MS #5457 TAXES, ORGANIZATIONAL FORM, AND THE DEAD WEIGHT LOSS OF THE CORPORATE INCOME TAX. Austan Goolsbee University of Chicago

|

|

|

- Octavia Weaver

- 8 years ago

- Views:

Transcription

1 MS #5457 TAXES, ORGANIZATIONAL FORM, AND THE DEAD WEIGHT LOSS OF THE CORPORATE INCOME TAX Austan Goolsbee University of Chicago ABSTRACT Corporate taxation can play an important role in a firm's choice of organizational form by changing the relative attractiveness of incorporating. Recent general equilibrium models have shown that with substantial shifting between corporate and noncorporate activity in response to taxation, the dead weight loss of the corporate income tax can be very high. This paper tests the empirical importance of this idea by estimating the impact of taxes on the noncorporate share of capital for various sectors using data from a period of large and frequent changes in both corporate and personal tax rates. The results indicate that taxes do matter for organizational form decisions but the magnitude of the effect is small. An increase in the corporate rate of.10 raises the noncorporate share of capital between.2 and 3 percentage points. At this magnitude, the dead weight loss of the corporate income tax is less than 10% of revenue. JEL Classification: Keywords: H25 Business Taxes L22 Firm Organization and Market Structure Corporate Taxation, Organizational Form, Taxation, Dead Weight Loss Austan Goolsbee, University of Chicago, GSB, 1101 E. 58th St., Chicago, IL Phone: (773) Fax: (773) goolsbee@gsb.uchicago.edu. 1

2 1. Introduction Partly in response to rate changes of the last fifteen years, new interest has emerged in the interaction between the tax system and the organizational form decisions of firms. An early discussion can be found in Feldstein and Slemrod (1980). Scholes and Wolfson (1990, 1991, 1992) show how tax rates changed incentives for various types of organizational restructuring. Gordon and Mackie-Mason (1990, 1994, 1997) look at the role of tax decisions and how large the nontax benefits of incorporation must be given the observed incorporation rates. Other work includes Ayers et al. (1995), Carrol and Joulfaian (1995), Gentry (1994) and Fullerton and Rogers (1993). Gravelle and Kotlikoff (1988, 1989, 1993) merge the analysis of organizational form with the study of the dead weight loss (DWL) of corporate taxation. Their simulations differ from standard work, like Harberger (1966), Shoven (1976) or Ballard et al. (1985), by allowing both corporate and noncorporate production within sector. In conventional models, one sector is corporate and the other not and the implied dead weight losses amount to 10-20% of tax revenue. Gravelle and Kotlikoff, by assuming a large elasticity of substitution within sector, find DWL greater than 100% of tax revenue. The critical issue in both strands of the literature is, empirically, the organizational form response to tax changes. Gordon and Mackie-Mason (1991) use the share of capital in C corporations since 1957 as a function of the relative taxation of corporate to personal taxation and find evidence of only small substitution across organizational forms. The results, however, do not completely refute the Gravelle and Kotlikof hypothesis: shifting due to corporate taxation because corporate taxes have changed little since Variation in relative taxation comes mainly from changes in personal 2

, Carrol and Joulfaian (1995), Gentry (1994) and Fullerton and Rogers (1993).")

3 taxes. This paper follows up on the work of Gordon and Mackie-Mason but with data from During this period the corporate tax rate changed repeatedly, as did the personal, dividend and capital gains rates. The obvious disadvantages are that the period may not be comparable to the present. At the least, there were fewer organizational choices (there were no S corporations, LLCs and so on). The results show that, although significant, taxes have only a small impact on organization form. A.10 increase in the corporate tax increases the noncorporate share of capital by only depending on the sector--much smaller than implied in the Gravelle and Kotlikof models and very close to the estimates of Gordon and Mackie-Mason for Shifting this magnitude implies a DWL from corporate income taxation on the order of 5-10% of tax revenue. The paper is divided into four sections. Section 1 presents historical background and describes the data. Section 2 gives a simple model of the organizational form decision based on the relative taxation of corporate and personal income and also presents the empirical specification. Section 3 gives the results for the various sectors, calculates the DWL of the tax, estimates the long- versus short-run impact of taxation and illustrates the impact for firms with and without taxable income. Section 4 concludes. 1. BACKGROUND AND DATA A. CORPORATIONS Following rapid industrialization in the U.S., the corporate form was widespread by the 3

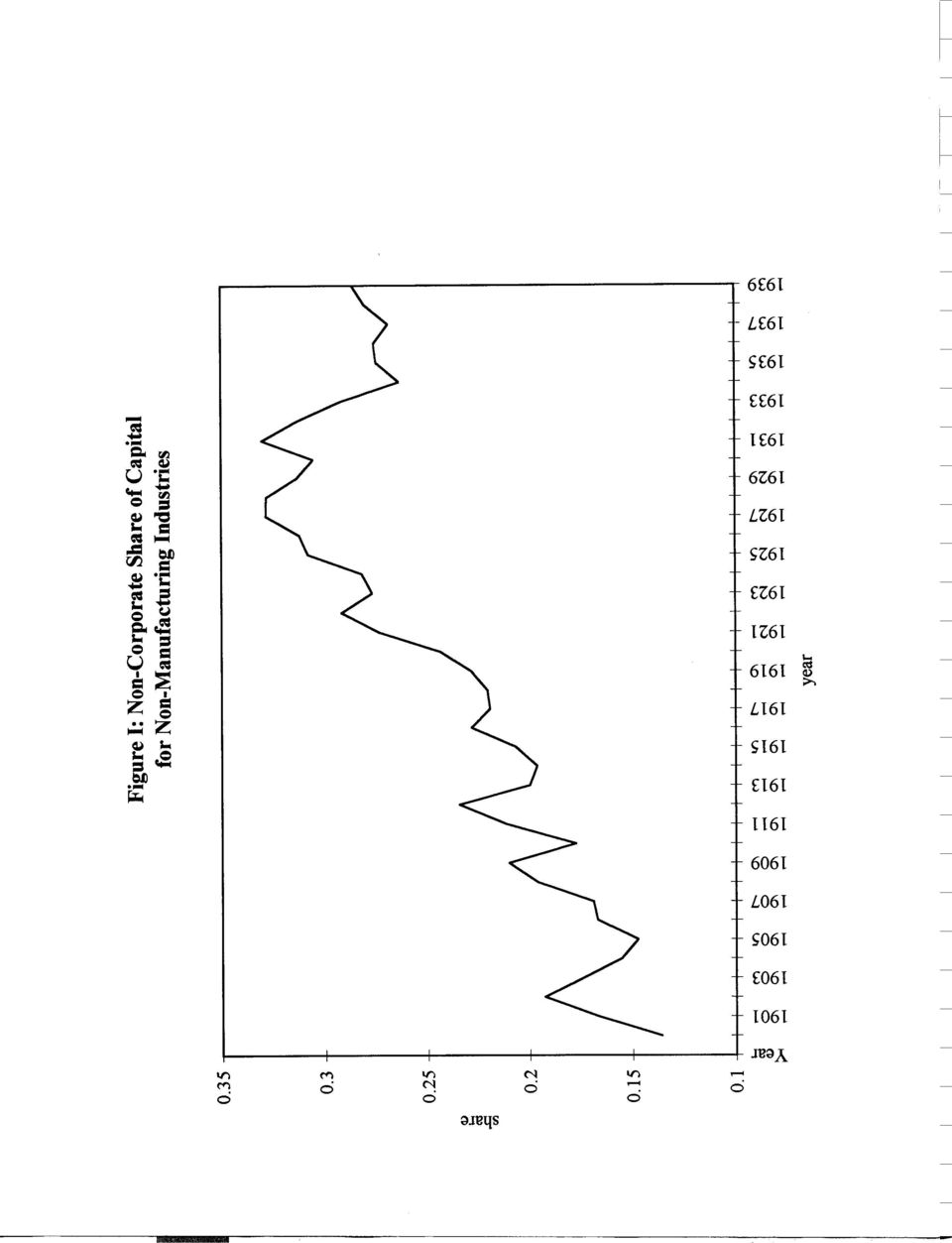

4 1 turn of the century. There are two major advantages to incorporation. First, corporations can issue public shares. Second, corporations have limited liability. These benefits help explain why the majority of business activity is done by corporations despite the corporate tax penalty. Given the data, though, it is impossible to account for these nontax benefits empirically so I follow Gordon and Mackie-Mason and assume that the nontax benefits of corporate status do not covary systematically with the time series changes in taxes. The sample begins before the corporate income tax started, giving a further control on the importance of the nontax factors. The data on the capital stock by organizational form are published by the Bureau of Economic Affairs in U.S. Department of Commerce (1987) and are available for the 2 manufacturing, non-manufacturing, and agricultural sectors. A graph of the noncorporate share in manufacturing is presented in Figure 1 as an illustration. B. TAXATION The U.S. instituted the first corporate income tax of 1% in 1909 and the first personal income tax in The basic structure of the personal income tax was a "normal" tax paid on all income above the standard deduction and then "surtaxes" whose marginal rates rose with income, often quite rapidly. These rates are compiled in various Statistics of Income from (U.S. Department of Treasury, various years). Corporate and personal taxes remained low until WWI when congress raised the corporate rate to 6% and then 12%. Personal rates rose as well and there were excess profits 1 The early history of corporations is in Whitten (1983) and Sklar (1988). 2 The BEA compiles the stock from investment data using the perpetual inventory method. A complete description of the BEA methods is presented in the introduction to U.S. Department of Commerce (1987). 4

