BILL OF SALE (AUTOMOBILE), PROMISSORY NOTE (AUTOMOBILE) & GUIDES

|

|

|

- Kristopher Wilkerson

- 8 years ago

- Views:

Transcription

1 BILL OF SALE (AUTOMOBILE), PROMISSORY NOTE (AUTOMOBILE) & GUIDES Included: Overview Dos and Don ts Checklist Bill of Sale (Automobile) Instructions Promissory Note (Automobile) Instructions Sample Bill of Sale (Automobile) Sample Promissory Note (Automobile)

Sample Promissory")

2 1. Overview You ve listed your car and you ve found your buyer - it s time to finish your deal. In the modern marketplace, your transaction can t be completed with a simple handshake and a wave goodbye. Your vehicle transfer also requires you to file with your state s motor vehicle department and other local agencies, This process calls for a complete, well-drafted bill of sale. With the enclosed documents and instructions, you can firm up the terms of your arrangement and prepare for your car s new titling and registration. A bill of sale is like a receipt. It proves that ownership of a particular piece of property has changed hands. It also details the terms of the sale, including information about price, delivery, and condition. Bills of sale can help to prove the identity of a vehicle s true legal owner. Moreover, many states and counties use these documents to determine the amount of sales tax owed on the transaction, if any. A promissory note is also included in this package, which allows the buyer to make vehicle payments over time and provides security for those payments. If you follow the enclosed samples and guidelines, you will have a written acknowledgment of the rights and responsibilities being transferred as part of your sale. This will provide essential documentation of your ownership and liability obligations and you will be well on your way to establishing a clear record of title for your property. 2. Dos & Don ts Checklist BILL OF SALE Getting the correct name and physical address of the other party to your deal is essential. If a question emerges about property title, you ll need to get in immediate contact with that person or company. If you are selling the vehicle, give the buyer a completed bill of sale only after you have received your money and the transaction is complete. Since the bill of sale states that you have already been paid, it may be difficult to collect any outstanding amounts if the buyer has written evidence that its payment obligations are complete. The enclosed bill of sale assumes that payment of the car s purchase price will be made over time. If buyer intends to complete the sale with one lump sum, the parties should use a bill of sale that contemplates such immediate payment. Sign two copies of the bill of sale, one for you and one for the other party. Although not strictly required, consider bringing a third party with you when the bill of sale is signed. If questions arise about the sale, that person can serve as a reporter of the transaction. Alternatively, you and the other party can notarize your signatures on the document. Once your bill of sale is complete and signed, visit your local county clerk or tax office to record the bill. They will use the bill of sale to estimate your sales (or use) tax and record the transaction. 1

3 The seller should contact its state Department of Motor Vehicles immediately after completion of the sale and let them know the vehicle has been sold and to whom. This will protect the seller if a ticket is issued or an accident occurs in the period between the sale and the re-titling of the car. To complete the transfer of title, both the seller and the buyer should send a copy of the bill of sale to their state s Department of Motor Vehicles (DMV). Some states require that the seller report the title transfer within five (5) days of the sale, and the buyer report the title transfer within ten (10). Additional steps may be required for your vehicle transfer. For example, the car s pink slip must be signed over to the purchasing party. Check with your local motor vehicle agency and tax authority to see what documents may be needed. Remove the vehicle s license plate before physically transferring it to the buyer. In many states, this is required by law. PROMISSORY NOTE Before sitting down to sign, decide exactly what your goals are for the note. How long is the loan for? How much will be paid each month (or other period)? What interest rates will be applicable? A good agreement is one that captures the intentions of the parties accurately. Take a moment to clarify the terms and conditions of your loan before memorializing them in written form. The promissory note should only be used if the buyer intends to make a down payment at the time of purchase and pay the remainder over time. If payment of the car s purchase price will be complete on the sale date, the parties should use a bill of sale that contemplates such immediate payment and do not need to sign a promissory note. Allow each party to spend some time reviewing the promissory note. This will reduce the likelihood, or at least the efficacy, of claims that a party did not understand any terms or know what their obligations were under the document. Both parties should review the note carefully to ensure that all relevant deal points have been included. Do not assume that certain expectations or terms are agreed to if they are not stated expressly on the document. The following form is a secured promissory note. This means that the lender takes a secured interest in the borrower s vehicle. If the borrower defaults on the loan, the lender can seize that car almost immediately. By contrast, with an unsecured note, the lender would have to go to court to demand payment if a default occurred. In general, secured promissory notes are supplemented with and supported by security agreements. Those security agreements are what allow lenders to take property if a default occurs. This package does not include a security agreement. 2

days of the sale, and the buyer report the title transfer within ten (10).")

