The Minnesota Model to Rein in Predatory Lending. Representative Jim Davnie Minneapolis, Minnesota

|

|

|

- Magnus Fleming

- 8 years ago

- Views:

Transcription

1 The Minnesota Model to Rein in Predatory Lending Representative Jim Davnie Minneapolis, Minnesota 1

2 Presentation overview Exploration of problem nationally, and in Minnesota. Review of Minnesota efforts. Looking forward in Minnesota and nationally. 2

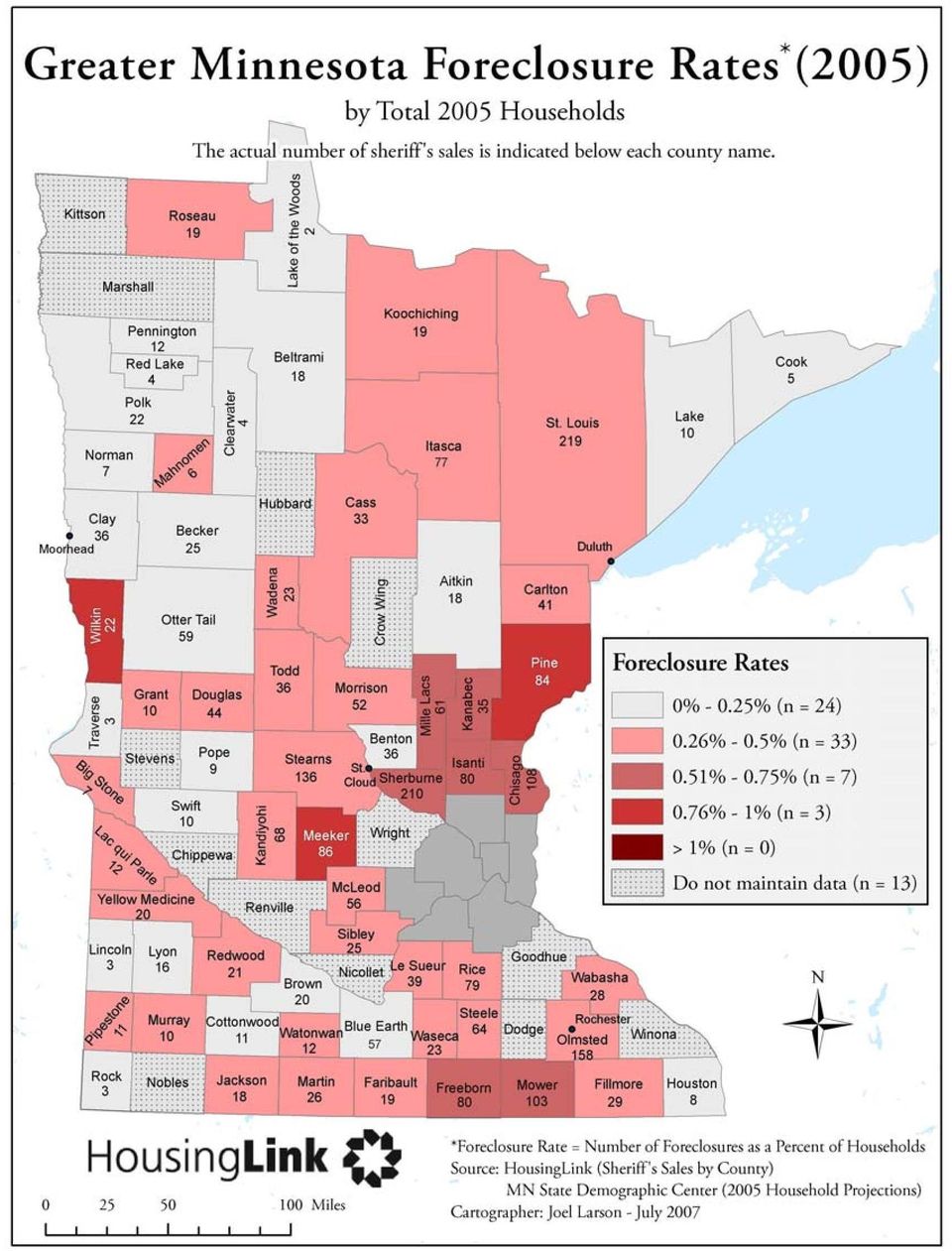

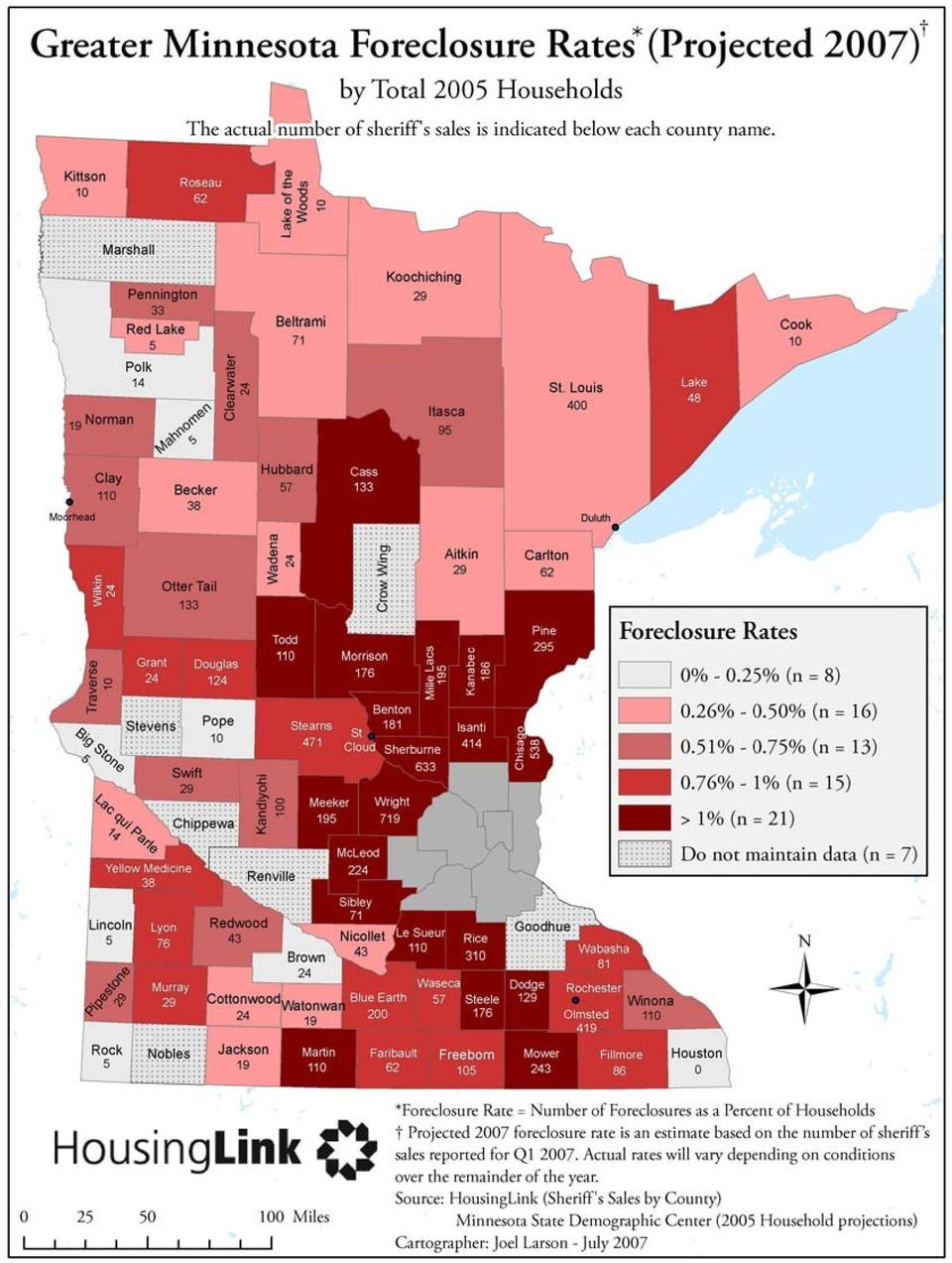

3 Foreclosure hotspots 3

4 National mortgage delinquency rates ARM & FRM Delinquency Rates (percent) 18 Prime Fixed Prime ARM Subprime Fixed Subprime ARM Q1/1998 Q1/1999 Q1/2000 Q1/2001 Q1/2002 Q1/2003 Q1/2004 Q1/2005 Q1/2006 Q1/1998 Q1/1999 Q1/2000 Q1/2001 Q1/2002 Q1/2003 Q1/2004 Q1/2005 Q1/2006 4

