Connecticut State Employee Collective Bargaining and Retirement Benefits

|

|

|

- Linda Bridges

- 8 years ago

- Views:

Transcription

1

2

3 Background Connecticut State Employee Collective Bargaining and Retirement Benefits State employees through their bargaining units have had the authority under state law to collectively bargain on wages, hours, and other conditions of employment since The State Employee Retirement Act was amended in 1981 making state employee retirement benefits a mandatory subject of collective bargaining, and required state employees to be represented by a coalition of all the bargaining units, the State Employees Bargaining Agent Coalition (SEBAC). The first pension agreement was collectively bargained between the state and the employee coalition in 1982 and has been modified by seven subsequent agreements, the most recent the 2011 SEBAC agreement, which expires in Despite the collective bargaining agreement authority between the state and its employees, any agreement, including a retirement benefits contract, must be filed with the legislature for approval or rejection by majority vote or for de facto approval by inaction after a certain amount of time. If any new agreement provisions conflict with state statute or regulation, approval of those conflicts must be specifically requested (C.G.S. Sec (b)). During the time an agreement is in force, the legislature cannot change any of the contract terms, even by legislation (C.G.S. Sec (e)). The current SEBAC retirement benefits agreement governs all current and future employees and is in place until a subsequent agreement is negotiated and approved. Types of Employer Retirement Plans: Defined Benefit or Defined Contribution The two main types of employer retirement plans are defined benefit (DB) and defined contribution (DC) plans. A defined benefit plan like SERS provides a fixed benefit, known as a pension, at retirement, determined by years of service and salary. The employer funds the plan, to which employees may or may not also contribute. In contrast, a defined contribution plan, such as a 401K, does not pay a fixed benefit; the income available from such a plan is based on the actual balance accrued at retirement in an individual tax-deferred account. Both DB and DC plans typically include annual contributions from employer and employee. The major difference between the two types of plans is that investment risk is assumed by the employer in DB plans, because a fixed benefit must be paid no matter what, while this risk is shifted to the employee in DC plans. 1

.")

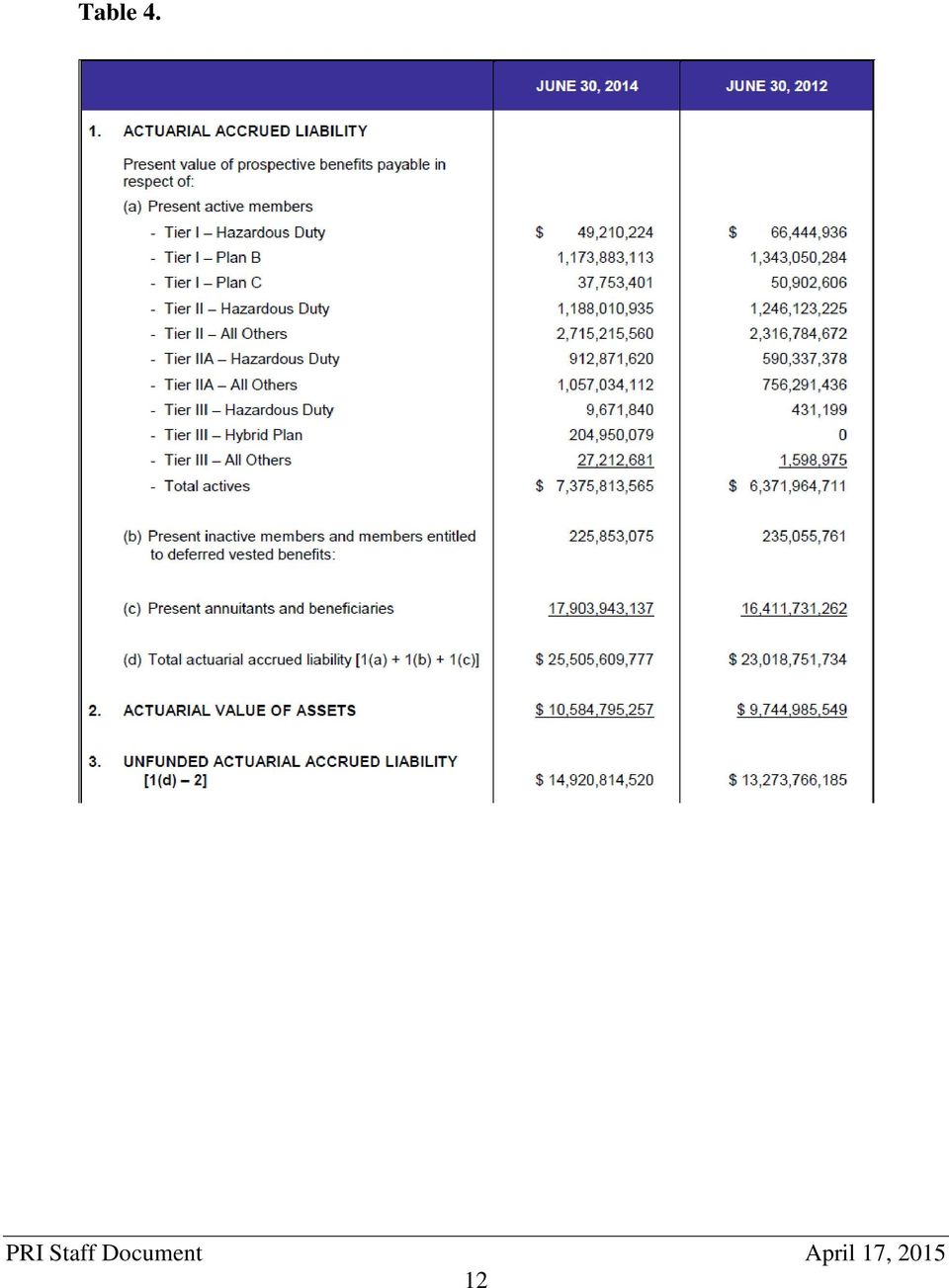

4 Questions Pertinent to Consideration of Defined Contribution Plan for New State Employees I. How Is SERS currently funded? a. SERS is statutorily required to be funded on an actuarial reserve basis. i. The state makes an annual contribution to the SERS fund, based on an actuarial valuation (e.g., averaged expectations about employee life span, years on job, and salary) prepared at least every two years to determine what dollar amount will ensure the fund will meet future payment obligations. (See Table 1) b. The state s annual contribution to the SERS fund is composed of two parts: 1) normal cost and 2) unfunded accrued pension liability amortization payment. i. Normal cost is the amount of the money the state needs to reserve in the current fiscal year for employees currently working in that year (i.e., current service), based on actuarial calculations of what the future costs of those workers retirement benefits will be. 1. Employee contributions lower the normal cost the state pays. 1 ii. Unfunded pension liability amortization payment is the annual amount of money that is calculated to pay off the unfunded liability (totaling $15 billion Table 4) over 30 years. According to this schedule, the unfunded liability should be eliminated by (See Table 3) 1. The unfunded liability is the bill for past years liabilities that were not funded when accrued. 2. Who accounts for this unfunded accrued liability? (See Figure 1) a. Retirees and beneficiaries account for 70 percent of the unfunded liability b. Active employees account for 29 percent c. Inactive members with vested benefits account for 1 percent 1 The annual normal cost and employee contributions combined equal the present value of the funds needed in the future to pay out the actuarially established retirement benefits of those current employees. 2

b. The state s annual contribution to the SERS fund is")

5 II. What impact could the implementation of a defined contribution (401K- type) plan for new employees have on Connecticut s unfunded accrued pension liability for the State Employees Retirement System (SERS)? a. Changing to a 401K-like plan for new state employees would not reduce this liability because the liability is attributed to retirees and current employees. (See Table 4) Newly hired employees do not start with any unfunded liability and, if their normal cost is fully funded each year, should not accrue an unfunded liability. b. Generally speaking, closing a defined benefit plan to new members can increase DB plan costs due to several factors: i. Shift to lower-return investments 1. A DB plan with a mix of young, middle-aged, and older workers allows for a diverse investment portfolio. In contrast, a closed DB plan with no new younger members must shift away from higher return/higher risk to more conservative investments. 2. Decreasing contributions to the plan relative to increasing payouts increases the need for more liquid assets. a. This creates a need to shift assets to investments with more predictable cash flows. This generally has a negative impact on the fund and results in lower investment income. 3. Decreased investment returns require higher employer and/or employee contributions a. Investment returns make up largest portion of pension plan revenue. ii. Loss of contributions from new members i. For a typical career employee, more than onehalf of the investment income earned on assets accumulated to pay benefits is received after the employee retires. 1. New SERS members contribute beginning with their first paycheck, but are not vested (i.e., eligible for a benefit at 3

