Residential Mortgage Lending in Oregon Calendar Year 2010

|

|

|

- Ethan McCoy

- 8 years ago

- Views:

Transcription

1 Residential Mortgage Lending in Oregon Calendar Year 2010 Department of Consumer and Business Services Division of Finance and Corporate Securities December 2011

2 Introduction: This report marks the fourth year mortgage lending data for Oregon have been collected by DCBS under Senate Bill 1064 (2008). The first report covered loans originated in calendar year This version covers loans originated in calendar year Only mortgage lending firms regulated by the State of Oregon are required to provide data. Banks and credit unions are excluded from the reporting requirement even if they are chartered with the state. Only loans for Oregon consumers, for properties located in Oregon, or loans produced in Oregon are included. Report highlights: 778 firms provided data. 545 firms originated 60,555 loans with a volume of $12.85 billion. Eighteen firms (3.3 percent) originated over half of the loans. The 2010 mortgage lending market is characterized by contraction. Twenty-two percent fewer firms produced 16 percent fewer loans. Interest-only loans, and loans with a prepayment penalty continued to make up a tiny share of Oregon s mortgage lending market. The number of subordinate-lien loans increased from 2009 to percent of the firms that produced loans were located in Oregon; they produced 49 percent of the loans. The average first-lien loan amount was $214,000 and the average subordinate-lien loan amount was approximately $88,000. The average first-lien amount declined by approximately $8,300 from 2009 to 2010 while the average subordinate-lien amount was essentially unchanged. About 950 reverse mortgages were produced in Legislative history: Because of concern about the Oregon housing market, legislators introduced several bills affecting residential mortgage lending during the 2007 legislative session. Although no bills passed, many people saw a need for statutory changes. As a result, the Governor asked DCBS to convene a work group consisting of legislative, industry, and consumer representatives. The Mortgage Lending Work Group worked from the fall of 2007 through the fall of 2008 to address enhanced enforcement laws and lending practices. Recommendations from the work group resulted in two bills passed during the February 2008 legislative session. HB 3630 modified the regulation of activities by mortgage loan foreclosure consultants and equity purchasers and improved the information that must be provided to homeowners facing foreclosure. SB 1064 increased the regulation of the activities of loan originators, the loan salespeople who are employed by licensed mortgage bankers or mortgage brokers and directly negotiate terms and conditions of mortgage loans with borrowers. The bill also required the department to provide consumers with a registry of information about loan originators, including justified complaints and enforcement actions. Page 2 of 15

3 SB 1064 also required state-regulated mortgage bankers and mortgage brokers to file information about their residential mortgage lending each year. 1 ORS (3) now reads: On or before May 1 of each year or on a date the director establishes by rule, every mortgage banker and mortgage broker shall file a report with the director in a form prescribed by the director. The report shall contain information the director requires concerning the mortgage banker s or mortgage broker s business and operations related to residential mortgage lending during the preceding calendar year. The information shall include the number and nature of loans originated by loan originators that the mortgage banker or mortgage broker employed. Other sections of the statute forbid the publication of data for any individual lender and impose penalties for non-reporting. Reporting is limited to the companies regulated by the state. Federally chartered financial institutions that originate residential mortgages are not under state regulation and do not report. The administrative rules for data reporting are OAR After considering input from industry stakeholders and consumer groups, the department adopted the rules in May In response to additional input from industry stakeholders, the department revised the rules and adopted them in final form in June As a result of discussions with industry representatives about the feasibility of some of the reporting, the department required the reporting of some data items and made optional the reporting of other items. 3 Revised rules were adopted in December 2008 for the forthcoming annual reports. The rules now require that mortgage bankers and brokers provide the annual data prior to March 31 each year. Changes in OAR for reporting year 2008 required that mortgage lenders provide additional data when reporting lending activity. Lenders are now required to report: Whether interest-only mortgages have a fixed or adjustable interest rate. Whether adjustable interest rate mortgages are the first- or subordinate-lien. Whether purchases or refinances are for owner occupied, non-owner occupied, or is for a secondary residence. Changes made for the 2010 reporting year required mortgage lenders to provide data on reverse mortgages. Data collection: This is the fourth year that state-regulated mortgage bankers and mortgage brokers have reported this data to DCBS. The department changed data collection methods between 2007 and 2008 to improve data validity. However, several firms had 2010 data that was internally inconsistent and required revision. Because data are self-reported, care needs to be taken when interpreting small loan numbers or volume. Also, responses to the optional questions are not included in this analysis due to a low response rate. 1 Sections of SB 1064 are provided in Appendix 1. 2 The current language for OAR is shown in Appendix 2. 3 The CY 2010 census questions are shown in Appendix 3. Page 3 of 15

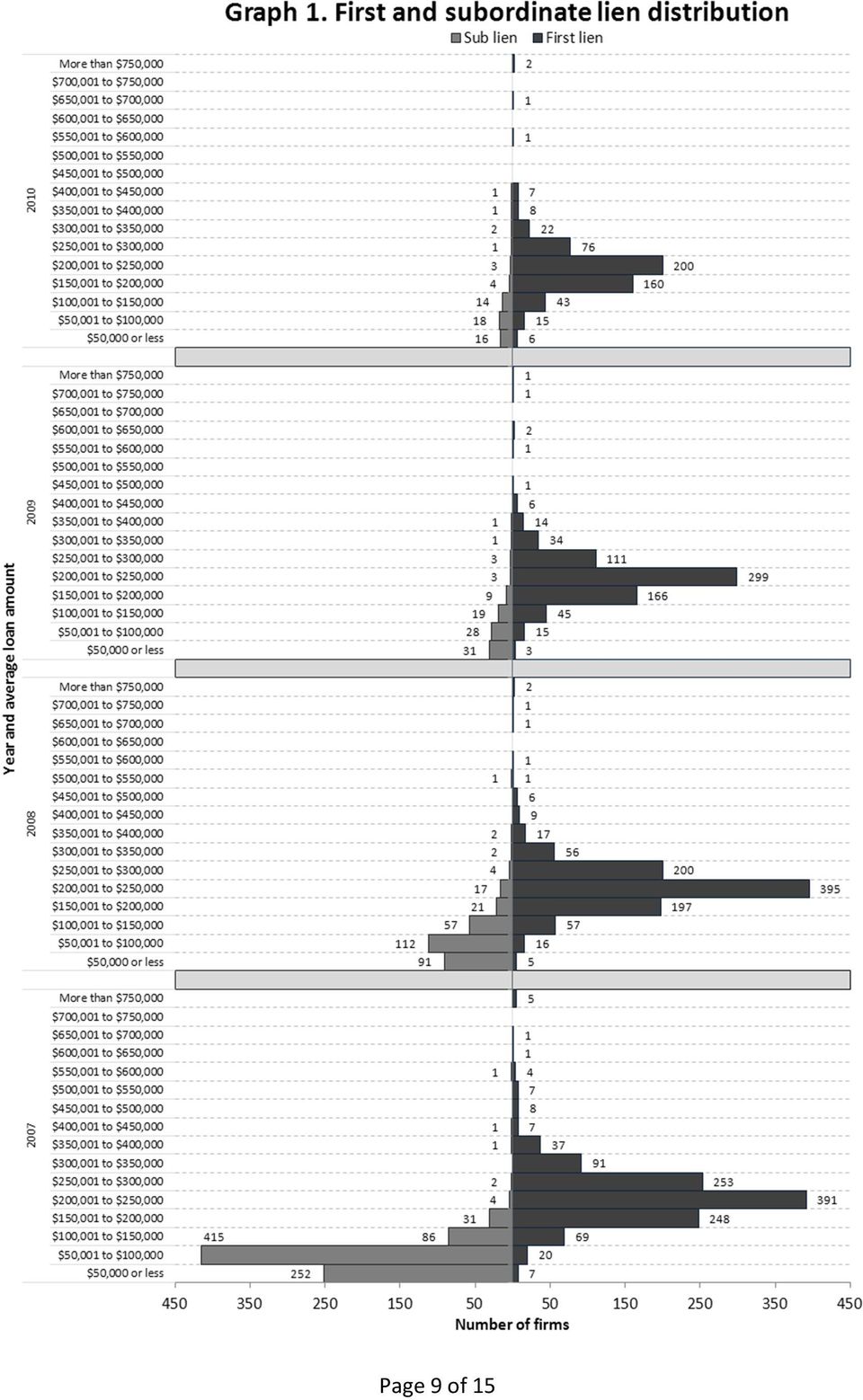

4 Mortgage bankers and brokers reported their loans by category. The categories are: Fixed rate mortgage: a mortgage loan where the interest rate on the note remains the same through the term of the loan. Interest-only loan: a loan in which for a set term the borrower pays only the interest on the principal balance, with the principal balance unchanged. At the end of the interestonly term, the borrower gets a new payment amount calculated on an updated amortization schedule. Interest-only loans can have either a fixed or an adjustable interest rate. Negative amortization loan: a mortgage loan where the loan payment for any period is less than the interest charged over that period so that the outstanding balance of the loan increases. This method is generally used in an introductory period before loan payments exceed interest and the loan becomes self-amortizing. In this report, this category includes reverse mortgages. With these loans, neither the capital nor interest is repaid. The interest is rolled up with the capital, increasing the debt each year. The homeowner's obligation to repay the loan is deferred until the owner leaves the home or the home is sold. Adjustable rate mortgage (ARM): a mortgage loan where the interest rate on the note is periodically adjusted based on an index. The loans often have low initial interest rates. Prepayment penalty loan: a loan that includes a penalty when the borrower repays the principal early. Number of firms, loans, and size of volume: Of the 778 firms that reported data for 2010, 545 issued loans while 233 did not. The number of firms that issued loans in 2010 was 22 percent lower than the 700 firms that originated loans in The 545 firms that produced loans originated 60,555 loans with a volume of $12.85 billion. The number of loans declined by 16 percent from last year and loan volume declined by 22 percent. Firm participation in Oregon s mortgage lending market underwent significant change between 2009 and 2010: 311 firms went out of business after firms entered the market. 487 of the firms that were active in 2009 were also active in firms offered no loans in 2009 or firms produced at least one loan in 2009 but none in firms produced no loans in 2009 but at least one in In 2010, in-state firms accounted for 44 percent of responding firms. These firms produced 49 percent of all loans. Page 4 of 15

