Interest Rate Insurance Prices Implicit in Option Prices

|

|

|

- Hilary Russell

- 8 years ago

- Views:

Transcription

1 Page 1 of 5 Interest Rate Insurance Prices Implicit in Option Prices June 16, 2015 (# ) Douglas T. Breeden William W. Priest Professor of Finance, Fuqua School of Business, Duke University and Senior Research Consultant, Amundi Smith Breeden 1 Rates increase globally as Eurozone and U.S. economies strengthen and deflation concerns abate. Option prices show increasing confidence in long-term normalization. I. Overview of Recent Events. The first half of June saw continued high volatility in global bond markets, especially in the first week. The 10-year German bund yield increased 33 basis points from 0.49% on May 29 th to 0.82% on June 15th. The U.S. 10-year rate increased 23 bp from 2.12% to 2.35%, and the U.K. 10-year Gilt increased 21 bp from 1.81% to 2.02%. Increases in rates were supported by strengthening retail sales and reduced deflation fears in Europe, as well as by a very strong job market in the USA. II. USA: Interest Rate Insurance Prices for USA LIBOR 3, 5, and 10 Years Out Seeing the much-improved job market, with unemployment claims running at very low levels and total job growth at very strong levels, Fed Chair Janet Yellen has said several times that she expects the U.S. economy to be strong enough to have liftoff in rates in Eurodollar futures markets appear to be betting that this will occur in September, rather than June Let s go to the prices for interest rate caps and floors (from Bloomberg) and see what the distributions are for the market s pricing per $1.00 of insurance for USA LIBOR. We will compare current pricing (yesterday s close, June 15, 2015) to March 6 th (immediately before ECB QE), and to May 29, 2015, two weeks ago. From Figure 1A, we see that the early June surge in rates globally brought the pricing of interest rate insurance for rates 3 years out back to the pricing before the ECB started QE. The mode is for 3-month LIBOR of about 2.00%, up considerably from the 0.29% rate today. Pricing is relatively symmetrical in the 3-year distribution, with roughly equal prices for 1.0% and 3.0% LIBOR scenarios. Prices for bets on LIBOR of 0.5% or less are likely dominated by fear of the likely bad economy if that happens (as well as probability of occurrence). As Figure 1B shows, these fears have diminished notably in the past two weeks. While the 5-year distribution remains bimodal, the pricing weights have shifted to more value being placed on the normalizing scenarios. This appears to be even more so in the 8-10 year prices (Figure 1C), as pricing for 3%, 4% and 5% scenarios have increased noticeably. With job growth quite rapid, labor market slack is being removed, and there are nascent signs of improving growth in real wages. Given the tightening labor market, most economists are now forecasting a pickup in real wage growth and in inflation. 1 I thank Rebekah Ackerman and Yue Teng of Amundi Smith Breeden for excellent research assistance.

