IMPERIAL COUNTY FIXED ASSET ACCOUNTING STANDARD PRACTICE MANUAL

|

|

|

- Rafe Blair

- 10 years ago

- Views:

Transcription

1 IMPERIAL COUNTY FIXED ASSET ACCOUNTING Adopted by Board of Supervisors December 23, 2008 Prepared by the Imperial County Auditor-Controller

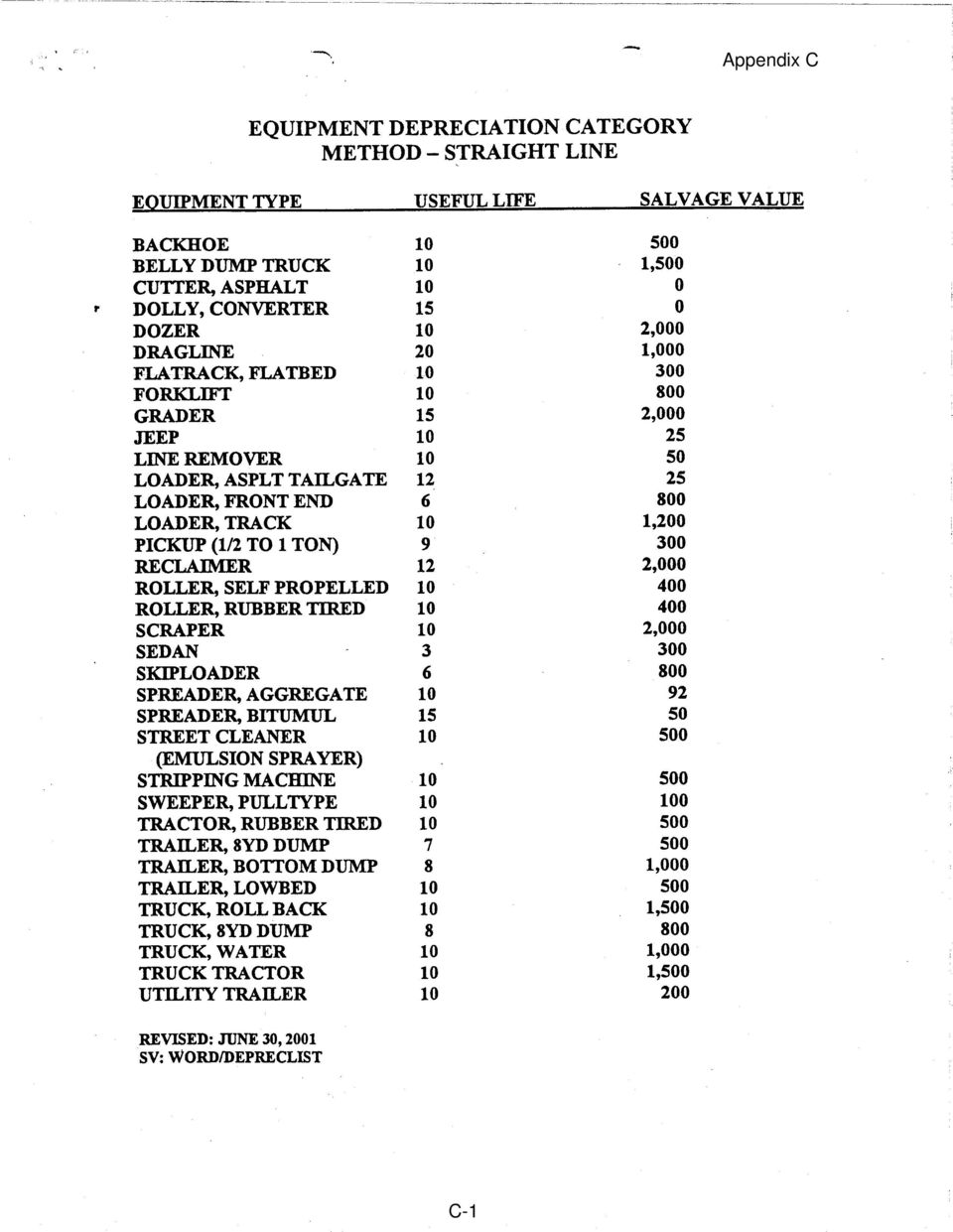

2 TABLE OF CONTENTS TITLE CHAPTER NO. PAGE NO. Fixed Asset Inventory 1 Purpose 1-1 Policy 1-1 to1-4 Depreciation of Fixed Assets 2 Purpose 2-1 Definition 2-1 Depreciable Base 2-1 Rates and method of depreciation 2-2 Depreciable lives of specified asset categories 2-2 Depreciation of assets purchased under a capital lease 2-2 Accounting for Capital Leases 3 Purpose 3-1 Policy 3-1 Background 3-1 to 3-2 Capitalization of Interest Costs 4 Purpose 4-1 Policy 4-1 Appendix Property Request Transfer Instructions/Form Automobile Depreciation Schedule Heavy Equipment Depreciation Schedule A B C

3 Chapter 1 FIXED ASSET INVENTORY PURPOSE Define accounting policy for the following types of transactions regarding fixed asset inventory: Original Acquisitions Structures and Improvements Land Retirements Betterments (Improvements) Repairs Infrastructure Sales and Involuntary Conversions POLICY General General equipment purchases with a life of more than one year, and a unit value of $7,500 or greater are to be capitalized and approved by the Board. General equipment purchases less than $7,500 are considered to be office supplies. Items having an individual unit cost of less than $7,500 are not to be capitalized, except for weapons which are capitalized regardless of cost. Groups of like designated assets individually less than $7,500, the cost of which in the aggregate exceeds $50,000 and are purchased under a program for installation over a period of time, are to be capitalized. In the case of grant programs that purchase Fixed Assets, the capitalization rules in the grant document override this policy, unless this policy has a lower amount. Additions or betterments to existing buildings that are not readily removable should be capitalized. Minimum cost to be capitalized in this respect is $50,000. All equipment purchases must have Board of Supervisors approval prior to purchase. Computer equipment such as CPU s, router s, etc. that interact with the County network must be approved by Information Systems prior to purchase. Monitors and non-network printers are deemed to be office supplies and follow the capitalization limits. 1-1

4 Original Acquisitions COUNTY OF IMPERIAL For purchased items, the capitalized amount includes the sum of the purchase price or construction cost less discounts, freight or other carriage charges, sale, use or transportation taxes, and installation costs. (State of California, Accounting Standards and Procedures for Counties, Section 15.11) Installation costs include internal costs billed by a County department or internal service fund. If equipment is being installed by a County department or internal service fund, an estimate of the installation costs should be included in determining whether the item should be capitalized and approved by the Board. An adjustment to the actual cost will be made after the actual billing has been issued. For assets donated to the County, the asset will be capitalized at the fair market value as of the date of acceptance by the Board of Supervisors. The Board action requesting acceptance should include the FMV and the rationale for the valuation. Fixed assets constructed by the County are recorded in the same manner as those acquired by purchase or construction contract. Costs included are direct labor, materials, equipment usage, and overhead. Overhead is limited to those items which can be distributed on the basis of direct labor such as worker s compensation, employee group insurance premiums, retirement costs, sick leave, and vacation allowances. Structures and Improvements The capitalized cost of structures and improvements will include the purchase price of construction costs, fixtures attached to the structure, architect s fees, accident or injury costs, payment of damages, insurance during construction, costs of permits and licenses, and net interest cost during construction. The capitalized cost should be reduced for sale of salvage, discounts, allowance and rebates, and amounts recovered through surrender of liability and casualty insurance. Interest paid during the construction period is considered a part of the cost of the asset in accordance with Statement of Financial Accounting Standards No. 34. The amount of the interest to be capitalized shall be determined in consultation with the Auditor-Controller s Office. Betterments (Improvements) A betterment (improvement) is defined as an expenditure having the effect of upgrading an existing asset, increasing its normal rate of output, lowering its operating cost or otherwise adding to the worth or benefits it can yield. The total cost of a major betterment project should be accumulated until the project is completed. At that time the cost should then be added to the original 1-2

