Control Identification Year end: Acquisition of Fixed Assets Recorded fixed asset acquisitions represent fixed assets acquired

Accounting Systems: Complying with FAR Requirements. John S. Sroka, CPA Acquisition Cost/Price Analyst

Accounting Systems: Complying with FAR Requirements John S. Sroka, CPA Acquisition Cost/Price Analyst Background Information FAR Requirements FAR Part 9: Contractor Qualifications FAR Part 16: Cost-reimbursement

Accounting Systems: Complying with FAR Requirements John S. Sroka, CPA Acquisition Cost/Price Analyst Background Information FAR Requirements FAR Part 9: Contractor Qualifications FAR Part 16: Cost-reimbursement

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL Revised 3-27-2014 TABLE OF CONTENTS Section 1: Section 2: Section 3: Section 4: Section 5: Section 6: Section 7: Section 8: Section 9: Cash Management

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL Revised 3-27-2014 TABLE OF CONTENTS Section 1: Section 2: Section 3: Section 4: Section 5: Section 6: Section 7: Section 8: Section 9: Cash Management

Richmond Public Schools ACCOUNTS PAYABLE DIVISION

Report Issue Date: May 18, 2015 Report Number: 2015-08 AUDIT OF ACCOUNTS PAYABLE DIVISION Richmond City Council Office of the City Auditor Richmond City Hall 900 E. Broad Street, Suite 806 Richmond, Virginia

Report Issue Date: May 18, 2015 Report Number: 2015-08 AUDIT OF ACCOUNTS PAYABLE DIVISION Richmond City Council Office of the City Auditor Richmond City Hall 900 E. Broad Street, Suite 806 Richmond, Virginia