2 Page 2 of 5 Figures 1A-1C

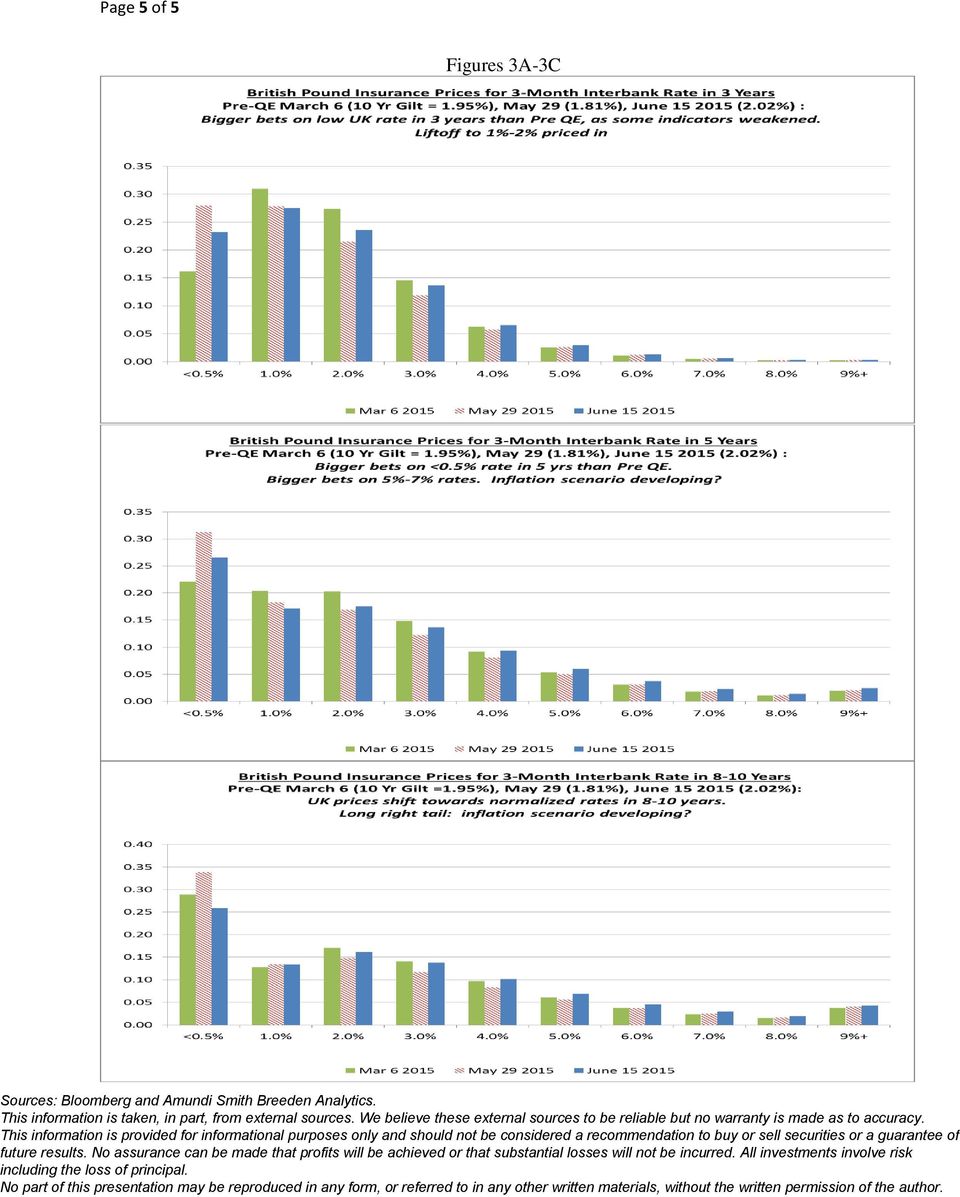

3 Page 3 of 5 III. Euro Area: Interest Rate Insurance Prices for Euribor 3, 5, nd 8-10 Years Out The insurance price graphs for Euribor, Figures 2A-2C, all show significant shifts in the past two weeks towards higher interest rates, reflecting the strengthening Eurozone economies, notably in Spain and France, but also in Germany and Italy. Deflation concerns are abating. As noted in the last letter, the ECB s QE policy has two potentially offsetting effects. First, there is the pure addition to the demand for long-term bonds, which pushes prices up and rates down. Secondly, and at least partially offsetting if not entirely reversing that effect, is that their goal is to stimulate higher growth through the way they implement this program. If they are successful, growth will be higher, future aggregate demand higher, and future inflation and interest rates higher. Figure 2A shows that for the 3-year Euribor rate, in the past two weeks we have seen a sharp move downward in pricing for the <0.5% rate scenario, and a sharp move upward in pricing for 1% Euribor. These moves appear to reflect increasing confidence that the Eurozone has turned the corner on growth and inflation. In Figures 2B and 2C, we see that in 5 years and 8-10 years, the prices for bets on Euribor of 2%, 3% and 4% have increased sharply in the past two weeks. And, as with the 3- year distribution, the pricing of the <0.5% recession scenario has diminished. Altogether, these moves show clear market bets moving towards ultimate economic normalization in the Eurozone. A number of factors likely are helping this develop, including (1) a lower Euro forex price, which helps competitiveness, (2) ECB QE stimulus, (3) structural employment changes in some countries, notably Spain, and (4) normal economic equilibrium adjustments. IV. U.K: Interest Rate Insurance Prices for Interbank Rates in 3, 5, and 8-10 Years The U.K. insurance price distributions in Figures 3A-3C show moves that are broadly similar to the moves in the Eurozone, but muted a bit, due to the weakness of some UK economic signals, as well as uncertainty about a possible Brexit vote. Prime Minister Cameron s promise of a vote in 2016 on staying in the European Union is causing anxiety in markets and possible uncertainty among business decision makers. However, in general, the UK economy has performed well in the past couple of years, stronger than other European economies. Housing prices continue to increase in the UK by 5% or so, year over year. As oil prices have bounced off their low levels and the unemployment rate is low at 5.5%, the stage is set for a possible buildup of inflation in coming years. Figures 2B and 2C show small, but notable increases in prices for interest rate insurance for interbank rates of 5%, 6% and 7% (rather high rates relative to a 2% inflation goal) in 5 to 10 years. Do note that the relationship of economic growth to inflation likely is a very nonlinear one that is shaped like an inverted U. Very low rates likely reflect very weak economies, as we saw in the recent Great Recession and Sovereign Debt Crisis. However, as in the 1970s and 1980s, very high rates of inflation can also be associated with poor economies. One would think that we are a long way from worrying much about that scenario, but it is a possibility, as is well known in many emerging markets. So, in terms of our insurance price distributions, we could see prices for very high rate scenarios (like 9%+) increase due to risk aversion and high marginal utility, as well as due to moves in probabilities.

4 Page 4 of 5 Figures 2A-C

5 Page 5 of 5 Figures 3A-3C

Interest Rate Insurance Prices Implicit in Option Prices

Page 1 of 6 November 2, 2015 (#2015-18) Interest Rate Insurance Prices Implicit in Option Prices Douglas T. Breeden William W. Priest Professor of Finance, Fuqua School of Business, Duke University and

Page 1 of 6 November 2, 2015 (#2015-18) Interest Rate Insurance Prices Implicit in Option Prices Douglas T. Breeden William W. Priest Professor of Finance, Fuqua School of Business, Duke University and

Interest Rate Insurance Prices Implicit in Option Prices

Page 1 of 6 Interest Rate Insurance Prices Implicit in Option Prices July 18, 2015 (#2015-15) Douglas T. Breeden William W. Priest Professor of Finance, Fuqua School of Business, Duke University and Senior

Page 1 of 6 Interest Rate Insurance Prices Implicit in Option Prices July 18, 2015 (#2015-15) Douglas T. Breeden William W. Priest Professor of Finance, Fuqua School of Business, Duke University and Senior

Why Treasury Yields Are Projected to Remain Low in 2015 March 2015

Why Treasury Yields Are Projected to Remain Low in 5 March 5 PERSPECTIVES Key Insights Monica Defend Head of Global Asset Allocation Research Gabriele Oriolo Analyst Global Asset Allocation Research While

Why Treasury Yields Are Projected to Remain Low in 5 March 5 PERSPECTIVES Key Insights Monica Defend Head of Global Asset Allocation Research Gabriele Oriolo Analyst Global Asset Allocation Research While

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013 U.S. stock market performance in 2012 * +12.59% total return +6.35%

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013 U.S. stock market performance in 2012 * +12.59% total return +6.35%

Weekly Economic Commentary

Weekly Economic Commentary March 21, 2015 by Carl Tannenbaum of Northern Trust What Is Full Employment, and Are We There Yet? March 20, 2015 One of my favorite jokes is the one about an economics graduate

Weekly Economic Commentary March 21, 2015 by Carl Tannenbaum of Northern Trust What Is Full Employment, and Are We There Yet? March 20, 2015 One of my favorite jokes is the one about an economics graduate

Statement by. Janet L. Yellen. Chair. Board of Governors of the Federal Reserve System. before the. Committee on Financial Services

For release at 8:30 a.m. EST February 10, 2016 Statement by Janet L. Yellen Chair Board of Governors of the Federal Reserve System before the Committee on Financial Services U.S. House of Representatives

For release at 8:30 a.m. EST February 10, 2016 Statement by Janet L. Yellen Chair Board of Governors of the Federal Reserve System before the Committee on Financial Services U.S. House of Representatives

October 2015. PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy October 2015 Market Volatility likely to Remain Elevated on China Growth Concerns & Fed Rate Uncertainty. Stocks

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy October 2015 Market Volatility likely to Remain Elevated on China Growth Concerns & Fed Rate Uncertainty. Stocks

FINANCIAL REPORT - MARCH 2015

FINANCIAL REPORT - MARCH 2015 SUMMARY OF THE MACROECONOMIC INFORMATION The macroeconomic scenario Deflation in Europe, the USA well. The passage of years is very positive for the United States: the positive

FINANCIAL REPORT - MARCH 2015 SUMMARY OF THE MACROECONOMIC INFORMATION The macroeconomic scenario Deflation in Europe, the USA well. The passage of years is very positive for the United States: the positive

Euro Zone s Economic Outlook and What it Means for the United States

WELCOME TO THE WEBINAR WEBINAR LINK: HTTP://FRBATL.ADOBECONNECT.COM/ECONOMY/ DIAL-IN NUMBER (MUST USE FOR AUDIO): 855-377-2663 ACCESS CODE: 71032685 Euro Zone s Economic Outlook and What it Means for the

