TIN Matching Compliance and Procedures

|

|

|

- Imogene Harvey

- 8 years ago

- Views:

Transcription

1 TIN Matching Compliance and Procedures FEATURED FACULTY: Teresa Erwin - Managing Partner / Accounting & Tax Consultant teresaerwin@myjdtassociates.com

2 Teresa Erwin - Managing Partner / Accounting & Tax Consultant After college in 1984, Teresa began her career as an accountant in the banking industry. She opened JDT Associates in 1990 to assist small business owners with Accounting, Income Tax and Management matters. Since then Teresa has been practicing various accounting and management functions. In 2005, when her son, Travis, joined her in business, JDT Associates went from sole proprietor to a partnership. Together they purchased an insurance brokerage and expanded the business to a full service financial firm. Teresa has a diverse background which includes partnership and corporate taxation, individual tax compliance and planning, trust and estate tax planning, and outside controller services for several industries including manufacturing, distribution, construction and hospitality. Teresa obtained her education most recently at Western State University, College of Law. Other institutions include Pepperdine University and Cal State L.A. Teresa treats every client with respect and integrity. She is dedicated to helping clients make intelligent financial decisions and ethically minimize tax liability. Her patience and determination ensure that every client is treated with regard.

3 **Certificates of attendance and CEUs, when available, must be requested through the online evaluation.** Evaluation for Live Event: We d like to hear what you thought about the audio conference. Please take a moment to fill in the survey located here: Requests for continuing education credits and certificates of attendance must be submitted within 10 days of the live event. Evaluation for CD Recording: Please use the following link to submit your evaluation of the recorded event: Please note: All links are case sensitive Receive 1.5 CPE credits by attending the live Audio Conference! CCM is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be addressed to the National Registry of CPE Sponsors, 150 Fourth Avenue North, Suite 700, Nashville, TN, Web site: Program Level: Intermediate Prerequisites: This course is for participants with some exposure to the subject. Advanced Preparation: None Delivery: Group Live CPE Credits: 1.5 Recordings of the program do not qualify for CPE credits. For more information regarding administrative policies such as complaint and refund, please contact our offices at C4CM (2426).

4 This image cannot currently be displayed. Brought to you by: Center for Competitive Management & Teresa Erwin, JDT Associates 1

5 The program is established for payers of Form 1099 income subject to the backup withholding provisions of section 3406(a)(1)(A) and (B) of the Internal Revenue Code. Prior to filing an information return, a Program participant may check the TIN (Taxpayer Identification Number) furnished by the payee against the name/tin (Taxpayer Identification Number) combination contained in the Internal Revenue Service database maintained for the Program. The IRS will maintain a separate name/tin (Taxpayer Identification Number) database specifically for the program and will inform the payor whether or not the name/tin (Taxpayer Identification Number) combination furnished by the payee matches a name/tin (taxpayer Identification Number) combination in the database. 2

database specifically for the program and will inform the payor whether or not the name/tin (Taxpayer")

6 The matching details provided to participating payors, and their authorized agents, will help avoid TIN (Taxpayer Identification Number) errors and reduce the number of backup withholding notice required under Section 3406(a)(1)(B) of the Internal Revenue Code. IRC Section 6721 provides a payer may be subject to a penalty for failure to file a complete and accurate information return, including a failure to include the correct payee TIN. The penalty is $50 per return, with a maximum penalty of $250,000 per year ($100,000 for small businesses). The penalty for intentional disregard is $100 per return, with no maximum penalty. Participant means a person that is either a payor, or a payors authorized agent and, that has applied and been accepted to participate in the Program. Participating Payor means a payor that is participating in the Program either on its own behalf or through an authorized agent that is a participant. Payee means a person with respect to whom a reportable payment, as defined in 3406(b), has been made or is likely to be made by a participating payor. Account - means any account, instrument, contract, or other relationship with a payee with respect to which a payer is likely to make a reportable payment. (See section (e) of the Temporary Employment Tax Regulations). Reportable Payment means interest and dividend payments as defined in IRC section 3406(b)(2), and other reportable payments as defined in IRC section 3406(b)(3). TIN means the taxpayer identification number that a payee is required to furnish to a payor. The TIN may be an Employer Identification Number (EIN), a Social Security Number (SSN), or an Internal Revenue Service Individual Taxpayer Identification Number (ITIN), per IRC section Principal means a partner or an individual who owns at least five percent (5%) of the firm that is applying to participate in the TIN Matching Program. The Principal may also be a corporate officer of a publicly traded firm, such as President, Vice- President, Secretary or Treasurer. The Principal must be the person who can legally bind the firm in matters before the IRS and must complete the original Application to TIN Match on behalf of the firm. Responsible Official means an individual who holds a supervisory position within the firm. A Responsible Official has the authority to update an application on behalf of their listed firm and firm Principal. The Responsible Official may also assign/disable authorized agent and delegated user roles, update locations and perform TIN Matching. Authorized Agent means a person or firm that, with the payor s authorization, transmits specific information Returns (IRP) documents to the IRS on behalf of the firm and may match name/tin combinations on behalf of the payor. An Authorized Agent may assign/disable user access within their assigned location, update their location address information and perform TIN Matching. Delegated User means an individual who will utilize the TIN Matching session options on behalf of the firm. A Delegated User may not assign or disable users or update applications on behalf of their assigned firm. A Delegated User may only perform TIN Matching on behalf of their assigned firm. Transmitter - means the Federal agency sending in the magnetic tape cartridge containing the TINs for matching purposes. Transmitter Control Code - TCC - means the IRS assigned code for each participant. Authorized Payor - means a payor who has filed Information Returns with the IRS in at least one of the two preceding tax years. 3

. The penalty for intentional disregard is $100 per return, with no maximum penalty.")

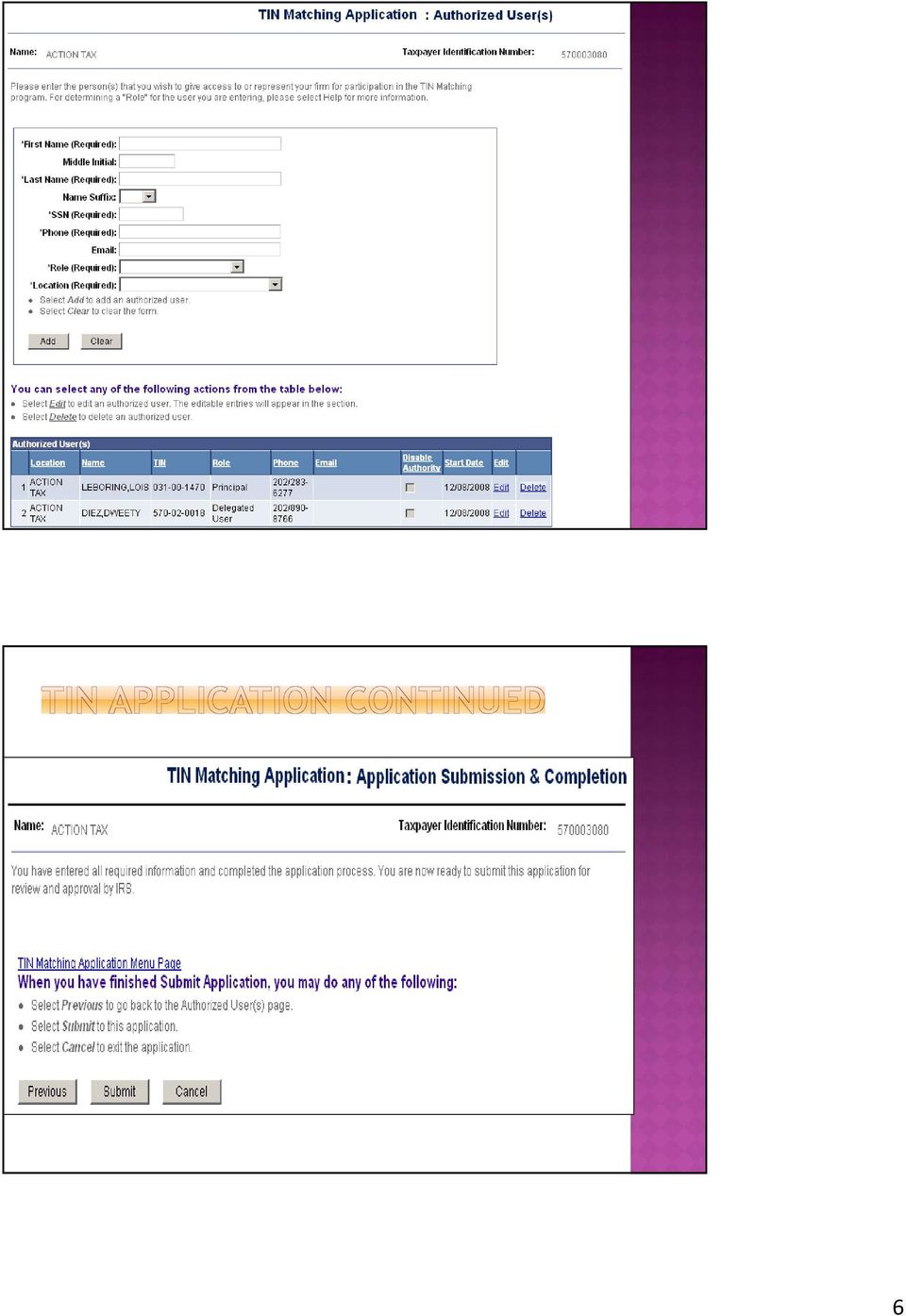

7 Required Information to complete application. Your firm's legal name, address, and phone number Your firm's Employer Identification Number (EIN). If your firm is a sole proprietorship without an EIN, you will need the proprietor's Social Security Number (SSN). The physical address of all locations of your firm which will be performing TIN Matching The names, SSNs and phone numbers of the authorized users within your organization The Personal Identification Number (PIN) you selected during the initial registration process Application will be completed through IRS e-services 4

you selected during the initial registration process Application will be")