5 cost of the asset which has been improved, so that the asset records reflect the cost of the complete asset in its improved condition. Minor betterments will be expensed as a repair. Repairs Land Repairs constitute expenditures made to place and/or maintain a fixed asset in good economic condition. In general, repairs properly chargeable to expense will include: o Minor replacements or betterment to assets where no retirement is recorded. o Major repairs which are incurred infrequently but are made to sustain the assets in normal operating condition. o Minor recurring repairs which keep the asset in normal operating condition. o Preventative maintenance costs. The capitalized cost of land will include the purchase price, appraisal and negotiation fees, title search fees, surveying fees, cost of consents, relocation costs, condemnation costs, clearing land for use, demolishing or removing structures, and filing costs. Infrastructure Public domain assets such as roads, bridges, and sidewalks are examples of infrastructure and according to Government Accounting Standards Board Statement 34 (GASB 34) the reporting of these as capital assets is required. Retirements, Sales. and Involuntary Conversions Regardless of how an asset is disposed of, the asset must be removed from the Fixed Asset Inventory at its recorded value. Involuntary conversions such as theft, loss by fire etc. should be documented by submitting a copy of the Sheriff s or police report and a loss declaration statement. 1-3

6 A Property Transfer Request (PTR) must be submitted anytime an asset is disposed or transferred. See Appendix A. Surplus equipment should be listed on a PTR if in a department s inventory and forwarded to Purchasing. If the items are not in inventory provide a simple listing of the items to Purchasing. If items need to be transported it is the departments responsibility to contact County Facilities Management for removal or some other option. 1-4

7 Chapter 2 DEPRECIATION OF FIXED ASSETS PURPOSE DEFINITION Set forth the method and regulations governing depreciation of County Fixed Assets. Depreciation is defined as an allocation of the entire cost of tangible capital assets to the operating expenses of a series of accounting periods comprising the service life of the asset, thus achieving the basic principle of matching revenue and costs. Because of the nature of governmental financing and the absence of profit determination, capital outlays are recorded as current expenditures and depreciation is not recognized. However, fixed assets utilized by Enterprise Funds, Internal Service Funds, and Nonexpendable Trust Funds are reported as fixed assets of each of these respective funds and are accounted for in the same manner as a commercial enterprise and should be depreciated. The depreciation would be recorded as a reduction in the general ledger account, Contribution from the General Fund. DEPRECIABLE BASE The depreciable base for all assets will be the total capitalized acquisition cost as defined previously. RATES AND METHOD OF DEPRECIATION General Depreciation rates are based on the estimated useful life of the asset. The useful life is determined by the estimated number of years the asset will remain in operating condition. 2-1

8 Method Unless otherwise specified by special instructions, all assets will be depreciated by the Straight Line method of depreciation. In the fiscal year that an asset is placed in service, depreciation for the full fiscal year will be taken. DEPRECIABLE LIVES OF SPECIFIED ASSET CATEGORIES Automobiles Buildings Improvements Radios Communication Equipment Furniture, Fixtures, and Office Equipment Computer Hardware Computer Software ($25,000 min) Heavy Equipment Bridges Road Systems Paved Road Systems Unpaved Life See Appendix B 40 years over remaining useful life 10 years 5 years 5 years 5 years See Appendix C 50 years 20 years 50 years The County does not establish a salvage value for fixed assets being depreciated. DEPRECIATION OF ASSETS PURCHASED UNDER A CAPITAL LEASE: For assets capitalized under a capital lease, depreciation will be recorded under the County s normal depreciation policy if the lease transfers ownership of the property to the lessee by the end of the lease term or the lease contains a bargain purchase option. However, if the capitalized lease does not meet either criterion, the County s normal depreciation policies should be followed, but the amortization period should be the lease term and not the economic life of the leased property. 2-2

Heavy Equipment Bridges Road Systems Paved Road Systems Unpaved Life See Appendix B 40 years over remaining useful life 10 years 5 years 5 years 5 years See Appendix C 50 years 20 years")

9 For further information regarding capital leases, please see Chapter 3, Accounting for Capital Leases. 2-3

10 Chapter 3 ACCOUNTING FOR CAPITAL LEASES PURPOSE POLICY This section sets forth the standards of accounting and reporting for leases in accordance with Statement of Financial Accounting Standards No. 13. The Auditor-Controller s Office will review all equipment leases to evaluate whether the lease should be treated as a capital or operating lease as defined under FAS No. 13. Assets valued at $7,500 or more, purchased through a capital lease, will be included in the fixed asset inventory at the time the lease is entered into. BACKGROUND FASB No. 13 specifies the classification, accounting and reporting of leases by both lessors and lessees. The statement takes the view that a lease that transfers substantially all of the benefits and risks of ownership should be accounted for as the acquisition of an asset and the incurrence of an obligation by the lessee (a capital lease) and as a sale or financing by the lessor (a sales type, direct financing or leveraged lease). All other leases should be accounted for as operating leases, that is, the rental of property. If a lease meets one of the following four (4) classification criteria, it is a capital lease: 1. The lease transfers ownership of the property to the lessee by the end of the lease term. 2. The lease contains an option to purchase the leased property at a bargain price. 3. The lease term is equal to or greater than 75% of the estimated economic life of the leased property. 4. The present value of rental and other minimum lease payments equals or exceeds 90% of the fair value of the lease property less any investment tax that is retained by the lessor. 3-1 December 2008

11 Criteria 3 and 4 are not applicable when the beginning of the lease term falls within the last 25 percent of the total estimated economic life of the leased property. When a lease is determined to be a capital lease because it meets one of the above criteria, the amount to be recorded is the lesser of the present value of the minimum lease payments or the fair value of the leased property. 3-2 December 2008

12 Chapter 4 CAPITALIZATION OF INTEREST COSTS PURPOSE POLICY To define the County s policy for capitalization of interest cost as provided in Statement of Financial Accounting Standards No. 34. FASB-34 states that interest costs should be capitalized as part of the acquisition cost of an asset. Interest cost must be capitalized for all assets that require an acquisition period to get them ready for their intended use. Acquisition period is defined as the period commencing with the first expenditure for a qualifying asset and ending when the asset is substantially complete and ready for its intended use. The average interest rate to be used will be applied to the average amount of accumulated expenditures on a monthly basis. It should be noted that the calculation is made only on cash spent excluding any necessary accruals. The amount of interest cost to be capitalized is limited to the actual amount of interest cost incurred for the period, i.e. capitalizing interest cost may not create a credit balance in the interest expense account. FASB-62 discusses the amount of capitalized interest cost related to tax exempt borrowings. The amount of capitalized interest cost allowable is equal to the net of total actual interest cost on the tax exempt borrowing, less any interest income earned on temporary investments of the tax exempt funds. FASB-62 applies only when an external restriction (i.e. law or contract) is imposed requiring that the borrowed funds must be directly used to acquire the assets. 4-1

13 Appendix A Property Transfer Request Form Preparation and Routing Instructions I. Originating Department: The originating department is responsible for completing the property transfer request form. (PTR). For each item transferred, list all the information requested. Any surplus items should be transferred to the Purchasing Office. Surplus items should use the following letters in the-"surplus code" column: Code A. Operating, no longer required. B. Non-operating, not economical to repair. C. Damaged/destroyed D. Traded-in E. Stolen; copy of sheriff's report and a loss declaration statement required. F. Other; explanation memo required. Forward all copies of the signed PTR and any other required documents (see E & F) to the receiving department for their approval signature. II Receiving Department: The receiving department is responsible for reviewing the PTR and approving the items transferred. After signing the PTR, forward the last copy (goldenrod) to Buildings and Grounds to schedule the move of the item(s). Forward all the other copies and any other attached documents to the Auditor-Controller. III Auditor-Controller The Auditor's office will review the PTR data for--completeness and accuracy, assign a PTR number, obtain the Administrative Office's approval and revise the internal property records to reflect the transfer. After the PTR has been approved by the Administrative Office, the Auditor-Controller will distribute copies of the completed PTR as follows: Original Green Canary Pink Auditor-Controller Originating department (transfer from) Receiving department (transfer to) Administrative Office A-1

14

15

16

CAPITALIZATION AND DEPRECIATION OF INFRASTRUCTURE. OFFICE OF THE STATE AUDITOR Division of Technical Assistance. Presentation to:

CAPITALIZATION AND DEPRECIATION OF INFRASTRUCTURE OFFICE OF THE STATE AUDITOR Division of Technical Assistance Presentation to: Mississippi Association of Governmental Purchasing and Property Agents October

CAPITALIZATION AND DEPRECIATION OF INFRASTRUCTURE OFFICE OF THE STATE AUDITOR Division of Technical Assistance Presentation to: Mississippi Association of Governmental Purchasing and Property Agents October

CHAPTER 4. 401. General Purpose... 1. 402. Definitions and Capitalization Policies... 1. 403. Budget Procedures... 2

Kern County Policy and Administrative Procedures Manual CHAPTER 4 CAPITAL ASSET ACCOUNTING Section Page 401. General Purpose... 1 402. Definitions and Capitalization Policies... 1 403. Budget Procedures...

