USDA RD Section 502/504 Programs

|

|

|

- Meghan Malone

- 8 years ago

- Views:

Transcription

1 USDA RD Section 502/504 Programs Welcome to HAC s webcast! The webcast, sound, and recording will begin at 2:00 pm EST. Due to the number of participants, questions can only be accepted via the internet. Please click on the Raise Hand button at any time during the webcast and send a chat to the Chairperson.

2 U. S. Department of Agriculture Rural Development Section 502 Direct Loan Program & Section 504 Loan and Elderly Grant Repair Program An Overview

3 Housing Assistance Council Building Rural Communities since 1971 Established in 1971, HAC is a national nonprofit corporation headquartered in Washington, D.C; HAC helps local organizations build affordable homes in rural America by providing: Below Market Financing; Training and Technical Assistance; Research and Information Services. HAC s programs focus on; Local Solutions; Empowerment of the poor; Reduced dependency and self help strategies. HAC s Executive Director is Mr. Moises Loza.

4 Housing Assistance Council Building Rural Communities Established in 1971 National nonprofit organization Created to increase the availability of decent and affordable housing for low income people in rural areas throughout the U.S. Provide services to local, state, and national organizations

5 Housing Assistance Council Housing Assistance Council 1025 Vermont Ave Ste 606 Washington DC (202) Southeast Regional Office 600 West Peachtree Street NW Ste 1500 Atlanta, GA (404) Midwest Regional Office N Ambassador Dr Ste 310 Kansas City, MO (816) midwest@ruralhome.org Southwest Regional Office 3939 C San Pedro, NE Ste 7 Albuquerque, NM (505) southwest@ruralhome.org West Regional Office 717 K Street Ste 404 Sacramento, CA (916) west@ruralhome.org

883 1003 southwest@ruralhome.")

6 HAC s Mission To improve housing conditions for the rural poor, with an emphasis on the poorest of the poor in the most rural places.

7 Services Offered Technical Assistance Training Loan Funds Information & Publications

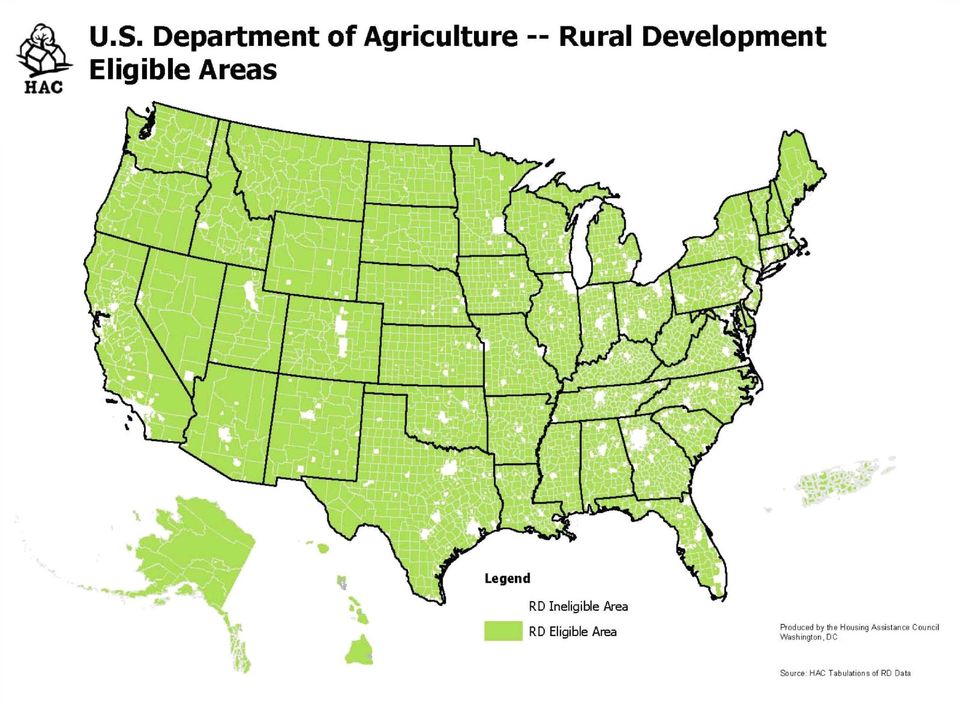

8 HAC News Regular Mail Version Version

9 Rural Voices

10 HAC Loan Products & Structure Uses Predevelopment Land Acquisition Site Development Construction Preservation Gap/Interim Structure Loans Guarantees Compensating Deposits Letters of Credit Lines of Credit

11 HAC Loan Fund at a Glance Loan Product Term Non-Profit Interest Rate For Profit Service Fee Pre-Development Up to 5 years 5% 8% 1% Site Acquisition Up to 5 years 5% 8% 1% Site Development Up to 5 years 5% 8% 1% Construction Varies $750,000 Max 5% 8% 1% Water/Waste Water Up to 5 years 5% 8% 1% Preservation Up to 30 Years 5% 8% 1% Self-Help Housing (SHOP) 2-3 years 0% N/A 1% Land Banking Letter of Credit Line of Credit Up to 10 years $750,000 Max Up to 5 years $250,000 Max Up to 5 years $250,000 Max 5% 8% 1% 5% 8% 1% 5% 8% 1%

12 Section 502 Direct Loan Program at a Glance The Section 502 Program was first authorized in the Housing Act of 1949 and for over 64 years has provided: Low and very low income people the opportunity to own adequate, modest, decent, safe and sanitary homes in rural areas; Critical mortgage credit to rural residents where there has been a serious lack of available credit, or when available, at rates and terms low and very low income rural residents could afford.

13 Section 502 Direct Loan Program at a Glance Rural Development provides direct, as well as guaranteed loans, in rural areas. Rural areas include open country and places with a population of 10,000 or less and, under certain conditions, towns and cities between 10,000 and 25,000 population; Low income is defined as between 50 and 80 percent of area median income (AMI); Very lowincome is at or below 50 percent AMI.

14

15 Section 502 Direct Loan Program at a Glance Loans may be used to: Purchase existing housing; Purchase, relocate and/or repair existing housing; Purchase a building site and construct a dwelling or; Purchase new housing, including manufactured housing (Must be new, permanently installed and from approved dealer or contractor); Refinance debts when necessary. Note: At least 40 percent of appropriated funds must be used to assist families with incomes at or below 50 percent of AMI.

16 Rural Development Service Area and Eligibility Information RD Section 502 Direct Loan Program is a rural program. Service area, income and property eligibility can be determined by contacting the local RD Service Center or online at meaction.do Web link can be used to learn more about a USDA home loan program; Determine if a property is located in an eligible rural area; Determine income eligibility of an applicant/ household; or to find out how to apply for a Rural Development Loan.

17

18 TYPES OF 502 LOANS INITIAL No existing Agency loan, eligible buyer; ASSUMED Eligible applicant: same rates and terms, or new rates and terms; SUBSEQUENT Eligible applicant, loan can be part of original purchase in combination with an assumption, if shortfall for construction funds, or during term of Agency loan to help existing loan pay for repairs or improvements to the property; NON PROGRAM Applicants and/or properties not eligible on program terms.

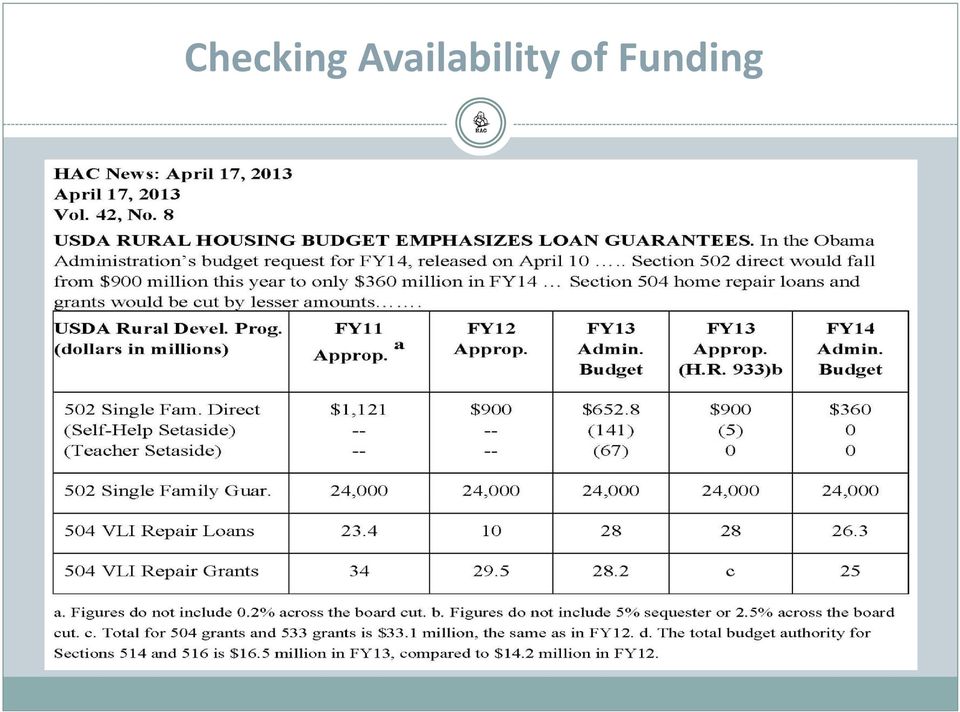

19 Checking Availability of Funding Fiscal year starts October 1 st of each year and ends September 30 th of the next year. Funding varies from State to State. Many States hold funds in the State Office and the Area Offices must request funds. Maintain a close relationship with your Area Office to determine when funds are available and the kind of funds that are available.

