CASH WORKING CAPITAL

|

|

|

- Joanna Sparks

- 8 years ago

- Views:

Transcription

1 Filed: Page of CASH WORKING CAPITAL.0 PURPOSE This evidence presents OPG s methodology for calculating cash working capital. Application of this methodology produces a forecast of annual cash working capital for the regulated hydroelectric facilities of $. M in both 0 and 0, and for the nuclear facilities, the test period forecast of annual cash working is $.0 M in both 0 and 0 as follows: OVERVIEW OPG conducted a lead/lag study as part of the EB application. A lead/lag study is used by utilities to determine their cash working capital requirements. A lead/lag study analyzes transactions throughout the year to determine the number of days between the time services are rendered and payment is received (revenue lag), and the number of days between the time expenditures are incurred and payment is made for such services (expense or payment lead). A revenue lag is determined and compared to an expense lead, and the resulting net lag is then applied to each category of operating expense to determine the cash working capital requirements. OPG has not conducted a new lead/lag study for this application given that: the OEB accepted OPG s cash working capital calculation in the last hearing; the OEB s filing

2 Filed: Page of 0 0 guidelines do not contemplate a lead/lag study; and the amount of cash working capital is small relative to the overall size of rate base. Instead, OPG has used a simpler approach and applied the net lag days provided in its EB evidence to 00 revenues and expenses. For the bridge year, OPG used this approach, but included a half year s impact of the Harmonized Sales Tax ( HST ) because HST comes into effect on July, 00. The test period includes the full impact of the HST..0 METHODOLOGY OPG s regulated business earns revenues from generation sales and other revenues. The two revenue types each have a distinct cash receipt cycle. Each component of working capital consists of revenue lags for each type of revenue and specific expense leads that relate to each type of expenditure. Consistent with the approach described in EB-00-00, OPG has applied the net lag days provided in EB to revenue and expense categories using 00 financial results for OPG s regulated assets because this is the most recent information available. The resulting cash working capital is then used for 00. The only change for subsequent years is to include the impact of the HST as discussed below. In addition to the working capital calculations for generation sales and other revenues, OPG s EB lead/lag study calculated cash working capital requirements related to the GST separately and included it as a component of cash working capital. The per cent GST is being replaced by a per cent HST effective July, 00. While the HST rules have not been finalized, OPG has assumed that they will be similar to the GST in terms of net lag days. OPG has maintained the 00 cash working capital component as the base, and prorated the impact the HST based on the time that it is in effect (i.e., half a year in 00 and a full year in 0 and 0). The full-year amount used in the test period is determined by applying per cent divided by per cent to each component of the 00 GST cash working capital component, Chart shows the prorated the effects of HST in 00, 0 and 0. As a result of the OEB s EB Decision, only net revenue from the Bruce Lease determined in accordance with Canadian GAAP is included in the revenue requirement for OPG s prescribed facilities. As cash working capital is not included in net revenues, the Bruce Lease revenue net revenue lag is no longer included in OPG s cash working capital calculation.

3 Filed: Page of Chart summarizes the results of applying the methodology discussed above to actual 00 data. 0.0 GENERATION SALES The largest component of revenue is generation sales, which consists of electricity sales and the provision of ancillary services to the IESO. The revenue lag associated with generation sales and the associated expense leads described in EB and detailed cash working capital calculations for 00 are provided in Chart (for nuclear generation) and Chart (for regulated hydroelectric generation). Expense categories for nuclear are listed if the expense amount is greater than $M; therefore the categories presented in the summary charts may differ from those shown for previous years in EB

4 Corrected: Page of Chart Cash Working Capital Generation Nuclear 00 Expense Amount Revenue Expense Net Lead/Lag CWC Line ($M) Lag Days Lead Days Days ($M) No. Expense Category (a) (b) (c) (d) = (b) (c) (e) = (a)*(d)/ OM&A direct Labour, EPSCA Labour Consultants Nuclear 0... (.) (.) Consultants Corporate.. 0. (.) (0.) Augmented Staff Nuclear... (.) (.) Augmented Staff Corporate.0.. (.) (0.) Outsourced Services Corporate Telecommunications... (.) (0.) Utilities... (.) (0.) 0 Facilities Operating Licences Membership Fees.. (.). 0. Transport Work Equipment.0..0 (0.) (0.) Donations All other cash expenses OM&A Centrally held Costs OPEB/Pensions (0.)... (.0) Incentives (0.) (.) PWU EHT (0.) (.) ONFA fee.. (.)..0 0 Gregorian Adjustment Insurance.. (0.).. Total OM&A. Other Costs: property taxes..... capital taxes income tax Total Other Costs. Total for Nuclear.

. 0. Transport Work Equipment.0..0 (0.) (0.) Donations.. 0.0. 0. All other cash expenses....0 0. OM&A Centrally held Costs OPEB/Pensions (0.)... (.0) Incentives.. 0.0 (0.) (.) PWU EHT.. 0.0 (0.) (.) ONFA fee.")

5 Filed: Page of.0 OTHER REVENUE Other Revenue consists of cobalt and tritium isotope sales and inspection and maintenance services as described in Ex G-T-S. The lead/lag days from the study presented in EB have been applied to the appropriate 00 expenses and Chart summarizes the results.

6 Filed: Page of 0.0 GOODS and SERVICES TAX/HARMONIZED SALES TAX OPG pays HST to suppliers for the purchase of goods and services and remits HST that is collected on revenue to the Federal Government. The HST lag is the time between the HST payment date (to the supplier or to the Receiver General) and the date the Federal Government either refunds the HST to OPG or when OPG receives the input tax credit. OPG also collects HST from the IESO before making the remittance to the Receiver General. OPG collects significantly more HST than it pays to suppliers. A HST cash working capital amount is calculated for each of the two types of revenue. The calculation of HST is as follows: Collections: OPG remits HST after the IESO pays for the previous month s power. The remittance is made at the end of the next fiscal month. For example, if the IESO pays OPG HST for June s power production on July, OPG reports it on the July HST remittance, which is paid on September. o On average OPG retains the HST for a net period of. days. For simplicity, the term HST will be used to refer to the goods and services tax whether it is GST up to July,00 or HST thereafter

