Your Guide to Proactive Foreclosure Avoidance STOP FORECLOSURE

|

|

|

- Leonard Ellis

- 8 years ago

- Views:

Transcription

1 Your Guide to Proactive Foreclosure Avoidance STOP FORECLOSURE Explains key elements of the foreclosure process with information essential to taking charge of your financial crisis today and in the future. Bob Ingols & Monica Contreras Keller Williams Realty Sacramento, California March 2010; Version 1 i

2 TABLE OF CONTENTS INTRODUCTION 1 SAVE YOUR HOME, SAVE YOUR CREDIT 1 WHAT IS FORECLOSURE? 2 CONSIDER YOUR OPTIONS 3 ALTERNATIVE ONE: STAY IN YOUR HOME 3 REFINANCE OPTION 4 FORBEARANCE OPTION 5 REINSTATEMENT OPTION OR REPAYMENT OPTION 5 FHA PARTIAL CLAIM OPTION 5 BANKRUPTCY, CHAPTER 13 OPTION 5 SUMMARY OF ALTERNATIVE ONE: STAY IN YOUR HOME 6 ALTERNATIVE TWO: LEAVE YOUR HOME AND MAKE A FRESH START 6 SHORT SALE OPTION 6 DEED IN LIEU OF FORECLOSURE OPTION 6 FORECLOSURE OPTION 7 BANKRUPTCY, CHAPTER 7 OPTION 8 SUMMARY OF ALTERNATIVE TWO: LEAVE YOUR HOME AND MAKE A FRESH START 8 THE FORECLOSURE TIMELINE DRIVES YOUR AVOIDANCE STRATEGIES 10 PROACTIVE STRATEGIES FOR STAYING IN YOUR HOME OR LETTING IT GO 13 OTHER CONSIDERATIONS 14 TAX CONSEQUENCES 14 DEFICIENCY JUDGMENT 14 PROMISSORY NOTE 14 PROACTIVE FORECLOSURE AVOIDANCE PROCESS 14 WEBSITE RESOURCES 15 APPENDIX 16 SOURCES 16 ii

3 INTRODUCTION Are you or someone you know finding it increasingly difficult to make the mortgage payments? You re not alone! Foreclosure of your home is devastating and stressful, both emotionally and financially, and should be avoided at all costs. There are steps you can take immediately to mitigate the situation. A Proactive Approach Is the Best Approach Nearly 10.7 million households had negative equity in their homes in the third quarter, 2009, according to First American Core Logic, a real estate information company based in Santa Ana, California. The First American report stated that home prices have plummeted so far that 5.3 million U.S. households are tied to mortgages that are at least 20% higher than their home s value. Economists from J.P. Morgan Chase & Company reported on November 23, 2009 that they didn t expect U.S. home prices to hit bottom until early 2011, citing the prospect of oversupply. You do have options to Stop Foreclosure and Save Your Home and/or Save Your Credit rating. Before you decide too quickly on Refinancing, a Loan Modification, or Selling Your Home, it s very important to learn the positives and negatives of these solutions. Even though time is of the essence, there are logical steps you have to take in order to act in the best interest of your particular financial situation. One solution does not fit all circumstances and expert guidance by someone familiar with all aspects of the Pre-foreclosure and Foreclosure Processes is highly recommended. We have developed a Your Guide to Proactive Foreclosure Avoidance to explain the key elements of the foreclosure process with your best interests as the top priority. The sooner you address your mortgage and home equity crisis the better your chances are of finding a solution that meets your needs. You ll learn information essential to taking charge of the financial challenge facing you and your family. SAVE YOUR HOME, SAVE YOUR CREDIT Most credit authorities advise that a foreclosure will significantly damage your credit and may prevent you from buying a home for three to seven years from the date of the foreclosure sale. Extenuating circumstances may reduce this time in a few cases. Home owners will most likely see a decrease to their credit score by going through foreclosure, giving their lender a deed-inlieu of foreclosure or working with their lender to achieve a short sale. Some sources indicate a lesser impact on the credit score for a short sale or deed-in-lieu of foreclosure. Effect of a Deed-in-Lieu of Foreclosure Fannie Mae estimates that a deed-in-lieu of foreclosure will prevent you from being eligible to purchase a property until four years from the date the deed-in-lieu was executed. 1

4 Effect of a Short Sale A preforeclosure sale or a short sale involves the sale of the property by the borrower to a third party for less than the amount owed to satisfy the delinquent mortgage, as agreed to by the lender, investor, and mortgage insurer. It will be a minimum of two years from the completion date of this sale before a consumer is eligible to purchase a property. Effect of a Bankruptcy A Chapter 7 bankruptcy may remain on your credit report up to 10 years and a Chapter 13 bankruptcy up to 7 years. A consumer may need to wait for four years after the dismissal date of a bankruptcy in order to obtain credit and purchase a property. Missing mortgage payments will immediately begin to reduce the credit score of a borrower. We strongly recommend that you verify the potential affect on your personal credit score by consulting with a credit counseling service. WHAT IS FORECLOSURE? Foreclosure is the legal process by which an owner's right to a property is terminated, usually due to default. This typically involves a forced sale of the property at public auction, with the proceeds being applied to the mortgage debt. The home is collateral for the mortgage loan and the act of foreclosure will result in the sale of your home to a new owner at a public auction, or a takeover of ownership by the mortgage holder. The loss of a home due to unexpected events such as unemployment, divorce or sickness can be financially and personally devastating. Maybe you haven't missed a house payment yet, but are afraid you might because of significant changes coming in your financial situation. Possibly your financial situation has already changed in a negative direction due to a mortgage payment increase, loss of job, forced job furlough, divorce, medical expenses, an increase in taxes or other reasons. Here are a few key indicators of trouble: You struggling to make your mortgage payment. Your credit card debt becoming unmanageable. You using your credit cards to buy groceries. It is becoming difficult to pay all your monthly bills on time. If it s becoming harder to make your house payment each month you may be facing foreclosure. The threat of foreclosure is serious. It poses a real threat to your financial well being that will not magically disappear. The foreclosure process can be like a runaway train on a clear track with no crossing stops ahead. Fortunately there are steps you can take to prevent foreclosure, slow down the foreclosure process or lessen the impact of losing your home if there is no other choice. Most homeowners financial situations are unique so it is important to consider all the possible Options and Strategies, and to have a proactive plan in order to make the best decision. It is highly recommended that you seek the advice of real estate, legal or tax professionals to help you during this period. 2

5 CONSIDER YOUR OPTIONS Alternative One: Stay in Your Home There are several options we can help you with in order for you to stay in your home. One option is a loan modification which may be your best solution. We ll show you how to approach this option so you are fully prepared to present your best position to your lender. In addition, refinancing may be an option to avoid foreclosure and poor credit. You may even be able to rent your home out and move to another dwelling in order to preserve the potential future equity appreciation in your present home Have you received a notice from your lender asking you to contact them? Don't ignore letters from your lender; contact your lender immediately. Foreclosure is expensive for lenders, mortgage insurers and investors. The U.S. Department of Housing and Urban Development (HUD) and the Federal Housing Authority (FHA), as well as private mortgage insurance companies and investors like Freddie Mac and Fannie Mae, now require lenders to work aggressively with borrowers who are facing money problems. There is a general notification and communication process most lenders use with borrowers that are falling behind in their monthly payments. Inherent in the process are options available to you to stay in your home. Don't ignore the problem and the danger signs The further behind you become the harder it will be to reinstate your loan, which consequently increases the likelihood that you will lose your house. Open and respond to all mail from your lender. The first notices you receive will offer good information about foreclosure prevention options that can help you weather financial problems. Future mailings may include important notices of pending legal action. Your failure to open the mail will not be an excuse to prevent the legal process from moving forward. First, contact your lender as soon as you realize that you have a problem. Second, contact a HUD-approved housing counselor. HUD funds free or very low cost housing counseling nationwide. Housing counselors can help you understand the law and your options, organize your finances and represent you in negotiations with your lender if you need this assistance. Visit the helpful HUD web site at Call for a HUD-approved loan counselor toll free at (800) Warning: Avoid scams and foreclosure prevention companies You don't need to pay fees for foreclosure prevention help; you could use that money to pay the mortgage instead. As of October 2009, it is illegal to require advance fees. Many for-profit companies will contact you promising to negotiate with your lender. While these may be legitimate businesses, they may want to charge you a hefty fee (often two or three month's 3

