PAPER presented by Belgium. Market situation in the inland waterway transport sector

|

|

|

- Robyn O’Brien’

- 8 years ago

- Views:

Transcription

1

2

3 PAPER presented by Belgium Market situation in the inland waterway transport sector

4 Brussels, 11 October 2013 Analysis of the market situation in the inland waterway transport sector - Final draft 1 Introduction. For some time now the Belgian inland waterway sector has been launching cries of alarm about the evolution on the national and international inland waterway transport market. During the last month of April this has lead to actions on the field and caused temporary disruptions of the transport system at several strategic points of the IWT network. At the origin of these actions is the decline of economic growth that started at the end of 2008 with the general economic and financial crisis in the world economy. Since the end of 2008 the slowing down of the economy together with an increase of the costs and an overcapacity of tonnage have put the prices under such pressure that for a large amount of companies it is no longer possible to cover the fixed and variable costs necessary for a healthy exploitation. This also causes a lack of financial means necessary for the maintenance of the vessel and the investments related to safety. 1 This problem has already been subject to an announcement of a structural disturbance of the market by the Netherlands at the end of The analysis of the situation by the committee installed by Directive 91/672/EC and the report presented to this committee following discussions in a sub-working group, lead to the conclusion that the expected recovery of the demand for transport would allow the sector to overcome the financial problems and lead to a return to the expected path of annual growth. In Figure 1 a global overview is given of the evolution of the transport performance on inland waterways and the fleet capacity (EU-27). This figure already shows that there is a disturbance of the balance between transport performance and fleet capacity.

5 Figure 1 Source : Eurostat, CCNR At this moment we have to admit that the expected recovery did not take place, or at least not in a sufficient way. Furthermore, in the years the fleet capacity still increased thus complicating the return to a normal market situation. Following the negotiations between the Belgian authorities and the sector it was agreed that Belgium would start up the procedure to announce a serious market disturbance at the European level according to Directive 96/75/EC, since it is clear that suitable measures will essentially have to be taken at that level. On the 26 th of April Belgium formally asked the European Commission to organize as soon as possible a meeting of the committee founded by Directive 91/672/EC in order to take up this issue. This has led to two meetings of this committee and a hearing of the sector. 2 In the meantime Belgium has further analyzed the situation and has completed the present document. This final draft supports the position of Belgium that the inland waterway transport sector in North-West Europe is dealing with a serious disturbance of the market situation. In the following points we give a more detailed analysis of the situation in order to get a clear view of the difficulties and we also make some suggestions of measures to be taken.

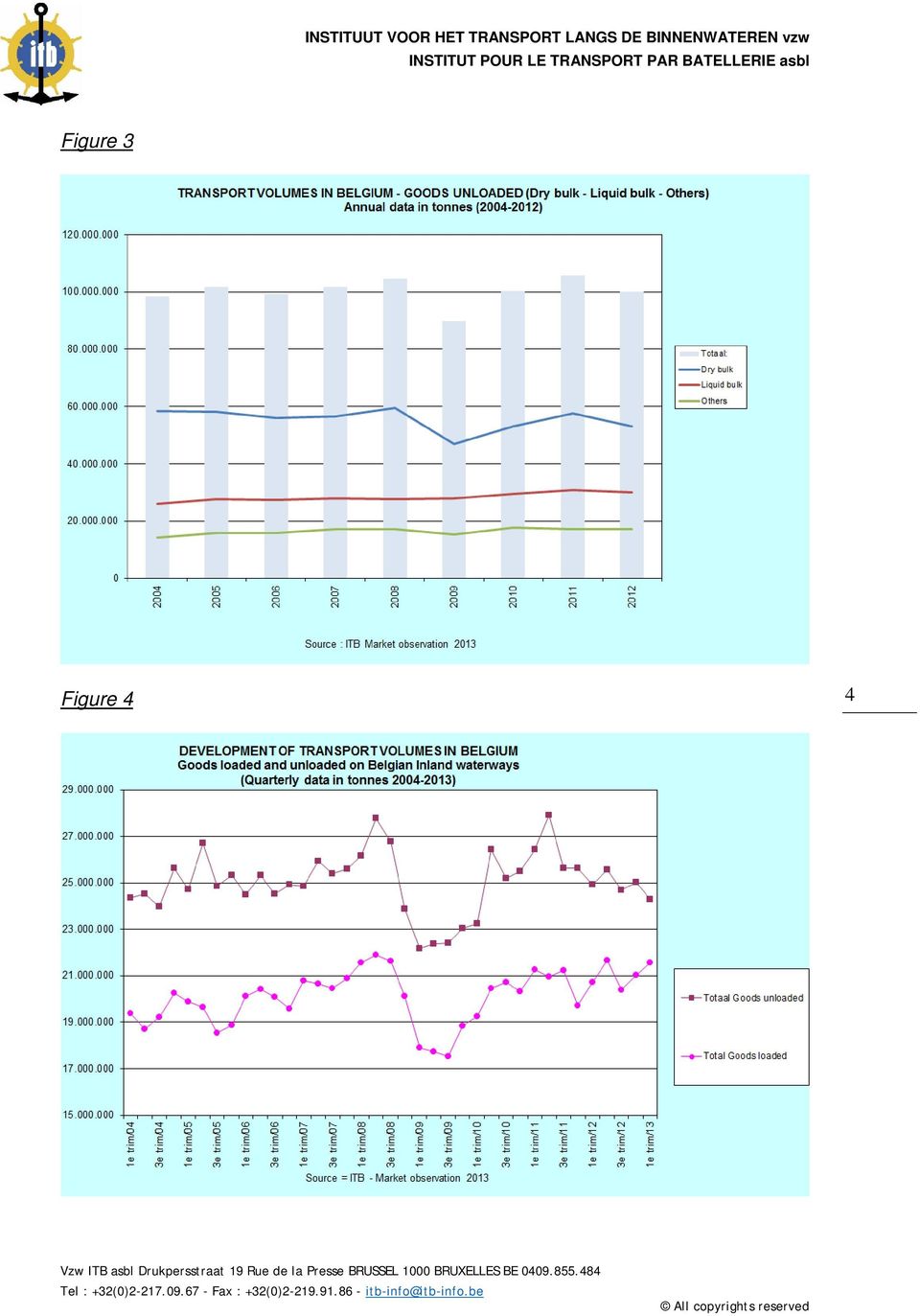

6 2 Evolution of the transport demand 2.1 Development of transport volumes in Belgium In the Figures 2 and 3 data are presented about the evolution of the yearly volumes of goods loaded and unloaded on Belgian waterways for the period These data contain national as well as international transports with origin or destination in Belgium. Loaded and unloaded volumes are presented separately in order to avoid a double counting of the transport within Belgium. The evolution clearly shows that there was a very serious decline in 2009, but the following years a recovery was noted, although a return to the growth trend of the years until 2008 is not yet the case. Figure 2 3 Source : ITB - inland waterways managers and Ports

7 Figure 3 Figure 4 4

8 In Figure 4 the evolution of the volumes is presented on a quarterly basis. The first quarter of 2013 shows a better result for the loaded volumes (+ 4 %) compared to the first quarter of 2012, but this is mainly thanks to a much higher transshipment in the port of Antwerp. The unloaded volumes show a further decline (-2,5 %), which means that the transport volumes towards the Belgian hinterland continue to decrease. More detailed data can be found in Annex I (pp ) 2.2 Development of transport volumes in Europe According to the statistical data from Eurostat (Statistics in focus 42/2012) after the serious drop in inland waterways transport in 2009, a recovery was observed but of a fragile nature taking into account the quarterly registered ups and downs. In Figure 5 the yearly registered transport performance for the EU-27 are presented for the years It shows that the recovery of the performance in 2010 did not continue in 2011 (-4,9 % compared to 2010). Figure 5 5 Source : Eurostat The economic survey presented by the CCNR for the transport activity on the Rhine is also an important indicator, since the Rhine River is a central artery in the IWT network.

2.")

9 Figure 6 shows that the recovery of the transport volumes after the problematic year 2009 is rather slow and the volumes registered before this crisis year are not yet reached. Figure 6 Rhine traffic between Rheinfelden and the German-Dutch border (in Mio. t) Source : CCNR - Destatis + calculation by CCNR-Secretariat 6 3 Evolution of the fleet capacity 3.1 Belgian fleet In Figure 7 the evolution of the Belgian dry cargo fleet is presented for the period It is clear that the development of the global capacity of this fleet is not at all unreasonable compared to the positive trend in transport volumes that we could see after In fact, the growth rate of the fleet capacity stayed below the growth rate of the transport volumes on the Belgian market. The efforts of the Belgian authorities to encourage a transfer from road transport to IWT, for instance through the cay wall program of the Flemish government, did not lead to a disproportionate investment tendency in new tonnage. What we do however see in the data is a further disappearance of the smaller vessels and an increase of high tonnage ships.

