2014 International Monetary Fund. Cover and Design: Luisa Menjivar and Jorge Salazar Composition: Maryland Composition. Cataloging-in-Publication Data

|

|

|

- Russell O’Connor’

- 8 years ago

- Views:

Transcription

1

2 2014 International Monetary Fund Cover and Design: Luisa Menjivar and Jorge Salazar Composition: Maryland Composition Cataloging-in-Publication Data Joint Bank-Fund Library World economic outlook (International Monetary Fund) World economic outlook : a survey by the staff of the International Monetary Fund. Washington, DC : International Monetary Fund, 1980 v. ; 28 cm. ( : Occasional paper / International Monetary Fund, ). (1986 : World economic and financial surveys, ) Semiannual. Some issues also have thematic titles. Has occasional updates, 1984 ISSN (print) ISSN (online) Economic development Periodicals. 2. Economic forecasting Periodicals. 3. Economic policy Periodicals. 4. International economic relations Periodicals. I. International Monetary Fund. II. Series: Occasional paper (International Monetary Fund). III. Series: World economic and financial surveys. HC10.80 ISBN (paper) (PDF) (epub) (Mobi) Disclaimer: The analysis and policy considerations expressed in this publication are those of the IMF staff and do not represent official IMF policy or the views of the IMF Executive Directors or their national authorities. Recommended citation: International Monetary Fund, World Economic Outlook Recovery Strengthens, Remains Uneven (Washington, April 2014). Publication orders may be placed online, by fax, or through the mail: International Monetary Fund, Publication Services P.O. Box 92780, Washington, DC 20090, U.S.A. Tel.: (202) Fax: (202) publications@imf.org

0256 6877 ISSN (online) 1564 5215 1. Economic development Periodicals. 2. Economic forecasting Periodicals. 3. Economic policy Periodicals. 4.")

3

4 WORLD ECONOMIC OUTLOOK: RECOVERY STRENGTHENS, REMAINS UNEVEN Appendix 3.5. Sensitivity of Saving and Investment to Real Rates 101 Appendix 3.6. Saving and Growth with Consumption Habit 102 Appendix 3.7. Sample of Countries Used in Tables and Figures 102 Box 3.1. Saving and Economic Growth 107 References 111 Chapter 4. On the Receiving End? External Conditions and Emerging Market Growth Before, During, and After the Global Financial Crisis 113 Effects of External Factors on Emerging Market Growth 116 Global Chain or Global China? Quantifying China s Impact 124 Growth Effects: The Long and the Short of It 126 Shifting Gears: Have Emerging Markets Growth Dynamics Changed since the Global Financial Crisis? 128 Policy Implications and Conclusions 133 Appendix 4.1. Data Definitions, Sources, and Descriptions 133 Appendix 4.2. Estimation Approach and Robustness Checks 137 Box 4.1. The Impact of External Conditions on Medium-Term Growth in Emerging Market Economies 145 References 150 Annex: IMF Executive Board Discussion of the Outlook, March Statistical Appendix 155 Assumptions 155 What s New 156 Data and Conventions 156 Classification of Countries 157 General Features and Composition of Groups in the World Economic Outlook Classification 157 Table A. Classification by World Economic Outlook Groups and Their Shares in Aggregate GDP, Exports of Goods and Services, and Population, Table B. Advanced Economies by Subgroup 160 Table C. European Union 160 Table D. Emerging Market and Developing Economies by Region and Main Source of Export Earnings 161 Table E. Emerging Market and Developing Economies by Region, Net External Position, Status as Heavily Indebted Poor Countries, and Low-Income Developing Countries 162 Table F. Key Data Documentation 164 Box A1. Economic Policy Assumptions Underlying the Projections for Selected Economies 174 List of Tables 179 Output (Tables A1 A4) 180 Inflation (Tables A5 A7) 187 Financial Policies (Table A8) 192 Foreign Trade (Table A9) 193 Current Account Transactions (Tables A10 A12) 195 Balance of Payments and External Financing (Tables A13 A14) 201 Flow of Funds (Table A15) 203 Medium-Term Baseline Scenario (Table A16) 207 World Economic Outlook, Selected Topics 209 iv International Monetary Fund April 2014

5 CONTENTS Tables Table 1.1. Overview of the World Economic Outlook Projections 2 Table 1.SF.1. Root-Mean-Squared Errors across Forecast Horizons h (Relative to the Random Walk Model) 31 Table Consensus Consumer Price Index Inflation Expectations 42 Table 2.1. Selected Advanced Economies: Real GDP, Consumer Prices, Current Account Balance, and Unemployment 52 Table 2.2. Selected European Economies: Real GDP, Consumer Prices, Current Account Balance, and Unemployment 54 Table 2.3. Selected Asian Economies: Real GDP, Consumer Prices, Current Account Balance, and Unemployment 59 Table 2.4. Selected Western Hemisphere Economies: Real GDP, Consumer Prices, Current Account Balance, and Unemployment 62 Table 2.5. Commonwealth of Independent States: Real GDP, Consumer Prices, Current Account Balance, and Unemployment 65 Table 2.6. Selected Middle East and North African Economies: Real GDP, Consumer Prices, Current Account Balance, and Unemployment 67 Table 2.7. Selected Sub-Saharan African Economies: Real GDP, Consumer Prices, Current Account Balance, and Unemployment 69 Table 2.SF.1. Exports to Emerging Market Economies, 1995 versus Table 3.1. Alternative Hypotheses Explaining a Decline in Real Interest Rates 87 Table 3.2. Factors Affecting Real Interest Rates 96 Table 3.3. Investment (Saving) and the Real Interest Rate, Reduced-Form Equations 102 Table 3.4. Data Coverage for Global Interest Rates, Investment, and Saving 103 Table Saving and Growth: Granger Causality Tests 108 Table Determinants of the Evolution in Saving-to-GDP Ratios 110 Table 4.1. Impulse Responses to Shocks within the External Block: Baseline Model 119 Table 4.2. Impulse Responses to Shocks within the External Block: Modified Baseline Model with China Real GDP Growth 126 Table 4.3. Share of Output Variance Due to External Factors 128 Table 4.4. Data Sources 134 Table 4.5 Sample of Emerging Market Economies and International Organization for Standardization Country Codes 135 Table 4.6. Correlations of Domestic Real GDP Growth with Key Variables, Table Growth Regressions for Emerging Markets, Table Growth Regressions for Emerging Markets: Brazil, China, India, Russia, and South Africa versus Other Emerging Market Partner Growth, Table Growth Regressions for Emerging Markets 149 Table A1. Summary of World Output 180 Table A2. Advanced Economies: Real GDP and Total Domestic Demand 181 Table A3. Advanced Economies: Components of Real GDP 182 Table A4. Emerging Market and Developing Economies: Real GDP 184 Table A5. Summary of Inflation 187 Table A6. Advanced Economies: Consumer Prices 188 Table A7. Emerging Market and Developing Economies: Consumer Prices 189 Table A8. Major Advanced Economies: General Government Fiscal Balances and Debt 192 Table A9. Summary of World Trade Volumes and Prices 193 Table A10. Summary of Balances on Current Account 195 Table A11. Advanced Economies: Balance on Current Account 197 International Monetary Fund April 2014 v

6 WORLD ECONOMIC OUTLOOK: RECOVERY STRENGTHENS, REMAINS UNEVEN Table A12. Emerging Market and Developing Economies: Balance on Current Account 198 Table A13. Emerging Market and Developing Economies: Net Financial Flows 201 Table A14. Emerging Market and Developing Economies: Private Financial Flows 202 Table A15. Summary of Sources and Uses of World Savings 203 Table A16. Summary of World Medium-Term Baseline Scenario 207 Online Tables Figures Table B1. Advanced Economies: Unemployment, Employment, and Real GDP per Capita Table B2. Emerging Market and Developing Economies: Real GDP Table B3. Advanced Economies: Hourly Earnings, Productivity, and Unit Labor Costs in Manufacturing Table B4. Emerging Market and Developing Economies: Consumer Prices Table B5. Summary of Fiscal and Financial Indicators Table B6. Advanced Economies: General and Central Government Net Lending/Borrowing and Excluding Social Security Schemes Table B7. Advanced Economies: General Government Structural Balances Table B8. Emerging Market and Developing Economies: General Government Net Lending/ Borrowing and Overall Fiscal Balance Table B9. Emerging Market and Developing Economies: General Government Net Lending/ Borrowing Table B10. Advanced Economies: Exchange Rates Table B11. Emerging Market and Developing Economies: Broad Money Aggregates Table B12. Advanced Economies: Export Volumes, Import Volumes, and Terms of Trade in Goods and Services Table B13. Emerging Market and Developing Economies by Region: Total Trade in Goods Table B14. Emerging Market and Developing Economies by Source of Export Earnings: Total Trade in Goods Table B15. Advanced Economies: Current Account Transactions Table B16. Emerging Market and Developing Economies: Balances on Current Account Table B17. Emerging Market and Developing Economies by Region: Current Account Transactions Table B18. Emerging Market and Developing Economies by Analytical Criteria: Current Account Transactions Table B19. Summary of Balance of Payments, Financial Flows, and External Financing Table B20. Emerging Market and Developing Economies by Region: Balance of Payments and External Financing Table B21. Emerging Market and Developing Economies by Analytical Criteria: Balance of Payments and External Financing Table B22. Summary of External Debt and Debt Service Table B23. Emerging Market and Developing Economies by Region: External Debt by Maturity and Type of Creditor Table B24. Emerging Market and Developing Economies by Analytical Criteria: External Debt by Maturity and Type of Creditor Table B25. Emerging Market and Developing Economies: Ratio of External Debt to GDP Table B26. Emerging Market and Developing Economies: Debt-Service Ratios Table B27. Emerging Market and Developing Economies, Medium-Term Baseline Scenario: Selected Economic Indicators Figure 1.1. Global Activity Indicators 3 Figure 1.2. GDP Growth Forecasts 3 Figure 1.3. Monetary Conditions in Advanced Economies 4 vi International Monetary Fund April 2014