6 mortgage payments) for information and services your lender or a HUD approved housing counselor will provide for free. If any firm claims they can stop your foreclosure immediately if you sign a document appointing them to act on your behalf, you may well be signing over the title to your property and becoming a renter in your own home! Never sign a legal document without reading and understanding all the terms and getting professional advice from an attorney, a trusted real estate professional, or a HUD approved housing counselor. Beware of anyone who asks you to pay a fee in exchange for a counseling service or modification of a delinquent loan. Loan Modification Option Under some circumstances the lender will modify the terms of your loan so that you will have a new loan that covers back payments, and may even be at a new, lower, more affordable monthly mortgage payment. This requires some work on your part to submit a detailed application and supporting documentation, but will get you started on the right path to work directly with your lender for a fast decision. The Making Home Affordable Program The Federal Government s Making Home Affordable (MHA) Program gives homeowners with loans owned or guaranteed by Fannie Mae or Freddie Mac an opportunity to refinance or modify loans into more affordable monthly payments to help prevent avoidable foreclosures. Their consumer website provides homeowners with detailed information about these programs along with self-assessment tools and calculators to empower borrowers with the resources they need to determine whether they might be eligible for a modification or a refinance under this program. Also on this website is a very helpful list of Frequently Asked Questions (FAQs) from borrowers in similar circumstances. The MHA Program offers two different potential solutions for borrowers: (1) Refinancing mortgage loans through the Home Affordable Refinance Program (HARP) and (2) Modifying mortgage loans through the Home Affordable Modification Program (HAMP). The Streamlined Modification Program The Federal Government offers a Streamlined Modification Program (SMP) to borrowers to help prevent foreclosures. It is available to servicers and borrowers of Fannie Mae and Freddie Mac who work with numerous lenders and servicing companies in the HOPE NOW alliance to implement the SMP. Under the program borrowers who meet certain eligibility criteria and demonstrate financial hardship may be eligible for a loan modification that reduces their monthly mortgage payment. If approved, the borrower is allowed to establish a new monthly payment for a three-month trial period. Loan modification terms will take effect if the borrower makes the new payments during the trial period. The program is potentially available to borrowers who have missed at least three monthly payments on their existing mortgages. Refinance Option Lenders do not want your house. Lenders have options to help borrowers through difficult financial times. Be honest with your lender about your finances. If your income has decreased 4

7 but is coming back it may be high enough that you can afford your existing loan or a new loan. If there is some equity left in your house, and you have acceptable credit, you may be able to refinance with a new loan at a more favorable interest rate and lower your monthly payments significantly. You may work directly with your lender or seek the services of a consultant. Forbearance Option Another possibility is that the lender may grant a forbearance which is simply allowing the current loan to be idle for a period of time, say a few months, at which time you will start paying on your current loan again. The lender will ask the borrower to show the ability to begin payments at the specified future date. Reinstatement Option or Repayment Option Alternatively, the borrower may be allowed to make a lump sum payment of all past due amounts to bring the loan account current and thus reinstate the original loan. Another method lenders offer some borrowers is a repayment plan that allows a certain amount of time to catch up by combining past due and current payments on a schedule. FHA Partial Claim Option Your lender may agree to help you apply for an interest-free loan from HUD to cover the cost of bringing your mortgage current. HUD will request financial information regarding your ability to pay and if a loan is granted, will file a lien against your property. The loan would be paid off when you refinance or sell the property. This option applies to FHA loans but contact HUD for the latest information on types of loans they will cover. Rent the Property Option If your financial position is strong, then one way to potentially increase your future net worth is to rent out your existing home before falling behind on payments. Most economists believe that home values will rise again in time. While your credit is good you could buy a new primary home at today s bargain prices, and turn your existing home into rental income property. You will then be positioned to receive the potential appreciation on two properties. Bankruptcy, Chapter 13 Option In chapter 13 bankruptcy you file a plan showing how you will pay off some of your past-due and current debts over a period of a few years. The most important thing about a chapter 13 case is that it will allow you to keep valuable property, like your home or car, even if you are behind on payments or have equity not covered by your exemptions. Your payments on these secured debts will generally be your regular monthly payments plus some extra amount if you need to get caught up on past due expenses. You may consider chapter 13 if you have valuable property not covered by an exemption, like a home or car, but want to keep this property. If you are behind on secured loan payments a chapter 13 bankruptcy can allow you to make up these payments over time while keeping the home or car. This information is intended to be only general in nature; it is highly recommended that you seek the advice of an attorney. 5

8 Summary of Alternative One: Stay in Your Home Apply for a loan modification to a new loan Apply to refinance to a new loan Apply for a forbearance with the same loan Agree to a reinstatement or repayment plan Apply for a partial claim Rent the property to retain potential appreciation File for bankruptcy, Chapter 13 A Proactive Approach Is the Best Approach Alternative Two: Leave Your Home and Make a Fresh Start Short Sale Option A short sale may occur once a home is in pre-foreclosure or prior, but before the property goes to foreclosure. In a short sale, the lender accepts an offer from a third party buyer for less than the outstanding loan on the property and forgives the deficiency owed by the borrower. This arrangement may be appealing to lenders because it saves time and money by stopping the legal foreclosure process and by taking the property off the lender s books. Before approving a short sale lenders weigh several factors and require a lot of financial information from the borrower and other information from the listing agent. Every bank can be different, but there has to be a hardship such as a job loss or health problem that makes it difficult for the borrower to keep up with payments. H.R.3648, the Mortgage Forgiveness Debt Relief Act of 2007, provides relief to homeowners facing foreclosure from the phantom income realized from debt forgiveness or foreclosure. The benefit to the borrower of a short sale is that the credit report will show that the loan settled for less than full value as opposed to a foreclosure. Owners most interested in the short sale opportunity are those hoping to receive a smaller negative hit on their credit by avoiding foreclosure. Deed in Lieu of Foreclosure Option An alternative to a short sale or foreclosure to be considered by property owners is the possibility of deeding the encumbered property back to the lender, thus giving the lender a deed in lieu of foreclosure. A deed in lieu of foreclosure is a deed given by the trustor (the borrower) to the beneficiary (the lender) to stop the foreclosure process. By accepting a deed in lieu of foreclosure, the lender avoids the costs and delays of foreclosing. However, remember that: 1. Any junior liens are not extinguished (a foreclosure wipes out junior liens) 2. The borrower may later try to set the conveyance aside, and/or 3. The borrower's other creditors may argue that the conveyance was a fraudulent conveyance which jeopardizes their ability to satisfy their claims against the borrower. Lenders can protect themselves against hidden junior liens by obtaining an endorsement 6

9 to the beneficiary's title insurance policy that places title in the beneficiary free and clear of any junior liens. By giving a deed in lieu of foreclosure and thus stopping the foreclosure, the borrower may avoid any further injury to his/her credit and insulates himself/herself from any possible exposure to a deficiency judgment. If the deed in lieu is given to the lender early on, the borrower avoids having a notice of default recorded against his or her name. However, the borrower will be denied any opportunity to retain the excess proceeds, if there are any, following a trustee's sale. In a deed in lieu of foreclosure plan the borrower returns the deed on the property to the lender in exchange for a release of the security interest and a cancellation of the note. As in the case of foreclosures and short sales, the borrower may be able to claim relief under the Mortgage Forgiveness Debt Relief Act. Foreclosure Option In California there are two types of foreclosure with which a home owner might face. These are the judicial foreclosure and the trustee sale sometimes called the power of sale foreclosure. Most foreclosures by far are by trustee sale. Foreclosure by Trustee Sale In contrast to the judicial foreclosure, in a trustee sale there is no court filing. Instead the lender elects to accelerate the loan under the power of sale clause contained in the deed of trust and the property is sold at a trustee sale. In actual practice, when the borrower is approximately 45 to 60 days in default, the lender sends a letter advising that the loan is in foreclosure and that the lender is going to exercise the option to accelerate the loan. The borrower is also provided information about how to reinstate the loan. If the borrower does not cure the default, the lender then records a notice of default against the property. The soonest the actual foreclosure sale can occur once the notice of default is recorded is three months and twenty one days. If the property sells at foreclosure for more than the amount due plus costs of foreclosure, the excess proceeds are distributed to junior lien holders whose loans or liens were wiped out by the foreclosure and any remaining excess is returned to the property owner. Where the junior lien holder s security is wiped out by the foreclosure of the primary lender, the junior lien holder may choose to sue on the note under a breach of contract claim. While this was rarely done in the past, some lenders are now pursuing this course of action to recover the lost security on their loans. The recovery of a deficiency is not possible on a purchase money loan, including seller-carried financing, on any real property or loans on property consisting of 1-4 family units of owner occupied residential property. Recovery of the deficiency amount is possible, however, on a refinanced property loan (non purchase money) or on 1-4 family non-owner occupied residential property loans. The property owner is advised to consult an attorney if there are questions about deficiency judgments. Judicial Foreclosure Fewer than 5% of residential foreclosures in the state of California are judicial foreclosures. A judicial foreclosure is initiated by the lender filing a lawsuit against the defaulting borrower in 7

