Platts Steel Raw Materials Asia Moving East: Establishing U.S. Origin Coking Coal in China May 30, 2013 Singapore

|

|

|

- Marybeth Powell

- 8 years ago

- Views:

Transcription

1 Platts Steel Raw Materials Asia 2013 Moving East: Establishing U.S. Origin Coking Coal in China May 30, 2013 Singapore 1

2 Why are customers in China important to U.S. Coking Coal producers?» China is the primary growth area for worldwide steel production» Traditional markets in the mature economies of Europe are struggling» Coking coal exports to Brazil, and other South American countries, are stable but have not experienced the growth that has been forecasted for this region» Growth in the North American steel market is limited Low cost supplies of natural gas are displacing PCI coal at U.S. steel mills Future production facilities in North America may shift to gas-based DRI production and reduce the demand for coking coal 2

3 World Blast Furnace Iron Production

4 World Steel Production

5 World Steel & Blast Furnace Iron Production CAGR Blast Furnace Iron Production Steel Production Asia 8.83% 8.64% ROW (-1.42%) 0.13% Total 5.18% 4.78% 5

0.13% Total 5.")

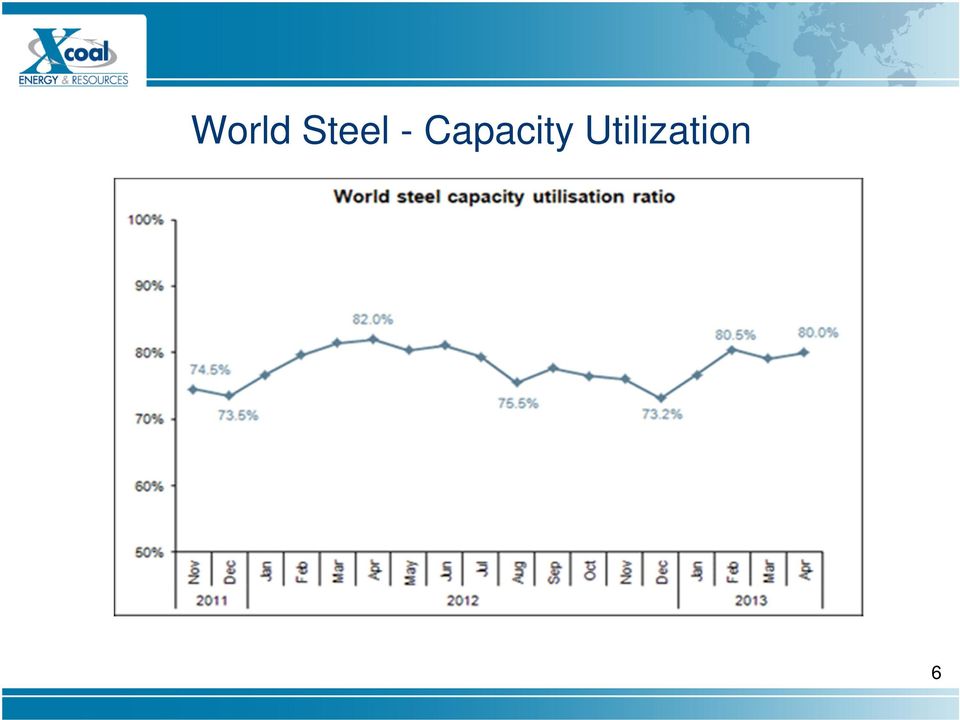

6 World Steel - Capacity Utilization 6

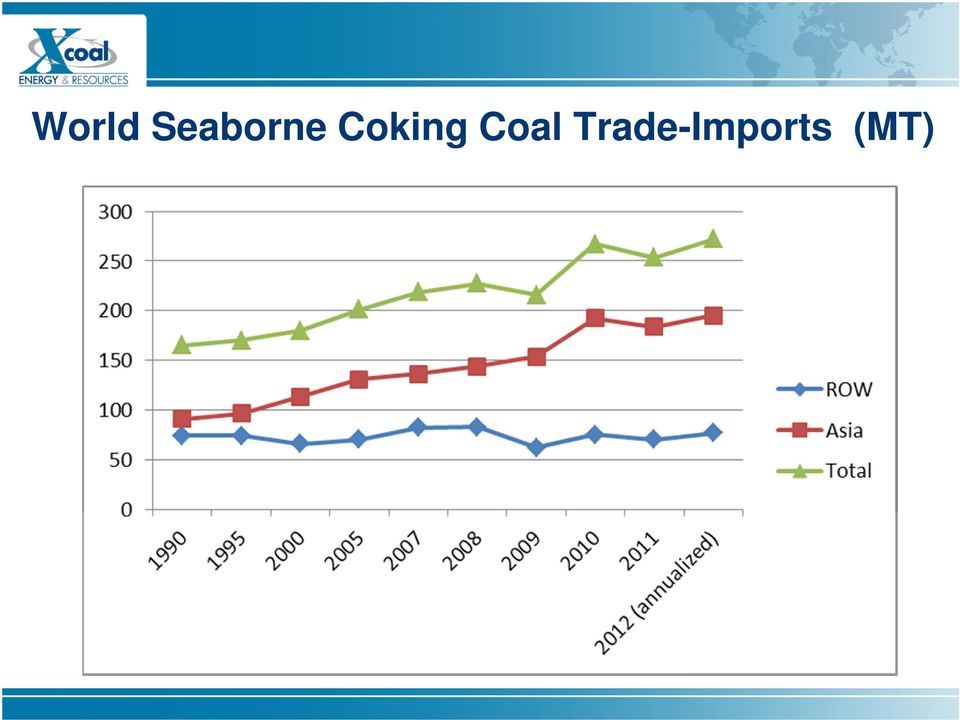

7 World Seaborne Coking Coal Trade-Imports (MT)

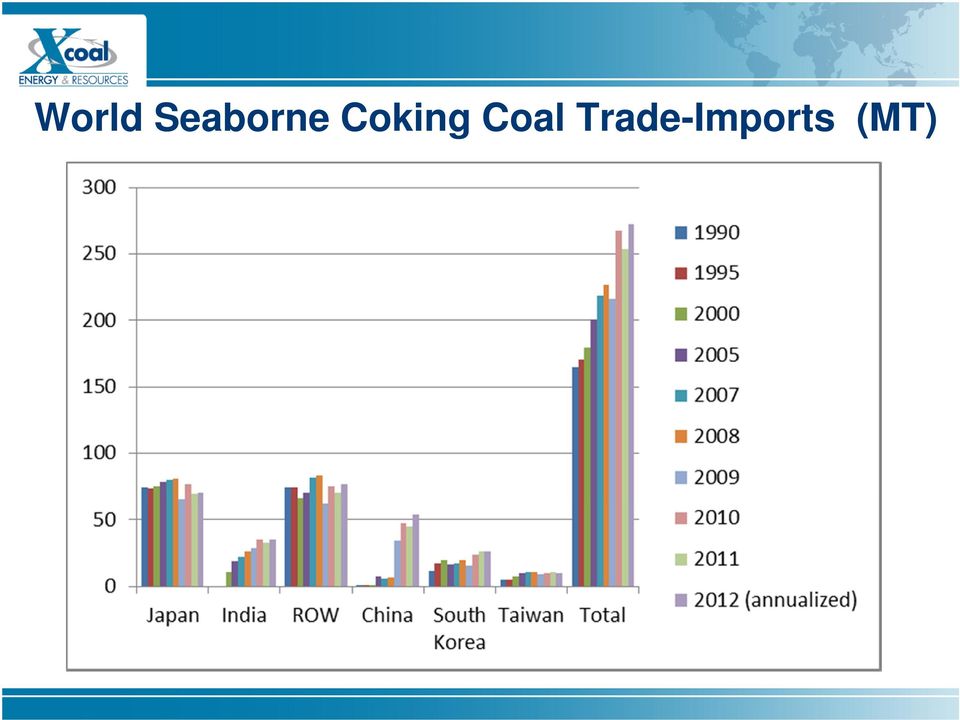

8 World Seaborne Coking Coal Trade-Imports (MT)

9 World Seaborne Coking Coal Imports CAGR Coking Coal Asia 6.05% ROW 0.31% Total 3.92% 9

10 World Seaborne Coking Coal Trade (MT)

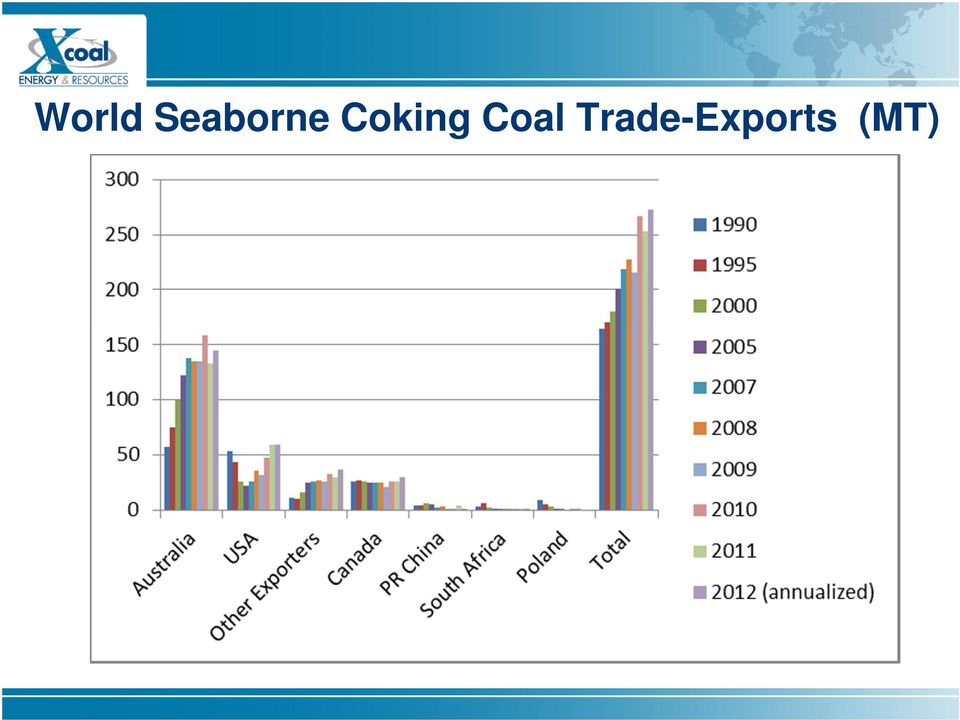

11 World Seaborne Coking Coal Trade-Exports (MT)

12 U.S. Coking Coal Exports 12

13 2012/2011 U.S. Coking Coal Exports 13

14 Primary US Coking Coal Destinations US Coking Coal Exports (MT) 2011 vs vs % % North America 4,200,638 3,833,549 4,610,580 5,050,355 10% 20% South America 3,330,914 7,445,538 8,242,443 7,947,604-4% 139% European Union 9,075,264 19,803,508 20,982,639 20,965, % 131% Other Europe 705,297 4,843,660 7,891,895 4,954,855-37% 603% Asia & Other 7,037,228 15,022,844 21,350,892 24,472, % 248% Domestic US Demand 22,000,000 19,000,000 21,400,000 21,800,000 2% -1%

15 USA-Coking Coal Exports to Asia & Other

16 USA-Coking Coal Exports to Asia (by country)

YTD '12 Qty (million tonne) Note: Total imports=thermal")

17 China Total Coal Imports in Mar YTD '13 Qty (million tonne) YTD '12 Qty (million tonne) Note: Total imports=thermal coal+coking coal+anthracite+other coal+coal-based solid fuel Primary Source: China Coal Resource (CCR) 17

Thermal Coal YTD '12 Qty (million tonne) Coking Coal YTD '13 Qty")

18 China Thermal Coal/ Coking Coal Imports in Mar Thermal Coal YTD '13 Qty (million tonne) Thermal Coal YTD '12 Qty (million tonne) Coking Coal YTD '13 Qty (million tonne) Coking Coal YTD '12 Qty (million tonne) Primary Source: China Coal Resource (CCR) 18

Coking Coal YTD '12 Qty (million tonne) Primary Source:")

19 North American Coal Market» Due to the decreased demand for all types of coal within the USA, exports reached a historic high in 2012» In this market environment, most coal producers in the USA need to export coal to balance their sales portfolio and to realize sufficient revenue to sustain operations» During 2012, significant quantities of coal were exported at aggressive prices to monetize inventories and sustain cash flow while companies restructured their operations» Those surplus inventories have been depleted. Ongoing sales are being priced at prevailing market levels» Coal producing companies continue to struggle to achieve profitability 19

20 U.S. Coking Coal Update» In 2011 despite financial and regulatory restrictions, the U.S. mining industry was able to expand coking coal production 2011 U.S. mining industry focused on coking coal investments / expansion / acquisitions. Many companies placed large bets on coking coal (acquisitions) 2012 companies adjusted production to match demand Nevertheless two themes remain unchanged going into 2013: Capital directed toward coking coal vs. thermal coal Industry banking on export growth» Regulatory restrictions continue to impact productivity and cost structure 20

21 U.S. Coal Producer s Evaluation Thermal vs. Coking / Domestic vs. Export» For the first time since 2009, prices realized on export sales of thermal coal are at, or near, parity to prices achievable in the U.S. domestic market» Some U.S. coal producers now have the option to shift thermal coal tonnage to the U.S. domestic market» The evaluation for some CAPP producers, and most NAPP producers, is not based on the API2 price, but on the clearing prices in the domestic thermal market 21

