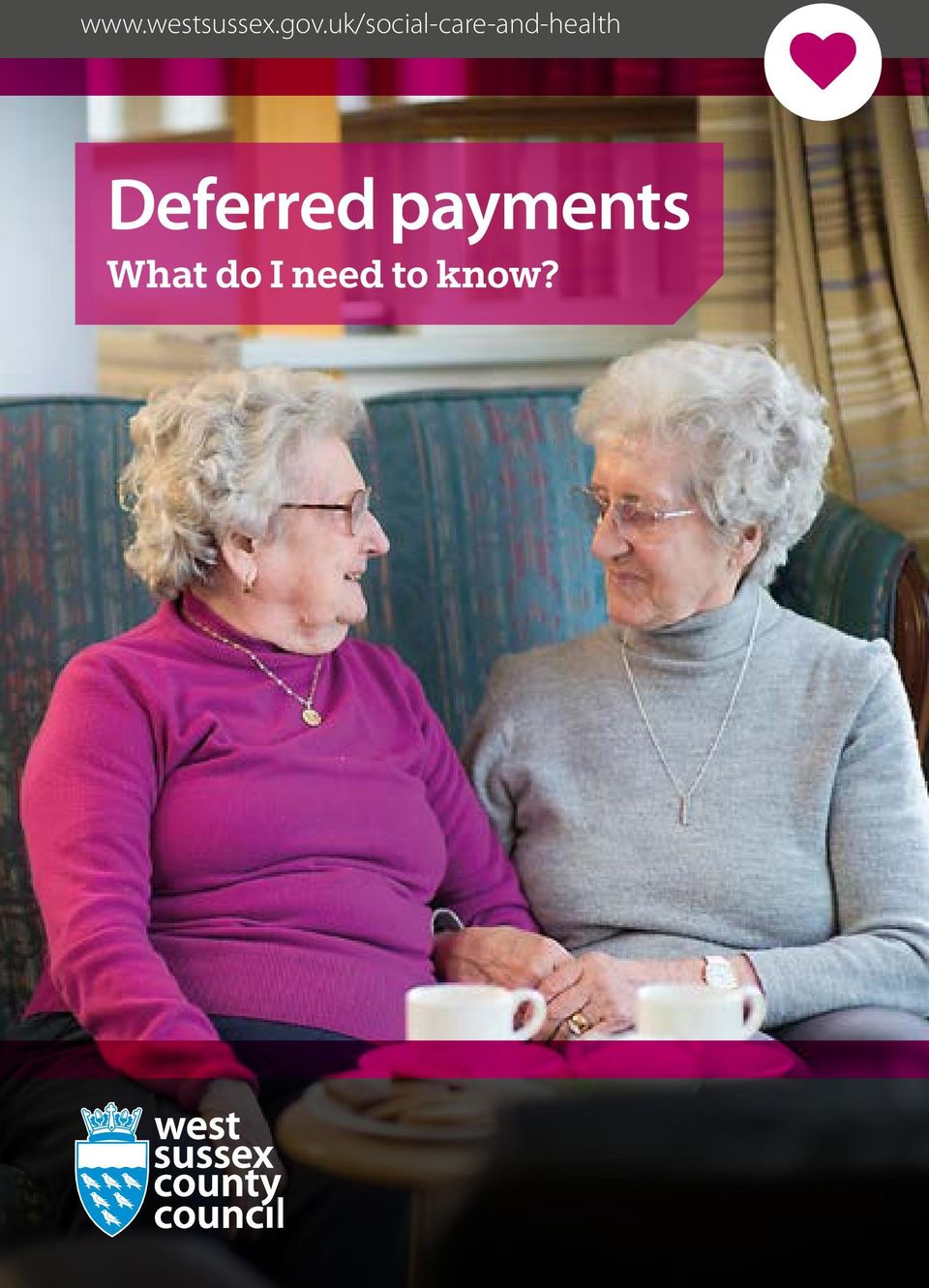

Deferred payments What do I need to know?

|

|

|

- Oswin Watts

- 8 years ago

- Views:

Transcription

1 Deferred payments What do I need to know?

2 What is a deferred payment agreement? A deferred payment agreement is an arrangement with us, West Sussex County Council, that allows you to use the value of your home to help pay the cost of your residential care. If you are paying for your own care, but can t afford to pay the full weekly cost because most of your money is tied up in your home, a deferred payment agreement means you don t have to sell your home immediately to release the money to pay for your care. Considering your options Deferred payment agreements will suit some people s circumstances better than others. A deferred payment agreement is only one way to pay for your care. We strongly recommend that you get independent financial advice if you are thinking about having a deferred payment. This will make sure that you understand all the options that are available to you and you will be clear about whether a deferred payment is right for you and your family. Please see the information about getting independent financial advice on page 10 of this leaflet. Other formats If you would like more copies of this leaflet or need this information in another format, for example, large print, easy read, on audio CD or in a different language, please call Adults CarePoint on or socialcare@westsussex.gov.uk. You can also use Typetalk on

3 How does a deferred payment agreement work? A deferred payment is a loan from us that uses your home as a guarantee that we will get the money back. You will still pay the weekly contribution towards your care that you have been assessed as being able to pay from your income and other savings, but we will pay the part of your weekly costs that you can t afford. We will pay your care costs up to a maximum total amount. The maximum amount will usually be 80-90% of the value of your share in your property, but this may vary. If the total amount deferred reaches the maximum amount and you are unable to pay your own costs, you may become eligible for funding from us. We will only pay up to the amount we have agreed to meet your assessed needs. If you, or someone on your behalf, have been paying an extra amount towards the cost of more expensive care than we have assessed that you need, the payments would need to continue or you may have to move to a different residential care setting. You will still need to pay a weekly contribution to the cost of your care. The deferred payment is usually paid back by selling your house and using the money to repay the loan. You can choose to sell your home and repay the loan at any time, or you can keep your home during your lifetime and the deferred payment will be repaid out of your estate after your death. You can also pay the debt back in another way if you prefer. If you rent out your home while you have a deferred payment agreement in place, we will expect you to use the rental income towards the cost of your care to reduce the amount of the deferred payment. 3

4 Who can have a deferred payment agreement? To be able to enter into a deferred payment agreement, you must: l be assessed by a social care worker as needing residential care; l be currently living or going to live permanently in a registered residential care or nursing home; l own or partly own your home; l have savings and investments of less than 23,250 (not including the value of your home); and l have the mental capacity to enter into a deferred payment agreement or have a legally-appointed person who is willing to do this for you. We will need to take account of any other interests in the property when deciding how much you can borrow. For example, another person may have a legal share in your home or some of the value may be tied up in a mortgage or an equity-release scheme. You will not be able to enter into a deferred payment agreement if your home is not counted in the financial assessment of how much you can pay towards the cost of your care. The value of your home will not normally be included in the financial assessment if: l you have lived in a care home for less than 12 weeks; l you are only staying in a care home temporarily; l your partner, a child under 18 or a relative (as defined in the Care and Support (Charging and Assessment of Resources) Regulations 2014) who is over 60 or disabled still lives in your home; or l you are receiving care in your own home rather than living in a residential care home. 4