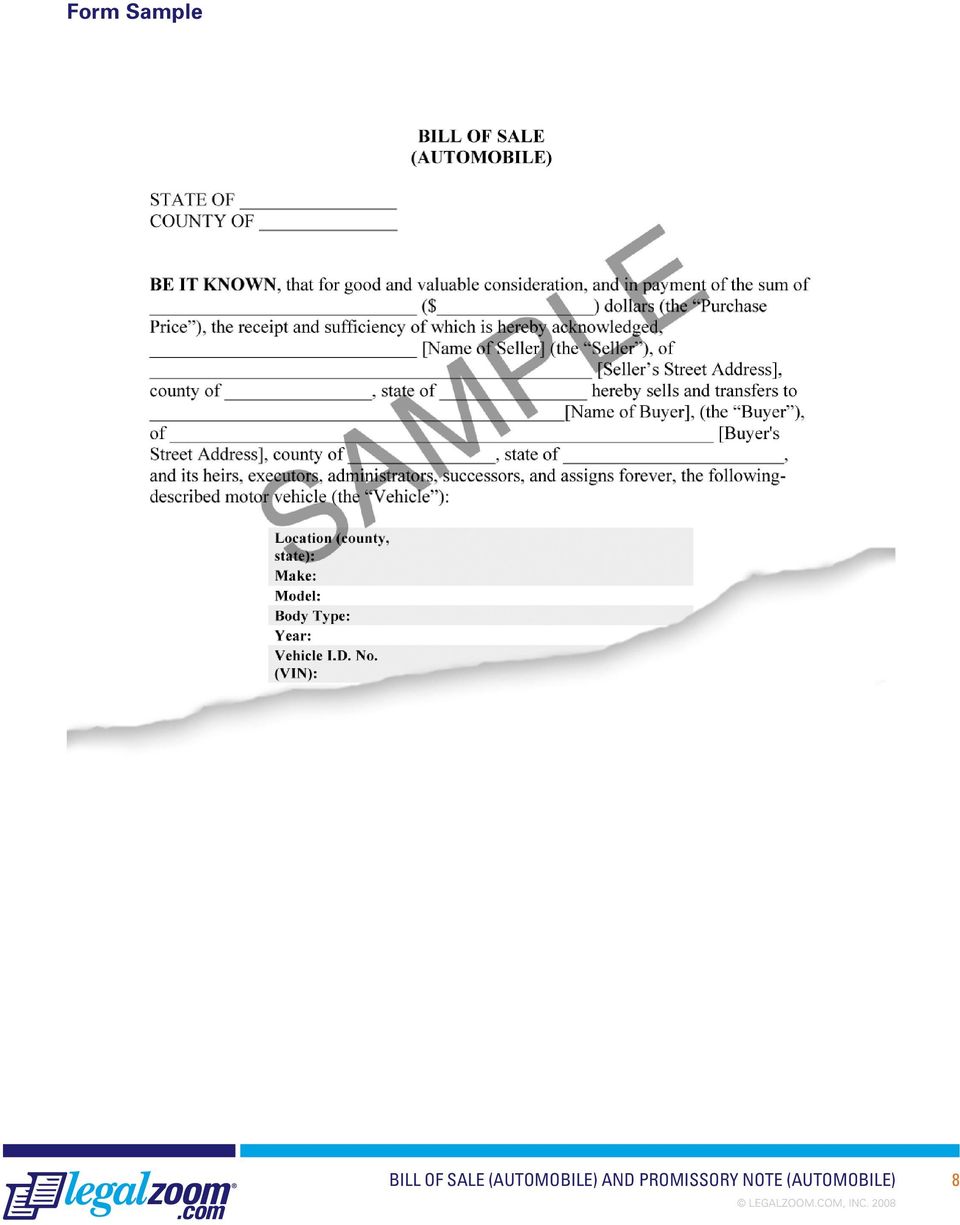

4 A security interest in a vehicle can (and should) be memorialized with a financing statement (more specifically, a document called a UCC financing statement). Once a financing statement is completed and filed with the correct governmental authority, the lender s interest in the property is considered perfected. This means that if future lenders also seek a security interest in the same asset (in this case, the car), the lender with the perfected interest would have top priority and could take the property for itself after a default. The enclosed note has a specific term, during which the borrower must make regular, equal payments. At the end of that term, the borrower must pay any outstanding amounts due under the document. This last payment is sometimes called a lump-sum or a balloon payment. Choose a fair interest rate. Although the enclosed note will rewrite any illegal interest rate to make it legal, it s a good idea to select a more reasonable number. This will decrease the chances of default and make for a less strained relationship between the parties. The parties should sign only the one original document, and that original should be given to the lender. Make at least one photocopy, make sure that the document says COPY in bold letters, and give the copy to the borrower. After the note has been paid in full, the lender should return the original document to the borrower. Depending on the nature of its terms, you may decide to have your note witnessed or notarized. This will limit later challenges to the validity of a party s signature. If your agreement is complicated, do not use the enclosed form. Contact an attorney to help you draft a document that will meet your specific needs. 3. Bill of Sale and Promissory Note (Automobile) Instructions The following provision-by-provision instructions will help you understand the terms of your bill of sale and promissory note. The numbers below (e.g., Section 1, Section 2, etc.) correspond to the provisions in the forms. Please review both documents in their entirety before starting your step-by-step process. BILL OF SALE Location of Sale. Write in the name of the state and county where the sale will take place. If the parties are from different counties, use the state and county in which the car is located. Purchase Price. Enter the purchase price in the first blank provided. Be sure to include the full price that will be paid, including previous down-payments and future payments. Names and Addresses of Parties. Identifies the parties and their street addresses (not P.O. Boxes). One party to this bill is called the Seller and the other is called the Buyer. As you probably guessed, the Seller is the party that will sell the car and the Buyer is the party that will purchase it. Note that only the individual whose name is on the title of a vehicle is permitted to sell it. This means that if a married couple is selling the car but it is in the wife s name only, only the wife should sign the bill of sale. 3

5 Vehicle Location and Description. These spaces allow you to describe fully the vehicle you are buying or selling. Be as specific as possible, making sure that the item being sold can be identified clearly from the description. You must include the location, make, model, body type, year, and VIN, examples of which are listed below:» Location: Include the county and state where the vehicle is currently situated.» Make: Ford, Chevrolet, Lincoln, BMW, etc.» Model: Corvette, M5, Mustang, etc.» Body Type: Sedan, Coupe, Convertible, SUV, etc.» VIN: The Vehicle Identification Number (or VIN ) is your car s 17-character unique identifier. Generally, the VIN is located in one of the following places: the dashboard; the steering column; the vehicle s firewall; driver side door; or passenger side post. Review your user manual if you can not locate the VIN. Section 1: Payment Method. The enclosed bill of sale assumes that the buyer will make a series of monthly payments, rather than paying all at once. Fill in the amount of the promissory note and the amount of any down payment. Although the promissory note is separate from the bill of sale, the documents should be kept together in your records. Section 2: Seller s Representations and Warranties of Title. The Seller s promise that it owns the car and that no other party holds an interest in the car. Section 3: Buyer s Representations and Warranties. The Buyer s promise that the person signing the bill of sale has the authority to do so. Section 4: No Other Warranties. Disclaims any warranty other than the warranty of title described in Section 2 and the manufacturer s warranty (if any). This vehicle is being offered as is. The buyer should note this provision: if the car has problems in the future, the seller is disclaiming responsibility. Section 5: Inspection. A summary of recent mechanical inspections. If the vehicle has been inspected within the last month, delete the bracketed not and attach a report of such inspection. If not, delete the second sentence. If the seller knows of any defects in the car, those problems must be disclosed in the space provided. Any known defects that are not reported could invalidate the sale, and may bring later charges of fraud. If there are no known defects, the blank space can be deleted. Section 6: Delivery of Vehicle. Explains where and when the vehicle should be picked up by the Buyer. Write in the date on which you want this to happen. Section 7: Conveyance of Title. Indicates that title to the vehicle will be given to the Buyer on the day on which it receives that vehicle. This section also includes the Seller s promise that it will sign every document needed to effectuate the title transfer. Section 8: Cancellation of Insurance and Tags. The Seller s agreement to cancel any remaining insurance or tags that it was maintaining on the vehicle. 4

6 Section 9: Additional Terms of Sale. If there are additional terms you d like to add to the form, enter those in the space provided. For example, the parties may wish to include a requirement that the car be cleaned thoroughly before sale completion. Signatures. Each party must sign and print their name. Several states require that each party provide a phone number as well. Although this may not be a requirement in your state, it s a good idea for both parties to provide as much contact information as possible. Be sure to date this document as well, as a number of deadlines start to run on the sale date (e.g. transfer of title and registration). If a third party witnessed the signing, have that person sign and date the space provided. If there is no such witness, you can delete this segment. Odometer Disclosure Statement. Federal and state laws require an accurate report of a vehicle s mileage on a bill of sale. Some states require this disclosure statement to be on a page separate from the bill of sale itself. The enclosed form has made this separation. Write in the seller s name and the number of miles on the car. Do not include tenths of a mile in your report of the current odometer reading. Do not check any of the blank lines if the odometer reading is, to the seller s knowledge, correct. Check the first line if the odometer goes to five digits, and the reported mileage is incorrect because the odometer has rolled over after passing 99,999 miles. For example, if the reading is 10,000, but the actual mileage is 110,000, the seller should record the number 10,000 and check this line. If the seller knows the odometer number is incorrect or the odometer itself is broken, it should check the second line. PROMISSORY NOTE Introduction. Identifies the document as a note. Write in the date on which the note becomes effective. Note that one party is called the Seller and the other the Buyer. Identify the parties and, if applicable, what type of organization(s) they are. Note that one party is called the Payee and the other the Borrower. As you may have guessed, the Borrower is the party that is borrowing money (and is the buyer under the bill of sale) and will pay it to the Payee (usually, the seller under the bill of sale) over time. The payee may or may not be the same entity as the lender. Since the promissory note and bill of sale are separate documents, there will be some information repeated in this document. Fill in the names of the parties and the vehicle s identifying characteristics. Section 1: Transfer of Title. This second part of the paragraph explains that the Buyer will receive title as provided under the bill of sale. However, the lender under the bill of sale will have a secured lien on that title until the note is completely paid off. The parties should consider also completing and signing a security agreement to provide complete security to the lender. Section 2: Promise of Payment. This is the meat of the note, where the total principal amount of the note and interest rate are stated. This is also where the Payee designates where exactly it will be paid (usually the Payee s business address). The other language ensures that the interest rates set by the parties aren t illegal. In other words, if an agreed-to interest rate is above what the law allows, this section rewrites that provision to make it legal. 5

7 Section 3: Monthly Installment Payments. Write the monthly amount that the Borrower will pay, and indicate the day of the month this amount is due. The remainder of this section explains that payments will go first to interest payments and second to paying down the principal. If you and the other party decide to set a different payment schedule (for example, yearly or quarterly installment payments), revise the language to reflect your agreement. Section 4: Initial Date. Provides the date on which installment payments will start, and reiterates that those payments will continue to be due monthly after that date. Again, if you and the other party have decided to set a different payment schedule (for example, yearly or quarterly installment payments), revise the language to reflect that agreement. Section 5: Prepayment. Explains that the Borrower can pay money to the Payee before it is due under the note, and it won t be penalized for doing that. Section 6: Lump-Sum Final Payment. The parties agreement about the due date of the loan. All payments on the note must be complete on or before that due date. Section 7: Security. Reiterates that the lender s continuing interest in the vehicle secures payment under the note. Section 8: Events of Default. Lists the situations in which the Payee can demand immediate payment of all unpaid amounts. Specifically, these events are defaults in payment, bankruptcy filings, or entries into receivership. If you and the other party want to include additional events of default, you can do that in this section. Section 9: Acceleration; Remedies on Default. A description of the actions the Payee can take if an event of default (listed in Section 8) occurs. Most importantly, this section explains that the Payee can move up the due date of the loan if a default occurs. Section 10: Waiver of Presentment. Indicates that if an event of default occurs, the Payee doesn t have to explain to the Borrower that it is going to take action (for example, requiring the entire note to be paid at once). The Payee can simply take that action without notice. Section 11: Time of Essence (Optional). This is an optional provision that is included to allow you and the other party to determine how strictly you want to enforce the time limits in your note. Generally, by including this provision, the Payee is allowing the Borrower no leeway if payment isn t within the exact time agreed, the Borrower is in default. By deleting this provision, you are usually allowing the Borrower some reasonable breathing room. If you remove this section, correct the section numbers and references in the note. Section 12: Successors and Assigns. States that the parties rights and obligations will be passed on to heirs or, in the case of companies, to successor organizations. Section 13: Notice. Lists the addresses to which all official or legal correspondence should be delivered. Write in a mailing address for both the Borrower and the Payee. Section 14: Governing Law. Allows the parties to choose the state and county laws that will be used to interpret the note. This is not a venue provision: the included language will not impact where a potential claim can be brought. Please write the applicable state and county in the blanks provided. 6

