Prosperity Insurance Group, Inc. Your Independent Agent Home * Auto * Business (561)

|

|

|

- Millicent Burke

- 8 years ago

- Views:

Transcription

1

2 Homeowners Insurance TOOLKIT Florida residents know firsthand that it pays to plan ahead. Dealing with wildfires, floods, tornadoes, hurricanes, winter storms, sinkholes and other disasters, not to mention individual home fires, lightning, smoke and theft, can drastically change our lives. While we all need to carefully prepare for hurricane season, it pays to make sure your homeowners insurance contains adequate coverage year-round. This toolkit provides helpful suggestions to prepare you for any type of claim that involves the largest investment you ve made - your home. This toolkit is yours - it can be as simple or as comprehensive as you want. Remember, the more detailed documentation you supply during the claims process, the fewer problems you ll have with the claim itself. Contents Section 1 What does your policy cover? Section 2 Property Inventory Section 3 The Claims Process Page 3 Page 6 Page 16 Prosperity Insurance Group, Inc. Your Independent Agent

3 1Coverage What does your policy cover and exclude? Standard homeowners policies usually limit coverage on valuables such as jewelry, silverware, guns, antiques, boats and other items. Check your policy and contact your insurance agent or company with questions or to request additional coverage. This is why your inventory is so important - it helps you realize the value of your belongings. Replacement cost versus actual cash value When buying coverage, you may insure your property and belongings for actual cash value or replacement cost. Replacement Cost Replacement cost is the amount needed to replace or repair your damaged property with materials of similar kind and quality, without deducting for depreciation (the decrease in the value of your home or personal property due to normal wear and tear). Actual Cash Value Actual cash value is the amount needed to repair or replace damage to your home after depreciation. For example, your insurance company would deduct for the age and condition of a 17-year-old roof with a 20-year life expectancy. Here is how the two types of coverage work in practice. Let s say you bought a new television in 1994 for $700. In 2005, a lightning strike destroys the TV. A policy for actual cash value will only pay an amount that reflects the TV s current value - say $300. A replacement cost policy would cover the entire cost of a new TV of the same type - say $900. Legislation passed in 2005 requires full payment without a depreciation hold-back for personal residential policies. Call the Consumer Helpline at MY-FL-CFO ( ) for further information. Your agent must offer you replacement cost coverage for your dwelling. If you reject this coverage, you must sign a statement on the application form indicating that you don t want it. Standard replacement cost depends upon the dwelling limit stated on your policy. Insurance companies design most homeowners policies to require the policyholder to insure the dwelling for at least 80 percent of its replacement cost. While it is rare, you can insure your home for less than 80 percent. If you do so, you will be charged a copayment penalty, in addition to your deductible, when you file a claim. Some companies offer guaranteed replacement cost dwelling insurance - an option that costs only a few dollars more, and insures your home for an increased amount, even if it exceeds policy limits. Many companies will not offer guaranteed replacement benefits for older homes. Prosperity Insurance Group, Inc. Your Independent Agent

4 Windstorm coverage Most homeowners insurance policies cover damage caused by windstorms, hurricanes and hail, unless your dwelling is in the high-risk area known as the Wind-Pool Zone. If your dwelling is in this area, it is likely that windstorm coverage will be excluded and you will need a separate policy for this coverage. If you have a mortgage, your mortgage company can require that you secure this specialized coverage or they will apply force-placed coverage, which can be more costly. Additional Living Expense Homeowners packages provide additional living expense (ALE) coverage that will pay some extra expenses if damage to your home prevents you from living there while it is being repaired. Most policies also will provide this coverage when a civil authority (law enforcement agency, emergency management service, etc.) prohibits the use of a residence due to direct damage to neighboring homes by a covered threat. The items typically covered - above and beyond normal expenses - include extra costs for food, housing, telephone, transportation (to and from work or school), relocation and storage, utility installation and furniture rental for a temporary residence. Be sure to check your policy to find out what is specifically covered. This coverage applies only to differences in expenses. For example, it would apply to the cost of restaurant meals minus normal food expenses. It does not cover your mortgage, groceries and utilities or the monthly cost of a telephone in a rented space (since you normally pay for the telephone in your house). Your policy may designate a limit of coverage for additional living expenses, but your policy does not obligate your company to pay this amount up front or in full if you suffer a total or partial loss. For this reason, you must keep receipts for additional living expenses and submit these to your company for reimbursement. Additional living expense coverage does not apply to your dependent children while they are away at college. It applies only to the primary insured structure in the event of a loss. Policies generally offer ALE coverage without any deductible. Biological Deterioration (mold and fungi) Typically, mold that results from a covered peril is a covered claim through your personal residential property insurance (homeowners ) policy. An example would be a sudden and accidental discharge of water - like a burst pipe or other plumbing failure, or claims that arise from water damage due to hurricanes or flooding. Please refer to your policy provisions for details of specific mold coverage and limitations. Most insurers now offer limited levels of mold-related property damage coverage within the basic policy. Many insurers offer $10,000 of limited coverage, with an opportunity to purchase additional coverage for an additional premium. Other insurers exclude mold-related property damage entirely, but offer coverage in amounts of $10,000, $15,000, $25,000, $50,000 and policy limits, for an additional premium. Prosperity Insurance Group, Inc. Your Independent Agent

coverage that will pay some extra expenses if damage to your home prevents you from living there while it is")

5 Ordinance or Law Exclusion If a local building ordinance or law increases the cost of repairing or replacing your dwelling, the insurance company will not pay that extra amount, unless you have added ordinance or law coverage to your policy. This is how it works: Your home was built in 1982 and the building code called for construction at least five feet off the ground. In 2001, the building code was changed to call for the same construction at least 10 feet above ground. Complying with this code will require a change in design and building materials; thus, you will pay more to repair or rebuild your home, if necessary. If you have a claim that is covered by your homeowners policy, and have ordinance or law excluded, the insurance company will not pay the cost of bringing the repaired home up to current building requirements. Your agent must offer you ordinance or law coverage. If you do not wish to buy this coverage, you must sign a form stating that you reject it. Some companies automatically include the coverage in their policies. Flood Insurance Typically, homeowners policies exclude flood damage (rising water). Depending on your home s location, however, you may qualify for flood insurance through the National Flood Insurance Program. You also may qualify for a discount if you include a special elevation report with your application. For more information, contact the National Flood Insurance Program at FLOOD29 ( ). The coverage involves a 30-day waiting period before the policy becomes effective; unless the policy is purchased at the same time you buy your home. Some insurance companies also offer flood insurance. Generally, you will get separate coverage for your home and personal property. Your insurance agent or company can assist you with application forms for flood coverage. Sinkholes and Catastrophic Ground Collapse Florida insurance companies are not required to include sinkhole coverage on new or existing homeowners insurance policies. However, they are required to inform homeowners that sinkhole coverage is available as an extra coverage - usually in the form of a rider, or addendum. A law passed in 2007 requires that insurance companies now include catastrophic ground cover collapse that results in an order to evacuate, and the insured structure being condemned by the governmental agency authorized by law to issue such an order for that structure. Surplus lines insurers are not required to offer sinkhole coverage, but many do. Ask your agent for details. Prosperity Insurance Group, Inc. Your Independent Agent