5

6

7

8 Roots of the crisis I Loosening of underwriting standards since 2005 Tax law changes making rental property ownership more inviting (Minnesota) Securitization and disconnect between brokers and borrowers interests Fraud 8

9 Roots of the crisis II Rapid escalation of housing values placing higher demands on borrowers Sophistication of mortgages outstripping sophistication of borrowers Betting on appreciation Fraud 9

10 Supply side yield hunger and ample investment capital drove the subprime lending push. It was not consumer driven. Tom Bengston, Editor North-Western Financial review Lawmakers magazine 10

11 Rise in subprime mortgage lending Not all subprime loans are predatory, but nearly all predatory loans are subprime Professor Jeff Crump, University of Minnesota 11

12 Unequal impact Lenders on average made subprime loans to higher-qualified African- Americans 54% of the time, compared to 23% for Caucasians. National Community Reinvestment Coalition 12

13 The Minnesota experience 400% in foreclosures in Twin Cities metro area % Increase in foreclosures in Greater Minnesota (outside the Minneapolis-St. Paul metro area). 100% increase in foreclosures in Minneapolis in 2006 from

14 Minneapolis 2,152 housing units went to public auction in Minneapolis in the first three quarters of

15 Timeline Summer 2006: Minneapolis and Hennepin County identify up tick in foreclosures December 2006: Attorney General-elect Lori Swanson convenes Predatory Lending Study Group January 2007: Study Group issues report February 2007: Legislation introduced April 2007: Signed by Governor August 2007: Effective date of legislation 15

16 Predatory Lending Study Group Created by Attorney General-elect Lori Swanson Chaired by University of Minnesota Law Professor Membership included representatives of the business community, Legal Aid, ACORN, community bankers, non-profit developers, legislators, and the Council Presidents from both central cities city councils. 16

17 Elements of the legislation Lenders and brokers must verify a borrower s ability to repay the loan Lenders may use criteria other than traditional documentation to justify making the loan but must document alternative criteria through reliable methods For ARMs, lender must verify that borrower can qualify for fully indexed rate, not just teaser rate 17

18 Brokers Must Act in Client s Best Interest Brokers now have a legal duty to act in the best interest of the borrower. Brokers cannot accept compensation that is undisclosed to the borrower. Payments from lender to broker must be included in calculation of lender fees. Lender fees are capped at 5% of loan amount. Side payments from lender to broker ( yield spread premiums ) count toward 5%. 18

19 Negative Amortization Loans Prohibited Lenders can no longer make loans that are structured so monthly payments don t cover all the interest that is accruing on the loan. 19

20 Other Prohibitions Churning refinancing that doesn t benefit the borrower Prepayment penalties for subprime loans Refinancing special mortgages without loan counseling Partial payment quotes (without taxes and insurance) without telling borrower must be able to compare accurately 20

without telling borrower must be able to compare")

21 Victims have new remedies Borrowers who are harmed by violations of the standards set forth for brokers, lenders, and appraisers now have a right to sue for damages, costs, and attorney fees Does not apply to loans originated by a state or federally chartered bank, savings bank, or credit union 21

22 A new crime-mortgage fraud Anyone who falsifies information on mortgage application, or anyone who facilitates the use of such information in connection with getting a mortgage with the knowledge that the information is false, can be prosecuted for the crime of mortgage fraud 22

23 Some Lenders Exempt Some provisions (verify ability to repay, churning, negative amortization, disclosing P&I) do not apply to a state or federally chartered bank, savings bank, or credit union, or to a loan originated or purchased by a state agency or tribal or local unit of government 23

24 Looking forward in Minnesota Five work groups created Foreclosure modernization Municipal impacts and tools Tenant/condo concerns Data requirements Foreclosure prevention assistance Broad stakeholder participation 24

25 Looking Forward I Median average home sales price down 4.6% over past 12 months. 25

26 Looking forward nationally II 26

27 Looking forward nationally III Increased stress on consumers Rising gasoline prices National average $3.08/gal regular Rising heating costs Natural gas prices projected 41% higher than 06!.2 million utility consumers disconnected nationally Rising grocery costs Grocery prices projected to rise 7.5% for 2007, roughly triple core inflation rate Increased revolving credit debt Card issuers seeing increased delinquency rates 27

28 Acknowledgements Senator Linda Higgins Dr. Michael Grover, Minneapolis Federal Reserve Board Greater Minnesota Housing Fund Housing Link Cara Letofsky, City of Minneapolis Amber Hawkins, Foreclosure Relief Law Project 28

29 Representative Jim Davnie District 62A South Minneapolis. 545 State Office Building, St. Paul, MN

National Delinquency and Foreclosure Trends Mortgage Category Definitions National percentage change in mortgage delinquencies and

Volume 31, December 2007 Policy Points A publication of the Southern Good Faith Fund Public Policy program Mortgage Foreclosures: A Review of Trends in Arkansas and Strategies Used The rising rate of mortgage

Volume 31, December 2007 Policy Points A publication of the Southern Good Faith Fund Public Policy program Mortgage Foreclosures: A Review of Trends in Arkansas and Strategies Used The rising rate of mortgage

FINAL REPORT PREDATORY LENDING STUDY GROUP FOR ATTORNEY GENERAL LORI SWANSON. January 2007

FINAL REPORT PREDATORY LENDING STUDY GROUP FOR ATTORNEY GENERAL LORI SWANSON January 27 1 Introduction In December 26, Attorney General Lori Swanson appointed a Study Group to propose legislation to help

FINAL REPORT PREDATORY LENDING STUDY GROUP FOR ATTORNEY GENERAL LORI SWANSON January 27 1 Introduction In December 26, Attorney General Lori Swanson appointed a Study Group to propose legislation to help

NCUA LETTER TO CREDIT UNIONS

NCUA LETTER TO CREDIT UNIONS NATIONAL CREDIT UNION ADMINISTRATION 1775 Duke Street, Alexandria, VA 22314 DATE: August 2008 LETTER NO.: 08-CU-19 TO: SUBJ: Federally Insured Credit Unions Third-Party Relationships:

NCUA LETTER TO CREDIT UNIONS NATIONAL CREDIT UNION ADMINISTRATION 1775 Duke Street, Alexandria, VA 22314 DATE: August 2008 LETTER NO.: 08-CU-19 TO: SUBJ: Federally Insured Credit Unions Third-Party Relationships:

MLO COMPENSATION, REGULATION Z, AND DODD-FRANK ACT

MLO COMPENSATION, REGULATION Z, AND DODD-FRANK ACT Vermont Mortgage Bankers Association & Mortgage Bankers/Brokers Association of NH Mortgage Compliance Conference Thursday, March 3, 2011 Sean P. Mahoney

MLO COMPENSATION, REGULATION Z, AND DODD-FRANK ACT Vermont Mortgage Bankers Association & Mortgage Bankers/Brokers Association of NH Mortgage Compliance Conference Thursday, March 3, 2011 Sean P. Mahoney

CONSUMER. Helping Elderly Homeowners Victimized by Predatory Mortgage Loans

CONSUMER Information for Advocates Representing Older Adults National Consumer Law Center Helping Elderly Homeowners Victimized by Predatory Mortgage Loans Equity-rich, cash poor, elderly homeowners are

CONSUMER Information for Advocates Representing Older Adults National Consumer Law Center Helping Elderly Homeowners Victimized by Predatory Mortgage Loans Equity-rich, cash poor, elderly homeowners are

Helping Elderly Homeowners Victimized by Predatory Mortgage Loans

Helping Elderly Homeowners Victimized by Predatory Mortgage Loans Equity-rich, cash poor elderly homeowners are an attractive target for unscrupulous mortgage lenders. Many elderly homeowners are on fixed

Helping Elderly Homeowners Victimized by Predatory Mortgage Loans Equity-rich, cash poor elderly homeowners are an attractive target for unscrupulous mortgage lenders. Many elderly homeowners are on fixed

