COMMERCIAL CREDIT REPORT SAMPLE

|

|

|

- Tobias Collins

- 10 years ago

- Views:

Transcription

1 COMMERCIAL CREDIT REPORT SAMPLE

2

3 1 DATE/TIME STAMP Provides the date and time when the inquiry was made as recorded by Equifax (Eastern Time). Average Open Balance: The average balance of all open, non-charged off accounts. (There must be at least two tradelines for this value to be returned.) 2 3 COMPANY PROFILE Provides the first business name and address on the returned folder which most closely matches your Equifax eport inquiry information, as well as firmographic information about the business. The EFX ID is a unique nine-digit number that identifies a business folder; the folder may contain multiple businesses and/or business locations for the same corporate entity; if the EFX ID is used on the inquiry, then only the EFX ID is used to locate a folder and the most recently reported business name and address are returned. Inquiry Information: Displays the information used to submit the inquiry. 8 Recent Activity: Highlights recent key activities that have occurred on the file within the last 120 to 150 days from the date of the inquiry. Number of Accounts Delinquent: Number of accounts that have been delinquent within the last 120 to 150 days. New Accounts Opened: Number of accounts opened within the last 120 to 150 days. Inquiries: Number of account origination inquiries that have occurred within the last 120 to 150 days. Accounts Updated: Number of accounts updated within the last 120 to 150 days Alerts: Provides alert notices to indicate key differences between the inquiry information and the file content; may also return alerts from a requested consumer product (e.g., FACT Act alerts). SCORES Available upon request; allows for more accurate assessment of the risk level of the business; detailed information is available by clicking on the hyperlink. (Refer to page 13.) PUBLIC RECORDS Public record summary table notes the presence of bankruptcies, judgments and liens, and returns the status, number, and dollar amounts for judgments and liens; eport users have the ability to sort by Dollar Amount and Most Recent Date Filed; detailed information is available by clicking on the hyperlink. (Refer to page 11.) CREDIT REPORT SUMMARY Summarizes credit data within the business folder into financial and non-financial segments; the attributes may use all of the credit experiences or cover a specific evaluation period of time; allows you to quickly assess the risk level of the business by providing nine key attributes: Number of Accounts: The count of open and closed accounts on the file. Credit Active Since: Returns the oldest Date Opened, Date Reported or Years Sold for that tradeline, indicating the duration of the relationship. Number of Charge-Offs: Number of open or closed accounts for which there has been any reported charge-off. Total Past Due: The total delinquent dollar amount on both open and closed accounts owed by this business as reported by its credit grantors. Most Severe Status in 24 Months: Returns the most severe Current Status experienced on any account during the most recent 24 months from the date of inquiry; refer to the Current Status Descriptions table on page 4 for the severity levels. Single Highest Credit Extended: The single largest high credit, original loan, current credit or balance dollar amount extended to this business based on reported accounts. This figure can reflect credit lines that have not yet been used. Total Current Credit Exposure: The maximum potential liability the business could incur today based upon recent account information. Financial amount includes total balances owed plus available credit limit; Non-Financial is a total of balances owed. Median Balance: Returns the median value of all open, noncharged-off accounts. (There must be at least three tradelines for this value to be returned and $0 balances are included.) Financial Information: Obtained through an exclusive data sharing agreement with the Small Business Financial Exchange, Inc. (SBFE), and consists of information on business credit cards, loans, leases, and other credit extended by financial institutions, leasing companies and credit card issuers; highlights of financial accounts are available by clicking on the hyperlink. (Refer to page 3.) Non-Financial Information: Composed of trade payment history from a wide variety of suppliers that provide products and services to businesses on an invoice basis; highlights of non-financial accounts are available by clicking on the hyperlink. (Refer to page 7.) CREDIT USAGE Illustrates available credit line dollars which could be used for meeting other financial obligations. Credit line dollars based on revolving financial accounts; excludes term loans, leases, and charged-off accounts; includes open, revolving accounts and closed accounts still owing a balance. AVERAGE DAYS BEYOND TERMS Displays the dollar-weighted average days beyond terms on nonfinancial accounts within the last 12 months from the date of the inquiry; calculated from dollar amounts reported for aging categories 1-5; if no information was reported for a given month within the 12- month period, no line will appear in the graph for that month. Recent Trend (Box): Average Days Beyond Terms calculated within the last 120 to 150 days from the date of inquiry. PAYMENT INDEX TM A dollar-weighted indicator of a business s past and current payment performance based on the total number of financial and non-financial payment experiences in the Equifax Commercial database. The median Payment Index for the inquired business s industry is also returned for benchmark purposes, provided there is enough information in the Equifax Commercial database on that particular industry to ensure a statistically valid value. The chart below provides a suggested interpretation of the Payment Index value: Payment Index Days Past Due 90+ Paid As Agreed Days Past Due Days Past Due Days Past Due Days Past Due Days Past Due 2