5 taxes. The corporate tax remained around 12% until well into the depression. On the personal side, rates on high income tax payers were high until the 1920s and then fell as part of Treasury Secretary Mellon's plan. Following this, from 1924 to 1931, there were small rate changes on the corporate side while the personal rates remained unchanged. By 1932, depression-era concern over income distribution led to big increases in the top personal tax rates but not the corporate rates. Figure 2 shows the corporate income tax rate (listed in Pechman, 1987) and the personal marginal tax rate for an individual with $30,000 of real (1917) income (approximately the top decile of tax filers in 1917). The changes in relative taxation are clear, though not extreme. I use $30,000 rather than the maximum personal rate, as commonly used for current data, because in this period, the top bracket was extremely progressive. In 1918, for example, only four filers qualified for the top marginal rate. Further, people earning $30,000 or more received approximately 90% of dividend payouts so this seemed like a reasonable choice for the marginal 3 investor. The choice of personal did not, however, make much difference to the results. As for equity taxes, laws changed several times between 1909 and Dividends were 4 consistently taxed at the surtax rate. Capital gains were taxed as regular income until After 1921, taxpayers could choose either their own personal tax rate or a rate of.125. During the period , the rate on capital gains was the full personal rate but with a 70% exclusion 3 Using tax rates assuming $20,000, $50,000, or $100,000 in income gave almost identical or even smaller results. It is not possible to use the tax rate for the top decile of taxpayers over time because of changes to exemption levels. 4 The Supreme Court occasionally declared that a "true stock dividend" should not be taxable income to shareholders so it is unclear how many people acutally paid such taxes. Results assuming no equity taxation, however, were basically the same. 5

6 for long-term gains. From , the exclusion fell to 50%. To calculate a single rate for equity, t, I use the equation e t e ' s d t d % (1!s d )("t cg, (1) where s is the share of gains distributed as dividends, " is the taxable share of long-term gains d and ( is a factor to account for capital gains deferral and for basis step up at death. The Statistics of Income from indicate that the ratio of dividends to capital gains was roughly two to one so I assume s = 2/3. Feldstein, Dicks-Mireaux and Poterba (1983) estimate ( to be.25 using d modern data. It is not clear that this parameter is valid for this earlier period but it has little impact on the results. The key point for the sample is that, although most of the changes were small, there were 14 corporate tax changes, 12 personal changes and at least three major changes on capital gains. 2. THEORY, DATA AND SPECIFICATION A. A SIMPLE THEORY OF INCORPORATION I present a stylized model of the firm's decision about whether to incorporate, following Gordon and Mackie-Mason (1991). Assume, for simplicity, that the income generated by a firm, Y, is the same regardless of organization type and that there is some relative nontax benefit G associated with being a corporation. Since this could be something like the value of limited liability, it would be more realistic to model G as a function of characteristics of the firm but there are no firm level data so I assume that it is the same for all firms within an industry and is not taxed. The after-tax income from operating as a corporation each period is then 6

estimate ( to be.25 using d modern data. It is not clear that this parameter is valid for this earlier period but it has little impact on the results.")

7 I c ' G%Y(1!t c!(1!t c )t e ), (2) where t is the tax rate on equity income. That is, a firm gets G plus income net of corporate and e equity taxes. A noncorporate firm gains no G but pays only personal taxes leaving it income I n ' Y(1!t p ). (3) The firm will prefer to incorporate when G > Y(t c %(1!t c )t e!t p ). (4) Equation (3) shows that it is the relative taxation of corporate versus personal income that determines the incentive to incorporate. It also implies that the direction of the incentive will depend on whether taxable income is greater than zero. B. SPECIFICATION Motivated by (3), the relative tax term (t + (1! t )t! t ) should empirically influence the c c e p organizational form decision and the noncorporate share of capital within a sector. The basic specification to be estimated is S it ' " i % ( i tax it % $ i1 (time) % $ i2 (time) 2 %$ i3 GNP t %, it, (5) where S it is the noncorporate share of capital for sector I in time t. Tax it is the relative tax term listed on the right hand side of equation (3) and GNP is the GNP growth rate. The coefficient on the tax term should be positive implying that higher relative taxation of corporations leads to more noncorporate activity. The time trends account for changing value of nontax benefits or 7

Equation (3) shows that it is the relative taxation of corporate versus personal income that determines the incentive to incorporate.")

8 5 other trends. This is the same equation estimated in Gordon and Mackie-Mason but with 6 controls for GNP growth. To calculate the tax term, I use the maximum corporate tax rate listed in Pechman (1987) for t. A previous version of this paper used the corporate rate including war and excess profits c taxes and the results were very similar. 3. RESULTS A. BASIC RESULTS The standard specification for the noncorporate share of capital is as follows for manufacturing (time and time squared are divided by 100 for ease of presentation): 2 NC t = * TAX * t * t * (GNP GROWTH) 2 (.001) (.015) (.014) (.0003) (.0053) R =.79 The coefficient on taxes indicates that raising the corporate rate significantly increases the noncorporate share of capital but the magnitude is small. An increase in the corporate income tax of.10 increases the noncorporate share of capital around.003. The tax coefficient from this specification for each of the three sectors is listed in column (1) of Table 1. All indicate effects that are significant but small. A.10 corporate tax increase raises the noncorporate share of nonmanufacturing by.035 and of farming by.002. These regressions include GNP growth to deal with the Great Depression. Column (2) shows that restricting the sample to pre-1929 does not 5 The value of the insurance associated with limited liability grows with the likelihood of bankruptcy. Since the Great Depression comes at the end of the sample, the value of G is likely to be increasing in these data. 6 Including other macroeconomic variables such as the unemployment rate or the interest rate had no impact on the estimated tax results that follow so they are left our for simplicity. 8

: 2 NC t =.071 +.")

9 increase the estimates. A.10 corporate increase raises the noncorporate share Gordon and Mackie-Mason, using data on the share of assets held by C corporations, get coefficients of very similar to the coefficients here. They have also shown that the Gravelle and Kotlikof model predicts that a.45 corporate tax should increase the noncorporate capital share by.63. Depending on the specification, applying the results in this paper suggests shifts 5 and 50 times smaller per unit. B. LONG-RUN EFFECTS With fixed costs to changing organizational form, temporary tax changes will have smaller effects than permanent ones. Since taxes changed frequently in this sample, this could explain the low estimates. To examine this, Table 2 includes lags and leads of tax policy in the regressions. Unfortunately, the variability of the relative tax term means that identifying permanent effects is difficult. The individual coefficients are imprecisely estimated as seen in the manufacturing regression (time, time squared and GNP growth are not reported): NC = (tax ) (tax ) (tax ) (tax ) (tax ) t t+1 t t+1 t+2 t+3 (.001)(.023) (.035) (.034) (.033) (.029) The point estimates indicate that anticipated increases to the corporate rate reduce the noncorporate share today followed by gradual increases upon passage. The sum of the coefficients for the contemporaneous tax change and then the sum of all the tax coefficients are reported for each sector in Table 2. The p-value is for an F-test of whether the sum equals zero. For manufacturing and farming, the impact of tax changes after three years is larger than in the contemporaneous period. For nonmanufacturing the sum is, oddly, smaller in the long run. 9

10 In each of the specifications, however, the long-run effects are still small. C. DEAD WEIGHT LOSS We can approximate the excess burden in an industry arising from the corporate tax by -.5*TAX *)K, where )K is the change in the noncorporate share of capital induced by i ni ni eliminating corporate taxation and TAX is the relative tax term. Doing this using the coefficients above, the long-run DWL is approximately 3-5% of revenue rather than the 110% in Gravelle and 7 Kotlikof. Even using the largest estimates of form shifting for each sector, the DWL is less than 3% for manufacturing and agriculture and 15% for nonmanufacturing. D. TAXABLE GAINS AND LOSSES The theory indicates that the impact of tax rates should depend on the income status of firms. When the corporate rate rises, firms have an incentive to get taxable gains out of corporate form. There are no good data to explore this issue for as there are very little data on noncorporate firms. There are data from , though, on the share of corporate returns with taxable income. When the relative taxation of corporate income rises, there should be shifting to the noncorporate sector but it should be concentrated among firms with taxable income. The remaining corporate sector should then have a higher share of firms with no taxable income. 7 Two reasons the DWL is so large in Gravelle and Kotlikof (1993) are (1) they use the full corporate rate as the tax distortion rather than the smaller, relative tax term and (2) they assume that corporate and noncorporate firms produce slightly different products and that the elasticity of substitution between the two is 30. A previous version of this paper, available on request, structurally estimated the Gravelle and Kotlikof model and estimated this elasticity to be less than 2 (implying less shifting and smaller DWL). 10

11 The share of corporate returns reporting no taxable income depends critically on the macro economy, so I estimated regressions including as control variables the GNP growth rate, the real level of GNP and the real interest rate (the commercial paper rate minus the rate of inflation) and sometimes restricted the sample to before the depression. The coefficients were significant or borderline significant and ranged from -.5 to -.9, indicating that increasing the corporate tax by.10 reduces the fraction of corporate returns reporting taxable income by , substantially larger than the estimated impacts on capital. 4. CONCLUSIONS This paper has presented evidence on the question of how tax rates affect the decision to incorporate. The evidence indicates that taxes played a statistically significant role in organizational form decisions from but the magnitude was quite small. A.10 increase in the corporate income tax increases the noncorporate share of capital by for farming and manufacturing and for nonmanufacturing; the magnitudes do not appear to be much larger in the long run. There is also evidence that firms with taxable income are more responsive to changes in the corporate rate than those without taxable income--as the theory would predict. Overall, these small effects on organizational form imply that the excess burden from the corporate income tax is around 5% and not more than 100% as calculated in Gravelle and Kotlikoff (1993) and likely mean that issues of organizational form are not of first-order importance in discussions about corporate income taxation. 11