10 Figure 7 Source : ITB Market Observation 2013 FPS Mobility and Transport The situation is slightly different for the tanker fleet, where an increase of the global capacity was registered (Figure 8). This is for a large part due to the replacement of single hull by double hull tankers, while in the meantime, at least until 2018, the first category still stays on the market. 7 Figure 8 Source : ITB Market Observation 2013 FPS Mobility and Transport

11 Taking into account that Belgium is a small country with an open economy it is difficult to compare at a Belgian level if there is a balance between the transport volumes on the Belgian waterways and the Belgian fleet capacity. We can indeed see that a large part of the transport volumes on Belgian waterways are carried by vessels that do not sail under a Belgian flag. When we look at the data of the foreign fleet that is participating in domestic transport on the Belgian market (transport between two points within Belgium) we notice that the capacity for the dry cargo fleet has developed from a capacity of tonnes in 2004 to tonnes in For the tankerfleet this evolution went from tonnes in 2004 to tonnes in If we take into account national transport within and international transport to and from Belgium in volumes (tons), the market share of the Belgian fleet decreased from an average of 46 % in 2008 to an average of 38 % in More details on the Belgian fleet can be found in Annex II (pp ). 3.2 European fleet In Figures 9 and 10 you can find the evolution of the European fleet for the period More details of the European fleet in Annex III (pp ). Figure 9 8 Development of the European Dry cargo fleet Capacity (Tonnes) Number Years 0 (Source : CCNR ) NL D B F Others NL D B F Others

12 Figure 10 Capacity (Tonnes) Development of the European Tanker fleet Years Number (Source : CCNR ) NL D B F Others NL D B F Others 3.3 Estimation of new built ships Table 11 9 Source : CCNR DG MOVE Market Observation

13 In table 11 you can find an estimation of the new capacity that came into the European fleet since It shows that the fleet capacity continued to grow after the top year 2008, although the market started to shrink. We also received information from our sector representatives that about 200 vessel hulls of more than 2000 tonnes are still waiting in West-European shipyards to be finished. If this information is confirmed we can fear that a slight recovery of the market might quickly lead to a further disproportionate increase of the fleet capacity. 4 Evolution of the financial situation and perspectives for the future 4.1 Evolution of the financial situation According to the information obtained from the sector organizations there is a strong decrease in freight prices since 2009 with only a temporary recovery in 2011 thanks to the low water levels on the Rhine. The decrease of freight prices continued in 2012 and the first half of 2013 with the consequence that the fixed and variable costs are no longer covered. This situation is going on for more than 4 years now and an increasing number of transport operators have payment problems. In Figure 12 the evolution of the book profits (EBITDA index 2006/2007 = 100) since 2006 is given for dry cargo ships in the category > 1500 tonnes, on the basis of the average results for a representative sample of concrete accountancy files. 10 Figure 12

14 Source : ITB Barometer 2012 in collaboration with accountants Taking into account that the given book profits don t include interests, taxes, depreciation and amortization and exclude as well the personal income of the entrepreneur, it is clear that the average financial situation is not brilliant. Furthermore the analysis of the detailed accountancy data and the evolution of certain cost elements show that an increasing number of transport operators try to economize by postponing the necessary maintenance of the vessel or even by sailing with insufficient crew. This is a dangerous evolution since it affects the safety of the transport sector. The financial situation also limits the possibilities of the sector to invest in improvement measures (e.g. greening). Furthermore we also have some information from Belgian banks. Although they are reluctant to give concrete financial data they confirm that more and more operators have problems to pay back their loans, especially in the dry cargo sector. The banks can of course play a supporting role by allowing operators to partially postpone the reimbursement of capital, but it is clear that in so far problems also concern the paying of interests the bank also reaches its limits. Data from the Flemish warranty system indicate that more cases can be registered during the recent years where banks proceed to the selling off. 4.2 Evolution of freight prices As more detailed information on the market situation a survey of the evolution of freight prices since 1998 has been made for several major transport relations for the dry cargo sector (e.g. Upper Rhine, Mosel, Main, Delta). In order to be able to calculate a global average the prices have been expressed in Euro/tkm. Figures 13 and 14 show the evolution of the average prices for the relations ARA Upstream and ARA downstream. 11 Figure 13 Source : ITB based on information from Belgian ship s operators

15 Figure 14 Source : ITB based on information from Belgian ship s operators These data lead to the conclusion that freight prices did not follow the increase of the cost elements and have been rather stable for a long time. 4.3 Evolution of costs As far as the costs are concerned, there is a tendency to a further increase. This is especially the case for the fuel costs, an important element of the variable costs. In Figure 15 you can find the evolution of the fuel prices on the Belgian market. It clearly indicates that the fuel prices were going up during the crisis years. 12 Figure 15 Source : FPS Economy, SMEs, Self-employed and Energy

16 Figure 16 shows the evolution of the global index for consumption prices. The wages for crew approximately follow this evolution, and so also this part of the cost price registers an increasing tendency. Figure 16 Consumption price index (basis 2004 = 100) Source : FPS Economy, SMEs, Self-employed and Energy 4.4 Prognosis Specific forecasts for the evolution of the market situation in the IWT sector for the following years are not so easy to be found. In general the transport market depends on the evolution of the global economy and therefore several sources can be consulted. In Table 17 data are based on the European Economic Forecast made by the European Commission. Other sources can of course give other indications. Anyhow, a high growth scenario for the European economy seems not to be expected for this and next year. 13 Table 17 Source : European Economic Forecast Spring 2013 European Economy 2/2013, European Commission A more specific analyses for the IWT sector is made by the CCNR (see the following page Figure 18).

17 Figure 18 Prognosen für 2014 Bereich Produktion/ Importe Anteil am Gesamtverkehr Landwirtschaft kaum Zuwächse 16,00% Voraussehbarer Einfluss auf die Beförderungsnachfrage (gegenüber dem Vorjahr) 0 Kohle Erhöhung der Importkohlemengen auf Grund der weltweiten + Energiepolitik 19,00% Stahlindustrie: Erze dt. Stahlprod. wird leicht sinken, angesichts der strukturellen - Probleme 20% Stahlindustrie: Eisen, Stahl dt. Stahlprod. wird leicht sinken, angesichts der strukturellen - Probleme 8,00% Baustoffe kaum Belebung in der Bauwirtschaft 27,00% 0 Andere Güter / Container Leichtes Container-Wachstum 10% + Gesamtprognose zur Entwicklung der Nachfrage in der Trockenschifffahrt 0 Erdölprodukte Seitwärts-Entwicklung beim Ölpreis, aber strukturelle sinkende 0 Mengen 60% Chemie Chemische Industrie +2 %; 40% + Gesamtprognose zur Entwicklung der Nachfrage in der Tankschifffahrt + Quellen: Eurofer Euracoal Verein deutscher Kohleimporteure Verband der chemischen Industrie CEFIC Prognosen ZKR auf Basis historischer Entwicklungen und Berechnungen Entwicklung 0 % 0 1 % bis 5 % - / + 6 % bis 10 % / % bis 15 % / % bis 20 % / über 20 % /

18 5 Evaluation of the origins of the market disturbance and conclusions On the basis of the data presented in the preceding points we think that there clearly is a serious disturbance of the European IWT market of a structural nature. The development of the fleet capacity after the crisis year 2009 is such that a recovery of the freight prices cannot be expected in the short term, even when the transport volumes are again increasing. So the first important problem that the sector is confronted with is the overcapacity of the European fleet. Furthermore we may fear that a further growth of the fleet might occur in the short term. Secondly, when in 2010 we came to the conclusion that the recovery of the economy would allow the sector to overcome its problems, this would only be possible if a high growth scenario would be realized (cf. Report to the committee established under Directive 91/672/EC on possible measures to combat the crisis in the IWT sector 15/09/2010). We have to admit at this moment that there was no high growth scenario for the period and such a scenario seems to be rather improbable for the next years. Furthermore there is the increase of the costs, especially the fuel costs, for which the operators weren t able to compensate this through the freight prices. Another element that plays an important role in the determination of market prices is the lack of market transparency, allowing intermediaries or brokers that operate in the market between shippers and IWT operators, to make use of the weak position of the latter, especially independent operators, to obtain the lowest possible prices. This also is a structural problem that regularly appears on the IWT market, and is aggravated in periods of overcapacity. In fact it limits the freedom of the transport operator to obtain a reasonable price for his transport performance, since refusing to accept these prices might put him out of the market. The Belgian IWT sector is of the opinion that Directive 96/75/EC should take into account that the objective of a free market is not to allow dumping prices. The basis for this opinion can be found in article 94 of the consolidated version of the treaty on the functioning of the European Union. This article determines that any measures taken within the framework of the Treaties in respect of transport rates and conditions shall take account of the economic circumstances of carriers. 15 As far as the operation of intermediaries or brokers is concerned, we can also underline that in some countries (e.g. Belgium, France) the profession of these intermediaries is regulated and depending on a license. In some other countries this profession is not regulated at all and anyone can start up a company with an intermediate activity in freight forwarding and try to obtain a position on the market by dumping prices, even when the real transport activity is taking place in another country. This aspect should also be examined at the European level. In our view the activity of these intermediaries should be regulated like the other transport professions.

19 All in all different elements together have consequences for the financial position of the transport operators and their survival capacities for the coming years. This brings the sector to ask questions about the European policy for the future. In the white paper objectives were formulated for the role of the IWT sector in the coming years. An important growth tendency and an increase of the modal share were forecasted. Initiatives for the greening of the fleet are expected. All these goals depend on the financial stability and prosperity of the sector. The actual evolution threatens to form a serious obstruction to reach them. For all those reasons Belgium is of the opinion that measures should be taken at an European level to help the sector survive this problematic period and to ensure that it can fulfill the role that is expected in the future. In the following point some suggestions are made on the basis of our discussions with our Belgian IWT sector. 6 Proposals for possible suitable measures at European level to strengthen the market mechanism. 6.1 Permanent measures 1) Measures concerning the coverage of costs anti dumping measure and transport conditions. Ensure that an operator works at prices that allow him to cover his costs, eventually on a periodical basis. Directive 96/75/EC could be modified and completed by a disposition in that sense. 2) Measures supporting the modernization of the fleet, especially when it comes to greening, with sufficient attention also for the smaller existing fleet. 3) Install a performing market observation system that can predict the capacity development, but also with the necessary means to adjust in order to prevent further structural overcapacity. One of the possibilities is to give a real substance to the wording of Regulation 718/99 that stipulates that new built ships have to be announced 6 months beforehand. This has not really been used. 4) Creation of a harmonized framework not only in the field of technical or manning prescriptions and implementation, but also in the fiscal and social field. 5) Review of technical prescriptions for the existing fleet. Especially the transitional provisions of the technical prescriptions for the Rhine seem to be an important problem for the existing fleet. 6) Analysis of the financing instruments. The lever that causes disproportionate investment tendencies should disappear Crisis measures limited in time Suitable measures that adjust the capacity. Support for all forms of cooperation to improve the market mechanism..