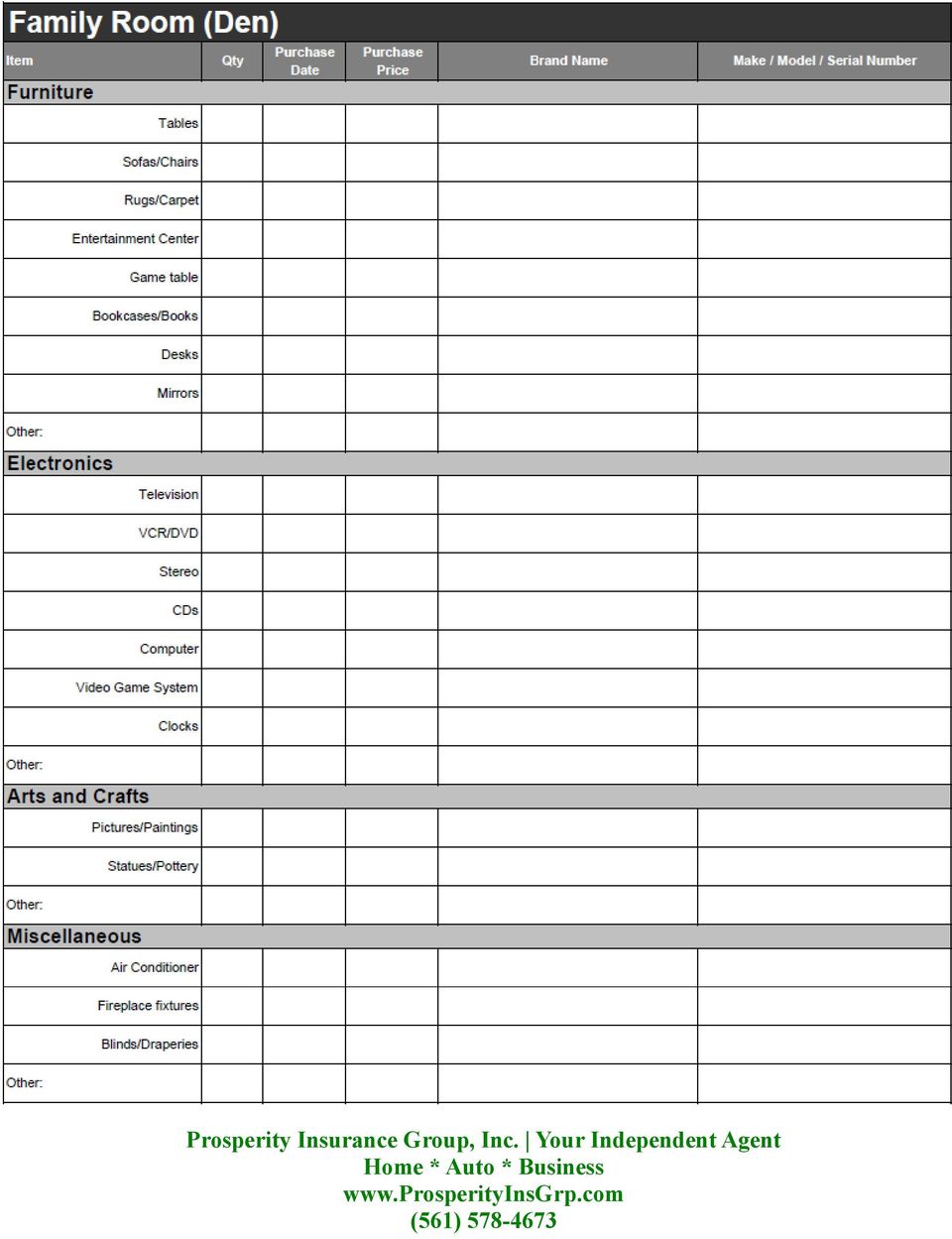

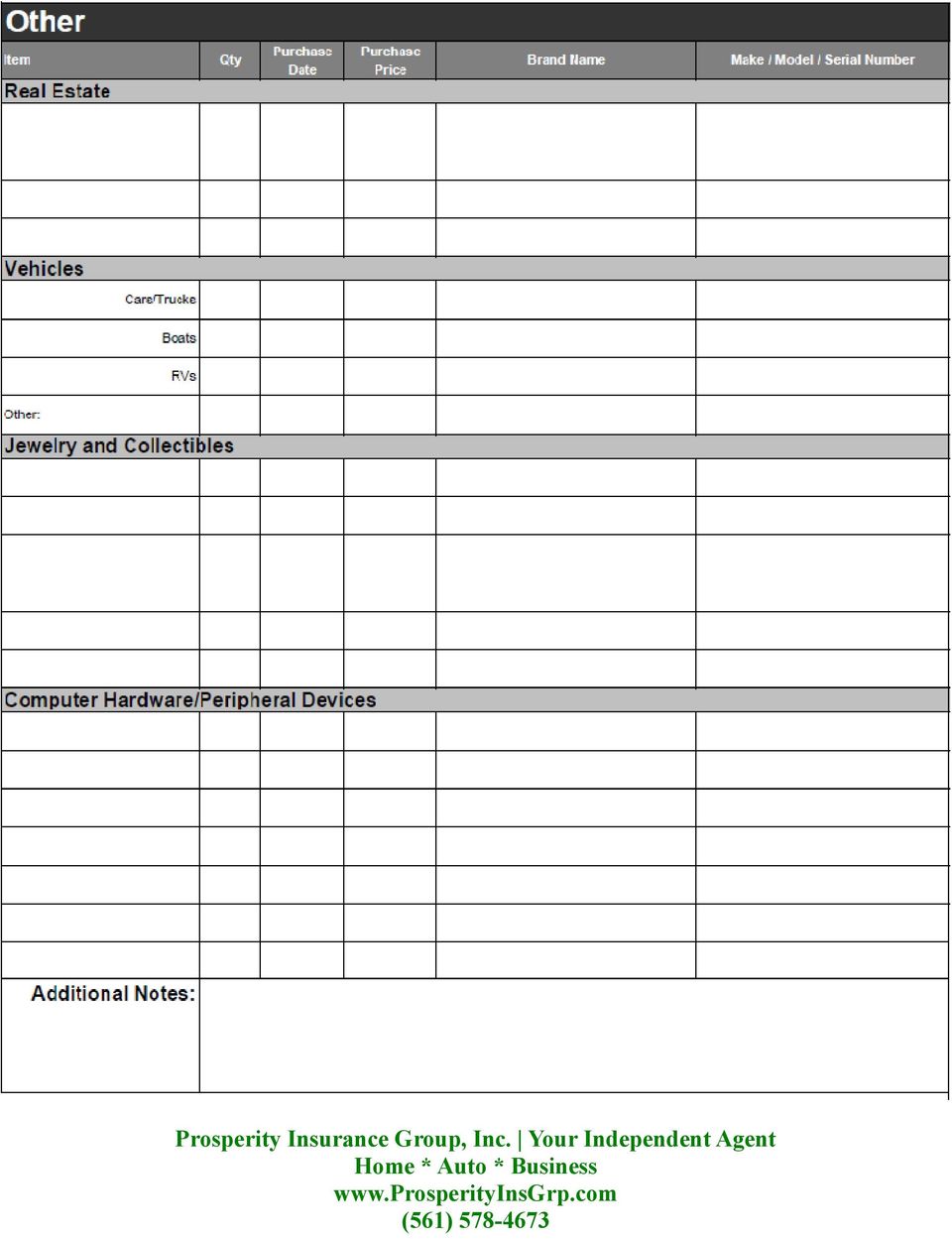

6 2Property Inventory The Department of Financial Services recommends conducting a room-by-room inventory so that if you have a claim caused by any of the covered perils in your insurance policy, you will be able to file an accurate claim and get better claims results. The following pages include the main rooms of the house, but don t forget other areas such as closets, basement, attic, garage, porch, patio, workroom or shed. When checking these areas, be sure to check all items. It s also a good idea to photograph your personal property. Pictures add details to your inventory that written documents can t. Also be sure to include the year of purchase, price and brand name. Once you ve completed your home inventory, compare the estimated value of your items to the amount of insurance coverage your current policy has. Also, you may want to check with your insurance agent or company to determine if you have any items that are underinsured, or if you need any additional coverage. It s very important to update your inventory at least once a year. Remember, your claim settlement depends on you supplying accurate, documented information. Personal Asset Inventory For each of the following categories, write down all the items that apply. Use separate sheets of paper for each if necessary. Living Room Dining Room Kitchen Family Room (Den) Bedrooms Bathrooms Other TIP: If possible, take photographs or video of your property and store all records in a safe, dry place. TIP: When dealing with a homeowners insurance claim, never give original inventories or documents to anyone. If the original document is damaged, there is no way to reproduce a replacement. Disclaimer: This manual may not be complete, do not omit any item from your inventory. Prosperity Insurance Group, Inc. Your Independent Agent

