CEO s review. Capital Markets Day President and CEO Pertti Korhonen. November 30 - Hamburg, Germany. Outotec - All rights reserved

|

|

|

- Rosaline Kennedy

- 8 years ago

- Views:

Transcription

1 CEO s review Capital Markets Day 2012 President and CEO Pertti Korhonen November 30 - Hamburg, Germany

2 OUTOTEC TODAY 2

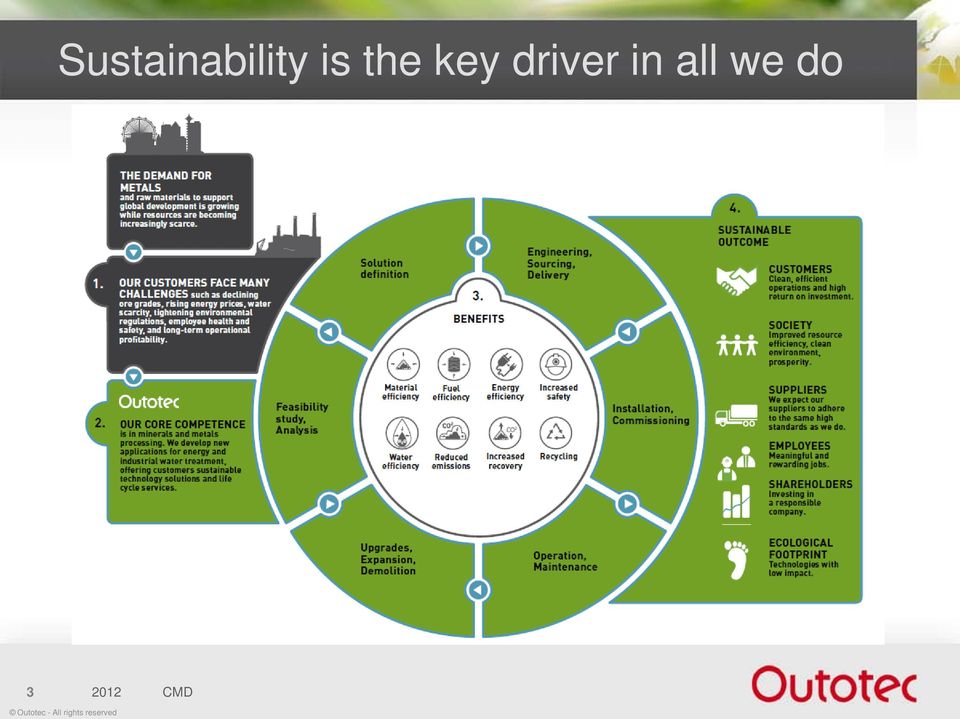

3 Sustainability is the key driver in all we do 3

4 Life cycle offerings delivered globally through four business areas Market Operations Supply Business Infrastructure Strategy Technology Management Non-ferrous Solutions Ferrous Solutions Energy, Light Metals & Environmental Solutions Services Finance & Control Legal Affairs Human Capital Communications and Corporate Responsibility for the processing of copper, nickel, zinc, lead, gold, silver, platinum group metals, industrial minerals as well as valuable minor metals for the production of concentrates, industrial minerals, pellets, sinter, pig iron, direct reduced iron, ferroalloys, and titanium feedstock for oil shale, oil sands and biomass processing, light metals and sulfuric acid production, off-gas handling, and industrial water treatment providing life cycle services partners peers competitors Competitive landscape is fragmented Jacobs (Aker), Andritz, Bateman Engineering/Litwin, BGRIMM, CITIC, Delcor, EPCM, FLS, Krupp Polysius, Mesco, Metso, PERI, Siemens, SMS Meer, Thermo Fisher, WesTech, Xstrata Jacobs (Aker), Bateman Engineering, BSIET, Danieli, Downer, FLS, Kobelco, Metso, Midrex, Siemens, SMS Siemag, Tenova Pyromet Jacobs (Aker), Alcan, Alstom, Brochot, FLS, Foster Wheeler, GEA, MECS, Siemens, Solios, Stultz, Veolia FLS, Metso, local competitors, internal maintenance departments Engineering: AMEC, Ausenco, Bechtel, Chalieco, Enfi, Fluor, Hatch, MCC, NERIN, NFC, SNC-Lavalin, SRK, Worley Parsons 4

5 Over a century as a technology leader, active M&A with 12 acquisitions since 2010 Year Listing on the Helsinki Stock Exchange OUTOKUMPU TECHNOLOGY BACKFILL SPECIALISTS TME GROUP, DEMIL MANUTENÇÃO INDUSTRIAL NUMCORE KILN SERVICES VPF, ASH DEC MILLTEAM EDMESTON AUBURN 2001 BOLIDEN CONTECH NORDBERG GRINDING MILLS OUTOKUMPU KHD ALUMINIUM AISCO, SUPAFLO WENMEC LURGI METALLURGIE LAROX AUSMELT ENERGY PRODUCTS OF IDAHO

6 Diversified sales split with roughly 2/3 coming from emerging markets Sales by destination Sales by end product 2011 (2010) 2011 (2010) Americas 31% (34%) EMEA (incl. CIS) 44% (38%) Other *) 11% (16%) Other metals Copper 33% (25%) 8% (6%) Sulfuric acid 5% (8%) Nickel 6% (7%) Zinc 3% (5%) Asia Pacific 25% (28%) Precious metals 10% (11%) Ferroalloys 4% (3%) *) incl. energy, water and chemical industry Aluminum 5% (7%) Iron 15% (12%) 6

Asia Pacific 25% (28%) Precious metals 10% (11%) Ferroalloys 4% (3%) *) incl.")

7 MARKET REVIEW INDUSTRY S MEGATRENDS PROVIDE ATTRACTIVE GROWTH OPPORTUNITIES FOR OUTOTEC 7

8 Emerging markets GDP growth is driving metals demand GDP (PPP) growth in BRIC and Emerging vs Advanced economies China 150 India 140 Russia 130 Brazil Emerging and developing economies Advanced economies Source: IMF, October

9 Metals demand has stayed on a good level and is expected to continue to grow 140 Demand growth for selected commodities (2011=100) Alumina Aluminium Copper Zinc Nickel Gold Iron Ore S-Acid Source: Brook Hunt, Macquarie, CRU /July-October

10 Middle class is growing globally and drives demand for metals 10

11 Constantly increasing demand for sustainable technologies drives Outotec s business Peak oil Water Emissions Energy Ore grade Ore grades are declining and becoming more complex Making metals is energy-intensive Cleaner solutions must be developed to limit CO 2 and other emissions Water availability and pollution are critical issues Alternative energy sources are needed We have a deep knowledge of minerals and metals processing technologies We provide the most energy efficient process technologies in the industry Adoption of our best practice technologies worldwide could save million tonnes of CO 2 in nonferrous metals production only Our solutions provide significant reduction in fresh water consumption and water loss and increase recycling of process water We enable environmentally sustainable use of waste, oil shale, oil sand and biomass as new alternative energy sources Recycling More recycling is needed We provide technologies for metals recycling 11

12 Economic growth and its impact on environment can be decoupled by using advanced technologies Welfare Environmental impact Eco-efficiency Advanced technologies Environmental impact Source: 12

13 Significant new production capacity is needed to meet the increasing metals demand with degrading ore grades 13

14 OUTOTEC S STRATEGY IN ACTION 14

15 We launched our current strategy in 2010 Our strategic intent: The leading provider of sustainable minerals and metals processing solutions, Sustainable life cycle solutions enabling customers get the best return on investment and license to operate. and an innovative provider of sustainable energy and water processing solutions. Services Best return on customer s investment with minimized ecological impact Strong local market presence and global integrated operations Our mission: Sustainable use of Earth s natural resources. Project delivery Systems integration Proprietary equipment Technology Increasing value through life cycle solutions Applying core technologies in new attractive growth areas Leadership in technology and innovation Improving cost competitiveness and scalability Sustainable use of Earth s natural resources Outotec Values 15

16 Outotec is a technology company with minerals and metals processing as core competence Technology development and deliveries since 1890s to over 80 countries in all key markets Strong R&D and IP portfolio 5,618 patents or applications (Q3/2012) EUR 33.5 million in R&D (2011) Several Best Available Techniques (BAT) 87% of order intake in 2011 is classified as Environmental Goods and Services (OECD definition) STOXX Global ESG Leaders Patented innovations by filing year 16

Several Best Available Techniques (BAT) 87% of order intake in 2011 is classified as")