7 CONTENTS Figure 1.4. Fiscal Policies 5 Figure 1.5. Global Inflation 6 Figure 1.6. Capacity, Unemployment, and Output Trend 7 Figure 1.7. Overheating Indicators for the Group of Twenty Economies 9 Figure 1.8. Financial Market Conditions in Advanced Economies 10 Figure 1.9. Financial Conditions and Capital Flows in Emerging Market Economies 11 Figure Monetary Policies and Credit in Emerging Market Economies 11 Figure Exchange Rates and Reserves 12 Figure External Sector 13 Figure Risks to the Global Outlook 14 Figure Recession and Deflation Risks 14 Figure Slower Growth in Emerging Market Economies and a Faster Recovery in the United States 18 Figure 1.SF.1. Commodity Market Developments 26 Figure 1.SF.2. Brent Forecast Errors and Futures 27 Figure 1.SF.3. Vector Autoregression and Combination Forecasts 29 Figure 1.SF.4. Rolling Root-Mean-Squared Errors: Recursive Estimation 30 Figure Cumulative Responses of GDP to a 10 Percentage Point Tightening of Lending Standards 33 Figure Credit Supply Shocks 34 Figure Contribution of Credit Supply Shocks to GDP 34 Figure China: Real GDP Growth and Commodity Prices 36 Figure Growth Rate of Global Commodity Consumption 37 Figure Actual and Predicted Per Capita Commodity Consumption 38 Figure Spending Patterns 39 Figure Inflation Expectations in Euro Area, United States, Japan, and Norway 41 Figure Distribution of Exchange Rate Regimes in Emerging Markets, Figure Predicted Crisis Probability in Emerging Markets, Figure Probability of Banking or Currency Crisis 46 Figure GDP Growth Forecasts and the Effects of a Plausible Downside Scenario 50 Figure 2.2. United States and Canada: Recovery Firming Up 51 Figure 2.3. Advanced Europe: From Recession to Recovery 55 Figure 2.4. Emerging and Developing Europe: Recovery Strengthening, but with Vulnerabilities 56 Figure 2.5. Asia: Steady Recovery 58 Figure 2.6. Latin America and the Caribbean: Subdued Growth 61 Figure 2.7. Commonwealth of Independent States: Subdued Prospects 64 Figure 2.8. Middle East, North Africa, Afghanistan, and Pakistan: Turning a Corner? 66 Figure 2.9. Sub-Saharan Africa: Accelerating Growth 70 Figure 2.SF.1. Real Trade Linkages between Advanced Economies and Emerging Market Economies 73 Figure 2.SF.2. Financial Exposure of Advanced Economies to Emerging Market Economies 74 Figure 2.SF.3. Event Studies around Downturn Episodes in Emerging Market Economies 75 Figure 2.SF.4. Peak Effect of a Growth Shock to Emerging Market Economies on Advanced Economies Output Growth 77 Figure 2.SF.5. Model Simulations of Potential Growth Spillover Effects from Emerging Market Economies on Advanced Economies 78 Figure 3.1. Ten-Year Interest Rate on Government Bonds and Inflation 81 Figure 3.2. Real Interest Rate Comparison 84 Figure 3.3. Real Interest Rates, Real Returns on Equity, and Cost of Capital 85 Figure 3.4. Common Factors in Real Interest Rates 85 Figure 3.5. Real Interest Rate and Shifts in Demand for and Supply of Funds 87 Figure 3.6. Investment-to-GDP Ratios 88 Figure 3.7. Investment Shifts in Advanced Economies 89 International Monetary Fund April 2014 vii

8 WORLD ECONOMIC OUTLOOK: RECOVERY STRENGTHENS, REMAINS UNEVEN Figure 3.8. Saving Shifts in Emerging Markets 90 Figure 3.9. Effect of Fiscal Policy on Real Interest Rates 91 Figure Effect of U.S. Monetary Policy Shocks on Real Interest Rates 92 Figure Real Long-Term Interest Rates and Real Returns on Equity 93 Figure Portfolio Shifts and Relative Demand for Bonds versus Equity 94 Figure Portfolio Shifts and Relative Riskiness of Bonds versus Equity, Figure Effect of Financial Crises on Saving- and Investment-to-GDP Ratios 95 Figure Implications of Lower Real Interest Rates for Debt Sustainability 97 Figure Investment Shifts in Advanced Economies 100 Figure Global Long-Term Real Interest Rates 106 Figure Convergence of Real Interest Rates in the Euro Area 106 Figure Saving Rate and Accelerations (Decelerations) in GDP 109 Figure Total Saving: Actual versus Conditional Forecasts 109 Figure 4.1. Growth Developments in Advanced and Emerging Market and Developing Economies 114 Figure 4.2. Average Country Rankings, Figure 4.3. Impulse Responses of Domestic Real GDP Growth to External Demand Shocks 120 Figure 4.4. Impulse Responses to External Financing Shock 120 Figure 4.5. Impulse Responses to U.S. High-Yield Spread Shock 121 Figure 4.6. Correlations between Growth Responses to External Shocks and Country-Specific Characteristics 122 Figure 4.7. Impulse Responses of Domestic Real GDP Growth to Terms-of-Trade Growth Shock 123 Figure 4.8. Historical Decompositions of Real GDP Growth into Internal and External Factors 124 Figure 4.9. Impulse Responses to Real GDP Growth Shock in China 125 Figure Historical Decomposition of Real GDP Growth with China as an Explicit External Factor 127 Figure Emerging Markets Output and Growth Performance after Global Recessions 129 Figure Out-of-Sample Growth Forecasts Conditional on External Factors, by Country 131 Figure Conditional Forecast and Actual Growth since the Global Financial Crisis, by Country 132 Figure Domestic Real GDP Growth across Emerging Markets versus United States and China 136 Figure Average Growth for Regional Groups of Emerging Market Economies 137 Figure Impact of Prior Choice on Average Impulse Responses 139 Figure Average Impulse Responses to Shocks from Alternative U.S. Monetary Policy Variables 140 Figure Domestic Real GDP Growth Response to U.S. Federal Funds Rate and 10-Year U.S. Treasury Bond Rate under Alternative Specifications 141 Figure Average Impulse Responses to Alternative Measures of U.S. Monetary Policy Shock 142 Figure Alternative Monetary Policy Shocks 142 Figure Impulse Response of Domestic Real GDP Growth to External Financing Shocks 143 Figure Average Impulse Responses of Domestic Real GDP Growth to Shocks under Alternative Vector Autoregression Specifications 143 Figure Brazil: Comparison of Responses under the Baseline Model with Responses from Model with Sample Beginning in the First Quarter of Figure Comparison of Impulse Responses from Panel Vector Autoregression with Responses from the Baseline Model 144 Figure Export Partner Growth Elasticity 147 Figure Export Partner Growth 147 viii International Monetary Fund April 2014

9

10 WORLD ECONOMIC OUTLOOK: RECOVERY STRENGTHENS, REMAINS UNEVEN As used in this report, the terms country and economy do not in all cases refer to a territorial entity that is a state as understood by international law and practice. As used here, the term also covers some territorial entities that are not states but for which statistical data are maintained on a separate and independent basis. Composite data are provided for various groups of countries organized according to economic characteristics or region. Unless noted otherwise, country group composites represent calculations based on 90 percent or more of the weighted group data. The boundaries, colors, denominations, and any other information shown on the maps do not imply, on the part of the International Monetary Fund, any judgment on the legal status of any territory or any endorsement or acceptance of such boundaries. x International Monetary Fund April 2014

