Advantages and Disadvantages of Using Credit

|

|

|

- Luke Allen

- 8 years ago

- Views:

Transcription

1 1 Lesson 7: About Credit Why Get Credit? To establish a credit history. Advantages and Disadvantages of Using Credit 1. Advantages Able to buy needed items now. Don t have to carry cash. Creates a record of purchases. More convenient than writing checks. Consolidates bills into one payment. 2. Disadvantages Interest (higher cost of items). Credit cards can be lost or stolen. May require additional fees.

.")

2 2 Financial difficulties may arise if one loses track of how much has been spent each month. Increased impulse buying may occur. Why Banks Issue Credit To offer service to customers To make money. The Three C s of Credit 1. Character will you repay the debt? From your credit history, does it look like you possess the honesty and reliability to pay credit debts? Have you used credit before? Do you pay your bills on time? Do you have a good credit report? Can you provide character references? How long have you lived at your present address? How long have you been at your present job?

3 3 2. Capital what if you don t repay the debt? Do you have any valuable assets such as real estate, savings, or investments that could be used to repay credit debts if income is unavailable? What property do you own that can secure the loan? Do you have a savings account? Do you have investments to use as collateral? 3. Capacity can you repay the debt? Have you been working regularly in an occupation that is likely to provide enough income to support your credit use? Do you have a steady job? What is your salary? How many other loan payments do you have? What are your current living expenses? What are your current debts? How many dependents do you have?

4 4 Your Responsibilities Borrow only what you can repay. Read and understand the credit contract. Not to exceed the credit limit established by your creditor. Pay debts promptly. Notify creditor if you cannot meet payments. Report lost or stolen credit cards promptly. Never give your credit card number over the phone unless you initiated the call or are certain of the caller s identity. Your Rights 1. Truth In Lending Act (1968) Ensures consumers are fully informed about cost and conditions of borrowing. 2. Fair Credit Reporting Act (1970) Protects the privacy and accuracy of information in a credit check.

5 5 3. Equal Opportunity Act (1974) Prohibits discrimination in giving credit on the basis of sex, race, color, religion, national origin, marital status, age, or receipt of public assistance. 4. Fair Credit Billing Act (1974) Sets up a procedure for the quick correction of mistakes that appear on consumer credit accounts. 5. Fair Debt Collection Practices Act (1977) Prevents abuse by professional debt collectors, and applies to anyone employed to collect debts owed to others; does not apply to banks or other businesses collecting their own accounts. Building a Credit History Establish a steady work record. Pay all bills promptly (examples: rent, phone, electricity, etc.). Open a checking account and don t bounce checks. Open a savings account and make regular deposits.

.")

6 6 Apply for a local store credit card and make regular monthly payments. Use a layaway plan. Apply for a small loan using your savings account or a certificate of deposit (CD) as collateral. Get a co-signer on a loan and pay back the loan as agreed.

as collateral.")