17 Outotec covers the entire ore-to-metal value chain and offers innovative applications to other industries Natural resources (ores, minerals, energy, water) Portfolio of the world s leading technologies Minerals processing Grinding Flotation Filtration Physical separation Thickening and clarification Analyzers and process automation Metallurgical processing Smelting and refining Roasting and off-gas handling Calcination Leaching and solution purification Solvent extraction Electrorefining and electrowinning Sintering and pelletizing Direct and smelting reduction Process control Chemicals Sulfuric acid production Water treatment Neutralization, effluent treatment, drinking water Energy Combustion and gasification, heat recovery, gas handling, bio energy, oil sand and oil shale processing Services Expert services, spare parts and maintenance, operation, modernization and expansion, life cycle service contracts Industrial minerals/concentrates Copper Nickel Zinc Cobalt Precious metals Aluminum Ferroalloys Pellets/sinter DRI/HBI/ Pig Iron Sulfuric acid Water Shale oil Char Energy 17

18 Example: combination of continuous own R&D and M&A has transformed Outotec to full minerals processing plant supplier Equipment supplier Process module supplier Plant supplier Acquisition of Backfill Specialists Acquisition of Larox filters Acquisition of Supaflo thickeners Acquisition of Nordberg grinding mills Acquisition of Boliden paste technology First flotation machines and analyzers developed (in house) 1960 Continuous R&D

1960")

19 Fully integrated solution offering of minerals processing plant - optimized production efficiency for entire life cycle Comminution Our comminution solutions include various proprietary grinding mill types and advanced control tools to optimize any comminution process. Flotation We are the leading supplier of flotation technology and modular process sections with low energy consumption. Industry benchmark proprietary flotation control system provides the best flotation performance. Dewatering We are a leading supplier of full service solid-liquid separation solutions. Our highly effective modular dewatering plant is based on proprietary filtration and thickening technologies. Paste backfill We offer comprehensive tailings treatment solutions that reduce the area needed for tailings storage. We provide operation and maintenance services to help customers to maintain and improve efficiency during the entire life cycle of the plant. 19

20 Increasing value capture of the industry CAPEX and OPEX by strengthening our earnings logic In 2010, we said we will... Strengthen our earnings logic by offering ore-to-metal total solutions and life cycle services Maximize life cycle profitability for our customers and Outotec Offer larger scopes leveraging our turnkey solution delivery and project management capability we... Introduced new offerings to the market to leverage all layers of our earnings logic Won several customer orders with scopes utilizing all layers of our earnings logic Introduced new life cycle services offerings Improved our capability to better price based on delivered value we will focus on... Offering industry benchmark process and plant solutions Leverage our unique capability to give process guarantees and deliver turnkey solutions with predictable performance, time and total cost Grow Services business through further penetration to installed base and expanding service offerings 20

21 Applying core technologies in attractive new growth areas In 2010, we said we will... Enter adjacent industries with high technological synergies and manageable risks Seek opportunities to provide innovative technological solutions for alternative and renewable energy and industrial water treatment applications we... Acquired EPI with biomass/wasteto-energy expertise Won customer orders for wastewater and effluent treatment Acquired AshDec to offer phosphorous recycling Started Narva oil shale plant commissioning and did several studies in oil shale for new customers Received biomass-to-energy and sludge incineration customer orders we will focus on... Promoting biomass and waste-to-energy solutions Advancing IWT technology and offerings Continuing oil shale and sand R&D and commercialization efforts Winning new off-gas treatment and sulfuric acid orders Acquisitions complementing our energy and IWT offerings 21

22 Improving cost-competitiveness and scalability Customers In 2010, we said we will... Establish platform for growth by implementing an integrated global operating model Build strong global engineering and supply capabilities Leverage modular core product designs Partner with the most innovative suppliers Maintain an asset-light business model we... Succeeded in scalability by doubling our business volume Invested significantly in development and implementation of global processes and tools Implemented global supply management Improved operating leverage we will focus on... Improving cost competitiveness and margins through supply savings Operating leverage by growing revenues faster than SG&A Improving productivity through global processes and tools implementation 22

23 Strong global presence and integrated operations ensure optimal solutions to customers wherever they are In 2010, we said we will... Establish strong local presence in growth markets Deliveries to over 80 countries Strengthen the collaboration and relationships with our customers Strengthen our global solutions offering and delivery capability Fully leverage our technologies and capabilities globally we... Strengthened our presence in emerging and rapidly growing markets Leveraged our global presence and strong offerings resulting to faster sales growth than our industry peers we will focus on... further strengthening our market reach growing our Services sales and delivery capabilities delivering more value to customers through highly skilled local market organisations leveraging the competitive strength of our end to end process technology offerings and lifecycle solutions 23

24 We guarantee performance and the best return on customer s investment with minimized ecological impact In 2010, we said we will... Leverage our unique capabilities to offer customers Performance guarantees Optimized processes Fast and reliable ramp up High material recovery Efficient use of raw materials, energy and water Low lifetime operating cost we... Have won a large number of solution deals Have grown our order intake and sales faster than our peers Have won several deals based on BAT environmental advantages we will focus on... Growing life cycle solutions offerings and orders Expanding Services product offerings and penetration to installed base Further differentiating from competitors through our unique capabilities in the industry 24

25 Acquisitions continue to be an integral part of our growth strategy We are looking for acquisitions which will complement the existing technology portfolio, accelerate growth in new application areas such as energy and industrial water treatment, and expand the Services offering and resources. Since 2010 we have completed 12 acquisitions in line with this strategy Life cycle solutions Services Processes Proprietary equipment Technology 25

26 Outotec SWOT Strengths Minerals and metals processing core competences Wide and Deep Proprietary technology portfolio Systems integration and turn-key project implementation capabilities Reputation, references and installed base Global footprint Weaknesses Sensitivity to minerals and metals process industry CAPEX cycles => We are expanding to adjacent industries like energy and industrial water treatment Low % share of services sales => We are growing our services business decisively (new target of 1 B by 2017) Opportunities Increasing sustainability demands due to global warming and other environmental problems Declining ore grades Growing renewable and alternative energy demand Underserved installed base Mergers and Acquisitions as additional source of growth Threaths Slow global GDP growth reduces metals prices, demand growth and industry s capacity investment growth => We are expanding our share of industry capex and opex and expanding to new industries Low energy prices slow down adaptation of renewable and alternative energy solutions => leverage Outotec s global footprint to grow Energy business 26

27 DELIVERING TOTAL SHAREHOLDER RETURN (TSR) 27

28 Outotec s goal is to deliver TSR through 1. Sustainable sales growth 2. Continuous profitability improvement 3. Distributing dividends 4. Reducing volatility of share price 28

29 EUR million Growing the order intake has been one of our top priorities in 2011 and Order backlog at the end of the period Order intake by quarter Share of unannounced orders 29

30 Outotec has been growing faster than its peers Net sales Outotec Metso FLSmidth e 2012e figures are based on consensus average estimates, rebased 2010=100 FLSmidth (incl. Customer Services, Non-Ferrous, Bulk Materials) Metso (Metso Mining & Construction) 30

31 We have been able to grow faster than what we targeted in 2010 MEUR Guidance 2012 Sales: EUR bn E Sales 10 % growth 20 % growth 31

32 12 % 10 % Steady positive EBIT % development toward the long term target Guidance 2012 Ebit%: approx % 6 % 4 % 2 % 0 % E EBIT % (from business operations excl. one time items and PPA) 32

33 Outotec can pull several levers to continue improving EBIT% in line with long term target Quartely and annual fluctuations Project scope & mix (CAPEX vs Service) Timing of license fees Timing and success of project completions Percentage of Completion schedules Foreign Exchange rates _ Larger scopes Expanding market reach Investments in processes & tools R&D investments Pricing pressures Competition Cost inflation + Services sales Life cycle solutions Leadership in technology Value pricing License fee incomes Supply savings Engineering productivity Global resourcing Operating leverage Long-term target: average 10% 33

34 Outotec has been distributing dividends in line with the dividend policy while executing the growth strategy 1,40 1,20 1,00 0,80 0,60 0,40 0,20 0,00 Dividend & Payout Ratio Dividend Payout ratio % 140 % 120 % 100 % 80 % 60 % 40 % 20 % 0 % 34

35 Good ROI and ROE due to asset light operating model and negative net working capital ROI %, quarterly ROE %, quarterly Net interest-bearing debt Working capital 35

36 Outotec s long-term financial targets Targeting continuous profitable growth CAGR 10-20% Outotec targets to achieve annual average sales growth of 10-20% Sales Services sales target EUR 1 billion by the end of 2017 Operating profit margin On average 10% Annual operating profit margin from business operations is targeted to be on average at 10% over the cycle, excluding one-time costs and purchase price allocations of acquired businesses. Balance sheet Outotec targets to maintain strong balance sheet to provide operational flexibility and enable acquisitions. Dividend policy: at least 40% of the annual net income 36