6 retirement) for five years. Many will leave state service before vesting and therefore forfeit these contributions. iii. Any unfunded liability must be spread across a shrinking payroll base and could change the amortization schedule to require larger payments earlier 1. Government accounting standards (GASB 25 and 27) require that the DB unfunded liability be amortized as a level percent of the projected payroll or as level dollar amounts. 2. For an open DB plan, payrolls can be expected to grow as new workers replace retiring employees and average pay generally increases. As a result, payment schedules can increase at the same rate as payroll. 3. However, once a DB plan is frozen, payroll will decline over time. Therefore, a frozen plan must be amortized over a decreasing payroll, as opposed to an open plan that can spread the costs over a growing payroll base. iv. Administrative costs are not eliminated for DB plan. 1. The plan must be administered until the last participant retires. III. What are some of the implications of offering a defined contribution plan for the state s annual normal cost contributions? (i.e., cost of current employees future benefits) a. There are many ways in which a defined contribution plan can be structured but, for the purposes of this discussion, we have assumed that any analysis of, or comparison between, defined benefit and defined contribution plans would be for equivalent benefits. b. In general, providing equivalent benefits under a defined benefit structure may be less expensive to the individual under a defined contribution plan due to: i. Longevity risk pooling 1. In a DB plan, only enough assets are required to pay for the average life expectancy. In a DC plan, the individual must guess his or her exact life span or accumulate more assets to last a maximum life expectancy. ii. Maintaining a more balanced portfolio over longer period of time 4

7 iii. Achieving higher investment returns due to diverse investments, professional management, and lower fees 1. There is an additional cost to manage a DC plan that is usually higher than a DB plan because administrative costs are driven by scale. a. In addition, in the first year of a DC plan, there can be significant start-up costs. c. The state s normal cost contribution (for current employees service) for newest non-hazardous Tier III employees is the lowest among all the SERS pension plans at 2.57percent of salary. The state could potentially save some money if it established a 401K plan that features a contribution that is less than 2.57 percent (Table 2). Employees may have to contribute more to obtain equivalent benefits, however. d. A DC plan usually has an employer contribution; most also match. i. According to the Plan Sponsor Council of America (PSCA), a national, non-profit industry association, companies contributed an average of 4.7 percent of pay to a DC plan in 2013 (up from 4.5 percent in 2012 and 4.1 percent five years ago) and 80.1 percent of such plans make a match on employee contributions. ii. (The state s contribution rate for the Alternate Retirement Plan, a DC plan for employees of the state s colleges and universities, is 8 percent. Employees contribute 5 percent.) IV. Does the governor s proposed budget reflect fully funding the state s actuarially determined annual contribution to SERS in FY 16 and FY 17? a. Yes. The state s total SERS contribution is calculated to be $1.514 billion in FY 16 and $1.569 in FY 17. The governor s proposed budget appropriates $1.220 billion in FY 16 and $1.255 in FY 17 to fully fund the General and Special Transportation funds portions of the SERS contribution. The balance of the contribution is made up of recoveries from other appropriated fund agencies as well as federal recoveries, which are approximately $294 million in FY 16 and $314 million in FY 17. 5

.")

8 V. Have any recent changes been made to SERS and retired and active employee health benefits to generate savings and reduce the state s long-term liabilities? a. The 2011 SEBAC agreement made numerous changes to SERS, retiree health insurance, and health benefits offered to active state employees. Changes are briefly summarized below. i. SERS 1. Pension changes included establishing a new benefit tier Tier III for new employees as of FY 12; increasing the normal retirement age by three years; increasing hazardous duty years of service from 20 to 25 years; increasing the early retirement penalty from 3 percent per year to 6 percent per year; imposing new caps on salary as well as mandatory overtime used in pension calculations; changing minimum and maximum cost of living adjustments (COLA) to 2 percent and to 7.5 percent; requiring a recalculation of the breakpoint used to determine pension amounts; and creating a new hybrid pension plan for employees eligible to join the state's defined contribution Alternative Retirement Plan (ARP). ii. Retiree Healthcare 1. The agreement made several changes intended to reduce state expenditures for retiree healthcare coverage by increasing service and age eligibility requirements, increasing contributions by employees and the state to the retiree healthcare trust fund, and by increasing retiree premiums under certain circumstances. iii. Employee Healthcare 1. The 2011 agreement created a new Health Enhancement Program (HEP) in the hope that increasing disease prevention and early intervention services will decrease long term expenses. It also made several changes to prescription drug copayments and increased participation in a mail-order pharmacy program. In addition, the agreement created a new emergency room visit copay to discourage unnecessary ER visits. 6

9 VI. Preliminarily, what have been some of the past experiences of other state and local governments that have made a switch to a defined contribution or other system? a. Case studies of three states that made the switch from defined benefit to defined contribution plans West Virginia (1991), Michigan (1997), and Alaska (2005) show they experienced exacerbated underfunding problems (decreasing solvency) and increased annual costs (decreasing liquidity). b. In 2005, West Virginia switched back to the DB plan. c. In addition, employees under the new defined contribution plans found it difficult to retire due to inadequate account balances. For instance, in Michigan, average retirement income was approximately $8,200/year for DC plan participants vs. over $20,000/year for DB plan members. d. In 2012, Kansas, Louisiana, and Virginia replaced defined benefit plans with cash balance or hybrid plans for new employees. A cash balance plan is a pension plan under which an employer credits a participant's account with a set percentage of his or her yearly compensation plus interest charges. A hybrid plan has elements of both a DB and DC plan. (See Rhode Island example below.) VII. More recently, what pension reforms have been enacted in Rhode Island? a. In 2011, Rhode Island passed a comprehensive pension overhaul called the Rhode Island Retirement Security Act of 2011 (RIRSA). This new law has been implemented but is being challenged in the Rhode Island Superior Court by current and retired state employees. Recent reports indicate that the unions and the state may have developed a settlement agreement to avoid a trial set to begin April 20. b. RIRSA includes four major parts: i. A new defined - contribution plan to work in tandem with the current defined - benefit pension plan (referred to as a hybrid plan). State employees contribute 3.75 percent toward a defined benefit plan and 5 percent toward a defined contribution plan. (This is the same total amount (8.75 percent) state employees contributed under the old defined benefit plan.) The state will contribute an additional 1 percent to the defined contribution account; 7

10 ii. A suspension of cost-of-living adjustments for all current retirees until the pension system reaches a combined 80 percent funding level; iii. An increase in the retirement age for current employees that matches Social Security thresholds, with provisions that accommodate those eligible to retire or close to retirement; and iv. A change in the amortization of liabilities. The legislation increases the amortization schedule by six years, from 19 to 25 years. 8

11 Table 1. Most Of The State s Current Contribution To SERS Is For Past Unfunded Pension Liabilities (FY 16) Contribution for Contribution Amount Contribution Rate A. Normal Cost: Service retirement benefits Disability benefits Survivor benefits Total Normal Cost $349,193,1 25 2,264,3 78 4,476, % 0.06% 0.13% 10.20% B. Less Member Contributions $355,934,377 (2.21)% C. Employer Normal Cost $278,812, % D. Unfunded Actuarial Accrued Liabilities (based on 17 years at level percent of payroll amortization) $1,235,654, % E. Total (C. + D.) $1,514,467, % 1. The current total SERS unfunded accrued pension liability is about $15 billion. o The FY 16 amortized payment toward that liability is set to be about 1.2 billion (Row D). o Row C shows the normal cost to the state to fund current active members of SERS of about $280 million, for FY The state s total SERS contribution for FY 16 is calculated to be $1.514 billion (Row E). The governor s proposed budget appropriates $1.220 billion in FY 16 to fully fund the General and Special Transportation funds portions of the SERS contribution. The balance of the contribution is made up of recoveries from other appropriated fund agencies as well as federal recoveries, which is approximately $294 million. 9

$1,235,654,507 35.43% E. Total (C. + D.) $1,514,467,324 43.42% 1.")

