THE LATEST IN APPRAISING AND LENDING ON GREEN BUILDINGS. Dave Porter, PorterWorks, Inc.

|

|

|

- Laureen Fields

- 8 years ago

- Views:

Transcription

1 THE LATEST IN APPRAISING AND LENDING ON GREEN BUILDINGS Dave Porter,

2 The National Association of Home Builders is a Registered Provider with The American Institute of Architects Continuing Education Systems. Credit earned on completion of this program will be reported to CES Records for AIA members. Certificates of Completion for non-aia members are available on request. This program is registered with the AIA/CES for continuing professional education. As such, it does not include content that may be deemed or construed to be an approval or endorsement by the AIA of any material of construction or any method or manner of handling, using, distributing, or dealing in any material or product. Questions related to specific materials, methods, and services will be addressed at the conclusion of this presentation. 2

3 Copyright Materials This presentation is protected by US and International Copyright laws. Reproduction, distribution, display and use of the presentation without written permission of the speaker is prohibited. PorterWorks, Inc

4 Learning Objectives 4 AS A RESULT OF ATTENDING THIS SESSION, THE PARTICIPANT WILL BE ABLE TO: Provide an overview of the greening of the MLS List 2 tools for appraising green buildings Define appraiser competency Outline key differences of EIMs and EEMs List key points for different EEMs: VA, FHA, CONV Establish personal action items

5 Quick Check-In 5 Who s Here? Have you (or your buyers) ever been offered an EEM/EIM? Has an appraiser ever asked for more details about energy efficient improvements or green features? Have you (or your buyers) ever been offered an incentive (lower rate or reduced costs) by the lender because the property is green or energy efficient?

ever been offered an incentive (lower rate or reduced")

6 We know this but 6 Buildings Account for 76% of energy produced by coal plants 72% of electricity consumption 39% of energy use 38% of all carbon dioxide (CO 2 ) emissions 40% of raw materials use 30% of waste output (136 million tons annually) 14% of potable water consumption

14% of potable water")

7 Does an Appraiser know it? Or This? 7 TYPICAL ENERGY LEAKS Floors, walls, ceilings 31% Ducts 15% Fireplace 14% Plumbing penetrations 13% Doors 11% Windows 10% Fans and vents 4% Electrical penetrations 2%

8 What is seen? What is Missed? 8 What is seen? What is missed? 170 sq. inches of hole exist between the garage and home!

9 Competency 9 A lender must not assume that the appraiser is qualified and knowledgeable about a market area aware of the appropriate market data sources for the area able to obtain access to market data sources Source: Fannie Mae Seller Servicer Guide

10 Ignorance is Not Bliss 10 Appraisers know nothing about this [green building] and it s shocking. ---John O Dwyer, MAI, JSO Valuation Group Don t wait until green building is the prevailing practice before getting familiar with it. Don t wait for all the data to be in before getting up to speed. ----Theddi Wright Chappell, MAI, Cushman & Wakefield

11 AMC s & Underwriters 11 HVCC has transferred the problem to these appraisal management companies, which are not regulated by anybody. Sometimes underwriters tinker with appraisal In both cases, a lack of training particularly in green building creates havoc

12 Residential Energy Report Form 12 Source: Fannie Mae

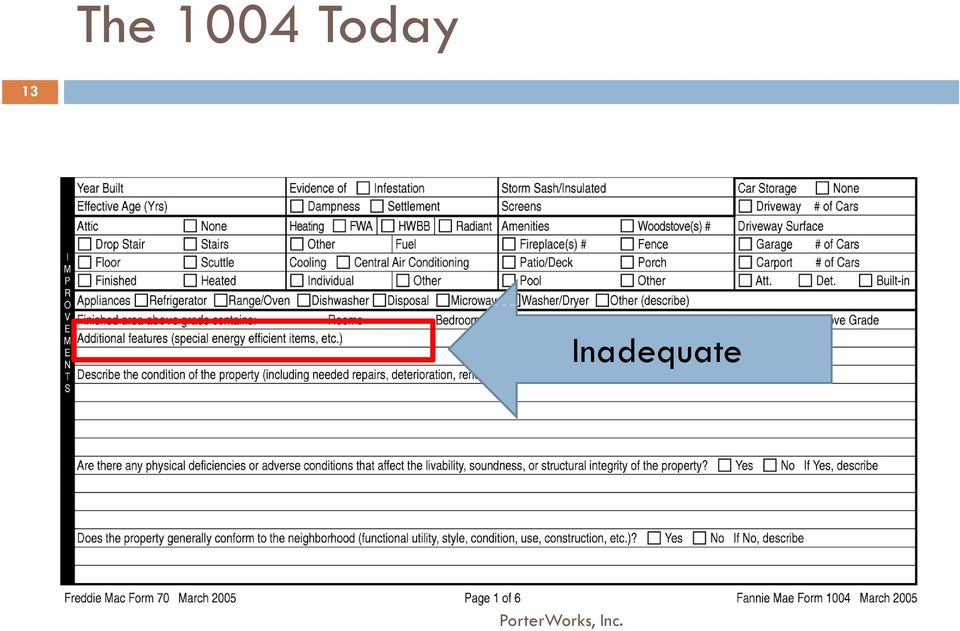

13 The 1004 Today 13 Inadequate

14 Filling in the Gaps 14 Source: EPA

15 Cost Premium Statistics 15 Cost premium of green retrofit project relative to a conventional (non-green) retrofit project 25% 38% 5-10% 1-5% Over 10% 37% Source: Delloitte and Lockwood, Dollars and Sense of Green Retrofitting

16 Sales Comparison Approach 16 All closed & verified comparable sales to be within 6 months (90 days in this current market) No further in distance than 1 mile Similar comparable sales with matching components as well as all single line-item adjustments not to exceed 10% Net adjustments not to exceed 15% and gross adjustments not to exceed 25%. Macro Comps?

17 Marshall & Swift 17 Green Building Costs Brief tutorial on green building New and Retrofit Line item adjustments Recently added 1500 items to the green cost guide Source: Marshall & Swift

18 Marshall & Swift Example 18 Equation for one kind of green component= Dollar/sq ft (e.g. reflective rubberized white roof coating) x number of sq ft x current cost multiplier x local multiplier $.64/sq ft x 5,000 sq ft x 1.0 x 1.05= $3,360 Current cost multiplier and local multiplier are assumed in this examples

19 The Green MLS Tool Kit 19

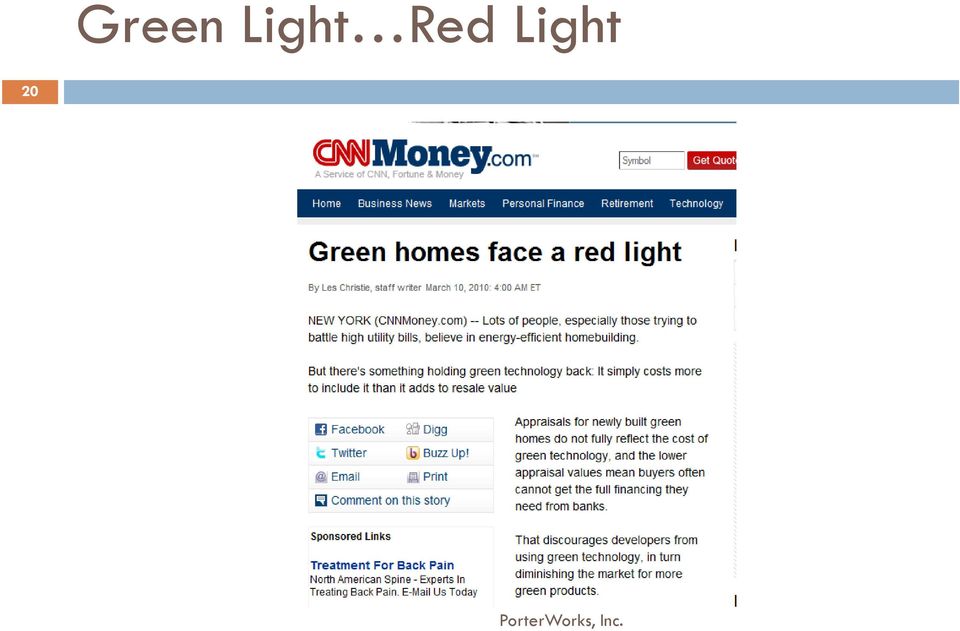

20 Green Light Red Light 20

21 Guarantees: How do you value? 21 The Energy Cost Savings Guarantee is backed by Bayer Material Science.

22 Could/should know the difference? 22 Induction Stove Tops Grid-tied appliances Photos Compliments: Whirlpool

23 PITIUM: Rethinking Lending 23 OPTION ONE Purchase Price $250,000 Down payment $ 50,000 Loan Amount $200,000 Interest 5.85% Monthly PITI $ 1,757 Average Electric $ 150 Total Expenses $ 1,907 OPTION TWO Purchase Price $253,000 New Appraisal $255,000 Down payment $ 50,600 Loan Amount $202,400 Interest 5.85% Monthly PITI $ 1,778 Average Electric $ 60 Total Expenses $ 1,838 Savings $ 69 Source: FNMA