37 Reducing share price volatility Outotec s Outotec s goal is goal to reduce is to reduce the dependency the dependency on mining on industry CAPEX mining volatility industry by CAPEX volatility by 1. Growing services business strongly Upgrading the Services sales target from EUR 500 million by 2015 to EUR 1 billion by Growing energy and industrial water treatment businesses 3. Further strengthening the end-to-end technology offering for all metals to increase self-hedging 37

38 KEY PRIORITIES AND GUIDANCE FOR

39 Key focus areas in 2013 Focus area Status Ensure continuous sales growth through order intake and services growth as well as earnings logic enhancement Improve profitability through value based pricing, supply savings and sales mix improvement Continue making acquisitions to strengthen the offering portfolio and accelerate growth Continue investments in developing and rolling out global platforms to lay the foundation for future growth and profitability improvement 39

40 Industry investments are expected to continue on high level in 2013 bus$ Global Mining Capex *) bus$ Global GDP growth and growing metals demand drive further investments e 2013e 2014e Capex Brook Hunt Outotec 0 *) Gray area on the graph represents a range of possible scenarios based on analysts and market institutes reports 40

41 We continue to see market activity in all market areas and metals as well as all parts of the value chain Greenfield (no existing infra) Brownfield Type of investment project No of projects 10/2012 Greenfield 540 Brownfield 134 Source: Raw Materials Data. Copyright: Raw Materials Group 41

42 2013 Financial guidance Based on the strong order backlog, current market outlook and the customer tendering activity, the management expects that in 2013: Sales will grow from 2012, and Operating profit margin from business operations ( * will further improve compared to 2012 ( *excluding one-time items and PPA amortizations Factors affecting Outotec s financial guidance are described in the Financial Statements and Interim Reports 42

43 Our mission: Sustainable use of Earth's natural resources. 43

44 Why to invest in Outotec - Key take-ways from CMD Outotec participates global growth markets with strong secular demand drivers Outotec has unique competitive advantages due to its technology core competences and technology porftolio covering all metals end-to-end Energy and Industrial Water treatment are new growth opportunities in addition to growing minerals and metals processing core business Outotec has a good growth strategy and good execution track record Outotec has a global footprint, 2/3 of the business comes from rapidly growing markets Outotec has ambituous financial goals and good momentum 44

45 Outotec CMD 2013 Save the date for next year December 4,

Solutions and life cycle services for the entire Minerals Processing value chain Life cycle solutions

Solutions and life cycle services for the entire Minerals Processing value chain Life cycle solutions Kalle Härkki President of Minerals Processing business area Outotec December 4, London Minerals Processing

Solutions and life cycle services for the entire Minerals Processing value chain Life cycle solutions Kalle Härkki President of Minerals Processing business area Outotec December 4, London Minerals Processing

Interim Report January June 2010. o President and CEO, Outotec Oyj

Interim Report January June 2010 Pertti ett Korhonen o President and CEO, Outotec Oyj New reporting segments as of April 1, 2010 Non-ferrous Solutions Ferrous Solutions Energy, Light Metals and Environmental

Interim Report January June 2010 Pertti ett Korhonen o President and CEO, Outotec Oyj New reporting segments as of April 1, 2010 Non-ferrous Solutions Ferrous Solutions Energy, Light Metals and Environmental

Innovative application of proven technology in energy, biomass and waste-to-energy solutions

Innovative application of proven technology in energy, biomass and waste-to-energy solutions Capital Markets Day 2012 Dr. Peter Weber, President Energy, Light Metals & Environmental Solutions (ELE) November

Innovative application of proven technology in energy, biomass and waste-to-energy solutions Capital Markets Day 2012 Dr. Peter Weber, President Energy, Light Metals & Environmental Solutions (ELE) November

Outotec Q1/2009 roadshow CEO Tapani Järvinen and CFO Vesa-Pekka Takala Helsinki - Dublin - London - Paris - Milan - Oslo - Zurich

Outotec Q1/2009 roadshow CEO Tapani Järvinen and CFO Vesa-Pekka Takala Helsinki - Dublin - London - Paris - Milan - Oslo - Zurich 2 Outotec in brief Technology developer and provider for mining, metals

Outotec Q1/2009 roadshow CEO Tapani Järvinen and CFO Vesa-Pekka Takala Helsinki - Dublin - London - Paris - Milan - Oslo - Zurich 2 Outotec in brief Technology developer and provider for mining, metals

Sustainable use of Earth s natural resources

Sustainable use of Earth s natural resources ANNUAL REPORT 2010 1 Vuosikertomus 2010 ContenTs ANNUAL REVIEW 2010 Year 2010 in brief 2 Mission and strategic intent 3 Outotec in brief 4 Technology and service

Sustainable use of Earth s natural resources ANNUAL REPORT 2010 1 Vuosikertomus 2010 ContenTs ANNUAL REVIEW 2010 Year 2010 in brief 2 Mission and strategic intent 3 Outotec in brief 4 Technology and service

Outotec developing and delivering

Outotec developing and delivering environmentally sound technologies Mr Vesa-Pekka e a Takala, aa, CFO Ms Rita Uotila, IR Öhman Raw Materials Day 2010 Stockholm Sustainable technology expertise D E M A

Outotec developing and delivering environmentally sound technologies Mr Vesa-Pekka e a Takala, aa, CFO Ms Rita Uotila, IR Öhman Raw Materials Day 2010 Stockholm Sustainable technology expertise D E M A

Outotec Thursday, 29 th September 2012 14:00 Hrs UK time Chaired by Pirjo Lifländer

Outotec Thursday, 29 th September 2012 14:00 Hrs UK time Chaired by Good afternoon and welcome to this Q3 Q&A session with Outotec s president and CEO,. I would like to remind you that this webcast will

Outotec Thursday, 29 th September 2012 14:00 Hrs UK time Chaired by Good afternoon and welcome to this Q3 Q&A session with Outotec s president and CEO,. I would like to remind you that this webcast will

ANNUAL REPORT2009. Outotec Oyj 5

ANNUAL REPORT2009 Outotec Oyj 5 ContenTs Annual Review 2009 Year 2009 in brief 1 Announcements in 2009 2 Technology and service offerings 4 Strategy 6 Interview of the CEOs 8 Market review 11 Minerals

ANNUAL REPORT2009 Outotec Oyj 5 ContenTs Annual Review 2009 Year 2009 in brief 1 Announcements in 2009 2 Technology and service offerings 4 Strategy 6 Interview of the CEOs 8 Market review 11 Minerals

How To Profit From Outotec

annual report 2007 Contents ANNUAL REVIEW Year 2007 in brief 1 Outotec in brief 2 Strategy 4 CEO s review 6 Market review 8 Minerals Processing division 12 Base Metals division 16 Metals Processing division

annual report 2007 Contents ANNUAL REVIEW Year 2007 in brief 1 Outotec in brief 2 Strategy 4 CEO s review 6 Market review 8 Minerals Processing division 12 Base Metals division 16 Metals Processing division

Outotec Gold Processing Solutions

Finland, September 2013. Outotec provides leading technologies and services for the sustainable use of Earth s natural resources. As the global leader in minerals and metals processing technology, Outotec

Finland, September 2013. Outotec provides leading technologies and services for the sustainable use of Earth s natural resources. As the global leader in minerals and metals processing technology, Outotec

Outotec Oyj ANNUAL REPORT 2008 ANNUAL REPORT2008

Outotec Oyj ANNUAL REPORT 2008 ANNUAL REPORT2008 Contents ANNUAL REVIEW 2008 FINANCIAL STATEMENTS 2008 Year in brief 1 Technology and service offerings 2 Strategy 4 CEO s review 6 Market review 8 Minerals

Outotec Oyj ANNUAL REPORT 2008 ANNUAL REPORT2008 Contents ANNUAL REVIEW 2008 FINANCIAL STATEMENTS 2008 Year in brief 1 Technology and service offerings 2 Strategy 4 CEO s review 6 Market review 8 Minerals

President and CEO Pertti Korhonen:

APRIL 26, 2013 INTERIM REPORT JANUARY-MARCH 2013 Continued growth in order intake and sales January-March 2013 in brief (2012 corresponding period): Order intake: EUR 491.1 (425.4) million, +15% Order

APRIL 26, 2013 INTERIM REPORT JANUARY-MARCH 2013 Continued growth in order intake and sales January-March 2013 in brief (2012 corresponding period): Order intake: EUR 491.1 (425.4) million, +15% Order