4 15 3

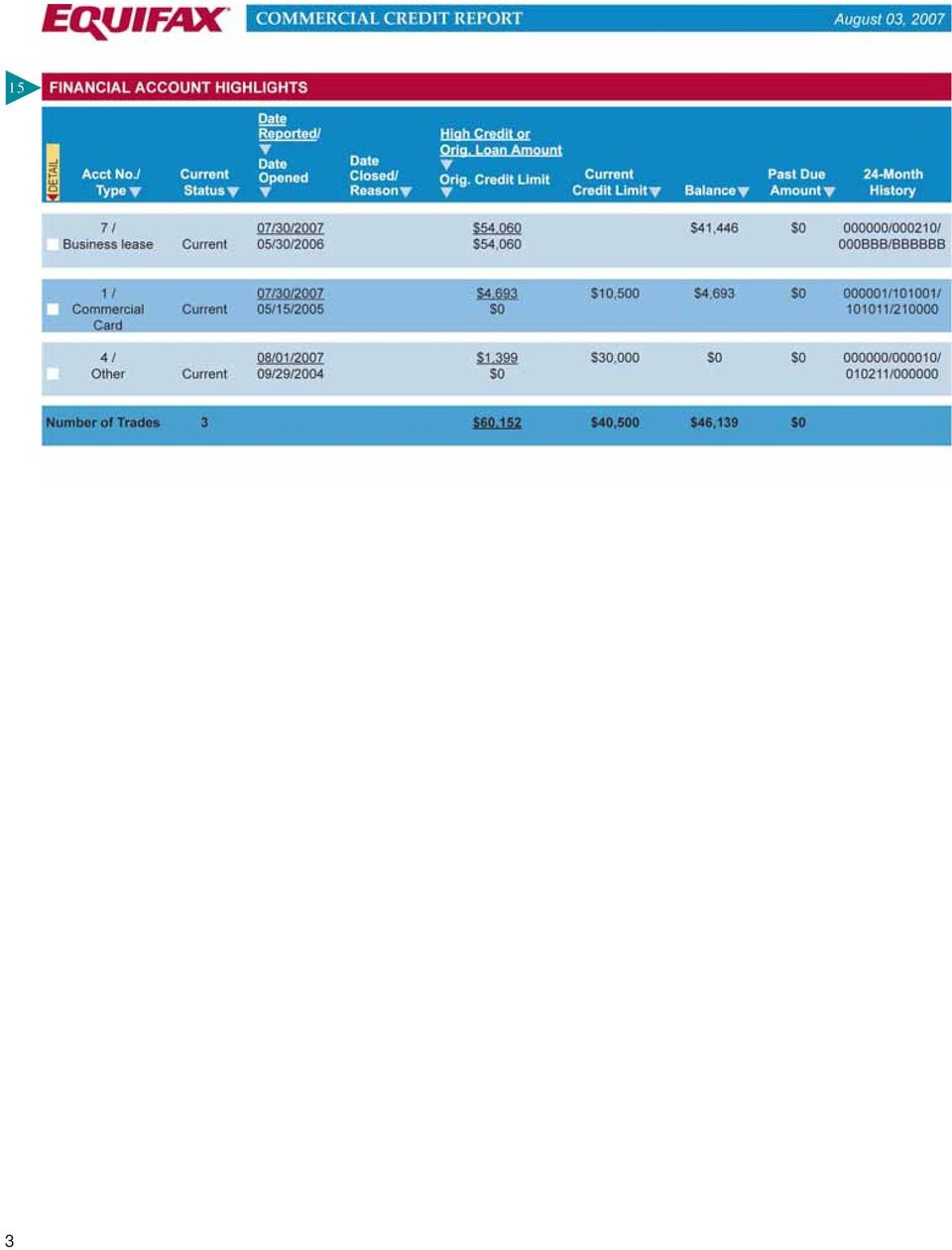

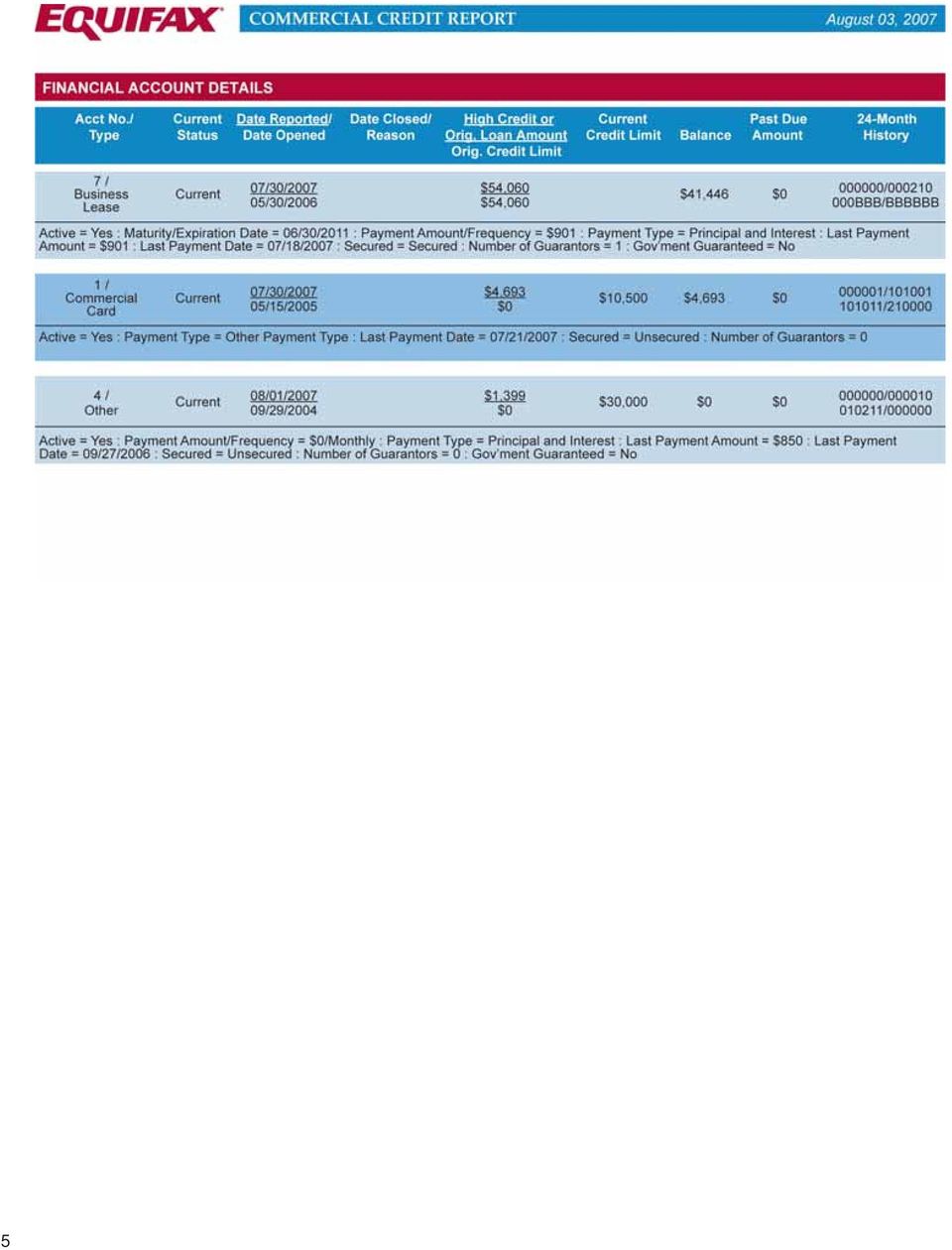

5 15 FINANCIAL ACCOUNT HIGHLIGHTS Displays summary information for each financial account on the business folder; columns can be sorted in ascending or descending order; check boxes enable the user to select one or more records and hyperlink to the Account Details section. (Refer to page 5.) Account Number/Type: Term loan, line of credit, commercial card, business lease, letter of credit, open-ended credit line, or other. Current Status: The overall payment performance status of the most recently reported period. Date Reported/Date Opened: Date Reported refers to the most recent data submission received from the contributing data source; Date Opened refers to the date on which the specific credit obligation was initiated. Date Closed/Reason: Date account was reported closed/reason for closing of account. High Credit/Original Loan Amount/ Original Credit Limit: Highest credit reported/original loan amount/original credit limit. Current Credit Limit: Current credit limit reported. Balance: Total reported balance, including any past due amount. Past Due Amount: Total amount past due from each aging category. 24-Month History: The 24-month grid contains consecutive payment performance indicators for the 24 months prior to the payment date. The far left position in the grid represents the previous month s overall account payment status, continuing in monthly increments from left to right for the entire 24-month period. The grid provides a convenient recap of historical payment performance for each of the business s accounts. CURRENT STATUS DESCRIPTIONS Status B Description Unknown, which may indicate that the credit relationship did not exist before this time period. 0 Current S Slow 1 Slow Up to 30 2 Slow Up to 60 3 Slow Up to 90 4 Slow Up to Slow Collection 7 Non-accrual account 8 Repossession/Foreclosure 9 Charge-Off 4

