Market Conditions for Housing Loans in Uganda

|

|

|

- Susan Owen

- 8 years ago

- Views:

Transcription

1 Market Conditions for Housing Loans in Uganda Annika Nilsson Ph.D student Centre for banking and finance (Cefin) Royal Institute of Technology, Sweden

Royal Institute of")

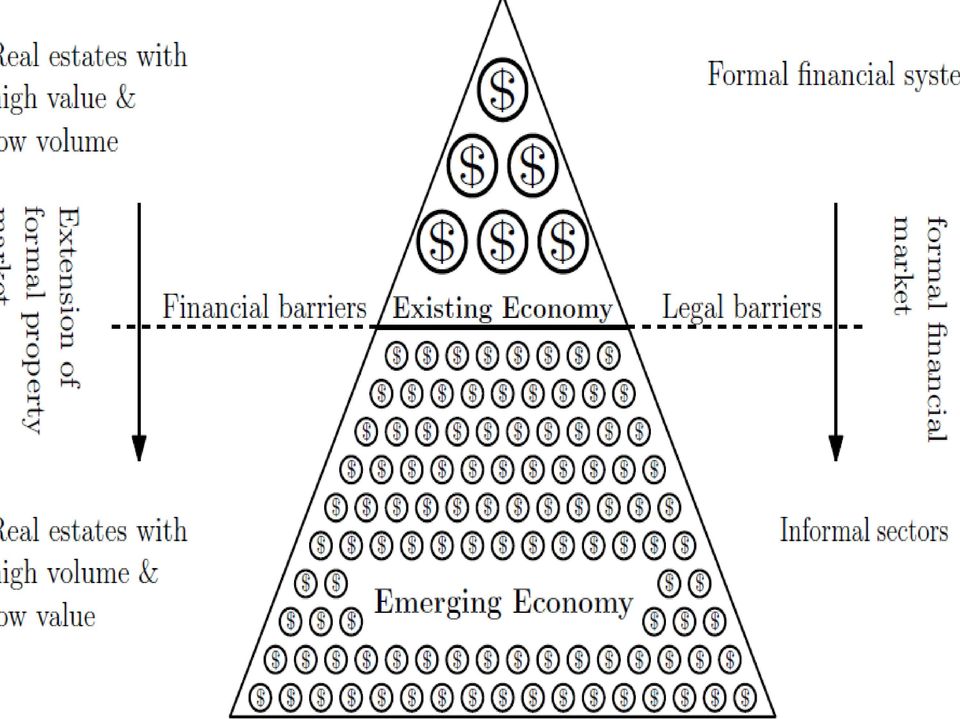

2 Background In developing countries the majority build their houses incrementally over a period of some years Some use small short term loans In Uganda, like in most developing countries, less than four per cent of the population can afford/qualify for a long term mortgage loan Purpose: Could the group of people building incrementally with the help of small loans be part of the mortgage market? Survey in Kampala, Uganda Potential demand of mortgage loans Actual demand of mortgage loans

3 A common example

4

5 Data collection: Centenary Bank in Uganda: one branch randomly selected in Kampala. Centenary Bank selected due to its popularity, the fifth largest bank, and way of screening and enforcing contracts Three and a half weeks survey: December-January ALL clients applying for a loan that was going to be used for housing or land were asked to fill in the questionnaire Response rate: 63%. 67 out of 107 clients filled in the questionnaire Approved: 82% of total sample. 76 % of men and 88 per cent of women.

-To complete construction")

6 Mortgage loan Home improvement loan Salary loan Housing Finance, DFCU, Stanbic etc. Centenary Development Bank Interest rate 16% 18-22% 19 % Repayment period Forcelosure Income Loan amount Max. 20 years After six months of failing to pay back is the security gone Monthly repayment not exceeding 40% of formal salary - Residental units 80% Loan to value ( LTV ) -To complete construction 50-70% LTV Average loan: ca UGX Max. 3 years The bank do everything to get the client to pay back Good source of income, formal and informal. Good relations with the bank. Minimum loan amount: UGX 100,000 Maximum loan amount : UGX

-To complete construction 50-70% LTV Average loan: ca UGX 100-200 Max.")

7 Potential demand for mortgages among short tem lenders Gender: 40% are women Age: 37% years, 24% years Employment: 72% regularly employed (62% of men, 85% women) Education: 83% have a University degree (66 % bachelor degree and 16 % a masters degree) Land ownership: among those owning land since before (62%) do 73% have a land title that is acceptable as collateral for long term mortgage loan. 22

do 73% have a land title that is acceptable as collateral for long term")

8 Short term loans for incremental building Use of the loan: Most, 66%, apply for a loan in order to buy land. Women want to buy land to a higher degree than men, 84 and 55 percent respectively. According to WB study do women only own 7 percent of registered Uganda (Ellis et al., 2006) Other financial sources: Mainly savings, around 80%, few had taken other loans, no loans from friends, relatives, very few inheritated land and house Demand for short term loans: The majority (42 per cent ) want to cover percent the cost of their housing with short term loans Estimated time to finish the house: The majority estimate it will take three years to finish their house

want to cover 30-50 percent the cost of their housing with short term loans Estimated time to finish the house: The")

9 Actual demand for mortgage loans: Have you applied before or will you within three years from now apply for a larger long term mortgage loan? % Total sample Regular job Women Men YES NO Do not know Answered Not answered

10 Why haven t you applied neither want to apply for a mortgage loan? Total Regular job Women Lack land as security Income to low Afraid loosing title if can t pay back in time Afraid loosing title due to corruption in Land Ministry Too complicated Bad credit history Other reason Answered Not answered Men

11 Final discussion Potential demand for mortgages larger than actual demand Lack of collateral not the main binding constraint to take long term mortgage loan Too complicated to apply for a mortgage loan Income too low Fear loosing title if fail to pay back in time (foreclosuring process) Market institutions available (banks) but not a strong legal system protecting borrowers

Market institutions available (banks) but not a strong legal system protecting")

12 Cont. final discussion Access to finance increases women s ownership of land 40 % of respondents in this survey are women. 84% of women are going to buy land. Women holds 7 per cent of registred land titles in Uganda. 9 % of all credit in Uganda goes to women.