10 Superior Court. Upon sufficient proof at trial, the court enters judgment of foreclosure and orders the sale of the property. After the sale the lender files an application for fair value deficiency after which there is a hearing on the deficiency. Upon approval the court issues a fair value finding on the deficiency and enters a conventional money judgment called a deficiency judgment. A judicial foreclosure generally takes much longer than a trustee sale. Subsequent to the issuance of the judgment there is a time period during which the borrower can exercise his right of redemption and repurchase the property by paying the full amount of the defaulted loan. Bankruptcy, Chapter 7 Option Chapter 7 bankruptcy is another option that defaulting borrowers may sometimes consider. Generally, bankruptcy will be attractive where the borrower is in debt with no feasible way of recovering. The most common scenario is where the borrower is in default on a loan where the lender is seeking judicial foreclosure or where the lender is suing on a note where the underlying security has been wiped out by a senior creditor. Again, whenever a borrower is facing possible foreclosure it is wise to contact a bankruptcy attorney who is qualified to address all of the available options. Under the federal bankruptcy statute, a discharge is a release of the debtor from personal liability for certain specified types of debts. In other words, the debtor is no longer required by law to pay any debts that are discharged. The discharge operates as a permanent order directed to the creditors of the debtor that they refrain from taking any form of collection action on discharged debts, including legal action and communications with the debtor, such as telephone calls, letters, and personal contacts. Although a debtor is relieved of personal liability for all debts that are discharged, a valid lien (i.e., a charge upon specific property to secure payment of a debt) that has not been avoided (i.e., made unenforceable) in the bankruptcy case will remain after the bankruptcy case. Therefore, a secured creditor may enforce the lien to recover the property secured by the lien. Generally people file chapter 7 bankruptcy if they have a large amount of unsecured debt such as credit card debt or medical expenses that they are no longer able to pay. Often unemployment, unexpected medical expenses, or divorce prompt the cause the debtor to seek protection from creditors by filing chapter 7 bankruptcy. This information is intended to be only general in nature; it is highly recommended that you seek the advice of an attorney. Summary of Alternative Two: Leave Your Home and Make a Fresh Start Sell as a short sale Agree to a deed in lieu of foreclosure Let the foreclosure process proceed File for bankruptcy, chapter 7 There are significant differences in the consequences of implementing a loan modification, a short sale or a foreclosure (see Table 1 for an overview). These differences affect your ability to purchase property in the future. 8

11 Table 1: CONSEQUENCES OF A HOME LOAN DEFICIENCY Issue Loan Modification Short Sale Foreclosure Credit Report Type of notation depends on type of modification program (e.g., governmentsponsored), lender s policy, and consumer s credit profile*. Generally, noted as not paid as agreed or settle. But depends on lender s policy*. Noted as not paid as agreed *. Credit Score May drop your score but depends on several factors (see above). There is conflicting information on this point. Some authorities state there isn t any difference between a short sale and foreclosure and how it affects your FICO score. And it depends on the consumer s credit profile. Others claim a short sale adversely affects your score between points. Whereas a foreclosure will ding your score upwards of 280 points. Home Purchase N/A Fannie Mae: 2 years from completion date. FHA: 3 years from completed sale for borrowers in default at time of sale. Immediately for borrower s current for the preceding 12 months. Lenders may make exceptions for extenuating circumstances (e.g., death, illness, etc.) or have their own requirements. Fannie Mae: 5 7 years from completed sale and 3 years with extenuating circumstances (e.g. divorce, death, job loss, etc.; documentation required). FHA: 3 years from completed sale. *Nothing precludes the consumers from negotiating with the lender on how they report the event to the credit bureaus. Any derogatory/negative items stay on the consumer s credit file for 7 years. 9

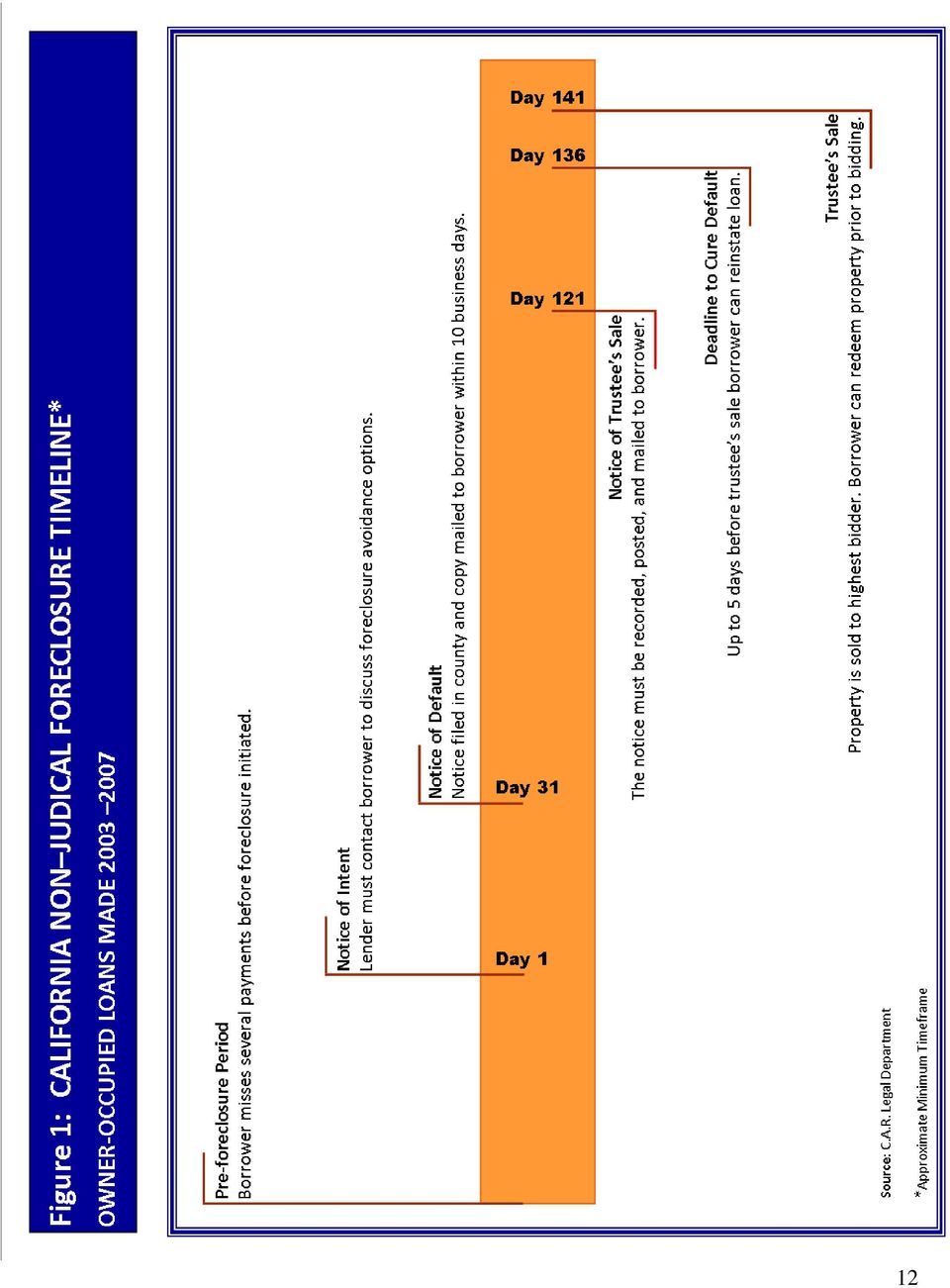

12 THE FORECLOSURE TIMELINE DRIVES YOUR AVOIDANCE STRATEGIES A lender may initiate the foreclosure process when a borrower defaults on a loan, such as by missing one or more mortgage payments. A slight delay may not justify acceleration and foreclosure by the lender. Hence, in practice, lenders generally wait a few months after a missed payment before starting the foreclosure process. The times will vary from lender to lender because of their workloads and policies, but a generalized timeline you can plan with follows: Step 1: Initial Contact from Lender For most loans the lender will contact the borrower in one or more ways to initiate the foreclosure process. The contact may by phone, by mail or in person to assess the borrower s financial situation and explore options for avoiding foreclosure. Step 2: Filing of a Notice of Default (NOD) For owner-occupied loans the lender may file a notice of default 30 days after contacting the borrower to explore options for avoiding foreclosure. After the second missed monthly payment your lender is likely to begin calling you to discuss why you have not made your payments. After the third payment is missed, you will receive a letter from your lender stating the amount you are delinquent, and that you have 30 days to bring your mortgage current. This is called a "Demand Letter" or "Notice to Accelerate. If you do not pay the specified amount or make some type of arrangements by the given date, the lender may begin foreclosure proceedings. After the fourth month missed payment you are nearing the end of time allowed in your demand or notice to accelerate letter. After 30 days, if you have not paid the full amount or worked out arrangements, you may be referred to your lender's attorneys. You will most likely incur all attorney fees as part of your delinquency. A housing counselor can still help you. Step 3: Filing of Notice of Sheriff s or Trustee s Sale Three months after the filing of the notice of default, the lender, through an attorney, may record a notice of trustee s sale setting forth the date, time and place of the upcoming trustee s sale. This is the actual day of foreclosure. Because of the gravity of a notice of trustee s sale, it must be widely disseminated. The notice of trustee s sale must be recorded, posted and mailed to the borrower, and to others, as well as published once a week for three consecutive weeks in a newspaper of general circulation. It often is posted on the front door of the property. The time between the demand or notice to accelerate letter and the actual sale varies by state. In some states it can be as soon as two to three months. This is not necessarily the move-out date. You have until the date of sale to make arrangements with your lender or to pay the total amount owed, including attorney fees. 10