Outokumpu Technology Capital Market Day March 8-9, 2007 Market and strategy update

Outokumpu Technology Capital Market Day March 8-9, 2007 Market and strategy update More out of ore! Tapani Järvinen, President and CEO Management Executive Committee Tapani Järvinen President & CEO Seppo

Outokumpu Technology Capital Market Day March 8-9, 2007 Market and strategy update More out of ore! Tapani Järvinen, President and CEO Management Executive Committee Tapani Järvinen President & CEO Seppo

Sustainable use of Earth s natural resources

Sustainable use of Earth s natural resources Outotec Oyj I Content Report by the Board of Directors 4 Consolidated financial statements, IFRS Statement of comprehensive income 12 Statement of financial

Sustainable use of Earth s natural resources Outotec Oyj I Content Report by the Board of Directors 4 Consolidated financial statements, IFRS Statement of comprehensive income 12 Statement of financial

Deco Media 927291 Thurs, 7 th February 2013 14:00 Hrs UK time Chaired by Rita Uotila

Deco Media 927291 Thurs, 7 th February 2013 14:00 Hrs UK time Chaired by Rita Uotila Rita Uotila Good afternoon everybody ladies and gentlemen, and welcome to Outotec s full year 2012 Financial Statement

Deco Media 927291 Thurs, 7 th February 2013 14:00 Hrs UK time Chaired by Rita Uotila Rita Uotila Good afternoon everybody ladies and gentlemen, and welcome to Outotec s full year 2012 Financial Statement

SUSTAINABILITY REPORT 2012

SUSTAINABILITY REPORT 2012 CONTENTS Outotec and sustainability 1 Outotec in brief 2 Highlights in 2012 3 Our approach 4 CEO s message to stakeholders 4 Strategy 6 Materiality assessment 8 Management approach

SUSTAINABILITY REPORT 2012 CONTENTS Outotec and sustainability 1 Outotec in brief 2 Highlights in 2012 3 Our approach 4 CEO s message to stakeholders 4 Strategy 6 Materiality assessment 8 Management approach

Healthy business model supporting strong financial development

KONE CMD 2014 Healthy business model supporting strong financial development Eriikka Söderström, CFO September 26, 2014 Graph on slide 13 has been updated February 18,2015. Agenda How we drive KONE s profitable

KONE CMD 2014 Healthy business model supporting strong financial development Eriikka Söderström, CFO September 26, 2014 Graph on slide 13 has been updated February 18,2015. Agenda How we drive KONE s profitable

Deco Media Oy 918327 Friday, 27 th July 2012 14:00 Hrs UK time Chaired by Pertti Korhonen

Deco Media Oy 918327 Friday, 27 th July 2012 14:00 Hrs UK time Chaired by Pertti Korhonen Good afternoon ladies and gentlemen and welcome to Outotec s second quarter interim report briefing. Before we

Deco Media Oy 918327 Friday, 27 th July 2012 14:00 Hrs UK time Chaired by Pertti Korhonen Good afternoon ladies and gentlemen and welcome to Outotec s second quarter interim report briefing. Before we

Tieto Corporation. 26 October 2015. Tanja Lounevirta Head of IR

Tieto Corporation 26 October 215 Tanja Lounevirta Head of IR Financial facts Customer sales in 214: EUR 1 523 million EBIT margin excl. one-off items *) : 9.9% Sales by Service Line Tieto s market position:

Tieto Corporation 26 October 215 Tanja Lounevirta Head of IR Financial facts Customer sales in 214: EUR 1 523 million EBIT margin excl. one-off items *) : 9.9% Sales by Service Line Tieto s market position:

ADVISORY CAPABILITY STATEMENT

ADVISORY CAPABILITY STATEMENT Bridging Two Disciplines We are independent Engineering Economists and Advisors. Our principal competency is as supply side and asset specialists. Since 1971 we have bridged

ADVISORY CAPABILITY STATEMENT Bridging Two Disciplines We are independent Engineering Economists and Advisors. Our principal competency is as supply side and asset specialists. Since 1971 we have bridged

Financial Information

Financial Information Solid results with in all key financial metrics of 23.6 bn, up 0.4% like-for like Adjusted EBITA margin up 0.3 pt on organic basis Net profit up +4% to 1.9 bn Record Free Cash Flow

Financial Information Solid results with in all key financial metrics of 23.6 bn, up 0.4% like-for like Adjusted EBITA margin up 0.3 pt on organic basis Net profit up +4% to 1.9 bn Record Free Cash Flow

Outotec and Environment

Outotec and Environment Kalle Härkki President, Pori Research Center CMD Seville May 15, 2008 2 Content General Ferroalloy technologies Flash Smelting and Converting technologies Acid plant technologies

Outotec and Environment Kalle Härkki President, Pori Research Center CMD Seville May 15, 2008 2 Content General Ferroalloy technologies Flash Smelting and Converting technologies Acid plant technologies

Process Automation Markets 2010

PRESS RELEASE Important Findings of the New Market, Strategy, and Technology Report Process Automation Markets 2010 Development of the automation world market for the process industries until 2010 World

PRESS RELEASE Important Findings of the New Market, Strategy, and Technology Report Process Automation Markets 2010 Development of the automation world market for the process industries until 2010 World

How To Develop A Water Technology Business In Kemira

Johan Grön Executive Vice President, R&D and Technology Environmental technology opportunities Global megatrends Clean water and water intensiveness Global markets and business opportunities Water technology

Johan Grön Executive Vice President, R&D and Technology Environmental technology opportunities Global megatrends Clean water and water intensiveness Global markets and business opportunities Water technology

An attractive business model with a high return on capital

KONE CMD 2015 An attractive business model with a high return on capital Eriikka Söderström, CFO Agenda Global position in a life cycle business Strong order book combined with recurring revenues Flexible

KONE CMD 2015 An attractive business model with a high return on capital Eriikka Söderström, CFO Agenda Global position in a life cycle business Strong order book combined with recurring revenues Flexible

Deco Media Fri, 29 th April 2011 12:00 Hrs UK time Chaired by Rita Uotila

Deco Media Fri, 29 th April 2011 12:00 Hrs UK time Chaired by Rita Uotila Rita Uotila Good afternoon ladies and gentlemen, and welcome to Outotec s First Quarter Results briefing. My name is Rita Uotila.

Deco Media Fri, 29 th April 2011 12:00 Hrs UK time Chaired by Rita Uotila Rita Uotila Good afternoon ladies and gentlemen, and welcome to Outotec s First Quarter Results briefing. My name is Rita Uotila.

Value Investing with Legends Spring 2015 Bruce Greenwald Stock Pitch Øystein Kværner 4/26/2015 The Weir Group (LSE: WEIR) BUY at target price $40 (+%)

BUY at target price $40 (+%)") The Weir Group (LSE: WEIR) BUY at target price $40 (+%) I recommend to BUY the Weir Group at $26.4 for a 39% upside to end of 2017 (11.5% IRR including dividends). Further upside beyond that can also be

The Weir Group (LSE: WEIR) BUY at target price $40 (+%) I recommend to BUY the Weir Group at $26.4 for a 39% upside to end of 2017 (11.5% IRR including dividends). Further upside beyond that can also be

Kemira well underway to return to profitable growth Kemira Capital Markets Day 2012. Wolfgang Büchele President and CEO

Kemira well underway to return to profitable growth Kemira Capital Markets Day 2012 President and CEO Three strategic priorities for achieving profitable growth Improving efficiency Simplicity Substantially

Kemira well underway to return to profitable growth Kemira Capital Markets Day 2012 President and CEO Three strategic priorities for achieving profitable growth Improving efficiency Simplicity Substantially

Siemens Canada Ltd Dr. Donald Wilson Industry DT Large Drives Mining and Minerals

History of Siemens in Canada and Mining Outlook according to Siemens Canadian German Chamber of Industry and Commerce Inc. German Business Delegation to Canada November 12-16, 2012, Toronto, Canada Siemens

History of Siemens in Canada and Mining Outlook according to Siemens Canadian German Chamber of Industry and Commerce Inc. German Business Delegation to Canada November 12-16, 2012, Toronto, Canada Siemens

SUSTAINABILITY REPORT 2013

SUSTAINABILITY REPORT 2013 CONTENTS 2 A year in the sustainability business OUR APPROACH 6 What is Outotec 8 CEO s message 10 Megatrends giving us tailwind 12 Megatrends, risks and opportunities 14 Strategy

SUSTAINABILITY REPORT 2013 CONTENTS 2 A year in the sustainability business OUR APPROACH 6 What is Outotec 8 CEO s message 10 Megatrends giving us tailwind 12 Megatrends, risks and opportunities 14 Strategy