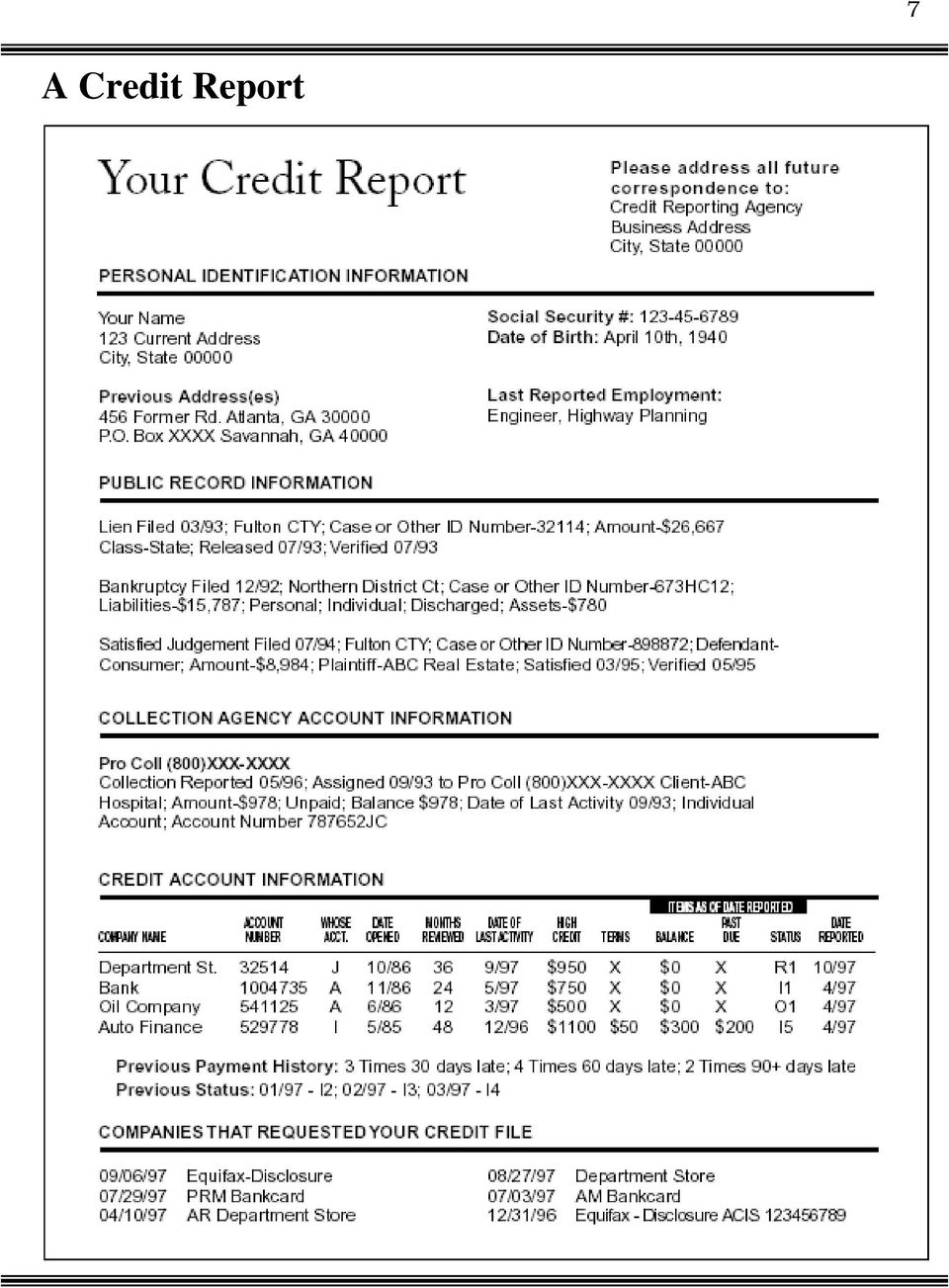

7 A Credit Report 7

8 8 Manner of Payment Codes Status O R I Type of account code Open (entire balance due each month) Revolving (payment amount variable) Installment (fixed number of payments) Status Timeliness of payment 0 Approved not used; too new to rate 1 Paid as agree days past due days past due days past due 5 Pays or paid 120+ days past the due date; or collection account 6 Making regular payments under wage earner plan or similar arrangement 7 Repossession 8 Charged off to bad debt

9 9 Types and Sources of Credit 1. Single-Payment Credit Items and services are paid for in a single payment, within a given time period, after the purchase. Interest is usually not charged. Utility companies, medical services Some retail businesses 2. Installment Credit Merchandise and services are paid for in two or more regularly scheduled payments of a set amount. Interest is included. Some retail businesses, such as car and appliance dealers Money may also be loaned for a special purpose, with the consumer agreeing to repay the debt in two or more regularly scheduled payments. Commercial banks Consumer finance companies Savings and loans Credit unions

10 10 3. Revolving Credit Many items can be bought using this plan as long as the total amount does not go over the credit user s assigned dollar limit. Repayment is made at regular time intervals for any amount at or above the minimum required amount. Interest is charged on the remaining balance. Retail stores (Macy s, Sears, Kohl s) Financial institutions that issue credit cards (VISA, Mastercard, American Express, Discover) How Much Can You Afford? (the rule) Never borrow more than 20% of your yearly net income. If you earn $400 a month after taxes, then your net income in one year is: 12 x $400 = $4,800 Calculate 20% of your annual net income to find your safe debt load. $4,800 x 20% = $960 So, you should never have more than $960 of debt outstanding. NOTE: Housing debt (i.e., mortgage payments) should not be counted as part of the 20%.

Never borrow more than 20% of your yearly net income.")

11 11 Monthly payments shouldn t exceed 10% of your monthly net income. If your take-home pay is $400 a month: $400 x 10% = $40 So, your total monthly debt payments shouldn t total more than $40 per month.

Presentation Slides. Lesson Seven. Credit 04/09

Presentation Slides $ Lesson Seven Credit 04/09 advantages and disadvantages of using credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient

Presentation Slides $ Lesson Seven Credit 04/09 advantages and disadvantages of using credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient

lesson seven about credit overheads

lesson seven about credit overheads advantages and disadvantages of using credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing

lesson seven about credit overheads advantages and disadvantages of using credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing

lesson seven about credit overheads

lesson seven about credit overheads advantages and disadvantages of using credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing

lesson seven about credit overheads advantages and disadvantages of using credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing

About Credit. Financial Literacy

About Credit Financial Literacy What is Credit? Credit is the ability to borrow money with a promise of future payment. Why borrow? Goals - car, appliances, furniture, etc Home Education Health Plan your

About Credit Financial Literacy What is Credit? Credit is the ability to borrow money with a promise of future payment. Why borrow? Goals - car, appliances, furniture, etc Home Education Health Plan your

The West Virginia State Treasurer s Office. A free publication provided by

CREDIT CARDS A free publication provided by The West Virginia State Treasurer s Office Visit www.wvtreasury.com or Call 1.800.422.7498 From the Office of West Virginia State Treasurer, John D. Perdue CREDIT

CREDIT CARDS A free publication provided by The West Virginia State Treasurer s Office Visit www.wvtreasury.com or Call 1.800.422.7498 From the Office of West Virginia State Treasurer, John D. Perdue CREDIT

Credit Cards: What You Need to Know

ALL ABOUT CREDIT A free publication provided by Consolidated Credit Counseling Services of Canada, Inc., a registered charitable credit counselling and debt management organization. Consolidated Credit

ALL ABOUT CREDIT A free publication provided by Consolidated Credit Counseling Services of Canada, Inc., a registered charitable credit counselling and debt management organization. Consolidated Credit

Teacher's Guide. Lesson Seven. Credit 04/09

Teacher's Guide $ Lesson Seven Credit 04/09 credit websites Consumers may use credit frequently, but many struggle to manage it wisely. To optimize credit and make sound financial decisions, students need

Teacher's Guide $ Lesson Seven Credit 04/09 credit websites Consumers may use credit frequently, but many struggle to manage it wisely. To optimize credit and make sound financial decisions, students need

Lesson 8: Credit Cards Types of Credit Card Accounts

1 Lesson 8: Credit Cards Types of Credit Card Accounts 1. Bank Card Examples: Visa, MasterCard, Discover, American Express Revolving Credit can pay all or some of the bill with the remaining balance put

1 Lesson 8: Credit Cards Types of Credit Card Accounts 1. Bank Card Examples: Visa, MasterCard, Discover, American Express Revolving Credit can pay all or some of the bill with the remaining balance put

Personal Finance Lessons: About Credit What Do You Know About Credit? PowerPoint Discussion Notes

Personal Finance Lessons: About Credit What Do You Know About Credit? PowerPoint Discussion Notes Slide 1 WHAT DO YOU KNOW ABOUT CREDIT? Debt is the worst poverty. Thomas Fuller None for this slide Slide

Personal Finance Lessons: About Credit What Do You Know About Credit? PowerPoint Discussion Notes Slide 1 WHAT DO YOU KNOW ABOUT CREDIT? Debt is the worst poverty. Thomas Fuller None for this slide Slide

Credit Workshop. What I need to know about credit and lending products of financial institutions. Financial Education Supported by:

Credit Workshop What I need to know about credit and lending products of financial institutions. Financial Education Supported by: Concept Checklist What will I learn today? [ ] What is Credit? [ ] Advantages/

Credit Workshop What I need to know about credit and lending products of financial institutions. Financial Education Supported by: Concept Checklist What will I learn today? [ ] What is Credit? [ ] Advantages/

Use and Misuse of Credit. Chapter 6. Advantages of Credit. What is Consumer Credit?