12 Table 2. The Normal Cost Contribution Rate The State Pays Is The Least For New Employees (Tier III- Other) (FY 16) Group Normal Cost Normal Rate Tier I Hazardous $ % Tier I Plan B 26,922, Tier I Plan C 630, Tier II Hazardous 34,043, Tier II Others 95,233, Tier IIA Hazardous 47,280, Tier IIA Others 57,438, Tier III Hazardous 3,392, Tier III Hybrid Plan 7,343, Tier III Others 6,527, Total $ 278,812, % The average normal cost contribution rate is nearly 8.00 percent of payroll, but the rate for new employees is the least at 2.57 percent; the most is for Tier II Hazardous at percent. 10

13 Table 3. There Is A Schedule To Eliminate The Unfunded Accrued Liability Over 17 Years Valuation Year Unfunded Accrued Liability ($ in thousands) Amortization Period Amortization Payment ($ in thousands) 2014 $14,920, $1,235, ,831, ,281, ,763, ,336, ,461, ,377, ,120, ,422, ,844, ,483, ,499, ,548, ,065, ,618, ,528, ,692, ,878, ,771, ,100, ,856, ,179, ,947, ,097, ,049, ,835, ,163, ,367, ,298, ,665, ,477, ,687, ,797, Figure 1. % Actuarial Accrued Liability by Group 70% 5% 15% 8% 1% 1% Inactives Retirees Active Tier I Active Tier II Active Tier IIA Active Tier III 11

14 Table 4. 12

State Notes TOPICS OF LEGISLATIVE INTEREST Summer 2010

Retirement Incentive and Pension Reform of the Michigan Public School Employees' Retirement System By Kathryn Summers, Chief Analyst Introduction On May 19, 2010, Governor Granholm signed into law Senate

Retirement Incentive and Pension Reform of the Michigan Public School Employees' Retirement System By Kathryn Summers, Chief Analyst Introduction On May 19, 2010, Governor Granholm signed into law Senate

SUMMARY OF THE CONFERENCE COMMITTEE REPORT ON PUBLIC EMPLOYEE PENSIONS

SUMMARY OF THE CONFERENCE COMMITTEE REPORT ON PUBLIC EMPLOYEE PENSIONS SUMMARY: Implements comprehensive public employee pension reform through enactment of the California Public Employees' Pension Reform

SUMMARY OF THE CONFERENCE COMMITTEE REPORT ON PUBLIC EMPLOYEE PENSIONS SUMMARY: Implements comprehensive public employee pension reform through enactment of the California Public Employees' Pension Reform

THE STATE OF VIRGINIA

SUMMARY February 2013 THE STATE OF VIRGINIA The plans: Virginia has two large state-administered pension systems, four smaller state-administered plans for various state and municipal workers and many

SUMMARY February 2013 THE STATE OF VIRGINIA The plans: Virginia has two large state-administered pension systems, four smaller state-administered plans for various state and municipal workers and many

Kansas Legislator Briefing Book 2015

K a n s a s L e g i s l a t i v e R e s e a r c h D e p a r t m e n t Q-1 Kansas Public Employees Retirement System Retirement Plans and History Retirement Kansas Legislator Briefing Book 2015 Q-1 Kansas

K a n s a s L e g i s l a t i v e R e s e a r c h D e p a r t m e n t Q-1 Kansas Public Employees Retirement System Retirement Plans and History Retirement Kansas Legislator Briefing Book 2015 Q-1 Kansas

MACOMB COUNTY, MICHIGAN Notes to Basic Financial Statements December 31, 2014

Notes to Basic Financial Statements Note 8 Employees Retirement System Plan Description and Provision The County sponsors the Macomb County Employees Retirement System (the System ), a single employer

Notes to Basic Financial Statements Note 8 Employees Retirement System Plan Description and Provision The County sponsors the Macomb County Employees Retirement System (the System ), a single employer

State of Alaska Public Employees Retirement System

Public Employees Retirement System Actuarial Valuation Report as of June 30, 2005 Submitted By: Buck Consultants 1200 Seventeenth Street, Suite 1200 Denver, CO 80202 September 15, 2006 Alaska Retirement

Public Employees Retirement System Actuarial Valuation Report as of June 30, 2005 Submitted By: Buck Consultants 1200 Seventeenth Street, Suite 1200 Denver, CO 80202 September 15, 2006 Alaska Retirement

Analysis of PERS Cost Allocation, Benefit Modification, and System Financing Concepts February 14, 2013

Analysis of Cost Allocation, Benefit Modification, and System Financing Concepts February 14, 2013 Version 1.2 Important Notes Regarding This Report This report is produced to support the Board in its

Analysis of Cost Allocation, Benefit Modification, and System Financing Concepts February 14, 2013 Version 1.2 Important Notes Regarding This Report This report is produced to support the Board in its

Many public employees and

Ohio Issues Development, Transportation & General Government Ohio s Public Employee Retirement Systems: Funding Requirements and Related Issues DEBRA PELLEY Are Ohio s five public employee retirement systems

Ohio Issues Development, Transportation & General Government Ohio s Public Employee Retirement Systems: Funding Requirements and Related Issues DEBRA PELLEY Are Ohio s five public employee retirement systems

Policy Brief June 2010

Policy Brief June 2010 Pension Tension: Understanding Arizona s Public Employee Retirement Plans The Arizona Chamber Foundation (501(c)3) is a non-partisan, objective educational and research foundation.

Policy Brief June 2010 Pension Tension: Understanding Arizona s Public Employee Retirement Plans The Arizona Chamber Foundation (501(c)3) is a non-partisan, objective educational and research foundation.

The Truth about the State Employees Retirement System of Illinois

The Truth about the State Employees Retirement System of Illinois The State Employees Retirement System (SERS) began in 1944 as a core benefit for state and local employers to use in attracting and retaining

The Truth about the State Employees Retirement System of Illinois The State Employees Retirement System (SERS) began in 1944 as a core benefit for state and local employers to use in attracting and retaining

Generic Local School District, Ohio Notes to the Basic Financial Statements For the Fiscal Year Ended June 30, 2015

Note 2 - Summary of Significant Accounting Policies Pensions For purposes of measuring the net pension liability, information about the fiduciary net position of the pension plans and additions to/deductions

Note 2 - Summary of Significant Accounting Policies Pensions For purposes of measuring the net pension liability, information about the fiduciary net position of the pension plans and additions to/deductions

COMPLIANCE AUDIT. Lansdowne Borough Police Pension Plan Delaware County, Pennsylvania For the Period January 1, 2012 to December 31, 2014

COMPLIANCE AUDIT Lansdowne Borough Police Pension Plan Delaware County, Pennsylvania For the Period January 1, 2012 to December 31, 2014 July 2015 The Honorable Mayor and Borough Council Lansdowne Borough

COMPLIANCE AUDIT Lansdowne Borough Police Pension Plan Delaware County, Pennsylvania For the Period January 1, 2012 to December 31, 2014 July 2015 The Honorable Mayor and Borough Council Lansdowne Borough

Kansas Legislator Briefing Book 2012

Kansas Legislator Briefing Book 2012 Retirement V-4 Long-Term Funding of KPERS Other Retirement reports available V-1 Kansas Public Employees Retirement System V-2 Kansas Defined Contribution Retirement

Kansas Legislator Briefing Book 2012 Retirement V-4 Long-Term Funding of KPERS Other Retirement reports available V-1 Kansas Public Employees Retirement System V-2 Kansas Defined Contribution Retirement

Long-term Liabilities for Retired Employee Health Benefits

Long-term Liabilities for Retired Employee Health Benefits House Select Committee on Legacy Costs from the State Health Plan, Pensions, and ESC December 13, 2011 Outline of Presentation 1) Benefits Overview

Long-term Liabilities for Retired Employee Health Benefits House Select Committee on Legacy Costs from the State Health Plan, Pensions, and ESC December 13, 2011 Outline of Presentation 1) Benefits Overview

PENSIONS AND RETIREMENT PLAN ENACTMENTS IN 2011 STATE LEGISLATURES. January 31, 2012. Ronald K. Snell ron.snell@ncsl.org

INTRODUCTION PENSIONS AND RETIREMENT PLAN ENACTMENTS IN 2011 STATE LEGISLATURES January 31, 2012 Ronald K. Snell ron.snell@ncsl.org ABOUT THIS REPORT. This report summarizes selected state pensions and

INTRODUCTION PENSIONS AND RETIREMENT PLAN ENACTMENTS IN 2011 STATE LEGISLATURES January 31, 2012 Ronald K. Snell ron.snell@ncsl.org ABOUT THIS REPORT. This report summarizes selected state pensions and

RHODE ISLAND STATE EMPLOYEES AND ELECTING TEACHERS OPEB

RHODE ISLAND STATE EMPLOYEES AND ELECTING TEACHERS OPEB ACTUARIAL VALUATION REPORT JUNE 30, 2011 TABLE OF CONTENTS Section Page Number -- Cover Letter A B C D E F G EXECUTIVE SUMMARY 1-5 Executive Summary

RHODE ISLAND STATE EMPLOYEES AND ELECTING TEACHERS OPEB ACTUARIAL VALUATION REPORT JUNE 30, 2011 TABLE OF CONTENTS Section Page Number -- Cover Letter A B C D E F G EXECUTIVE SUMMARY 1-5 Executive Summary

Things New Yorkers Should Know About. Public Retirement Benefits in New York State

Things New Yorkers Should Know About Public Retirement Benefits in New York State October 2010 INTRODUCTION Citizens Budget Commission One Penn Plaza, Suite 640 New York, NY 10119 411 State Street Albany,

Things New Yorkers Should Know About Public Retirement Benefits in New York State October 2010 INTRODUCTION Citizens Budget Commission One Penn Plaza, Suite 640 New York, NY 10119 411 State Street Albany,