5 What will I need to do to enter into a deferred payment agreement? You will need to do the following. l Make sure your home is registered with the Land Registry. If it isn t, you must arrange and pay for it to be registered. l Have a responsible person who is able to make sure that any necessary maintenance is carried out on your home (you will continue to pay for maintenance). l Continue to insure your home at your own expense and give us evidence that there is appropriate insurance in place. l Pay your own contributions to your care costs on time. If your home cannot be insured for any reason, you will not be able to enter into a deferred payment agreement. Charges for deferred payment agreements We will charge fees to arrange and manage a deferred payment agreement. The fees are simply to cover our costs and not to make a profit. They will meet the costs of legal fees, property valuation, Land Registry fees and administrative costs. There is a one-off administration charge of 495 and a property valuation charge of 250. There will also be an ongoing weekly charge of We will write to you separately about these charges if you decide to enter into a deferred payment agreement. 5

6 Interest on deferred payments We will charge interest on deferred payments in the same way as a bank would charge it on a loan. We will charge interest in line with the national rate that local authorities can charge. The national interest rate changes every six months. The interest rate charged from April 2015 until 30 June 2015 will be 2.65%. The rate will then change for all customers to 2.25% from 1 July 2015 until 31 December Interest will apply from the day you enter into the deferred payment agreement. It will be compound interest. This means that we will calculate the interest and add it to the loan every day. You will receive statements every six months. These will tell you how we are calculating your interest and the outstanding amount on your deferred payment account. Entering into the deferred payment agreement with us If you decide to enter into a deferred payment agreement, you will sign a legal contract or agreement with us. The legal agreement covers both your responsibilities and ours. To be accepted for a deferred payment agreement, you must meet the requirements for the scheme and we must be able to gain adequate security for the loan. We would usually do this by placing a legal charge or mortgage on your home. To find out more about taking out a deferred payment agreement, speak to your social care worker. If you don t have a social care worker, you can contact our Adults CarePoint. See the back of this leaflet for their contact details. 6

7 Ending a deferred payment agreement You, or someone acting on your behalf, can pay off the loan and end the agreement at any time. For example, you may decide to sell your home and pay off the loan. There are circumstances in which we may stop deferring costs for your care. For example: l if your savings and investments fall below a minimum limit of 14,250 and you become eligible for local authority support; l if you no longer need to be in a care home; l if you do not keep to the requirements of the deferred payment agreement; or l if your home is no longer included in the assessment of your finances for any reason and you then become eligible for funding from us, for example: in certain exceptional circumstances, if a husband, wife or relative (as defined in the Care and Support (Charging and Assessment of Resources) Regulations 2014) has moved into the property after the deferred payment agreement started; or if a relative who was living in in the property at the time the deferred payment agreement started becomes a dependent relative. You will still have to pay the interest that builds up on the amount of money we have already paid for your care (the deferred payments). We would give you at least 30 days notice that further deferred payments will stop. Your social care worker or another member of staff will explain these circumstances to you in more detail. 7

8 If you do not end the agreement, it will finish when you die and the loan will need to be paid from your estate within 90 days. Interest will continue to build up on the deferred payment following your death until the loan is paid in full. Advantages of deferred payment agreements l You won t have to sell your home during your lifetime to pay for care if you don t want to. l If you receive funding from us towards the cost of your care, you could pay an extra amount towards the cost of more expensive care than we have assessed that you need. We would need to be satisfied that you would be able to continue paying this extra amount of money. If you failed to keep up with the payments, this may mean you would have to move to other accommodation. l If someone already pays extra money towards your care, you may be able to add the cost of these payments to your deferred payment agreement, if there is enough equity or financial value in your home. This means that the person would no longer need to pay the extra money towards your care. 8

9 Other options You do not have to take out a deferred payment agreement. There may be other ways for you to pay for your care without selling your home. l You might choose to rent out your home, which could give you enough income to cover the cost of your care. The advantages of this option are that you would not build up debt and your property would be occupied, with your tenant paying the bills and council tax. l There are equity-release schemes available which you can use to release money from the value of your home. l You can buy immediate care plans or annuities (insurance plans) to pay for your care. l You could choose to pay the cost of your care from your available income, savings and assets, or a family member could pay some or all of this for you. We strongly recommend that you get independent financial advice before you decide whether a deferred payment agreement is right for you. We can provide you with information about the Carewise care funding scheme which provides specialist independent financial advice. You can of course, get advice from other financial advisers if you prefer. 9

to pay for your care.")

10 Carewise care funding advice If you are considering a deferred payment agreement or would like to find out more about the different ways to pay for care, the Carewise care funding advice scheme can help. Carewise was set up by us, Age UK West Sussex, West Sussex Partners in Care and the Society of Later Life Advisers to offer information and advice on the different care options that are available and the best ways to pay for care. The scheme includes a panel of Carewise-approved independent financial advisers who specialise in providing financial advice about paying for long-term care. To find out more, call Adults CarePoint on or go to Other information about residential care You can find more information about choosing residential care in our leaflet Choosing and paying for care in a residential or nursing home. Go to Adults social care publications on or phone Adults CarePoint and ask for a copy. See the back of this leaflet for their contact details. The information in this leaflet is just a guide. It does not replace independent legal and financial advice or the law. You can get specific information based on your own circumstances from a social care worker. Please contact Adults CarePoint for more information. See the back of this leaflet for contact details. 10

11 Notes 11

12 Adults CarePoint social-care-and-health Second Floor The Grange County Hall Chichester West Sussex PO19 1RG WS

The Deferred Payments Scheme. An information leaflet for home owners, paying for residential or nursing home care

The Deferred Payments Scheme An information leaflet for home owners, paying for residential or nursing home care What is the Deferred Payment Scheme? The deferred payment scheme is designed to help if

The Deferred Payments Scheme An information leaflet for home owners, paying for residential or nursing home care What is the Deferred Payment Scheme? The deferred payment scheme is designed to help if

People moving into a care home who have a property Information sheet D4 April 2016

People moving into a care home who have a property Information sheet D4 April 2016 This information sheet explains your rights as a homeowner if you are moving into a care home with financial support from

People moving into a care home who have a property Information sheet D4 April 2016 This information sheet explains your rights as a homeowner if you are moving into a care home with financial support from

Blackburn with Darwen Borough Council Deferred Payments Scheme

Blackburn with Darwen Borough Council Deferred Payments Scheme A guide to Deferred Payments paying for residential care or nursing care if you own your own home. 1 What is the Deferred Payments Scheme?