13 Step 4: Deadline to Cure Default Up to five business days before the trustee s sale, the borrower may reinstate the loan by curing the default or paying the missed payments plus allowable costs. After the reinstatement period expires, the borrower still has the right to redeem the property by paying the entire debt, plus interest and costs (not just the arrearage), before the bidding begins at the trustee s sale. Step 5: The Trustee s Sale Although California law allows a trustee s sale to take place 20 days after the posting of the notice of trustee s sale, lenders customarily wait at least 31 days instead to help protect against federal tax liens. At the trustee s sale, the property is sold through a public auction to the highest bidder. Title is transferred to the successful bidder by trustee s deed. Even after the sale you need to check with your lender to make sure they don t come after you with a deficiency judgment. Step 6: Foreclosed New Owner The actual public auction may result in an immediate purchase by a private party, a corporation or some other organization. If the property fails to sell at the auction it becomes the property of your lender and is recorded as such with the county. Once title has transferred to the lender it is commonly called Real Estate Owned or an REO property. The new owner will make arrangements for the departure of anyone still occupying the property. The non-judicial timeline shows the approximate times of key events as the foreclosure process moves forward from the borrower s missed payments to a possible trustee sale which will render the property foreclosed. Although the legal proceedings move forward at a steady pace, the borrower can take proactive steps to change, delay or resolve the process. See Figure 1: California Non-Judicial Foreclosure Timeline. This shows the progression of legal activity through the foreclosure process. This applies to a large majority of cases in California. The authors are not attorneys or tax professionals and do not intend any information in this guide to give legal or tax advice. It is highly recommended that you seek the advice of real estate, legal or tax professionals to help you during this period. 11

14 12

15 PROACTIVE STRATEGIES FOR STAYING IN YOUR HOME OR LETTING IT GO Now that you understand the entire foreclosure process and the possible options you have available, it s time to determine your course of action. Our experience shows that it is much better for you to take decisive steps that will benefit you most, and not wait for events to happen. If you allow your bank, the foreclosure timeline or other outside forces to have their way you may end up much worse off. A Proactive Approach Is the Best Approach Here is a summary of the decision-making process you can move forward with instead of being stuck in a state of financial paralysis that a foreclosure can cause. Step 1. First determine if you have the financial assets and income to refinance, repay or modify your loan. Fill out a financial statement to determine your current and projected income and expenses; or a profit and loss statement if you are an independent business person. Also produce a personal balance sheet to determine your net worth. Step 2. If you believe that you may be able to afford to Save Your Home, you can decide if you want to live there or rent it out as an investment and move to a new property. You may do much of the work yourself by negotiating with your lender to determine what loan terms you can afford and commit to. You may choose to work with a consultant to help you through the process. Or you may decide to invest in a reputable loan modification negotiator. Step 3. If you determine that there is no way any of the Save Your Home options are affordable with your current and projected income, then you should Leave Your Home and Make a Fresh Start by immediately choosing the best option that will have the least negative impact on your ability to purchase and hold assets in the future. There are pros and cons for each of these paths that depend on your personal situation. There is not an automatic answer that can be covered in a short guide such as this one. Again, you may choose to work with a consultant to help you through the process. But never just do absolutely nothing as that will likely cause you the most financial pain, physical stress and emotional discomfort. In summary, even with numerous options possible, you have only two strategic directions to choose from: Stay In Your Home or Leave Your Home to Make a Fresh Start. To implement either strategy you can do a lot of the work yourself and will benefit the most by deciding to make it a financial business decision where you actively drive the process, and rise above the emotion and trauma of the financial predicament. Expert consultants are available to help every step of the way if needed. 13

16 OTHER CONSIDERATIONS Tax Consequences Depending on the option you choose there may be tax consequences. Therefore, you should consult with a tax preparation professional to weigh the various outcomes against your ability to pay income taxes at both the federal and state level. Do not rely on friends, guesses or on-line information sources. Your situation is unique and deserves an objective, professional analysis. There are different tax ramifications for personal residences, second homes and investment property. A qualified tax professional will be able to show you the pros and cons of a short sale, foreclosure or bankruptcy. The authors are not attorneys or tax professional and do not intend any information in this guide to give legal or tax advice. Deficiency Judgment Upon foreclosure your lender may seek a deficiency judgment against you and attempt to collect any amount they do not recuperate at the trustee sale. Promissory Note Some lenders may approve a short sale but still request a promissory note for some amount, especially if they believe you have the assets and earning power to pay over time. Reminder: we recommend you seek tax advice from a qualified tax professional. PROACTIVE FORECLOSURE AVOIDANCE PROCESS There is not one solution that fits everyone so we offer our foreclosure services and real estate experience as an option to consider. We believe that you will make the best decision by gathering information from trusted, licensed professionals. Each professional may have a contribution to make to your unique financial situation. Consulting with a licensed REALTOR is a good place to start. We also have access to financial advisors, accountants and attorneys if you need such help. Caution: seeking answers from family and friends can be misleading and cost you valuable time and money. Always validate your information sources. An expert consultant may be able to save you both time and money by providing the materials and decision making process your particular situation warrants. You may contact us directly for a free, private consultation session at our Sacramento office where we can help you decide on the best actions to take. You will be under no obligation to use our services. You will leave filled with new knowledge that could help meet your financial challenges. We call our solutions-based approach the Proactive Foreclosure Avoidance Process. This is a hands-on, teamwork-oriented, consulting methodology that we implement in person with our clients. We develop a personalized, step-by-step plan, using our own unique, easy-to-follow materials that enable us to implement your plan together. 14

17 WEBSITE RESOURCES 1. Making Home Affordable: A government consumer website that provides information on the Making Home Affordable program and tools to help borrowers determine their eligibility for a modification or refinance. 2. Fannie Mae: Fannie Mae is a government-sponsored enterprise (GSE) that deals in the U.S. secondary market. It works directly with mortgage banks, brokers, and other primary mortgage partners. The website has a wealth of information for investors, business partners, homebuyers, and distressed homeowners. For distressed homeowners it s a good place to find out if your mortgage is owned by Fannie Mae and find information about your options. 3. Freddie Mac: Freddie Mac is another GSE and their website provides similar resources as Fannie Mae to distressed homeowners. 4. U. S. Dept. of Housing and Urban Development (HUD) Portal: A redesigned website to facilitate usability. The website provides information on avoiding foreclosure, the HOPE for Homeowners (H4H), finding a HUD-approved counseling center, and on Federal Housing Administration s (FHA) home buying programs, 5. HOPE NOW: Is an alliance between counselors, mortgage companies, investors, and other mortgage market participants. The organization s goal is to maximize outreach efforts and provide a cohesive game plan for distressed homeowners. The website provides similar information and links and the sites mentioned above. 6. Service member s Civil Relief Act: Formerly known as the Soldiers' and Sailors' Civil Relief Act of 1940 (SSCRA), is a federal law that gives all military members important rights as they enter active duty. It covers such issues as rental agreements, security deposits, prepaid rent, eviction, installment contracts, credit card interest rates, mortgage interest rates, mortgage foreclosure, civil judicial proceedings, and income tax payments. 7. Help for veterans. See 8. Help for seniors. See 15

18 APPENDIX Sources California Association of Realtors. Credit After Foreclosure, Bankruptcy, or Short Sale, by the C.A.R Legal Department, 2009 California Department of Real Estate. HUD. FNMA Announcement 08-16, Money Alert. 16

19 OWNERSHIP AND DISTRIBUTION INFORMATION The entire content of this document in its present form is the sole property of the authors. Making copies for personal use is authorized and encouraged. It is forbidden to reproduce this Guide for sale or distribution, or to use it for any other purpose or under any other name. This Guide is intended as a general purpose guide to the real estate topics contained herein, specifically related to real estate and the issues surrounding foreclosure. It does not purport to give financial, legal or accounting advice; readers are advised to contact an appropriate licensed professional with questions regarding specific issues and potential problems. About The Authors We are real estate professionals licensed by the California Department of Real Estate. We provide consulting services to help homeowners stay in their home or go through the foreclosure process in the best way possible. We do not charge up-front fees. For years we have represented many clients in the process of buying, selling and investing in California real estate. Bob Ingols, DRE # Mr. Ingols has over 25 years experience in marketing consulting, ownership of real estate companies, technology brand building, corporate communications and community service. He is currently a broker-associate at Keller Williams Realty, the third largest and fastest growing real estate company in the U.S. Ingols services include negotiating contracts for short sales, bankowned properties, 1031 exchanges and conventional sales or purchases of residential and income property. Ingols also owns and operates Apple One Property Management. Monica Contreras, DRE # Ms. Contreras combined professional experience includes over 30 years in the fields of accounting, business analysis and information technology. Her corporate business acumen, tech savvy and sharp negotiation skills have helped her real estate clients successfully achieve their goals. She is currently an associate at Keller Williams Realty where she has implemented a five-step process to facilitate clients real estate transactions Be Proactive, Call Immediately Bob Ingols bobingols@yahoo.com Keller Williams Realty 4180 Truxel Road, Suite 150 Sacramento, CA