11

12

13

14

15

16 WORLD ECONOMIC OUTLOOK: RECOVERY STRENGTHENS, REMAINS UNEVEN to deflation if other downside risks to activity materialize. The result would be higher real interest rates, an increase in private and public debt burdens, and weaker demand and output. The strengthening of the recovery from the Great Recession in the advanced economies is a welcome development. But growth is not evenly robust across the globe, and more policy efforts are needed to fully restore confidence, ensure robust growth, and lower downside risks. Policymakers in advanced economies need to avoid a premature withdrawal of monetary accommodation. In an environment of continued fiscal consolidation, still-large output gaps, and very low inflation, monetary policy should remain accommodative. In the euro area, more monetary easing, including unconventional measures, is necessary to sustain activity and help achieve the European Central Bank s price stability objective, thus lowering risks of even lower inflation or outright deflation. Sustained low inflation would not likely be conducive to a suitable recovery of economic growth. In Japan, implementation of the remaining two arrows of Abenomics structural reform and plans for fiscal consolidation beyond 2015 is essential to achieve the inflation target and higher sustained growth. The need for credible medium-term fiscal plans, however, extends beyond Japan. The April 2014 Fiscal Monitor highlights that the combination of large public debt stocks and the absence of medium-term adjustment plans that include specific measures and strong entitlement reforms is the main factor behind important mediumterm fiscal risks in advanced economies, including in the United States. In the euro area, repairing bank balance sheets in the context of a credible asset quality review and recapitalizing weak banks will be critical if confidence is to improve and credit is to revive. Also essential for achieving these goals is progress on completing the banking union including an independent Single Resolution Mechanism with the capacity to undertake timely bank resolution and common backstops to sever the link between sovereigns and banks. More structural reforms are needed to lift investment and activity prospects. Emerging market economies will have to weather turbulence and maintain high medium-term growth. The appropriate policy measures will differ across these economies. However, many of them have some policy priorities in common. First, policymakers should allow exchange rates to respond to changing fundamentals and facilitate external adjustment. Where international reserves are adequate, foreign exchange interventions can be used to smooth volatility and avoid financial disruption. Second, in economies in which inflation is still relatively high or the risks that recent currency depreciation could feed into underlying inflation are high, further monetary policy tightening may be necessary. If policy credibility is a problem, strengthening the transparency and consistency of policy frameworks may be necessary for tightening to be effective. Third, on the fiscal front, policymakers must lower budget deficits, although the urgency for action varies across economies. Early steps are required if public debt is already elevated and the associated refinancing needs are a source of vulnerability. Fourth, many economies need a new round of structural reforms that include investment in public infrastructure, removal of barriers to entry in product and services markets, and in China, rebalancing growth away from investment toward consumption. Low-income countries will need to avoid a buildup of external and public debt. Many of these countries have succeeded in maintaining strong growth, partly reflecting better macroeconomic policies, but their external environment has also been changing. Foreign direct investment has started to moderate with declining commodity prices, and commodity-related budget revenues and foreign exchange earnings are at risk. Timely policy adjustments will be important to avoid a buildup in external debt and public debt. xvi International Monetary Fund April 2014

17

18

19

20

21

22

23

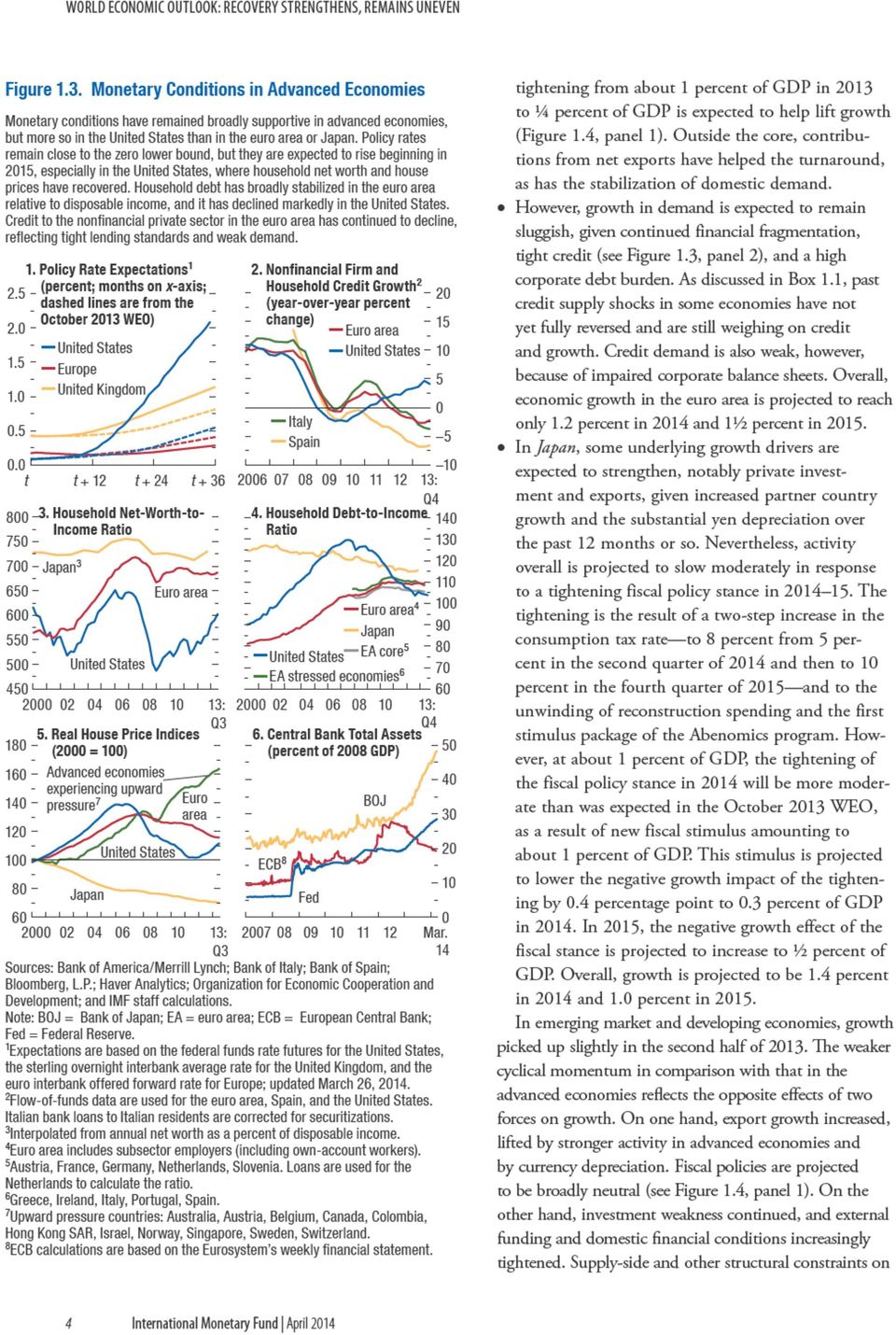

24 WORLD ECONOMIC OUTLOOK: RECOVERY STRENGTHENS, REMAINS UNEVEN 2013 as a whole, inflation was 1.3 percent, which is closer to the lower end of the range forecast provided by the European Central Bank (ECB) staff at the end of 2012 and below the lowest value provided by Consensus Forecast survey participants at the time. Inflation is projected to increase slightly as the recovery strengthens and output gaps slowly decrease. Under the current baseline projections, inflation is expected to remain below the ECB s price stability objective until at least In Japan, inflation started to increase with stronger growth and the depreciation of the yen during the past year or so. In , it is projected to accelerate temporarily in response to increases in the consumption tax. Indications are, however, that labor market conditions have started to tighten. Nominal wages have also begun to increase, and underlying inflation is projected to converge gradually toward the 2 percent target. In emerging market and developing economies, inflation is expected to decline from about 6 percent currently to about 5¼ percent by 2015 (Figure 1.5, panel 1). Softer world commodity prices in U.S. dollar terms should help reduce price pressures, although in some economies, this reduction will be more than offset by recent exchange rate depreciation. In addition, activityrelated price pressures will ease with the recent growth declines in many emerging market economies. That said, this relief will be limited in some emerging market economies, given evidence of domestic demand pressures and capacity constraints in some sectors (red and yellow overheating indicators in Figure 1.7). This picture is consistent with output remaining above crisis trend and unemployment having declined further in a number of emerging market economies (Figure 1.6, panels 1 and 2). In low-income developing economies, softer commodity prices and careful monetary policy tightening have helped lower inflation from about 9.8 percent in 2012 to 7.8 percent in Based on current policies, inflation is expected to decline further to about 6½ percent. Monetary Policy, Financial Conditions, and Capital Flows Are Diverging Monetary conditions have stayed mostly supportive in advanced economies despite lasting increases in longerterm interest rates since May 2013, when the Federal Reserve announced its intention to begin tapering its asset purchase program (Figure 1.8, panels 2 and 5). However, longer-term rates are still lower than rates that would prevail if the term premium had reversed to precrisis levels, and broad financial conditions have remained easy equity markets have rallied and bond risk spreads remain low (Figure 1.8, panel 3). Monetary policy stances across advanced economies are, however, expected to start diverging in Surveys of market participants (such as the Federal Reserve Bank of New York s January 2014 Survey of Primary Dealers) suggest that the policy rate is expected to increase in the United States in the second half of Information based on futures prices, however, implies that the timing has been advanced to the first half of 2015 (Figure 1.8, panel 1). The WEO projections are in line with the Federal Reserve s forward guidance for a continued growth-friendly policy stance and assume that the first U.S. policy rate hike will take place in the third quarter of The projections take into account that inflation is forecast to remain low, inflation expectations to stay well anchored, and the unemployment rate to continue its slow decline until then. The forecasts also assume that the Federal Reserve will continue tapering asset purchases at the current pace over the next few months and that the program will end by late Markets continue to expect a prolonged period of low interest rates and supportive monetary policy for the euro area and Japan (Figure 1.3, panel 1). Unlike in Europe, Japanese long-term bond yields have remained virtually unchanged since tapering talk began, reflecting both strong demand for bonds by nonresidents and residents and the Bank of Japan s asset purchases. In the euro area, low inflation remains the dominant concern, including deflation pressure in some countries, amid a weak recovery. The WEO projections assume further small declines in sovereign spreads in countries with high debt, consistent with views that sovereign risks have decreased. The projections also assume, however, that financial fragmentation will remain a problem for the transmission of monetary policy impulses in the euro area. Credit conditions will thus remain tight, and credit outstanding will continue to decline for some time, albeit at a slower pace (Figure 1.3, panel 2). The major contributing factors are remaining weaknesses in bank balance sheets and, more generally, the weak economic environment aggravated by high unemployment and large debt burdens. 8 International Monetary Fund April 2014