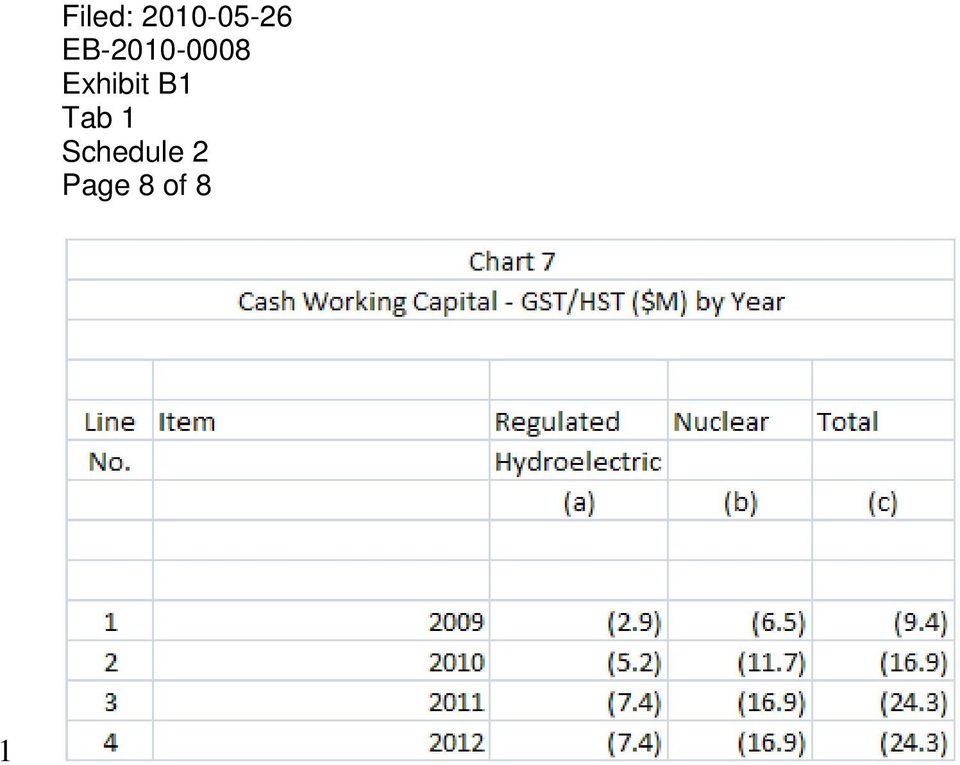

7 Filed: Page of o The amount of regulated HST = total HST collected from the IESO x the regulated station s share of total generation sales. Payments: OPG generally pays HST on all purchases and then claims an input tax credit on its monthly HST remittance. For example, the goods received in June are included in the June HST remittance paid on July. o On average, OPG paid HST 0 days before receiving the HST credits. The 00 GST cash working capital is calculated as shown in Chart : 0 Since there will be a significant increase with the move from the GST ( per cent) in 00 to the HST ( per cent) in the test period, OPG applied a simple average to determine the annual cash working capital impacts. For example, 0 was calculated as the 00 amounts times per cent divided by per cent. Chart provides the annual amounts:

in 00 to the HST ( per cent) in the test period,")

8 Filed: Page of

CASH WORKING CAPITAL

Filed: 0-09- EB-0-0 Exhibit B Page of.0 PURPOSE CASH WORKING CAPITAL This evidence presents OPG s methodology for calculating cash working capital. Application of this methodology produces a forecast of

Filed: 0-09- EB-0-0 Exhibit B Page of.0 PURPOSE CASH WORKING CAPITAL This evidence presents OPG s methodology for calculating cash working capital. Application of this methodology produces a forecast of

COMPARISON OF CENTRALLY HELD COSTS

Filed: 0-0- EB-0-000 Schedule Page of 0 0 COMPARISON OF CENTRALLY HELD COSTS.0 PURPOSE This evidence presents the period-over-period comparisons of centrally held costs that are directly assigned and allocated

Filed: 0-0- EB-0-000 Schedule Page of 0 0 COMPARISON OF CENTRALLY HELD COSTS.0 PURPOSE This evidence presents the period-over-period comparisons of centrally held costs that are directly assigned and allocated

2. Cash Working Capital Lead/Lag Study. Cash Working Capital Lead/Lag Study

Cash Working Capital Lead/Lag Study May 2007 Table of Contents 1.0 Introduction...1 2.0 Method and Approach...1 2.1 Method...1 2.2 Approach...2 3.0 Lead/Lag Study...3 3.1 Revenue Lag...4 3.2 Expense Lag...4

Cash Working Capital Lead/Lag Study May 2007 Table of Contents 1.0 Introduction...1 2.0 Method and Approach...1 2.1 Method...1 2.2 Approach...2 3.0 Lead/Lag Study...3 3.1 Revenue Lag...4 3.2 Expense Lag...4

SCHEDULE OF SELECT ASSETS AND LIABILITIES OF OPG S NEWLY REGULATED HYDROELECTRIC FACILITIES AS AT DECEMBER 31, 2013

SCHEDULE OF SELECT ASSETS AND LIABILITIES OF OPG S NEWLY REGULATED HYDROELECTRIC FACILITIES AS AT DECEMBER 31, 2013 Page 1 of 7 The Ontario Energy Board Act, 1998 and Ontario Regulation 53/05 provide that,

SCHEDULE OF SELECT ASSETS AND LIABILITIES OF OPG S NEWLY REGULATED HYDROELECTRIC FACILITIES AS AT DECEMBER 31, 2013 Page 1 of 7 The Ontario Energy Board Act, 1998 and Ontario Regulation 53/05 provide that,

WORKING CAPITAL AND LEAD/LAG

Updated: February 23, 2007 EB-2005-0501 Exhibit D1 Tab 1 Schedule 5 Page 1 of 2 1 2 3 1.0 INTRODUCTION WORKING CAPITAL AND LEAD/LAG 4 5 6 7 Working capital is the amount of funds required to finance the

Updated: February 23, 2007 EB-2005-0501 Exhibit D1 Tab 1 Schedule 5 Page 1 of 2 1 2 3 1.0 INTRODUCTION WORKING CAPITAL AND LEAD/LAG 4 5 6 7 Working capital is the amount of funds required to finance the

RATE BASE. Filed: 2013-12-19 EB-2013-0416 Exhibit D1 Tab 1 Schedule 1 Page 1 of 8 1.0 INTRODUCTION

Filed: 0-- EB-0-0 Exhibit D Tab Schedule Page of.0 INTRODUCTION RATE BASE This exhibit provides the forecast of Hydro One Distribution s rate base for the test years 0 to 0 and provides a detailed description

Filed: 0-- EB-0-0 Exhibit D Tab Schedule Page of.0 INTRODUCTION RATE BASE This exhibit provides the forecast of Hydro One Distribution s rate base for the test years 0 to 0 and provides a detailed description

PROJECT AND PORTFOLIO MANAGEMENT - NUCLEAR

Page 1 of 5 PROJECT AND PORTFOLIO MANAGEMENT - NUCLEAR 1.0 PURPOSE This evidence provides an overview of the nuclear operations project portfolio and other related project work. The project portfolio includes

Page 1 of 5 PROJECT AND PORTFOLIO MANAGEMENT - NUCLEAR 1.0 PURPOSE This evidence provides an overview of the nuclear operations project portfolio and other related project work. The project portfolio includes

Return to PST Questions and Answers

Return to PST Questions and Answers Is there a transitional period introduced in the Provincial Sales Tax Act ( PSTA )? When the Harmonized Sales Tax ( HST ) replaced the Goods and Services Tax ( GST )

Return to PST Questions and Answers Is there a transitional period introduced in the Provincial Sales Tax Act ( PSTA )? When the Harmonized Sales Tax ( HST ) replaced the Goods and Services Tax ( GST )

Corporate Support Functions and Cost Allocation

Corporate Support Functions and Cost Allocation OPG Regulated Facilities Payment Amounts Stakeholder Meeting #2 April 1, 2010 Tom Staines Director, Finance Outline Corporate Support Functions Corporate

Corporate Support Functions and Cost Allocation OPG Regulated Facilities Payment Amounts Stakeholder Meeting #2 April 1, 2010 Tom Staines Director, Finance Outline Corporate Support Functions Corporate

Line 2007 2008 2009 2010 2011 2012 No. Corporate Costs Actual Actual Actual Budget Plan Plan (a) (b) (c) (d) (e) (f)

(b) (c) (d) (e) (f)") Table 1 Table 1 Corporate Support & Administrative Groups - OPG ($M) No. Corporate Costs Actual Actual Actual Budget Plan Plan 1 Business Services & IT 1 214.0 207.4 207.2 205.2 208.2 207.9 2 Finance 2

Table 1 Table 1 Corporate Support & Administrative Groups - OPG ($M) No. Corporate Costs Actual Actual Actual Budget Plan Plan 1 Business Services & IT 1 214.0 207.4 207.2 205.2 208.2 207.9 2 Finance 2

TRANSITIONAL RULES FOR THE NEW BRUNSWICK HST RATE INCREASE

TRANSITIONAL RULES FOR THE NEW BRUNSWICK HST RATE INCREASE March 30, 2016 This Notice provides general descriptions of transitional rules for the increase in the Harmonized Sales Tax (HST) rate to 15 per