Kern County Policy and Administrative Procedures Manual CHAPTER 4 CAPITAL ASSET ACCOUNTING Section Page 401. General Purpose... 1 402. Definitions and Capitalization Policies... 1 403. Budget Procedures...

Chapter 30 Fixed Assets

Chapter 30 Fixed Assets 30.20 Valuing, Capitalizing and Depreciating Fixed Assets 30.20.10 How to value Fixed Assets July 1, 2004 30.20.20 When to capitalize Fixed Assets July 1, 2004 30.20.22 Assets not

Chapter 30 Fixed Assets 30.20 Valuing, Capitalizing and Depreciating Fixed Assets 30.20.10 How to value Fixed Assets July 1, 2004 30.20.20 When to capitalize Fixed Assets July 1, 2004 30.20.22 Assets not

Fixed Asset Inventory

Fixed Asset Inventory The purpose of the district-wide fixed asset inventory system is to gather information for the preparation of financial statements, including estimated annual depreciation costs of

Fixed Asset Inventory The purpose of the district-wide fixed asset inventory system is to gather information for the preparation of financial statements, including estimated annual depreciation costs of

The Town of Fort Frances POLICY SECTION ACCOUNTING FOR TANGIBLE CAPITAL ASSETS. ADMINISTRATION AND FINANCE NEW: May 2009 1. PURPOSE: 2.

The Town of Fort Frances ACCOUNTING FOR TANGIBLE CAPITAL ASSETS SECTION ADMINISTRATION AND FINANCE NEW: May 2009 REVISED: POLICY Resolution Number: 05/09 Consent 156 Policy Number: 1.18 PAGE 1 of 11 Supercedes

The Town of Fort Frances ACCOUNTING FOR TANGIBLE CAPITAL ASSETS SECTION ADMINISTRATION AND FINANCE NEW: May 2009 REVISED: POLICY Resolution Number: 05/09 Consent 156 Policy Number: 1.18 PAGE 1 of 11 Supercedes

SAN FRANCISCO COMMUNITY COLLEGE DISTRICT ADMINISTRATIVE PROCEDURES MANUAL

1 of 6 A. Property Accounting All District Property shall be accounted for through the use of appropriate records and inventory procedures. Deeds shall be properly recorded and safeguarded. All equipment

1 of 6 A. Property Accounting All District Property shall be accounted for through the use of appropriate records and inventory procedures. Deeds shall be properly recorded and safeguarded. All equipment

CITY OF PORT ST LUCIE FINANCIAL POLICY CAPITAL ASSETS

CITY OF PORT ST LUCIE FINANCIAL POLICY CAPITAL ASSETS I. PURPOSE To provide effective guidelines for the recording, tracking, capitalizing, and safeguarding of the City's Capital assets. II. POLICY In

CITY OF PORT ST LUCIE FINANCIAL POLICY CAPITAL ASSETS I. PURPOSE To provide effective guidelines for the recording, tracking, capitalizing, and safeguarding of the City's Capital assets. II. POLICY In

ACCOUNTING BY GOVERNMENTAL ENTITIES ACCOUNTING AND CONTROL OF FIXED ASSETS OF STATE GOVERNMENT, ACCOUNTING FOR ACQUISITIONS AND ESTABLISHING CONTROLS

This rule was filed as 1 NMAC 1.2.1. TITLE 2 CHAPTER 20 PART 1 PUBLIC FINANCE ACCOUNTING BY GOVERNMENTAL ENTITIES ACCOUNTING AND CONTROL OF FIXED ASSETS OF STATE GOVERNMENT, ACCOUNTING FOR ACQUISITIONS

This rule was filed as 1 NMAC 1.2.1. TITLE 2 CHAPTER 20 PART 1 PUBLIC FINANCE ACCOUNTING BY GOVERNMENTAL ENTITIES ACCOUNTING AND CONTROL OF FIXED ASSETS OF STATE GOVERNMENT, ACCOUNTING FOR ACQUISITIONS

POLICY TITLE: Capitalization of Fixed Assets Policy No.: 700.16 Page 1 of 5

Page 1 of 5 A. Capitalization Policy This policy determines which District-owned and leased assets will be capitalized for purposes of financial reporting and inventory control processes. It is important

Page 1 of 5 A. Capitalization Policy This policy determines which District-owned and leased assets will be capitalized for purposes of financial reporting and inventory control processes. It is important

Regulations of the University of North Texas System Chapter 08. Fiscal Management. 08.9000 Asset Capitalization

Regulations of the University of North Texas System Chapter 08 08.9000 Asset Capitalization Fiscal Management 08.9001 Regulation Statement. The University of North Texas System shall identify, measure,

Regulations of the University of North Texas System Chapter 08 08.9000 Asset Capitalization Fiscal Management 08.9001 Regulation Statement. The University of North Texas System shall identify, measure,

CAPITALIZATION OF PROPERTY, PLANT, AND EQUIPMENT P-415-10 ACCOUNTING MANUAL Page 1 CAPITALIZATION OF PROPERTY, PLANT, AND EQUIPMENT.

ACCOUNTING MANUAL Page 1 CAPITALIZATION OF PROPERTY, PLANT, AND EQUIPMENT Contents I. Introduction 2 II. Definitions 2 III. Principles 2 IV. Basic Capitalization Framework at UC 3 A. Asset Acquired for

ACCOUNTING MANUAL Page 1 CAPITALIZATION OF PROPERTY, PLANT, AND EQUIPMENT Contents I. Introduction 2 II. Definitions 2 III. Principles 2 IV. Basic Capitalization Framework at UC 3 A. Asset Acquired for

FIXED ASSET PROCEDURES

FIXED ASSET PROCEDURES To comply with the fixed asset capitalization and inventory policy adopted by the Governing Board, and to ensure compliance with the GASB 34 (Government Accounting Board Statement

FIXED ASSET PROCEDURES To comply with the fixed asset capitalization and inventory policy adopted by the Governing Board, and to ensure compliance with the GASB 34 (Government Accounting Board Statement

Collin County Community College District Business Administrative Services Procedures Manual Section 8 Capital Assets

Revision Log: Collin County Community College District Business Administrative Services Procedures Manual Section 8 Capital Assets Sub Section Revision Date Summary of Change 8.1 Introduction The District

Revision Log: Collin County Community College District Business Administrative Services Procedures Manual Section 8 Capital Assets Sub Section Revision Date Summary of Change 8.1 Introduction The District

Fixed Asset Management

Fixed Asset Management Policy/Procedure This policy applies to faculty and staff with responsibility for purchasing, maintaining or disposing of Fixed Assets, including Department Chairs, Department Heads,

Fixed Asset Management Policy/Procedure This policy applies to faculty and staff with responsibility for purchasing, maintaining or disposing of Fixed Assets, including Department Chairs, Department Heads,