Blackburn with Darwen Borough Council Deferred Payments Scheme A guide to Deferred Payments paying for residential care or nursing care if you own your own home. 1 What is the Deferred Payments Scheme?

Deferred Payment Scheme. This leaflet gives a guide to Derbyshire County Council s Deferred Payment Scheme

Deferred Payment Scheme This leaflet gives a guide to Derbyshire County Council s Deferred Payment Scheme Contents What is the Deferred Payment Scheme? Page 3 To apply for a Deferred Payment you must...

Deferred Payment Scheme This leaflet gives a guide to Derbyshire County Council s Deferred Payment Scheme Contents What is the Deferred Payment Scheme? Page 3 To apply for a Deferred Payment you must...

Paying for your Care in a Home The Council s Deferred Payment Scheme. Introduction

Paying for your Care in a Home The Council s Deferred Payment Scheme Introduction Our leaflet A Guide to entering a care home explains how you can ask the Council to help you with the cost of your care

Paying for your Care in a Home The Council s Deferred Payment Scheme Introduction Our leaflet A Guide to entering a care home explains how you can ask the Council to help you with the cost of your care

Deferred Payment Agreements

Deferred Payment Agreements Paying for your Care in a Home Barnet Council s Deferred Payment Scheme What is a Deferred Payment Agreement? A Deferred Payment Agreement is an arrangement with the Council

Deferred Payment Agreements Paying for your Care in a Home Barnet Council s Deferred Payment Scheme What is a Deferred Payment Agreement? A Deferred Payment Agreement is an arrangement with the Council

Information on the Council s Deferred Payments Scheme

Information on the Council s Deferred Payments Scheme What is the Deferred Payments Scheme? The Deferred Payments Scheme is designed to help you if you have been assessed as having to pay the full cost

Information on the Council s Deferred Payments Scheme What is the Deferred Payments Scheme? The Deferred Payments Scheme is designed to help you if you have been assessed as having to pay the full cost

What is the Deferred Payments Scheme? Help with paying for your care

What is the Deferred Payments Scheme? Help with paying for your care The Deferred Payment Scheme can help you pay for your care home fees, if you own your home and cannot afford to pay the full fee, as

What is the Deferred Payments Scheme? Help with paying for your care The Deferred Payment Scheme can help you pay for your care home fees, if you own your home and cannot afford to pay the full fee, as

Information for people in residential care with property

Information for people in residential care with property If you are assessed as eligible for permanent residential care and you have a property and your other capital is valued at less than 23,250 the

Information for people in residential care with property If you are assessed as eligible for permanent residential care and you have a property and your other capital is valued at less than 23,250 the

Deferred Payment Scheme Information Leaflet

Deferred Payment Scheme Information Leaflet What is the Deferred Payments Scheme? The Deferred Payments Scheme is designed to help you if you have been assessed as having to pay the full cost of your residential

Deferred Payment Scheme Information Leaflet What is the Deferred Payments Scheme? The Deferred Payments Scheme is designed to help you if you have been assessed as having to pay the full cost of your residential

Information on: Deferred Payment Scheme

Information on: Deferred Payment Scheme From 1 April 2015 Introduction From April 2015 the way care and support is provided is changing for the better. The Care Act 2014 is a recent piece of legislation

Information on: Deferred Payment Scheme From 1 April 2015 Introduction From April 2015 the way care and support is provided is changing for the better. The Care Act 2014 is a recent piece of legislation

Deferred Payments. Information for people moving into residential care who own a property

Deferred Payments Information for people moving into residential care who own a property Deferred Payments The Deferred Payment Scheme is designed to help you if you have been assessed as having to pay

Deferred Payments Information for people moving into residential care who own a property Deferred Payments The Deferred Payment Scheme is designed to help you if you have been assessed as having to pay

FIAS factsheet 4 October 2015

Deferred payment agreements in Suffolk Please note we strongly recommend that you take independent financial advice if you are considering using the deferred payment scheme from Suffolk County Council.

Deferred payment agreements in Suffolk Please note we strongly recommend that you take independent financial advice if you are considering using the deferred payment scheme from Suffolk County Council.

Deferred Payment Scheme Information and guidance 2015/16

Deferred Payment Scheme Information and guidance 2015/16 What is the Deferred Payment Scheme? The Deferred Payment Scheme is designed to prevent people from having to sell their home, in their lifetime,

Deferred Payment Scheme Information and guidance 2015/16 What is the Deferred Payment Scheme? The Deferred Payment Scheme is designed to prevent people from having to sell their home, in their lifetime,

Deferred Payment Agreement Charging

Deferred Payment Agreement Charging What is a Deferred Payment Agreement? A Deferred Payment Agreement is an arrangement with the council that will enable you to use the value of your home to help pay

Deferred Payment Agreement Charging What is a Deferred Payment Agreement? A Deferred Payment Agreement is an arrangement with the council that will enable you to use the value of your home to help pay

A guide to Deferred Payments

A guide to Deferred Payments Paying for residential care or nursing care if you own your home What is the deferred payment scheme? If you are a home owner moving to residential or nursing care, this scheme

A guide to Deferred Payments Paying for residential care or nursing care if you own your home What is the deferred payment scheme? If you are a home owner moving to residential or nursing care, this scheme

Deferred payment agreements April 2015

Deferred payment agreements April 2015 This leaflet explains how a deferred payment agreement may help you when you move to a care home What is a deferred payment? A deferred payment is when the council

Deferred payment agreements April 2015 This leaflet explains how a deferred payment agreement may help you when you move to a care home What is a deferred payment? A deferred payment is when the council

Deferred Payment Agreement Scheme

Adult Social Care and Health Deferred Payment Agreement Scheme Information about the Council s Deferred Payment Agreement Scheme an option to help you manage care home costs if you own your property www.reading.gov.uk/carecharges

Adult Social Care and Health Deferred Payment Agreement Scheme Information about the Council s Deferred Payment Agreement Scheme an option to help you manage care home costs if you own your property www.reading.gov.uk/carecharges

Guide to Charges for Residential Accommodation for People with Property

Guide to Charges for Residential Accommodation for People with Property Adult Services Big plans for the care we provide What is the Deferred Payment Scheme? If you need to have permanent residential/nursing

Guide to Charges for Residential Accommodation for People with Property Adult Services Big plans for the care we provide What is the Deferred Payment Scheme? If you need to have permanent residential/nursing

Deferred Payments. A guide to. Paying for residential care if you own your home

Deferred Payments A guide to Paying for residential care if you own your home What is the deferred payment scheme? If you are a home owner moving to residential care this scheme is designed to assist you