7 Financial Account Information Name of Institution: Address: Phone Number: Account Number: Web Site: Mortgage Information If your home is mortgaged, any insurance claim settlement will be made out to you and the mortgage holder. You will need to keep the mortgage holder informed of the process and arrange a schedule of release of funds for repairs. Name of Institution: Address: Phone Number: Account Number: Web Site: Additional accounts (utility company, cell phone provider, ect): Prosperity Insurance Group, Inc. Your Independent Agent

:")

8

9

10

11

12

13

14

15

16 3The Claims Process Once you have determined that the claim exceeds your policy deductible, immediately report property damage to your agent and insurance company. The company will arrange for an insurance adjuster to visit your property and begin the claim. Make emergency repairs and document them - keeping a file with all of your receipts, as well as any photos or video of the damage, to submit with your claim. Don t make extensive repairs before the claims adjuster arrives or throw out damaged furniture and other expensive items; the adjuster will want to see them. Make sure your adjuster is properly licensed to conduct business in Florida, and be sure to write down contact information including phone numbers and addresses for the adjuster and firm he or she may work for. If you have any questions about the license status of an adjuster, or the way your claim was handled, call the DFS Consumer Helpline tollfree at My-FL-CFO ( ). Keep a record of the date, time, and name of all people you speak to regarding the claim. Also keep a copy of anything you sign, as well as any photos, receipts, and other documentary evidence. Note about mediation: In this free, informal process, a trained, neutral mediator tries to help resolve the dispute without dictating the outcome. However, it is important to remember that mediation is nonbinding. To find out if you qualify, call the DFS Consumer Helpline toll-free at My-FL-CFO ( ). If you and your company representative cannot reach a satisfactory settlement together, you may hire an appraiser to reach a compromise figure. You and the company split the cost. If you both still disagree, you may hire a second appraiser, called an umpire. The decision of any two of these people is binding. Adjuster Information and Contact Log When you submit a claim for damage from a hurricane, your insurance company will schedule an evaluation conducted by an adjuster. Adjusters must be licensed in the state of Florida. There are three types of adjusters who are authorized to estimate damages following a disaster. Company Adjusters work for your insurance company and are paid by them to estimate your damage and submit a report that will be used as the basis of the claim settlement. You do not pay this adjuster. These adjusters must be licensed in Florida. Emergency adjusters are temporarily licensed adjusters hired by insurance companies to assist with a large volume of claims, usually as a result of a disaster. Independent adjusters usually work as employees of an independent adjusting firm that has been hired by an insurance company to handle the company s claims. Independent adjusters obtain and submit the claim information to the insurance company. The insurance company makes the final decision regarding benefits paid. Public adjusters are self-employed and do not work for insurance companies or independent adjusting firms. They may work in a public adjusting firm. Public adjusters are hired to settle claims with the insurance company on your behalf. Generally their payment fee is a contracted percentage of the total claim settlement amount, but cannot exceed 20%. Public adjuster s fees aren t set by the state, although in the event of a state of emergency declared by the Governor of Florida, a 10% cap applies to all claims as a result of the state of emergency for a period of one (1) year an emergency order may be issued limiting the percentage of the fee that may be charged for adjusting hurricane claims. In either case, the public adjuster can only collect fees on the portion of the settlement that is actually attributed to the work of the public adjuster. Prosperity Insurance Group, Inc. Your Independent Agent

17 You negotiate and agree on the fee you pay for their services. The Department of Financial Services has no regulatory authority over contractual provisions between the public adjuster and the insured. In the event you need to file a claim, you will deal with an insurance adjuster. Keep this person s name and contact information handy at all times to facilitate evaluation of the loss and to handle any dispute. Also, use this space to record information from your contacts with the adjuster and the insurance company - include dates, the information discussed, and the names and phone numbers of the people you talk to. This log will help in the event of a claim dispute. Aduster Name: Adjuster Company Adjuster Phone Number: Adjuster License Number: Claim Number: Log of Events: Date/Time Action Prosperity Insurance Group, Inc. Your Independent Agent

Alex Sink. Florida Department of Financial Services

Alex Sink Chief Financial Officer State of Florida Florida Department of Financial Services Homeowners Financial TOOL KIT Florida residents know firsthand that it pays to plan ahead. Dealing with wildfires,

Alex Sink Chief Financial Officer State of Florida Florida Department of Financial Services Homeowners Financial TOOL KIT Florida residents know firsthand that it pays to plan ahead. Dealing with wildfires,

Abel Insurance Agency

After a wildfire, people may have questions about their insurance coverage. The Insurance Information Institute offers answers to some of these basic questions. HOMEOWNERS COVERAGE Q. If my house burns

After a wildfire, people may have questions about their insurance coverage. The Insurance Information Institute offers answers to some of these basic questions. HOMEOWNERS COVERAGE Q. If my house burns

How to Determine How Much Homeowners Insurance You Need

How to Determine How Much Homeowners Insurance You Need You need enough insurance to cover the following: 1. The structure of your home. 2. Your personal possessions. 3. The cost of additional living expenses

How to Determine How Much Homeowners Insurance You Need You need enough insurance to cover the following: 1. The structure of your home. 2. Your personal possessions. 3. The cost of additional living expenses

Insurance for Your House and Personal Possessions

Make sure your insurance agent knows about any improvements or additions to your house since you last talked about your insurance policy. If you don't increase your limits to cover the cost of Insurance

Make sure your insurance agent knows about any improvements or additions to your house since you last talked about your insurance policy. If you don't increase your limits to cover the cost of Insurance

Homeowners Insurance. made simple

Homeowners Insurance made simple What s included: How to read your Allstate Policy Declarations Protecting your home and personal property Understanding deductibles Additional protection How to file a

Homeowners Insurance made simple What s included: How to read your Allstate Policy Declarations Protecting your home and personal property Understanding deductibles Additional protection How to file a

Consumer Guide to Manufactured-Homeowners Insurance North Carolina Department of Insurance

Consumer Guide to Manufactured-Homeowners Insurance North Carolina Department of Insurance Wayne Goodwin, Insurance Commissioner A Message from the Commissioner The North Carolina Department of Insurance

Consumer Guide to Manufactured-Homeowners Insurance North Carolina Department of Insurance Wayne Goodwin, Insurance Commissioner A Message from the Commissioner The North Carolina Department of Insurance

Consumer s Quick Check Guide Dwelling Property Policy

Explanation of Coverage Limits and Options Consumer s Quick Check Guide Dwelling Property Policy There are three Dwelling Policy Forms offered in the State of Florida. This Consumer s Quick Check Guide

Explanation of Coverage Limits and Options Consumer s Quick Check Guide Dwelling Property Policy There are three Dwelling Policy Forms offered in the State of Florida. This Consumer s Quick Check Guide

A Consumer s Guide to Homeowners Insurance

A Consumer s Guide to Homeowners Insurance This brochure was developed through the combined efforts of: Illinois Insurance Hotline 1-800-444-3338 Illinois Department of Insurance University of Illinois

A Consumer s Guide to Homeowners Insurance This brochure was developed through the combined efforts of: Illinois Insurance Hotline 1-800-444-3338 Illinois Department of Insurance University of Illinois

Insuring. Home. your. A guide for consumers

Insuring your Home A guide for consumers Insurance coverage is an integral part of a solid financial foundation. Insurance can help us recover financially after illness, accidents, natural disasters or

Insuring your Home A guide for consumers Insurance coverage is an integral part of a solid financial foundation. Insurance can help us recover financially after illness, accidents, natural disasters or

Consumer s Quick Check Guide Condominium Unit-Owners Policy

Consumer s Quick Check Guide Condominium Unit-Owners Policy Explanation of Coverage Limits and Options: This Consumer s Quick Check Guide to the Condominium Unit-Owners Policy is based, in part, on Insurance

Consumer s Quick Check Guide Condominium Unit-Owners Policy Explanation of Coverage Limits and Options: This Consumer s Quick Check Guide to the Condominium Unit-Owners Policy is based, in part, on Insurance