State Defined Contribution and Hybrid Pension Plans

State Defined Contribution and Hybrid Pension Plans Ronald Snell June 2010 The overwhelming majority of statewide retirement plans for public employees and for teachers are traditional defined benefit

State Defined Contribution and Hybrid Pension Plans Ronald Snell June 2010 The overwhelming majority of statewide retirement plans for public employees and for teachers are traditional defined benefit

Utah State Retirement Systems Overview. September 9, 2009 Prepared by the Office of Legislative Research and General Counsel

Utah State Retirement Systems Overview September 9, 2009 Prepared by the Office of Legislative Research and General Counsel Utah State Retirement Systems Six Participant Systems Judges Public Employees

Utah State Retirement Systems Overview September 9, 2009 Prepared by the Office of Legislative Research and General Counsel Utah State Retirement Systems Six Participant Systems Judges Public Employees

Warwick Public School System

Warwick Public School System Actuarial Valuation Post Employment Benefits Other Than Pensions as of July 1, 2011 under Governmental Accounting Standards Board Statement No. 45 (GASB 45) (Estimated Disclosures

Warwick Public School System Actuarial Valuation Post Employment Benefits Other Than Pensions as of July 1, 2011 under Governmental Accounting Standards Board Statement No. 45 (GASB 45) (Estimated Disclosures

How To Fund Trs Care

Teacher Retirement System of Texas Senate Committee on State Affairs December 9, 2014 TRS Created in 1936 by Constitutional amendment (enabling legislation in 1937) and established by Article XVI, Section

Teacher Retirement System of Texas Senate Committee on State Affairs December 9, 2014 TRS Created in 1936 by Constitutional amendment (enabling legislation in 1937) and established by Article XVI, Section

FY10 Illinois Pension Reform Proposals SURS Implications Fact Sheet 5/22/09

FY10 Illinois Pension Reform Proposals SURS Implications Fact Sheet 5/22/09 Pension reform measures covering all of the State employee retirement systems were initially proposed in the Governor s Fiscal

FY10 Illinois Pension Reform Proposals SURS Implications Fact Sheet 5/22/09 Pension reform measures covering all of the State employee retirement systems were initially proposed in the Governor s Fiscal

SUMMARY February 2013 The plans: The impact of the crisis: The impact of pension plan reforms: Total state costs:

SUMMARY February 2013 THE STATE OF GEORGIA The plans: Georgia has three large state-administered pension systems, six smaller state-administered systems, and many locally-administered systems. The state

SUMMARY February 2013 THE STATE OF GEORGIA The plans: Georgia has three large state-administered pension systems, six smaller state-administered systems, and many locally-administered systems. The state

THE STATE OF CONNECTICUT

SUMMARY February 2013 THE STATE OF CONNECTICUT The plans: Connecticut has two large state-administered pension systems, four smaller state-administered systems, and many locally-administered systems. The

SUMMARY February 2013 THE STATE OF CONNECTICUT The plans: Connecticut has two large state-administered pension systems, four smaller state-administered systems, and many locally-administered systems. The

Report of the Actuary on the Annual Valuation of the Retirement System for Employees of the City of Cincinnati. Pension Report

Report of the Actuary on the Annual Valuation of the Retirement System for Employees of the City of Cincinnati Pension Report Prepared as of December 31, 2011 and Approved by the Board of Trustees on May

Report of the Actuary on the Annual Valuation of the Retirement System for Employees of the City of Cincinnati Pension Report Prepared as of December 31, 2011 and Approved by the Board of Trustees on May

The Texas Municipal Retirement System

The Texas Municipal Retirement System (TMRS) Understanding Benefits, Funding, and Economic Impact TMRS provides valuable benefits that help cities attract and retain quality employees. It is important

The Texas Municipal Retirement System (TMRS) Understanding Benefits, Funding, and Economic Impact TMRS provides valuable benefits that help cities attract and retain quality employees. It is important

Public Pension Issues and Trends

Public Pension Issues and Trends Texas Municipal Retirement System Keith Brainard Research Director National Association of State Retirement Administrators May 22, 2015 Comparison of retirement benefits

Public Pension Issues and Trends Texas Municipal Retirement System Keith Brainard Research Director National Association of State Retirement Administrators May 22, 2015 Comparison of retirement benefits

Cavanaugh Macdonald. The experience and dedication you deserve

Cavanaugh Macdonald C O N S U L T I N G, L L C The experience and dedication you deserve Mr. David L. Senn Executive Director Teachers Retirement System State of Montana 1500 Sixth Avenue Helena, MT 59620-0139

Cavanaugh Macdonald C O N S U L T I N G, L L C The experience and dedication you deserve Mr. David L. Senn Executive Director Teachers Retirement System State of Montana 1500 Sixth Avenue Helena, MT 59620-0139

The Retirement Codes and Systems

COMMONWEALTH OF PENNSYLVANIA May 12, 2015 PUBLIC EMPLOYEE RETIREMENT COMMISSION ACTUARIAL NOTE TRANSMITTAL Bill ID: Senate Bill Number 1, Printer s Number 886 System: Subject: Public School Employees Retirement

COMMONWEALTH OF PENNSYLVANIA May 12, 2015 PUBLIC EMPLOYEE RETIREMENT COMMISSION ACTUARIAL NOTE TRANSMITTAL Bill ID: Senate Bill Number 1, Printer s Number 886 System: Subject: Public School Employees Retirement

What You Need to Know About Nevada's Retirement Plan

VOLUME 1 ISSUE 3 Comparative Analysis of the Nevada Public Employees Page 1 Hobbs, Ong & Associates and Applied Analysis were retained by the Las Vegas Chamber of Commerce to review and analyze various

VOLUME 1 ISSUE 3 Comparative Analysis of the Nevada Public Employees Page 1 Hobbs, Ong & Associates and Applied Analysis were retained by the Las Vegas Chamber of Commerce to review and analyze various

GASB STATEMENT NO. 68 REPORT FOR THE SHERIFFS RETIREMENT FUND OF GEORGIA

GASB STATEMENT NO. 68 REPORT FOR THE SHERIFFS RETIREMENT FUND OF GEORGIA PREPARED AS OF JUNE 30, 2014 Cavanaugh Macdonald C O N S U L T I N G, L L C The experience and dedication you deserve May 7, 2015

GASB STATEMENT NO. 68 REPORT FOR THE SHERIFFS RETIREMENT FUND OF GEORGIA PREPARED AS OF JUNE 30, 2014 Cavanaugh Macdonald C O N S U L T I N G, L L C The experience and dedication you deserve May 7, 2015

Retirements and Beneficiaries Added to and Removed from Rolls

FIREMEN S ANNUITY AND BENEFIT FUND OF CHICAGO ACTUARIAL VALUATION REPORT FOR THE YEAR ENDING DECEMBER 31, 2012 May 16, 2013 Retirement Board of the Firemen s Annuity and Benefit Fund of Chicago 20 South

FIREMEN S ANNUITY AND BENEFIT FUND OF CHICAGO ACTUARIAL VALUATION REPORT FOR THE YEAR ENDING DECEMBER 31, 2012 May 16, 2013 Retirement Board of the Firemen s Annuity and Benefit Fund of Chicago 20 South

Benefit Reductions in the Central States Multiemployer DB Pension Plan: Frequently Asked Questions

Benefit Reductions in the Central States Multiemployer DB Pension Plan: Frequently Asked Questions John J. Topoleski Analyst in Income Security Gary Sidor Technical Information Specialist January 28, 2016

Benefit Reductions in the Central States Multiemployer DB Pension Plan: Frequently Asked Questions John J. Topoleski Analyst in Income Security Gary Sidor Technical Information Specialist January 28, 2016

Report on the Actuarial Valuation of the Health Insurance Credit Program

Report on the Actuarial Valuation of the Health Insurance Credit Program Prepared as of June 30, 2013 Cavanaugh Macdonald C O N S U L T I N G, L L C The experience and dedication you deserve December 19,

Report on the Actuarial Valuation of the Health Insurance Credit Program Prepared as of June 30, 2013 Cavanaugh Macdonald C O N S U L T I N G, L L C The experience and dedication you deserve December 19,

JUNE 30, 2013 POST RETIREMENT BENEFITS ANALYSIS OF THE TOWN OF SMITHFIELD

JUNE 30, 2013 POST RETIREMENT BENEFITS ANALYSIS OF THE TOWN OF SMITHFIELD September 2013 2013 Smithfield OPEB report - Sept TABLE OF CONTENTS Section Item Page SECTION I OVERVIEW... 1 SECTION II REQUIRED

JUNE 30, 2013 POST RETIREMENT BENEFITS ANALYSIS OF THE TOWN OF SMITHFIELD September 2013 2013 Smithfield OPEB report - Sept TABLE OF CONTENTS Section Item Page SECTION I OVERVIEW... 1 SECTION II REQUIRED

2011 Public Act 152: Publicly Funded Health Insurance Contribution Act (MCL 15.561 15.569), as amended by 2013 Public Acts numbered 269 through 273

, as amended by 2013 Public Acts numbered 269 through 273") 2011 Public Act 152: Publicly Funded Health Insurance Contribution Act (MCL 15.561 15.569), as amended by 2013 Public Acts numbered 269 through 273 Frequently Asked Questions Table of Contents 1. General...