8 5

9 6

10 Interactive TIN Matching Can submit up to 25 name/tin combinations at a time and receive a response within 5 seconds. 7

11 Bulk TIN Matching May download.txt files composed of up to 100,000 name/tin combinations and receive a response within 24 hrs. TIN TYPE;TIN NUMBER;TIN NAME;ACCOUNT NUMBER (optional) Taxpayer Identification Number (TIN) Type is a one-digit number; "1" represents an Employer Identification Number (EIN) "2" represents a Social Security Number (SSN), "3" represents an "unknown" TIN type TIN Number is the nine-digit SSN or EIN for the taxpayer TIN Name is the taxpayer's full name or business name. Enter a minimum of 1 and maximum of 40 alphanumeric characters. Account Number is an optional field which may contain a payer-provided number which will help you interpret your Bulk TIN results. Use this field to identify, for example, a bank account number. Enter a maximum of 20 alphanumeric characters. 8

12 NRA withholding applies only to payments made to a payee that is a foreign person. Usually 30% unless there is a tax treaty in place. Payee is identified as U.S. or foreign based on the documentation provided In most cases this is the person to whom you make the payment regardless of whether the person is the beneficial owner of the income. However there are some situations in which the payee is a person other than the one to whom you make the payment Wages and Salaries Interest Received Dividends Business Income Capital Gains and Losses Pensions and Annuities Lump-Sum Distributions Rollovers from Retirement Plans Rental Income & Expenses Farming and Fishing Income Earnings for Clergy Gambling Income and Losses Bartering Income Scholarship and Fellowship Grants Social Security and Equivalent Railroad Retirement Benefits 401(k) Plans Canceled Debt 9

13 Taxpaying Entities Individual Disregarded entities C Corporation Flow Through Entity AKA Fiscally Transparent Entity Sole Proprietor S corporation Partnerships LLCs LLPs PLLC Trusts Individual/Foreign Person Resident Resident Alien Nonresident Alien Domestic/Foreign Disregarded entities Domestic/Foreign Flow Through Entity 10

14 U.S. Agent of Foreign Persons If you have knowledge that the payee is an agent of a foreign person you must treat the payment as made to a foreign person May be treated as made to a U.S. person if this person is a financial institution Foreign Intermediaries Qualified Intermediary any foreign intermediary that has entered into a qualified intermediary withholding agreement with the IRS. You can determine whether a QI has assumed responsibility from the Form W- 8IMY provided by the QI. Must Have Form W-8IMY to treat as U.S. Person. Nonqualified Intermediary nonqualified intermediary, foreign flow-through entity, or U.S. branch that is using Form W-8IMY to transmit information about account holders, you can treat the payment as reliably associated with valid documentation only if, the following 3 requirements are met prior to making the payment: You can allocate the payment to a valid Form W-8IMY, You can reliably determine how much of the payment relates to valid documentation provided by a payee and You have sufficient information to report the payment on Form W-8IMY or Form 1099, if reporting is required. Form W-9 for U.S. Payees Can be obtained from the IRS via Back Up withholding rate is 28% Form W-8 Series for foreign Payees Can be obtained from the IRS via NRA withholding rate is 30% unless a tax treaty applies Order Forms by mail Products 11

15 Payments subject to backup withholding: Backup withholding can apply to most kinds of payments that are reported on Form Interest payments (Form 1099 INT) Dividends (Form 1099 DIV) Patronage dividends, but only if at least half of the payment is in money (Form 1099 PATR) Rents, profits, or other gains (Form 1099 MISC) Commissions, fees, or other payments for work you do as an independent contractor (Form 1099 MISC) Royalty payments (Form 1099 MISC), and Certain other payments. Backup withholding also may apply to gambling winnings (Form W-2G), unless subject to regular gambling withholding. Withholding rules. The bank or other business must issue Form W-9, Request for Taxpayer Identification Number and Certification, or a similar form. The Payee must enter their TIN on the form and must certify (under penalties of perjury) that their TIN is correct and that they are not subject to backup withholding. When a new account is opened When an investment is made When payments reported on Form 1099 begin The payer must withhold at a flat 28% rate in the following situations: Payee does not give the payer their TIN in the required manner The IRS notifies the payer that the TIN you given is incorrect The payee is required, but fails, to certify that they are not subject to backup withholding The IRS notifies the payer to start withholding on interest or dividends because the payee has underreported interest or dividends on their income tax return. The IRS will do this only after it has mailed the payee four notices over at least a 210-day period. 12

, unless subject to regular gambling withholding. Withholding rules.")

16 The payer must withhold at a flat 28% rate in the following situations: Payee does not give the payer their TIN in the required manner The IRS notifies the payer that the TIN you given is incorrect The payee is required, but fails, to certify that they are not subject to backup withholding The IRS notifies the payer to start withholding on interest or dividends because the payee has underreported interest or dividends on their income tax return. The IRS will do this only after it has mailed the payee four notices over at least a 210-day period. After receiving a CP2100 or CP2100A For Missing TINs if not already withholding begin withholding Immediately. Continue until TIN is received 3 Solicitations must be made to avoid a penalty for failure to include TIN on the information return Initial This should be done when the account is opened. If Payee fails to provide backup withholding should begin immediately. First annual Must be made by December 31 of the year in which the account is opened (for accounts opened before December) or January 31 of the following year (for accounts opened during the preceding December). Second Annual Must be made by December 31 of the year following the calendar year in which the account was opened. 13

17 For Incorrect TINs Compare the accounts on the listing with your business records. If your records do not agree this could be the result of a recent update to SSA records, an error in the information you submitted, or an IRS processing error. If this type of error occurred, the only thing you should do is correct or update your records, if necessary. If payees Name/TIN combination and account number on your records agree with the combination the IRS identified as incorrect you must send a B notice and form W-9 to the Payee. This requires that up to two annual solicitations be made in response to the CP2100 or CP 2100A First B notice must be sent within 15 business days after receiving the CP2100 or CP2100A. If a Proposed Penalty Notice (972CG) is received the annual solicitation must be made by December 31 st unless a B notice has already been sent out. You must send the second B Notice to a payee after you receive a second CP2100 or CP2100A Notice within a 3 calendar year period. The Second B Notice tells the payee to contact IRS or SSA to obtain the correct Name/TIN combination. The mailing of the second notice should not include a Form W-9. The payee must certify the Name/TIN combination after receiving the second B Notice. Most types of U.S. source income are subject to U.S. tax of 30% A reduced rate, including exemption may apply if there is a tax treaty between the foreign persons country of residence and the U.S. Tax is generally withheld from the payment made to the foreign person. 14

18 Subject to NRA withholding if it is from a source within the U.S. and it is either: Fixed or determinable annual or periodic (FDAP) income. Certain gains from the disposition of timber, coal, and iron ore, or from the sale or exchange of patents, copyrights, and similar intangible property. Subject to NRA withholding if withholding is specifically required even though income may not constitute U.S. source income or FDAP income. Corporate distributions may be subject to NRA withholding even though a portion of the distribution may be a return of capital or capital gain that would not otherwise be subject to NRA withholding 15

19 Summary of Source Rules for FDAP Income IF you have: Pay for personal services THEN the source of that income is determined by: Where the service is performed Dividends Interest Rents Royalties-Patents, copyrights, etc Royalties-Natural resources Pensions: Distributions attributable to contributions The type of corporation (U.S. or foreign) The residence of the payer Where the property is located Where the property is used Where the property is located Where the services were performed while a nonresident alien Pensions: Investment earnings on contributions Scholarships and fellowship grants Guarantee of indebtedness The location of the pension trust In most cases the residence of the payer The residence of the debtor whether the payment is effectively connected with a U.S. trade or business Employees services are performed partly in the United States and partly outside the United States by an employee allocation of pay, other than certain fringe benefits, is determined on a time basis. The following fringe benefits are sourced on a geographical basis as shown below. Housing employee's main job location. Education employee's main job location. Local transportation employee's main job location. Tax reimbursement jurisdiction imposing tax. Hazardous or hardship duty pay location of pay zone. Moving expense reimbursement employee's new main job location. main job location (principal place of work) is usually the place where the employee spends most of his or her working time If no one place is where most of the work time is spent, the main job location is the place where the work is centered, such as where the employee reports for work or is otherwise required to base his or her work. 16