25

26

27

28

29

30

31 CHAPTER 1 RECENT DEVELOPMENTS AND PROSPECTS ability of a recession (two successive quarters of negative growth) in the four quarters ahead. Nevertheless, recession risks of about 20 percent in the euro area and Japan which partly reflect the relatively low growth projected for these economies and in the Rest of the World group highlight that a number of fragilities remain present in the global recovery. In most economies, the risk of deflation by the end of 2014 is virtually negligible, according to the Global Projection Model simulations. In the euro area, however, the risk of deflation estimated at about 20 percent remains a concern despite some recent declines (Figure 1.14, panel 2). 1 Similarly, broad indicators of deflation vulnerability, which measure the risk of more persistent price level declines, remain above or close to the high-risk threshold for some euro area economies, notwithstanding recent improvements (Figure 1.14, panel 3). In Japan, the absence of near-term deflation risks reflects primarily the price-level effects of the increase in the consumption tax rate to 8 percent in the second quarter of 2014 from the previous 5 percent. A Qualitative Risk Assessment: Some Risks Remain and New Ones Have Emerged Some downside risks identified in the October 2013 WEO have become less relevant, notably shorter-term U.S. fiscal risks because of the two-year budget agreement of December 2013 and the suspension of the debt ceiling until March The other risks, however, remain a concern; new ones have emerged; and the risks related to emerging market economies have increased. More recently, developments in Ukraine have increased geopolitical risks. At the same time, however, upside risks to growth in some advanced economies have developed, improving the balance of risks compared with the October 2013 WEO. 1 The probability of deflation increases with a longer forecast horizon, everything else equal. A longer horizon in this WEO report compared with the October 2013 WEO (three quarters ahead vs. one quarter ahead) is an important reason for a higher probability of deflation in the euro area in panel 2 of Figure The comparable one-quarter-ahead probability for the second quarter of 2014 in this WEO report would be 9 percent, compared to 15 percent in October. While deflation risks have decreased, the estimated probability of euro area inflation being above the ECB s price stability target is only 28 percent in the fourth quarter of 2015 and 42 percent in the fourth quarter of 2016 (probabilities calculated as inflation exceeding 1.9 percent). Advanced economy risks Risks to activity from low inflation: With current inflation lower than expected in many advanced economies, there is a risk, albeit a declining one, of treading into deflation in the event of adverse shocks to activity. In addition, if inflation stays below target for an extended period, as it would under the baseline forecasts, longer-term inflation expectations are likely to drift down. The main reason to be concerned about an adverse impact on activity and debt burdens is that monetary policy will likely be constrained in lowering nominal interest rates for some time, given that policy-relevant rates are already close to the zero lower bound. This risk is primarily a concern in the euro area and, to a lesser extent, in Japan. In the euro area, risks are that inflation could undershoot the ECB s price stability target by more or for longer than under the baseline forecasts, given the very high unemployment and slack in many economies. In Japan, the issues are entrenched expectations after a long period of deflation and the ongoing shifts in employment from regular, full-time positions to nonregular, part-time positions, which hinder nominal wage adjustment in response to the Bank of Japan s new 2 percent inflation target. More generally, if there were to be a persistent decline in commodity prices, possibly because of a larger-than-expected supply response to recent high prices, risks from low inflation could be broader. Reduced appetite for completing national and euroarea-wide reforms as the result of improved growth prospects and reduced market pressures: Downside risks to euro area growth have decreased relative to the October 2013 WEO with important progress in macroeconomic adjustment and improvements in market confidence, but they remain significant. More policy action is needed to reduce unemployment and debt from the current unacceptably high levels and to preserve market confidence. An important short-term concern is that progress in banking sector repair and reform could fall short of what is needed to address financial fragmentation, restore financial market confidence, and enable banks to pass on improved funding conditions and lower policy rates to borrowers. Insufficient bank balance sheet repair could also hold back the restructuring of debt of nonfinancial corporations with balance sheet stresses. Risks related to the normalization of monetary policy in the United States: Tapering risks are expected to International Monetary Fund April

International Monetary and Financial Committee

International Monetary and Financial Committee Twenty-Seventh Meeting April 20, 2013 Statement by Koen Geens, Minister of Finance, Ministere des Finances, Belgium On behalf of Armenia, Belgium, Bosnia

International Monetary and Financial Committee Twenty-Seventh Meeting April 20, 2013 Statement by Koen Geens, Minister of Finance, Ministere des Finances, Belgium On behalf of Armenia, Belgium, Bosnia

RIA Novosti Press Meeting. Economic Outlook and Policy Challenges for Russia in 2012. Odd Per Brekk Senior Resident Representative.

RIA Novosti Press Meeting Economic Outlook and Policy Challenges for Russia in 2012 Odd Per Brekk Senior Resident Representative January 26, 2012 This morning I will start with introductory remarks on

RIA Novosti Press Meeting Economic Outlook and Policy Challenges for Russia in 2012 Odd Per Brekk Senior Resident Representative January 26, 2012 This morning I will start with introductory remarks on

INFLATION REPORT PRESS CONFERENCE. Thursday 4 th February 2016. Opening remarks by the Governor

INFLATION REPORT PRESS CONFERENCE Thursday 4 th February 2016 Opening remarks by the Governor Good afternoon. At its meeting yesterday, the Monetary Policy Committee (MPC) voted 9-0 to maintain Bank Rate

INFLATION REPORT PRESS CONFERENCE Thursday 4 th February 2016 Opening remarks by the Governor Good afternoon. At its meeting yesterday, the Monetary Policy Committee (MPC) voted 9-0 to maintain Bank Rate

Statement by. Janet L. Yellen. Chair. Board of Governors of the Federal Reserve System. before the. Committee on Financial Services

For release at 8:30 a.m. EST February 10, 2016 Statement by Janet L. Yellen Chair Board of Governors of the Federal Reserve System before the Committee on Financial Services U.S. House of Representatives

For release at 8:30 a.m. EST February 10, 2016 Statement by Janet L. Yellen Chair Board of Governors of the Federal Reserve System before the Committee on Financial Services U.S. House of Representatives

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA On the basis of the information available up to 22 May 2009, Eurosystem staff have prepared projections for macroeconomic developments in the

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA On the basis of the information available up to 22 May 2009, Eurosystem staff have prepared projections for macroeconomic developments in the

percentage points to the overall CPI outcome. Goods price inflation increased to 4,6

South African Reserve Bank Press Statement Embargo on Delivery 28 January 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the

South African Reserve Bank Press Statement Embargo on Delivery 28 January 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the

OVERVIEW. A cyclical upswing is underway favoured by several temporary tailwinds

OVERVIEW A cyclical upswing is underway favoured by several temporary tailwinds whose strength underpins an upward revision to the growth forecast this year The outlook for economic growth in the EU has

OVERVIEW A cyclical upswing is underway favoured by several temporary tailwinds whose strength underpins an upward revision to the growth forecast this year The outlook for economic growth in the EU has

Mario Draghi: Europe and the euro a family affair

Mario Draghi: Europe and the euro a family affair Keynote speech by Mr Mario Draghi, President of the European Central Bank, at the conference Europe and the euro a family affair, organised by the Bundesverband

Mario Draghi: Europe and the euro a family affair Keynote speech by Mr Mario Draghi, President of the European Central Bank, at the conference Europe and the euro a family affair, organised by the Bundesverband

Project LINK Meeting New York, 20-22 October 2010. Country Report: Australia

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

World Economic Outlook

World Economic Outlook Transitions and Tensions Rupa Duttagupta Deputy Division Chief Research Department, IMF United Nations, Project LINK Meetings, October 21, 213 1 Global growth dynamics are in transition

World Economic Outlook Transitions and Tensions Rupa Duttagupta Deputy Division Chief Research Department, IMF United Nations, Project LINK Meetings, October 21, 213 1 Global growth dynamics are in transition

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation

August 2014 Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook for factors that typically impact

August 2014 Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook for factors that typically impact

International Monetary and Financial Committee

International Monetary and Financial Committee Twenty-Ninth Meeting April 12, 2014 Statement by Christophe Akagha-Mba, Minister of Economy and Prospective, Gabon On behalf of Benin, Burkina Faso, Cameroon,

International Monetary and Financial Committee Twenty-Ninth Meeting April 12, 2014 Statement by Christophe Akagha-Mba, Minister of Economy and Prospective, Gabon On behalf of Benin, Burkina Faso, Cameroon,