Responses to the Foreclosure Crisis University of Iowa October 2008

Responses to the Foreclosure Crisis University of Iowa October 2008 National Community Reinvestment Coalition http://www.ncrc.org 202-628-8866 1 What is Abusive Lending Prime lending market rate lending

Responses to the Foreclosure Crisis University of Iowa October 2008 National Community Reinvestment Coalition http://www.ncrc.org 202-628-8866 1 What is Abusive Lending Prime lending market rate lending

Litigation Related to a Mortgage: Expert Witness Considerations

MORTGAGE EXPERT WITNESS Litigation Related to a Mortgage: Expert Witness Considerations By Joffrey Long Joffrey Long Joffrey Long is a mortgage lender / broker who makes, arranges and services both private

MORTGAGE EXPERT WITNESS Litigation Related to a Mortgage: Expert Witness Considerations By Joffrey Long Joffrey Long Joffrey Long is a mortgage lender / broker who makes, arranges and services both private

Financing Residential Real Estate

Financing Residential Real Estate Chapter 1: Finance and Investment Borrowing Money to Buy a Home Investments and Returns Types of Investments Ownership Investments Debt Investments Securities Investment

Financing Residential Real Estate Chapter 1: Finance and Investment Borrowing Money to Buy a Home Investments and Returns Types of Investments Ownership Investments Debt Investments Securities Investment

Testimony of Minnesota Attorney General Lori Swanson

Testimony of Minnesota Attorney General Lori Swanson Regarding Predatory Mortgage Lending and Use of the Board's Authority Under the Home Ownership and Equity Protection Act of 1994 (HOEPA) to Curb Abusive

Testimony of Minnesota Attorney General Lori Swanson Regarding Predatory Mortgage Lending and Use of the Board's Authority Under the Home Ownership and Equity Protection Act of 1994 (HOEPA) to Curb Abusive

Guide to Fair Mortgage Lending and Home Preservation

Guide to Fair Mortgage Lending and Home Preservation Fair Housing Legal Support Center & Clinic Guide to Fair Mortgage Lending and Home Preservation What does this guide cover? What is Fair Lending? What

Guide to Fair Mortgage Lending and Home Preservation Fair Housing Legal Support Center & Clinic Guide to Fair Mortgage Lending and Home Preservation What does this guide cover? What is Fair Lending? What

OFFICE OF THE ATTORNEY GENERAL GUIDANCE WITH RESPECT TO 940 CMR 8.00 et. seq. (as amended)

") OFFICE OF THE ATTORNEY GENERAL GUIDANCE WITH RESPECT TO 940 CMR 8.00 et. seq. (as amended) On October 17, 2007 the Office of the Attorney General amended 940 CMR 8.00 et. seq., the regulation under the

OFFICE OF THE ATTORNEY GENERAL GUIDANCE WITH RESPECT TO 940 CMR 8.00 et. seq. (as amended) On October 17, 2007 the Office of the Attorney General amended 940 CMR 8.00 et. seq., the regulation under the

Tip Sheet. Keep in mind we are not a law firm and this is not legal advice. All advertising should be reviewed by an attorney prior to distribution.

Mortgage Acts and Practices Act (MAP) Advertising Rule (Regulation N) Tip Sheet Keep in mind we are not a law firm and this is not legal advice. All advertising should be reviewed by an attorney prior

Mortgage Acts and Practices Act (MAP) Advertising Rule (Regulation N) Tip Sheet Keep in mind we are not a law firm and this is not legal advice. All advertising should be reviewed by an attorney prior

Glossary of Lending Terms

Glossary of Lending Terms Adjustable Rate Loan or Adjustable Rate Mortgage (ARM) A loan with an interest rate that changes during the term of the loan. The payments generally increase or decrease with

Glossary of Lending Terms Adjustable Rate Loan or Adjustable Rate Mortgage (ARM) A loan with an interest rate that changes during the term of the loan. The payments generally increase or decrease with

Mortgage Lending laws and how it affects you, the REALTOR. Presented by Anders Hostelley and Leonard Loventhal

Mortgage Lending laws and how it affects you, the REALTOR. Presented by Anders Hostelley and Leonard Loventhal Secure and Fair Enforcement for Mortgage Licensing Act Title V of P.L. 110-289, the Secure

Mortgage Lending laws and how it affects you, the REALTOR. Presented by Anders Hostelley and Leonard Loventhal Secure and Fair Enforcement for Mortgage Licensing Act Title V of P.L. 110-289, the Secure

COLORADO CONSUMER EQUITY PROTECTION ACT July 1, 2011

COLORADO CONSUMER EQUITY PROTECTION ACT July 1, 2011 Table of Contents COLORADO CONSUMER EQUITY PROTECTION ACT... 1 PART 1 OBLIGOR PROTECTION... 1 5-3.5-101. Definitions.... 1 5-3.5-102. Protection of

COLORADO CONSUMER EQUITY PROTECTION ACT July 1, 2011 Table of Contents COLORADO CONSUMER EQUITY PROTECTION ACT... 1 PART 1 OBLIGOR PROTECTION... 1 5-3.5-101. Definitions.... 1 5-3.5-102. Protection of

9-Jul-08 State Responses to Housing Crisis: Legislative Solutions

9-Jul-08 State Responses to Housing Crisis: Legislative Solutions Arkansas 4/16/03 7/15/03 HB 2598 California 7/8/08 7/8/08 SB 1137 10/5/07 10/5/07 SB 223 10/5/07 SB 385 Enacts Arkansas Home Loan Protection

9-Jul-08 State Responses to Housing Crisis: Legislative Solutions Arkansas 4/16/03 7/15/03 HB 2598 California 7/8/08 7/8/08 SB 1137 10/5/07 10/5/07 SB 223 10/5/07 SB 385 Enacts Arkansas Home Loan Protection

1. Only 20 days to file answer or other responsive pleading to summons and complaint in foreclosure action.

PREDATORY MORTGAGE LENDING FORECLOSURE DEFENSE Attorney Catherine M. Doyle Legal Aid Society of Milwaukee 521 N. 8 th Street Milwaukee, WI 53233 (414) 727-5331 cdoyle@lasmilwaukee.com I. MORTGAGE FORECLOSURE

PREDATORY MORTGAGE LENDING FORECLOSURE DEFENSE Attorney Catherine M. Doyle Legal Aid Society of Milwaukee 521 N. 8 th Street Milwaukee, WI 53233 (414) 727-5331 cdoyle@lasmilwaukee.com I. MORTGAGE FORECLOSURE

Mortgage Crisis Summit

Mortgage Crisis Summit Hosted by Michigan Credit Union League January 10, 2008 Instructions to Access Summit For the Web portion go to: http://cuv.on.raindance.com/confmgr/public_u nsched.jsp?confld=4291923

Mortgage Crisis Summit Hosted by Michigan Credit Union League January 10, 2008 Instructions to Access Summit For the Web portion go to: http://cuv.on.raindance.com/confmgr/public_u nsched.jsp?confld=4291923

Lesson 13: Applying for a Mortgage Loan

1 Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 2 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit unions

1 Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 2 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit unions

To: Counsel, Agents, and Readers From: Michael J. Berey Dated: September 5, 2008 Re: Mortgages: Chapter 472, Laws of 2008

To: Counsel, Agents, and Readers From: Michael J. Berey Dated: September 5, 2008 Re: Mortgages: Chapter 472, Laws of 2008 Chapter 472 of the Laws of 2008 was signed into law on August 5, 2008. According

To: Counsel, Agents, and Readers From: Michael J. Berey Dated: September 5, 2008 Re: Mortgages: Chapter 472, Laws of 2008 Chapter 472 of the Laws of 2008 was signed into law on August 5, 2008. According

2. The Fair Housing Act requires lenders to display what in all branch offices? 3. Which is LEAST LIKLEY to be an indicator of predatory lending?

Course: Lesson: National Mortgage Loan Originator Review Crammer (ml) Ethics 1. At closing, buyer Steve sees that the lender changed the terms of the loan that they had agreed to, but he felt he had no

Course: Lesson: National Mortgage Loan Originator Review Crammer (ml) Ethics 1. At closing, buyer Steve sees that the lender changed the terms of the loan that they had agreed to, but he felt he had no

Ability to Repay and Qualified Mortgages. Dave Loyst SVP Financial Institutions Group Stearns Lending, Inc.