20 Checking Availability of Funding

21 POOLING Non obligated funds for redistribution by National Office. Usually occurs in mid July. Applications may be selected for processing based on date completed and on processing priority, in the event there is a waiting list at the local office.

22 Regulations Regulations for all USDA/RD single family housing programs, including Section 502 direct loans, are compiled in 7 CFR Part 3550; Two handbooks provide details and instructions about the various aspects of the 502 program. HB covers tasks undertaken by RD field offices; HB explains the work of the agency s centralized servicing center.

23 Regulations Other Instructions governing the 502 loan program include: 1924 C (Site and Building Design); 1924 A (Construction and Repair); 1940 I (Truth in Lending) and; 1901 E (Civil Rights). (For Handbooks, Instructions, AN s, PN s, UL s, and Forms)

24 Standards Houses constructed, purchased, or rehabilitated with Section 502 loans must meet: Voluntary national model building code adopted by the state; International Code Series, and RD site Standards; Manufactured housing must be permanently installed and meet HUD Manufactured Housing Construction and Safety Standards, 2006 International Energy Conservation Code and RD site standards.

25 Properties Eligible Properties Must be modest in size, design, and cost. The value of a dwelling may not exceed the Area Loan Limits. Area Loan Limits are reviewed annually. n%20limits.htm Sample RD Loan Limits County / State EST LIMIT Effective Starr County, TX $ 130,100 Zavala County, TX $ 141,800 Cheyenne County, CO $ 150,600 Jefferson County, CO $ 250,000

26 Properties Lot Size A modest and adequate lot should not exceed 30 % of the appraised value; and cannot be subdivided to make another house. Prohibited Features Include In ground swimming pools and income producing properties. (Exception 502 Guaranteed Program AN 4701)

27 Rates, Terms and Interest Subsidy The standard term of a Section 502 loan is 33 years. (Applicants unable to afford a loan at 33 year term and have incomes at or below 60 percent of AMI are eligible for an extended term of 38 years.) The borrower s payment for PITI is the higher of: 24 percent of borrower s adjusted annual income; less any eligible leveraged loan payment; less taxes & insurance; or Principal payment calculated at 1 percent on the RD loan, plus any eligible leveraged loan payment, plus taxes & insurance. An eligible leveraged loan for the purposes of payment subsidy only, is a loan with payments amortized over a period not less than 30 years and an interest rate not exceeding 3 percent. (2 % maximum over agency rate)

28 Rates, Terms and Interest Subsidy Payment will never be more than the payment calculated at RD Market Rate at time the loan was made. (Fixed Promissory Note Rate) Private Mortgage Insurance (PMI) is not required.

29 Down Payment Requirements and Asset Limitations A down payment is not required. Loans may be made for up to 100 percent of the market (appraised) value. If the sales price of the property is equal to or less than the appraised value, no down payment is needed. Asset Limitations Cash value above limits must be used toward down payment. Nonretirement Assets vary for Non elderly (> $15,000) and Elderly (> $20,000).

30 Income Eligibility Limits elcomeaction.do?pageaction=pageload&req uestinfo=directincomelimits&navkey=income

31

32 Borrower Eligibility Requirements Have an adjusted income at or below applicable low income limit at loan approval; Be unable to obtain sufficient credit from another source; Agree to personally occupy the dwelling;

33 Borrower Eligibility Requirements Meet citizenship or eligible non citizen requirements; Have the legal capacity to incur a loan obligation; Not be suspended or debarred from participation in Federal programs; Demonstrate both the willingness and ability to repay the loan.

34 Security and Ownership Position RD must be able to foreclose to settle debt. Therefore, RD will seek the best mortgage obtainable. At closing applicant must have an ownership position acceptable to RD which can include: (HB , Section 4) Fee Simple Ownership Title evidenced by a deed with full interest in property to borrower; Secure Leasehold Interest Term must be at least 150 percent of mortgage term; Life Estate or Undivided Interest May require others with interest to co sign; Possessory Rights Native American Lands.

35 Repayment Ratios PITI (principal + interest + taxes + insurance) Very low income family: 29% Low income family: 33% Total Debt Ratio (PITI + long term obligations and deferred debts) Low or Very Low Income: 41%

36 Energy Plus Program Discontinued The Rural Energy Plus Program which allowed a 2% increase to both ratios if the home purchased meets certain energy efficiency standards was discontinued. (Unnumbered Letter ) New Homes Constructed Under Specific Efficiency Programs as a Compensating Factor. (Unnumbered Letter ) Homes built to exceed International Energy Conservation Code results in greater energy efficiency and lower homeowners utility costs by up to 30 percent.

37 Unnumbered letter Energy Efficiency Programs When a new home is constructed under a specific energy efficiency program will be used as a compensating factor, the qualifying ratios may exceed the established thresholds by up to two percentage points. (VLI 31/43 LI 35/43 PITI/TD) Efficiency programs include: Energy Star for New Homes U.S. EPA Green Communities Enterprise Community Partners Challenge Home U.S. Department of Energy Leadership in Energy and Environment Design (LEED) U.S. Green Building Council National Green Building Standard National Association of Home Builders

38 Other Unnumbered Letters RD UNNUMBERED LETTERS Dated Subject Discontinuation of the Rural Energy Plus Program Single Family Direct Loan Program Processing Joint Application for Assistance Single Family Housing Direct Program Modest Housing Determination Property and Repair Inspections for Direct Single Family Housing Programs in Fiscal Year New Homes Constructed Under Specific Efficiency Programs as a Compensating Factor Establishing the 2013 Area Loan Limits Single Family Housing Section 502 Direct Loan Application Processing

39 Subsidy Recapture Requirements If payments are subsidized through a reduction in the interest rate, some of the subsidy granted may have to be repaid when: The title to the property transfers, or; The borrower is no longer living in the dwelling; Unless the borrower ceases to occupy the property for a reason that is acceptable to RD. (HB , Section 5 of Chapter 2)

40 Special 502 Loan Servicing Authority Interest Subsidy Workout Agreement Moratorium (7 CFR ) A moratorium is an agreement between RD and a program borrower to suspend the requirement for the borrower to make payments for up to a 2 year period; A borrower must first be considered for payment subsidy or an increase in payment subsidy. Restructure loan over remaining life of loan.

41 Homebuyer Education First time homebuyers must complete homeowner education training and receive a certificate prior to closing. Certificate valid up to one year prior to closing. The RD State Office will maintain a list of providers with costs to homebuyer (if any). Packagers should refer borrowers to free homebuyer programs first. If there is a charge, the fee may be included in the loan.

42 Civil Rights Laws Packagers are subject to Civil Rights laws, the requirements of RD Instruction 1901 E; and other federal laws, including: The Equal Credit Opportunity Act; Title VIII of the Civil Rights Act of 1968 (Fair Housing Act), as amended; Civil Rights Act of 1964, Title VI; Limited English Proficiency, Executive Order 13166; Section 504 of the Rehabilitation Act of 1973; Americans with Disabilities Act, Title II; Age Discrimination Act of 1975, as amended.

43 Affirmative Fair Housing Marketing Plans (AFHMP) Required when marketing 5 or more housing units; includes packaging. (HB and RD Instruction 1901 E); AFHMP goal is to reflect the demographics in eligible communities (Most Recent Census); The AFHMP should focus on reaching out to under served and unrepresented groups in the service area and the outreach methods to reach them.

44 Affirmative Fair Housing Marketing Plans (AFHMP) To attract applicants least likely to apply for housing in the housing marketing area regardless of their race, color, religion, sex, national origin, disability or familial status. AFHMP plan remains in effect for 1 year; Successful when community contacts are made.

45 Variations There are several variations of the basic Section 502 direct loan program. These include: Mutual self help housing; Manufactured housing; Leveraged Loans (With 20% participation RD will subordinate first position); Loans for Condominiums and in Community land trusts; Housing Demonstration Program; Rural housing disaster loan program; and

46 Variations A Separate Section 502 guaranteed loan program provides government guarantees of loans made by banks or other approved lenders such as state housing agencies, lenders approved by HUD, VA, Fannie Mae, or Freddie Mac; Borrower incomes up to 115 percent AMI; Lender underwrites, inspects, issues credit waiver, sets interest and approves loan; Term up to 30 years with no down payment required.

47 Construction Options / Methods Contractor Built Borrower qualifies for home loan and contracts with a builder to construct the home. Owner Built Borrower qualifies for a home loan, demonstrates expertise to handle subcontracts and build own home.

48 Construction Options / Methods Conditional Commitment (7 CFR ) Builder qualifies the home for RD financing. The builder then finds eligible family to purchase the home. Separating borrower eligibility and home/property eligibility can have advantages in shorter processing times, and program design and financing if assisting multiple borrowers and building multiple SFH units.