24 EEM Programs 24 FHA VA Rural Housing Fannie Mae Freddie Mac DEMAND THESE PROGRAMS ARE OFFERED DEMAND LENDERS KNOW THESE PROGRAMS

25 EEM s & EIM s 25 EEM s (Energy Efficient Mortgages) provide additional qualifying income credits to help offset the costs of purchasing an energy efficient home. EIM s (Energy Improvement Mortgages) allow for energy improvements to be made to existing homes so that the monthly energy savings pay for the cost of the energy improvements. RICK NEVINS APPRAISAL JOURNAL ARTICLE 1999 $1 IN ANNUAL ENERGY SAVINGS = $20 TO VALUE

26 EEM Process 26 Lender offers/ Consumer indicates interest in EEM (purchase or refinance) HERS or similar home rating is ordered indicating work needed Lender completes worksheet to determine amount available to borrower for improvements Work is completed; funds dispersed to contractors The costs are escrowed; loan closes. Borrower selects the Improvements he/she wants to include

27 EEM/EIM Program The Builder constructs home that can meet HERS rating requirements or the rater provides a list of recommended energy efficiency actions. The RESNET website can assist with these details: 2. A Certified Energy Rater rates home, then provides a report with estimated monthly energy savings and the energy value of the energy efficient measures. 3. The Lender uses monthly energy savings as a credit toward borrower income during loan underwriting. In addition, the energy value is added to the appraised value of the home. How this credit is used depends on the loan program.

28 The Languishing EEM 28 EEMs/EIMs have not been viable mostly because: Lenders, Realtors & Builders have not been aware of the program Those who knew about it simply don t (didn t) care There are not enough certified Raters There is a general perception that the process is too complicated Most folks in the industry don t (didn t) see the value However now with the normalization of lending we are seeing a resurgence of interest in the EEM.

29 FHA EEM Calculator 29

30 HUD EEM Worksheet, Cont. 30 Step Two: Adding the Cost of Energy Efficient Items to the Mortgage Amount 1.If the borrower is an acceptable credit risk for the mortgage amount requested before adding the cost of the energy efficient items, complete the EE Premium Worksheet (page 3) for each eligible improvement to determine if the cost of the energy efficient improvements may be added to the mortgage amount. Total EE Premium $ (from Page 3) 2. Installed Cost $ Compare EE Premium $ to Installed Cost $

31 HUD Challenge 31 Recovery Reform Act Section 2902 of the new act requires the Secretary of Housing and Urban Development (HUD) to develop recommendations to eliminate the barriers to the use of EEMs The act also calls for HUD to carry out an education and outreach campaign for consumers, home builders, residential lenders, and other real estate professionals on EEMs and on the benefits of energy efficiency in housing.

32 FHA EEM/EIM Energy improvement help homebuyers or homeowners save money on utility bills 2. Cost of energy improvements and estimate of energy savings must be determined by home energy rating system (HERS ) or energy consultant 3. HERS report & FHA EEM/EIM worksheet calculates dollar $$ amount of cost effective energy package that may be added to base loan.

33 FHA EEM/EIM Cost effective =total cost of the improvements + maintenance < total present value of the energy saved 2. The cost of the energy efficient improvements that may be eligible for financing into the mortgage 3. The appraisal does not need to reflect the value of the energy added package for either new or existing construction. 4. Stretched ratios to 33/45.

34 HUD Web Site 34

35 Green Loan? FHA 203K 35 Standard Program No reserves are required (except for 3-4 unit properties) 203K closest thing to a true green loan Financing contributions are allowed up to 6% of the property's sales price toward the buyer's actual closing costs, prepaid expenses, or discount points No minimum credit score (borrower's overall pattern of payment is considered) Non-Occupant co-borrowers are allowed 203(k) loans are assumable DTI generally 31/43% (up to allowed 33/45% with Energy Efficient mortgages) Full/Alt doc

36 FHA 203K 36 Standard Program, cont. 6 month rehabilitation period (work must begin within 30 days of funding) UFMIP and monthly mortgage insurance are required Premium pricing is allowed Streamline Program 1.5% additional fee on the improvement 35,000 cap on cost of improvements As is appraisal and contractors bid on the work Streamline Up to $35,000 Faster escrow and approval process Purchase and Refinance Great way to go green

37 VA 37 Energy efficiency improvements up to $3,000 Energy efficiency improvements more than $3,000, up to $6,000 Energy efficiency improvements over $6,000 A VA Certificate of Commitment issued before the decision to make energy efficiency improvements over $6,000 must be returned to VA for a determination that the applicant still qualifies.

38 Energy Improvements for VA 38 THE CONDITIONS/REQUIREMENTS CHECKED BELOW APPLY TO THIS PROPERTY: Lenders may increase the loan 1. ENERGY CONSERVATION IMPROVEMENTS. You may amount [for] energy efficiency wish Solar to contact or conventional the utility heating/cooling company or a reputable firm for a home improvements energy systems, audit water to identify heaters, insulation, needed weatherstripping/caulking occupied and storm property. Lenders needed may increase energy efficiency the loan amount windows/doors. to allow buyers to make energy efficiency improvements improvements energy efficiency.energy audit improvements to identify to this previously such as: Solar or conventional heating/cooling systems, water heaters, insulation, weather-stripping/caulking and storm windows/doors. Other energy-related improvements may also be considered. The mortgage may be increased by up to $3,000 based solely on documented costs; or up to $6,000 provided the increase in monthly mortgage payment does not exceed the likely reduction in monthly utility costs; or more than $6,000 subject to a value determination by VA.

39 Rural Housing 39

40 Fannie Mae 40 Today 15% of value (not supported by appraisal) EEM fee financeable Works within Delegated Underwriting platform Fixed Rates Savings added to income Tomorrow?

41 News Worthy? 41 On Fannie Mae, from NY Times Fannie Mae [ ] said that by this summer it would unveil incentives for those who use part of their mortgages for energyrelated improvements Amy Bonitanibus, a spokeswoman for Fannie Mae, said the company would introduce a program before the summer offering incentives to borrowers Ms. Bonitanibus declined to disclose details about the program.

42 Fannie Mae EEM 42 One-unit SFR, Condo and PUDs with qualifying Energy Rating. Owner-occupied primary residence, purchase or rate & term refinance. Used with fixed-rate only programs. Income must be input in the "Other Income" field with a description of Energy Efficient Mortgage No first-time home buyer education requirement, specifically related to EEM, or restrictions on borrower s maximum income Home buyer assistance programs that assist with down payment and closing costs can be used in conjunction with the EEM program.

43 Energy Report And Addendum 43

44 Freddie Mac 44 No maximum amount the income to expense ratios may be extended due to energy efficiency Permits the purchase of a property that is to be retrofitted, refurbished or improved with energy efficient components. The cost of the energy efficient improvements may be included in the mortgage delivered to Freddie Mac prior to completion of the improvements. Energy efficient items should be noted on the appraisal in the comments section and included in the value as appropriate for the property and location.