13 THANKS!

Market Conditions for Housing Loans in Uganda

Market Conditions for Housing Loans in Uganda Annika Nilsson Introduction Housing is very capital intensive and constitute an important part of the development process. Housing finance markets are highly

Market Conditions for Housing Loans in Uganda Annika Nilsson Introduction Housing is very capital intensive and constitute an important part of the development process. Housing finance markets are highly

Developing Kenya s Mortgage Market

Developing Kenya s Mortgage Market Simon Walley Senior Housing Finance Specialist World Bank 17 February, 2011 - Nairobi Outline Rationale for developing the mortgage market Mortgage Market Summary Housing

Developing Kenya s Mortgage Market Simon Walley Senior Housing Finance Specialist World Bank 17 February, 2011 - Nairobi Outline Rationale for developing the mortgage market Mortgage Market Summary Housing

6 th African Microfinance Conference

6 th African Microfinance Conference Presentation by: Mr. Wilson Twamuhabwa CEO, UGAFODE Microfinance Limited (MDI) President AMFIU- Uganda MFI Network Contact: wtwamuhabwa@ugafode.co.ug About UGAFODE

6 th African Microfinance Conference Presentation by: Mr. Wilson Twamuhabwa CEO, UGAFODE Microfinance Limited (MDI) President AMFIU- Uganda MFI Network Contact: wtwamuhabwa@ugafode.co.ug About UGAFODE

Houses into Homes Empty Property Loan Scheme. Georgina Wayman Environmental Health Officer Private Sector Housing

Houses into Homes Empty Property Loan Scheme Georgina Wayman Environmental Health Officer Private Sector Housing Houses into Homes Loan Scheme In 2012, Welsh Government committed a 10 million recyclable

Houses into Homes Empty Property Loan Scheme Georgina Wayman Environmental Health Officer Private Sector Housing Houses into Homes Loan Scheme In 2012, Welsh Government committed a 10 million recyclable

For more information on plain English go to www.simplyput.ie. Transactions Involving Directors - A Quick Guide

For more information on plain English go to www.simplyput.ie Transactions Involving Directors - A Quick Guide Transactions Involving Directors A Quick Guide Contents About this booklet 2 Who do the rules

For more information on plain English go to www.simplyput.ie Transactions Involving Directors - A Quick Guide Transactions Involving Directors A Quick Guide Contents About this booklet 2 Who do the rules

HOME LOAN CfC Stanbic bank home loan facility

HOME LOAN CfC Stanbic bank home loan facility Have you found a house you d like to buy? 100% financing available for salaried individuals for property between 3M to 10M 70% financing available for Kenyans

HOME LOAN CfC Stanbic bank home loan facility Have you found a house you d like to buy? 100% financing available for salaried individuals for property between 3M to 10M 70% financing available for Kenyans

The crowdfunding platform for. professionals. Mortgage Loans

The crowdfunding platform for professionals Mortgage Loans INDEX Executive Summary 3 The borrowing counter 4 How it works 5 Conditions and costs 6 Interest 7 Refinancing and redemption 8 Guarantees 9 Other

The crowdfunding platform for professionals Mortgage Loans INDEX Executive Summary 3 The borrowing counter 4 How it works 5 Conditions and costs 6 Interest 7 Refinancing and redemption 8 Guarantees 9 Other

Home Mortgage Rates - The Different Types

UNIT 6 3 Fixed vs. Adjustable Rate Mortgages Slightly more than half of the mortgages issued in 2005 were fixed rate mortgages, while the majority of the remaining ones were of the adjustable rate variety.

UNIT 6 3 Fixed vs. Adjustable Rate Mortgages Slightly more than half of the mortgages issued in 2005 were fixed rate mortgages, while the majority of the remaining ones were of the adjustable rate variety.

4. Profit. 5. Credit

What do you want and how are you going to get it? Personal Finance 1. Income 2. Budget 3. Investing 4. Profit 6. Spending 7. Savings 8. Assets 9. Expenses Income vs. Expenses 5. Credit 10.Liabilities SS8E5

What do you want and how are you going to get it? Personal Finance 1. Income 2. Budget 3. Investing 4. Profit 6. Spending 7. Savings 8. Assets 9. Expenses Income vs. Expenses 5. Credit 10.Liabilities SS8E5

REVERSE MORTGAGE GUIDE

REVERSE MORTGAGE GUIDE Retire comfortably with a Reverse Mortgage CRAIG MINTON - AMERICAN NATIONWIDE MORTGAGE - 757-254-1331 Introduction Hello my name is Craig Minton, Regional Manager and Reverse Mortgage

REVERSE MORTGAGE GUIDE Retire comfortably with a Reverse Mortgage CRAIG MINTON - AMERICAN NATIONWIDE MORTGAGE - 757-254-1331 Introduction Hello my name is Craig Minton, Regional Manager and Reverse Mortgage

LIFETIME MORTGAGE LUMP SUM

LIFETIME MORTGAGE LUMP SUM Terms and Conditions (version 5) This is an important document. Please keep it in a safe place. LV= Lifetime Mortgage lump sum Terms and Conditions Welcome to LV=, and thank

LIFETIME MORTGAGE LUMP SUM Terms and Conditions (version 5) This is an important document. Please keep it in a safe place. LV= Lifetime Mortgage lump sum Terms and Conditions Welcome to LV=, and thank

Payment Protection Refunds.co.uk Claims Pack

Payment Protection Refunds.co.uk Claims Pack The following claim papers are all you need to begin your claim for a refund of Payment Protection Insurance 0161 495 3990 www.paymentprotectionrefunds.co.uk

Payment Protection Refunds.co.uk Claims Pack The following claim papers are all you need to begin your claim for a refund of Payment Protection Insurance 0161 495 3990 www.paymentprotectionrefunds.co.uk

Choosing life policies

Choosing life policies CHOOSING LIFE POLICIES Most people believe that life insurance is a good thing. For most of us, it underpins our financial planning, protecting our family, while for others it can

Choosing life policies CHOOSING LIFE POLICIES Most people believe that life insurance is a good thing. For most of us, it underpins our financial planning, protecting our family, while for others it can

Additional borrowing guide 1. Additional borrowing. We re with you every step of the way

Additional borrowing guide 1 Additional borrowing We re with you every step of the way Additional borrowing guide 2 What is additional borrowing? Sometimes you may be able to borrow extra money from your

Additional borrowing guide 1 Additional borrowing We re with you every step of the way Additional borrowing guide 2 What is additional borrowing? Sometimes you may be able to borrow extra money from your

The Home Loan Process

The Home Loan Process Step 1: Find out how much you can borrow Our mortgage consultants will work with you to find your borrowing capacity with our full range of lenders. Many banks and mortgage lenders

The Home Loan Process Step 1: Find out how much you can borrow Our mortgage consultants will work with you to find your borrowing capacity with our full range of lenders. Many banks and mortgage lenders

Government mortgage rescue scheme What will it mean for me and my family?