Chapter 6 Use and Misuse of Credit Introduction to Consumer Credit Before you use credit for a major purchase, ask yourself some questions. Do I have the cash for the down payment? Do I want to use my

Chapter 6 Use and Misuse of Credit Introduction to Consumer Credit Before you use credit for a major purchase, ask yourself some questions. Do I have the cash for the down payment? Do I want to use my

Understanding Credit

Teacher's Guide $ Lesson Seven Understanding Credit 01/11 understanding credit websites websites for understanding credit The internet is probably the most extensive and dynamic source of information in

Teacher's Guide $ Lesson Seven Understanding Credit 01/11 understanding credit websites websites for understanding credit The internet is probably the most extensive and dynamic source of information in

Credit arrangements can be formal or informal. The three most common types of credit used by consumers are described below.

1-888-842-6328 For toll-free numbers when overseas, visit Collect internationally 1-703-255-8837 TDD for hearing impaired 1-888-869-5863 Credit Wise Credit: a Useful Tool Most of us use consumer credit

1-888-842-6328 For toll-free numbers when overseas, visit Collect internationally 1-703-255-8837 TDD for hearing impaired 1-888-869-5863 Credit Wise Credit: a Useful Tool Most of us use consumer credit

Using Credit to Your Advantage Credit Cards and Loans Participant Guide

Hands on Banking Using Credit to Your Advantage The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the program anytime at www.handsonbanking.org & www.elfuturoentusmanos.org

Hands on Banking Using Credit to Your Advantage The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the program anytime at www.handsonbanking.org & www.elfuturoentusmanos.org

How To Cut The Cost of Credit

Published by the NATIONAL ASSOCIATION OF CONSUMER CREDIT ADMINISTRATORS May be reproduced with appropriate credit. For more information, contact: [ ] How To Cut The Cost of Credit Distributed by: Missouri

Published by the NATIONAL ASSOCIATION OF CONSUMER CREDIT ADMINISTRATORS May be reproduced with appropriate credit. For more information, contact: [ ] How To Cut The Cost of Credit Distributed by: Missouri

Personal Loans 101: Understanding

Personal Loans 101: Understanding Small Dollar Loans If you are looking for a small loan, you may not be sure where to turn. Most banks and credit unions do not lend small amounts of money. Payday loans

Personal Loans 101: Understanding Small Dollar Loans If you are looking for a small loan, you may not be sure where to turn. Most banks and credit unions do not lend small amounts of money. Payday loans

Chapter 06. What is Consumer Credit? Chapter 6 Learning Objectives. Introduction to Consumer Credit

Chapter 06 Introduction to Consumer Credit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 6-1 Chapter 6 Learning Objectives 1. Define consumer credit and analyze

Chapter 06 Introduction to Consumer Credit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 6-1 Chapter 6 Learning Objectives 1. Define consumer credit and analyze

LINX EDUCATIONAL INSTRUCTOR S GUIDE

EXTRA CREDIT: UNDERSTANDING THE DO S & DON TS OF USING CREDIT TAKING CHARGE OF CREDIT: 10 TIPS TO CREDIT DISCIPLINE Use the following suggestions as guidelines to self-discipline to keep your credit in

EXTRA CREDIT: UNDERSTANDING THE DO S & DON TS OF USING CREDIT TAKING CHARGE OF CREDIT: 10 TIPS TO CREDIT DISCIPLINE Use the following suggestions as guidelines to self-discipline to keep your credit in

Understanding Credit Reports

Understanding Credit Reports What is a Credit Report and Score? Your success in managing credit is reflected in your credit report and score. A credit report is a history of everything you are doing with

Understanding Credit Reports What is a Credit Report and Score? Your success in managing credit is reflected in your credit report and score. A credit report is a history of everything you are doing with

Lending 101 The Basics

Lending 101 The Basics Overview Loan categories Credit types Different loan types Interest rate Applying for a loan Credit & credit reports Simple loan tips Test Loan Categories Secured loan - a loan that

Lending 101 The Basics Overview Loan categories Credit types Different loan types Interest rate Applying for a loan Credit & credit reports Simple loan tips Test Loan Categories Secured loan - a loan that

Using Credit to Your Advantage

Hands on Banking Using Credit to Your Advantage Credit Reports, Credit Scores and Dealing with Debt The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the

Hands on Banking Using Credit to Your Advantage Credit Reports, Credit Scores and Dealing with Debt The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the

How to Establish, Use, and Protect Your Credit

How to Establish, Use, and Protect Your Credit How to Establish, Use, and Protect Your Credit What you need to know Good credit is valuable. Having the ability to borrow funds allows us to buy things we

How to Establish, Use, and Protect Your Credit How to Establish, Use, and Protect Your Credit What you need to know Good credit is valuable. Having the ability to borrow funds allows us to buy things we

Understanding Vehicle Financing

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Federal Reserve Bank of Philadelphia

Federal Reserve Bank of Philadelphia 1 Credit is a valuable commodity. Having the ability to borrow funds enables us to obtain things we would otherwise have to save years to afford: homes, cars, a college

Federal Reserve Bank of Philadelphia 1 Credit is a valuable commodity. Having the ability to borrow funds enables us to obtain things we would otherwise have to save years to afford: homes, cars, a college

Don t Become a Victim

Don t Become a Victim Life Smarts: 1. Determine the federal laws that assist consumers from becoming victims of predatory lending. What is predatory lending? Predatory lending is the unfair, deceptive,

Don t Become a Victim Life Smarts: 1. Determine the federal laws that assist consumers from becoming victims of predatory lending. What is predatory lending? Predatory lending is the unfair, deceptive,

Familiarize yourself with laws that authorize and regulate vehicle dealership financing and leasing.