20 Territorial limits. Wages received for services rendered inside the territorial limits of the United States and wages of an alien seaman earned on a voyage along the coast of the United States are regarded as from sources in the United States. Wages or salaries for personal services performed in a mine or on an oil or gas well located or being developed on the continental shelf of the United States are treated as from sources in the United States. Income from the performance of services directly related to the use of a vessel or aircraft is treated as derived entirely from sources in the United States if the use begins and ends in the United States. This income is subject to NRA withholding if it is not effectively connected with a U.S. trade or business. If the use either begins or ends in the U.S. it will fall under transportation income Crew members. Income from the performance of services by a nonresident alien in connection with the individual's temporary presence in the United States as a regular member of the crew of a foreign vessel engaged in transportation between the United States and a foreign country or a U.S. possession is not income from U.S. sources. 17

21 Scholarships, fellowships, and grants. Scholarships, fellowships, and grants are sourced according to the residence of the payer. Those made by entities created or domiciled in the United States are generally treated as income from sources within the United States. However, those made by entities created or domiciled in a foreign country are treated as income from foreign sources. Activities outside the United States. A scholarship, fellowship, grant, targeted grant, or an achievement award received by a nonresident alien for activities conducted outside the United States is treated as foreign source income. Pension payments. The source of pension payments is determined by the part of the distribution that constitutes the compensation element (employer contributions) and the part that constitutes the earnings element (the investment income). The compensation element is sourced the same as compensation from the performance of personal services. The part attributable to services performed in the United States is U.S. source income, and the part attributable to services performed outside the United States is foreign source income. Employer contributions to a defined benefit plan covering more than one individual are not made for the benefit of a specific participant, but are made based on the total liabilities to all participants. All funds held under the plan are available to provide benefits to any participant. If the payment is from such a plan, you can use the method in Revenue Procedure to allocate the payment to sources in and out of the United States. The earnings part of a pension payment is U.S. source income if the trust is a U.S. trust. 18

22 FDAP income is all income except: Gains from the sale of property (including market discount and option premiums but not including original issue discount), and Items of income excluded from gross income without regard to U.S. or foreign status of the owner of the income, such as tax-exempt municipal bond interest and qualified scholarship income. Compensation for personal services. Dividends, including dividend equivalent payments. Interest. Original issue discount. REMIC excess inclusion income. Pensions and annuities. Alimony. Real property income, such as rents, other than gains from the sale of real property. Royalties. Taxable scholarships and fellowship grants. Other taxable grants, prizes, and awards. A sales commission paid or credited monthly. A commission paid for a single transaction. The distributable net income of an estate or trust that is FDAP income and must be distributed currently, or has been paid or credited during the tax year. FDAP income distributed by a partnership that, or such an amount that, although not actually distributed, is includible in the gross income of a foreign partner. Taxes, mortgage interest, or insurance premiums paid to or for the account of, a nonresident alien landlord by a tenant under the terms of a lease. Publication rights. Prizes awarded to nonresident alien artists for pictures exhibited in the United States. Purses paid to nonresident alien boxers for prize fights in the United States. Prizes awarded to nonresident alien professional golfers in golfing tournaments in the United States. 19

23 Installment payments. Income can be FDAP income whether it is paid in a series of repeated payments or in a single lump sum. For example, $5,000 in royalty income would be FDAP income whether paid in 10 payments of $500 each or in one payment of $5,000. Insurance proceeds. Income derived by an insured nonresident alien from U.S. sources upon the surrender of, or at the maturity of, a life insurance policy, is FDAP income and is subject to NRA withholding. This includes income derived under a life insurance contract issued by a foreign branch of a U.S. life insurance company. The proceeds are income to the extent they exceed the cost of the policy. However, certain payments received under a life insurance contract on the life of a terminally or chronically ill individual before death (accelerated death benefits) may not be subject to tax. This also applies to certain payments received for the sale or assignment of any part of the death benefit under contract to a viatical settlement provider. Racing purses. Racing purses are FDAP income and racetrack operators must withhold 30% on any purse paid to a nonresident alien racehorse owner in the absence of definite information contained in a statement filed together with a Form W-8BEN that the owner has not raced, or does not intend to enter, a horse in another race in the United States during the tax year. If available information indicates that the racehorse owner has raced a horse in another race in the United States during the tax year, then the statement and Form W-8BEN filed for that year are ineffective. The owner may be exempt from withholding of tax at 30% on the purses if the owner gives you Form W-8ECI, which provides that the income is effectively connected with the conduct of a U.S. trade or business and that the income is includible in the owner's gross income. Covenant not to compete. Payment received for a promise not to compete is generally FDAP income. Its source is the place where the promisor forfeited his or her right to act. Amounts paid to a nonresident alien for his or her promise not to compete in the United States are subject to NRA withholding. 20

24 Effectively Connected Income In most cases, when a foreign person engages in a trade or business in the United States, all income from sources in the United States connected with the conduct of that trade or business is considered effectively connected with a U.S. business. FDAP income may or may not be effectively connected with a U.S. business. For example, effectively connected income includes rents from real property if the alien chooses to treat that income as effectively connected with a U.S. trade or business. The factors to be considered in establishing whether FDAP income and similar amounts are effectively connected with a U.S. trade or business include: Whether the income is from assets used in, or held for use in, the conduct of that trade or business; or Whether the activities of that trade or business were a material factor in the realization of the income. Income from securities. There is a special rule determining whether income from securities is effectively connected with the active conduct of a U.S. banking, financing, or similar business. If the foreign person's U.S. office actively and materially participates in soliciting, negotiating, or performing other activities required to arrange the acquisition of securities, the U.S. source interest or dividend income from the securities, gain or loss from their sale or exchange, income or gain economically equivalent to such amounts, or amounts received for providing a guarantee of indebtedness, is attributable to the U.S. office and is effectively connected income. 21

25 Portfolio interest on bearer obligations or foreign-targeted registered obligations if those obligations meet certain requirements. Bank deposit interest that is not effectively connected with the conduct of a U.S. trade or business. Original issue discount on certain short- term obligations. Non-business gambling income of a nonresident alien playing blackjack, baccarat, craps, roulette, or big-6 wheel in the United States. Amounts paid as part of the purchase price of an obligation sold between interest payment dates. Original issue discount paid on the sale of an obligation other than a redemption. Insurance premiums paid on a contract issued by a foreign insurer. 22

Information Reporting Forms 1099. Sponsored by Office of Financial Management and Internal Revenue Service December 12, 2012

Information Reporting Forms 1099 Sponsored by Office of Financial Management and Internal Revenue Service December 12, 2012 Information Reporting Form Code Section 1098 6050H 1098-E 6050S 1098-T 6050S

Information Reporting Forms 1099 Sponsored by Office of Financial Management and Internal Revenue Service December 12, 2012 Information Reporting Form Code Section 1098 6050H 1098-E 6050S 1098-T 6050S

Withholding of Tax on Nonresident Aliens and Foreign Entities

Department of the Treasury Internal Revenue Service Publication 515 Cat. No. 15019L Withholding of Tax on Nonresident Aliens and Foreign Entities For use in 2013 Contents What's New... 1 Reminders... 2

Department of the Treasury Internal Revenue Service Publication 515 Cat. No. 15019L Withholding of Tax on Nonresident Aliens and Foreign Entities For use in 2013 Contents What's New... 1 Reminders... 2

1. Nonresident Alien or Resident Alien?

U..S.. Tax Guiide for Non-Resiidents Table of Contents A. U.S. INCOME TAXES ON NON-RESIDENTS 1. Nonresident Alien or Resident Alien? o Nonresident Aliens o Resident Aliens Green Card Test Substantial Presence

U..S.. Tax Guiide for Non-Resiidents Table of Contents A. U.S. INCOME TAXES ON NON-RESIDENTS 1. Nonresident Alien or Resident Alien? o Nonresident Aliens o Resident Aliens Green Card Test Substantial Presence

How To Participate In The Taxpayer Identification Number Matching Program

On-Line Taxpayer Identification Number (TIN) MATCHING PROGRAM PUBLICATION 2108A Guidelines and Instructions for the Interactive and Bulk On-Line Taxpayer Identification Number (TIN) Matching Programs INTENDED

On-Line Taxpayer Identification Number (TIN) MATCHING PROGRAM PUBLICATION 2108A Guidelines and Instructions for the Interactive and Bulk On-Line Taxpayer Identification Number (TIN) Matching Programs INTENDED

Instructions for the Requester of Forms W 8BEN, W 8BEN E, W 8ECI, W 8EXP, and W 8IMY (Rev. July 2014)

") Instructions for the Requester of Forms W 8BEN, W 8BEN E, W 8ECI, W 8EXP, and W 8IMY (Rev. July 2014) Section references are to the Internal Revenue Code unless otherwise noted. Future developments. For

Instructions for the Requester of Forms W 8BEN, W 8BEN E, W 8ECI, W 8EXP, and W 8IMY (Rev. July 2014) Section references are to the Internal Revenue Code unless otherwise noted. Future developments. For