Deferred Payments A guide to Paying for residential care if you own your home What is the deferred payment scheme? If you are a home owner moving to residential care this scheme is designed to assist you

Deferred Payment Agreement Factsheet

Deferred Payment Agreement Factsheet What is a Deferred Payment Agreement? Deferred Payment Agreements are designed to help you if you have been assessed as having to pay the full cost of your residential

Deferred Payment Agreement Factsheet What is a Deferred Payment Agreement? Deferred Payment Agreements are designed to help you if you have been assessed as having to pay the full cost of your residential

Deferred Payments. People & Communities. What is a Deferred Payment? Your agreement with us

Deferred Payments People & Communities What is a Deferred Payment? A Deferred Payment is designed to help you, if you have to pay the full cost of your residential care, but cannot afford to pay the full

Deferred Payments People & Communities What is a Deferred Payment? A Deferred Payment is designed to help you, if you have to pay the full cost of your residential care, but cannot afford to pay the full

factsheet Deferred payments adult care and support Introduction Sheffield City Council Adult Care and Support Service

Sheffield City Council Adult Care and Support Service Deferred payments adult care and support factsheet Deferred payments allow people who own their own home to use the value of their property to defer

Sheffield City Council Adult Care and Support Service Deferred payments adult care and support factsheet Deferred payments allow people who own their own home to use the value of their property to defer

Deferred payment information

Deferred payment information London Borough of Care Act April 2014 April 2015 1 The London Borough of Deferred Payments Scheme From April 2015 Charges for Residential Accommodation and other specific settings

Deferred payment information London Borough of Care Act April 2014 April 2015 1 The London Borough of Deferred Payments Scheme From April 2015 Charges for Residential Accommodation and other specific settings

Deferred payments for people in permanent residential care

Money and legal matters Deferred payments for people in permanent residential care Deferred payment agreements scheme - Information for residents 2 Deferred payment agreements scheme Contents Introduction

Money and legal matters Deferred payments for people in permanent residential care Deferred payment agreements scheme - Information for residents 2 Deferred payment agreements scheme Contents Introduction

Deferred Payments Scheme Guidance Notes for residents, relatives and carers

Royal Borough of Windsor and Maidenhead Deferred Payments Scheme Guidance Notes for residents, relatives and carers What you need to know June 2015 Windsor, Ascot and Maidenhead What is the Deferred Payments

Royal Borough of Windsor and Maidenhead Deferred Payments Scheme Guidance Notes for residents, relatives and carers What you need to know June 2015 Windsor, Ascot and Maidenhead What is the Deferred Payments

Paying for your own residential care

Paying for your own residential care June 2015 Page 1 Contents How will I know whether my needs have to be met by residential care?... 3 How do I find a home?... 3 How much will I have to pay towards the

Paying for your own residential care June 2015 Page 1 Contents How will I know whether my needs have to be met by residential care?... 3 How do I find a home?... 3 How much will I have to pay towards the

Deferred Payment Scheme: Frequently Asked Questions

Deferred Payment Scheme: Frequently Asked Questions What is a deferred payment scheme? The Deferred Payments Scheme is designed to help you if you have been assessed as having to pay the full cost of your

Deferred Payment Scheme: Frequently Asked Questions What is a deferred payment scheme? The Deferred Payments Scheme is designed to help you if you have been assessed as having to pay the full cost of your

West Sussex Care Funding Advice

West Sussex Care Funding Advice Information and advice to help you make the right choices and ease the worry of paying for care. 1 The Carewise partnership Carewise is a pathway to information and advice

West Sussex Care Funding Advice Information and advice to help you make the right choices and ease the worry of paying for care. 1 The Carewise partnership Carewise is a pathway to information and advice

What is the Deferred Payments Scheme?

What is the Deferred Payments Scheme? The Deferred Payments Scheme is designed to help you if you have been assessed as having to pay the full cost of your residential care but cannot afford to pay the

What is the Deferred Payments Scheme? The Deferred Payments Scheme is designed to help you if you have been assessed as having to pay the full cost of your residential care but cannot afford to pay the

Paying for residential and nursing home care if you own property

M ay 20 15 Paying for residential and nursing home care if you own property If you need help understanding this leaflet, an interpreting service is available. Please phone Stockport Interpreting Unit on

M ay 20 15 Paying for residential and nursing home care if you own property If you need help understanding this leaflet, an interpreting service is available. Please phone Stockport Interpreting Unit on

MOVING INTO A CARE HOME Frequently asked questions

MOVING INTO A CARE HOME Frequently asked questions What types of income and savings are counted as part of a financial assessment? Employment Support Allowance / Incapacity Benefit Pension Credit Former

MOVING INTO A CARE HOME Frequently asked questions What types of income and savings are counted as part of a financial assessment? Employment Support Allowance / Incapacity Benefit Pension Credit Former

Version 0.1 Adult Social Care Deferred Payment Policy Issued: April 2015

Adult Social Care Deferred Payment Policy 1 Introduction 1.1 This Policy details how Deferred Payment Agreements (DPAs) are to be operated by Rochdale Council from April 2015. 1.2 When a person enters

Adult Social Care Deferred Payment Policy 1 Introduction 1.1 This Policy details how Deferred Payment Agreements (DPAs) are to be operated by Rochdale Council from April 2015. 1.2 When a person enters

Deferred Payment Agreement (DPA) Fact Sheet

Fact Sheet") Deferred Payment Agreement (DPA) Fact Sheet From April 2015, all councils in England are required to provide a Deferred Payment scheme for local residents. This will apply to anyone who owns a property

Deferred Payment Agreement (DPA) Fact Sheet From April 2015, all councils in England are required to provide a Deferred Payment scheme for local residents. This will apply to anyone who owns a property

Newcastle City Council. Deferred Payment Scheme. Effective from 1 April 2015

Newcastle City Council Deferred Payment Scheme Effective from 1 April 2015 1 1. Introduction and Legal Status 1.1 The Care Act 2014 (section 34-36) establishes a universal deferred payment scheme, which

Newcastle City Council Deferred Payment Scheme Effective from 1 April 2015 1 1. Introduction and Legal Status 1.1 The Care Act 2014 (section 34-36) establishes a universal deferred payment scheme, which

DEFERRED PAYMENT AGREEMENT. Information Pack for our service users and their families or representatives

12 WEEK PROPERTY DISREGARD PERIOD AND THE DEFERRED PAYMENT AGREEMENT Information Pack for our service users and their families or representatives What is the 12 week Property Disregard Period? The Council

12 WEEK PROPERTY DISREGARD PERIOD AND THE DEFERRED PAYMENT AGREEMENT Information Pack for our service users and their families or representatives What is the 12 week Property Disregard Period? The Council

Government mortgage rescue scheme What will it mean for me and my family?