8 Section 15: Entire Agreement. The parties agreement that the note (together with the bill of sale) they re signing is the agreement about the issues involved. Unfortunately, the inclusion of this provision will not prevent a party from arguing that other enforceable promises exist, but it will provide you some protection from these claims. Section 16: No Implied Waiver. Explains that even if the Payee allows the Borrower to break or ignore an obligation, the Payee does not waive any future right to require those (or any other) obligations to be fulfilled. Section 17: Collection Costs and Attorney s Fees. Places the responsibility for paying any costs of collecting money under the note on the Borrower s shoulders. If the Payee has to hire a third party to get its money, the Borrower will pay all of that third party s fees and costs. Section 18: Severability. Protects the terms of the note as a whole, even if one part is later invalidated. Section 19: Headings. Notes that the headings at the beginning of each section are meant to organize the document, and should not be considered operational parts of the note. DISCLAIMER LegalZoom is not a law firm. The information contained in the packet is general legal information and should not be construed as legal advice to be applied to any specific factual situation. The use of the materials in this packet does not create or constitute an attorney-client relationship between the user of this form and LegalZoom, its employees or any other person associated with LegalZoom. Because the law differs in each legal jurisdiction and may be interpreted or applied differently depending on your location or situation, you should not rely upon the materials provided in this packet without first consulting an attorney with respect to your specific situation. The materials in this packet are provided "As-Is," without warranty or condition of any kind whatsoever. LegalZoom does not warrant the materials' quality, accuracy, timeliness, completeness, merchantability or fitness for use or purpose. To the maximum extent provided by law, LegalZoom, it agents and officers shall not be liable for any damages whatsoever (including compensatory, special, direct, incidental, indirect, consequential, punitive or any other damages) arising out of the use or the inability to use the materials provided in this packet. 7

obligations to be fulfilled.")

9 Form Sample 8

10 Form Sample 9

BILL OF SALE (AUTOMOBILE) & GUIDE

& GUIDE") & GUIDE Included: Overview Dos and Don ts Checklist Bill of Sale (Automobile) Instructions Sample Bill of Sale (Automobile) 1. Overview You ve listed your car and you ve found your buyer - it s time to

& GUIDE Included: Overview Dos and Don ts Checklist Bill of Sale (Automobile) Instructions Sample Bill of Sale (Automobile) 1. Overview You ve listed your car and you ve found your buyer - it s time to

UNSECURED PROMISSORY NOTE (AMORTIZED PAYMENTS) & GUIDE

& GUIDE") UNSECURED PROMISSORY NOTE (AMORTIZED PAYMENTS) & GUIDE Included: Overview Dos and Don ts Checklist Unsecured Promissory Note (Amortized Payments) Instructions Sample Unsecured Promissory Note (Amortized

UNSECURED PROMISSORY NOTE (AMORTIZED PAYMENTS) & GUIDE Included: Overview Dos and Don ts Checklist Unsecured Promissory Note (Amortized Payments) Instructions Sample Unsecured Promissory Note (Amortized

SECURED PROMISSORY NOTE (DEMAND) & GUIDE

& GUIDE") & GUIDE Included: Overview Dos and Don ts Checklist Secured Promissory Note (Demand) Instructions Sample Secured Promissory Note (Demand) 1. Overview Successful businesses are built on big ideas and long-range

& GUIDE Included: Overview Dos and Don ts Checklist Secured Promissory Note (Demand) Instructions Sample Secured Promissory Note (Demand) 1. Overview Successful businesses are built on big ideas and long-range

WARRANTY BILL OF SALE (BOAT) & GUIDE

& GUIDE") & GUIDE Included: Overview Dos and Don ts Checklist Warranty Bill of Sale (Boat) Instructions Sample Warranty Bill of Sale (Boat) 1. Overview You ve listed your boat and you ve found your buyer - it s

& GUIDE Included: Overview Dos and Don ts Checklist Warranty Bill of Sale (Boat) Instructions Sample Warranty Bill of Sale (Boat) 1. Overview You ve listed your boat and you ve found your buyer - it s

EARNEST MONEY PROMISSORY NOTE & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Earnest Money Promissory Note Instructions Sample Earnest Money Promissory Note 1. Overview Buying real estate is an expensive and time-consuming activity.

& GUIDE Included: Overview Dos and Don ts Checklist Earnest Money Promissory Note Instructions Sample Earnest Money Promissory Note 1. Overview Buying real estate is an expensive and time-consuming activity.

EQUIPMENT LEASE AGREEMENT & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Equipment Lease Agreement Instructions Sample Equipment Lease Agreement 1. Overview To compete effectively in today s business world, your operation

& GUIDE Included: Overview Dos and Don ts Checklist Equipment Lease Agreement Instructions Sample Equipment Lease Agreement 1. Overview To compete effectively in today s business world, your operation

DEBT SETTLEMENT AGREEMENT & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Debt Settlement Agreement Instructions Sample Debt Settlement Agreement 1. Overview No matter the protective measures taken, it is a simple market fact

& GUIDE Included: Overview Dos and Don ts Checklist Debt Settlement Agreement Instructions Sample Debt Settlement Agreement 1. Overview No matter the protective measures taken, it is a simple market fact

CONSULTING SERVICES AGREEMENT & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Consulting Services Agreement Instructions Sample Consulting Services Agreement 1. Overview From an accounting perspective, hiring consultants is cheaper

& GUIDE Included: Overview Dos and Don ts Checklist Consulting Services Agreement Instructions Sample Consulting Services Agreement 1. Overview From an accounting perspective, hiring consultants is cheaper

CONSIGNMENT AGREEMENT & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Consignment Agreement Instructions Sample Consignment Agreement 1. Overview Businesses choose consignment arrangements for many reasons. Retail stores

& GUIDE Included: Overview Dos and Don ts Checklist Consignment Agreement Instructions Sample Consignment Agreement 1. Overview Businesses choose consignment arrangements for many reasons. Retail stores

DOMAIN NAME ASSIGNMENT & GUIDELINES

Included: Overview Dos and Don ts Checklist Domain Name Assignment Instructions Sample Domain Name Assignment 1. Overview A company s ability to sell and purchase property is essential to its long-term

Included: Overview Dos and Don ts Checklist Domain Name Assignment Instructions Sample Domain Name Assignment 1. Overview A company s ability to sell and purchase property is essential to its long-term

SAMPLE BILL OF SALE (CAT) & GUIDELINES

& GUIDELINES") & GUIDELINES Included: Overview Dos and Don ts Checklist Bill of Sale (Cat) Instructions Sample Bill of Sale (Cat) 1. Overview Bringing a pet into a family is both an emotional and practical decision.

& GUIDELINES Included: Overview Dos and Don ts Checklist Bill of Sale (Cat) Instructions Sample Bill of Sale (Cat) 1. Overview Bringing a pet into a family is both an emotional and practical decision.