How To Avoid Foreclosure

For most families, a home is a place to live and raise children; it s a plan for the future, and also a source of pride. The Town of Davie promotes home preservation. Your home is not only a significant

For most families, a home is a place to live and raise children; it s a plan for the future, and also a source of pride. The Town of Davie promotes home preservation. Your home is not only a significant

OPTIONS IN FORECLOSURE

Section II: KEEPING YOUR HOME OPTIONS IN FORECLOSURE Deciding whether or not to keep your home is something that only you, the homeowner, can determine. The best housing counselors will ask what you d

Section II: KEEPING YOUR HOME OPTIONS IN FORECLOSURE Deciding whether or not to keep your home is something that only you, the homeowner, can determine. The best housing counselors will ask what you d

Foreclosure Process Timeline

Foreclosure A legal process spanning 150-415+ days, by which a creditor (bank, mortgage company, etc..) takes ownership of a property to satisfy a debt (mortgage, second mortgage or home equity loan).

Foreclosure A legal process spanning 150-415+ days, by which a creditor (bank, mortgage company, etc..) takes ownership of a property to satisfy a debt (mortgage, second mortgage or home equity loan).

FORECLOSURE. I don t think I can make my mortgage payments but I don t want to go through a foreclosure. What are some of my options?

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy. This means that if you don t pay, the creditor can foreclose upon (or take

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy. This means that if you don t pay, the creditor can foreclose upon (or take

Handling Default and Foreclosure

Handling Default and Foreclosure Delinquency Vs. Default Delinquency = less than 3 payments behind. A collections account. Only late fees accrue Default= more than 3 payments behind. Mortgage automatically

Handling Default and Foreclosure Delinquency Vs. Default Delinquency = less than 3 payments behind. A collections account. Only late fees accrue Default= more than 3 payments behind. Mortgage automatically

FOR SALE. Sheeley Moving Co. AVOIDING FORECLOSURE & FORECLOSURE SCAMS

FAIR HOUSING UNIVERSITY FOR SALE Sheeley Moving Co. AVOIDING FORECLOSURE & FORECLOSURE SCAMS WHAT IS FORECLOSURE When a lender takes possession of a house from a homeowner who has not met the mortgage

FAIR HOUSING UNIVERSITY FOR SALE Sheeley Moving Co. AVOIDING FORECLOSURE & FORECLOSURE SCAMS WHAT IS FORECLOSURE When a lender takes possession of a house from a homeowner who has not met the mortgage

Glossary of Foreclosure Fairness Mediation Terminology

Glossary of Foreclosure Fairness Mediation Terminology Adjustable-Rate Mortgage (ARM) Mortgage repaid at the rate of interest that increases or decreases over the life of the loan based on market conditions.

Glossary of Foreclosure Fairness Mediation Terminology Adjustable-Rate Mortgage (ARM) Mortgage repaid at the rate of interest that increases or decreases over the life of the loan based on market conditions.

Short Sale Seller Advisory

Short Sale Seller Advisory Short Sale Seller Advisory Recent economic challenges have resulted in many homeowners needing to sell their home but owing more on their home than the home is worth. This advisory

Short Sale Seller Advisory Short Sale Seller Advisory Recent economic challenges have resulted in many homeowners needing to sell their home but owing more on their home than the home is worth. This advisory

TEN LOOPHOLES THAT CAN STOP FORCLOSURE FAST

TEN LOOPHOLES THAT CAN STOP FORCLOSURE FAST Copyright Notice All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means electronic or mechanical. Any

TEN LOOPHOLES THAT CAN STOP FORCLOSURE FAST Copyright Notice All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means electronic or mechanical. Any

To help you better understand the foreclosure process, these definitions are presented in a logical order, rather than alphabetical order.

FORECLOSURE GLOSSARY NOTICE: This glossary of legal words and phrases related to foreclosure is provided to you by the Clermont County Common Pleas Court to help you better understand your legal problem

FORECLOSURE GLOSSARY NOTICE: This glossary of legal words and phrases related to foreclosure is provided to you by the Clermont County Common Pleas Court to help you better understand your legal problem

PATHS OF A FORECLOSURE IN NEW YORK STATE

PATHS OF A FORECLOSURE IN NEW YORK STATE BORROWER DELINQUENT 2-3 months late with mortgage payments 90-DAY PRE-FORECLOSURE NOTICE Lender sends notices, bills, letters to borrower stating that he/she is

PATHS OF A FORECLOSURE IN NEW YORK STATE BORROWER DELINQUENT 2-3 months late with mortgage payments 90-DAY PRE-FORECLOSURE NOTICE Lender sends notices, bills, letters to borrower stating that he/she is

H O W T O A V O I D F O R E C L O S U R E F O R E C L O S U R E

U.S. Department of Housing and Urban Development H O W T O A V O I D F O R E C L O S U R E F O R E C L O S U R E This booklet explains how property owners can avoid losing their homes because of delinquent

U.S. Department of Housing and Urban Development H O W T O A V O I D F O R E C L O S U R E F O R E C L O S U R E This booklet explains how property owners can avoid losing their homes because of delinquent

Central Mortgage Company

Central Mortgage Company Dear Borrower Are you struggling with your mortgage payment? We are concerned about your missed or potentially missed mortgage payment and want you to be aware of assistance available

Central Mortgage Company Dear Borrower Are you struggling with your mortgage payment? We are concerned about your missed or potentially missed mortgage payment and want you to be aware of assistance available

How to Stop and Avoid Foreclosure in Today's Market

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

T E X A S Y O U N G L A W Y E R S A S S O C I A T I O N A N D T H E S T A T E B A R O F T E X A S FA CING

T E X A S Y O U N G L A W Y E R S A S S O C I A T I O N A N D T H E S T A T E B A R O F T E X A S FA CING F ORECLOSURE FACING F O RECLOSURE "Facing Foreclosure" has been prepared as a public service by

T E X A S Y O U N G L A W Y E R S A S S O C I A T I O N A N D T H E S T A T E B A R O F T E X A S FA CING F ORECLOSURE FACING F O RECLOSURE "Facing Foreclosure" has been prepared as a public service by

PATHS OF A FORECLOSURE IN NEW YORK STATE

PATHS OF A FORECLOSURE IN NEW YORK STATE BORROWER DELINQUENT 2-3 months late with mortgage payments Lender sends notices, bills, letters to borrower stating that he/she is delinquent Borrower has multiple

PATHS OF A FORECLOSURE IN NEW YORK STATE BORROWER DELINQUENT 2-3 months late with mortgage payments Lender sends notices, bills, letters to borrower stating that he/she is delinquent Borrower has multiple

The 8 Fastest Ways to STOP FORECLOSURE in 48 Hours or Less

The 8 Fastest Ways to STOP FORECLOSURE in 48 Hours or Less Copyright Notice All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means electronic or mechanical.

The 8 Fastest Ways to STOP FORECLOSURE in 48 Hours or Less Copyright Notice All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means electronic or mechanical.

Foreclosure Overview

Foreclosure Overview Foreclosure is the legal action that your financial institution can use to take back your home when you miss your monthly mortgage payments. When this happens, you lose your house,

Foreclosure Overview Foreclosure is the legal action that your financial institution can use to take back your home when you miss your monthly mortgage payments. When this happens, you lose your house,

HOW TO AVOID FORECLOSURE

U.S. Department of Housing and Urban Development HOW TO AVOID FORECLOSURE This booklet explains how property owners can avoid losing their homes because of delinquent payments. Este folleto explica a los

U.S. Department of Housing and Urban Development HOW TO AVOID FORECLOSURE This booklet explains how property owners can avoid losing their homes because of delinquent payments. Este folleto explica a los

FTC FACTS for Consumers

ftc.gov FEDERAL TRADE COMMISSION FOR THE CONSUMER 1-877-FTC-HELP FTC FACTS for Consumers Mortgage Payments Sending You Reeling? Here s What to Do T he possibility of losing your home because you can t

ftc.gov FEDERAL TRADE COMMISSION FOR THE CONSUMER 1-877-FTC-HELP FTC FACTS for Consumers Mortgage Payments Sending You Reeling? Here s What to Do T he possibility of losing your home because you can t

HOME PRESERVATION BASICS

HOME PRESERVATION BASICS - Know what to do and when to do it The current economic crisis has greatly affected the housing industry, and our local community is no exception. This has forced different households

HOME PRESERVATION BASICS - Know what to do and when to do it The current economic crisis has greatly affected the housing industry, and our local community is no exception. This has forced different households