Application Procedures for Qualified Intermediary Status Under Section 1441; Final Qualified Intermediary Withholding Agreement

Part III Administrative, Procedural, and Miscellaneous Application Procedures for Qualified Intermediary Status Under Section 1441; Final Qualified Intermediary Withholding Agreement Rev. Proc 2000-12

Part III Administrative, Procedural, and Miscellaneous Application Procedures for Qualified Intermediary Status Under Section 1441; Final Qualified Intermediary Withholding Agreement Rev. Proc 2000-12

Vendor & Supplier Guide

Vendor & Supplier Guide IRS & FTB Withholding Guidelines for Foreign Payees California Institute of Technology Payment Services Department 1200 E. California Blvd., Suite 101, MC 103-6, Pasadena, CA 91125

Vendor & Supplier Guide IRS & FTB Withholding Guidelines for Foreign Payees California Institute of Technology Payment Services Department 1200 E. California Blvd., Suite 101, MC 103-6, Pasadena, CA 91125

IRS FORM 1099 REPORTING REQUIREMENTS

IRS FORM 1099 REPORTING REQUIREMENTS The Internal Revenue Service (IRS) requires businesses (including not-for-profit organizations) to issue a Form 1099 to any individual or unincorporated business paid

IRS FORM 1099 REPORTING REQUIREMENTS The Internal Revenue Service (IRS) requires businesses (including not-for-profit organizations) to issue a Form 1099 to any individual or unincorporated business paid

Babcock & Brown Infrastructure. Guide for Completing IRS Forms: W-8IMY & W-8BEN

Babcock & Brown Infrastructure Guide for Completing IRS Forms: W-8IMY & W-8BEN GUIDE FOR COMPLETING IRS FORMS: W-8IMY & W-8BEN Contents Introduction...2 Guide for Completing Form W-8IMY...3 Guide for Completing

Babcock & Brown Infrastructure Guide for Completing IRS Forms: W-8IMY & W-8BEN GUIDE FOR COMPLETING IRS FORMS: W-8IMY & W-8BEN Contents Introduction...2 Guide for Completing Form W-8IMY...3 Guide for Completing

Limited Liability: Owners of a LLC have the limited liability protection of a corporation.

Type of Business Structures & Abbreviation Limited Liability Company (LLC) Description A Limited Liability Company (LLC) is generally accepted type of small business entity. For the majority of small business

Type of Business Structures & Abbreviation Limited Liability Company (LLC) Description A Limited Liability Company (LLC) is generally accepted type of small business entity. For the majority of small business

IMPORTANT INFORMATION PLEASE READ BEFORE FILLING OUT FORM

CASH WITHDRAWAL from your After-Tax Annuity IMPORTANT INFORMATION PLEASE READ BEFORE FILLING OUT FORM Questions? For account information, to check the status of your request or any other questions, call:

CASH WITHDRAWAL from your After-Tax Annuity IMPORTANT INFORMATION PLEASE READ BEFORE FILLING OUT FORM Questions? For account information, to check the status of your request or any other questions, call:

Customer Tax Guide - U.S.A. Debt Securities Equities Withholding Tax Capital Gains Tax Stamp Duty

Customer Tax Guide - U.S.A. Debt Securities Equities Withholding Tax Capital Gains Tax Stamp Duty March 2013 Customer Tax Guide - U.S.A. March 2013 edition Document No. US6065 This document is the property

Customer Tax Guide - U.S.A. Debt Securities Equities Withholding Tax Capital Gains Tax Stamp Duty March 2013 Customer Tax Guide - U.S.A. March 2013 edition Document No. US6065 This document is the property

DISCLAIMER. The information contained in this presentation is current as of the date it was presented. It should not be considered official guidance.

DISCLAIMER The information contained in this presentation is current as of the date it was presented. It should not be considered official guidance. 1 INTRODUCTION This webinar is intended to provide basic

DISCLAIMER The information contained in this presentation is current as of the date it was presented. It should not be considered official guidance. 1 INTRODUCTION This webinar is intended to provide basic

CONTRACTOR APPLICATION HOUSING REHABILITATION PROGRAM

CITY OF GALVESTON GRANTS & HOUSING DEPARTMENT P.O. Box 779 Galveston, Texas 77553 Office (409) 797 3820 Fax (409) 797 3888 CONTRACTOR APPLICATION HOUSING REHABILITATION PROGRAM CONTRACTOR APPLICATION HOUSING

CITY OF GALVESTON GRANTS & HOUSING DEPARTMENT P.O. Box 779 Galveston, Texas 77553 Office (409) 797 3820 Fax (409) 797 3888 CONTRACTOR APPLICATION HOUSING REHABILITATION PROGRAM CONTRACTOR APPLICATION HOUSING

IMPORTANT INFORMATION PLEASE READ BEFORE FILLING OUT FORM

CASH WITHDRAWAL IMPORTANT INFORMATION PLEASE READ BEFORE FILLING OUT FORM Questions? For account information, to check the status of your request or any other questions, call: 800 223-1200, Monday - Friday,

CASH WITHDRAWAL IMPORTANT INFORMATION PLEASE READ BEFORE FILLING OUT FORM Questions? For account information, to check the status of your request or any other questions, call: 800 223-1200, Monday - Friday,

HCUL TECHNICAL DATE PAGE ADVISORY GUIDE 5/14/04 IIIH 1 BACKUP WITHHOLDING

ADVISORY GUIDE 5/14/04 IIIH 1 OVERVIEW Backup withholding is federally mandated by the Interest and Dividend Tax Compliance Act of 1983. The intent of the Act is to ensure that interest and dividends are

ADVISORY GUIDE 5/14/04 IIIH 1 OVERVIEW Backup withholding is federally mandated by the Interest and Dividend Tax Compliance Act of 1983. The intent of the Act is to ensure that interest and dividends are

Form 1099 Miscellaneous The Good, The Bad, and The Ugly

Form 1099 Miscellaneous The Good, The Bad, and The Ugly Complimentary Guidance from The Tax Office, Inc., on What Can Happen If You Do Not File Your 1099-Misc Forms Table of Contents What is a Form 1099

Form 1099 Miscellaneous The Good, The Bad, and The Ugly Complimentary Guidance from The Tax Office, Inc., on What Can Happen If You Do Not File Your 1099-Misc Forms Table of Contents What is a Form 1099

Request for Taxpayer Identification Number and Certification

Form W-9 (Rev. December 2014) Department of the Treasury Internal Revenue Service Request for Taxpayer Identification Number and Certification 1 Name (as shown on your income tax return). Name is required

Form W-9 (Rev. December 2014) Department of the Treasury Internal Revenue Service Request for Taxpayer Identification Number and Certification 1 Name (as shown on your income tax return). Name is required

STATE OF WYOMING WOLFS-109(a)

") STATE OF WYOMING WOLFS-109(a) The State of Wyoming must have a properly completed form before payment will be made. STATE AGENCY INFORMATION Agency #, Agency Name, Contact Name, Title, Address; Phone #

STATE OF WYOMING WOLFS-109(a) The State of Wyoming must have a properly completed form before payment will be made. STATE AGENCY INFORMATION Agency #, Agency Name, Contact Name, Title, Address; Phone #

Missouri Lottery Winner Claim Form Official Missouri Lottery Claim Form

[ STAPLE TICKET HERE ] Missouri Lottery Winner Claim Form Official Missouri Lottery Claim Form A B C PLEASE PRINT your name, address and phone number on the back of your ticket - YOU MUST SIGN YOUR TICKET.

[ STAPLE TICKET HERE ] Missouri Lottery Winner Claim Form Official Missouri Lottery Claim Form A B C PLEASE PRINT your name, address and phone number on the back of your ticket - YOU MUST SIGN YOUR TICKET.

FORM 1099 MISC REMINDERS FOR STATE AND LOCAL GOVERNMENTS

FORM 1099 MISC REMINDERS FOR STATE AND LOCAL GOVERNMENTS WHO MUST FILE Any entity conducting a trade or business is required to file Form 1099. Government Agencies and non-profit organizations are also

FORM 1099 MISC REMINDERS FOR STATE AND LOCAL GOVERNMENTS WHO MUST FILE Any entity conducting a trade or business is required to file Form 1099. Government Agencies and non-profit organizations are also

Guideline Income Tax Withholding

Guideline Income Tax Withholding Information Returns Ryan Rauschenberger For Tax Year 2015 Tax Commissioner Information returns for payments other than wages Form 1099, 1042-S and W-2G Who must file Every

Guideline Income Tax Withholding Information Returns Ryan Rauschenberger For Tax Year 2015 Tax Commissioner Information returns for payments other than wages Form 1099, 1042-S and W-2G Who must file Every

TAX ASPECTS OF MUTUAL FUND INVESTING

Tax Guide for 2015 TAX ASPECTS OF MUTUAL FUND INVESTING INTRODUCTION I. Mutual Fund Distributions A. Distributions From All Mutual Funds 1. Net Investment Income and Short-Term Capital Gain Distributions

Tax Guide for 2015 TAX ASPECTS OF MUTUAL FUND INVESTING INTRODUCTION I. Mutual Fund Distributions A. Distributions From All Mutual Funds 1. Net Investment Income and Short-Term Capital Gain Distributions

Instructions for Forms 1099-INT and 1099-OID

2009 Instructions for Forms 1099-INT and 1099-OID Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless This interest is not subject to backup withholding.