49 Construction Options / Methods Conditional Commitment A conditional commitment is a written assurance from RD to a qualified builder, dealer contractor, or seller that a dwelling to be constructed or rehabilitated will be certified as acceptable for purchase by qualified loan applicants, as long as the construction and sales price meet certain conditions.

50 Construction Options / Methods A conditional commitment is not a reservation of loan funds, nor a guarantee that an eligible loan applicant will be available to purchase the property. Provides a reasonable assurance to the builder that the home will be eligible for financing once it is completed. Because an appraisal is completed, a conditional commitment identifies the maximum loan limit for the home and lot as developed. Conditional commitments can be viewed as soft commitments for lending purposes

51

52

53

54 Section 504 Rural Home Repair Loans and Grants

55 Section 504 Home Repair Loans and Grants Purpose: The Very Low Income Housing Repair program provides loans and grants to very low income homeowners to repair, improve, or modernize their dwellings or to remove health and safety hazards.

56 Section 504 Home Repair Loans and Grants Eligibility: Homeowner occupants must be unable to obtain affordable credit elsewhere and must have very low incomes, (below 50 percent of the area median income). Repairs and improvements must make the dwelling more safe and sanitary or remove health and safety hazards.

57 Section 504 Home Repair Loans and Grants Eligibility: Grants are only available to homeowners who are 62 years old or older and cannot repay a Section 504 loan.

58 Section 504 Home Repair Loans and Grants Terms: Loans of up to $20,000 and grants of up to $7,500 are available. Loans are for up to 20 years at 1 percent interest.

59 Section 504 Home Repair Loans and Grants Terms: Grants must be repaid if the property is sold in less than three years. Repairs financed with grant funds must result in the removal of health and safety hazards.

60 Section 504 Home Repair Loans and Grants Terms: A grant/loan combination is made if the applicant can repay part of the cost. Loans and grants can be combined for up to $27,500 in Section 504 assistance.

61 Section 504 Home Repair Loans and Grants Standards: Repaired properties need not meet RHS code requirements, but water and waste systems and related fixtures must meet local health department requirements. Water supply and sewage disposal systems should meet RHS requirements.

62 Section 504 Home Repair Loans and Grants Standards: Major health and safety hazards must be corrected. All work performed must meet local codes and standards.

63 Section 504 Home Repair Loans and Grants Regulation/Handbook: 7 CFR Part 3550 and HB1 3550

64

65

66 Additional Information For additional information on the Section 502 Direct Loan and 504 Home Repair Loan and Grant Programs, and Rural Development, contact the National Office, 1400 Independence Avenue, S.W., Washington, DC 20250; , or your Rural Development State Office which can be identified at or contacted by telephone through

67 Strategic Contacts and Partnerships Keep HAC in mind for potential training, information, loan assistance, and as a gateway to other federal programs, funding notices, or housing information and policy in general; Visit the HAC website at

68 Office Locations Housing Assistance Council 1025 Vermont Ave Ste 606 Washington DC (202) Southeast Regional Office 600 West Peachtree Street NW Ste 1500 Atlanta, GA (404) Midwest Regional Office N Ambassador Dr Ste 310 Kansas City, MO (816) midwest@ruralhome.org Southwest Regional Office 3939 C San Pedro, NE Ste 7 Albuquerque, NM (505) southwest@ruralhome.org West Regional Office 717 K Street Ste 404 Sacramento, CA (916) west@ruralhome.org

69 Wrap Up Participant Questions Conclude

70 Resources Important Websites: Housing Assistance Council Energy Star for New Homes mes.hm_index Enterprise Community Partners Green Communities innovation/enterprise green communities

71 Wrap Up Materials from today s webinar and the recording will be available on HAC s website.

THANKS TO THE HOME DEPOT FOUNDATION

Housing Resources for Rural Veterans National Coalition for Homeless Veterans September 2012 THANKS TO THE HOME DEPOT FOUNDATION Housing Assistance Council Celebrating 40 Years of Building Rural Communities

Housing Resources for Rural Veterans National Coalition for Homeless Veterans September 2012 THANKS TO THE HOME DEPOT FOUNDATION Housing Assistance Council Celebrating 40 Years of Building Rural Communities

An Introduction to Grant Writing

An Introduction to Grant Writing Welcome to HAC s webcast! This webcast is a part of the HAC/OWEESTA Rural Housing and Economic Development webcast series. The webcast, sound, and recording will begin

An Introduction to Grant Writing Welcome to HAC s webcast! This webcast is a part of the HAC/OWEESTA Rural Housing and Economic Development webcast series. The webcast, sound, and recording will begin

CHAPTER 10: LEVERAGED LOANS SECTION 1: UNDERSTANDING LEVERAGED LOANS

CHAPTER 10: LEVERAGED LOANS SECTION 1: UNDERSTANDING LEVERAGED LOANS 10.1 OVERVIEW A leveraged loan is an Agency loan that is supplemented by an affordable housing loan or grant from another funding source

CHAPTER 10: LEVERAGED LOANS SECTION 1: UNDERSTANDING LEVERAGED LOANS 10.1 OVERVIEW A leveraged loan is an Agency loan that is supplemented by an affordable housing loan or grant from another funding source

HAC. Resource Guide USDA RURAL HOUSING SERVICE S SECTION 504 REPAIR AND REHABILATION PROGRAM A GUIDE FOR LOAN AND GRANT APPLICANTS

USDA RURAL HOUSING SERVICE S SECTION 504 REPAIR AND REHABILATION PROGRAM A GUIDE FOR LOAN AND GRANT APPLICANTS HAC Resource Guide Through the Section 504 loan and grant program, the federal Rural Housing

USDA RURAL HOUSING SERVICE S SECTION 504 REPAIR AND REHABILATION PROGRAM A GUIDE FOR LOAN AND GRANT APPLICANTS HAC Resource Guide Through the Section 504 loan and grant program, the federal Rural Housing

506 Loan Terms The Loan amount is $14,000.00 and will be a second mortgage lien closed with a DCA-approved Lender s first mortgage.

Chapter 5 Georgia Dream NSP Purchase Program 501 Georgia Dream NSP Purchase Program The Georgia Dream NSP Purchase Program is funded with proceeds from an allocation of federal funds from the Housing and

Chapter 5 Georgia Dream NSP Purchase Program 501 Georgia Dream NSP Purchase Program The Georgia Dream NSP Purchase Program is funded with proceeds from an allocation of federal funds from the Housing and

CHAPTER 6: UNDERWRITING THE LOAN SECTION 1: OVERVIEW OF THE UNDERWRITING PROCESS

CHAPTER 6: UNDERWRITING THE LOAN SECTION 1: OVERVIEW OF THE UNDERWRITING PROCESS 6.1 INTRODUCTION The underwriting process brings together the applicant eligibility requirements discussed in Chapter 4

CHAPTER 6: UNDERWRITING THE LOAN SECTION 1: OVERVIEW OF THE UNDERWRITING PROCESS 6.1 INTRODUCTION The underwriting process brings together the applicant eligibility requirements discussed in Chapter 4

Brooklyn Park Economic Development Authority

Brooklyn Park Economic Development Authority Neighborhood Stabilization Program NSP HOMEBUYER ASSISTANCE PROGRAM FOR CITY/PARTNER ACQUISITION AND REHAB Program Description & Guidelines July 2011 TABLE

Brooklyn Park Economic Development Authority Neighborhood Stabilization Program NSP HOMEBUYER ASSISTANCE PROGRAM FOR CITY/PARTNER ACQUISITION AND REHAB Program Description & Guidelines July 2011 TABLE

Housing Assistance Council A GUIDE TO FEDERAL HOUSING AND COMMUNITY DEVELOPMENT PROGRAMS FOR SMALL TOWNS AND RURAL AREAS

Housing Assistance Council A GUIDE TO FEDERAL HOUSING AND COMMUNITY DEVELOPMENT PROGRAMS FOR SMALL TOWNS AND RURAL AREAS $7.00 February 2003 Housing Assistance Council 1025 Vermont Avenue, N.W. Suite 606

Housing Assistance Council A GUIDE TO FEDERAL HOUSING AND COMMUNITY DEVELOPMENT PROGRAMS FOR SMALL TOWNS AND RURAL AREAS $7.00 February 2003 Housing Assistance Council 1025 Vermont Avenue, N.W. Suite 606

ReNew Grant Guidelines

Brooklyn Center ReNew Buyer Incentive Program Greater Metropolitan Housing Corporation Program Summary The Economic Development Authority (EDA) of Brooklyn Center, Minnesota (EDA) has partnered with the

Brooklyn Center ReNew Buyer Incentive Program Greater Metropolitan Housing Corporation Program Summary The Economic Development Authority (EDA) of Brooklyn Center, Minnesota (EDA) has partnered with the

USDA Home Loans. USDA Income Limitations. What is a USDA Home Loan?