THE ROLE OF METALLURGY IN ENHANCING BENEFICIATION IN THE SOUTH AFRICAN MINING INDUSTRY

THE ROLE OF METALLURGY IN ENHANCING BENEFICIATION IN THE SOUTH AFRICAN MINING INDUSTRY Marek Dworzanowski, Presidential Address, SAIMM AGM, 22 August 2013 CONTENTS Introduction Definitions Phases of metallurgical

THE ROLE OF METALLURGY IN ENHANCING BENEFICIATION IN THE SOUTH AFRICAN MINING INDUSTRY Marek Dworzanowski, Presidential Address, SAIMM AGM, 22 August 2013 CONTENTS Introduction Definitions Phases of metallurgical

Interim results for the six months ended 31 December 2009

Interim results for the six months ended 31 December 29 ARM s financial position continues to be robust with net debt to equity of 8.4%. We are pleased about the significant increase in headline earnings

Interim results for the six months ended 31 December 29 ARM s financial position continues to be robust with net debt to equity of 8.4%. We are pleased about the significant increase in headline earnings

Consulting Services Mining & Metals

Consulting Services Mining & Metals Amec Foster Wheeler is an industry-recognized expert in every facet of mining project assessment, development and optimization for all major commodities. Our Consulting

Consulting Services Mining & Metals Amec Foster Wheeler is an industry-recognized expert in every facet of mining project assessment, development and optimization for all major commodities. Our Consulting

Tieto Corporation. Lasse Heinonen CFO Tanja Lounevirta Head of Investor Relations 27 October 2014

Tieto Corporation Lasse Heinonen CFO Tanja Lounevirta Head of Investor Relations 27 October 2014 Financial facts Customer sales in 2013* ) : EUR 1607 million EBIT margin excl. one-off items **) : 8.8%

Tieto Corporation Lasse Heinonen CFO Tanja Lounevirta Head of Investor Relations 27 October 2014 Financial facts Customer sales in 2013* ) : EUR 1607 million EBIT margin excl. one-off items **) : 8.8%

ABB Next Level Accelerating sustainable value creation

Eric Elzvik, CFO, Capital Markets Day, London, ABB Next Level Accelerating sustainable value creation Slide 1 Important notices Presentations made during Capital Markets Day 2014 include forward-looking

Eric Elzvik, CFO, Capital Markets Day, London, ABB Next Level Accelerating sustainable value creation Slide 1 Important notices Presentations made during Capital Markets Day 2014 include forward-looking

CONFERENCE CALL PRELIMINARY FIGURES FISCAL YEAR 2013

WELCOME DÜRR AKTIENGESELLSCHAFT CONFERENCE CALL PRELIMINARY FIGURES FISCAL YEAR 2013 Ralf W. Dieter, CEO Ralph Heuwing, CFO Bietigheim-Bissingen, February 25, 2014 www.durr.com DISCLAIMER This presentation

WELCOME DÜRR AKTIENGESELLSCHAFT CONFERENCE CALL PRELIMINARY FIGURES FISCAL YEAR 2013 Ralf W. Dieter, CEO Ralph Heuwing, CFO Bietigheim-Bissingen, February 25, 2014 www.durr.com DISCLAIMER This presentation

PACIFIC ENERGY LIMITED POWER GENERATION

PACIFIC ENERGY LIMITED POWER GENERATION 2015 RESULTS PRESENTATION August 2015 ASX: PEA Important Notice and Disclaimer This presentation has been prepared by (PEL) for information purposes only. This presentation

PACIFIC ENERGY LIMITED POWER GENERATION 2015 RESULTS PRESENTATION August 2015 ASX: PEA Important Notice and Disclaimer This presentation has been prepared by (PEL) for information purposes only. This presentation

Adelaide Brighton Ltd Morgan Stanley Emerging Companies Conference 14 June 1012. Presented by: Mark Chellew Managing Director & CEO.

Adelaide Brighton Ltd Morgan Stanley Emerging Companies Conference 14 June 1012 Presented by: Mark Chellew Managing Director & CEO Disclaimer The following presentation has been prepared by Adelaide Brighton

Adelaide Brighton Ltd Morgan Stanley Emerging Companies Conference 14 June 1012 Presented by: Mark Chellew Managing Director & CEO Disclaimer The following presentation has been prepared by Adelaide Brighton

Unilever First Half 2015 Results Paul Polman / Jean-Marc Huët 23 rd July 2015

Unilever First Half 2015 Results Paul Polman / Jean-Marc Huët 23 rd July 2015 SAFE HARBOUR STATEMENT This announcement may contain forward-looking statements, including forward-looking statements within

Unilever First Half 2015 Results Paul Polman / Jean-Marc Huët 23 rd July 2015 SAFE HARBOUR STATEMENT This announcement may contain forward-looking statements, including forward-looking statements within

JP Morgan European Capital Goods CEO Conference 2015

JP Morgan European Capital Goods CEO Conference 2015 Jean-Pascal Tricoire, Chairman and CEO June 11, 2015 1 A technology company with strong foundations 2 We are the global specialist in energy management

JP Morgan European Capital Goods CEO Conference 2015 Jean-Pascal Tricoire, Chairman and CEO June 11, 2015 1 A technology company with strong foundations 2 We are the global specialist in energy management

FINANCIAL STATEMENTS REVIEW JANUARY-DECEMBER 2014

FEBRUARY 6, 2015 FINANCIAL STATEMENTS REVIEW JANUARY-DECEMBER 2014 Challenging Capex market, growth in service sales January-December 2014 in brief (2013 comparison period): Order intake 1) : EUR 1,177.9

FEBRUARY 6, 2015 FINANCIAL STATEMENTS REVIEW JANUARY-DECEMBER 2014 Challenging Capex market, growth in service sales January-December 2014 in brief (2013 comparison period): Order intake 1) : EUR 1,177.9

Tutkimuksen merkitys menestyvässä liiketoiminnassa- Innovaatiosta tuotteeksi

Tutkimuksen merkitys menestyvässä liiketoiminnassa- Innovaatiosta tuotteeksi Matti Rautanen Manager, External Networks, Power-wide R&D Tutkimuksella tulevaisuuteen- seminaari Kaukolämpöpäivät, Kuopio 29.8.2013

Tutkimuksen merkitys menestyvässä liiketoiminnassa- Innovaatiosta tuotteeksi Matti Rautanen Manager, External Networks, Power-wide R&D Tutkimuksella tulevaisuuteen- seminaari Kaukolämpöpäivät, Kuopio 29.8.2013

Mineral Deposits and their Global Strategic Supply. Group Executive and Chief Executive Non-Ferrous 14 December 2011

Mineral Deposits and their Global Strategic Supply Andrew Mackenzie Andrew Mackenzie Group Executive and Chief Executive Non-Ferrous 14 December 2011 Disclaimer Reliance on Third Party Information The

Mineral Deposits and their Global Strategic Supply Andrew Mackenzie Andrew Mackenzie Group Executive and Chief Executive Non-Ferrous 14 December 2011 Disclaimer Reliance on Third Party Information The

Metsä Fibre s Bioproduct mill

s Bioproduct mill Camilla Wikström VP, Bioproduct mill Manager, Metsä Group part of Metsä Group We focus on products and services with promising growth prospects and in which we have strong competence

s Bioproduct mill Camilla Wikström VP, Bioproduct mill Manager, Metsä Group part of Metsä Group We focus on products and services with promising growth prospects and in which we have strong competence

Investor Day. Group Strategy. Jean-Pascal Tricoire Chairman & CEO. February 20, 2014

Investor Day February 20, 2014 Group Strategy Jean-Pascal Tricoire Chairman & CEO Disclaimer All forward-looking statements are Schneider Electric management s present expectations of future events and

Investor Day February 20, 2014 Group Strategy Jean-Pascal Tricoire Chairman & CEO Disclaimer All forward-looking statements are Schneider Electric management s present expectations of future events and

JANUARY-JUNE 2012 INTERIM REPORT

JANUARY-JUNE 212 INTERIM REPORT JULY 27, 212 Jukka Pahta, CFO PRESENTATION CONTENTS January-June 212 overview January-June 212 financials Outlook Appendices Q2/212 PRESENTATION 2 JANUARY-JUNE 212 OVERVIEW

JANUARY-JUNE 212 INTERIM REPORT JULY 27, 212 Jukka Pahta, CFO PRESENTATION CONTENTS January-June 212 overview January-June 212 financials Outlook Appendices Q2/212 PRESENTATION 2 JANUARY-JUNE 212 OVERVIEW

A Leading Global Health Care Group

A Leading Global Health Care Group Commerzbank German Investment Seminar January 11/12, 2016 For detailed financial information please see our annual/quarterly reports and/or conference call materials

A Leading Global Health Care Group Commerzbank German Investment Seminar January 11/12, 2016 For detailed financial information please see our annual/quarterly reports and/or conference call materials

Article no. 2: METEC 2015 (business) Promising outlook for metals: More than 3,500 different types of steel around the world

Promising outlook for metals: More than 3,500 different types of steel around the world") Article no. 2: METEC 2015 (business) Promising outlook for metals: More than 3,500 different types of steel around the world Strong demand for copper in car manufacturing and medical engineering: conductive

Article no. 2: METEC 2015 (business) Promising outlook for metals: More than 3,500 different types of steel around the world Strong demand for copper in car manufacturing and medical engineering: conductive

A.B.N. 35 068 232 708 A.C.N.