2011 Public Act 152: Publicly Funded Health Insurance Contribution Act (MCL 15.561 15.569), as amended by 2013 Public Acts numbered 269 through 273 Frequently Asked Questions Table of Contents 1. General...

Other Postemployment Benefits: A Plain-Language Summary of GASB Statements No. 43 and No. 45

Governmental Accounting Standards Board Other Postemployment Benefits: A Plain-Language Summary of GASB Statements No. 43 and No. 45 Please note: This document, prepared by the GASB staff, has not been

Governmental Accounting Standards Board Other Postemployment Benefits: A Plain-Language Summary of GASB Statements No. 43 and No. 45 Please note: This document, prepared by the GASB staff, has not been

DEPT: EMPLOYEE FRINGE BENEFITS UNIT NO. 1950 FUND: General - 0001. Approximate Tax Levy Cost, Employee & Retiree Fringe Benefits: $138,193,986

BUDGET SUMMARY 2012 Actual 2013 Budget 2014 Budget 2013/2014 Change Health Benefit Expenditures $ 113,308,978 $ 118,502,180 $ 118,676,177 $ 173,997 Pension Related Expenditures 64,388,961 66,724,779 65,198,296

BUDGET SUMMARY 2012 Actual 2013 Budget 2014 Budget 2013/2014 Change Health Benefit Expenditures $ 113,308,978 $ 118,502,180 $ 118,676,177 $ 173,997 Pension Related Expenditures 64,388,961 66,724,779 65,198,296

COUNTY EMPLOYEES' ANNUITY AND BENEFIT FUND OF COOK COUNTY ACTUARIAL VALUATION AS OF DECEMBER 31,2011

COUNTY EMPLOYEES' ANNUITY AND BENEFIT FUND OF COOK COUNTY ACTUARIAL VALUATION AS OF DECEMBER 31,2011 GOLDSTEIN & ASSOCIATES Actuaries and Consultants 29 SOUTH LaSALLE STREET CHICAGO, ILLINOIS 60603 PHONE

COUNTY EMPLOYEES' ANNUITY AND BENEFIT FUND OF COOK COUNTY ACTUARIAL VALUATION AS OF DECEMBER 31,2011 GOLDSTEIN & ASSOCIATES Actuaries and Consultants 29 SOUTH LaSALLE STREET CHICAGO, ILLINOIS 60603 PHONE

PUBLIC EMPLOYEES RETIREMENT SYSTEM OF THE STATE OF NEVADA ANALYSIS AND COMPARISON OF DEFINED BENEFIT AND DEFINED CONTRIBUTION RETIREMENT PLANS

Benefits, Compensation and HR Consulting PUBLIC EMPLOYEES RETIREMENT SYSTEM OF THE STATE OF NEVADA ANALYSIS AND COMPARISON OF DEFINED BENEFIT AND DEFINED CONTRIBUTION RETIREMENT PLANS Copyright 2010 THE

Benefits, Compensation and HR Consulting PUBLIC EMPLOYEES RETIREMENT SYSTEM OF THE STATE OF NEVADA ANALYSIS AND COMPARISON OF DEFINED BENEFIT AND DEFINED CONTRIBUTION RETIREMENT PLANS Copyright 2010 THE

ANTRIM COUNTY TRANSPORTATION BASIC FINANCIAL STATEMENTS DECEMBER 31, 2005

ANTRIM COUNTY TRANSPORTATION BASIC FINANCIAL STATEMENTS DECEMBER 31, 2005 ANTRIM COUNTY TRANSPORTATION TABLE OF CONTENTS PAGE Independent Auditor's Report 1 FINANCIAL STATEMENTS Statement of Net Assets

ANTRIM COUNTY TRANSPORTATION BASIC FINANCIAL STATEMENTS DECEMBER 31, 2005 ANTRIM COUNTY TRANSPORTATION TABLE OF CONTENTS PAGE Independent Auditor's Report 1 FINANCIAL STATEMENTS Statement of Net Assets

Pension Plan Reform in Virginia. By Robert C. Carlson

Pension Plan Reform in Virginia By Robert C. Carlson August 2011 Thomas Jefferson Institute for Public Policy The Thomas Jefferson Institute for Public Policy is a non-partisan research and education organization

Pension Plan Reform in Virginia By Robert C. Carlson August 2011 Thomas Jefferson Institute for Public Policy The Thomas Jefferson Institute for Public Policy is a non-partisan research and education organization

CASH BALANCE PLAN PRIMER

CASH BALANCE PLAN PRIMER Cash balance plans: Have features of both defined benefit and defined contribution plans. Can be designed to be generous, reasonable or inadequate, but will be more costly if the

CASH BALANCE PLAN PRIMER Cash balance plans: Have features of both defined benefit and defined contribution plans. Can be designed to be generous, reasonable or inadequate, but will be more costly if the

6101 - DEPARTMENT OF ADMINISTRATION 21-HEALTH CARE & BENEFITS DIVISION

Program Description The Health Care and Benefits Division provides state employees, retirees, members of the Legislature, judges and judicial branch employees, and their dependents with group benefits

Program Description The Health Care and Benefits Division provides state employees, retirees, members of the Legislature, judges and judicial branch employees, and their dependents with group benefits

THINKING OF RETIRING?

S T A T E O F C O N N E C T I C U T DEPARTMENT OF CORRECTION 24 WOLCOTT HILL ROAD WETHERSFIELD, CONNECTICUT 06109 THINKING OF RETIRING? We know this is a big decision and want to help you with the entire

S T A T E O F C O N N E C T I C U T DEPARTMENT OF CORRECTION 24 WOLCOTT HILL ROAD WETHERSFIELD, CONNECTICUT 06109 THINKING OF RETIRING? We know this is a big decision and want to help you with the entire

What Small Employers (and their Boards) Need to Know About IMRF

Need to Know About IMRF") What Small Employers (and their Boards) Need to Know About IMRF August 18, 2015 Louis W. Kosiba, Executive Director Mark Nannini, Chief Financial Officer 1 Background Agenda Benefit Structure Retirement

What Small Employers (and their Boards) Need to Know About IMRF August 18, 2015 Louis W. Kosiba, Executive Director Mark Nannini, Chief Financial Officer 1 Background Agenda Benefit Structure Retirement

Report on the Actuarial Valuation of the Group Life Insurance Program

Report on the Actuarial Valuation of the Group Life Insurance Program Prepared as of June 30, 2014 Cavanaugh Macdonald C O N S U L T I N G, L L C The experience and dedication you deserve December 19,

Report on the Actuarial Valuation of the Group Life Insurance Program Prepared as of June 30, 2014 Cavanaugh Macdonald C O N S U L T I N G, L L C The experience and dedication you deserve December 19,

Table Of Contents. iii

GASB Statement 45 Table Of Contents Overview...1 Compliance with GASB 45...2 GASB 45 Compared to Pension Requirements...2 Retiree Health Benefits: Potential Ramifications of GASB 45...3 Addressing Retiree

GASB Statement 45 Table Of Contents Overview...1 Compliance with GASB 45...2 GASB 45 Compared to Pension Requirements...2 Retiree Health Benefits: Potential Ramifications of GASB 45...3 Addressing Retiree

How many members are there? As of June 30, 2010. Active Members: Vested: 66,078 Non-Vested: 28,332 Total Active Members: 94,410

For More information, contact: Chief Executive Office Office of Public Affairs (213) 974-1363 pio@ceo.lacounty.gov Los Angeles County is already a model example of pension reform Key points Pension reform

For More information, contact: Chief Executive Office Office of Public Affairs (213) 974-1363 pio@ceo.lacounty.gov Los Angeles County is already a model example of pension reform Key points Pension reform

Scheduled for a Public Hearing Before the SUBCOMMITTEE ON SELECT REVENUE MEASURES of the HOUSE COMMITTEE ON WAYS AND MEANS on June 28, 2005

PRESENT LAW AND BACKGROUND RELATING TO MULTIEMPLOYER DEFINED BENEFIT PENSION PLANS AND RELATED PROVISIONS OF H.R. 2830, THE PENSION PROTECTION ACT OF 2005 Scheduled for a Public Hearing Before the SUBCOMMITTEE

PRESENT LAW AND BACKGROUND RELATING TO MULTIEMPLOYER DEFINED BENEFIT PENSION PLANS AND RELATED PROVISIONS OF H.R. 2830, THE PENSION PROTECTION ACT OF 2005 Scheduled for a Public Hearing Before the SUBCOMMITTEE