W ith prices averaging more than $28,000 for a new vehicle and $15,000 for a used vehicle, most consumers need financing or leasing to acquire a vehicle. In some cases, buyers use direct lending: they

W ith prices averaging more than $28,000 for a new vehicle and $15,000 for a used vehicle, most consumers need financing or leasing to acquire a vehicle. In some cases, buyers use direct lending: they

Financial Literacy. Credit is widely misunderstood and, perhaps even more to the point, widely misused. - Author Unknown. Section V.

Credit is widely misunderstood and, perhaps even more to the point, widely misused. - Author Unknown Section V Credit 113 Credit: Friend or Foe? Families today do not spend much time together talking about

Credit is widely misunderstood and, perhaps even more to the point, widely misused. - Author Unknown Section V Credit 113 Credit: Friend or Foe? Families today do not spend much time together talking about

Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money.

TEACHER GUIDE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Priority Academic Student Skills

TEACHER GUIDE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Priority Academic Student Skills

CreditShop Financial Educa3on Program July 2015

CreditShop Financial Educa3on Program July 2015 What is a Personal Installment Loan? A personal installment loan is a one 3me loan where the principal loan amount plus interest are repaid in equal payments

CreditShop Financial Educa3on Program July 2015 What is a Personal Installment Loan? A personal installment loan is a one 3me loan where the principal loan amount plus interest are repaid in equal payments

lesson seven understanding credit teacher s guide

lesson seven understanding credit teacher s guide understanding credit web sites web sites for consumer credit The Internet is probably the most extensive and dynamic source of information in our society.

lesson seven understanding credit teacher s guide understanding credit web sites web sites for consumer credit The Internet is probably the most extensive and dynamic source of information in our society.

Chapter Objectives. Chapter 6. Short Term Credit Management. Major Topics. Reasons for Using Credit. How to Get Credit. Disadvantages of Using Credit

Chapter Objectives Chapter 6. Short Term Credit Management To evaluate reasons for and against using credit and decide whether or not credit is appropriate for you. To be able to take the necessary steps

Chapter Objectives Chapter 6. Short Term Credit Management To evaluate reasons for and against using credit and decide whether or not credit is appropriate for you. To be able to take the necessary steps

Loan Lessons. The Low-Down on Loans, Interest and Keeping Your Head Above Water. Course Objectives Learn About:

Loan Lessons Course Objectives Learn About: Different Types of Loans How to Qualify for a Loan Different Types of Interest The Low-Down on Loans, Interest and Keeping Your Head Above Water usbank.com/financialeducation

Loan Lessons Course Objectives Learn About: Different Types of Loans How to Qualify for a Loan Different Types of Interest The Low-Down on Loans, Interest and Keeping Your Head Above Water usbank.com/financialeducation

03.04. Overview. Goal. Time Frame. We become what we behold. We shape our tools and then our tools shape us. Marshall McLuhan

Section 03 Unit 04 Banking Services Credit Cards 03.04. We become what we behold. We shape our tools and then our tools shape us. Marshall McLuhan Overview A credit card can be a useful financial tool.

Section 03 Unit 04 Banking Services Credit Cards 03.04. We become what we behold. We shape our tools and then our tools shape us. Marshall McLuhan Overview A credit card can be a useful financial tool.

Loan Lessons. The Low-Down on Loans, Interest and Keeping Your Head Above Water. Course Objectives Learn About:

usbank.com/student financialgenius.usbank.com Course Objectives Learn About: Different Types of Loans How to Qualify for a Loan Different Types of Interest Loan Lessons The Low-Down on Loans, Interest

usbank.com/student financialgenius.usbank.com Course Objectives Learn About: Different Types of Loans How to Qualify for a Loan Different Types of Interest Loan Lessons The Low-Down on Loans, Interest

Personal Loans 101: Understanding Personal Loans

Personal Loans 101: Understanding Personal Loans When it comes to borrowing money, consumers have a variety of choices, ranging from credit cards to home equity loans. Personal loans are used for various

Personal Loans 101: Understanding Personal Loans When it comes to borrowing money, consumers have a variety of choices, ranging from credit cards to home equity loans. Personal loans are used for various

Consumer and Community Affairs. Consumer Protection

Consumer and Community Affairs The number of federal laws intended to protect consumers in credit and other financial transactions has been growing since the late 1960s. Congress has assigned to the Federal

Consumer and Community Affairs The number of federal laws intended to protect consumers in credit and other financial transactions has been growing since the late 1960s. Congress has assigned to the Federal

Buying with credit lets you purchase something and use it while you are still paying for it.

8) Credit Buying with credit lets you purchase something and use it while you are still paying for it. There are two common types of credit: Credit Cards Offered by credit card companies, department stores

8) Credit Buying with credit lets you purchase something and use it while you are still paying for it. There are two common types of credit: Credit Cards Offered by credit card companies, department stores

Lesson 11 Take Control of Debt: Are You Credit Worthy? Check Your Credit Report

Lesson 11 Take Control of Debt: Are You Credit Worthy? Check Your Credit Report Lesson Description Students take on the role of lender in the introduction to this lesson as they consider the information

Lesson 11 Take Control of Debt: Are You Credit Worthy? Check Your Credit Report Lesson Description Students take on the role of lender in the introduction to this lesson as they consider the information

Using Credit Wisely LESSON 14: TEACHERS GUIDE

Using Credit Wisely LESSON 14: TEACHERS GUIDE As teens prepare to enter the financial world, there are many elements for them to consider when it comes to credit. Whether they are off to college in a few

Using Credit Wisely LESSON 14: TEACHERS GUIDE As teens prepare to enter the financial world, there are many elements for them to consider when it comes to credit. Whether they are off to college in a few

If you have not established credit, several options can help you obtain a credit card:

Credit Cards The Basics. Do you understand what credit is and how to use it wisely? Like many of today's teenagers and college students, you appreciate the convenience and relative safety of credit cards.

Credit Cards The Basics. Do you understand what credit is and how to use it wisely? Like many of today's teenagers and college students, you appreciate the convenience and relative safety of credit cards.

