Pricing of electricity futures The risk premium

|

|

|

- Dennis Hall

- 8 years ago

- Views:

Transcription

1 Pricing of electricity futures The risk premium Fred Espen Benth In collaboration with Alvaro Cartea, Rüdiger Kiesel and Thilo Meyer-Brandis Centre of Mathematics for Applications (CMA) University of Oslo, Norway Advanced Modelling in Finance and Insurance, RICAM Linz, September 22 26, 2008

2 Introduction Problem: what is the connection between spot and forward prices in electricity? Electricity is a non-storable commodity How to explain the risk premium? Empirical and economical evidence: Sign varies with time to delivery Propose two approaches: 1. Information approach 2. Equilibrium approach Purpose: try to explain the risk premium for electricity

3 Outline of talk 1. Example of an electricity market: NordPool 2. The classical spot-forward relation 3. The information approach 4. The equilibrium approach 5. Conclusions

4 Example of an electricity market: NordPool

5 The NordPool market organizes trade in Hourly spot electricity, next-day delivery Financial forward contracts In reality mostly futures, but we make no distinction here European options on forwards Difference from classical forwards: Delivery over a period rather than at a fixed point in time

6 Elspot: the spot market A (non-mandatory) hourly market with physical delivery of electricity Participants hand in bids before noon the day ahead Volume and price for each of the 24 hours next day Maximum of 64 bids within technical volume and price limits NordPool creates demand and production curves for the next day before 1.30 pm

7 The system price is the equilibrium Reference price for the forward market Historical system price from the beginning in 1992 note the spikes...

8 The forward market Forward with delivery over a period Financial market Settlement with respect to system price in the delivery period Delivery periods Next day, week or month Quarterly (earlier seasons) Yearly Overlapping settlement periods (!) Contracts also called swaps: Fixed for floating price

9 The option market European call and put options on electricity forwards Quarterly and yearly electricity forwards Low activity on the exchange OTC market for electricity derivatives huge Average-type (Asian) options, swing options...

options,")

10 The spot-forward relation

11 The spot-forward relation: some classical theory The no-arbitrage forward price (based on the buy-and-hold strategy) r(t t) F (t, T ) = S(t)e A risk-neutral expression of the price as F (t, T ) = E Q [S(T ) F t ] The risk premium is defined as R(t, T ) = F (t, T ) E [S(T ) F t ]

F t ] The risk premium is defined as R(t, T ) = F (t, T ) E [S(T )")

12 In the case of electricity: Storage of spot is not possible (only indirectly in water reservoirs) Buy-and-hold strategy fails No foundation for the classical spot-forward relation...and hence no rule for what Q should be! Thus: What is the link between F (t, T ) and S(t)?

13 Economical intuition for electricity Short-term positive risk premium Retailers (consumers) hedge spike risk Spikes lead to expensive electricity Accept to pay a premium for locking in prices in the short-term Long-term negative risk premium Producers hedge their future production Long-term contracts (quarters/years) The market may have a change in the sign of the risk premium

The market may have a change in the sign of")

14 Empirical evidence for electricity Longstaff & Wang (2004), Geman & Vasicek : PJM market Positive premium in the short-term market Diko, Lawford & Limpens (2006) Study of EEX, PWN, APX, based on multi-factor models Changing sign of the risk premium Kolos & Ronn (2008) Market price of risk: expected risk-adjusted return Multi-factor models Negative on the short-term, positive on the long term

15 Explore two possible approaches to price electricity futures 1. The information approach based on market forecasts 2. An equilibrium approach based on market power of the consumers and producers For simplicity we first restrict our attention to F (t, T ) Electricity forwards deliver over a time period Creates technical difficulties for most spot models Ignore this here In the equilibrium approach we consider delivery periods

Electricity forwards deliver over a time period Creates technical")

16 The information approach

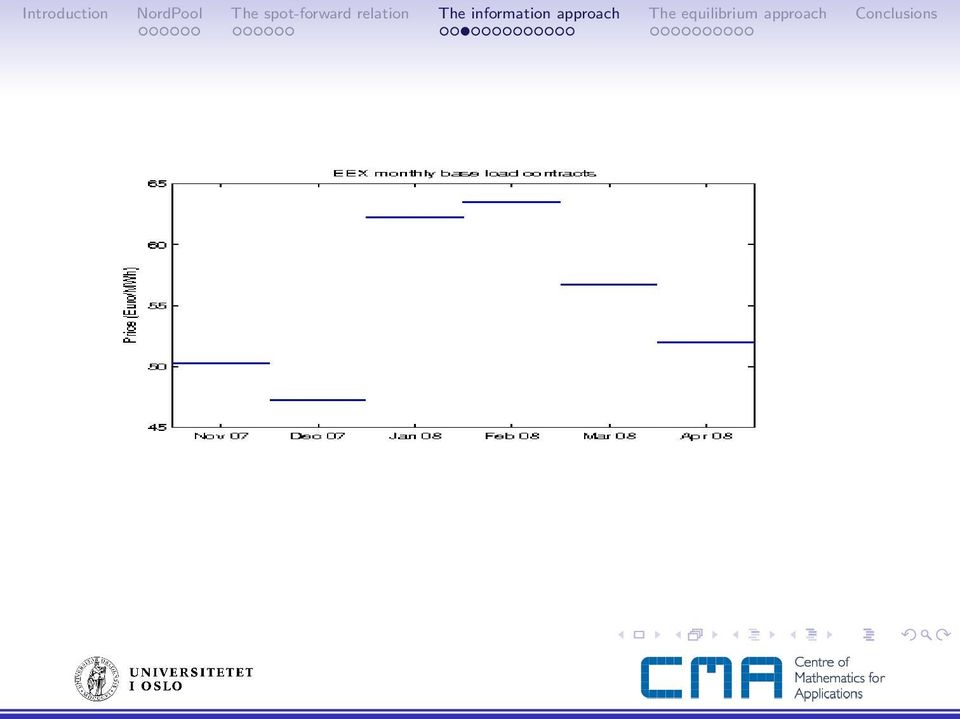

17 The information approach: idea Idea is the following: Electricity is non-storable Future predicitions about market will not affect current spot However, it will affect forward prices Stylized example: Planned outage of a power plant in one month Will affect forwards delivering in one month But not spot today Market example In 2007 market knew that in 2008 CO2 emission costs will be introduced No effect on spot prices in the EEX market in 2007 However, clear effect on the forward prices around New Year

18

19 The information approach: definition Define the forward price as F G (t, T ) = E [S(T ) G t ] G t includes spot information up to current time (F t ) and forward-looking information The information premium I G (t, T ) = F G (t, T ) E [S(T ) F t ]

= F G (t, T ) E [S(T ) F t ]")

20 Rewrite the information premium using double conditioning and F t G t I G (t, T ) = E [S(T ) G t ] E [E [S(T ) G t ] F t ] The information premium is the residual random variable after projecting F G (t, T ) onto L 2 (F t, P) I G measures how much more information is contained in G t compared to F t

I G measures how much more information is contained in G t compared")

21 Note that E [I G (t, T ) F t ] = 0 I G (t, T ) is orthogonal to R(t, T ) The risk premium R(t, T ) is F t -adapted Thus, impossible to obtain a given I G (t, T ) from an appropriate choice of Q in R(t, T ) Including future information creates new ways of explaining risk premia

22 Example: temperature predictions Temperature dynamics dy (t) = γ(µ(t) Y (t)) dt + η db(t) Spot price dynamics ds(t) = α(λ(t) S(t)) dt + σρ db(t) + σ 1 ρ 2 dw (t) ρ is the correlation between temperature and spot price NordPool: ρ < 0, since high temperature implies low prices, and vice versa