WELCOME TO THE WEBINAR WEBINAR LINK: HTTP://FRBATL.ADOBECONNECT.COM/ECONOMY/ DIAL-IN NUMBER (MUST USE FOR AUDIO): 855-377-2663 ACCESS CODE: 71032685 Euro Zone s Economic Outlook and What it Means for the

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation

August 2014 Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook for factors that typically impact

August 2014 Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook for factors that typically impact

Markets Roundup. Yellen mildly hawkish at this week s FOMC? 14 March 2016 Research

Markets Roundup Research CONTENTS Market Movers 2 Economics Weekly Calendar 5 Yellen mildly hawkish at this week s FOMC? After the ECB surprised the markets last Thursday, financial market participants

Markets Roundup Research CONTENTS Market Movers 2 Economics Weekly Calendar 5 Yellen mildly hawkish at this week s FOMC? After the ECB surprised the markets last Thursday, financial market participants

Please note the Weekly Market Commentary will be on hiatus until January 5, 2014.

Weekly Market Commentary: December 16, 2013 Will 2014 Bring An End to Central Bank Intervention? Please note the Weekly Market Commentary will be on hiatus until January 5, 2014. Economic Data - Previous

Weekly Market Commentary: December 16, 2013 Will 2014 Bring An End to Central Bank Intervention? Please note the Weekly Market Commentary will be on hiatus until January 5, 2014. Economic Data - Previous

Growth and volatility will define global economy in 2016, says PineBridge Investments

Growth and volatility will define global economy in 2016, says PineBridge Investments PineBridge Investments forecasts 2.7% GDP growth in the United States Eurozone growth projected to slightly improve

Growth and volatility will define global economy in 2016, says PineBridge Investments PineBridge Investments forecasts 2.7% GDP growth in the United States Eurozone growth projected to slightly improve

TREASURY MANAGEMENT UPDATE QUARTER 4 2014/15

Committee and Date Cabinet 10 June 2015 12.30 pm Item 9 Public TREASURY MANAGEMENT UPDATE QUARTER 4 2014/15 Responsible Officer James Walton e-mail: james.walton@shropshire.gov.uk Tel: (01743) 255011 1.

Committee and Date Cabinet 10 June 2015 12.30 pm Item 9 Public TREASURY MANAGEMENT UPDATE QUARTER 4 2014/15 Responsible Officer James Walton e-mail: james.walton@shropshire.gov.uk Tel: (01743) 255011 1.

Market Bulletin. European assets: Volatility strikes back. 12 June 2015. What has happened? AUTHOR. What has been driving this?

Market Bulletin 12 June 2015 European assets: Volatility strikes back What has happened? Rather than abating, as many had expected, the sell-off in European markets that began in late April has continued

Market Bulletin 12 June 2015 European assets: Volatility strikes back What has happened? Rather than abating, as many had expected, the sell-off in European markets that began in late April has continued

FOREX WEEKLY REPORT. 22 April - 28 April 2013. Dieter Merz, Chief Investment Officer. Luciano Jannelli, Ph.D. Chief Economist

Dieter Merz, Chief Investment Officer FOREX WEEKLY REPORT Luciano Jannelli, Ph.D. Chief Economist Luc Luyet, CIIA, CMT Senior Analyst www.migbank.com DISCLAIMER & DISCLOSURES FOREX WEEKLY REPORT - An overview

Dieter Merz, Chief Investment Officer FOREX WEEKLY REPORT Luciano Jannelli, Ph.D. Chief Economist Luc Luyet, CIIA, CMT Senior Analyst www.migbank.com DISCLAIMER & DISCLOSURES FOREX WEEKLY REPORT - An overview

Report to the public on the Bank of Israel s discussions prior to deciding on. the interest rate for January 2015

BANK OF ISRAEL Office of the Spokesperson and Economic Information January 12, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on General the interest rate for January 2015

BANK OF ISRAEL Office of the Spokesperson and Economic Information January 12, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on General the interest rate for January 2015

UPDATE ON CURRENT MACRO ENVIRONMENT

1 Oct 213 Macro & Strategy Equity Credit Commodities 13 13 #1 Global Strategy #1 Multi Asset Research #3 Global Economics #2 Equity Quant #2 Index Analysis #3 SRI Research 12 sector teams in the Top 1

1 Oct 213 Macro & Strategy Equity Credit Commodities 13 13 #1 Global Strategy #1 Multi Asset Research #3 Global Economics #2 Equity Quant #2 Index Analysis #3 SRI Research 12 sector teams in the Top 1

US Labour Market Monitor July report set to attract much attention as both employment and growth have slowed in 2016

Investment Research General Market Conditions 02 August 2016 US Labour Market Monitor July report set to attract much attention as both employment and growth have slowed in 2016 Jobs report preview We

Investment Research General Market Conditions 02 August 2016 US Labour Market Monitor July report set to attract much attention as both employment and growth have slowed in 2016 Jobs report preview We

Project LINK Meeting New York, 20-22 October 2010. Country Report: Australia

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

INFLATION REPORT PRESS CONFERENCE. Thursday 4 th February 2016. Opening remarks by the Governor

INFLATION REPORT PRESS CONFERENCE Thursday 4 th February 2016 Opening remarks by the Governor Good afternoon. At its meeting yesterday, the Monetary Policy Committee (MPC) voted 9-0 to maintain Bank Rate

INFLATION REPORT PRESS CONFERENCE Thursday 4 th February 2016 Opening remarks by the Governor Good afternoon. At its meeting yesterday, the Monetary Policy Committee (MPC) voted 9-0 to maintain Bank Rate

Eurozone Economic dashboard

Eurozone Economic dashboard Our Economic Dashboard is designed to help investors understand the true state of the eurozone economy. It is not meant to serve as a direct prediction regarding the future

Eurozone Economic dashboard Our Economic Dashboard is designed to help investors understand the true state of the eurozone economy. It is not meant to serve as a direct prediction regarding the future

Markets Roundup. Research. US data show that deflation risks are rising

Markets Roundup August 24 t h, 29 C O N T E N T S Market Movers 2 Economics Weekly Calendar 5 Central Bank Policies 6 US data show that deflation risks are rising Research Although Chinese equities have

Markets Roundup August 24 t h, 29 C O N T E N T S Market Movers 2 Economics Weekly Calendar 5 Central Bank Policies 6 US data show that deflation risks are rising Research Although Chinese equities have

Chapter Two FINANCIAL AND ECONOMIC INDICATORS

Chapter Two FINANCIAL AND ECONOMIC INDICATORS 1. Introduction In Chapter One we discussed the concept of risk and the importance of protecting a portfolio from losses. Managing your investment risk should