Understanding Credit. Megan Stearns, Credit Counselor

Understanding Credit Megan Stearns, Credit Counselor Obtaining your free credit report will lower your credit score. Closing old accounts can help your credit score. Paying off the balances on your credit

Understanding Credit Megan Stearns, Credit Counselor Obtaining your free credit report will lower your credit score. Closing old accounts can help your credit score. Paying off the balances on your credit

Responsibilities of Credit. Chapter 18

Responsibilities of Credit Chapter 18 Responsibilities of Consumer Credit To Yourself To Your Creditors Creditors to You Loan Offer I (Mr. Vesper) will loan you $100.00 today if you agree to pay me $105.00

Responsibilities of Credit Chapter 18 Responsibilities of Consumer Credit To Yourself To Your Creditors Creditors to You Loan Offer I (Mr. Vesper) will loan you $100.00 today if you agree to pay me $105.00

Money Management How to Manage Credit

FCS5-103 Money Management How to Manage Credit Credit is a service that lets you buy now and pay later. You use someone else s money to buy something you want to use now. Credit means using your money

FCS5-103 Money Management How to Manage Credit Credit is a service that lets you buy now and pay later. You use someone else s money to buy something you want to use now. Credit means using your money

Loan. Application. Money Smarts for Kids. Money Skills for Life. Member FDIC. What to Know About Loans. Completing a Loan Application

Loan Application What to Know About Loans What do I need to know about applying for a loan? A loan is used to help you pay for something that you want to buy, like a car, college tuition, school trip or

Loan Application What to Know About Loans What do I need to know about applying for a loan? A loan is used to help you pay for something that you want to buy, like a car, college tuition, school trip or

LEGAL BRIEF RESOLVING CREDIT PROBLEMS March 2014

LEGAL BRIEF RESOLVING CREDIT PROBLEMS March 2014 PREPARED BY NELLIS LAW CENTER, 4428 England Ave (Bldg 18), Nellis AFB, Nevada 89191-6505 702-652-5407, Appt. Line 702-652-7531 If the problems you are experiencing

LEGAL BRIEF RESOLVING CREDIT PROBLEMS March 2014 PREPARED BY NELLIS LAW CENTER, 4428 England Ave (Bldg 18), Nellis AFB, Nevada 89191-6505 702-652-5407, Appt. Line 702-652-7531 If the problems you are experiencing

Presentation Slides. Lesson Eight. Credit Cards 04/09

Presentation Slides $ Lesson Eight Credit Cards 04/09 applying for a credit card costs: Annual Percentage Rate (APR) Grace period Annual fees Transaction fees Balancing computation method for the finance

Presentation Slides $ Lesson Eight Credit Cards 04/09 applying for a credit card costs: Annual Percentage Rate (APR) Grace period Annual fees Transaction fees Balancing computation method for the finance

Coping with a Money Crunch Dealing with Creditors

Chapter 4: After the Disaster Coping with a Money Crunch Dealing with Creditors Outstanding bills and no money to pay creditors can be very frightening. Unemployment, death, illness, divorce or accident

Chapter 4: After the Disaster Coping with a Money Crunch Dealing with Creditors Outstanding bills and no money to pay creditors can be very frightening. Unemployment, death, illness, divorce or accident

3. How to Use Credit

3. How to Use Credit Building a Better Future 103 104 Building a Better Future UNIT 3: HOW TO USE CREDIT Lesson 1: What is Credit? Lesson Objectives: Students will understand why credit is important Students

3. How to Use Credit Building a Better Future 103 104 Building a Better Future UNIT 3: HOW TO USE CREDIT Lesson 1: What is Credit? Lesson Objectives: Students will understand why credit is important Students

Mortgage Loans. Understand the Terms of Your Loan before You Sign. Mortgage Loans. Standard Home Equity Loans or Second Mortgages

Mortgage Loans Understand the Terms of Your Loan before You Sign This brochure can help you determine what is best for your situation, become familiar with mortgage loan terms, and learn what is involved

Mortgage Loans Understand the Terms of Your Loan before You Sign This brochure can help you determine what is best for your situation, become familiar with mortgage loan terms, and learn what is involved

Money Management Questions & Answers about Credit & Debt

FCS5-105 Money Management Questions & Answers about Credit & Debt Questions that you might have about credit include: Can I afford more debt? When can I afford more debt? Should I consolidate my loan?

FCS5-105 Money Management Questions & Answers about Credit & Debt Questions that you might have about credit include: Can I afford more debt? When can I afford more debt? Should I consolidate my loan?

Teacher's Guide. Lesson Eight. Credit Cards 04/09

Teacher's Guide $ Lesson Eight Credit Cards 04/09 credit cards websites Before students use credit cards, it's important that they familiarize themselves with: the advantages and disadvantages of credit

Teacher's Guide $ Lesson Eight Credit Cards 04/09 credit cards websites Before students use credit cards, it's important that they familiarize themselves with: the advantages and disadvantages of credit

CREDIT CARDS: WHAT YOU NEED TO KNOW

CREDIT CARDS: WHAT YOU NEED TO KNOW A free publication provided by Consolidated Counseling Services, Inc. A nonprofit educational credit counseling and debt management organization. Consolidated Credit

CREDIT CARDS: WHAT YOU NEED TO KNOW A free publication provided by Consolidated Counseling Services, Inc. A nonprofit educational credit counseling and debt management organization. Consolidated Credit

NORTH & EAST LUBBOCK CDC

NORTH & EAST LUBBOCK CDC FINANCIAL LITERACY TRAINING UNIT 3 UNIT 3 UNDERSTANDING CREDIT Instructor: Reggie Dial, NELCDC Program Manager & HUD-Certified Housing Counselor AGENDA Your credit rating Credit

NORTH & EAST LUBBOCK CDC FINANCIAL LITERACY TRAINING UNIT 3 UNIT 3 UNDERSTANDING CREDIT Instructor: Reggie Dial, NELCDC Program Manager & HUD-Certified Housing Counselor AGENDA Your credit rating Credit

BUSINESS LOAN APPLICATION

BUSINESS LOAN APPLICATION Each owner, shareholder, partner or member owning 20 cent or more interest in the business must sign a sonal guaranty. A minimum of 1 guarantor is required regardless of cent

BUSINESS LOAN APPLICATION Each owner, shareholder, partner or member owning 20 cent or more interest in the business must sign a sonal guaranty. A minimum of 1 guarantor is required regardless of cent

Using Credit to Your Advantage.