AND. T. Hudgens. Insurance. Ralph. Consumer

INSURANCE BEFORE AND AFTER A DISASTER Information You Can Use Regarding Property Insurance Ralph T. Hudgens Commissioner of Insurance Consumer Services Division INSURANCE BEFORE AND AFTER A DISASTER Consumer

INSURANCE BEFORE AND AFTER A DISASTER Information You Can Use Regarding Property Insurance Ralph T. Hudgens Commissioner of Insurance Consumer Services Division INSURANCE BEFORE AND AFTER A DISASTER Consumer

Florida Department of Financial Services 1-877-MY-FL-CFO (1-877-693-5236) www.myfloridacfo.com

www.myfloridacfo.com") Homeowners Insurance TOOLKIT Florida residents know firsthand that it pays to plan ahead. Dealing with wildfires, floods, tornadoes, hurricanes, winter storms, sinkholes and other disasters, can drastically

Homeowners Insurance TOOLKIT Florida residents know firsthand that it pays to plan ahead. Dealing with wildfires, floods, tornadoes, hurricanes, winter storms, sinkholes and other disasters, can drastically

Insuring. Home. your. A guide for consumers

Insuring your Home A guide for consumers Insurance coverage is an integral part of a solid financial foundation. Insurance can help us recover financially after illness, accidents, natural disasters or

Insuring your Home A guide for consumers Insurance coverage is an integral part of a solid financial foundation. Insurance can help us recover financially after illness, accidents, natural disasters or

A CONSUMER'S GUIDE TO RENTER S INSURANCE. from YOUR North Carolina Department of Insurance CONSUMER'SGUIDE

A CONSUMER'S GUIDE TO RENTER S INSURANCE from YOUR North Carolina Department of Insurance CONSUMER'SGUIDE A MESSAGE FROM YOUR INSURANCE COMMISSIONER Greetings, The North Carolina Department of Insurance

A CONSUMER'S GUIDE TO RENTER S INSURANCE from YOUR North Carolina Department of Insurance CONSUMER'SGUIDE A MESSAGE FROM YOUR INSURANCE COMMISSIONER Greetings, The North Carolina Department of Insurance

Florida Department of Financial Services 1-877-MY-FL-CFO (1-877-693-5236) www.myfloridacfo.com

www.myfloridacfo.com") 1 Homeowners Insurance TOOLKIT Florida residents know firsthand that it pays to plan ahead. Dealing with wildfires, floods, tornadoes, hurricanes, winter storms, sinkholes and other disasters, can drastically

1 Homeowners Insurance TOOLKIT Florida residents know firsthand that it pays to plan ahead. Dealing with wildfires, floods, tornadoes, hurricanes, winter storms, sinkholes and other disasters, can drastically

Illinois Insurance Facts Illinois Department of Insurance

Illinois Insurance Facts Illinois Department of Insurance Shopping for Homeowners Insurance Updated January 2014 Note: This information was developed to provide consumers with general information and guidance

Illinois Insurance Facts Illinois Department of Insurance Shopping for Homeowners Insurance Updated January 2014 Note: This information was developed to provide consumers with general information and guidance

A Shopping Tool for. Homeowners Insurance. Mississippi Insurance Department

Homeowners Insurance Mississippi Insurance Department 1 2014 National Association of Insurance Commissioners All rights reserved. National Association of Insurance Commissioners Insurance Products & Services

Homeowners Insurance Mississippi Insurance Department 1 2014 National Association of Insurance Commissioners All rights reserved. National Association of Insurance Commissioners Insurance Products & Services

Home. The Instant Insurance Guide: Info and tips for buying homeowners and renters insurance in Delaware. www.delawareinsurance.

The Instant Insurance Guide: Home Info and tips for buying homeowners and renters insurance in Delaware From Karen Weldin Stewart, CIR-ML Delaware s Insurance Commissioner 1-800-282-8611 www.delawareinsurance.gov

The Instant Insurance Guide: Home Info and tips for buying homeowners and renters insurance in Delaware From Karen Weldin Stewart, CIR-ML Delaware s Insurance Commissioner 1-800-282-8611 www.delawareinsurance.gov

What is home insurance? What are perils? Whether you own or rent the roof over your head, that roof and everything beneath it has a value.

Whether you own or rent the roof over your head, that roof and everything beneath it has a value. Have you considered how hard it would be to replace everything if a tornado leveled your home? What if

Whether you own or rent the roof over your head, that roof and everything beneath it has a value. Have you considered how hard it would be to replace everything if a tornado leveled your home? What if

Homeowners Insurance Life Advice

Homeowners Insurance Life Advice Protecting your home Homeowners insurance protects your financial investment in your home. Based on your individual needs, you choose specific coverage to provide as much

Homeowners Insurance Life Advice Protecting your home Homeowners insurance protects your financial investment in your home. Based on your individual needs, you choose specific coverage to provide as much

Eight Ways To Save On Your Homeowners Insurance! A Special Report Compliments of

Eight Ways To Save On Your Homeowners Insurance! A Special Report Compliments of 4301 Darrow Rd., Ste 4200 Stow OH 44224 330.688.0998 Email: mailbox@angleinsurance.com 1 Eight Ways To Save On Your Homeowners

Eight Ways To Save On Your Homeowners Insurance! A Special Report Compliments of 4301 Darrow Rd., Ste 4200 Stow OH 44224 330.688.0998 Email: mailbox@angleinsurance.com 1 Eight Ways To Save On Your Homeowners

A simple GUIDE TO HOME INSURANCE

A simple GUIDE TO HOME INSURANCE Inside THIS GUIDE What s in this guide?...5 Insurance 101...5 How insurance works...6 Insurance lingo...7 Types of insurance...8 How often should you review your home insurance

A simple GUIDE TO HOME INSURANCE Inside THIS GUIDE What s in this guide?...5 Insurance 101...5 How insurance works...6 Insurance lingo...7 Types of insurance...8 How often should you review your home insurance

Glossary of Common Homeowners Insurance Terms

Glossary of Common Homeowners Insurance Terms A Actual cash value (ACV) - The value of your property, based on the current cost to replace it minus depreciation. Also see replacement cost. Additional living

Glossary of Common Homeowners Insurance Terms A Actual cash value (ACV) - The value of your property, based on the current cost to replace it minus depreciation. Also see replacement cost. Additional living

Insurance Information Institute. Am I Covered? homeowners about insurance. common questions asked by

Insurance Information Institute Am I Covered? common questions asked by homeowners about insurance If a fire, flood, earthquake, or some other natural disaster were to destroy or damage your home, would

Insurance Information Institute Am I Covered? common questions asked by homeowners about insurance If a fire, flood, earthquake, or some other natural disaster were to destroy or damage your home, would

insurance for your house and personal possessions

Insurance Information Institute insurance for your house and personal possessions If your house burns down or if your possessions are stolen, you don t want to find out that your homeowners insurance policy

Insurance Information Institute insurance for your house and personal possessions If your house burns down or if your possessions are stolen, you don t want to find out that your homeowners insurance policy

All about. home. insurance

All about home insurance Legal Deposit Bibliothèque et Archives nationales du Québec, 2011 Legal Deposit Library and Archives Canada, 2011 Table of contents Buying home insurance 4 Who is insured? 4 Who

All about home insurance Legal Deposit Bibliothèque et Archives nationales du Québec, 2011 Legal Deposit Library and Archives Canada, 2011 Table of contents Buying home insurance 4 Who is insured? 4 Who

Business Owners Insurance. made simple

Business Owners Insurance made simple What s inside: How to read an Allstate Businessowners Policy Declarations Protecting your building and business personal property Understanding deductibles and coverage

Business Owners Insurance made simple What s inside: How to read an Allstate Businessowners Policy Declarations Protecting your building and business personal property Understanding deductibles and coverage

Texas Fair Plan Association

Texas Fair Plan Association RESIDENTIAL PROPERTY INSURANCE The Texas FAIR Plan Association provides limited coverage through the Texas Homeowners Policy - Form A (HO-A), Texas Dwelling Policy Form 1 (TDP-1),

Texas Fair Plan Association RESIDENTIAL PROPERTY INSURANCE The Texas FAIR Plan Association provides limited coverage through the Texas Homeowners Policy - Form A (HO-A), Texas Dwelling Policy Form 1 (TDP-1),

On Your Home. by John Adams, for Fox5 GOOD DAY ATLANTA

SPECIAL REPORT: Ways To Save On Your Home Insurance- by John Adams, for Fox5 GOOD DAY ATLANTA 1 12 Ways to Lower Your Homeowners Insurance Costs edited by John Adams The following originally appeared in

SPECIAL REPORT: Ways To Save On Your Home Insurance- by John Adams, for Fox5 GOOD DAY ATLANTA 1 12 Ways to Lower Your Homeowners Insurance Costs edited by John Adams The following originally appeared in

settling insurance claims after a disaster

Insurance Information Institute settling insurance claims after a disaster What you need to know about how to file a claim how the claim process works what s covered and what s not First Steps Contact

Insurance Information Institute settling insurance claims after a disaster What you need to know about how to file a claim how the claim process works what s covered and what s not First Steps Contact

The Top FAQ s on. Home Insurance. Will my Homeowner s or Tenant s insurance in Calgary cover damage caused by a flood?