Ability to Repay and Qualified Mortgages Dave Loyst SVP Financial Institutions Group Stearns Lending, Inc. 1 Effective Date CFPB issued Final QM Rule January 2013 First revision to the final rule: May

Ability to Repay and Qualified Mortgages Dave Loyst SVP Financial Institutions Group Stearns Lending, Inc. 1 Effective Date CFPB issued Final QM Rule January 2013 First revision to the final rule: May

New State Law Addresses Mortgage Foreclosure Crisis and Subprime Lending Abuses. By Kirsten Keefe and Elizabeth Hasper

119 Washington Ave. Albany, NY 12210 Phone 518.462.6831 Fax 518.462.6687 www.empirejustice.org New State Law Addresses Mortgage Foreclosure Crisis and Subprime Lending Abuses By Kirsten Keefe and Elizabeth

119 Washington Ave. Albany, NY 12210 Phone 518.462.6831 Fax 518.462.6687 www.empirejustice.org New State Law Addresses Mortgage Foreclosure Crisis and Subprime Lending Abuses By Kirsten Keefe and Elizabeth

Understanding Mortgage Foreclosures: Trends and Policy Issues

Understanding Mortgage Foreclosures: Trends and Policy Issues National Interagency Community Reinvestment Conference April 1, 2008 Caryn Becker Policy Counsel (510) 379-5500 http://www.responsiblelending.org

Understanding Mortgage Foreclosures: Trends and Policy Issues National Interagency Community Reinvestment Conference April 1, 2008 Caryn Becker Policy Counsel (510) 379-5500 http://www.responsiblelending.org

Assumable mortgage: A mortgage that can be transferred from a seller to a buyer. The buyer then takes over payment of an existing loan.

MORTGAGE GLOSSARY Adjustable Rate Mortgage (ARM): A mortgage loan with payments usually lower than a fixed rate initially, but is subject to changes in interest rates. There are a variety of ARMs that

MORTGAGE GLOSSARY Adjustable Rate Mortgage (ARM): A mortgage loan with payments usually lower than a fixed rate initially, but is subject to changes in interest rates. There are a variety of ARMs that

Residential Mortgage Lending in Oregon, CY 2007

Introduction Residential Mortgage Lending in Oregon, CY 2007 By Senate Bill 1064 (2008), the Oregon Legislature required that all mortgage banker and mortgage brokers licensed by the Oregon Division of

Introduction Residential Mortgage Lending in Oregon, CY 2007 By Senate Bill 1064 (2008), the Oregon Legislature required that all mortgage banker and mortgage brokers licensed by the Oregon Division of

CONFERENCE OF STATE BANK SUPERVISORS AMERICAN ASSOCIATION OF RESIDENTIAL MORTGAGE REGULATORS NATIONAL ASSOCIATION OF CONSUMER CREDIT ADMINISTRATORS

CONFERENCE OF STATE BANK SUPERVISORS AMERICAN ASSOCIATION OF RESIDENTIAL MORTGAGE REGULATORS NATIONAL ASSOCIATION OF CONSUMER CREDIT ADMINISTRATORS STATEMENT ON SUBPRIME MORTGAGE LENDING I. INTRODUCTION

CONFERENCE OF STATE BANK SUPERVISORS AMERICAN ASSOCIATION OF RESIDENTIAL MORTGAGE REGULATORS NATIONAL ASSOCIATION OF CONSUMER CREDIT ADMINISTRATORS STATEMENT ON SUBPRIME MORTGAGE LENDING I. INTRODUCTION

Mortgage Laws and Regulations-Georgia. Introduction. LegalEase was asked to review and summarize any legislation since January of 2007

Mortgage Laws and Regulations-Georgia Introduction 23400 Michigan Avenue, Suite 101 Dearborn, MI 48124 Tel: 1-(866) 534-6177 (toll-free) Fax: 1-(734) 943-6051 Email: contact@legaleasesolutions.com www.legaleasesolutions.com

Mortgage Laws and Regulations-Georgia Introduction 23400 Michigan Avenue, Suite 101 Dearborn, MI 48124 Tel: 1-(866) 534-6177 (toll-free) Fax: 1-(734) 943-6051 Email: contact@legaleasesolutions.com www.legaleasesolutions.com

CONFERENCE OF STATE BANK SUPERVISORS AMERICAN ASSOCIATION OF RESIDENTIAL MORTGAGE REGULATORS NATIONAL ASSOCIATION OF CONSUMER CREDIT ADMINISTRATORS

CONFERENCE OF STATE BANK SUPERVISORS AMERICAN ASSOCIATION OF RESIDENTIAL MORTGAGE REGULATORS NATIONAL ASSOCIATION OF CONSUMER CREDIT ADMINISTRATORS STATEMENT ON SUBPRIME MORTGAGE LENDING I. INTRODUCTION

CONFERENCE OF STATE BANK SUPERVISORS AMERICAN ASSOCIATION OF RESIDENTIAL MORTGAGE REGULATORS NATIONAL ASSOCIATION OF CONSUMER CREDIT ADMINISTRATORS STATEMENT ON SUBPRIME MORTGAGE LENDING I. INTRODUCTION

Ch. 46 PROPER CONDUCT OF LENDING 10 46.1 CHAPTER 46. PROPER CONDUCT OF LENDING AND BROKERING IN THE MORTGAGE LOAN BUSINESS

Ch. 46 PROPER CONDUCT OF LENDING 10 46.1 CHAPTER 46. PROPER CONDUCT OF LENDING AND BROKERING IN THE MORTGAGE LOAN BUSINESS Sec. 46.1. Definitions. 46.2. Proper conduct of lending and brokering in the mortgage

Ch. 46 PROPER CONDUCT OF LENDING 10 46.1 CHAPTER 46. PROPER CONDUCT OF LENDING AND BROKERING IN THE MORTGAGE LOAN BUSINESS Sec. 46.1. Definitions. 46.2. Proper conduct of lending and brokering in the mortgage

Presented by the Baxter Credit Union Audit Team

Presented by the Baxter Credit Union Audit Team 1. Who offers Mortgage or Home Equity Loans? 2. Do you perform your SAFE Act Audit in-house, or do you outsource it? 3. Who in the room is your Credit Union

Presented by the Baxter Credit Union Audit Team 1. Who offers Mortgage or Home Equity Loans? 2. Do you perform your SAFE Act Audit in-house, or do you outsource it? 3. Who in the room is your Credit Union

The Effects of Vacant and Abandoned Property Part I, The History

The Effects of Vacant and Abandoned Property Part I, The History Vacant and Abandoned Properties THE HISTORY Print date: February 19, 2013 Target Audience This course is intended for Law Enforcement officers

The Effects of Vacant and Abandoned Property Part I, The History Vacant and Abandoned Properties THE HISTORY Print date: February 19, 2013 Target Audience This course is intended for Law Enforcement officers

Home Based Business Foreclosures - Overview and Methodology of the Foreclosure Process

Oakland NEIGHBORHOODS 1 Overview There is an epidemic of foreclosures throughout the country, including in Oakland and California. Last year there were 1.2 million foreclosures filed nationwide (that s

Oakland NEIGHBORHOODS 1 Overview There is an epidemic of foreclosures throughout the country, including in Oakland and California. Last year there were 1.2 million foreclosures filed nationwide (that s

Residential Mortgage Lending in Oregon Calendar Year 2010

Residential Mortgage Lending in Oregon Calendar Year 2010 Department of Consumer and Business Services Division of Finance and Corporate Securities December 2011 Introduction: This report marks the fourth

Residential Mortgage Lending in Oregon Calendar Year 2010 Department of Consumer and Business Services Division of Finance and Corporate Securities December 2011 Introduction: This report marks the fourth

Title XIV - Mortgage Reform and Anti-Predatory Lending Act. Short title: "Mortgage Reform and Anti-Predatory Lending Act"

Title XIV - Mortgage Reform and Anti-Predatory Lending Act Short title: "Mortgage Reform and Anti-Predatory Lending Act" Subtitles A, B, C, and E are designated as Enumerated Consumer Law under the Bureau

Title XIV - Mortgage Reform and Anti-Predatory Lending Act Short title: "Mortgage Reform and Anti-Predatory Lending Act" Subtitles A, B, C, and E are designated as Enumerated Consumer Law under the Bureau