22 USA-Natural Gas Pricing Natural gas prices increased by 65% since May 10, 2012

23 U.S. Coal Producer s Evaluation Thermal vs. Coking / Domestic vs. Export Our Northern App coal right now is going to 13 different countries. We have 53 different customers. Bailey coal goes into the high-vol coking coal market, it goes into the PCI market, and it goes to the thermal coal market. All these different markets including the Southeast. We're building a portfolio that gives us the flexibility to send the coal to the Southeast, if that's given us the best net back, or to keep it in the PJM markets if that s the best net back, or to look overseas in other markets. Depending on the market, the net back, and the timing, that's where we'll send the coal to. Jim Grech Consol Energy Earnings Call April 25,

24 Significant Themes - Global Coking Coal Market» 2011 and 2012 Strong start, followed by a global economic slowdown, during the second half of each year.» Encouraging developments in early 2013 petered out. Will 2013 follow the same pattern as 2011 and 2012? Chinese Domestic Coking Coal prices in May 2013 lower than trough pricing in Oct 2012 Weakness in market conditions could persist through Q3. Recent weakness in the Australian Dollar could exacerbate the situation as it might allow Australian suppliers to put off difficult supply cut decisions.» Concerns related to the global financial situation created an environment where many buyers did not want to make long-term commitments in Sentiment turned positive in 2013 but now concerns about China now coming to forefront.» The result may be more quarterly and less spot buying, similar to buying patterns before the 2008/2009 and 2011/2012 downturns 24

25 Significant Themes / Events (cont.)» In 2010 and 2011, higher levels of U.S. seaborne coking coal tonnage were needed to balance the market.» 2012 exports were stable but strong by historical standards US export levels returned to levels not achieved since the 1990 s» A structural shift in seaborne coking coal trade U.S. origin coal remains as a long term, sustainable supply source Customers worldwide implemented diversification strategy» Expect U.S. origin coking coal exports to remain relatively strong over the coming year 25

26 Seaborne Coking Coal to Customers in China» Quality does matter. Although imports of seaborne coking coal are price sensitive, Chinese customers require unblended coking coals that satisfy their quality requirements New suppliers may have the perception that you can ship anything to China. This perception is not true» Suppliers need to establish coal brands that provide customers a reliable, consistent, and sustainable supply of coking coal. The customer needs to know that Buchanan coking coal, Windber coking coal, Toms Run coking coal, Bailey coking coal, etc., will be consistent on a shipment by shipment basis» Suppliers need to provide technical support to ensure the customers utilize the seaborne coking coal to their maximum benefit. Since Chinese customers were not familiar with U.S. origin coking coal when imports of U.S. coal started in 2009, it has taken a few years to educate customers on the benefits of U.S. origin coal 26

27 U.S. Origin Coking Coal to Customers in China The Challenges» The coking coal deposits in the U.S.A. are located in the Appalachian Mountain region of the eastern United States. Exports are primarily from U.S. East Coast and U.S. Gulf Coast ports, i.e. a long way from the customers in China» U.S. coking coal producers also supply domestic customers in the U.S.A., customers in Europe, and customers in South America. These customers are located closer to the export terminals for U.S. origin coking coal» Coking coal production in the U.S.A. represents approximately 9% of total U.S. coal production. Most coking coal producers also produce other grades of coal 27

28 U.S. Origin Coking Coal to Customers in China The Benefits» U.S. origin coking coal exhibits strong coking characteristics with high Y and G index values U.S. origin coking coal, when properly used in a coking coal blend, offsets lower grades of coking coal from other sources» Low Volatile (Shou Jiao Mei and Zhu Jiao Mei), Mid Volatile (Fei Mei), and Hi Volatile (1/3 Jiao Mei and Qi Fei Mei), are available from the U.S.A.» U.S. coking coal producers can supply unblended coking coal of consistent quality Shipments of blended coking coal from trading companies is not representative of U.S. coking coal supplied by producers 28