23 Suppose we have some temperature forecast at time T 1 Full, or at least some, knowledge of Y (T 1 ) F t G t H t F t σ(y (T 1 )) We want to compute (for T T 1 ) F G (t, T ) = E [S(T ) G t ] Program: 1. Find a Brownian motion wrt G t 2. Compute the conditional expectation

24 From the theory of enlargement of filtrations : There exists a G t -adapted drift θ 1 such that B is a G t -Brownian motion, d B(t) = db(t) θ 1 (t) dt The drift is expressed as ( T1 ) θ 1 (t) = a 1 (t) e γt 1 E[Y (T 1 ) G t ] e γt Y (t) γ µ(u)e γu du t a 1 (t) = 2γe γt η(e 2γT 1 e 2γt )

25 Dynamics of S in terms of B: ( ds(t) = α ρ σ ) α θ 1(t) + λ(t) S(t) dt + σρ d B(t) + σ 1 ρ 2 dw (t) Note that we have a mean-reversion level being stochastic Explicitly dependent on the temperature prediction and todays temperature θ 1 (t) is the market price of information, or information yield

26 Calculate the forward price F G (t, u) = E [S(u) F t ] + I G (t, T ) = S(t) exp( α(t t)) + α T t λ(s)e α(t s) ds + I G (t, T ) The information premium is, by applying the definition [ T ] I G (t, T ) = ρσe e α(t s) db(s) G t t Use that B is a G t -Brownian motion

27 Expression for the information premium I G (t, T ) = where ρa(t, T ) ( T1 ) e γt 1 E [Y (T 1 ) G t ] e γt Y (t) γ µ(s)e γs ds t A(t, T ) = 2γσeγT (1 e (α+γ)(t t) ) η(α + γ)(e 2γT 1 e 2γt ) Observe that A(t, T ) is positive The sign of the information premium is determined by The correlation ρ The temperature prediction

28 Example with complete information Suppose we know the temperature at T 1 The information set is H t Unlikely situation of perfect future knowledge... Assume we we expect a temperature drop T1 Y (T 1 ) < e γ(t1 t) Y (t) + γ µ(s)e γ(t1 s) ds t At NordPool, where ρ < 0: The information premium is positive Drop in temperature will lead to increasing demand, and thus higher prices

29 The equilibrium approach

30 The equilibrium approach: idea Producers and consumers can trade in both spot and forward markets No speculators in our set-up We suppose that the forwards deliver electricity over an agreed period No fixed delivery time as in other commodity markets Natural for electricity due to its nature Choice of an electricity producer Sell production on spot market, or on the forward market

31 Producer is indifferent when (U pr is the utility function) [ τ2 ] E U pr ( S(u) du) = E [U pr ((τ 2 τ 1 )F pr (t, τ 1, τ 2 ))] τ 1 The certainty equivalence principle F pr is the lowest acceptable price for the producer can accept to be interested in entering a forward Similarly, F c is the highest acceptable price for the consumer, for a given utility function U c We assume exponential utility U(x) = 1 exp( γx), with respective risk aversion for producer and consumer γ pr and γ c

32 By Jensen s inequality, the predicted average spot price is within the price bounds [ 1 F pr (t, τ 1, τ 2 ) E τ 2 τ 1 τ2 τ 1 ] S(u) du F t F c (t, τ 1, τ 2 ) Hypothesis: The settlement price of the forward will depend on the market power p [0, 1] of the producer F p (t, τ 1, τ 2 ) = pf c (t, τ 1, τ 2 ) + (1 p)f pr (t, τ 1, τ 2 )

33 Assume a simple two-factor spot model with jump component S(t) = Λ(t) + X (t) + Y (t) Λ(t) seasonal function dy (t) = λy (t) dt + Z dn(t) Jumps (accounting for spikes) Z jump size N Poisson process Slowly varying base component dx (t) = αx (t) dt + σ db(t)

34 Calculate prices for weekly contracts and compute the risk premium The market power set to p = 0.25 Constant positive jumps at rate 2/year Note the positive risk premium in the short end Caused by the jump risk

35 Empirical example: EEX (Metka, Ulm) Fit two-factor model to daily EEX spot prices (Jan 02 Dec 05)

36 Using observed prices for 18 monthly forward contracts and fitted spot model Calculate the risk premium, Difference between forward price and predicted spot Observe a positive premium in the short end, and negative in the long end

37 Based on all available forward prices in the study, risk aversion parameters were determined γ pr and γ c are such that F pr (t, τ 1, τ 2 ) F (t, τ 1, τ 2 ) F c (t, τ 1, τ) Calculate the empirical market power p(t, τ 1, τ 2 ) = F (t, τ 1, τ 2 ) F pr (t, τ 1, τ 2 ) F c (t, τ 1, τ 2 ) F pr (t, τ 1, τ 2 )

38 Observe that producer s power is strong in the short end, while decreasing to be rather weak in the long end

39 Conclusions Discussed two potential ways to understand the link between spot and forward prices in electricity markets Information approach: Include future information in pricing Equilbrium approach: Certainty equivalence principle for upper and lower bounds of prices Use market power as an explanantory variable for price formation

40 Coordinates folk.uio.no/fredb

A spot price model feasible for electricity forward pricing Part II

A spot price model feasible for electricity forward pricing Part II Fred Espen Benth Centre of Mathematics for Applications (CMA) University of Oslo, Norway Wolfgang Pauli Institute, Wien January 17-18

A spot price model feasible for electricity forward pricing Part II Fred Espen Benth Centre of Mathematics for Applications (CMA) University of Oslo, Norway Wolfgang Pauli Institute, Wien January 17-18

A non-gaussian Ornstein-Uhlenbeck process for electricity spot price modeling and derivatives pricing

A non-gaussian Ornstein-Uhlenbeck process for electricity spot price modeling and derivatives pricing Thilo Meyer-Brandis Center of Mathematics for Applications / University of Oslo Based on joint work

A non-gaussian Ornstein-Uhlenbeck process for electricity spot price modeling and derivatives pricing Thilo Meyer-Brandis Center of Mathematics for Applications / University of Oslo Based on joint work

Rafał Weron. Hugo Steinhaus Center Wrocław University of Technology

Rafał Weron Hugo Steinhaus Center Wrocław University of Technology Options trading at Nord Pool commenced on October 29, 1999 with two types of contracts European-style Electric/Power Options (EEO/EPO)

Rafał Weron Hugo Steinhaus Center Wrocław University of Technology Options trading at Nord Pool commenced on October 29, 1999 with two types of contracts European-style Electric/Power Options (EEO/EPO)

Lecture IV: Option pricing in energy markets

Lecture IV: Option pricing in energy markets Fred Espen Benth Centre of Mathematics for Applications (CMA) University of Oslo, Norway Fields Institute, 19-23 August, 2013 Introduction OTC market huge for

Lecture IV: Option pricing in energy markets Fred Espen Benth Centre of Mathematics for Applications (CMA) University of Oslo, Norway Fields Institute, 19-23 August, 2013 Introduction OTC market huge for

The Pass-Through Cost of Carbon in Australian Electricity Markets

The Pass-Through Cost of Carbon in Australian Electricity Markets Stefan Trück Department of Applied Finance and Actuarial Studies Macquarie University, Sydney Mini-Symposium on Reducing Carbon Emissions

The Pass-Through Cost of Carbon in Australian Electricity Markets Stefan Trück Department of Applied Finance and Actuarial Studies Macquarie University, Sydney Mini-Symposium on Reducing Carbon Emissions

Pricing of an Exotic Forward Contract

Pricing of an Exotic Forward Contract Jirô Akahori, Yuji Hishida and Maho Nishida Dept. of Mathematical Sciences, Ritsumeikan University 1-1-1 Nojihigashi, Kusatsu, Shiga 525-8577, Japan E-mail: {akahori,

Pricing of an Exotic Forward Contract Jirô Akahori, Yuji Hishida and Maho Nishida Dept. of Mathematical Sciences, Ritsumeikan University 1-1-1 Nojihigashi, Kusatsu, Shiga 525-8577, Japan E-mail: {akahori,