F.A.C.T. Starter Kit. Foreclosure Avoidance Comprehensive Training. COPYRIGHT 2009 Will Weaver

F.A.C.T. Foreclosure Avoidance Comprehensive Training Starter Kit COPYRIGHT 2009 Will Weaver Foreclosure Prevention Law Public Acts 29 31 of 2009 Requires lenders to send a default notice to borrowers;

F.A.C.T. Foreclosure Avoidance Comprehensive Training Starter Kit COPYRIGHT 2009 Will Weaver Foreclosure Prevention Law Public Acts 29 31 of 2009 Requires lenders to send a default notice to borrowers;

Homeownership Preservation Toolkit

Homeownership Preservation Toolkit A guide to understanding and avoiding foreclosure Sponsored and Endorsed by Loveland Berthoud Association of REALTORS CONSUMER CREDIT COUNSELING SERVICE OF NORTHERN COLORADO

Homeownership Preservation Toolkit A guide to understanding and avoiding foreclosure Sponsored and Endorsed by Loveland Berthoud Association of REALTORS CONSUMER CREDIT COUNSELING SERVICE OF NORTHERN COLORADO

AVOID FORECLOSURE HOW TO A CONSUMER GUIDE. Open mail from your mortgage company. Can you afford your home? Contact your mortgage company

HOW TO AVOID FORECLOSURE A CONSUMER GUIDE Open mail from your mortgage company Can you afford your home? Contact your mortgage company Keeping or not keeping your home What happens if you do not contact

HOW TO AVOID FORECLOSURE A CONSUMER GUIDE Open mail from your mortgage company Can you afford your home? Contact your mortgage company Keeping or not keeping your home What happens if you do not contact

FTC FACTS for Consumers

ftc.gov FEDERAL TRADE COMMISSION FOR THE CONSUMER 1-877-FTC-HELP FTC FACTS for Consumers Mortgage Payments Sending You Reeling? Here s What to Do T he possibility of losing your home because you can t

ftc.gov FEDERAL TRADE COMMISSION FOR THE CONSUMER 1-877-FTC-HELP FTC FACTS for Consumers Mortgage Payments Sending You Reeling? Here s What to Do T he possibility of losing your home because you can t

How To Prevent Or End Foreclosure In Canada And Keep Your Home

How To Prevent Or End Foreclosure In Canada And Keep Your Home 2012 Don t Lose Your Home, dontloseyourhome.ca How To Prevent Or End Foreclosure In Canada And Keep Your Home 2012 Don t Lose Your Home, dontloseyourhome.ca

How To Prevent Or End Foreclosure In Canada And Keep Your Home 2012 Don t Lose Your Home, dontloseyourhome.ca How To Prevent Or End Foreclosure In Canada And Keep Your Home 2012 Don t Lose Your Home, dontloseyourhome.ca

PATHS OF A FORECLOSURE IN NEW YORK STATE

PATHS OF A FORECLOSURE IN NEW YORK STATE BORROWER DELINQUENT 2-3 months late with mortgage payments if S/P or N/T 90-DAY PRE-FORECLOSURE NOTICE* for all subprime and non-traditional loans (as defined by

PATHS OF A FORECLOSURE IN NEW YORK STATE BORROWER DELINQUENT 2-3 months late with mortgage payments if S/P or N/T 90-DAY PRE-FORECLOSURE NOTICE* for all subprime and non-traditional loans (as defined by

AVOID FORECLOSURE HOW TO A CONSUMER GUIDE. Open mail from your mortgage company. Can you afford your home? Contact your mortgage company

HOW TO AVOID FORECLOSURE A CONSUMER GUIDE Open mail from your mortgage company Can you afford your home? Contact your mortgage company Keeping or not keeping your home What happens if you do not contact

HOW TO AVOID FORECLOSURE A CONSUMER GUIDE Open mail from your mortgage company Can you afford your home? Contact your mortgage company Keeping or not keeping your home What happens if you do not contact

What to Do When You Can t Pay Your Mortgage

What to Do When You Can t Pay Your Mortgage Marti Kilby, REALTOR Broker/Owner Steele Group Realty Distressed Property Consultant CA DRE License #01474222 Copyright 2013 Steele Group, Inc. Introduction

What to Do When You Can t Pay Your Mortgage Marti Kilby, REALTOR Broker/Owner Steele Group Realty Distressed Property Consultant CA DRE License #01474222 Copyright 2013 Steele Group, Inc. Introduction

Home Mortgage Foreclosures in Maine

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

Q: Will I have to pay federal taxes on the money my lender loses in the short sale?

Q: What is a Short Sale? Answer: In a short sale, the lender agrees to settle the debt owed on the property for less than the full amount. Settled means that the lender is writing off the debt (which is

Q: What is a Short Sale? Answer: In a short sale, the lender agrees to settle the debt owed on the property for less than the full amount. Settled means that the lender is writing off the debt (which is

Avoid a Foreclosure Notebook

Avoid a Foreclosure Notebook A foreclosure is a catastrophic event for any property owner and has serious legal, credit and tax implications. Working with homeowners on the verge of foreclosure or in the

Avoid a Foreclosure Notebook A foreclosure is a catastrophic event for any property owner and has serious legal, credit and tax implications. Working with homeowners on the verge of foreclosure or in the

LEARN ABOUT YOUR RIGHTS AND OPTIONS IN A FORECLOSURE

Helpful Agencies Here are some agencies which may lead you to lawyers who can help you: Lake County Bar Association 7 North County Street Waukegan, IL 60085 847-244-3140 www.lakebar.org Prairie State Legal

Helpful Agencies Here are some agencies which may lead you to lawyers who can help you: Lake County Bar Association 7 North County Street Waukegan, IL 60085 847-244-3140 www.lakebar.org Prairie State Legal

An Overview of Foreclosure

An Overview of Foreclosure While the rising number of foreclosures is an alarming national trend, the real hardship is for any individual or family who knows the threat of foreclosure firsthand. Unfortunately,

An Overview of Foreclosure While the rising number of foreclosures is an alarming national trend, the real hardship is for any individual or family who knows the threat of foreclosure firsthand. Unfortunately,

Common Mortgage and Foreclosure Terms

H ELP FOR N EW Y ORK S TATE H OMEOWNERS C ONCERNED A BOUT F ORECLOSURE Common Mortgage and Foreclosure Terms Talking about mortgages can feel like speaking a foreign language and is even more confusing

H ELP FOR N EW Y ORK S TATE H OMEOWNERS C ONCERNED A BOUT F ORECLOSURE Common Mortgage and Foreclosure Terms Talking about mortgages can feel like speaking a foreign language and is even more confusing

How to Avoid Foreclosure

How to Avoid Foreclosure M ost lenders do not want to foreclose. The process costs them money and they often sell the properties at less than the amount of the mortgage. Plus, lenders have some legal requirements

How to Avoid Foreclosure M ost lenders do not want to foreclose. The process costs them money and they often sell the properties at less than the amount of the mortgage. Plus, lenders have some legal requirements

Foreclosure Prevention Guide

Foreclosure Prevention Guide 8 Ways to Stop Your Foreclosure in Today s Challenging Economy About Foreclosure Foreclosure begins when a Homeowner is unable to make their mortgage payments on the scheduled

Foreclosure Prevention Guide 8 Ways to Stop Your Foreclosure in Today s Challenging Economy About Foreclosure Foreclosure begins when a Homeowner is unable to make their mortgage payments on the scheduled

Steps you can take to protect your home and your credit

Steps you can take to protect your home and your credit Oregon Division of Finance and Corporate Securities Our mission To encourage a wide range of financial services, products, and information for Oregonians,

Steps you can take to protect your home and your credit Oregon Division of Finance and Corporate Securities Our mission To encourage a wide range of financial services, products, and information for Oregonians,

Foreclosure Options. Know Your Rights! Your Trusted Real Estate Resource

Foreclosure Options Know Your Rights! Kirk Russell Managing Broker John L. Scott Firm Kirkrussell@johnlscott.com 206.390.5640 Your Trusted Real Estate Resource If you re listed with a license Realtor,

Foreclosure Options Know Your Rights! Kirk Russell Managing Broker John L. Scott Firm Kirkrussell@johnlscott.com 206.390.5640 Your Trusted Real Estate Resource If you re listed with a license Realtor,

Avoid Foreclosure. How to Help Yourself (or someone you know) A Step-By-Step Consumer Self-Help Kit. Plus: How to Spot & Report Loan Scams!

A Step-By-Step Consumer Self-Help Kit. Plus: How to Spot & Report Loan Scams!") How to Help Yourself (or someone you know) Plus: How to Spot & Report Loan Scams! Avoid Foreclosure A Step-By-Step Consumer Self-Help Kit Open mail from your mortgage company Can you afford your home?

How to Help Yourself (or someone you know) Plus: How to Spot & Report Loan Scams! Avoid Foreclosure A Step-By-Step Consumer Self-Help Kit Open mail from your mortgage company Can you afford your home?