20 Bibliography 1. Introduction Sources : - Eurostat Statistics in focus Inland waterways freight transport quarterly and annual data, , European Union (b) - Market observation Inland waterways CCNR-DG MOVE Evolution of the transport demand 2.1. Development of transport volumes in Belgium (see Annex 1) Sources : - Instituut voor het Transport langs de Binnenwateren vzw, Marktobservatie - Ladingen en lossingen met binnenschepen op Belgische waterwegen 4de kwartaal 2012, ste kwartaal 2013, , pp 7-10, Bruxelles 2.2. Development of transport volumes in Europe Sources : - Eurostat Pocketbooks «Energy, transport and environment indicators», Edition 2012 (a) - Eurostat Statistics in focus Inland waterways freight transport quarterly and annual data, , European Union (b) - Market observation Inland waterways CCNR-DG MOVE 2012 (Destatis, Secrétariat CCNR) 17 (a) Table (pag ) (b) Figure 1 (p. 1) Table 1 + Table 2 (p. 2) + Table 3 (p. 3) (c) Trafics sur le Rhin (exprimé en millions de tonnes) 3. Evolution of the fleet capacity 3.1. Belgian fleet (see Annex 1I) Source : - Instituut voor het Transport langs de Binnenwateren vzw, Marktobservatie Binnenvaartvloot toebehorend aan in Belgïë gesvestigde eigenaars» Toestand op 31-12, 2004 tot en met 2012, Tableau de l évolution de la flotte de cargaison sèche par catégorie de bateaux en nombre et en port en lourd < à 2.000t ou > 2.000t et tonnage moyen Evolution Tableau de l évolution de la flotte de citerne par catégories de bateaux en nombre et en port en lourd < à 2.000t ou > 2.000t et tonnage moyen Evolution

21 Belgian fleet market share Plan national cabotage ( ) Source : - Instituut voor het Transport langs de Binnenwateren vzw, Tableau d évolution de la flotte appartenant à des entrepreneurs non domiciliés en Belgique Evolution par nationalité en nombre, port en lourd et puissance Port d Anvers Source : - Gemeentelijk Havenbedrijf Antwerpen, Algemene Directie, Bulletin trimestriel de statistiques : navigation intérieure, Allèges entrées, classées selon les principaux pavillons Tableau de comparaison exprimés en nombre et en capacité (m3) Gestionnaires des voies navigables Sources : - De Scheepvaart NV (a) NV Waterwegen en Zeekanaal, 2013 (b) et Service Public de Wallonie (c) 18 (a) Tableau d évolution des tonnages transportés par groupe de marchandises et nationalité du bateau (en nombre et tonnage transporté) - (b) Tableau d évolution des tonnages transportés par nationalité du bateau et 1tr2013 (en nombre et tonnage transporté) (c) Nombre de bateaux de marchandises et tonnage transporté par nationalité au point 4058 (Ecluse d Ivoz-ramet) sur la voie 40 Meuse (en nombre et tonnage transporté) 3.2. European fleet (see Annex 1II) Sources : - Observation du marché européen de la navigation intérieure Etat de la flotte intérieure Années », rapports semestriels 2005-I à 2012-I, CCNR-DG MOVE (Secrétariat CCNR) Tableau de l évolution de la flotte de cargaison sèche par nationalité et catégories de bateaux (à l exclusion des chalands) Evolution en nombre, port en lourd et tonnage moyen Tableau de l évolution de la flotte de citerne par nationalité et catégories de bateaux (à l exclusion des chalands) Evolution Evolution en nombre, port en lourd et tonnage moyen 3.3. Estimation of new built ships Sources : - Market observation Inland waterways CCNR-DG MOVE (Secrétariat CCNR)

22 Tableau du rapport semestriel de l observation du marché : Annexe Nouvelles constructions Evolution of the financial situation and perspectives for the future 4.1. Evolution of the financial situation Source : - Instituut voor het Transport langs de Binnenwateren vzw, Barometer 2012 in cooperation with accountants - Ons Recht/Notre droit aisbl (b) 4.2. Evolution of freight prices Source : - Instituut voor het Transport langs de Binnenwateren vzw, Ons Recht/Notre droit aisbl Evolution average freight prices in /tkm for Dry cargo vessels ( ) 4.3. Evolution of costs Source : - FPS Economy, SMEs, Self-employed and Energy 19 (a) Evolution of fuel prices ( ) (b) Evolution of consumption price index CPI 2004 ( ) 4.4. Prognosis Sources : - European Economic Forecast Spring 2013 European Economy 2/2013, European Commission - Analyse et évaluation des tendances structurelles du marché (Observation du marché 2013 annexe 1, p. 112), Secrétariat CCNR, 1er octobre 2013.

23 Annex I - Loaded and unloaded goods on Belgian inland waterways

24 21

25 Annex II - Belgian Dry cargo and Tank fleet - capacity < or > t ( ) 22

26 23

27 Annex III - Flag share in European Fleet (Dry cargo fleet and Tank fleet in number and in capacity) 24

28 25

CENTRAL COMMISSION FOR THE NAVIGATION OF THE RHINE 25 March 2011 SECRETARIAT

CENTRAL COMMISSION FOR THE NAVIGATION OF THE RHINE 25 March 2011 SECRETARIAT Establishing the carbon footprint and the specific CO 2 emissions () of inland navigation - Overview of studies establishing

CENTRAL COMMISSION FOR THE NAVIGATION OF THE RHINE 25 March 2011 SECRETARIAT Establishing the carbon footprint and the specific CO 2 emissions () of inland navigation - Overview of studies establishing

Brésil: take full MA and NT commitments in all modes of supply in accordance with the model schedule in all corresponding CPCs.

11. Transport services A. Maritime transport services Remarque: Vu l échec des négociations sur les services de transport maritime en juin 1996, l UE (sauf l Autriche) n a pas pris d engagements pour ce

11. Transport services A. Maritime transport services Remarque: Vu l échec des négociations sur les services de transport maritime en juin 1996, l UE (sauf l Autriche) n a pas pris d engagements pour ce

The 2004 Guidelines on State aid to maritime transport

European Commission Directorate General for Energy and Transport The 2004 Guidelines on State aid to maritime transport and their recent application by the Commission European Dredging Association General

European Commission Directorate General for Energy and Transport The 2004 Guidelines on State aid to maritime transport and their recent application by the Commission European Dredging Association General

13/11/2013. Logistics Day 2013

Logistics Day 2013 1 1. Current trends of the logistics market 3. Agenda 2014 2 1. Current trends of the logistics market 3 1. Current trends of the logistics market Source: top 100 in European transport

Logistics Day 2013 1 1. Current trends of the logistics market 3. Agenda 2014 2 1. Current trends of the logistics market 3 1. Current trends of the logistics market Source: top 100 in European transport

The road haulage market and its social dimension, including the impact on safety

The road haulage market and its social dimension, including the impact on safety - European Parliament - TRAN Committee Brussels 5 May 2015 What is the ETF? Structure Pan-European trade union organisation;

The road haulage market and its social dimension, including the impact on safety - European Parliament - TRAN Committee Brussels 5 May 2015 What is the ETF? Structure Pan-European trade union organisation;

Cefic Position on Intermodal Transport Network Development

Summary Cefic Position on Intermodal Transport Network Development June 2014 The goal of the European Union to shift 30 % of road transport to intermodal means is very ambitious. The chemical industry

Summary Cefic Position on Intermodal Transport Network Development June 2014 The goal of the European Union to shift 30 % of road transport to intermodal means is very ambitious. The chemical industry

MFFA Belastingadvies Tax Advice

MFFA Belastingadvies Tax Advice Specialized in Expats and International Companies Amsterdam Zwolle Assen The Netherlands VAT in Europe an introduction General comments European Union: 27 member states

MFFA Belastingadvies Tax Advice Specialized in Expats and International Companies Amsterdam Zwolle Assen The Netherlands VAT in Europe an introduction General comments European Union: 27 member states

ANNEX XV APPROXIMATION

579 der Beilagen XXV. GP - Staatsvertrag - 16 Anhang XV in englischer Sprachfassung (Normativer Teil) 1 von 29 ANNEX XV APPROXIMATION EU/GE/Annex XV/en 1 2 von 29 579 der Beilagen XXV. GP - Staatsvertrag

579 der Beilagen XXV. GP - Staatsvertrag - 16 Anhang XV in englischer Sprachfassung (Normativer Teil) 1 von 29 ANNEX XV APPROXIMATION EU/GE/Annex XV/en 1 2 von 29 579 der Beilagen XXV. GP - Staatsvertrag

Interim financial report for the period 1 January to 30 September 2011

Company announcement no. 11/ 18 November Page 1 of 9 Interim financial report for the period 1 January to 30 September Highlights Results improved in the third quarter with a gross profit of USD 8 million

Company announcement no. 11/ 18 November Page 1 of 9 Interim financial report for the period 1 January to 30 September Highlights Results improved in the third quarter with a gross profit of USD 8 million

Austerity policy and consolidation measures hit EU SMEs hardest. Chart 1. SME Business Climate Index 64,7 59,3 55,1

55,1 56,4 59,3 60,7 58,8 64,7 65,5 64,1 69,2 67,5 73,2 72,1 70,8 70,5 78,7 78,6 72,6 75,9 75,5 75,9 The EU Craft and SME Barometer 2012/H2 The EU in recession: SME Climate Index down to 67.5 Austerity

55,1 56,4 59,3 60,7 58,8 64,7 65,5 64,1 69,2 67,5 73,2 72,1 70,8 70,5 78,7 78,6 72,6 75,9 75,5 75,9 The EU Craft and SME Barometer 2012/H2 The EU in recession: SME Climate Index down to 67.5 Austerity