45 45 PACE (Property Assessed Clean Energy) System for financing home solar energy systems and energy efficiency improvements Partners with a city or municipality Adds cost of solar systems or improvements onto the homeowner s property tax bill Amortized over twenty years Source:

46 Smart Commute Program 46 The Smart Commute Initiative assumes that borrowers will be more likely to use public transit if their homes are located near it. $ per month where only one borrower's income is used to qualify for the mortgage. $ per month where the income of more than one borrower is used to qualify for the mortgage. Requires that the borrower submit an affidavit Use the GeoCoder on the Fannie website This program is not available in all metro areas. The future? Tied with

47 Incentives: Don t they impact value? 47

48 Education 48 The key to recognizing and accurately valuing energy efficient, sustainable homes lies in educating consumers, real estate brokers, and the appraiser and lending communities. --Dan Weldon, LEED AP, Vice President and Eco-banking Manager, Umpqua Bank (Emphasis added)

49 Education Is Key 49 GreenLending Specialist GreenValuation Specialist GreenInsurance Specialist GreenRealEstate Specialist Green Specialist: CA, OR, WA, AZ, NV, CO, TX, NY, LA, WI Approved in: WA, OR, CA, NV, AZ, LA, PA, DC, NC

50 links

51 51

52 Action Items 52 Get Financing Form on all HERS Ratings Get your MLS to Go Green Local Builder Assoc and Realtor Assoc to Help Have your lenders provide information to the appraisers by way of the Underwriter and Appraisal Management Company (AMC) Have your lenders present to you details on EEMs (this will force them to learn about it) Prepare detailed information packages for appraisers Support legislation

53 Thanks For Your Time 53 This presentation: This concludes The American Institute of Architects Continuing Education Systems Program Dave Porter MIRM, CGP, CGA, CAPS, GLS

ENERGY EFFICENCY IN THE HOME BUYING PROCESS. October 16 th 2014

ENERGY EFFICENCY IN THE HOME BUYING PROCESS October 16 th 2014 Today s Presenters Shannon Peer Brothers Redevelopment / Colorado Housing Connects Peter Rusin Colorado Energy Office Kate Gregory Environmental

ENERGY EFFICENCY IN THE HOME BUYING PROCESS October 16 th 2014 Today s Presenters Shannon Peer Brothers Redevelopment / Colorado Housing Connects Peter Rusin Colorado Energy Office Kate Gregory Environmental

How to Finance an Energy-Efficient Home

U ENERGY EFFICIENCY AND RENEWABLE ENERGY CLEARINGHOUSE Financing an Energy-Efficient Home The average homeowner spends close to $1,300 a year on utility bills. But an energy-efficient home with such features

U ENERGY EFFICIENCY AND RENEWABLE ENERGY CLEARINGHOUSE Financing an Energy-Efficient Home The average homeowner spends close to $1,300 a year on utility bills. But an energy-efficient home with such features

Energy Efficient Mortgages & HERS Ratings. Peter V. Vargo Nu-Tech Energy Solutions, Co LLC

Energy Efficient Mortgages & HERS Ratings Peter V. Vargo Nu-Tech Energy Solutions, Co LLC PA Housing & Land Development Conference February 20, 2013 Energy Efficient Mortgages & HERS Ratings Peter V. Vargo

Energy Efficient Mortgages & HERS Ratings Peter V. Vargo Nu-Tech Energy Solutions, Co LLC PA Housing & Land Development Conference February 20, 2013 Energy Efficient Mortgages & HERS Ratings Peter V. Vargo

FHA 203(k) Rehabilitation Loans

Rehabilitation Loans") Everything You Need to Know About FHA 203(k) Rehabilitation Loans Presented April 10, 2009 Senior Loan Officer, FHA Consultant Bill@YourFhaGuru.com http://www.yourfhaguru.com FHA/VA Since 1970 CLASS TOPICS

Everything You Need to Know About FHA 203(k) Rehabilitation Loans Presented April 10, 2009 Senior Loan Officer, FHA Consultant Bill@YourFhaGuru.com http://www.yourfhaguru.com FHA/VA Since 1970 CLASS TOPICS

California Home Finance Authority (CHF)

") Presentation for Real Estate Professionals California Home Finance Authority (CHF) 1215 K Street, Suite 1650, Sacramento, CA 95814 www.chfloan.org (855) 740-8422 Often first point of contact for a new

Presentation for Real Estate Professionals California Home Finance Authority (CHF) 1215 K Street, Suite 1650, Sacramento, CA 95814 www.chfloan.org (855) 740-8422 Often first point of contact for a new

Introduction to the Fannie Mae HomeStyle Renovation Mortgage. Presented by Damon Richardson, Program Specialist - American Financial Resources, Inc.

Introduction to the Fannie Mae HomeStyle Renovation Mortgage Presented by Damon Richardson, Program Specialist - American Financial Resources, Inc. About the Presenter With 12 years of mortgage industry

Introduction to the Fannie Mae HomeStyle Renovation Mortgage Presented by Damon Richardson, Program Specialist - American Financial Resources, Inc. About the Presenter With 12 years of mortgage industry

HUD Real Estate Owned (REO) Loan Program Guide

Loan Program Guide") Table of Contents HUD Real Estate Owned (REO) Loan Program Guide Wholesale Lending January 9, 2014 Program Guide... 2 Pacific Union Financial Credit Philosophy... 2 Ability to Repay and Qualified Mortgages...

Table of Contents HUD Real Estate Owned (REO) Loan Program Guide Wholesale Lending January 9, 2014 Program Guide... 2 Pacific Union Financial Credit Philosophy... 2 Ability to Repay and Qualified Mortgages...

RESIDENTIAL MORTGAGE PRODUCT INFORMATION DISCLOSURE

RESIDENTIAL MORTGAGE PRODUCT INFORMATION DISCLOSURE Whether you are buying a house or refinancing an existing mortgage, this information can help you decide what type of mortgage is right for you. You

RESIDENTIAL MORTGAGE PRODUCT INFORMATION DISCLOSURE Whether you are buying a house or refinancing an existing mortgage, this information can help you decide what type of mortgage is right for you. You

Which Loan Is Best. For You?

Which Loan Is Best For You? US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed

Which Loan Is Best For You? US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed

Endorsing a Single Family FHA Case

Endorsing a Single Family FHA Case The Direct Endorsement (DE) process allows FHA-approved lenders to submit a mortgage insurance application for a loan to a single family, low-to-moderate-income homebuyer.

Endorsing a Single Family FHA Case The Direct Endorsement (DE) process allows FHA-approved lenders to submit a mortgage insurance application for a loan to a single family, low-to-moderate-income homebuyer.

Renovate your home your way. The FHA 203(k) Renovation Loan

Renovation Loan") Renovate your home your way The FHA 203(k) Renovation Loan Agenda What is an FHA 203(k) Renovation Loan? Advantages of an FHA 203(k) Renovation Loan FHA 203(k) Renovation Loan: Standard vs. Streamline

Renovate your home your way The FHA 203(k) Renovation Loan Agenda What is an FHA 203(k) Renovation Loan? Advantages of an FHA 203(k) Renovation Loan FHA 203(k) Renovation Loan: Standard vs. Streamline

Agency Conforming Fixed Rate Products. Agency 20 Year Fixed

Agency Conforming Fixed Rate Products Agency 30 Year Fixed Agency 20 Year Fixed APR APR Non-Escrowed Loans ***No charge for non-escrowed loans*** 3.250 1.000 3.445 State Adjustment Zone 1: 3.375 0.250

Agency Conforming Fixed Rate Products Agency 30 Year Fixed Agency 20 Year Fixed APR APR Non-Escrowed Loans ***No charge for non-escrowed loans*** 3.250 1.000 3.445 State Adjustment Zone 1: 3.375 0.250

Adjustable Rate Mortgage (ARM) a mortgage with a variable interest rate, which adjusts monthly, biannually or annually.

a mortgage with a variable interest rate, which adjusts monthly, biannually or annually.") Glossary Adjustable Rate Mortgage (ARM) a mortgage with a variable interest rate, which adjusts monthly, biannually or annually. Amortization the way a loan is paid off over time in installments, detailing