Government mortgage rescue scheme What will it mean for me and my family? What is mortgage rescue? Mortgage rescue is help that the Government is offering if: you are struggling to keep up with your mortgage

Government mortgage rescue scheme What will it mean for me and my family? What is mortgage rescue? Mortgage rescue is help that the Government is offering if: you are struggling to keep up with your mortgage

Paying for Adult Social Care services in Leeds

Paying for Adult Social Care services in Leeds Financial information from April 2015 Introduction From April 2015 the way that care and support is provided is changing for the better. The Care Act 2014

Paying for Adult Social Care services in Leeds Financial information from April 2015 Introduction From April 2015 the way that care and support is provided is changing for the better. The Care Act 2014

Paying for a care home Will I have to sell my home?

Paying for a care home Will I have to sell my home? www.brent.gov.uk Information for those considering residential or nursing care Revised April 2010 Who is this booklet for? This booklet is to help adults

Paying for a care home Will I have to sell my home? www.brent.gov.uk Information for those considering residential or nursing care Revised April 2010 Who is this booklet for? This booklet is to help adults

Deferred Payment Scheme

Deferred Payment Scheme Deferred Payments Scheme for people going into permanent residential / nursing care Introduction This leaflet is for people who are about to move into permanent residential accommodation

Deferred Payment Scheme Deferred Payments Scheme for people going into permanent residential / nursing care Introduction This leaflet is for people who are about to move into permanent residential accommodation

POLICY FOR THE BREATHING SPACE SCHEME

POLICY FOR THE BREATHING SPACE SCHEME PREFACE The Council is participating in a regional scheme called Breathing Space. The scheme facilitates the provision of loans in accordance with powers given under

POLICY FOR THE BREATHING SPACE SCHEME PREFACE The Council is participating in a regional scheme called Breathing Space. The scheme facilitates the provision of loans in accordance with powers given under

Wiltshire Council PAYING FOR RESIDENTIAL OR NURSING CARE WHERE PEOPLE OWN THEIR PROPERTY INTERIM ADVICE PENDING NEW POLICY

Wiltshire Council PAYING FOR RESIDENTIAL OR NURSING CARE WHERE PEOPLE OWN THEIR PROPERTY INTERIM ADVICE PENDING NEW POLICY 2015 2016 Please note, this is interim guidance pending changes to the Councils

Wiltshire Council PAYING FOR RESIDENTIAL OR NURSING CARE WHERE PEOPLE OWN THEIR PROPERTY INTERIM ADVICE PENDING NEW POLICY 2015 2016 Please note, this is interim guidance pending changes to the Councils

Understanding mortgages

This information is an extract from the booklet Housing costs, which is part of our Financial guidance series. You may find the full booklet helpful. We can send you a free copy see page 7. Contents What

This information is an extract from the booklet Housing costs, which is part of our Financial guidance series. You may find the full booklet helpful. We can send you a free copy see page 7. Contents What

Your Guide to Equity Release

Equity release has provided me with financial stability. I now have the opportunity to help my family, go on holiday, and make some home improvements. Mr W, East Sussex Your Guide to Equity Release Contents

Equity release has provided me with financial stability. I now have the opportunity to help my family, go on holiday, and make some home improvements. Mr W, East Sussex Your Guide to Equity Release Contents

WHAT IS EQUITY RELEASE? WHY CONSIDER EQUITY RELEASE?

WHAT IS EQUITY RELEASE? Equity Release can free some of the capital tied up in your home, while you continue to live there. This money can be in the form of a tax-free lump sum, a regular income or a combination

WHAT IS EQUITY RELEASE? Equity Release can free some of the capital tied up in your home, while you continue to live there. This money can be in the form of a tax-free lump sum, a regular income or a combination

Care Home Fees: Paying them in Scotland

Guide Guide 52 Care Home Fees: Paying them in Scotland Living in a care home can be expensive. Some people are able to pay their own care home fees, but others may need financial support from their local

Guide Guide 52 Care Home Fees: Paying them in Scotland Living in a care home can be expensive. Some people are able to pay their own care home fees, but others may need financial support from their local

Dealing with your mortgage shortfall

Dealing with your mortgage shortfall The options available Things to consider Helping you stay on track The Money Advice Service is independent and set up by government to help people make the most of

Dealing with your mortgage shortfall The options available Things to consider Helping you stay on track The Money Advice Service is independent and set up by government to help people make the most of

Chadwick s. Equity Release

c Independent Chadwick s Financial Advisers Equity Release Contents Chadwick s IFA Page 4 Equity Release Page 5 Lifetime Mortgages Page 6 Home Reversion Schemes Page 7 Considerations Pages 8&9 Safe Guards

c Independent Chadwick s Financial Advisers Equity Release Contents Chadwick s IFA Page 4 Equity Release Page 5 Lifetime Mortgages Page 6 Home Reversion Schemes Page 7 Considerations Pages 8&9 Safe Guards

Deferred Payment Scheme Application Form

Deferred Payment Scheme Application Form How to complete this application form You will need to fully complete the form starting on page three of this booklet. Please ensure you have read the leaflet Information

Deferred Payment Scheme Application Form How to complete this application form You will need to fully complete the form starting on page three of this booklet. Please ensure you have read the leaflet Information

Retirement Mortgage Product summary

Retirement Mortgage Product summary The Retirement Mortgage from Hodge Lifetime provides you with a flexible way to borrow money in retirement. A legal charge is secured on your home. AIMS The Retirement

Retirement Mortgage Product summary The Retirement Mortgage from Hodge Lifetime provides you with a flexible way to borrow money in retirement. A legal charge is secured on your home. AIMS The Retirement

Your Guide to Equity Release

Equity release has enabled me to go on more holidays, purchase a new car and make some major household purchases. The service provided met our financial needs in an efficient and helpful way. John, Sutton

Equity release has enabled me to go on more holidays, purchase a new car and make some major household purchases. The service provided met our financial needs in an efficient and helpful way. John, Sutton

Proposed Information Statement Reverse Mortgage. Things you should know about your reverse mortgage

Page 1 of 7 Proposed Information Statement Reverse Mortgage Things you should know about your reverse mortgage This statement is provided to you because reverse mortgages operate differently to other credit

Page 1 of 7 Proposed Information Statement Reverse Mortgage Things you should know about your reverse mortgage This statement is provided to you because reverse mortgages operate differently to other credit

RELEASING CASH FROM YOUR HOME

RELEASING CASH FROM YOUR HOME As a recommended adviser for the Society of Later Life Advisers (SOLLA) we are frequently asked to advise on home income/equity release plans. These notes are designed to