COMMISSIE VOOR HET BANK-, FINANCIE- EN ASSURANTIEWEZEN COMMISSION BANCAIRE, FINANCIÈRE ET DES ASSURANCES BANKING, FINANCE AND INSURANCE COMMISSION

COMMISSIE VOOR HET BANK-, FINANCIE- EN ASSURANTIEWEZEN BANKING, FINANCE AND INSURANCE COMMISSION The financial architecture and control measures of the financial institutions CONFERENCE OF THE FINANCE

COMMISSIE VOOR HET BANK-, FINANCIE- EN ASSURANTIEWEZEN BANKING, FINANCE AND INSURANCE COMMISSION The financial architecture and control measures of the financial institutions CONFERENCE OF THE FINANCE

Recommendation for a COUNCIL RECOMMENDATION. on the 2015 National Reform Programme of Portugal

EUROPEAN COMMISSION Brussels, 13.5.2015 COM(2015) 271 final Recommendation for a COUNCIL RECOMMENDATION on the 2015 National Reform Programme of Portugal and delivering a Council opinion on the 2015 Stability

EUROPEAN COMMISSION Brussels, 13.5.2015 COM(2015) 271 final Recommendation for a COUNCIL RECOMMENDATION on the 2015 National Reform Programme of Portugal and delivering a Council opinion on the 2015 Stability

Public investment: recording in EDP statistics and treatment under the SGP

Public investment: recording in EDP statistics and treatment under the SGP Lourdes Prado Ureña 1 1 Eurostat, Luxembourg, Luxembourg; Lourdes.prado-urena@ec.europa.eu Abstract This paper provides an overview

Public investment: recording in EDP statistics and treatment under the SGP Lourdes Prado Ureña 1 1 Eurostat, Luxembourg, Luxembourg; Lourdes.prado-urena@ec.europa.eu Abstract This paper provides an overview

SOUTH EAST EUROPE TRANSNATIONAL CO-OPERATION PROGRAMME. Terms of reference

SOUTH EAST EUROPE TRANSNATIONAL CO-OPERATION PROGRAMME 3 rd Call for Proposals Terms of reference Efficient access to a SEE coordinated multimodal freight network between ports and landlocked countries

SOUTH EAST EUROPE TRANSNATIONAL CO-OPERATION PROGRAMME 3 rd Call for Proposals Terms of reference Efficient access to a SEE coordinated multimodal freight network between ports and landlocked countries

In electronic form on the EUR-Lex website under document number 32011M6389

EN Case No COMP/M.6389 - ENI / NUON BELGIUM / NUON WIND BELGIUM / NUON POWER GENERATION Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION

EN Case No COMP/M.6389 - ENI / NUON BELGIUM / NUON WIND BELGIUM / NUON POWER GENERATION Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION

COMPTE RENDU SOMMAIRE SUMMARY RECORD

EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR AGRICULTURE AND RURAL DEVELOPMENT Directorate C. Single CMO, economics and analysis of agricultural markets Director Brussels, 05.03.05 ares 978009 (...) D(05)0396

EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR AGRICULTURE AND RURAL DEVELOPMENT Directorate C. Single CMO, economics and analysis of agricultural markets Director Brussels, 05.03.05 ares 978009 (...) D(05)0396

Final Report Main Report. Medium and Long Term Perspectives of IWT in the European Union

Final Report Main Report Medium and Long Term Perspectives of IWT in the European Union Final Report Main Report Medium and Long Term Perspectives of IWT in the European Union This report has been financed

Final Report Main Report Medium and Long Term Perspectives of IWT in the European Union Final Report Main Report Medium and Long Term Perspectives of IWT in the European Union This report has been financed

Market Update 08 2011

Market Update 8 211 Le travail intérimaire en Belgique Uitzendarbeid in België Temporary Agency Work in Belgium TAW activity slightly slows down in August Monthly Evolution 8/211 7/211.52%.26%.9% [Note

Market Update 8 211 Le travail intérimaire en Belgique Uitzendarbeid in België Temporary Agency Work in Belgium TAW activity slightly slows down in August Monthly Evolution 8/211 7/211.52%.26%.9% [Note

The Dutch Health Insurance Sector and EU Competition Law

The Dutch Health Insurance Sector and EU Competition Law Henriette E. AKYUREK-KIEVITS Netherlands Comptetion Authority (Nma) Den Haag, The Netherlands Please do not quote or publish without the permission

The Dutch Health Insurance Sector and EU Competition Law Henriette E. AKYUREK-KIEVITS Netherlands Comptetion Authority (Nma) Den Haag, The Netherlands Please do not quote or publish without the permission

WEALTH MANAGEMENT. Review of tax compliance procedure for undisclosed foreign assets

Olivier HOEBANX Associé BMH AVOCATS Review of tax compliance procedure for undisclosed foreign assets Introduction For several years, many countries have been introducing measures designed to punish taxpayers

Olivier HOEBANX Associé BMH AVOCATS Review of tax compliance procedure for undisclosed foreign assets Introduction For several years, many countries have been introducing measures designed to punish taxpayers

Tax Year 2013 - Income 2012

L UNION FAIT LA FORCE - EENDRACHT MAAKT MACHT Federal Public Service FINANCE NOTIONAL INTEREST DEDUCTION: an innovative Belgian tax incentive Tax Year 2013 - Income 2012 www.invest.belgium.be 2 Content

L UNION FAIT LA FORCE - EENDRACHT MAAKT MACHT Federal Public Service FINANCE NOTIONAL INTEREST DEDUCTION: an innovative Belgian tax incentive Tax Year 2013 - Income 2012 www.invest.belgium.be 2 Content

MAFIOK CONFERENCE SZOLNOK, 29-31 AUGUST 2011.

MAFIOK CONFERENCE SZOLNOK, 29-31 AUGUST 2011. THE INTRODUCTION OF FLEET MANAGEMENT SYSTEM (FMS) AT BI-KA LOGISTICS LTD. THE IMPACT OF FMS ON THE COMPETITIVENESS OF MARKET ACTORS Introduction György Karmazin

MAFIOK CONFERENCE SZOLNOK, 29-31 AUGUST 2011. THE INTRODUCTION OF FLEET MANAGEMENT SYSTEM (FMS) AT BI-KA LOGISTICS LTD. THE IMPACT OF FMS ON THE COMPETITIVENESS OF MARKET ACTORS Introduction György Karmazin

1. Supplemental explanation of FY2014 Q3 financial results

February 2015 1. Supplemental explanation of FY2014 Q3 financial results Overall view Despite the favorable winds of a depreciating yen and lower bunker prices, we could not fully leverage these benefits,

February 2015 1. Supplemental explanation of FY2014 Q3 financial results Overall view Despite the favorable winds of a depreciating yen and lower bunker prices, we could not fully leverage these benefits,

White Paper. Ten Points to Rationalize and Revitalize the United States Maritime Industry

White Paper Ten Points to Rationalize and Revitalize the United States Maritime Industry Cartner & Fiske, LLC 1629 K St., NW Ste. 300 Washington, DC 20006 jacc@cflaw.net John A C Cartner Managing Member

White Paper Ten Points to Rationalize and Revitalize the United States Maritime Industry Cartner & Fiske, LLC 1629 K St., NW Ste. 300 Washington, DC 20006 jacc@cflaw.net John A C Cartner Managing Member

163rd General Report of the Belgian Court of Audit, presented to the House of Representatives on November 6, 2006.

163rd General Report of the Belgian Court of Audit, presented to the House of Representatives on November 6, 2006. Summary 1 Federal Government budget implementation Filing of the Federal Government general

163rd General Report of the Belgian Court of Audit, presented to the House of Representatives on November 6, 2006. Summary 1 Federal Government budget implementation Filing of the Federal Government general

DEVELOPMENT STRATEGY FOR INLAND WATERWAY TRANSPORT IN THE REPUBLIC OF CROATIA (2008-2018)

") REPUBLIC OF CROATIA MINISTRY OF THE SEA, TRANSPORT AND INFRASTRUCTURE DEVELOPMENT STRATEGY FOR INLAND WATERWAY TRANSPORT IN THE REPUBLIC OF CROATIA (2008-2018) April, 2008 Contents page 1 Introduction.

REPUBLIC OF CROATIA MINISTRY OF THE SEA, TRANSPORT AND INFRASTRUCTURE DEVELOPMENT STRATEGY FOR INLAND WATERWAY TRANSPORT IN THE REPUBLIC OF CROATIA (2008-2018) April, 2008 Contents page 1 Introduction.