USDA Home Loans What is a USDA Home Loan? USDA Home Loans provide up to 100% financing for a home purchase or refinance. These loans are guaranteed by the USDA and are serviced by direct lenders that meet

USDA Home Loans What is a USDA Home Loan? USDA Home Loans provide up to 100% financing for a home purchase or refinance. These loans are guaranteed by the USDA and are serviced by direct lenders that meet

SWNCBC OOR Program Guidelines 1

Southwest Nebraska Community Betterment Corporation (SWNCBC) Owner Occupied Rehabilitation Program Guidelines Amended January 20, 2011 PURPOSE : To promote safe, affordable and appropriate housing in the

Southwest Nebraska Community Betterment Corporation (SWNCBC) Owner Occupied Rehabilitation Program Guidelines Amended January 20, 2011 PURPOSE : To promote safe, affordable and appropriate housing in the

FROM: Tammye Treviño (Signed by Tammye Treviño) Administrator Housing and Community Facilities Programs

Administrator Housing and Community Facilities Programs") RD AN No. 4635 (1980-D) April 2, 2012 TO: State Directors Rural Development ATTENTION: Rural Housing Program Directors, Guaranteed Loan Coordinators, Area Directors and Area Specialists FROM: Tammye Treviño

RD AN No. 4635 (1980-D) April 2, 2012 TO: State Directors Rural Development ATTENTION: Rural Housing Program Directors, Guaranteed Loan Coordinators, Area Directors and Area Specialists FROM: Tammye Treviño

COEUR D ALENE TRIBAL HOUSING AUTHORITY MORTGAGE FINANCING ASSISTANCE FINAL POLICY (CDTHA MFA)

") COEUR D ALENE TRIBAL HOUSING AUTHORITY MORTGAGE FINANCING ASSISTANCE FINAL POLICY (CDTHA MFA) November 2006 TABLE OF CONTENTS I. General...3 II. Eligible Recipients...3 III. Selection Criteria...4 IV.

COEUR D ALENE TRIBAL HOUSING AUTHORITY MORTGAGE FINANCING ASSISTANCE FINAL POLICY (CDTHA MFA) November 2006 TABLE OF CONTENTS I. General...3 II. Eligible Recipients...3 III. Selection Criteria...4 IV.

COMMUNITY ACQUISITION REHABILITATION LOAN CARL CARL TERM SHEET AND GUIDELINES

COMMUNITY ACQUISITION REHABILITATION LOAN I. PROGRAM OBJECTIVE CARL CARL TERM SHEET AND GUIDELINES URBAN REDEVELOPMENT AUTHORITY OF PITTSBURGH PITTSBURGH COMMUNITY REINVESTMENT GROUP The main objective

COMMUNITY ACQUISITION REHABILITATION LOAN I. PROGRAM OBJECTIVE CARL CARL TERM SHEET AND GUIDELINES URBAN REDEVELOPMENT AUTHORITY OF PITTSBURGH PITTSBURGH COMMUNITY REINVESTMENT GROUP The main objective

Residential Rehabilitation Loan Program Guidelines

Residential Rehabilitation Loan Program Guidelines City of Middletown Department of Planning, Conservation and Development Community Development Division February 1999 Table of Contents Purpose 1 General

Residential Rehabilitation Loan Program Guidelines City of Middletown Department of Planning, Conservation and Development Community Development Division February 1999 Table of Contents Purpose 1 General

City of Somerville Closing Cost and Down Payment Assistance Programs

City of Somerville Closing Cost and Down Payment Assistance Programs WHAT DO THESE PROGRAMS OFFER? The City of Somerville can provide assistance in purchasing a home through two different programs. You

City of Somerville Closing Cost and Down Payment Assistance Programs WHAT DO THESE PROGRAMS OFFER? The City of Somerville can provide assistance in purchasing a home through two different programs. You

CITY OF HUNTSVILLE, ALABAMA. DOWNPAYMENT ASSISTANCE PROGRAM - DAP Program Description & Guidelines

CITY OF HUNTSVILLE, ALABAMA DOWNPAYMENT ASSISTANCE PROGRAM - DAP Program Description & Guidelines Contact information: Community Development, 120 E. Holmes Ave, Huntsville, Ala. 35801, 256-427-5400, fax.

CITY OF HUNTSVILLE, ALABAMA DOWNPAYMENT ASSISTANCE PROGRAM - DAP Program Description & Guidelines Contact information: Community Development, 120 E. Holmes Ave, Huntsville, Ala. 35801, 256-427-5400, fax.

A Guide To USDA Rural Development Programs and Services

A Guide To USDA Rural Development Programs and Services Vermont/New Hampshire www.rurdev.usda.gov/nh-vthome.html Follow Us on Twitter: http://twitter.com/rd_vtandnh Rural Housing and Community Facilities

A Guide To USDA Rural Development Programs and Services Vermont/New Hampshire www.rurdev.usda.gov/nh-vthome.html Follow Us on Twitter: http://twitter.com/rd_vtandnh Rural Housing and Community Facilities

MICHIGAN STATE HOUSING DEVELOPMENT AUTHORITY COMMUNITY DEVELOPMENT DIVISION

MICHIGAN STATE HOUSING DEVELOPMENT AUTHORITY COMMUNITY DEVELOPMENT DIVISION Subject: SUBSIDY LIMITS AND LIEN REQUIREMENTS Effective Date: September 1, 2015 (revised 10/15/15) This policy defines the subsidy

MICHIGAN STATE HOUSING DEVELOPMENT AUTHORITY COMMUNITY DEVELOPMENT DIVISION Subject: SUBSIDY LIMITS AND LIEN REQUIREMENTS Effective Date: September 1, 2015 (revised 10/15/15) This policy defines the subsidy

CHAPTER 6: LOAN PURPOSES 7 CFR 3555.101

CHAPTER 6: LOAN PURPOSES 7 CFR 3555.101 6.1 INTRODUCTION SFHGLP loan funds can be used to acquire new or existing housing that will be the applicant s principal residence, and to pay costs associated with

CHAPTER 6: LOAN PURPOSES 7 CFR 3555.101 6.1 INTRODUCTION SFHGLP loan funds can be used to acquire new or existing housing that will be the applicant s principal residence, and to pay costs associated with

Joplin Homebuyer s Assistance Program (J-HAP)

") Joplin Homebuyer s Assistance Program (J-HAP) Community Development Block Grant Disaster Recovery (CDBG-DR) Program City of Joplin, Missouri HOMEBUYER ASSISTANCE AGREEMENT THIS AGREEMENT, entered into

Joplin Homebuyer s Assistance Program (J-HAP) Community Development Block Grant Disaster Recovery (CDBG-DR) Program City of Joplin, Missouri HOMEBUYER ASSISTANCE AGREEMENT THIS AGREEMENT, entered into

CITY OF MURFREESBORO AFFORDABLE HOUSING ASSISTANCE PROGRAM POLICIES AND PROCEDURES

CITY OF MURFREESBORO AFFORDABLE HOUSING ASSISTANCE PROGRAM POLICIES AND PROCEDURES 100. Purpose The Murfreesboro Affordable Housing Assistance Program (the Program) encourages homeownership for low-income,

CITY OF MURFREESBORO AFFORDABLE HOUSING ASSISTANCE PROGRAM POLICIES AND PROCEDURES 100. Purpose The Murfreesboro Affordable Housing Assistance Program (the Program) encourages homeownership for low-income,

AFFORDABLE HOUSING SYMPOSIUM FINANCING JOE DIEGO, FACILITATOR

AFFORDABLE HOUSING SYMPOSIUM FINANCING JOE DIEGO, FACILITATOR FINANCING PANEL: USDA RURAL DEVELOPMENT DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT GUAM HOUSING AND URBAN RENEWAL AUTHORITY GUAM HOUSING CORPORATION

AFFORDABLE HOUSING SYMPOSIUM FINANCING JOE DIEGO, FACILITATOR FINANCING PANEL: USDA RURAL DEVELOPMENT DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT GUAM HOUSING AND URBAN RENEWAL AUTHORITY GUAM HOUSING CORPORATION

Southeast Texas Housing Finance Corporation (SETH) 5 Star Texas Advantage Program Invitation to Participate

5 Star Texas Advantage Program Invitation to Participate") Southeast Texas Housing Finance Corporation (SETH) 5 Star Texas Advantage Program Invitation to Participate Southeast Texas Housing Finance Corporation (SETH) is pleased to extend an invitation to its

Southeast Texas Housing Finance Corporation (SETH) 5 Star Texas Advantage Program Invitation to Participate Southeast Texas Housing Finance Corporation (SETH) is pleased to extend an invitation to its

MORTGAGE BANKING TERMS

MORTGAGE BANKING TERMS Acquisition cost: Add-on interest: In a HUD/FHA transaction, the price the borrower paid for the property plus any of the following costs: closing, repairs, or financing (except

MORTGAGE BANKING TERMS Acquisition cost: Add-on interest: In a HUD/FHA transaction, the price the borrower paid for the property plus any of the following costs: closing, repairs, or financing (except

Single Family Housing

Section 502/523/504 Programs Home Ownership Programs Section 502 Direct 100% Section 502 Guaranteed 100% Section 523 Self Help Program Home Repair Programs Section 504 Loan/Grant Program Section 502 Direct