RELEASING CASH FROM YOUR HOME As a recommended adviser for the Society of Later Life Advisers (SOLLA) we are frequently asked to advise on home income/equity release plans. These notes are designed to

Welcome to. OneFamily

OneFamily Lifetime Mortgages 1 Welcome to OneFamily Welcome to our OneFamily Lifetime Mortgages. This brochure acts as an easyto-digest introduction to lifetime mortgages and provides you with a summary

OneFamily Lifetime Mortgages 1 Welcome to OneFamily Welcome to our OneFamily Lifetime Mortgages. This brochure acts as an easyto-digest introduction to lifetime mortgages and provides you with a summary

Financial Information Guide: Residential / Nursing

Financial Information Guide: Residential / Nursing Financial Information Guide for people going into a care home, or care home with nursing on a permanent basis 2015/2016 This booklet explains: 1. About

Financial Information Guide: Residential / Nursing Financial Information Guide for people going into a care home, or care home with nursing on a permanent basis 2015/2016 This booklet explains: 1. About

Roll-up Lifetime Mortgage Lump Sum Plus Lifetime Mortgage

Lifetime Mortgages Roll-up Lifetime Mortgage Lump Sum Plus Lifetime Mortgage Using the value in your home for a better retirement Just Retirement s Lifetime Mortgages Who are we? Just Retirement Limited

Lifetime Mortgages Roll-up Lifetime Mortgage Lump Sum Plus Lifetime Mortgage Using the value in your home for a better retirement Just Retirement s Lifetime Mortgages Who are we? Just Retirement Limited

www.haringey.gov.uk Loans for Leaseholders

www.haringey.gov.uk Loans for Leaseholders What is the Houseproud scheme? Houseproud aims to help homeowners to continue to live safely and independently in their own homes. It is a national scheme supported

www.haringey.gov.uk Loans for Leaseholders What is the Houseproud scheme? Houseproud aims to help homeowners to continue to live safely and independently in their own homes. It is a national scheme supported

are you in danger of losing your home?

are you in danger of losing your home? Mortgage to Rent Scheme help is at hand... We want to make it as easy as possible for you to get information about Mortgage to Rent. You can ask for this document

are you in danger of losing your home? Mortgage to Rent Scheme help is at hand... We want to make it as easy as possible for you to get information about Mortgage to Rent. You can ask for this document

Mortgage advice you can depend on

Our Mortgage advice you can depend on Whether buying your first home, buying to let, or remortgaging, this guide tackles the main considerations. If you want to learn more and receive advice tailored to

Our Mortgage advice you can depend on Whether buying your first home, buying to let, or remortgaging, this guide tackles the main considerations. If you want to learn more and receive advice tailored to

largeequityrelease.com EQUITY RELEASE GUIDE Speak to one of our specialists today on 020 3824 0904

largeequityrelease.com EQUITY RELEASE GUIDE Speak to one of our specialists today on 020 3824 0904 CONTENTS What is equity release?... 3 How much money could I raise through an equity release?... 4 What

largeequityrelease.com EQUITY RELEASE GUIDE Speak to one of our specialists today on 020 3824 0904 CONTENTS What is equity release?... 3 How much money could I raise through an equity release?... 4 What

Mortgage & Equity Release Guide

Edward Wilson Financial Services OVERVIEW Experience We have been advising clients since 1994, and have a wealth of experience for which there is no substitute. As an appointed representative of the Sesame

Edward Wilson Financial Services OVERVIEW Experience We have been advising clients since 1994, and have a wealth of experience for which there is no substitute. As an appointed representative of the Sesame

Pathways Shared Equity Loan

Department of Housing and Public Works Pathways Shared Equity Loan Become a home owner by purchasing a share of the property you are renting Questions and Answers Booklet Great state. Great opportunity.

Department of Housing and Public Works Pathways Shared Equity Loan Become a home owner by purchasing a share of the property you are renting Questions and Answers Booklet Great state. Great opportunity.

Tariff of Mortgage Charges

Tariff of Mortgage Charges Also known as Your Guide to Standard Mortgage Charges Bank of Ireland is closely involved in the mortgage industry s initiative with the Council of Mortgage Lenders and Which?

Tariff of Mortgage Charges Also known as Your Guide to Standard Mortgage Charges Bank of Ireland is closely involved in the mortgage industry s initiative with the Council of Mortgage Lenders and Which?

Care home fees: paying them in England

Guide Guide 16 Care home fees: paying them in England This guide explains the system of funding for people who need to live in a care home in England, whether they are able, or unable to pay their own

Guide Guide 16 Care home fees: paying them in England This guide explains the system of funding for people who need to live in a care home in England, whether they are able, or unable to pay their own

A Guide to Equity Release in Retirement

A Guide to Equity Release in Retirement 1. Introduction For the retirement you deserve 2. What is Equity Release? 3. Equity Release Plans The options available to you 4. The Application Process 5. Questions

A Guide to Equity Release in Retirement 1. Introduction For the retirement you deserve 2. What is Equity Release? 3. Equity Release Plans The options available to you 4. The Application Process 5. Questions

IT S LIFETIME LOAN A SIGN OF THE TIMES AUSTRALIAN SENIORS FINANCE. The Home Equity Release Specialist

IT S A SIGN OF THE TIMES LIFETIME LOAN AUSTRALIAN SENIORS FINANCE The Home Equity Release Specialist UNLOCK THE IN YOUR EQUITY HOME If you want the financial freedom to spend your retirement how you choose,

IT S A SIGN OF THE TIMES LIFETIME LOAN AUSTRALIAN SENIORS FINANCE The Home Equity Release Specialist UNLOCK THE IN YOUR EQUITY HOME If you want the financial freedom to spend your retirement how you choose,

Our Home Reversion Plan. Enjoy your retirement by unlocking the value of your home

Our Home Reversion Plan Enjoy your retirement by unlocking the value of your home I can now have the garden I ve always wanted. 1 Bridgewater Equity Release Limited the Home Reversion Plan experts Bridgewater

Our Home Reversion Plan Enjoy your retirement by unlocking the value of your home I can now have the garden I ve always wanted. 1 Bridgewater Equity Release Limited the Home Reversion Plan experts Bridgewater

IT S MORTGAGE REVERSE A SIGN OF THE TIMES

IT S A SIGN OF THE TIMES REVERSE MORTGAGE UNLOCK THE EQUITY IN YOUR HOME If you want the financial freedom to spend your retirement how you choose, with independence and dignity, you should talk to us.

IT S A SIGN OF THE TIMES REVERSE MORTGAGE UNLOCK THE EQUITY IN YOUR HOME If you want the financial freedom to spend your retirement how you choose, with independence and dignity, you should talk to us.

Have you heard about Open Market HomeBuy?