WEBSITE DEVELOPMENT AGREEMENT & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Website Development Agreement Instructions Sample Website Development Agreement 1. Overview In the modern marketplace, developing and maintaining an

& GUIDE Included: Overview Dos and Don ts Checklist Website Development Agreement Instructions Sample Website Development Agreement 1. Overview In the modern marketplace, developing and maintaining an

MODEL WARRANTY BILL OF SALE & GUIDELINES

Included: Overview Dos and Don ts Checklist Warranty Bill of Sale Instructions Sample Warranty Bill of Sale 1. Overview A company s ability to sell and purchase property is essential to its long-term life

Included: Overview Dos and Don ts Checklist Warranty Bill of Sale Instructions Sample Warranty Bill of Sale 1. Overview A company s ability to sell and purchase property is essential to its long-term life

PROPERTY MANAGEMENT AGREEMENT & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Property Management Agreement Instructions Sample Property Management Agreement 1. Overview You ve found the building. You ve made your investment. Now

& GUIDE Included: Overview Dos and Don ts Checklist Property Management Agreement Instructions Sample Property Management Agreement 1. Overview You ve found the building. You ve made your investment. Now

TERMINATION OF LEASE AGREEMENT & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Termination of Lease Agreement Instructions Sample Termination of Lease Agreement 1. Overview The end of a lease is as important as its beginning. A

& GUIDE Included: Overview Dos and Don ts Checklist Termination of Lease Agreement Instructions Sample Termination of Lease Agreement 1. Overview The end of a lease is as important as its beginning. A

PARTNERSHIP DISSOLUTION AGREEMENT & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Partnership Dissolution Agreement Instructions Sample Partnership Dissolution Agreement 1. Overview A change in the business climate or individual goals

& GUIDE Included: Overview Dos and Don ts Checklist Partnership Dissolution Agreement Instructions Sample Partnership Dissolution Agreement 1. Overview A change in the business climate or individual goals

GENERAL CONTRACT AGREEMENT & GUIDE

Included: Overview Dos and Don ts Checklist General Agreement Instructions Model General Agreement 1. Overview Every agreement has terms and conditions that should be understood by every party that signs

Included: Overview Dos and Don ts Checklist General Agreement Instructions Model General Agreement 1. Overview Every agreement has terms and conditions that should be understood by every party that signs

INTELLECTUAL PROPERTY ASSIGNMENT & GUIDELINES

& GUIDELINES Included: Overview Dos and Don ts Checklist Intellectual Property Assignment Instructions Sample Intellectual Property Assignment 1. Overview A company s ability to buy and sell property is

& GUIDELINES Included: Overview Dos and Don ts Checklist Intellectual Property Assignment Instructions Sample Intellectual Property Assignment 1. Overview A company s ability to buy and sell property is

LETTER OF INTENT FOR BUSINESS TRANSACTION & GUIDELINES

& GUIDELINES Included: Overview Dos and Don ts Checklist Letter of Intent for Business Transaction Instructions Sample Letter of Intent for Business Transaction 1. Overview Before settling on the final

& GUIDELINES Included: Overview Dos and Don ts Checklist Letter of Intent for Business Transaction Instructions Sample Letter of Intent for Business Transaction 1. Overview Before settling on the final

TRADEMARK ASSIGNMENT & GUIDELINES

& GUIDELINES Included: Overview Dos and Don ts Checklist Trademark Assignment Instructions Sample Trademark Assignment 1. Overview A company s ability to buy and sell property is essential to its long-term

& GUIDELINES Included: Overview Dos and Don ts Checklist Trademark Assignment Instructions Sample Trademark Assignment 1. Overview A company s ability to buy and sell property is essential to its long-term

EMPLOYEE TERMINATION LETTER & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Employee Termination Letter Instructions Sample Employee Termination Letter 1. Overview At some point in the life of every organization, managers will

& GUIDE Included: Overview Dos and Don ts Checklist Employee Termination Letter Instructions Sample Employee Termination Letter 1. Overview At some point in the life of every organization, managers will

PATENT APPLICATION ASSIGNMENT & GUIDELINES

PATENT APPLICATION ASSIGNMENT & GUIDELINES Included: Overview Dos and Don ts Checklist Patent Application Assignment Instructions Sample Patent Application Assignment USPTO Recordation Form Cover Sheet

PATENT APPLICATION ASSIGNMENT & GUIDELINES Included: Overview Dos and Don ts Checklist Patent Application Assignment Instructions Sample Patent Application Assignment USPTO Recordation Form Cover Sheet

NON-DISCLOSURE AGREEMENT (Mutual)

") Included: Overview Dos & Don ts Checklist Non-Disclosure Agreement Instructions Model Mutual Non-Disclosure Agreement 1. Overview Non-disclosure agreements (also called NDAs or confidentiality agreements)

Included: Overview Dos & Don ts Checklist Non-Disclosure Agreement Instructions Model Mutual Non-Disclosure Agreement 1. Overview Non-disclosure agreements (also called NDAs or confidentiality agreements)

PET SITTING AGREEMENT & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Pet Sitting Agreement Instructions Sample Pet Sitting Agreement 1. Overview Pets (like humans) are most comfortable in their own homes. If you go away

& GUIDE Included: Overview Dos and Don ts Checklist Pet Sitting Agreement Instructions Sample Pet Sitting Agreement 1. Overview Pets (like humans) are most comfortable in their own homes. If you go away

ILLINOIS GENERAL AFFIDAVIT & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Illinois General Affidavit Instructions Sample Illinois General Affidavit 1. Overview An affidavit is a sworn written statement that can be used in a

& GUIDE Included: Overview Dos and Don ts Checklist Illinois General Affidavit Instructions Sample Illinois General Affidavit 1. Overview An affidavit is a sworn written statement that can be used in a

TRADEMARK LICENSE AGREEMENT & GUIDELINES

& GUIDELINES Included: Overview Dos and Don ts Checklist Trademark License Agreement Instructions Sample Trademark License Agreement 1. Overview A company s ability to buy and sell property is essential

& GUIDELINES Included: Overview Dos and Don ts Checklist Trademark License Agreement Instructions Sample Trademark License Agreement 1. Overview A company s ability to buy and sell property is essential

LANDLORD S LETTER RETURNING SECURITY DEPOSIT & GUIDE

LANDLORD S LETTER RETURNING SECURITY DEPOSIT & GUIDE Included: Overview Dos and Don ts Checklist Landlord s Letter Returning Security Deposit Instructions Sample Landlord s Letter Returning Security Deposit

LANDLORD S LETTER RETURNING SECURITY DEPOSIT & GUIDE Included: Overview Dos and Don ts Checklist Landlord s Letter Returning Security Deposit Instructions Sample Landlord s Letter Returning Security Deposit

DOMAIN NAME CEASE AND DESIST LETTER & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Domain Name Cease and Desist Letter Instructions Sample Domain Name Cease and Desist Letter 1. Overview You ve started a business, established a brand

& GUIDE Included: Overview Dos and Don ts Checklist Domain Name Cease and Desist Letter Instructions Sample Domain Name Cease and Desist Letter 1. Overview You ve started a business, established a brand

CALIFORNIA GENERAL AFFIDAVIT & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist California General Affidavit Instructions Sample California General Affidavit 1. Overview An affidavit is a sworn written statement that can be used

& GUIDE Included: Overview Dos and Don ts Checklist California General Affidavit Instructions Sample California General Affidavit 1. Overview An affidavit is a sworn written statement that can be used

GENERAL CONTRACTOR AGREEMENT & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist General Contractor Agreement Instructions Sample General Contractor Agreement 1. Overview Hiring a general contractor is a nerve-wracking experience

& GUIDE Included: Overview Dos and Don ts Checklist General Contractor Agreement Instructions Sample General Contractor Agreement 1. Overview Hiring a general contractor is a nerve-wracking experience

EMPLOYMENT OFFER LETTER & GUIDE

Included: Overview Dos and Don ts Checklist General Offer Letter Instructions Model Offer Letter 1. Overview Starting out on the right foot is essential to establishing a productive, successful, and professional

Included: Overview Dos and Don ts Checklist General Offer Letter Instructions Model Offer Letter 1. Overview Starting out on the right foot is essential to establishing a productive, successful, and professional

TRADEMARK CEASE AND DESIST LETTER PACKET

Included: Overview Dos and Don ts Checklist Sample Trademark Cease and Desist Letter 1. Overview You ve started a business, established a brand name, and built up a strong reputation for quality and service.

Included: Overview Dos and Don ts Checklist Sample Trademark Cease and Desist Letter 1. Overview You ve started a business, established a brand name, and built up a strong reputation for quality and service.