United Nations Conference on Trade and Development CONTAINER SECURITY: MAJOR INITIATIVES AND RELATED INTERNATIONAL DEVELOPMENTS

United Nations Conference on Trade and Development CONTAINER SECURITY: MAJOR INITIATIVES AND RELATED INTERNATIONAL DEVELOPMENTS Comments received from the United States Government on US Container Security

United Nations Conference on Trade and Development CONTAINER SECURITY: MAJOR INITIATIVES AND RELATED INTERNATIONAL DEVELOPMENTS Comments received from the United States Government on US Container Security

CASES FORWARDED WITH REGARD TO CORRUPTION

BELGIAN FINANCIAL INTELLIGENCE PROCESSING UNIT CTIF-CFI Avenue de la Toison d Or - Gulden Vlieslaan 55/1-1060 Brussels - BELGIUM Tel.: + 32 (0)2 533 72 11 Fax: + 32 (0)2 533 72 00 E-mail: info@ctif-cfi.be

BELGIAN FINANCIAL INTELLIGENCE PROCESSING UNIT CTIF-CFI Avenue de la Toison d Or - Gulden Vlieslaan 55/1-1060 Brussels - BELGIUM Tel.: + 32 (0)2 533 72 11 Fax: + 32 (0)2 533 72 00 E-mail: info@ctif-cfi.be

Currency Options and Swaps: Hedging Currency Risk

Currency Options and Swaps: Hedging Currency Risk By Louis Morel ECON 826 International Finance Queen s Economics Department January 23, 2004 Table of Contents 1. Introduction...2 2. Currency risk exposure...2

Currency Options and Swaps: Hedging Currency Risk By Louis Morel ECON 826 International Finance Queen s Economics Department January 23, 2004 Table of Contents 1. Introduction...2 2. Currency risk exposure...2

Study on the Impact of E-Commerce on Tax and Accounting Activities

World Applied Sciences Journal 24 (4): 534-539, 2013 ISSN 1818-4952 IDOSI Publications, 2013 DOI: 10.5829/idosi.wasj.2013.24.04.329 Study on the Impact of E-Commerce on Tax and Accounting Activities Claudiu

World Applied Sciences Journal 24 (4): 534-539, 2013 ISSN 1818-4952 IDOSI Publications, 2013 DOI: 10.5829/idosi.wasj.2013.24.04.329 Study on the Impact of E-Commerce on Tax and Accounting Activities Claudiu

COMMUNICATION FROM THE COMMISSION TO THE COUNCIL, THE EUROPEAN PARLIAMENT AND THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE

EN EN EN EUROPEAN COMMISSION Brussels, COM(2010) COMMUNICATION FROM THE COMMISSION TO THE COUNCIL, THE EUROPEAN PARLIAMENT AND THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE Removing cross-border tax obstacles

EN EN EN EUROPEAN COMMISSION Brussels, COM(2010) COMMUNICATION FROM THE COMMISSION TO THE COUNCIL, THE EUROPEAN PARLIAMENT AND THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE Removing cross-border tax obstacles

GIS-based location analyses for intermodal terminal landscape in Belgium

GIS-based location analyses for intermodal terminal landscape in Belgium Ethem Pekin Promotor: Prof. Dr. Cathy Macharis MOSI Transport en Logistiek http://www.vub.ac.be/mosi-t Outline Introduction Promoting

GIS-based location analyses for intermodal terminal landscape in Belgium Ethem Pekin Promotor: Prof. Dr. Cathy Macharis MOSI Transport en Logistiek http://www.vub.ac.be/mosi-t Outline Introduction Promoting

FREIGHT FORWARDERS INSURANCE (FFL) Schenker Expeditie Verzekering SEV Indemnity Insurance for the party interested in the goods

Schenker Expeditie Verzekering SEV Indemnity Insurance for the party interested in the goods") FREIGHT FORWARDERS INSURANCE (FFL) Schenker Expeditie Verzekering SEV Indemnity Insurance for the party interested in the goods Policy Holder: Schenker Nederland B.V. Holding Co-insured: Schenker B.V.

FREIGHT FORWARDERS INSURANCE (FFL) Schenker Expeditie Verzekering SEV Indemnity Insurance for the party interested in the goods Policy Holder: Schenker Nederland B.V. Holding Co-insured: Schenker B.V.

002236/EU XXV.GP Eingelangt am 15/11/13

002236/EU XXV.GP Eingelangt am 15/11/13 EUROPEAN MISSION Brussels, 15.11.2013 (2013) 908 final REPORT FROM THE MISSION Lithuania Report prepared in accordance with Article 126(3) of the Treaty EN EN REPORT

002236/EU XXV.GP Eingelangt am 15/11/13 EUROPEAN MISSION Brussels, 15.11.2013 (2013) 908 final REPORT FROM THE MISSION Lithuania Report prepared in accordance with Article 126(3) of the Treaty EN EN REPORT

ESPO Port Performance Dashboard. May 2013

ESPO Port Performance Dashboard May 2013 1 1. INTRODUCTION Part of ESPO s mission is to contribute to public policy in the EU to achieve a safe, efficient and environmentally sustainable European port

ESPO Port Performance Dashboard May 2013 1 1. INTRODUCTION Part of ESPO s mission is to contribute to public policy in the EU to achieve a safe, efficient and environmentally sustainable European port

EDITION 2015 TREND REPORT MARCHÉ CIBLE PARIS

EDITION 15 TREND REPORT MARCHÉ CIBLE PARIS Février 15 5, rue Dombasle - 7515 Paris - Tél. : 1 56 56 87 87 Fax : 1 56 56 87 88 - www.mkg-hospitality.com Completed in April 15 HOTEL SUPPLY / OFFRE HÔTELIERE

EDITION 15 TREND REPORT MARCHÉ CIBLE PARIS Février 15 5, rue Dombasle - 7515 Paris - Tél. : 1 56 56 87 87 Fax : 1 56 56 87 88 - www.mkg-hospitality.com Completed in April 15 HOTEL SUPPLY / OFFRE HÔTELIERE

Position Paper. on the

Position Paper on the Communication from the European Commission to the European Parliament and the Council on Strengthening the Social Dimension of the Economic and Monetary Union (COM (2013) 690) from

Position Paper on the Communication from the European Commission to the European Parliament and the Council on Strengthening the Social Dimension of the Economic and Monetary Union (COM (2013) 690) from

terms and conditions of transport Tank-barge

terms and conditions of transport Tank-barge 2010 Tank-barge terms and conditions of transport 1. Contract 1.1 Execution of order 1.2 Right of cancellation 1.3 Temporary suspension of the contract 2. Vessels

terms and conditions of transport Tank-barge 2010 Tank-barge terms and conditions of transport 1. Contract 1.1 Execution of order 1.2 Right of cancellation 1.3 Temporary suspension of the contract 2. Vessels

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007 IPP Policy Briefs n 10 June 2014 Guillaume Bazot www.ipp.eu Summary Finance played an increasing

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007 IPP Policy Briefs n 10 June 2014 Guillaume Bazot www.ipp.eu Summary Finance played an increasing

Recommendation for a COUNCIL RECOMMENDATION. on Poland s 2014 national reform programme

EUROPEAN COMMISSION Brussels, 2.6.2014 COM(2014) 422 final Recommendation for a COUNCIL RECOMMENDATION on Poland s 2014 national reform programme and delivering a Council opinion on Poland s 2014 convergence

EUROPEAN COMMISSION Brussels, 2.6.2014 COM(2014) 422 final Recommendation for a COUNCIL RECOMMENDATION on Poland s 2014 national reform programme and delivering a Council opinion on Poland s 2014 convergence

PLAN OF ACTION MARITIME TRANSPORT

AFRICAN UNION UNION AFRICAINE UNIÃO AFRICANA SECOND AFRICAN UNION CONFERENCE OF MINISTERS RESPONSIBLE FOR MARITIME TRANSPORT 12-16 OCTOBER 2009 DURBAN, SOUTH AFRICA AU/MT/MIN/DRAFT/Pl.Ac. (II) PLAN OF

AFRICAN UNION UNION AFRICAINE UNIÃO AFRICANA SECOND AFRICAN UNION CONFERENCE OF MINISTERS RESPONSIBLE FOR MARITIME TRANSPORT 12-16 OCTOBER 2009 DURBAN, SOUTH AFRICA AU/MT/MIN/DRAFT/Pl.Ac. (II) PLAN OF

developement at the Danube Commission Ivana Kunc, Horst Schindler Vienna, April 6, 2011 Danube Commission, Budapest

The JS system for information exchange and developement at the Danube Commission Ivana Kunc, Horst Schindler Vienna, April 6, 2011 Danube Commission, Budapest 1. Ship waste management along the Danube

The JS system for information exchange and developement at the Danube Commission Ivana Kunc, Horst Schindler Vienna, April 6, 2011 Danube Commission, Budapest 1. Ship waste management along the Danube

BENDEKOVIC, J. & SIMONIC, T. & NALETINA, D.

IMPORTANCE OF MARKETING STRATEGY FOR ACHIEVEMENT OF COMPETITIVE ADVANTAGE OF CROATIAN ROAD TRANSPORTERS BENDEKOVIC, J. & SIMONIC, T. & NALETINA, D. Abstract: Much attention was not given to marketing and

IMPORTANCE OF MARKETING STRATEGY FOR ACHIEVEMENT OF COMPETITIVE ADVANTAGE OF CROATIAN ROAD TRANSPORTERS BENDEKOVIC, J. & SIMONIC, T. & NALETINA, D. Abstract: Much attention was not given to marketing and

9210/16 ADB/SBC/mz 1 DG B 3A - DG G 1A

Council of the European Union Brussels, 13 June 2016 (OR. en) 9210/16 NOTE From: To: No. Cion doc.: General Secretariat of the Council ECOFIN 455 UEM 202 SOC 319 EMPL 216 COMPET 289 V 335 EDUC 190 RECH

Council of the European Union Brussels, 13 June 2016 (OR. en) 9210/16 NOTE From: To: No. Cion doc.: General Secretariat of the Council ECOFIN 455 UEM 202 SOC 319 EMPL 216 COMPET 289 V 335 EDUC 190 RECH

Trade in Services Agreement (TiSA) Annex on International Maritime Transport Services (February 2015)

Annex on International Maritime Transport Services (February 2015)") Trade in Services Agreement (TiSA) Annex on International Maritime Transport Services (February 2015) WikiLeaks release: June 3, 2015 Keywords: TiSA, Trade in Services Agreement, WTO, GATS, G20, BCBS,

Trade in Services Agreement (TiSA) Annex on International Maritime Transport Services (February 2015) WikiLeaks release: June 3, 2015 Keywords: TiSA, Trade in Services Agreement, WTO, GATS, G20, BCBS,

MARITIME LIEN FOR SEAFARERS WAGES IN GERMANY. This document is not intended to be legal advice, nor does it constitute legal advice.