Have you heard about Open Market HomeBuy? A guide to buying a home on the open market using an equity loan Contents What is Open Market HomeBuy? 3 Who is eligible for the scheme? 4 How does Open Market

Have you heard about Open Market HomeBuy? A guide to buying a home on the open market using an equity loan Contents What is Open Market HomeBuy? 3 Who is eligible for the scheme? 4 How does Open Market

Thinking of Buying Your Council Flat?

Thinking of Buying Your Council Flat? Things to consider before you buy a flat where the freeholder is a council, housing association or other social landlord May 2015 Department for Communities and Local

Thinking of Buying Your Council Flat? Things to consider before you buy a flat where the freeholder is a council, housing association or other social landlord May 2015 Department for Communities and Local

Equity release. A guide for those considering unlocking the value in their home

Equity release A guide for those considering unlocking the value in their home Purpose Equity release is a big decision that will affect the rest of your life. It will mean giving up full control over

Equity release A guide for those considering unlocking the value in their home Purpose Equity release is a big decision that will affect the rest of your life. It will mean giving up full control over

What will happen to my home?

What will happen to my home? Information about your home when bankruptcy occurs. This section covers the questions you are most likely to want answered about your home if you are made bankrupt: Will I

What will happen to my home? Information about your home when bankruptcy occurs. This section covers the questions you are most likely to want answered about your home if you are made bankrupt: Will I

Your retirement could have even more going for it

Your retirement could have even more going for it A straightforward guide to equity release For no obligation advice: call 0800 015 0993 www.justretirementsolutions.com Contents Imagine what you could

Your retirement could have even more going for it A straightforward guide to equity release For no obligation advice: call 0800 015 0993 www.justretirementsolutions.com Contents Imagine what you could

A HOME OF YOUR OWN. A Guide to Low Cost Housing in Hounslow for People on Moderate Incomes and for Key Workers

A HOME OF YOUR OWN A Guide to Low Cost Housing in Hounslow for People on Moderate Incomes and for Key Workers WHAT IS LOW COST HOUSING? Low Cost Housing is a general term for a number of schemes aimed

A HOME OF YOUR OWN A Guide to Low Cost Housing in Hounslow for People on Moderate Incomes and for Key Workers WHAT IS LOW COST HOUSING? Low Cost Housing is a general term for a number of schemes aimed

Equity Release Guide. Helping you make the right decision. nationwide service all lenders available personal visits. www.therightequityrelease.co.

Equity Release Guide 0800 612 5749 www.therightequityrelease.co.uk Helping you make the right decision nationwide service all lenders available personal visits 1 Welcome to The Right Equity Release Who

Equity Release Guide 0800 612 5749 www.therightequityrelease.co.uk Helping you make the right decision nationwide service all lenders available personal visits 1 Welcome to The Right Equity Release Who

EQUITY LOAN HOME HOWDO WE STAY IN OUR FAMILY HOME?

HOWDO WE STAY IN OUR FAMILY HOME? HOME EQUITY LOAN Welcome If you want the financial freedom to spend your retirement how you choose, with independence and dignity, you should talk to us. A Heartland Home

HOWDO WE STAY IN OUR FAMILY HOME? HOME EQUITY LOAN Welcome If you want the financial freedom to spend your retirement how you choose, with independence and dignity, you should talk to us. A Heartland Home

Saga Equity Release Advice Guide

Your guide to Equity Release Expert advice with no obligation Your introduction to equity release Your retirement should give you the freedom to do all the things in life you haven t had time for. However,

Your guide to Equity Release Expert advice with no obligation Your introduction to equity release Your retirement should give you the freedom to do all the things in life you haven t had time for. However,

new-build homebuy South Staffordshire Housing Association

new-build homebuy South Staffordshire Housing Association What is new build HomeBuy? New build HomeBuy, also widely known as shared ownership, is a government-funded scheme to help first-time buyers buy

new-build homebuy South Staffordshire Housing Association What is new build HomeBuy? New build HomeBuy, also widely known as shared ownership, is a government-funded scheme to help first-time buyers buy

LIFETIME MORTGAGE LUMP SUM

LIFETIME MORTGAGE LUMP SUM Terms and Conditions (version 5) This is an important document. Please keep it in a safe place. LV= Lifetime Mortgage lump sum Terms and Conditions Welcome to LV=, and thank

LIFETIME MORTGAGE LUMP SUM Terms and Conditions (version 5) This is an important document. Please keep it in a safe place. LV= Lifetime Mortgage lump sum Terms and Conditions Welcome to LV=, and thank

WEYBRIDGE FINANCIAL SERVICES EQUITY RELEASE QUESTIONNAIRE

WEYBRIDGE FINANCIAL SERVICES EQUITY RELEASE QUESTIONNAIRE PERSONAL DETAILS Title: Mr/Mrs/Miss/Ms/Other Surname First Name(s) Date of Birth Nationality Marital Status Previous/Former (e.g. Maiden) Name

WEYBRIDGE FINANCIAL SERVICES EQUITY RELEASE QUESTIONNAIRE PERSONAL DETAILS Title: Mr/Mrs/Miss/Ms/Other Surname First Name(s) Date of Birth Nationality Marital Status Previous/Former (e.g. Maiden) Name

Paying for your own care and support. Important information if you are paying for your own care and support needs or may need to in the future

Paying for your own care and support Important information if you are paying for your own care and support needs or may need to in the future Contents Page Paying for your care and support 3 What options

Paying for your own care and support Important information if you are paying for your own care and support needs or may need to in the future Contents Page Paying for your care and support 3 What options

Use your home to your advantage. A guide to equity release

Use your home to your advantage A guide to equity release 2 A guide to equity release Introducing Retirement Advantage Previously known as MGM Advantage and Stonehaven, we are a wellestablished company

Use your home to your advantage A guide to equity release 2 A guide to equity release Introducing Retirement Advantage Previously known as MGM Advantage and Stonehaven, we are a wellestablished company

A Guide to Releasing Capital from your Home

Advice for older people A Guide to Releasing Capital from your Home Advice provided by Advice for older people FirstStop Advice brings together the expertise of some of the most trusted and respected organisations

Advice for older people A Guide to Releasing Capital from your Home Advice provided by Advice for older people FirstStop Advice brings together the expertise of some of the most trusted and respected organisations

LIFETIME MORTGAGE LUMP SUM

LIFETIME MORTGAGE LUMP SUM Terms and Conditions (version 4) This is an important document. Please keep it in a safe place. LV= Lifetime Mortgage lump sum Terms and Conditions Welcome to LV=, and thank

LIFETIME MORTGAGE LUMP SUM Terms and Conditions (version 4) This is an important document. Please keep it in a safe place. LV= Lifetime Mortgage lump sum Terms and Conditions Welcome to LV=, and thank

Just the facts about home purchase plans.