12 I wish to thank Josh Angrist, Chip Case, Roger Gordon, Jerry Hausman, Steve Levitt, Jack Porter, Jim Poterba and participants in the NBER Summer Institute for helpful comments and to thank the National Science Foundation for financial support. 12

13 References Ayers, B., C. Cloyd, and J. Robinson, 1995, Organizational form and taxes: an empirical analysis of small businesses (Austin: University of Texas, mimeograph). Ballard, C., J. Shoven, and J. Whalley, 1985, The total welfare cost of the United States tax system: A general equilibrium approach, National Tax Journal 38, Congressional Record, 1894, June 27, 26:6888 Feldstein, M., J. Dicks-Mireaux, and J. Poterba, 1983, The Effective tax rate and the pretax rate of return, Journal of Public Economics 21, Feldstein, M., and J. Slemrod, 1980, Personal Taxation, portfolio choice, and the effect of the corporate income tax, Journal of Political Economy 21, Fullerton, D., and D. Rogers, 1993, Who bears the lifetime tax burden. (Brookings, Washington D.C.). Gentry, W., 1994, Taxes, financial decisions and organizational form: evidence from publicly traded partnerships Journal of Public Economics 33, Gordon, R., and J. Mackie-Mason, 1990, Effects of the tax reform act of 1986 on corporate financial policy and organizational form, in: J. Slemrod, ed., Do taxes matter (MIT Press, Cambridge, MA), Gordon, R., and J. Mackie-Mason, 1991, Taxes and the choice of organizational form, NBER Working Paper #3781. Gordon, R., and J. Mackie-Mason, 1994, Tax distortions to the choice of organizational form, Journal of Public Economics 55, Gravelle, J., and L. Kotlikoff, 1988, Does the Harberger model greatly understate the excess 13

14 burden of the corporate income tax? NBER Working Paper # Gravelle, J., and L. Kotlikoff, 1989, The incidence and efficiency costs of corporate taxation when corporate and noncorporate firms produce the same good, Journal of Political Economy 97, Gravelle, J., and L. Kotlikoff, 1993, Corporate tax incidence and inefficiency when corporate and noncorporate goods are close substitutes, Economic Inquiry, vol #, pp Harberger, A., 1966, Efficiency effects of taxes on income from capital, in: M. Krzyzaniak, Effects of the corporation income tax. (Wayne State University Press, Detroit, MI), Pechman, J., 1987, Federal tax policy, 5th ed. (Brookings, Washington D.C.). Ratner, S., 1967, Taxation and democracy in America (John Wiley and Sons, New York). Scholes, M., and M. Wolfson, 1990, The effects of changes in tax laws on corporate reorganization activity, Journal of Business 63, S141-S164. Scholes, M., and M. Wolfson, 1991, The role of tax rules in the recent restructuring of U.S. corporations, in: D. Bradford ed. Tax policy and the economy v 5 (Publisher, City), Scholes, M., and M. Wolfson, 1992, Taxes and business strategy: A planning approach. (Prentice-Hall, Englewood Cliffs, NJ). Shoven, J., 1976, The incidence and efficiency effects of taxes on income from capital, Journal of Political Economy #, Sklar, M., 1988, The corporate reconstruction of american capitalism, (Cambridge University Press, Cambridge). United States Department of Commerce, 1987, Fixed reproducible tangible wealth in the united 14

, 107-117. Pechman, J.")

15 states (U.S. Government Printing Office, Washington, D.C.).. United States Department of the Treasury, , Statistics of income: Corporate income tax returns (U.S. Government Printing Office, Washington, D.C.). Whitten, D., 1983, The emergence of giant enterprise, Greenwood Press, Westport, CT). 15

16 TABLE 1: TAX COEFFICIENTS FOR SHARE OF CAPITAL IN NON-CORPORATE FORM (1) (2) Manufacturing (.0152) (.0145) Nonmanufacturing (.1521) (.1103) Farming (.0094) (.0103) 16

Nonmanufacturing.3567.1615 (.1521) (.")

17 TABLE 2: SUM OF THE TAX COEFFICIENTS IN LONG-RUN REGRESSIONS (1) J 30Kr+e Contemp Three Years Manufacturing F-test (p-value) Nonmanufacturing F-test (p-value) Farms F-test (p-value) Notes: The dependent variable in each case if the share of noncorporate to total capital. Each entry is the sum of the coefficients on the tax terms of various lag lengths, as described in the paper. The first column sums the contemporaneous and one lead coefficients while the second column adds coefficients from one, two and three lags. The sample is The p-value listed is from an F-test that the sum of the coefficients is equal to zero. 17

18

19

Notes and References

1. meet the federal income tax The Declaration of Independence is on display in the main lobby of the National Archives in Washington, D.C. Standard sources of tax forms, laws, and regulations include

1. meet the federal income tax The Declaration of Independence is on display in the main lobby of the National Archives in Washington, D.C. Standard sources of tax forms, laws, and regulations include

Corporate Taxation. James R. Hines Jr. University of Michigan and NBER

Corporate Taxation by James R. Hines Jr. University of Michigan and NBER February, 2001 This paper is prepared as an entry in the International Encyclopedia of the Social and Behavioral Sciences. Corporate

Corporate Taxation by James R. Hines Jr. University of Michigan and NBER February, 2001 This paper is prepared as an entry in the International Encyclopedia of the Social and Behavioral Sciences. Corporate

MACROECONOMIC ANALYSIS OF VARIOUS PROPOSALS TO PROVIDE $500 BILLION IN TAX RELIEF

MACROECONOMIC ANALYSIS OF VARIOUS PROPOSALS TO PROVIDE $500 BILLION IN TAX RELIEF Prepared by the Staff of the JOINT COMMITTEE ON TAXATION March 1, 2005 JCX-4-05 CONTENTS INTRODUCTION... 1 EXECUTIVE SUMMARY...

MACROECONOMIC ANALYSIS OF VARIOUS PROPOSALS TO PROVIDE $500 BILLION IN TAX RELIEF Prepared by the Staff of the JOINT COMMITTEE ON TAXATION March 1, 2005 JCX-4-05 CONTENTS INTRODUCTION... 1 EXECUTIVE SUMMARY...

Capital Gains Taxes: An Overview

Order Code 96-769 Updated January 24, 2007 Summary Capital Gains Taxes: An Overview Jane G. Gravelle Senior Specialist in Economic Policy Government and Finance Division Tax legislation in 1997 reduced

Order Code 96-769 Updated January 24, 2007 Summary Capital Gains Taxes: An Overview Jane G. Gravelle Senior Specialist in Economic Policy Government and Finance Division Tax legislation in 1997 reduced

How Elastic is the Corporate Income Tax Base?

How Elastic is the Corporate Income Tax Base? Jonathan Gruber, MIT and NBER Joshua Rauh, University of Chicago and NBER June 2005 Presented at Taxing Corporate Income in the 21 st Century, May 5-6, 2005.

How Elastic is the Corporate Income Tax Base? Jonathan Gruber, MIT and NBER Joshua Rauh, University of Chicago and NBER June 2005 Presented at Taxing Corporate Income in the 21 st Century, May 5-6, 2005.

The 2001 and 2003 Tax Relief: The Benefit of Lower Tax Rates

FISCAL Au 2008 No. 141 FACT The 2001 and 2003 Tax Relief: The Benefit of Lower Tax Rates By Robert Carroll Summary Recent research on President Bush's tax relief in 2001 and 2003 has found that the lower

FISCAL Au 2008 No. 141 FACT The 2001 and 2003 Tax Relief: The Benefit of Lower Tax Rates By Robert Carroll Summary Recent research on President Bush's tax relief in 2001 and 2003 has found that the lower

THE FEDERAL REVENUE EFFECTS OF TAX-EXEMPT AND DIRECT-PAY TAX CREDIT BOND PROVISIONS

THE FEDERAL REVENUE EFFECTS OF TAX-EXEMPT AND DIRECT-PAY TAX CREDIT BOND PROVISIONS Prepared by the Staff of the JOINT COMMITTEE ON TAXATION July 16, 2012 JCX-60-12 CONTENTS INTRODUCTION... 1 I. ESTIMATING

THE FEDERAL REVENUE EFFECTS OF TAX-EXEMPT AND DIRECT-PAY TAX CREDIT BOND PROVISIONS Prepared by the Staff of the JOINT COMMITTEE ON TAXATION July 16, 2012 JCX-60-12 CONTENTS INTRODUCTION... 1 I. ESTIMATING

The recent proposal by the Bush Administration to eliminate

The Effect of Dividend Tax Relief on Investment Incentives The Effect of Dividend Tax Relief on Investment Incentives Abstract - Reducing the double tax on corporate income has an ambiguous effect on marginal

The Effect of Dividend Tax Relief on Investment Incentives The Effect of Dividend Tax Relief on Investment Incentives Abstract - Reducing the double tax on corporate income has an ambiguous effect on marginal

TAX REDUCTION AND ECONOMIC WELFARE

TAX REDUCTION AND ECONOMIC WELFARE by Richard K. Vedder and Lowell E. Gallaway Distinguished Professors of Economics, Ohio University Prepared for the Joint Economic Committee Vice Chairman Jim Saxton