29 Xcoal / Rosebud Mining - Coal Brands Product Volatile Matter CSN Y Value G Value Windber (Shou Jiao Mei) 17.50%-19.50% Twin Rocks (Fei Mei) 24%-26% Toms Run (Fei Mei) 27%-29% Dutch Run (Fei Mei) 31%-33% Little Toby (Qi Fei Mei) 34.50%-35.50%

30 Xcoal / Consol Energy - Coal Brands Product Volatile Matter CSN Y Value G Value Buchanan (Shou Jiao Mei) 18.50%-19.75% Bailey (Qi Fei Mei) 37.50%-38.75%

31 Overcoming the Geographical Challenge Xcoal s top off operation has been recognized by World Coal magazine in its Annual Review of major coal projects

32 Capesize Vessel Top-off Operation

33 Capesize Vessel Top-off Operation

34 Summary (1)» China will remain a major factor in the Spot Seaborne coking coal market.» Mongolia still an important source of coking coal into China. However, constrained by regulatory & political environment in Mongolia as well as infrastructure and logistical hurdles.» Chinese buyers are interested in overall Value proposition and buying patterns vary from province to province and also depending on market conditions and domestic supply. However, US Hi-Vol Cross over Coals and low-vol coals will always find a home in China. 34

35 Summary (2)» The market for U.S. origin coking coal and thermal coal is challenging» Demand remains fragile as consumers and producers struggle to generate profits» Although 2012 was a challenging year for U.S. coal producers, 2013 is not shaping up to be much better but U.S. origin coal will be able to maintain a significant share of the seaborne market» Coal produced by U.S. origin low cost producers, with value added products, will benefit from the adjustment in the marketplace 35

36 Summary (3)» Although global consumers may not be concerned about the pricing of U.S. origin coals, a sudden departure of U.S. origin coal from the global markets would have an affect on market pricing» There will be fewer U.S. coal mines / companies, i.e. survivors, when the U.S. domestic market reaches equilibrium (expected in late 2013/2014).» The global market for U.S. coal exports will not save every mine / every company 36

37 Summary (4)» Exports of premium grades of U.S. origin coking coal will continue to play a significant role in the seaborne coking coal market, including China» When utilizing Xcoal s top off operation, capesize shipments of U.S. origin coking coal will remain competitive, on a delivered basis, to customers in China and throughout Asia» Everyone involved in the supply chain, i.e. the coal producers, railways, export terminals, and vessel owners, is committed to ensuring the sustainable supply of U.S. origin coal to customers in China 37

38 Credits» American Iron & Steel Institute» China-National Bureau of Statistics» CRU Analysis» International Iron and Steel Institute» John T. Boyd Company» Macquarie Research» McCloskey Group» National Mining Association (USA)» T. Parker Host» World Steel Association» World Steel Dynamics» China Coal Resources 38

39 Contact Info Muktesh Mukherjee Xcoal Energy & Resources Beijing Representative Office 39A20 China World Tower No. 1 Jian Guo Men Wai Avenue Beijing, China Phone +86 (10) xcoal-china@xcoal-china.com Web: 39

LABRADOR IRON MINES REPORTS QUARTERLY RESULTS

LABRADOR IRON MINES REPORTS QUARTERLY RESULTS Toronto, Ontario, August 28, 2015. Labrador Iron Mines Holdings Limited ( LIM or the Company ) today reports its operating and financial results for its first

LABRADOR IRON MINES REPORTS QUARTERLY RESULTS Toronto, Ontario, August 28, 2015. Labrador Iron Mines Holdings Limited ( LIM or the Company ) today reports its operating and financial results for its first

DIVERSITY & REACH CONNECTING COAL MARKETS

DIVERSITY & REACH CONNECTING COAL MARKETS Trafigura is a leading independent thermal coal trader. We focus on sourcing, storing, blending and delivering coal to exact customer specifications across all

DIVERSITY & REACH CONNECTING COAL MARKETS Trafigura is a leading independent thermal coal trader. We focus on sourcing, storing, blending and delivering coal to exact customer specifications across all

Table 1: Resource Exports Per cent of total nominal exports; selected years

Australia and the Global market for Bulk Commodities Introduction The share of Australia s export earnings derived from bulk commodities coking coal, thermal coal and iron ore has increased over recent

Australia and the Global market for Bulk Commodities Introduction The share of Australia s export earnings derived from bulk commodities coking coal, thermal coal and iron ore has increased over recent

Comparison Analysis of the Australian Dollar with BFI Production, Commodity Exports and Mining Industry

Comparison Analysis of the Australian Dollar with BFI Production, Commodity Exports and Mining Industry Hee Joong Kim (James) hvk5120@gmail.com September 10, 2015 ABSTRACT Australia is the largest iron

Comparison Analysis of the Australian Dollar with BFI Production, Commodity Exports and Mining Industry Hee Joong Kim (James) hvk5120@gmail.com September 10, 2015 ABSTRACT Australia is the largest iron

Carlos Fernández Alvarez

Carlos Fernández Alvarez Senior Coal Analyst Madrid, 30 January 2014 About the IEA Established in November 1974 in order to: Promote energy security Provide analysis to ensure reliable, affordable and

Carlos Fernández Alvarez Senior Coal Analyst Madrid, 30 January 2014 About the IEA Established in November 1974 in order to: Promote energy security Provide analysis to ensure reliable, affordable and

Market outlook. Kathrine Fog. Capital Markets Day 2015

Market outlook Kathrine Fog Capital Markets Day 215 Agenda market outlook 1 Macroeconomic and downstream outlook 2 Primary metal market 3 Bauxite and alumina market 4 Long-term outlook 2 Macroeconomic

Market outlook Kathrine Fog Capital Markets Day 215 Agenda market outlook 1 Macroeconomic and downstream outlook 2 Primary metal market 3 Bauxite and alumina market 4 Long-term outlook 2 Macroeconomic

Disclaimer. No offer of securities This presentation does not constitute an offer to sell or the solicitation of an offer to buy any securities.

Disclaimer Forward looking statements Certain statements in this document are not historical facts and are or are deemed to be forward-looking. NWR s prospects, plans, financial position and business strategy,

Disclaimer Forward looking statements Certain statements in this document are not historical facts and are or are deemed to be forward-looking. NWR s prospects, plans, financial position and business strategy,

Yara International ASA Second quarter results 2014

Yara International ASA Second quarter results 214 18 July 214 1 Summary second quarter Strong result Lower nitrate deliveries amid early end to season in Europe Continued strong NPK deliveries and value-added

Yara International ASA Second quarter results 214 18 July 214 1 Summary second quarter Strong result Lower nitrate deliveries amid early end to season in Europe Continued strong NPK deliveries and value-added

Fourth Quarter 2015. Questions and Answers

Fourth Quarter 2015 Questions and Answers Forward-Looking Statements This document may contain forward-looking information and statements about ArcelorMittal and its subsidiaries. These statements include

Fourth Quarter 2015 Questions and Answers Forward-Looking Statements This document may contain forward-looking information and statements about ArcelorMittal and its subsidiaries. These statements include

Golden Ocean Group Limited Q3 2006 results December 1, 2006

Golden Ocean Group Limited Q3 2006 results December 1, 2006 PROFIT & LOSS 2005 2006 (in thousands of $) 2006 2005 2005 Jul-Sep Jul-Sep Jan - Sep Jan - Sep Jan - Dec Operating Revenues 26,265 66,431 Time

Golden Ocean Group Limited Q3 2006 results December 1, 2006 PROFIT & LOSS 2005 2006 (in thousands of $) 2006 2005 2005 Jul-Sep Jul-Sep Jan - Sep Jan - Sep Jan - Dec Operating Revenues 26,265 66,431 Time

Baader Investment Conference

Baader Investment Conference Bernhard Kleinermann, Director Corporate Communication and IR Munich, September 23, 20 1 Market Situation 2 Financial Accounts First Half of 20 3 Salzgitter AG 20 / Prospects

Baader Investment Conference Bernhard Kleinermann, Director Corporate Communication and IR Munich, September 23, 20 1 Market Situation 2 Financial Accounts First Half of 20 3 Salzgitter AG 20 / Prospects

NORDEN RESULTS. 1 st quarter of 2013. Hellerup, Denmark 15 May 2013. Our business is global tramp shipping. NORDEN 1st quarter of 2013 results 1

NORDEN RESULTS 1 st quarter of 2013 Hellerup, Denmark 15 May 2013 NORDEN 1st quarter of 2013 results 1 AGENDA Group highlights Financial highlights Market update Full year financial guidance Q & A NORDEN

NORDEN RESULTS 1 st quarter of 2013 Hellerup, Denmark 15 May 2013 NORDEN 1st quarter of 2013 results 1 AGENDA Group highlights Financial highlights Market update Full year financial guidance Q & A NORDEN

Dr. Burkhard Lohr, CFO

Experience growth. K+S Group Q2/15 Results 13 August 2015 Dr. Burkhard Lohr, CFO K+S Group Highlights Rejection of Potash Corp s unsolicited proposal The proposed transaction does not reflect the fundamental