MARITIME LIEN FOR SEAFARERS WAGES IN GERMANY This Guide deals with the rights of seafarers of any nationality to unpaid or underpaid wages in respect of German flagged ships, and foreign ships which are

MARITIME LIEN FOR SEAFARERS WAGES IN GERMANY This Guide deals with the rights of seafarers of any nationality to unpaid or underpaid wages in respect of German flagged ships, and foreign ships which are

FINAL TERMS DATED 12 JANUARY 2012

FINAL TERMS DATED 12 JANUARY 2012 NOK 50,000,000 4.375% FIXED COUPON NOTE DUE 18 AUGUST 2015 TRANCHE NO. 3 100% CAPITAL PROTECTION ISSUE PRICE: 102% This issue of the 3rd tranche of Notes described herein

FINAL TERMS DATED 12 JANUARY 2012 NOK 50,000,000 4.375% FIXED COUPON NOTE DUE 18 AUGUST 2015 TRANCHE NO. 3 100% CAPITAL PROTECTION ISSUE PRICE: 102% This issue of the 3rd tranche of Notes described herein

How To Develop A Waterborne

Waterborne TP and Vessels for the Future Initiative in H2020 Luciano Manzon WATERBORNE Secretary, SEARDI Chairman the RDI Group of SEA Europe 27 November Santiago de Compostela ETP WATERBORNE All the Stakeholders

Waterborne TP and Vessels for the Future Initiative in H2020 Luciano Manzon WATERBORNE Secretary, SEARDI Chairman the RDI Group of SEA Europe 27 November Santiago de Compostela ETP WATERBORNE All the Stakeholders

FINAL TERMS DATED 11 APRIL 2011

FINAL TERMS DATED 11 APRIL 2011 EUR 100,000,000 EURIBOR 3M FLOARED FLOATING RATE NOTE (MIN CP 3.00%); 3% RENTE PROTECT OBLIGATIE II DUE 5 MAY 2016 100% CAPITAL PROTECTION ISSUE PRICE: 100% (INDICATIVE)

FINAL TERMS DATED 11 APRIL 2011 EUR 100,000,000 EURIBOR 3M FLOARED FLOATING RATE NOTE (MIN CP 3.00%); 3% RENTE PROTECT OBLIGATIE II DUE 5 MAY 2016 100% CAPITAL PROTECTION ISSUE PRICE: 100% (INDICATIVE)

Recommendation for a COUNCIL RECOMMENDATION. on the 2015 National Reform Programme of Slovenia

EUROPEAN COMMISSION Brussels, 13.5.2015 COM(2015) 273 final Recommendation for a COUNCIL RECOMMENDATION on the 2015 National Reform Programme of Slovenia and delivering a Council opinion on the 2015 Stability

EUROPEAN COMMISSION Brussels, 13.5.2015 COM(2015) 273 final Recommendation for a COUNCIL RECOMMENDATION on the 2015 National Reform Programme of Slovenia and delivering a Council opinion on the 2015 Stability

PART IV: SECTOR SPECIFIC RULES

Page 1 PART IV: SECTOR SPECIFIC RULES GUIDANCE ON STATE AID TO SHIP MANAGEMENT COMPANIES 1. Scope This Chapter deals with the eligibility of crew and technical managers of ships for the reduction of corporate

Page 1 PART IV: SECTOR SPECIFIC RULES GUIDANCE ON STATE AID TO SHIP MANAGEMENT COMPANIES 1. Scope This Chapter deals with the eligibility of crew and technical managers of ships for the reduction of corporate

CURRENT TRENDS AND DEVELOPMENT OF THE AUTOMOTIVE INDUSTRY IN THE SLOVAK REPUBLIC

CURRENT TRENDS AND DEVELOPMENT OF THE AUTOMOTIVE INDUSTRY IN THE SLOVAK REPUBLIC Martin Jurkovič 1, Tomáš Kalina 2 Summary: Automakers often use the services of logistics operators who provide comprehensive

CURRENT TRENDS AND DEVELOPMENT OF THE AUTOMOTIVE INDUSTRY IN THE SLOVAK REPUBLIC Martin Jurkovič 1, Tomáš Kalina 2 Summary: Automakers often use the services of logistics operators who provide comprehensive

EMERGENCY PLAN FOR SECURITY OF SUPPLY OF NATURAL GAS THE NETHERLANDS

EMERGENCY PLAN FOR SECURITY OF SUPPLY OF NATURAL GAS THE NETHERLANDS Based on Regulation (EU) No 994/2010 of the European Parliament and of the Council of 20 October 2010 concerning measures to safeguard

EMERGENCY PLAN FOR SECURITY OF SUPPLY OF NATURAL GAS THE NETHERLANDS Based on Regulation (EU) No 994/2010 of the European Parliament and of the Council of 20 October 2010 concerning measures to safeguard

ECTRI POSITION PAPER. December 2012

ECTRI POSITION PAPER Research Needs in the field of Transport Funding, Procurement and Public Private Partnerships (PPP) The European Conference of Transport Research Institutes (ECTRI) is an international

ECTRI POSITION PAPER Research Needs in the field of Transport Funding, Procurement and Public Private Partnerships (PPP) The European Conference of Transport Research Institutes (ECTRI) is an international

COMMUNICATION FROM THE COMMISSION 2014 DRAFT BUDGETARY PLANS OF THE EURO AREA: OVERALL ASSESSMENT OF THE BUDGETARY SITUATION AND PROSPECTS

EUROPEAN COMMISSION Brussels, 15.11.2013 COM(2013) 900 final COMMUNICATION FROM THE COMMISSION 2014 DRAFT BUDGETARY PLANS OF THE EURO AREA: OVERALL ASSESSMENT OF THE BUDGETARY SITUATION AND PROSPECTS EN

EUROPEAN COMMISSION Brussels, 15.11.2013 COM(2013) 900 final COMMUNICATION FROM THE COMMISSION 2014 DRAFT BUDGETARY PLANS OF THE EURO AREA: OVERALL ASSESSMENT OF THE BUDGETARY SITUATION AND PROSPECTS EN

PROSPECTS FOR BETTER COMPENSATION FOR ECOLOGICAL DAMAGE RESULTING FROM ACCIDENTS IN EUROPEAN MARINE WATERS

CRPMDTR110 077 B3 CONFERENCE DES REGIONS PERIPHERIQUES MARITIMES D EUROPE CONFERENCE OF PERIPHERAL MARITIME REGIONS OF EUROPE 6, rue Saint-Martin, 35700 RENNES - FR Tel. : + 33 (0)2 99 35 40 50 - Fax :

CRPMDTR110 077 B3 CONFERENCE DES REGIONS PERIPHERIQUES MARITIMES D EUROPE CONFERENCE OF PERIPHERAL MARITIME REGIONS OF EUROPE 6, rue Saint-Martin, 35700 RENNES - FR Tel. : + 33 (0)2 99 35 40 50 - Fax :

Estonia and the European Debt Crisis Juhan Parts

Estonia and the European Debt Crisis Juhan Parts Estonia has had a quick recovery from the recent recession and its economy is in better shape than before the crisis. It is now much leaner and significantly

Estonia and the European Debt Crisis Juhan Parts Estonia has had a quick recovery from the recent recession and its economy is in better shape than before the crisis. It is now much leaner and significantly

GREEN SHORTSEA SHIPPING The shipowners perspective Juan Riva President European Community Shipowners Associations ECSA Flota Suardíaz

GREEN SHORTSEA SHIPPING The shipowners perspective Juan Riva President European Community Shipowners Associations ECSA Flota Suardíaz European Community Shipowners Associations ECSA Established in 1965,

GREEN SHORTSEA SHIPPING The shipowners perspective Juan Riva President European Community Shipowners Associations ECSA Flota Suardíaz European Community Shipowners Associations ECSA Established in 1965,

Meeting with Analysts

CNB s New Forecast (Inflation Report II/2015) Meeting with Analysts Petr Král Prague, 11 May, 2015 1 Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

CNB s New Forecast (Inflation Report II/2015) Meeting with Analysts Petr Král Prague, 11 May, 2015 1 Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

CIF Cost, Insurance & Freight

CIF Cost, Insurance & Freight Cost, Insurance and Freight means that the seller delivers when the goods pass the ship's rail in the port of shipment. The seller must pay the costs and freight necessary

CIF Cost, Insurance & Freight Cost, Insurance and Freight means that the seller delivers when the goods pass the ship's rail in the port of shipment. The seller must pay the costs and freight necessary

River Information Services

River Information Services Ivo ten Broeke Programme Manager RIS Rhine Commissioner CCNR Contents RIS definition RIS background and development RIS implementation RIS services RIS video: http://youtu.be/vbuhknjmyew

River Information Services Ivo ten Broeke Programme Manager RIS Rhine Commissioner CCNR Contents RIS definition RIS background and development RIS implementation RIS services RIS video: http://youtu.be/vbuhknjmyew

Item 11 on the agenda

EXECUTIVE COMMITTEE Brussels, 17-18 March 2009 EC. 183 Item 11 on the agenda More protection of workers, and preventing protectionism The Executive Committee is asked: to discuss the document with a view

EXECUTIVE COMMITTEE Brussels, 17-18 March 2009 EC. 183 Item 11 on the agenda More protection of workers, and preventing protectionism The Executive Committee is asked: to discuss the document with a view

MARKET OBSERVATION. for inland navigation in Europe 2007-1. Central Commission for Navigation on the Rhine

MARKET OBSERVATION 2007-1 for inland navigation in Europe Central Commission for Navigation on the Rhine European Commission Directorate-General for Energy and Transport Market Observation for inland navigation

MARKET OBSERVATION 2007-1 for inland navigation in Europe Central Commission for Navigation on the Rhine European Commission Directorate-General for Energy and Transport Market Observation for inland navigation

Country Profile: Wallonia (Belgium)

") Country Profile: Wallonia (Belgium) Last updated: 15/10/2012 1 Implementation of Tracking Systems 1.1 Electricity Disclosure In Wallonia disclosure is implemented by order of the Walloon Government: [1]