Joint Economic Forecast Spring 2013. German Economy Recovering Long-Term Approach Needed to Economic Policy

Joint Economic Forecast Spring 2013 German Economy Recovering Long-Term Approach Needed to Economic Policy Press version Embargo until: Thursday, 18 April 2013, 11.00 a.m. CEST Joint Economic Forecast

Joint Economic Forecast Spring 2013 German Economy Recovering Long-Term Approach Needed to Economic Policy Press version Embargo until: Thursday, 18 April 2013, 11.00 a.m. CEST Joint Economic Forecast

Meeting with Analysts

CNB s New Forecast (Inflation Report II/2015) Meeting with Analysts Petr Král Prague, 11 May, 2015 1 Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

CNB s New Forecast (Inflation Report II/2015) Meeting with Analysts Petr Král Prague, 11 May, 2015 1 Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

CESEE DELEVERAGING AND CREDIT MONITOR 1

DELEVERAGING AND CREDIT MONITOR 1 February 1, 1 BIS reporting banks continued to scale back their funding to Central, Eastern and South Eastern Europe () in Q3 13, at broadly the same pace as in Q 13,

DELEVERAGING AND CREDIT MONITOR 1 February 1, 1 BIS reporting banks continued to scale back their funding to Central, Eastern and South Eastern Europe () in Q3 13, at broadly the same pace as in Q 13,

March 2016 ECB staff macroeconomic projections for the euro area 1

March 2016 ECB staff macroeconomic projections for the euro area 1 1 Euro area outlook: overview and key features The economic recovery in the euro area is expected to continue, albeit with less momentum

March 2016 ECB staff macroeconomic projections for the euro area 1 1 Euro area outlook: overview and key features The economic recovery in the euro area is expected to continue, albeit with less momentum

X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

18 ECB FACTORS AFFECTING LENDING TO THE PRIVATE SECTOR AND THE SHORT-TERM OUTLOOK FOR MONEY AND LOAN DYNAMICS

Box 2 FACTORS AFFECTING LENDING TO THE PRIVATE SECTOR AND THE SHORT-TERM OUTLOOK FOR MONEY AND LOAN DYNAMICS The intensification of the financial crisis in the fourth quarter of 211 had a considerable

Box 2 FACTORS AFFECTING LENDING TO THE PRIVATE SECTOR AND THE SHORT-TERM OUTLOOK FOR MONEY AND LOAN DYNAMICS The intensification of the financial crisis in the fourth quarter of 211 had a considerable

Lecture 4: The Aftermath of the Crisis

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

SEPTEMBER 2015 ECB STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA 1

SEPTEMBER 2015 STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA 1 1. EURO AREA OUTLOOK: OVERVIEW AND KEY FEATURES The recovery in activity in the euro area is expected to continue, albeit at a somewhat

SEPTEMBER 2015 STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA 1 1. EURO AREA OUTLOOK: OVERVIEW AND KEY FEATURES The recovery in activity in the euro area is expected to continue, albeit at a somewhat

OECD Interim Economic Projections Real GDP 1 Percentage change 2015 2016. September 2015 Interim Projections. Outlook

ass Interim Economic Outlook 16 September 2015 Puzzles and uncertainties Global growth prospects have weakened slightly and become less clear in recent months. World trade growth has stagnated and financial

ass Interim Economic Outlook 16 September 2015 Puzzles and uncertainties Global growth prospects have weakened slightly and become less clear in recent months. World trade growth has stagnated and financial

INTERNATIONAL MONETARY FUND. Russian Federation Concluding Statement for the 2012 Article IV Consultation Mission. Moscow, June 13, 2012

INTERNATIONAL MONETARY FUND Russian Federation Concluding Statement for the 2012 Article IV Consultation Mission Moscow, June 13, 2012 The Russian economy has recovered from the 2008-09 crisis and is now

INTERNATIONAL MONETARY FUND Russian Federation Concluding Statement for the 2012 Article IV Consultation Mission Moscow, June 13, 2012 The Russian economy has recovered from the 2008-09 crisis and is now

EFN REPORT. ECONOMIC OUTLOOK FOR THE EURO AREA IN 2013 and 2014

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2013 and 2014 Summer 2013 1 About the European Forecasting Network The European Forecasting Network (EFN) is a research group of European institutions,

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2013 and 2014 Summer 2013 1 About the European Forecasting Network The European Forecasting Network (EFN) is a research group of European institutions,

New Monetary Policy Challenges

New Monetary Policy Challenges 63 Journal of Central Banking Theory and Practice, 2013, 1, pp. 63-67 Received: 5 December 2012; accepted: 4 January 2013 UDC: 336.74 Alexey V. Ulyukaev * New Monetary Policy

New Monetary Policy Challenges 63 Journal of Central Banking Theory and Practice, 2013, 1, pp. 63-67 Received: 5 December 2012; accepted: 4 January 2013 UDC: 336.74 Alexey V. Ulyukaev * New Monetary Policy

Caucasus and Central Asia: Oil Price Decline and Regional Spillovers Darken the Outlook

Caucasus and Central Asia: Oil Price Decline and Regional Spillovers Darken the Outlook Economic activity in the Caucasus and Central Asia (CCA) will continue to decelerate in 215 mainly as a consequence

Caucasus and Central Asia: Oil Price Decline and Regional Spillovers Darken the Outlook Economic activity in the Caucasus and Central Asia (CCA) will continue to decelerate in 215 mainly as a consequence

Adjusting to a Changing Economic World. Good afternoon, ladies and gentlemen. It s a pleasure to be with you here in Montréal today.

Remarks by David Dodge Governor of the Bank of Canada to the Board of Trade of Metropolitan Montreal Montréal, Quebec 11 February 2004 Adjusting to a Changing Economic World Good afternoon, ladies and

Remarks by David Dodge Governor of the Bank of Canada to the Board of Trade of Metropolitan Montreal Montréal, Quebec 11 February 2004 Adjusting to a Changing Economic World Good afternoon, ladies and

BANK OF ISRAEL Office of the Spokesperson and Economic Information. Report to the public on the Bank of Israel s discussions prior to deciding on the

BANK OF ISRAEL Office of the Spokesperson and Economic Information September 7, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on the General interest rate for September

BANK OF ISRAEL Office of the Spokesperson and Economic Information September 7, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on the General interest rate for September

6. Economic Outlook. The International Economy. Graph 6.1 Australia s Trading Partner Growth* Year-average RBA forecast

6. Economic Outlook The International Economy Overall, growth of Australia s major trading partners (MTPs) is expected to be a bit above its long-run average in 014 and 015 (Graph 6.1). Forecasts for most

6. Economic Outlook The International Economy Overall, growth of Australia s major trading partners (MTPs) is expected to be a bit above its long-run average in 014 and 015 (Graph 6.1). Forecasts for most

Euro Zone s Economic Outlook and What it Means for the United States

WELCOME TO THE WEBINAR WEBINAR LINK: HTTP://FRBATL.ADOBECONNECT.COM/ECONOMY/ DIAL-IN NUMBER (MUST USE FOR AUDIO): 855-377-2663 ACCESS CODE: 71032685 Euro Zone s Economic Outlook and What it Means for the

WELCOME TO THE WEBINAR WEBINAR LINK: HTTP://FRBATL.ADOBECONNECT.COM/ECONOMY/ DIAL-IN NUMBER (MUST USE FOR AUDIO): 855-377-2663 ACCESS CODE: 71032685 Euro Zone s Economic Outlook and What it Means for the

EFN REPORT. ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016. Winter 2014/15

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016 Winter 2014/15 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016 Winter 2014/15 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market

Communications P.O. Box, CH-8022 Zurich Telephone +41 44 631 31 11 Fax +41 44 631 39 10 Zurich, 13 September 2007 Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market The

Communications P.O. Box, CH-8022 Zurich Telephone +41 44 631 31 11 Fax +41 44 631 39 10 Zurich, 13 September 2007 Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market The

Growth and volatility will define global economy in 2016, says PineBridge Investments

Growth and volatility will define global economy in 2016, says PineBridge Investments PineBridge Investments forecasts 2.7% GDP growth in the United States Eurozone growth projected to slightly improve

Growth and volatility will define global economy in 2016, says PineBridge Investments PineBridge Investments forecasts 2.7% GDP growth in the United States Eurozone growth projected to slightly improve

PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY

- SUMMARY") PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY PUBLIC FINANCE REVIEW February 2013 SUMMARY Key messages The purpose of our analysis is to highlight the risks that fiscal policy

PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY PUBLIC FINANCE REVIEW February 2013 SUMMARY Key messages The purpose of our analysis is to highlight the risks that fiscal policy

EFN REPORT. ECONOMIC OUTLOOK FOR THE EURO AREA IN 2013 and 2014

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2013 and 2014 Autumn 2013 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2013 and 2014 Autumn 2013 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

Outlook for Economic Activity and Prices

Not to be released until : p.m. Japan Standard Time on Saturday, January 3, 16. January 3, 16 Bank of Japan Outlook for Economic Activity and Prices January 16 (English translation prepared by the Bank's

Not to be released until : p.m. Japan Standard Time on Saturday, January 3, 16. January 3, 16 Bank of Japan Outlook for Economic Activity and Prices January 16 (English translation prepared by the Bank's