Chapter Two FINANCIAL AND ECONOMIC INDICATORS 1. Introduction In Chapter One we discussed the concept of risk and the importance of protecting a portfolio from losses. Managing your investment risk should

Markit Global Business Outlook Survey

News Release EMBARGOED UNTIL: :1 (UK), 1 March 14 Markit Global Business Outlook Survey Developed world set to lead strengthening global upturn in 14 Global business optimism hits two-year high Improved

News Release EMBARGOED UNTIL: :1 (UK), 1 March 14 Markit Global Business Outlook Survey Developed world set to lead strengthening global upturn in 14 Global business optimism hits two-year high Improved

M&G Corporate Bond Fund

Quarterly Review M&G Corporate Bond Fund Third quarter 2015 Fund manager Richard Woolnough Overview A general risk-off tone prevailed in the third quarter amid significant volatility in risk markets, driving

Quarterly Review M&G Corporate Bond Fund Third quarter 2015 Fund manager Richard Woolnough Overview A general risk-off tone prevailed in the third quarter amid significant volatility in risk markets, driving

General Certificate of Education Advanced Level Examination January 2010

General Certificate of Education Advanced Level Examination January 2010 Economics ECON4 Unit 4 The National and International Economy Tuesday 2 February 2010 1.30 pm to 3.30 pm For this paper you must

General Certificate of Education Advanced Level Examination January 2010 Economics ECON4 Unit 4 The National and International Economy Tuesday 2 February 2010 1.30 pm to 3.30 pm For this paper you must

Markit Global Business Outlook Survey

News Release EMBARGOED UNTIL: 00:01 (UK), 14 July 2014 Markit Global Business Outlook Survey Worldwide business confidence wanes Global optimism slips from two-year high Waning confidence centred on eurozone

News Release EMBARGOED UNTIL: 00:01 (UK), 14 July 2014 Markit Global Business Outlook Survey Worldwide business confidence wanes Global optimism slips from two-year high Waning confidence centred on eurozone

South African Reserve Bank. Statement of the Monetary Policy Committee. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank Press Statement Embargo Delivery 21 July 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank The UK vote to

South African Reserve Bank Press Statement Embargo Delivery 21 July 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank The UK vote to

IW Monetary Outlook December 2015

IW policy paper 37/2015 Contributions to the political debate by the Cologne Institute for Economic Research IW Monetary Outlook December 2015 Weak Credit Growth Hinders Eurozone Inflation to Increase

IW policy paper 37/2015 Contributions to the political debate by the Cologne Institute for Economic Research IW Monetary Outlook December 2015 Weak Credit Growth Hinders Eurozone Inflation to Increase

Bond to Fall in 2008 - Janet Yellen and the Euro

FUND MANAGEMENT DIARY Meeting held on 5 August 2014 Bond yields Yellen s dilemma The major questions now being asked by markets are concerns about the strength of the US recovery, the direction for interest

FUND MANAGEMENT DIARY Meeting held on 5 August 2014 Bond yields Yellen s dilemma The major questions now being asked by markets are concerns about the strength of the US recovery, the direction for interest

Monthly Economic Dashboard

RETIREMENT INSTITUTE SM Economic perspective Monthly Economic Dashboard Modest acceleration in economic growth appears in store for 2016 as the inventory-caused soft patch ends, while monetary policy moves

RETIREMENT INSTITUTE SM Economic perspective Monthly Economic Dashboard Modest acceleration in economic growth appears in store for 2016 as the inventory-caused soft patch ends, while monetary policy moves

Research US Fed on hold: uncertainty set to keep Fed sidelined

Investment Research General Market Conditions 11 February 2016 Research US Fed on hold: uncertainty set to keep Fed sidelined In our view, the uncertainty in financial markets and rising risk of a systemic

Investment Research General Market Conditions 11 February 2016 Research US Fed on hold: uncertainty set to keep Fed sidelined In our view, the uncertainty in financial markets and rising risk of a systemic

How To Be Cheerful About 2012

2012: Deeper into crisis or the long road to recovery? Bart Van Craeynest Hoofdeconoom Petercam Bart.vancraeynest@petercam.be 1 2012: crises looking for answers Global slowdown No 2008-0909 rerun Crises

2012: Deeper into crisis or the long road to recovery? Bart Van Craeynest Hoofdeconoom Petercam Bart.vancraeynest@petercam.be 1 2012: crises looking for answers Global slowdown No 2008-0909 rerun Crises

Preparing for 2015 Housing Market Opportunities

January U.S. Economic & Housing Market Outlook Preparing for 2015 Housing Market Opportunities As we enter 2015, the U.S. economy and housing markets are prepared for a robust start. Unlike one year ago,

January U.S. Economic & Housing Market Outlook Preparing for 2015 Housing Market Opportunities As we enter 2015, the U.S. economy and housing markets are prepared for a robust start. Unlike one year ago,

Why Are Government Bond Yields Still Low, and Are They Going up Any Time Soon?

September 015 MONTHLY MARKET INSIGHT Why Are Government Bond Yields Still Low, and Are They Going up Any Time Soon? The fear of rising interest rates, which has clouded investors psyches for years, has

September 015 MONTHLY MARKET INSIGHT Why Are Government Bond Yields Still Low, and Are They Going up Any Time Soon? The fear of rising interest rates, which has clouded investors psyches for years, has

Will 2014 Bring an End to Central Bank Intervention?

Will 2014 Bring an End to Central Bank Intervention? December 17, 2013 by Chris Maxey, Ryan Davis of Fortigent Please note the Economic and Market Update will be on hiatus until January 5, 2014. Stocks

Will 2014 Bring an End to Central Bank Intervention? December 17, 2013 by Chris Maxey, Ryan Davis of Fortigent Please note the Economic and Market Update will be on hiatus until January 5, 2014. Stocks

April 2015. PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy April 2015 Stocks to Stabilize & Post Gains with Further Rate Cuts & Easing Measures, ECB s QE, Gradual, Modest

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy April 2015 Stocks to Stabilize & Post Gains with Further Rate Cuts & Easing Measures, ECB s QE, Gradual, Modest

Research paper London property market snapshot JULY 2015

Research paper London property market snapshot JULY 2015 UK economy The average asking price increased by 3pc between May and June as buyers and sellers reacted to the vote. There was a major surprise

Research paper London property market snapshot JULY 2015 UK economy The average asking price increased by 3pc between May and June as buyers and sellers reacted to the vote. There was a major surprise

Spain Economic Outlook. Rafael Doménech EUI-nomics 2015 Debating the Economic Conditions in the Euro Area and Beyond Firenze, 24th of April, 2015