Towards a European Market of Electricity : Spot and Derivatives Trading

Towards a European Market of Electricity : Spot and Derivatives Trading by Helyette Geman Professor of Finance University Paris IX Dauphine and ESSEC May 2002 Abstract Deregulation of electricity markets

Towards a European Market of Electricity : Spot and Derivatives Trading by Helyette Geman Professor of Finance University Paris IX Dauphine and ESSEC May 2002 Abstract Deregulation of electricity markets

The Behavior of Bonds and Interest Rates. An Impossible Bond Pricing Model. 780 w Interest Rate Models

780 w Interest Rate Models The Behavior of Bonds and Interest Rates Before discussing how a bond market-maker would delta-hedge, we first need to specify how bonds behave. Suppose we try to model a zero-coupon

780 w Interest Rate Models The Behavior of Bonds and Interest Rates Before discussing how a bond market-maker would delta-hedge, we first need to specify how bonds behave. Suppose we try to model a zero-coupon

When to Refinance Mortgage Loans in a Stochastic Interest Rate Environment

When to Refinance Mortgage Loans in a Stochastic Interest Rate Environment Siwei Gan, Jin Zheng, Xiaoxia Feng, and Dejun Xie Abstract Refinancing refers to the replacement of an existing debt obligation

When to Refinance Mortgage Loans in a Stochastic Interest Rate Environment Siwei Gan, Jin Zheng, Xiaoxia Feng, and Dejun Xie Abstract Refinancing refers to the replacement of an existing debt obligation

A BOUND ON LIBOR FUTURES PRICES FOR HJM YIELD CURVE MODELS

A BOUND ON LIBOR FUTURES PRICES FOR HJM YIELD CURVE MODELS VLADIMIR POZDNYAKOV AND J. MICHAEL STEELE Abstract. We prove that for a large class of widely used term structure models there is a simple theoretical

A BOUND ON LIBOR FUTURES PRICES FOR HJM YIELD CURVE MODELS VLADIMIR POZDNYAKOV AND J. MICHAEL STEELE Abstract. We prove that for a large class of widely used term structure models there is a simple theoretical

A spot market model for pricing derivatives in electricity markets

A spot market model for pricing derivatives in electricity markets Markus Burger, Bernhard Klar, Alfred Müller* and Gero Schindlmayr EnBW Gesellschaft für Stromhandel, Risk Controlling, Durlacher Allee

A spot market model for pricing derivatives in electricity markets Markus Burger, Bernhard Klar, Alfred Müller* and Gero Schindlmayr EnBW Gesellschaft für Stromhandel, Risk Controlling, Durlacher Allee

The Relationship between Spot and Futures Prices: an Empirical Analysis of Australian Electricity Markets. Abstract

The Relationship between Spot and Futures Prices: an Empirical Analysis of Australian Electricity Markets Rangga Handika, Stefan Trück Macquarie University, Sydney Abstract This paper presents an empirical

The Relationship between Spot and Futures Prices: an Empirical Analysis of Australian Electricity Markets Rangga Handika, Stefan Trück Macquarie University, Sydney Abstract This paper presents an empirical

Mathematical Finance

Mathematical Finance Option Pricing under the Risk-Neutral Measure Cory Barnes Department of Mathematics University of Washington June 11, 2013 Outline 1 Probability Background 2 Black Scholes for European

Mathematical Finance Option Pricing under the Risk-Neutral Measure Cory Barnes Department of Mathematics University of Washington June 11, 2013 Outline 1 Probability Background 2 Black Scholes for European

From Exotic Options to Exotic Underlyings: Electricity, Weather and Catastrophe Derivatives

From Exotic Options to Exotic Underlyings: Electricity, Weather and Catastrophe Derivatives Dr. Svetlana Borovkova Vrije Universiteit Amsterdam History of derivatives Derivative: a financial contract whose

From Exotic Options to Exotic Underlyings: Electricity, Weather and Catastrophe Derivatives Dr. Svetlana Borovkova Vrije Universiteit Amsterdam History of derivatives Derivative: a financial contract whose

Studies in Nonlinear Dynamics & Econometrics

Studies in Nonlinear Dynamics & Econometrics Volume 10, Issue 3 2006 Article 7 NONLINEAR ANALYSIS OF ELECTRICITY PRICES Risk Premia in Electricity Forward Prices Pavel Diko Steve Lawford Valerie Limpens

Studies in Nonlinear Dynamics & Econometrics Volume 10, Issue 3 2006 Article 7 NONLINEAR ANALYSIS OF ELECTRICITY PRICES Risk Premia in Electricity Forward Prices Pavel Diko Steve Lawford Valerie Limpens

Modelling electricity market data: the CARMA spot model, forward prices and the risk premium

Modelling electricity market data: the CARMA spot model, forward prices and the risk premium Formatvorlage des Untertitelmasters Claudia Klüppelberg durch Klicken bearbeiten Technische Universität München

Modelling electricity market data: the CARMA spot model, forward prices and the risk premium Formatvorlage des Untertitelmasters Claudia Klüppelberg durch Klicken bearbeiten Technische Universität München

Life-insurance-specific optimal investment: the impact of stochastic interest rate and shortfall constraint

Life-insurance-specific optimal investment: the impact of stochastic interest rate and shortfall constraint An Radon Workshop on Financial and Actuarial Mathematics for Young Researchers May 30-31 2007,

Life-insurance-specific optimal investment: the impact of stochastic interest rate and shortfall constraint An Radon Workshop on Financial and Actuarial Mathematics for Young Researchers May 30-31 2007,

Energy Markets. Weather Derivates

III: Weather Derivates René Bendheim Center for Finance Department of Operations Research & Financial Engineering Princeton University Banff, May 2007 Weather and Commodity Stand-alone temperature precipitation

III: Weather Derivates René Bendheim Center for Finance Department of Operations Research & Financial Engineering Princeton University Banff, May 2007 Weather and Commodity Stand-alone temperature precipitation

A Regime-Switching Model for Electricity Spot Prices. Gero Schindlmayr EnBW Trading GmbH g.schindlmayr@enbw.com

A Regime-Switching Model for Electricity Spot Prices Gero Schindlmayr EnBW Trading GmbH g.schindlmayr@enbw.com May 31, 25 A Regime-Switching Model for Electricity Spot Prices Abstract Electricity markets

A Regime-Switching Model for Electricity Spot Prices Gero Schindlmayr EnBW Trading GmbH g.schindlmayr@enbw.com May 31, 25 A Regime-Switching Model for Electricity Spot Prices Abstract Electricity markets

Notes on Black-Scholes Option Pricing Formula

. Notes on Black-Scholes Option Pricing Formula by De-Xing Guan March 2006 These notes are a brief introduction to the Black-Scholes formula, which prices the European call options. The essential reading

. Notes on Black-Scholes Option Pricing Formula by De-Xing Guan March 2006 These notes are a brief introduction to the Black-Scholes formula, which prices the European call options. The essential reading

Modelling Electricity Spot Prices A Regime-Switching Approach

Modelling Electricity Spot Prices A Regime-Switching Approach Dr. Gero Schindlmayr EnBW Trading GmbH Financial Modelling Workshop Ulm September 2005 Energie braucht Impulse Agenda Model Overview Daily

Modelling Electricity Spot Prices A Regime-Switching Approach Dr. Gero Schindlmayr EnBW Trading GmbH Financial Modelling Workshop Ulm September 2005 Energie braucht Impulse Agenda Model Overview Daily

On Market-Making and Delta-Hedging

On Market-Making and Delta-Hedging 1 Market Makers 2 Market-Making and Bond-Pricing On Market-Making and Delta-Hedging 1 Market Makers 2 Market-Making and Bond-Pricing What to market makers do? Provide