IV. Investment dynamics in the euro area since the crisis (40)

") 199Q1 1997Q1 1999Q1 21Q1 23Q1 2Q1 27Q1 29Q1 211Q1 213Q1 IV. Investment dynamics in the euro area since the crisis (4) This section analyses the investment dynamics in the euro area since the global financial

199Q1 1997Q1 1999Q1 21Q1 23Q1 2Q1 27Q1 29Q1 211Q1 213Q1 IV. Investment dynamics in the euro area since the crisis (4) This section analyses the investment dynamics in the euro area since the global financial

2015 Article IV Consultation with Sweden Concluding Statement of the IMF Mission

2015 Article IV Consultation with Sweden Concluding Statement of the IMF Mission Sweden s economy is performing well. But housing prices and household debt are elevated and rising and unemployment is high

2015 Article IV Consultation with Sweden Concluding Statement of the IMF Mission Sweden s economy is performing well. But housing prices and household debt are elevated and rising and unemployment is high

Naturally, these difficult external conditions have affected the Mexican economy. I would stress in particular three developments in this regard:

REMARKS BY MR. JAVIER GUZMÁN CALAFELL, DEPUTY GOVERNOR AT THE BANCO DE MÉXICO, ON THE MEXICAN ECONOMY IN AN ADVERSE EXTERNAL ENVIRONMENT: CHALLENGES AND POLICY RESPONSE, SANTANDER MEXICO DAY 2016, Mexico

REMARKS BY MR. JAVIER GUZMÁN CALAFELL, DEPUTY GOVERNOR AT THE BANCO DE MÉXICO, ON THE MEXICAN ECONOMY IN AN ADVERSE EXTERNAL ENVIRONMENT: CHALLENGES AND POLICY RESPONSE, SANTANDER MEXICO DAY 2016, Mexico

South African Reserve Bank. Statement of the Monetary Policy Committee. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 17 March 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 17 March 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

Final Assessment 1 of Spain's eligibility for an EFSF/ESM loan to recapitalize certain financial institutions

Final Assessment 1 of Spain's eligibility for an EFSF/ESM loan to recapitalize certain financial institutions Background On 25 June 2012, the Spanish Government applied for external financial assistance

Final Assessment 1 of Spain's eligibility for an EFSF/ESM loan to recapitalize certain financial institutions Background On 25 June 2012, the Spanish Government applied for external financial assistance

THE POTENTIAL MACROECONOMIC EFFECT OF DEBT CEILING BRINKMANSHIP

OCTOBER 2013 THE POTENTIAL MACROECONOMIC EFFECT OF DEBT CEILING BRINKMANSHIP Introduction The United States has never defaulted on its obligations, and the U. S. dollar and Treasury securities are at the

OCTOBER 2013 THE POTENTIAL MACROECONOMIC EFFECT OF DEBT CEILING BRINKMANSHIP Introduction The United States has never defaulted on its obligations, and the U. S. dollar and Treasury securities are at the

Statement to Parliamentary Committee

Statement to Parliamentary Committee Opening Remarks by Mr Glenn Stevens, Governor, in testimony to the House of Representatives Standing Committee on Economics, Sydney, 14 August 2009. The Bank s Statement

Statement to Parliamentary Committee Opening Remarks by Mr Glenn Stevens, Governor, in testimony to the House of Representatives Standing Committee on Economics, Sydney, 14 August 2009. The Bank s Statement

Report to the public on the Bank of Israel s discussions prior to deciding on. the interest rate for January 2015

BANK OF ISRAEL Office of the Spokesperson and Economic Information January 12, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on General the interest rate for January 2015

BANK OF ISRAEL Office of the Spokesperson and Economic Information January 12, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on General the interest rate for January 2015

UK Economic Forecast Q3 2014

UK Economic Forecast Q3 2014 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

UK Economic Forecast Q3 2014 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

ANNEX 1 - MACROECONOMIC IMPLICATIONS FOR ITALY OF ACHIEVING COMPLIANCE WITH THE DEBT RULE UNDER TWO DIFFERENT SCENARIOS

ANNEX 1 - MACROECONOMIC IMPLICATIONS FOR ITALY OF ACHIEVING COMPLIANCE WITH THE DEBT RULE UNDER TWO DIFFERENT SCENARIOS The aim of this note is first to illustrate the impact of a fiscal adjustment aimed

ANNEX 1 - MACROECONOMIC IMPLICATIONS FOR ITALY OF ACHIEVING COMPLIANCE WITH THE DEBT RULE UNDER TWO DIFFERENT SCENARIOS The aim of this note is first to illustrate the impact of a fiscal adjustment aimed

IW Monetary Outlook December 2015

IW policy paper 37/2015 Contributions to the political debate by the Cologne Institute for Economic Research IW Monetary Outlook December 2015 Weak Credit Growth Hinders Eurozone Inflation to Increase

IW policy paper 37/2015 Contributions to the political debate by the Cologne Institute for Economic Research IW Monetary Outlook December 2015 Weak Credit Growth Hinders Eurozone Inflation to Increase

Meeting with Analysts

CNB s New Forecast (Inflation Report IV/) Meeting with Analysts Tibor Hlédik Prague, 7 November, Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

CNB s New Forecast (Inflation Report IV/) Meeting with Analysts Tibor Hlédik Prague, 7 November, Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

Global Economic Prospects and Policy Changes

G R O U P O F T W E N T Y MEETIING OF G--20 FIINANCE MIINIISTERS AND CENTRAL BANK GOVERNORS FEBRUARY 25--26,, 2012 MEXIICO CIITY Global Economic Prospects and Policy Changes Prepared by Staff of the International

G R O U P O F T W E N T Y MEETIING OF G--20 FIINANCE MIINIISTERS AND CENTRAL BANK GOVERNORS FEBRUARY 25--26,, 2012 MEXIICO CIITY Global Economic Prospects and Policy Changes Prepared by Staff of the International

EIOPA Risk Dashboard March 2015 Q4 2014 data PUBLIC. EIOPA-FS-15/209 Frankfurt, 20th March 2015

EIOPA Risk Dashboard March 2015 Q4 2014 data PUBLIC EIOPA-FS-15/209 Frankfurt, 20th March 2015 Summary The release of this EIOPA Risk Dashboard is based on 2014- Q4 indicators submitted on a best effort

EIOPA Risk Dashboard March 2015 Q4 2014 data PUBLIC EIOPA-FS-15/209 Frankfurt, 20th March 2015 Summary The release of this EIOPA Risk Dashboard is based on 2014- Q4 indicators submitted on a best effort

6. Economic Outlook. The International Economy. Graph 6.2 Terms of Trade Log scale, 2012/13 average = 100

6. Economic Outlook The International Economy Growth of Australia s major trading partners is expected to be around its long-run average in 015 and 016 (Graph 6.1). Forecasts for 015 have been revised

6. Economic Outlook The International Economy Growth of Australia s major trading partners is expected to be around its long-run average in 015 and 016 (Graph 6.1). Forecasts for 015 have been revised

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Second Meeting October 9-10, 2015 IMFC Statement by Immongault Tatagani Minister of Economy, Investments, Promotion and Prospective, Gabon On behalf

International Monetary and Financial Committee Thirty-Second Meeting October 9-10, 2015 IMFC Statement by Immongault Tatagani Minister of Economy, Investments, Promotion and Prospective, Gabon On behalf

Recent Developments in Economic Activity, Prices, and Monetary Policy

June 23, 2016 Bank of Japan Recent Developments in Economic Activity, Prices, and Monetary Policy Speech at a Meeting with Business Leaders in Ishikawa Takahide Kiuchi Member of the Policy Board (English

June 23, 2016 Bank of Japan Recent Developments in Economic Activity, Prices, and Monetary Policy Speech at a Meeting with Business Leaders in Ishikawa Takahide Kiuchi Member of the Policy Board (English

EFN REPORT. ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016 Spring 2015 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016 Spring 2015 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

2015Q1 INVESTMENT OUTLOOK

TTG WEALTH MANAGEMENT 2015Q1 INVESTMENT OUTLOOK TABLE OF CONTENTS Contents 2015Q1 Core Asset Allocation Summary 1 2015Q1 Satellite Asset Allocation Summary 2 2014 Year-End Review 3 Investment Outlook for

TTG WEALTH MANAGEMENT 2015Q1 INVESTMENT OUTLOOK TABLE OF CONTENTS Contents 2015Q1 Core Asset Allocation Summary 1 2015Q1 Satellite Asset Allocation Summary 2 2014 Year-End Review 3 Investment Outlook for

Analysis of the Impact of High Oil Prices on the Global Economy. International Energy Agency May 2004

Analysis of the Impact of High Oil Prices on the Global Economy International Energy Agency May 2004 SUMMARY Oil prices still matter to the health of the world economy. Higher oil prices since 1999 partly

Analysis of the Impact of High Oil Prices on the Global Economy International Energy Agency May 2004 SUMMARY Oil prices still matter to the health of the world economy. Higher oil prices since 1999 partly

7. Spillovers from Russia to the CCA

7. Spillovers from Russia to the CCA In the face of sharply lower oil prices and geopolitical tensions and sanctions, economic activity in Russia has rapidly decelerated, resulting in negative spillovers

7. Spillovers from Russia to the CCA In the face of sharply lower oil prices and geopolitical tensions and sanctions, economic activity in Russia has rapidly decelerated, resulting in negative spillovers

PROJECTIONS FOR THE PORTUGUESE ECONOMY: 2015-2017. Box 1 Projection assumptions

PROJECTIONS FOR THE PORTUGUESE ECONOMY: 2015-2017 Box 1 Projection assumptions Projections for the Portuguese economy: 2015-2017 7 Projections for the Portuguese economy: 2015-2017 1. Introduction Projections

PROJECTIONS FOR THE PORTUGUESE ECONOMY: 2015-2017 Box 1 Projection assumptions Projections for the Portuguese economy: 2015-2017 7 Projections for the Portuguese economy: 2015-2017 1. Introduction Projections

LEE BUSI N ESS SCHOOL UNITED STATES QUARTERLY ECONOMIC FORECAST. U.S. Economic Growth to Accelerate. Chart 1. Growth Rate of U.S.