Glossary Adjustable Rate Mortgage (ARM) a mortgage with a variable interest rate, which adjusts monthly, biannually or annually. Amortization the way a loan is paid off over time in installments, detailing

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

PRMI 203K Streamline Loan. FHA Renovation Loan

PRMI 203K Streamline Loan FHA Renovation Loan Put the finishing touches on your borrowers Dream home. Purchase or Refinances Help you to sell more homes, and represent more buyers. Work with contractors

PRMI 203K Streamline Loan FHA Renovation Loan Put the finishing touches on your borrowers Dream home. Purchase or Refinances Help you to sell more homes, and represent more buyers. Work with contractors

Bill Fay Exec. Dir. of Energy Efficient Codes Coalition Laureen Blissard Technical Director of Green Builder Coalition & HERS rater Mike Collignon

Bill Fay Exec. Dir. of Energy Efficient Codes Coalition Laureen Blissard Technical Director of Green Builder Coalition & HERS rater Mike Collignon Exec. Dir. of Green Builder Coalition US homes & commercial

Bill Fay Exec. Dir. of Energy Efficient Codes Coalition Laureen Blissard Technical Director of Green Builder Coalition & HERS rater Mike Collignon Exec. Dir. of Green Builder Coalition US homes & commercial

Homebuyer Education: What You Need to Know

Homebuyer Education: What You Need to Know Today s Objectives Prepare your finances for home ownership Steps to mortgage prequalification Shopping for a home- who are the major players? Choosing the correct

Homebuyer Education: What You Need to Know Today s Objectives Prepare your finances for home ownership Steps to mortgage prequalification Shopping for a home- who are the major players? Choosing the correct

Down Payment Assistance Programs

Down Payment Assistance Programs Schedule an Appointment 6 8 hour Homebuyers Education Course 2-hour Pre-Purchase Counseling The Homeowners Employment Corporation SunTrust Bank Building - A 1530 Georgia

Down Payment Assistance Programs Schedule an Appointment 6 8 hour Homebuyers Education Course 2-hour Pre-Purchase Counseling The Homeowners Employment Corporation SunTrust Bank Building - A 1530 Georgia

HUD Marketing Approaches Each HUD REO property will be offered for sale using one of the approaches listed below.

HUD REOs Overview Through the Property Disposition Insured Sales Program, HUD offers its Real Estate Owned (REO) properties for sale with FHA-insured financing available. Properties must meet the intent

HUD REOs Overview Through the Property Disposition Insured Sales Program, HUD offers its Real Estate Owned (REO) properties for sale with FHA-insured financing available. Properties must meet the intent

Florida Solar Energy Center

Florida Solar Energy Center Overview of Energy Efficiency Financing Why Should A Lender be Concerned with Financing Energy Efficiency? David Carey, Director of Energy Finance for Fannie Mae said, "This

Florida Solar Energy Center Overview of Energy Efficiency Financing Why Should A Lender be Concerned with Financing Energy Efficiency? David Carey, Director of Energy Finance for Fannie Mae said, "This

Mortgage Loan Programs, Part I. Presented by Minnesota Housing

Mortgage Loan Programs, Part I Presented by Minnesota Housing Questions During Presentation We will batch online questions and answer them throughout the webinar A complete Q & A list will be posted to

Mortgage Loan Programs, Part I Presented by Minnesota Housing Questions During Presentation We will batch online questions and answer them throughout the webinar A complete Q & A list will be posted to

Green Financial Options in North Carolina

Green Financial Options in North Carolina Presented by Scott Suddreth Technical Program Director Building Performance Engineering October 2008 RENEWABLES NORTH CAROLINA SEO North Carolina - Energy Improvement

Green Financial Options in North Carolina Presented by Scott Suddreth Technical Program Director Building Performance Engineering October 2008 RENEWABLES NORTH CAROLINA SEO North Carolina - Energy Improvement

HOMESTYLE RENOVATION. Look at the possibilities

HOMESTYLE RENOVATION Look at the possibilities HOMESTREET: WHO ARE WE? Based in the Northwest, HomeStreet Bank if one of the largest community banks in the Northwest and Hawaii. HomeStreet began in 1921

HOMESTYLE RENOVATION Look at the possibilities HOMESTREET: WHO ARE WE? Based in the Northwest, HomeStreet Bank if one of the largest community banks in the Northwest and Hawaii. HomeStreet began in 1921

506 Loan Terms The Loan amount is $14,000.00 and will be a second mortgage lien closed with a DCA-approved Lender s first mortgage.

Chapter 5 Georgia Dream NSP Purchase Program 501 Georgia Dream NSP Purchase Program The Georgia Dream NSP Purchase Program is funded with proceeds from an allocation of federal funds from the Housing and

Chapter 5 Georgia Dream NSP Purchase Program 501 Georgia Dream NSP Purchase Program The Georgia Dream NSP Purchase Program is funded with proceeds from an allocation of federal funds from the Housing and

MAGNOLIA BANK FHA STANDARD REFINANCE OPTIONS MATRIX

RATE REDUCTION REFINANCES EQUITY (CASH OUT) REFINANCES 5. CACULATING THE MORTGAGE AMOUNT WITH A NEW APPRAISAL If the junior lien is a home equity line of credit, the maximum CLTV is based on the full credit

RATE REDUCTION REFINANCES EQUITY (CASH OUT) REFINANCES 5. CACULATING THE MORTGAGE AMOUNT WITH A NEW APPRAISAL If the junior lien is a home equity line of credit, the maximum CLTV is based on the full credit

FHA Fixed. FICO <580 Requirements: 1-4 580 (c) Varies by County (a) 97.75% 97.75% Per AUS (d) Sub 580 (560-579 FICO) FF30580SG FF15580SG

Varies by County (a) 97.75% 97.75% Per AUS (d) Sub 580 (560-579 FICO) FF30580SG FF15580SG") NOTES Primary Residence Units Minimum Credit Score SERIES G Max Loan Amount Continental US PURCHASE LTV CLTV Max Debt-to- Income Ratio 1-2 560 (e) Varies by County (a) 90% (e) 90% (e) 31/43% (e) 1-4 580

NOTES Primary Residence Units Minimum Credit Score SERIES G Max Loan Amount Continental US PURCHASE LTV CLTV Max Debt-to- Income Ratio 1-2 560 (e) Varies by County (a) 90% (e) 90% (e) 31/43% (e) 1-4 580

Purchase and rate/terms only. Streamline Standard (aka full consultant) Cash out to borrowers is not allowed

Cash out to borrowers is not allowed") February 2014 The FHA 203K program is HUD s primary program for the rehabilitation and repair of residential properties There are 2 different 203(k) programs offered: Streamline Standard (aka full consultant)

February 2014 The FHA 203K program is HUD s primary program for the rehabilitation and repair of residential properties There are 2 different 203(k) programs offered: Streamline Standard (aka full consultant)

http://www.allregs.com/tpl/documentprint.aspx?did3=fbac4aa6751c4ea0b8e44256c659d9f...

Page 1 of 5 Lending Library / Correspondent Seller Guide / 500. Products / 508. HIP Full FHA 203(k) 508. HIP Full FHA 203(k) HIP Full FHA 203(k) Product Matrix/Guidelines The FHA 203(k) program (i.e. Full

Page 1 of 5 Lending Library / Correspondent Seller Guide / 500. Products / 508. HIP Full FHA 203(k) 508. HIP Full FHA 203(k) HIP Full FHA 203(k) Product Matrix/Guidelines The FHA 203(k) program (i.e. Full

SECTION 4 REHABILITATION MORTGAGES 203(k) Standard & 203(k) Limited

Standard & 203(k) Limited") SECTION 4 REHABILITATION MORTGAGES 203(k) Standard & 203(k) Limited 4.1 Program Descriptions 4.2 Borrower Eligibility 4.3 Property Eligibility 4.4 Principal Residence Requirement 4.5 Rehabilitation Loan

SECTION 4 REHABILITATION MORTGAGES 203(k) Standard & 203(k) Limited 4.1 Program Descriptions 4.2 Borrower Eligibility 4.3 Property Eligibility 4.4 Principal Residence Requirement 4.5 Rehabilitation Loan

VA HOME LOANS A QUICK GUIDE FOR HOMEBUYERS AND REAL ESTATE PROFESSIONALS

VA HOME LOANS A QUICK GUIDE FOR HOMEBUYERS AND REAL ESTATE PROFESSIONALS Disclaimer: The information contained herein is strictly provided as information only. Veterans seeking more detailed information

VA HOME LOANS A QUICK GUIDE FOR HOMEBUYERS AND REAL ESTATE PROFESSIONALS Disclaimer: The information contained herein is strictly provided as information only. Veterans seeking more detailed information

MSHDA's Down Payment Assistance and Mortgage Credit Certificate. May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by:

Facilitated by: Carol Brito (MSHDA) Sponsored by:") MSHDA's Down Payment Assistance and Mortgage Credit Certificate May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by: CREDIT UNIONS A DRIVING FORCE OF COMMUNITIES MSHDA Overview

MSHDA's Down Payment Assistance and Mortgage Credit Certificate May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by: CREDIT UNIONS A DRIVING FORCE OF COMMUNITIES MSHDA Overview

Appraiser: a qualified individual who uses his or her experience and knowledge to prepare the appraisal estimate.