Section 502/523/504 Programs Home Ownership Programs Section 502 Direct 100% Section 502 Guaranteed 100% Section 523 Self Help Program Home Repair Programs Section 504 Loan/Grant Program Section 502 Direct

Southeast Texas Housing Finance Corporation (SETH) 5 Star Texas Advantage Program Invitation to Participate

5 Star Texas Advantage Program Invitation to Participate") Southeast Texas Housing Finance Corporation (SETH) 5 Star Texas Advantage Program Invitation to Participate Southeast Texas Housing Finance Corporation (SETH) is pleased to extend an invitation to its

Southeast Texas Housing Finance Corporation (SETH) 5 Star Texas Advantage Program Invitation to Participate Southeast Texas Housing Finance Corporation (SETH) is pleased to extend an invitation to its

Economic Development and Housing Challenge Program

Economic Development and Housing Challenge Program 8/6/2015 Minnesota Housing does not discriminate on the basis of race, color, creed, national origin, sex, religion, marital status, status with regard

Economic Development and Housing Challenge Program 8/6/2015 Minnesota Housing does not discriminate on the basis of race, color, creed, national origin, sex, religion, marital status, status with regard

Vacant Properties Rehabilitation Program

City of Columbus Department of Development Housing Division Vacant Properties Rehabilitation Program Redevelopment for Homeownership/ Lease-Purchase Guidelines Old Oaks City of Columbus Department of Development

City of Columbus Department of Development Housing Division Vacant Properties Rehabilitation Program Redevelopment for Homeownership/ Lease-Purchase Guidelines Old Oaks City of Columbus Department of Development

Lake County Homebuyer Programs Lender Guidelines as of 1/22/2014

Lake County Homebuyer Programs Lender Guidelines as of 1/22/2014 ABOUT THE AFFORDABLE HOUSING CORPORATION OF LAKE COUNTY AHC is a nonprofit agency that increases and preserves affordable housing opportunities

Lake County Homebuyer Programs Lender Guidelines as of 1/22/2014 ABOUT THE AFFORDABLE HOUSING CORPORATION OF LAKE COUNTY AHC is a nonprofit agency that increases and preserves affordable housing opportunities

13 DOWNPAYMENT PROGRAMS

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Home Advantage Downpayment Assistance Program can

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Home Advantage Downpayment Assistance Program can

The RSH Webinar: Aging In Place will begin shortly

Welcome!! The RSH will begin shortly This will be a muted call, please submit your questions via the Q&A feature. (please do not use chat) Housing Assistance Council Webinar Aging In Place: Home Repair

Welcome!! The RSH will begin shortly This will be a muted call, please submit your questions via the Q&A feature. (please do not use chat) Housing Assistance Council Webinar Aging In Place: Home Repair

Funding Programs: HUD Performance Funding System (operating subsidy for PHA) Private foundation operating grants

Private foundation operating grants") Funding Programs by Funding Tools Federal Funding Programs 1. Owner or participant investment - An investment of funds from agency operation or fees paid by a participant to offset the cost of providing

Funding Programs by Funding Tools Federal Funding Programs 1. Owner or participant investment - An investment of funds from agency operation or fees paid by a participant to offset the cost of providing

PIMA COUNTY COMMUNITY LAND TRUST HOME BUYER SELECTION POLICIES & PROCEDURES

PIMA COUNTY COMMUNITY LAND TRUST HOME BUYER SELECTION POLICIES & PROCEDURES I. OVERVIEW This policy paper is intended to guide the development and implementation of both general and projectspecific homebuyer

PIMA COUNTY COMMUNITY LAND TRUST HOME BUYER SELECTION POLICIES & PROCEDURES I. OVERVIEW This policy paper is intended to guide the development and implementation of both general and projectspecific homebuyer

Definitions. In some cases a survey rather than an ILC is required.

Definitions 1. What is the closing? The closing is a formal meeting at which both the buyer and seller meet to sign all the final documentation required for the buyer's mortgage loan. Once the closing

Definitions 1. What is the closing? The closing is a formal meeting at which both the buyer and seller meet to sign all the final documentation required for the buyer's mortgage loan. Once the closing

CITY OF PASSAIC DEPARTMENT OF COMMUNITY DEVELOPMENT 330 PASSAIC STREET PASSAIC, NEW JERSEY 07055

CASE NUMBER enter number (office use only) CITY OF PASSAIC DEPARTMENT OF COMMUNITY DEVELOPMENT 330 PASSAIC STREET PASSAIC, NEW JERSEY 07055 FIRST TIME HOMEBUYER ASSISTANCE PROGRAM AGREEMENT HUD # APPLICANT

CASE NUMBER enter number (office use only) CITY OF PASSAIC DEPARTMENT OF COMMUNITY DEVELOPMENT 330 PASSAIC STREET PASSAIC, NEW JERSEY 07055 FIRST TIME HOMEBUYER ASSISTANCE PROGRAM AGREEMENT HUD # APPLICANT

Vacant Properties Rehabilitation Program

City of Columbus Department of Development Housing Division Vacant Properties Rehabilitation Program Redevelopment for Homeownership/ Lease-Purchase Guidelines Capital Bond Funds Home Funds NSP 1, 2, 3

City of Columbus Department of Development Housing Division Vacant Properties Rehabilitation Program Redevelopment for Homeownership/ Lease-Purchase Guidelines Capital Bond Funds Home Funds NSP 1, 2, 3

City of Alameda First-Time Homebuyer Program

- City of Alameda First-Time Homebuyer Program Down Payment Assistance Loan for Low to Moderate Income Households The City of Alameda is now accepting applications for its down payment assistance loan.

- City of Alameda First-Time Homebuyer Program Down Payment Assistance Loan for Low to Moderate Income Households The City of Alameda is now accepting applications for its down payment assistance loan.

Office of Community Planning and Development

RELOCATION ASSISTANCE TO DISPLACED HOMEOWNER OCCUPANTS www.hud.gov/relocation U. S. Department of Housing and Urban Development Office of Community Planning and Development Introduction This booklet describes

RELOCATION ASSISTANCE TO DISPLACED HOMEOWNER OCCUPANTS www.hud.gov/relocation U. S. Department of Housing and Urban Development Office of Community Planning and Development Introduction This booklet describes

Workforce Homebuyer. Down Payment Loan Program. Program Orientation Packet. Housing Trust Fund of Santa Barbara County

Housing Trust Fund of Santa Barbara County Workforce Homebuyer Down Payment Loan Program Program Orientation Packet 2013 Housing Trust Fund of Santa Barbara County P. O. Box 60909 Santa Barbara, CA 93160-0909

Housing Trust Fund of Santa Barbara County Workforce Homebuyer Down Payment Loan Program Program Orientation Packet 2013 Housing Trust Fund of Santa Barbara County P. O. Box 60909 Santa Barbara, CA 93160-0909

Chapter 13: Residential and Commercial Property Financing

Chapter 13 Outline / Page 1 Chapter 13: Residential and Commercial Property Financing Understanding the Mortgage Concept - secured vs. unsecured debt - mortgage pledge of property to secure a debt (See

Chapter 13 Outline / Page 1 Chapter 13: Residential and Commercial Property Financing Understanding the Mortgage Concept - secured vs. unsecured debt - mortgage pledge of property to secure a debt (See

CITY OF YOUNGSTOWN HOME BUYER PROGRAM. Community Development Agency Housing Division CITY OF YOUNGSTOWN Mayor Jay Williams. Revised 3/2008 (LH)

") CITY OF YOUNGSTOWN HOME BUYER PROGRAM Community Development Agency Housing Division CITY OF YOUNGSTOWN Mayor Jay Williams Revised 3/2008 (LH) PROGRAM SUMMARY HOMEBUYER PROGRAM Purpose: To provide low and

CITY OF YOUNGSTOWN HOME BUYER PROGRAM Community Development Agency Housing Division CITY OF YOUNGSTOWN Mayor Jay Williams Revised 3/2008 (LH) PROGRAM SUMMARY HOMEBUYER PROGRAM Purpose: To provide low and

Very Low-Income Loan Obligations Within USDA s Section 502 Direct Homeownership Loan Program

Report Very Low-Income Loan Obligations Within USDA s Section 502 Direct Homeownership Loan Program Housing Assistance Council December 2010 Housing Assistance Council 1025 Vermont Avenue, NW Suite 606

Report Very Low-Income Loan Obligations Within USDA s Section 502 Direct Homeownership Loan Program Housing Assistance Council December 2010 Housing Assistance Council 1025 Vermont Avenue, NW Suite 606

Achieving your goals through Financing. Cooperative Financing Models that may work for you

Achieving your goals through Financing Cooperative Financing Models that may work for you Overview Cooperative Financing Mortgage programs for Cooperatives Overview of current rate environment Reasons

Achieving your goals through Financing Cooperative Financing Models that may work for you Overview Cooperative Financing Mortgage programs for Cooperatives Overview of current rate environment Reasons

HOUSING. Community Housing Development Organizations (CHDOs) Apartment Living

Apartment Living") HOUSING City Home Repair Programs Emergency Repair and Weatherization Programs Cowtown Brush Up Lead Hazard Control Program Model Blocks Home Improvement Loans Housing Trust Fund (HTF) Community Housing