Government mortgage rescue scheme What will it mean for me and my family? What is mortgage rescue? Mortgage rescue is help that the Government is offering if: you are struggling to keep up with your mortgage

Government mortgage rescue scheme What will it mean for me and my family? What is mortgage rescue? Mortgage rescue is help that the Government is offering if: you are struggling to keep up with your mortgage

Switching your mortgage deal

Switching guide 1 Switching your mortgage deal We re with you every step of the way Switching guide 2 Why switch? If you re thinking about switching your mortgage, you might not have to shop around. You

Switching guide 1 Switching your mortgage deal We re with you every step of the way Switching guide 2 Why switch? If you re thinking about switching your mortgage, you might not have to shop around. You

Vendor Finance. Huonville: 8/16 Main St, Huonville 7109 DX 70754, Huonville PO Box 239, Huonville 7109 Ph: 03 6264 2967

Vendor Finance Huonville: 8/16 Main St, Huonville 7109 DX 70754, Huonville PO Box 239, Huonville 7109 Ph: 03 6264 2967 Hobart: Level 1, 18 Elizabeth St, Hobart 7000 DX 231, Hobart GPO Box 16, Hobart 7001

Vendor Finance Huonville: 8/16 Main St, Huonville 7109 DX 70754, Huonville PO Box 239, Huonville 7109 Ph: 03 6264 2967 Hobart: Level 1, 18 Elizabeth St, Hobart 7000 DX 231, Hobart GPO Box 16, Hobart 7001

Negative Equity Home Movers. Guiding you through your next move

Negative Equity Home Movers Guiding you through your next move WHAT IS NEGATIVE EQUITY? Negative equity occurs when the value of your house is less than the amount you owe on the mortgage. That means that

Negative Equity Home Movers Guiding you through your next move WHAT IS NEGATIVE EQUITY? Negative equity occurs when the value of your house is less than the amount you owe on the mortgage. That means that

LOANS, MORTGAGES, AND GUARANTEES APPLICATION FORM. 1 of 13 CBOQ Mortgage Application

LOANS, MORTGAGES, AND GUARANTEES APPLICATION FORM 1 of 13 CBOQ Mortgage Application Introduction The Canadian Baptists of Ontario and Quebec assists local churches through a program of Convention Loans

LOANS, MORTGAGES, AND GUARANTEES APPLICATION FORM 1 of 13 CBOQ Mortgage Application Introduction The Canadian Baptists of Ontario and Quebec assists local churches through a program of Convention Loans

Everything you need to know about equity release.

Everything you need to know about equity release. An informative guide from the equity release specialists Welcome to the Retiredom guide to equity release. Equity release has come a long way since regulation

Everything you need to know about equity release. An informative guide from the equity release specialists Welcome to the Retiredom guide to equity release. Equity release has come a long way since regulation

Uganda Housing Finance Bank UGANDA HOUSING FINANCE CONFERENCE 2 nd 3 rd July 2015 Kampala, Uganda

Uganda Housing Finance Bank UGANDA HOUSING FINANCE CONFERENCE 2 nd 3 rd July 2015 Kampala, Uganda A Mortgage Liquidity Facility (MLF) is a specialized financial institution designed to support long term

Uganda Housing Finance Bank UGANDA HOUSING FINANCE CONFERENCE 2 nd 3 rd July 2015 Kampala, Uganda A Mortgage Liquidity Facility (MLF) is a specialized financial institution designed to support long term

The default rate leapt up because:

The financial crisis What led up to the crisis? Short-term interest rates were very low, starting as a policy by the federal reserve, and stayed low in 2000-2005 partly due to policy, partly to expanding

The financial crisis What led up to the crisis? Short-term interest rates were very low, starting as a policy by the federal reserve, and stayed low in 2000-2005 partly due to policy, partly to expanding

How To Buy Life Insurance In Texas

TMAIT Insurance Guides for Physicians Life Insurance TMAIT Insurance Guides The TMAIT Insurance Guides are intended to help physicians make sound insurance decisions for themselves and their families.

TMAIT Insurance Guides for Physicians Life Insurance TMAIT Insurance Guides The TMAIT Insurance Guides are intended to help physicians make sound insurance decisions for themselves and their families.

Owner Title Insurance

Owner Title Insurance How it protects your equity Buying a home? Speak with an attorney. Your title may have some very expensive strings attached. Just imagine, you close on your new home. You move in.

Owner Title Insurance How it protects your equity Buying a home? Speak with an attorney. Your title may have some very expensive strings attached. Just imagine, you close on your new home. You move in.

1 Save a deposit. 2 Know your budget. 3 Find your new home. 4 Check everything. 5 Closing the deal

3 4 2 5 1 Buying a home is an exciting experience, but it can also be very stressful. So, being prepared before you start looking for a home will help you through the whole process. 1 Save a deposit 2

3 4 2 5 1 Buying a home is an exciting experience, but it can also be very stressful. So, being prepared before you start looking for a home will help you through the whole process. 1 Save a deposit 2

THE RESPONSIBLE EQUITY RELEASE GUIDE. Everything you need to know about equity release.

THE RESPONSIBLE EQUITY RELEASE GUIDE Everything you need to know about. An informative guide from the specialists Welcome to the Responsible guide to. Equity release has come a long way since regulation

THE RESPONSIBLE EQUITY RELEASE GUIDE Everything you need to know about. An informative guide from the specialists Welcome to the Responsible guide to. Equity release has come a long way since regulation

LIFETIME MORTGAGE LUMP SUM

LIFETIME MORTGAGE LUMP SUM Terms and Conditions (version 4) This is an important document. Please keep it in a safe place. LV= Lifetime Mortgage lump sum Terms and Conditions Welcome to LV=, and thank

LIFETIME MORTGAGE LUMP SUM Terms and Conditions (version 4) This is an important document. Please keep it in a safe place. LV= Lifetime Mortgage lump sum Terms and Conditions Welcome to LV=, and thank

WHAT IS EQUITY RELEASE? WHY CONSIDER EQUITY RELEASE?