6 5

7 6

8 16 7

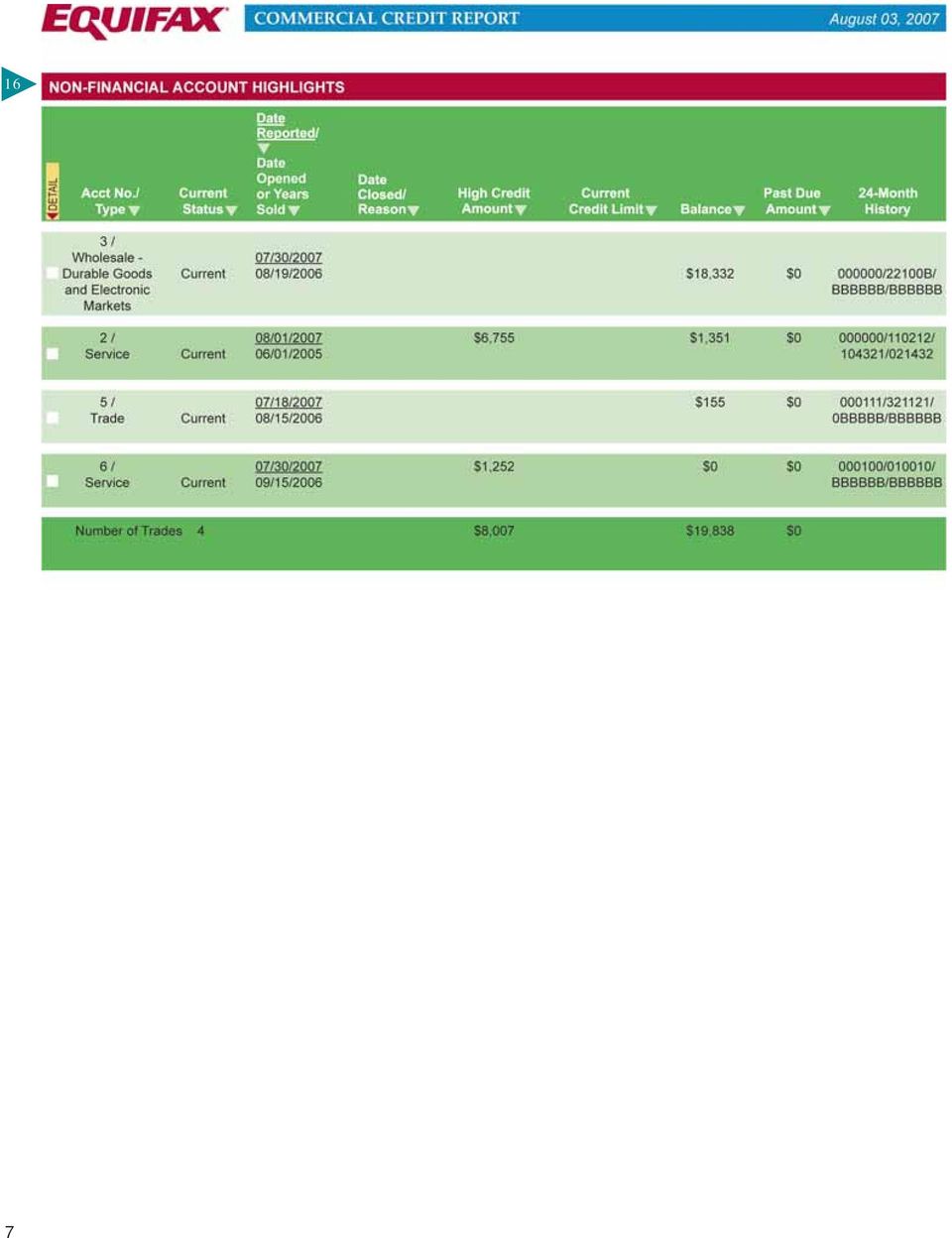

9 16 NON-FINANCIAL ACCOUNT HIGHLIGHTS Displays summary information for each non-financial account on the business folder; columns can be sorted in ascending or descending order; check boxes enable the user to select one or more records and hyperlink to the Account Details section. (Refer to page 9.) Account Number/Type: Trade, service or other industry. Current Status: The overall payment performance status of the most recently reported period. Date Reported/Date Opened/Years Sold: Date Reported refers to the most recent data submission received from the contributing data source; Date Opened/Years Sold refers to when the overall supplier/customer relationship was initiated. Date Closed/Reason: Date account was reported closed/reason for closing of account. High Credit Amount: Highest reported balance from a supplier. Current Credit Limit: Current credit limit reported. Balance: Total reported balance including any past due amount. Past Due Amount: Total amount past due from each aging category. 24-Month History: The 24-month grid contains consecutive payment performance indicators for the 24 months prior to the payment date. The far left position in the grid represents the previous month s overall account payment status, continuing in monthly increments from left to right for the entire 24-month period. The grid provides a convenient recap of historical payment performance for each of the business s accounts. CURRENT STATUS DESCRIPTIONS Status B Description Unknown, which may indicate that the credit relationship did not exist before this time period. 0 Current S Slow 1 Slow Up to 30 2 Slow Up to 60 3 Slow Up to 90 4 Slow Up to Slow Collection 7 Non-accrual account 8 Repossession/Foreclosure 9 Charge-Off 8