Kentucky Retirement Systems Health Benefits. Mike Burnside, Executive Director National Conference of State Legislators July 28, 2010

Kentucky Retirement Systems Health Benefits Mike Burnside, Executive Director National Conference of State Legislators July 28, 2010 Kentucky Retirement Systems Kentucky Retiree Health Plan Statutory changes

Kentucky Retirement Systems Health Benefits Mike Burnside, Executive Director National Conference of State Legislators July 28, 2010 Kentucky Retirement Systems Kentucky Retiree Health Plan Statutory changes

South Dakota Retirement System. Actuarial Valuation As of June 30, 2014

South Dakota Retirement System Actuarial Valuation As of June 30, 2014 2014 Xerox Corporation and Buck Consultants, LLC. All rights reserved. Xerox and Xerox and Design are trademarks of Xerox Corporation

South Dakota Retirement System Actuarial Valuation As of June 30, 2014 2014 Xerox Corporation and Buck Consultants, LLC. All rights reserved. Xerox and Xerox and Design are trademarks of Xerox Corporation

PRESENT LAW AND BACKGROUND RELATING TO EMPLOYER-SPONSORED DEFINED BENEFIT PENSION PLANS AND THE PENSION BENEFIT GUARANTY CORPORATION ( PBGC )

") PRESENT LAW AND BACKGROUND RELATING TO EMPLOYER-SPONSORED DEFINED BENEFIT PENSION PLANS AND THE PENSION BENEFIT GUARANTY CORPORATION ( PBGC ) Scheduled for a Public Hearing Before the SENATE COMMITTEE

PRESENT LAW AND BACKGROUND RELATING TO EMPLOYER-SPONSORED DEFINED BENEFIT PENSION PLANS AND THE PENSION BENEFIT GUARANTY CORPORATION ( PBGC ) Scheduled for a Public Hearing Before the SENATE COMMITTEE

West Virginia Department of Public Safety Death, Disability and Retirement Fund (Plan A)

") West Virginia Department of Public Safety Death, Disability and Retirement Fund (Plan A) Actuarial Valuation As of July 1, 2013 Prepared by: for the West Virginia Consolidated Public Retirement Board January

West Virginia Department of Public Safety Death, Disability and Retirement Fund (Plan A) Actuarial Valuation As of July 1, 2013 Prepared by: for the West Virginia Consolidated Public Retirement Board January

v02979gl.doc PUBLIC EMPLOYEES RETIREMENT SYSTEM OF NEW JERSEY FORTY-EIGHTH ANNUAL REPORT OF THE ACTUARY PREPARED AS OF JULY 1, 2002

v02979gl.doc PUBLIC EMPLOYEES RETIREMENT SYSTEM OF NEW JERSEY FORTY-EIGHTH ANNUAL REPORT OF THE ACTUARY PREPARED AS OF JULY 1, 2002 March 12, 2003 Board of Trustees Public Employees Retirement System of

v02979gl.doc PUBLIC EMPLOYEES RETIREMENT SYSTEM OF NEW JERSEY FORTY-EIGHTH ANNUAL REPORT OF THE ACTUARY PREPARED AS OF JULY 1, 2002 March 12, 2003 Board of Trustees Public Employees Retirement System of

Fund 73030 OPEB Trust

Focus Fund 73030,, was created to capture long term investment returns and make progress towards reducing the unfunded actuarial accrued liability under Governmental Accounting Standards Board (GASB) Statement

Focus Fund 73030,, was created to capture long term investment returns and make progress towards reducing the unfunded actuarial accrued liability under Governmental Accounting Standards Board (GASB) Statement

COMPLIANCE AUDIT. Donora Borough Police Pension Plan Washington County, Pennsylvania For the Period January 1, 2011 to December 31, 2013

COMPLIANCE AUDIT Donora Borough Police Pension Plan Washington County, Pennsylvania For the Period January 1, 2011 to December 31, 2013 August 2014 The Honorable Mayor and Borough Council Donora Borough

COMPLIANCE AUDIT Donora Borough Police Pension Plan Washington County, Pennsylvania For the Period January 1, 2011 to December 31, 2013 August 2014 The Honorable Mayor and Borough Council Donora Borough

Health Care Legislation Frequently Asked Questions

Health Care Legislation Frequently Asked Questions http://www.strsoh.org/whatsnew/hc-faqs.html There are six categories that most questions asked about the health care initiative fall under. Select a category

Health Care Legislation Frequently Asked Questions http://www.strsoh.org/whatsnew/hc-faqs.html There are six categories that most questions asked about the health care initiative fall under. Select a category

City of Newton Retiree Benefits A Primer

City of Newton Retiree Benefits A Primer Ruthanne Fuller with Gail Deegan Dan Fahey Ellen Grody Tony Logalbo Rob Mashal Howard Merkowitz Mal Salter Becky Searles Terry Yoffie April 22, 2014 Updated October

City of Newton Retiree Benefits A Primer Ruthanne Fuller with Gail Deegan Dan Fahey Ellen Grody Tony Logalbo Rob Mashal Howard Merkowitz Mal Salter Becky Searles Terry Yoffie April 22, 2014 Updated October

DEPT: EMPLOYEE FRINGE BENEFITS UNIT NO. 1950 FUND: General - 0001

BUDGET SUMMARY 2010 Actual 2011 Budget 2012 Budget 2011/2012 Change Health Benefit Expenditures $ 132,619,138 $ 138,642,087 $ 120,566,786 $ (18,075,301) Pension Related Expenditures 67,972,949 66,872,988

BUDGET SUMMARY 2010 Actual 2011 Budget 2012 Budget 2011/2012 Change Health Benefit Expenditures $ 132,619,138 $ 138,642,087 $ 120,566,786 $ (18,075,301) Pension Related Expenditures 67,972,949 66,872,988

HOW TO EFFECTIVELY REDESIGN BENEFIT PLANS TO BALANCE YOUR BUDGET CONSTRAINTS AND YOUR EMPLOYEES NEEDS. Robert D. Klausner Klausner & Kaufman, P.A.

HOW TO EFFECTIVELY REDESIGN BENEFIT PLANS TO BALANCE YOUR BUDGET CONSTRAINTS AND YOUR EMPLOYEES NEEDS Robert D. Klausner Klausner & Kaufman, P.A. Presentation Overview Pension restructuring and cost control

HOW TO EFFECTIVELY REDESIGN BENEFIT PLANS TO BALANCE YOUR BUDGET CONSTRAINTS AND YOUR EMPLOYEES NEEDS Robert D. Klausner Klausner & Kaufman, P.A. Presentation Overview Pension restructuring and cost control

VOLUME 1 ISSUE 4. An Overview and Comparative Analysis of Nevada s State Retiree Health Insurance Subsidy

VOLUME 1 ISSUE 4 Analysis of Nevada s State Retiree Page 1 Hobbs, Ong & Associates and Applied Analysis were retained by the Las Vegas Chamber of Commerce to review and analyze various state and local

VOLUME 1 ISSUE 4 Analysis of Nevada s State Retiree Page 1 Hobbs, Ong & Associates and Applied Analysis were retained by the Las Vegas Chamber of Commerce to review and analyze various state and local

BARGAINING IN THE AGE OF HEALTH CARE AND PENSION REFORM I. HEALTH INSURANCE - IDENTIFYING THE ISSUES AND PREPARING FOR BARGAINING

BARGAINING IN THE AGE OF HEALTH CARE AND PENSION REFORM I. HEALTH INSURANCE - IDENTIFYING THE ISSUES AND PREPARING FOR BARGAINING A. Health Care Costs 1. The issue of employee health care is one of the

BARGAINING IN THE AGE OF HEALTH CARE AND PENSION REFORM I. HEALTH INSURANCE - IDENTIFYING THE ISSUES AND PREPARING FOR BARGAINING A. Health Care Costs 1. The issue of employee health care is one of the

April 15, 2015. Senate Finance Committee Public Hearing Hearing Room 1, North Office Building, Capitol Complex, Harrisburg, PA

April 15, 2015 Senate Finance Committee Public Hearing Hearing Room 1, North Office Building, Capitol Complex, Harrisburg, PA Dear Members of the Committee, Thank you for the opportunity to provide testimony

April 15, 2015 Senate Finance Committee Public Hearing Hearing Room 1, North Office Building, Capitol Complex, Harrisburg, PA Dear Members of the Committee, Thank you for the opportunity to provide testimony

Company Pension Plans in Canada

Company Pension Plans in Canada This article provides an introduction to company pension plans as well as a discussion of several issues currently facing company pension plans in Canada. Company pension

Company Pension Plans in Canada This article provides an introduction to company pension plans as well as a discussion of several issues currently facing company pension plans in Canada. Company pension

Understanding Montana's Public Employee Retirement Plans

Understanding Montana's Public Employee Retirement Plans By Rachel Weiss, Legislative Services Division Jon Moe, Legislative Fiscal Division November 2010 Purpose This report is an introduction to Montana's

Understanding Montana's Public Employee Retirement Plans By Rachel Weiss, Legislative Services Division Jon Moe, Legislative Fiscal Division November 2010 Purpose This report is an introduction to Montana's

The GPO predominantly penalizes women educators in California, while the WEP penalizes many individuals who switch careers into public service.