ESCROW REQUIREMENTS UNDER TILA

Overview Escrow Requirements Reg. Z High Cost Mortgage and Counseling - Reg. Z & X Ability to Repay & Qualified Mortgages Reg. Z & X Mortgage Servicing Reg. Z & X Loan Originator Compensation Reg. Z Copies

Overview Escrow Requirements Reg. Z High Cost Mortgage and Counseling - Reg. Z & X Ability to Repay & Qualified Mortgages Reg. Z & X Mortgage Servicing Reg. Z & X Loan Originator Compensation Reg. Z Copies

DEPARTMENT OF FINANCIAL AND PROFESSIONAL REGULATION NOTICE OF PROPOSED AMENDMENTS

TITLE 38: FINANCIAL INSTITUTIONS CHAPTER II: PART 346 PREDATORY LENDING DATABASE Section 346.10 Definitions 346.15 Information Required 346.20 Standards for Credit Counseling (Repealed) 346.21 Standards

TITLE 38: FINANCIAL INSTITUTIONS CHAPTER II: PART 346 PREDATORY LENDING DATABASE Section 346.10 Definitions 346.15 Information Required 346.20 Standards for Credit Counseling (Repealed) 346.21 Standards

Course Dates: Purpose of the Course: Course Description:

TrainingPro: 8 Hour Massachusetts SAFE Comprehensive _ Maintaining Momentum in the Changing Mortgage Marketplace (Course Number: 2769) Online Self-Paced Class Syllabus Course Dates: Purpose of the Course:

TrainingPro: 8 Hour Massachusetts SAFE Comprehensive _ Maintaining Momentum in the Changing Mortgage Marketplace (Course Number: 2769) Online Self-Paced Class Syllabus Course Dates: Purpose of the Course:

MRS Title 9-A 8-103. Definitions and rules of construction

9-A 8-103. Definitions and rules of construction The text included in this publication was prepared by the Maine Bureau of Financial Institutions and is current through July 15, 2008. It is a version that

9-A 8-103. Definitions and rules of construction The text included in this publication was prepared by the Maine Bureau of Financial Institutions and is current through July 15, 2008. It is a version that

Assembly Bill No. 344 CHAPTER 733

Assembly Bill No. 344 CHAPTER 733 An act to amend Sections 4970, 4973, 4974, 4975, 4977, 4978, 4978.6, 4979, and 4979.7 of the Financial Code, as added by Assembly Bill 489 of the 2001-02 Regular Session,

Assembly Bill No. 344 CHAPTER 733 An act to amend Sections 4970, 4973, 4974, 4975, 4977, 4978, 4978.6, 4979, and 4979.7 of the Financial Code, as added by Assembly Bill 489 of the 2001-02 Regular Session,

Implications. Housing Market Meltdown: Subprime Lending and Foreclosure Jeff R. Crump, Ph.D. IN THIS ISSUE

VOL. 06 ISSUE 08 A Newsletter by InformeDesign. A Web site for design and human behavior research. IN THIS ISSUE Housing Market Meltdown: Subprime Lending and Foreclosure Related Research Summaries Housing

VOL. 06 ISSUE 08 A Newsletter by InformeDesign. A Web site for design and human behavior research. IN THIS ISSUE Housing Market Meltdown: Subprime Lending and Foreclosure Related Research Summaries Housing

OLR RESEARCH REPORT ANALYSIS OF STATE SMALL BUSINESS LOAN GUARANTEE PROGRAMS. By: Michelle Kirby, Associate Analyst

OLR RESEARCH REPORT February 19, 2013 2013-R-0054 ANALYSIS OF STATE SMALL BUSINESS LOAN GUARANTEE PROGRAMS By: Michelle Kirby, Associate Analyst You asked for an analysis of state small business loan guarantee

OLR RESEARCH REPORT February 19, 2013 2013-R-0054 ANALYSIS OF STATE SMALL BUSINESS LOAN GUARANTEE PROGRAMS By: Michelle Kirby, Associate Analyst You asked for an analysis of state small business loan guarantee

Subprime lending & Foreclosure Crisis

Subprime lending & Foreclosure Crisis Legislative Responses Assembly Committee on The Mortgage Crisis Facts and Figures A Credit Suisse report this spring predicted that 6.5 million loans will fall into

Subprime lending & Foreclosure Crisis Legislative Responses Assembly Committee on The Mortgage Crisis Facts and Figures A Credit Suisse report this spring predicted that 6.5 million loans will fall into

HOUSE BILL 2242 AN ACT AMENDING TITLE 6, ARIZONA REVISED STATUTES, BY ADDING CHAPTER 16; RELATING TO REVERSE MORTGAGES.

Senate Engrossed House Bill State of Arizona House of Representatives Forty-ninth Legislature Second Regular Session HOUSE BILL AN ACT AMENDING TITLE, ARIZONA REVISED STATUTES, BY ADDING CHAPTER ; RELATING

Senate Engrossed House Bill State of Arizona House of Representatives Forty-ninth Legislature Second Regular Session HOUSE BILL AN ACT AMENDING TITLE, ARIZONA REVISED STATUTES, BY ADDING CHAPTER ; RELATING

STRUGGLING TO MAKE YOUR MORTGAGE PAYMENT PAGE 4

Michigan Lending & Foreclosure Guide Attorney General Bill Schuette TABLE OF CONTENTS PREDATORY MORTGAGE LENDING PAGE 1 PREDATORY LENDING RED FLAGS PAGE 3 STRUGGLING TO MAKE YOUR MORTGAGE PAYMENT PAGE

Michigan Lending & Foreclosure Guide Attorney General Bill Schuette TABLE OF CONTENTS PREDATORY MORTGAGE LENDING PAGE 1 PREDATORY LENDING RED FLAGS PAGE 3 STRUGGLING TO MAKE YOUR MORTGAGE PAYMENT PAGE

Definitions. In some cases a survey rather than an ILC is required.

Definitions 1. What is the closing? The closing is a formal meeting at which both the buyer and seller meet to sign all the final documentation required for the buyer's mortgage loan. Once the closing

Definitions 1. What is the closing? The closing is a formal meeting at which both the buyer and seller meet to sign all the final documentation required for the buyer's mortgage loan. Once the closing

Chapter 30 Home Equity Conversion Mortgages. 47-30-103. Authorized lenders Designation Application.

Chapter 30 Home Equity Conversion Mortgages 47-30-101. Short title. 47-30-102. Definitions. 47-30-103. Authorized lenders Designation Application. 47-30-104. Compliance Noncomplying loans unenforceable

Chapter 30 Home Equity Conversion Mortgages 47-30-101. Short title. 47-30-102. Definitions. 47-30-103. Authorized lenders Designation Application. 47-30-104. Compliance Noncomplying loans unenforceable

Protecting Your Investment

Protecting Your Investment Understanding Home Financing and Avoiding Foreclosure Massachusetts Attorney General Consumer Hotline One Ashburton Place Boston, MA 02108-1518 (617) 727-8400 or (617) 727-4765

Protecting Your Investment Understanding Home Financing and Avoiding Foreclosure Massachusetts Attorney General Consumer Hotline One Ashburton Place Boston, MA 02108-1518 (617) 727-8400 or (617) 727-4765

Mortgage Meltdown Is Every State Impacted?