Spain Economic Outlook Rafael Doménech EUI-nomics 2015 Debating the Economic Conditions in the Euro Area and Beyond Firenze, 24th of April, 2015 The outlook one year ago: the risks were to the upside for

Spain Economic Outlook Rafael Doménech EUI-nomics 2015 Debating the Economic Conditions in the Euro Area and Beyond Firenze, 24th of April, 2015 The outlook one year ago: the risks were to the upside for

Statement to Parliamentary Committee

Statement to Parliamentary Committee Opening Remarks by Mr Glenn Stevens, Governor, in testimony to the House of Representatives Standing Committee on Economics, Sydney, 14 August 2009. The Bank s Statement

Statement to Parliamentary Committee Opening Remarks by Mr Glenn Stevens, Governor, in testimony to the House of Representatives Standing Committee on Economics, Sydney, 14 August 2009. The Bank s Statement

How To Get Through The Month Of August

London Market Snapshot October 2015 10/15 Global Macro Overview Global equities experienced their sharpest falls since 2011, with most major markets moving into correction territory (a fall of more than

London Market Snapshot October 2015 10/15 Global Macro Overview Global equities experienced their sharpest falls since 2011, with most major markets moving into correction territory (a fall of more than

How To Understand The Financial Market For Insurers In Swissitzerland

Actuarial and Insurance Solutions Financial Market Analysis at endyear 2014 15 th January 2015 Audit. Tax. Consulting. Corporate Finance. Contents Executive Summary 1 1 Interest Rates 2 2 Equity Markets

Actuarial and Insurance Solutions Financial Market Analysis at endyear 2014 15 th January 2015 Audit. Tax. Consulting. Corporate Finance. Contents Executive Summary 1 1 Interest Rates 2 2 Equity Markets

EFN REPORT. ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016 Spring 2015 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016 Spring 2015 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

Bond markets vote for global recovery

Bond markets vote for global recovery Weekly Market View 11 May 2015 1 % Euro area recovery, oil rebound lead to bond sell-off German bund yields recovered from record low levels, leading a surge in global

Bond markets vote for global recovery Weekly Market View 11 May 2015 1 % Euro area recovery, oil rebound lead to bond sell-off German bund yields recovered from record low levels, leading a surge in global

Greek banks and corporate funding costs

NATIONAL BANK OF GREECE Greek banks and corporate funding costs January 214 Paul Mylonas CRO & Chief Economist National Bank of Greece NBG: ECONOMIC ANALYSIS DEPARTMENT Economic Analysis Department Roadmap

NATIONAL BANK OF GREECE Greek banks and corporate funding costs January 214 Paul Mylonas CRO & Chief Economist National Bank of Greece NBG: ECONOMIC ANALYSIS DEPARTMENT Economic Analysis Department Roadmap

Insurance Market Outlook

Munich Re Economic Research May 2014 Premium growth is again slowly gathering momentum After a rather restrained 2013 (according to partly preliminary data), we expect growth in global primary insurance

Munich Re Economic Research May 2014 Premium growth is again slowly gathering momentum After a rather restrained 2013 (according to partly preliminary data), we expect growth in global primary insurance

General Certificate of Education Advanced Level Examination June 2013

General Certificate of Education Advanced Level Examination June 2013 Economics ECON4 Unit 4 The National and International Economy Tuesday 11 June 2013 9.00 am to 11.00 am For this paper you must have:

General Certificate of Education Advanced Level Examination June 2013 Economics ECON4 Unit 4 The National and International Economy Tuesday 11 June 2013 9.00 am to 11.00 am For this paper you must have:

Global Financials Update April 13, 2012

Global Financials Update April 13, 2012 Global Market Update After posting a fairly strong and consistent rally over much of the last six months, the global equity markets have changed course over the

Global Financials Update April 13, 2012 Global Market Update After posting a fairly strong and consistent rally over much of the last six months, the global equity markets have changed course over the

MBA Forecast Commentary Joel Kan

MBA Forecast Commentary Joel Kan Mortgage Originations Estimates Revised Higher MBA Economic and Mortgage Finance Commentary: February 2016 In our most recent forecast, we presented revisions to our mortgage

MBA Forecast Commentary Joel Kan Mortgage Originations Estimates Revised Higher MBA Economic and Mortgage Finance Commentary: February 2016 In our most recent forecast, we presented revisions to our mortgage

Economy, Capital Markets & Strategy

Sébastien Mc Mahon, CFA Economist Member, Asset Mix Committee Economy, Capital Markets & Strategy 2014 National Business Conference October 2014 1 October 23, 2014 Disclaimer Opinions expressed in this

Sébastien Mc Mahon, CFA Economist Member, Asset Mix Committee Economy, Capital Markets & Strategy 2014 National Business Conference October 2014 1 October 23, 2014 Disclaimer Opinions expressed in this

Summary of macroeconomic forecasts

ECONOMIC RESEARCH DEPARTMENT Summary of macroeconomic forecasts GDP Growth Inflation Curr. account / GDP Fiscal balances / GDP En % 215 216 e 217 e 215 216 e 217 e 215 216 e 217 e 215 216 e 217 e Advanced

ECONOMIC RESEARCH DEPARTMENT Summary of macroeconomic forecasts GDP Growth Inflation Curr. account / GDP Fiscal balances / GDP En % 215 216 e 217 e 215 216 e 217 e 215 216 e 217 e 215 216 e 217 e Advanced

BANK OF ISRAEL Office of the Spokesperson and Economic Information. Report to the public on the Bank of Israel s discussions prior to deciding on the

BANK OF ISRAEL Office of the Spokesperson and Economic Information September 7, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on the General interest rate for September

BANK OF ISRAEL Office of the Spokesperson and Economic Information September 7, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on the General interest rate for September

GLOBAL CENTRAL BANK WATCH

GLOBAL CENTRAL BANK WATCH How far will interest rates rise? The neutral level of interest rates in most economies is much lower than in the past However, we expect the US Fed funds rate to rise temporarily

GLOBAL CENTRAL BANK WATCH How far will interest rates rise? The neutral level of interest rates in most economies is much lower than in the past However, we expect the US Fed funds rate to rise temporarily

Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market

Communications P.O. Box, CH-8022 Zurich Telephone +41 44 631 31 11 Fax +41 44 631 39 10 Zurich, 13 September 2007 Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market The

Communications P.O. Box, CH-8022 Zurich Telephone +41 44 631 31 11 Fax +41 44 631 39 10 Zurich, 13 September 2007 Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market The

The global economy Banco de Portugal Lisbon, 24 September 2013 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

FOREX CURRENCY FORECAST (2015-2016)

") 2750 14th Avenue, Suite 30 Markham Ontario, Canada, L3R 0B Fax: 1.8.20.1740 FOREX CURRENCY FORECAST (2015-201) FOREX MAJORS (USD) 2015 201 SPOT Q1a Q2f Q3f Q4f Q1f Q2f Q3f Q4f Canadian Dollar USD/CAD 1.27