Downer EDI Limited Presentation by:- Engineered for Success STEPHEN GILLIES Chief Executive Officer GEOFFREY BRUCE Chief Financial Officer Credit Suisse First Boston Australia Equities Limited Participating

Downer EDI Limited Presentation by:- Engineered for Success STEPHEN GILLIES Chief Executive Officer GEOFFREY BRUCE Chief Financial Officer Credit Suisse First Boston Australia Equities Limited Participating

How To Make Money From Energy And Mining

INDUSTRIES Daniel VALOT INVESTOR DAY, PARIS, FRANCE - October 22, 2004 GLOBAL MARKET: MUCH BIGGER THAN OIL & GAS GLOBAL MARKET ($372 Bn) Others Process Industries 6% 12% 21% Oil & Gas Power 7% Infrastructures

INDUSTRIES Daniel VALOT INVESTOR DAY, PARIS, FRANCE - October 22, 2004 GLOBAL MARKET: MUCH BIGGER THAN OIL & GAS GLOBAL MARKET ($372 Bn) Others Process Industries 6% 12% 21% Oil & Gas Power 7% Infrastructures

Value Creation through Transformation of Business Models

Value Creation through Transformation of Business Models Dr. Jürgen Köhler, CEO Dr. Michael Majerus, CFO Investor Relations July 2015 Table of Contents. September 2014: Cornerstones of strategic realignment

Value Creation through Transformation of Business Models Dr. Jürgen Köhler, CEO Dr. Michael Majerus, CFO Investor Relations July 2015 Table of Contents. September 2014: Cornerstones of strategic realignment

Commerzbank German Investment Seminar. Dr. Jürgen Köhler, CEO New York. January 2016

SGL Group s Strategic Realignment Commerzbank German Investment Seminar Dr. Jürgen Köhler, CEO New York January 2016 Transformation of SGL Group. Guided by clearly defined targets (Sept. 2014) Capital

SGL Group s Strategic Realignment Commerzbank German Investment Seminar Dr. Jürgen Köhler, CEO New York January 2016 Transformation of SGL Group. Guided by clearly defined targets (Sept. 2014) Capital

Nordex SE Conference Call 9M 2012. Hamburg, 13/11/2012

Nordex SE Conference Call 9M 2012 Hamburg, 13/11/2012 AGENDA 1. Highlights 9M 2012 Dr. J. Zeschky 2. Financials 9M 2012 B. Schäferbarthold 3. Guidance 2012 and market outlook B. Schäferbarthold 4. Strategy

Nordex SE Conference Call 9M 2012 Hamburg, 13/11/2012 AGENDA 1. Highlights 9M 2012 Dr. J. Zeschky 2. Financials 9M 2012 B. Schäferbarthold 3. Guidance 2012 and market outlook B. Schäferbarthold 4. Strategy

Nokia Conference Call Third Quarter 2004 Financial Results. Jorma Ollila Chairman and CEO Rick Simonson Senior Vice President and CFO

Nokia Conference Call Third Quarter 2004 Financial Results Jorma Ollila Chairman and CEO Rick Simonson Senior Vice President and CFO Ulla James Vice President, Investor Relations October 14, 2004 15.00

Nokia Conference Call Third Quarter 2004 Financial Results Jorma Ollila Chairman and CEO Rick Simonson Senior Vice President and CFO Ulla James Vice President, Investor Relations October 14, 2004 15.00

Preferred partner. Investor Day 2015. London, March 17, 2015 Luis Araujo, CEO Svein Stoknes, CFO

Investor Day 2015 London, March 17, 2015 Luis Araujo, CEO Svein Stoknes, CFO 2015 Aker Solutions Slide 1 March 17, 2015 Investor Day 2015 Forward-Looking Statements and Copyright This Presentation includes

Investor Day 2015 London, March 17, 2015 Luis Araujo, CEO Svein Stoknes, CFO 2015 Aker Solutions Slide 1 March 17, 2015 Investor Day 2015 Forward-Looking Statements and Copyright This Presentation includes

Electrical Products Group Conference. Jean-Pascal Tricoire Chairman & CEO May 2014

Electrical Products Group Conference Jean-Pascal Tricoire Chairman & CEO May 2014 1 Disclaimer All forward-looking statements are Schneider Electric management s present expectations of future events and

Electrical Products Group Conference Jean-Pascal Tricoire Chairman & CEO May 2014 1 Disclaimer All forward-looking statements are Schneider Electric management s present expectations of future events and

Schneider Electric new company program presentation. January 28, 2009

Schneider Electric new company program presentation January 28, 2009 03 09 16 49 54 A Successful Transformation Our Vision One Company Program One Finance Presentation Conclusion 2 A successful transformation

Schneider Electric new company program presentation January 28, 2009 03 09 16 49 54 A Successful Transformation Our Vision One Company Program One Finance Presentation Conclusion 2 A successful transformation

CONFERENCE CALL PRELIMINARY FIGURES FISCAL YEAR 2014

WELCOME DÜRR AKTIENGESELLSCHAFT CONFERENCE CALL PRELIMINARY FIGURES FISCAL YEAR 2014 Ralf W. Dieter, CEO Ralph Heuwing, CFO Bietigheim-Bissingen, March 9, 2015 www.durr.com DISCLAIMER This presentation

WELCOME DÜRR AKTIENGESELLSCHAFT CONFERENCE CALL PRELIMINARY FIGURES FISCAL YEAR 2014 Ralf W. Dieter, CEO Ralph Heuwing, CFO Bietigheim-Bissingen, March 9, 2015 www.durr.com DISCLAIMER This presentation

A Leading Global Health Care Group

A Leading Global Health Care Group HSBC Healthcare Day, November 12, 2014 For detailed financial information please see our annual/quarterly reports and/or conference call materials on www.fresenius.com/ir.

A Leading Global Health Care Group HSBC Healthcare Day, November 12, 2014 For detailed financial information please see our annual/quarterly reports and/or conference call materials on www.fresenius.com/ir.

2013 Half Year Results

2013 Half Year Results Erwin Stoller, Executive Chairman Joris Gröflin, Chief Financial Officer Agenda 1. Introduction and summary of first half year 2013 2. Financial results first half year 2013 3. Outlook

2013 Half Year Results Erwin Stoller, Executive Chairman Joris Gröflin, Chief Financial Officer Agenda 1. Introduction and summary of first half year 2013 2. Financial results first half year 2013 3. Outlook

Euro Bond Offering April 2002

Euro Bond Offering April 2002 Offering summary Issuer Guarantor Issue Long term ratings Anticipated maturity Listing Use of proceeds Joint bookrunners Rio Tinto Finance plc Rio Tinto Plc Benchmark Euro

Euro Bond Offering April 2002 Offering summary Issuer Guarantor Issue Long term ratings Anticipated maturity Listing Use of proceeds Joint bookrunners Rio Tinto Finance plc Rio Tinto Plc Benchmark Euro

Protection notice / Copyright notice

Infrastructure & Cities (IC) Analyst Call Dr. Roland Busch Member of the Managing Board of Siemens AG CEO of Infrastructure & Cities Sector December 5, 2011 Protection notice / Copyright notice Safe Harbour

Infrastructure & Cities (IC) Analyst Call Dr. Roland Busch Member of the Managing Board of Siemens AG CEO of Infrastructure & Cities Sector December 5, 2011 Protection notice / Copyright notice Safe Harbour

Health Care Worldwide. Citi - European Credit Conference September 24, 2015 - London

Health Care Worldwide Citi - European Credit Conference September 24, 2015 - London Safe Harbor Statement This presentation contains forward-looking statements that are subject to various risks and uncertainties.