AAM 55. CAPITAL ASSETS

AAM 55. CAPITAL ASSETS 55.010 Accounting 06/02 55.020 Valuation of 07/12 55.025 Thresholds for Capitalizing 07/12 55.030 Acquisition of 06/02 55.040 Repairs & Improvements 07/12 55.050 Depreciation 01/03

AAM 55. CAPITAL ASSETS 55.010 Accounting 06/02 55.020 Valuation of 07/12 55.025 Thresholds for Capitalizing 07/12 55.030 Acquisition of 06/02 55.040 Repairs & Improvements 07/12 55.050 Depreciation 01/03

SOLUTIONS TO EXERCISES

EXERCISE 10-1 (15 20 minutes) SOLUTIONS TO EXERCISES Item Land Land Improvements Building Other Accounts (a) ($275,000) Notes Payable (b) $275,000 (c) $ 8,000 (d) 7,000 (e) 6,000 (f) (1,000) (g) 22,000

EXERCISE 10-1 (15 20 minutes) SOLUTIONS TO EXERCISES Item Land Land Improvements Building Other Accounts (a) ($275,000) Notes Payable (b) $275,000 (c) $ 8,000 (d) 7,000 (e) 6,000 (f) (1,000) (g) 22,000

AGATE FIRE PROTECTION DISTRICT RESOLUTION NO. 11-0908 A RESOLUTION OF THE AGATE FIRE PROTECTION DISTRICT BOARD OF

RESOLUTION NO. 11-0908 A RESOLUTION OF THE AGATE FIRE PROTECTION DISTRICT BOARD OF DIRECTORS ADOPTING A CAPITALIZATION POLICY WHEREAS, the Governmental Accounting Standards Board issued Pronouncement #34

RESOLUTION NO. 11-0908 A RESOLUTION OF THE AGATE FIRE PROTECTION DISTRICT BOARD OF DIRECTORS ADOPTING A CAPITALIZATION POLICY WHEREAS, the Governmental Accounting Standards Board issued Pronouncement #34

Title: FIXED ASSET ACCOUNTING Code: B0108

POLICY Title: FIXED ASSET ACCOUNTING Code: B0108 Authority: Board Minutes, 9/16/91; 10/28/97 Original Adoption: 9/16/91 Revised/Reviewed: 10/28/97 Effective: 10/29/97 It is the policy of the Board that

POLICY Title: FIXED ASSET ACCOUNTING Code: B0108 Authority: Board Minutes, 9/16/91; 10/28/97 Original Adoption: 9/16/91 Revised/Reviewed: 10/28/97 Effective: 10/29/97 It is the policy of the Board that

This policy sets forth system-wide standards for financial accounting and reporting of leases.

Accounting for Leases Section: Accounting and Financial Reporting Title: Accounting for Leases Number: 05.281 Index POLICY.100 POLICY STATEMENT.110 POLICY RATIONALE.120 AUTHORITY.130 APPROVAL AND EFFECTIVE

Accounting for Leases Section: Accounting and Financial Reporting Title: Accounting for Leases Number: 05.281 Index POLICY.100 POLICY STATEMENT.110 POLICY RATIONALE.120 AUTHORITY.130 APPROVAL AND EFFECTIVE

Manual of Accounting and Financial Reporting for Pennsylvania Public Schools CHAPTER 11 TABLE OF CONTENTS 11.A. Chapter 11 11.1

Manual of Accounting and Financial Reporting for Pennsylvania Public Schools CHAPTER 11 TABLE OF CONTENTS 11.1 Capital Assets And Infrastructure 11.1 What Are Capital Assets? 11.1 Valuation Of Capital

Manual of Accounting and Financial Reporting for Pennsylvania Public Schools CHAPTER 11 TABLE OF CONTENTS 11.1 Capital Assets And Infrastructure 11.1 What Are Capital Assets? 11.1 Valuation Of Capital

E. Custodian - the Vice President for Administrative Services and Finance or designee.

Florida Gulf Coast University Policy Manual TITLE: Tangible Personal Property Policy Policy: 3.033 Approved: 1/13/12 Responsible Executive: Vice President for Administrative Services and Finance Responsible

Florida Gulf Coast University Policy Manual TITLE: Tangible Personal Property Policy Policy: 3.033 Approved: 1/13/12 Responsible Executive: Vice President for Administrative Services and Finance Responsible

Property, Plant and Equipment

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 16 Property, Plant and Equipment SB-FRS 16 Property, Plant and Equipment applies to Statutory Boards for annual periods beginning on or after 1 January

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 16 Property, Plant and Equipment SB-FRS 16 Property, Plant and Equipment applies to Statutory Boards for annual periods beginning on or after 1 January

CAPITAL ASSETS. POLICY No. 07-04

CAPITAL ASSETS POLICY No. 07-04 PURPOSE: DEFINITION: To provide for the safeguarding of fixed assets and to provide County personnel with accounting guidance applicable to the several categories of fixed

CAPITAL ASSETS POLICY No. 07-04 PURPOSE: DEFINITION: To provide for the safeguarding of fixed assets and to provide County personnel with accounting guidance applicable to the several categories of fixed

AP 531 - TANGIBLE CAPITAL ASSETS

AP 531 - TANGIBLE CAPITAL ASSETS The following topics are discussed in this administrative procedure: 1.0 Policy 2.0 Purpose 3.0 Scope 4.0 Glossary 5.0 Categorization of Assets 6.0 Accounting and Reporting

AP 531 - TANGIBLE CAPITAL ASSETS The following topics are discussed in this administrative procedure: 1.0 Policy 2.0 Purpose 3.0 Scope 4.0 Glossary 5.0 Categorization of Assets 6.0 Accounting and Reporting

Statewide Accounting Policy & Procedure

Statewide Accounting Policy & Procedure Accounting Manual Reference: Section: Capital Assets Sub-section: Asset Transfers and Other Disposals Effective Date: 07/01/2010 Revision Date: 06/30/2011 Index:

Statewide Accounting Policy & Procedure Accounting Manual Reference: Section: Capital Assets Sub-section: Asset Transfers and Other Disposals Effective Date: 07/01/2010 Revision Date: 06/30/2011 Index:

DEPARTMENT OF ADMINISTRATION POLICY MANUAL Revision Date 06/20/2013 Filing Number 13,001 Date Issued 07/72 Page 1 of 12 Revisions throughout

Date Issued 07/72 Page 1 of 12 SUBJECT Capital Asset Records PURPOSE To provide capital asset policies and procedures for both Comprehensive Annual Financial Report (CAFR) and non-cafr reporting AUTHORITATIVE

Date Issued 07/72 Page 1 of 12 SUBJECT Capital Asset Records PURPOSE To provide capital asset policies and procedures for both Comprehensive Annual Financial Report (CAFR) and non-cafr reporting AUTHORITATIVE

FAYETTEVILLE STATE UNIVERSITY

FAYETTEVILLE STATE UNIVERSITY FIXED ASSETS Authority: Category: Issued by the Chancellor. Changes or exceptions to administrative policies issued by the Chancellor may only be made by the Chancellor. Business,

FAYETTEVILLE STATE UNIVERSITY FIXED ASSETS Authority: Category: Issued by the Chancellor. Changes or exceptions to administrative policies issued by the Chancellor may only be made by the Chancellor. Business,

City of Laredo, Texas Capital Asset Policy and Procedures Effective October 1, 2006

City of Laredo, Texas Capital Asset Policy and Procedures Effective October 1, 2006 1.0 Policy Goal The goal of a capital asset inventory system and this policy is to provide control and accountability

City of Laredo, Texas Capital Asset Policy and Procedures Effective October 1, 2006 1.0 Policy Goal The goal of a capital asset inventory system and this policy is to provide control and accountability

MARQUETTE UNIVERSITY Office of the Comptroller Capitalization, Inventory, Depreciation and Retirement of Property, Buildings, and Equipment

MARQUETTE UNIVERSITY Office of the Comptroller Capitalization, Inventory, Depreciation and Retirement of Property, Buildings, and Equipment Direct all inquiries to: Comptroller s Office 288-0833 Effective