Mortgage Meltdown Is Every State Impacted? Good morning and thank you for taking your valuable time to learn more about the current status of the mortgage lending industry. I am glad to have the opportunity

Mortgage Meltdown Is Every State Impacted? Good morning and thank you for taking your valuable time to learn more about the current status of the mortgage lending industry. I am glad to have the opportunity

STATE OF NEW JERSEY DEPARTMENT OF BANKING AND INSURANCE STATEMENT ON SUBPRIME MORTGAGE LENDING

STATE OF NEW JERSEY DEPARTMENT OF BANKING AND INSURANCE STATEMENT ON SUBPRIME MORTGAGE LENDING I. INTRODUCTION AND BACKGROUND On June 29, 2007, the Federal Deposit Insurance Corporation (FDIC), the Board

STATE OF NEW JERSEY DEPARTMENT OF BANKING AND INSURANCE STATEMENT ON SUBPRIME MORTGAGE LENDING I. INTRODUCTION AND BACKGROUND On June 29, 2007, the Federal Deposit Insurance Corporation (FDIC), the Board

Dodd Frank Act Consumer Financial Protection Bureau Mortgage Lending

Dodd Frank Act Consumer Financial Protection Bureau Mortgage Lending A Briefing for the Texas House Investments and Financial Services Committee John C. Fleming Consumer Financial Protection Bureau (CFPB)

Dodd Frank Act Consumer Financial Protection Bureau Mortgage Lending A Briefing for the Texas House Investments and Financial Services Committee John C. Fleming Consumer Financial Protection Bureau (CFPB)

Countrywide Settlement FAQ s

Countrywide Settlement FAQ s 1. Does the settlement impact my Countrywide loan? The Attorney General s settlement with Countrywide provides for loan modifications for eligible borrowers who are 60 days

Countrywide Settlement FAQ s 1. Does the settlement impact my Countrywide loan? The Attorney General s settlement with Countrywide provides for loan modifications for eligible borrowers who are 60 days

Tips for Avoiding a Predatory Mortgage Loan

Tips for Avoiding a Predatory Mortgage Loan What is Predatory Mortgage Lending? A predatory mortgage is a needlessly expensive home loan that provides no financial benefit to the borrower in return for

Tips for Avoiding a Predatory Mortgage Loan What is Predatory Mortgage Lending? A predatory mortgage is a needlessly expensive home loan that provides no financial benefit to the borrower in return for

This chapter shall be known and may be cited as the "Home Equity Conversion Mortgage Act."

Source: http://www.lexisnexis.com/hottopics/tncode/ 47-30-101. Short title. This chapter shall be known and may be cited as the "Home Equity Conversion Mortgage Act." HISTORY: Acts 1993, ch. 410, 2. 47-30-102.

Source: http://www.lexisnexis.com/hottopics/tncode/ 47-30-101. Short title. This chapter shall be known and may be cited as the "Home Equity Conversion Mortgage Act." HISTORY: Acts 1993, ch. 410, 2. 47-30-102.

COMMUNICATION NO. 313635 PROPOSED ORDINANCE AMENDMENT. Sponsored by

COMMUNICATION NO. 313635 PROPOSED ORDINANCE AMENDMENT Sponsored by THE HONORABLE TONI PRECKWINKLE, PRESIDENT, EARLEAN COLLINS, JERRY BUTLER, JOHN P. DALEY, JESUS G. GARCIA, EDWIN REYES, ROBERT B. STEELE

COMMUNICATION NO. 313635 PROPOSED ORDINANCE AMENDMENT Sponsored by THE HONORABLE TONI PRECKWINKLE, PRESIDENT, EARLEAN COLLINS, JERRY BUTLER, JOHN P. DALEY, JESUS G. GARCIA, EDWIN REYES, ROBERT B. STEELE

CFPB issues ability-to-repay and qualified mortgage rules

1 FEBRUARY 4, 2013 CFPB issues ability-to-repay and qualified mortgage rules By Raymond J. Gustini, Lloyd H. Spencer, Tiana M. Butcher, Courtney L. Lindsay II, and Pierce Han No standard is perfect, but

1 FEBRUARY 4, 2013 CFPB issues ability-to-repay and qualified mortgage rules By Raymond J. Gustini, Lloyd H. Spencer, Tiana M. Butcher, Courtney L. Lindsay II, and Pierce Han No standard is perfect, but

The Coordinated Plan. to Address Foreclosures in Minnesota

The Coordinated Plan to Address Foreclosures in Minnesota A review of and as summarized by the Minnesota Foreclosure Partners Council March 2009 The Problem The number of mortgage foreclosures in Minnesota

The Coordinated Plan to Address Foreclosures in Minnesota A review of and as summarized by the Minnesota Foreclosure Partners Council March 2009 The Problem The number of mortgage foreclosures in Minnesota

The New Ability-to-Pay Rules; Qualified Mortgage Lending under the Dodd-Frank Act

The New Ability-to-Pay Rules; Qualified Mortgage Lending under the Dodd-Frank Act October 2011 Scott D. Samlin Partner T +1 212-398-5819 scott.samlin@snrdenton.com Stephen F. J. Ornstein Partner T +1 202-408-9122

The New Ability-to-Pay Rules; Qualified Mortgage Lending under the Dodd-Frank Act October 2011 Scott D. Samlin Partner T +1 212-398-5819 scott.samlin@snrdenton.com Stephen F. J. Ornstein Partner T +1 202-408-9122

SB 1343. REFERENCE TITLE: home loans; prohibited activities. State of Arizona Senate Forty-fifth Legislature Second Regular Session 2002

PLEASE NOTE: In most BUT NOT ALL instances, the page and line numbering of bills on this web site correspond to the page and line numbering of the official printed version of the bills. REFERENCE TITLE:

PLEASE NOTE: In most BUT NOT ALL instances, the page and line numbering of bills on this web site correspond to the page and line numbering of the official printed version of the bills. REFERENCE TITLE:

PRE-APPLICATION DISCLOSURE AND FEE AGREEMENT FOR USE BY NEW YORK REGISTERED MORTGAGE BROKERS

PRE-APPLICATION DISCLOSURE AND FEE AGREEMENT FOR USE BY NEW YORK REGISTERED MORTGAGE BROKERS THE USE OF THIS FORM IS OPTIONAL. If you use this form properly without alteration, you may assume that you

PRE-APPLICATION DISCLOSURE AND FEE AGREEMENT FOR USE BY NEW YORK REGISTERED MORTGAGE BROKERS THE USE OF THIS FORM IS OPTIONAL. If you use this form properly without alteration, you may assume that you

Q & A with Lykken on Lending Team and Glen Corso

Blog Talk Radio Show July 12, 2010 Q & A with Lykken on Lending Team and Glen Corso General Questions Q: Throughout the MBA analysis of this legislation the term loan originator is used. Sometimes it seems

Blog Talk Radio Show July 12, 2010 Q & A with Lykken on Lending Team and Glen Corso General Questions Q: Throughout the MBA analysis of this legislation the term loan originator is used. Sometimes it seems

Financing Residential Real Estate: SAFE Comprehensive 20 Hours

Financing Residential Real Estate: SAFE Comprehensive 20 Hours COURSE ORGANIZATION and DESIGN Roy L. Ponthier, Ph.D., Ed.D., CDEI, DREI Executive Director Module 1: Finance and Investment Mortgage loans

Financing Residential Real Estate: SAFE Comprehensive 20 Hours COURSE ORGANIZATION and DESIGN Roy L. Ponthier, Ph.D., Ed.D., CDEI, DREI Executive Director Module 1: Finance and Investment Mortgage loans

BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law MEMORANDUM

BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law J. Alton Alsup 10333 Richmond, Suite 860 Telephone 713/468-0400 Board Certified in Residential Real Estate Law Texas Board of Legal Specialization

BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law J. Alton Alsup 10333 Richmond, Suite 860 Telephone 713/468-0400 Board Certified in Residential Real Estate Law Texas Board of Legal Specialization

Using the Services of a Mortgage Broker

WHAT YOU SHOULD KNOW: Using the Services of a Mortgage Broker Real Estate MATTERS DEPARTMENT OF REAL ESTATE August 2011 WHAT YOU SHOULD KNOW: Using the Services of a Mortgage Broker (Revised by the DRE,

WHAT YOU SHOULD KNOW: Using the Services of a Mortgage Broker Real Estate MATTERS DEPARTMENT OF REAL ESTATE August 2011 WHAT YOU SHOULD KNOW: Using the Services of a Mortgage Broker (Revised by the DRE,

Your rights as a borrower

Your rights as a borrower A guide from the Better Business Bureau Protecting your home and the American dream What you need to know about predatory lending Commercials and door-to-door representatives

Your rights as a borrower A guide from the Better Business Bureau Protecting your home and the American dream What you need to know about predatory lending Commercials and door-to-door representatives

Chapter 19. Residential Real Estate Finance: Mortgage Choices, Pricing and Risks. Residential Financing: Loans

Chapter 19 Residential Real Estate Finance: Mortgage Choices, Pricing and Risks 10/25/2005 FIN4777 - Special Topics in Real Estate - Professor Rui Yao 1 Residential Financing: Loans Loans are classified

Chapter 19 Residential Real Estate Finance: Mortgage Choices, Pricing and Risks 10/25/2005 FIN4777 - Special Topics in Real Estate - Professor Rui Yao 1 Residential Financing: Loans Loans are classified

FRESH. Agenda. Credit Union Integrated Mortgage Disclosures Are you Prepared?