10 9

11 10

12 6 11

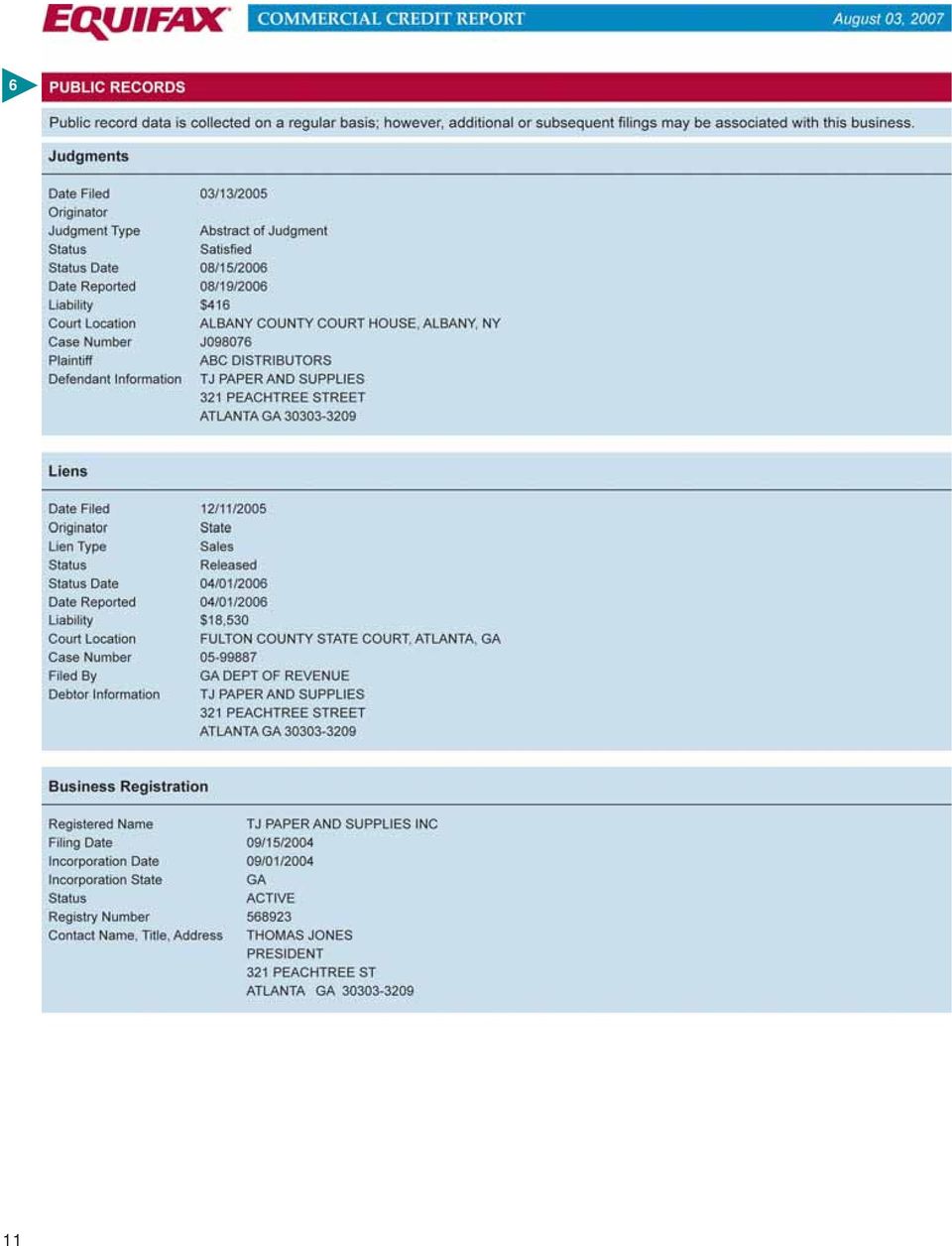

13 6 PUBLIC RECORDS Returns detailed information for any bankruptcies, judgments or liens on file for the business; also returns business registration information obtained from Secretary of State Offices or other trusted sources. Business registration fields include: Registered Name: The business name provided at the time of registration. Filing Date: This is the date the state recorded as the paperwork transaction date. It may or may not be the same as the incorporation date. This date will usually change annually and is used to indicate when the most recent update was received by the state. It is possible that the filing date is several years old because the state did not update a "lapsed or inactive" filing. Incorporation Date: This is the date of the original filing of incorporation papers. It will not change from year to year. This is not the date the business filed with the papers with the state. Incorporation State: This may include any of the 50 U.S. states plus Washington D.C.; only the "domestic" incorporation state is returned. Status: This field reflects the status of the business on the records of the Secretary of State. It is not necessarily an indication of whether the business actively engages in business activity. It will not reflect whether the entity has filed for bankruptcy. There are two valid status values: active and inactive. Registry Number: This is the number assigned by the state office. Contact Name, Title, Address: This field includes officer names, titles and addresses. More than one officer may be returned. Additionally, not all the officers may be listed. 12

14

15 5 DECISIONING DETAIL Displays the definition, the numeric value and reason codes (if applicable) for each score appended to the business folder. Currently, the following decisioning tools are available with the Commercial Credit Report. Small Business Credit Risk Score for Suppliers: Predicts the likelihood of a small business incurring greater than 90 days severe delinquency, charge-off or bankruptcy on supplier (trade) accounts over the next 12 months; score range is , with the lower score indicating higher risk and 0 indicating a bankruptcy on the folder; up to four reason codes are returned indicating the top factors influencing the score. *This score includes an option that blends principal (consumer) credit information with the commercial data sources. Small Business Credit Risk Score for Financial Services: Predicts the likelihood of a small business incurring greater than 90 days severe delinquency, charge-off or bankruptcy on financial services accounts over the next 12 months; score range is , with the lower score indicating higher risk and a 0 indicating a bankruptcy on the folder; up to four reason codes may be returned indicating the top factors influencing the score. *This score includes an option that blends principal (consumer) credit information with the commercial data sources. Risk Class : A statistically valid tool designed specifically for the supplier industry; returns an easy-to-understand measurement of the risk level a prospect or customer poses; population is segmented into five risk classes based on the likelihood that the business will incur greater than 90 days severe delinquency, charge-off or bankruptcy over the next 12 months. Risk Class Likelihood of Delinquency Delinquency Rate (out of 1,000) 1 Low 27 2 Below Average 60 3 Average High Severe Bankruptcy on file N/A No recent account information on file The delinquency rate indicates how many prospects/customers out of every thousand may become a serious credit risk. For example: in Risk Class 1, 27 out of every 1,000 are likely to become delinquent. Business Failure Risk Score : Predicts the likelihood of a business failure (formal or informal bankruptcies) within a 12-month period; score range is , with the lower score indicating higher risk and a 0 indicating a bankruptcy on the folder; up to four reason codes are returned indicating the top factors influencing the score. Suggested Credit Limit : A suggested credit amount to extend to a particular prospect or customer; this guideline is based upon the credit amount that historically has been extended to those with similar firmographics and risk profiles. *Suggested Credit Limit is only a guideline and should not be used as the sole or primary factor in making a credit decision. Equifax is not responsible for any liability or losses based on the recommendation ADDITIONAL INFORMATION Provides alternate company information including DBA names, addresses, phone numbers and SIC/NAICS; also returns owner/guarantor information, comments from business owners or credit grantors, and recent inquiries. CONTACT US Provides address, phone number and address where your customer can initiate a dispute. 14

16 1550 Peachtree Street Atlanta, Georgia Phone: Equifax and Equifax eport are registered trademarks of Equifax Inc. Equifax Commercial Credit Report, Small Business Credit Risk Score, Risk Class, Business Failure Risk Score, Suggested Credit Limit, Payment Index and EFX ID are trademarks of Equifax Inc. Copyright 2007, Equifax Inc., Atlanta, Georgia. All rights reserved. Printed in the U.S.A. EFS-715-ADV 11/07

Commercial Credit ReportTM

COMMERCIAL INFORMATION SOLUTIONS >Training Guide Commercial Credit ReportTM 1 2 4 3 5 6 11 7 9 10 12 8 13 14 1 1 2 3 4 DATE/TIME STAMP Provides the date and time when the inquiry was made as recorded by

COMMERCIAL INFORMATION SOLUTIONS >Training Guide Commercial Credit ReportTM 1 2 4 3 5 6 11 7 9 10 12 8 13 14 1 1 2 3 4 DATE/TIME STAMP Provides the date and time when the inquiry was made as recorded by

Commercial Credit ReportTM

COMMERCIAL INFORMATION SOLUTIONS >Training Guide Commercial Credit ReportTM 1 2 4 3 5 6 11 7 9 10 12 8 13 14 1 1 2 3 4 5 6 7 DATE/TIME STAMP Provides the date and time when the inquiry was made as recorded

COMMERCIAL INFORMATION SOLUTIONS >Training Guide Commercial Credit ReportTM 1 2 4 3 5 6 11 7 9 10 12 8 13 14 1 1 2 3 4 5 6 7 DATE/TIME STAMP Provides the date and time when the inquiry was made as recorded

COMMERCIAL CREDIT REPORT SAMPLE

COMMERCIAL CREDIT REPORT SAMPLE 1 2 3 4 5 6 11 7 8 9 12 10 13 14 1 1 DATE/TIME STAMP Provides the date and time when the inquiry was made as recorded by Equifax (Eastern Time). Average Open Balance: Average

COMMERCIAL CREDIT REPORT SAMPLE 1 2 3 4 5 6 11 7 8 9 12 10 13 14 1 1 DATE/TIME STAMP Provides the date and time when the inquiry was made as recorded by Equifax (Eastern Time). Average Open Balance: Average

SMALL BUSINESS CREDIT REPORT SAMPLE

SMALL BUSINESS CREDIT REPORT SAMPLE BUSINESS AT A GLANCE Equifax Small Business Credit Report 1 COMPANY PROFILE SCORES 4 Inquiry on 8/11/2004 Customer Ref: SEAST The Knapsack D/B/A TK s 1115 Magnolia Place

SMALL BUSINESS CREDIT REPORT SAMPLE BUSINESS AT A GLANCE Equifax Small Business Credit Report 1 COMPANY PROFILE SCORES 4 Inquiry on 8/11/2004 Customer Ref: SEAST The Knapsack D/B/A TK s 1115 Magnolia Place