WHAT IS EQUITY RELEASE? Equity Release can free some of the capital tied up in your home, while you continue to live there. This money can be in the form of a tax-free lump sum, a regular income or a combination

WHAT IS EQUITY RELEASE? Equity Release can free some of the capital tied up in your home, while you continue to live there. This money can be in the form of a tax-free lump sum, a regular income or a combination

EQUITY RELEASE GUIDE. Everything you need to know about equity release.

EQUITY RELEASE GUIDE Everything you need to know about equity release. An informative guide from the equity release specialists The informative guide to equity release... Equity release has come a long

EQUITY RELEASE GUIDE Everything you need to know about equity release. An informative guide from the equity release specialists The informative guide to equity release... Equity release has come a long

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased.

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Buy a new home from Berkeley with just 5% deposit*

Buy a new home from Berkeley with just 5% deposit* NewBuy with Berkeley% It can be hard to save for that all important mortgage deposit but now NewBuy is here to assist. NewBuy* is an innovative new government

Buy a new home from Berkeley with just 5% deposit* NewBuy with Berkeley% It can be hard to save for that all important mortgage deposit but now NewBuy is here to assist. NewBuy* is an innovative new government

Reverse Mortgage Presented by Ian MacGillivray, NMLS #638502 American Capital Corporation, NMLS #264422 Phone: 505-690-1089 Website:

Reverse Mortgage American Capital Corporation, Phone: 505-690-1089 Website: http://mortgagepartners-santafe.com Contents I. What Is a Reverse Mortgage? II. Benefits and Typical Uses III. Is the Home at

Reverse Mortgage American Capital Corporation, Phone: 505-690-1089 Website: http://mortgagepartners-santafe.com Contents I. What Is a Reverse Mortgage? II. Benefits and Typical Uses III. Is the Home at

Home loans for Indigenous Australians

Home loans for Indigenous Australians Buying a home Buying a home is one of the most significant steps you can take. Owning your own home can give you and your family stability and security. Deciding if,

Home loans for Indigenous Australians Buying a home Buying a home is one of the most significant steps you can take. Owning your own home can give you and your family stability and security. Deciding if,

Justin Kribs, CFP. Manager, Student Debt Counseling and Financial Management

Credit Management Justin Kribs, CFP Manager, Student Debt Counseling and Financial Management Overview After attending this session students should be able to Understand the parts of their credit score

Credit Management Justin Kribs, CFP Manager, Student Debt Counseling and Financial Management Overview After attending this session students should be able to Understand the parts of their credit score

4 Things Your Credit Score Determines:

4 Things Your Credit Score Determines: 1. Whether you ll be approved for credit for mortgages, car loans, installment loans, and credit cards 2. What interest rate you ll get on those loans 3. The cost

4 Things Your Credit Score Determines: 1. Whether you ll be approved for credit for mortgages, car loans, installment loans, and credit cards 2. What interest rate you ll get on those loans 3. The cost

AIB Mortgages Helping you move home. Tracker Interest Rate Retention and Negative Equity Mover Brochure. Guiding you through your next move.

AIB Mortgages Helping you move home. Tracker Interest Rate Retention and Negative Equity Mover Brochure. Guiding you through your next move. Contents 01 Introduction Tracker Interest Rate Retention Negative

AIB Mortgages Helping you move home. Tracker Interest Rate Retention and Negative Equity Mover Brochure. Guiding you through your next move. Contents 01 Introduction Tracker Interest Rate Retention Negative

Negative Equity Home Movers. Guiding you through your next move

Negative Equity Home Movers Guiding you through your next move WHAT IS NEGATIVE EQUITY? Negative equity occurs when the value of your house is less than the amount you owe on the mortgage. That means that

Negative Equity Home Movers Guiding you through your next move WHAT IS NEGATIVE EQUITY? Negative equity occurs when the value of your house is less than the amount you owe on the mortgage. That means that

No Money Down Investing R E I E T U T O R

No Money Down Investing R E I E T U T O R What is No Money Down Investing? Different Investors Have Different Meanings Meaning # 1 No cash out of your pocket Meaning # 2 No cash or financing out of your

No Money Down Investing R E I E T U T O R What is No Money Down Investing? Different Investors Have Different Meanings Meaning # 1 No cash out of your pocket Meaning # 2 No cash or financing out of your

Amortized Loan Example

Amortized Loan Example Chris Columbus bought a house for $293,000. He put 20% down and obtained a 3 simple interest amortized loan for the balance at 5 % annually interest for 30 8 years. a. Find the amount

Amortized Loan Example Chris Columbus bought a house for $293,000. He put 20% down and obtained a 3 simple interest amortized loan for the balance at 5 % annually interest for 30 8 years. a. Find the amount

IMPROVING YOUR CREDIT AND DEBT

IMPROVING YOUR CREDIT AND DEBT The Credit & Debt Problem Americans are loaded with credit-card debt. The average American household with at least one credit card has nearly $15,950 in credit-card debt

IMPROVING YOUR CREDIT AND DEBT The Credit & Debt Problem Americans are loaded with credit-card debt. The average American household with at least one credit card has nearly $15,950 in credit-card debt

If you would like this information in large print, in braille or on cassette or CD, please call 0845 271 0900. Financial Questionnaire.

Financial Questionnaire You must fill in this form fully and truthfully to the best of your knowledge and belief. If you do not do this, and this affects our assessment of the risk, your insurance may

Financial Questionnaire You must fill in this form fully and truthfully to the best of your knowledge and belief. If you do not do this, and this affects our assessment of the risk, your insurance may

What is a Short Sale?