2009 Instructions for Forms 1099-INT and 1099-OID Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless This interest is not subject to backup withholding.

FOREIGNERS DOING BUSINESS IN THE UNITED STATES U.S. Taxation Overview

FOREIGNERS DOING BUSINESS IN THE UNITED STATES U.S. Taxation Overview The U.S. economic activities of foreign individuals and entities are classified as inbound transactions while the foreign economic

FOREIGNERS DOING BUSINESS IN THE UNITED STATES U.S. Taxation Overview The U.S. economic activities of foreign individuals and entities are classified as inbound transactions while the foreign economic

AUTOMATED INQUIRY AND MATCH PROCEDURES 01-01-02 RESOURCE TYPE DESCRIPTION:

FRR RESOURCE TYPES AND DESCRIPTIONS The following are resource types and descriptions that may appear on the annual report. ADWINIDWG AGGPROFLOS AGRISUBS BUSINCOME CAPGAINS CAPGNBSNST CAPGNRLPRO CAPRATEGN

FRR RESOURCE TYPES AND DESCRIPTIONS The following are resource types and descriptions that may appear on the annual report. ADWINIDWG AGGPROFLOS AGRISUBS BUSINCOME CAPGAINS CAPGNBSNST CAPGNRLPRO CAPRATEGN

How To Withhold From A Tax Return

BACKUP WITHHOLDING FOR MISSING AND INCORRECT NAME/TIN(S) (Including instructions for reading tape cartridges and CD/DVD Formats) Publication 1281 (Rev. 12-2014) Catalog Number 63327A Department of the

BACKUP WITHHOLDING FOR MISSING AND INCORRECT NAME/TIN(S) (Including instructions for reading tape cartridges and CD/DVD Formats) Publication 1281 (Rev. 12-2014) Catalog Number 63327A Department of the

North Carolina. 2016 Income Tax Withholding Tables and Instructions for Employers. www.dornc.com. NC - 30 Web 12-15. New for 2016

NC - 30 Web 12-15 North Carolina www.dornc.com 2016 Income Tax Withholding Tables and Instructions for Employers You can file your return and pay your tax online at www.dornc.com. Click on eservices. New

NC - 30 Web 12-15 North Carolina www.dornc.com 2016 Income Tax Withholding Tables and Instructions for Employers You can file your return and pay your tax online at www.dornc.com. Click on eservices. New

Iron Horse Acquisition Holding LLC 1345 Avenue of the Americas, 46 th Floor New York, New York 10105

Iron Horse Acquisition Holding LLC 1345 Avenue of the Americas, 46 th Floor New York, New York 10105 Dear Former Shareholder of Florida East Coast Industries, Inc. As you are likely aware, on July 24,

Iron Horse Acquisition Holding LLC 1345 Avenue of the Americas, 46 th Floor New York, New York 10105 Dear Former Shareholder of Florida East Coast Industries, Inc. As you are likely aware, on July 24,

Merchant Card Reporting and Form 1099-K FAQs

Merchant Card Reporting and Form 1099-K FAQs January 2014 This document contains a detailed list of answers to questions you might have about IRS Form 1099-K reporting requirements. Merchants should contact

Merchant Card Reporting and Form 1099-K FAQs January 2014 This document contains a detailed list of answers to questions you might have about IRS Form 1099-K reporting requirements. Merchants should contact

1 Rents. 2 Royalties. $ 3 Other income. 5 Fishing boat proceeds. $ 7 Nonemployee compensation

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

UNPAID CHECK FUND INSTRUCTIONS

UNPAID CHECK FUND INSTRUCTIONS How to file a claim: If you are an individual filing a claim: Complete the claimant portion of the claim form to the best of your knowledge. The claim form must include each

UNPAID CHECK FUND INSTRUCTIONS How to file a claim: If you are an individual filing a claim: Complete the claimant portion of the claim form to the best of your knowledge. The claim form must include each

UPDATED INFORMATION ON USE OF FORM W-8IMY (REVISION DATE FEBRUARY 2006) BEFORE JANUARY 1, 2015

BEFORE JANUARY 1, 2015") UPDATED INFORMATION ON USE OF FORM W-8IMY (REVISION DATE FEBRUARY 2006) BEFORE JANUARY 1, 2015 This Form W-8IMY (revision date April 2014) reflects the changes made in the Foreign Account Tax Compliance

UPDATED INFORMATION ON USE OF FORM W-8IMY (REVISION DATE FEBRUARY 2006) BEFORE JANUARY 1, 2015 This Form W-8IMY (revision date April 2014) reflects the changes made in the Foreign Account Tax Compliance

Prepared by the Disbursing Office This replaces Administrative Procedure No. A8.868 dated December 1993 A8.868 July 1996

Prepared by the Disbursing Office This replaces Administrative Procedure No. A8.868 dated December 1993 A8.868 July 1996 A8.868 Disbursing/Accounts Payable and Payroll p 1 of 53 A8.868 Reporting and Withholding

Prepared by the Disbursing Office This replaces Administrative Procedure No. A8.868 dated December 1993 A8.868 July 1996 A8.868 Disbursing/Accounts Payable and Payroll p 1 of 53 A8.868 Reporting and Withholding

University of South Florida Request for Taxpayer Identification Number and Certification Substitute IRS Form W-9

University of South Florida Request for Taxpayer Identification Number and Certification Substitute IRS Form W9 Name (as shown on your income tax return) Print or type See Specific Instructions on Instruction

University of South Florida Request for Taxpayer Identification Number and Certification Substitute IRS Form W9 Name (as shown on your income tax return) Print or type See Specific Instructions on Instruction

1 Rents. 2 Royalties. $ 3 Other income. 5 Fishing boat proceeds. $ 7 Nonemployee compensation

Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable,

Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable,

Guide to tax statements: Ameriprise brokerage and managed accounts not part of an IRA or other retirement plan

Guide to tax statements: Ameriprise brokerage and managed accounts not part of an IRA or other retirement plan Updated: Dec. 14, 2015 Table of Contents Introduction Summary Information statement (includes

Guide to tax statements: Ameriprise brokerage and managed accounts not part of an IRA or other retirement plan Updated: Dec. 14, 2015 Table of Contents Introduction Summary Information statement (includes

GENERAL INSTRUCTIONS FOR COMPLETING YOUR RETURN

GENERAL INSTRUCTIONS FOR COMPLETING YOUR RETURN PITTSBURGH CITY & SCHOOL DISTRICT The City of Pittsburgh Earned Income Tax is levied at the rate of 1% under ACT 511. The Pittsburgh School District Earned

GENERAL INSTRUCTIONS FOR COMPLETING YOUR RETURN PITTSBURGH CITY & SCHOOL DISTRICT The City of Pittsburgh Earned Income Tax is levied at the rate of 1% under ACT 511. The Pittsburgh School District Earned

TECHNICAL EXPLANATION OF THE FOREIGN ACCOUNT TAX COMPLIANCE ACT OF 2009

TECHNICAL EXPLANATION OF THE FOREIGN ACCOUNT TAX COMPLIANCE ACT OF 2009 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION October 27, 2009 JCX-42-09 CONTENTS INTRODUCTION... 1 Page I. INCREASED

TECHNICAL EXPLANATION OF THE FOREIGN ACCOUNT TAX COMPLIANCE ACT OF 2009 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION October 27, 2009 JCX-42-09 CONTENTS INTRODUCTION... 1 Page I. INCREASED

US FATCA FAQ and Glossary of FATCA terms

US FATCA FAQ and Glossary of FATCA terms These FAQs are intended to aid you in your understanding how FATCA affects your relationship with UBS. This is not intended as tax advice. If you are uncertain

US FATCA FAQ and Glossary of FATCA terms These FAQs are intended to aid you in your understanding how FATCA affects your relationship with UBS. This is not intended as tax advice. If you are uncertain

SPECIALTY INSURANCE MANAGERS OF OKLAHOMA, INC PRODUCER QUESTIONNAIRE

SPECIALTY INSURANCE MANAGERS OF OKLAHOMA, INC PRODUCER QUESTIONNAIRE Complete Legal Name of Agency Physical Address County City State ZIP Mailing Address County City State ZIP Phone Number Fax Number Business

SPECIALTY INSURANCE MANAGERS OF OKLAHOMA, INC PRODUCER QUESTIONNAIRE Complete Legal Name of Agency Physical Address County City State ZIP Mailing Address County City State ZIP Phone Number Fax Number Business

Instructions: Lines 1 through 21, on pages 1 and 2

Instructions: Lines 1 through 21, on pages 1 and 2 This form is to be used by individuals who receive income reported on Federal Forms W-2, W- 2G, Form 5754, 1099-MISC, and/or Federal Schedules C, E, F