MARQUETTE UNIVERSITY Office of the Comptroller Capitalization, Inventory, Depreciation and Retirement of Property, Buildings, and Equipment Direct all inquiries to: Comptroller s Office 288-0833 Effective

Uniform Accounting Network Inventory Manual. Table of Contents. Warranty Maintenance Debt Management Depreciation Disposal

Inventory Manual Uniform Accounting Network Inventory Manual Table of Contents Introduction Parts of the Manual Part 1 Assets Chapter 1 Acquisition Warranty Maintenance Debt Management Depreciation Disposal

Inventory Manual Uniform Accounting Network Inventory Manual Table of Contents Introduction Parts of the Manual Part 1 Assets Chapter 1 Acquisition Warranty Maintenance Debt Management Depreciation Disposal

FIXED ASSET AND CAPITAL PURCHASE POLICY

FIXED ASSET AND CAPITAL PURCHASE POLICY Section I: Definition of a Fixed Asset: A Fixed Asset is any tangible asset purchased for use in the day-to-day operations of the College from which an economic

FIXED ASSET AND CAPITAL PURCHASE POLICY Section I: Definition of a Fixed Asset: A Fixed Asset is any tangible asset purchased for use in the day-to-day operations of the College from which an economic

Table of Contents. Volume No. 1 Policies and Procedures TOPIC NO 30210 - Cardinal Section No. 30200 Asset Acquisition TOPIC Acquisition Valuation

Table of Contents Overview...2 Introduction...2 Cardinal Transition Entries...2 Policy...3 General...3 Procedures...5 Acquisition Value...5 Valuation Methods...8 Salvage Value...8 Avoid Overstating Asset

Table of Contents Overview...2 Introduction...2 Cardinal Transition Entries...2 Policy...3 General...3 Procedures...5 Acquisition Value...5 Valuation Methods...8 Salvage Value...8 Avoid Overstating Asset

Student Learning Outcomes

Chapter 15 Leases Part 2: Capital Leases Intermediate Accounting II Dr. Chula King Student Learning Outcomes Explain and use the criteria for determining whether a lease is capital or not Describe and

Chapter 15 Leases Part 2: Capital Leases Intermediate Accounting II Dr. Chula King Student Learning Outcomes Explain and use the criteria for determining whether a lease is capital or not Describe and

Capital Asset Accounting Policies POLICY STATEMENT

Responsible Executive: Controller Responsible Department: A&FS Review Date: May, 2015 Accounting & Financial Services Capital Asset Accounting Policies POLICY STATEMENT I. Capital Asset Policy A. General

Responsible Executive: Controller Responsible Department: A&FS Review Date: May, 2015 Accounting & Financial Services Capital Asset Accounting Policies POLICY STATEMENT I. Capital Asset Policy A. General

COUNTY OF FLUVANNA ACCOUNTING & FINANCIAL REPORTING POLICIES AND PROCEDURES

COUNTY OF FLUVANNA ACCOUNTING & FINANCIAL REPORTING POLICIES AND PROCEDURES Consolidation of Capital Expenditures (1.2), Vendor Refunds and Credit Memos (1.3), and Adjusting Journal Entries (1.6) Adopted

COUNTY OF FLUVANNA ACCOUNTING & FINANCIAL REPORTING POLICIES AND PROCEDURES Consolidation of Capital Expenditures (1.2), Vendor Refunds and Credit Memos (1.3), and Adjusting Journal Entries (1.6) Adopted

ADMINISTRATION AND FINANCE POLICIES AND PROCEDURES. FIXED & MOVABLE ASSETS ACCOUNTING/INVENTORY CONTROL Revision Date: 01/01/2014 TABLE OF CONTENTS

Chapter 10 ADMINISTRATION AND FINANCE POLICIES AND PROCEDURES FIXED & MOVABLE ASSETS ACCOUNTING/INVENTORY CONTROL Revision Date: 01/01/2014 TABLE OF CONTENTS 10-01 Overview 10-02 Types of Capital Assets

Chapter 10 ADMINISTRATION AND FINANCE POLICIES AND PROCEDURES FIXED & MOVABLE ASSETS ACCOUNTING/INVENTORY CONTROL Revision Date: 01/01/2014 TABLE OF CONTENTS 10-01 Overview 10-02 Types of Capital Assets

Audit Program for Fixed Assets

Form AP 35 Index Audit Program for Fixed Assets Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding of the

Form AP 35 Index Audit Program for Fixed Assets Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding of the

Money Grants From Private and Public Sources

CHAPTER 15 COUNTY FINANCES; PURCHASING Accounting Systems and Policies 15.010 Definitions. 15.020 County fund types and account groups. 15.030 Basis of accounting for governmental, expendable trust, agency

CHAPTER 15 COUNTY FINANCES; PURCHASING Accounting Systems and Policies 15.010 Definitions. 15.020 County fund types and account groups. 15.030 Basis of accounting for governmental, expendable trust, agency

Capital Asset Policy. User Guide for Cobb County Employees 4/21/2015. Created for: The Cobb County School District

User Guide for Cobb County Employees 4/21/2015 Created for: The Cobb County School District 514 Glover Street Marietta, Ga. 30060 (770) 426-3300 Created by: CCSD Financial Services Accounting Services

User Guide for Cobb County Employees 4/21/2015 Created for: The Cobb County School District 514 Glover Street Marietta, Ga. 30060 (770) 426-3300 Created by: CCSD Financial Services Accounting Services

HOWARD UNIVERSITY. I. Policy Statement. II. Rationale. III. Entities Affected by the Policy. IV. Definitions. Policy Number: 300-004

HOWARD UNIVERSITY Policy Number: 300-004 Policy Title: ASSET CAPITALIZATION Responsible Officer: Chief Financial Officer Responsible Offices: Office of the Controller, Departments of Strategic Sourcing

HOWARD UNIVERSITY Policy Number: 300-004 Policy Title: ASSET CAPITALIZATION Responsible Officer: Chief Financial Officer Responsible Offices: Office of the Controller, Departments of Strategic Sourcing

Accounting Notes. Types (classifications) of Assets:

of Assets:") Types (classifications) of s: 1) Current s - short lived assets used in the operations of a business 2) Plant s - long lived tangible assets used in the operations of a business 3) Long Term Investment

Types (classifications) of s: 1) Current s - short lived assets used in the operations of a business 2) Plant s - long lived tangible assets used in the operations of a business 3) Long Term Investment

Number: 1-3 Date Issued: July 15, 1999 Date Revised: October 26, 2010. Subject: Responsible Department: Approved: Purpose. Definitions of Terms

ADMINISTRATIVE ORDER Subject: Responsible Department: Financial Fixed Assets Inventory Finance Number: 1-3 Date Issued: July 15, 1999 Date Revised: Approved: Purpose To establish a uniform policy for the

ADMINISTRATIVE ORDER Subject: Responsible Department: Financial Fixed Assets Inventory Finance Number: 1-3 Date Issued: July 15, 1999 Date Revised: Approved: Purpose To establish a uniform policy for the

TATE COUNTY SCHOOL DISTRICT FIXED ASSET REPORTING TABLE OF CONTENTS BOARD POLICY FIXED ASSET ACCOUNTABILITY ASSET FORM A ASSET REPORTING FORM

TATE COUNTY SCHOOL DISTRICT FIXED ASSET REPORTING TABLE OF CONTENTS INTRODUCTION BOARD POLICY FIXED ASSET ACCOUNTABILITY FORM INSTRUCTIONS ASSET FORM A ASSET REPORTING FORM ASSET FORM B ASSET TRANSFER

TATE COUNTY SCHOOL DISTRICT FIXED ASSET REPORTING TABLE OF CONTENTS INTRODUCTION BOARD POLICY FIXED ASSET ACCOUNTABILITY FORM INSTRUCTIONS ASSET FORM A ASSET REPORTING FORM ASSET FORM B ASSET TRANSFER