What is a Short Sale? A Short Sale is used to describe the sale of a home in which the homeowner owes the bank more than the home is worth. The bank agrees to allow the home to be sold for less than what

What is a Short Sale? A Short Sale is used to describe the sale of a home in which the homeowner owes the bank more than the home is worth. The bank agrees to allow the home to be sold for less than what

Central Bank of Ireland Macro-prudential policy for residential mortgage lending Consultation Paper CP87

Central Bank of Ireland Macro-prudential policy for residential mortgage lending Consultation Paper CP87 An initial assessment from Genworth Financial The Central Bank ( CB ) published a consultation paper

Central Bank of Ireland Macro-prudential policy for residential mortgage lending Consultation Paper CP87 An initial assessment from Genworth Financial The Central Bank ( CB ) published a consultation paper

Mortgage Loans in the Czech Republic

Mortgage Loans in the Czech Republic BIVŠ 10. 3. 2014 Petr Kielar http://petr.kielar.cz/download Overview What is the Mortgage Loan? Mortgage Loans and Mortgage Bonds Credit Process Repayment Market Overview

Mortgage Loans in the Czech Republic BIVŠ 10. 3. 2014 Petr Kielar http://petr.kielar.cz/download Overview What is the Mortgage Loan? Mortgage Loans and Mortgage Bonds Credit Process Repayment Market Overview

BUSINESS FINANCIAL QUESTIONNAIRE (NOVEMBER 2015)

") Plan number BUSINESS FINANCIAL QUESTIONNAIRE (NOVEMBER 2015) Important Note: Please answer all of the questions on this form honestly and in full. If you miss any information out, or give us misleading

Plan number BUSINESS FINANCIAL QUESTIONNAIRE (NOVEMBER 2015) Important Note: Please answer all of the questions on this form honestly and in full. If you miss any information out, or give us misleading

Unfair Credit Agreement & Mis-sold Payment Protection Insurance Claim Pack

Unfair Credit Agreement & Mis-sold Payment Protection Insurance Claim Pack Contents: Client Disclaimer & Audit Confirmation About You Loan & Credit Card Questionnaire: fill out one form for each credit

Unfair Credit Agreement & Mis-sold Payment Protection Insurance Claim Pack Contents: Client Disclaimer & Audit Confirmation About You Loan & Credit Card Questionnaire: fill out one form for each credit

Bankruptcy/Debt Collection

Bankruptcy/Debt Collection [ADVOCATE: Give caller advice per script. Check case acceptance list and refer to appropriate offfice for more services.] I. Explain Judgment Proof Judgment proof means you have

Bankruptcy/Debt Collection [ADVOCATE: Give caller advice per script. Check case acceptance list and refer to appropriate offfice for more services.] I. Explain Judgment Proof Judgment proof means you have

MORTGAGES4REAL LIMITED

WELCOME TO MIKE ROGERSON.CO.UK ESTATE AGENTS SURVEYORS LETTINGS MANGEMENT MIKE ROGERSON MORTGAGES4REAL LIMITED We know that taking out a mortgage will probably be the biggest financial commitment you can

WELCOME TO MIKE ROGERSON.CO.UK ESTATE AGENTS SURVEYORS LETTINGS MANGEMENT MIKE ROGERSON MORTGAGES4REAL LIMITED We know that taking out a mortgage will probably be the biggest financial commitment you can

Accion Venture Lab. Job Description Bank INSERT REPORT TITLE HERE

INSERT REPORT TITLE HERE Accion Venture Lab Author s Name Date Page This work is licensed under the Creative Commons Attribution-ShareAlike 4.0 International License. To view a copy of this license, visit

INSERT REPORT TITLE HERE Accion Venture Lab Author s Name Date Page This work is licensed under the Creative Commons Attribution-ShareAlike 4.0 International License. To view a copy of this license, visit

First Time Buyer Mortgage Information

First Time Buyer Mortgage Information If you re thinking about a Mortgage for your first home talk to us today A good time to talk to us? We re here to listen and help you whenever you need to talk to

First Time Buyer Mortgage Information If you re thinking about a Mortgage for your first home talk to us today A good time to talk to us? We re here to listen and help you whenever you need to talk to

SBA LOAN APPLICATION

Please submit application to Mike Litton at mlitton@plainscapital.com. SBA LOAN APPLICATION PlainsCapital Bank is a Preferred SBA Lender. The following information is required for initial processing, however,

Please submit application to Mike Litton at mlitton@plainscapital.com. SBA LOAN APPLICATION PlainsCapital Bank is a Preferred SBA Lender. The following information is required for initial processing, however,

Mortgage Term Glossary

Mortgage Term Glossary Advance - The mortgage Loan. Adverse Credit - This is the term used if the borrower has suffered a poor credit history. This could include previous mortgage or loan arrears, CCJ's

Mortgage Term Glossary Advance - The mortgage Loan. Adverse Credit - This is the term used if the borrower has suffered a poor credit history. This could include previous mortgage or loan arrears, CCJ's

payment protection insurance: consumer questionnaire

our ref: payment protection insurance: consumer questionnaire WHAT IS THIS QUESTIONNAIRE FOR? This questionnaire is for consumers to bring a complaint about the sale of payment protection insurance (PPI).

our ref: payment protection insurance: consumer questionnaire WHAT IS THIS QUESTIONNAIRE FOR? This questionnaire is for consumers to bring a complaint about the sale of payment protection insurance (PPI).

2015 U.S. BANK STUDENTS AND PERSONAL FINANCE STUDY

2015 U.S. BANK STUDENTS AND PERSONAL FINANCE STUDY Student Perspectives on Money and Finances July 7, 2015 2015 U.S. Bancorp. All Rights Reserved. This information is not intended to be a forecast of future

2015 U.S. BANK STUDENTS AND PERSONAL FINANCE STUDY Student Perspectives on Money and Finances July 7, 2015 2015 U.S. Bancorp. All Rights Reserved. This information is not intended to be a forecast of future

SCHULICH SCHOOL OF LAW BURSARY APPLICATION FREQUENTLY ASKED QUESTIONS

SCHULICH SCHOOL OF LAW BURSARY APPLICATION FREQUENTLY ASKED QUESTIONS Here is a list of questions and answers we have compiled that will answer some of the most frequent question we get each year from

SCHULICH SCHOOL OF LAW BURSARY APPLICATION FREQUENTLY ASKED QUESTIONS Here is a list of questions and answers we have compiled that will answer some of the most frequent question we get each year from

REGULATION ON MORTGAGE LENDING PROCESS

UNOFFICIAL TRANSLATION Appendix to the Resolution No 446, of the Governor of the Bank of Mongolia, dated October 17, 2008 REGULATION ON MORTGAGE LENDING PROCESS CONTENTS One. GENERAL PROVISION 1. Purpose