Mortgage Glossary 203(b): FHA program which provides mortgage insurance to protect lenders from default; used to finance the purchase of new or existing one- to four family housing; characterized by low

Mortgage Glossary 203(b): FHA program which provides mortgage insurance to protect lenders from default; used to finance the purchase of new or existing one- to four family housing; characterized by low

Assumable mortgage: A mortgage that can be transferred from a seller to a buyer. The buyer then takes over payment of an existing loan.

MORTGAGE GLOSSARY Adjustable Rate Mortgage (ARM): A mortgage loan with payments usually lower than a fixed rate initially, but is subject to changes in interest rates. There are a variety of ARMs that

MORTGAGE GLOSSARY Adjustable Rate Mortgage (ARM): A mortgage loan with payments usually lower than a fixed rate initially, but is subject to changes in interest rates. There are a variety of ARMs that

HUD PowerSaver Pilot Loan Program

December 10, 2010 HUD PowerSaver Pilot Loan Program The U.S. Department of Housing and Urban Development (HUD) recently announced the creation of a pilot loan program for home energy improvements. The

December 10, 2010 HUD PowerSaver Pilot Loan Program The U.S. Department of Housing and Urban Development (HUD) recently announced the creation of a pilot loan program for home energy improvements. The

A Presentation On the State of the Real Estate Crisis 1/30/2009

A Presentation On the State of the Real Estate Crisis 1/30/2009 Presented by Mike Anderson, CRMS President, Essential Mortgage, a Latter & Blum Realtors Company Immediate past president/legislative Chair

A Presentation On the State of the Real Estate Crisis 1/30/2009 Presented by Mike Anderson, CRMS President, Essential Mortgage, a Latter & Blum Realtors Company Immediate past president/legislative Chair

Achieving your goals through Financing. Cooperative Financing Models that may work for you

Achieving your goals through Financing Cooperative Financing Models that may work for you Overview Cooperative Financing Overview of the environment Interest Rates Why now is the best time to borrow Reasons

Achieving your goals through Financing Cooperative Financing Models that may work for you Overview Cooperative Financing Overview of the environment Interest Rates Why now is the best time to borrow Reasons

The First Time Homebuyer requirement in non-targeted counties will be waived for Veterans. Sales Price and Income Limits

SC Housing Mortgage Tax Credit (MCC) Program Guide The SC Mortgage Tax Credit Program is made available by the South Carolina State Housing Finance and Development Authority ( SC Housing ). An eligible

SC Housing Mortgage Tax Credit (MCC) Program Guide The SC Mortgage Tax Credit Program is made available by the South Carolina State Housing Finance and Development Authority ( SC Housing ). An eligible

Energy Efficient Mortgage Home Owner Guide

This page is located on the U.S. Department of Housing and Urban Development's Homes and Communities Web site at http://www.nls.gov/offices/hsg/sfh/eem/eemhog96.cfm. Energy Efficient Mortgage Home Owner

This page is located on the U.S. Department of Housing and Urban Development's Homes and Communities Web site at http://www.nls.gov/offices/hsg/sfh/eem/eemhog96.cfm. Energy Efficient Mortgage Home Owner

Date: January 21, 2014 All Approved Mortgagees Mortgagee Letter 2014-02

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER Date: January 21, 2014 To: All Approved Mortgagees Mortgagee Letter

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER Date: January 21, 2014 To: All Approved Mortgagees Mortgagee Letter

Introduction to PowerSaver For Virginia LEAP and Chapel Hill WISE

Introduction to PowerSaver For Virginia LEAP and Chapel Hill WISE What You Will Learn Today Who is behind the PowerSaver loan Why PowerSaver loan was developed About Sun West and EGIA Loan Specifications

Introduction to PowerSaver For Virginia LEAP and Chapel Hill WISE What You Will Learn Today Who is behind the PowerSaver loan Why PowerSaver loan was developed About Sun West and EGIA Loan Specifications

Fannie Mae Short Sale: Improving the Short Sale Experience. June 2013

Fannie Mae Short Sale: Improving the Short Sale Experience June 2013 2010 Fannie 2013 Fannie Mae Mae 1 What does Fannie Mae do? Keep funds flowing to the mortgage market Issue mortgage-backed securities

Fannie Mae Short Sale: Improving the Short Sale Experience June 2013 2010 Fannie 2013 Fannie Mae Mae 1 What does Fannie Mae do? Keep funds flowing to the mortgage market Issue mortgage-backed securities

A Guide To An FHA 203(k) Loan

Loan") A Guide To An FHA 203(k) Loan US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed

A Guide To An FHA 203(k) Loan US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed

What s s New With FHA?

What s s New With FHA? Presented By: Bill Ladewig 866.204.9733 http://www.mortgage- FHA Calculator Calculates everything needed to quote or qualify FHA loans Click to Open: http://www.themtgmentor.com/fha_mortgage_calculator.html

What s s New With FHA? Presented By: Bill Ladewig 866.204.9733 http://www.mortgage- FHA Calculator Calculates everything needed to quote or qualify FHA loans Click to Open: http://www.themtgmentor.com/fha_mortgage_calculator.html

Financing Options to support Energy Efficiency & Contractors

Financing Options to support Energy Efficiency & Contractors Renovation Loan Overview Renovation Loans offer a buyer the opportunity to buy a property and close as-is, financing both the purchase and repair

Financing Options to support Energy Efficiency & Contractors Renovation Loan Overview Renovation Loans offer a buyer the opportunity to buy a property and close as-is, financing both the purchase and repair

Think FHA: Session 1

Think FHA: Session 1 Thank you for joining the Webinar! We will begin at 1:00 pm. Your phone will be muted, as there are hundreds of Members on the call. Don t forget to turn on your computer speakers

Think FHA: Session 1 Thank you for joining the Webinar! We will begin at 1:00 pm. Your phone will be muted, as there are hundreds of Members on the call. Don t forget to turn on your computer speakers

MORTGAGE BANKING TERMS

MORTGAGE BANKING TERMS Acquisition cost: Add-on interest: In a HUD/FHA transaction, the price the borrower paid for the property plus any of the following costs: closing, repairs, or financing (except

MORTGAGE BANKING TERMS Acquisition cost: Add-on interest: In a HUD/FHA transaction, the price the borrower paid for the property plus any of the following costs: closing, repairs, or financing (except

Mortgage Loan Program Loan Transmittal 1 st Mortgage

Mortgage Loan Program Loan Transmittal 1 st Mortgage INSTRUCTIONS: Deliver a copy of this form along with the following documents as specified. Finance Agency 400 Sibley Street, Suite 300 St. Paul, 55101

Mortgage Loan Program Loan Transmittal 1 st Mortgage INSTRUCTIONS: Deliver a copy of this form along with the following documents as specified. Finance Agency 400 Sibley Street, Suite 300 St. Paul, 55101

203K Loan Parameters

Full documentation only. 203K Loan Parameters AUS approval required, no manual underwriting permitted. Maximum DTI ratios of 31%/43% regardless of AUS findings. Both purchase or rate and term refinance