On Market-Making and Delta-Hedging 1 Market Makers 2 Market-Making and Bond-Pricing On Market-Making and Delta-Hedging 1 Market Makers 2 Market-Making and Bond-Pricing What to market makers do? Provide

Chapter 2 Forward and Futures Prices

Chapter 2 Forward and Futures Prices At the expiration date, a futures contract that calls for immediate settlement, should have a futures price equal to the spot price. Before settlement, futures and

Chapter 2 Forward and Futures Prices At the expiration date, a futures contract that calls for immediate settlement, should have a futures price equal to the spot price. Before settlement, futures and

ELECTRICITY REAL OPTIONS VALUATION

Vol. 37 (6) ACTA PHYSICA POLONICA B No 11 ELECTRICITY REAL OPTIONS VALUATION Ewa Broszkiewicz-Suwaj Hugo Steinhaus Center, Institute of Mathematics and Computer Science Wrocław University of Technology

Vol. 37 (6) ACTA PHYSICA POLONICA B No 11 ELECTRICITY REAL OPTIONS VALUATION Ewa Broszkiewicz-Suwaj Hugo Steinhaus Center, Institute of Mathematics and Computer Science Wrocław University of Technology

Master s Thesis. Pricing Constant Maturity Swap Derivatives

Master s Thesis Pricing Constant Maturity Swap Derivatives Thesis submitted in partial fulfilment of the requirements for the Master of Science degree in Stochastics and Financial Mathematics by Noemi

Master s Thesis Pricing Constant Maturity Swap Derivatives Thesis submitted in partial fulfilment of the requirements for the Master of Science degree in Stochastics and Financial Mathematics by Noemi

Pricing catastrophe options in incomplete market

Pricing catastrophe options in incomplete market Arthur Charpentier arthur.charpentier@univ-rennes1.fr Actuarial and Financial Mathematics Conference Interplay between finance and insurance, February 2008

Pricing catastrophe options in incomplete market Arthur Charpentier arthur.charpentier@univ-rennes1.fr Actuarial and Financial Mathematics Conference Interplay between finance and insurance, February 2008

Marginal value approach to pricing temperature options and its empirical example on daily temperatures in Nagoya. Yoshiyuki Emoto and Tetsuya Misawa

Discussion Papers in Economics No. Marginal value approach to pricing temperature options and its empirical example on daily temperatures in Nagoya Yoshiyuki Emoto and Tetsuya Misawa August 2, 2006 Faculty

Discussion Papers in Economics No. Marginal value approach to pricing temperature options and its empirical example on daily temperatures in Nagoya Yoshiyuki Emoto and Tetsuya Misawa August 2, 2006 Faculty

Risk-minimization for life insurance liabilities

Risk-minimization for life insurance liabilities Francesca Biagini Mathematisches Institut Ludwig Maximilians Universität München February 24, 2014 Francesca Biagini USC 1/25 Introduction A large number

Risk-minimization for life insurance liabilities Francesca Biagini Mathematisches Institut Ludwig Maximilians Universität München February 24, 2014 Francesca Biagini USC 1/25 Introduction A large number

Pricing Swing Options and other Electricity Derivatives

Pricing Swing Options and other Electricity Derivatives Tino Kluge St Hugh s College University of Oxford Doctor of Philosophy Hillary 26 This thesis is dedicated to my mum and dad for their love and support.

Pricing Swing Options and other Electricity Derivatives Tino Kluge St Hugh s College University of Oxford Doctor of Philosophy Hillary 26 This thesis is dedicated to my mum and dad for their love and support.

ELECTRICITY FORWARD PRICES: A High-Frequency Empirical Analysis. Francis A. Longstaff Ashley W. Wang

ELECTRICITY FORWARD PRICES: A High-Frequency Empirical Analysis Francis A. Longstaff Ashley W. Wang Initial version: January 22. Current version: July 22. Francis Longstaff is with the Anderson School

ELECTRICITY FORWARD PRICES: A High-Frequency Empirical Analysis Francis A. Longstaff Ashley W. Wang Initial version: January 22. Current version: July 22. Francis Longstaff is with the Anderson School

Black-Scholes Equation for Option Pricing

Black-Scholes Equation for Option Pricing By Ivan Karmazin, Jiacong Li 1. Introduction In early 1970s, Black, Scholes and Merton achieved a major breakthrough in pricing of European stock options and there

Black-Scholes Equation for Option Pricing By Ivan Karmazin, Jiacong Li 1. Introduction In early 1970s, Black, Scholes and Merton achieved a major breakthrough in pricing of European stock options and there

Volatility Index: VIX vs. GVIX

I. II. III. IV. Volatility Index: VIX vs. GVIX "Does VIX Truly Measure Return Volatility?" by Victor Chow, Wanjun Jiang, and Jingrui Li (214) An Ex-ante (forward-looking) approach based on Market Price

I. II. III. IV. Volatility Index: VIX vs. GVIX "Does VIX Truly Measure Return Volatility?" by Victor Chow, Wanjun Jiang, and Jingrui Li (214) An Ex-ante (forward-looking) approach based on Market Price

Pension Risk Management with Funding and Buyout Options

Pension Risk Management with Funding and Buyout Options Samuel H. Cox, Yijia Lin, Tianxiang Shi Department of Finance College of Business Administration University of Nebraska-Lincoln FIRM 2015, Beijing

Pension Risk Management with Funding and Buyout Options Samuel H. Cox, Yijia Lin, Tianxiang Shi Department of Finance College of Business Administration University of Nebraska-Lincoln FIRM 2015, Beijing

A decade of "Rough" storage trading results in the UK NBP gas market:

A decade of "Rough" storage trading results in the UK NBP gas market: Benchmarking storage trading strategies Cyriel de Jong, Alexander Boogert, Christopher Clancy KYOS Energy Consulting How much money

A decade of "Rough" storage trading results in the UK NBP gas market: Benchmarking storage trading strategies Cyriel de Jong, Alexander Boogert, Christopher Clancy KYOS Energy Consulting How much money

The Effect of Management Discretion on Hedging and Fair Valuation of Participating Policies with Maturity Guarantees

The Effect of Management Discretion on Hedging and Fair Valuation of Participating Policies with Maturity Guarantees Torsten Kleinow Heriot-Watt University, Edinburgh (joint work with Mark Willder) Market-consistent

The Effect of Management Discretion on Hedging and Fair Valuation of Participating Policies with Maturity Guarantees Torsten Kleinow Heriot-Watt University, Edinburgh (joint work with Mark Willder) Market-consistent

The Term Structure of Interest Rates, Spot Rates, and Yield to Maturity

Chapter 5 How to Value Bonds and Stocks 5A-1 Appendix 5A The Term Structure of Interest Rates, Spot Rates, and Yield to Maturity In the main body of this chapter, we have assumed that the interest rate

Chapter 5 How to Value Bonds and Stocks 5A-1 Appendix 5A The Term Structure of Interest Rates, Spot Rates, and Yield to Maturity In the main body of this chapter, we have assumed that the interest rate

Moral Hazard. Itay Goldstein. Wharton School, University of Pennsylvania

Moral Hazard Itay Goldstein Wharton School, University of Pennsylvania 1 Principal-Agent Problem Basic problem in corporate finance: separation of ownership and control: o The owners of the firm are typically

Moral Hazard Itay Goldstein Wharton School, University of Pennsylvania 1 Principal-Agent Problem Basic problem in corporate finance: separation of ownership and control: o The owners of the firm are typically

Bayesian Adaptive Trading with a Daily Cycle

Bayesian Adaptive Trading with a Daily Cycle Robert Almgren and Julian Lorenz July 28, 26 Abstract Standard models of algorithmic trading neglect the presence of a daily cycle. We construct a model in