HOUSING City Home Repair Programs Emergency Repair and Weatherization Programs Cowtown Brush Up Lead Hazard Control Program Model Blocks Home Improvement Loans Housing Trust Fund (HTF) Community Housing

West Valley City Grants Department Rehabilitation Loan Program Policy & Information Packet

West Valley City Grants Department Rehabilitation Loan Program Policy & Information Packet Current Revision: 9/09 1 CONTENTS REHABILITATION LOAN PROGRAM (RLP) POLICY: Section I Section II Section III Section

West Valley City Grants Department Rehabilitation Loan Program Policy & Information Packet Current Revision: 9/09 1 CONTENTS REHABILITATION LOAN PROGRAM (RLP) POLICY: Section I Section II Section III Section

MSHDA's Down Payment Assistance and Mortgage Credit Certificate. May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by:

Facilitated by: Carol Brito (MSHDA) Sponsored by:") MSHDA's Down Payment Assistance and Mortgage Credit Certificate May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by: CREDIT UNIONS A DRIVING FORCE OF COMMUNITIES MSHDA Overview

MSHDA's Down Payment Assistance and Mortgage Credit Certificate May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by: CREDIT UNIONS A DRIVING FORCE OF COMMUNITIES MSHDA Overview

West Valley City Grants Department Down Payment Assistance Policy & Information Packet

West Valley City Grants Department Down Payment Assistance Policy & Information Packet Current Revision: 9/09 1 CONTENTS DOWN PAYMENT ASSISTANCE (DPA) POLICY: Section I Section II Section III Section IV

West Valley City Grants Department Down Payment Assistance Policy & Information Packet Current Revision: 9/09 1 CONTENTS DOWN PAYMENT ASSISTANCE (DPA) POLICY: Section I Section II Section III Section IV

Homeownership Division

Michigan Credit Union League & Affiliates Annual Convention and Exposition Helping Credit Unions Serve, Grow and Remain Strong #mculace MSHDA s Homeownership Programs Delivering the Dream to Michigan Families

Michigan Credit Union League & Affiliates Annual Convention and Exposition Helping Credit Unions Serve, Grow and Remain Strong #mculace MSHDA s Homeownership Programs Delivering the Dream to Michigan Families

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER Special Attention of All Multifamily Hub Directors Notice H 2011-05

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER Special Attention of All Multifamily Hub Directors Notice H 2011-05

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

FSA can guarantee OLs or FO loans up to $1,392,000 (amount adjusted annually based on inflation).

.") Guaranteed Loan Program Loan Purposes Guaranteed Ownership Loans Guaranteed Farm Ownership (FO) Loans may be made to purchase farmland, construct or repair buildings and other fixtures, develop farmland

Guaranteed Loan Program Loan Purposes Guaranteed Ownership Loans Guaranteed Farm Ownership (FO) Loans may be made to purchase farmland, construct or repair buildings and other fixtures, develop farmland

CITY OF SOLEDAD FIRST-TIME HOMEBUYER ASSISTANCE PROGRAM FIRST MORTGAGE LENDER INSTRUCTIONS 248 MAIN STREET, SOLEDAD CA 93960

FIRST MORTGAGE LENDER INSTRUCTIONS Maximum Home Sales Price Home sale prices cannot exceed 95% of the area median home value for Soledad (see Table 1: Maximum Purchase Price per Unit). Maximum Loan-to-Value

FIRST MORTGAGE LENDER INSTRUCTIONS Maximum Home Sales Price Home sale prices cannot exceed 95% of the area median home value for Soledad (see Table 1: Maximum Purchase Price per Unit). Maximum Loan-to-Value

Broker. Financing Real Estate. Chapter 12. Copyright Gold Coast Schools 1

Broker Chapter 12 Financing Real Estate Copyright Gold Coast Schools 1 Learning Objectives Describe the difference between a note and a mortgage Explain the benefits of having the first recorded lien on

Broker Chapter 12 Financing Real Estate Copyright Gold Coast Schools 1 Learning Objectives Describe the difference between a note and a mortgage Explain the benefits of having the first recorded lien on

City of Perris First Time Homebuyer Homebuyer Assistance Program (HAP) Lender Training

Lender Training") City of Perris First Time Homebuyer Homebuyer Assistance Program (HAP) Lender Training 2010 Agenda Staff Introductions HAP Program Summary HAP Program Requirements HAP Program Procedures Becoming an Approved

City of Perris First Time Homebuyer Homebuyer Assistance Program (HAP) Lender Training 2010 Agenda Staff Introductions HAP Program Summary HAP Program Requirements HAP Program Procedures Becoming an Approved

Mortgage Credit Certificate Program Presented By:

Mortgage Credit Certificate Program Presented By: Partners in Building Your Dream Define Affordable Housing Overview What is Mortgage Credit Certificate Enabling Legislation How The MCC Program Works Who

Mortgage Credit Certificate Program Presented By: Partners in Building Your Dream Define Affordable Housing Overview What is Mortgage Credit Certificate Enabling Legislation How The MCC Program Works Who

Developing a Cooperative through FHA Financing. A model that works for Individuals, developers and the community

Developing a Cooperative through FHA Financing A model that works for Individuals, developers and the community Contents Basic Cooperative Concepts Basic Cooperative Qualities Cooperative Legal Documents

Developing a Cooperative through FHA Financing A model that works for Individuals, developers and the community Contents Basic Cooperative Concepts Basic Cooperative Qualities Cooperative Legal Documents

Freddie Mac Condominium Unit Mortgages

For all mortgages secured by a Condominium Unit in a Condominium Project, you must meet the requirements of Freddie Mac Single-Family Seller/Servicer Guide (Guide) Chapter 42, Special for Condominiums,

For all mortgages secured by a Condominium Unit in a Condominium Project, you must meet the requirements of Freddie Mac Single-Family Seller/Servicer Guide (Guide) Chapter 42, Special for Condominiums,

SMALL BUSINESS REVOLVING LOAN FUND APPLICANT CHECKLIST

SMALL BUSINESS REVOLVING LOAN FUND APPLICANT CHECKLIST The following can be mailed or dropped off to: EDC of Gladwin County Attn: Bob Balzer 110 Buckeye Street Gladwin, Ml 48624 Loan Application Credit

SMALL BUSINESS REVOLVING LOAN FUND APPLICANT CHECKLIST The following can be mailed or dropped off to: EDC of Gladwin County Attn: Bob Balzer 110 Buckeye Street Gladwin, Ml 48624 Loan Application Credit

Mortgage Loan Programs, Part I. Presented by Minnesota Housing

Mortgage Loan Programs, Part I Presented by Minnesota Housing Questions During Presentation We will batch online questions and answer them throughout the webinar A complete Q & A list will be posted to

Mortgage Loan Programs, Part I Presented by Minnesota Housing Questions During Presentation We will batch online questions and answer them throughout the webinar A complete Q & A list will be posted to

11.1 INTRODUCTION 11.2 THE RATIOS

0BCHAPTER 11: RATIO ANALYSIS 11.1 INTRODUCTION Ratios are used to determine whether the borrower s repayment income can reasonably be expected to meet the anticipated monthly housing expense and total

0BCHAPTER 11: RATIO ANALYSIS 11.1 INTRODUCTION Ratios are used to determine whether the borrower s repayment income can reasonably be expected to meet the anticipated monthly housing expense and total

Achieving your goals through Financing. Cooperative Financing Models that may work for you

Achieving your goals through Financing Cooperative Financing Models that may work for you Overview Cooperative Financing Overview of the environment Interest Rates Why now is the best time to borrow Reasons

Achieving your goals through Financing Cooperative Financing Models that may work for you Overview Cooperative Financing Overview of the environment Interest Rates Why now is the best time to borrow Reasons

COEUR D ALENE TRIBAL HOUSING AUTHORITY HOUSING REHABILITATION POLICY (CDTHA REHAB)

") COEUR D ALENE TRIBAL HOUSING AUTHORITY HOUSING REHABILITATION POLICY (CDTHA REHAB) Adopted by the Housing Board May 25, 2005 CDTHA HOUSING REHAB POLICY Programs Available... 3 Reconstruction... 3 Relocation/Displacement...

COEUR D ALENE TRIBAL HOUSING AUTHORITY HOUSING REHABILITATION POLICY (CDTHA REHAB) Adopted by the Housing Board May 25, 2005 CDTHA HOUSING REHAB POLICY Programs Available... 3 Reconstruction... 3 Relocation/Displacement...