TAX REDUCTION AND ECONOMIC WELFARE by Richard K. Vedder and Lowell E. Gallaway Distinguished Professors of Economics, Ohio University Prepared for the Joint Economic Committee Vice Chairman Jim Saxton

What do Aggregate Consumption Euler Equations Say about the Capital Income Tax Burden? *

What do Aggregate Consumption Euler Equations Say about the Capital Income Tax Burden? * by Casey B. Mulligan University of Chicago and NBER January 2004 Abstract Aggregate consumption Euler equations

What do Aggregate Consumption Euler Equations Say about the Capital Income Tax Burden? * by Casey B. Mulligan University of Chicago and NBER January 2004 Abstract Aggregate consumption Euler equations

Effective Federal Income Tax Rates Faced By Small Businesses in the United States

Effective Federal Income Tax Rates Faced By Small Businesses in the United States by Quantria Strategies, LLC Cheverly, MD 20785 for Under contract number SBAHQ-07-Q-0012 Release Date: April 2009 This

Effective Federal Income Tax Rates Faced By Small Businesses in the United States by Quantria Strategies, LLC Cheverly, MD 20785 for Under contract number SBAHQ-07-Q-0012 Release Date: April 2009 This

Chapter URL: http://www.nber.org/chapters/c7726

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Taxing Multinational Corporations Volume Author/Editor: Martin Feldstein, James R. Hines

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Taxing Multinational Corporations Volume Author/Editor: Martin Feldstein, James R. Hines

DISTRIBUTING THE CORPORATE INCOME TAX: REVISED U.S. TREASURY METHODOLOGY

National Tax Journal, March 2013, 66 (1), 239 262 DISTRIBUTING THE CORPORATE INCOME TAX: REVISED U.S. TREASURY METHODOLOGY Julie Anne Cronin, Emily Y. Lin, Laura Power, and Michael Cooper The purpose of

National Tax Journal, March 2013, 66 (1), 239 262 DISTRIBUTING THE CORPORATE INCOME TAX: REVISED U.S. TREASURY METHODOLOGY Julie Anne Cronin, Emily Y. Lin, Laura Power, and Michael Cooper The purpose of

Volume Title: Tax Policy and the Economy, Volume 6. Volume Author/Editor: James M. Poterba, editor. Volume URL: http://www.nber.

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Tax Policy and the Economy, Volume 6 Volume Author/Editor: James M. Poterba, editor Volume

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Tax Policy and the Economy, Volume 6 Volume Author/Editor: James M. Poterba, editor Volume

The Elasticity of Taxable Income: A Non-Technical Summary

The Elasticity of Taxable Income: A Non-Technical Summary John Creedy The University of Melbourne Abstract This paper provides a non-technical summary of the concept of the elasticity of taxable income,

The Elasticity of Taxable Income: A Non-Technical Summary John Creedy The University of Melbourne Abstract This paper provides a non-technical summary of the concept of the elasticity of taxable income,

HOW BIG SHOULD GOVERNMENT BE? MARTIN FELDSTEIN *

HOW BIG SHOULD GOVERNMENT BE? MARTIN FELDSTEIN * * Economics Department, Harvard University, and National Bureau of Economic Research, Cambridge, MA 02138. Abstract - The appropriate size and role of government

HOW BIG SHOULD GOVERNMENT BE? MARTIN FELDSTEIN * * Economics Department, Harvard University, and National Bureau of Economic Research, Cambridge, MA 02138. Abstract - The appropriate size and role of government

How To Find Out How Effective Stimulus Is

Do Tax Cuts Boost the Economy? David Rosnick and Dean Baker September 2011 Center for Economic and Policy Research 1611 Connecticut Avenue, NW, Suite 400 Washington, D.C. 20009 202-293-5380 www.cepr.net

Do Tax Cuts Boost the Economy? David Rosnick and Dean Baker September 2011 Center for Economic and Policy Research 1611 Connecticut Avenue, NW, Suite 400 Washington, D.C. 20009 202-293-5380 www.cepr.net

The Role of Taxes in Organizational Choice: S Conversions After the Tax Reform Act of 1986

The Role of Taxes in Organizational Choice: S Conversions After the Tax Reform Act of 1986 George A. Plesko * Sloan School of Management Massachusetts Institute of Technology Correspondence: E52-325, Sloan

The Role of Taxes in Organizational Choice: S Conversions After the Tax Reform Act of 1986 George A. Plesko * Sloan School of Management Massachusetts Institute of Technology Correspondence: E52-325, Sloan

INCOME TAXATION AND BUSINESS INCORPORATION: EVIDENCE FROM THE EARLY TWENTIETH CENTURY. Li Liu

INCOME TAXATION AND BUSINESS INCORPORATION: EVIDENCE FROM THE EARLY TWENTIETH CENTURY Li Liu If the corporate income tax is set at a different rate from non-corporate in-come tax, it can play an important

INCOME TAXATION AND BUSINESS INCORPORATION: EVIDENCE FROM THE EARLY TWENTIETH CENTURY Li Liu If the corporate income tax is set at a different rate from non-corporate in-come tax, it can play an important

Proposals for broadening the income tax base often call for eliminating or restricting

National Tax Journal, June 2011, 64 (2, Part 2), 591 614 PORTFOLIO SUBSTITUTION AND THE REVENUE COST OF THE FEDERAL INCOME TAX EXEMPTION FOR STATE AND LOCAL GOVERNMENT BONDS James M. Poterba and Arturo

National Tax Journal, June 2011, 64 (2, Part 2), 591 614 PORTFOLIO SUBSTITUTION AND THE REVENUE COST OF THE FEDERAL INCOME TAX EXEMPTION FOR STATE AND LOCAL GOVERNMENT BONDS James M. Poterba and Arturo

DO TAXES AFFECT CORPORATE DEBT POLICY? Evidence from U.S. Corporate Tax Return Data

DO TAXES AFFECT CORPORATE DEBT POLICY? Evidence from U.S. Corporate Tax Return Data by Roger H. Gordon and Young Lee University of Michigan and Korea Development Institute August 25, 2000 Abstract. This

DO TAXES AFFECT CORPORATE DEBT POLICY? Evidence from U.S. Corporate Tax Return Data by Roger H. Gordon and Young Lee University of Michigan and Korea Development Institute August 25, 2000 Abstract. This

1%(5:25.,1*3$3(56(5,(6 $//2&$7,1*3$<52//7$;5(9(18(72 3(5621$/5(7,5(0(17$&&28176720$,17$,1 62&,$/6(&85,7<%(1(),76$1'7+(3$<52//7$;5$7(

,76$1'7+(3$<52//7$;5$7(") 1%(5:25.,1*3$3(56(5,(6 $//2&$7,1*3$

1%(5:25.,1*3$3(56(5,(6 $//2&$7,1*3$

RECENT EVIDENCE ON TAXPAYERS RESPONSE TO THE RATE INCREASES IN THE 1990 S FRANK SAMMARTINO DAVID WEINER *

TAXPAYERS RESPONSE TO THE RATE INCREASES IN THE 1990S RECENT EVIDENCE ON TAXPAYERS RESPONSE TO THE RATE INCREASES IN THE 1990 S FRANK SAMMARTINO DAVID WEINER * * & * Tax Analysis Division, Congressional

TAXPAYERS RESPONSE TO THE RATE INCREASES IN THE 1990S RECENT EVIDENCE ON TAXPAYERS RESPONSE TO THE RATE INCREASES IN THE 1990 S FRANK SAMMARTINO DAVID WEINER * * & * Tax Analysis Division, Congressional

The Case for a Tax Cut

The Case for a Tax Cut Alan C. Stockman University of Rochester, and NBER Shadow Open Market Committee April 29-30, 2001 1. Tax Increases Have Created the Surplus Any discussion of tax policy should begin

The Case for a Tax Cut Alan C. Stockman University of Rochester, and NBER Shadow Open Market Committee April 29-30, 2001 1. Tax Increases Have Created the Surplus Any discussion of tax policy should begin

Retirement Investing: Analyzing the Roth Conversion Option*

Retirement Investing: Analyzing the Roth Conversion Option* Robert M. Dammon Tepper School of Bsiness Carnegie Mellon University 12/3/2009 * The author thanks Chester Spatt for valuable discussions. The

Retirement Investing: Analyzing the Roth Conversion Option* Robert M. Dammon Tepper School of Bsiness Carnegie Mellon University 12/3/2009 * The author thanks Chester Spatt for valuable discussions. The

Volume Publisher: University of Chicago Press. Volume URL: http://www.nber.org/books/hall82-1

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Inflation: Causes and Effects Volume Author/Editor: Robert E. Hall Volume Publisher: University

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Inflation: Causes and Effects Volume Author/Editor: Robert E. Hall Volume Publisher: University

CBO STAFF DISTRIBUTIONAL EFFECTS OF SUBSTITUTING A FLAT-RATE INCOME TAX AND AVALUE-ADDEDTAXFORCURRENT FEDERAL INCOME, PAYROLL, AND EXCISE TAXES

CBO STAFF MEMORANDUM DISTRIBUTIONAL EFFECTS OF SUBSTITUTING A FLAT-RATE INCOME TAX AND AVALUE-ADDEDTAXFORCURRENT FEDERAL INCOME, PAYROLL, AND EXCISE TAXES April 1992 CONGRESSIONAL BUDGET OFFICE SECOND

CBO STAFF MEMORANDUM DISTRIBUTIONAL EFFECTS OF SUBSTITUTING A FLAT-RATE INCOME TAX AND AVALUE-ADDEDTAXFORCURRENT FEDERAL INCOME, PAYROLL, AND EXCISE TAXES April 1992 CONGRESSIONAL BUDGET OFFICE SECOND