Bayesian Adaptive Trading with a Daily Cycle Robert Almgren and Julian Lorenz July 28, 26 Abstract Standard models of algorithmic trading neglect the presence of a daily cycle. We construct a model in

Fund Manager s Portfolio Choice

Fund Manager s Portfolio Choice Zhiqing Zhang Advised by: Gu Wang September 5, 2014 Abstract Fund manager is allowed to invest the fund s assets and his personal wealth in two separate risky assets, modeled

Fund Manager s Portfolio Choice Zhiqing Zhang Advised by: Gu Wang September 5, 2014 Abstract Fund manager is allowed to invest the fund s assets and his personal wealth in two separate risky assets, modeled

Pricing Forwards and Futures

Pricing Forwards and Futures Peter Ritchken Peter Ritchken Forwards and Futures Prices 1 You will learn Objectives how to price a forward contract how to price a futures contract the relationship between

Pricing Forwards and Futures Peter Ritchken Peter Ritchken Forwards and Futures Prices 1 You will learn Objectives how to price a forward contract how to price a futures contract the relationship between

Real Estate Investments with Stochastic Cash Flows

Real Estate Investments with Stochastic Cash Flows Riaz Hussain Kania School of Management University of Scranton Scranton, PA 18510 hussain@scranton.edu 570-941-7497 April 2006 JEL classification: G12

Real Estate Investments with Stochastic Cash Flows Riaz Hussain Kania School of Management University of Scranton Scranton, PA 18510 hussain@scranton.edu 570-941-7497 April 2006 JEL classification: G12

On the Existence of a Unique Optimal Threshold Value for the Early Exercise of Call Options

On the Existence of a Unique Optimal Threshold Value for the Early Exercise of Call Options Patrick Jaillet Ehud I. Ronn Stathis Tompaidis July 2003 Abstract In the case of early exercise of an American-style

On the Existence of a Unique Optimal Threshold Value for the Early Exercise of Call Options Patrick Jaillet Ehud I. Ronn Stathis Tompaidis July 2003 Abstract In the case of early exercise of an American-style

On exponentially ane martingales. Johannes Muhle-Karbe

On exponentially ane martingales AMAMEF 2007, Bedlewo Johannes Muhle-Karbe Joint work with Jan Kallsen HVB-Institut für Finanzmathematik, Technische Universität München 1 Outline 1. Semimartingale characteristics

On exponentially ane martingales AMAMEF 2007, Bedlewo Johannes Muhle-Karbe Joint work with Jan Kallsen HVB-Institut für Finanzmathematik, Technische Universität München 1 Outline 1. Semimartingale characteristics

COMPLETE MARKETS DO NOT ALLOW FREE CASH FLOW STREAMS

COMPLETE MARKETS DO NOT ALLOW FREE CASH FLOW STREAMS NICOLE BÄUERLE AND STEFANIE GRETHER Abstract. In this short note we prove a conjecture posed in Cui et al. 2012): Dynamic mean-variance problems in

COMPLETE MARKETS DO NOT ALLOW FREE CASH FLOW STREAMS NICOLE BÄUERLE AND STEFANIE GRETHER Abstract. In this short note we prove a conjecture posed in Cui et al. 2012): Dynamic mean-variance problems in

2 The Term Structure of Interest Rates in a Hidden Markov Setting

2 The Term Structure of Interest Rates in a Hidden Markov Setting Robert J. Elliott 1 and Craig A. Wilson 2 1 Haskayne School of Business University of Calgary Calgary, Alberta, Canada relliott@ucalgary.ca

2 The Term Structure of Interest Rates in a Hidden Markov Setting Robert J. Elliott 1 and Craig A. Wilson 2 1 Haskayne School of Business University of Calgary Calgary, Alberta, Canada relliott@ucalgary.ca

Market price of risk implied by Asian-style electricity options and futures

Available online at www.sciencedirect.com Energy Economics 30 (2008) 1098 1115 www.elsevier.com/locate/eneco Market price of risk implied by Asian-style electricity options and futures Rafał Weron Hugo

Available online at www.sciencedirect.com Energy Economics 30 (2008) 1098 1115 www.elsevier.com/locate/eneco Market price of risk implied by Asian-style electricity options and futures Rafał Weron Hugo

Modeling the Implied Volatility Surface. Jim Gatheral Stanford Financial Mathematics Seminar February 28, 2003

Modeling the Implied Volatility Surface Jim Gatheral Stanford Financial Mathematics Seminar February 28, 2003 This presentation represents only the personal opinions of the author and not those of Merrill

Modeling the Implied Volatility Surface Jim Gatheral Stanford Financial Mathematics Seminar February 28, 2003 This presentation represents only the personal opinions of the author and not those of Merrill

Forward Contracts and Forward Rates

Forward Contracts and Forward Rates Outline and Readings Outline Forward Contracts Forward Prices Forward Rates Information in Forward Rates Reading Veronesi, Chapters 5 and 7 Tuckman, Chapters 2 and 16

Forward Contracts and Forward Rates Outline and Readings Outline Forward Contracts Forward Prices Forward Rates Information in Forward Rates Reading Veronesi, Chapters 5 and 7 Tuckman, Chapters 2 and 16

Explicit Option Pricing Formula for a Mean-Reverting Asset in Energy Markets

Explicit Option Pricing Formula for a Mean-Reverting Asset in Energy Markets Anatoliy Swishchuk Mathematical & Computational Finance Lab Dept of Math & Stat, University of Calgary, Calgary, AB, Canada

Explicit Option Pricing Formula for a Mean-Reverting Asset in Energy Markets Anatoliy Swishchuk Mathematical & Computational Finance Lab Dept of Math & Stat, University of Calgary, Calgary, AB, Canada

Pricing Interest-Rate- Derivative Securities

Pricing Interest-Rate- Derivative Securities John Hull Alan White University of Toronto This article shows that the one-state-variable interest-rate models of Vasicek (1977) and Cox, Ingersoll, and Ross

Pricing Interest-Rate- Derivative Securities John Hull Alan White University of Toronto This article shows that the one-state-variable interest-rate models of Vasicek (1977) and Cox, Ingersoll, and Ross

Optimisation Problems in Non-Life Insurance

Frankfurt, 6. Juli 2007 1 The de Finetti Problem The Optimal Strategy De Finetti s Example 2 Minimal Ruin Probabilities The Hamilton-Jacobi-Bellman Equation Two Examples 3 Optimal Dividends Dividends in

Frankfurt, 6. Juli 2007 1 The de Finetti Problem The Optimal Strategy De Finetti s Example 2 Minimal Ruin Probabilities The Hamilton-Jacobi-Bellman Equation Two Examples 3 Optimal Dividends Dividends in

Hedging Options In The Incomplete Market With Stochastic Volatility. Rituparna Sen Sunday, Nov 15

Hedging Options In The Incomplete Market With Stochastic Volatility Rituparna Sen Sunday, Nov 15 1. Motivation This is a pure jump model and hence avoids the theoretical drawbacks of continuous path models.

Hedging Options In The Incomplete Market With Stochastic Volatility Rituparna Sen Sunday, Nov 15 1. Motivation This is a pure jump model and hence avoids the theoretical drawbacks of continuous path models.