Experience growth. K+S Group Q2/15 Results 13 August 2015 Dr. Burkhard Lohr, CFO K+S Group Highlights Rejection of Potash Corp s unsolicited proposal The proposed transaction does not reflect the fundamental

Investors Meeting (For 1st Half Business Results)

") Fiscal Year Ending March 31, 29 Investors Meeting (For 1st Half Business Results) November 7, 28 Eizo Kobayashi, President and CEO 1.Summary for the 1H of FY29 2.Segment Information (1H of FY29) 3.Forecast

Fiscal Year Ending March 31, 29 Investors Meeting (For 1st Half Business Results) November 7, 28 Eizo Kobayashi, President and CEO 1.Summary for the 1H of FY29 2.Segment Information (1H of FY29) 3.Forecast

EVRAZ H1 2013 results Transcript of the conference call. Management Presentation. Corporate Participants

EVRAZ H1 2013 results Transcript of the conference call Corporate Participants Alexander Frolov Giacomo Baizini Pavel Tatyanin Management Presentation Operator Thank you for standing by and welcome to

EVRAZ H1 2013 results Transcript of the conference call Corporate Participants Alexander Frolov Giacomo Baizini Pavel Tatyanin Management Presentation Operator Thank you for standing by and welcome to

Financial Year 2013/14

Financial Year Investor Relations June 2014 voestalpineag AG www.voestalpine.com Overview From a steel producer to a technology and industrial goods corporation High-tech steel is the base of voestalpine,

Financial Year Investor Relations June 2014 voestalpineag AG www.voestalpine.com Overview From a steel producer to a technology and industrial goods corporation High-tech steel is the base of voestalpine,

Carlos Fernández Alvarez. Senior Coal Analyst

Carlos Fernández Alvarez. Senior Coal Analyst AGENDA BACKGROUND What is coal, how is coal mined, where is coal used for COAL ATTRIBUTES Coal is cheap, abundant and diversified SUPPLY AND DEMAND TRENDS

Carlos Fernández Alvarez. Senior Coal Analyst AGENDA BACKGROUND What is coal, how is coal mined, where is coal used for COAL ATTRIBUTES Coal is cheap, abundant and diversified SUPPLY AND DEMAND TRENDS

Global Energy Dynamics: Outlook for the Future. Dr Fatih Birol Chief Economist, IEA 18 June 2014

Global Energy Dynamics: Outlook for the Future Dr Fatih Birol Chief Economist, IEA 18 June 2014 The world energy scene today Some long held tenets of the energy sector are being rewritten Countries are

Global Energy Dynamics: Outlook for the Future Dr Fatih Birol Chief Economist, IEA 18 June 2014 The world energy scene today Some long held tenets of the energy sector are being rewritten Countries are

Changes Underway in the Central Appalachian Coal Industry

July 14, 2014 Changes Underway in the Central Appalachian Coal Industry Changes Underway in the Central Appalachian Coal Industry but first some background on the political drivers of this change 1 Some

July 14, 2014 Changes Underway in the Central Appalachian Coal Industry Changes Underway in the Central Appalachian Coal Industry but first some background on the political drivers of this change 1 Some

2Q15 Earnings Conference Call

2Q15 Earnings Conference Call André B. Gerdau Johannpeter President and CEO Harley Lorentz Scardoelli Financial, Planning and IR Director - CFO Credit: New York State Thruway Authority Gerdau is supplying

2Q15 Earnings Conference Call André B. Gerdau Johannpeter President and CEO Harley Lorentz Scardoelli Financial, Planning and IR Director - CFO Credit: New York State Thruway Authority Gerdau is supplying

Tim Howkins, CEO. Steve Clutton, Finance Director

Tim Howkins, CEO Steve Clutton, Finance Director Highlights Revenue Revenue up 36% Earnings per share up 33% All parts of business contributed to growth Benefits of increased IT spend Proposed final dividend

Tim Howkins, CEO Steve Clutton, Finance Director Highlights Revenue Revenue up 36% Earnings per share up 33% All parts of business contributed to growth Benefits of increased IT spend Proposed final dividend

SSAB Europe. Olavi Huhtala EVP & Head of SSAB Europe

SSAB Europe EVP & Head of SSAB Europe A leading Nordic-based steel producer of highest-quality strip, plate and tubular products 2 Our steel product offering Hot-rolled strip & plate High-strength grades

SSAB Europe EVP & Head of SSAB Europe A leading Nordic-based steel producer of highest-quality strip, plate and tubular products 2 Our steel product offering Hot-rolled strip & plate High-strength grades

STEEL: CHAOS IN THE INDUSTRY

Spring Manufacturers Institute Charlotte, NC October 20-21 2015 STEEL: CHAOS IN THE INDUSTRY Differentiating between fundamental and cyclical, and what it means for your 2016 budget John Anton, Director,

Spring Manufacturers Institute Charlotte, NC October 20-21 2015 STEEL: CHAOS IN THE INDUSTRY Differentiating between fundamental and cyclical, and what it means for your 2016 budget John Anton, Director,

Energy OIL S WILD RIDE DRIVING VALUE FROM THE SUPPLY CHAIN AUTHORS. Keric Morris, Partner Curt Underwood, Partner Bob Peterson, Partner

Energy OIL S WILD RIDE DRIVING VALUE FROM THE SUPPLY CHAIN AUTHORS Keric Morris, Partner Curt Underwood, Partner Bob Peterson, Partner TAMING THE SUPPLY CHAIN The recent decline in oil prices has begun

Energy OIL S WILD RIDE DRIVING VALUE FROM THE SUPPLY CHAIN AUTHORS Keric Morris, Partner Curt Underwood, Partner Bob Peterson, Partner TAMING THE SUPPLY CHAIN The recent decline in oil prices has begun

PRESS RELEASE. Revenue as of March 31, 2011. Sharp growth in Bureau Veritas Q1 2011 revenue Revenue up 23% to 775 million Organic growth of 6.

1 PRESS RELEASE Neuilly-sur-Seine, France, May 4, 2011 Sharp growth in Bureau Veritas Q1 2011 revenue Revenue up 23% to 775 million Organic growth of 6.5% Frank Piedelièvre, Chairman and Chief Executive

1 PRESS RELEASE Neuilly-sur-Seine, France, May 4, 2011 Sharp growth in Bureau Veritas Q1 2011 revenue Revenue up 23% to 775 million Organic growth of 6.5% Frank Piedelièvre, Chairman and Chief Executive

Metals Monitor July 2012

Metals Monitor July 212 Group Economics Sector & Commodity Research Casper Burgering casper.burgering@nl.abnamro.comcm Metals in macro context... Metal markets are dominated by macroeconomic developments.

Metals Monitor July 212 Group Economics Sector & Commodity Research Casper Burgering casper.burgering@nl.abnamro.comcm Metals in macro context... Metal markets are dominated by macroeconomic developments.

The Global Ferrous Scrap Metal Markets

The Global Ferrous Scrap Metal Markets Joseph C. Pickard Chief Economist and Director of Commodities Institute of Scrap Recycling Industries, Inc. Platts 2 nd Annual Scrap Seminar March 11, 2013 Chicago,

The Global Ferrous Scrap Metal Markets Joseph C. Pickard Chief Economist and Director of Commodities Institute of Scrap Recycling Industries, Inc. Platts 2 nd Annual Scrap Seminar March 11, 2013 Chicago,

MECHEL REPORTS THE 1Q 2015 FINANCIAL RESULTS

MECHEL REPORTS THE 1Q 2015 FINANCIAL RESULTS amounted to $1.1 billion Consolidated EBITDA(a) * amounted to $211 million Net loss attributable to shareholders of Mechel OAO amounted to $273 million Moscow,

MECHEL REPORTS THE 1Q 2015 FINANCIAL RESULTS amounted to $1.1 billion Consolidated EBITDA(a) * amounted to $211 million Net loss attributable to shareholders of Mechel OAO amounted to $273 million Moscow,

Core Strengths, Sustainable Returns

Nordic Senior Investor Day 2012 Core Strengths, Sustainable Returns Daniel Fairclough, Head of Investor Relations Hetal Patel, General Manager Investor Relations 23 May 2012 Disclaimer Forward-Looking

Nordic Senior Investor Day 2012 Core Strengths, Sustainable Returns Daniel Fairclough, Head of Investor Relations Hetal Patel, General Manager Investor Relations 23 May 2012 Disclaimer Forward-Looking

Makita Corporation. Consolidated Financial Results for the nine months ended December 31, 2007 (U.S. GAAP Financial Information)

") Makita Corporation Consolidated Financial Results for the nine months ended (U.S. GAAP Financial Information) (English translation of "ZAIMU/GYOSEKI NO GAIKYO" originally issued in Japanese language) CONSOLIDATED