Corporate Income Taxation

Corporate Income Taxation We have stressed that tax incidence must be traced to people, since corporations cannot bear the burden of a tax. Why then tax corporations at all? There are several possible

Corporate Income Taxation We have stressed that tax incidence must be traced to people, since corporations cannot bear the burden of a tax. Why then tax corporations at all? There are several possible

DATA APPENDIX: Taxes, Regulations, and the Value of U.S. and U.K. Corporations

Federal Reserve Bank of Minneapolis Research Department Staff Report 309 June 2004 DATA APPENDIX: Taxes, Regulations, and the Value of U.S. and U.K. Corporations Ellen R. McGrattan Federal Reserve Bank

Federal Reserve Bank of Minneapolis Research Department Staff Report 309 June 2004 DATA APPENDIX: Taxes, Regulations, and the Value of U.S. and U.K. Corporations Ellen R. McGrattan Federal Reserve Bank

WHAT HAPPENS WHEN YOU TAX THE RICH? EVIDENCE FROM EXECUTIVE COMPENSATION. Austan Goolsbee University of Chicago, G.S.B. and American Bar Foundation

WHAT HAPPENS WHEN YOU TAX THE RICH? EVIDENCE FROM EXECUTIVE COMPENSATION Austan Goolsbee University of Chicago, G.S.B. and American Bar Foundation Original Submission: October, 1997 Revision: February,

WHAT HAPPENS WHEN YOU TAX THE RICH? EVIDENCE FROM EXECUTIVE COMPENSATION Austan Goolsbee University of Chicago, G.S.B. and American Bar Foundation Original Submission: October, 1997 Revision: February,

CAPITAL INCOME TAXATION AND PROGRESSIVITY IN A GLOBAL ECONOMY. Abstract

CAPITAL INCOME TAXATION AND PROGRESSIVITY IN A GLOBAL ECONOMY Rosanne Altshuler raltshuler@urban.org Benjamin Harris bharris@brookings.edu Eric Toder etoder@urban.org May 12, 2010 Abstract The increase

CAPITAL INCOME TAXATION AND PROGRESSIVITY IN A GLOBAL ECONOMY Rosanne Altshuler raltshuler@urban.org Benjamin Harris bharris@brookings.edu Eric Toder etoder@urban.org May 12, 2010 Abstract The increase

Average Debt and Equity Returns: Puzzling?

Federal Reserve Bank of Minneapolis Research Department Staff Report 313 January 2003 Average Debt and Equity Returns: Puzzling? Ellen R. McGrattan Federal Reserve Bank of Minneapolis, University of Minnesota,

Federal Reserve Bank of Minneapolis Research Department Staff Report 313 January 2003 Average Debt and Equity Returns: Puzzling? Ellen R. McGrattan Federal Reserve Bank of Minneapolis, University of Minnesota,

The Tax Benefits and Revenue Costs of Tax Deferral

The Tax Benefits and Revenue Costs of Tax Deferral Copyright 2012 by the Investment Company Institute. All rights reserved. Suggested citation: Brady, Peter. 2012. The Tax Benefits and Revenue Costs of

The Tax Benefits and Revenue Costs of Tax Deferral Copyright 2012 by the Investment Company Institute. All rights reserved. Suggested citation: Brady, Peter. 2012. The Tax Benefits and Revenue Costs of

Reducing the Deficit by Increasing Individual Income Tax Rates

Reducing the Deficit by Increasing Individual Income Tax Rates Eric Toder, Jim Nunns, and Joseph Rosenberg March 2012 The authors are all affiliated with the Urban-Brookings Tax Policy Center. Toder is

Reducing the Deficit by Increasing Individual Income Tax Rates Eric Toder, Jim Nunns, and Joseph Rosenberg March 2012 The authors are all affiliated with the Urban-Brookings Tax Policy Center. Toder is

CHAPTER 7 TAXATION OF BUSINESS ORGANIZATIONS

CHAPTER 7 TAXATION OF BUSINESS ORGANIZATIONS Equity investment in the corporate sector is discouraged by the relatively high effective rate of taxation imposed on the return from such investment. The only

CHAPTER 7 TAXATION OF BUSINESS ORGANIZATIONS Equity investment in the corporate sector is discouraged by the relatively high effective rate of taxation imposed on the return from such investment. The only

ECONOMIC CONSEQUENCES OF THE TAX POLICIES OF THE KENNEDY AND JOHNSON ADMINISTRATIONS

September 6, 2011 No. 99 ECONOMIC CONSEQUENCES OF THE TAX POLICIES OF THE KENNEDY AND JOHNSON ADMINISTRATIONS Introduction This paper is the first in a series examining federal tax policies implemented

September 6, 2011 No. 99 ECONOMIC CONSEQUENCES OF THE TAX POLICIES OF THE KENNEDY AND JOHNSON ADMINISTRATIONS Introduction This paper is the first in a series examining federal tax policies implemented

APPENDIX E STUDY ON THE QUESTION "SHOULD HAWAII REPLACE ITS INCOME AND FRANCHISE TAXES WITH AN INCREASE IN THE GENERAL EXCISE TAX?

APPENDIX E STUDY ON THE QUESTION "SHOULD HAWAII REPLACE ITS INCOME AND FRANCHISE TAXES WITH AN INCREASE IN THE GENERAL EXCISE TAX?" Tax Research and Planning Office Department of Taxation State of Hawaii

APPENDIX E STUDY ON THE QUESTION "SHOULD HAWAII REPLACE ITS INCOME AND FRANCHISE TAXES WITH AN INCREASE IN THE GENERAL EXCISE TAX?" Tax Research and Planning Office Department of Taxation State of Hawaii

Jobs and Growth Effects of Tax Rate Reductions in Ohio

Jobs and Growth Effects of Tax Rate Reductions in Ohio BY ALEX BRILL May 2014 This report was sponsored by American Freedom Builders, Inc., a 501(c)4 organization. The author is solely responsible for

Jobs and Growth Effects of Tax Rate Reductions in Ohio BY ALEX BRILL May 2014 This report was sponsored by American Freedom Builders, Inc., a 501(c)4 organization. The author is solely responsible for

Eliminating Double Taxation through Corporate Integration

FISCAL FACT Feb. 2015 No. 453 Eliminating Double Taxation through Corporate Integration By Kyle Pomerleau Economist Key Findings The United States tax code places a double-tax on corporate income with

FISCAL FACT Feb. 2015 No. 453 Eliminating Double Taxation through Corporate Integration By Kyle Pomerleau Economist Key Findings The United States tax code places a double-tax on corporate income with

DOUBLE DIVIDEND TAXATION RELIEF: A NEW VIEW FROM THE CORPORATE INCOME TAX PERSPECTIVE

DOUBLE DIVIDEND TAXATION RELIEF: A NEW VIEW FROM THE CORPORATE INCOME TAX PERSPECTIVE Sebastian LAZAR Faculty of Economics and Business Administration "Al. I. Cuza" University Iasi, Romania slazar@uaic.ro

DOUBLE DIVIDEND TAXATION RELIEF: A NEW VIEW FROM THE CORPORATE INCOME TAX PERSPECTIVE Sebastian LAZAR Faculty of Economics and Business Administration "Al. I. Cuza" University Iasi, Romania slazar@uaic.ro

Crunch or Crucible? Upcoming Changes in the Federal Tax Law A Special Edition Tax Guide for Friends and Alumni of Pomona College

Upcoming Changes in the Federal Tax Law A Special Edition Tax Guide for Friends and Alumni of Pomona College Pomona College, Office of Trusts & Estates, 550 N. College Ave., Claremont, CA 91711 www.pomona.planyourlegacy.org

Upcoming Changes in the Federal Tax Law A Special Edition Tax Guide for Friends and Alumni of Pomona College Pomona College, Office of Trusts & Estates, 550 N. College Ave., Claremont, CA 91711 www.pomona.planyourlegacy.org

On the relationship between defense and non-defense spending in the U.S. during the world wars

Economics Letters 95 (2007) 415 421 www.elsevier.com/locate/econbase On the relationship between defense and non-defense spending in the U.S. during the world wars Roel M.W.J. Beetsma a,, Alex Cukierman

Economics Letters 95 (2007) 415 421 www.elsevier.com/locate/econbase On the relationship between defense and non-defense spending in the U.S. during the world wars Roel M.W.J. Beetsma a,, Alex Cukierman

The Taxation of Retirement Saving: Choosing Between Front-Loaded and Back-Loaded Options *

The Taxation of Retirement Saving: Choosing Between Front-Loaded and Back-Loaded Options * Leonard E. Burman The Urban Institute William G. Gale The Brookings Institution David Weiner Congressional Budget

The Taxation of Retirement Saving: Choosing Between Front-Loaded and Back-Loaded Options * Leonard E. Burman The Urban Institute William G. Gale The Brookings Institution David Weiner Congressional Budget

Tax Subsidies for Health Insurance An Issue Brief

Tax Subsidies for Health Insurance An Issue Brief Prepared by the Kaiser Family Foundation July 2008 Tax Subsidies for Health Insurance Most workers pay both federal and state taxes for wages paid to them

Tax Subsidies for Health Insurance An Issue Brief Prepared by the Kaiser Family Foundation July 2008 Tax Subsidies for Health Insurance Most workers pay both federal and state taxes for wages paid to them

CORPORATE INCOME TAX. Effective Tax Rates Can Differ Significantly from the Statutory Rate. Report to Congressional Requesters