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

SOME IDEAS THAT MAY HELP WITH. Understanding and Using Credit

66291 1098 9/9/04 2:58 PM Page 1 SOME IDEAS THAT MAY HELP WITH Understanding and Using Credit 66291 1098 9/9/04 2:58 PM Page 2 Table of Contents What is consumer credit? 1 Should you use credit? 2 The

66291 1098 9/9/04 2:58 PM Page 1 SOME IDEAS THAT MAY HELP WITH Understanding and Using Credit 66291 1098 9/9/04 2:58 PM Page 2 Table of Contents What is consumer credit? 1 Should you use credit? 2 The

lesson eight credit cards overheads

lesson eight credit cards overheads shopping for a credit card costs: Annual Percentage Rate (APR) or Finance (Interest) Charges Grace period Annual fees Transaction fees Balancing computation method for

lesson eight credit cards overheads shopping for a credit card costs: Annual Percentage Rate (APR) or Finance (Interest) Charges Grace period Annual fees Transaction fees Balancing computation method for

COMMERCIAL/BUSINESS LOAN APPLICATION PACKAGE

COMMERCIAL/BUSINESS LOAN APPLICATION PACKAGE CONTENTS: Member Business Loan Application Authorization to Obtain Credit Information Financial Statement Schedule of Business Debt REAL ESTATE & COMMERCIAL

COMMERCIAL/BUSINESS LOAN APPLICATION PACKAGE CONTENTS: Member Business Loan Application Authorization to Obtain Credit Information Financial Statement Schedule of Business Debt REAL ESTATE & COMMERCIAL

Keys to Your Financial Future Step 2.5: Credit Repair or Building Plan

46 MODULE 2: Good credit Keys to Your Financial Future Step 2.5: Credit Repair or Building Plan Use the questions to develop your credit repair or building plan. Do you need to repair your credit history?

46 MODULE 2: Good credit Keys to Your Financial Future Step 2.5: Credit Repair or Building Plan Use the questions to develop your credit repair or building plan. Do you need to repair your credit history?

About credit reports. Credit Reporting Agencies. Creating Your Credit Report

About credit reports Credit Reporting Agencies Credit reporting agencies maintain files on millions of borrowers. Lenders making credit decisions buy credit reports on their prospects, applicants and customers

About credit reports Credit Reporting Agencies Credit reporting agencies maintain files on millions of borrowers. Lenders making credit decisions buy credit reports on their prospects, applicants and customers

How To Check Your Credit Report For Not Credit History

Your Credit Report P.O. Box 15128 Spokane Valley, WA 99215 800.852.5316 www.hzcu.org You may not think about them every day, but your credit report and the three little digits that make up your credit

Your Credit Report P.O. Box 15128 Spokane Valley, WA 99215 800.852.5316 www.hzcu.org You may not think about them every day, but your credit report and the three little digits that make up your credit

Business Credit Application

Business Credit Application (Please type or print all information. Answers requiring additional space submitted on separate pages.) Firm Name: Firm Address: Firm Telephone: Firm Web Site URL: Email: EIN/Tax

Business Credit Application (Please type or print all information. Answers requiring additional space submitted on separate pages.) Firm Name: Firm Address: Firm Telephone: Firm Web Site URL: Email: EIN/Tax

How To Pay Off Debt Through Bankruptcy

Bankruptcy 13 Bankruptcy Debts & Debt Collection What happens if I can't pay my bills? Persons to whom you owe money have several methods of recourse if you fail to pay a debt. The method used depends

Bankruptcy 13 Bankruptcy Debts & Debt Collection What happens if I can't pay my bills? Persons to whom you owe money have several methods of recourse if you fail to pay a debt. The method used depends

IMPROVE YOUR CREDIT SCORE. Effective Credit Management At Your Fingertips

IMPROVE YOUR CREDIT SCORE Effective Credit Management At Your Fingertips Introduction In this ebook, you will get valuable information including: What is a credit score The score breakdown Managing your

IMPROVE YOUR CREDIT SCORE Effective Credit Management At Your Fingertips Introduction In this ebook, you will get valuable information including: What is a credit score The score breakdown Managing your

AT THE STORE CONSUMER CREDIT AND PROTECTION

AT THE STORE CONSUMER CREDIT AND PROTECTION Purchase of goods and services with a credit card is a part of modern life. As you may know, credit is easy to get. You may be required to have your mom or dad

AT THE STORE CONSUMER CREDIT AND PROTECTION Purchase of goods and services with a credit card is a part of modern life. As you may know, credit is easy to get. You may be required to have your mom or dad

BUSINESS LOAN PACKAGE. First Federal Bank of Florida

BUSINESS LOAN PACKAGE First Federal Bank of Florida BUSINESS CREDIT APPLICATION INFORMATION ABOUT THE BUSINESS: Legal Business Name Physical Address City State Zip Type of Organization: Sole Proprietorship

BUSINESS LOAN PACKAGE First Federal Bank of Florida BUSINESS CREDIT APPLICATION INFORMATION ABOUT THE BUSINESS: Legal Business Name Physical Address City State Zip Type of Organization: Sole Proprietorship

How To Know Your Credit Risk

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Credit Cards

Understanding Credit Cards INTRODUCTION This brochure can help you understand how credit cards work, become familiar with common terms offered with a credit card, and avoid the dangers of using credit

Understanding Credit Cards INTRODUCTION This brochure can help you understand how credit cards work, become familiar with common terms offered with a credit card, and avoid the dangers of using credit

Glossary of Terms. Automated Clearing House (ACH) -Electronic method that allows debits and credits to run through member s account.

-Electronic method that allows debits and credits to run through member s account.") 1 ABIL (Avoid Being In Line) -Automated service which allows members to make transfers, payments, and check balances. Accessible 24/7. Automated Clearing House (ACH) -Electronic method that allows debits

1 ABIL (Avoid Being In Line) -Automated service which allows members to make transfers, payments, and check balances. Accessible 24/7. Automated Clearing House (ACH) -Electronic method that allows debits

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account.