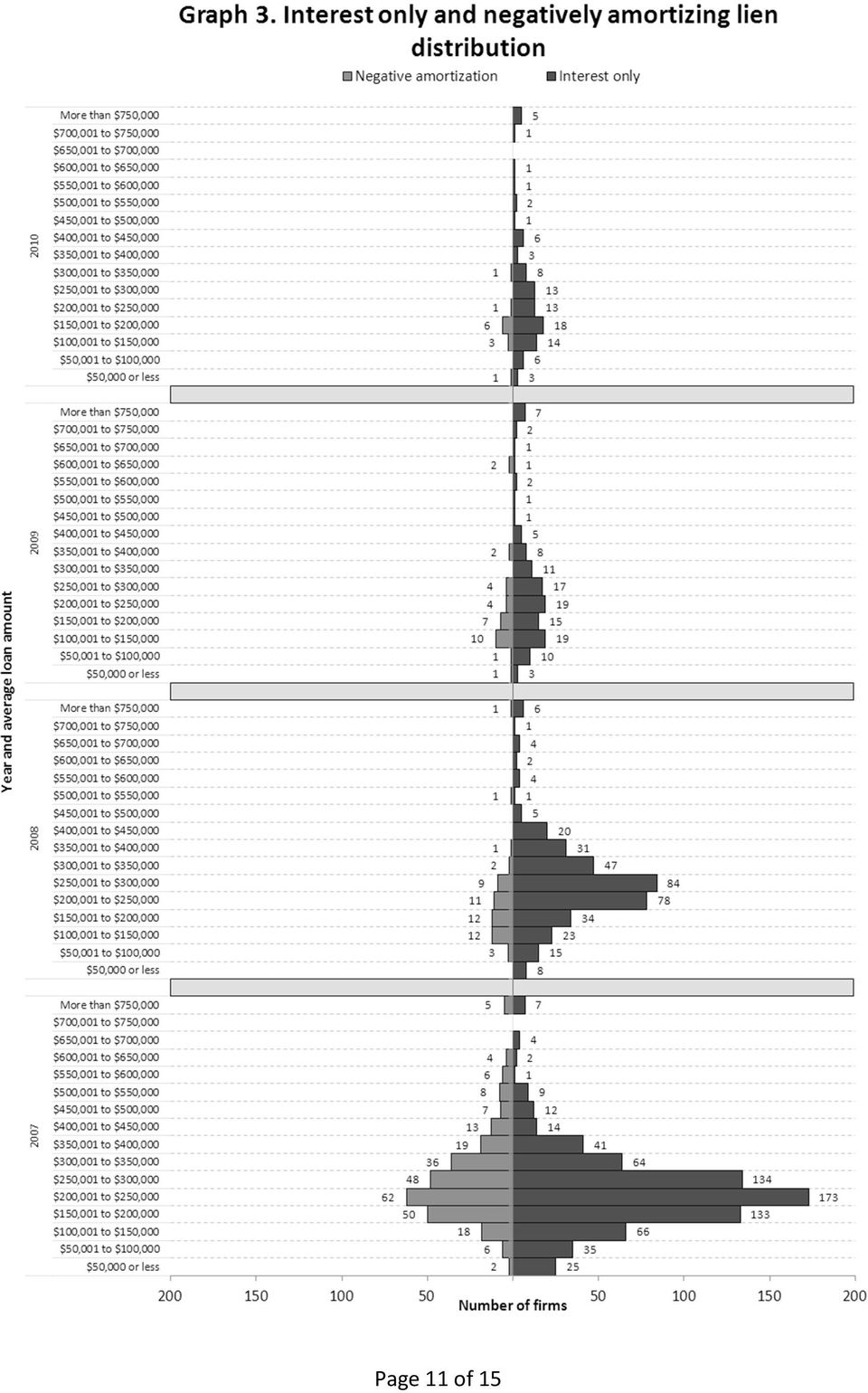

5 In 2010, 93 percent of Oregon loans had a fixed interest rate, an increase of about three percent from Only 5 percent of loans had an adjustable interest rate. This is two percentage points higher than 2009 and similar to The number of interest-only loans and loans with a prepayment penalty have continued to decline since The reported number of negatively amortized loans declined significantly from 2007 to 2008, increased slightly in 2009, and fell significantly in The number of fixed loans grew by approximately 3,000, in 2009 but fell by about 8,000 in Fixed-rate loan volume declined by approximately $2.9 billion over the same period. Large firms again dominated mortgage lending in Oregon in Firms that originated more than 1,000 loans, about 2 percent of the entire population, produced 43 percent of all loans. The smallest firms, those that originated 25 or fewer loans, produced less than 5 percent of all loans. Page 5 of 15

6 No firm size cohort grew in The loan and loan cohorts remained the same size, 71 firms and 12 firms, respectively. The largest cohort shrunk by three firms. The smallest cohort shrunk by 112 firms. There was moderate year-to-year variation in the number of firms, loan counts, and volume by firm size. Large firms produced 47.5 percent of all loan volume in 2009 but 44.5 percent of all loan volume in First-lien originations continued to dominate the mortgage lending market in Oregon. Of the 60,555 total Oregon originations, 59,583 were first-lien. Large firms dominated this market segment. The two largest firm-size cohorts, those that produced more than 501 loans, accounted for 57 percent of first-lien originations, but constituted about 4 percent of all firms. First-lien changes between 2009 and 2010 mirror the changes for all Oregon loans because firstlien loans constitute the vast majority of all loans. Between 2009 and 2010, 23 percent fewer firms produced 16 percent fewer first-lien loans at a 19 percent smaller volume. The largest firms Page 6 of 15

7 significantly decreased originations. Firms that produced more than 1,000 loans decreased their originations from approximately 33,000 in 2009 to about 26,000 in Subordinate-lien loans played a very small role in Oregon s mortgage lending market. Only 60 firms originated subordinate-lien loans in Oregon regulated mortgage lenders and brokers produced about 970 subordinate liens with a total volume of $85.2 million. The average loan amount for a 2010 subordinate-lien was about $88,000. There was significant variance in the average loan amount depending on firm size. Firms that offered fewer than 25 total loans tended to produce subordinate-lien loans with an average amount nearly $20,000 higher than the average for all firm sizes. However, given the small number of subordinate-lien loans, care should be taken when interpreting the average volume per firm and the average loan amount as outliers may significantly influence those statistics saw fewer firms producing more subordinate-lien mortgages with a larger volume than Page 7 of 15

8 Firms and the average prices of loans: The average loan amount for each firm was calculated by dividing the total volume of a particular loan type by the total number of loans of that type. These average loan amounts were then placed into a range of values and counted to derive the following graphs that show how many firms offered a particular loan product in a given price range. This year has seen a continuation of the trend for fewer firms in all average price ranges across all loan types (with some exceptions in price ranges with very few firms). The following three graphs show this for first and subordinate-liens, fixed and adjustable rates, and interest-only and negatively amortizing loans. Page 8 of 15

9 Page 9 of 15

10 Page 10 of 15

11 Page 11 of 15

12 Appendix 1. Sections 1 and 5 of SB 1064 (2008) (Sections in bold are language added by SB 1064) SECTION 1. ORS is amended to read: (1) Every mortgage banker and mortgage broker shall make and keep such accounts, correspondence, memoranda, papers, books and other records as the Director of the Department of Consumer and Business Services by rule or order prescribes. All such records shall be preserved for five years unless the director by rule prescribes otherwise. The director may examine all such records within or without this state at any reasonable time or times and may require without subpoena the production of such records at the office of the director as often as is reasonably necessary. (2) Every mortgage banker and mortgage broker shall file financial reports or other information as the director by rule or order may require and shall promptly correct any document filed with the director that is or becomes incomplete or inaccurate in any material respect. (3) On or before May 1 of each year or on a date the director establishes by rule, every mortgage banker and mortgage broker shall file a report with the director in a form prescribed by the director. The report shall contain information the director requires concerning the mortgage banker s or mortgage broker s business and operations related to residential mortgage lending during the preceding calendar year. The information shall include the number and nature of loans originated by loan originators that the mortgage banker or mortgage broker employed. (4) The report and any records submitted to the director under this section are exempt from disclosure or production and are confidential as provided under ORS Notwithstanding the exemption and confidentiality provisions of subsection (4) of this section, the director may abstract information contained in reports submitted under subsection (3) of this section and may make the abstracted information available for public inspection provided that the abstracted information does not identify a particular mortgage banker or mortgage broker as a source of the information. SECTION 5. ORS is amended to read: (1) In addition to all other penalties and enforcement provisions provided by law, any person who violates or who procures, aids or abets in the violation of any provision of ORS to or any rule or order of the Director of the Department of Consumer and Business Services shall be subject to a penalty of not more than $5,000 for every violation, which shall be paid to the General Fund of the State Treasury. (2) Notwithstanding subsection (1) of this section, a person who fails to submit a report required under ORS (3) on the date specified is subject to a penalty of not more than $100 per day for each day after the specified date during which the failure continues. [(2)] (3) Every violation is a separate offense and, in the case of a continuing violation, each day s continuance is a separate violation, but the maximum penalty for any continuing violation shall not exceed $20,000 for each offense. [(3)] (4) Civil penalties under this section shall be imposed as provided in ORS Page 12 of 15