Step-by-step process to apply for a loan modification with your lender/servicer

Step-by-step process to apply for a loan modification with your lender/servicer Step 1: Determine your eligibility status before contacting your lender You must have a steady income and a positive budget

Step-by-step process to apply for a loan modification with your lender/servicer Step 1: Determine your eligibility status before contacting your lender You must have a steady income and a positive budget

Do You HAFA? The HAFA Short Sale Program under Making Home Affordable 2

Table of Contents Do You HAFA? The HAFA Short Sale Program under Making Home Affordable 2 INTRODUCTION 2 Overview: Making Home Affordable ( MHA ) 2 HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM ( HAFA

Table of Contents Do You HAFA? The HAFA Short Sale Program under Making Home Affordable 2 INTRODUCTION 2 Overview: Making Home Affordable ( MHA ) 2 HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM ( HAFA

Barbara W. Griest Trident Land Transfer Company

Barbara W. Griest Trident Land Transfer Company 1 Why learn about Short Sales & Foreclosures? Excellent opportunity to grow your real estate business! Changes in the Real Estate Market Declining Markets

Barbara W. Griest Trident Land Transfer Company 1 Why learn about Short Sales & Foreclosures? Excellent opportunity to grow your real estate business! Changes in the Real Estate Market Declining Markets

Foreclosure Rescue. You Have Options! Inside: Powerful Strategies to Avoid Foreclosure. Are You at Risk of Losing Your Home in Foreclosure?

inside >>> The Foreclosure Process Your Options: - Negotiate a Loan Modification - Work out a Forbearance Plan - Obtain A Deed in Lieu of Foreclosure - Refinance Your House - File for Bankruptcy - Sell

inside >>> The Foreclosure Process Your Options: - Negotiate a Loan Modification - Work out a Forbearance Plan - Obtain A Deed in Lieu of Foreclosure - Refinance Your House - File for Bankruptcy - Sell

14 Options Every Home Owner Must Know When Faced With Foreclosure. By: Scott MacDonald

14 Options Every Home Owner Must Know When Faced With Foreclosure By: Scott MacDonald Foreclosure is affecting millions of Americans today. It can be a very frightening time for many families who do not

14 Options Every Home Owner Must Know When Faced With Foreclosure By: Scott MacDonald Foreclosure is affecting millions of Americans today. It can be a very frightening time for many families who do not

MORTGAGE TERMS. Assignment of Mortgage A document used to transfer ownership of a mortgage from one party to another.

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

8 Ways to Avoid or Stop Foreclosure...

Free Special Report 8 Ways to Avoid or Stop Foreclosure... Dear Homeowner, If you are headed toward foreclosure, or are already in foreclosure, you need to know the rights and options available to you

Free Special Report 8 Ways to Avoid or Stop Foreclosure... Dear Homeowner, If you are headed toward foreclosure, or are already in foreclosure, you need to know the rights and options available to you

How to Stop and Avoid Foreclosure in Today's Market

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

Early Delinquency Intervention: Saving Your Home From Foreclosure

Early Delinquency Intervention: Saving Your Home From Foreclosure There are many circumstances in a homeowner s life that could result in missed mortgage payments: unexpected expenses, loss of overtime,

Early Delinquency Intervention: Saving Your Home From Foreclosure There are many circumstances in a homeowner s life that could result in missed mortgage payments: unexpected expenses, loss of overtime,

How to Stop and Avoid Foreclosure in Today's Market

Solutions Home Buyers, Inc. 800-478-9213 ext. 700 SolutionsHomeBuyersFL.com How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company

Solutions Home Buyers, Inc. 800-478-9213 ext. 700 SolutionsHomeBuyersFL.com How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company

I m behind in my mortgage payments, what should I do?

FORECLOSURES This handout was prepared by Legal Services of Greater Miami, Inc.(LSGMI) with support from the Institute for Foreclosure Legal Assistance. LSGMI represents homeowners in foreclosure and homeowners

FORECLOSURES This handout was prepared by Legal Services of Greater Miami, Inc.(LSGMI) with support from the Institute for Foreclosure Legal Assistance. LSGMI represents homeowners in foreclosure and homeowners

State by State Foreclosure Laws

State by State Foreclosure Laws Alabama Foreclosure Laws 49-74 21 365 Trustee Comments: Judicial Foreclosures are not common Alabama foreclosures occur both in court and out-of-court. The typical foreclosure

State by State Foreclosure Laws Alabama Foreclosure Laws 49-74 21 365 Trustee Comments: Judicial Foreclosures are not common Alabama foreclosures occur both in court and out-of-court. The typical foreclosure

Guide. Completing the Mortgage Assistance Application

Guide Completing the Mortgage Assistance Application Getting Started PNC Mortgage Assistance Application Early communication with PNC is very important to ensure your assistance options are not limited.

Guide Completing the Mortgage Assistance Application Getting Started PNC Mortgage Assistance Application Early communication with PNC is very important to ensure your assistance options are not limited.

Information on Avoiding Foreclosure

Whitney Bank offers and provides financial products and services through its locations in Louisiana and Texas as "Whitney Bank" and as "Hancock Bank" in Mississippi, Alabama and Florida. Information on

Whitney Bank offers and provides financial products and services through its locations in Louisiana and Texas as "Whitney Bank" and as "Hancock Bank" in Mississippi, Alabama and Florida. Information on

DO NOTHING and as long as you can make the payments, this is probably the default option, and it really is not a bad one

DO NOTHING This option is for those who do not consider their house as a Short-Term Investment, but rather they think of it as their home If your house still serves as shelter, you consider it your home,

DO NOTHING This option is for those who do not consider their house as a Short-Term Investment, but rather they think of it as their home If your house still serves as shelter, you consider it your home,

The Top Seven Financial Pitfalls Every Homeowner Facing Foreclosure Must Avoid

The Top Seven Financial Pitfalls Every Homeowner Facing Foreclosure Must Avoid The foreclosure process is perplexing, even for those experienced in real estate. Real estate agents, attorneys, mortgage

The Top Seven Financial Pitfalls Every Homeowner Facing Foreclosure Must Avoid The foreclosure process is perplexing, even for those experienced in real estate. Real estate agents, attorneys, mortgage

AVOIDING. Foreclosure. Learn What Steps You Can Take to Save Your Home

AVOIDING Foreclosure Learn What Steps You Can Take to Save Your Home Don t Give Up Until You ve Explored Every Option Without a doubt, foreclosure is one of the scariest words in the financial dictionary.

AVOIDING Foreclosure Learn What Steps You Can Take to Save Your Home Don t Give Up Until You ve Explored Every Option Without a doubt, foreclosure is one of the scariest words in the financial dictionary.

COLORADO FORECLOSURE LAWS

COLORADO FORECLOSURE LAWS Orten Cavanagh & Holmes, LLC Community Association Attorneys Denver Phone 720.221.9780 Fax 720.221.9781 Toll Free 888.841.5149 Colorado Springs Phone 719.457.8420 Fax 719.457.8419

COLORADO FORECLOSURE LAWS Orten Cavanagh & Holmes, LLC Community Association Attorneys Denver Phone 720.221.9780 Fax 720.221.9781 Toll Free 888.841.5149 Colorado Springs Phone 719.457.8420 Fax 719.457.8419

Homeowner Request for Assistance

Homeowner Request for Assistance In this packet. Thank you in advance for allowing your Credit Union to review your account for mortgage assistance. Homeowner Checklist Details the documents and forms

Homeowner Request for Assistance In this packet. Thank you in advance for allowing your Credit Union to review your account for mortgage assistance. Homeowner Checklist Details the documents and forms

6 Steps to Completing Your Loan Modification Yourself

6 Steps to Completing Your Loan Modification Yourself Page 1 of 12 You hear it in the news almost every day, more and more hard working Americans are falling behind on their mortgage payments. Many real

6 Steps to Completing Your Loan Modification Yourself Page 1 of 12 You hear it in the news almost every day, more and more hard working Americans are falling behind on their mortgage payments. Many real

Florida Foreclosure/Real Estate Law. E-Book. A Simple Guide to Florida Foreclosure/Real Estate Law. by: Florida Law Advisers, P.A.

Florida Foreclosure/Real Estate Law E-Book A Simple Guide to Florida Foreclosure/Real Estate Law by: Florida Law Advisers, P.A. 1 Call: 800-990-7763 Web: www.floridalegaladvice.com TABLE OF CONTENTS INTRODUCTION...

Florida Foreclosure/Real Estate Law E-Book A Simple Guide to Florida Foreclosure/Real Estate Law by: Florida Law Advisers, P.A. 1 Call: 800-990-7763 Web: www.floridalegaladvice.com TABLE OF CONTENTS INTRODUCTION...