United States Government Accountability Office Report to Congressional Requesters May 2013 CORPORATE INCOME TAX Effective Tax Rates Can Differ Significantly from the Statutory Rate GAO-13-520 May 2013

United States Government Accountability Office Report to Congressional Requesters May 2013 CORPORATE INCOME TAX Effective Tax Rates Can Differ Significantly from the Statutory Rate GAO-13-520 May 2013

Tax Expenditures for Owner-Occupied Housing: Deductions for Property Taxes and Mortgage Interest and the Exclusion of Imputed Rental Income AUTHORS

Tax Expenditures for Owner-Occupied Housing: Deductions for Property Taxes and Mortgage Interest and the Exclusion of Imputed Rental Income AUTHORS James Poterba (corresponding) Todd Sinai Department of

Tax Expenditures for Owner-Occupied Housing: Deductions for Property Taxes and Mortgage Interest and the Exclusion of Imputed Rental Income AUTHORS James Poterba (corresponding) Todd Sinai Department of

National Small Business Network

National Small Business Network WRITTEN STATEMENT FOR THE RECORD US SENATE COMMITTEE ON FINANCE U.S. HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS JOINT HEARING ON TAX REFORM AND THE TAX TREATMENT

National Small Business Network WRITTEN STATEMENT FOR THE RECORD US SENATE COMMITTEE ON FINANCE U.S. HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS JOINT HEARING ON TAX REFORM AND THE TAX TREATMENT

Cash Versus Accrual Accounting: Tax Policy Considerations

Cash Versus Accrual Accounting: Tax Policy Considerations Raj Gnanarajah Analyst in Financial Economics Mark P. Keightley Specialist in Economics April 24, 2015 Congressional Research Service 7-5700 www.crs.gov

Cash Versus Accrual Accounting: Tax Policy Considerations Raj Gnanarajah Analyst in Financial Economics Mark P. Keightley Specialist in Economics April 24, 2015 Congressional Research Service 7-5700 www.crs.gov

The Effect on Housing Prices of Changes in Mortgage Rates and Taxes

Preliminary. Comments welcome. The Effect on Housing Prices of Changes in Mortgage Rates and Taxes Lars E.O. Svensson SIFR The Institute for Financial Research, Swedish House of Finance, Stockholm School

Preliminary. Comments welcome. The Effect on Housing Prices of Changes in Mortgage Rates and Taxes Lars E.O. Svensson SIFR The Institute for Financial Research, Swedish House of Finance, Stockholm School

The Latest on S-Corps: Practical Lessons from Research and the Trenches. (and as we ll see, leave aside)

") Pass-through Entity Valuation Update Nancy Fannon, CPA, ASA, MCBA, ABV Meyers, Harrison & Pia Keith Sellers, CPA, CVA, ABV Daniels College of Business University of Denver Let s set aside (and as we ll

Pass-through Entity Valuation Update Nancy Fannon, CPA, ASA, MCBA, ABV Meyers, Harrison & Pia Keith Sellers, CPA, CVA, ABV Daniels College of Business University of Denver Let s set aside (and as we ll

TAXATION AND CORPORATE USE OF DEBT: IMPLICATIONS FOR TAX POLICY. Roger H. Gordon

National Tax Journal, March 2010, 63 (1), 151 174 TAXATION AND CORPORATE USE OF DEBT: IMPLICATIONS FOR TAX POLICY Roger H. Gordon There is growing empirical evidence showing that taxes encourage use of

National Tax Journal, March 2010, 63 (1), 151 174 TAXATION AND CORPORATE USE OF DEBT: IMPLICATIONS FOR TAX POLICY Roger H. Gordon There is growing empirical evidence showing that taxes encourage use of

Volume URL: http://www.nber.org/books/feld87-2. Chapter Title: Individual Retirement Accounts and Saving

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Taxes and Capital Formation Volume Author/Editor: Martin Feldstein, ed. Volume Publisher:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Taxes and Capital Formation Volume Author/Editor: Martin Feldstein, ed. Volume Publisher:

April 8,2005 JEFFREY KUPFER, EXECUTIVE DIRECTOR PRESIDENT S ADVISORY PANEL ON FEDERAL TAX REFORM

DEPARTMENT OF THE TREASURY WASHINGTON, D.C. 20220 April 8,2005 MEMORANDUM FOR FROM SUBJECT JEFFREY KUPFER, EXECUTIVE DIRECTOR PRESIDENT S ADVISORY PANEL ON FEDERAL TAX REFORM ROBERT CAmoLi& DEPUTY ASSISTANT

DEPARTMENT OF THE TREASURY WASHINGTON, D.C. 20220 April 8,2005 MEMORANDUM FOR FROM SUBJECT JEFFREY KUPFER, EXECUTIVE DIRECTOR PRESIDENT S ADVISORY PANEL ON FEDERAL TAX REFORM ROBERT CAmoLi& DEPUTY ASSISTANT

The U.S. Tax Reform Experience 1

The U.S. Tax Reform Experience 1 Alan J. Auerbach University of California, Berkeley The Tax Reform Act of 1986 (TRA86) represented the most sweeping change in the U.S. federal income tax since World War

The U.S. Tax Reform Experience 1 Alan J. Auerbach University of California, Berkeley The Tax Reform Act of 1986 (TRA86) represented the most sweeping change in the U.S. federal income tax since World War

FOREIGN TAXES AND THE GROWING SHARE OF U.S. MULTINATIONAL COMPANY INCOME ABROAD: PROFITS, NOT SALES, ARE BEING GLOBALIZED.

National Tax Journal, June 2012, 65 (2), 247 282 FOREIGN TAXES AND THE GROWING SHARE OF U.S. MULTINATIONAL COMPANY INCOME ABROAD: PROFITS, NOT SALES, ARE BEING GLOBALIZED Harry Grubert The foreign share

National Tax Journal, June 2012, 65 (2), 247 282 FOREIGN TAXES AND THE GROWING SHARE OF U.S. MULTINATIONAL COMPANY INCOME ABROAD: PROFITS, NOT SALES, ARE BEING GLOBALIZED Harry Grubert The foreign share

THE GRADUATED PERSONAL INCOME TAX ASSESSMENT: FREQUENTLY ASKED QUESTIONS

LEGISLATIVE REVENUE OFFICE State Capitol Building 900 Court St. NE, Room H-197 Salem, Oregon 97301 Research Brief (503) 986-1266 FAX (503) 986-1770 http://www.leg.state.or.us/comm/lro/home.htm Number 3-03

LEGISLATIVE REVENUE OFFICE State Capitol Building 900 Court St. NE, Room H-197 Salem, Oregon 97301 Research Brief (503) 986-1266 FAX (503) 986-1770 http://www.leg.state.or.us/comm/lro/home.htm Number 3-03

Volume Title: Tax Policy and the Economy, Volume 12. Volume Author/Editor: James M. Poterba, editor. Volume URL: http://www.nber.

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Tax Policy and the Economy, Volume 12 Volume Author/Editor: James M. Poterba, editor Volume

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Tax Policy and the Economy, Volume 12 Volume Author/Editor: James M. Poterba, editor Volume

Taxation and Small Businesses in Minnesota

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Nina Manzi, Legislative Analyst, 651-296-5204 Joel Michael, Legislative Analyst, 651-296-5057

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Nina Manzi, Legislative Analyst, 651-296-5204 Joel Michael, Legislative Analyst, 651-296-5057

THE IRA PROPOSAL CONTAINED IN S. 1682: EFFECTS ON LONG-TERM REVENUES AND ON INCENTIVES FOR SAVING. Staff Memorandum November 2, 1989

THE IRA PROPOSAL CONTAINED IN S. 1682: EFFECTS ON LONG-TERM REVENUES AND ON INCENTIVES FOR SAVING Staff Memorandum November 2, 1989 The Congress of the United States Congressional Budget Office This mcmorandura

THE IRA PROPOSAL CONTAINED IN S. 1682: EFFECTS ON LONG-TERM REVENUES AND ON INCENTIVES FOR SAVING Staff Memorandum November 2, 1989 The Congress of the United States Congressional Budget Office This mcmorandura

Since 1960's, U.S. personal savings rate (fraction of income saved) averaged 7%, lower than 15% OECD average. Why? Why do we care?

averaged 7%, lower than 15% OECD average. Why? Why do we care?") Taxation and Personal Saving, G 22 Since 1960's, U.S. personal savings rate (fraction of income saved) averaged 7%, lower than 15% OECD average. Why? Why do we care? Efficiency issues 1. Negative consumption

Taxation and Personal Saving, G 22 Since 1960's, U.S. personal savings rate (fraction of income saved) averaged 7%, lower than 15% OECD average. Why? Why do we care? Efficiency issues 1. Negative consumption

Retirement Income Effects of Changing theincometaxtreatmentofdc Pension Plans

Retirement Income Effects of Changing theincometaxtreatmentofdc Pension Plans Martin Holmer, Policy Simulation Group May 14, 2012 Abstract This paper presents estimates of the after-tax retirement income

Retirement Income Effects of Changing theincometaxtreatmentofdc Pension Plans Martin Holmer, Policy Simulation Group May 14, 2012 Abstract This paper presents estimates of the after-tax retirement income

Life Insurance Companies and Products

Part B. Life Insurance Companies and Products The current Federal income tax treatment of life insurance companies and their products al.lows investors in such products to obtain a substantially higher

Part B. Life Insurance Companies and Products The current Federal income tax treatment of life insurance companies and their products al.lows investors in such products to obtain a substantially higher

MEASURING INCOME FOR DISTRIBUTIONAL ANALYSIS. Joseph Rosenberg Urban-Brookings Tax Policy Center July 25, 2013 ABSTRACT

MEASURING INCOME FOR DISTRIBUTIONAL ANALYSIS Joseph Rosenberg Urban-Brookings Tax Policy Center July 25, 2013 ABSTRACT This document describes the income measure the Tax Policy Center (TPC) uses to analyze

MEASURING INCOME FOR DISTRIBUTIONAL ANALYSIS Joseph Rosenberg Urban-Brookings Tax Policy Center July 25, 2013 ABSTRACT This document describes the income measure the Tax Policy Center (TPC) uses to analyze

2.If actual investment is greater than planned investment, inventories increase more than planned. TRUE.