CELL PHONE USAGE POLICY & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Cell Phone Usage Policy Instructions Sample Cell Phone Usage Policy 1. Overview Mobile phones, personal digital assistants, and other electronic innovations

& GUIDE Included: Overview Dos and Don ts Checklist Cell Phone Usage Policy Instructions Sample Cell Phone Usage Policy 1. Overview Mobile phones, personal digital assistants, and other electronic innovations

GENERAL CONTRACTOR AGREEMENT (COST PLUS FEE) & GUIDE

& GUIDE") GENERAL CONTRACTOR AGREEMENT (COST PLUS FEE) & GUIDE Included: Overview Dos and Don ts Checklist General Contractor Agreement (Cost Plus Fee) Instructions Sample General Contractor Agreement (Cost Plus

GENERAL CONTRACTOR AGREEMENT (COST PLUS FEE) & GUIDE Included: Overview Dos and Don ts Checklist General Contractor Agreement (Cost Plus Fee) Instructions Sample General Contractor Agreement (Cost Plus

NOTICE OF DISSOLUTION OF PARTNERSHIP (DEBTORS AND CREDITORS) & GUIDE

& GUIDE") NOTICE OF DISSOLUTION OF PARTNERSHIP (DEBTORS AND CREDITORS) & GUIDE Included: Overview Dos and Don ts Checklist Notice of Dissolution of Partnership (Debtors and Creditors) Instructions Sample Notice

NOTICE OF DISSOLUTION OF PARTNERSHIP (DEBTORS AND CREDITORS) & GUIDE Included: Overview Dos and Don ts Checklist Notice of Dissolution of Partnership (Debtors and Creditors) Instructions Sample Notice

EMPLOYEE WRITTEN WARNING & GUIDE

Included: Overview Dos and Don ts Checklist Employee Written Warning Instructions Sample Employee Written Warning 1. Overview Employees are some of the most valuable resources that a company has, and can

Included: Overview Dos and Don ts Checklist Employee Written Warning Instructions Sample Employee Written Warning 1. Overview Employees are some of the most valuable resources that a company has, and can

WORKPLACE INJURY AND ILLNESS INCIDENT REPORT & GUIDE

WORKPLACE INJURY AND ILLNESS INCIDENT REPORT & GUIDE Included: Overview Dos and Don ts Checklist Sample Workplace Injury and Illness Incident Report 1. Overview Employees are some of the most valuable

WORKPLACE INJURY AND ILLNESS INCIDENT REPORT & GUIDE Included: Overview Dos and Don ts Checklist Sample Workplace Injury and Illness Incident Report 1. Overview Employees are some of the most valuable

EMPLOYMENT AGREEMENT & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Employment Agreement Instructions Sample Employment Agreement 1. Overview Having a good start to an employment relationship and making a positive first

& GUIDE Included: Overview Dos and Don ts Checklist Employment Agreement Instructions Sample Employment Agreement 1. Overview Having a good start to an employment relationship and making a positive first

Dealer Registration Package

Dealer Registration Package REQUESTED by: 6 pages ATTENTION: Angela Boots (Dealer Registration) FAX NUMBER: (954)739-3359 EMAIL: dealreg@sflaa.com *****THIS PAGE DOES NOT NEED TO BE FILLED OUT IT IS ONLY

Dealer Registration Package REQUESTED by: 6 pages ATTENTION: Angela Boots (Dealer Registration) FAX NUMBER: (954)739-3359 EMAIL: dealreg@sflaa.com *****THIS PAGE DOES NOT NEED TO BE FILLED OUT IT IS ONLY

THESE FORMS ARE NOT A SUBSTITUTE FOR LEGAL ADVICE.

DISCLAIMER The forms provided on our site were drafted by lawyers with knowledge of equine and contractual matters. However, the forms are not State specific. THESE FORMS ARE NOT A SUBSTITUTE FOR LEGAL

DISCLAIMER The forms provided on our site were drafted by lawyers with knowledge of equine and contractual matters. However, the forms are not State specific. THESE FORMS ARE NOT A SUBSTITUTE FOR LEGAL

Installment Sales and Security Agreement

Installment Sales and Security Agreement This Packet Includes: 1. General Information 2. Instructions and Checklist 3. 1 General Information This is between a buyer and seller of goods which are being

Installment Sales and Security Agreement This Packet Includes: 1. General Information 2. Instructions and Checklist 3. 1 General Information This is between a buyer and seller of goods which are being

Contract for the Sale of Motor Vehicle Owner Financed with Provisions for Note and Security Agreement

Contract for the Sale of Motor Vehicle Owner Financed with Provisions for Note and Security Agreement Agreement made on the (date), between (Name of Buyer) of (street address, city, county, state, zip

Contract for the Sale of Motor Vehicle Owner Financed with Provisions for Note and Security Agreement Agreement made on the (date), between (Name of Buyer) of (street address, city, county, state, zip

New Cars Buying from a Licensed Dealer New Vehicle Warranty Florida s New Car Lemon Law

Buying a car is one of the most important and most expensive decisions most of us have to make. There is certainly no shortage of vehicles available, but buyers must know what to look for, what to ask

Buying a car is one of the most important and most expensive decisions most of us have to make. There is certainly no shortage of vehicles available, but buyers must know what to look for, what to ask

Referral Agency and Packaging Agency Agreement

Referral Agency and Packaging Agency Agreement Please read this agreement carefully. In signing this agreement, you acknowledge that you have read, understood and agree to be bound by each and every provision

Referral Agency and Packaging Agency Agreement Please read this agreement carefully. In signing this agreement, you acknowledge that you have read, understood and agree to be bound by each and every provision

Figure: 7 TAC 84.809(b)

") Figure: 7 TAC 84.809(b) MOTOR VEHICLE RETAIL INSTALLMENT SALES CONTRACT (Optional: DATE ) BUYER SELLER/CREDITOR ADDRESS ADDRESS CITY STATE ZIP CITY STATE ZIP PHONE PHONE The Buyer is referred to as "I"

Figure: 7 TAC 84.809(b) MOTOR VEHICLE RETAIL INSTALLMENT SALES CONTRACT (Optional: DATE ) BUYER SELLER/CREDITOR ADDRESS ADDRESS CITY STATE ZIP CITY STATE ZIP PHONE PHONE The Buyer is referred to as "I"

DRIVING RELATED ISSUES. Student Legal Service University of Illinois at Urbana-Champaign

DRIVING RELATED ISSUES Student Legal Service University of Illinois at Urbana-Champaign License Issues You are not required to obtain an Illinois Driver s license while you are enrolled as a student in

DRIVING RELATED ISSUES Student Legal Service University of Illinois at Urbana-Champaign License Issues You are not required to obtain an Illinois Driver s license while you are enrolled as a student in

SAMPLE LAND CONTRACT

This material is provided to answer general questions about the law in New York State. The information and forms were created to assist readers with general issues and not specific situations, and, as

This material is provided to answer general questions about the law in New York State. The information and forms were created to assist readers with general issues and not specific situations, and, as

One Year Contract Cover Letter & Instructions

One Year Contract Cover Letter & Instructions Thank you for purchasing our yearly search engine optimization services. We have attached our yearly agreement for your review, completion, and execution.

One Year Contract Cover Letter & Instructions Thank you for purchasing our yearly search engine optimization services. We have attached our yearly agreement for your review, completion, and execution.

BUSINESS LETTER OF RECOMMENDATION & GUIDE

& GUIDE Included: Overview Dos and Don ts Checklist Business Letter of Recommendation Instructions Sample Business Letter of Recommendation 1. Overview The modern job market is competitive, and applicants

& GUIDE Included: Overview Dos and Don ts Checklist Business Letter of Recommendation Instructions Sample Business Letter of Recommendation 1. Overview The modern job market is competitive, and applicants

Credit Card Disclosure ACCOUNT OPENING TABLE

Credit Card Disclosure VISA Account Opening Disclosure Effective April 1, 2014 See below for a summary of the rates, fees and other costs of this credit offer. The Card Agreement sent with the card will

Credit Card Disclosure VISA Account Opening Disclosure Effective April 1, 2014 See below for a summary of the rates, fees and other costs of this credit offer. The Card Agreement sent with the card will

BILL OF SALE AND AGREEMENT. THIS BILL OF SALE AND AGREEMENT ( Agreement ) is made and entered into. as of the day of by and between,

is made and entered into. as of the day of by and between,") DISCLAIMER This form is provided by way of example only, and is not intended to replace or supplant advice from an attorney, and does not create any relationship between TOBA, its counsel, and any individual

DISCLAIMER This form is provided by way of example only, and is not intended to replace or supplant advice from an attorney, and does not create any relationship between TOBA, its counsel, and any individual

2A. Investment Objective Definitions. Capital Preservation - a conservative investment strategy characterized by a desire to avoid risk of loss;

CUSTOMER ACCOUNT AGREEMENT This Customer Account Agreement (the Agreement ) sets forth the respective rights and obligations of Apex Clearing Corporation ( you or your or Apex ) and the Customer s (as