13 Appendix 2. OAR (effective December 2008) Residential Mortgage Lending Reports On or before March 31 of each calendar year, a mortgage banker or a mortgage broker licensed at any time during the preceding calendar year must file a report concerning the banker s or broker s business and operations conducted during the preceding calendar year related to residential mortgage transactions. (1) A licensee must report the total number and dollar amount of all loans made or funded by the licensee in any state and those loans that are Oregon residential mortgage transactions. 2) For loans made or funded for a property located in Oregon, a licensee must report the total number and dollar amount of: (a) First-lien mortgage loans. (b) Subordinate-lien mortgage loans including, but not limited to, home equity lines of credit. (c) Mortgage loans having a fixed periodic payment of principal and interest throughout the mortgage term. (d) Interest-only first-lien mortgage loans having a fixed interest rate. (e) Interest-only first-lien mortgage loans having an adjustable interest rate. (f) Negative amortization mortgage loans. (g) Adjustable rate first-lien mortgage loans. (h) Adjustable rate subordinate-lien mortgage loans. (i) Loans with a prepayment penalty in the contract at the time of closing. (j) Mortgage loans closed for the purchase of a primary owner-occupied residential dwelling. (k) Mortgage loans closed for the purchase of a secondary residence. (L) Mortgage loans closed for the purchase of a non-owner occupied property that is a one-to-four family residential dwelling. (m) Mortgage loans closed for the purpose of refinancing an existing mortgage loan secured by a primary owner-occupied residential dwelling. (n) Mortgage loans closed for the purpose of refinancing an existing mortgage loan secured by a secondary residence. (o) Mortgage loans closed for the purpose of refinance an existing mortgage loan secured by a nonowner occupied property that is a one-to-four family residential dwelling. (p) Mortgage loans insured or guaranteed by a federal agency. (3) For loans made or funded for a property located in Oregon, a licensee may report the total number and dollar amount of: (a) Loans that were originated based on all of the following factors: (A) Income documentation; (B) Employment documentation; and (C) Asset documentation. (b) Loans that were originated based on one or two of the following factors: (A) Income documentation; (B) Employment documentation; or (C) Asset documentation. (c) Loans that were not originated based on any of the following factors: (A) Income documentation; (B) Employment documentation; or (C) Asset documentation. Page 13 of 15

A licensee must report the total number and dollar amount of all loans made or funded by the licensee in any state and those loans that are Oregon residential mortgage transactions.")

14 (d) Loans with a combined loan-to-value ratio of 80% or lower made to an individual having a middle credit bureau risk score of 620 or above. (e) Loans with a combined loan-to-value ratio of 80% or lower made to an individual having a middle credit bureau risk score below 620. (f) Loans with a loan-to-value ratio of greater than 80% made to an individual having a middle credit bureau risk score of 620 or above. (g) Loans with a loan-to-value ratio of greater than 80% made to an individual having a middle credit bureau risk score below 620. (4) For purposes of this rule: (a) Loan-to-value ratio means the ratio between the amount of a mortgage loan and the value of the property pledged as security, expressed as a percentage. (b) Residential mortgage transaction has the same meaning as ORS Page 14 of 15

Loans with a loan-to-value ratio of greater than 80% made to an individual having a middle credit bureau risk score below 620.")

15 The mandatory CY 2010 questions were: Provide the number and volume of loans that are: Appendix 3. CY 2010 reporting and data revisions 1) Produced in any state 2) Produced in Oregon a) First-lien mortgages b) Subordinate-lien mortgages c) Fixed interest d) Interest-only with a fixed rate e) Interest-only with an adjustable rate f) Negatively amortized g) Adjustable rate first-lien h) Adjustable rate subordinate-lien i) Associated with a prepayment penalty j) Closed for the purchase of a primary home k) Closed for the purchase of a second home l) Closed for the purchase of a non-owner occupied one-to-four family residential dwelling m) Closed for the refinancing of a primary home n) Closed for the refinancing of a secondary home o) Closed for the refinancing a non-owner occupied one-to-four family residence p) Federally guaranteed q) Reverse mortgages The optional CY 2010 questions were: Respondent may provide the number and volume of Oregon loans that are: 1) Based on all three: income, employment, and asset documentation 2) Based on one or two of the three: income, employment, and/or asset documentation 3) Based on none of the three: income, employment, and asset documentation 4) Low loan-to-value ratio and high credit score 5) Low loan-to-value ratio and low credit score 6) High loan-to-value ratio and high credit score 7) High loan-to-value ratio and low credit score Because of experience gained during CY2007 reporting, measures were put into place to check validity of data while it was being entered. Due to this, the numbers of possible errors were significantly reduced although we were not able to validate all responses. Page 15 of 15

Closed for the purchase of a second home l) Closed for the purchase of a non-owner occupied one-to-four family residential dwelling m) Closed for the refinancing of a primary home n)")

Residential Mortgage Lending in Oregon, CY 2007

Introduction Residential Mortgage Lending in Oregon, CY 2007 By Senate Bill 1064 (2008), the Oregon Legislature required that all mortgage banker and mortgage brokers licensed by the Oregon Division of

Introduction Residential Mortgage Lending in Oregon, CY 2007 By Senate Bill 1064 (2008), the Oregon Legislature required that all mortgage banker and mortgage brokers licensed by the Oregon Division of

SENATE BILL 465. 3lr2733 CF HB 522 A BILL ENTITLED. Refinancing of First Mortgage Loans Subordination

I SENATE BILL By: Senator Klausmeier Introduced and read first time: January 0, Assigned to: Judicial Proceedings and Finance lr CF HB A BILL ENTITLED AN ACT concerning Refinancing of First Mortgage Loans

I SENATE BILL By: Senator Klausmeier Introduced and read first time: January 0, Assigned to: Judicial Proceedings and Finance lr CF HB A BILL ENTITLED AN ACT concerning Refinancing of First Mortgage Loans

QUARTERLY UPDATE TO THE SENATE BUSINESS AND COMMERCE COMMITTEE January 16, 2014 BY THE OFFICE OF CONSUMER CREDIT COMMISSIONER

QUARTERLY UPDATE TO THE SENATE BUSINESS AND COMMERCE COMMITTEE January 16, 2014 BY THE OFFICE OF CONSUMER CREDIT COMMISSIONER SB 247: Property Tax Loans IMPLEMENTATION OF LEGISLATION FROM THE 83RD LEGISLATURE

QUARTERLY UPDATE TO THE SENATE BUSINESS AND COMMERCE COMMITTEE January 16, 2014 BY THE OFFICE OF CONSUMER CREDIT COMMISSIONER SB 247: Property Tax Loans IMPLEMENTATION OF LEGISLATION FROM THE 83RD LEGISLATURE

Chapter 2d Utah High Cost Home Loan Act

Chapter 2d Utah High Cost Home Loan Act 61-2d-101 Title. This chapter is known as the "Utah High Cost Home Loan Act." 61-2d-102 Definitions. As used in this part: (1) "Accelerate" means a demand for immediate

Chapter 2d Utah High Cost Home Loan Act 61-2d-101 Title. This chapter is known as the "Utah High Cost Home Loan Act." 61-2d-102 Definitions. As used in this part: (1) "Accelerate" means a demand for immediate

ANALYSIS OF HOME MORTGAGE DISCLOSURE ACT (HMDA) DATA FOR TEXAS, 1999-2001

DATA FOR TEXAS, 1999-2001") LEGISLATIVE REPORT ANALYSIS OF HOME MORTGAGE DISCLOSURE ACT (HMDA) DATA FOR TEXAS, 1999-2001 REPORT PREPARED FOR THE FINANCE COMMISSION OF TEXAS AND THE OFFICE OF CONSUMER CREDIT COMMISSIONER BY THE TEXAS

LEGISLATIVE REPORT ANALYSIS OF HOME MORTGAGE DISCLOSURE ACT (HMDA) DATA FOR TEXAS, 1999-2001 REPORT PREPARED FOR THE FINANCE COMMISSION OF TEXAS AND THE OFFICE OF CONSUMER CREDIT COMMISSIONER BY THE TEXAS

Florida Mortgage Laws and Regulations. Introduction. LegalEase was asked to review and summarize any legislation since January of 2007

23400 Michigan Avenue, Suite 101 Dearborn, MI 48124 Tel: 1-(866) 534-6177 (toll-free) Fax: 1-(734) 943-6051 Email: contact@legaleasesolutions.com www.legaleasesolutions.com Florida Mortgage Laws and Regulations

23400 Michigan Avenue, Suite 101 Dearborn, MI 48124 Tel: 1-(866) 534-6177 (toll-free) Fax: 1-(734) 943-6051 Email: contact@legaleasesolutions.com www.legaleasesolutions.com Florida Mortgage Laws and Regulations

COMMUNICATION NO. 313635 PROPOSED ORDINANCE AMENDMENT. Sponsored by

COMMUNICATION NO. 313635 PROPOSED ORDINANCE AMENDMENT Sponsored by THE HONORABLE TONI PRECKWINKLE, PRESIDENT, EARLEAN COLLINS, JERRY BUTLER, JOHN P. DALEY, JESUS G. GARCIA, EDWIN REYES, ROBERT B. STEELE

COMMUNICATION NO. 313635 PROPOSED ORDINANCE AMENDMENT Sponsored by THE HONORABLE TONI PRECKWINKLE, PRESIDENT, EARLEAN COLLINS, JERRY BUTLER, JOHN P. DALEY, JESUS G. GARCIA, EDWIN REYES, ROBERT B. STEELE

CUNA s SUMMARY OF THE CFPB s MORTGAGE LENDING RULES Spring 2013

MANDATORY ESCROW ACCOUNTS Effective: June 1, 2013 REGULATION Requires escrow accounts be maintained for five years (rather than the current one year) for higher-priced mortgage loans. A higher-priced mortgage