MCUL & Affiliates 2015 Annual Convention and Exposition Credit Union Integrated Mortgage Disclosures Are you Prepared? Glory LeDu Thursday, June 4, 2015 2:00 p.m. Sponsored by: FRESH Ideas to Reinvent

MCUL & Affiliates 2015 Annual Convention and Exposition Credit Union Integrated Mortgage Disclosures Are you Prepared? Glory LeDu Thursday, June 4, 2015 2:00 p.m. Sponsored by: FRESH Ideas to Reinvent

MORTGAGE TERMS. Assignment of Mortgage A document used to transfer ownership of a mortgage from one party to another.

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

HOME EQUITY LINES OF CREDIT

HOME EQUITY LINES OF CREDIT WHAT YOU SHOULD KNOW ABOUT HOME EQUITY LINES OF CREDIT: More and more lenders are offering home equity lines of credit. By using the equity in your home, you may qualify for

HOME EQUITY LINES OF CREDIT WHAT YOU SHOULD KNOW ABOUT HOME EQUITY LINES OF CREDIT: More and more lenders are offering home equity lines of credit. By using the equity in your home, you may qualify for

LOAN WORKSHEET #11 NONTRADITIONAL AND SUBPRIME MORTGAGE LENDING

While some institutions have offered nontraditional mortgages for many years with appropriate risk management and sound portfolio performance, the market for these products and the number of institutions

While some institutions have offered nontraditional mortgages for many years with appropriate risk management and sound portfolio performance, the market for these products and the number of institutions

Jim Campen, Senior Fellow, Americans for Fairness in Lending

policy brief #8 Reforming Mortgage Lending Jim Campen, Senior Fellow, Americans for Fairness in Lending October 19, 2009 Abstract: Campen observes that an unprecedented wave of abusive and irresponsible

policy brief #8 Reforming Mortgage Lending Jim Campen, Senior Fellow, Americans for Fairness in Lending October 19, 2009 Abstract: Campen observes that an unprecedented wave of abusive and irresponsible

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2009 SESSION LAW 2009-457 HOUSE BILL 1222

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2009 SESSION LAW 2009-457 HOUSE BILL 1222 AN ACT TO UPDATE THE RATE SPREAD AND HIGH-COST HOME LOANS STATUTES, AND TO MAKE A CONFORMING CHANGE TO THE EMERGENCY

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2009 SESSION LAW 2009-457 HOUSE BILL 1222 AN ACT TO UPDATE THE RATE SPREAD AND HIGH-COST HOME LOANS STATUTES, AND TO MAKE A CONFORMING CHANGE TO THE EMERGENCY

CONTRACT FOR DEED. What Homebuyers and Sellers Need to Know to Achieve a Successful Outcome

CONTRACT FOR DEED What Homebuyers and Sellers Need to Know to Achieve a Successful Outcome Copyright 2012 CONTRACT FOR DEED Is it the right option for me? This publication is intended to provide advice

CONTRACT FOR DEED What Homebuyers and Sellers Need to Know to Achieve a Successful Outcome Copyright 2012 CONTRACT FOR DEED Is it the right option for me? This publication is intended to provide advice

National Mortgage Settlement

National Mortgage Settlement Housing and Land Use Policy Program University of Iowa Public Policy Center Sally Scott, Ph.D. and Jerry Anthony, Ph.D. October 2012 Overview On February 9 of 2012, a bipartisan

National Mortgage Settlement Housing and Land Use Policy Program University of Iowa Public Policy Center Sally Scott, Ph.D. and Jerry Anthony, Ph.D. October 2012 Overview On February 9 of 2012, a bipartisan

Brooklyn Park Economic Development Authority

Brooklyn Park Economic Development Authority Neighborhood Stabilization Program NSP HOMEBUYER ASSISTANCE PROGRAM FOR CITY/PARTNER ACQUISITION AND REHAB Program Description & Guidelines July 2011 TABLE

Brooklyn Park Economic Development Authority Neighborhood Stabilization Program NSP HOMEBUYER ASSISTANCE PROGRAM FOR CITY/PARTNER ACQUISITION AND REHAB Program Description & Guidelines July 2011 TABLE

MORTGAGE DICTIONARY. Amortization - Amortization is a decrease in the value of assets with time, which is normally the useful life of tangible assets.

MORTGAGE DICTIONARY Adjustable-Rate Mortgage An adjustable-rate mortgage (ARM) is a product with a floating or variable rate that adjusts based on some index. Amortization - Amortization is a decrease

MORTGAGE DICTIONARY Adjustable-Rate Mortgage An adjustable-rate mortgage (ARM) is a product with a floating or variable rate that adjusts based on some index. Amortization - Amortization is a decrease

Home Equity Loans and Credit Lines HELOC

Home Equity Loans and Credit Lines HELOC If you re thinking about making some home improvements or looking at ways to pay for your child s college education, you may be thinking about tapping into your

Home Equity Loans and Credit Lines HELOC If you re thinking about making some home improvements or looking at ways to pay for your child s college education, you may be thinking about tapping into your

Mortgage Loans. Understand the Terms of Your Loan Before You Sign...

Mortgage Loans Understand the Terms of Your Loan Before You Sign... This brochure can help you become familiar with basic mortgage loans, determine what terms are best for your situation, and identify

Mortgage Loans Understand the Terms of Your Loan Before You Sign... This brochure can help you become familiar with basic mortgage loans, determine what terms are best for your situation, and identify

The Home Ownership Preservation Initiative in Chicago (HOPI) Reducing Foreclosures through Strategic Partnerships

Reducing Foreclosures through Strategic Partnerships") The Home Ownership Preservation Initiative in Chicago (HOPI) Reducing Foreclosures through Strategic Partnerships Bruce Gottschall, Executive Director Neighborhood Housing Services of Chicago Neighborhood

The Home Ownership Preservation Initiative in Chicago (HOPI) Reducing Foreclosures through Strategic Partnerships Bruce Gottschall, Executive Director Neighborhood Housing Services of Chicago Neighborhood

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Appraiser: a qualified individual who uses his or her experience and knowledge to prepare the appraisal estimate.

Mortgage Glossary 203(b): FHA program which provides mortgage insurance to protect lenders from default; used to finance the purchase of new or existing one- to four family housing; characterized by low

Mortgage Glossary 203(b): FHA program which provides mortgage insurance to protect lenders from default; used to finance the purchase of new or existing one- to four family housing; characterized by low

IOWA DIVISION OF BANKING STATEMENT ON SUBPRIME MORTGAGE LENDING

CHESTER J. CULVER GOVERNOR PATTY JUDGE LT. GOVERNOR THOMAS B. GRONSTAL SUPERINTENDENT IOWA DIVISION OF BANKING STATEMENT ON SUBPRIME MORTGAGE LENDING I. INTRODUCTION AND BACKGROUND On June 29, 2007, the

CHESTER J. CULVER GOVERNOR PATTY JUDGE LT. GOVERNOR THOMAS B. GRONSTAL SUPERINTENDENT IOWA DIVISION OF BANKING STATEMENT ON SUBPRIME MORTGAGE LENDING I. INTRODUCTION AND BACKGROUND On June 29, 2007, the

WOODSTOCK INSTITUTE. Using Research to Limit the Impacts of Foreclosures at the Local Level. Geoff Smith, Vice President Woodstock Institute

WOODSTOCK INSTITUTE Using Research to Limit the Impacts of Foreclosures at the Local Level Geoff Smith, Vice President Woodstock Institute The Subprime Housing Crisis: Interdisiplinary Policy Perspectives

WOODSTOCK INSTITUTE Using Research to Limit the Impacts of Foreclosures at the Local Level Geoff Smith, Vice President Woodstock Institute The Subprime Housing Crisis: Interdisiplinary Policy Perspectives

Residential Mortgage Finance. Early American Mortgages. Early Mortgage Lenders

Residential Mortgage Finance Early American Mortgages Mortgages before the Great Depression Generally were interest only (non- amortizing) loans Had Loan to Value Ratios under 50 % Were short term loans