IMPLICIT OPTIONS IN LIFE INSURANCE CONTRACTS The case of lump sum options in deferred annuity contracts Tobias S. Dillmann Institut fur Finanz- und Aktuarwissenschaften c/o Abteilung Unternehmensplanung

IMPLICIT OPTIONS IN LIFE INSURANCE CONTRACTS The case of lump sum options in deferred annuity contracts Tobias S. Dillmann Institut fur Finanz- und Aktuarwissenschaften c/o Abteilung Unternehmensplanung

Stock Price Dynamics, Dividends and Option Prices with Volatility Feedback

Stock Price Dynamics, Dividends and Option Prices with Volatility Feedback Juho Kanniainen Tampere University of Technology New Thinking in Finance 12 Feb. 2014, London Based on J. Kanniainen and R. Piche,

Stock Price Dynamics, Dividends and Option Prices with Volatility Feedback Juho Kanniainen Tampere University of Technology New Thinking in Finance 12 Feb. 2014, London Based on J. Kanniainen and R. Piche,

Application of options in hedging of crude oil price risk

AMERICAN JOURNAL OF SOCIAL AND MANAGEMEN SCIENCES ISSN rint: 156-154, ISSN Online: 151-1559 doi:1.551/ajsms.1.1.1.67.74 1, ScienceHuβ, http://www.scihub.org/ajsms Application of options in hedging of crude

AMERICAN JOURNAL OF SOCIAL AND MANAGEMEN SCIENCES ISSN rint: 156-154, ISSN Online: 151-1559 doi:1.551/ajsms.1.1.1.67.74 1, ScienceHuβ, http://www.scihub.org/ajsms Application of options in hedging of crude

Electricity Market Management: The Nordic and California Experiences

Electricity Market Management: The Nordic and California Experiences Thomas F. Rutherford Energy Economics and Policy Lecture 11 May 2011 This talk is based in part on material pepared by Einar Hope, Norwegian

Electricity Market Management: The Nordic and California Experiences Thomas F. Rutherford Energy Economics and Policy Lecture 11 May 2011 This talk is based in part on material pepared by Einar Hope, Norwegian

Black-Scholes-Merton approach merits and shortcomings

Black-Scholes-Merton approach merits and shortcomings Emilia Matei 1005056 EC372 Term Paper. Topic 3 1. Introduction The Black-Scholes and Merton method of modelling derivatives prices was first introduced

Black-Scholes-Merton approach merits and shortcomings Emilia Matei 1005056 EC372 Term Paper. Topic 3 1. Introduction The Black-Scholes and Merton method of modelling derivatives prices was first introduced

PRICING OF GAS SWING OPTIONS. Andrea Pokorná. UNIVERZITA KARLOVA V PRAZE Fakulta sociálních věd Institut ekonomických studií

9 PRICING OF GAS SWING OPTIONS Andrea Pokorná UNIVERZITA KARLOVA V PRAZE Fakulta sociálních věd Institut ekonomických studií 1 Introduction Contracts for the purchase and sale of natural gas providing

9 PRICING OF GAS SWING OPTIONS Andrea Pokorná UNIVERZITA KARLOVA V PRAZE Fakulta sociálních věd Institut ekonomických studií 1 Introduction Contracts for the purchase and sale of natural gas providing

The Black-Scholes Formula

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Black-Scholes Formula These notes examine the Black-Scholes formula for European options. The Black-Scholes formula are complex as they are based on the

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Black-Scholes Formula These notes examine the Black-Scholes formula for European options. The Black-Scholes formula are complex as they are based on the

Decomposition of life insurance liabilities into risk factors theory and application to annuity conversion options

Decomposition of life insurance liabilities into risk factors theory and application to annuity conversion options Joint work with Daniel Bauer, Marcus C. Christiansen, Alexander Kling Research Training

Decomposition of life insurance liabilities into risk factors theory and application to annuity conversion options Joint work with Daniel Bauer, Marcus C. Christiansen, Alexander Kling Research Training

How To Model The Yield Curve

Modeling Bond Yields in Finance and Macroeconomics Francis X. Diebold, Monika Piazzesi, and Glenn D. Rudebusch* January 2005 Francis X. Diebold, Department of Economics, University of Pennsylvania, Philadelphia,

Modeling Bond Yields in Finance and Macroeconomics Francis X. Diebold, Monika Piazzesi, and Glenn D. Rudebusch* January 2005 Francis X. Diebold, Department of Economics, University of Pennsylvania, Philadelphia,

Chapter 6. Commodity Forwards and Futures. Question 6.1. Question 6.2

Chapter 6 Commodity Forwards and Futures Question 6.1 The spot price of a widget is $70.00. With a continuously compounded annual risk-free rate of 5%, we can calculate the annualized lease rates according

Chapter 6 Commodity Forwards and Futures Question 6.1 The spot price of a widget is $70.00. With a continuously compounded annual risk-free rate of 5%, we can calculate the annualized lease rates according

INTERNATIONAL COMPARISON OF INTEREST RATE GUARANTEES IN LIFE INSURANCE

INTERNATIONAL COMPARISON OF INTEREST RATE GUARANTEES IN LIFE INSURANCE J. DAVID CUMMINS, KRISTIAN R. MILTERSEN, AND SVEIN-ARNE PERSSON Abstract. Interest rate guarantees seem to be included in life insurance

INTERNATIONAL COMPARISON OF INTEREST RATE GUARANTEES IN LIFE INSURANCE J. DAVID CUMMINS, KRISTIAN R. MILTERSEN, AND SVEIN-ARNE PERSSON Abstract. Interest rate guarantees seem to be included in life insurance

Energy-Related Commodity Futures

CURANDO Universität Ulm Institut für Finanzmathematik Energy-Related Commodity Futures Statistics, Models and Derivatives Dissertation zur Erlangung des Doktorgrades Dr. rer. nat. der Fakultät für Mathematik

CURANDO Universität Ulm Institut für Finanzmathematik Energy-Related Commodity Futures Statistics, Models and Derivatives Dissertation zur Erlangung des Doktorgrades Dr. rer. nat. der Fakultät für Mathematik

ASSESSING THE RISK POTENTIAL OF PREMIUM PAYMENT OPTIONS

ASSESSING THE RISK POTENTIAL OF PREMIUM PAYMENT OPTIONS IN PARTICIPATING LIFE INSURANCE CONTRACTS Nadine Gatzert phone: +41 71 2434012, fax: +41 71 2434040 nadine.gatzert@unisg.ch Hato Schmeiser phone:

ASSESSING THE RISK POTENTIAL OF PREMIUM PAYMENT OPTIONS IN PARTICIPATING LIFE INSURANCE CONTRACTS Nadine Gatzert phone: +41 71 2434012, fax: +41 71 2434040 nadine.gatzert@unisg.ch Hato Schmeiser phone:

Exam MFE Spring 2007 FINAL ANSWER KEY 1 B 2 A 3 C 4 E 5 D 6 C 7 E 8 C 9 A 10 B 11 D 12 A 13 E 14 E 15 C 16 D 17 B 18 A 19 D

Exam MFE Spring 2007 FINAL ANSWER KEY Question # Answer 1 B 2 A 3 C 4 E 5 D 6 C 7 E 8 C 9 A 10 B 11 D 12 A 13 E 14 E 15 C 16 D 17 B 18 A 19 D **BEGINNING OF EXAMINATION** ACTUARIAL MODELS FINANCIAL ECONOMICS

Exam MFE Spring 2007 FINAL ANSWER KEY Question # Answer 1 B 2 A 3 C 4 E 5 D 6 C 7 E 8 C 9 A 10 B 11 D 12 A 13 E 14 E 15 C 16 D 17 B 18 A 19 D **BEGINNING OF EXAMINATION** ACTUARIAL MODELS FINANCIAL ECONOMICS

A Martingale System Theorem for Stock Investments

A Martingale System Theorem for Stock Investments Robert J. Vanderbei April 26, 1999 DIMACS New Market Models Workshop 1 Beginning Middle End Controversial Remarks Outline DIMACS New Market Models Workshop

A Martingale System Theorem for Stock Investments Robert J. Vanderbei April 26, 1999 DIMACS New Market Models Workshop 1 Beginning Middle End Controversial Remarks Outline DIMACS New Market Models Workshop

How To Price A Life Insurance Portfolio With A Mortality Risk

Indifference pricing of a life insurance portfolio with systematic mortality risk in a market with an asset driven by a Lévy process Łukasz Delong Institute of Econometrics, Division of Probabilistic Methods