MANDATORY ESCROW ACCOUNTS Effective: June 1, 2013 REGULATION Requires escrow accounts be maintained for five years (rather than the current one year) for higher-priced mortgage loans. A higher-priced mortgage

ESCROW REQUIREMENTS UNDER TILA

Overview Escrow Requirements Reg. Z High Cost Mortgage and Counseling - Reg. Z & X Ability to Repay & Qualified Mortgages Reg. Z & X Mortgage Servicing Reg. Z & X Loan Originator Compensation Reg. Z Copies

Overview Escrow Requirements Reg. Z High Cost Mortgage and Counseling - Reg. Z & X Ability to Repay & Qualified Mortgages Reg. Z & X Mortgage Servicing Reg. Z & X Loan Originator Compensation Reg. Z Copies

Department of Legislative Services Maryland General Assembly 2010 Session

House Bill 799 Economic Matters Department of Legislative Services Maryland General Assembly 2010 Session FISCAL AND POLICY NOTE Revised (Delegate Kramer, et al.) Reverse Mortgage Homeowners Protection

House Bill 799 Economic Matters Department of Legislative Services Maryland General Assembly 2010 Session FISCAL AND POLICY NOTE Revised (Delegate Kramer, et al.) Reverse Mortgage Homeowners Protection

Comparison of Section 35(HPML) & Section 32(HOEPA) Regulations Including CFPB 2013 & 2014 Updates As of 01/07/2014

& Section 32(HOEPA) Regulations Including CFPB 2013 & 2014 Updates As of 01/07/2014") Comparison of Section 35(HPML) & Section 32(HOEPA) Regulations Including CFPB 2013 & 2014 Updates As of 01/07/2014 General Consumer Loan Type Not Applicable HPML (12 CFR 1026.35) A closed-end consumer

Comparison of Section 35(HPML) & Section 32(HOEPA) Regulations Including CFPB 2013 & 2014 Updates As of 01/07/2014 General Consumer Loan Type Not Applicable HPML (12 CFR 1026.35) A closed-end consumer

Early Summary of Ability to Repay and Qualified Mortgage Rules under Dodd-Frank Wall Street Reform and Consumer Protection Act.

Early Summary of Ability to Repay and Qualified Mortgage Rules under Dodd-Frank Wall Street Reform and Consumer Protection Act January 11, 2013 OVERVIEW - On January 10, 2013, the Consumer Financial Protection

Early Summary of Ability to Repay and Qualified Mortgage Rules under Dodd-Frank Wall Street Reform and Consumer Protection Act January 11, 2013 OVERVIEW - On January 10, 2013, the Consumer Financial Protection

SPECIAL ALERT: CFPB PROPOSES SIGNIFICANT EXPANSION OF HMDA REPORTING REQUIREMENTS

SPECIAL ALERT: CFPB PROPOSES SIGNIFICANT EXPANSION OF HMDA REPORTING REQUIREMENTS JULY 30, 2014 On July 24, the Consumer Financial Protection Bureau (the CFPB or Bureau) issued a proposed rule that would

SPECIAL ALERT: CFPB PROPOSES SIGNIFICANT EXPANSION OF HMDA REPORTING REQUIREMENTS JULY 30, 2014 On July 24, the Consumer Financial Protection Bureau (the CFPB or Bureau) issued a proposed rule that would

Comparison of Section 32(HOEPA) Regulation; Current Rules vs. January 10, 2014 CFPB Changes As of 10/16/14

Regulation; Current Rules vs. January 10, 2014 CFPB Changes As of 10/16/14") Comparison of Section 32(HOEPA) Regulation; Current Rules vs. January 10, 2014 CFPB Changes As of 10/16/14 General Loan Type 1994 TILA amendments apply to homeowners that already owned their homes and

Comparison of Section 32(HOEPA) Regulation; Current Rules vs. January 10, 2014 CFPB Changes As of 10/16/14 General Loan Type 1994 TILA amendments apply to homeowners that already owned their homes and

Section 1715z-20. Insurance of home equity conversion mortgages for elderly homeowners 1

Section 1715z-20. Insurance of home equity conversion mortgages for elderly homeowners 1 (a) Purpose The purpose of this section is to authorize the Secretary to carry out a program of mortgage insurance

Section 1715z-20. Insurance of home equity conversion mortgages for elderly homeowners 1 (a) Purpose The purpose of this section is to authorize the Secretary to carry out a program of mortgage insurance

GENERAL ASSEMBLY OF NORTH CAROLINA 1991 SESSION CHAPTER 546 HOUSE BILL 22

GENERAL ASSEMBLY OF NORTH CAROLINA 1991 SESSION CHAPTER 546 HOUSE BILL 22 AN ACT TO REGULATE REVERSE MORTGAGES. The General Assembly of North Carolina enacts: Section 1. Chapter 53 of the General Statutes

GENERAL ASSEMBLY OF NORTH CAROLINA 1991 SESSION CHAPTER 546 HOUSE BILL 22 AN ACT TO REGULATE REVERSE MORTGAGES. The General Assembly of North Carolina enacts: Section 1. Chapter 53 of the General Statutes

STATE HIGH COST/PREDATORY LENDING REGULATIONS Updated 1/10/2014

STATE HIGH COST/PREDATORY LENDING REGULATIONS Updated 1/10/2014 State: Law: Cite: North Carolina NC High Cost Home Loan Law NC Rate Spread Home Loans Check both rules HB 2188 effective 10/01/2008 changes

STATE HIGH COST/PREDATORY LENDING REGULATIONS Updated 1/10/2014 State: Law: Cite: North Carolina NC High Cost Home Loan Law NC Rate Spread Home Loans Check both rules HB 2188 effective 10/01/2008 changes

House of Representatives

House of Representatives General Assembly File No. 44 February Session, 2002 Substitute House Bill No. 5073 House of Representatives, March 18, 2002 The Committee on Banks reported through REP. DOYLE of

House of Representatives General Assembly File No. 44 February Session, 2002 Substitute House Bill No. 5073 House of Representatives, March 18, 2002 The Committee on Banks reported through REP. DOYLE of

Assumable mortgage: A mortgage that can be transferred from a seller to a buyer. The buyer then takes over payment of an existing loan.

MORTGAGE GLOSSARY Adjustable Rate Mortgage (ARM): A mortgage loan with payments usually lower than a fixed rate initially, but is subject to changes in interest rates. There are a variety of ARMs that

MORTGAGE GLOSSARY Adjustable Rate Mortgage (ARM): A mortgage loan with payments usually lower than a fixed rate initially, but is subject to changes in interest rates. There are a variety of ARMs that

ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C

Revisions to Regulation C") ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C November 2015 Month Year Mon Contact: Joe Gormley Assistant Vice President & Regulatory Counsel joseph.gormley@icba.org

ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C November 2015 Month Year Mon Contact: Joe Gormley Assistant Vice President & Regulatory Counsel joseph.gormley@icba.org

QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS)

(CLOSED-END HOME MORTGAGE TRANSACTIONS)") QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS) Type of (2) Contents of Truth in Lending Statements 226.17 226.36 Early s 226.19(a)(1)

QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS) Type of (2) Contents of Truth in Lending Statements 226.17 226.36 Early s 226.19(a)(1)

CONSUMER MORTGAGE PROTECTION ACT Act 660 of 2002. The People of the State of Michigan enact:

CONSUMER MORTGAGE PROTECTION ACT Act 660 of 2002 AN ACT to prohibit certain lending practices; to require disclosure of certain information for home loans; to prescribe certain duties and obligations of

CONSUMER MORTGAGE PROTECTION ACT Act 660 of 2002 AN ACT to prohibit certain lending practices; to require disclosure of certain information for home loans; to prescribe certain duties and obligations of

HOUSE BILL 2242 AN ACT AMENDING TITLE 6, ARIZONA REVISED STATUTES, BY ADDING CHAPTER 16; RELATING TO REVERSE MORTGAGES.

Senate Engrossed House Bill State of Arizona House of Representatives Forty-ninth Legislature Second Regular Session HOUSE BILL AN ACT AMENDING TITLE, ARIZONA REVISED STATUTES, BY ADDING CHAPTER ; RELATING

Senate Engrossed House Bill State of Arizona House of Representatives Forty-ninth Legislature Second Regular Session HOUSE BILL AN ACT AMENDING TITLE, ARIZONA REVISED STATUTES, BY ADDING CHAPTER ; RELATING

June 10, 2010. 2010 Legislative Amendments to the Indiana Code Relating to First Lien Mortgage Act (the Act )

") June 10, 2010 2010 Legislative Amendments to the Indiana Code Relating to First Lien Mortgage Act (the Act ) Effective July 1, 2010 (except as otherwise indicated) Questions, Answers, and Administrative

June 10, 2010 2010 Legislative Amendments to the Indiana Code Relating to First Lien Mortgage Act (the Act ) Effective July 1, 2010 (except as otherwise indicated) Questions, Answers, and Administrative

The Consumer Financial Protection Bureau s Ability-to-Repay and Qualified Mortgage Rule

ADVISORY February 2013 The Consumer Financial Protection Bureau s Ability-to-Repay and Qualified Mortgage Rule On January 10, 2013, the Consumer Financial Protection Bureau ( CFPB ) issued its final Ability-to-Repay

ADVISORY February 2013 The Consumer Financial Protection Bureau s Ability-to-Repay and Qualified Mortgage Rule On January 10, 2013, the Consumer Financial Protection Bureau ( CFPB ) issued its final Ability-to-Repay

Page 1417 TITLE 12 BANKS AND BANKING 2802

Page 1417 TITLE 12 BANKS AND BANKING 2802 loans to the Corporation for such purpose in the same manner as loans may be made for insurance purposes under such section, subject to the maximum limitation

Page 1417 TITLE 12 BANKS AND BANKING 2802 loans to the Corporation for such purpose in the same manner as loans may be made for insurance purposes under such section, subject to the maximum limitation