Full documentation only. 203K Loan Parameters AUS approval required, no manual underwriting permitted. Maximum DTI ratios of 31%/43% regardless of AUS findings. Both purchase or rate and term refinance

Actions to Take Before Buying a Home Today

Actions to Take Before Buying a Home Today As the housing downturn has shown, homeownership is about more than buying a home you have to make sure you can keep the home over the long term. If you re thinking

Actions to Take Before Buying a Home Today As the housing downturn has shown, homeownership is about more than buying a home you have to make sure you can keep the home over the long term. If you re thinking

FHA MIP TRAINING (Mortgage Insurance Premium)

") FHA MIP TRAINING (Mortgage Insurance Premium) Offered by FIRST MORTGAGE CORPORATION APRIL 10, 2013 Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark

FHA MIP TRAINING (Mortgage Insurance Premium) Offered by FIRST MORTGAGE CORPORATION APRIL 10, 2013 Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark

Texas Home Equity Section 50(a)(6)

(6)") Texas Home Equity Section 50(a)(6) Revised 09/16/2015 rev. 16 Plaza s Underwriting Guidelines are designed to provide guidance as a standard to underwriting loans. There are cases where specific loan programs

Texas Home Equity Section 50(a)(6) Revised 09/16/2015 rev. 16 Plaza s Underwriting Guidelines are designed to provide guidance as a standard to underwriting loans. There are cases where specific loan programs

HOME BUYING101. 701.255.0042 www.capcu.org i

HOME BUYING101 701.255.0042 www.capcu.org i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended,

HOME BUYING101 701.255.0042 www.capcu.org i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended,

Product Product Code Loan Term 30-Year FRM FHA FHA30 30-years 15-Year FRM FHA FHA15 15-Years. Property Type Lowest Maximum (Floor)

") FHA Guidelines Product Description FHA Fixed Rate 15 and 30 Year Terms Fully Amortizing Product Codes Maximum s Product Product Code Loan Term 30-Year FRM FHA FHA30 30-years 15-Year FRM FHA FHA15 15-Years

FHA Guidelines Product Description FHA Fixed Rate 15 and 30 Year Terms Fully Amortizing Product Codes Maximum s Product Product Code Loan Term 30-Year FRM FHA FHA30 30-years 15-Year FRM FHA FHA15 15-Years

Lender Letter 07-2009 September 18, 2009. To: All Fannie Mae Single-Family Sellers and Servicers

Lender Letter 07-2009 September 18, 2009 To: All Fannie Mae Single-Family Sellers and Servicers Energy Loan Tax Assessment Programs Introduction Fannie Mae has recently received questions from lenders

Lender Letter 07-2009 September 18, 2009 To: All Fannie Mae Single-Family Sellers and Servicers Energy Loan Tax Assessment Programs Introduction Fannie Mae has recently received questions from lenders

Minnesota Housing & U.S. Bank Home Mortgage- MRBP Division. Product and Underwriting Guidelines

Minnesota Housing & U.S. Bank Home Mortgage- MRBP Division Product and Underwriting Guidelines Lou Caresani 2014 Agenda Minnesota Housing vs. US Bank Roles and Responsibilities US Bank Home Mortgage- MRBP

Minnesota Housing & U.S. Bank Home Mortgage- MRBP Division Product and Underwriting Guidelines Lou Caresani 2014 Agenda Minnesota Housing vs. US Bank Roles and Responsibilities US Bank Home Mortgage- MRBP

REALTORS AND FHA WORKING TOGETHER TO HELP PEOPLE FULFILL THE AMERICAN DREAM

Shopping for a Mortgage? FHA Improvements Benefit You FHA Insured Mortgages Realtors and FHA: Partners in Homeownership National Association of REALTORS FHA REALTORS AND FHA WORKING TOGETHER TO HELP PEOPLE

Shopping for a Mortgage? FHA Improvements Benefit You FHA Insured Mortgages Realtors and FHA: Partners in Homeownership National Association of REALTORS FHA REALTORS AND FHA WORKING TOGETHER TO HELP PEOPLE

City of Miramar. Neighborhood Stabilization Program (NSP)

") City of Miramar Neighborhood Stabilization Program (NSP) Q. What type of assistance is available? HOME BUYERS Frequently Asked Questions The City will assist with the purchase and qualified repairs of

City of Miramar Neighborhood Stabilization Program (NSP) Q. What type of assistance is available? HOME BUYERS Frequently Asked Questions The City will assist with the purchase and qualified repairs of

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE January 02, 2015 In case of any queries regarding the information available in this guide, please reach us at qmteam@swmc.com. Sun West Mortgage Company,

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE January 02, 2015 In case of any queries regarding the information available in this guide, please reach us at qmteam@swmc.com. Sun West Mortgage Company,

Guide to Purchasing a Home

Your journey to homeownership starts at your credit union. Purchasing your first home is a big decision, and it may even seem overwhelming. Rest assured Beacon Credit Union is here to assist you in understanding

Your journey to homeownership starts at your credit union. Purchasing your first home is a big decision, and it may even seem overwhelming. Rest assured Beacon Credit Union is here to assist you in understanding

navigating premier nationwide lending locking online system Logging in...2 pipeline...2

How To... navigating premier nationwide lending locking online system Contents Logging in and pipeline...2 Logging in...2 pipeline...2 pricing and locking a loan...3 product search...3 locking or pricing

How To... navigating premier nationwide lending locking online system Contents Logging in and pipeline...2 Logging in...2 pipeline...2 pricing and locking a loan...3 product search...3 locking or pricing

Program Overview For MRED

Program Overview For MRED 1 How searching for a new home has changed: Over 90% of homebuyers begin their search and view property listings online Over 72% of these homebuyers then EXIT the listing to search

Program Overview For MRED 1 How searching for a new home has changed: Over 90% of homebuyers begin their search and view property listings online Over 72% of these homebuyers then EXIT the listing to search

HOME BUYING101 TM %*'9 [[[ EPXEREJGY SVK i

HOME BUYING101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

HOME BUYING101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

Improving the Short Sale

Fannie Mae Short Sale: Improving the Short Sale Experience An Important Note About the Content of This Presentation While every effort has been made to ensure the accuracy of the content, Fannie Mae s

Fannie Mae Short Sale: Improving the Short Sale Experience An Important Note About the Content of This Presentation While every effort has been made to ensure the accuracy of the content, Fannie Mae s

13 DOWNPAYMENT PROGRAMS

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Home Advantage Downpayment Assistance Program can

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Home Advantage Downpayment Assistance Program can

Energy Efficient Mortgage Program DOYLE Loan #: 3001716496 Case #: 045-8129173-703

Date: MAY 28, 2014 U.S. Department of Housing and Urban Development Energy Efficient Mortgage Program Case #: 045-8129173-703 FHA's Energy Efficient Mortgage program (EEM) helps homebuyers or homeowners

Date: MAY 28, 2014 U.S. Department of Housing and Urban Development Energy Efficient Mortgage Program Case #: 045-8129173-703 FHA's Energy Efficient Mortgage program (EEM) helps homebuyers or homeowners

Homebuyer s Guide. Brought to you by:

Homebuyer s Guide Brought to you by: AmeriSouth Mortgage Company NMLS ID: 67050 Phone: (704) 845-9400 info@amerisouth.com www.amerisouth.com The basics What is a mortgage? A mortgage is a loan secured

Homebuyer s Guide Brought to you by: AmeriSouth Mortgage Company NMLS ID: 67050 Phone: (704) 845-9400 info@amerisouth.com www.amerisouth.com The basics What is a mortgage? A mortgage is a loan secured

VHDA. Homeownership Program Guidelines for Realtors & Lenders. Updated 04/04

VHDA Homeownership Program Guidelines for Realtors & Lenders Updated 04/04 2 Benefits of a VHDA Loan: Creative financing programs Reduced interest rates Lower monthly payments More house for less money

VHDA Homeownership Program Guidelines for Realtors & Lenders Updated 04/04 2 Benefits of a VHDA Loan: Creative financing programs Reduced interest rates Lower monthly payments More house for less money

6176 VA IRRRL. DW0114 Page 1 of 8

6176 VA IRRRL Interest Rate The loan must be to reduce the interest rate. If refinancing an adjustable rate mortgage (ARM) loan to a fixed rate loan, an exception is made allowing the new interest rate

6176 VA IRRRL Interest Rate The loan must be to reduce the interest rate. If refinancing an adjustable rate mortgage (ARM) loan to a fixed rate loan, an exception is made allowing the new interest rate

Homeownership Division

Michigan Credit Union League & Affiliates Annual Convention and Exposition Helping Credit Unions Serve, Grow and Remain Strong #mculace MSHDA s Homeownership Programs Delivering the Dream to Michigan Families

Michigan Credit Union League & Affiliates Annual Convention and Exposition Helping Credit Unions Serve, Grow and Remain Strong #mculace MSHDA s Homeownership Programs Delivering the Dream to Michigan Families

General Lending Criteria

1-888-324-3578 www.gregoryfunding.com info@gregoryfunding.com General Lending Criteria While we consider every loan on a case-by-case basis, following are general answers to some commonly asked questions.