Macro final exam study guide True/False questions - Solutions Case, Fair, Oster Chapter 8 Aggregate Expenditure and Equilibrium Output 1.Firms react to unplanned inventory investment by reducing output.

Macro final exam study guide True/False questions - Solutions Case, Fair, Oster Chapter 8 Aggregate Expenditure and Equilibrium Output 1.Firms react to unplanned inventory investment by reducing output.

READING 11: TAXES AND PRIVATE WEALTH MANAGEMENT IN A GLOBAL CONTEXT

READING 11: TAXES AND PRIVATE WEALTH MANAGEMENT IN A GLOBAL CONTEXT Introduction Taxes have a significant impact on net performance and affect an adviser s understanding of risk for the taxable investor.

READING 11: TAXES AND PRIVATE WEALTH MANAGEMENT IN A GLOBAL CONTEXT Introduction Taxes have a significant impact on net performance and affect an adviser s understanding of risk for the taxable investor.

The dynamic economic effects of a US corporate income tax rate reduction

The dynamic economic effects of a US corporate income tax rate reduction April 2014 WP 14/05 John W Diamond Rice University George R Zodrow Rice University Working paper series 2014 The paper is circulated

The dynamic economic effects of a US corporate income tax rate reduction April 2014 WP 14/05 John W Diamond Rice University George R Zodrow Rice University Working paper series 2014 The paper is circulated

The Impact of Individual Retirement Accounts on Savings Jonathan McCarthy and Han N. Pham

September 1995 Volume 1 Number 6 The Impact of Individual Retirement Accounts on Savings Jonathan McCarthy and Han N. Pham Bills to expand individual retirement accounts have been introduced in both houses

September 1995 Volume 1 Number 6 The Impact of Individual Retirement Accounts on Savings Jonathan McCarthy and Han N. Pham Bills to expand individual retirement accounts have been introduced in both houses

How Much Equity Does the Government Hold?

How Much Equity Does the Government Hold? Alan J. Auerbach University of California, Berkeley and NBER January 2004 This paper was presented at the 2004 Meetings of the American Economic Association. I

How Much Equity Does the Government Hold? Alan J. Auerbach University of California, Berkeley and NBER January 2004 This paper was presented at the 2004 Meetings of the American Economic Association. I

The Economists Voice

The Economists Voice Volume 2, Issue 1 2005 Article 8 A Special Issue on Social Security Saving Social Security: The Diamond-Orszag Plan Peter A. Diamond Peter R. Orszag Summary Social Security is one

The Economists Voice Volume 2, Issue 1 2005 Article 8 A Special Issue on Social Security Saving Social Security: The Diamond-Orszag Plan Peter A. Diamond Peter R. Orszag Summary Social Security is one

LONG-RUN CHANGES IN TAX EXPENDITURES ON 401(K)-TYPE RETIREMENT PLANS. Ithai Z. Lurie and Shanthi P. Ramnath

-TYPE RETIREMENT PLANS. Ithai Z. Lurie and Shanthi P. Ramnath") National Tax Journal, December 2011, 64 (4), 1025 1038 LONG-RUN CHANGES IN TAX EXPENDITURES ON 401(K)-TYPE RETIREMENT PLANS Ithai Z. Lurie and Shanthi P. Ramnath In this paper, we explore the long-run

National Tax Journal, December 2011, 64 (4), 1025 1038 LONG-RUN CHANGES IN TAX EXPENDITURES ON 401(K)-TYPE RETIREMENT PLANS Ithai Z. Lurie and Shanthi P. Ramnath In this paper, we explore the long-run

Social Security Eligibility and the Labor Supply of Elderly Immigrants. George J. Borjas Harvard University and National Bureau of Economic Research

Social Security Eligibility and the Labor Supply of Elderly Immigrants George J. Borjas Harvard University and National Bureau of Economic Research Updated for the 9th Annual Joint Conference of the Retirement

Social Security Eligibility and the Labor Supply of Elderly Immigrants George J. Borjas Harvard University and National Bureau of Economic Research Updated for the 9th Annual Joint Conference of the Retirement

To Roth Or Not To Roth?

To Roth Or Not To Roth? 05.07.2015 FPA Rhode Island Michael E. Kitces MSFS, MTAX, CFP, CLU, ChFC, RHU, REBC, CASL Partner. Director of Research, Pinnacle Advisory Group Publisher. The Kitces Report, www.kitces.com

To Roth Or Not To Roth? 05.07.2015 FPA Rhode Island Michael E. Kitces MSFS, MTAX, CFP, CLU, ChFC, RHU, REBC, CASL Partner. Director of Research, Pinnacle Advisory Group Publisher. The Kitces Report, www.kitces.com

MUNICIPAL DEBT: WHAT DOES IT BUY AND WHO BENEFITS?

National Tax Journal, December 2014, 67 (4), 901 924 MUNICIPAL DEBT: WHAT DOES IT BUY AND WHO BENEFITS? Harvey Galper, Kim Rueben, Richard Auxier, and Amanda Eng This paper examines the incidence of the

National Tax Journal, December 2014, 67 (4), 901 924 MUNICIPAL DEBT: WHAT DOES IT BUY AND WHO BENEFITS? Harvey Galper, Kim Rueben, Richard Auxier, and Amanda Eng This paper examines the incidence of the

DOES HOUSEHOLD DEBT HELP FORECAST CONSUMER SPENDING? Robert G. Murphy Department of Economics Boston College Chestnut Hill, MA 02467

DOES HOUSEHOLD DEBT HELP FORECAST CONSUMER SPENDING? By Robert G. Murphy Department of Economics Boston College Chestnut Hill, MA 02467 E-mail: murphyro@bc.edu Revised: December 2000 Keywords : Household

DOES HOUSEHOLD DEBT HELP FORECAST CONSUMER SPENDING? By Robert G. Murphy Department of Economics Boston College Chestnut Hill, MA 02467 E-mail: murphyro@bc.edu Revised: December 2000 Keywords : Household

DUAL INCOME TAXES: A NORDIC TAX SYSTEM

DUAL INCOME TAXES: A NORDIC TAX SYSTEM Peter Birch SørensenS University of Copenhagen Presentation at the conference on New Zealand Tax Reform Where to Next? Wellington, February 11-13,, 2009 AGENDA What

DUAL INCOME TAXES: A NORDIC TAX SYSTEM Peter Birch SørensenS University of Copenhagen Presentation at the conference on New Zealand Tax Reform Where to Next? Wellington, February 11-13,, 2009 AGENDA What

Taxes and Transitions

Taxes and Transitions THE NEW FRONTIER FOR RETIREMENT PLANNING Wealthy individuals have been hit with their first major tax increase in more than 20 years, with tax hikes on ordinary income, dividends

Taxes and Transitions THE NEW FRONTIER FOR RETIREMENT PLANNING Wealthy individuals have been hit with their first major tax increase in more than 20 years, with tax hikes on ordinary income, dividends

Health Care Reform and Small Business

Jane G. Gravelle Senior Specialist in Economic Policy July 5, 2013 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research Service 7-5700 www.crs.gov R40775 c11173008

Jane G. Gravelle Senior Specialist in Economic Policy July 5, 2013 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research Service 7-5700 www.crs.gov R40775 c11173008

The Effect of Tax-Based Savings Incentives on Government Revenue

Fiscal Studies (1997) vol. 18, no. 2, pp. 143 159 The Effect of Tax-Based Savings Incentives on Government Revenue GIUSEPPE RUGGERI and MAXIME FOUGÈRE * Abstract There is an unresolved debate on the effect

Fiscal Studies (1997) vol. 18, no. 2, pp. 143 159 The Effect of Tax-Based Savings Incentives on Government Revenue GIUSEPPE RUGGERI and MAXIME FOUGÈRE * Abstract There is an unresolved debate on the effect

Federal Income Taxes and Investment Strategy

Federal Income Taxes and Investment Strategy By Sholom Feldblum, FCAS, FSA, MAAA June 2007 CAS Study Note EXAM 7 STUDY NOTE: FEDERAL INCOME TAXES AND INVESTMENT STRATEGY This reading explains tax influences

Federal Income Taxes and Investment Strategy By Sholom Feldblum, FCAS, FSA, MAAA June 2007 CAS Study Note EXAM 7 STUDY NOTE: FEDERAL INCOME TAXES AND INVESTMENT STRATEGY This reading explains tax influences

Volume Title: Financial Aspects of the United States Pension System. Volume Author/Editor: Zvi Bodie and John B. Shoven, editors

This PDF is a selection from an outofprint volume from the National Bureau of Economic Research Volume Title: Financial Aspects of the United States Pension System Volume Author/Editor: Zvi Bodie and John

This PDF is a selection from an outofprint volume from the National Bureau of Economic Research Volume Title: Financial Aspects of the United States Pension System Volume Author/Editor: Zvi Bodie and John