Chair Pomeroy and Members, Social Security has met the social insurance promise to ensure workers will not have to live in old age poverty. This promise needs to be guaranteed for current and future workers.

Chair Pomeroy and Members, Social Security has met the social insurance promise to ensure workers will not have to live in old age poverty. This promise needs to be guaranteed for current and future workers.

COMPLIANCE AUDIT. Municipality of Kingston Police Pension Plan Luzerne County, Pennsylvania For the Period January 1, 2012 to December 31, 2014

COMPLIANCE AUDIT Municipality of Kingston Police Pension Plan Luzerne County, Pennsylvania For the Period January 1, 2012 to December 31, 2014 July 2015 The Honorable Mayor and Municipal Council Municipality

COMPLIANCE AUDIT Municipality of Kingston Police Pension Plan Luzerne County, Pennsylvania For the Period January 1, 2012 to December 31, 2014 July 2015 The Honorable Mayor and Municipal Council Municipality

2014 NCPERS Public Retirement Systems Study

2014 NCPERS Public Retirement Systems Study November 2014 Study conducted by the National Conference on Public Employee Retirement Systems and Cobalt Community Research 1 Table of Contents This study reviews

2014 NCPERS Public Retirement Systems Study November 2014 Study conducted by the National Conference on Public Employee Retirement Systems and Cobalt Community Research 1 Table of Contents This study reviews

NORTH STAR SCHOOL GASB 68 Notes to the Financial Statements For the Year Ended June 30, 2015. The employer s proportionate share associated with TRS

NORTH STAR SCHOOL GASB 68 Notes to the Financial Statements For the Year Ended June 30, 2015 Pension Amounts Total for Employer Employer s proportion of TRS and PERS pension amounts combined 74 The employer

NORTH STAR SCHOOL GASB 68 Notes to the Financial Statements For the Year Ended June 30, 2015 Pension Amounts Total for Employer Employer s proportion of TRS and PERS pension amounts combined 74 The employer

You Have an Important Choice to Make!

You Have an Important Choice to Make! July 04 As a new employee, you must choose one of three retirement plans available to eligible State University System employees. They are the: State University System

You Have an Important Choice to Make! July 04 As a new employee, you must choose one of three retirement plans available to eligible State University System employees. They are the: State University System

Utah Postretirement Employment Restrictions

BRIEFING PAPER December 2014 UTAH LEGISLATURE Utah Postretirement Employment Restrictions OFFICE OF LEGISLATIVE RESEARCH AND GENERAL COUNSEL HIGHLIGHTS Postretirement employment restrictions for public

BRIEFING PAPER December 2014 UTAH LEGISLATURE Utah Postretirement Employment Restrictions OFFICE OF LEGISLATIVE RESEARCH AND GENERAL COUNSEL HIGHLIGHTS Postretirement employment restrictions for public

Local Elected Official Toolkit

Local Elected Official Toolkit Pension Funding and Retiree Health Benefits Funding March 2011 LOCAL ELECTED OFFICIAL TOOLKIT PENSION FUNDING & RETIREE HEALTH BENEFITS FUNDING a MARCH 2011 TABLE OF CONTENTS

Local Elected Official Toolkit Pension Funding and Retiree Health Benefits Funding March 2011 LOCAL ELECTED OFFICIAL TOOLKIT PENSION FUNDING & RETIREE HEALTH BENEFITS FUNDING a MARCH 2011 TABLE OF CONTENTS

Philadelphia s Pension System: Reducing Risk and Achieving Fiscal Stability

Pennsylvania Intergovernmental Cooperation Authority Philadelphia s Pension System: Reducing Risk and Achieving Fiscal Stability Staff Report January 2015 Pennsylvania Intergovernmental Cooperation Authority

Pennsylvania Intergovernmental Cooperation Authority Philadelphia s Pension System: Reducing Risk and Achieving Fiscal Stability Staff Report January 2015 Pennsylvania Intergovernmental Cooperation Authority

ADMINISTRATION & BENEFITS

OVERVIEW OF THE KENTUCKY RETIREMENT SYSTEMS ADMINISTRATION & BENEFITS Background Most Kentucky public employees are provided retirement coverage through one of six state administered retirement systems.

OVERVIEW OF THE KENTUCKY RETIREMENT SYSTEMS ADMINISTRATION & BENEFITS Background Most Kentucky public employees are provided retirement coverage through one of six state administered retirement systems.

2012 COMPARATIVE STUDY OF MAJOR PUBLIC EMPLOYEE RETIREMENT SYSTEMS

WISCONSIN LEGISLATIVE COUNCIL 2012 COMPARATIVE STUDY OF MAJOR PUBLIC EMPLOYEE RETIREMENT SYSTEMS Prepared by: Daniel Schmidt, Principal Analyst Wisconsin Legislative Council December 2013 One East Main

WISCONSIN LEGISLATIVE COUNCIL 2012 COMPARATIVE STUDY OF MAJOR PUBLIC EMPLOYEE RETIREMENT SYSTEMS Prepared by: Daniel Schmidt, Principal Analyst Wisconsin Legislative Council December 2013 One East Main

COMPLIANCE AUDIT. Mount Carmel Township Police Pension Plan Northumberland County, Pennsylvania For the Period January 1, 2012 to December 31, 2014

COMPLIANCE AUDIT Mount Carmel Township Police Pension Plan Northumberland County, Pennsylvania For the Period January 1, 2012 to December 31, 2014 September 2015 Board of Township Supervisors Mount Carmel

COMPLIANCE AUDIT Mount Carmel Township Police Pension Plan Northumberland County, Pennsylvania For the Period January 1, 2012 to December 31, 2014 September 2015 Board of Township Supervisors Mount Carmel

FUNDING NEW JERSEY PUBLIC EMPLOYEE RETIREMENT SYSTEMS

FUNDING NEW JERSEY PUBLIC EMPLOYEE RETIREMENT SYSTEMS N ew Jersey has six major Stateadministered retirement systems. Along with the required contributions of the public employees, these systems are funded

FUNDING NEW JERSEY PUBLIC EMPLOYEE RETIREMENT SYSTEMS N ew Jersey has six major Stateadministered retirement systems. Along with the required contributions of the public employees, these systems are funded

SUMMARY February 2013 The plans: The impact of the crisis: The impact of pension plan reforms: Total state costs:

SUMMARY February 2013 THE STATE OF OHIO The plans: Ohio has four large state-administered pension systems, two smaller state-administered systems, and some locally-administered systems. The state also

SUMMARY February 2013 THE STATE OF OHIO The plans: Ohio has four large state-administered pension systems, two smaller state-administered systems, and some locally-administered systems. The state also

Retirement Security. Public Policy Issue Statement

Retirement Security June 2006 Public Policy Issue Statement Background Retirement plans represent an important aspect of the total compensation package used by employers to recruit and retain employees.

Retirement Security June 2006 Public Policy Issue Statement Background Retirement plans represent an important aspect of the total compensation package used by employers to recruit and retain employees.

GAO STATE AND LOCAL GOVERNMENT RETIREE BENEFITS. Current Funded Status of Pension and Health Benefits. Report to the Committee on Finance, U.S.

GAO United States Government Accountability Office Report to the Committee on Finance, U.S. Senate January 2008 STATE AND LOCAL GOVERNMENT RETIREE BENEFITS Current Funded Status of Pension and Health Benefits

GAO United States Government Accountability Office Report to the Committee on Finance, U.S. Senate January 2008 STATE AND LOCAL GOVERNMENT RETIREE BENEFITS Current Funded Status of Pension and Health Benefits

TESTIMONY BY KANOE MARGOL INTERIM EXECUTIVE DIRECTOR, EMPLOYEES RETIREMENT SYSTEM STATE OF HAWAII

TESTIMONY BY KANOE MARGOL INTERIM EXECUTIVE DIRECTOR, EMPLOYEES RETIREMENT SYSTEM STATE OF HAWAII TO THE HOUSE COMMITTEE ON LABOR AND PUBLIC EMPLOYMENT ON HOUSE BILL NO. 602 FEBRUARY 13, 2015, 9:30 A.M.