Instructions: Lines 1 through 21, on pages 1 and 2 This form is to be used by individuals who receive income reported on Federal Forms W-2, W- 2G, Form 5754, 1099-MISC, and/or Federal Schedules C, E, F

Instructions for Forms W-2G and 5754

2016 Instructions for Forms W-2G and 5754 Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Future Developments Information

2016 Instructions for Forms W-2G and 5754 Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Future Developments Information

Original Issue Discount

Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable,

Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable,

STATE OF WYOMING WOLFS-109a Vendor Form

STATE OF WYOMING WOLFS-109a Vendor Form The State of Wyoming must have a properly completed form before payment will be made. PLEASE RETURN THIS FORM TO STATE AGENCY CONTACT VENDOR IS DOING BUSINESS WITH

STATE OF WYOMING WOLFS-109a Vendor Form The State of Wyoming must have a properly completed form before payment will be made. PLEASE RETURN THIS FORM TO STATE AGENCY CONTACT VENDOR IS DOING BUSINESS WITH

http://www.w2mate.com

Below is a Sample PDF 1099-MISC Form Generated from inside our 1099-MISC Software To learn more please visit http://www.w2mate.com VOID PAYER S name, street address, city, state, ZIP code, and telephone

Below is a Sample PDF 1099-MISC Form Generated from inside our 1099-MISC Software To learn more please visit http://www.w2mate.com VOID PAYER S name, street address, city, state, ZIP code, and telephone

CONTACT ACCOUNTS PAYABLE FOR QUESTIONS (541) 885-1226

885-1226") OREGON INSTITUTE OF TECHNOLOGY NEW VENDOR SETUP FORM Mail Attn: Accounts Payable, 3201 Campus Dr., Klamath Falls, OR 97601, or Fax (541) 885-1115 Oregon Tech Department (To be completed by Dept. Requester)

OREGON INSTITUTE OF TECHNOLOGY NEW VENDOR SETUP FORM Mail Attn: Accounts Payable, 3201 Campus Dr., Klamath Falls, OR 97601, or Fax (541) 885-1115 Oregon Tech Department (To be completed by Dept. Requester)

MISSISSIPPI RETAILER SETTLEMENT AUTHORIZATION FORM. (Full Legal Business Name)

") MISSISSIPPI RETAILER SETTLEMENT AUTHORIZATION FORM SNAP Authorization #: (Full Legal Business Name) authorizes XEROX State & Local Solutions, Inc. (XEROX) or its designee and the financial institution

MISSISSIPPI RETAILER SETTLEMENT AUTHORIZATION FORM SNAP Authorization #: (Full Legal Business Name) authorizes XEROX State & Local Solutions, Inc. (XEROX) or its designee and the financial institution

Tax Consequences for Canadians Doing Business in the U.S.

April 2012 CONTENTS U.S. basis of taxation The benefits of the Canada-U.S. tax treaty U.S. filing requirements U.S. taxpayer identification U.S. withholding Tax U.S. state taxation Other considerations

April 2012 CONTENTS U.S. basis of taxation The benefits of the Canada-U.S. tax treaty U.S. filing requirements U.S. taxpayer identification U.S. withholding Tax U.S. state taxation Other considerations

2011 Tax Information Statement reference guide

2011 Tax Information Statement reference guide Table of contents What s new for 2011 1 General information about your Tax Information Statement 2 Form 1099 Consolidated overview 4 Form 1099-B: Proceeds

2011 Tax Information Statement reference guide Table of contents What s new for 2011 1 General information about your Tax Information Statement 2 Form 1099 Consolidated overview 4 Form 1099-B: Proceeds

Type of Business. Trade Specialty. President or Owner. Address

Subcontractor Pre-Qualification Questionnaire Name of Business Trade Specialty President or Owner Address Phone Number Email Fax Number Has the company changed names within the last three years? Type of

Subcontractor Pre-Qualification Questionnaire Name of Business Trade Specialty President or Owner Address Phone Number Email Fax Number Has the company changed names within the last three years? Type of

Name: Tribal Number:

Name: Tribal Number: Drum Group Name: Indicate: Northern Southern # of Members in group Name: Address: Phone no: / Email: Tribe/Tribal Affiliation: Lead Singer: #8: #1: #2: #3: #4: #5: #6: #7: #9: #10:

Name: Tribal Number: Drum Group Name: Indicate: Northern Southern # of Members in group Name: Address: Phone no: / Email: Tribe/Tribal Affiliation: Lead Singer: #8: #1: #2: #3: #4: #5: #6: #7: #9: #10:

AHIA. Affordable Health Insurance Agency, LLC. Dear Referring Agent,

AHIA Affordable Health Affordable Health Insurance Agency, LLC 7330 San Pedro Rd., Ste 150 San Antonio, TX 78216 Toll Free (888) 803-3537 Local (210) 738-3537 Fax (210) 738-1093 Dear Referring Agent, Thank

AHIA Affordable Health Affordable Health Insurance Agency, LLC 7330 San Pedro Rd., Ste 150 San Antonio, TX 78216 Toll Free (888) 803-3537 Local (210) 738-3537 Fax (210) 738-1093 Dear Referring Agent, Thank

US Tax Issues for Foreign Partners: US Withholding Taxes & Tax Treaties

US Tax Issues for Foreign Partners: US Withholding Taxes & Tax Treaties Hope P. Krebs January 2015 2015 Duane Morris LLP. All Rights Reserved. Duane Morris is a registered service mark of Duane Morris

US Tax Issues for Foreign Partners: US Withholding Taxes & Tax Treaties Hope P. Krebs January 2015 2015 Duane Morris LLP. All Rights Reserved. Duane Morris is a registered service mark of Duane Morris

Producer Application

5300 Adolfo Road, Suite 200 Camarillo, California 93012 United with you on the road Marketing NAIC Number 10920 866-530-5500 Fax 800-761-8680 www.allianceunited.com Unidos contigo en el camino Producer

5300 Adolfo Road, Suite 200 Camarillo, California 93012 United with you on the road Marketing NAIC Number 10920 866-530-5500 Fax 800-761-8680 www.allianceunited.com Unidos contigo en el camino Producer

Form W-8BEN Completion & Submission Guidelines for Corbis Corporation Contributors

Form W-8BEN Completion & Submission Guidelines for Corbis Corporation Contributors Overview - Corbis Corporation, a US corporation, is required to deduct 30% withholding tax from royalties paid to individuals

Form W-8BEN Completion & Submission Guidelines for Corbis Corporation Contributors Overview - Corbis Corporation, a US corporation, is required to deduct 30% withholding tax from royalties paid to individuals

$ 2 Royalties. Form 1099-MISC 3 Other income. 4 Federal income tax withheld. 5 Fishing boat proceeds 6 Medical and health care payments

Attention: Do not download, print, and file Copy A with the IRS. Copy A appears in red, similar to the official IRS form, but is for informational purposes only. A penalty of 50 per information return

Attention: Do not download, print, and file Copy A with the IRS. Copy A appears in red, similar to the official IRS form, but is for informational purposes only. A penalty of 50 per information return

Year-End Fringe Benefit Reporting and Other Reporting Requirements

and Other Reporting Requirements November 2013 TO: RE: All Business Clients Year-End Fringe Benefit Reporting and Other Reporting Requirements DATE: November 20, 2013 Certain fringe benefits paid for or

and Other Reporting Requirements November 2013 TO: RE: All Business Clients Year-End Fringe Benefit Reporting and Other Reporting Requirements DATE: November 20, 2013 Certain fringe benefits paid for or

FORM FOR SPONSORSHIP OR DONATION REQUEST SUBMISSION

FORM FOR SPONSORSHIP OR DONATION REQUEST SUBMISSION TODAY S DATE: NAME OF ORGANIZATION: PERSON SUBMITTING REQUEST: NAME OF ORGANIZATION REP: EMAIL ADDRESS: STREET ADDRESS/P.O. BOX: _ TELEPHONE NUMBER(S):

FORM FOR SPONSORSHIP OR DONATION REQUEST SUBMISSION TODAY S DATE: NAME OF ORGANIZATION: PERSON SUBMITTING REQUEST: NAME OF ORGANIZATION REP: EMAIL ADDRESS: STREET ADDRESS/P.O. BOX: _ TELEPHONE NUMBER(S):

Certificate for Trust or Entity Ownership

Instructions Certificate for Trust or Entity Ownership Complete when applying for a nonqualified contract with a trust or entity as the owner or for ownership changes. Examples include contracts owned

Instructions Certificate for Trust or Entity Ownership Complete when applying for a nonqualified contract with a trust or entity as the owner or for ownership changes. Examples include contracts owned

BUSINESS ACCOUNT AGREEMENT

BUSINESS ACCOUNT AGREEMENT OWNERSHIP OF ACCOUNT SOLE PROPRIETORSHIP CORPORATION NOT FOR PROFIT CORPORATION FOR PROFIT PARTNERSHIP LIMITED LIABILITY CO. DATE OPENED OPENED BY INITIAL AMOUNT $ FORM: CASH

BUSINESS ACCOUNT AGREEMENT OWNERSHIP OF ACCOUNT SOLE PROPRIETORSHIP CORPORATION NOT FOR PROFIT CORPORATION FOR PROFIT PARTNERSHIP LIMITED LIABILITY CO. DATE OPENED OPENED BY INITIAL AMOUNT $ FORM: CASH

GUIDE TO U.S. INCOME TAXATION FOR IDB-IIC FCU MEMBERS

GUIDE TO U.S. INCOME TAXATION FOR IDB-IIC FCU MEMBERS Prepared Exclusively for IDB-IIC FCU Members by The Wolf Group, P.C. January, 2013 Copyright 2013 - The Wolf Group, P.C. January 2013 1 Copyright 2013

GUIDE TO U.S. INCOME TAXATION FOR IDB-IIC FCU MEMBERS Prepared Exclusively for IDB-IIC FCU Members by The Wolf Group, P.C. January, 2013 Copyright 2013 - The Wolf Group, P.C. January 2013 1 Copyright 2013

Enclosed are copies of the Synchrony Bank Account Agreement and Fee Schedule please retain them for future reference.