Health Care Worldwide Citi - European Credit Conference September 24, 2015 - London Safe Harbor Statement This presentation contains forward-looking statements that are subject to various risks and uncertainties.

Earnings Release Q1 FY 2016 October 1 to December 31, 2015

Munich, Germany, January 25, 2016 Earnings Release FY 2016 October 1 to December 31, 2015 Strong start into the fiscal year earnings outlook raised»we delivered a strong quarter and are well underway in

Munich, Germany, January 25, 2016 Earnings Release FY 2016 October 1 to December 31, 2015 Strong start into the fiscal year earnings outlook raised»we delivered a strong quarter and are well underway in

ABB Q3: Solid performance across the business

ABB Q3: Solid performance across the business Revenues 1 and operational EBITDA 2 higher in all divisions, net income up 10 percent Base orders 3 return to year-on-year growth, large project awards remain

ABB Q3: Solid performance across the business Revenues 1 and operational EBITDA 2 higher in all divisions, net income up 10 percent Base orders 3 return to year-on-year growth, large project awards remain

Vattenfall Q2 2013 results

Vattenfall Q2 2013 results Øystein Løseth, CEO and Ingrid Bonde, CFO Conference call for analysts and investors, 23 July 2013 Q2 Highlights Impairment charges on thermal assets and goodwill amounting to

Vattenfall Q2 2013 results Øystein Løseth, CEO and Ingrid Bonde, CFO Conference call for analysts and investors, 23 July 2013 Q2 Highlights Impairment charges on thermal assets and goodwill amounting to

Introduction to our Business in Valmet. Marita Niemelä VP, Strategy Pulp & Energy 20 August 2014

Introduction to our Business in Valmet Marita Niemelä VP, Strategy Pulp & Energy 20 August 2014 Valmet in brief Metso Demerger Two independent stock listed companies Metso is a global supplier of technology

Introduction to our Business in Valmet Marita Niemelä VP, Strategy Pulp & Energy 20 August 2014 Valmet in brief Metso Demerger Two independent stock listed companies Metso is a global supplier of technology

Steve Angel Chairman, President and

Praxair, Inc. Steve Angel Chairman, President and Chief Executive Officer 19 th Annual Citi Chemicals Conference New York City, Dec 2, 2008 1 Forward Looking Statement This document contains forward-looking

Praxair, Inc. Steve Angel Chairman, President and Chief Executive Officer 19 th Annual Citi Chemicals Conference New York City, Dec 2, 2008 1 Forward Looking Statement This document contains forward-looking

Company update. Frans van Houten, CEO Royal Philips

Company update Frans van Houten, CEO Royal Philips 1 Key takeaways Accelerate! is working and we are committed to achieving our 2013 targets; on-going headwinds remain a concern We have actively restructured

Company update Frans van Houten, CEO Royal Philips 1 Key takeaways Accelerate! is working and we are committed to achieving our 2013 targets; on-going headwinds remain a concern We have actively restructured

A Leading Global Health Care Group

A Leading Global Health Care Group Commerzbank Sector Conference September 8, 2014 For detailed financial information please see our annual/quarterly reports and/or conference call materials on www.fresenius.com/ir.

A Leading Global Health Care Group Commerzbank Sector Conference September 8, 2014 For detailed financial information please see our annual/quarterly reports and/or conference call materials on www.fresenius.com/ir.

Annual Report. More. ore!

Annual Report More out ore! of Contents ANNUAL REVIEW Outokumpu Technology in brief 3 CEO s review 6 Strategy 8 Management analysis of the financial performance 11 Market review 12 Minerals Processing

Annual Report More out ore! of Contents ANNUAL REVIEW Outokumpu Technology in brief 3 CEO s review 6 Strategy 8 Management analysis of the financial performance 11 Market review 12 Minerals Processing

Praxair, Inc. Matthew J. White Senior Vice President and Chief Financial Officer

Praxair, Inc. Matthew J. White Senior Vice President and Chief Financial Officer November 10, 2014 Forward Looking Statement This document contains forward-looking statements within the meaning of the

Praxair, Inc. Matthew J. White Senior Vice President and Chief Financial Officer November 10, 2014 Forward Looking Statement This document contains forward-looking statements within the meaning of the

Health Care Worldwide

Health Care Worldwide Barclays European High Yield and Leveraged Finance Conference October 30, 2014 London Barclays European High Yield and Leveraged Finance Conference, October 30, 2014 Copyright Page

Health Care Worldwide Barclays European High Yield and Leveraged Finance Conference October 30, 2014 London Barclays European High Yield and Leveraged Finance Conference, October 30, 2014 Copyright Page

H1 2015 RESULTS. July 30, 2015

H1 2015 RESULTS July 30, 2015 Sébastien Bazin CHAIRMAN AND CEO ACCORHOTELS H1 2015 Results 07/30/2015 2 Staying the course in a changing environment Solid H1 2015 results reflecting transformation Strong

H1 2015 RESULTS July 30, 2015 Sébastien Bazin CHAIRMAN AND CEO ACCORHOTELS H1 2015 Results 07/30/2015 2 Staying the course in a changing environment Solid H1 2015 results reflecting transformation Strong

Company announcement from Vestas Wind Systems A/S

Company announcement from Aarhus, 9 February 2016 Company announcement No. 3/2016 Page 1 of 9 Annual report 2015 - Yet another year with strong financial and operational results Summary: For full-year

Company announcement from Aarhus, 9 February 2016 Company announcement No. 3/2016 Page 1 of 9 Annual report 2015 - Yet another year with strong financial and operational results Summary: For full-year

Health Care Worldwide

Health Care Worldwide Credit Suisse Global Credit Products Conference September 18, 2014 Miami Credit Suisse Global Credit Products Conference, September 18, 2014 Copyright Page 1 Safe Harbor Statement

Health Care Worldwide Credit Suisse Global Credit Products Conference September 18, 2014 Miami Credit Suisse Global Credit Products Conference, September 18, 2014 Copyright Page 1 Safe Harbor Statement

China Energy efficiency report

China Energy efficiency report Objective: 16% reduction in primary energy intensity by 215 Overview 211-211 (%/year) Primary intensity (EU=1)¹ 222 -- -2.8% ++ CO 2 intensity (EU=1) 294 -- -2.5% + CO 2

China Energy efficiency report Objective: 16% reduction in primary energy intensity by 215 Overview 211-211 (%/year) Primary intensity (EU=1)¹ 222 -- -2.8% ++ CO 2 intensity (EU=1) 294 -- -2.5% + CO 2

CORPORATE PRESENTATION

CORPORATE PRESENTATION November 2015 sttenvirocorp.com SMART THINKING TECHNOLOGY FORWARD LOOKING STATEMENT This presentation may contain forward looking statements that reflect current views, including

CORPORATE PRESENTATION November 2015 sttenvirocorp.com SMART THINKING TECHNOLOGY FORWARD LOOKING STATEMENT This presentation may contain forward looking statements that reflect current views, including

An Enterprise Resource Planning Solution (ERP) for Mining Companies Driving Operational Excellence and Sustainable Growth

for Mining Companies Driving Operational Excellence and Sustainable Growth") SAP for Mining Solutions An Enterprise Resource Planning Solution (ERP) for Mining Companies Driving Operational Excellence and Sustainable Growth 2013 SAP AG or an SAP affi iate company. All rights reserved.

SAP for Mining Solutions An Enterprise Resource Planning Solution (ERP) for Mining Companies Driving Operational Excellence and Sustainable Growth 2013 SAP AG or an SAP affi iate company. All rights reserved.