Makita Corporation Consolidated Financial Results for the nine months ended (U.S. GAAP Financial Information) (English translation of "ZAIMU/GYOSEKI NO GAIKYO" originally issued in Japanese language) CONSOLIDATED

Interim financial report for the period 1 January to 30 September 2011

Company announcement no. 11/ 18 November Page 1 of 9 Interim financial report for the period 1 January to 30 September Highlights Results improved in the third quarter with a gross profit of USD 8 million

Company announcement no. 11/ 18 November Page 1 of 9 Interim financial report for the period 1 January to 30 September Highlights Results improved in the third quarter with a gross profit of USD 8 million

Financial Information

Financial Information Solid results with in all key financial metrics of 23.6 bn, up 0.4% like-for like Adjusted EBITA margin up 0.3 pt on organic basis Net profit up +4% to 1.9 bn Record Free Cash Flow

Financial Information Solid results with in all key financial metrics of 23.6 bn, up 0.4% like-for like Adjusted EBITA margin up 0.3 pt on organic basis Net profit up +4% to 1.9 bn Record Free Cash Flow

PEABODY ENERGY ANNOUNCES RESULTS FOR THE YEAR ENDED DECEMBER 31, 2015

News Release CONTACT: Vic Svec (314) 342-7768 FOR IMMEDIATE RELEASE February 11, 2016 PEABODY ENERGY ANNOUNCES RESULTS FOR THE YEAR ENDED DECEMBER 31, 2015 2015 revenues of $5.61 billion lead to Adjusted

News Release CONTACT: Vic Svec (314) 342-7768 FOR IMMEDIATE RELEASE February 11, 2016 PEABODY ENERGY ANNOUNCES RESULTS FOR THE YEAR ENDED DECEMBER 31, 2015 2015 revenues of $5.61 billion lead to Adjusted

Annual General and Special Meeting

TSX:NML www.nmliron.com Annual General and Special Meeting June 23, 2016 Toronto, ON Robert Patzelt, Q.C. President & CEO Taconite Project Proposed Concentrator Forward Looking Statements and Other Legal

TSX:NML www.nmliron.com Annual General and Special Meeting June 23, 2016 Toronto, ON Robert Patzelt, Q.C. President & CEO Taconite Project Proposed Concentrator Forward Looking Statements and Other Legal

Mining Canada G.P. Pierre Lapointe General Manager Operational Excellence September 2014

Mining Canada G.P. Pierre Lapointe General Manager Operational Excellence September 2014 0 ArcelorMittal Mining Portfolio 29 mines in 11 countries Canada Baffinland 50% Bosnia Iron Ore 51% Ukraine Iron

Mining Canada G.P. Pierre Lapointe General Manager Operational Excellence September 2014 0 ArcelorMittal Mining Portfolio 29 mines in 11 countries Canada Baffinland 50% Bosnia Iron Ore 51% Ukraine Iron

RHI AG. May 12, 2016

RHI AG Results 1Q/16 May 12, 2016 Highlights & Lowlights Highlights Positiv Steel Division operating EBIT margin of 7.8% in 1Q/16 driven by Europe and North America as a result of an improved product mix

RHI AG Results 1Q/16 May 12, 2016 Highlights & Lowlights Highlights Positiv Steel Division operating EBIT margin of 7.8% in 1Q/16 driven by Europe and North America as a result of an improved product mix

Prices are set to firm in early Q2, but demand and prices likely to weaken before holiday periods

Prices are set to firm in early Q2, but demand and prices likely to weaken before holiday periods The Eurozone crisis has eased slightly, though concerns could re emerge at any time and any unforeseen

Prices are set to firm in early Q2, but demand and prices likely to weaken before holiday periods The Eurozone crisis has eased slightly, though concerns could re emerge at any time and any unforeseen

Symptoms of Network Marketing - Year End Performance

Slide 1, Conference call operator: Good morning. My name is [ ] and I will be your conference operator today. At this time, I would like to welcome everyone to Catalyst Paper Corporation s Fourth Quarter

Slide 1, Conference call operator: Good morning. My name is [ ] and I will be your conference operator today. At this time, I would like to welcome everyone to Catalyst Paper Corporation s Fourth Quarter

Chlor-Alkali & Derivatives Markets

Chlor-Alkali & Derivatives Markets PVC Committee Meeting at APIC 213 Taipei, 1 May 213 Charles Fryer US GULF CAUSTIC SODA & CHLORINE PRICES $/Metric Ton 1,4 1,3 1,2 1,1 1, 9 8 7 6 5 4 3 2 1 Caustic Caustic

Chlor-Alkali & Derivatives Markets PVC Committee Meeting at APIC 213 Taipei, 1 May 213 Charles Fryer US GULF CAUSTIC SODA & CHLORINE PRICES $/Metric Ton 1,4 1,3 1,2 1,1 1, 9 8 7 6 5 4 3 2 1 Caustic Caustic

Statement of Lawrence W. Kavanagh Vice President, Environment and Technology American Iron and Steel Institute Washington, D.C.

Statement of Lawrence W. Kavanagh Vice President, Environment and Technology American Iron and Steel Institute Washington, D.C. Submitted for the Record Committee on Small Business U.S. House of Representatives

Statement of Lawrence W. Kavanagh Vice President, Environment and Technology American Iron and Steel Institute Washington, D.C. Submitted for the Record Committee on Small Business U.S. House of Representatives

OLYMPIC STEEL BALANCE SHEET MANAGEMENT AT

Cover Story BALANCE SHEET MANAGEMENT AT OLYMPIC STEEL How the company survived volatility in the steel service industry and came out ahead using good management accounting practices. B Y W ILLIAM J. C

Cover Story BALANCE SHEET MANAGEMENT AT OLYMPIC STEEL How the company survived volatility in the steel service industry and came out ahead using good management accounting practices. B Y W ILLIAM J. C

1. Supplemental explanation of FY2014 Q3 financial results

February 2015 1. Supplemental explanation of FY2014 Q3 financial results Overall view Despite the favorable winds of a depreciating yen and lower bunker prices, we could not fully leverage these benefits,

February 2015 1. Supplemental explanation of FY2014 Q3 financial results Overall view Despite the favorable winds of a depreciating yen and lower bunker prices, we could not fully leverage these benefits,

Result up on higher volumes and prices

Result up on higher volumes and prices First quarter presentation 2013 (1) highlights Underlying EBIT NOK 1 077 million Higher sales volumes driven by seasonality Increased realized alumina and aluminium

Result up on higher volumes and prices First quarter presentation 2013 (1) highlights Underlying EBIT NOK 1 077 million Higher sales volumes driven by seasonality Increased realized alumina and aluminium

Coffee Year 2014-15 Futures Trading Analysis

Lower coffee exports lend support to Robusta prices The coffee market rallied slightly in June, led in most part by a recovery in Robusta prices. For the sixth month in a row exports were lower than last

Lower coffee exports lend support to Robusta prices The coffee market rallied slightly in June, led in most part by a recovery in Robusta prices. For the sixth month in a row exports were lower than last

FRANKLIN ELECTRIC REPORTS RECORD SECOND QUARTER 2013 SALES AND EARNINGS

For Immediate Release For Further Information Refer to: John J. Haines 260-824-2900 FRANKLIN ELECTRIC REPORTS RECORD SECOND QUARTER 2013 SALES AND EARNINGS Bluffton, Indiana July 30, 2013 - Franklin Electric

For Immediate Release For Further Information Refer to: John J. Haines 260-824-2900 FRANKLIN ELECTRIC REPORTS RECORD SECOND QUARTER 2013 SALES AND EARNINGS Bluffton, Indiana July 30, 2013 - Franklin Electric

COAL MARKET FREQUENTLY ASKED QUESTIONS

COAL MARKET FREQUENTLY ASKED QUESTIONS Over the course of the past decade, numerous issues have arisen in the U.S. coal trading arena. Bankruptcies, standardized trading contracts, and liquidity are a

COAL MARKET FREQUENTLY ASKED QUESTIONS Over the course of the past decade, numerous issues have arisen in the U.S. coal trading arena. Bankruptcies, standardized trading contracts, and liquidity are a

ADVISORY CAPABILITY STATEMENT

ADVISORY CAPABILITY STATEMENT Bridging Two Disciplines We are independent Engineering Economists and Advisors. Our principal competency is as supply side and asset specialists. Since 1971 we have bridged

ADVISORY CAPABILITY STATEMENT Bridging Two Disciplines We are independent Engineering Economists and Advisors. Our principal competency is as supply side and asset specialists. Since 1971 we have bridged

GLOBAL COMMODITIES TRADING

GLOBAL COMMODITIES TRADING CONTENTS INTRODUCTION 3 Strategic Growth 5 Our History 6 Key Figures 8 A Global Business 13 APPROACH, CULTURE & VALUES 14 Our People 17 Risk Management 18 Compliance 19 HSEC