Training Guide. Business Credit Industry Report Plus TM 2.0

Training Guide Business Credit Industry Report Plus TM 2.0 BUSINESS CREDIT INDUSTRY REPORT PLUS 2.0 1 September 3, 2010 12:27 p.m. EDT 2 Customer Ref: SW1224 EFX ID: Company Profile: Telephone: Tax ID/SSN:

Training Guide Business Credit Industry Report Plus TM 2.0 BUSINESS CREDIT INDUSTRY REPORT PLUS 2.0 1 September 3, 2010 12:27 p.m. EDT 2 Customer Ref: SW1224 EFX ID: Company Profile: Telephone: Tax ID/SSN:

Canada Business Credit Report

COMMERCIAL INFORMATION SOLUTIONS >User Guide Canada Business Credit Report COMMERCIAL INFORMATION SOLUTIONS BUSINESS CREDIT REPORT 1 Business information Company name BUSINESS CREDIT Requestor ID NBREN

COMMERCIAL INFORMATION SOLUTIONS >User Guide Canada Business Credit Report COMMERCIAL INFORMATION SOLUTIONS BUSINESS CREDIT REPORT 1 Business information Company name BUSINESS CREDIT Requestor ID NBREN

CREDIT SCORE USER GUIDE

Page 1 of 11 ABOUT EQUIFAX Equifax empowers businesses and consumers with information they can trust. A global leader in information solutions, we leverage one of the largest sources of consumer and commercial

Page 1 of 11 ABOUT EQUIFAX Equifax empowers businesses and consumers with information they can trust. A global leader in information solutions, we leverage one of the largest sources of consumer and commercial

ALERTS NOTIFICATION USER GUIDE

Page 1 of 10 ABOUT EQUIFAX ALERTS NOTIFICATION USER GUIDE Equifax Canada Inc. Box 190 Jean Talon Station Montreal, Quebec H1S 2Z2 Equifax empowers businesses and consumers with information they can trust.

Page 1 of 10 ABOUT EQUIFAX ALERTS NOTIFICATION USER GUIDE Equifax Canada Inc. Box 190 Jean Talon Station Montreal, Quebec H1S 2Z2 Equifax empowers businesses and consumers with information they can trust.

CREDIT REPORT USER GUIDE

Page 1 of 17 ABOUT EQUIFAX CREDIT REPORT USER GUIDE Equifax Canada Inc. Box 190 Jean Talon Station Montreal, Quebec H1S 2Z2 Equifax empowers businesses and consumers with information they can trust. A

Page 1 of 17 ABOUT EQUIFAX CREDIT REPORT USER GUIDE Equifax Canada Inc. Box 190 Jean Talon Station Montreal, Quebec H1S 2Z2 Equifax empowers businesses and consumers with information they can trust. A

The TransUnion Credit Report Training Guide

The TransUnion Credit Report Training Guide Credit Report TransUnion Credit Report Codes ECOA (Equal Credit Opportunity Act) Inquiry and Account Designators A Authorized user of shared account C Joint

The TransUnion Credit Report Training Guide Credit Report TransUnion Credit Report Codes ECOA (Equal Credit Opportunity Act) Inquiry and Account Designators A Authorized user of shared account C Joint

Reviewing C Your Credit Report

chapter 2 Reviewing C Your Credit Report What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

chapter 2 Reviewing C Your Credit Report What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

Enhanced Commercial Credit Report - Help

Enhanced Commercial Credit Report - Help Report Item Payment Index (PI) Description The Payment Index (PI) is a numeric measure of the businesses payment habits, and is calculated strictly on the distribution

Enhanced Commercial Credit Report - Help Report Item Payment Index (PI) Description The Payment Index (PI) is a numeric measure of the businesses payment habits, and is calculated strictly on the distribution

Credco Instant Merge Credit Report

2 Credco Instant Merge Credit Report Ref#: 74504 05/26/205 Upgrade TID#: 74504 05/26/205 2:38:43 Prepared For: Prepared By: INSTANT MERGE Client Loan # :42234B CoreLogic Credco SAMPLE RPEORT Account #

2 Credco Instant Merge Credit Report Ref#: 74504 05/26/205 Upgrade TID#: 74504 05/26/205 2:38:43 Prepared For: Prepared By: INSTANT MERGE Client Loan # :42234B CoreLogic Credco SAMPLE RPEORT Account #

TransUnion Credit Report User Guide UNITED STATES

TransUnion Credit Report User Guide UNITED STATES Introduction to the Credit Report User Guide Thousands of companies around the world depend on TransUnion Credit Reports for the consumer insight they

TransUnion Credit Report User Guide UNITED STATES Introduction to the Credit Report User Guide Thousands of companies around the world depend on TransUnion Credit Reports for the consumer insight they

Canada Business Credit Report

COMMERCIAL INFORMATION SOLUTIONS >Sample Report Canada Business Credit Report COMMERCIAL INFORMATION SOLUTIONS BUSINESS CREDIT Business information Company name BUSINESS CREDIT Requestor ID NBREN TEST

COMMERCIAL INFORMATION SOLUTIONS >Sample Report Canada Business Credit Report COMMERCIAL INFORMATION SOLUTIONS BUSINESS CREDIT Business information Company name BUSINESS CREDIT Requestor ID NBREN TEST

Understanding Your Credit Score and How You Can Improve It

Understanding Your Credit Score and How You Can Improve It How is your score calculated? The exact formula is a mystery and protected by the Federal Trade Commission Think of it as a secret recipe. Credit

Understanding Your Credit Score and How You Can Improve It How is your score calculated? The exact formula is a mystery and protected by the Federal Trade Commission Think of it as a secret recipe. Credit

CBCInnovis Infile Credit Report Reference Guide

1 2 3 4 5 6 6 7 7 8 A A A B C C C 9 D E F G H I J K 10 11 1 1 2 3 4 5 6 7 8 9 PROCESSING CENTER CONTACT INFORMATION: Please contact the Processing Center if you have any questions regarding a CBCInnovis

1 2 3 4 5 6 6 7 7 8 A A A B C C C 9 D E F G H I J K 10 11 1 1 2 3 4 5 6 7 8 9 PROCESSING CENTER CONTACT INFORMATION: Please contact the Processing Center if you have any questions regarding a CBCInnovis

How To Know Your Credit Risk

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Credit Profile Report for Tenant Screening

Credit Profile Report for Tenant Screening Identify who s likely to be your best tenant. The best screening decisions begin with the best information. Experian s Credit Profile Report and Score helps you

Credit Profile Report for Tenant Screening Identify who s likely to be your best tenant. The best screening decisions begin with the best information. Experian s Credit Profile Report and Score helps you

Business Funding Evaluation YOUR BUSINESS NAME

Business Funding Evaluation Prepared Exclusively For: YOUR BUSINESS NAME YOUR ADDRESS & CONTACT Prepared By: The Credit and Funding Pros Thank You For Allowing Us to Serve You! Business Funding Evaluation

Business Funding Evaluation Prepared Exclusively For: YOUR BUSINESS NAME YOUR ADDRESS & CONTACT Prepared By: The Credit and Funding Pros Thank You For Allowing Us to Serve You! Business Funding Evaluation

Live Report : YOUR BASIC BUSINESS CREDIT, LLC. Today: Thursday, October 27, 2011. Company Summary. Currency: Shown in USD unless otherwise indicated