TRANSITIONAL RULES FOR THE NEW BRUNSWICK HST RATE INCREASE March 30, 2016 This Notice provides general descriptions of transitional rules for the increase in the Harmonized Sales Tax (HST) rate to 15 per

Attachment 2-1 Distribution System Plan Attachment 2-2 OEB Appendix 2-FA and 2-FC REG Expansion Investment

Waterloo North Hydro Inc. EB-2015-0108 Exhibit 2 Page 1 of 95 Filed: May 1, 2015 TABLE OF CONTENTS 2.5 EXHIBIT 2 - RATE BASE.... 2 2.5.1 Rate Base...2 2.5.1.1 Overview... 2 2.5.1.2 Gross Assets Property

Waterloo North Hydro Inc. EB-2015-0108 Exhibit 2 Page 1 of 95 Filed: May 1, 2015 TABLE OF CONTENTS 2.5 EXHIBIT 2 - RATE BASE.... 2 2.5.1 Rate Base...2 2.5.1.1 Overview... 2 2.5.1.2 Gross Assets Property

AUTOMOBILE EXPENSES & RECORDKEEPING

February 2015 CONTENTS Who should keep records? Expenses to track Deductible expenses Keeping a kilometre log Business vs. personal Other motor vehicles The standby charge GST/HST and QST considerations

February 2015 CONTENTS Who should keep records? Expenses to track Deductible expenses Keeping a kilometre log Business vs. personal Other motor vehicles The standby charge GST/HST and QST considerations

FACTS & FIGURES. Tax Audit Accounting Consulting

FACTS & FIGURES Tax Audit Accounting Consulting FACTS AND FIGURES FOR TAX PREPARATION AND PLANNING JULY, 2013 CHAPTER 1B PERSONAL INCOME TAX 1.1 Federal Tax Rates - Individuals... 1 1.2 Federal Personal

FACTS & FIGURES Tax Audit Accounting Consulting FACTS AND FIGURES FOR TAX PREPARATION AND PLANNING JULY, 2013 CHAPTER 1B PERSONAL INCOME TAX 1.1 Federal Tax Rates - Individuals... 1 1.2 Federal Personal

DEPRECIATION AND AMORTIZATION EXPENSES

Filed: September, 00 Exhibit C Tab Schedule Page of DEPRECIATION AND AMORTIZATION EXPENSES.0 INTRODUCTION The depreciation and amortization expense for Hydro One s Distribution business in its 00 test

Filed: September, 00 Exhibit C Tab Schedule Page of DEPRECIATION AND AMORTIZATION EXPENSES.0 INTRODUCTION The depreciation and amortization expense for Hydro One s Distribution business in its 00 test

2015 FEDERAL BUDGET SUMMARY

2015 FEDERAL BUDGET SUMMARY April 21, 2015 TABLE OF CONTENTS Table of contents Introduction Personal Income Tax Measures Business Income Tax Measures Charities International Tax Notice to Users 2 2015

2015 FEDERAL BUDGET SUMMARY April 21, 2015 TABLE OF CONTENTS Table of contents Introduction Personal Income Tax Measures Business Income Tax Measures Charities International Tax Notice to Users 2 2015

TREASURER S DIRECTIONS ACCOUNTING ASSETS Section A2.9 : Prepayments

TREASURER S DIRECTIONS ACCOUNTING ASSETS Section A2.9 : Prepayments STATEMENT OF INTENT Accurate recording of prepayments allows costs to be apportioned over more than one reporting period rather than

TREASURER S DIRECTIONS ACCOUNTING ASSETS Section A2.9 : Prepayments STATEMENT OF INTENT Accurate recording of prepayments allows costs to be apportioned over more than one reporting period rather than

How To Read The Financial Statements Of The Osc

Management s Responsibility and Certification Management is responsible for the integrity, consistency and reliability of the financial statements and other information presented in the annual report.

Management s Responsibility and Certification Management is responsible for the integrity, consistency and reliability of the financial statements and other information presented in the annual report.

July 1, 2010 TO THE GOVERNING AUTHORITIES OF ALL MISSISSIPPI MUNICIPALITIES

OFFICE OF THE STATE AUDITOR STACEY E. PICKERING AUDITOR July 1, 2010 TO THE GOVERNING AUTHORITIES OF ALL MISSISSIPPI MUNICIPALITIES We are pleased to provide the 2010 Municipal Audit and Accounting Guide.

OFFICE OF THE STATE AUDITOR STACEY E. PICKERING AUDITOR July 1, 2010 TO THE GOVERNING AUTHORITIES OF ALL MISSISSIPPI MUNICIPALITIES We are pleased to provide the 2010 Municipal Audit and Accounting Guide.

Doing Business in Canada GST/HST Information for Non-Residents

Doing Business in Canada GST/HST Information for Non-Residents RC4027(E) Rev.10 Is this guide for you? T his guide explains how the Canadian goods and services tax/harmonized sales tax (GST/HST) applies

Doing Business in Canada GST/HST Information for Non-Residents RC4027(E) Rev.10 Is this guide for you? T his guide explains how the Canadian goods and services tax/harmonized sales tax (GST/HST) applies

EXPERIENCE ECONALYSIS CONSULTING SERVICES. William O. Harper

ECONALYSIS CONSULTING SERVICES William O. Harper Mr. Harper has over 30 years experience in the design of rates and the regulation of electricity utilities. While employed by Ontario Hydro, he has testified

ECONALYSIS CONSULTING SERVICES William O. Harper Mr. Harper has over 30 years experience in the design of rates and the regulation of electricity utilities. While employed by Ontario Hydro, he has testified

Ontario Energy Board. 2014-2017 Business Plan

Ontario Energy Board 2014-2017 Business Plan Ontario Energy Board P.O. Box 2319 2300 Yonge Street 27th Floor Toronto ON M4P 1E4 Telephone: (416) 481-1967 Facsimile: (416) 440-7656 Toll-free: 1 888 632-6273

Ontario Energy Board 2014-2017 Business Plan Ontario Energy Board P.O. Box 2319 2300 Yonge Street 27th Floor Toronto ON M4P 1E4 Telephone: (416) 481-1967 Facsimile: (416) 440-7656 Toll-free: 1 888 632-6273

Prince Edward Island announces transitional rules for harmonized sales tax

Prince Edward Island announces transitional rules for harmonized sales tax November 2012 Effective April 1, 2013, Prince Edward Island (PEI) is replacing its federal and provincial sales tax system with

Prince Edward Island announces transitional rules for harmonized sales tax November 2012 Effective April 1, 2013, Prince Edward Island (PEI) is replacing its federal and provincial sales tax system with

CAMBRIDGE AND NORTH DUMFRIES HYDRO INC. Financial Statements. Year Ended December 31, 2013

CAMBRIDGE AND NORTH DUMFRIES HYDRO INC. Financial Statements Financial Statements Contents Page Auditors Report 3 4 Financial Statements Balance Sheet 5 6 Statement of Income and Comprehensive Income 7

CAMBRIDGE AND NORTH DUMFRIES HYDRO INC. Financial Statements Financial Statements Contents Page Auditors Report 3 4 Financial Statements Balance Sheet 5 6 Statement of Income and Comprehensive Income 7

Customer Bill Impacts of Generation Sources in Ontario. Canadian Wind Energy Association

Customer Bill Impacts of Generation Sources in Ontario Prepared for: Canadian Wind Energy Association February 15, 2013 poweradvisoryllc.com 978 369-2465 Table of Contents Executive Summary... i 1. Introduction

Customer Bill Impacts of Generation Sources in Ontario Prepared for: Canadian Wind Energy Association February 15, 2013 poweradvisoryllc.com 978 369-2465 Table of Contents Executive Summary... i 1. Introduction

Scorecard - Oakville Hydro Electricity Distribution Inc.