CUSTOMER ACCOUNT AGREEMENT This Customer Account Agreement (the Agreement ) sets forth the respective rights and obligations of Apex Clearing Corporation ( you or your or Apex ) and the Customer s (as

CHAPTER 51-13 RETAIL INSTALLMENT SALES ACT

CHAPTER 51-13 RETAIL INSTALLMENT SALES ACT 51-13-01. Definitions. In this chapter, unless the context or subject matter otherwise requires: 1. "Amount financed" or "unpaid balance" means the cash price

CHAPTER 51-13 RETAIL INSTALLMENT SALES ACT 51-13-01. Definitions. In this chapter, unless the context or subject matter otherwise requires: 1. "Amount financed" or "unpaid balance" means the cash price

YORKMONT AUTO AUCTIONS, INC. 799 South Main St. Fair Haven, VT 05743. Office: 802.278.8057 Fax: 802.278.8114. www.yorkmontaa.com

REGISTRATION FORMS YORKMONT AUTO AUCTIONS, INC. 799 South Main St. Fair Haven, VT 05743 Office: 802.278.8057 Fax: 802.278.8114 info@yorkmontaa.com Auction Insurance policy requires all registration forms

REGISTRATION FORMS YORKMONT AUTO AUCTIONS, INC. 799 South Main St. Fair Haven, VT 05743 Office: 802.278.8057 Fax: 802.278.8114 info@yorkmontaa.com Auction Insurance policy requires all registration forms

TERMS AND CONDITIONS

TERMS AND CONDITIONS 1. Definitions. Buyer means the person, corporation or other entity purchasing Products from Seller. Products means all goods and materials to be provided pursuant to this Sales Acknowledgment.

TERMS AND CONDITIONS 1. Definitions. Buyer means the person, corporation or other entity purchasing Products from Seller. Products means all goods and materials to be provided pursuant to this Sales Acknowledgment.

Real Estate Salesman Agreement (Independent Contractor)

") Real Estate Salesman Agreement (Independent Contractor) This Packet Includes: 1. General Information 2. Instructions and Checklist 3. Real Estate Salesman Agreement (Independent Contractor ) 1 General

Real Estate Salesman Agreement (Independent Contractor) This Packet Includes: 1. General Information 2. Instructions and Checklist 3. Real Estate Salesman Agreement (Independent Contractor ) 1 General

Below is an overview of the Molex lease process as it applies to Molex Application Tooling equipment.

Dear Valued Customer, Below is an overview of the Molex lease process as it applies to Molex Application Tooling equipment. Lease process: Molex does not offer leases for all of the equipment that we promote.

Dear Valued Customer, Below is an overview of the Molex lease process as it applies to Molex Application Tooling equipment. Lease process: Molex does not offer leases for all of the equipment that we promote.

Stock Redemption Agreement

Stock Redemption Agreement The Shareholder presently owns [xxx] shares of the issued and outstanding capital stock of the Company. The Shareholder wishes to sell to the Company, and the Company wishes

Stock Redemption Agreement The Shareholder presently owns [xxx] shares of the issued and outstanding capital stock of the Company. The Shareholder wishes to sell to the Company, and the Company wishes

THESE FORMS ARE NOT A SUBSTITUTE FOR LEGAL ADVICE.

DISCLAIMER The forms provided on our site were drafted by lawyers with knowledge of equine and contractual matters. However, the forms are not State specific. THESE FORMS ARE NOT A SUBSTITUTE FOR LEGAL

DISCLAIMER The forms provided on our site were drafted by lawyers with knowledge of equine and contractual matters. However, the forms are not State specific. THESE FORMS ARE NOT A SUBSTITUTE FOR LEGAL

TERMS AND CONDITIONS OF SALE. Quotations, Purchase Orders, Acknowledgements, Packing Lists/Slips, Invoices & Credits

Quotations, Purchase Orders, Acknowledgements, Packing Lists/Slips, Invoices & Credits All quotations of Seller ( Quotations ) and purchase orders of Buyer ( Purchase Orders ) shall be subject to these

Quotations, Purchase Orders, Acknowledgements, Packing Lists/Slips, Invoices & Credits All quotations of Seller ( Quotations ) and purchase orders of Buyer ( Purchase Orders ) shall be subject to these

VIRTUAL OFFICE WEBSITE LICENSE AGREEMENT

Florida Keys Multiple Listing Service, Inc. VIRTUAL OFFICE WEBSITE LICENSE AGREEMENT Florida Keys MLS, Inc. 92410 Overseas Hwy, Ste. 11 Tavernier FL 33070 305-852-92940 305-852-0716 (fax) www.flexmls.com

Florida Keys Multiple Listing Service, Inc. VIRTUAL OFFICE WEBSITE LICENSE AGREEMENT Florida Keys MLS, Inc. 92410 Overseas Hwy, Ste. 11 Tavernier FL 33070 305-852-92940 305-852-0716 (fax) www.flexmls.com

BUSINESS CREDIT AND CONTINUING SECURITY AGREEMENT

BUSINESS CREDIT AND CONTINUING SECURITY AGREEMENT This Business Credit and Continuing Security Agreement ("Agreement") includes this Agreement and may include a Business Credit Agreement Rider and Business

BUSINESS CREDIT AND CONTINUING SECURITY AGREEMENT This Business Credit and Continuing Security Agreement ("Agreement") includes this Agreement and may include a Business Credit Agreement Rider and Business

SELLING TERMS AND CONDITIONS

SELLING TERMS AND CONDITIONS 1. The Agreement. All sales by Sterling Machinery, Inc., an Arkansas corporation (the Seller ) to the purchaser of Seller s Goods (the Buyer ) shall be governed by the following

SELLING TERMS AND CONDITIONS 1. The Agreement. All sales by Sterling Machinery, Inc., an Arkansas corporation (the Seller ) to the purchaser of Seller s Goods (the Buyer ) shall be governed by the following

IMPORTANT: PLEASE READ THE INFORMATION BELOW

3-7 Day Processing IMPORTANT: PLEASE READ THE INFORMATION BELOW COMMERCIAL CREDIT APPLICATION CORLISS RESOURCES, INC. PO BOX 487 SUMNER, WA 98390 PHONE: 253-826-8014 FAX: 253-501-1622 Listed below are

3-7 Day Processing IMPORTANT: PLEASE READ THE INFORMATION BELOW COMMERCIAL CREDIT APPLICATION CORLISS RESOURCES, INC. PO BOX 487 SUMNER, WA 98390 PHONE: 253-826-8014 FAX: 253-501-1622 Listed below are

CUSTOMER LIST PURCHASE AGREEMENT BY AND BETWEEN RICHARD PENNER SELLER. and S&W SEED COMPANY BUYER

EXHIBIT 10.1 CUSTOMER LIST PURCHASE AGREEMENT BY AND BETWEEN RICHARD PENNER as SELLER and S&W SEED COMPANY as BUYER CUSTOMER LIST PURCHASE AGREEMENT THIS CUSTOMER LIST PURCHASE AGREEMENT ( Agreement )

EXHIBIT 10.1 CUSTOMER LIST PURCHASE AGREEMENT BY AND BETWEEN RICHARD PENNER as SELLER and S&W SEED COMPANY as BUYER CUSTOMER LIST PURCHASE AGREEMENT THIS CUSTOMER LIST PURCHASE AGREEMENT ( Agreement )

First Technology Federal Credit Union Visa Platinum Credit Card Agreement and Federal Truth-in-Lending Disclosure Statement

In this ( Agreement and Disclosure Statement ) the words: I, me, my and mine mean any and all of those who apply for or use the Visa Platinum Credit Card. First Tech, you, your and yours mean. Card means

In this ( Agreement and Disclosure Statement ) the words: I, me, my and mine mean any and all of those who apply for or use the Visa Platinum Credit Card. First Tech, you, your and yours mean. Card means

BUSINESS CASH RESERVE AGREEMENT Effective: January 1, 2016

BUSINESS CASH RESERVE AGREEMENT Effective: January 1, 2016 This Business Cash Reserve Agreement ("Cash Reserve Agreement"), Borrower's Application for Business Cash Reserve (Business Overdraft Protection),

BUSINESS CASH RESERVE AGREEMENT Effective: January 1, 2016 This Business Cash Reserve Agreement ("Cash Reserve Agreement"), Borrower's Application for Business Cash Reserve (Business Overdraft Protection),

Return completed applications to: APAC-Texas, Inc. P.O. Box 20779 Beaumont, TX 77720 (409) 866-1444 Phone (409) 866-5541 Fax