TESTIMONY BY KANOE MARGOL INTERIM EXECUTIVE DIRECTOR, EMPLOYEES RETIREMENT SYSTEM STATE OF HAWAII TO THE HOUSE COMMITTEE ON LABOR AND PUBLIC EMPLOYMENT ON HOUSE BILL NO. 602 FEBRUARY 13, 2015, 9:30 A.M.

ISSUE REVIEW Fiscal Services Division

ISSUE REVIEW Fiscal Services Division December 6, 2013 Overview of Iowa Public Pension Systems ISSUE This Issue Review provides basic comparative information between the three public pension systems for

ISSUE REVIEW Fiscal Services Division December 6, 2013 Overview of Iowa Public Pension Systems ISSUE This Issue Review provides basic comparative information between the three public pension systems for

County of Santa Barbara Office of the Auditor-Controller County Retirement Costs: White Paper by Robert W. Geis, CPA (Through June, 30, 2006)

") County of Santa Barbara Office of the Auditor-Controller County Retirement Costs: White Paper by Robert W. Geis, CPA (Through June, 30, 2006) The County Retirement plan and underlying systems can be difficult

County of Santa Barbara Office of the Auditor-Controller County Retirement Costs: White Paper by Robert W. Geis, CPA (Through June, 30, 2006) The County Retirement plan and underlying systems can be difficult

VI The Defined Benefit Member (Tiers I and II)

") VI The Defined Benefit Member (Tiers I and II) Enrollment Members who first entered the TRS: Before July 1, 1990, are in Tier I; On or after July 1, 1990, are in Tier II. Tier status is established when

VI The Defined Benefit Member (Tiers I and II) Enrollment Members who first entered the TRS: Before July 1, 1990, are in Tier I; On or after July 1, 1990, are in Tier II. Tier status is established when

Commonwealth of Puerto Rico Pension Overview

Morningstar Pension Report Release Date: 20 v 2013 Page 1 of 5 Pension Overview Pension Funded Level Pension Level Management Overall Pension Quality Poor Poor Poor Poor # of Plans Administered By State:

Morningstar Pension Report Release Date: 20 v 2013 Page 1 of 5 Pension Overview Pension Funded Level Pension Level Management Overall Pension Quality Poor Poor Poor Poor # of Plans Administered By State:

CRS Report for Congress

CRS Report for Congress Received through the CRS Web Order Code RS20927 Federal Employees Retirement Benefits: Bills in the 108 th Congress Summary Patrick J. Purcell Specialist in Social Legislation Domestic

CRS Report for Congress Received through the CRS Web Order Code RS20927 Federal Employees Retirement Benefits: Bills in the 108 th Congress Summary Patrick J. Purcell Specialist in Social Legislation Domestic

Choosing Your Retirement Plan Optional Retirement Plan for Higher Education VRS Hybrid Retirement Plan Membership Date: On or after January 1, 2014

Choosing Your Retirement Plan Optional Retirement Plan for Higher Education VRS Hybrid Retirement Plan Membership Date: On or after January 1, 2014 A comparison guide to help you select the best plan for

Choosing Your Retirement Plan Optional Retirement Plan for Higher Education VRS Hybrid Retirement Plan Membership Date: On or after January 1, 2014 A comparison guide to help you select the best plan for

MICHIGAN PUBLIC SCHOOL EMPLOYEES RETIREMENT SYSTEM (MPSERS) REFORM SB 1040 PA 300 OF 2012. Bethany Wicksall, Senior Fiscal Analyst September 7, 2012

REFORM SB 1040 PA 300 OF 2012. Bethany Wicksall, Senior Fiscal Analyst September 7, 2012") MICHIGAN PUBLIC SCHOOL EMPLOYEES RETIREMENT SYSTEM (MPSERS) REFORM SB 1040 PA 300 OF 2012 Bethany Wicksall, Senior Fiscal Analyst September 7, 2012 MPSERS Basic Facts For the Fiscal Year Ending September

MICHIGAN PUBLIC SCHOOL EMPLOYEES RETIREMENT SYSTEM (MPSERS) REFORM SB 1040 PA 300 OF 2012 Bethany Wicksall, Senior Fiscal Analyst September 7, 2012 MPSERS Basic Facts For the Fiscal Year Ending September

National Conference on Public Employee Retirement Systems. The Secure Choice

The Secure Choice Pension (SCP) National Conference on Public Employee Retirement Systems Sponsor Basic Design National Conference on Public Employee Retirement Systems Additional Design Details Funding

The Secure Choice Pension (SCP) National Conference on Public Employee Retirement Systems Sponsor Basic Design National Conference on Public Employee Retirement Systems Additional Design Details Funding

Governor S Proposal - Proposed Retiree Health Benefits and Taxpayers

The 2015-16 Budget: Health Benefits for Retired State Employees MAC TAYLOR LEGISLATIVE ANALYST MARCH 16, 2015 2 Legislative Analyst s Office www.lao.ca.gov 2015-16 BUDGET EXECUTIVE SUMMARY The Governor

The 2015-16 Budget: Health Benefits for Retired State Employees MAC TAYLOR LEGISLATIVE ANALYST MARCH 16, 2015 2 Legislative Analyst s Office www.lao.ca.gov 2015-16 BUDGET EXECUTIVE SUMMARY The Governor

ILLINOIS PENSION PRIMER. A Plain-English Guide to Public Employee Pensions in the State of Illinois

ILLINOIS PENSION PRIMER A Plain-English Guide to Public Employee Pensions in the State of Illinois April 22, 2015 The Civic Federation would like to express its gratitude to the Chicago Community Trust,

ILLINOIS PENSION PRIMER A Plain-English Guide to Public Employee Pensions in the State of Illinois April 22, 2015 The Civic Federation would like to express its gratitude to the Chicago Community Trust,

Diverging Trends Underlie Stable Overall U.S. OPEB Liability

Diverging Trends Underlie Stable Overall U.S. OPEB Liability Primary Credit Analyst: Sussan S Corson, New York (1) 212-438-2014; sussan.corson@standardandpoors.com Secondary Contacts: John A Sugden, New

Diverging Trends Underlie Stable Overall U.S. OPEB Liability Primary Credit Analyst: Sussan S Corson, New York (1) 212-438-2014; sussan.corson@standardandpoors.com Secondary Contacts: John A Sugden, New

Understanding Indiana s Largest Pension System

INDIANA PUBLIC RETIREMENT SYSTEM Understanding Indiana s Largest Pension System March 27, 2015 Funds Overview The Indiana Public Retirement System (INPRS) includes the two largest public retirement plans

INDIANA PUBLIC RETIREMENT SYSTEM Understanding Indiana s Largest Pension System March 27, 2015 Funds Overview The Indiana Public Retirement System (INPRS) includes the two largest public retirement plans

GOVERNOR S PROGRAM BILL 2011 MEMORANDUM

GOVERNOR S PROGRAM BILL 2011 MEMORANDUM AN ACT to amend the retirement and social security law, the education law and the administrative code of the city of New York, in relation to persons joining the

GOVERNOR S PROGRAM BILL 2011 MEMORANDUM AN ACT to amend the retirement and social security law, the education law and the administrative code of the city of New York, in relation to persons joining the

SB0001 Enrolled - 2 - LRB098 05457 JDS 35491 b

SB0001 Enrolled LRB098 05457 JDS 35491 b 1 AN ACT concerning public employee benefits. 2 Be it enacted by the People of the State of Illinois, 3 represented in the General Assembly: 4 Section 1. Legislative

SB0001 Enrolled LRB098 05457 JDS 35491 b 1 AN ACT concerning public employee benefits. 2 Be it enacted by the People of the State of Illinois, 3 represented in the General Assembly: 4 Section 1. Legislative

Fully Insured Pension Plan

Fully Insured Pension Plan Marketing Guide There are approximately 23 million small businesses in the U.S.* *Small Business Administration: Small Business Trends (sba.gov) The Market for Fully Insured

Fully Insured Pension Plan Marketing Guide There are approximately 23 million small businesses in the U.S.* *Small Business Administration: Small Business Trends (sba.gov) The Market for Fully Insured

Employee Benefits. To provide centralized budgetary and financial control over employee fringe benefits paid by the County.

Mission To provide centralized budgetary and financial control over employee fringe benefits paid by the County. Focus Agency 89, Employee Benefits, is a set of consolidated accounts that provide budgetary

Mission To provide centralized budgetary and financial control over employee fringe benefits paid by the County. Focus Agency 89, Employee Benefits, is a set of consolidated accounts that provide budgetary

Adjusting for Underfunded Pension and Postretirement Liabilities

Business Valuation Insights Adjusting for Underfunded Pension and Postretirement Liabilities Christopher W. Peifer Fewer and fewer companies have pension liabilities recorded on their balance sheets. This

Business Valuation Insights Adjusting for Underfunded Pension and Postretirement Liabilities Christopher W. Peifer Fewer and fewer companies have pension liabilities recorded on their balance sheets. This