1-888-324-3578 www.gregoryfunding.com info@gregoryfunding.com General Lending Criteria While we consider every loan on a case-by-case basis, following are general answers to some commonly asked questions.

ditech BUSINESS LENDING FHA STANDARD REFINANCE PRODUCT FOR CASE NUMBERS ASSIGNED ON OR AFTER 9/14/15

1. PRODUCT FHA Fixed Rate and ARM Mortgages for Rate and Term Refinance, Cash-Out Refinance and Simple Refinance Transactions DESCRIPTION Fixed Rate 5 to 30 year term in annual increments Fully amortizing

1. PRODUCT FHA Fixed Rate and ARM Mortgages for Rate and Term Refinance, Cash-Out Refinance and Simple Refinance Transactions DESCRIPTION Fixed Rate 5 to 30 year term in annual increments Fully amortizing

The SAPPHIRE. Program Training. Offered through FIRST MORTGAGE CORPORATION

The SAPPHIRE Program Training Offered through FIRST MORTGAGE CORPORATION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This presentation

The SAPPHIRE Program Training Offered through FIRST MORTGAGE CORPORATION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This presentation

Presents. FHA Streamlined(K) & 203(k) Training. July 20, 2011 7/18/2011. FHA Streamlined(k) Rehab Program

& 203(k) Training. July 20, 2011 7/18/2011. FHA Streamlined(k) Rehab Program") Presents FHA Streamlined(K) & 203(k) Training July 20, 2011 FHA Streamlined(k) Rehab Program Enables borrowers to finance both the purchase or refinance of a home and the cost of its rehabilitation through

Presents FHA Streamlined(K) & 203(k) Training July 20, 2011 FHA Streamlined(k) Rehab Program Enables borrowers to finance both the purchase or refinance of a home and the cost of its rehabilitation through

NON CREDIT QUALIFYING WITHOUT APPRAISAL, STANDARD & HIGH BALANCE, FIXED & ARM

NON CREDIT QUALIFYING WITHOUT APPRAISAL, STANDARD & HIGH BALANCE, FIXED & ARM Occupancy Maximum LTV/CLTV # of Units MAX Base Loan* High MIN Base* Min FICO Max Ratios Mortgage History** Primary 125% Non

NON CREDIT QUALIFYING WITHOUT APPRAISAL, STANDARD & HIGH BALANCE, FIXED & ARM Occupancy Maximum LTV/CLTV # of Units MAX Base Loan* High MIN Base* Min FICO Max Ratios Mortgage History** Primary 125% Non

Maryland Mortgage Program Realtor Workshop

Martin O'Malley GOVERNOR Anthony G. Brown LT. GOVERNOR Raymond A. Skinner SECRETARY Clarence J. Snuggs DEPUTY SECRETARY Maryland Mortgage Program Realtor Workshop May 8, 2013 1 Maryland Mortgage Program

Martin O'Malley GOVERNOR Anthony G. Brown LT. GOVERNOR Raymond A. Skinner SECRETARY Clarence J. Snuggs DEPUTY SECRETARY Maryland Mortgage Program Realtor Workshop May 8, 2013 1 Maryland Mortgage Program

QM - Qualified Mortgages. Internal Training Use only July 1, 2014 #T014

QM - Qualified Mortgages Internal Training Use only July 1, 2014 #T014 Rules & Terms to Know QM ATR HPML High Cost Rebuttable Presumption Safe Harbor Excludable Discount Pts History of QM & ATR Rules The

QM - Qualified Mortgages Internal Training Use only July 1, 2014 #T014 Rules & Terms to Know QM ATR HPML High Cost Rebuttable Presumption Safe Harbor Excludable Discount Pts History of QM & ATR Rules The

FHA 30, 15 Year Fixed Refinance Products 203b, 234c F30; F15; F30HPML Loan Amount and LTV Limitations

Units Length of Ownership 1 1-4 Units FHA 30, 15 Year Fixed Refinance Products 203b, 234c F30; F15; F30HPML Loan Amount and LTV Limitations < 1 year prior to application and the loan is not an existing

Units Length of Ownership 1 1-4 Units FHA 30, 15 Year Fixed Refinance Products 203b, 234c F30; F15; F30HPML Loan Amount and LTV Limitations < 1 year prior to application and the loan is not an existing

Incentivizing Pre-Disaster Mitigation

Incentivizing Pre-Disaster Mitigation Philip Schneider, AIA, MMC Director Leanne Tobias, CFIRE Chair October 28, 2015 Part 1 Incentivization Overview Philip Schneider, AIA What is Incentivization? For

Incentivizing Pre-Disaster Mitigation Philip Schneider, AIA, MMC Director Leanne Tobias, CFIRE Chair October 28, 2015 Part 1 Incentivization Overview Philip Schneider, AIA What is Incentivization? For

THE BASICS: Andrew Allen Updated 3/24/2015 COPYRIGHT 2013 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

R THE BASICS: Andrew Allen Updated 3/24/2015 The Formula for Success = AFR s Wholesale division is the #1 203(k) lender in the country for sponsored originations. HomeStyle Questions HomeStyle Explained

R THE BASICS: Andrew Allen Updated 3/24/2015 The Formula for Success = AFR s Wholesale division is the #1 203(k) lender in the country for sponsored originations. HomeStyle Questions HomeStyle Explained

FROM: Tammye Treviño (Signed by Tammye Treviño) Administrator Housing and Community Facilities Programs

Administrator Housing and Community Facilities Programs") RD AN No. 4635 (1980-D) April 2, 2012 TO: State Directors Rural Development ATTENTION: Rural Housing Program Directors, Guaranteed Loan Coordinators, Area Directors and Area Specialists FROM: Tammye Treviño

RD AN No. 4635 (1980-D) April 2, 2012 TO: State Directors Rural Development ATTENTION: Rural Housing Program Directors, Guaranteed Loan Coordinators, Area Directors and Area Specialists FROM: Tammye Treviño

Lending Guide. Section 400 Loan Submission & Standards

General Brokers have the option to submit loans to Rushmore Home Loans, a division of Rushmore Loan Management Services LLC (Rushmore) for underwriting via e-mail, Rushmore s IQ2 System, or courier/mail

General Brokers have the option to submit loans to Rushmore Home Loans, a division of Rushmore Loan Management Services LLC (Rushmore) for underwriting via e-mail, Rushmore s IQ2 System, or courier/mail

How to Finance Energy Upgrades Green Building for Cool Cities Rick Williams CGBP, CMPS

How to Finance Energy Upgrades Green Building for Cool Cities Rick Williams CGBP, CMPS October 9, 2010 Energy Upgrade California Financial Clearinghouse Web Portal One-stop shopping by zip code for local

How to Finance Energy Upgrades Green Building for Cool Cities Rick Williams CGBP, CMPS October 9, 2010 Energy Upgrade California Financial Clearinghouse Web Portal One-stop shopping by zip code for local

Private Mortgage Insurance (PMI)

") Private Mortgage Insurance (PMI) Private Mortgage Insurance (PMI) New Law Requires Lenders to Cancel PMI If you are a homeowner, you will want to be aware of a new law that establishes rights for homeowners