ATTN: Report Printed:October 27, 2011 Live Report : YOUR BASIC BUSINESS CREDIT, LLC. D-U-N-S Number: 00-000-0000 Endorsement/Billing Reference: Endorsement : Company Summary Currency: Shown in USD unless

ATTN: Report Printed:October 27, 2011 Live Report : YOUR BASIC BUSINESS CREDIT, LLC. D-U-N-S Number: 00-000-0000 Endorsement/Billing Reference: Endorsement : Company Summary Currency: Shown in USD unless

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549. FORM 8-K Current Report

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K Current Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K Current Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event

TransUnion Credit Report. Training Guide

TransUnion Credit Report Training Guide Sample TransUnion Credit Report 1 1A This sample report is intended for education purposes. 2 2A 2B 2C The actual Credit Report you receive will be customized to

TransUnion Credit Report Training Guide Sample TransUnion Credit Report 1 1A This sample report is intended for education purposes. 2 2A 2B 2C The actual Credit Report you receive will be customized to

CREDIT REPORTING FOR A SMALL BUSINESS

CREDIT REPORTING FOR A SMALL BUSINESS Objectives Northern Initiatives is committed to entrepreneurs like you, because you are the people who are creating jobs and enabling the communities of our region

CREDIT REPORTING FOR A SMALL BUSINESS Objectives Northern Initiatives is committed to entrepreneurs like you, because you are the people who are creating jobs and enabling the communities of our region

Understanding and managing your credit

Understanding and managing your credit Overview Understanding how credit works and how it affects your chances of getting approved for a loan is important. In this presentation, you ll learn helpful ways

Understanding and managing your credit Overview Understanding how credit works and how it affects your chances of getting approved for a loan is important. In this presentation, you ll learn helpful ways

Insurance Score Models

Insurance Score Models Prepared by State of Alaska Division of Insurance Department of Community and Economic Development www.dced.state.ak.us/insurance (907) 465-2020 Insurance Score Models Some insurers

Insurance Score Models Prepared by State of Alaska Division of Insurance Department of Community and Economic Development www.dced.state.ak.us/insurance (907) 465-2020 Insurance Score Models Some insurers

Experian BusinessIQ Premier Profile SM

Experian BusinessIQ Premier Profile SM Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc. Other product and company names mentioned herein

Experian BusinessIQ Premier Profile SM Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc. Other product and company names mentioned herein

United States of America 46-0358360

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K Current Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K Current Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event

Trans Union Credit Report Tutorial

FROM THE TOP 1. The Heading is at the very top right of the report. It contains the Credit Bureau's information. The Credit Agency, their address, their phone number, and the date the report was inquired

FROM THE TOP 1. The Heading is at the very top right of the report. It contains the Credit Bureau's information. The Credit Agency, their address, their phone number, and the date the report was inquired

CITIBANK CREDIT CARD ISSUANCE TRUST

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K Current Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K Current Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event

Earning Extra Credit. Understanding what it takes to maintain and manage good credit now and for your future

Credit 101 Why Credit is Important 3 Your Credit Score 5 FICO Scoring - From Good to Bad 7 Credit Bureaus 8 Credit-Worthy vs. Credit-Ready 9 Are you Drowning in Debt? 10 2 Why Credit is Important College

Credit 101 Why Credit is Important 3 Your Credit Score 5 FICO Scoring - From Good to Bad 7 Credit Bureaus 8 Credit-Worthy vs. Credit-Ready 9 Are you Drowning in Debt? 10 2 Why Credit is Important College

Student Loans and Credit Reports

Student Loans and Credit Reports We Will Discuss The role of credit in personal finance Review of credit terms and factors Impact of student loans on reports and scores Next steps you can take to encourage

Student Loans and Credit Reports We Will Discuss The role of credit in personal finance Review of credit terms and factors Impact of student loans on reports and scores Next steps you can take to encourage

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549. FORM 8-K Current Report

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K Current Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K Current Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event

Profitably Managing Risk in Your Credit Portfolio

Profitably Managing Risk in Your Credit Portfolio An Equifax White Paper February 2007 Author: Richard Becker Assistant Vice President, Product Development Equifax Inc. As Acquisition Marketing Cools Off,

Profitably Managing Risk in Your Credit Portfolio An Equifax White Paper February 2007 Author: Richard Becker Assistant Vice President, Product Development Equifax Inc. As Acquisition Marketing Cools Off,

Citibank (South Dakota), National Association on behalf of Citibank Credit Card Master Trust I. United States of America 46-0358360

, National Association on behalf of Citibank Credit Card Master Trust I. United States of America 46-0358360") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K Current Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K Current Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event

FICO Score Factors Guide

Key score factors explain the top factors that affected your FICO Score. The order in which your FICO Score factors are listed is important. The first indicates the area that most affected your FICO Score

Key score factors explain the top factors that affected your FICO Score. The order in which your FICO Score factors are listed is important. The first indicates the area that most affected your FICO Score

How to improve your FICO Score in perilous times By Blair Ball. National Distribution of FICO Scores

How to improve your FICO Score in perilous times By Blair Ball When you re applying for credit whether it s a credit card, a car loan, a personal loan or a mortgage lenders want to know your credit risk

How to improve your FICO Score in perilous times By Blair Ball When you re applying for credit whether it s a credit card, a car loan, a personal loan or a mortgage lenders want to know your credit risk

Understanding Your FICO Score

Understanding Your FICO Score 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Report 1 Checking Your Credit Report

Understanding Your FICO Score 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Report 1 Checking Your Credit Report

Live Report : Your Future Business Credit, Inc. Today: Friday, October 28, 2011. Company Summary. Currency: Shown in USD unless otherwise indicated

ATTN: Report Printed:October 28, 2011 Live Report : Your Future Business Credit, Inc. D-U-N-S Number: 00-000-0000 Endorsement/Billing Reference: D&B Address Address Phone Location Type Single Location

ATTN: Report Printed:October 28, 2011 Live Report : Your Future Business Credit, Inc. D-U-N-S Number: 00-000-0000 Endorsement/Billing Reference: D&B Address Address Phone Location Type Single Location

All About Credit Reports from A to Z

All About Credit Reports from A to Z Adverse Action Notice A notice that you have been denied credit, employment, insurance, or other benefits based on information in a credit report. The notice should

All About Credit Reports from A to Z Adverse Action Notice A notice that you have been denied credit, employment, insurance, or other benefits based on information in a credit report. The notice should

FICO Score Factors Guide - TransUnion

Factors Guide - TransUnion The consumer-friendly reason descriptions and things to keep in mind below are provided for use within FICO Open Access customer displays. The table includes a reason description

Factors Guide - TransUnion The consumer-friendly reason descriptions and things to keep in mind below are provided for use within FICO Open Access customer displays. The table includes a reason description

How to read a CBCWeb Credit Report

How to read a Web redit Report 1 2 4 3 5 6 7 1. ureau ddress. 2. ureau phone and fax numbers. 3. The header identifies what type the report is, such as Infile, Full Report or Decision reports. 4. Prepared

How to read a Web redit Report 1 2 4 3 5 6 7 1. ureau ddress. 2. ureau phone and fax numbers. 3. The header identifies what type the report is, such as Infile, Full Report or Decision reports. 4. Prepared

TABLE OF CONTENTS. CHAPTER 1: Credit Report.. Page 1. CHAPTER 2: Credit Score...Page 3. CHAPTER 3: Credit Reporting Agencies.