Net income up 41% as ABB accelerates top line growth

Net income up 41% as ABB accelerates top line growth Orders up 25% 1 (19% organic 2 ); 18% revenue growth (12% organic) at two-year high Top-line strength and solid business execution lead to higher operational

Net income up 41% as ABB accelerates top line growth Orders up 25% 1 (19% organic 2 ); 18% revenue growth (12% organic) at two-year high Top-line strength and solid business execution lead to higher operational

F-Secure Corporation - Interim report Q3 2011

F-Secure Corporation - Interim report Q3 2011 (Unaudited) October 26, 2011 Kimmo Alkio, President & CEO Protecting the irreplaceable f-secure.com Q3 highlights Good financial performance Total revenues

F-Secure Corporation - Interim report Q3 2011 (Unaudited) October 26, 2011 Kimmo Alkio, President & CEO Protecting the irreplaceable f-secure.com Q3 highlights Good financial performance Total revenues

News release. No. 7/2015 KATANGA MINING ANNOUNCES 2015 SECOND QUARTER RESULTS

No. 7/2015 News release KATANGA MINING ANNOUNCES 2015 SECOND QUARTER RESULTS BAAR, SWITZERLAND, August 12, 2015 Katanga Mining Limited (TSX: KAT) ("Katanga" or the "Company") today announces its financial

No. 7/2015 News release KATANGA MINING ANNOUNCES 2015 SECOND QUARTER RESULTS BAAR, SWITZERLAND, August 12, 2015 Katanga Mining Limited (TSX: KAT) ("Katanga" or the "Company") today announces its financial

A Leading Global Health Care Group

A Leading Global Health Care Group Credit Suisse Global Health Care Conference, March 4, 2015 For detailed financial information please see our annual/quarterly reports and/or conference call materials

A Leading Global Health Care Group Credit Suisse Global Health Care Conference, March 4, 2015 For detailed financial information please see our annual/quarterly reports and/or conference call materials

Adelaide Brighton Ltd ACN 007 596 018

Level 1 157 Grenfell Street Adelaide SA 5000 GPO Box 2155 Adelaide SA 5001 Adelaide Brighton Ltd ACN 007 596 018 Telephone (08) 8223 8000 International +618 8223 8000 Facsimile (08) 8215 0030 www.adbri.com.au

Level 1 157 Grenfell Street Adelaide SA 5000 GPO Box 2155 Adelaide SA 5001 Adelaide Brighton Ltd ACN 007 596 018 Telephone (08) 8223 8000 International +618 8223 8000 Facsimile (08) 8215 0030 www.adbri.com.au

A Leading Global Health Care Group

A Leading Global Health Care Group JP Morgan Milan Investor Forum October 1, 2015 For detailed financial information please see our annual/quarterly reports and/or conference call materials on www.fresenius.com/ir.

A Leading Global Health Care Group JP Morgan Milan Investor Forum October 1, 2015 For detailed financial information please see our annual/quarterly reports and/or conference call materials on www.fresenius.com/ir.

Fiscal Year 2015 1st Quarter Earnings Conference Call

Fiscal Year 2015 1st Quarter Earnings Conference Call January, 2015 www.jacobs.com worldwide Forward-Looking Statement Disclaimer Statements included in this presentation that are not based on historical

Fiscal Year 2015 1st Quarter Earnings Conference Call January, 2015 www.jacobs.com worldwide Forward-Looking Statement Disclaimer Statements included in this presentation that are not based on historical

Nemetschek Group Company Presentation. July 2014

Nemetschek Group Company Presentation July 2014 Agenda Nemetschek Group: In brief Strategy Internationalization Industry mega trends Innovations Financial data Q1 2014 Nemetschek share Why invest? 2 A

Nemetschek Group Company Presentation July 2014 Agenda Nemetschek Group: In brief Strategy Internationalization Industry mega trends Innovations Financial data Q1 2014 Nemetschek share Why invest? 2 A

Data and Trends. Environmental protection and Safety

Data and Trends Environmental protection and Safety 2006 EMS-GRIVORY Performance Polymers EMS-GRIVORY Extrusion Polymers EMS-GRILTECH EMS-PRIMID EMS-PATVAG EMS-SERVICES Data and Trends 2006 Protection

Data and Trends Environmental protection and Safety 2006 EMS-GRIVORY Performance Polymers EMS-GRIVORY Extrusion Polymers EMS-GRILTECH EMS-PRIMID EMS-PATVAG EMS-SERVICES Data and Trends 2006 Protection

1Q 2016 Highlights Total volume (kmt) Adjusted EBITDA (EUR/Millions) Adjusted EPS (EUR) 1Q16 1Q15 Y-o-Y Comparison 277.8 252.9 9.9% 54.0 53.9 0.1% 0.28 0.33-15.2% Strong volume gains from both Specialty

1Q 2016 Highlights Total volume (kmt) Adjusted EBITDA (EUR/Millions) Adjusted EPS (EUR) 1Q16 1Q15 Y-o-Y Comparison 277.8 252.9 9.9% 54.0 53.9 0.1% 0.28 0.33-15.2% Strong volume gains from both Specialty

K+S Group FY/Q4 2014 Analyst conference. 12 March 2015, Frankfurt am Main. Norbert Steiner, CEO Dr. Burkhard Lohr, CFO

Experience growth. FY/Q4 2014 Analyst conference 12 March 2015, Frankfurt am Main Norbert Steiner, CEO Dr. Burkhard Lohr, CFO Agenda A. FY 2014 Financials B. Projects and initiatives C. Q4 Financials D.

Experience growth. FY/Q4 2014 Analyst conference 12 March 2015, Frankfurt am Main Norbert Steiner, CEO Dr. Burkhard Lohr, CFO Agenda A. FY 2014 Financials B. Projects and initiatives C. Q4 Financials D.

Realizing the full potential of maintenance. Company Introduction

Realizing the full potential of maintenance Company Introduction CONTENTS Quant is a global leader in industrial maintenance. For over 25 years, we have been realizing the full potential of maintenance

Realizing the full potential of maintenance Company Introduction CONTENTS Quant is a global leader in industrial maintenance. For over 25 years, we have been realizing the full potential of maintenance

Analysts and press conference for the financial year 2010. March 16, 2011

Analysts and press conference for the financial year 2010 March 16, 2011 Welcome Walter Gränicher Jost Sigrist Werner Schmidli Chairman of the Board of Directors Chief Executive Officer Chief Financial

Analysts and press conference for the financial year 2010 March 16, 2011 Welcome Walter Gränicher Jost Sigrist Werner Schmidli Chairman of the Board of Directors Chief Executive Officer Chief Financial

Q3/2015 Results Analyst and Investor Conference Call. 29 October 2015

Q3/2015 Results Analyst and Investor Conference Call 29 October 2015 Deutsche Börse Group 1 Highlights Q3/2015 Results Presentation Index derivatives and cash equities benefitted from higher volatility;

Q3/2015 Results Analyst and Investor Conference Call 29 October 2015 Deutsche Börse Group 1 Highlights Q3/2015 Results Presentation Index derivatives and cash equities benefitted from higher volatility;

DCC Overview DCC is an international sales, marketing, distribution and business support services group operating across four divisions

Company Overview DCC Overview DCC is an international sales, marketing, distribution and business support services group operating across four divisions Profit by division * Profit by geography * 14% 4%

Company Overview DCC Overview DCC is an international sales, marketing, distribution and business support services group operating across four divisions Profit by division * Profit by geography * 14% 4%

Global Oil & Gas Suite

IHS ENERGY Global Oil & Gas Suite Comprehensive analysis and insight on upstream opportunities, risk, infrastructure dynamics, and downstream markets Global Oil & Gas Suite Make optimal decisions about

IHS ENERGY Global Oil & Gas Suite Comprehensive analysis and insight on upstream opportunities, risk, infrastructure dynamics, and downstream markets Global Oil & Gas Suite Make optimal decisions about

F-Secure Corporation - Interim report Q3 2009 (Unaudited)

") F-Secure Corporation - Interim report Q3 2009 (Unaudited) Kimmo Alkio, President and CEO Protecting the irreplaceable f-secure.com Highlights in Q3 2009 Solid profitability; EBIT 21% of revenues Revenue

F-Secure Corporation - Interim report Q3 2009 (Unaudited) Kimmo Alkio, President and CEO Protecting the irreplaceable f-secure.com Highlights in Q3 2009 Solid profitability; EBIT 21% of revenues Revenue

THE WAY TO MAKE IT. Results 2013 and Outlook 2014. Agenda. 26 March 2014. Results 2013. Focus and outlook 2014 Discussion

Results 2013 and Outlook 2014 26 March 2014 26 March 2014 / Results 2013 and Outlook 2014 / 1 Agenda Results 2013 Operational performance Financial performance Focus and outlook 2014 Discussion 26 March

Results 2013 and Outlook 2014 26 March 2014 26 March 2014 / Results 2013 and Outlook 2014 / 1 Agenda Results 2013 Operational performance Financial performance Focus and outlook 2014 Discussion 26 March

INTERIM REPORT 1.1.-30.6.2004

INTERIM REPORT 1.1.-30.6.2004 RAUTE OYJ 1 (9) RAUTE OYJ S INTERIM REPORT FOR JANUARY 1 JUNE 30, 2004 Net sales MEUR 41.9 (MEUR 33.0) and operating profit MEUR 4.1 (MEUR -7.4) increased. Net sales of current

INTERIM REPORT 1.1.-30.6.2004 RAUTE OYJ 1 (9) RAUTE OYJ S INTERIM REPORT FOR JANUARY 1 JUNE 30, 2004 Net sales MEUR 41.9 (MEUR 33.0) and operating profit MEUR 4.1 (MEUR -7.4) increased. Net sales of current