A PUBLICATION BY: GODFREY MORROW GODFREY INSURANCE MORROW AND INSURANCE FINANCIAL AND SERVICES FINANCIAL LTD. SERVICES LTD. 2012 The Top FAQ s on Home Insurance Will my Homeowner s or Tenant s insurance

A PUBLICATION BY: GODFREY MORROW GODFREY INSURANCE MORROW AND INSURANCE FINANCIAL AND SERVICES FINANCIAL LTD. SERVICES LTD. 2012 The Top FAQ s on Home Insurance Will my Homeowner s or Tenant s insurance

KNOW YOUR RIGHTS AND

IN THE EVENT OF UNEXPECTED WATER INTRUSION... KNOW YOUR RIGHTS AND Alex Sink Chief Financial Officer of Florida RESPONSIBILITIES Mold can adversely affect homes in Florida s humid climate. As an insured

IN THE EVENT OF UNEXPECTED WATER INTRUSION... KNOW YOUR RIGHTS AND Alex Sink Chief Financial Officer of Florida RESPONSIBILITIES Mold can adversely affect homes in Florida s humid climate. As an insured

UNDERSTANDING HOMEOWNERS INSURANCE

UNDERSTANDING HOMEOWNERS INSURANCE Marjorie J. Hudson MCM Insurance Services, Inc. 31 Robbins StaDon Road, Suite C North HunDngdon, PA 15642 724-765- 0745 (VP) 724-863- 1600 (V) 724-863- 7060 (Fax) How

UNDERSTANDING HOMEOWNERS INSURANCE Marjorie J. Hudson MCM Insurance Services, Inc. 31 Robbins StaDon Road, Suite C North HunDngdon, PA 15642 724-765- 0745 (VP) 724-863- 1600 (V) 724-863- 7060 (Fax) How

Texas Fair Plan Association

Texas Fair Plan Association FREQUENTLY ASKED QUESTIONS What is the Texas FAIR Plan Association and its purpose? The Texas FAIR Plan Association is an entity established by Texas Insurance Code Article

Texas Fair Plan Association FREQUENTLY ASKED QUESTIONS What is the Texas FAIR Plan Association and its purpose? The Texas FAIR Plan Association is an entity established by Texas Insurance Code Article

Brightway Makes Homeowners Insurance Simple

Brightway Makes Homeowners Insurance Simple Congratulations on your new home! Just as you relied on a real estate professional to help you find the home of your dreams, rely on an insurance professional

Brightway Makes Homeowners Insurance Simple Congratulations on your new home! Just as you relied on a real estate professional to help you find the home of your dreams, rely on an insurance professional

How will your insurance policy respond in your time of need?

Department of Business and Industry Nevada Division of Insurance Scott J. Kipper, Commissioner Terry Johnson, Director Brian Sandoval, Governor How will your insurance policy respond in your time of need?

Department of Business and Industry Nevada Division of Insurance Scott J. Kipper, Commissioner Terry Johnson, Director Brian Sandoval, Governor How will your insurance policy respond in your time of need?

7 Ways You Can Save $ on Your Homeowners Insurance -- And Provide Better Protection for Yourself and the People You Love!

7 Ways You Can Save $ on Your Homeowners Insurance -- And Provide Better Protection for Yourself and the People You Love! Your home is probably your most valuable asset. It is also a huge risk for you

7 Ways You Can Save $ on Your Homeowners Insurance -- And Provide Better Protection for Yourself and the People You Love! Your home is probably your most valuable asset. It is also a huge risk for you

Consumer s Guide to. Homeowners. Insurance LOUISIANA DEPARTMENT OF INSURANCE

Consumer s Guide to Homeowners Insurance LOUISIANA DEPARTMENT OF INSURANCE A message from The Louisiana Department of Insurance Chances are your home is the single most expensive item you will ever purchase,

Consumer s Guide to Homeowners Insurance LOUISIANA DEPARTMENT OF INSURANCE A message from The Louisiana Department of Insurance Chances are your home is the single most expensive item you will ever purchase,

A Shopping Tool for. Homeowners Insurance. Mississippi Insurance Department

Homeowners Insurance Mississippi Insurance Department 1 2014 National Association of Insurance Commissioners All rights reserved. National Association of Insurance Commissioners Insurance Products & Services

Homeowners Insurance Mississippi Insurance Department 1 2014 National Association of Insurance Commissioners All rights reserved. National Association of Insurance Commissioners Insurance Products & Services

Home and Automobile Insurance Guide

Home and Automobile Insurance Guide General Information Finding the best insurance policies to suit your needs can be a complex and confusing business. To help you, we have addressed questions and defined

Home and Automobile Insurance Guide General Information Finding the best insurance policies to suit your needs can be a complex and confusing business. To help you, we have addressed questions and defined

Homeowners Insurance

LOUISIANA DEPARTMENT OF INSURANCE Consumer s Guide to Homeowners Insurance James J. Donelon, Commissioner of Insurance A message from Commissioner of Insurance Jim Donelon Chances are your home is the

LOUISIANA DEPARTMENT OF INSURANCE Consumer s Guide to Homeowners Insurance James J. Donelon, Commissioner of Insurance A message from Commissioner of Insurance Jim Donelon Chances are your home is the

Insuring Your Farm... The Basics of Property & Liability Coverage. A Publication of the Maine Bureau of Insurance

Maine Bureau of Insurance 34 State House Station Augusta ME 04333 Insuring Your Farm... The Basics of Property & Liability Coverage A Publication of the Maine Bureau of Insurance Table of Contents The

Maine Bureau of Insurance 34 State House Station Augusta ME 04333 Insuring Your Farm... The Basics of Property & Liability Coverage A Publication of the Maine Bureau of Insurance Table of Contents The

CONSUMER'SGUIDE. A Consumer s Guide to WHAT TO DO IN THE EVENT OF DISASTER. from your North Carolina Department of Insurance

CONSUMER'SGUIDE A Consumer s Guide to WHAT TO DO IN THE EVENT OF DISASTER from your North Carolina Department of Insurance A MESSAGE FROM YOUR INSURANCE COMMISSIONER We all want to remain safe and secure,

CONSUMER'SGUIDE A Consumer s Guide to WHAT TO DO IN THE EVENT OF DISASTER from your North Carolina Department of Insurance A MESSAGE FROM YOUR INSURANCE COMMISSIONER We all want to remain safe and secure,

Frequently Asked Questions About Property Damage Insurance Claims in Tennessee

Roadmap to Recovery Program Frequently Asked Questions About Property Damage Insurance Claims in Tennessee This Roadmap to Recovery publication offers general guidance and answers to common questions people

Roadmap to Recovery Program Frequently Asked Questions About Property Damage Insurance Claims in Tennessee This Roadmap to Recovery publication offers general guidance and answers to common questions people

Homeowners Insurance. Don t Forget The

Homeowners Insurance Don t Forget The A guide to protecting your home and personal possessions Are you buying insurance on a new home, selling a home or just wanting to gain a better understanding of the

Homeowners Insurance Don t Forget The A guide to protecting your home and personal possessions Are you buying insurance on a new home, selling a home or just wanting to gain a better understanding of the

10 Ways You Can Save $ on Your Homeowners Insurance -- And Provide Better Protection for Yourself and the People You Love!