TABLE OF CONTENTS CHAPTER 1: Credit Report.. Page 1 CHAPTER 2: Credit Score.....Page 3 CHAPTER 3: Credit Reporting Agencies.Page 6 CHAPTER 4: How to get a FREE Credit Report Page 8 CHAPTER 5: The 4 th

TABLE OF CONTENTS CHAPTER 1: Credit Report.. Page 1 CHAPTER 2: Credit Score.....Page 3 CHAPTER 3: Credit Reporting Agencies.Page 6 CHAPTER 4: How to get a FREE Credit Report Page 8 CHAPTER 5: The 4 th

CREDIT REPORTS WHAT EVERY CONSUMER SHOULD KNOW ABOUT MORTGAGE EQUITY P A R T N E R S

F WHAT EVERY CONSUMER SHOULD KNOW ABOUT CREDIT REPORTS MORTGAGE EQUITY P A R T N E R S Your Leaders in Lending B The information contained herein is for informational purposes only. The algorithymes and

F WHAT EVERY CONSUMER SHOULD KNOW ABOUT CREDIT REPORTS MORTGAGE EQUITY P A R T N E R S Your Leaders in Lending B The information contained herein is for informational purposes only. The algorithymes and

Credit Reports & Credit Scores

Credit Reports & Credit Scores Reviewing: Information that is and isn t in your credit report. What information determines your credit score. Tips to improve your credit score. What s In Your Credit Report

Credit Reports & Credit Scores Reviewing: Information that is and isn t in your credit report. What information determines your credit score. Tips to improve your credit score. What s In Your Credit Report

Mastering The Small- Business Market:

Commercial Information Solutions Mastering The Small- Business Market: A Guide To Understanding 4 Critical Credit Risk Trends The Great Recession may be over, but U.S. businesses still face an uncertain

Commercial Information Solutions Mastering The Small- Business Market: A Guide To Understanding 4 Critical Credit Risk Trends The Great Recession may be over, but U.S. businesses still face an uncertain

TransUnion Enhanced Credit Report User Guide UNITED STATES

TransUnion Enhanced Credit Report User Guide UNITED STATES Introduction to the Credit Report User Guide Thousands of companies around the world depend on TransUnion Credit Reports for the consumer insight

TransUnion Enhanced Credit Report User Guide UNITED STATES Introduction to the Credit Report User Guide Thousands of companies around the world depend on TransUnion Credit Reports for the consumer insight

Credit Scores. www.howtogainwealth.com. Copyright 2009 How to Gain Wealth. All rights reserved.

Credit Scores Why is my Credit Score important? Lenders, such as banks and credit card companies, use credit scores to evaluate the potential risk posed by lending money to consumers and to mitigate losses

Credit Scores Why is my Credit Score important? Lenders, such as banks and credit card companies, use credit scores to evaluate the potential risk posed by lending money to consumers and to mitigate losses

SCORES OVERVIEW. TransUnion Scores

S OVERVIEW Scores 1 Table of Contents CreditVision Scores CreditVision Account Management Score.... 2 CreditVision Auto Score....3 CreditVision Bankruptcy Score....3 CreditVision HELOC Score....4 CreditVision

S OVERVIEW Scores 1 Table of Contents CreditVision Scores CreditVision Account Management Score.... 2 CreditVision Auto Score....3 CreditVision Bankruptcy Score....3 CreditVision HELOC Score....4 CreditVision

How to Read an Equifax Credit Report

How to Read an Equifax Credit Report June 2014 CONFIDENTIAL & PROPRIETARY The recipient of this material (hereinafter "the Material") acknowledges that it contains confidential and proprietary data the

How to Read an Equifax Credit Report June 2014 CONFIDENTIAL & PROPRIETARY The recipient of this material (hereinafter "the Material") acknowledges that it contains confidential and proprietary data the

TransUnion Enhanced Credit Report User Guide UNITED STATES

TransUnion Enhanced Credit Report User Guide UNITED STATES Introduction to the Enhanced Credit Report User Guide Thousands of companies around the world depend on TransUnion Credit Reports for the consumer

TransUnion Enhanced Credit Report User Guide UNITED STATES Introduction to the Enhanced Credit Report User Guide Thousands of companies around the world depend on TransUnion Credit Reports for the consumer

USER GUIDE. TransUnion Credit Report User Guide

USER GUIDE TransUnion Credit Report User Guide Table of Contents Introduction to the Credit Report User Guide....3 Sample credit report (print image format)...4 Credit report codes...5 Credit report fields....6

USER GUIDE TransUnion Credit Report User Guide Table of Contents Introduction to the Credit Report User Guide....3 Sample credit report (print image format)...4 Credit report codes...5 Credit report fields....6

UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor

By Bill Taylor") UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor Most studies about consumer debt have only focused on credit cards and mortgages. However, personal debt also may include medical expenses, school

UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor Most studies about consumer debt have only focused on credit cards and mortgages. However, personal debt also may include medical expenses, school

PA HealthCare Credit Union. The Credit Clinic. The PA HealthCare Credit Union contributes to the financial success of our members.

PA HealthCare Credit Union The Credit Clinic The PA HealthCare Credit Union contributes to the financial success of our members. 1 Copyright 2006 Agenda Welcome & Introduction Overview Product Rate Credit

PA HealthCare Credit Union The Credit Clinic The PA HealthCare Credit Union contributes to the financial success of our members. 1 Copyright 2006 Agenda Welcome & Introduction Overview Product Rate Credit

Familiarize yourself with laws that authorize and regulate vehicle dealership financing and leasing.

W ith prices averaging more than $28,000 for a new vehicle and $15,000 for a used vehicle, most consumers need financing or leasing to acquire a vehicle. In some cases, buyers use direct lending: they

W ith prices averaging more than $28,000 for a new vehicle and $15,000 for a used vehicle, most consumers need financing or leasing to acquire a vehicle. In some cases, buyers use direct lending: they

100 Percent Financed. Getting Started in Applying for Business Credit with a Personal Guarantee. By Juan Pablo

100 Percent Financed Getting Started in Applying for Business Credit with a Personal Guarantee By Juan Pablo Juan Pablo The 100% Financed ebook 2 100 Percent Financed Disclaimer @2014 Grey Rose Consulting,

100 Percent Financed Getting Started in Applying for Business Credit with a Personal Guarantee By Juan Pablo Juan Pablo The 100% Financed ebook 2 100 Percent Financed Disclaimer @2014 Grey Rose Consulting,

Understanding, managing, and rebuilding your credit

Understanding, managing, and rebuilding your credit Objective Bank of America is committed to providing information that will help you understand the effect credit can have on lending, and what you can

Understanding, managing, and rebuilding your credit Objective Bank of America is committed to providing information that will help you understand the effect credit can have on lending, and what you can

Accounts Total Number Balance Available

Equifax Credit Report for Kimberly Guzman As of: 03/20/2008 Available until: 04/20/2008 Confirmation #: 123456789 Section Title Section Description 1. Credit Summary Summary of account activity 2. Account

Equifax Credit Report for Kimberly Guzman As of: 03/20/2008 Available until: 04/20/2008 Confirmation #: 123456789 Section Title Section Description 1. Credit Summary Summary of account activity 2. Account

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Through financial knowledge and expertise, we provide high-quality products and services that enable people to enjoy a better

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Through financial knowledge and expertise, we provide high-quality products and services that enable people to enjoy a better

Understanding your Credit Score

Understanding your Credit Score Understanding Your Credit Score Fair, Isaac and Co. is the San Rafael, California Company founded in 1956 by Bill Fair and Earl Isaac. They pioneered the field of credit