CENTER FOR BUSINESS & ECONOMIC RESEARCH LEE BUSI N ESS SCHOOL UNITED STATES QUARTERLY ECONOMIC FORECAST O U.S. Economic Growth to Accelerate ver the past few years, U.S. economic activity has remained

CENTER FOR BUSINESS & ECONOMIC RESEARCH LEE BUSI N ESS SCHOOL UNITED STATES QUARTERLY ECONOMIC FORECAST O U.S. Economic Growth to Accelerate ver the past few years, U.S. economic activity has remained

Insurance market outlook

Munich Re Economic Research 2 May 2013 Global economic recovery provides stimulus to the insurance industry long-term perspective positive as well Once a year, MR Economic Research produces long-term forecasts

Munich Re Economic Research 2 May 2013 Global economic recovery provides stimulus to the insurance industry long-term perspective positive as well Once a year, MR Economic Research produces long-term forecasts

Monetary Policy and the Economy. Goals of Monetary Policy

Monetary Policy and the Economy The Federal Reserve sets the nation's monetary policy to promote the objectives of maximum employment, stable prices, and moderate long-term interest rates. The challenge

Monetary Policy and the Economy The Federal Reserve sets the nation's monetary policy to promote the objectives of maximum employment, stable prices, and moderate long-term interest rates. The challenge

The global economy Banco de Portugal Lisbon, 24 September 2013 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

THE EURO AREA BANK LENDING SURVEY 3RD QUARTER OF 2014

THE EURO AREA BANK LENDING SURVEY 3RD QUARTER OF 214 OCTOBER 214 European Central Bank, 214 Address Kaiserstrasse 29, 6311 Frankfurt am Main, Germany Postal address Postfach 16 3 19, 666 Frankfurt am Main,

THE EURO AREA BANK LENDING SURVEY 3RD QUARTER OF 214 OCTOBER 214 European Central Bank, 214 Address Kaiserstrasse 29, 6311 Frankfurt am Main, Germany Postal address Postfach 16 3 19, 666 Frankfurt am Main,

Monetary Policy Report

Monetary Policy Report February 15 S V E R I G E S R I K S B A N K Correction 15--13 Two figures on page 3 were switched around in the previous version of the report. This meant that references to Figures

Monetary Policy Report February 15 S V E R I G E S R I K S B A N K Correction 15--13 Two figures on page 3 were switched around in the previous version of the report. This meant that references to Figures

South African Reserve Bank. Statement of the Monetary Policy Committee. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank Press Statement Embargo Delivery 21 July 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank The UK vote to

South African Reserve Bank Press Statement Embargo Delivery 21 July 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank The UK vote to

2013 2014e 2015f. www.economics.gov.nl.ca. Real GDP Growth (%)

") The global economy recorded modest growth in 2014. Real GDP rose by 3.4%, however, economic performance varied by country and region (see table). Several regions turned in a lackluster performance. The

The global economy recorded modest growth in 2014. Real GDP rose by 3.4%, however, economic performance varied by country and region (see table). Several regions turned in a lackluster performance. The

Insurance Market Outlook

Munich Re Economic Research May 2014 Premium growth is again slowly gathering momentum After a rather restrained 2013 (according to partly preliminary data), we expect growth in global primary insurance

Munich Re Economic Research May 2014 Premium growth is again slowly gathering momentum After a rather restrained 2013 (according to partly preliminary data), we expect growth in global primary insurance

28.10.2013. The recovery of the Spanish economy XVI Congreso Nacional de la Empresa Familiar/Instituto de la Empresa Familiar Luis M.

28.10.2013 The recovery of the Spanish economy XVI Congreso Nacional de la Empresa Familiar/Instituto de la Empresa Familiar Luis M. Linde Governor Let me begin by thanking you for inviting me to take

28.10.2013 The recovery of the Spanish economy XVI Congreso Nacional de la Empresa Familiar/Instituto de la Empresa Familiar Luis M. Linde Governor Let me begin by thanking you for inviting me to take

Introduction B.2 & B.3 111

Risks and Scenarios Introduction The forecasts presented in the Economic and Tax Outlook chapter incorporate a number of judgements about how both the New Zealand and the world economies evolve. Some judgements

Risks and Scenarios Introduction The forecasts presented in the Economic and Tax Outlook chapter incorporate a number of judgements about how both the New Zealand and the world economies evolve. Some judgements

Section 2 Evaluation of current account balance fluctuations

Section 2 Evaluation of current account balance fluctuations Key points 1. The Japanese economy and IS balance trends From a macroeconomic perspective, the current account balance weighs the Japanese economy

Section 2 Evaluation of current account balance fluctuations Key points 1. The Japanese economy and IS balance trends From a macroeconomic perspective, the current account balance weighs the Japanese economy

Japan s Economic Challenges

Japan s Economic Challenges LUC EVERAERT ASIA PACIFIC DEPARTMENT INTERNATIONAL MONETARY FUND UNIVERSITY OF TOKYO JANUARY 18, 216 1 Global Overview I. Global outlook and risks II. Prospects for Japan III.

Japan s Economic Challenges LUC EVERAERT ASIA PACIFIC DEPARTMENT INTERNATIONAL MONETARY FUND UNIVERSITY OF TOKYO JANUARY 18, 216 1 Global Overview I. Global outlook and risks II. Prospects for Japan III.

Spain Economic Outlook. Rafael Doménech EUI-nomics 2015 Debating the Economic Conditions in the Euro Area and Beyond Firenze, 24th of April, 2015

Spain Economic Outlook Rafael Doménech EUI-nomics 2015 Debating the Economic Conditions in the Euro Area and Beyond Firenze, 24th of April, 2015 The outlook one year ago: the risks were to the upside for

Spain Economic Outlook Rafael Doménech EUI-nomics 2015 Debating the Economic Conditions in the Euro Area and Beyond Firenze, 24th of April, 2015 The outlook one year ago: the risks were to the upside for

44 ECB STOCK MARKET DEVELOPMENTS IN THE LIGHT OF THE CURRENT LOW-YIELD ENVIRONMENT

Box STOCK MARKET DEVELOPMENTS IN THE LIGHT OF THE CURRENT LOW-YIELD ENVIRONMENT Stock market developments are important for the formulation of monetary policy for several reasons. First, changes in stock

Box STOCK MARKET DEVELOPMENTS IN THE LIGHT OF THE CURRENT LOW-YIELD ENVIRONMENT Stock market developments are important for the formulation of monetary policy for several reasons. First, changes in stock

Governor's Statement No. 34 October 9, 2015. Statement by the Hon. BARRY WHITESIDE, Governor of the Bank and the Fund for the REPUBLIC OF FIJI

Governor's Statement No. 34 October 9, 2015 Statement by the Hon. BARRY WHITESIDE, Governor of the Bank and the Fund for the REPUBLIC OF FIJI Statement by the Hon. Mr. Barry Whiteside, Governor of the

Governor's Statement No. 34 October 9, 2015 Statement by the Hon. BARRY WHITESIDE, Governor of the Bank and the Fund for the REPUBLIC OF FIJI Statement by the Hon. Mr. Barry Whiteside, Governor of the

Global Economic Outlook

Global Economic Outlook 3rd Quarter 2014 Offprint Economic Outlook Eurozone Global Economic Outlook 3rd Quarter 2014 Contents United States: A major first-quarter stumble, but future prospects remain undimmed

Global Economic Outlook 3rd Quarter 2014 Offprint Economic Outlook Eurozone Global Economic Outlook 3rd Quarter 2014 Contents United States: A major first-quarter stumble, but future prospects remain undimmed

Impact of Global Financial Crisis on South Asia

Impact of Global Financial Crisis on South Asia February 17, 2009 - The global financial crisis hit South Asia at a time when it had barely recovered from severe terms of trade shock resulting from the

Impact of Global Financial Crisis on South Asia February 17, 2009 - The global financial crisis hit South Asia at a time when it had barely recovered from severe terms of trade shock resulting from the

The U.S. Outlook and Monetary Policy. Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City

The U.S. Outlook and Monetary Policy Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City February 2, 2016 Central Exchange Kansas City, Mo. The views expressed by