Fixed Assets Accounting Policy & Procedure

Fixed Assets Accounting Policy & Procedure Table of Contents 01. Policy Statement... 2 02. Reason for Policy... 2 03. Roles and Responsibilities... 2 04. Capitalization Policy... 3 05. Classifications

Fixed Assets Accounting Policy & Procedure Table of Contents 01. Policy Statement... 2 02. Reason for Policy... 2 03. Roles and Responsibilities... 2 04. Capitalization Policy... 3 05. Classifications

CITY OF COLEMAN, TEXAS FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR'S REPORT SEPTEMBER 30, 2014

CITY OF COLEMAN, TEXAS FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR'S REPORT SEPTEMBER 30, 2014 Becky Roberts, CPA 104 Pine Street, Suite 610 Abilene, Texas 79601 325-665-5239 [email protected]

CITY OF COLEMAN, TEXAS FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR'S REPORT SEPTEMBER 30, 2014 Becky Roberts, CPA 104 Pine Street, Suite 610 Abilene, Texas 79601 325-665-5239 [email protected]

How To Account For Property, Plant And Equipment

International Accounting Standard 16 Property, Plant and Equipment Objective 1 The objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of

International Accounting Standard 16 Property, Plant and Equipment Objective 1 The objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of

Department of State Treasurer. Policy Manual for Local Governments. Section 20: Capital Assets

Department of State Treasurer Policy Manual for Local Governments Revision Issued: August 2014 Table of Contents Executive Summary... 1 Part I Introduction... 3 A Purpose and Applicability... 3 B. Functions

Department of State Treasurer Policy Manual for Local Governments Revision Issued: August 2014 Table of Contents Executive Summary... 1 Part I Introduction... 3 A Purpose and Applicability... 3 B. Functions

Accounting Policies. 4.02 Land and Land Improvements. 4.03 Buildings and Building Service Equipment. 4.04 Leasehold Improvements

Page 1 of 14 Accounting Policies Section 4.0 Capital Assets 4.01 Capital Assets Defined 4.02 Land and Land Improvements 4.03 Buildings and Building Service Equipment 4.04 Leasehold Improvements 4.05 Equipment

Page 1 of 14 Accounting Policies Section 4.0 Capital Assets 4.01 Capital Assets Defined 4.02 Land and Land Improvements 4.03 Buildings and Building Service Equipment 4.04 Leasehold Improvements 4.05 Equipment

CHAPTER 10. Acquisition and Disposition of Property, Plant, and Equipment 1, 2, 3, 4, 6, 7, 12, 13, 18 16, 18, 19, 22

CHAPTER 10 Acquisition and Disposition of Property, Plant, and Equipment ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Valuation

CHAPTER 10 Acquisition and Disposition of Property, Plant, and Equipment ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Valuation

PINAL COUNTY POLICY AND PROCEDURE 8.8. Replaces Policy Dated: January 12, 1981, and subsequent revisions to date

PINAL COUNTY POLICY AND PROCEDURE 8.8 Subject: CAPITAL ASSETS Date: Effective as of July 1, 2009 Pages: 1 of 6 Replaces Policy Dated: January 12, 1981, and subsequent revisions to date Purpose: The purpose

PINAL COUNTY POLICY AND PROCEDURE 8.8 Subject: CAPITAL ASSETS Date: Effective as of July 1, 2009 Pages: 1 of 6 Replaces Policy Dated: January 12, 1981, and subsequent revisions to date Purpose: The purpose

INDONESIAN INSTITUTE OF ACCOUNTANTS FIXED ASSETS AND OTHER ASSETS

STATEMENT OF SFAS No. FINANCIAL ACCOUNTING STANDARD 16 INDONESIAN INSTITUTE OF ACCOUNTANTS FIXED ASSETS AND OTHER ASSETS Statement of Financial Accounting Standard (SFAS) No.16, Fixed Assets and Other

STATEMENT OF SFAS No. FINANCIAL ACCOUNTING STANDARD 16 INDONESIAN INSTITUTE OF ACCOUNTANTS FIXED ASSETS AND OTHER ASSETS Statement of Financial Accounting Standard (SFAS) No.16, Fixed Assets and Other

Capitalization and Depreciation Guidelines

Capitalization and Depreciation Guidelines Guidelines Statement University of Vermont assets that are capitalized are considered fixed assets and are recorded in the Capital Assets section of the University's

Capitalization and Depreciation Guidelines Guidelines Statement University of Vermont assets that are capitalized are considered fixed assets and are recorded in the Capital Assets section of the University's

Accounting for Long-term Assets,

1 Accounting for Long-term Assets, Long-term Debt and Leases TABLE OF CONTENTS Introduction 2 Long-term Assets 2 Acquiring or creating 2 Tangible assets 2 Intangible assets 3 Depreciating, amortizing and

1 Accounting for Long-term Assets, Long-term Debt and Leases TABLE OF CONTENTS Introduction 2 Long-term Assets 2 Acquiring or creating 2 Tangible assets 2 Intangible assets 3 Depreciating, amortizing and

Charter Township of Fenton. Financial Report with Supplemental Information December 31, 2013

Financial Report with Supplemental Information December 31, 2013 Contents Report Letter 1-2 Management's Discussion and Analysis 3-7 Basic Financial Statements Government-wide Financial Statements: Statement

Financial Report with Supplemental Information December 31, 2013 Contents Report Letter 1-2 Management's Discussion and Analysis 3-7 Basic Financial Statements Government-wide Financial Statements: Statement

State of Florida Statewide Financial Statements Capital Asset Policy. Introduction

Introduction For fiscal year ending June 30, 2002, the State of Florida will be required to implement Statement No. 34 of the Governmental Accounting Standards Board (GASB), Basic Financial Statements

Introduction For fiscal year ending June 30, 2002, the State of Florida will be required to implement Statement No. 34 of the Governmental Accounting Standards Board (GASB), Basic Financial Statements

FIXED ASSET ACCOUNTING AND MANAGEMENT PROCEDURES MANUAL. 1 Purpose. 2 Scope. 3 Guidelines. SECTION 2 Asset Valuation

Section 2 1 Purpose The purpose of this section is to define procedures and organizational responsibilities for establishing total fixed asset acquisition costs. All fixed assets and controlled items acquired

Section 2 1 Purpose The purpose of this section is to define procedures and organizational responsibilities for establishing total fixed asset acquisition costs. All fixed assets and controlled items acquired

SOUTH CAROLINA APPALACHIAN COUNCIL OF GOVERNMENTS AUDITED FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2012

SOUTH CAROLINA APPALACHIAN COUNCIL OF GOVERNMENTS AUDITED FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2012 SOUTH CAROLINA APPALACHIAN COUNCIL OF GOVERNMENTS AUDITED FINANCIAL STATEMENTS YEAR ENDED JUNE 30,

SOUTH CAROLINA APPALACHIAN COUNCIL OF GOVERNMENTS AUDITED FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2012 SOUTH CAROLINA APPALACHIAN COUNCIL OF GOVERNMENTS AUDITED FINANCIAL STATEMENTS YEAR ENDED JUNE 30,

Adapted, with permission, from The Canadian Institute of Chartered Accountants, Toronto, Canada, October, 1998.