UNOFFICIAL TRANSLATION Appendix to the Resolution No 446, of the Governor of the Bank of Mongolia, dated October 17, 2008 REGULATION ON MORTGAGE LENDING PROCESS CONTENTS One. GENERAL PROVISION 1. Purpose

banking Your Home A guide to buying your next home www.bendigobank.com.au

banking Your Home A guide to buying your next home www.bendigobank.com.au Your Home A guide to buying your next home As you would already know from past experience, buying a new home is a great achievement

banking Your Home A guide to buying your next home www.bendigobank.com.au Your Home A guide to buying your next home As you would already know from past experience, buying a new home is a great achievement

A roadmap for funding your business

A Citibank Resource for Your Business A roadmap for funding your business Jupiterimages/BananaStock/Thinkstock Successfully launching a new business takes a good deal of skill and hard work. It also requires

A Citibank Resource for Your Business A roadmap for funding your business Jupiterimages/BananaStock/Thinkstock Successfully launching a new business takes a good deal of skill and hard work. It also requires

SBA 7(a) Government. Guaranteed Loan Program

Government. Guaranteed Loan Program") SBA 7(a) Government Guaranteed Loan Program SBA Overview The U.S. Small Business Administration (SBA) Was Created By Congress In 1953 To Assist And Counsel Small Business Growth And Prosperity, Thereby

SBA 7(a) Government Guaranteed Loan Program SBA Overview The U.S. Small Business Administration (SBA) Was Created By Congress In 1953 To Assist And Counsel Small Business Growth And Prosperity, Thereby

Home Loans for Foreigners in Thailand

Asia Pacific Region Fourth quarter 2012 housing finance news from Thailand GH Bank home loans to qualified foreign borrowers More and more foreigner non-thai citizens are now finally able under certain

Asia Pacific Region Fourth quarter 2012 housing finance news from Thailand GH Bank home loans to qualified foreign borrowers More and more foreigner non-thai citizens are now finally able under certain

Product Guide. For intermediary use only FOUNDATION HOME LOANS. Effective from December 2015

01276 601041 info@buytoletclub.com www.buytoletclub.com Guide For intermediary use only FOUNDATION HOME LOANS Effective from December 2015 Foundation Home s is a trading style of Paratus AMC Limited who

01276 601041 info@buytoletclub.com www.buytoletclub.com Guide For intermediary use only FOUNDATION HOME LOANS Effective from December 2015 Foundation Home s is a trading style of Paratus AMC Limited who

Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money.

TEACHER GUIDE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Priority Academic Student Skills

TEACHER GUIDE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Priority Academic Student Skills

Executive Summary. Applicant (Principal) Name: Street Address: City: State: Zip Code: Business name or dba: Office: Cell: Fax: Email:

Name: Street Address: City: State: Zip Code: Business name or dba: Office: Cell: Fax: Email:") Executive Summary Applicant (Principal) Name: Street Address: City: State: Zip Code: Business name or dba: Office: Cell: Fax: Email: Amount Requested : $ Value/Purchase Price: $ Project Description : What

Executive Summary Applicant (Principal) Name: Street Address: City: State: Zip Code: Business name or dba: Office: Cell: Fax: Email: Amount Requested : $ Value/Purchase Price: $ Project Description : What

Recommended Solution

October 17, 2011 TM Recommended Solution Your Debt Reduction Goal: Increase cash flow by making debt payments smaller You ve indicated that you re fairly comfortable with your financial situation. Since

October 17, 2011 TM Recommended Solution Your Debt Reduction Goal: Increase cash flow by making debt payments smaller You ve indicated that you re fairly comfortable with your financial situation. Since

Buying a Property. The steps to buying a property. Finding a Property

Buying a Property For most of us, buying a house or a flat is the most important financial transaction that we will ever get involved with. It can be a complicated business but your solicitor can help

Buying a Property For most of us, buying a house or a flat is the most important financial transaction that we will ever get involved with. It can be a complicated business but your solicitor can help

MORTGAGE DICTIONARY. Amortization - Amortization is a decrease in the value of assets with time, which is normally the useful life of tangible assets.

MORTGAGE DICTIONARY Adjustable-Rate Mortgage An adjustable-rate mortgage (ARM) is a product with a floating or variable rate that adjusts based on some index. Amortization - Amortization is a decrease

MORTGAGE DICTIONARY Adjustable-Rate Mortgage An adjustable-rate mortgage (ARM) is a product with a floating or variable rate that adjusts based on some index. Amortization - Amortization is a decrease

are you financially well organised? Good Debt, Bad Debt Developing an effective Debt Plan www.financiallywellorganised.com info@fwo.net.

are you financially well organised? Good Debt, Bad Debt Developing an effective Debt Plan www.financiallywellorganised.com info@fwo.net.au Good Debt, Bad Debt In today s society, it is unusual if you do

are you financially well organised? Good Debt, Bad Debt Developing an effective Debt Plan www.financiallywellorganised.com info@fwo.net.au Good Debt, Bad Debt In today s society, it is unusual if you do

businessmortgagesolutions

businessmortgagesolutions Tel: 01834 849797 email: info@business-mortgage.com All you need to know about funding the purchase of a leasehold business Introduction Backed by over 20 years experience in

businessmortgagesolutions Tel: 01834 849797 email: info@business-mortgage.com All you need to know about funding the purchase of a leasehold business Introduction Backed by over 20 years experience in

Account Receivable Financing/Leveraging

Account Receivable Financing/Leveraging Copyright, The WPI 2006 1 Introduction The concept of Accounts Receivable Financing has evolved from traditional factoring (selling A/R at a discount for immediate

Account Receivable Financing/Leveraging Copyright, The WPI 2006 1 Introduction The concept of Accounts Receivable Financing has evolved from traditional factoring (selling A/R at a discount for immediate

HALIFAX INTERMEDIARIES MORTGAGE CREDIT DIRECTIVE FREQUENTLY ASKED QUESTIONS. For the use of mortgage intermediaries and other professionals only.