866-1444 Phone (409) 866-5541 Fax") Return completed applications to: APAC-Texas, Inc. P.O. Box 20779 Beaumont, TX 77720 (409) 866-1444 Phone (409) 866-5541 Fax APPLICATION FOR BUSINESS CREDIT Date: NOTE: This application for Business Credit

Return completed applications to: APAC-Texas, Inc. P.O. Box 20779 Beaumont, TX 77720 (409) 866-1444 Phone (409) 866-5541 Fax APPLICATION FOR BUSINESS CREDIT Date: NOTE: This application for Business Credit

All About Autos. New Cars, Used Cars, and Repairs

New Cars, Used Cars, and Repairs Table of Contents Introduction...2 New Cars Lemon Law...4 The Importance of Car Titles...6 Used Cars As Is: No Warranty...7 Warranty...7 Online Car Auctions...9 Odometer

New Cars, Used Cars, and Repairs Table of Contents Introduction...2 New Cars Lemon Law...4 The Importance of Car Titles...6 Used Cars As Is: No Warranty...7 Warranty...7 Online Car Auctions...9 Odometer

SAMPLE RETURN POLICY

DISCLAIMER The sample documents below are provided for general information purposes only. Your use of any of these sample documents is at your own risk, and you should not use any of these sample documents

DISCLAIMER The sample documents below are provided for general information purposes only. Your use of any of these sample documents is at your own risk, and you should not use any of these sample documents

"Owner" "Designer" 1. Description of the Services. "Website" Schedule A "Services" 2. Design Team. "Design Team" 3. Term / Scheduling.

The following outlines the terms of service by and between the CLIENT (the "Owner") and Made Right Media (the "Designer"), of 720 W. Idaho St. #32, Boise, Idaho 83702. 1. Description of the Services. The

The following outlines the terms of service by and between the CLIENT (the "Owner") and Made Right Media (the "Designer"), of 720 W. Idaho St. #32, Boise, Idaho 83702. 1. Description of the Services. The

330-492-3090. Be The First On Your Block To Understand Title Insurance

330-492-3090 Be The First On Your Block To Understand Title Insurance UNLESS YOU MAKE A HABIT OF BUYING A HOME EVERY YEAR chances are you re not too familiar with the topic of title insurance. You re not

330-492-3090 Be The First On Your Block To Understand Title Insurance UNLESS YOU MAKE A HABIT OF BUYING A HOME EVERY YEAR chances are you re not too familiar with the topic of title insurance. You re not

CALIFORNIA LEMON LAW SUMMARY

CALIFORNIA LEMON LAW SUMMARY 1. Citation Song-Beverly Consumer Warranty Act, Cal. Civil Code 1790-1795.7; Tanner Consumer Protection Act, 1793.22; Cal. Business and Professions Code 472-472.5; 16 Cal.

CALIFORNIA LEMON LAW SUMMARY 1. Citation Song-Beverly Consumer Warranty Act, Cal. Civil Code 1790-1795.7; Tanner Consumer Protection Act, 1793.22; Cal. Business and Professions Code 472-472.5; 16 Cal.

This AGREEMENT is made as of the day of in the year of, by and between the following parties, for the sale of materials.

MCPU Standard Contract 101 Agreement Between Seller and Buyer For Sale on Credit This document has important legal consequences. Consultation with an attorney is recommended with respect to its completion,

MCPU Standard Contract 101 Agreement Between Seller and Buyer For Sale on Credit This document has important legal consequences. Consultation with an attorney is recommended with respect to its completion,

Appendix B Sample Contract for Deed. This Agreement, made this day of, between, called Seller,

Appendix B Sample Contract for Deed This Agreement, made this day of, between, called Seller, whose address is [NUMBER AND STREET] [CITY] [STATE] [ZIP], and, called Buyer, whose address is [NUMBER AND

Appendix B Sample Contract for Deed This Agreement, made this day of, between, called Seller, whose address is [NUMBER AND STREET] [CITY] [STATE] [ZIP], and, called Buyer, whose address is [NUMBER AND

CSI MasterCard Corporate Fleet Card

CSI MasterCard Corporate Fleet Card Accepted Everywhere Your Fleet Operates CSI MasterCard Corporate Fleet Card For BlueVend Car Wash Merchants Program Guidelines/Client Benefits: Reduced Monthly Card

CSI MasterCard Corporate Fleet Card Accepted Everywhere Your Fleet Operates CSI MasterCard Corporate Fleet Card For BlueVend Car Wash Merchants Program Guidelines/Client Benefits: Reduced Monthly Card

Promissory Note Comparison Guide

Borrowing from or lending money to a friend or colleague is a sensitive situation. A lender wants to be sure money is returned on a timely basis. A borrower wants enough time to repay the amounts and some

Borrowing from or lending money to a friend or colleague is a sensitive situation. A lender wants to be sure money is returned on a timely basis. A borrower wants enough time to repay the amounts and some

Dealer Registration. Please provide the following:

Dealer Registration Please provide the following: A copy of your Dealer s License A copy of your Sales Tax Certificate A copy of the Driver s License for all representatives A copy of your Master Tag Receipt

Dealer Registration Please provide the following: A copy of your Dealer s License A copy of your Sales Tax Certificate A copy of the Driver s License for all representatives A copy of your Master Tag Receipt

TCU VISA Platinum Rewards Credit Card Account Agreement

TCU VISA Platinum Rewards Credit Card Account Agreement This TCU VISA Platinum Rewards Credit Card Account Agreement and Disclosure Statement ("Agreement"), sets forth your rights and obligations and ours

TCU VISA Platinum Rewards Credit Card Account Agreement This TCU VISA Platinum Rewards Credit Card Account Agreement and Disclosure Statement ("Agreement"), sets forth your rights and obligations and ours

TERMS AND CONDITIONS

TERMS AND CONDITIONS THIS AGREEMENT IS FOR THE RENTAL OF ALL ITEMS, EQUIPMENT AND/OR VEHICLES SHOWN ON THE OTHER SIDE THIS PAGE, INCLUDING ALL PARTS OF AND ACCESSORIES TO SUCH ( EQUIPMENT ). 1. RENTAL

TERMS AND CONDITIONS THIS AGREEMENT IS FOR THE RENTAL OF ALL ITEMS, EQUIPMENT AND/OR VEHICLES SHOWN ON THE OTHER SIDE THIS PAGE, INCLUDING ALL PARTS OF AND ACCESSORIES TO SUCH ( EQUIPMENT ). 1. RENTAL

28. Time is of the essence in this Lease and in each and all of its provisions.

COMMERCIAL VEHICLE/EQUIPMENT LEASE AGREEMENT Please print and fax to: 281-842-9345 Stutes Enterprise Systems, Inc. ("Lessor"), located at 1426 Sens Rd #5, LaPorte, Texas 77571, leases to, ("Lessee"), located

COMMERCIAL VEHICLE/EQUIPMENT LEASE AGREEMENT Please print and fax to: 281-842-9345 Stutes Enterprise Systems, Inc. ("Lessor"), located at 1426 Sens Rd #5, LaPorte, Texas 77571, leases to, ("Lessee"), located

Advantage Education Loan Promissory Note

Promissory Note with Kentucky Higher Education Student Loan Corporation in Louisville, KY In this Promissory Note ( Note ) the words I, me, my, and we mean the borrower and cosigner(s) who have signed

Promissory Note with Kentucky Higher Education Student Loan Corporation in Louisville, KY In this Promissory Note ( Note ) the words I, me, my, and we mean the borrower and cosigner(s) who have signed

INTERNET BANKING SERVICES AGREEMENT

INTERNET BANKING SERVICES AGREEMENT THIS AGREEMENT sets out the terms on which the undersigned ( you ) may obtain services from Provident State Bank (the Bank ) using the internet. 1. Internet Services;

INTERNET BANKING SERVICES AGREEMENT THIS AGREEMENT sets out the terms on which the undersigned ( you ) may obtain services from Provident State Bank (the Bank ) using the internet. 1. Internet Services;

MASTER DEALER AGREEMENT

MASTER DEALER AGREEMENT DATE: PARTIES: Finco Holding Corp. (dba The Equitable Finance Company) 4124 SE 82 nd Ave Suite 650 Portland, OR 97266 ( Company ) ( Dealer ) AGREEMENT: IN CONSIDERATION, of the