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Credit Cards. Megan Stearns, Credit Counselor

Credit Cards Megan Stearns, Credit Counselor Agenda What is a credit card? Types of credit cards Shopping for a credit card Advantages and disadvantages Using credit cards wisely Fraud What is a credit

Credit Cards Megan Stearns, Credit Counselor Agenda What is a credit card? Types of credit cards Shopping for a credit card Advantages and disadvantages Using credit cards wisely Fraud What is a credit

CREDIT IN A NEW COUNTRY:

CREDIT IN A NEW COUNTRY: A GUIDE TO CREDIT IN CANADA A free publication provided by Consolidated Credit Counseling Services of Canada, Inc., a registered charitable credit counselling and debt management

CREDIT IN A NEW COUNTRY: A GUIDE TO CREDIT IN CANADA A free publication provided by Consolidated Credit Counseling Services of Canada, Inc., a registered charitable credit counselling and debt management

Solving the Credit Puzzle. L G & W Federal Credit Union

Solving the Credit Puzzle L G & W Federal Credit Union Knowledge Check How much do you already know about credit scoring? Sample Credit Report Credit Bureaus Equifax TransUnion Experian Who Can Pull Your

Solving the Credit Puzzle L G & W Federal Credit Union Knowledge Check How much do you already know about credit scoring? Sample Credit Report Credit Bureaus Equifax TransUnion Experian Who Can Pull Your

Your Credit Report. 595 Market Street, 16th Floor San Francisco, CA 94105 888.456.2227 www.balancepro.net

Your Credit Report 750. 670. 620. 575. You may not think about them every day, but your credit reports and the three little digits that make up your credit score probably influence your life in many ways.

Your Credit Report 750. 670. 620. 575. You may not think about them every day, but your credit reports and the three little digits that make up your credit score probably influence your life in many ways.

A Roof Over Your Head

A Roof Over Your Head FDIC Money Smart for Young Adults Building: Knowledge, Security, Confidence Objectives Identify initial and continuing costs of renting an apartment. List questions to ask when determining

A Roof Over Your Head FDIC Money Smart for Young Adults Building: Knowledge, Security, Confidence Objectives Identify initial and continuing costs of renting an apartment. List questions to ask when determining

Recommended Solution

October 17, 2011 TM Recommended Solution Your Debt Reduction Goal: Increase cash flow by making debt payments smaller You ve indicated that you re fairly comfortable with your financial situation. Since

October 17, 2011 TM Recommended Solution Your Debt Reduction Goal: Increase cash flow by making debt payments smaller You ve indicated that you re fairly comfortable with your financial situation. Since

Credit Cards: Advantages & Disadvantages

Credit Cards: Advantages & Disadvantages Latino Community Credit Union & Latino Community Development Center CREDIT CARDS: BUILDING A better FUTURE ADVANTAGES AND DISADVANTAGES Latino Community Credit

Credit Cards: Advantages & Disadvantages Latino Community Credit Union & Latino Community Development Center CREDIT CARDS: BUILDING A better FUTURE ADVANTAGES AND DISADVANTAGES Latino Community Credit

B u t t e r f i e l d P e r s o n a l L o a n s

Personal Loans B u t t e r f i e l d P e r s o n a l L o a n s Whether your borrowing needs are large or small, long or short term, we have a loan that suits your needs. At Butterfield Bank, we pride ourselves

Personal Loans B u t t e r f i e l d P e r s o n a l L o a n s Whether your borrowing needs are large or small, long or short term, we have a loan that suits your needs. At Butterfield Bank, we pride ourselves

B U S I N E S S C R E D I T APPLICATION & AGREEMENT

B U S I N E S S C R E D I T APPLICATION & AGREEMENT In this Application and Agreement, you and your mean each person signing this Application and Agreement. Company is your business identified in this

B U S I N E S S C R E D I T APPLICATION & AGREEMENT In this Application and Agreement, you and your mean each person signing this Application and Agreement. Company is your business identified in this

Welcome. 1. Agenda. 2. Ground Rules. 3. Introductions. Borrowing Basics 2

Borrowing Basics Welcome 1. Agenda 2. Ground Rules 3. Introductions Borrowing Basics 2 Objectives Define what credit and a loan is Distinguish between secured and unsecured loans Identify three types of

Borrowing Basics Welcome 1. Agenda 2. Ground Rules 3. Introductions Borrowing Basics 2 Objectives Define what credit and a loan is Distinguish between secured and unsecured loans Identify three types of

Your Credit Report. 595 Market Street, 16th Floor San Francisco, CA 94105 888.456.2227 www.balancepro.net

Your Credit Report 750. 670. 620. 575. You may not think about them every day, but your credit report and the three little digits that make up your credit score probably influence your life in many ways.

Your Credit Report 750. 670. 620. 575. You may not think about them every day, but your credit report and the three little digits that make up your credit score probably influence your life in many ways.

u n i t f i v e Credit: Buy Now, Pay Later To use credit wisely you need to know oming soon to a what s really

Unit Five Credit: Buy Now, Pay Later To use credit wisely you C need to know oming soon to a what s really mailbox near you credit card offers! involved. If you haven t started receiving them already,

Unit Five Credit: Buy Now, Pay Later To use credit wisely you C need to know oming soon to a what s really mailbox near you credit card offers! involved. If you haven t started receiving them already,

About your credit score. About FICO Score. Other names for FICO Score. http://www.myfico.com/crediteducation/creditscores.aspx

http://www.myfico.com/crediteducation/creditscores.aspx About your credit score Your credit score influences the credit that s available to you and the terms (interest rate, etc.) that lenders offer you.

http://www.myfico.com/crediteducation/creditscores.aspx About your credit score Your credit score influences the credit that s available to you and the terms (interest rate, etc.) that lenders offer you.

lesson six banking services supplemental materials 04/09

lesson six banking services supplemental materials 04/09 banking terms account Money deposited with a financial institution for investment and/or safekeeping purposes. assets Items of monetary value (e.g.,

lesson six banking services supplemental materials 04/09 banking terms account Money deposited with a financial institution for investment and/or safekeeping purposes. assets Items of monetary value (e.g.,

Financial Literacy. Credit basics

Literacy Credit basics 2 Contents HANDOUT 6-1 Types of credit Type of credit Lender Uses Conditions Revolving credit Credit Cards (secured and unsecured NOT prepaid) To make purchases, pay bills, make

Literacy Credit basics 2 Contents HANDOUT 6-1 Types of credit Type of credit Lender Uses Conditions Revolving credit Credit Cards (secured and unsecured NOT prepaid) To make purchases, pay bills, make

Agriculture & Business Management Notes...