Business Organization\Tax Structure

Business Organization\Tax Structure Kansas Secretary of State s Office Business Services Division First Floor, Memorial Hall 120 S.W. 10th Avenue Topeka, KS 66612-1594 Phone: (785) 296-4564 Fax: (785)

Business Organization\Tax Structure Kansas Secretary of State s Office Business Services Division First Floor, Memorial Hall 120 S.W. 10th Avenue Topeka, KS 66612-1594 Phone: (785) 296-4564 Fax: (785)

Farmer Savings Accounts

Farmer Savings Accounts Mark A. Edelman, Iowa State University James D. Monke, Economic Research Service, USDA Ron Durst, Economic Research Service, USDA Introduction Various incentives can be used to

Farmer Savings Accounts Mark A. Edelman, Iowa State University James D. Monke, Economic Research Service, USDA Ron Durst, Economic Research Service, USDA Introduction Various incentives can be used to

Taxes and Choice of Organizational Form by Entrepreneurs in Sweden 1

Preliminary version please do not quote! Taxes and Choice of Organizational Form by Entrepreneurs in Sweden 1 Karin Edmark and Roger Gordon January 29, 2012 1 We thank Magnus Henrekson, Pontus Braunerhjelm,

Preliminary version please do not quote! Taxes and Choice of Organizational Form by Entrepreneurs in Sweden 1 Karin Edmark and Roger Gordon January 29, 2012 1 We thank Magnus Henrekson, Pontus Braunerhjelm,

Choice of Entity: Corporation or Limited Liability Company?

March 2014 Choice of Entity: Corporation or Limited Liability Company? By Gianfranco A. Pietrafesa* Attorney at Law There are many different types of business entities, including corporations, general

March 2014 Choice of Entity: Corporation or Limited Liability Company? By Gianfranco A. Pietrafesa* Attorney at Law There are many different types of business entities, including corporations, general

TAX REFORM AND SMALL BUSINESS

REFERENCES TAX REFORM AND SMALL BUSINESS Eric J. Toder * Institute Fellow, Urban Institute and Co-Director, Urban-Brookings Tax Policy Center House Committee on Small Business April 15, 2015 Chairman Chabot,

REFERENCES TAX REFORM AND SMALL BUSINESS Eric J. Toder * Institute Fellow, Urban Institute and Co-Director, Urban-Brookings Tax Policy Center House Committee on Small Business April 15, 2015 Chairman Chabot,

Small Business Tax Benefits: Overview and Economic Rationale

Small Business Tax Benefits: Overview and Economic Rationale Gary Guenther Analyst in Public Finance March 26, 2009 Congressional Research Service CRS Report for Congress Prepared for Members and Committees

Small Business Tax Benefits: Overview and Economic Rationale Gary Guenther Analyst in Public Finance March 26, 2009 Congressional Research Service CRS Report for Congress Prepared for Members and Committees

The Effect of Money Market Certificates of Deposit on the Monetary Aggregates and Their Components

The Effect of Money Market Certificates of Deposit on the Monetary Aggregates and Their Components By Scott Winningham On June 1, 1978, the Federal Reserve System and other regulatory agencies gave banks

The Effect of Money Market Certificates of Deposit on the Monetary Aggregates and Their Components By Scott Winningham On June 1, 1978, the Federal Reserve System and other regulatory agencies gave banks

WEALTH TRANSFER TAXES

WEALTH TRANSFER TAXES How do the estate, gift, and generation-skipping transfer taxes work?... 1 Who pays the estate tax?... 2 How many people pay the estate tax?... 2 How could we reform the estate tax?...

WEALTH TRANSFER TAXES How do the estate, gift, and generation-skipping transfer taxes work?... 1 Who pays the estate tax?... 2 How many people pay the estate tax?... 2 How could we reform the estate tax?...

Taxation of Owner-Occupied and Rental Housing

Working Paper Series Congressional Budget Office Washington, D.C. Taxation of Owner-Occupied and Rental Housing Larry Ozanne Congressional Budget Office Larry.Ozanne@cbo.gov November 2012 Working Paper

Working Paper Series Congressional Budget Office Washington, D.C. Taxation of Owner-Occupied and Rental Housing Larry Ozanne Congressional Budget Office Larry.Ozanne@cbo.gov November 2012 Working Paper

Eric T. Thoele Income Tax Inequalities. Intermediate Macroeconomics EC3100 Rockhurst University. Dr. Gerald Miller 03/31/05

Eric T. Thoele Income Tax Inequalities Intermediate Macroeconomics EC3100 Rockhurst University Dr. Gerald Miller 03/31/05 Executive Summary 1) The Origin and History - This gives the basic background of

Eric T. Thoele Income Tax Inequalities Intermediate Macroeconomics EC3100 Rockhurst University Dr. Gerald Miller 03/31/05 Executive Summary 1) The Origin and History - This gives the basic background of

IRA'S AND HOUSEHOLD SAVING REVISITED: SOME NEW EVIDENCE. Working Paper No. 4900

NBER WORKING PAPER SERIES IRA'S AND HOUSEHOLD SAVING REVISITED: SOME NEW EVIDENCE Orazio P. Attanasio Thomas C. DeLeire Working Paper No. 4900 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue

NBER WORKING PAPER SERIES IRA'S AND HOUSEHOLD SAVING REVISITED: SOME NEW EVIDENCE Orazio P. Attanasio Thomas C. DeLeire Working Paper No. 4900 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue

Chapter 4 Consumption, Saving, and Investment

Chapter 4 Consumption, Saving, and Investment Multiple Choice Questions 1. Desired national saving equals (a) Y C d G. (b) C d + I d + G. (c) I d + G. (d) Y I d G. 2. With no inflation and a nominal interest

Chapter 4 Consumption, Saving, and Investment Multiple Choice Questions 1. Desired national saving equals (a) Y C d G. (b) C d + I d + G. (c) I d + G. (d) Y I d G. 2. With no inflation and a nominal interest

In this article, we go back to basics, but

Asset Allocation and Asset Location Decisions Revisited WILLIAM REICHENSTEIN WILLIAM REICHENSTEIN holds the Pat and Thomas R. Powers Chair in Investment Management at the Hankamer School of Business at

Asset Allocation and Asset Location Decisions Revisited WILLIAM REICHENSTEIN WILLIAM REICHENSTEIN holds the Pat and Thomas R. Powers Chair in Investment Management at the Hankamer School of Business at

Tax Reform: An Overview of Proposals in the 112 th Congress

Tax Reform: An Overview of Proposals in the 112 th Congress James M. Bickley Specialist in Public Finance January 14, 2011 Congressional Research Service CRS Report for Congress Prepared for Members and

Tax Reform: An Overview of Proposals in the 112 th Congress James M. Bickley Specialist in Public Finance January 14, 2011 Congressional Research Service CRS Report for Congress Prepared for Members and

THE BUFFETT RULE: A BASIC PRINCIPLE OF TAX FAIRNESS. The National Economic Council

THE BUFFETT RULE: A BASIC PRINCIPLE OF TAX FAIRNESS The National Economic Council April 2012 The Buffett Rule: A Basic Principle of Tax Fairness The Buffett Rule is the basic principle that no household

THE BUFFETT RULE: A BASIC PRINCIPLE OF TAX FAIRNESS The National Economic Council April 2012 The Buffett Rule: A Basic Principle of Tax Fairness The Buffett Rule is the basic principle that no household

Preserving Retirement Assets: An IRA Rollover Review

Preserving Retirement Assets: An IRA Rollover Review How will you replace your income when you retire? What will happen to your standard of living when your income ceases at retirement? Table of Contents

Preserving Retirement Assets: An IRA Rollover Review How will you replace your income when you retire? What will happen to your standard of living when your income ceases at retirement? Table of Contents

Chapter 3: The effect of taxation on behaviour. Alain Trannoy AMSE & EHESS

Chapter 3: The effect of taxation on behaviour Alain Trannoy AMSE & EHESS Introduction The most important empirical question for economics: the behavorial response to taxes Calibration of macro models

Chapter 3: The effect of taxation on behaviour Alain Trannoy AMSE & EHESS Introduction The most important empirical question for economics: the behavorial response to taxes Calibration of macro models

Effects of Income Tax Changes on Economic Growth

September 2014 William G. Gale, and Tax Policy Center Andrew A. Samwick, Dartmouth College and National Bureau of Economic Research Abstract This paper examines how changes to the individual income tax

September 2014 William G. Gale, and Tax Policy Center Andrew A. Samwick, Dartmouth College and National Bureau of Economic Research Abstract This paper examines how changes to the individual income tax

Taxes and Financing Decisions

Taxes and Financing Decisions Jonathan Lewellen * MIT and NBER lewellen@mit.edu Katharina Lewellen + MIT klew@mit.edu Revision: February 2005 First draft: June 2003 We are grateful to Nittai Bergman, Ian

Taxes and Financing Decisions Jonathan Lewellen * MIT and NBER lewellen@mit.edu Katharina Lewellen + MIT klew@mit.edu Revision: February 2005 First draft: June 2003 We are grateful to Nittai Bergman, Ian

Do Dividend Taxes Affect Corporate Investment?

Arbeitskreis Quantitative Steuerlehre Quantitative Research in Taxation Discussion Papers Annette Alstadsæter / Martin Jacob Do Dividend Taxes Affect Corporate Investment? arqus Discussion Paper No. 172

Arbeitskreis Quantitative Steuerlehre Quantitative Research in Taxation Discussion Papers Annette Alstadsæter / Martin Jacob Do Dividend Taxes Affect Corporate Investment? arqus Discussion Paper No. 172