Dear Valued Customer, Thank you for your interest in establishing a business account with Synchrony Bank. Establishing an account is convenient and easy to manage. We look forward to bringing you a new

Dear Valued Customer, Thank you for your interest in establishing a business account with Synchrony Bank. Establishing an account is convenient and easy to manage. We look forward to bringing you a new

PRODUCER QUESTIONNAIRE

PRODUCER QUESTIONNAIRE Agency Name: Main Address: Phone: Fax: Email: Website: (*Note: If multiple locations, please provide address, phone, etc., on attached Schedule A.) Tax Identification Number: (*Note:

PRODUCER QUESTIONNAIRE Agency Name: Main Address: Phone: Fax: Email: Website: (*Note: If multiple locations, please provide address, phone, etc., on attached Schedule A.) Tax Identification Number: (*Note:

Merchant Reseller Application

Green Payment Processing 2905 Jordan Court, Ste B-120 Alpharetta, GA 30004 Merchant Reseller Application Company Information Section Reseller Number Company Name: Tax ID: Type of Company (Circle One) :

Green Payment Processing 2905 Jordan Court, Ste B-120 Alpharetta, GA 30004 Merchant Reseller Application Company Information Section Reseller Number Company Name: Tax ID: Type of Company (Circle One) :

Payer's RTN (optional) 1 Interest income. $ 2 Early withdrawal penalty. $ 3 Interest on U.S. Savings Bonds and Treas. obligations

1 Interest income. $ 2 Early withdrawal penalty. $ 3 Interest on U.S. Savings Bonds and Treas. obligations") Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable,

Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable,

A GUIDE TO BACKUP WITHHOLDING (for Missing and Incorrect Name/TINs)

") Department of the Treasury Internal Revenue Service Publication 1679 (Rev. 9/97) Catalogue Number 14701C A GUIDE TO BACKUP WITHHOLDING (for Missing and Incorrect Name/TINs) TABLE OF CONTENTS Page Part

Department of the Treasury Internal Revenue Service Publication 1679 (Rev. 9/97) Catalogue Number 14701C A GUIDE TO BACKUP WITHHOLDING (for Missing and Incorrect Name/TINs) TABLE OF CONTENTS Page Part

North Carolina. 2014 Income Tax Withholding Tables and Instructions for Employers. www.dornc.com. NC - 30 Web 11-13. New for 2014

NC - 30 Web 11-13 2014 Income Tax Withholding Tables and Instructions for Employers North Carolina www.dornc.com You can file your return and pay your tax online at www.dornc.com. Click on Electronic Services.

NC - 30 Web 11-13 2014 Income Tax Withholding Tables and Instructions for Employers North Carolina www.dornc.com You can file your return and pay your tax online at www.dornc.com. Click on Electronic Services.

Request For Proposal. Locum Tenens Psychiatric Coverage

Request For Proposal Locum Tenens Psychiatric Coverage Heartland Behavioral Healthcare, an innovative multi-service behavioral healthcare organization located in Massillon, Ohio, is seeking to enter into

Request For Proposal Locum Tenens Psychiatric Coverage Heartland Behavioral Healthcare, an innovative multi-service behavioral healthcare organization located in Massillon, Ohio, is seeking to enter into

PLEASE SEE IMPORTANT NOTE FOR RESIDENTS OF CERTAIN STATES LISTED AT THE BOTTOM OF THIS SHEET

PLEASE SEE IMPORTANT NOTE FOR RESIDENTS OF CERTAIN STATES LISTED AT THE BOTTOM OF THIS SHEET Dear Valued Customer, Please complete the attached Traditional IRA Request for Distribution mai P.O. Box 1 If

PLEASE SEE IMPORTANT NOTE FOR RESIDENTS OF CERTAIN STATES LISTED AT THE BOTTOM OF THIS SHEET Dear Valued Customer, Please complete the attached Traditional IRA Request for Distribution mai P.O. Box 1 If

Tips on Completing Form 1099 Misc

Certified Public Accountants Medical Dental Practice Consultants Tips on Completing Form 1099 Misc Who Must File Form 1099 Misc Form 1099 is used to report made to certain vendors (see list below). When

Certified Public Accountants Medical Dental Practice Consultants Tips on Completing Form 1099 Misc Who Must File Form 1099 Misc Form 1099 is used to report made to certain vendors (see list below). When

Nursing Educational Loan Checklist (for individuals not currently employed by Wellmont)

") Nursing Educational Loan Checklist (for individuals not currently employed by Wellmont) What is included in this packet? Guidelines and loan application form Two faculty reference forms W-9 form Wellmont

Nursing Educational Loan Checklist (for individuals not currently employed by Wellmont) What is included in this packet? Guidelines and loan application form Two faculty reference forms W-9 form Wellmont

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Counting Income for MAGI What Counts as Income

Counting Income for MAGI What Counts as Income Wages, salaries, tips, gratuities, bonuses, commissions (before taxes are taken out). Form(s) W 2. Alimony received Annuities Awards and Prizes (In addition

Counting Income for MAGI What Counts as Income Wages, salaries, tips, gratuities, bonuses, commissions (before taxes are taken out). Form(s) W 2. Alimony received Annuities Awards and Prizes (In addition

Instructions for Form 1116

2014 Instructions for Form 1116 Foreign Tax Credit (Individual, Estate, or Trust) Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest information

2014 Instructions for Form 1116 Foreign Tax Credit (Individual, Estate, or Trust) Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest information

Instructions for Form 1116 Foreign Tax Credit (Individual, Estate, or Trust)

") 2009 Instructions for Form 1116 Foreign Tax Credit (Individual, Estate, or Trust) Department of the Treasury Internal Revenue Service Section references are to the Internal K-1 (Form 1041), Schedule K-1

2009 Instructions for Form 1116 Foreign Tax Credit (Individual, Estate, or Trust) Department of the Treasury Internal Revenue Service Section references are to the Internal K-1 (Form 1041), Schedule K-1

Desk Aid 56: Income and Income Deductions

Employee compensation: (wages, salary, tips, bonuses, awards, and fringe benefits) Interest income: (taxable and non-taxable) Count 1040 line 7 Count 1040 line 7 Count 1040 line 7 Count 1040 line 8a and

Employee compensation: (wages, salary, tips, bonuses, awards, and fringe benefits) Interest income: (taxable and non-taxable) Count 1040 line 7 Count 1040 line 7 Count 1040 line 7 Count 1040 line 8a and

General Instructions for Forms 1099, 1098, 5498, and W-2G

2008 General Instructions for Forms 1099, 1098, 5498, and W-2G Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Contents Page

2008 General Instructions for Forms 1099, 1098, 5498, and W-2G Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Contents Page

Credit Application Contact Information

Dear Valued Customer, Thank you for your interest in establishing a credit account with Carlile Transportation Systems. In order to process your application in an efficient and timely manner we ask that

Dear Valued Customer, Thank you for your interest in establishing a credit account with Carlile Transportation Systems. In order to process your application in an efficient and timely manner we ask that

Social Security Number: Occupation: Email Address: Current Address (if not listed on W2 form or 1099 Taxpayer Name: Spouse Name: form):

:") For New Clients only - please submit with your forms and documentations TAX RETURN QUESTIONNAIRE - TAX YEAR 2014 Current Address (if not listed on W2 form or 1099 Taxpayer Name: Spouse Name: form): Phone

For New Clients only - please submit with your forms and documentations TAX RETURN QUESTIONNAIRE - TAX YEAR 2014 Current Address (if not listed on W2 form or 1099 Taxpayer Name: Spouse Name: form): Phone

Substitute W-4P Tax Withholding Certificate for Pension or Annuity Payments Wis. Stat. 40.08 (1)

") Substitute W-4P Tax Withholding Certificate for Pension or Annuity Payments Wis. Stat. 40.08 (1) Wisconsin Department of Employee Trust Funds 801 W Badger Road PO Box 7931 Madison WI 53707-7931 1-877-533-5020

Substitute W-4P Tax Withholding Certificate for Pension or Annuity Payments Wis. Stat. 40.08 (1) Wisconsin Department of Employee Trust Funds 801 W Badger Road PO Box 7931 Madison WI 53707-7931 1-877-533-5020

1 Rents. 2 Royalties. 3 Other income. 5 Fishing boat proceeds. 7 Nonemployee compensation

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Shareholder's Instructions for Schedule K-1 (Form 1120S)

") 2015 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

2015 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

Attention: See IRS Publications 1141, 1167, 1179 and other IRS resources for information about printing these tax forms.