Introduction to LEASING Adapted, with permission, from The Canadian Institute of Chartered Accountants, Toronto, Canada, October, 1998. COMMON LEASING TERMS The following list comprises some standard definitions

Introduction to LEASING Adapted, with permission, from The Canadian Institute of Chartered Accountants, Toronto, Canada, October, 1998. COMMON LEASING TERMS The following list comprises some standard definitions

CHAPTER 10. Acquisition and Disposition of Property, Plant, and Equipment 1, 2, 3, 5, 6, 11, 12, 21 11, 15, 16 8, 9, 10, 11, 12

CHAPTER 10 Acquisition and Disposition of Property, Plant, and Equipment ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Valuation

CHAPTER 10 Acquisition and Disposition of Property, Plant, and Equipment ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Valuation

CHAPTER 21. Accounting for Leases ASSIGNMENT CLASSIFICATION TABLE

CHAPTER 21 Accounting for Leases ASSIGNMENT CLASSIFICATION TABLE Topics Questions Brief Exercises Exercises Problems Cases *1. Rationale for leasing. 1, 2, 4 1, 2 *2. Lessees; classification of leases;

CHAPTER 21 Accounting for Leases ASSIGNMENT CLASSIFICATION TABLE Topics Questions Brief Exercises Exercises Problems Cases *1. Rationale for leasing. 1, 2, 4 1, 2 *2. Lessees; classification of leases;

University System of Maryland Capital Asset & Depreciation Guidance

University System of Maryland Capital Asset & Depreciation Guidance Prepared by USM Office Final as of June 27, 2002 Introduction The purpose of this document is to provide guidance for the uniform recording

University System of Maryland Capital Asset & Depreciation Guidance Prepared by USM Office Final as of June 27, 2002 Introduction The purpose of this document is to provide guidance for the uniform recording

HEADING: CONTRACT AGENCY LEGAL NAME

COUNTY OF LOS ANGELES - DEPARTMENT OF HEALTH SERVICES ALCOHOL AND DRUG PROGRAM ADMINISTRATION COST REPORT FOR CONTRACTED SERVICES OUTPATIENT DRUG FREE SERVICES INSTRUCTIONS COST REPORT FOR CONTRACTED SERVICES

COUNTY OF LOS ANGELES - DEPARTMENT OF HEALTH SERVICES ALCOHOL AND DRUG PROGRAM ADMINISTRATION COST REPORT FOR CONTRACTED SERVICES OUTPATIENT DRUG FREE SERVICES INSTRUCTIONS COST REPORT FOR CONTRACTED SERVICES

AUTOMOBILE ACCIDENT COMPENSATION ADMINISTRATION. Financial Statements and Independent Auditors Report. June 30, 2001 and 2000

AUTOMOBILE ACCIDENT COMPENSATION ADMINISTRATION Financial Statements and Independent Auditors Report Balance Sheets Assets 2001 2000 Cash and cash equivalents $ 5,175,507 $ 5,012,402 Collateral received

AUTOMOBILE ACCIDENT COMPENSATION ADMINISTRATION Financial Statements and Independent Auditors Report Balance Sheets Assets 2001 2000 Cash and cash equivalents $ 5,175,507 $ 5,012,402 Collateral received

COUNTY OF LOS ANGELES - DEPARTMENT OF HEALTH SERVICES ALCOHOL AND DRUG PROGRAM ADMINISTRATION COST REPORT FOR CONTRACTED SERVICES INSTRUCTIONS

COUNTY OF LOS ANGELES - DEPARTMENT OF HEALTH SERVICES ALCOHOL AND DRUG PROGRAM ADMINISTRATION COST REPORT FOR CONTRACTED SERVICES INSTRUCTIONS COST REPORT FOR CONTRACTED SERVICES (SUMMARY PAGE) Complete

COUNTY OF LOS ANGELES - DEPARTMENT OF HEALTH SERVICES ALCOHOL AND DRUG PROGRAM ADMINISTRATION COST REPORT FOR CONTRACTED SERVICES INSTRUCTIONS COST REPORT FOR CONTRACTED SERVICES (SUMMARY PAGE) Complete

NATIONAL ENERGY EDUCATION DEVELOPMENT PROJECT, INC. Financial Statements and Supplemental Information

NATIONAL ENERGY EDUCATION DEVELOPMENT PROJECT, INC. Financial Statements and Supplemental Information (With Summarized Financial Information for the Year Ended December 31, 2011) and Report Thereon TABLE

NATIONAL ENERGY EDUCATION DEVELOPMENT PROJECT, INC. Financial Statements and Supplemental Information (With Summarized Financial Information for the Year Ended December 31, 2011) and Report Thereon TABLE

CAPITAL / FIXED ASSET POLICY

Town of Emerald Isle CAPITAL / FIXED ASSET POLICY Adopted August, 10, 2004 Mayor Arthur B. Schools, Jr. Board of Commissioners Nita Hedreen Robert Isenhour Patricia McElraft Floyd Messer, Jr. John Wootten

Town of Emerald Isle CAPITAL / FIXED ASSET POLICY Adopted August, 10, 2004 Mayor Arthur B. Schools, Jr. Board of Commissioners Nita Hedreen Robert Isenhour Patricia McElraft Floyd Messer, Jr. John Wootten

ASSET MANAGEMENT MANUAL

ASSET MANAGEMENT MANUAL Prepared by The Department of Internal Audit W. Chuck Jackson, Senior Internal Auditor Business Office Sharolyn Miller Chief Financial Officer First Issued July 2000 Revised July

ASSET MANAGEMENT MANUAL Prepared by The Department of Internal Audit W. Chuck Jackson, Senior Internal Auditor Business Office Sharolyn Miller Chief Financial Officer First Issued July 2000 Revised July

FLORIDA HIGH SCHOOL FOR ACCELERATED LEARNING - WEST PALM BEACH CAMPUS, INC. d/b/a QUANTUM HIGH SCHOOL

LEARNING - WEST PALM BEACH CAMPUS, INC. Financial Statements with Independent Auditors Reports Thereon June 30, 2015 CONTENTS Page Management s Discussion and Analysis 1 6 Report of Independent Auditors

LEARNING - WEST PALM BEACH CAMPUS, INC. Financial Statements with Independent Auditors Reports Thereon June 30, 2015 CONTENTS Page Management s Discussion and Analysis 1 6 Report of Independent Auditors

Expenditure Accounting: Governmental Funds. Chapter 6

Expenditure Accounting: Governmental Funds Chapter 6 Learning Objectives Define expenditures Understand & apply expenditure recognition guidance Understand multiple classifications of expenditures Account

Expenditure Accounting: Governmental Funds Chapter 6 Learning Objectives Define expenditures Understand & apply expenditure recognition guidance Understand multiple classifications of expenditures Account

Orange County s United Way

Financial Statements Years Ended June 30, 2015 and 2014 The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member of BDO

Financial Statements Years Ended June 30, 2015 and 2014 The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member of BDO

Manual of Accounting and Financial Reporting for Pennsylvania Public Schools CHAPTER 9 TABLE OF CONTENTS. Chapter 9 9.1

Manual of Accounting and Financial Reporting for Pennsylvania Public Schools CHAPTER 9 TABLE OF CONTENTS 9.1 9.1 ENTERPRISE FUNDS 9.2 Nature And Purpose 9.2 Food Service Fund 9.2 Basis Of Accounting And

Manual of Accounting and Financial Reporting for Pennsylvania Public Schools CHAPTER 9 TABLE OF CONTENTS 9.1 9.1 ENTERPRISE FUNDS 9.2 Nature And Purpose 9.2 Food Service Fund 9.2 Basis Of Accounting And

The following document was not prepared by the Office of the State Auditor, but was prepared by and submitted to the Office of the State Auditor by a

The following document was not prepared by the Office of the State Auditor, but was prepared by and submitted to the Office of the State Auditor by a private CPA firm. The document was placed on this web

The following document was not prepared by the Office of the State Auditor, but was prepared by and submitted to the Office of the State Auditor by a private CPA firm. The document was placed on this web

RANDALL COUNTY FIXED ASSET POLICY April 2002 Revised 5/20/2014

RANDALL COUNTY FIXED ASSET POLICY April 2002 Revised 5/20/2014 Fixed Asset Policy 1 I. INTRODUCTION The Taxpayers of Randall County have an enormous investment in our county buildings, land, furnishings,

RANDALL COUNTY FIXED ASSET POLICY April 2002 Revised 5/20/2014 Fixed Asset Policy 1 I. INTRODUCTION The Taxpayers of Randall County have an enormous investment in our county buildings, land, furnishings,

3. ACCOUNTING. 3.3 Capital Assets 3.3.4 Capital Asset System Accounting

3. ACCOUNTING 3.3 Capital Assets 3.3.4 Capital Asset System Accounting 3.3.4.10 Once the capital asset system is in operation, the government needs to make sure that assets which should be capitalized