Private Mortgage Insurance (PMI) Private Mortgage Insurance (PMI) New Law Requires Lenders to Cancel PMI If you are a homeowner, you will want to be aware of a new law that establishes rights for homeowners

FHA HIGH BALANCE FIXED PROGRAM HIGHLIGHTS

Product Summary These guidelines represent underwriting requirements for FHA fixed rate and ARM mortgages with increased loan size limits with a minimum floor of greater than $417,000. These guidelines

Product Summary These guidelines represent underwriting requirements for FHA fixed rate and ARM mortgages with increased loan size limits with a minimum floor of greater than $417,000. These guidelines

FHA Office of Single Family Housing. Training: Origination Through Post-Closing/ Endorsement

Training: Origination Through Post-Closing/ Endorsement 1 Module 8A Programs and Products: Refinance Single Family Housing Policy Handbook 4000.1 Title II Insured Housing Program Forward Mortgages Origination

Training: Origination Through Post-Closing/ Endorsement 1 Module 8A Programs and Products: Refinance Single Family Housing Policy Handbook 4000.1 Title II Insured Housing Program Forward Mortgages Origination

Introduction to Renovation Lending. Presented by: Jane King Freedom Mortgage

Introduction to Renovation Lending Presented by: Jane King Freedom Mortgage Agenda Renovation Lending Overview of renovation products Identifying the right borrower Identifying the right property Evaluating

Introduction to Renovation Lending Presented by: Jane King Freedom Mortgage Agenda Renovation Lending Overview of renovation products Identifying the right borrower Identifying the right property Evaluating

Sun West Overview. Privately Held Flexibility to respond to Customers needs. CONFIDENTIAL Sun West Mortgage Company, Inc.

Sun West Overview Headquartered in Cerritos, California - Sun West has been serving our nationwide client base since 1980. Our diversified loan program experience includes FHA Single Family, FHA Reverse

Sun West Overview Headquartered in Cerritos, California - Sun West has been serving our nationwide client base since 1980. Our diversified loan program experience includes FHA Single Family, FHA Reverse

Enhancements to Streamlined (k) Limited Repair Program

Limited Repair Program") U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER December 29, 2005 MORTGAGEE LETTER 2005-50 TO: ALL APPROVED MORTGAGEES

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER December 29, 2005 MORTGAGEE LETTER 2005-50 TO: ALL APPROVED MORTGAGEES

Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA)

![Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA)](/thumbs/25/5268134.jpg "Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA)") Chapter 42 Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA) INTRODUCTION Besides conventional loans discussed

Chapter 42 Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA) INTRODUCTION Besides conventional loans discussed

Principal Lending Manager Education Curriculum Outline 40 Hours

Principal Lending Manager Education Curriculum Outline 40 Hours Utah Division of Real Estate PO Box 146711 Salt Lake City, UT 84114-6711 Subject Matter Number of Hours 1. General Mortgage Industry Knowledge

Principal Lending Manager Education Curriculum Outline 40 Hours Utah Division of Real Estate PO Box 146711 Salt Lake City, UT 84114-6711 Subject Matter Number of Hours 1. General Mortgage Industry Knowledge

Section C. Maximum Mortgage Amounts on Streamline Refinances Overview

Section C. Maximum Mortgage Amounts on Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 General Information on 3-C-2 2 Without an Appraisal

Section C. Maximum Mortgage Amounts on Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 General Information on 3-C-2 2 Without an Appraisal

Southeast Texas Housing Finance Corporation (SETH) 5 Star Texas Advantage Program Invitation to Participate

5 Star Texas Advantage Program Invitation to Participate") Southeast Texas Housing Finance Corporation (SETH) 5 Star Texas Advantage Program Invitation to Participate Southeast Texas Housing Finance Corporation (SETH) is pleased to extend an invitation to its

Southeast Texas Housing Finance Corporation (SETH) 5 Star Texas Advantage Program Invitation to Participate Southeast Texas Housing Finance Corporation (SETH) is pleased to extend an invitation to its

Single Family Bond Program Lender Training PROGRAM OVERVIEW

Single Family Bond Program Lender Training PROGRAM OVERVIEW What this program ISN T NOT A DOWN PAYMENT ASSISTANCE PROGRAM NOT FOR BUYERS WITH POOR CREDIT DOES NOT PROVIDE A SUBPRIME PRODUCT NOT FOR LOW

Single Family Bond Program Lender Training PROGRAM OVERVIEW What this program ISN T NOT A DOWN PAYMENT ASSISTANCE PROGRAM NOT FOR BUYERS WITH POOR CREDIT DOES NOT PROVIDE A SUBPRIME PRODUCT NOT FOR LOW

Summary of the Obama Administration s MAKING HOME AFFORDABLE PROGRAM

Summary of the Obama Administration s MAKING HOME AFFORDABLE PROGRAM Prepared By: Empire Justice Center Kevin Purcell and Salah Maker The Telesca Center for Justice One West Main Street, Suite 200 Rochester,

Summary of the Obama Administration s MAKING HOME AFFORDABLE PROGRAM Prepared By: Empire Justice Center Kevin Purcell and Salah Maker The Telesca Center for Justice One West Main Street, Suite 200 Rochester,

S. 720 Energy Savings and Industrial Competitiveness Act of 2015

CONGRESSIONAL BUDGET OFFICE COST ESTIMATE October 19, 2015 S. 720 Energy Savings and Industrial Competitiveness Act of 2015 As reported by the Senate Committee on Energy and Natural Resources on September

CONGRESSIONAL BUDGET OFFICE COST ESTIMATE October 19, 2015 S. 720 Energy Savings and Industrial Competitiveness Act of 2015 As reported by the Senate Committee on Energy and Natural Resources on September

LOCAL LENDING FOR SOLAR PV:

November2013 LOCAL LENDING FOR SOLAR PV: A GUIDE FOR LOCAL GOVERNMENTS SEEKING TO ENGAGE FINANCIAL INSTITUTIONS www.mc-group.com 98 North Washington Street Suite 302 Boston MA 02114 617.934.4847 TABLE

November2013 LOCAL LENDING FOR SOLAR PV: A GUIDE FOR LOCAL GOVERNMENTS SEEKING TO ENGAGE FINANCIAL INSTITUTIONS www.mc-group.com 98 North Washington Street Suite 302 Boston MA 02114 617.934.4847 TABLE

NOTE: This matrix includes overlays, which may be more restrictive than VA requirements. A thorough reading of this matrix is recommended.

VA Refinance IRRRL This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected

VA Refinance IRRRL This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected

2479 South Lake Park Blvd. West Valley City, UT 84120 801-902-8200 801-902-8327 - fax www.utahhousingcorp.org

2479 South Lake Park Blvd. West Valley City, UT 84120 801-902-8200 801-902-8327 - fax www.utahhousingcorp.org MORTGAGE BANKING STAFF Deon Spilker Mortgage Banking Director (801-902-8256) dspilker@uthc.org

2479 South Lake Park Blvd. West Valley City, UT 84120 801-902-8200 801-902-8327 - fax www.utahhousingcorp.org MORTGAGE BANKING STAFF Deon Spilker Mortgage Banking Director (801-902-8256) dspilker@uthc.org

Disclosure Specialist Responsibilities. Lock Procedures. Processor Responsibilities. Appraisal Ordering

FHA 203K Streamline - Policies & Procedures FHA 203K Streamline will now be underwritten and funded in house. These applications should be originated in Mortgage Builder under the FHA203K-SR program code.

FHA 203K Streamline - Policies & Procedures FHA 203K Streamline will now be underwritten and funded in house. These applications should be originated in Mortgage Builder under the FHA203K-SR program code.

HomeStreet Bank s. Preferred Builder Program

HomeStreet Bank s Preferred Builder Program Company Overview Key Facts and Statistics Oldest Fannie Mae Relationship in the United States HomeStreet, Inc. (NASDAQ:HMST) is a diversified financial services

HomeStreet Bank s Preferred Builder Program Company Overview Key Facts and Statistics Oldest Fannie Mae Relationship in the United States HomeStreet, Inc. (NASDAQ:HMST) is a diversified financial services