HALIFAX INTERMEDIARIES MORTGAGE CREDIT DIRECTIVE FREQUENTLY ASKED S. MORTGAGE ILLUSTRATION OPENING SECTION On the Mortgage Illustration why is the valid until date the same as the date the illustration

HALIFAX INTERMEDIARIES MORTGAGE CREDIT DIRECTIVE FREQUENTLY ASKED S. MORTGAGE ILLUSTRATION OPENING SECTION On the Mortgage Illustration why is the valid until date the same as the date the illustration

Financing Residential Real Estate: SAFE Comprehensive 20 Hours

Financing Residential Real Estate: SAFE Comprehensive 20 Hours COURSE ORGANIZATION and DESIGN Roy L. Ponthier, Ph.D., Ed.D., CDEI, DREI Executive Director Module 1: Finance and Investment Mortgage loans

Financing Residential Real Estate: SAFE Comprehensive 20 Hours COURSE ORGANIZATION and DESIGN Roy L. Ponthier, Ph.D., Ed.D., CDEI, DREI Executive Director Module 1: Finance and Investment Mortgage loans

GH Bank announcement Subject: Mortgage Fees

GH Bank announcement Subject: Mortgage Fees No. Types of fees Fee Rate (Baht) Terms / Remarks 1 Appraisal Fees 1.1 General retail loans; Refinancing and welfare loans without Bank deposits Appraisal fees

GH Bank announcement Subject: Mortgage Fees No. Types of fees Fee Rate (Baht) Terms / Remarks 1 Appraisal Fees 1.1 General retail loans; Refinancing and welfare loans without Bank deposits Appraisal fees

Your guide to conveyancing. The journey starts here. Minimise delays with our top tips. navigat r. a nudge in the right direction

Minimise delays with our top tips The journey starts here navigat r a nudge in the right direction Things you can do to help We know you want to move quickly. This guide highlights things you can do along

Minimise delays with our top tips The journey starts here navigat r a nudge in the right direction Things you can do to help We know you want to move quickly. This guide highlights things you can do along

Appraisal A written analysis prepared by a qualified appraiser and estimating the value of a property

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

David Miles Imperial College London

David Miles Imperial College London House Prices, Credit and the Wider Economy GLA, December 15 th 2015 1 12-2 Many forces at work that have a big impact on UK housing often a disproportionate effect on

David Miles Imperial College London House Prices, Credit and the Wider Economy GLA, December 15 th 2015 1 12-2 Many forces at work that have a big impact on UK housing often a disproportionate effect on

Introduction to Mortgage Lending

Many experts think that credit unions have a high potential for greater growth in the mortgage lending area. In this chapter we explain the development of mortgage lending at credit unions, how mortgage

Many experts think that credit unions have a high potential for greater growth in the mortgage lending area. In this chapter we explain the development of mortgage lending at credit unions, how mortgage

Mortgage Loan Prequalification Application

Mortgage Loan Prequalification Application You will need Adobe Acrobat Reader to submit this form. If you do not have Adobe, you can click here to download a free copy. NBG is committed to protecting your

Mortgage Loan Prequalification Application You will need Adobe Acrobat Reader to submit this form. If you do not have Adobe, you can click here to download a free copy. NBG is committed to protecting your

Understanding Your Finances

Understanding Your Finances Getting a handle on your finances can be difficult, especially when you find yourself... Dealing with low credit scores, Living paycheck to paycheck, Not knowing where your

Understanding Your Finances Getting a handle on your finances can be difficult, especially when you find yourself... Dealing with low credit scores, Living paycheck to paycheck, Not knowing where your

What Foreign Banks Need to Know About the Law and Taxes in Myanmar Sebastian Pawlita 9 February 2015

What Foreign Banks Need to Know About the Law and Taxes in Myanmar Sebastian Pawlita 9 February 2015 INTRODUCTION Regulatory framework of the banking sector Sources of law: New Banks and Financial Institution

What Foreign Banks Need to Know About the Law and Taxes in Myanmar Sebastian Pawlita 9 February 2015 INTRODUCTION Regulatory framework of the banking sector Sources of law: New Banks and Financial Institution

Share Loan and Underlying Mortgage Financing. Jeremy Morgan, NCB Larry Mathe, NCB

Share Loan and Underlying Mortgage Financing Jeremy Morgan, NCB Larry Mathe, NCB About NCB NCB is the premier lender to housing cooperatives nationwide. NCB has financed over $6 Billion to housing cooperatives

Share Loan and Underlying Mortgage Financing Jeremy Morgan, NCB Larry Mathe, NCB About NCB NCB is the premier lender to housing cooperatives nationwide. NCB has financed over $6 Billion to housing cooperatives

TAKING THE MYSTERY OUT OF FINANCE

TAKING THE MYSTERY OUT OF FINANCE Presented By: Eva Brown, Director of Access to Capital 312 853 3477 x 560 OBJECTIVES Determine how much money you need to start/expand your business. Determine your ability

TAKING THE MYSTERY OUT OF FINANCE Presented By: Eva Brown, Director of Access to Capital 312 853 3477 x 560 OBJECTIVES Determine how much money you need to start/expand your business. Determine your ability

FIRST TIME HOME BUYER PROGRAM FREQUENTLY ASKED QUESTIONS

FIRST TIME HOME BUYER PROGRAM FREQUENTLY ASKED QUESTIONS QUALIFICATION/ELIGIBILITY QUESTIONS 1. What if I haven t previously bought a home, but my spouse has? If my spouse is not going to be on the mortgage,

FIRST TIME HOME BUYER PROGRAM FREQUENTLY ASKED QUESTIONS QUALIFICATION/ELIGIBILITY QUESTIONS 1. What if I haven t previously bought a home, but my spouse has? If my spouse is not going to be on the mortgage,

new-build homebuy South Staffordshire Housing Association

new-build homebuy South Staffordshire Housing Association What is new build HomeBuy? New build HomeBuy, also widely known as shared ownership, is a government-funded scheme to help first-time buyers buy

new-build homebuy South Staffordshire Housing Association What is new build HomeBuy? New build HomeBuy, also widely known as shared ownership, is a government-funded scheme to help first-time buyers buy

WELCOME COURSE OUTLINE

WELCOME COURSE OUTLINE Dear Home Buyer: Thank you for giving us the opportunity to help guide you through your home lending process. It is typically the largest financial transaction you will make and

WELCOME COURSE OUTLINE Dear Home Buyer: Thank you for giving us the opportunity to help guide you through your home lending process. It is typically the largest financial transaction you will make and