Here s the information you requested! Special Report for Homeowners Insurance Insider Reveals Little-Known Secrets: 10 Ways You Can Save $ on Your Homeowners Insurance -- And Provide Better Protection

Here s the information you requested! Special Report for Homeowners Insurance Insider Reveals Little-Known Secrets: 10 Ways You Can Save $ on Your Homeowners Insurance -- And Provide Better Protection

If you rent a house or apartment. Renters Insurance

Renters Insurance If you rent a house or apartment and think that your landlord is financially responsible when there is a fire, theft or other catastrophe think again. Your landlord may have insurance

Renters Insurance If you rent a house or apartment and think that your landlord is financially responsible when there is a fire, theft or other catastrophe think again. Your landlord may have insurance

Homeowners insurance. protecting your dreams

Homeowners insurance protecting your dreams Your Home is A Dream Come True You ve worked hard for your home. It is a reflection of you and it may serve as the launch pad for your dreams. It s a special

Homeowners insurance protecting your dreams Your Home is A Dream Come True You ve worked hard for your home. It is a reflection of you and it may serve as the launch pad for your dreams. It s a special

**READ YOUR INSURANCE POLICY FOR COMPLETE POLICY TERMS AND CONDITIONS**

HOMEOWNERS HO P 002 06 11 IMPORTANT INFORMATION REQUIRED BY THE LOUISIANA DEPARTMENT OF INSURANCE Homeowners Insurance Policy Coverage Disclosure Summary This form is promulgated pursuant to LSA-R.S. 22:1332

HOMEOWNERS HO P 002 06 11 IMPORTANT INFORMATION REQUIRED BY THE LOUISIANA DEPARTMENT OF INSURANCE Homeowners Insurance Policy Coverage Disclosure Summary This form is promulgated pursuant to LSA-R.S. 22:1332

belongings? It may surprise you to know that the average renter purchases approximately

Renters Insurance State Farm coverage for just pennies a day belongings? It may surprise you to know that the average renter purchases approximately own if something should happen? With a State Farm Renters

Renters Insurance State Farm coverage for just pennies a day belongings? It may surprise you to know that the average renter purchases approximately own if something should happen? With a State Farm Renters

TABLE OF CONTENTS. 1 Introduction. 2 How insurance works. 3 What to look for when buying insurance. 4 Homeowners, condo and renters insurance

Insurance Guide TABLE OF CONTENTS 1 Introduction 2 How insurance works 3 What to look for when buying insurance 4 Homeowners, condo and renters insurance 7 Auto insurance 9 Flood insurance 11 Personal

Insurance Guide TABLE OF CONTENTS 1 Introduction 2 How insurance works 3 What to look for when buying insurance 4 Homeowners, condo and renters insurance 7 Auto insurance 9 Flood insurance 11 Personal

Additional Living Expenses - With Direct Damage

Common Coverage Questions HO3 Hurricane losses Special Note Please Read This information is for general information only. The insurance policy and endorsement forms, not this document, define the terms

Common Coverage Questions HO3 Hurricane losses Special Note Please Read This information is for general information only. The insurance policy and endorsement forms, not this document, define the terms

Homeowners Insurance. made simple

House & Home Insurance Homeowners Insurance made simple What s inside: How to read an Allstate House & Home SM Policy Declarations Understanding homeowners insurance Protecting your home and personal property

House & Home Insurance Homeowners Insurance made simple What s inside: How to read an Allstate House & Home SM Policy Declarations Understanding homeowners insurance Protecting your home and personal property

Reading an Insurance Policy

Reading an Insurance Policy Here are some tips for maximizing your understanding of insurance policies. A. Get the Complete Policy Sometimes just obtaining the policy is a challenge. The client may not

Reading an Insurance Policy Here are some tips for maximizing your understanding of insurance policies. A. Get the Complete Policy Sometimes just obtaining the policy is a challenge. The client may not

Homeowners Insurance. » Make sure you get enough insurance to be able to replace your home should you experience a total loss.

HOMEOWneRS Insurance What it is and why it s important At the most basic level, homeowners insurance protects you financially should you experience a total loss of your home and possessions. Key considerations

HOMEOWneRS Insurance What it is and why it s important At the most basic level, homeowners insurance protects you financially should you experience a total loss of your home and possessions. Key considerations

When a Disaster Strikes:

When a Disaster Strikes: What to Do After an Insured Homeowners Loss A Question and Answer Guide for Homeowners Prepared by Commonwealth of Virginia State Corporation Commission Bureau of Insurance This

When a Disaster Strikes: What to Do After an Insured Homeowners Loss A Question and Answer Guide for Homeowners Prepared by Commonwealth of Virginia State Corporation Commission Bureau of Insurance This

HOME INSURANCE MADE SIMPLE

HOME INSURANCE MADE SIMPLE Working with the profession to simplify the language of insurance TAKE COVER AT HOME! What would you do if your home was flooded or struck by lightning or your valuables were

HOME INSURANCE MADE SIMPLE Working with the profession to simplify the language of insurance TAKE COVER AT HOME! What would you do if your home was flooded or struck by lightning or your valuables were

A Guide For Homeowners

A Guide For Homeowners If you are ever sued, your standard homeowners or auto policy will provide you with some liability coverage, paying for judgments against you and your attorney's fees, up to a limit

A Guide For Homeowners If you are ever sued, your standard homeowners or auto policy will provide you with some liability coverage, paying for judgments against you and your attorney's fees, up to a limit

Homeowners Insurance: The Basics. List as many perils that could happen to your home that you can think of.

Homeowners Insurance: The Basics List as many perils that could happen to your home that you can think of. Homeowners Insurance: The Basics A binding, legal contract between the insured and the insurer

Homeowners Insurance: The Basics List as many perils that could happen to your home that you can think of. Homeowners Insurance: The Basics A binding, legal contract between the insured and the insurer

Farmers Homeowners Insurance

Farmers Homeowners Insurance Cover your biggest investment Coverage you need, the options you want Your home is perhaps your most valuable possession. You need the best coverage available at a reasonable

Farmers Homeowners Insurance Cover your biggest investment Coverage you need, the options you want Your home is perhaps your most valuable possession. You need the best coverage available at a reasonable

A Consumer s Guide to Homeowners Insurance. A Publication of the Maine Bureau of Insurance

Maine Bureau of Insurance State House Station 34 Augusta, ME 04333-0034 A Consumer s Guide to Homeowners Insurance A Publication of the Maine Bureau of Insurance April 2015 A Consumer s Guide to Homeowners

Maine Bureau of Insurance State House Station 34 Augusta, ME 04333-0034 A Consumer s Guide to Homeowners Insurance A Publication of the Maine Bureau of Insurance April 2015 A Consumer s Guide to Homeowners

What s UP with Renters Insurance?