MASTER DEALER AGREEMENT DATE: PARTIES: Finco Holding Corp. (dba The Equitable Finance Company) 4124 SE 82 nd Ave Suite 650 Portland, OR 97266 ( Company ) ( Dealer ) AGREEMENT: IN CONSIDERATION, of the

MASTERCARD CONSUMER CREDIT CARD AGREEMENT

MASTERCARD CONSUMER CREDIT CARD AGREEMENT In this Agreement, Agreement means this Consumer Credit Card Agreement. Disclosure means the Credit Card Account Opening Disclosure. The Account Opening Disclosure

MASTERCARD CONSUMER CREDIT CARD AGREEMENT In this Agreement, Agreement means this Consumer Credit Card Agreement. Disclosure means the Credit Card Account Opening Disclosure. The Account Opening Disclosure

Collecting Your Judgment: A Step-By-Step Approach

Collecting Your Judgment: A Step-By-Step Approach YOUR LEGAL RIGHTS Employees who win money judgments against their employers often need help collecting those judgments on their own or in court. This packet

Collecting Your Judgment: A Step-By-Step Approach YOUR LEGAL RIGHTS Employees who win money judgments against their employers often need help collecting those judgments on their own or in court. This packet

Missouri Bank Business Credit Card Agreement

Missouri Bank Business Credit Card Agreement THIS BUSINESS CREDIT CARD AGREEMENT ( AGREEMENT ) CONTAINS THE TERMS WHICH GOVERN THE USE OF YOUR MOBANK VISA BUSINESS CREDIT CARD ( CARD ) AND CORRESPONDING

Missouri Bank Business Credit Card Agreement THIS BUSINESS CREDIT CARD AGREEMENT ( AGREEMENT ) CONTAINS THE TERMS WHICH GOVERN THE USE OF YOUR MOBANK VISA BUSINESS CREDIT CARD ( CARD ) AND CORRESPONDING

By placing an order with International Checkout Inc. and / or using its website, you agree and are bound to the Terms & Conditions below.

By placing an order with International Checkout Inc. and / or using its website, you agree and are bound to the Terms & Conditions below. 1. How It Works International Checkout Inc. ( we / us ) has agreements

By placing an order with International Checkout Inc. and / or using its website, you agree and are bound to the Terms & Conditions below. 1. How It Works International Checkout Inc. ( we / us ) has agreements

Loan Agreement (Short Form)

") Loan Agreement (Short Form) Document 2050A Access to this document and the LeapLaw web site is provided with the understanding that neither LeapLaw Inc. nor any of the providers of information that appear

Loan Agreement (Short Form) Document 2050A Access to this document and the LeapLaw web site is provided with the understanding that neither LeapLaw Inc. nor any of the providers of information that appear

13.75% VISA CLASSIC 12.75% VISA GOLD

Account Opening Disclosure Notice regarding the terms of your West Suburban Bank Visa Credit Card account. Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases 13.75% VISA CLASSIC

Account Opening Disclosure Notice regarding the terms of your West Suburban Bank Visa Credit Card account. Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases 13.75% VISA CLASSIC

VISA PLATINUM CONSUMER CREDIT CARD AGREEMENT

In this Agreement, Agreement means this Consumer Credit Card Agreement. Disclosure means the Visa Credit Card Rates and Terms disclosure. The Fee Schedule means the Consumer Services Fee Schedule. The

In this Agreement, Agreement means this Consumer Credit Card Agreement. Disclosure means the Visa Credit Card Rates and Terms disclosure. The Fee Schedule means the Consumer Services Fee Schedule. The

FOR SALE_ By South Carolina Department of Transportation

FOR SALE_ By South Carolina Department of Transportation Approximately 10.21 Acres and Improvements Offered at $2,540,000.00 Includes five vacant office buildings @ 1439 Laurens Road, Greenville, SC 29607

FOR SALE_ By South Carolina Department of Transportation Approximately 10.21 Acres and Improvements Offered at $2,540,000.00 Includes five vacant office buildings @ 1439 Laurens Road, Greenville, SC 29607

DEALER FUNDING CHECKLIST Effective 10/15/14 PLEASE NOTE: ALL PAPERWORK SHOULD BE ASSIGNED TO PELICAN AUTO FINANCE, LLC Original Approval Sheet

DEALER FUNDING CHECKLIST Effective 10/15/14 PLEASE NOTE: ALL PAPERWORK SHOULD BE ASSIGNED TO PELICAN AUTO FINANCE, LLC Original Approval Sheet o Amount financed on Approval must be within $25 of contracted

DEALER FUNDING CHECKLIST Effective 10/15/14 PLEASE NOTE: ALL PAPERWORK SHOULD BE ASSIGNED TO PELICAN AUTO FINANCE, LLC Original Approval Sheet o Amount financed on Approval must be within $25 of contracted

WHAT IS TITLE INSURANCE?

WHAT IS TITLE INSURANCE? A title is the collective ownership records of a piece of real estate, including the transfer of any property rights and any loans using the property as collateral. A clear line

WHAT IS TITLE INSURANCE? A title is the collective ownership records of a piece of real estate, including the transfer of any property rights and any loans using the property as collateral. A clear line

ELKHART COUNTY BOARD OF REALTORS AND MULTIPLE LISTING SERVICE OF ELKHART COUNTY INC. VIRTUAL OFFICE WEBSITE (VOW) LICENSE AGREEMENT

LICENSE AGREEMENT") ELKHART COUNTY BOARD OF REALTORS AND MULTIPLE LISTING SERVICE OF ELKHART COUNTY INC. VIRTUAL OFFICE WEBSITE (VOW) LICENSE AGREEMENT This License Agreement (the Agreement) is made and entered into between

ELKHART COUNTY BOARD OF REALTORS AND MULTIPLE LISTING SERVICE OF ELKHART COUNTY INC. VIRTUAL OFFICE WEBSITE (VOW) LICENSE AGREEMENT This License Agreement (the Agreement) is made and entered into between

visa platinum and visa secured Fax: (786) 845-3150 www.dcfcu.org

845-3150 www.dcfcu.org") Dade County Federal Credit Union 1500 NW 107th Ave Doral, FL 33172 (305) 471-5080 (800) 299-7147 visa platinum and visa secured Fax: (786) 845-3150 www.dcfcu.org consumer credit card agreement In this

Dade County Federal Credit Union 1500 NW 107th Ave Doral, FL 33172 (305) 471-5080 (800) 299-7147 visa platinum and visa secured Fax: (786) 845-3150 www.dcfcu.org consumer credit card agreement In this

VISA: % This APR will vary with the market based on the Prime Rate. VISA Gold: % This APR will vary with the market based on the Prime Rate.

KEMBA CREDIT UNION, INC P O BOX 14090 CINCINNATI, OH 45250 (800) 825-3622 FAX (513) 762-1619 (513) 762-5070 CREDIT CARD AGREEMENT AND FEDERAL DISCLOSURE STATEMENT THIS IS YOUR CREDIT CARD AGREEMENT AND

KEMBA CREDIT UNION, INC P O BOX 14090 CINCINNATI, OH 45250 (800) 825-3622 FAX (513) 762-1619 (513) 762-5070 CREDIT CARD AGREEMENT AND FEDERAL DISCLOSURE STATEMENT THIS IS YOUR CREDIT CARD AGREEMENT AND

MODULAR HOME PURCHASE & CONSTRUCTION AGREEMENT

This document has been prepared as an aid to retailers selling a modular home for placement on the customer s land. We would like to remind you this is a general form and will need to be amended to fit

This document has been prepared as an aid to retailers selling a modular home for placement on the customer s land. We would like to remind you this is a general form and will need to be amended to fit

VISA CREDIT CARD AGREEMENT AND TRUTH IN LENDING DISCLOSURE

Annual Percentage Rates (APRs) for purchases APR for Balance Transfers APR for Cash Advances Penalty APR and When It Applies Paying Interest For Credit Card Tips from the Federal Reserve Board VISA CREDIT

Annual Percentage Rates (APRs) for purchases APR for Balance Transfers APR for Cash Advances Penalty APR and When It Applies Paying Interest For Credit Card Tips from the Federal Reserve Board VISA CREDIT

Web Site Development Agreement

Web Site Development Agreement 1. Parties; Effective Date. This Web Site Development Agreement ( Agreement ) is between Plug-N-Run, its affiliates, (including but not limited to USA Financial, USA Financial

Web Site Development Agreement 1. Parties; Effective Date. This Web Site Development Agreement ( Agreement ) is between Plug-N-Run, its affiliates, (including but not limited to USA Financial, USA Financial