2750 14th Avenue, Suite 30 Markham Ontario, Canada, L3R 0B Fax: 1.8.20.1740 FOREX CURRENCY FORECAST (2015-201) FOREX MAJORS (USD) 2015 201 SPOT Q1a Q2f Q3f Q4f Q1f Q2f Q3f Q4f Canadian Dollar USD/CAD 1.27

M&G Corporate Bond Fund

M&G Corporate Bond Fund a sub-fund of M&G Investment Funds (3) Annual Short Report June 2015 For the year ended 30 June 2015 Fund information The Authorised Corporate Director (ACD) of M&G Investment Funds

M&G Corporate Bond Fund a sub-fund of M&G Investment Funds (3) Annual Short Report June 2015 For the year ended 30 June 2015 Fund information The Authorised Corporate Director (ACD) of M&G Investment Funds

VAKIFBANK GLOBAL ECONOMY WEEKLY

VAKIFBANK GLOBAL ECONOMY WEEKLY Is Italy Going To Be The New Weak Link After Greece? T. Vakıflar Bankası T.A.O 25 July 2011 No: 27 1 Vakıfbank Economic Research Introduction... Debt crisis which has threatened

VAKIFBANK GLOBAL ECONOMY WEEKLY Is Italy Going To Be The New Weak Link After Greece? T. Vakıflar Bankası T.A.O 25 July 2011 No: 27 1 Vakıfbank Economic Research Introduction... Debt crisis which has threatened

Eurozone. EY Eurozone Forecast September 2013

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Finland

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Finland

Contents. Key points from the 2014 Q4 Survey 4. General economic environment 5. Market conditions and the economy 6. Cash flow and risk 9 M&A 11

The Deloitte CFO Survey 2014 Q4 Results 2 Contents Key points from the 2014 Q4 Survey 4 General economic environment 5 Market conditions and the economy 6 Cash flow and risk 9 M&A 11 A note on methodology

The Deloitte CFO Survey 2014 Q4 Results 2 Contents Key points from the 2014 Q4 Survey 4 General economic environment 5 Market conditions and the economy 6 Cash flow and risk 9 M&A 11 A note on methodology

Perspective. Economic and Market. Does a 2% 10-year U.S. Bond Yield Make Sense When...

James W. Paulsen, Ph.D. Perspective Bringing you national and global economic trends for more than 30 years Economic and Market January 27, 2015 Does a 2% 10-year U.S. Bond Yield Make Sense When... For

James W. Paulsen, Ph.D. Perspective Bringing you national and global economic trends for more than 30 years Economic and Market January 27, 2015 Does a 2% 10-year U.S. Bond Yield Make Sense When... For

Oil, Russia and Greece, the leading market players

Oil, Russia and Greece, the leading market players Banca March Market Strategy Team: Miguel Ángel García, Unit Director, Market Strategy Rose Marie Boudeguer, Service Director, Study Service Pedro Sastre,

Oil, Russia and Greece, the leading market players Banca March Market Strategy Team: Miguel Ángel García, Unit Director, Market Strategy Rose Marie Boudeguer, Service Director, Study Service Pedro Sastre,

Markets Roundup. Markets eyeing falling oil prices and Japanese yen. 17 November 2014 Research

Markets Roundup 17 November 214 Research CONTENTS Market Movers 2 Economics Weekly Calendar 7 Central Bank Policies 8 Forecast Table 9 Interest Rates (3M 1yr) 1 Gov t Bond Yields (2yr 1yr) 11 Interest

Markets Roundup 17 November 214 Research CONTENTS Market Movers 2 Economics Weekly Calendar 7 Central Bank Policies 8 Forecast Table 9 Interest Rates (3M 1yr) 1 Gov t Bond Yields (2yr 1yr) 11 Interest

Recession Risk Recedes as Jobs Grow

SUMMER 2016 Recession Risk Recedes as Jobs Grow ANTHONY CHAN, PHD CHIEF ECONOMIST FOR CHASE Anthony is a member of the J.P. Morgan Global Investment Committee. He travels extensively to meet with Chase

SUMMER 2016 Recession Risk Recedes as Jobs Grow ANTHONY CHAN, PHD CHIEF ECONOMIST FOR CHASE Anthony is a member of the J.P. Morgan Global Investment Committee. He travels extensively to meet with Chase

Econ 116 Mid-Term Exam

Econ 116 Mid-Term Exam Part 1 1. True. Large holdings of excess capital and labor are indeed bad news for future investment and employment demand. This is because if firms increase their output, they will

Econ 116 Mid-Term Exam Part 1 1. True. Large holdings of excess capital and labor are indeed bad news for future investment and employment demand. This is because if firms increase their output, they will

Be prepared Four in-depth scenarios for the eurozone and for Switzerland

www.pwc.ch/swissfranc Be prepared Four in-depth scenarios for the eurozone and for Introduction The Swiss economy is cooling down and we are currently experiencing unprecedented levels of uncertainty in

www.pwc.ch/swissfranc Be prepared Four in-depth scenarios for the eurozone and for Introduction The Swiss economy is cooling down and we are currently experiencing unprecedented levels of uncertainty in

PRESENT DISCOUNTED VALUE

THE BOND MARKET Bond a fixed (nominal) income asset which has a: -face value (stated value of the bond) - coupon interest rate (stated interest rate) - maturity date (length of time for fixed income payments)

THE BOND MARKET Bond a fixed (nominal) income asset which has a: -face value (stated value of the bond) - coupon interest rate (stated interest rate) - maturity date (length of time for fixed income payments)

Summary. Economic Update 1 / 7 May 2016

Economic Update Economic Update 1 / 7 Summary 2 Global World GDP is forecast to grow only 2.4% in 2016, weighed down by emerging market weakness and increasing uncertainty. 3 Eurozone The modest eurozone

Economic Update Economic Update 1 / 7 Summary 2 Global World GDP is forecast to grow only 2.4% in 2016, weighed down by emerging market weakness and increasing uncertainty. 3 Eurozone The modest eurozone

Except for China (& Ukraine), OK?

, OK?") Except for China (& Ukraine), OK? Global economic & market outlook Riga, May 28, 2014 Harald Magnus Andreassen +47 23 23 82 60 hma@swedbank.no Usually, it has paid well off to be a sober optimist Usually,

Except for China (& Ukraine), OK? Global economic & market outlook Riga, May 28, 2014 Harald Magnus Andreassen +47 23 23 82 60 hma@swedbank.no Usually, it has paid well off to be a sober optimist Usually,

How should we assess the implications of a rise in bond yields for UK pension schemes?