Financing your home to fit the rest of your life. UBS Mortgage

Financing your home to fit the rest of your life UBS Mortgage I didn t realize that UBS even offered home financing. But when I told my Financial Advisor that I was in the market for a vacation home, he

Financing your home to fit the rest of your life UBS Mortgage I didn t realize that UBS even offered home financing. But when I told my Financial Advisor that I was in the market for a vacation home, he

Residential Mortgages

2 December 2014 We have two ranges of residential mortgages: Special Situations for borrowers with specific requirements such as the self-employed with just one years accounts, or contractors and professionals

2 December 2014 We have two ranges of residential mortgages: Special Situations for borrowers with specific requirements such as the self-employed with just one years accounts, or contractors and professionals

Week 2: Personal Guarantor

Week 2: Personal Guarantor Before you begin the credit building process, you need to identify who will personally guarantee the business credit lines. Your choices are as follows: yourself, someone you

Week 2: Personal Guarantor Before you begin the credit building process, you need to identify who will personally guarantee the business credit lines. Your choices are as follows: yourself, someone you

Getting a Difficult Business Loan Is Easy

Getting a Difficult Business Loan Is Easy Learn How Easy IT Is To Get a Business Loan Even IF You Have Bad Credit And Have Been Turned Down Before Every Winner Has A Coach! John P Fazzio, Your Coach www.winning-advantage.com

Getting a Difficult Business Loan Is Easy Learn How Easy IT Is To Get a Business Loan Even IF You Have Bad Credit And Have Been Turned Down Before Every Winner Has A Coach! John P Fazzio, Your Coach www.winning-advantage.com

CAN MEAN A LOWER COST

REALTOR Presentation FOR MOST HOME BUYERS, A CONVENTIONAL LOAN CAN MEAN A LOWER COST Right for You, Right for the Buyer Carolyn Delaney Senior Account Executive Cell: 571-212-1411 carolyn.delaney@ugcorp.com

REALTOR Presentation FOR MOST HOME BUYERS, A CONVENTIONAL LOAN CAN MEAN A LOWER COST Right for You, Right for the Buyer Carolyn Delaney Senior Account Executive Cell: 571-212-1411 carolyn.delaney@ugcorp.com

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing I. Purpose of asset financing Fixed asset financing refers to the financing for real estate and equipment needs of a business.

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing I. Purpose of asset financing Fixed asset financing refers to the financing for real estate and equipment needs of a business.

Flexible and convenient equipment finance for your business. Expect nothing less.

Equipment Finance equipment finance Flexible and convenient equipment finance for your business. Expect nothing less. Delphi Bank s flexible and convenient equipment finance solutions are a competitively

Equipment Finance equipment finance Flexible and convenient equipment finance for your business. Expect nothing less. Delphi Bank s flexible and convenient equipment finance solutions are a competitively

Fact find template BUSINESS PROTECTION. Contact details. Protection Business Menu

BUSINESS PROTECTION Fact find template This fact find template will help you to understand more about your client s business and provide an opportunity for you to ask them where the money would come from

BUSINESS PROTECTION Fact find template This fact find template will help you to understand more about your client s business and provide an opportunity for you to ask them where the money would come from

Acquiring land April 2001

Acquiring land April 2001 Contents 1. What is this guidance about? 2 2. In this guidance 2 3. Trustees powers and duties 3 4. What are the general duties of trustees when acquiring land for their charity?

Acquiring land April 2001 Contents 1. What is this guidance about? 2 2. In this guidance 2 3. Trustees powers and duties 3 4. What are the general duties of trustees when acquiring land for their charity?

Peer-to-peer bad debt relief: proposed technical criteria. Technical Note 24 March 2015

Peer-to-peer bad debt relief: proposed technical criteria Technical Note 24 March 2015 1 Contents Page Chapter 1 Introduction 3 Chapter 2 Summary of Proposed Relief 4 Chapter 3 Amount of Proposed Relief

Peer-to-peer bad debt relief: proposed technical criteria Technical Note 24 March 2015 1 Contents Page Chapter 1 Introduction 3 Chapter 2 Summary of Proposed Relief 4 Chapter 3 Amount of Proposed Relief

The Mortgage Guide. Helping you find the right mortgage for you. Brought to you by. V0050713a

The Mortgage Guide Helping you find the right mortgage for you Brought to you by Hello. Contents We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us ever

The Mortgage Guide Helping you find the right mortgage for you Brought to you by Hello. Contents We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us ever

WELCOME. To the Wonderful World Of Reverse Mortgages

WELCOME To the Wonderful World Of Reverse Mortgages Reverse Mortgage Loans Borrowing Against Your Home Basic Questions: 1. Do you really need a reverse mortgage? -- Why are you interested in these loans?

WELCOME To the Wonderful World Of Reverse Mortgages Reverse Mortgage Loans Borrowing Against Your Home Basic Questions: 1. Do you really need a reverse mortgage? -- Why are you interested in these loans?

PERSONAL LOANS 101: UNDERSTANDING PAYMENT PROTECTION INSURANCE

PERSONAL LOANS 101: UNDERSTANDING PAYMENT PROTECTION INSURANCE Payment protection insurance can be a valuable tool in helping protect your credit and your loved ones from unexpected life events. If something

PERSONAL LOANS 101: UNDERSTANDING PAYMENT PROTECTION INSURANCE Payment protection insurance can be a valuable tool in helping protect your credit and your loved ones from unexpected life events. If something

Personal Loans 101: Understanding

Personal Loans 101: Understanding PAYMENT PROTECTION INSURANCE Payment protection insurance can be a valuable tool in helping protect your credit and your loved ones from unexpected life events. If something

Personal Loans 101: Understanding PAYMENT PROTECTION INSURANCE Payment protection insurance can be a valuable tool in helping protect your credit and your loved ones from unexpected life events. If something

www.citizenshipteacher.co.uk 2011 16228 1

The stock market www.citizenshipteacher.co.uk 2011 16228 1 Lesson objectives I will understand what a stock market is. I will identify what caused the downturn in the American Stock Market. www.citizenshipteacher.co.uk

The stock market www.citizenshipteacher.co.uk 2011 16228 1 Lesson objectives I will understand what a stock market is. I will identify what caused the downturn in the American Stock Market. www.citizenshipteacher.co.uk