Indifference pricing of a life insurance portfolio with systematic mortality risk in a market with an asset driven by a Lévy process Łukasz Delong Institute of Econometrics, Division of Probabilistic Methods

ARBITRAGE-FREE OPTION PRICING MODELS. Denis Bell. University of North Florida

ARBITRAGE-FREE OPTION PRICING MODELS Denis Bell University of North Florida Modelling Stock Prices Example American Express In mathematical finance, it is customary to model a stock price by an (Ito) stochatic

ARBITRAGE-FREE OPTION PRICING MODELS Denis Bell University of North Florida Modelling Stock Prices Example American Express In mathematical finance, it is customary to model a stock price by an (Ito) stochatic

Term Structure of Interest Rates

Appendix 8B Term Structure of Interest Rates To explain the process of estimating the impact of an unexpected shock in short-term interest rates on the entire term structure of interest rates, FIs use

Appendix 8B Term Structure of Interest Rates To explain the process of estimating the impact of an unexpected shock in short-term interest rates on the entire term structure of interest rates, FIs use

Maximum likelihood estimation of mean reverting processes

Maximum likelihood estimation of mean reverting processes José Carlos García Franco Onward, Inc. jcpollo@onwardinc.com Abstract Mean reverting processes are frequently used models in real options. For

Maximum likelihood estimation of mean reverting processes José Carlos García Franco Onward, Inc. jcpollo@onwardinc.com Abstract Mean reverting processes are frequently used models in real options. For

Using Currency Futures to Hedge Currency Risk

Using Currency Futures to Hedge Currency Risk By Sayee Srinivasan & Steven Youngren Product Research & Development Chicago Mercantile Exchange Inc. Introduction Investment professionals face a tough climate.

Using Currency Futures to Hedge Currency Risk By Sayee Srinivasan & Steven Youngren Product Research & Development Chicago Mercantile Exchange Inc. Introduction Investment professionals face a tough climate.

Pricing and Hedging of swing options in the European electricity and gas markets. John Hedestig

Pricing and Hedging of swing options in the European electricity and gas markets John Hedestig June, Acknowledgments I would like to thank my supervisors at Lund University, Erik Lindström and Rikard Green,

Pricing and Hedging of swing options in the European electricity and gas markets John Hedestig June, Acknowledgments I would like to thank my supervisors at Lund University, Erik Lindström and Rikard Green,

Sensitivity analysis of utility based prices and risk-tolerance wealth processes

Sensitivity analysis of utility based prices and risk-tolerance wealth processes Dmitry Kramkov, Carnegie Mellon University Based on a paper with Mihai Sirbu from Columbia University Math Finance Seminar,

Sensitivity analysis of utility based prices and risk-tolerance wealth processes Dmitry Kramkov, Carnegie Mellon University Based on a paper with Mihai Sirbu from Columbia University Math Finance Seminar,

Hedging of Life Insurance Liabilities

Hedging of Life Insurance Liabilities Thorsten Rheinländer, with Francesca Biagini and Irene Schreiber Vienna University of Technology and LMU Munich September 6, 2015 horsten Rheinländer, with Francesca

Hedging of Life Insurance Liabilities Thorsten Rheinländer, with Francesca Biagini and Irene Schreiber Vienna University of Technology and LMU Munich September 6, 2015 horsten Rheinländer, with Francesca

VALUATION OF PLAIN VANILLA INTEREST RATES SWAPS

Graduate School of Business Administration University of Virginia VALUATION OF PLAIN VANILLA INTEREST RATES SWAPS Interest-rate swaps have grown tremendously over the last 10 years. With this development,

Graduate School of Business Administration University of Virginia VALUATION OF PLAIN VANILLA INTEREST RATES SWAPS Interest-rate swaps have grown tremendously over the last 10 years. With this development,

Barrier Options. Peter Carr

Barrier Options Peter Carr Head of Quantitative Financial Research, Bloomberg LP, New York Director of the Masters Program in Math Finance, Courant Institute, NYU March 14th, 2008 What are Barrier Options?

Barrier Options Peter Carr Head of Quantitative Financial Research, Bloomberg LP, New York Director of the Masters Program in Math Finance, Courant Institute, NYU March 14th, 2008 What are Barrier Options?

Generation Asset Valuation with Operational Constraints A Trinomial Tree Approach

Generation Asset Valuation with Operational Constraints A Trinomial Tree Approach Andrew L. Liu ICF International September 17, 2008 1 Outline Power Plants Optionality -- Intrinsic vs. Extrinsic Values

Generation Asset Valuation with Operational Constraints A Trinomial Tree Approach Andrew L. Liu ICF International September 17, 2008 1 Outline Power Plants Optionality -- Intrinsic vs. Extrinsic Values

Creating Customer Value in Participating

in Participating Life Insurance Nadine Gatzert, Ines Holzmüller, and Hato Schmeiser Page 2 1. Introduction Participating life insurance contracts contain numerous guarantees and options: - E.g., minimum

in Participating Life Insurance Nadine Gatzert, Ines Holzmüller, and Hato Schmeiser Page 2 1. Introduction Participating life insurance contracts contain numerous guarantees and options: - E.g., minimum

EXIT TIME PROBLEMS AND ESCAPE FROM A POTENTIAL WELL

EXIT TIME PROBLEMS AND ESCAPE FROM A POTENTIAL WELL Exit Time problems and Escape from a Potential Well Escape From a Potential Well There are many systems in physics, chemistry and biology that exist

EXIT TIME PROBLEMS AND ESCAPE FROM A POTENTIAL WELL Exit Time problems and Escape from a Potential Well Escape From a Potential Well There are many systems in physics, chemistry and biology that exist

A Genetic Algorithm to Price an European Put Option Using the Geometric Mean Reverting Model

Applied Mathematical Sciences, vol 8, 14, no 143, 715-7135 HIKARI Ltd, wwwm-hikaricom http://dxdoiorg/11988/ams144644 A Genetic Algorithm to Price an European Put Option Using the Geometric Mean Reverting

Applied Mathematical Sciences, vol 8, 14, no 143, 715-7135 HIKARI Ltd, wwwm-hikaricom http://dxdoiorg/11988/ams144644 A Genetic Algorithm to Price an European Put Option Using the Geometric Mean Reverting

LECTURE 9: A MODEL FOR FOREIGN EXCHANGE

LECTURE 9: A MODEL FOR FOREIGN EXCHANGE 1. Foreign Exchange Contracts There was a time, not so long ago, when a U. S. dollar would buy you precisely.4 British pounds sterling 1, and a British pound sterling

LECTURE 9: A MODEL FOR FOREIGN EXCHANGE 1. Foreign Exchange Contracts There was a time, not so long ago, when a U. S. dollar would buy you precisely.4 British pounds sterling 1, and a British pound sterling

Risk analysis of annuity conversion options in a stochastic mortality environment

Risk analysis of annuity conversion options in a stochastic mortality environment Alexander Kling, Jochen Ruß und Katja Schilling Preprint Series: 22-2 Fakultät für Mathematik und Wirtschaftswissenschaften

Risk analysis of annuity conversion options in a stochastic mortality environment Alexander Kling, Jochen Ruß und Katja Schilling Preprint Series: 22-2 Fakultät für Mathematik und Wirtschaftswissenschaften

Program for Energy Trading, Derivatives and Risk Management by Kyos Energy Consulting, dr Cyriel de Jong Case studies

Program for Energy Trading, Derivatives and Risk Management by Kyos Energy Consulting, dr Cyriel de Jong Case studies We use cases throughout its course in various forms. The cases support the application

Program for Energy Trading, Derivatives and Risk Management by Kyos Energy Consulting, dr Cyriel de Jong Case studies We use cases throughout its course in various forms. The cases support the application