How should we assess the implications of a rise in bond yields for UK pension schemes? Executive Summary In common with other, core sovereign bond markets, gilt yields are extraordinarily low by comparison

How should we assess the implications of a rise in bond yields for UK pension schemes? Executive Summary In common with other, core sovereign bond markets, gilt yields are extraordinarily low by comparison

New Plan Aims to End European Debt Crisis

New Plan Aims to End European Debt Crisis AP EU heads of state at their summit meeting in Brussels This story comes from VOA Special English, Voice of America's daily news and information service for English

New Plan Aims to End European Debt Crisis AP EU heads of state at their summit meeting in Brussels This story comes from VOA Special English, Voice of America's daily news and information service for English

FOMC review Less confident Fed likely to stay on hold in March as well

Investment Research General Market Conditions 27 January 2016 FOMC review Less confident Fed likely to stay on hold in March as well As expected, the Fed funds target rate was unchanged at 0.25%-0.50%.

Investment Research General Market Conditions 27 January 2016 FOMC review Less confident Fed likely to stay on hold in March as well As expected, the Fed funds target rate was unchanged at 0.25%-0.50%.

The following text represents the notes on which Mr. Parry based his remarks. 1998: Issues in Monetary Policymaking

Phoenix Society of Financial Analysts and Arizona State University Business School ASU, Memorial Union - Ventana Room April 24, 1998, 12:30 PM Robert T. Parry, President, FRBSF The following text represents

Phoenix Society of Financial Analysts and Arizona State University Business School ASU, Memorial Union - Ventana Room April 24, 1998, 12:30 PM Robert T. Parry, President, FRBSF The following text represents

Global Investment Outlook

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook May 2014 Stocks to Rebound with Q2 GDP & Earnings Recovery, Fresh ECB (& BoJ) Stimulus, Fed keeping U.S. Rates Low & Easing

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook May 2014 Stocks to Rebound with Q2 GDP & Earnings Recovery, Fresh ECB (& BoJ) Stimulus, Fed keeping U.S. Rates Low & Easing

Fixed Income Strategy Quarterly April 2015

Doucet Asset Management Fixed Income Strategy Quarterly April 2015 The first quarter of 2015 was a fairly uneventful one. Across the world, the pullback in yields we witnessed in 2014 continued; however,

Doucet Asset Management Fixed Income Strategy Quarterly April 2015 The first quarter of 2015 was a fairly uneventful one. Across the world, the pullback in yields we witnessed in 2014 continued; however,

Thinking tactically: What really happens next?

Thinking tactically: What really happens next? Guy Monson March 2015 Since 2008, Central bank asset purchases have successfully protected markets from an array of global risks... A SHARP INCREASE IN CENTRAL

Thinking tactically: What really happens next? Guy Monson March 2015 Since 2008, Central bank asset purchases have successfully protected markets from an array of global risks... A SHARP INCREASE IN CENTRAL

FLEXIBLE EXCHANGE RATES

FLEXIBLE EXCHANGE RATES Along with globalization has come a high degree of interdependence. Central to this is a flexible exchange rate system, where exchange rates are determined each business day by

FLEXIBLE EXCHANGE RATES Along with globalization has come a high degree of interdependence. Central to this is a flexible exchange rate system, where exchange rates are determined each business day by

PERSONAL RETIREMENT SAVINGS ACCOUNT INVESTMENT REPORT

PENSIONS INVESTMENTS LIFE INSURANCE PERSONAL RETIREMENT SAVINGS ACCOUNT INVESTMENT REPORT FOR PERSONAL RETIREMENT SAVINGS ACCOUNT () PRODUCTS WITH AN ANNUAL FUND MANAGEMENT CHARGE OF 1% - JULY 201 Thank

PENSIONS INVESTMENTS LIFE INSURANCE PERSONAL RETIREMENT SAVINGS ACCOUNT INVESTMENT REPORT FOR PERSONAL RETIREMENT SAVINGS ACCOUNT () PRODUCTS WITH AN ANNUAL FUND MANAGEMENT CHARGE OF 1% - JULY 201 Thank

ACCESS TO FINANCE. of SMEs in the euro area, European Commission and European Central Bank (ECB), November 2013.

, November 2013.") ACCESS TO FINANCE Improving access to finance is essential to restoring growth and enhancing competitiveness. Investment and innovation are not possible without adequate financing. Difficulties in accessing

ACCESS TO FINANCE Improving access to finance is essential to restoring growth and enhancing competitiveness. Investment and innovation are not possible without adequate financing. Difficulties in accessing

Wild Swings in Bonds, Currencies: Are Stocks Next? By: Bryan Rich Founder FXTraderProfessional.com

Wild Swings in Bonds, Currencies: Are Stocks Next? By: Bryan Rich Founder FXTraderProfessional.com Copyright 2015 Logic Fund Management, Inc. - Do Not Distribute or Use Without Written Permission RISK

Wild Swings in Bonds, Currencies: Are Stocks Next? By: Bryan Rich Founder FXTraderProfessional.com Copyright 2015 Logic Fund Management, Inc. - Do Not Distribute or Use Without Written Permission RISK

DTZ Foresight UK Fair Value Q2 2011 Widening yield gap raises scores

DTZ Foresight UK Fair Value Q2 Widening yield gap raises scores 23 August Contents Overview 1 Fair Value Index 2 UK market classifications 4 UK versus global forecasts 5 Office market forecasts 6 Retail

DTZ Foresight UK Fair Value Q2 Widening yield gap raises scores 23 August Contents Overview 1 Fair Value Index 2 UK market classifications 4 UK versus global forecasts 5 Office market forecasts 6 Retail

The expectation on the Korean stock market after the exit strategy of QE3

The expectation on the Korean stock market after the exit strategy of QE3 - International Finance Seoul National University Young Kwang Kong Youn Han Lee Hyoeun Kim Kyuho Lee Table of Contents

The expectation on the Korean stock market after the exit strategy of QE3 - International Finance Seoul National University Young Kwang Kong Youn Han Lee Hyoeun Kim Kyuho Lee Table of Contents

UK Economic Forecast Q1 2015

UK Economic Forecast Q1 2015 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

UK Economic Forecast Q1 2015 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

Summary Suitability of the STOXX GC Pooling EUR Deferred Funding Rate as an alternative benchmark for the money market

Summary Suitability of the STOXX GC Pooling EUR Deferred Funding Rate as an alternative benchmark for the money market An abridged version of a thesis by Jennifer Ertel (June 17,214) Sperrvermerk Die vorliegende

Summary Suitability of the STOXX GC Pooling EUR Deferred Funding Rate as an alternative benchmark for the money market An abridged version of a thesis by Jennifer Ertel (June 17,214) Sperrvermerk Die vorliegende