3. ACCOUNTING 3.3 Capital Assets 3.3.4 Capital Asset System Accounting 3.3.4.10 Once the capital asset system is in operation, the government needs to make sure that assets which should be capitalized

BA 351 CORPORATE FINANCE. John R. Graham Adapted from S. Viswanathan LECTURE 5 LEASING FUQUA SCHOOL OF BUSINESS DUKE UNIVERSITY

BA 351 CORPORATE FINANCE John R. Graham Adapted from S. Viswanathan LECTURE 5 LEASING FUQUA SCHOOL OF BUSINESS DUKE UNIVERSITY 1 Leasing has long been an important alternative to buying an asset. In this

BA 351 CORPORATE FINANCE John R. Graham Adapted from S. Viswanathan LECTURE 5 LEASING FUQUA SCHOOL OF BUSINESS DUKE UNIVERSITY 1 Leasing has long been an important alternative to buying an asset. In this

International Accounting Standard 40 Investment Property

International Accounting Standard 40 Investment Property Objective 1 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

International Accounting Standard 40 Investment Property Objective 1 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

Montgomery County Nursing Home

County Nursing Home A Component Unit of County, Arkansas Accountants Report and Financial Statements County Nursing Home A Component Unit of County, Arkansas Contents Independent Accountants Report on

County Nursing Home A Component Unit of County, Arkansas Accountants Report and Financial Statements County Nursing Home A Component Unit of County, Arkansas Contents Independent Accountants Report on

Board Memorandum. Objective: Establish procedures for the disposal of the District s surplus property within the Fixed Asset and Capital Asset Policy.

Board Memorandum September 24, 2015 To: From: General Manager Tamara Sexton, Business Services Manager Subject: Amend the Fixed Asset and Capital Asset Policy Objective: Establish procedures for the disposal

Board Memorandum September 24, 2015 To: From: General Manager Tamara Sexton, Business Services Manager Subject: Amend the Fixed Asset and Capital Asset Policy Objective: Establish procedures for the disposal

TOWN OF MANCHESTER, MARYLAND. FINANCIAL STATEMENTS June 30, 2015

FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT... 1 MANAGEMENT S DISCUSSION AND ANALYSIS... 3 FINANCIAL STATEMENTS... 13 Government wide Financial Statements Statement of Net Position...14

FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT... 1 MANAGEMENT S DISCUSSION AND ANALYSIS... 3 FINANCIAL STATEMENTS... 13 Government wide Financial Statements Statement of Net Position...14

CAPITAL ASSET/LONG TERM DEBT ACCOUNTING ENTRY EXAMPLES

NOTE: All items in RED are offsets between the governmental fund and the SWGF 80 or SWGF 90. ADDITIONS: CAPITAL ASSET/LONG TERM DEBT ACCOUNTING ENTRY EXAMPLES CAPITAL ASSET EXAMPLES A vehicle was purchased

NOTE: All items in RED are offsets between the governmental fund and the SWGF 80 or SWGF 90. ADDITIONS: CAPITAL ASSET/LONG TERM DEBT ACCOUNTING ENTRY EXAMPLES CAPITAL ASSET EXAMPLES A vehicle was purchased

AD VALOREM TAX ADOPTED BUDGET

AD VALOREM TAX ADOPTED BUDGET AGGREGATE TAX RATE AMENDMENT APPROPRIATION ASSESSED VALUE BALANCE FORWARD BALANCE FORWARD - CAPITAL A tax levied on the assessed value of real property (also known as "property

AD VALOREM TAX ADOPTED BUDGET AGGREGATE TAX RATE AMENDMENT APPROPRIATION ASSESSED VALUE BALANCE FORWARD BALANCE FORWARD - CAPITAL A tax levied on the assessed value of real property (also known as "property

CONTENTS. Independent Auditors Report... 1. Consolidated Statements of Financial Position... 2. Consolidated Statements of Activities...

CONTENTS Independent Auditors Report... 1 Consolidated Statements of Financial Position... 2 Consolidated Statements of Activities...3-4 Consolidated Statements of Cash Flows... 5 Notes to the Consolidated

CONTENTS Independent Auditors Report... 1 Consolidated Statements of Financial Position... 2 Consolidated Statements of Activities...3-4 Consolidated Statements of Cash Flows... 5 Notes to the Consolidated

Accounting Norms and Principles January 7, 2003

1 Accounting Norms and Principles January 7, 2003 The purpose of an accounting system is to provide credit union management with complete and accurate financial information that can be used to operate

1 Accounting Norms and Principles January 7, 2003 The purpose of an accounting system is to provide credit union management with complete and accurate financial information that can be used to operate

AS 10 : Accounting for Fixed Assets

AS 10 : Accounting for Fixed Assets IPCC Paper 1: Accounting Chapter 1 Unit 2 Fixed Assets - AS 10 Related ASI is 2 CA. Yagnesh Desai 1 Applicability This standards was introduced in 1985 It is applicable

AS 10 : Accounting for Fixed Assets IPCC Paper 1: Accounting Chapter 1 Unit 2 Fixed Assets - AS 10 Related ASI is 2 CA. Yagnesh Desai 1 Applicability This standards was introduced in 1985 It is applicable

General Ledger Accounts Report

General Ledger Accounts Report AcctID 1010 Cash in Bank All funds on deposit with a bank or savings and loan institution, normally in non-interest-bearing accounts. Interest-bearing accounts are recorded

General Ledger Accounts Report AcctID 1010 Cash in Bank All funds on deposit with a bank or savings and loan institution, normally in non-interest-bearing accounts. Interest-bearing accounts are recorded

The Basics of Lease Accounting

The Basics of Lease Accounting Joe Sebik, VP - Global Originations & Structuring J. P. Morgan Leasing, Inc. (212) 899-1249 [email protected] Howard Thompson, Director - Pricing & Economics Key

The Basics of Lease Accounting Joe Sebik, VP - Global Originations & Structuring J. P. Morgan Leasing, Inc. (212) 899-1249 [email protected] Howard Thompson, Director - Pricing & Economics Key

Revised Fixed Assets Policy & Procedures Manual

Revised Fixed Assets Policy & Procedures Manual November 2008 0 TABLE OF CONTENTS 1 INTRODUCTION... 5 2 FIXED ASSET DEFINITION... 5 3 FIXED ASSET SYSTEM PURPOSE... 7 3.1 FINANCIAL STATEMENT INFORMATION...

Revised Fixed Assets Policy & Procedures Manual November 2008 0 TABLE OF CONTENTS 1 INTRODUCTION... 5 2 FIXED ASSET DEFINITION... 5 3 FIXED ASSET SYSTEM PURPOSE... 7 3.1 FINANCIAL STATEMENT INFORMATION...

COMMUNITY BLOOD CENTERS OF FLORIDA, INC. AND AFFILIATE

CONSOLIDATED FINANCIAL STATEMENTS CONTENTS Independent Auditors Report...1 Consolidated Financial Statements Statement of Financial Position... 2-3 Statement of Activities and Changes in Net Assets...4

CONSOLIDATED FINANCIAL STATEMENTS CONTENTS Independent Auditors Report...1 Consolidated Financial Statements Statement of Financial Position... 2-3 Statement of Activities and Changes in Net Assets...4

6. Depreciation is a process of a. asset devaluation. b. cost accumulation. c. cost allocation. d. asset valuation.

1. A company purchased land for $72,000 cash. Real estate brokers' commission was $5,000 and $7,000 was spent for demolishing an old building on the land before construction of a new building could start.

1. A company purchased land for $72,000 cash. Real estate brokers' commission was $5,000 and $7,000 was spent for demolishing an old building on the land before construction of a new building could start.

WATER UTILITY REFERENCE MANUAL

Utility Plant and Accumulated Depreciation Capitalization Policy Costs are capitalized in the utility plant accounts, rather than being expensed in the current year, if: the service life is more than one

Utility Plant and Accumulated Depreciation Capitalization Policy Costs are capitalized in the utility plant accounts, rather than being expensed in the current year, if: the service life is more than one