Agriculture & Business Management Notes... Obtaining and Using Agricultural Credit Effectively Quick Notes... Credit is important and necessary in nearly all commercial farm businesses. Be sure uses of

Agriculture & Business Management Notes... Obtaining and Using Agricultural Credit Effectively Quick Notes... Credit is important and necessary in nearly all commercial farm businesses. Be sure uses of

Understanding Your Credit Score

Understanding Your Credit Score Contents Your Credit Score A Vital Part of Your Credit Health...... 1 How Credit Scoring Helps You........ 2 Your Credit Report The Basis of Your Score............. 4 How

Understanding Your Credit Score Contents Your Credit Score A Vital Part of Your Credit Health...... 1 How Credit Scoring Helps You........ 2 Your Credit Report The Basis of Your Score............. 4 How

Instructions To Fill Out Personal Financial Statement

Member FDIC Instructions To Fill Out Personal Financial Statement We suggest that you start with the Schedules in Part C, and then carry forward the totals to the Financial Data section on page 2. Part

Member FDIC Instructions To Fill Out Personal Financial Statement We suggest that you start with the Schedules in Part C, and then carry forward the totals to the Financial Data section on page 2. Part

Establishing and maintaining good credit is an important part of financial planning. Typically most individuals do not have enough cash on hand for

Basics of Credit Establishing and maintaining good credit is an important part of financial planning. Typically most individuals do not have enough cash on hand for emergencies, or to make major purchases

Basics of Credit Establishing and maintaining good credit is an important part of financial planning. Typically most individuals do not have enough cash on hand for emergencies, or to make major purchases

MANAGING CREDIT101 TM %*'9 [[[ EPXEREJGY SVK i

MANAGING CREDIT101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

MANAGING CREDIT101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

Preparing Family Net Worth and Income Statements

Family and Consumer Sciences FSFCS49 Preparing Family Net Worth and Income Statements Laura Connerly Instructor - Family Resource Management Arkansas Is Our Campus Visit our web site at: http://www.uaex.edu

Family and Consumer Sciences FSFCS49 Preparing Family Net Worth and Income Statements Laura Connerly Instructor - Family Resource Management Arkansas Is Our Campus Visit our web site at: http://www.uaex.edu

Teacher's Guide. Lesson Three. Credit Cards 07/13

Teacher's Guide $ Lesson Three Credit Cards 07/13 credit cards websites Before students use credit cards, it's important that they familiarise themselves with: the advantages and disadvantages of credit

Teacher's Guide $ Lesson Three Credit Cards 07/13 credit cards websites Before students use credit cards, it's important that they familiarise themselves with: the advantages and disadvantages of credit

It Is In Your Interest

STUDENT MODULE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Jason did not understand how it

STUDENT MODULE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Jason did not understand how it

Money Management How to Get Out of Debt

FCS5-104 Money Management How to Get Out of Debt Individuals and families turn to credit as an extra source of income. People use credit because it is easily available. As the debts pile up, families who

FCS5-104 Money Management How to Get Out of Debt Individuals and families turn to credit as an extra source of income. People use credit because it is easily available. As the debts pile up, families who

TransUnion Credit Report User Guide

TransUnion Credit Report User Guide SOUTH AFRICA Page 1 of 8/.. TransUnion Credit Report USER Guide Using this guide This guide will walk you through the three sections of your report and the standard

TransUnion Credit Report User Guide SOUTH AFRICA Page 1 of 8/.. TransUnion Credit Report USER Guide Using this guide This guide will walk you through the three sections of your report and the standard

BUSINESS LOAN APPLICATION CHECKLIST

Growing Businesses, Building Communities BUSINESS LOAN APPLICATION CHECKLIST Please complete the attached loan application, provide all requested documentation, and mail to: Texas Mezzanine Fund, Inc.

Growing Businesses, Building Communities BUSINESS LOAN APPLICATION CHECKLIST Please complete the attached loan application, provide all requested documentation, and mail to: Texas Mezzanine Fund, Inc.

Exercise 4A: What Info Do You Need for a Loan?

Exercise 4A: What Info Do You Need for a Loan? What information do you think is needed to get a loan? Review several samples of loan applications to see what The Cost of Using Credit As mentioned earlier,

Exercise 4A: What Info Do You Need for a Loan? What information do you think is needed to get a loan? Review several samples of loan applications to see what The Cost of Using Credit As mentioned earlier,

RELIANT COMMUNITY FEDERAL CREDIT UNION BUSINESS CREDIT APPLICATION

Main Office: 10 Benton Pl., PO Box 40, Sodus, NY 14551 800.724.9282 reliantcu.com Brockport Canandaigua Geneva Henrietta Irondequoit Macedon Newark Sodus Webster RELIANT COMMUNITY FEDERAL CREDIT UNION

Main Office: 10 Benton Pl., PO Box 40, Sodus, NY 14551 800.724.9282 reliantcu.com Brockport Canandaigua Geneva Henrietta Irondequoit Macedon Newark Sodus Webster RELIANT COMMUNITY FEDERAL CREDIT UNION

Credit ~ The Basics Participant s Guide

1 Credit ~ The Basics Participant s Guide Table of Contents Welcome Pre-Test What is Credit & Why is it Important? Types of Loans The Cost of Credit The Four C s of Credit Credit Reports Credit Scores

1 Credit ~ The Basics Participant s Guide Table of Contents Welcome Pre-Test What is Credit & Why is it Important? Types of Loans The Cost of Credit The Four C s of Credit Credit Reports Credit Scores

Welcome. 1. Agenda. 2. Ground Rules. 3. Introductions. Your Own Home 2

Your Own Home Welcome 1. Agenda 2. Ground Rules 3. Introductions Your Own Home 2 Objectives If you are a pre-homebuyer: Explain the advantages and disadvantages of renting versus owning a home Identify

Your Own Home Welcome 1. Agenda 2. Ground Rules 3. Introductions Your Own Home 2 Objectives If you are a pre-homebuyer: Explain the advantages and disadvantages of renting versus owning a home Identify