Home Equity Conversion Mortgage Basics

Home Equity Conversion Mortgage Basics Kelly Zitlow NMLS#164330 Vice President, CMPS 480.398.4908 kzitlow@ccmclending.com www.kellyzitlow.com Cherry Creek Mortgage Co., Inc. NMLS#3001 AZ BK#0904024 17015

Home Equity Conversion Mortgage Basics Kelly Zitlow NMLS#164330 Vice President, CMPS 480.398.4908 kzitlow@ccmclending.com www.kellyzitlow.com Cherry Creek Mortgage Co., Inc. NMLS#3001 AZ BK#0904024 17015

NEIGHBORHOOD STABILIZATION PROGRAM (NSP) APPLICATION FOR NSP LOAN. Program Guidelines

APPLICATION FOR NSP LOAN. Program Guidelines") APPLICATION FOR NSP LOAN Income limits per household Program Guidelines Maximum Income 1 48,150 2 55,000 3 61,900 4 68,750 5 74,250 6 79,750 7 85,250 8 90,750 Homebuyer Requirements Home Education Minimum

APPLICATION FOR NSP LOAN Income limits per household Program Guidelines Maximum Income 1 48,150 2 55,000 3 61,900 4 68,750 5 74,250 6 79,750 7 85,250 8 90,750 Homebuyer Requirements Home Education Minimum

DeKalb County First-Time Homebuyers Program. For the Provision of Down Payment Assistance with the use of HOME Investment Partnerships Program funds

DeKalb County First-Time Homebuyers Program For the Provision of Down Payment Assistance with the use of HOME Investment Partnerships Program funds First Time Homebuyer Program A. Program Overview: The

DeKalb County First-Time Homebuyers Program For the Provision of Down Payment Assistance with the use of HOME Investment Partnerships Program funds First Time Homebuyer Program A. Program Overview: The

GLOSSARY OF TERMS. Amortization Repayment of a debt in regular installments of principal and interest, rather than interest only payments

GLOSSARY OF TERMS Ability to Repay (ATR) The Ability to Repay rule protects consumers from taking on mortgages that exceed their financial means, by mandating the documentation / proof of income and assets.

GLOSSARY OF TERMS Ability to Repay (ATR) The Ability to Repay rule protects consumers from taking on mortgages that exceed their financial means, by mandating the documentation / proof of income and assets.

Rural Development Program Guide Building Rural Communities from the Ground Up. www.rd.usda.gov/me

Rural Development Program Guide Building Rural Communities from the Ground Up www.rd.usda.gov/me Housing Programs Program Objective Applicant Uses Population / Direct s Direct Repair s and s Guaranteed

Rural Development Program Guide Building Rural Communities from the Ground Up www.rd.usda.gov/me Housing Programs Program Objective Applicant Uses Population / Direct s Direct Repair s and s Guaranteed

Lesson 15: Closing Real Estate Transactions

1 Real Estate Principles of Georgia Lesson 15: Closing Real Estate Transactions 2 Closing Closing: Final stage in real estate transaction. Also called settlement. Buyer pays seller; seller transfers title

1 Real Estate Principles of Georgia Lesson 15: Closing Real Estate Transactions 2 Closing Closing: Final stage in real estate transaction. Also called settlement. Buyer pays seller; seller transfers title

The Guide to Single Family Home Mortgage Insurance

U.S. Department of Housing and Urban Development Office of Housing Office of Single Family Housing The Guide to Single Family Home Mortgage Insurance www.hud.gov espanol.hud.gov Becoming a Homeowner Many

U.S. Department of Housing and Urban Development Office of Housing Office of Single Family Housing The Guide to Single Family Home Mortgage Insurance www.hud.gov espanol.hud.gov Becoming a Homeowner Many

TEXAS DEPARTMENT OF HOUSING AND COMMUNITY AFFAIRS

In this packet... Introduction... 2 TDHCA s Homebuyer Assistance Options... 2 My First Texas Home (MFTH)... 2 Texas Mortgage Credit Certificate (MCC)... 2 Features of TDHCA s Homebuyer Assistance Programs...

In this packet... Introduction... 2 TDHCA s Homebuyer Assistance Options... 2 My First Texas Home (MFTH)... 2 Texas Mortgage Credit Certificate (MCC)... 2 Features of TDHCA s Homebuyer Assistance Programs...

Appraiser: a qualified individual who uses his or her experience and knowledge to prepare the appraisal estimate.

Mortgage Glossary 203(b): FHA program which provides mortgage insurance to protect lenders from default; used to finance the purchase of new or existing one- to four family housing; characterized by low

Mortgage Glossary 203(b): FHA program which provides mortgage insurance to protect lenders from default; used to finance the purchase of new or existing one- to four family housing; characterized by low

Commonwealth of Massachusetts HOUSING STABILIZATION FUND (HSF) Rental Application Guidelines

Rental Application Guidelines") Commonwealth of Massachusetts HOUSING STABILIZATION FUND (HSF) Rental Application Guidelines A. Overview Thousands of residential properties requiring moderate or substantial rehabilitation are located

Commonwealth of Massachusetts HOUSING STABILIZATION FUND (HSF) Rental Application Guidelines A. Overview Thousands of residential properties requiring moderate or substantial rehabilitation are located

Glossary of Foreclosure Fairness Mediation Terminology

Glossary of Foreclosure Fairness Mediation Terminology Adjustable-Rate Mortgage (ARM) Mortgage repaid at the rate of interest that increases or decreases over the life of the loan based on market conditions.

Glossary of Foreclosure Fairness Mediation Terminology Adjustable-Rate Mortgage (ARM) Mortgage repaid at the rate of interest that increases or decreases over the life of the loan based on market conditions.

Rural Business Enterprise Loan Program (RBE)

") Courthouse PO Box 607 Carlton, MN 55718 Rural Business Enterprise Loan Program (RBE) Mailing Address: Carlton County Economic Development Office PO Box 607 Carlton, MN 55718 (218) 384-9597 or (218)384-9564

Courthouse PO Box 607 Carlton, MN 55718 Rural Business Enterprise Loan Program (RBE) Mailing Address: Carlton County Economic Development Office PO Box 607 Carlton, MN 55718 (218) 384-9597 or (218)384-9564

SHIP LOCAL HOUSING ASSISTANCE PLAN (LHAP)

") CITY OF OCALA SHIP LOCAL HOUSING ASSISTANCE PLAN (LHAP) FISCAL YEARS COVERED 2013/2014, 2014/2015 AND 2015/2016-1 - Table of Contents Title Page #. Section I. Program Description: 3 Section II. Strategies:

CITY OF OCALA SHIP LOCAL HOUSING ASSISTANCE PLAN (LHAP) FISCAL YEARS COVERED 2013/2014, 2014/2015 AND 2015/2016-1 - Table of Contents Title Page #. Section I. Program Description: 3 Section II. Strategies:

2004, 2005, 2010 & 2011

City of Pasadena, Texas Home Investment Partnerships Program DRAFT Substantial Amendments 2004, 2005, 2010 & 2011 The Community Development Department proposes a Substantial Amendment to reallocate funds

City of Pasadena, Texas Home Investment Partnerships Program DRAFT Substantial Amendments 2004, 2005, 2010 & 2011 The Community Development Department proposes a Substantial Amendment to reallocate funds

Detroit Land Bank Authority Request for Qualifications:

Detroit Land Bank Authority Request for Qualifications: Organizations to serve as Homeownership Educators and Third Party Advisors during the Purchase and Rehab of Homes from the Detroit Land Bank Authority

Detroit Land Bank Authority Request for Qualifications: Organizations to serve as Homeownership Educators and Third Party Advisors during the Purchase and Rehab of Homes from the Detroit Land Bank Authority

California Home Finance Authority (CHF)

") Presentation for Real Estate Professionals California Home Finance Authority (CHF) 1215 K Street, Suite 1650, Sacramento, CA 95814 www.chfloan.org (855) 740-8422 Often first point of contact for a new

Presentation for Real Estate Professionals California Home Finance Authority (CHF) 1215 K Street, Suite 1650, Sacramento, CA 95814 www.chfloan.org (855) 740-8422 Often first point of contact for a new

Fin 5413: Chapter 8 Mortgage Underwriting

Fin 5413: Chapter 8 Mortgage Underwriting Some Basic Mortgage Underwriting Questions Who should you grant a loan to? How do we determine the appropriate interest rate for a loan? What is the maximum dollar

Fin 5413: Chapter 8 Mortgage Underwriting Some Basic Mortgage Underwriting Questions Who should you grant a loan to? How do we determine the appropriate interest rate for a loan? What is the maximum dollar

SMALL BUSINESS LOAN FUND GUIDELINES. Funded By: Fay-Penn Economic Development Council

SMALL BUSINESS LOAN FUND GUIDELINES Funded By: Fay-Penn Economic Development Council SMALL BUSINESS LOAN FUND 1.0 INTRODUCTION Fay-Penn Economic Development Council has established a Small Business Loan

SMALL BUSINESS LOAN FUND GUIDELINES Funded By: Fay-Penn Economic Development Council SMALL BUSINESS LOAN FUND 1.0 INTRODUCTION Fay-Penn Economic Development Council has established a Small Business Loan

EXPAND HOMEOWNERSHIP PROGRAM

EXPAND HOMEOWNERSHIP PROGRAM Administrator Guidelines Published: March 12, 2015 Revised March 13, 2015 Updates are shown on Page 4! FANO EXPAND HOMEOWNERSHIP PROGRAM - Administrator Guidelines Page 2 Time

EXPAND HOMEOWNERSHIP PROGRAM Administrator Guidelines Published: March 12, 2015 Revised March 13, 2015 Updates are shown on Page 4! FANO EXPAND HOMEOWNERSHIP PROGRAM - Administrator Guidelines Page 2 Time

Please contact this office at the numbers listed above should you have any questions about the program, its requirements or procedures.