September 2007 Our guides here to help you This guide is part of our Buying a home series. About the Financial Services Authority. Pensions andeveryday retirement. money. Saving and investing. If things

September 2007 Our guides here to help you This guide is part of our Buying a home series. About the Financial Services Authority. Pensions andeveryday retirement. money. Saving and investing. If things

MORTGAGE ADVICE YOU CAN DEPEND ON

MORTGAGE ADVICE YOU CAN DEPEND ON INTRODUCTION Whether you re buying your first home, remortgaging, or purchasing an investment property, there are lots of processes to go through, issues to tackle and

MORTGAGE ADVICE YOU CAN DEPEND ON INTRODUCTION Whether you re buying your first home, remortgaging, or purchasing an investment property, there are lots of processes to go through, issues to tackle and

Home Buying Glossary of terms

Home Buying Glossary of terms GLOSSARY OF AFFORDABLE HOME OWNERSHIP TERMINOLOGY The terms below are often used in house buying or mortgage process. You may come across these terms when you are in the process

Home Buying Glossary of terms GLOSSARY OF AFFORDABLE HOME OWNERSHIP TERMINOLOGY The terms below are often used in house buying or mortgage process. You may come across these terms when you are in the process

Certificate in Regulated Equity Release

Unit 1: Fundamentals of Equity Release Certificate in Regulated Equity Release Attainment Level knowledge of: K1 Definition of a Home Reversion (HR) plan & alternative methods of equity release/capital

Unit 1: Fundamentals of Equity Release Certificate in Regulated Equity Release Attainment Level knowledge of: K1 Definition of a Home Reversion (HR) plan & alternative methods of equity release/capital

Affordable Home Ownership YOUR GUIDE

Areas We Cover as a HomeBuy Agent Affordable Home Ownership YOUR GUIDE Registered Head Office Jubilee House, Stenson Road, Coalville, Leicestershire LE67 4NA Tel: 0844 892 0112 Fax: 01530 276033 For general

Areas We Cover as a HomeBuy Agent Affordable Home Ownership YOUR GUIDE Registered Head Office Jubilee House, Stenson Road, Coalville, Leicestershire LE67 4NA Tel: 0844 892 0112 Fax: 01530 276033 For general

What will happen to my Home. Information about your home when bankruptcy occurs.

What will happen to my Home Information about your home when bankruptcy occurs. This leaflet covers the questions you are most likely to want answered about your home if you are made bankrupt. 1. Will

What will happen to my Home Information about your home when bankruptcy occurs. This leaflet covers the questions you are most likely to want answered about your home if you are made bankrupt. 1. Will

Your Right to Buy Your Home: A guide for tenants of councils, new towns and registered social landlords including housing associations

Your Right to Buy Your Home: A guide for tenants of councils, new towns and registered social landlords including housing associations Your Right to Buy Your Home: A guide for tenants of councils, new

Your Right to Buy Your Home: A guide for tenants of councils, new towns and registered social landlords including housing associations Your Right to Buy Your Home: A guide for tenants of councils, new

IT S MORTGAGE REVERSE A SIGN OF THE TIMES

IT S A SIGN OF THE TIMES REVERSE MORTGAGE UNLOCK THE EQUITY IN YOUR HOME If you want the financial freedom to spend your retirement how you choose, with independence and dignity, you should talk to us.

IT S A SIGN OF THE TIMES REVERSE MORTGAGE UNLOCK THE EQUITY IN YOUR HOME If you want the financial freedom to spend your retirement how you choose, with independence and dignity, you should talk to us.

EQUITY HOME. HowDO. we stay in. our family. home?

HowDO we stay in our family home? HOME EQUITY loan Welcome If you want the financial freedom to spend your retirement how you choose, with independence and dignity, you should talk to us. A Heartland Home

HowDO we stay in our family home? HOME EQUITY loan Welcome If you want the financial freedom to spend your retirement how you choose, with independence and dignity, you should talk to us. A Heartland Home

Are you in danger of losing your home?

Are you in danger of losing your home? Help is at hand. Mortgage to Rent scheme Mortgage to Shared Equity scheme The Scottish Government Home Owners Support Fund What are the Mortgage to Rent and Mortgage

Are you in danger of losing your home? Help is at hand. Mortgage to Rent scheme Mortgage to Shared Equity scheme The Scottish Government Home Owners Support Fund What are the Mortgage to Rent and Mortgage

RELEASING CASH FROM YOUR HOME

RELEASING CASH FROM YOUR HOME As a recommended SOLLA adviser we are frequently asked to advise on home income/equity release plans. These notes are designed to provide some general background to clients

RELEASING CASH FROM YOUR HOME As a recommended SOLLA adviser we are frequently asked to advise on home income/equity release plans. These notes are designed to provide some general background to clients

Deferred Loan Application

Deferred Loan Application MINISTRY OF HEALTH MANATU HAUO RA Deferred Loans When a residential care loan becomes repayable, a deferred loan can be offered to people in certain circumstances. Residential

Deferred Loan Application MINISTRY OF HEALTH MANATU HAUO RA Deferred Loans When a residential care loan becomes repayable, a deferred loan can be offered to people in certain circumstances. Residential

Care and Support Charging and Financial Assessment Framework

Care and Support Charging and Financial Assessment Framework Effective date 1 st April, 2015 Approved by Adult Social Care, Children s Services and Education Committee Date approved 4 th March, 2015 Service

Care and Support Charging and Financial Assessment Framework Effective date 1 st April, 2015 Approved by Adult Social Care, Children s Services and Education Committee Date approved 4 th March, 2015 Service

EQUITY LOAN HOME STAY WHERE YOU BELONG. Seniors Finance

STAY WHERE YOU BELONG. HOME EQUITY LOAN Seniors Finance Welcome If you want the financial freedom to spend your retirement how you choose with independence and peace of mind knowing that unexpected costs

STAY WHERE YOU BELONG. HOME EQUITY LOAN Seniors Finance Welcome If you want the financial freedom to spend your retirement how you choose with independence and peace of mind knowing that unexpected costs

Equity release using your home to get a cash sum

Equity release using your home to get a cash sum for independent information About us We are an independent watchdog set up by the Government to: regulate firms that provide financial services; and help

Equity release using your home to get a cash sum for independent information About us We are an independent watchdog set up by the Government to: regulate firms that provide financial services; and help

Award winning. One of the UK s leading mortgage brokers. MAB is the UK s largest independent high street mortgage broker

Award winning One of the UK s leading mortgage brokers MAB is the UK s largest independent high street mortgage broker We operate out of over 700 offices across the UK We pride ourselves on the quality

Award winning One of the UK s leading mortgage brokers MAB is the UK s largest independent high street mortgage broker We operate out of over 700 offices across the UK We pride ourselves on the quality