Is Cancellation of Debt Income Taxable? One question that I am asked often these days is whether cancellation of debt (COD) income is taxable or not?

income is taxable or not?") Is Cancellation of Debt Income Taxable? One question that I am asked often these days is whether cancellation of debt (COD) income is taxable or not? For tax purposes, the general rule is that all debt

Is Cancellation of Debt Income Taxable? One question that I am asked often these days is whether cancellation of debt (COD) income is taxable or not? For tax purposes, the general rule is that all debt

Guide to Fair Mortgage Lending and Home Preservation

Guide to Fair Mortgage Lending and Home Preservation Fair Housing Legal Support Center & Clinic Guide to Fair Mortgage Lending and Home Preservation What does this guide cover? What is Fair Lending? What

Guide to Fair Mortgage Lending and Home Preservation Fair Housing Legal Support Center & Clinic Guide to Fair Mortgage Lending and Home Preservation What does this guide cover? What is Fair Lending? What

Tired of the Foreclosure Threat?

Y o u r R e a l E s t a t e S t r e s s R e l i e f Tired of the Foreclosure Threat? Learn about the 6 options available to you when you are facing foreclosure Loan Modification Foreclosure Prevention

Y o u r R e a l E s t a t e S t r e s s R e l i e f Tired of the Foreclosure Threat? Learn about the 6 options available to you when you are facing foreclosure Loan Modification Foreclosure Prevention

FHA Servicing Compliance The Collingwood Group Conference Call Summary April 12, 2012

FHA Servicing Compliance The Collingwood Group Conference Call Summary April 12, 2012 Below is a summary of the April 12, 2012 mortgage industry call sponsored by The Collingwood Group. Questions may be

FHA Servicing Compliance The Collingwood Group Conference Call Summary April 12, 2012 Below is a summary of the April 12, 2012 mortgage industry call sponsored by The Collingwood Group. Questions may be

Providing legal help for low-income and disadvantaged people in Missouri. How to Avoid Losing Your Home in a Mortgage Foreclosure - Revised 2006.

Missouri Legal Aid Programs Providing legal help for low-income and disadvantaged people in Missouri www.lsmo.org Home Foreclosures How to Avoid Losing Your Home in a Mortgage Foreclosure - Revised 2006.

Missouri Legal Aid Programs Providing legal help for low-income and disadvantaged people in Missouri www.lsmo.org Home Foreclosures How to Avoid Losing Your Home in a Mortgage Foreclosure - Revised 2006.

Q. Under what circumstances wil my loan be cal ed due and payable? Q. What happens if one of the above occurs and my loan is cal ed due and payable?

Financial Freedom, as servicer for your Home Equity Conversion Mortgage ( HECM or loan ), is required by the U.S. Department of Housing and Urban Development ( HUD ) to perform certain actions depending

Financial Freedom, as servicer for your Home Equity Conversion Mortgage ( HECM or loan ), is required by the U.S. Department of Housing and Urban Development ( HUD ) to perform certain actions depending

Help for Rhode Islanders in Housing Trouble

Help for Rhode Islanders in Housing Trouble An Update from Rhode Island Housing June 2009 Table of Contents: Getting Out of Mortgage Trouble... 2 Modification, Refinancing and Beyond... 3 Homeowner gets

Help for Rhode Islanders in Housing Trouble An Update from Rhode Island Housing June 2009 Table of Contents: Getting Out of Mortgage Trouble... 2 Modification, Refinancing and Beyond... 3 Homeowner gets

CONSUMER. Steps that Advocates Can Take to Help Older Homeowners Prevent Foreclosure

CONSUMER Information for Advocates Representing Older Adults N a t i o n a l C o n s u m e r L a w C e n t e r CONCERNS Steps that Advocates Can Take to Help Older Homeowners Prevent Foreclosure Foreclosure

CONSUMER Information for Advocates Representing Older Adults N a t i o n a l C o n s u m e r L a w C e n t e r CONCERNS Steps that Advocates Can Take to Help Older Homeowners Prevent Foreclosure Foreclosure

SPECIAL REPORT. How To Avoid Foreclosure!

SPECIAL REPORT How To Avoid Foreclosure! Homeowner Solutions, LLC Placing People Before Profits To Solve Real Estate Problems P.O. Box 5782, Aiken, SC 29804 Phone: (803) 602-3913 Fax: (877) 245-3646 www.housebuyingcompany.com

SPECIAL REPORT How To Avoid Foreclosure! Homeowner Solutions, LLC Placing People Before Profits To Solve Real Estate Problems P.O. Box 5782, Aiken, SC 29804 Phone: (803) 602-3913 Fax: (877) 245-3646 www.housebuyingcompany.com

CALL TODAY: 480.948.6260. Options for Avoiding Foreclosure in Arizona ArizonaForeclosureRelief.com

Options for Avoiding Foreclosure in Arizona ArizonaForeclosureRelief.com Thank you for taking the time to request our free report on how to avoid foreclosure in Arizona. We greatly empathize with anyone

Options for Avoiding Foreclosure in Arizona ArizonaForeclosureRelief.com Thank you for taking the time to request our free report on how to avoid foreclosure in Arizona. We greatly empathize with anyone

How to STOP Foreclosure

1 How to STOP Foreclosure A Free Report from KentuckySolutions.com Kentucky s Real Estate Problem Solvers (Press Control-P to Print) 2 Introduction As Local Investors experienced in the Kentucky foreclosure

1 How to STOP Foreclosure A Free Report from KentuckySolutions.com Kentucky s Real Estate Problem Solvers (Press Control-P to Print) 2 Introduction As Local Investors experienced in the Kentucky foreclosure

The 5 Fastest. Foreclosure in

The 5 Fastest Ways to Stop Foreclosure in 48 Hours Or Less Copyright Notice All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means electronic or mechanical.

The 5 Fastest Ways to Stop Foreclosure in 48 Hours Or Less Copyright Notice All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means electronic or mechanical.

HAFA Short Sales, US Treasury, Fannie Mae & Freddie Mac Programs. Learning Objectives

HAFA Short Sales, US Treasury, Fannie Mae & Freddie Mac Programs Learning Objectives Module 1: HARP, HAMP & HAFA Overview Upon completion of Module 1 the student will be able to: Explain the advantages

HAFA Short Sales, US Treasury, Fannie Mae & Freddie Mac Programs Learning Objectives Module 1: HARP, HAMP & HAFA Overview Upon completion of Module 1 the student will be able to: Explain the advantages

Effective Foreclosure Time Line Management Reference Guide

Effective Foreclosure Time Line Management Reference Guide A foreclosure time line is the number of days it takes to process a foreclosure, from the due date of the last paid installment (DDLPI) to the

Effective Foreclosure Time Line Management Reference Guide A foreclosure time line is the number of days it takes to process a foreclosure, from the due date of the last paid installment (DDLPI) to the

LOAN DEFAULT AND FORECLOSURE: A BRIEF GUIDE FOR CALIFORNIA HOMEOWNERS

LOAN DEFAULT AND FORECLOSURE: A BRIEF GUIDE FOR CALIFORNIA HOMEOWNERS Compiled by: UNIVERSITY OF SAN FRANCISCO, Provided by: COMMUNITY LEGAL SERVICES IN E. PALO ALTO SCHOOL OF LAW 2117 (B) UNIVERSITY AVENUE

LOAN DEFAULT AND FORECLOSURE: A BRIEF GUIDE FOR CALIFORNIA HOMEOWNERS Compiled by: UNIVERSITY OF SAN FRANCISCO, Provided by: COMMUNITY LEGAL SERVICES IN E. PALO ALTO SCHOOL OF LAW 2117 (B) UNIVERSITY AVENUE

About Northwest Counseling Service

About Northwest Counseling Service Non Profit Agency No Cost Housing Counseling Services Any Service Related To A Home Specialize In Mortgage Delinquency 96% Rate In Keeping Residents In Homes HUD Certified/OHCD

About Northwest Counseling Service Non Profit Agency No Cost Housing Counseling Services Any Service Related To A Home Specialize In Mortgage Delinquency 96% Rate In Keeping Residents In Homes HUD Certified/OHCD

GLOSSARY COMMONLY USED REAL ESTATE TERMS

GLOSSARY COMMONLY USED REAL ESTATE TERMS Adjustable-Rate Mortgage (ARM): a mortgage loan with an interest rate that is subject to change and is not fixed at the same level for the life of the loan. These

GLOSSARY COMMONLY USED REAL ESTATE TERMS Adjustable-Rate Mortgage (ARM): a mortgage loan with an interest rate that is subject to change and is not fixed at the same level for the life of the loan. These

Home Affordable Modification Program (HAMP )

") Home Affordable Modification Program (HAMP ) Training for Trusted Advisors April 2015 Making Home Affordable Objectives 1 2 3 4 5 6 Step 1 Step 2 Step 3 Step 4 Step 5 7 8 MHA Program Highlights HAMP Overview

Home Affordable Modification Program (HAMP ) Training for Trusted Advisors April 2015 Making Home Affordable Objectives 1 2 3 4 5 6 Step 1 Step 2 Step 3 Step 4 Step 5 7 8 MHA Program Highlights HAMP Overview

WELCOME TO THE MASCIA LAW FIRM NEW CLIENT PACKAGE