Scorecard - Oakville Hydro Electricity Distribution Inc. 9/24/215 Performance Outcomes Performance Categories Measures 21 211 212 213 214 Trend Industry Distributor Target Customer Focus Services are provided

Scorecard - Oakville Hydro Electricity Distribution Inc. 9/24/215 Performance Outcomes Performance Categories Measures 21 211 212 213 214 Trend Industry Distributor Target Customer Focus Services are provided

PART II. TERMS AND CONDITIONS

I acknowledge and agree with the Seller as follows: PART II. TERMS AND CONDITIONS 1. Entire Agreement These Terms and Conditions and the Sign Up Form together make up the agreement with the Seller (my

I acknowledge and agree with the Seller as follows: PART II. TERMS AND CONDITIONS 1. Entire Agreement These Terms and Conditions and the Sign Up Form together make up the agreement with the Seller (my

Basic Accounting. Supplement for Using Simply Accounting Version 8.0 for Windows by. M. Purbhoo and D. Purbhoo

Basic Accounting Supplement for Using Simply Accounting Version 8.0 for Windows by M. Purbhoo and D. Purbhoo Basic Accounting Contents: Accounting Theory 3 Basic Accounting 3 Balance Sheet 3 Income Statement

Basic Accounting Supplement for Using Simply Accounting Version 8.0 for Windows by M. Purbhoo and D. Purbhoo Basic Accounting Contents: Accounting Theory 3 Basic Accounting 3 Balance Sheet 3 Income Statement

Consolidated Financial Statements. Toronto Hydro Corporation December 31, 2005

Consolidated Financial Statements Toronto Hydro Corporation Contents Page Auditors' Report 1 Consolidated Balance Sheet 2 Consolidated Statement of Retained Earnings 3 Consolidated Statement of Income

Consolidated Financial Statements Toronto Hydro Corporation Contents Page Auditors' Report 1 Consolidated Balance Sheet 2 Consolidated Statement of Retained Earnings 3 Consolidated Statement of Income

COST OF LONG-TERM DEBT

Filed: 0-- EB-0-0 Exhibit B Tab Schedule Page of COST OF LONG-TERM DEBT.0 HYDRO ONE DISTRIBUTION LONG-TERM DEBT The debt portfolio for Hydro One Distribution, as set out in Exhibit B, Tab, Schedule, is

Filed: 0-- EB-0-0 Exhibit B Tab Schedule Page of COST OF LONG-TERM DEBT.0 HYDRO ONE DISTRIBUTION LONG-TERM DEBT The debt portfolio for Hydro One Distribution, as set out in Exhibit B, Tab, Schedule, is

OPG READY TO DELIVER REFURBISHMENT OF DARLINGTON NUCLEAR STATION OPG also planning continued operation of Pickering Station

OPG READY TO DELIVER REFURBISHMENT OF DARLINGTON NUCLEAR STATION OPG also planning continued operation of Pickering Station Toronto - Ontario Power Generation (OPG) is ready to deliver on the Government

OPG READY TO DELIVER REFURBISHMENT OF DARLINGTON NUCLEAR STATION OPG also planning continued operation of Pickering Station Toronto - Ontario Power Generation (OPG) is ready to deliver on the Government

ONTARIO VOLLEYBALL ASSOCIATION FINANCIAL STATEMENTS AUGUST 31, 2015

FINANCIAL STATEMENTS CONTENTS Page INDEPENDENT AUDITOR'S REPORT 1-2 FINANCIAL STATEMENTS Statement of Financial Position 3 Statement of Revenues and Expenditures and Changes in Fund Balance 4 Statement

FINANCIAL STATEMENTS CONTENTS Page INDEPENDENT AUDITOR'S REPORT 1-2 FINANCIAL STATEMENTS Statement of Financial Position 3 Statement of Revenues and Expenditures and Changes in Fund Balance 4 Statement

HUMAN RESOURCES PROCEDURE 10.5

HUMAN RESOURCES PROCEDURE 10.5 Subject: Master Facilities Planning and Construction Committee Date: August 10, 2011 Pages: 14 Replaces Procedure Dated: N/A Purpose The purpose of the Master Facility Planning

HUMAN RESOURCES PROCEDURE 10.5 Subject: Master Facilities Planning and Construction Committee Date: August 10, 2011 Pages: 14 Replaces Procedure Dated: N/A Purpose The purpose of the Master Facility Planning

Ohio Tax. Workshop KK. Canadian Commodity Tax Update for U.S.-Based Companies. Wednesday, January 29, 2014 2:00 p.m. to 3:00 p.m.

Ohio Tax Workshop KK Canadian Commodity Tax Update for U.S.-Based Companies Wednesday, January 29, 2014 2:00 p.m. to 3:00 p.m. Biographical Information Darryl Rankin, Director, Commodity Tax, DuCharme,

Ohio Tax Workshop KK Canadian Commodity Tax Update for U.S.-Based Companies Wednesday, January 29, 2014 2:00 p.m. to 3:00 p.m. Biographical Information Darryl Rankin, Director, Commodity Tax, DuCharme,

DRAFT FOR DISCUSSION ONLY

FINANCIAL STATEMENTS March 31, 2015 March 31, 2015 CONTENTS Page INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS Statement of Financial Position 2 Statement of Financial Activities and Changes in Net

FINANCIAL STATEMENTS March 31, 2015 March 31, 2015 CONTENTS Page INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS Statement of Financial Position 2 Statement of Financial Activities and Changes in Net

Appendix C: Examples of Common Accounting and Bookkeeping Procedures

Appendix C: Examples of Common Accounting and Bookkeeping Procedures In this Appendix the use of the term monthly means on a regular cycle, based on the needs of your district. Some of the sample accounting

Appendix C: Examples of Common Accounting and Bookkeeping Procedures In this Appendix the use of the term monthly means on a regular cycle, based on the needs of your district. Some of the sample accounting

Auditing and Property Records

Auditing and Property Records Must be in compliance with state guidelines. Main account numbers always end in.00 and can only be added by Auditing. Can never change the name of the main account or pre

Auditing and Property Records Must be in compliance with state guidelines. Main account numbers always end in.00 and can only be added by Auditing. Can never change the name of the main account or pre

Doing Business in Canada GST/HST Information for Non-Residents

Doing Business in Canada GST/HST Information for Non-Residents RC4027(E) Rev. 13 Is this guide for you? T his guide explains how the Canadian goods and services tax/harmonized sales tax (GST/HST) applies

Doing Business in Canada GST/HST Information for Non-Residents RC4027(E) Rev. 13 Is this guide for you? T his guide explains how the Canadian goods and services tax/harmonized sales tax (GST/HST) applies

Advance Payments to Suppliers (Prepayments)

") Advance Payments to Suppliers (Prepayments) Purpose Generally, goods and services provided to the Institute are paid for after receipt. On occasion, it may be necessary or desirable to provide a known

Advance Payments to Suppliers (Prepayments) Purpose Generally, goods and services provided to the Institute are paid for after receipt. On occasion, it may be necessary or desirable to provide a known

CHAPTER 26. SUBSTANTIVE RULES APPLICABLE TO TELECOMMUNICATIONS SERVICE PROVIDERS.