GLOBAL COMMODITIES TRADING CONTENTS INTRODUCTION 3 Strategic Growth 5 Our History 6 Key Figures 8 A Global Business 13 APPROACH, CULTURE & VALUES 14 Our People 17 Risk Management 18 Compliance 19 HSEC

Outotec Thursday, 29 th September 2012 14:00 Hrs UK time Chaired by Pirjo Lifländer

Outotec Thursday, 29 th September 2012 14:00 Hrs UK time Chaired by Good afternoon and welcome to this Q3 Q&A session with Outotec s president and CEO,. I would like to remind you that this webcast will

Outotec Thursday, 29 th September 2012 14:00 Hrs UK time Chaired by Good afternoon and welcome to this Q3 Q&A session with Outotec s president and CEO,. I would like to remind you that this webcast will

Hay Point Coal Terminal Queensland, Australia

Hay Point Coal Terminal Queensland, Australia Overview of Operations 1 BMA Coal Logistics Chain Export Terminals BMA owned and operated Shipping Tonnes FY02 Hay Point Services 30.6mt Common User Facilities

Hay Point Coal Terminal Queensland, Australia Overview of Operations 1 BMA Coal Logistics Chain Export Terminals BMA owned and operated Shipping Tonnes FY02 Hay Point Services 30.6mt Common User Facilities

EARNINGS RELEASE FOR IMMEDIATE RELEASE EXPEDITORS REPORTS FOURTH QUARTER 2014 EPS OF $0.51 PER SHARE 1

By: Expeditors International of Washington, Inc. 1015 Third Avenue, Suite 1200 Seattle, Washington 98104 EARNINGS RELEASE CONTACTS: R. Jordan Gates Bradley S. Powell President and Chief Operating Officer

By: Expeditors International of Washington, Inc. 1015 Third Avenue, Suite 1200 Seattle, Washington 98104 EARNINGS RELEASE CONTACTS: R. Jordan Gates Bradley S. Powell President and Chief Operating Officer

Managing Financial Risk

Giddy Financial Risk Management /1 Managing Financial Risk Prof. Ian Giddy New York University Corporate Finance CORPORATE FINANCE DECISONS INVESTMENT FINANCING RISK MGT MGT PORTFOLIO CAPITAL M&A DEBT

Giddy Financial Risk Management /1 Managing Financial Risk Prof. Ian Giddy New York University Corporate Finance CORPORATE FINANCE DECISONS INVESTMENT FINANCING RISK MGT MGT PORTFOLIO CAPITAL M&A DEBT

Biomass Pellet Prices Drivers and Outlook What is the worst that can happen?

Biomass Pellet Prices Drivers and Outlook What is the worst that can happen? European Biomass Power Generation 1st October 2012 Cormac O Carroll Director, London Office Pöyry Management Consulting (UK)

Biomass Pellet Prices Drivers and Outlook What is the worst that can happen? European Biomass Power Generation 1st October 2012 Cormac O Carroll Director, London Office Pöyry Management Consulting (UK)

Managing Shipping Risk in the Global Supply Chain The Case for Freight Options

Managing Shipping Risk in the Global Supply Chain The Case for Professor in Shipping Risk management Director, MSc Shipping, Trade & Finance Cass Business School email: n.nomikos@city.ac.uk Presentation

Managing Shipping Risk in the Global Supply Chain The Case for Professor in Shipping Risk management Director, MSc Shipping, Trade & Finance Cass Business School email: n.nomikos@city.ac.uk Presentation

Q2 2015 Earnings Conference Call. July 30, 2015

Q2 2015 Earnings Conference Call July 30, 2015 Industry Data and Forward-Looking Statements Disclaimer Broadwind obtained the industry and market data used throughout this presentation from our own research,

Q2 2015 Earnings Conference Call July 30, 2015 Industry Data and Forward-Looking Statements Disclaimer Broadwind obtained the industry and market data used throughout this presentation from our own research,

Q4 2015 AND 12M 2015 NLMK GROUP CONSOLIDATED FINANCIAL RESULTS UNDER IFRS

Media contact info: Sergey Babichenko +7 (916) 824 6743 babichenko_sy@nlmk.com IR contact info: Sergey Takhiev +7 (495) 915 1575 st@nlmk.com Press release 24 March 2016 Q4 2015 AND 12M 2015 NLMK GROUP

Media contact info: Sergey Babichenko +7 (916) 824 6743 babichenko_sy@nlmk.com IR contact info: Sergey Takhiev +7 (495) 915 1575 st@nlmk.com Press release 24 March 2016 Q4 2015 AND 12M 2015 NLMK GROUP

Ferro-nickel / NPI Production from Laterite Nickel Ore in China. Jiang Xinfang Tsingshan Holding Group

Ferro-nickel / NPI Production from Laterite Nickel Ore in China Jiang Xinfang Tsingshan Holding Group 1. Nickel Ore Importation in China World Land Based Nickel Resource Sulfide 28% Laterite 72% World

Ferro-nickel / NPI Production from Laterite Nickel Ore in China Jiang Xinfang Tsingshan Holding Group 1. Nickel Ore Importation in China World Land Based Nickel Resource Sulfide 28% Laterite 72% World

DEVELOPMENTS IN INTERNATIONAL SEABORNE TRADE

1 DEVELOPMENTS IN INTERNATIONAL SEABORNE TRADE Global economic growth faltered in 2013 as economic activity in developing regions suffered setbacks and as the situation in the advanced economies improved

1 DEVELOPMENTS IN INTERNATIONAL SEABORNE TRADE Global economic growth faltered in 2013 as economic activity in developing regions suffered setbacks and as the situation in the advanced economies improved

Mining Supply Chain Optimization:

Mining Supply Chain Optimization: From Pit to Port Coal is a continually dominant element of the energy supply mix, and its importance is growing due to rapid population and income growth in developing

Mining Supply Chain Optimization: From Pit to Port Coal is a continually dominant element of the energy supply mix, and its importance is growing due to rapid population and income growth in developing

NATURAL GAS PRICES TO REMAIN AT HIGHER LEVELS

I. Summary NATURAL GAS PRICES TO REMAIN AT HIGHER LEVELS This brief white paper on natural gas prices is intended to discuss the continued and sustained level of natural gas prices at overall higher levels.

I. Summary NATURAL GAS PRICES TO REMAIN AT HIGHER LEVELS This brief white paper on natural gas prices is intended to discuss the continued and sustained level of natural gas prices at overall higher levels.

Fully diluted net income per share. Yen. Total Assets Net Assets Equity Ratio. Millions of yen Millions of yen % 565,019 255,311 41.

November 10, Consolidated Financial Results (Japanese Accounting Standards) For the Second Quarter of the March 31,2016 Fiscal Year AIR WATER INC. Head Office: 12-8, Minami semba 2-chome, Chuo-ku, Osaka,

November 10, Consolidated Financial Results (Japanese Accounting Standards) For the Second Quarter of the March 31,2016 Fiscal Year AIR WATER INC. Head Office: 12-8, Minami semba 2-chome, Chuo-ku, Osaka,

MMG LIMITED 五 礦 資 源 有 限 公 司

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness

CORPORATE PRESENTATION September 2012

CORPORATE PRESENTATION September 2012 Timeline CSN Share Ownership June 30, 2012 VICUNHA 47.9% RIO IACO CBS 4.0% 0.9% 1946 1.9% BNDESPAR 1974/1989 3 Expansions in Volta Redonda Steel Mill ADRs 25.5% Bovespa

CORPORATE PRESENTATION September 2012 Timeline CSN Share Ownership June 30, 2012 VICUNHA 47.9% RIO IACO CBS 4.0% 0.9% 1946 1.9% BNDESPAR 1974/1989 3 Expansions in Volta Redonda Steel Mill ADRs 25.5% Bovespa

HIGH-LEVEL SYMPOSIUM Excess Capacity and Structural Adjustment in the Steel Sector

HIGH-LEVEL SYMPOSIUM Excess Capacity and Structural Adjustment in the Steel Sector 18 April 216, Brussels, Belgium BACKGROUND NOTE NO. 1 LATEST GLOBAL STEEL MARKET DEVELOPMENTS This background document

HIGH-LEVEL SYMPOSIUM Excess Capacity and Structural Adjustment in the Steel Sector 18 April 216, Brussels, Belgium BACKGROUND NOTE NO. 1 LATEST GLOBAL STEEL MARKET DEVELOPMENTS This background document

4Q14 Conference Call. André B. Gerdau Johannpeter President and CEO. André Pires de Oliveira Dias Vice-President and IR Director

4Q14 Conference Call André B. Gerdau Johannpeter President and CEO André Pires de Oliveira Dias Vice-President and IR Director World steel oversupply remains the industry s challenge Overcapacity and weaker