What s UP with Renters Insurance? Renters insurance is a bargain compared to most kinds of insurance. It s the best way to make sure you ll have cash to repair or replace your belongings if a fire or natural

What s UP with Renters Insurance? Renters insurance is a bargain compared to most kinds of insurance. It s the best way to make sure you ll have cash to repair or replace your belongings if a fire or natural

A Massachusetts Guide to Understanding the Insurance Policy Covering Your Home

A Massachusetts Guide to Understanding the Insurance Policy Covering Your Home DEVAL L. PATRICK GOVERNOR DANIEL O CONNELL SECRETARY OF HOUSING AND ECONOMIC DEVELOPMENT DANIEL C. CRANE DIRECTOR OF THE OFFICE

A Massachusetts Guide to Understanding the Insurance Policy Covering Your Home DEVAL L. PATRICK GOVERNOR DANIEL O CONNELL SECRETARY OF HOUSING AND ECONOMIC DEVELOPMENT DANIEL C. CRANE DIRECTOR OF THE OFFICE

PERSONAL INSURANCE. Renters Insurance. Affordable protection for you

PERSONAL INSURANCE Renters Insurance Affordable protection for you ...and Your Personal Possessions In all likelihood, your landlord has insurance on the building you call home. It protects your landlord

PERSONAL INSURANCE Renters Insurance Affordable protection for you ...and Your Personal Possessions In all likelihood, your landlord has insurance on the building you call home. It protects your landlord

Insuring Fuller Center Houses

Insuring Fuller Center Houses Builders Risk Construction Insurance Once the Fuller Center Covenant Partner acquires property, the task of risk management becomes the responsibility of the organization

Insuring Fuller Center Houses Builders Risk Construction Insurance Once the Fuller Center Covenant Partner acquires property, the task of risk management becomes the responsibility of the organization

Charting Your Course to Home Ownership

Charting Your Course to Home Ownership Insuring Your Home Home owners insurance is important to help you recover from losses you could not afford. In fact, most lenders require home buyers to get and keep

Charting Your Course to Home Ownership Insuring Your Home Home owners insurance is important to help you recover from losses you could not afford. In fact, most lenders require home buyers to get and keep

You may be able to save hundreds of dollars a year on homeowners insurance by shopping around. You can also save money with these tips.

Hazard Insurance You may be able to save hundreds of dollars a year on homeowners insurance by shopping around. You can also save money with these tips. Consider a higher deductible. Increasing your deductible

Hazard Insurance You may be able to save hundreds of dollars a year on homeowners insurance by shopping around. You can also save money with these tips. Consider a higher deductible. Increasing your deductible

your claim Understanding the catastrophe claim process

your claim Understanding the catastrophe claim process YOU SHOULD NEVER have to face a catastrophe alone. That s Allstate s stand. When severe weather or a catastrophic event occurs, Allstate understands

your claim Understanding the catastrophe claim process YOU SHOULD NEVER have to face a catastrophe alone. That s Allstate s stand. When severe weather or a catastrophic event occurs, Allstate understands

Texas Homeowner Forms and Endorsements Description

Texas Homeowner The following is a brief description of the ISO Homeowners Policy Forms. HO 00 03 10 00. Homeowners 3 Special Form. This form is analogous to the Texas Homeowners Policy - Form B. A side-by-side

Texas Homeowner The following is a brief description of the ISO Homeowners Policy Forms. HO 00 03 10 00. Homeowners 3 Special Form. This form is analogous to the Texas Homeowners Policy - Form B. A side-by-side

Coverage that fits your lifestyle

CONDOMINIUM UNITOWNERS Coverage that fits your lifestyle Your condominium (condo) association may include insurance for the building s structure, but covering your unit and personal possessions is up to

CONDOMINIUM UNITOWNERS Coverage that fits your lifestyle Your condominium (condo) association may include insurance for the building s structure, but covering your unit and personal possessions is up to

Personal Property Inventory

Personal Property Inventory Our policy is performance. The Hanover Insurance Company 440 Lincoln Street, Worcester, MA 01653 Citizens Insurance Company of America 645 West Grand River Avenue, Howell, MI

Personal Property Inventory Our policy is performance. The Hanover Insurance Company 440 Lincoln Street, Worcester, MA 01653 Citizens Insurance Company of America 645 West Grand River Avenue, Howell, MI

Renters Insurance. Handout 1. Who, me? Why would I need renters insurance?

Handout 1 Renters Insurance Who, me? Why would I need renters insurance? As you wade through the boxes in your bedroom packing for college, look around at each of the things that you value. Whether it's

Handout 1 Renters Insurance Who, me? Why would I need renters insurance? As you wade through the boxes in your bedroom packing for college, look around at each of the things that you value. Whether it's

CONDOMINIUM INSURANCE CONSIDERATIONS OWNER-OCCUPANT AND OWNER WHO RENTS OUT

1 CONDOMINIUM INSURANCE CONSIDERATIONS OWNER-OCCUPANT AND OWNER WHO RENTS OUT BY: ROY L. KAUFMANN CLAUDIO SAYAN LAZARTE 1 OF JACKSON & CAMPBELL, P.C. While the need for casualty and other insurance in

1 CONDOMINIUM INSURANCE CONSIDERATIONS OWNER-OCCUPANT AND OWNER WHO RENTS OUT BY: ROY L. KAUFMANN CLAUDIO SAYAN LAZARTE 1 OF JACKSON & CAMPBELL, P.C. While the need for casualty and other insurance in

A Consumer s Guide Quick

A Consumer s Quick Guide Headquartered in Kansas City, Mo., the National Association of Insurance Commissioners (NAIC) is a voluntary organization of the chief insurance regulatory officials of the 50

A Consumer s Quick Guide Headquartered in Kansas City, Mo., the National Association of Insurance Commissioners (NAIC) is a voluntary organization of the chief insurance regulatory officials of the 50

How To Get A Condominium Unit Owners Insurance

PERSONAL INSURANCE Condominium Unit Owners Insurance You need homeowners insurance, too. Who Pays for the Damage to Your Possessions? Answer: You do. As an owner of a condominium unit, you are also a member

PERSONAL INSURANCE Condominium Unit Owners Insurance You need homeowners insurance, too. Who Pays for the Damage to Your Possessions? Answer: You do. As an owner of a condominium unit, you are also a member

Guide to Boat Insurance:

Guide to Boat Insurance: Coverage for Non-Commercial Boats and Ways to Reduce Costs Commonwealth of Massachusetts Division of Insurance January 2007 How to Use This Guide Your boat is one of your most

Guide to Boat Insurance: Coverage for Non-Commercial Boats and Ways to Reduce Costs Commonwealth of Massachusetts Division of Insurance January 2007 How to Use This Guide Your boat is one of your most

CONDO insurance. protecting your dreams

CONDO insurance protecting your dreams Home is more than where you live. It s how you live. Think of how your personal possessions turn the space you own into a place that s uniquely yours. Now consider

CONDO insurance protecting your dreams Home is more than where you live. It s how you live. Think of how your personal possessions turn the space you own into a place that s uniquely yours. Now consider

Chapter 8 Homeowners Insurance: Section I Coverages

Chapter 8 Homeowners Insurance: Section I Coverages Overview With this chapter we begin our study of property and liability insurance contracts. The first coverage we will examine is a popular personal

Chapter 8 Homeowners Insurance: Section I Coverages Overview With this chapter we begin our study of property and liability insurance contracts. The first coverage we will examine is a popular personal

HOME INSURANCE OUR MISSION IS YOU. HOMEOWNERS INSURANCE. www.afi.org

HOME INSURANCE OUR MISSION IS YOU. HOMEOWNERS INSURANCE www.afi.org Our Mission Like those who serve our nation, AFI is dedicated to delivering protection and peace of mind. Our unwavering commitment to

HOME INSURANCE OUR MISSION IS YOU. HOMEOWNERS INSURANCE www.afi.org Our Mission Like those who serve our nation, AFI is dedicated to delivering protection and peace of mind. Our unwavering commitment to

made simple Renters Insurance What s inside:

Renters Insurance made simple What s inside: How to read an Allstate Renters Policy Declarations Understanding renters insurance Coverages Deductibles Coverage limits Additional protection How to file

Renters Insurance made simple What s inside: How to read an Allstate Renters Policy Declarations Understanding renters insurance Coverages Deductibles Coverage limits Additional protection How to file

gold star homeowners insurance protecting your dreams

gold star homeowners insurance protecting your dreams Home is where the real you lives. You're the type who pays attention to detail. You keep up to date. From the curb to the backyard, you take pride

gold star homeowners insurance protecting your dreams Home is where the real you lives. You're the type who pays attention to detail. You keep up to date. From the curb to the backyard, you take pride

Not for Reprint. About the NAIC

t rin ep N ot fo rr A Consumer s Guide About the NAIC The National Association of Insurance Commissioners (NAIC) is the oldest association of state government officials. Its members consist of the chief

t rin ep N ot fo rr A Consumer s Guide About the NAIC The National Association of Insurance Commissioners (NAIC) is the oldest association of state government officials. Its members consist of the chief