26.201. Cost of Service. (a) (b) (c) Application. Unless the context clearly indicates otherwise, in this section the term "utility," insofar as it relates to telecommunications utilities, shall refer

26.201. Cost of Service. (a) (b) (c) Application. Unless the context clearly indicates otherwise, in this section the term "utility," insofar as it relates to telecommunications utilities, shall refer

Accessible Community Counselling and Employment Services (A.C.C.E.S.) Report and Financial Statements. March 31, 2014

Report and Financial Statements. March 31, 2014") Accessible Community Counselling and Employment Services Report and Financial Statements March 31, 2014 Statement of Financial Position As at March 31 2014 2013 Assets Current Cash and cash equivalents

Accessible Community Counselling and Employment Services Report and Financial Statements March 31, 2014 Statement of Financial Position As at March 31 2014 2013 Assets Current Cash and cash equivalents

Regular and Special Bingo Licence Terms and Conditions

Alcohol and Gaming Commission of Ontario Gaming Registration & Lotteries 90 SHEPPARD AVENUE EAST SUITE 200 TORONTO ON M2N 0A4 Tel.: 416 326-8700 Fax: 416 326-5555 1 800 522-2876 toll free in Ontario Website:

Alcohol and Gaming Commission of Ontario Gaming Registration & Lotteries 90 SHEPPARD AVENUE EAST SUITE 200 TORONTO ON M2N 0A4 Tel.: 416 326-8700 Fax: 416 326-5555 1 800 522-2876 toll free in Ontario Website:

Guide. Ontario First Nations Point-of-Sale Exemptions. About this Guide. September 2010

80 Guide September 2010 About this Guide Ontario First Nations Point-of-Sale Exemptions The contents of this Guide do not affect, or interfere with, the application of the exemption under section 87 of

80 Guide September 2010 About this Guide Ontario First Nations Point-of-Sale Exemptions The contents of this Guide do not affect, or interfere with, the application of the exemption under section 87 of

4.09. Ontario Power Generation Acquisition of Goods and Services. Chapter 4 Section. Background. Follow-up on VFM Section 3.09, 2006 Annual Report

Chapter 4 Section 4.09 Ontario Power Generation Acquisition of Goods and Services Follow-up on VFM Section 3.09, 2006 Annual Report Background As part of the reorganization of Ontario Hydro, Ontario Power

Chapter 4 Section 4.09 Ontario Power Generation Acquisition of Goods and Services Follow-up on VFM Section 3.09, 2006 Annual Report Background As part of the reorganization of Ontario Hydro, Ontario Power

2015/16 EDUCATION PAYROLL LIMITED STATEMENT OF PERFORMANCE EXPECTATIONS

2015/16 EDUCATION PAYROLL LIMITED STATEMENT OF PERFORMANCE EXPECTATIONS Published in August 2015 Education Payroll Limited 2015/16 EDUCATION PAYROLL LIMITED STATEMENT OF PERFORMANCE EXPECTATIONS CONTENTS

2015/16 EDUCATION PAYROLL LIMITED STATEMENT OF PERFORMANCE EXPECTATIONS Published in August 2015 Education Payroll Limited 2015/16 EDUCATION PAYROLL LIMITED STATEMENT OF PERFORMANCE EXPECTATIONS CONTENTS

UNDERTAKINGS. Undertaking. Response. Filed: 2010-08-27 EB-2010-0008 JT1.11 Page 1 of 1. To provide copies of Ministry of Energy backgrounder document.

JT1.11 Page 1 of 1 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 UNDERTAKINGS Undertaking To provide copies of Ministry of Energy backgrounder document. Response Attached is the February 2005 Ministry of Energy

JT1.11 Page 1 of 1 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 UNDERTAKINGS Undertaking To provide copies of Ministry of Energy backgrounder document. Response Attached is the February 2005 Ministry of Energy

Ontario Energy Board

Ontario Energy Board Commission de l énergie de l Ontario Ontario Energy Board Filing Requirements For Electricity Distribution Rate Applications - 2014 Edition for 2015 Rates Applications - Chapter 2

Ontario Energy Board Commission de l énergie de l Ontario Ontario Energy Board Filing Requirements For Electricity Distribution Rate Applications - 2014 Edition for 2015 Rates Applications - Chapter 2

Business Plan template

template If you re considering establishing or purchasing a small business, it s important that you have a Business Plan. This plan will help provide you with an essential road map for your new business.

template If you re considering establishing or purchasing a small business, it s important that you have a Business Plan. This plan will help provide you with an essential road map for your new business.

Toronto Hydro-Electric System Limited EB-2011-0144 Exhibit C1 Tab 1 Schedule 1 ORIGINAL Page 1 of 1 POLICY INTRODUCTION

Toronto Hydro-Electric System Limited EB-2011-0144 Exhibit C1 Tab 1 Schedule 1 ORIGINAL Page 1 of 1 1 POLICY 2 3 INTRODUCTION 4 5 6 7 8 9 10 11 12 13 In prior applications, THESL presented evidence in

Toronto Hydro-Electric System Limited EB-2011-0144 Exhibit C1 Tab 1 Schedule 1 ORIGINAL Page 1 of 1 1 POLICY 2 3 INTRODUCTION 4 5 6 7 8 9 10 11 12 13 In prior applications, THESL presented evidence in

Applebaum Commisso Tax Tips

Tax Tips Corporate: Tax information everyone should know: Small business deduction: The effective tax rate for a corporation that is defined as a Canadian Controlled Private Corporation is 15.5% on the

Tax Tips Corporate: Tax information everyone should know: Small business deduction: The effective tax rate for a corporation that is defined as a Canadian Controlled Private Corporation is 15.5% on the

BUSINESS PLANNING ASSUMPTIONS

EB-00-0 Exhibit C Tab Schedule Page of BUSINESS PLANNING ASSUMPTIONS INTRODUCTION Following is a summary of key assumptions related to THESL s financial projections included in the Application. 0 ECONOMIC

EB-00-0 Exhibit C Tab Schedule Page of BUSINESS PLANNING ASSUMPTIONS INTRODUCTION Following is a summary of key assumptions related to THESL s financial projections included in the Application. 0 ECONOMIC

Cash Working Capital Allowance. Analysis of Semi-Annual Long-Term Bond Interest Payments. Newfoundland and Labrador Hydro

Cash Working Capital Allowance Analysis of Semi-Annual Long-Term Bond Interest Payments Newfoundland and Labrador Hydro April 2003 Table of Contents Page # 1. INTRODUCTION... 1 2. REGULATORY CONSIDERATIONS...

Cash Working Capital Allowance Analysis of Semi-Annual Long-Term Bond Interest Payments Newfoundland and Labrador Hydro April 2003 Table of Contents Page # 1. INTRODUCTION... 1 2. REGULATORY CONSIDERATIONS...

4 b) Where to Record Revenue. 4 5 c) When to Record Revenue. 6-11 Recognition of Unrestricted Revenue Recognition of Restricted Revenue Sources

Where to Record Revenue. 4 5 c) When to Record Revenue. 6-11 Recognition of Unrestricted Revenue Recognition of Restricted Revenue Sources") Revenue Recognition Policy Guidelines These guidelines are organized within the following sections: Pages I. Purpose 1 II. Responsibilities 1 III. Definitions 2-3 IV. Major Sources of Revenue and Normal

Revenue Recognition Policy Guidelines These guidelines are organized within the following sections: Pages I. Purpose 1 II. Responsibilities 1 III. Definitions 2-3 IV. Major Sources of Revenue and Normal

MOUNTAIN EQUIPMENT CO-OPERATIVE

Consolidated Financial Statements of MOUNTAIN EQUIPMENT CO-OPERATIVE KPMG LLP PO Box 10426 777 Dunsmuir Street Vancouver BC V7Y 1K3 Canada Telephone (604) 691-3000 Fax (604) 691-3031 Internet www.kpmg.ca

Consolidated Financial Statements of MOUNTAIN EQUIPMENT CO-OPERATIVE KPMG LLP PO Box 10426 777 Dunsmuir Street Vancouver BC V7Y 1K3 Canada Telephone (604) 691-3000 Fax (604) 691-3031 Internet www.kpmg.ca