4Q14 Conference Call André B. Gerdau Johannpeter President and CEO André Pires de Oliveira Dias Vice-President and IR Director World steel oversupply remains the industry s challenge Overcapacity and weaker

The Growing Commodity Trading Market in Asia. Rebecca Brosnan Head of Asia Commodities 22 April 2015

The Growing Commodity Trading Market in Asia Rebecca Brosnan Head of Asia Commodities 22 April 2015 I. HKEx s Entry into Commodities Vertical Value Chain HKEx Group Business Strategy Horizontal Asset Classes

The Growing Commodity Trading Market in Asia Rebecca Brosnan Head of Asia Commodities 22 April 2015 I. HKEx s Entry into Commodities Vertical Value Chain HKEx Group Business Strategy Horizontal Asset Classes

People with energy. Adding value right across the supply chain

People with energy 140 million tonnes of fuel delivered in the last 10 years* Marine fuels is a large and complex global industry and is one of the world s foremost suppliers. Delivering on our commitment

People with energy 140 million tonnes of fuel delivered in the last 10 years* Marine fuels is a large and complex global industry and is one of the world s foremost suppliers. Delivering on our commitment

November 2, 2011 (For your information) Mazda Motor Corporation FISCAL YEAR ENDING MARCH 2012 FIRST HALF FINANCIAL RESULTS (Speech Outline)

Mazda Motor Corporation FISCAL YEAR ENDING MARCH 2012 FIRST HALF FINANCIAL RESULTS (Speech Outline)") November 2, 2011 (For your information) Mazda Motor Corporation FISCAL YEAR ENDING MARCH 2012 FIRST HALF FINANCIAL RESULTS (Speech Outline) Representative Director, Chairman of the Board, President and

November 2, 2011 (For your information) Mazda Motor Corporation FISCAL YEAR ENDING MARCH 2012 FIRST HALF FINANCIAL RESULTS (Speech Outline) Representative Director, Chairman of the Board, President and

Listings Officer Company Announcements ASX Limited, Melbourne

ASX Release 09 September 2015 Listings Officer Company Announcements ASX Limited, Melbourne UPDATED PRELIMINARY FEASIBILITY ECONOMIC EVALUATION AMMAROO PHOSPHATE PROJECT ASX ANNOUNCEMENT ASX CODE: RUM

ASX Release 09 September 2015 Listings Officer Company Announcements ASX Limited, Melbourne UPDATED PRELIMINARY FEASIBILITY ECONOMIC EVALUATION AMMAROO PHOSPHATE PROJECT ASX ANNOUNCEMENT ASX CODE: RUM

Corporate Risk Management Advisory Services FX and interest rate solutions for clients

Corporate Risk Management Advisory Services FX and interest rate solutions for clients Risk Management: The UBS Warburg approach UBS Warburg has built an outstanding reputation in the management of foreign

Corporate Risk Management Advisory Services FX and interest rate solutions for clients Risk Management: The UBS Warburg approach UBS Warburg has built an outstanding reputation in the management of foreign

Statement by Kasper Rorsted Chairman of the Management Board Conference-Call November 11, 2015, 10.30 a.m.

Statement by Kasper Rorsted Chairman of the Management Board Conference-Call November 11, 2015, 10.30 a.m. Welcome to our conference call today. As you will have seen, this morning we sent out our news

Statement by Kasper Rorsted Chairman of the Management Board Conference-Call November 11, 2015, 10.30 a.m. Welcome to our conference call today. As you will have seen, this morning we sent out our news

Contents. Part I: The Global Financial Environment 1

Contents List of Figures List of Tables Preface and Acknowledgments About the Authors xii xv xviii xxvii Part I: The Global Financial Environment 1 Chapter 1: Introduction 3 Opening Case 1: TIAA-CREF Goes

Contents List of Figures List of Tables Preface and Acknowledgments About the Authors xii xv xviii xxvii Part I: The Global Financial Environment 1 Chapter 1: Introduction 3 Opening Case 1: TIAA-CREF Goes

Q2-14 Financial Results. July 30, 2014

Q2-14 Financial Results July 30, 2014 Forward-looking Statements & Non-GAAP Measures Information contained in these materials or presented orally on the earnings conference call, either in prepared remarks

Q2-14 Financial Results July 30, 2014 Forward-looking Statements & Non-GAAP Measures Information contained in these materials or presented orally on the earnings conference call, either in prepared remarks

APEC Young Leaders Forum Report Beijing & Shanghai, China 9-14 July 2001

APEC Young Leaders Forum Report Beijing & Shanghai, China 9-14 July 2001 Prepared By Elizabeth Quat President, Internet Professionals Association Economic Forecast Global economic go downward: 2000 growth

APEC Young Leaders Forum Report Beijing & Shanghai, China 9-14 July 2001 Prepared By Elizabeth Quat President, Internet Professionals Association Economic Forecast Global economic go downward: 2000 growth

Finance. Eivind Kallevik. Capital Markets Day 2013 (1)

") Finance Eivind Kallevik Capital Markets Day 2013 (1) Agenda Financial policy Financial reporting going forward Internal measures External results Earning drivers (2) Financial policy 01 (3) Priorities

Finance Eivind Kallevik Capital Markets Day 2013 (1) Agenda Financial policy Financial reporting going forward Internal measures External results Earning drivers (2) Financial policy 01 (3) Priorities

FOR IMMEDIATE RELEASE

FOR IMMEDIATE RELEASE O-I REPORTS FULL YEAR AND FOURTH QUARTER 2014 RESULTS O-I generates second highest free cash flow in the Company s history PERRYSBURG, Ohio (February 2, 2015) Owens-Illinois, Inc.

FOR IMMEDIATE RELEASE O-I REPORTS FULL YEAR AND FOURTH QUARTER 2014 RESULTS O-I generates second highest free cash flow in the Company s history PERRYSBURG, Ohio (February 2, 2015) Owens-Illinois, Inc.

Delivering Long-Term Shareholder Value

Delivering Long-Term Shareholder Value 9 October 214, Perth Cautionary statement 2 This presentation has been prepared by Rio Tinto plc and Rio Tinto Limited ( Rio Tinto ) and consisting of the slides

Delivering Long-Term Shareholder Value 9 October 214, Perth Cautionary statement 2 This presentation has been prepared by Rio Tinto plc and Rio Tinto Limited ( Rio Tinto ) and consisting of the slides

Delivering a Competitive Edge Across the Supply Chain

Delivering a Competitive Edge Across the Supply Chain An Industry White Paper By Laura Rokohl, Supply Chain Manager, AspenTech Supply chain leaders face significant challenges today amidst market volatility

Delivering a Competitive Edge Across the Supply Chain An Industry White Paper By Laura Rokohl, Supply Chain Manager, AspenTech Supply chain leaders face significant challenges today amidst market volatility

Yara International ASA Fourth quarter results 2011. 7 February 2012

Yara International ASA Fourth quarter results 211 7 February 212 1 Summary fourth quarter Strong quarter and best full-year results so far Good farm profitability drove improved margins, more than offsetting

Yara International ASA Fourth quarter results 211 7 February 212 1 Summary fourth quarter Strong quarter and best full-year results so far Good farm profitability drove improved margins, more than offsetting

A New Age for Steel Metallics: A Global Market Outlook to 2020

NEW A New Age for Steel Metallics: A Global Market Outlook to 2020 l Obsolete Scrap l Prompt Industrial Scrap l Home (Revert) Scrap l Pig Iron l DRI/HBI Also featuring coverage on: l Iron Ore l Which markets

NEW A New Age for Steel Metallics: A Global Market Outlook to 2020 l Obsolete Scrap l Prompt Industrial Scrap l Home (Revert) Scrap l Pig Iron l DRI/HBI Also featuring coverage on: l Iron Ore l Which markets

Announcement of FY2010-FY2011 Medium-Term Management Plan, Frontier e 2010 - Enhancing Corporate Value on the World Stage, Shaping the Future -

April 30, 2009 ITOCHU Corporation (Code No. 8001, Tokyo Stock Exchange, 1 st Section) Contact: Isamu Nakayama General Manager, Corporate Communication Division (TEL. +81-3-3497-7291) This document is an

April 30, 2009 ITOCHU Corporation (Code No. 8001, Tokyo Stock Exchange, 1 st Section) Contact: Isamu Nakayama General Manager, Corporate Communication Division (TEL. +81-3-3497-7291) This document is an

Holcim Leadership Journey 2012-2014. May 14, 2012

Holcim Leadership Journey 2012-2014 Summary of the Holcim Leadership Journey 2012-2014 Focus on health and safety strengthen the social dialog Development and generation of leaders and talents By 2014

Holcim Leadership Journey 2012-2014 Summary of the Holcim Leadership Journey 2012-2014 Focus on health and safety strengthen the social dialog Development and generation of leaders and talents By 2014