Your Guide to Homeowners Insurance For Michigan Consumers Page 1

Your Guide to Homeowners Insurance For Michigan Consumers Page 1 Your Guide to Homeowners Insurance For Michigan Consumers Page 2 Table of Contents Page 4 Page 5 Page 6 Page 7 Page 8 Page 9 Page 10 Page

Your Guide to Homeowners Insurance For Michigan Consumers Page 1 Your Guide to Homeowners Insurance For Michigan Consumers Page 2 Table of Contents Page 4 Page 5 Page 6 Page 7 Page 8 Page 9 Page 10 Page

How to Prepare Your Business for an Emergency

/ business Small steps toward preparing your business for emergencies Step 4: Insurance THE GOAL: Make sure you have insurance that will enable you to get back into business after a disaster. Finding the

/ business Small steps toward preparing your business for emergencies Step 4: Insurance THE GOAL: Make sure you have insurance that will enable you to get back into business after a disaster. Finding the

Insuring Your Business... The Basics of Property & Liability Coverage. A Publication of the Maine Bureau of Insurance

Maine Bureau of Insurance 34 State House Station Augusta ME 04333 Insuring Your Business... The Basics of Property & Liability Coverage A Publication of the Maine Bureau of Insurance Table of Contents

Maine Bureau of Insurance 34 State House Station Augusta ME 04333 Insuring Your Business... The Basics of Property & Liability Coverage A Publication of the Maine Bureau of Insurance Table of Contents

condo insurance protecting your dreams

condo insurance protecting your dreams Home is more than where you live. it s how you live. Now you need to protect it. Think of how your personal possessions turn the space you own into a place that s

condo insurance protecting your dreams Home is more than where you live. it s how you live. Now you need to protect it. Think of how your personal possessions turn the space you own into a place that s

Home Building Insurance - Information Sheets

BUSHFIRES AND INSURANCE - WHAT YOU NEED TO KNOW INSURING YOUR HOME AND CONTENTS INTRODUCTION People buy home building and contents insurance to try to protect themselves from significant financial loss,

BUSHFIRES AND INSURANCE - WHAT YOU NEED TO KNOW INSURING YOUR HOME AND CONTENTS INTRODUCTION People buy home building and contents insurance to try to protect themselves from significant financial loss,

RENTERS INSURANCE PROTECTING YOUR DREAMS

RENTERS INSURANCE PROTECTING YOUR DREAMS You ve Always Dreamed of Your Own Things, in Your Own Place A Place You Call Home Think of how your personal possessions turn the space you rent into a place that

RENTERS INSURANCE PROTECTING YOUR DREAMS You ve Always Dreamed of Your Own Things, in Your Own Place A Place You Call Home Think of how your personal possessions turn the space you rent into a place that

Condominium Unitowners Insurance

Condominium Unitowners Insurance Coverage that fits your lifestyle Your condominium (condo) association may include insurance for the building s structure, but covering your unit and personal possessions

Condominium Unitowners Insurance Coverage that fits your lifestyle Your condominium (condo) association may include insurance for the building s structure, but covering your unit and personal possessions

Chapter 10. Chapter 10 Learning Objectives. Insurance and Risk Management: An Introduction. Property and Motor Vehicle Insurance

Chapter 10 Property and Motor Vehicle Insurance McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 10-1 Chapter 10 Learning Objectives 1. Develop a risk management

Chapter 10 Property and Motor Vehicle Insurance McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 10-1 Chapter 10 Learning Objectives 1. Develop a risk management

Insuring Against A Hurricane

Insuring Against A Hurricane Protecting Your Home or Business Against Hurricane-related Financial Losses About A trusted choice for more than 20 years, of Ponte Vedra offers inspired solutions to a broad

Insuring Against A Hurricane Protecting Your Home or Business Against Hurricane-related Financial Losses About A trusted choice for more than 20 years, of Ponte Vedra offers inspired solutions to a broad

Insuring Your Home BANKING AND INSURANCE. to Homeowners, Renters and

New A Jersey consumer Department guide of to Homeowners, Renters and BANKING AND INSURANCE Chris Christie Governor Kim Guadagno Lt. Governor Kenneth E. Kobylowski Commissioner Insuring Your Home The New

New A Jersey consumer Department guide of to Homeowners, Renters and BANKING AND INSURANCE Chris Christie Governor Kim Guadagno Lt. Governor Kenneth E. Kobylowski Commissioner Insuring Your Home The New

Home insurance basics

Home insurance basics By Nicholas Schidowka, President Insurance Cleveland Agency, LLC When shopping for home insurance, it is important for a homeowner to consider more than how much coverage will cost.

Home insurance basics By Nicholas Schidowka, President Insurance Cleveland Agency, LLC When shopping for home insurance, it is important for a homeowner to consider more than how much coverage will cost.

Condominium Insurance

Condominium Insurance made simple What s inside: How to read an Allstate Condominium Policy Declarations Understanding condominium insurance Coverages Deductibles Coverage limits Additional protection

Condominium Insurance made simple What s inside: How to read an Allstate Condominium Policy Declarations Understanding condominium insurance Coverages Deductibles Coverage limits Additional protection

HOME INSURANCE NEVADA CONSUMER S GUIDE

HOME INSURANCE NEVADA CONSUMER S GUIDE State of Nevada Department of Business and Industry DIVISION OF INSURANCE Scott J. Kipper, Commissioner Brian Sandoval, Governor Bruce H. Breslow, Director Published:

HOME INSURANCE NEVADA CONSUMER S GUIDE State of Nevada Department of Business and Industry DIVISION OF INSURANCE Scott J. Kipper, Commissioner Brian Sandoval, Governor Bruce H. Breslow, Director Published:

INSURANCE ESSENTIALS: PREPARE FOR THE FUTURE. Weissman, Nowack, Curry & Wilco, P.C.

INSURANCE ESSENTIALS: PREPARE FOR THE FUTURE Weissman, Nowack, Curry & Wilco, P.C. The Board of Directors of a community association is charged with operating the association in a manner that preserves,

INSURANCE ESSENTIALS: PREPARE FOR THE FUTURE Weissman, Nowack, Curry & Wilco, P.C. The Board of Directors of a community association is charged with operating the association in a manner that preserves,

Adviceguide Advice that makes a difference

Buildings insurance What is buildings insurance Buildings insurance covers the cost of damage to the structure of your property. This includes the roof, walls, ceilings, floors, doors and windows. Outdoor

Buildings insurance What is buildings insurance Buildings insurance covers the cost of damage to the structure of your property. This includes the roof, walls, ceilings, floors, doors and windows. Outdoor

DIVISION OF INSURANCE

Alaska Consumer Guide to Home insurance State of Alaska Department of Commerce, Community, and Economic Development DIVISION OF INSURANCE About the Alaska Division of Insurance The most important function

Alaska Consumer Guide to Home insurance State of Alaska Department of Commerce, Community, and Economic Development DIVISION OF INSURANCE About the Alaska Division of Insurance The most important function

MANUFACTURED/MOBILE HOME PROGRAM UNDERWRITING RULES & COVERAGE OPTIONS

MANUFACTURED/MOBILE HOME PROGRAM UNDERWRITING RULES & COVERAGE OPTIONS Underwritten by A Rated Carriers Effective: January 1, 2011 This Underwriting Guide is for informational purposes only. Coverage authorization

MANUFACTURED/MOBILE HOME PROGRAM UNDERWRITING RULES & COVERAGE OPTIONS Underwritten by A Rated Carriers Effective: January 1, 2011 This Underwriting Guide is for informational purposes only. Coverage authorization

your claim Understanding catastrophe auto claims

your claim Understanding catastrophe auto claims You deserve prompt and professional CLAIM SERVICE. That s Allstate s Stand. When severe weather or a catastrophic event occurs, we understand your need

your claim Understanding catastrophe auto claims You deserve prompt and professional CLAIM SERVICE. That s Allstate s Stand. When severe weather or a catastrophic event occurs, we understand your need