HOUSE BILL NO. HB0207. Representative(s) Cohee, Edwards, Gentile and McOmie and Senator(s) Barrasso and Peck A BILL. for

Cohee, Edwards, Gentile and McOmie and Senator(s) Barrasso and Peck A BILL. for") 00 STATE OF WYOMING 0LSO-0 HOUSE BILL NO. HB00 Emergency telephone service. Sponsored by: Representative(s) Cohee, Edwards, Gentile and McOmie and Senator(s) Barrasso and Peck A BILL for AN ACT relating

00 STATE OF WYOMING 0LSO-0 HOUSE BILL NO. HB00 Emergency telephone service. Sponsored by: Representative(s) Cohee, Edwards, Gentile and McOmie and Senator(s) Barrasso and Peck A BILL for AN ACT relating

This policy applies to all communities and describes the following financial issues:

General Financial Administration Issues Policy F6 Effective Date April 2002 Revision Date March 2016 Page Number 1 of 5 Approval Robert Wavey This policy applies to all communities and describes the following

General Financial Administration Issues Policy F6 Effective Date April 2002 Revision Date March 2016 Page Number 1 of 5 Approval Robert Wavey This policy applies to all communities and describes the following

BUDGET AND FINANCIAL PLAN SUMMARY FILE

REVENUE & FINANCING SOURCES Operating Revenues Charges for services Rental & financing income Last Year (Actual) 2014 Other operating revenues 0 Nonoperating Revenues Current Year (Estimated) 2015 Next

REVENUE & FINANCING SOURCES Operating Revenues Charges for services Rental & financing income Last Year (Actual) 2014 Other operating revenues 0 Nonoperating Revenues Current Year (Estimated) 2015 Next

GST/HST Technical Information Bulletin

GST/HST Technical Information Bulletin B-105 February 2011 Changes to the Definition of Financial Service NOTE: This GST/HST Technical Information Bulletin replaces the publications listed under Cancelled

GST/HST Technical Information Bulletin B-105 February 2011 Changes to the Definition of Financial Service NOTE: This GST/HST Technical Information Bulletin replaces the publications listed under Cancelled

BP 3600 RULES FOR AUXILIARY ORGANIZATIONS

BP 3600 RULES FOR AUXILIARY ORGANIZATIONS References: Education Code Sections 72670 et seq.; 76060, 76063, 76064, 72241, 72303 Title 5 Sections 59250 et seq. The Napa Valley Community College District

BP 3600 RULES FOR AUXILIARY ORGANIZATIONS References: Education Code Sections 72670 et seq.; 76060, 76063, 76064, 72241, 72303 Title 5 Sections 59250 et seq. The Napa Valley Community College District

TOPIC ACCOUNTING PRINCIPLES SUB-SECTION 03.00.00 SUB-SECTION INDEX REVISION NUMBER 99-004

Page 1 of 1 TOPIC ACCOUNTING PRINCIPLES SUB-SECTION 03.00.00 SECTION ISSUANCE DATE JUNE 30, 1999 SUB-SECTION INDEX REVISION NUMBER 99-004 03 Accounting Principles 10 Organization Structure of State Government

Page 1 of 1 TOPIC ACCOUNTING PRINCIPLES SUB-SECTION 03.00.00 SECTION ISSUANCE DATE JUNE 30, 1999 SUB-SECTION INDEX REVISION NUMBER 99-004 03 Accounting Principles 10 Organization Structure of State Government

THE COLLEGE OF DENTURISTS OF BRITISH COLUMBIA Financial Statements Year Ended March 31, 2015

Financial Statements Index to Financial Statements Page INDEPENDENT AUDITOR S REPORT 1 FINANCIAL STATEMENTS Statement of Financial Position 2 Statement of Revenues and Expenditures 3 Statement of Changes

Financial Statements Index to Financial Statements Page INDEPENDENT AUDITOR S REPORT 1 FINANCIAL STATEMENTS Statement of Financial Position 2 Statement of Revenues and Expenditures 3 Statement of Changes

Ontario First Nations Point-of-Sale Exemptions

Ontario First Nations Point-of-Sale Exemptions Harmonized Sales Tax Guide 80 Published: September 2010 Content last reviewed: October 2010 ISBN: 978-1-4435-4529-7 (Print), 978-1-4435-4531-0 (PDF), 978-1-4435-4530-3

Ontario First Nations Point-of-Sale Exemptions Harmonized Sales Tax Guide 80 Published: September 2010 Content last reviewed: October 2010 ISBN: 978-1-4435-4529-7 (Print), 978-1-4435-4531-0 (PDF), 978-1-4435-4530-3

Financial Information Kit

Financial Information Kit The purpose of this kit is to provide basic information on keeping financial records to facilitate compliance by registered charities with the requirements of the Canada Revenue

Financial Information Kit The purpose of this kit is to provide basic information on keeping financial records to facilitate compliance by registered charities with the requirements of the Canada Revenue

How To Account For Construction Contracts In Indian Accounting Standard (Indas)

") Contents Indian Accounting Standard (Ind AS) 11 Construction Contracts Paragraphs OBJECTIVE SCOPE 1 2 DEFINITIONS 3 6 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 7 10 CONTRACT REVENUE 11 15 CONTRACT

Contents Indian Accounting Standard (Ind AS) 11 Construction Contracts Paragraphs OBJECTIVE SCOPE 1 2 DEFINITIONS 3 6 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 7 10 CONTRACT REVENUE 11 15 CONTRACT

BUDGET AND FINANCIAL PLAN SUMMARY FILE

BUDGET AND FINANCIAL PLAN SUMMARY FILE BUDGETED REVENUES, EXPENDITURES, AND CHANGES IN CURRENT NET ASSETS Last Year (Actual) 2013 Current Year (Estimated) 2014 Adopted 2015 Proposed 2016 Proposed 2017

BUDGET AND FINANCIAL PLAN SUMMARY FILE BUDGETED REVENUES, EXPENDITURES, AND CHANGES IN CURRENT NET ASSETS Last Year (Actual) 2013 Current Year (Estimated) 2014 Adopted 2015 Proposed 2016 Proposed 2017

Yes. Although incorporation is often associated with a formal business enterprise, Not-For- Profit organizations also can incorporate.

NOT-FOR-PROFIT ORGANIZATIONS A LEGAL GUIDE The purpose of this booklet is to provide information to community groups and organizations, which may be considering incorporating as Not-For-Profit, organizations.

NOT-FOR-PROFIT ORGANIZATIONS A LEGAL GUIDE The purpose of this booklet is to provide information to community groups and organizations, which may be considering incorporating as Not-For-Profit, organizations.

Handout # 2: Allocating Fundraising Expenses to the T3010

Handout # 2: Allocating Fundraising Expenses to the T3010 The following information is organized to assist a charity in allocating fundraising expenses to the appropriate reporting line on the T3010 Information

Handout # 2: Allocating Fundraising Expenses to the T3010 The following information is organized to assist a charity in allocating fundraising expenses to the appropriate reporting line on the T3010 Information

COST OF CAPITAL, COST OF EQUITY, DEBT FINANCING AND DIVIDEND POLICY

Page of 4 5 6 7 8 9 0 COST OF CAPITAL, COST OF EQUITY, DEBT FINANCING AND DIVIDEND POLICY Overview PowerStream has followed the Report of the Board on Cost of Capital for Ontario s Regulated Utilities,

Page of 4 5 6 7 8 9 0 COST OF CAPITAL, COST OF EQUITY, DEBT FINANCING AND DIVIDEND POLICY Overview PowerStream has followed the Report of the Board on Cost of Capital for Ontario s Regulated Utilities,