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

APPLICATION CONTINUES ON THE NEXT PAGE

CITY & COUNTY OF SAN FRANCISCO OFFICE OF THE TREASURER & TAX COLLECTOR JOSÉ CISNEROS, TREASURER Taxpayer Assistance, City Hall Room 140 #1 Dr. Carlton B. Goodlett Place, San Francisco, CA 94102 Customer

CITY & COUNTY OF SAN FRANCISCO OFFICE OF THE TREASURER & TAX COLLECTOR JOSÉ CISNEROS, TREASURER Taxpayer Assistance, City Hall Room 140 #1 Dr. Carlton B. Goodlett Place, San Francisco, CA 94102 Customer

Fleming, Tawfall & Company, P.C. 2015 Tax Questionnaire

Fleming, Tawfall & Company, P.C. 2015 Tax Questionnaire COMPLETION OF THIS TAX QUESTIONNAIRE, ALONG WITH YOUR SIGNATURE, IS MANDATORY FOR THE 2015 TAX SEASON. Date of Spouse s Date of Name Birth Name Birth

Fleming, Tawfall & Company, P.C. 2015 Tax Questionnaire COMPLETION OF THIS TAX QUESTIONNAIRE, ALONG WITH YOUR SIGNATURE, IS MANDATORY FOR THE 2015 TAX SEASON. Date of Spouse s Date of Name Birth Name Birth

Internal Revenue Service Number: 200702006 Release Date: 1/12/2007 Index Number: 3406.00-00, 6041.03-00, 6041.05-00, 6045.00-00, 6049.

Internal Revenue Service Number: 200702006 Release Date: 1/12/2007 Index Number: 3406.00-00, 6041.03-00, 6041.05-00, 6045.00-00, 6049.01-00 -------------------------------- ------------------------------------

Internal Revenue Service Number: 200702006 Release Date: 1/12/2007 Index Number: 3406.00-00, 6041.03-00, 6041.05-00, 6045.00-00, 6049.01-00 -------------------------------- ------------------------------------

Attention: See IRS Publications 1141, 1167, 1179 and other IRS resources for information about printing these tax forms.

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

INCOME AND DEDUCTIBLE ITEMS, SUMMARY CHART

ICOME AD DEDUCTIBLE ITEMS, SUMMAR CHART otes: = ot included = Included = Adjusted Gross = Total Household Resources = Household (2011 and prior years only) Items Alimony received Awards, prizes (in excess

ICOME AD DEDUCTIBLE ITEMS, SUMMAR CHART otes: = ot included = Included = Adjusted Gross = Total Household Resources = Household (2011 and prior years only) Items Alimony received Awards, prizes (in excess

enc3 Specifications for 1099 Reporting

Form enc3 1099 Format (11-2015) http://www.dornc.com/enc3/ North Carolina Department of Revenue P. O. Box 25000 Raleigh, NC 27640 (877) 252-3052 toll-free enc3 Specifications for 1099 Reporting Submit

Form enc3 1099 Format (11-2015) http://www.dornc.com/enc3/ North Carolina Department of Revenue P. O. Box 25000 Raleigh, NC 27640 (877) 252-3052 toll-free enc3 Specifications for 1099 Reporting Submit

Federal Agency Seminar 2011. Withholding and Reporting of Tax on Wage Payments to Foreign Persons

Federal Agency Seminar 2011 Withholding and Reporting of Tax on Wage Payments to Foreign Persons 1 Objectives Know why tax residency is important Which income non-resident alien are subject to FIT withholding

Federal Agency Seminar 2011 Withholding and Reporting of Tax on Wage Payments to Foreign Persons 1 Objectives Know why tax residency is important Which income non-resident alien are subject to FIT withholding

Income Made Easy Election Form

Income Made Easy Election Form Instructions This form should ONLY be used if you have an optional Withdrawal Benefit Rider with your annuity contract and would like to enroll in John Hancock s Income Made

Income Made Easy Election Form Instructions This form should ONLY be used if you have an optional Withdrawal Benefit Rider with your annuity contract and would like to enroll in John Hancock s Income Made

TO: OUR FRIENDS AND PROSPECTIVE CLIENTS FROM: THOMAS WILLIAMS, CPA RE: U.S. INCOME TAX ISSUES OF FOREIGN NATIONALS DATE: AS OF JANUARY 1, 2010

THOMAS WILLIAMS CPA, PLLC TO: OUR FRIENDS AND PROSPECTIVE CLIENTS FROM: THOMAS WILLIAMS, CPA RE: U.S. INCOME TAX ISSUES OF FOREIGN NATIONALS DATE: AS OF JANUARY 1, 2010 Dear Friends: The following is an

THOMAS WILLIAMS CPA, PLLC TO: OUR FRIENDS AND PROSPECTIVE CLIENTS FROM: THOMAS WILLIAMS, CPA RE: U.S. INCOME TAX ISSUES OF FOREIGN NATIONALS DATE: AS OF JANUARY 1, 2010 Dear Friends: The following is an

U.S.A. Chapter I. Scope of the Convention

U.S.A. Convention between the Kingdom of the Netherlands and the United States of America for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income Done

U.S.A. Convention between the Kingdom of the Netherlands and the United States of America for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income Done

Receita Federal do Brasil (RFB) www.receita.fazenda.gov.br 1 January to 31 December Last working day of April following end of tax year

www.receita.fazenda.gov.br 1 January to 31 December Last working day of April following end of tax year") Worldwide personal tax guide 2013 2014 Brazil Local Information Tax Authority Receita Federal do Brasil (RFB) Website www.receita.fazenda.gov.br Tax Year 1 January to 31 December Tax Return due date: Last

Worldwide personal tax guide 2013 2014 Brazil Local Information Tax Authority Receita Federal do Brasil (RFB) Website www.receita.fazenda.gov.br Tax Year 1 January to 31 December Tax Return due date: Last

HSBC Securities (USA) Inc. Instructions for 1099/5498 Recipients 2008

Inc. Instructions for 1099/5498 Recipients 2008") HSBC Securities (USA) Inc. Instructions for 1099/5498 Recipients 2008 Dear Investor, Please note: In June of 2008, Pershing LLC ( Pershing ) became the clearing agent for HSBC Securities (USA) Inc. ( HSBC

HSBC Securities (USA) Inc. Instructions for 1099/5498 Recipients 2008 Dear Investor, Please note: In June of 2008, Pershing LLC ( Pershing ) became the clearing agent for HSBC Securities (USA) Inc. ( HSBC

Provinces and territories also impose income taxes on individuals in addition to federal taxes

Worldwide personal tax guide 2013 2014 Canada Local information Tax Authority Website Tax Year Tax Return due date Is joint filing possible Are tax return extensions possible Canada Revenue Agency (CRA)

Worldwide personal tax guide 2013 2014 Canada Local information Tax Authority Website Tax Year Tax Return due date Is joint filing possible Are tax return extensions possible Canada Revenue Agency (CRA)

How To Pay Taxes In Wisconsin

State of Wisconsin Department of Revenue Tax Information for Part-Year Residents and Nonresidents of Wisconsin for 2014 (Including Information for Aliens) Publication 122 (12/14) Printed on Recycled Paper

State of Wisconsin Department of Revenue Tax Information for Part-Year Residents and Nonresidents of Wisconsin for 2014 (Including Information for Aliens) Publication 122 (12/14) Printed on Recycled Paper

Form 1099 Update for Controllers. Marianne Couch, J.D. COKALA Tax Information Reporting, LLC www.cokala.com office@cokala.com September 15, 2014

Form 1099 Update for Controllers Marianne Couch, J.D. COKALA Tax Information Reporting, LLC www.cokala.com office@cokala.com September 15, 2014 Agenda Form W-9 TINs and Treaties ACA Treasury Green Book

Form 1099 Update for Controllers Marianne Couch, J.D. COKALA Tax Information Reporting, LLC www.cokala.com office@cokala.com September 15, 2014 Agenda Form W-9 TINs and Treaties ACA Treasury Green Book

U.S. Taxation of J-1 Exchange Visitors

U.S. Taxation of J-1 Exchange Visitors By Paula N. Singer, Esq. 1 ONESOURCE TAX INFORMATION REPORTING The J-1 Exchange Visitor Program has long been used by institutions of higher education, teaching hospitals

U.S. Taxation of J-1 Exchange Visitors By Paula N. Singer, Esq. 1 ONESOURCE TAX INFORMATION REPORTING The J-1 Exchange Visitor Program has long been used by institutions of higher education, teaching hospitals