Residential Mortgage Finance Early American Mortgages Mortgages before the Great Depression Generally were interest only (non- amortizing) loans Had Loan to Value Ratios under 50 % Were short term loans

Be it enacted by the People of the State of Illinois,

SB Enrolled LRB0 EGJ b AN ACT concerning regulation. Be it enacted by the People of the State of Illinois, represented in the General Assembly: Section. The Residential Real Property Disclosure Act is

SB Enrolled LRB0 EGJ b AN ACT concerning regulation. Be it enacted by the People of the State of Illinois, represented in the General Assembly: Section. The Residential Real Property Disclosure Act is

The Massachusetts Attorney General s. Guide to Consumer Credit

The Massachusetts Attorney General s Guide to Consumer Credit June 2014 Table of Contents A Note from the Attorney General 3 Truth In Lending 4 Billing Rights 7 Costs of Credit 9 Fair Credit Reporting

The Massachusetts Attorney General s Guide to Consumer Credit June 2014 Table of Contents A Note from the Attorney General 3 Truth In Lending 4 Billing Rights 7 Costs of Credit 9 Fair Credit Reporting

PURCHASE MORTGAGE. Mortgage loan types

PURCHASE MORTGAGE Mortgage loan types There are many types of mortgages used worldwide, but several factors broadly define the characteristics of the mortgage. All of these may be subject to local regulation

PURCHASE MORTGAGE Mortgage loan types There are many types of mortgages used worldwide, but several factors broadly define the characteristics of the mortgage. All of these may be subject to local regulation

Loan Foreclosure Analysis and Comparison. A Briefing To The Housing Committee March 3, 2008

Loan Foreclosure Analysis and Comparison A Briefing To The Housing Committee March 3, 2008 Purpose To determine the cause of the Subprime mortgage crisis which was triggered by a sharp rise in home foreclosures

Loan Foreclosure Analysis and Comparison A Briefing To The Housing Committee March 3, 2008 Purpose To determine the cause of the Subprime mortgage crisis which was triggered by a sharp rise in home foreclosures

STATE OF MICHIGAN IN THE CIRCUIT COURT FOR THE COUNTY OF WAYNE

STATE OF MICHIGAN IN THE CIRCUIT COURT FOR THE COUNTY OF WAYNE HARRY O. LUTZ AND PAULA G. LUTZ; Hon. Case No. v ONE WEST, a successor in interest to INDYMAC BANK, F.S.B.; TITLE SOURCE, INC.; THE MORTGAGE

STATE OF MICHIGAN IN THE CIRCUIT COURT FOR THE COUNTY OF WAYNE HARRY O. LUTZ AND PAULA G. LUTZ; Hon. Case No. v ONE WEST, a successor in interest to INDYMAC BANK, F.S.B.; TITLE SOURCE, INC.; THE MORTGAGE

Agencies and Resources

The following local, state and federal agencies administer programs or provide funds for housing programs and projects: Murray County EDA P.O. Box 57 Slayton, MN 56172 Contact: Amy Hoglin, Economic Development

The following local, state and federal agencies administer programs or provide funds for housing programs and projects: Murray County EDA P.O. Box 57 Slayton, MN 56172 Contact: Amy Hoglin, Economic Development

Title 9-A: MAINE CONSUMER CREDIT CODE

Maine Revised Statutes Title 9-A: MAINE CONSUMER CREDIT CODE Article : 8-506. ENHANCED RESTRICTIONS ON CERTAIN CREDITORS In addition to the compliance requirements of section 8-504, subsection 1, unless

Maine Revised Statutes Title 9-A: MAINE CONSUMER CREDIT CODE Article : 8-506. ENHANCED RESTRICTIONS ON CERTAIN CREDITORS In addition to the compliance requirements of section 8-504, subsection 1, unless

Senate Bill 1149 Summary -- Prohibit Predatory Lending

MEMORANDUM TO: FROM: Hal D. Lingerfelt Commissioner of Banks L. McNeil Chestnut Assistant Attorney General DATE: August 25, 1999 RE: Senate Bill 1149 Summary -- Prohibit Predatory Lending I. Background

MEMORANDUM TO: FROM: Hal D. Lingerfelt Commissioner of Banks L. McNeil Chestnut Assistant Attorney General DATE: August 25, 1999 RE: Senate Bill 1149 Summary -- Prohibit Predatory Lending I. Background

Home Equity Lines of Credit

The Federal Reserve Board What you should know about Home Equity Lines of Credit Board of Governors of the Federal Reserve System www.federalreserve.gov 0708 i What You Should Know about Home Equity Lines

The Federal Reserve Board What you should know about Home Equity Lines of Credit Board of Governors of the Federal Reserve System www.federalreserve.gov 0708 i What You Should Know about Home Equity Lines

Chapter 10 6/16/2010. Mortgage Types and Borrower Decisions: Overview Role of the secondary market. Mortgage types:

Mortgage Types and Borrower Decisions: Overview Role of the secondary market Chapter 10 Residential Mortgage Types and Borrower Decisions Mortgage types: Conventional mortgages FHA mortgages VA mortgages

Mortgage Types and Borrower Decisions: Overview Role of the secondary market Chapter 10 Residential Mortgage Types and Borrower Decisions Mortgage types: Conventional mortgages FHA mortgages VA mortgages

BILL ANALYSIS. Senate Research Center S.B. 173 By: Patterson State Affairs 3-24-97 Committee Report (Amended)

") BILL ANALYSIS Senate Research Center S.B. 173 By: Patterson State Affairs 3-24-97 Committee Report (Amended) DIGEST Currently, the Texas Constitution prohibits the use of equity in a home for collateral

BILL ANALYSIS Senate Research Center S.B. 173 By: Patterson State Affairs 3-24-97 Committee Report (Amended) DIGEST Currently, the Texas Constitution prohibits the use of equity in a home for collateral

Professor Chris Mayer (Columbia Business School; NBER; Visiting Scholar, Federal Reserve Bank of New York)

") Professor Chris Mayer (Columbia Business School; NBER; Visiting Scholar, Federal Reserve Bank of New York) Lessons Learned from the Crisis: Housing, Subprime Mortgages, and Securitization THE PAUL MILSTEIN

Professor Chris Mayer (Columbia Business School; NBER; Visiting Scholar, Federal Reserve Bank of New York) Lessons Learned from the Crisis: Housing, Subprime Mortgages, and Securitization THE PAUL MILSTEIN

First Time Home Buyer Glossary

First Time Home Buyer Glossary For first time home buyers, knowing and understanding the following terms are very important when purchasing your first home. By understanding these terms, you will make

First Time Home Buyer Glossary For first time home buyers, knowing and understanding the following terms are very important when purchasing your first home. By understanding these terms, you will make

CHAPTER 10: LEVERAGED LOANS SECTION 1: UNDERSTANDING LEVERAGED LOANS

CHAPTER 10: LEVERAGED LOANS SECTION 1: UNDERSTANDING LEVERAGED LOANS 10.1 OVERVIEW A leveraged loan is an Agency loan that is supplemented by an affordable housing loan or grant from another funding source

CHAPTER 10: LEVERAGED LOANS SECTION 1: UNDERSTANDING LEVERAGED LOANS 10.1 OVERVIEW A leveraged loan is an Agency loan that is supplemented by an affordable housing loan or grant from another funding source

CONSUMER GROUPS: FIX BANKRUPTCY LAWS SO HUNDREDS OF THOUSANDS OF AMERICANS CAN AVOID HOME FORECLOSURES IN SUBPRIME MORTGAGE CRISIS

CONSUMER GROUPS: FIX BANKRUPTCY LAWS SO HUNDREDS OF THOUSANDS OF AMERICANS CAN AVOID HOME FORECLOSURES IN SUBPRIME MORTGAGE CRISIS 81 Percent of Bankruptcy Attorneys Say It s Now Tougher for Clients to

CONSUMER GROUPS: FIX BANKRUPTCY LAWS SO HUNDREDS OF THOUSANDS OF AMERICANS CAN AVOID HOME FORECLOSURES IN SUBPRIME MORTGAGE CRISIS 81 Percent of Bankruptcy Attorneys Say It s Now Tougher for Clients to