State Chart of Accounts and Other Accounting Identifiers

100000 CASH ON HAND DEFINITIONS Currency, coin, checks, money orders and bankers' drafts on hand. 101000-103000 CASH IN BANKS Funds on deposit with financial institutions. 104000 PETTY CASH 105000 CASH

100000 CASH ON HAND DEFINITIONS Currency, coin, checks, money orders and bankers' drafts on hand. 101000-103000 CASH IN BANKS Funds on deposit with financial institutions. 104000 PETTY CASH 105000 CASH

Outside Looking In Financial Statements

www.publicaccountants.com Outside Looking In Financial Statements . Contents Page Independent Auditors Report 1 Statement of Financial Position 2 Statement of Operations and Changes in Net Deficiency 3

www.publicaccountants.com Outside Looking In Financial Statements . Contents Page Independent Auditors Report 1 Statement of Financial Position 2 Statement of Operations and Changes in Net Deficiency 3

University of Missouri System Accounting Policies and Procedures

University of Missouri System Accounting Policies and Procedures Policy Number: APM 65.10 Policy Name: Allowance and Write-off for Uncollectible Student Loans General Policy and Procedure Overview: In

University of Missouri System Accounting Policies and Procedures Policy Number: APM 65.10 Policy Name: Allowance and Write-off for Uncollectible Student Loans General Policy and Procedure Overview: In

ELECTRICITY PRICING INFORMATION. This list shows the terms that appear on electricity bills and what they mean:

ELECTRICITY PRICING INFORMATION GLOSSARY OF BILLING TERMS: The Government of Ontario requires all electricity distributors to issue standardized bills to their low- volume consumers, such as residential

ELECTRICITY PRICING INFORMATION GLOSSARY OF BILLING TERMS: The Government of Ontario requires all electricity distributors to issue standardized bills to their low- volume consumers, such as residential

If you have questions, or need assistance with completing this form, please call 1-800-667-6102, extension 0956.

Ministry of Finance Revenue Division 2350 Albert Street Regina, Sask. S4P 4A6 Phone: 1-800-667-6102 Fax: (306) 798-3045 NON-RESIDENT CONTRACTORS REQUEST FOR CONTRACT CLEARANCE SUPPLEMENTARY WORKSHEETS

Ministry of Finance Revenue Division 2350 Albert Street Regina, Sask. S4P 4A6 Phone: 1-800-667-6102 Fax: (306) 798-3045 NON-RESIDENT CONTRACTORS REQUEST FOR CONTRACT CLEARANCE SUPPLEMENTARY WORKSHEETS

Income Tax Issues in the Purchase and Sale of Assets. Catherine A. Brayley

Income Tax Issues in the Purchase and Sale of Assets Catherine A. Brayley Income Tax Issues in the Purchase and Sale of Assets Catherine A. Brayley Bennett Jones LLP (Toronto) Table of Contents Scope of

Income Tax Issues in the Purchase and Sale of Assets Catherine A. Brayley Income Tax Issues in the Purchase and Sale of Assets Catherine A. Brayley Bennett Jones LLP (Toronto) Table of Contents Scope of

SHEET 1: CASH FLOW PROJECTED

Blended Value Business Plan Cash Flow Forecast User Guide OVERVIEW The Cash Flow Forecast is the listing of the sources and expenditures of cash plus the timing of when the cash is moving in and out of

Blended Value Business Plan Cash Flow Forecast User Guide OVERVIEW The Cash Flow Forecast is the listing of the sources and expenditures of cash plus the timing of when the cash is moving in and out of

WOMEN'S INTER-CHURCH COUNCIL OF CANADA

FINANCIAL STATEMENTS AUGUST 31, 2013 AND AUGUST 31, 2012 C H A R T E R E D A C C O U N T A N T S INDEPENDENT AUDITOR'S REPORT To the Members, Women's Inter-Church Council of Canada: Report on the Financial

FINANCIAL STATEMENTS AUGUST 31, 2013 AND AUGUST 31, 2012 C H A R T E R E D A C C O U N T A N T S INDEPENDENT AUDITOR'S REPORT To the Members, Women's Inter-Church Council of Canada: Report on the Financial

SALES AND USE TAX TECHNICAL BULLETINS SECTION 18

SECTION 18 - CERTAIN GOVERNMENTAL ENTITIES - THE STATE, COUNTIES, CITIES AND OTHER POLITICAL SUBDIVISIONS 18-1 PURCHASES AND SALES BY AND DONATIONS TO GOVERNMENTAL ENTITIES A. Purchases By Governmental

SECTION 18 - CERTAIN GOVERNMENTAL ENTITIES - THE STATE, COUNTIES, CITIES AND OTHER POLITICAL SUBDIVISIONS 18-1 PURCHASES AND SALES BY AND DONATIONS TO GOVERNMENTAL ENTITIES A. Purchases By Governmental

Lougheed House Conservation Society. (a not-for-profit organization) Financial Statements December 31, 2013

Financial Statements December 31, 2013") Financial Statements Collins Barrow Calgary LLP 1400 First Alberta Place 777 8 th Avenue S.W. Calgary, Alberta, Canada T2P 3R5 Independent Auditors' Report T. 403.298.1500 F. 403.298.5814 e-mail: calgary@collinsbarrow.com

Financial Statements Collins Barrow Calgary LLP 1400 First Alberta Place 777 8 th Avenue S.W. Calgary, Alberta, Canada T2P 3R5 Independent Auditors' Report T. 403.298.1500 F. 403.298.5814 e-mail: calgary@collinsbarrow.com

HOUSE BILL NO. HB0207. Representative(s) Cohee, Edwards, Gentile and McOmie and Senator(s) Barrasso and Peck A BILL. for

Cohee, Edwards, Gentile and McOmie and Senator(s) Barrasso and Peck A BILL. for") 00 STATE OF WYOMING 0LSO-0.E ENGROSSED HOUSE BILL NO. HB00 Emergency telephone service. Sponsored by: Representative(s) Cohee, Edwards, Gentile and McOmie and Senator(s) Barrasso and Peck A BILL for AN

00 STATE OF WYOMING 0LSO-0.E ENGROSSED HOUSE BILL NO. HB00 Emergency telephone service. Sponsored by: Representative(s) Cohee, Edwards, Gentile and McOmie and Senator(s) Barrasso and Peck A BILL for AN

2. Units are required to contribute Levies at the rates approved by the NPP Board Meeting of 22 January 2004 as follows:

CANADIAN FORCES CENTRAL FUND CONTRIBUTIONS - LOANS AND GRANTS INTRODUCTION 1. This chapter deals with contributions and with the accounting procedures to be followed when CFCF loans and grants have been

CANADIAN FORCES CENTRAL FUND CONTRIBUTIONS - LOANS AND GRANTS INTRODUCTION 1. This chapter deals with contributions and with the accounting procedures to be followed when CFCF loans and grants have been

Create a credit card and/or cash reimbursement expense report

Create a credit card and/or cash reimbursement expense report iexpenses is used by employees or their delegates to process expense reports for University credit card transactions, cash reimbursements and

Create a credit card and/or cash reimbursement expense report iexpenses is used by employees or their delegates to process expense reports for University credit card transactions, cash reimbursements and

SEP 2014 OCT 2014 DEC 2014 NOV 2014 HOEP* 3.23 1.70 2.73 2.25 2.06 1.41 0.62 1.52 2.02 2.86 4.97 2.42 1.57 1.42 1.42 2.41

Ontario Energy Report Q2 Electricity April June Electricity Prices Commodity Cost ( /kwh) Commodity cost comprises two components, the wholesale price (the Hourly Ontario Energy Price or HOEP) and the

Ontario Energy Report Q2 Electricity April June Electricity Prices Commodity Cost ( /kwh) Commodity cost comprises two components, the wholesale price (the Hourly Ontario Energy Price or HOEP) and the

Business plan outline

Note: Some of the following information may not be relevant for your business type. However, this should provide you with a clear guide so that you cover everything you need to write a comprehensive business

Note: Some of the following information may not be relevant for your business type. However, this should provide you with a clear guide so that you cover everything you need to write a comprehensive business

This article, prepared by PARO s auditors Rosenswig McRae Thorpe LLP, outlines some points to consider in preparing your income tax returns.