QUARTERLY UPDATE TO THE SENATE BUSINESS AND COMMERCE COMMITTEE October 10, 2013 BY THE OFFICE OF CONSUMER CREDIT COMMISSIONER

QUARTERLY UPDATE TO THE SENATE BUSINESS AND COMMERCE COMMITTEE October 10, 2013 BY THE OFFICE OF CONSUMER CREDIT COMMISSIONER SB 247: Property Tax Loans IMPLEMENTATION OF LEGISLATION FROM THE 83RD LEGISLATURE

QUARTERLY UPDATE TO THE SENATE BUSINESS AND COMMERCE COMMITTEE October 10, 2013 BY THE OFFICE OF CONSUMER CREDIT COMMISSIONER SB 247: Property Tax Loans IMPLEMENTATION OF LEGISLATION FROM THE 83RD LEGISLATURE

Mortgage Laws and Regulations-Georgia. Introduction. LegalEase was asked to review and summarize any legislation since January of 2007

Mortgage Laws and Regulations-Georgia Introduction 23400 Michigan Avenue, Suite 101 Dearborn, MI 48124 Tel: 1-(866) 534-6177 (toll-free) Fax: 1-(734) 943-6051 Email: contact@legaleasesolutions.com www.legaleasesolutions.com

Mortgage Laws and Regulations-Georgia Introduction 23400 Michigan Avenue, Suite 101 Dearborn, MI 48124 Tel: 1-(866) 534-6177 (toll-free) Fax: 1-(734) 943-6051 Email: contact@legaleasesolutions.com www.legaleasesolutions.com

PRIVATE MORTGAGE INSURANCE DISCLOSURES AND DOCUMENTS

PRIVATE MORTGAGE INSURANCE DISCLOSURES AND DOCUMENTS By Michael H. Patterson Peirson & Patterson, L.L.P. 1111 W. Arkansas Lane Arlington, Texas 76013 (817) 461-5500 mike@ppdocs.com Presented to Independent

PRIVATE MORTGAGE INSURANCE DISCLOSURES AND DOCUMENTS By Michael H. Patterson Peirson & Patterson, L.L.P. 1111 W. Arkansas Lane Arlington, Texas 76013 (817) 461-5500 mike@ppdocs.com Presented to Independent

*HB0160S02* H.B. 160 2nd Sub. (Gray) LEGISLATIVE GENERAL COUNSEL 6 Approved for Filing: S.M. Snyder 6 6 02-10-04 4:26 PM 6

LEGISLATIVE GENERAL COUNSEL 6 Approved for Filing: S.M. Snyder 6 6 02-10-04 4:26 PM 6") LEGISLATIVE GENERAL COUNSEL 6 Approved for Filing: S.M. Snyder 6 6 02-10-04 4:26 PM 6 H.B. 160 2nd Sub. (Gray) Representative Wayne A. Harper proposes the following substitute bill: 1 MORTGAGE ACT AMENDMENTS

LEGISLATIVE GENERAL COUNSEL 6 Approved for Filing: S.M. Snyder 6 6 02-10-04 4:26 PM 6 H.B. 160 2nd Sub. (Gray) Representative Wayne A. Harper proposes the following substitute bill: 1 MORTGAGE ACT AMENDMENTS

Florida Senate - 2010 SB 1532

By Senator Fasano 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 A bill to be entitled An act relating to reverse mortgage loans to senior individuals; providing purposes;

By Senator Fasano 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 A bill to be entitled An act relating to reverse mortgage loans to senior individuals; providing purposes;

CFPB Regulations on Ability to Repay and Qualified Mortgages. MDDCCUA Training

CFPB Regulations on Ability to Repay and Qualified Mortgages MDDCCUA Training October 30, 2013 E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. Ability-to-Repay and Qualified Mortgage Rules E. Andrew Keeney,

CFPB Regulations on Ability to Repay and Qualified Mortgages MDDCCUA Training October 30, 2013 E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. Ability-to-Repay and Qualified Mortgage Rules E. Andrew Keeney,

DEPARTMENT OF CORPORATIONS

STATE OF CALIFORNIA -- BUSINESS, TRANSPORTATION AND HOUSING AGENCY DEPARTMENT OF CORPORATIONS EDMUND G. BROWN Jr., Governor INSTRUCTIONS FOR COMPLETING THE 2012 ANNUAL REPORT FOR LENDERS AND BROKERS LICENSED

STATE OF CALIFORNIA -- BUSINESS, TRANSPORTATION AND HOUSING AGENCY DEPARTMENT OF CORPORATIONS EDMUND G. BROWN Jr., Governor INSTRUCTIONS FOR COMPLETING THE 2012 ANNUAL REPORT FOR LENDERS AND BROKERS LICENSED

HOME OWNERSHIP EQUITY PROTECTION ACT OF 1994. Raymond Natter 1

HOME OWNERSHIP EQUITY PROTECTION ACT OF 1994 Raymond Natter 1 Recent Congressional attention to the problems of predatory mortgage lending has led for calls for the Federal Reserve Board to use its authority

HOME OWNERSHIP EQUITY PROTECTION ACT OF 1994 Raymond Natter 1 Recent Congressional attention to the problems of predatory mortgage lending has led for calls for the Federal Reserve Board to use its authority

Hinckley Allen Client Update 6.21.13 Nancy R. Wilsker

Alert Mortgage Foreclosure Procedures New Massachusetts Regulations Effective June 21, 2013 Hinckley Allen Client Update 6.21.13 Nancy R. Wilsker This is a summary of a detailed and complex Massachusetts

Alert Mortgage Foreclosure Procedures New Massachusetts Regulations Effective June 21, 2013 Hinckley Allen Client Update 6.21.13 Nancy R. Wilsker This is a summary of a detailed and complex Massachusetts

To: Counsel, Agents, and Readers From: Michael J. Berey Dated: September 5, 2008 Re: Mortgages: Chapter 472, Laws of 2008

To: Counsel, Agents, and Readers From: Michael J. Berey Dated: September 5, 2008 Re: Mortgages: Chapter 472, Laws of 2008 Chapter 472 of the Laws of 2008 was signed into law on August 5, 2008. According

To: Counsel, Agents, and Readers From: Michael J. Berey Dated: September 5, 2008 Re: Mortgages: Chapter 472, Laws of 2008 Chapter 472 of the Laws of 2008 was signed into law on August 5, 2008. According

What You Should Know About Home Equity Lines of Credit and Important Terms of FlexEquity SM

What You Should Know About Home Equity Lines of Credit and Important Terms of FlexEquity SM Effective March 1, 2008 The Housing Financial Discrimination Act of 1977 Fair Lending Notice It is illegal to

What You Should Know About Home Equity Lines of Credit and Important Terms of FlexEquity SM Effective March 1, 2008 The Housing Financial Discrimination Act of 1977 Fair Lending Notice It is illegal to

Assembly Bill No. 344 CHAPTER 733

Assembly Bill No. 344 CHAPTER 733 An act to amend Sections 4970, 4973, 4974, 4975, 4977, 4978, 4978.6, 4979, and 4979.7 of the Financial Code, as added by Assembly Bill 489 of the 2001-02 Regular Session,

Assembly Bill No. 344 CHAPTER 733 An act to amend Sections 4970, 4973, 4974, 4975, 4977, 4978, 4978.6, 4979, and 4979.7 of the Financial Code, as added by Assembly Bill 489 of the 2001-02 Regular Session,

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 1991 H 1 HOUSE BILL 22

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION H HOUSE BILL Short Title: Regulate Reverse Mortgages. (Public) Sponsors: Representatives Brubaker, Easterling, Hasty, Ligon, Lineberry, Privette, and Woodard.

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION H HOUSE BILL Short Title: Regulate Reverse Mortgages. (Public) Sponsors: Representatives Brubaker, Easterling, Hasty, Ligon, Lineberry, Privette, and Woodard.

Regulatory Practice Letter February 2013 RPL 13-07

Regulatory Practice Letter February 2013 RPL 13-07 High Cost Mortgages and Homeownership Counseling; Escrow Requirements - CFPB Final Rules Executive Summary The Bureau of Consumer Financial Protection

Regulatory Practice Letter February 2013 RPL 13-07 High Cost Mortgages and Homeownership Counseling; Escrow Requirements - CFPB Final Rules Executive Summary The Bureau of Consumer Financial Protection

BILL ANALYSIS. Senate Research Center S.B. 173 By: Patterson State Affairs 3-24-97 Committee Report (Amended)

") BILL ANALYSIS Senate Research Center S.B. 173 By: Patterson State Affairs 3-24-97 Committee Report (Amended) DIGEST Currently, the Texas Constitution prohibits the use of equity in a home for collateral

BILL ANALYSIS Senate Research Center S.B. 173 By: Patterson State Affairs 3-24-97 Committee Report (Amended) DIGEST Currently, the Texas Constitution prohibits the use of equity in a home for collateral

MORTGAGE REFORM AND THE IMPACT ON FINANCING AND FORECLOSURES

MORTGAGE REFORM AND THE IMPACT ON FINANCING AND FORECLOSURES Lauren E. Winters, Senior Policy Analyst (503) 947-7039 Department of Consumer and Business Services, March 20, 2013 IMPORTANT INFORMATION ABOUT

MORTGAGE REFORM AND THE IMPACT ON FINANCING AND FORECLOSURES Lauren E. Winters, Senior Policy Analyst (503) 947-7039 Department of Consumer and Business Services, March 20, 2013 IMPORTANT INFORMATION ABOUT

SB 1343. REFERENCE TITLE: home loans; prohibited activities. State of Arizona Senate Forty-fifth Legislature Second Regular Session 2002

PLEASE NOTE: In most BUT NOT ALL instances, the page and line numbering of bills on this web site correspond to the page and line numbering of the official printed version of the bills. REFERENCE TITLE:

PLEASE NOTE: In most BUT NOT ALL instances, the page and line numbering of bills on this web site correspond to the page and line numbering of the official printed version of the bills. REFERENCE TITLE:

2012 Foreclosure Trends Report

2012 2012 Foreclosure Trends Report Division of Banks Commonwealth of Massachusetts 12/20/2013 Background In November of 2007, to address rising foreclosures in the Commonwealth, Governor Deval Patrick

2012 2012 Foreclosure Trends Report Division of Banks Commonwealth of Massachusetts 12/20/2013 Background In November of 2007, to address rising foreclosures in the Commonwealth, Governor Deval Patrick

High-Cost, Higher-Priced What s the Difference? Comparison of the Similarities and Differences of Terms in Regulation Z

High-Cost, Higher-Priced What s the Difference? Comparison of the Similarities and Differences of Terms in Regulation Z Regulation Z uses the terms high-cost mortgage, higher-priced mortgage and higher-priced

High-Cost, Higher-Priced What s the Difference? Comparison of the Similarities and Differences of Terms in Regulation Z Regulation Z uses the terms high-cost mortgage, higher-priced mortgage and higher-priced

Mon. ICBA Summary of the Military Lending Act Updated Regulation. August 2015. Month Year. Contact:

ICBA Summary of the Military Lending Act Updated Regulation August 2015 Month Year Mon Contact: Joe Gormley Assistant Vice President & Regulatory Counsel joseph.gormley@icba.org www.icba.org ICBA Summary

ICBA Summary of the Military Lending Act Updated Regulation August 2015 Month Year Mon Contact: Joe Gormley Assistant Vice President & Regulatory Counsel joseph.gormley@icba.org www.icba.org ICBA Summary

FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA. General Background

March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted by Congress in 1975, requires most mortgage lenders

March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted by Congress in 1975, requires most mortgage lenders

Mortgage Lending laws and how it affects you, the REALTOR. Presented by Anders Hostelley and Leonard Loventhal

Mortgage Lending laws and how it affects you, the REALTOR. Presented by Anders Hostelley and Leonard Loventhal Secure and Fair Enforcement for Mortgage Licensing Act Title V of P.L. 110-289, the Secure

Mortgage Lending laws and how it affects you, the REALTOR. Presented by Anders Hostelley and Leonard Loventhal Secure and Fair Enforcement for Mortgage Licensing Act Title V of P.L. 110-289, the Secure

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2009 SESSION LAW 2009-457 HOUSE BILL 1222

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2009 SESSION LAW 2009-457 HOUSE BILL 1222 AN ACT TO UPDATE THE RATE SPREAD AND HIGH-COST HOME LOANS STATUTES, AND TO MAKE A CONFORMING CHANGE TO THE EMERGENCY

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2009 SESSION LAW 2009-457 HOUSE BILL 1222 AN ACT TO UPDATE THE RATE SPREAD AND HIGH-COST HOME LOANS STATUTES, AND TO MAKE A CONFORMING CHANGE TO THE EMERGENCY

MRS Title 9-A 8-103. Definitions and rules of construction

9-A 8-103. Definitions and rules of construction The text included in this publication was prepared by the Maine Bureau of Financial Institutions and is current through July 15, 2008. It is a version that

9-A 8-103. Definitions and rules of construction The text included in this publication was prepared by the Maine Bureau of Financial Institutions and is current through July 15, 2008. It is a version that

CFPB Issues Much Anticipated Final Rules: Ability to Repay, Qualified Mortgages, Escrow Requirements and Homeownership Counseling

CFPB Issues Much Anticipated Final Rules: Ability to Repay, Qualified Mortgages, Escrow Requirements and Homeownership Counseling The Consumer Financial Protection Bureau ( CFPB ) issued their much anticipated

CFPB Issues Much Anticipated Final Rules: Ability to Repay, Qualified Mortgages, Escrow Requirements and Homeownership Counseling The Consumer Financial Protection Bureau ( CFPB ) issued their much anticipated

CHAPTER 11 ADJUSTABLE MORTGAGE LOANS [Prior to 3/25/87, Auditor of State[130] Ch 11]

![CHAPTER 11 ADJUSTABLE MORTGAGE LOANS [Prior to 3/25/87, Auditor of State[130] Ch 11]](/thumbs/32/15352082.jpg "CHAPTER 11 ADJUSTABLE MORTGAGE LOANS [Prior to 3/25/87, Auditor of State[130] Ch 11]") Ch 11, p.1 CHAPTER 11 ADJUSTABLE MORTGAGE LOANS [Prior to 3/25/87, Auditor of State[130] Ch 11] 197 11.1(534) Authorization. 11.1(1) A state-chartered savings and loan association may make, purchase or

Ch 11, p.1 CHAPTER 11 ADJUSTABLE MORTGAGE LOANS [Prior to 3/25/87, Auditor of State[130] Ch 11] 197 11.1(534) Authorization. 11.1(1) A state-chartered savings and loan association may make, purchase or

Uncertainty Regarding Fed Proposal and CFPB Action on Minimum Underwriting Standards for Consideration of a Consumer s Ability to Repay

June 2011 Uncertainty Regarding Fed Proposal and CFPB Action on Minimum Underwriting Standards for Consideration of a Consumer s Ability to Repay BY KEVIN L. PETRASIC, HELEN Y. LEE & AMANDA M. JABOUR Comments

June 2011 Uncertainty Regarding Fed Proposal and CFPB Action on Minimum Underwriting Standards for Consideration of a Consumer s Ability to Repay BY KEVIN L. PETRASIC, HELEN Y. LEE & AMANDA M. JABOUR Comments

FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA. General Background

April 3, 2006 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted by Congress in 1975, requires most mortgage lenders

April 3, 2006 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted by Congress in 1975, requires most mortgage lenders

The New Mortgage Servicing Rules. FMS East Coast Regional Conference September 17, 2013

The New Mortgage Servicing Rules FMS East Coast Regional Conference September 17, 2013 What are the new Mortgage Servicing Rules? Ability to Repay/Qualified Mortgage Rule 2013 HOEPA Rule Loan Originator

The New Mortgage Servicing Rules FMS East Coast Regional Conference September 17, 2013 What are the new Mortgage Servicing Rules? Ability to Repay/Qualified Mortgage Rule 2013 HOEPA Rule Loan Originator

The CFPB s Ability-to-Repay Regulation Z Rules: (12 CFR 1026.43)

") The CFPB s Ability-to-Repay Regulation Z Rules: (12 CFR 1026.43) This has been updated to include changes from the CFPB final rule issued on September 13, 2013. In addition, this CompNOTES only covers

The CFPB s Ability-to-Repay Regulation Z Rules: (12 CFR 1026.43) This has been updated to include changes from the CFPB final rule issued on September 13, 2013. In addition, this CompNOTES only covers

The New Ability-to-Pay Rules; Qualified Mortgage Lending under the Dodd-Frank Act

The New Ability-to-Pay Rules; Qualified Mortgage Lending under the Dodd-Frank Act October 2011 Scott D. Samlin Partner T +1 212-398-5819 scott.samlin@snrdenton.com Stephen F. J. Ornstein Partner T +1 202-408-9122

The New Ability-to-Pay Rules; Qualified Mortgage Lending under the Dodd-Frank Act October 2011 Scott D. Samlin Partner T +1 212-398-5819 scott.samlin@snrdenton.com Stephen F. J. Ornstein Partner T +1 202-408-9122

Senate Bill 1149 Summary -- Prohibit Predatory Lending

MEMORANDUM TO: FROM: Hal D. Lingerfelt Commissioner of Banks L. McNeil Chestnut Assistant Attorney General DATE: August 25, 1999 RE: Senate Bill 1149 Summary -- Prohibit Predatory Lending I. Background

MEMORANDUM TO: FROM: Hal D. Lingerfelt Commissioner of Banks L. McNeil Chestnut Assistant Attorney General DATE: August 25, 1999 RE: Senate Bill 1149 Summary -- Prohibit Predatory Lending I. Background

BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law MEMORANDUM

BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law J. Alton Alsup 10333 Richmond, Suite 860 Telephone 713/468-0400 Board Certified in Residential Real Estate Law Texas Board of Legal Specialization

BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law J. Alton Alsup 10333 Richmond, Suite 860 Telephone 713/468-0400 Board Certified in Residential Real Estate Law Texas Board of Legal Specialization

Comparison of Section 35(HPML) & Section 43(HPCT) Regulations

& Section 43(HPCT) Regulations") Comparison of Section 35(HPML) & Section 43(HPCT) Regulations As of 01/07/2014-VS General Consumer Loan Type Not Applicable A closed-end consumer credit transaction secured by the consumer s principal

Comparison of Section 35(HPML) & Section 43(HPCT) Regulations As of 01/07/2014-VS General Consumer Loan Type Not Applicable A closed-end consumer credit transaction secured by the consumer s principal

New Mortgage Rules Update

New Mortgage Rules Update 1 OBJECTIVES To provide information regarding the new mortgage rules, in particular: Ability-to-Repay/Qualified Mortgages; Mortgage Loan Origination Compensation; High-Cost Loans

New Mortgage Rules Update 1 OBJECTIVES To provide information regarding the new mortgage rules, in particular: Ability-to-Repay/Qualified Mortgages; Mortgage Loan Origination Compensation; High-Cost Loans

63rd Legislature AN ACT REPEALING THE MONTANA TITLE LOAN ACT; AMENDING SECTIONS 31-1-106, 31-1-111,

63rd Legislature HB0118 AN ACT REPEALING THE MONTANA TITLE LOAN ACT; AMENDING SECTIONS 31-1-106, 31-1-111, 31-1-112, 31-1-401, AND 32-5-103, MCA; REPEALING SECTIONS 31-1-801, 31-1-802, 31-1-803, 31-1-804,