Country Profile: Wallonia (Belgium) Last updated: 15/10/2012 1 Implementation of Tracking Systems 1.1 Electricity Disclosure In Wallonia disclosure is implemented by order of the Walloon Government: [1]

VIVRE ET TRAVAILLER EN BELGIQUE LEVEN EN WERKEN IN BELGIË LIVING AND WORKING IN BELGIUM

Services Publics de l emploi / Openbare Arbeidsbemiddelingsdiensten / Public Employment Services ACTIRIS - Office Régional Bruxellois de l'emploi / Brusselse Gewestelijke Dienst voor Arbeidsbemiddeling

Services Publics de l emploi / Openbare Arbeidsbemiddelingsdiensten / Public Employment Services ACTIRIS - Office Régional Bruxellois de l'emploi / Brusselse Gewestelijke Dienst voor Arbeidsbemiddeling

Trends in the development of European inland freight transport

Scientific Journals Maritime University of Szczecin Zeszyty Naukowe Akademia Morska w Szczecinie 2014, 37(109) pp. 66 71 2014, 37(109) s. 66 71 ISSN 1733-8670 Trends in the development of European inland

Scientific Journals Maritime University of Szczecin Zeszyty Naukowe Akademia Morska w Szczecinie 2014, 37(109) pp. 66 71 2014, 37(109) s. 66 71 ISSN 1733-8670 Trends in the development of European inland

Inventarisatie toepassing EU btw-regelgeving op hoveniersdiensten

Inventarisatie toepassing EU btw-regelgeving op hoveniersdiensten Governments can stimulate citizens to contribute to ecological, social and economic goals. By using a reduced VAT-rate for private gardening

Inventarisatie toepassing EU btw-regelgeving op hoveniersdiensten Governments can stimulate citizens to contribute to ecological, social and economic goals. By using a reduced VAT-rate for private gardening

THE INTELLIGENT CONTAINER - AN ESTIMATION OF BENEFITS AND COSTS

THE INTELLIGENT CONTAINER - AN ESTIMATION OF BENEFITS AND COSTS Marius Veigt, Patrick Dittmer, Rasmus Haass, Franziska Wittig BIBA - Bremer Institut für Produktion und Logistik GmbH Hochschulring 20 28359

THE INTELLIGENT CONTAINER - AN ESTIMATION OF BENEFITS AND COSTS Marius Veigt, Patrick Dittmer, Rasmus Haass, Franziska Wittig BIBA - Bremer Institut für Produktion und Logistik GmbH Hochschulring 20 28359

THE ECONOMIC IMPACTS OF THE PORTS OF LOUISIANA AND THE MARITIME INDUSTRY

THE ECONOMIC IMPACTS OF THE PORTS OF LOUISIANA AND THE MARITIME INDUSTRY Prepared by: TIMOTHY P. RYAN UNIVERSITY OF NEW ORLEANS February, 2001 EXECUTIVE SUMMARY The ports of Louisiana and the maritime

THE ECONOMIC IMPACTS OF THE PORTS OF LOUISIANA AND THE MARITIME INDUSTRY Prepared by: TIMOTHY P. RYAN UNIVERSITY OF NEW ORLEANS February, 2001 EXECUTIVE SUMMARY The ports of Louisiana and the maritime

PUBLIC CONSULTATION 1. INTRODUCTION

PUBLIC CONSULTATION ON LIMITATION PERIODS FOR COMPENSATION CLAIMS OF VICTIMS OF CROSS-BORDER ROAD TRAFFIC ACCIDENTS IN THE EUROPEAN UNION 1. INTRODUCTION For more than 10 years the European Union has developed

PUBLIC CONSULTATION ON LIMITATION PERIODS FOR COMPENSATION CLAIMS OF VICTIMS OF CROSS-BORDER ROAD TRAFFIC ACCIDENTS IN THE EUROPEAN UNION 1. INTRODUCTION For more than 10 years the European Union has developed

Steel Production in Czech Republic. Eurofer Economic Committee Meeting Brussels April 2015

Steel Production in Czech Republic Eurofer Economic Committee Meeting Brussels April 2015 Main Economic Indicators % Change Czech Republic 10 11 12 13 14 15E 16P Private Consumption 1,0 0.2-1,8 0,4 1,7

Steel Production in Czech Republic Eurofer Economic Committee Meeting Brussels April 2015 Main Economic Indicators % Change Czech Republic 10 11 12 13 14 15E 16P Private Consumption 1,0 0.2-1,8 0,4 1,7

Briefing on Personnel Leasing in the European Union

Annex 13 Briefing on Personnel Leasing in the European Union 1. Economic significance In the EU (15 Member States; there are not yet any figures of the 10 new Member States) there are about 1,4 million

Annex 13 Briefing on Personnel Leasing in the European Union 1. Economic significance In the EU (15 Member States; there are not yet any figures of the 10 new Member States) there are about 1,4 million

COMITÉ EUROPÉEN DES ASSURANCES

COMITÉ EUROPÉEN DES ASSURANCES SECRÉTARIAT GÉNÉRAL 3bis, rue de la Chaussée d'antin F 75009 Paris Tél. : +33 1 44 83 11 83 Fax : +33 1 47 70 03 75 Web : cea.assur.org DÉLÉGATION À BRUXELLES Square de Meeûs,

COMITÉ EUROPÉEN DES ASSURANCES SECRÉTARIAT GÉNÉRAL 3bis, rue de la Chaussée d'antin F 75009 Paris Tél. : +33 1 44 83 11 83 Fax : +33 1 47 70 03 75 Web : cea.assur.org DÉLÉGATION À BRUXELLES Square de Meeûs,

Mexico Shipments Made Simple. Third-party logistics providers help streamline the U.S. Mexico cross-border process WHITE PAPER

Mexico Shipments Made Simple Third-party logistics providers help streamline the U.S. Mexico cross-border process WHITE PAPER Introduction With the cost of manufacturing rising in Asia, many companies

Mexico Shipments Made Simple Third-party logistics providers help streamline the U.S. Mexico cross-border process WHITE PAPER Introduction With the cost of manufacturing rising in Asia, many companies

London International Shipping Week. 10 September 2015

London International Shipping Week 10 September 2015 Session 3 13:15 14:45 The role of governments in a global maritime industry: Should governments lend their support and how can they participate in growing

London International Shipping Week 10 September 2015 Session 3 13:15 14:45 The role of governments in a global maritime industry: Should governments lend their support and how can they participate in growing

Transport and Logistics Chain Intermediaries

Transport and Logistics Chain Intermediaries FIATA World Congress 2014, Istanbul 16 October 2014 Ms Isabelle Bon-Garcin President of the IRU Commission on Legal Affairs This is the IRU 2 Evolution of IRU

Transport and Logistics Chain Intermediaries FIATA World Congress 2014, Istanbul 16 October 2014 Ms Isabelle Bon-Garcin President of the IRU Commission on Legal Affairs This is the IRU 2 Evolution of IRU

Indicator fact sheet Fishing fleet trends

Indicator fact sheet Fishing fleet trends Key message: The big EU 15 fishing fleet (1989 2000) has decreased in numbers of vessels (10 %), in tonnage (6 %) and power (12 %) The much smaller EFTA fishing

Indicator fact sheet Fishing fleet trends Key message: The big EU 15 fishing fleet (1989 2000) has decreased in numbers of vessels (10 %), in tonnage (6 %) and power (12 %) The much smaller EFTA fishing

The Training Material on Multimodal Transport Law and Operations has been produced under Project Sustainable Human Resource Development in Logistic

The Training Material on Multimodal Transport Law and Operations has been produced under Project Sustainable Human Resource Development in Logistic Services for ASEAN Member States with the support from

The Training Material on Multimodal Transport Law and Operations has been produced under Project Sustainable Human Resource Development in Logistic Services for ASEAN Member States with the support from

Recommendation for a COUNCIL RECOMMENDATION. on the 2015 National Reform Programme of Bulgaria

EUROPEAN COMMISSION Brussels, 13.5.2015 COM(2015) 253 final Recommendation for a COUNCIL RECOMMENDATION on the 2015 National Reform Programme of Bulgaria and delivering a Council opinion on the 2015 Convergence

EUROPEAN COMMISSION Brussels, 13.5.2015 COM(2015) 253 final Recommendation for a COUNCIL RECOMMENDATION on the 2015 National Reform Programme of Bulgaria and delivering a Council opinion on the 2015 Convergence

COMMISSION STAFF WORKING DOCUMENT THE FUTURE OF THE COMMISSION GUIDELINES ON THE APPLICATION OF ARTICLE 101 TFEU TO MARITIME TRANSPORT SERVICES

EUROPEAN COMMISSION COMMISSION STAFF WORKING DOCUMENT THE FUTURE OF THE COMMISSION GUIDELINES ON THE APPLICATION OF ARTICLE 101 TFEU TO MARITIME TRANSPORT SERVICES EN EN This document is a European Commission

EUROPEAN COMMISSION COMMISSION STAFF WORKING DOCUMENT THE FUTURE OF THE COMMISSION GUIDELINES ON THE APPLICATION OF ARTICLE 101 TFEU TO MARITIME TRANSPORT SERVICES EN EN This document is a European Commission

AS PUBLISHED IN THE SUPPLEMENT OF THE BULLETIN OF THE CVMQ OF JULY 11, 2003, VOL. 34 N 27

AS PUBLISHED IN THE SUPPLEMENT OF THE BULLETIN OF THE CVMQ OF JULY 11, 2003, VOL. 34 N 27 RÈGLEMENT MODIFIANT LA VERSION ANGLAISE DU RÈGLEMENT 21-101 SUR LE FONCTIONNEMENT DU MARCHÉ PARTIE 1 MODIFICATIONS