2014 Edition for 2013 Returns This article, prepared by PARO s auditors Rosenswig McRae Thorpe LLP, outlines some points to consider in preparing your income tax returns. Remember that: RRSP Contribution

2014 Edition for 2013 Returns This article, prepared by PARO s auditors Rosenswig McRae Thorpe LLP, outlines some points to consider in preparing your income tax returns. Remember that: RRSP Contribution

A/R INVOICING EXTERNAL CUSTOMERS

Accounts Receivable (A/R) is money owed to an entity by customers (individuals or corporations) for goods and/or services that have been delivered or used, but not yet paid for. The intention of this guidance

Accounts Receivable (A/R) is money owed to an entity by customers (individuals or corporations) for goods and/or services that have been delivered or used, but not yet paid for. The intention of this guidance

INTRODUCTION AND SUMMARY OF O&M COSTS

EB-00-0 Exhibit F Tab Schedule Page of CUSTOMER SERVICES INTRODUCTION AND SUMMARY OF O&M COSTS The Customer Services division performs activities that are required to provide services to customers connected

EB-00-0 Exhibit F Tab Schedule Page of CUSTOMER SERVICES INTRODUCTION AND SUMMARY OF O&M COSTS The Customer Services division performs activities that are required to provide services to customers connected

Legend Power Systems Inc. MANAGEMENT S DISCUSSION AND ANALYSIS For the six months ended March 31, 2011

This management discussion and analysis ( MD&A ) focuses on key statistics from the consolidated financial statements and pertains to known risks and uncertainties relating to Legend Power Systems Inc.

This management discussion and analysis ( MD&A ) focuses on key statistics from the consolidated financial statements and pertains to known risks and uncertainties relating to Legend Power Systems Inc.

Texas A&M University Commerce Prompt Payment and Payment Scheduling Procedures

Texas A&M University Commerce Prompt Payment and Payment Scheduling Procedures I. Purpose This document applies to all payments processed through Texas A&M University - Commerce (TAMC) Accounts Payable.

Texas A&M University Commerce Prompt Payment and Payment Scheduling Procedures I. Purpose This document applies to all payments processed through Texas A&M University - Commerce (TAMC) Accounts Payable.

REGULAR AND SPECIAL BINGO LICENCE TERMS AND CONDITIONS DEFINITIONS

Alcohol and Gaming Commission of Ontario Gaming Registration & Lotteries Commission des alcools et des jeux de l=ontario Inscription pour les jeux et loteries 20 Dundas Street West 20, rue Dundas ouest

Alcohol and Gaming Commission of Ontario Gaming Registration & Lotteries Commission des alcools et des jeux de l=ontario Inscription pour les jeux et loteries 20 Dundas Street West 20, rue Dundas ouest

Guelph Chamber of Commerce Financial Statements For the Year Ended June 30, 2015

Financial Statements For the Year Ended June 30, 2015 Financial Statements For the Year Ended June 30, 2015 Contents Independent Auditor's Report 1 Financial Statements Statement of Financial Position

Financial Statements For the Year Ended June 30, 2015 Financial Statements For the Year Ended June 30, 2015 Contents Independent Auditor's Report 1 Financial Statements Statement of Financial Position

Land Title and Survey Authority of British Columbia

Land Title and Survey Authority of British Columbia Management s Discussion and Analysis For the three months ended June 30, 2012 The following is a discussion and analysis of the financial condition and

Land Title and Survey Authority of British Columbia Management s Discussion and Analysis For the three months ended June 30, 2012 The following is a discussion and analysis of the financial condition and

Regulations of the University of North Texas System Chapter 08. Fiscal Management. 08.9000 Asset Capitalization

Regulations of the University of North Texas System Chapter 08 08.9000 Asset Capitalization Fiscal Management 08.9001 Regulation Statement. The University of North Texas System shall identify, measure,

Regulations of the University of North Texas System Chapter 08 08.9000 Asset Capitalization Fiscal Management 08.9001 Regulation Statement. The University of North Texas System shall identify, measure,

TAX NEWSLETTER. February 2012

TAX NEWSLETTER February 2012 RECORDING YOUR BUSINESS AUTOMOBILE EXPENSES PRESCRIBED AUTOMOBILE AMOUNTS FOR 2012 EMPLOYEE LOANS CRA SIMPLIFIED RATES FOR MOVING EXPENSES INCURRED IN 2011 CRA PUTS END TO

TAX NEWSLETTER February 2012 RECORDING YOUR BUSINESS AUTOMOBILE EXPENSES PRESCRIBED AUTOMOBILE AMOUNTS FOR 2012 EMPLOYEE LOANS CRA SIMPLIFIED RATES FOR MOVING EXPENSES INCURRED IN 2011 CRA PUTS END TO

CCA Tax Guide to Employer-Provided Vehicles & Allowances

June 2003 CCA Tax Guide to Employer-Provided Vehicles & Allowances IMPORTANT: This document is intended as a summary guide on the current rules and regulations respecting the tax treatment of employer-provided

June 2003 CCA Tax Guide to Employer-Provided Vehicles & Allowances IMPORTANT: This document is intended as a summary guide on the current rules and regulations respecting the tax treatment of employer-provided

Telegraphic transfers and bank drafts

Telegraphic transfers and bank drafts Businesses and individuals frequently need to transfer funds abroad in payment of goods or services provided by an overseas supplier. These transfers are a convenient

Telegraphic transfers and bank drafts Businesses and individuals frequently need to transfer funds abroad in payment of goods or services provided by an overseas supplier. These transfers are a convenient

Car expenses. A tax guide. pwc.com/ca/carexpenses

pwc.com/ca/carexpenses Car expenses and benefits A tax guide Our road map guides drivers and business managers through the maze of Canadian tax rules for car expenses and benefits. 2012 Cette brochure est

pwc.com/ca/carexpenses Car expenses and benefits A tax guide Our road map guides drivers and business managers through the maze of Canadian tax rules for car expenses and benefits. 2012 Cette brochure est

Employment income and investment income are not subject to HST and would not be considered in this calculation.

People Count. HST and Income Tax Considerations for Participants in Ontario s microfit Solar Energy Program The Ontario Power Authority has developed a Feed-In Tariff (the "FIT") Program for the province

People Count. HST and Income Tax Considerations for Participants in Ontario s microfit Solar Energy Program The Ontario Power Authority has developed a Feed-In Tariff (the "FIT") Program for the province

No. 90 Fall 2013. Table of Contents

Excise GST/HST News No. 90 Fall 2013 Table of Contents Bill C-4... 1 Line 101 of the GST/HST return (GST34-2)... 3 Third-party fundraising... 4 Red tape reduction and CRA s online mail service... 6 Electronic

Excise GST/HST News No. 90 Fall 2013 Table of Contents Bill C-4... 1 Line 101 of the GST/HST return (GST34-2)... 3 Third-party fundraising... 4 Red tape reduction and CRA s online mail service... 6 Electronic

Blended Value Feasibility Study Cash Flow Forecast User Guide

Blended Value Feasibility Study Cash Flow Forecast User Guide OVERVIEW The Cash Flow Forecast is the listing of the sources and expenditures of cash plus the timing of when the cash is moving in and out

Blended Value Feasibility Study Cash Flow Forecast User Guide OVERVIEW The Cash Flow Forecast is the listing of the sources and expenditures of cash plus the timing of when the cash is moving in and out