63rd Legislature HB0118 AN ACT REPEALING THE MONTANA TITLE LOAN ACT; AMENDING SECTIONS 31-1-106, 31-1-111, 31-1-112, 31-1-401, AND 32-5-103, MCA; REPEALING SECTIONS 31-1-801, 31-1-802, 31-1-803, 31-1-804,

4/20/2015. Dodd Frank Sections 1411 and 1412. Defines pretty specifically the terms and dimensions of each. On this one, you can't blame the CFPB

Ability To Repay and Qualified Mortgages Presented by: TriComply, a Temenos Product Presenter: Blair Rugh, Compliance Director Florida Banker's Association, Annual Consumer Compliance Seminar April 29

Ability To Repay and Qualified Mortgages Presented by: TriComply, a Temenos Product Presenter: Blair Rugh, Compliance Director Florida Banker's Association, Annual Consumer Compliance Seminar April 29

JANUARY 2014. Shopping for a mortgage? What you can expect under federal rules

JANUARY 2014 Shopping for a mortgage? What you can expect under federal rules You ll be offered a mortgage that s set up to be affordable. When you apply for a mortgage, you may struggle to understand

JANUARY 2014 Shopping for a mortgage? What you can expect under federal rules You ll be offered a mortgage that s set up to be affordable. When you apply for a mortgage, you may struggle to understand

Consumer Handbook on Home Equity Lines of Credit

Consumer Handbook on Home Equity Lines of Credit The Housing Financial Discrimination Act of 1977 Fair Lending Notice (CALIFORNIA RESIDENTS ONLY) It is illegal to discriminate in the provision of or in

Consumer Handbook on Home Equity Lines of Credit The Housing Financial Discrimination Act of 1977 Fair Lending Notice (CALIFORNIA RESIDENTS ONLY) It is illegal to discriminate in the provision of or in

Break Out Session: Mortgage Loan Underwriting and Pricing

Break Out Session: Mortgage Loan Underwriting and Pricing Agenda Ability to Repay (ATR)/Qualified Mortgages (QMs) Effective Date: Applications received on or after January 10, 2014 2013 Home Ownership

Break Out Session: Mortgage Loan Underwriting and Pricing Agenda Ability to Repay (ATR)/Qualified Mortgages (QMs) Effective Date: Applications received on or after January 10, 2014 2013 Home Ownership

Objectives for today s program

2013-2014 Connecticut Legislative Update Fritz Conway Gaffney, Bennett & Associates Norm Roos Robinson+Cole, LLP June 11, 2014 Objectives for today s program Discuss the following: CMBA initiatives enacted

2013-2014 Connecticut Legislative Update Fritz Conway Gaffney, Bennett & Associates Norm Roos Robinson+Cole, LLP June 11, 2014 Objectives for today s program Discuss the following: CMBA initiatives enacted

SHOPPING FOR A MORTGAGE

SHOPPING FOR A MORTGAGE The Traditional Fixed-Rate Mortgage Key characteristics: Level payments, fixed interest rate, fixed term. This mortgage is the one which most of us know, and it is still the loan

SHOPPING FOR A MORTGAGE The Traditional Fixed-Rate Mortgage Key characteristics: Level payments, fixed interest rate, fixed term. This mortgage is the one which most of us know, and it is still the loan

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Interest-Only Mortgage Payments and Payment-Option ARMs Are They for You?

Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation National Credit Union Administration Office of the Comptroller of the Currency Office of Thrift Supervision Interest-Only

Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation National Credit Union Administration Office of the Comptroller of the Currency Office of Thrift Supervision Interest-Only

TILA Escrow Requirements for High Priced Mortgage Loans (12 CFR 1026.35)

") TILA Escrow Requirements for High Priced Mortgage Loans (12 CFR 1026.35) The Consumer Financial Protection Bureau s (CFPB) mortgage rules include new escrow account requirements for higher-priced mortgage

TILA Escrow Requirements for High Priced Mortgage Loans (12 CFR 1026.35) The Consumer Financial Protection Bureau s (CFPB) mortgage rules include new escrow account requirements for higher-priced mortgage

TITLE I-RESIDENTIAL MORTGAGE LOAN ORIGINATION STANDARDS

TITLE I-RESIDENTIAL MORTGAGE LOAN ORIGINATION STANDARDS Residential Mortgage Origination: Adds a number of new regulations and requirements to mortgage loan originators. The bill requires originators to

TITLE I-RESIDENTIAL MORTGAGE LOAN ORIGINATION STANDARDS Residential Mortgage Origination: Adds a number of new regulations and requirements to mortgage loan originators. The bill requires originators to

NEW CFPB RULES FOR HIGH COST MORTGAGES AND HOMEOWNERSHIP COUNSELING February 3, 2013

NEW CFPB RULES FOR HIGH COST MORTGAGES AND HOMEOWNERSHIP COUNSELING February 3, 2013 On January 10, 2013, the Consumer Financial Protection Bureau ( CFPB ) issued a final rule that carries out changes

NEW CFPB RULES FOR HIGH COST MORTGAGES AND HOMEOWNERSHIP COUNSELING February 3, 2013 On January 10, 2013, the Consumer Financial Protection Bureau ( CFPB ) issued a final rule that carries out changes

MORTGAGE TERMS. Assignment of Mortgage A document used to transfer ownership of a mortgage from one party to another.

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

Frequently Asked Questions Short Sale Negotiators & Foreclosure Consultants

***These questions and answers represent a majority of the specific issues contained in the questions that were collected at the Fraud Symposium. The answers are a collaborative effort from DOJ, DCBS and

***These questions and answers represent a majority of the specific issues contained in the questions that were collected at the Fraud Symposium. The answers are a collaborative effort from DOJ, DCBS and

IC 24-9-3 Chapter 3. Prohibited Lending Practices Generally

IC 24-9-3 Chapter 3. Prohibited Lending Practices Generally IC 24-9-3-0.1 Chapter not applicable to loans made before January 1, 2005 Sec. 0.1. Notwithstanding the addition of this chapter and IC 24-9-4

IC 24-9-3 Chapter 3. Prohibited Lending Practices Generally IC 24-9-3-0.1 Chapter not applicable to loans made before January 1, 2005 Sec. 0.1. Notwithstanding the addition of this chapter and IC 24-9-4

Be it enacted by the People of the State of Illinois,

AN ACT concerning financial regulation. Be it enacted by the People of the State of Illinois, represented in the General Assembly: Section 5. The Illinois Credit Union Act is amended by changing Sections

AN ACT concerning financial regulation. Be it enacted by the People of the State of Illinois, represented in the General Assembly: Section 5. The Illinois Credit Union Act is amended by changing Sections

Enrolled Copy S.B. 120

Enrolled Copy S.B. 120 1 REGULATION OF REVERSE MORTGAGES 2 2015 GENERAL SESSION 3 STATE OF UTAH 4 Chief Sponsor: Wayne A. Harper 5 House Sponsor: Ken Ivory 6 7 LONG TITLE 8 General Description: 9 This

Enrolled Copy S.B. 120 1 REGULATION OF REVERSE MORTGAGES 2 2015 GENERAL SESSION 3 STATE OF UTAH 4 Chief Sponsor: Wayne A. Harper 5 House Sponsor: Ken Ivory 6 7 LONG TITLE 8 General Description: 9 This

CFPB proposes amendments to the ability-to-repay and qualified mortgage rules

1 MARCH 15, 2013 CFPB proposes amendments to the ability-to-repay and qualified mortgage rules By Raymond J. Gustini and Lloyd H. Spencer The Consumer Financial Protection Bureau ( CFPB or the Bureau )

1 MARCH 15, 2013 CFPB proposes amendments to the ability-to-repay and qualified mortgage rules By Raymond J. Gustini and Lloyd H. Spencer The Consumer Financial Protection Bureau ( CFPB or the Bureau )

Title 9-A: MAINE CONSUMER CREDIT CODE

Maine Revised Statutes Title 9-A: MAINE CONSUMER CREDIT CODE Article : 8-506. ENHANCED RESTRICTIONS ON CERTAIN CREDITORS In addition to the compliance requirements of section 8-504, subsection 1, unless

Maine Revised Statutes Title 9-A: MAINE CONSUMER CREDIT CODE Article : 8-506. ENHANCED RESTRICTIONS ON CERTAIN CREDITORS In addition to the compliance requirements of section 8-504, subsection 1, unless

Home Mortgage Disclosure Act 1

Home Mortgage Disclosure Act 1 The Home Mortgage Disclosure Act (HMDA) was enacted by the Congress in 1975 and is implemented by Regulation C (12 CFR Part 1003). 2 The period of 1988 through 1992 saw substantial

Home Mortgage Disclosure Act 1 The Home Mortgage Disclosure Act (HMDA) was enacted by the Congress in 1975 and is implemented by Regulation C (12 CFR Part 1003). 2 The period of 1988 through 1992 saw substantial

Chapter 30 Home Equity Conversion Mortgages. 47-30-103. Authorized lenders Designation Application.