Issue. September 2012

September 2012 Issue In a future world of 8.5 billion people in 2035, the Energy Information Administration s (EIA) projected 50% increase in energy consumption will require true all of the above energy

September 2012 Issue In a future world of 8.5 billion people in 2035, the Energy Information Administration s (EIA) projected 50% increase in energy consumption will require true all of the above energy

DANIELI & C. OFFICINE MECCANICHE S.p.A. Buttrio (UD) via Nazionale n. 41

via Nazionale n. 41") DANIELI & C. OFFICINE MECCANICHE S.p.A. Buttrio (UD) via Nazionale n. 41 Fully paid-up share capital of euro 81,304,566 Registration Number with the Register of Companies of Udine, tax number and VAT registration

DANIELI & C. OFFICINE MECCANICHE S.p.A. Buttrio (UD) via Nazionale n. 41 Fully paid-up share capital of euro 81,304,566 Registration Number with the Register of Companies of Udine, tax number and VAT registration

Centralised Company Announcements Platform Australian Stock Exchange Exchange Centre, 20 Bridge Street Sydney NSW 2000

Suite 2, 12 Parliament Place, West Perth WA 6005 PO Box 902, West Perth WA 6872 Ph: 08 9482 0515 Fax: 08 9482 0505 Web: www.transitholdings.com.au 22 nd December 2010 Centralised Company Announcements

Suite 2, 12 Parliament Place, West Perth WA 6005 PO Box 902, West Perth WA 6872 Ph: 08 9482 0515 Fax: 08 9482 0505 Web: www.transitholdings.com.au 22 nd December 2010 Centralised Company Announcements

Fertilizer is a world market commodity, which means that supply

Supply & demand, Energy Drive Global fertilizer prices The Fertilizer Institute Nourish, Replenish, Grow Fertilizer is a world market commodity necessary for the production of food, feed, fuel fiber. &

Supply & demand, Energy Drive Global fertilizer prices The Fertilizer Institute Nourish, Replenish, Grow Fertilizer is a world market commodity necessary for the production of food, feed, fuel fiber. &

Platts Oil Benchmarks & Price Assessment Methodology. October 4, 2012 - London

Platts Oil Benchmarks & Price Assessment Methodology October 4, 2012 - London Agenda Introduction and the role of benchmarks Platts price discovery process Global commodity markets outlook Platts MOC liquidity:

Platts Oil Benchmarks & Price Assessment Methodology October 4, 2012 - London Agenda Introduction and the role of benchmarks Platts price discovery process Global commodity markets outlook Platts MOC liquidity:

COCERAL Position Position on MiFID II Level 2 legislation Definition of regulatory and implementing technical standards

COCERAL Position Position on MiFID II Level 2 legislation Definition of regulatory and implementing technical standards Brussels, 2 December 2014 COCERAL would like to bring the views of agricultural commodities

COCERAL Position Position on MiFID II Level 2 legislation Definition of regulatory and implementing technical standards Brussels, 2 December 2014 COCERAL would like to bring the views of agricultural commodities

COMMITTEE ON FOREIGN AFFAIRS SUBCOMMITTEE ON TERRORISM NON-PROLIFERATION AND TRADE

TESTIMONY OF THOMAS J. RAGUSO EXECUTIVE VICE PRESIDENT AMEGY BANK N.A. Before the COMMITTEE ON FOREIGN AFFAIRS SUBCOMMITTEE ON TERRORISM NON-PROLIFERATION AND TRADE UNITED STATES HOUSE OF REPRESENTATIVES

TESTIMONY OF THOMAS J. RAGUSO EXECUTIVE VICE PRESIDENT AMEGY BANK N.A. Before the COMMITTEE ON FOREIGN AFFAIRS SUBCOMMITTEE ON TERRORISM NON-PROLIFERATION AND TRADE UNITED STATES HOUSE OF REPRESENTATIVES

Consolidated Settlement of Accounts for the First 3 Quarters Ended December 31, 2011 [Japanese Standards]

![Consolidated Settlement of Accounts for the First 3 Quarters Ended December 31, 2011 [Japanese Standards]](/thumbs/37/17704792.jpg "Consolidated Settlement of Accounts for the First 3 Quarters Ended December 31, 2011 [Japanese Standards]") The figures for these Financial Statements are prepared in accordance with the accounting principles based on Japanese law. Accordingly, they do not necessarily match the figures in the Annual Report issued

The figures for these Financial Statements are prepared in accordance with the accounting principles based on Japanese law. Accordingly, they do not necessarily match the figures in the Annual Report issued

UBS Staff Agencies and Support Services Conference. 14 September 2011

UBS Staff Agencies and Support Services Conference 14 September 2011 Disclaimer This presentation may contain forward-looking statements based on current assumptions and forecasts made by Brenntag AG and

UBS Staff Agencies and Support Services Conference 14 September 2011 Disclaimer This presentation may contain forward-looking statements based on current assumptions and forecasts made by Brenntag AG and

World Energy Outlook. Dr. Fatih Birol IEA Chief Economist Paris, 27 February 2014

World Energy Outlook Dr. Fatih Birol IEA Chief Economist Paris, 27 February 2014 The world energy scene today Some long-held tenets of the energy sector are being rewritten Countries are switching roles:

World Energy Outlook Dr. Fatih Birol IEA Chief Economist Paris, 27 February 2014 The world energy scene today Some long-held tenets of the energy sector are being rewritten Countries are switching roles:

State of the Oil Markets?

State of the Oil Markets? U.S. and Global Refining Prospects John R. Auers, P.E. Executive Vice President Washington DC February 17, 2016 U.S. Refining is YUGE! 2 What Determines Refining Winners? Refined

State of the Oil Markets? U.S. and Global Refining Prospects John R. Auers, P.E. Executive Vice President Washington DC February 17, 2016 U.S. Refining is YUGE! 2 What Determines Refining Winners? Refined

December 2015 Quarterly Production Report

28 January 2016 December 2015 Quarterly Production Report Fortescue shipped 42.1 million tonnes of iron ore at a record low cash production cost (C1) of US$15.80 per wet metric tonne (wmt) for the December

28 January 2016 December 2015 Quarterly Production Report Fortescue shipped 42.1 million tonnes of iron ore at a record low cash production cost (C1) of US$15.80 per wet metric tonne (wmt) for the December

Iron & Steel Outlook March 2007

Group Economics Iron & Steel Outlook March 27 Minerals & Energy: Gerard Burg Gerard.Burg@nab.com.au (+613) 8641 3984 Summary iron ore prices reach new record in 27, but set to decline in 28 Chinese producers

Group Economics Iron & Steel Outlook March 27 Minerals & Energy: Gerard Burg Gerard.Burg@nab.com.au (+613) 8641 3984 Summary iron ore prices reach new record in 27, but set to decline in 28 Chinese producers

RMB solutions for importers and exporters

RMB solutions for importers and exporters Unravel the complexities of RMB Mind the gap The potential Share of world trade vs payments The proof of the pudding Percentage of China s trade in RMB RMB 13th

RMB solutions for importers and exporters Unravel the complexities of RMB Mind the gap The potential Share of world trade vs payments The proof of the pudding Percentage of China s trade in RMB RMB 13th

CLTX Weekly Market Summary

CLTX Weekly Market Summary Summary Dry Bulk The main dry bulk index dropped to new historical lows Rates decreased for Capesize, Supramax and Handysize vessels Iron Ore and Steel ANZ bank cut its iron

CLTX Weekly Market Summary Summary Dry Bulk The main dry bulk index dropped to new historical lows Rates decreased for Capesize, Supramax and Handysize vessels Iron Ore and Steel ANZ bank cut its iron

UPS International Services

UPS International Services Logistics keeps the world moving. Your world runs on logistics To keep your world running at its best healthcare, high tech, retail, professional services or manufacturing you

UPS International Services Logistics keeps the world moving. Your world runs on logistics To keep your world running at its best healthcare, high tech, retail, professional services or manufacturing you

QUARTERLY REPORT FOR THE PERIOD ENDING 31 MARCH 2015

QUARTERLY REPORT FOR THE PERIOD ENDING 31 MARCH 2015 HIGHLIGHTS Positive free cashflow (revenue less operating costs and CAPEX) of $191k for the month of March; a first in the history of Lynas Amended

QUARTERLY REPORT FOR THE PERIOD ENDING 31 MARCH 2015 HIGHLIGHTS Positive free cashflow (revenue less operating costs and CAPEX) of $191k for the month of March; a first in the history of Lynas Amended

NATURAL GAS PRICE VOLATILITY

NATURAL GAS PRICE VOLATILITY I. Summary This brief white paper on natural gas prices is intended to discuss the potential for natural gas prices to be very volatile during the winter of 2003-04. Prices

NATURAL GAS PRICE VOLATILITY I. Summary This brief white paper on natural gas prices is intended to discuss the potential for natural gas prices to be very volatile during the winter of 2003-04. Prices