Understanding your Credit Score Understanding Your Credit Score Fair, Isaac and Co. is the San Rafael, California Company founded in 1956 by Bill Fair and Earl Isaac. They pioneered the field of credit

Understanding Credit. Megan Stearns, Credit Counselor

Understanding Credit Megan Stearns, Credit Counselor Obtaining your free credit report will lower your credit score. Closing old accounts can help your credit score. Paying off the balances on your credit

Understanding Credit Megan Stearns, Credit Counselor Obtaining your free credit report will lower your credit score. Closing old accounts can help your credit score. Paying off the balances on your credit

Utilizing Credit Scoring to Predict Patient Outcomes. An Equifax Predictive Sciences Research Paper September 2005

Utilizing Credit Scoring to Predict Patient Outcomes An Equifax Predictive Sciences Research Paper September 2005 Introduction Improving Your Revenue Cycle Performance Through Financial Management Solutions

Utilizing Credit Scoring to Predict Patient Outcomes An Equifax Predictive Sciences Research Paper September 2005 Introduction Improving Your Revenue Cycle Performance Through Financial Management Solutions

Financial payment profile Fair Isaac Corporation (FICO) 300 to 850 the higher, the better

300 to 850 the higher, the better") What is a credit score? Financial payment profile Fair Isaac Corporation (FICO) 300 to 850 the higher, the better National distribution of FICO scores What a low score could cost you? Tens of thousands

What is a credit score? Financial payment profile Fair Isaac Corporation (FICO) 300 to 850 the higher, the better National distribution of FICO scores What a low score could cost you? Tens of thousands

Oracle FLEXCUBE Direct Banking Release 12.0.0 Corporate E-Factoring User Manual. Part No. E52305-01

Oracle FLEXCUBE Direct Banking Release 12.0.0 Corporate E-Factoring User Manual Part No. E52305-01 Corporate E-Factoring User Manual Table of Contents 1. Transaction Host Integration Matrix... 4 2. Assignment

Oracle FLEXCUBE Direct Banking Release 12.0.0 Corporate E-Factoring User Manual Part No. E52305-01 Corporate E-Factoring User Manual Table of Contents 1. Transaction Host Integration Matrix... 4 2. Assignment

Enhanced Commercial Credit Report

Sample Enhanced Commercial Credit Report REPORT SUMMARY Enhanced Commercial Credit Report BUSINESS IDENTIFICATION INFORMATION Business ABC COMPANY Inquiry on Apr 08, 2003 File Number 000254893 Address

Sample Enhanced Commercial Credit Report REPORT SUMMARY Enhanced Commercial Credit Report BUSINESS IDENTIFICATION INFORMATION Business ABC COMPANY Inquiry on Apr 08, 2003 File Number 000254893 Address

Business Information Services. Product overview

Business Information Services Product overview Capabilities Quality data with an approach you can count on every step of the way Gain the distinctive edge you need to make better decisions throughout the

Business Information Services Product overview Capabilities Quality data with an approach you can count on every step of the way Gain the distinctive edge you need to make better decisions throughout the

569 601 +32 ACCOUNT SUMMARY

11132 Winners Circle Ste 207 Los Alamitos, CA 90720 www.asuitesolution.com Tel: (877) 311-1234 Fax: (877) 388-1234 Email: [email protected] ONLINE CREDIT REPORTING CORPORATION DEBTOR INFORMATION Debtor:

11132 Winners Circle Ste 207 Los Alamitos, CA 90720 www.asuitesolution.com Tel: (877) 311-1234 Fax: (877) 388-1234 Email: [email protected] ONLINE CREDIT REPORTING CORPORATION DEBTOR INFORMATION Debtor:

How to Build Credit for Your EIN That is Not Linked to Your SSN

How to Build Credit for Your EIN That is Not Linked to Your SSN How To Build Credit For Tour EIN That is Not Linked to Your SSN Business Credit is credit that is obtained in a Business Name. With business

How to Build Credit for Your EIN That is Not Linked to Your SSN How To Build Credit For Tour EIN That is Not Linked to Your SSN Business Credit is credit that is obtained in a Business Name. With business

TransUnion Credit Report Training Guide

TransUnion Credit Report Training Guide Sample TransUnion Credit Report 1 1A GOi duncan,elizabeth*2 9932,woodbine,chicago,il,60068*3 555,e,jackson,st,cleveland,oh,44123*5 002-02-2222** TRANSUNION CREDIT

TransUnion Credit Report Training Guide Sample TransUnion Credit Report 1 1A GOi duncan,elizabeth*2 9932,woodbine,chicago,il,60068*3 555,e,jackson,st,cleveland,oh,44123*5 002-02-2222** TRANSUNION CREDIT

The Truth About Credit Repair

The Truth About Credit Repair Discover The Insider Secrets Of How The Credit System Really Works and How To Beat The Credit Bureaus At Their Own Game. David Shapiro Esq. Applied Credit Repair Solutions

The Truth About Credit Repair Discover The Insider Secrets Of How The Credit System Really Works and How To Beat The Credit Bureaus At Their Own Game. David Shapiro Esq. Applied Credit Repair Solutions

Credit Repair For Court Reporters. When Bad Dings Happen To Good People. By Julie Samford Realtime Ready. Julie Samford julie@realtimeready.

Credit Repair For Court Reporters When Bad Dings Happen To Good People By Realtime Ready 1 $96,634.00 difference! That s $5,496.00 straight out of your pocket when you could have had 0% interest! (Info

Credit Repair For Court Reporters When Bad Dings Happen To Good People By Realtime Ready 1 $96,634.00 difference! That s $5,496.00 straight out of your pocket when you could have had 0% interest! (Info

Improving a Credit Profile

Improving a Credit Profile Steps to improving a credit profile STEP 1. Order your credit Report STEP 2. Evaluate & develop a plan STEP 3. Is the personal information accurate? STEP 4. Are the tradelines

Improving a Credit Profile Steps to improving a credit profile STEP 1. Order your credit Report STEP 2. Evaluate & develop a plan STEP 3. Is the personal information accurate? STEP 4. Are the tradelines

Understanding Credit & Credit Risk Scores. Plus, Helping Consumers Get The Most From Their Credit Rating

Understanding Credit & Credit Risk Scores Plus, Helping Consumers Get The Most From Their Credit Rating This document contains actual excerpts from Fair Isaac, TransUnion, Equifax and Experian. CoreLogic

Understanding Credit & Credit Risk Scores Plus, Helping Consumers Get The Most From Their Credit Rating This document contains actual excerpts from Fair Isaac, TransUnion, Equifax and Experian. CoreLogic

New Direction. Within Your Reach! A Financial Literacy Training Presentation for our Members by:

New Direction Within Your Reach! A Financial Literacy Training Presentation for our Members by: Maintaining a Checking Account Keeping track of Deposits and Withdrawals Why Should I Keep a Check Register?

New Direction Within Your Reach! A Financial Literacy Training Presentation for our Members by: Maintaining a Checking Account Keeping track of Deposits and Withdrawals Why Should I Keep a Check Register?

How to Improve and Maintain your Credit Score

How to Improve and Maintain your Credit Score Special points of interest: Factors that influence your credit score How your credit score is calculated Improving your credit score How to fix flawed credit

How to Improve and Maintain your Credit Score Special points of interest: Factors that influence your credit score How your credit score is calculated Improving your credit score How to fix flawed credit