Chapter 30 Home Equity Conversion Mortgages 47-30-101. Short title. 47-30-102. Definitions. 47-30-103. Authorized lenders Designation Application. 47-30-104. Compliance Noncomplying loans unenforceable

Chapter 30 Home Equity Conversion Mortgages 47-30-101. Short title. 47-30-102. Definitions. 47-30-103. Authorized lenders Designation Application. 47-30-104. Compliance Noncomplying loans unenforceable

STATE OF OKLAHOMA. 2nd Session of the 44th Legislature (1994) AS INTRODUCED An Act relating to mortgages; providing for reverse

AS INTRODUCED An Act relating to mortgages; providing for reverse") STATE OF OKLAHOMA 2nd Session of the 44th Legislature (1994) HOUSE BILL NO. 2004 By: Caldwell AS INTRODUCED An Act relating to mortgages; providing for reverse mortgages; stating legislative intent; providing

STATE OF OKLAHOMA 2nd Session of the 44th Legislature (1994) HOUSE BILL NO. 2004 By: Caldwell AS INTRODUCED An Act relating to mortgages; providing for reverse mortgages; stating legislative intent; providing

CHAPTER 114. (Senate Bill 1036) Credit Regulation Mortgage Loans Proof of Ability to Repay Exception

Credit Regulation Mortgage Loans Proof of Ability to Repay Exception") CHAPTER 114 (Senate Bill 1036) AN ACT concerning Credit Regulation Mortgage Loans Proof of Ability to Repay Exception FOR the purpose of establishing an exception certain exceptions for certain mortgage

CHAPTER 114 (Senate Bill 1036) AN ACT concerning Credit Regulation Mortgage Loans Proof of Ability to Repay Exception FOR the purpose of establishing an exception certain exceptions for certain mortgage

NC General Statutes - Chapter 53 Article 21 1

Article 21. Reverse Mortgages. 53-255. Title. This Article shall be known and may be cited as the Reverse Mortgage Act. (1991, c. 546, s. 1; 1995, c. 115, s. 1.) 53-256. Purpose. It is the intent of the

Article 21. Reverse Mortgages. 53-255. Title. This Article shall be known and may be cited as the Reverse Mortgage Act. (1991, c. 546, s. 1; 1995, c. 115, s. 1.) 53-256. Purpose. It is the intent of the

GLOSSARY COMMONLY USED REAL ESTATE TERMS

GLOSSARY COMMONLY USED REAL ESTATE TERMS Adjustable-Rate Mortgage (ARM): a mortgage loan with an interest rate that is subject to change and is not fixed at the same level for the life of the loan. These

GLOSSARY COMMONLY USED REAL ESTATE TERMS Adjustable-Rate Mortgage (ARM): a mortgage loan with an interest rate that is subject to change and is not fixed at the same level for the life of the loan. These

Loan Originator Compensation: The New Paradigm

Loan Originator Compensation: The New Paradigm Presented for Maryland Association of Mortgage Professionals on March 3, 2011 by Marjorie A. Corwin Gordon, Feinblatt, Rothman, Hoffberger & Hollander, LLC

Loan Originator Compensation: The New Paradigm Presented for Maryland Association of Mortgage Professionals on March 3, 2011 by Marjorie A. Corwin Gordon, Feinblatt, Rothman, Hoffberger & Hollander, LLC

CHAPTER 10: LEVERAGED LOANS SECTION 1: UNDERSTANDING LEVERAGED LOANS

CHAPTER 10: LEVERAGED LOANS SECTION 1: UNDERSTANDING LEVERAGED LOANS 10.1 OVERVIEW A leveraged loan is an Agency loan that is supplemented by an affordable housing loan or grant from another funding source

CHAPTER 10: LEVERAGED LOANS SECTION 1: UNDERSTANDING LEVERAGED LOANS 10.1 OVERVIEW A leveraged loan is an Agency loan that is supplemented by an affordable housing loan or grant from another funding source

This chapter shall be known and may be cited as the "Home Equity Conversion Mortgage Act."

Source: http://www.lexisnexis.com/hottopics/tncode/ 47-30-101. Short title. This chapter shall be known and may be cited as the "Home Equity Conversion Mortgage Act." HISTORY: Acts 1993, ch. 410, 2. 47-30-102.

Source: http://www.lexisnexis.com/hottopics/tncode/ 47-30-101. Short title. This chapter shall be known and may be cited as the "Home Equity Conversion Mortgage Act." HISTORY: Acts 1993, ch. 410, 2. 47-30-102.

BILL ANALYSIS. Senate Research Center H.B. 1188 By: Danburg (Patterson, Harris) State Affairs 5-14-97 Engrossed

State Affairs 5-14-97 Engrossed") BILL ANALYSIS Senate Research Center H.B. 1188 By: Danburg (Patterson, Harris) State Affairs 5-14-97 Engrossed DIGEST Currently, state law permits a homeowner to use a home as collateral for only five

BILL ANALYSIS Senate Research Center H.B. 1188 By: Danburg (Patterson, Harris) State Affairs 5-14-97 Engrossed DIGEST Currently, state law permits a homeowner to use a home as collateral for only five

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2003 SESSION LAW 2004-171 SENATE BILL 676

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2003 SESSION LAW 2004-171 SENATE BILL 676 AN ACT TO AMEND CERTAIN BANKING LAWS OF NORTH CAROLINA AND TO AUTHORIZE THE LEGISLATIVE RESEARCH COMMISSION TO STUDY

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2003 SESSION LAW 2004-171 SENATE BILL 676 AN ACT TO AMEND CERTAIN BANKING LAWS OF NORTH CAROLINA AND TO AUTHORIZE THE LEGISLATIVE RESEARCH COMMISSION TO STUDY

CHAPTER 454M MORTGAGE SERVICERS

CHAPTER 454M MORTGAGE SERVICERS SECTION 454M-1 Definitions 454M-2 License required 454M-2.5 Unlicensed foreclosure actions voided 454M-3 Exemptions 454M-4 License; fees; renewals; voluntary surrender of

CHAPTER 454M MORTGAGE SERVICERS SECTION 454M-1 Definitions 454M-2 License required 454M-2.5 Unlicensed foreclosure actions voided 454M-3 Exemptions 454M-4 License; fees; renewals; voluntary surrender of

CHAPTER 86. C.46:10B-36 Short title. 1. This act shall be known and may be cited as the Save New Jersey Homes Act of 2008.

CHAPTER 86 AN ACT concerning certain residential mortgages, and supplementing Title 46 of the Revised Statutes. BE IT ENACTED by the Senate and General Assembly of the State of New Jersey: C.46:10B-36

CHAPTER 86 AN ACT concerning certain residential mortgages, and supplementing Title 46 of the Revised Statutes. BE IT ENACTED by the Senate and General Assembly of the State of New Jersey: C.46:10B-36

LOAN WORKSHEET #10 HOME EQUITY LENDING

LOAN WORKSHEET #10 HOME EQUITY LENDING OVERVIEW Home equity lending in Texas was allowed by an amendment to the Texas Constitution approved by the voters on November 4, 1997 and became effective January

LOAN WORKSHEET #10 HOME EQUITY LENDING OVERVIEW Home equity lending in Texas was allowed by an amendment to the Texas Constitution approved by the voters on November 4, 1997 and became effective January

FOR IMMEDIATE RELEASE November 7, 2013 MEDIA CONTACT: Lisa Gagnon 703-903-3385 INVESTOR CONTACT: Robin Phillips 571-382-4732

FOR IMMEDIATE RELEASE MEDIA CONTACT: Lisa Gagnon 703-903-3385 INVESTOR CONTACT: Robin Phillips 571-382-4732 FREDDIE MAC REPORTS PRE-TAX INCOME OF $6.5 BILLION FOR THIRD QUARTER 2013 Release of Valuation

FOR IMMEDIATE RELEASE MEDIA CONTACT: Lisa Gagnon 703-903-3385 INVESTOR CONTACT: Robin Phillips 571-382-4732 FREDDIE MAC REPORTS PRE-TAX INCOME OF $6.5 BILLION FOR THIRD QUARTER 2013 Release of Valuation

Citi U.S. Mortgage Lending Data and Servicing Foreclosure Prevention Efforts

Citi U.S. Mortgage Lending Data and Servicing Foreclosure Prevention Efforts Third Quarter 28 EXECUTIVE SUMMARY In February 28, we published our initial data report on Citi s U.S. mortgage lending businesses,

Citi U.S. Mortgage Lending Data and Servicing Foreclosure Prevention Efforts Third Quarter 28 EXECUTIVE SUMMARY In February 28, we published our initial data report on Citi s U.S. mortgage lending businesses,

9-Jul-08 State Responses to Housing Crisis: Legislative Solutions

9-Jul-08 State Responses to Housing Crisis: Legislative Solutions Arkansas 4/16/03 7/15/03 HB 2598 California 7/8/08 7/8/08 SB 1137 10/5/07 10/5/07 SB 223 10/5/07 SB 385 Enacts Arkansas Home Loan Protection

9-Jul-08 State Responses to Housing Crisis: Legislative Solutions Arkansas 4/16/03 7/15/03 HB 2598 California 7/8/08 7/8/08 SB 1137 10/5/07 10/5/07 SB 223 10/5/07 SB 385 Enacts Arkansas Home Loan Protection

TILA RESPA Integrated Disclosure

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-25(E) Mortgage Loan Transaction Closing Disclosure Refinance Transaction Sample This is a sample of a completed Closing Disclosure for the refinance

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-25(E) Mortgage Loan Transaction Closing Disclosure Refinance Transaction Sample This is a sample of a completed Closing Disclosure for the refinance

The CFPB s Qualified Mortgage Requirements from the ATR/QM Final Rule (12 CFR 1026.43)

") The CFPB s Qualified Mortgage Requirements from the ATR/QM Final Rule (12 CFR 1026.43) This has been updated to include changes from the CFPB final rule issued on September 13, 2013. In addition, this

The CFPB s Qualified Mortgage Requirements from the ATR/QM Final Rule (12 CFR 1026.43) This has been updated to include changes from the CFPB final rule issued on September 13, 2013. In addition, this

Be it enacted by the People of the State of Illinois,

SB Enrolled LRB0 EGJ b AN ACT concerning regulation. Be it enacted by the People of the State of Illinois, represented in the General Assembly: Section. The Residential Real Property Disclosure Act is

SB Enrolled LRB0 EGJ b AN ACT concerning regulation. Be it enacted by the People of the State of Illinois, represented in the General Assembly: Section. The Residential Real Property Disclosure Act is