The U.S. Outlook and Monetary Policy Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City February 2, 2016 Central Exchange Kansas City, Mo. The views expressed by

THE RETURN OF CAPITAL EXPENDITURE OR CAPEX CYCLE IN MALAYSIA

PUBLIC BANK BERHAD ECONOMICS DIVISION MENARA PUBLIC BANK 146 JALAN AMPANG 50450 KUALA LUMPUR TEL : 03 2176 6000/666 FAX : 03 2163 9929 Public Bank Economic Review is published bi monthly by Economics Division,

PUBLIC BANK BERHAD ECONOMICS DIVISION MENARA PUBLIC BANK 146 JALAN AMPANG 50450 KUALA LUMPUR TEL : 03 2176 6000/666 FAX : 03 2163 9929 Public Bank Economic Review is published bi monthly by Economics Division,

Reducing public debt: Turkey

Reducing public debt: Turkey Abstract Turkey halved the ratio of public debt to GDP from almost 80 percent in 2001 to less than 40 percent before the global crisis of 2009. Several factors helped. First,

Reducing public debt: Turkey Abstract Turkey halved the ratio of public debt to GDP from almost 80 percent in 2001 to less than 40 percent before the global crisis of 2009. Several factors helped. First,

How To Get A Better Deal On A Euro Bond

21 st ASSIOM FOREX Congress Speech by the Governor of the Bank of Italy Ignazio Visco Milan, 7 February 2015 The positive signs emerging from the global economy are still accompanied by marked uncertainty.

21 st ASSIOM FOREX Congress Speech by the Governor of the Bank of Italy Ignazio Visco Milan, 7 February 2015 The positive signs emerging from the global economy are still accompanied by marked uncertainty.

Czech Economic Outlook and Prospects for the Exchange Rate Floor

Czech Economic Outlook and Prospects for the Exchange Rate Floor Vladimir Tomsik Vice-Governor Czech National Bank Small Talks Symposium 9 October 2015 Investor Seminar 10 October 2015 IMF/WB Annual Meeting

Czech Economic Outlook and Prospects for the Exchange Rate Floor Vladimir Tomsik Vice-Governor Czech National Bank Small Talks Symposium 9 October 2015 Investor Seminar 10 October 2015 IMF/WB Annual Meeting

ARC Assigns BBB Rating to Italy

ARC Assigns BBB Rating to Italy ISSUER RATINGS DATE Republic of Italy August 28, 2015 ISSUER RATINGS - FOREIGN CURRENCY Medium and Long Term BBB (BBB, Stable) ISSUER RATINGS - LOCAL CURRENCY Medium and

ARC Assigns BBB Rating to Italy ISSUER RATINGS DATE Republic of Italy August 28, 2015 ISSUER RATINGS - FOREIGN CURRENCY Medium and Long Term BBB (BBB, Stable) ISSUER RATINGS - LOCAL CURRENCY Medium and

October 2015. PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy October 2015 Market Volatility likely to Remain Elevated on China Growth Concerns & Fed Rate Uncertainty. Stocks

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy October 2015 Market Volatility likely to Remain Elevated on China Growth Concerns & Fed Rate Uncertainty. Stocks

Why Treasury Yields Are Projected to Remain Low in 2015 March 2015

Why Treasury Yields Are Projected to Remain Low in 5 March 5 PERSPECTIVES Key Insights Monica Defend Head of Global Asset Allocation Research Gabriele Oriolo Analyst Global Asset Allocation Research While

Why Treasury Yields Are Projected to Remain Low in 5 March 5 PERSPECTIVES Key Insights Monica Defend Head of Global Asset Allocation Research Gabriele Oriolo Analyst Global Asset Allocation Research While

An outlook on the Spanish economy Official Monetary and Financial Institutions Forum (OMFIF), London

, London") 09.02.2016 An outlook on the Spanish economy Official Monetary and Financial Institutions Forum (OMFIF), London Luis M. Linde Governor I would like to thank OMFIF and Mr. David Marsh for the invitation

09.02.2016 An outlook on the Spanish economy Official Monetary and Financial Institutions Forum (OMFIF), London Luis M. Linde Governor I would like to thank OMFIF and Mr. David Marsh for the invitation

Financial Stability Report 2015/2016

Financial Stability Report 2015/2016 Press Conference Presentation Miroslav Singer Governor Prague, 14 June 2016 Structure of presentation I. Overall assessment of risks and setting of countercyclical

Financial Stability Report 2015/2016 Press Conference Presentation Miroslav Singer Governor Prague, 14 June 2016 Structure of presentation I. Overall assessment of risks and setting of countercyclical

2013 global equity outlook: Searching for alpha in a stock picker s market

March 2013 2013 global equity outlook: Searching for alpha in a stock picker s market Saira Malik, Head of Global Equity Research, TIAA-CREF Executive summary The outlook for equity markets is favorable

March 2013 2013 global equity outlook: Searching for alpha in a stock picker s market Saira Malik, Head of Global Equity Research, TIAA-CREF Executive summary The outlook for equity markets is favorable

Decomposition of External Capital Inflows and Outflows in the Small Open Transition Economy (The Case Analysis of the Slovak Republic)

") PANOECONOMICUS, 2008, 2, str. 219-231 UDC 330.342(437.6) ORIGINAL SCIENTIFIC PAPER Decomposition of External Capital Inflows and Outflows in the Small Open Transition Economy (The Case Analysis of the

PANOECONOMICUS, 2008, 2, str. 219-231 UDC 330.342(437.6) ORIGINAL SCIENTIFIC PAPER Decomposition of External Capital Inflows and Outflows in the Small Open Transition Economy (The Case Analysis of the

World Economic Situation Prospects

World Economic Situation Prospects and 2016 United Nations World Economic Situation and Prospects 2016 asdf United Nations New York, 2016 vi World Economic Situation and Prospects 2016 Executive summary

World Economic Situation Prospects and 2016 United Nations World Economic Situation and Prospects 2016 asdf United Nations New York, 2016 vi World Economic Situation and Prospects 2016 Executive summary

Outlook for Economic Activity and Prices

Not to be released until : p.m. Japan Standard Time on Saturday, April 7, 13. April 7, 13 Bank of Japan Outlook for Economic Activity and Prices April 13 (English translation prepared by the Bank's staff

Not to be released until : p.m. Japan Standard Time on Saturday, April 7, 13. April 7, 13 Bank of Japan Outlook for Economic Activity and Prices April 13 (English translation prepared by the Bank's staff

UK Economic Forecast Q1 2015

UK Economic Forecast Q1 2015 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

UK Economic Forecast Q1 2015 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

5 Comparison with the Previous Convergence Programme and Sensitivity Analysis

5 Comparison with the Previous Convergence Programme and Sensitivity Analysis 5.1 Comparison with the Previous Macroeconomic Scenario The differences between the macroeconomic scenarios of the current

5 Comparison with the Previous Convergence Programme and Sensitivity Analysis 5.1 Comparison with the Previous Macroeconomic Scenario The differences between the macroeconomic scenarios of the current

Glenn Stevens: The path to prosperity

Glenn Stevens: The path to prosperity Address by Mr Glenn Stevens, Governor of the Reserve Bank of Australia, at the 2015 Economic and Social Outlook Conference, organized by The Melbourne Institute and

Glenn Stevens: The path to prosperity Address by Mr Glenn Stevens, Governor of the Reserve Bank of Australia, at the 2015 Economic and Social Outlook Conference, organized by The Melbourne Institute and

Switzerland 2013 Article for Consultation Preliminary Conclusions Bern, March 18, 2013

Switzerland 2013 Article for Consultation Preliminary Conclusions Bern, March 18, 2013 With the exchange rate floor in place for over a year, the Swiss economy remains stable, though inflation remains

Switzerland 2013 Article for Consultation Preliminary Conclusions Bern, March 18, 2013 With the exchange rate floor in place for over a year, the Swiss economy remains stable, though inflation remains

2. The European insurance sector 1

2. The European insurance sector 1 As discussed in Chapter 1, the economic conditions in European countries are still fragile, despite some improvements in the first half of 2013. 2.1. Market growth The

2. The European insurance sector 1 As discussed in Chapter 1, the economic conditions in European countries are still fragile, despite some improvements in the first half of 2013. 2.1. Market growth The

The Global Economic Impacts of Oil Price Shocks

The Global Economic Impacts of Oil Price Shocks Presented to: Project LINK, United Nations New York, NY November 22, 2004 Presented by: Sara Johnson Managing Director, Global Macroeconomics Group 781-301-9115

The Global Economic Impacts of Oil Price Shocks Presented to: Project LINK, United Nations New York, NY November 22, 2004 Presented by: Sara Johnson Managing Director, Global Macroeconomics Group 781-301-9115

Figure C Supervisory risk assessment for insurance and pension funds expected future development

5. Risk assessment This chapter aims to asses those risks which were identified in the first chapter and further elaborated in the next parts on insurance, reinsurance and occupational pensions. 5.1. Qualitative

5. Risk assessment This chapter aims to asses those risks which were identified in the first chapter and further elaborated in the next parts on insurance, reinsurance and occupational pensions. 5.1. Qualitative

Highlights from the OECD Sovereign Borrowing Outlook N 4 *