Optimal Auctions Continued

Lecture 6 Optimal Auctions Continued 1 Recap Last week, we... Set up the Myerson auction environment: n risk-neutral bidders independent types t i F i with support [, b i ] residual valuation of t 0 for

Lecture 6 Optimal Auctions Continued 1 Recap Last week, we... Set up the Myerson auction environment: n risk-neutral bidders independent types t i F i with support [, b i ] residual valuation of t 0 for

Real option valuation of expansion and abandonment options in offshore petroleum production

NORWEGIAN UNIVERSITY OF SCIENCE AND TECHNOLOGY PROJECT THESIS Real option valuation of expansion and abandonment options in offshore petroleum production Authors: Øystein Dahl HEM Alexander SVENDSEN Academic

NORWEGIAN UNIVERSITY OF SCIENCE AND TECHNOLOGY PROJECT THESIS Real option valuation of expansion and abandonment options in offshore petroleum production Authors: Øystein Dahl HEM Alexander SVENDSEN Academic

Martingale Pricing Applied to Options, Forwards and Futures

IEOR E4706: Financial Engineering: Discrete-Time Asset Pricing Fall 2005 c 2005 by Martin Haugh Martingale Pricing Applied to Options, Forwards and Futures We now apply martingale pricing theory to the

IEOR E4706: Financial Engineering: Discrete-Time Asset Pricing Fall 2005 c 2005 by Martin Haugh Martingale Pricing Applied to Options, Forwards and Futures We now apply martingale pricing theory to the

National Institute for Applied Statistics Research Australia. Working Paper

National Institute for Applied Statistics Research Australia The University of Wollongong Working Paper 10-14 Cointegration with a Time Trend and Pairs Trading Strategy: Empirical Study on the S&P 500

National Institute for Applied Statistics Research Australia The University of Wollongong Working Paper 10-14 Cointegration with a Time Trend and Pairs Trading Strategy: Empirical Study on the S&P 500

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2008 Answers 1 (a) Rights issue price = 2 5 x 0 8 = $2 00 per share Theoretical ex rights price = ((2 50 x 4) + (1 x 2 00)/5=$2

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2008 Answers 1 (a) Rights issue price = 2 5 x 0 8 = $2 00 per share Theoretical ex rights price = ((2 50 x 4) + (1 x 2 00)/5=$2

A Primer on Credit Default Swaps

A Primer on Credit Default Swaps Liuren Wu Baruch College and Bloomberg LP July 9, 2008, Beijing, China Liuren Wu CDS July 9, 2008, Beijing 1 / 25 The basic contractual structure of CDS A CDS is an OTC

A Primer on Credit Default Swaps Liuren Wu Baruch College and Bloomberg LP July 9, 2008, Beijing, China Liuren Wu CDS July 9, 2008, Beijing 1 / 25 The basic contractual structure of CDS A CDS is an OTC

Pricing Forwards and Swaps

Chapter 7 Pricing Forwards and Swaps 7. Forwards Throughout this chapter, we will repeatedly use the following property of no-arbitrage: P 0 (αx T +βy T ) = αp 0 (x T )+βp 0 (y T ). Here, P 0 (w T ) is

Chapter 7 Pricing Forwards and Swaps 7. Forwards Throughout this chapter, we will repeatedly use the following property of no-arbitrage: P 0 (αx T +βy T ) = αp 0 (x T )+βp 0 (y T ). Here, P 0 (w T ) is

Econ 132 C. Health Insurance: U.S., Risk Pooling, Risk Aversion, Moral Hazard, Rand Study 7

Econ 132 C. Health Insurance: U.S., Risk Pooling, Risk Aversion, Moral Hazard, Rand Study 7 C2. Health Insurance: Risk Pooling Health insurance works by pooling individuals together to reduce the variability

Econ 132 C. Health Insurance: U.S., Risk Pooling, Risk Aversion, Moral Hazard, Rand Study 7 C2. Health Insurance: Risk Pooling Health insurance works by pooling individuals together to reduce the variability

Risk-Neutral Valuation of Participating Life Insurance Contracts

Risk-Neutral Valuation of Participating Life Insurance Contracts DANIEL BAUER with R. Kiesel, A. Kling, J. Russ, and K. Zaglauer ULM UNIVERSITY RTG 1100 AND INSTITUT FÜR FINANZ- UND AKTUARWISSENSCHAFTEN

Risk-Neutral Valuation of Participating Life Insurance Contracts DANIEL BAUER with R. Kiesel, A. Kling, J. Russ, and K. Zaglauer ULM UNIVERSITY RTG 1100 AND INSTITUT FÜR FINANZ- UND AKTUARWISSENSCHAFTEN

Review of Basic Options Concepts and Terminology

Review of Basic Options Concepts and Terminology March 24, 2005 1 Introduction The purchase of an options contract gives the buyer the right to buy call options contract or sell put options contract some

Review of Basic Options Concepts and Terminology March 24, 2005 1 Introduction The purchase of an options contract gives the buyer the right to buy call options contract or sell put options contract some

Forwards, Swaps and Futures

IEOR E4706: Financial Engineering: Discrete-Time Models c 2010 by Martin Haugh Forwards, Swaps and Futures These notes 1 introduce forwards, swaps and futures, and the basic mechanics of their associated

IEOR E4706: Financial Engineering: Discrete-Time Models c 2010 by Martin Haugh Forwards, Swaps and Futures These notes 1 introduce forwards, swaps and futures, and the basic mechanics of their associated

VALUATION IN DERIVATIVES MARKETS

VALUATION IN DERIVATIVES MARKETS September 2005 Rawle Parris ABN AMRO Property Derivatives What is a Derivative? A contract that specifies the rights and obligations between two parties to receive or deliver

VALUATION IN DERIVATIVES MARKETS September 2005 Rawle Parris ABN AMRO Property Derivatives What is a Derivative? A contract that specifies the rights and obligations between two parties to receive or deliver

Contents. 5 Numerical results 27 5.1 Single policies... 27 5.2 Portfolio of policies... 29

Abstract The capital requirements for insurance companies in the Solvency I framework are based on the premium and claim expenditure. This approach does not take the individual risk of the insurer into

Abstract The capital requirements for insurance companies in the Solvency I framework are based on the premium and claim expenditure. This approach does not take the individual risk of the insurer into

QUANTIZED INTEREST RATE AT THE MONEY FOR AMERICAN OPTIONS

QUANTIZED INTEREST RATE AT THE MONEY FOR AMERICAN OPTIONS L. M. Dieng ( Department of Physics, CUNY/BCC, New York, New York) Abstract: In this work, we expand the idea of Samuelson[3] and Shepp[,5,6] for

QUANTIZED INTEREST RATE AT THE MONEY FOR AMERICAN OPTIONS L. M. Dieng ( Department of Physics, CUNY/BCC, New York, New York) Abstract: In this work, we expand the idea of Samuelson[3] and Shepp[,5,6] for

Moreover, under the risk neutral measure, it must be the case that (5) r t = µ t.

r t = µ t.") LECTURE 7: BLACK SCHOLES THEORY 1. Introduction: The Black Scholes Model In 1973 Fisher Black and Myron Scholes ushered in the modern era of derivative securities with a seminal paper 1 on the pricing

LECTURE 7: BLACK SCHOLES THEORY 1. Introduction: The Black Scholes Model In 1973 Fisher Black and Myron Scholes ushered in the modern era of derivative securities with a seminal paper 1 on the pricing

An exact formula for default swaptions pricing in the SSRJD stochastic intensity model

An exact formula for default swaptions pricing in the SSRJD stochastic intensity model Naoufel El-Bachir (joint work with D. Brigo, Banca IMI) Radon Institute, Linz May 31, 2007 ICMA Centre, University

An exact formula for default swaptions pricing in the SSRJD stochastic intensity model Naoufel El-Bachir (joint work with D. Brigo, Banca IMI) Radon Institute, Linz May 31, 2007 ICMA Centre, University