AS PUBLISHED IN THE SUPPLEMENT OF THE BULLETIN OF THE CVMQ OF JULY 11, 2003, VOL. 34 N 27 RÈGLEMENT MODIFIANT LA VERSION ANGLAISE DU RÈGLEMENT 21-101 SUR LE FONCTIONNEMENT DU MARCHÉ PARTIE 1 MODIFICATIONS

Charter owners view on container lines grouping into alliances

Charter owners view on container lines grouping into alliances Results Results of of the the 8th 8th Maritime Maritime Trend Trend Barometer Barometer Hamburg, Hamburg, February February 2014 2014 2 Contents

Charter owners view on container lines grouping into alliances Results Results of of the the 8th 8th Maritime Maritime Trend Trend Barometer Barometer Hamburg, Hamburg, February February 2014 2014 2 Contents

Impact Assessment of the Shipping Cluster on the Greek Economy & Society

Impact Assessment of the Shipping Cluster on the Greek Economy & Society May 2013 The full study can be found at http://www.bcg.gr/media - 1 - Impact Assessment of the Shipping Cluster on the Greek Economy

Impact Assessment of the Shipping Cluster on the Greek Economy & Society May 2013 The full study can be found at http://www.bcg.gr/media - 1 - Impact Assessment of the Shipping Cluster on the Greek Economy

Statistical Review of the Annual Report on the Performance of Maritime Safety Inspection in Croatia

Statistical Review of the Annual Report on the Performance of Maritime Safety Inspection in Croatia Tatjana Stanivuk a, Boris Medić a, Marta Medić b This paper provides a detailed analysis of the annual

Statistical Review of the Annual Report on the Performance of Maritime Safety Inspection in Croatia Tatjana Stanivuk a, Boris Medić a, Marta Medić b This paper provides a detailed analysis of the annual

Financing China s Energy Transportation:

SHIPPING CHINA ENERGY 2008 Financing China s Energy Transportation: Ship Lending and Leasing Dr. Yan Jun Industrial and Commercial Bank of China April 25, 2008 Shanghai -1- AGENDA I. I. CHINESE FACTOR

SHIPPING CHINA ENERGY 2008 Financing China s Energy Transportation: Ship Lending and Leasing Dr. Yan Jun Industrial and Commercial Bank of China April 25, 2008 Shanghai -1- AGENDA I. I. CHINESE FACTOR

Eurotunnel 2020 potential traffic estimate (Extract)

") Strategy 2020 potential traffic estimate (Extract) Executive summary (1/3) Context and objectives The cross-channel passenger rail traffic was 9.91mpax in 2012, split between Brussels - London and Paris

Strategy 2020 potential traffic estimate (Extract) Executive summary (1/3) Context and objectives The cross-channel passenger rail traffic was 9.91mpax in 2012, split between Brussels - London and Paris

General Terms and Conditions

General Terms and Conditions for Ship Brokers and Ship Agents in Germany (In case of doubt the German wording is valid) Art. 1 Scope (1) The General Terms and Conditions set out below are applicable for

General Terms and Conditions for Ship Brokers and Ship Agents in Germany (In case of doubt the German wording is valid) Art. 1 Scope (1) The General Terms and Conditions set out below are applicable for

foundations for success québec infrastructures plan

foundations for success québec infrastructures plan The content of this publication was drafted by the Secrétariat du Conseil du trésor. This edition was produced by the Direction des communications. Legal

foundations for success québec infrastructures plan The content of this publication was drafted by the Secrétariat du Conseil du trésor. This edition was produced by the Direction des communications. Legal

FINAL TERMS DATED 15 JUNE 2011

FINAL TERMS DATED 15 JUNE 2011 EUR 10,000,000 AEX INDEX COUPON NOTES (BARRIER LEVEL 270) DUE 23 JUNE 2016 100% CAPITAL PROTECTION ISSUE PRICE: 100% THE SECURITIES HAVE NOT BEEN AND WILL NOT BE REGISTERED

FINAL TERMS DATED 15 JUNE 2011 EUR 10,000,000 AEX INDEX COUPON NOTES (BARRIER LEVEL 270) DUE 23 JUNE 2016 100% CAPITAL PROTECTION ISSUE PRICE: 100% THE SECURITIES HAVE NOT BEEN AND WILL NOT BE REGISTERED

Accident risk of Norwegian-operated cargo ships in Norwegian waters

Summary: Accident risk of Norwegian-operated cargo ships in Norwegian waters TØI Report /2014 Authors: Tor-Olav Nævestad, Elise Caspersen, Inger Beate Hovi, Torkel Bjørnskau & Christian Steinsland Oslo

Summary: Accident risk of Norwegian-operated cargo ships in Norwegian waters TØI Report /2014 Authors: Tor-Olav Nævestad, Elise Caspersen, Inger Beate Hovi, Torkel Bjørnskau & Christian Steinsland Oslo

CMNI-Convention in relation to

-Convention in relation to the Bratislava Agreements Zsolt Kovács Gárdos, Füredi, Mosonyi, Tomori Law Firm 6th IVR-Colloquium 22nd and 23rd January 2009 Prague HISTORY IN BRIEF Unlike on the Rhine, alongside

-Convention in relation to the Bratislava Agreements Zsolt Kovács Gárdos, Füredi, Mosonyi, Tomori Law Firm 6th IVR-Colloquium 22nd and 23rd January 2009 Prague HISTORY IN BRIEF Unlike on the Rhine, alongside

MARINE LIABILITY PRODUCTS

MARINE LIABILITY PRODUCTS www.prosightspecialty.com/marine Tim McAndrew tmcandrew@prosightspecialty.com 212-551-0618 Tom Zdrojeski tzdrojeski@prosightspecialty.com 212-551-0623 Robert Palmer rpalmer@prosightspecialty.com

MARINE LIABILITY PRODUCTS www.prosightspecialty.com/marine Tim McAndrew tmcandrew@prosightspecialty.com 212-551-0618 Tom Zdrojeski tzdrojeski@prosightspecialty.com 212-551-0623 Robert Palmer rpalmer@prosightspecialty.com

MAKK Prepared for the WWF-Danube Carpathian Programme Prepared by MAKK Hungarian Environmental Economics Centre, with contribution from WWF-DCP

Socio-economic considerations on Plans for Inland Waterway Transport for the Danube River MAKK Prepared for the WWF-Danube Carpathian Programme Prepared by MAKK Hungarian Environmental Economics Centre,

Socio-economic considerations on Plans for Inland Waterway Transport for the Danube River MAKK Prepared for the WWF-Danube Carpathian Programme Prepared by MAKK Hungarian Environmental Economics Centre,

Belgium Logistics, your competitive gateway to Europe

Belgium Logistics, your competitive gateway to Europe 1 Preface Belgium is the perfect country in which to set up a European logistics base, headquarters or distribution center because the country s infrastructure,

Belgium Logistics, your competitive gateway to Europe 1 Preface Belgium is the perfect country in which to set up a European logistics base, headquarters or distribution center because the country s infrastructure,

FINAL TERMS DATED 15 JUNE 2011

FINAL TERMS DATED 15 JUNE 2011 EUR 10,000,000 EURO STOXX 50 INDEX COUPON NOTES (BARRIER LEVEL 2250) DUE 23 JUNE 2016 100% CAPITAL PROTECTION ISSUE PRICE: 100% THE SECURITIES HAVE NOT BEEN AND WILL NOT

FINAL TERMS DATED 15 JUNE 2011 EUR 10,000,000 EURO STOXX 50 INDEX COUPON NOTES (BARRIER LEVEL 2250) DUE 23 JUNE 2016 100% CAPITAL PROTECTION ISSUE PRICE: 100% THE SECURITIES HAVE NOT BEEN AND WILL NOT

ENG - 2015. Federal Public Service FINANCE

STRENGTH THROUGH UNITY ENG - 2015 Federal Public Service FINANCE FOREWORD This brochure provides general information on the reform of the Belgian Tax Shelter system, based on the Law of 12.05.2014, mentioned

STRENGTH THROUGH UNITY ENG - 2015 Federal Public Service FINANCE FOREWORD This brochure provides general information on the reform of the Belgian Tax Shelter system, based on the Law of 12.05.2014, mentioned

COMMUNICATION FROM THE COMMISSION. replacing the Communication from the Commission on

EUROPEAN COMMISSION Brussels, 28.10.2014 COM(2014) 675 final COMMUNICATION FROM THE COMMISSION replacing the Communication from the Commission on Harmonized framework for draft budgetary plans and debt

EUROPEAN COMMISSION Brussels, 28.10.2014 COM(2014) 675 final COMMUNICATION FROM THE COMMISSION replacing the Communication from the Commission on Harmonized framework for draft budgetary plans and debt

Owner of the type approval Titulaire de l agrément de type Inhaber der Typgenehmigung Houder van de typegoedkeuring

8.2.2016 List of approved Inland AIS equipment in accordance with the Rhine Vessel Inspection Regulations Liste des appareils AIS Intérieur agréés conformément au Règlement de Visite des Bateaux du Rhin

8.2.2016 List of approved Inland AIS equipment in accordance with the Rhine Vessel Inspection Regulations Liste des appareils AIS Intérieur agréés conformément au Règlement de Visite des Bateaux du Rhin

Authorisation and Restriction Newsletter

Authorisation and Restriction Newsletter August 2010, N 1 The information contained in this document is intended for guidance only and whilst the information is provided in utmost good faith and has been

Authorisation and Restriction Newsletter August 2010, N 1 The information contained in this document is intended for guidance only and whilst the information is provided in utmost good faith and has been

Optimizing Inventory Management at SABIC

escf Operations Practices: Insights from Science European Supply Chain Forum Optimizing Inventory Management at SABIC dr. V.C.S. Wiers Where innovation starts 1 Margin pressure from the Middle East The

escf Operations Practices: Insights from Science European Supply Chain Forum Optimizing Inventory Management at SABIC dr. V.C.S. Wiers Where innovation starts 1 Margin pressure from the Middle East The