TOWN OF RIVERHEAD HOUSING PRESERVATION HOME IMPROVEMENT PROGRAM APPLICATION TOWN OF RIVERHEAD COMMUNITY DEVELOPMENT DEPARTMENT 200 Howell Avenue, Riverhead, NY 11901 Tel. (631)727-3200 Ext. 238 Fax (631)

TOWN OF RIVERHEAD HOUSING PRESERVATION HOME IMPROVEMENT PROGRAM APPLICATION TOWN OF RIVERHEAD COMMUNITY DEVELOPMENT DEPARTMENT 200 Howell Avenue, Riverhead, NY 11901 Tel. (631)727-3200 Ext. 238 Fax (631)

OWN IN OGDEN PROGRAM GUIDELINES

CITY OF OGDEN, UTAH COMMUNITY AND ECONOMIC DEVELOPMENT OWN IN OGDEN PROGRAM GUIDELINES I. PROGRAM SUMMARY Own in Ogden is an Ogden City program designed to increase home ownership in specific target neighborhoods.

CITY OF OGDEN, UTAH COMMUNITY AND ECONOMIC DEVELOPMENT OWN IN OGDEN PROGRAM GUIDELINES I. PROGRAM SUMMARY Own in Ogden is an Ogden City program designed to increase home ownership in specific target neighborhoods.

AFFORDABLE HOUSING RESOURCES FLORIDA 2012

AFFORDABLE HOUSING RESOURCES FLORIDA 2012 The sources of financing and assistance for affordable housing that appear in these pages are a summary that may be useful for housing providers, support providers

AFFORDABLE HOUSING RESOURCES FLORIDA 2012 The sources of financing and assistance for affordable housing that appear in these pages are a summary that may be useful for housing providers, support providers

FROM: Tony Hernandez /s/ Tony Hernandez Administrator Housing and Community Facilities Programs

January 21, 2016 TO: State Directors Rural Development ATTENTION: Rural Housing Program Directors, Guaranteed Loan Coordinators, Area Directors and Specialists FROM: Tony Hernandez /s/ Tony Hernandez Administrator

January 21, 2016 TO: State Directors Rural Development ATTENTION: Rural Housing Program Directors, Guaranteed Loan Coordinators, Area Directors and Specialists FROM: Tony Hernandez /s/ Tony Hernandez Administrator

The City of MIDWEST CITY GRANTS MANAGEMENT DEPARTMENT Terri L. Craft, Grants Manager. MIDWEST CITY Homebuyer Assistance Program

The City of MIDWEST CITY GRANTS MANAGEMENT DEPARTMENT Terri L. Craft, Grants Manager Grant Amount: $5,000.00 MIDWEST CITY Homebuyer Assistance Program The Homebuyer Assistance Program promotes homeownership

The City of MIDWEST CITY GRANTS MANAGEMENT DEPARTMENT Terri L. Craft, Grants Manager Grant Amount: $5,000.00 MIDWEST CITY Homebuyer Assistance Program The Homebuyer Assistance Program promotes homeownership

5. CONSERVATION OF AFFORDABLE UNITS

5. CONSERVATION OF AFFORDABLE UNITS The analysis of the Conservation of Affordable Units section relied primarily on data from the San Benito County Housing and Economic Development Department, San Benito

5. CONSERVATION OF AFFORDABLE UNITS The analysis of the Conservation of Affordable Units section relied primarily on data from the San Benito County Housing and Economic Development Department, San Benito

VHDA. Homeownership Program Guidelines for Realtors & Lenders. Updated 04/04

VHDA Homeownership Program Guidelines for Realtors & Lenders Updated 04/04 2 Benefits of a VHDA Loan: Creative financing programs Reduced interest rates Lower monthly payments More house for less money

VHDA Homeownership Program Guidelines for Realtors & Lenders Updated 04/04 2 Benefits of a VHDA Loan: Creative financing programs Reduced interest rates Lower monthly payments More house for less money

IV. HOME NARRATIVES (AP-90)

") IV. HOME NARRATIVES (AP-90) A. INTRODUCTION Los Angeles County is an Urban County-participating jurisdiction for HUD s HOME Investment Partnerships (HOME) Program. It receives an annual formula allocation

IV. HOME NARRATIVES (AP-90) A. INTRODUCTION Los Angeles County is an Urban County-participating jurisdiction for HUD s HOME Investment Partnerships (HOME) Program. It receives an annual formula allocation

City of North Miami NSP 3 Substantial Amendment

City of North Miami NSP 3 Substantial Amendment 1. NSP3 Grantee Information NSP3 Program Administrator Contact Information Name (Last, First) Calloway, Maxine Email Address mcalloway@northmiamifl.gov Phone

City of North Miami NSP 3 Substantial Amendment 1. NSP3 Grantee Information NSP3 Program Administrator Contact Information Name (Last, First) Calloway, Maxine Email Address mcalloway@northmiamifl.gov Phone

Thank you for considering a grant from Homes Are Possible, Inc. (HAPI)!

!") Thank you for considering a grant from Homes Are Possible, Inc. (HAPI)! Home rehabilitation work may include but is not limited to: Roof repairs/shingles Siding Windows/Door Plumbing Electrical Foundation

Thank you for considering a grant from Homes Are Possible, Inc. (HAPI)! Home rehabilitation work may include but is not limited to: Roof repairs/shingles Siding Windows/Door Plumbing Electrical Foundation

REALTORS AND FHA WORKING TOGETHER TO HELP PEOPLE FULFILL THE AMERICAN DREAM

Shopping for a Mortgage? FHA Improvements Benefit You FHA Insured Mortgages Realtors and FHA: Partners in Homeownership National Association of REALTORS FHA REALTORS AND FHA WORKING TOGETHER TO HELP PEOPLE

Shopping for a Mortgage? FHA Improvements Benefit You FHA Insured Mortgages Realtors and FHA: Partners in Homeownership National Association of REALTORS FHA REALTORS AND FHA WORKING TOGETHER TO HELP PEOPLE

A Presentation On the State of the Real Estate Crisis 1/30/2009

A Presentation On the State of the Real Estate Crisis 1/30/2009 Presented by Mike Anderson, CRMS President, Essential Mortgage, a Latter & Blum Realtors Company Immediate past president/legislative Chair

A Presentation On the State of the Real Estate Crisis 1/30/2009 Presented by Mike Anderson, CRMS President, Essential Mortgage, a Latter & Blum Realtors Company Immediate past president/legislative Chair

The Chase Guaranteed Rural Housing Refinance Program Features

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

Appraisal Standards and Guidelines chapter

Appraisal Standards and Guidelines chapter Union Capital requires appraisers and appraisal reports to meet USPAP and applicable Union Capital, FNMA, FHLMC, FHA and VA policies and requirements, as applicable.

Appraisal Standards and Guidelines chapter Union Capital requires appraisers and appraisal reports to meet USPAP and applicable Union Capital, FNMA, FHLMC, FHA and VA policies and requirements, as applicable.

SMALL BUSINESS REVOLVING LOAN FUND GUIDELINES

SMALL BUSINESS REVOLVING LOAN FUND GUIDELINES 1.0 INTRODUCTION Fay-Penn Economic Development Council has established a Small Business Loan Fund. The Small Business Loan Fund Program is designed to stimulate

SMALL BUSINESS REVOLVING LOAN FUND GUIDELINES 1.0 INTRODUCTION Fay-Penn Economic Development Council has established a Small Business Loan Fund. The Small Business Loan Fund Program is designed to stimulate

The USDA 502 Direct Loan: Making It Work for Your Affiliate

The USDA 502 Direct Loan: Making It Work for Your Affiliate The USDA 502 Direct Loan: Making It Work for Your Affiliate Panelist Lori Anderson, executive director, Habitat for Humanity of Douglas County

The USDA 502 Direct Loan: Making It Work for Your Affiliate The USDA 502 Direct Loan: Making It Work for Your Affiliate Panelist Lori Anderson, executive director, Habitat for Humanity of Douglas County

First Time Home Buyer Glossary

First Time Home Buyer Glossary For first time home buyers, knowing and understanding the following terms are very important when purchasing your first home. By understanding these terms, you will make

First Time Home Buyer Glossary For first time home buyers, knowing and understanding the following terms are very important when purchasing your first home. By understanding these terms, you will make

Southborough Housing Opportunity Partnership Committee (SHOPC) Town of Southborough 17 Common Street Southborough, Massachusetts, 01772

Town of Southborough 17 Common Street Southborough, Massachusetts, 01772") Southborough Housing Opportunity Partnership Committee (SHOPC) Town of Southborough 17 Common Street Southborough, Massachusetts, 01772 Telephone (508-0710 ext. 3027 Jennifer Burney, Town Planner jburney@southboroughma.com

Southborough Housing Opportunity Partnership Committee (SHOPC) Town of Southborough 17 Common Street Southborough, Massachusetts, 01772 Telephone (508-0710 ext. 3027 Jennifer Burney, Town Planner jburney@southboroughma.com