Market Review September 2015

Market Review September 2015 Markets remained volatile in September, impacted by the ongoing concerns over slower growth in China and other emerging markets and fears over possible contagion to the global

Market Review September 2015 Markets remained volatile in September, impacted by the ongoing concerns over slower growth in China and other emerging markets and fears over possible contagion to the global

Europe s Financial Crisis: The Euro s Flawed Design and the Consequences of Lack of a Government Banker

Europe s Financial Crisis: The Euro s Flawed Design and the Consequences of Lack of a Government Banker Abstract This paper argues the euro zone requires a government banker that manages the bond market

Europe s Financial Crisis: The Euro s Flawed Design and the Consequences of Lack of a Government Banker Abstract This paper argues the euro zone requires a government banker that manages the bond market

Monthly Economic Indicators And Charts

Monthly Economic Indicators And Charts September 15 Richard F. Moody- Chief Economist Steve Pfitzer Strategic and Corporate Planning Information contained herein is based on data obtained from recognized

Monthly Economic Indicators And Charts September 15 Richard F. Moody- Chief Economist Steve Pfitzer Strategic and Corporate Planning Information contained herein is based on data obtained from recognized

Recent U.S. Economic Growth In Charts MAY 2012

Recent U.S. Economic Growth In Charts MAY 212 GROWTH SINCE 29 The Growth Story Since 29 Despite the worst financial crisis since the Great Depression and a series of shocks in its aftermath, the economy

Recent U.S. Economic Growth In Charts MAY 212 GROWTH SINCE 29 The Growth Story Since 29 Despite the worst financial crisis since the Great Depression and a series of shocks in its aftermath, the economy

Klicken Sie, um das Titelformat. zu bearbeiten. The Eurocrisis: new challenges for the EU s. economic policy. Thomas Westphal. 23th of February 2015

The Eurocrisis: new challenges for the EU s Klicken Sie, um das Titelformat economic policy zu bearbeiten Thomas Westphal Klicken Director Sie, General um das European Format Policy des Untertitel-Masters

The Eurocrisis: new challenges for the EU s Klicken Sie, um das Titelformat economic policy zu bearbeiten Thomas Westphal Klicken Director Sie, General um das European Format Policy des Untertitel-Masters

M&G YouGov Inflation Expectations Survey

M&G YouGov Inflation Expectations Survey Q3 213 Executive summary Consumers continue to lack confidence that inflation will decline below current levels in either the short (1 year) or medium (5 years)

M&G YouGov Inflation Expectations Survey Q3 213 Executive summary Consumers continue to lack confidence that inflation will decline below current levels in either the short (1 year) or medium (5 years)

UK Economic Forecast Q3 2014

UK Economic Forecast Q3 2014 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

UK Economic Forecast Q3 2014 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

DOLLARS & SENSE TD Economics

DOLLARS & SENSE TD Economics THE FED S MESSAGE IS CLEAR: GET READY FOR HIGHER POLICY RATES Highlights Economic data and hawkish commentary from Federal Reserve members have re-adjusted market expectations

DOLLARS & SENSE TD Economics THE FED S MESSAGE IS CLEAR: GET READY FOR HIGHER POLICY RATES Highlights Economic data and hawkish commentary from Federal Reserve members have re-adjusted market expectations

TIMING YOUR INVESTMENT STRATEGIES USING BUSINESS CYCLES AND STOCK SECTORS. Developed by Peter Dag & Associates, Inc.

TIMING YOUR INVESTMENT STRATEGIES USING BUSINESS CYCLES AND STOCK SECTORS Developed by Peter Dag & Associates, Inc. 5 4 6 7 3 8 3 1 2 Fig. 1 Introduction The business cycle goes through 4 major growth

TIMING YOUR INVESTMENT STRATEGIES USING BUSINESS CYCLES AND STOCK SECTORS Developed by Peter Dag & Associates, Inc. 5 4 6 7 3 8 3 1 2 Fig. 1 Introduction The business cycle goes through 4 major growth

THE POTENTIAL MACROECONOMIC EFFECT OF DEBT CEILING BRINKMANSHIP

OCTOBER 2013 THE POTENTIAL MACROECONOMIC EFFECT OF DEBT CEILING BRINKMANSHIP Introduction The United States has never defaulted on its obligations, and the U. S. dollar and Treasury securities are at the

OCTOBER 2013 THE POTENTIAL MACROECONOMIC EFFECT OF DEBT CEILING BRINKMANSHIP Introduction The United States has never defaulted on its obligations, and the U. S. dollar and Treasury securities are at the

CIO Flash U.S. Fed tapering

CIO Flash U.S. Fed tapering 19 December 2013 The art of tapering without spoiling markets (I) Final decision and first reaction Taper light, with strengthened forward guidance The Federal Open Market Committee

CIO Flash U.S. Fed tapering 19 December 2013 The art of tapering without spoiling markets (I) Final decision and first reaction Taper light, with strengthened forward guidance The Federal Open Market Committee

New Monetary Policy Challenges

New Monetary Policy Challenges 63 Journal of Central Banking Theory and Practice, 2013, 1, pp. 63-67 Received: 5 December 2012; accepted: 4 January 2013 UDC: 336.74 Alexey V. Ulyukaev * New Monetary Policy

New Monetary Policy Challenges 63 Journal of Central Banking Theory and Practice, 2013, 1, pp. 63-67 Received: 5 December 2012; accepted: 4 January 2013 UDC: 336.74 Alexey V. Ulyukaev * New Monetary Policy

2. UK Government debt and borrowing

2. UK Government debt and borrowing How well do you understand the current UK debt position and the options open to Government to reduce the deficit? This leaflet gives you a general background to the

2. UK Government debt and borrowing How well do you understand the current UK debt position and the options open to Government to reduce the deficit? This leaflet gives you a general background to the

2013 global equity outlook: Searching for alpha in a stock picker s market

March 2013 2013 global equity outlook: Searching for alpha in a stock picker s market Saira Malik, Head of Global Equity Research, TIAA-CREF Executive summary The outlook for equity markets is favorable

March 2013 2013 global equity outlook: Searching for alpha in a stock picker s market Saira Malik, Head of Global Equity Research, TIAA-CREF Executive summary The outlook for equity markets is favorable

Annual Economic Report 2015/16 German council of economic experts. Discussion. Lucrezia Reichlin, London Business School

Annual Economic Report 2015/16 German council of economic experts Discussion Lucrezia Reichlin, London Business School Bruegel Brussels, December 4 th 2015 Four parts I. Euro area economic recovery and

Annual Economic Report 2015/16 German council of economic experts Discussion Lucrezia Reichlin, London Business School Bruegel Brussels, December 4 th 2015 Four parts I. Euro area economic recovery and