THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

|

|

|

- Dorthy Blake

- 8 years ago

- Views:

Transcription

1 THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination CORPORATE FINANCIAL MANAGEMENT DECEMBER 2013 Time allowed 3 hours Section A Compulsory case study Section B 5 long questions (attempt any 3) DO NOT OPEN THIS PAPER UNTIL INSTRUCTED TO DO SO BY THE INVIGILATOR Important Note: Candidates are allowed 15 minutes reading time to read through the question paper before the commencement of the examination between 9:15a.m.- 9:30a.m. During the reading time, all candidates must be silent and must not write or mark anything on their question papers or answer books. Candidates must close all their reference books, notes or other unauthorised materials and put these under their chairs. If any candidates write or make any marks during the reading time, or if they speak or in any other way communicate with anyone either in or outside the examination hall during this period or read any unauthorised materials, they will be disqualified from continuing this examination paper. Once candidates have opened the question paper, they are not allowed to leave the examination hall until 10:00a.m. Page 1 of 16

2 THIS IS A BLANK PAGE Page 2 of 16

3 SUBJECT NO. 16J CORPORATE FINANCIAL MANAGEMENT DECEMBER 2013 The examination paper is divided into TWO sections. Section A is a case study with compulsory questions and carries 40 marks. Candidates should attempt THREE questions from Section B, all of which carry 20 marks each. You should allow yourself approximately 70 minutes in total to answer the question in Section A, and 35 minutes for each of the questions attempted in Section B. Unless otherwise stated, $ denotes Hong Kong dollars. All interest rates are annual rates. Round your numerical answers to two decimal places. Friday morning, 6 December 2013 Time allowed: 3 hours SECTION A (Compulsory answer ALL questions in this section) 1. RetailMart Limited (RL) is a public limited company with a financial year end of 31 March. The company runs a number of chain stores selling various popular household items in Hong Kong and China. In recent years, the company has experienced negative business growth due to the economic recession. To boost its turnover, the company has made several plans. At the October 2013 board meeting, RL management identified a merger target in Malaysia. After the board meeting, all directors agreed to acquire Abnormal Trading Limited (ATL) to increase RL s shareholder wealth. Due diligence was performed. An independent financial consultant estimated that the amount needed for the merger would be around $380 million. Since the management plans to execute the merger in December 2013, RL was going to issue shares to raise sufficient funds to complete the potential merger. The announcement of the proposed merger and share issue would be made public at the same time. Some directors raised concerns about the timing of the announcement as they believed that the timing would have a big impact on RL s share price. At the time, the share price was $2.00 per share. Page 3 of 16

4 The outlook of external business environment was bleak. At the November 2013 board meeting, the directors agreed to borrow $80 million at a fixed rate of interest to secure sufficient resources to cope with the expansion. Since the company s long-term debt is rated BBB Grade by the credit rating agencies, RL s bankers have agreed to grant a loan at a fixed interest rate of 9.25% per annum. Alternatively, the company could borrow floating rate funding at prime minus 2.25% per annum. The company is aware, however, that Good Supplies Limited (GSL), one of its long-term business partners, is also looking to borrow $80 million at a floating rate; and its AAA rating will enable it to borrow funds at a fixed rate of 7.50% per annum and at a floating rate of prime minus 1.5% per annum. At the time, the prime rate is 5.5% per annum. At its most recent meeting in December 2013, the board discussed not only concerns about the sufficiency of its cash flow to meet its daily operational expenses but also whether there would be enough cash available for future investment opportunities. To reserve its cash flows for potential capital expenditure in the near future, the management decided to reduce the dividend payment for the year ended 31 March Upon the release of the decision in reduction of dividend payment, the high share trading volume signified that the market is sensitive to the announcement. Ten years ago, RL opened chain stores in Mainland China. This strategy had proved to be less successful than expected and so in December 2013 RL s directors decided to withdraw from the China market and to concentrate on the local Hong Kong market. To raise the finance needed to close the China stores, RL s directors also decided to make a one-for-five rights issue at a discount of 30% on the market value at that time. The most recent income statement of RL is as follows: Income statement for the year ended 31 March 2013 $ m Sales 14,000 Profit before interest and tax 520 Finance costs 240 Profit before tax 280 Profits tax 70 Profit after tax 210 Dividends paid for the year ended 31 March 2013 $140 The outstanding shares and reserves of RL as at 31 March 2013 are as follows: $ m Ordinary share capital, $0.25 each 600 Revaluation reserve 1,400 Retained earnings 3,200 5,200 Page 4 of 16

5 RL s shares currently trade on the stock exchange at a price-earnings ratio of 16 times. An investor owning 100,000 ordinary shares in RL has received information about the forthcoming rights issue but cannot decide whether to take up the rights issue, sell the rights or allow the rights offer to lapse. REQUIRED: (a) Discuss the market reaction on the announcement date of the proposed merger/share issue if the pending merger announcement has NOT been leaked. (Assume that the market is semi-strong form efficient.) (5 marks) (b) RL is considering whether it would be worth entering into an interest rate swap with GSL. Illustrate how an interest rate swap could be used so that both companies derive equal benefit. (Assume that RL s swap payment to GSL is 7.50% fixed per annum under the swap agreement.) (11 marks) (c) Explain, with reasons, why some investors react positively but others negatively when RL s decision to reduce the dividend payment is released to the market. (9 marks) (d) Evaluate the theoretical ex-rights price of an ordinary share in RL, and the price at which the rights in RL are likely to be traded. (6 marks) (e) Evaluate each of the options regarding the rights issue available to the investor with 100,000 ordinary shares. (9 marks) (Total: 40 marks) Page 5 of 16

(5 marks) (b) RL is considering whether it would be worth entering into an interest rate swap with GSL.")

6 SECTION B (Answer THREE questions from this section) 2. Fashion Design Holding Limited (FDHL) is a listed company with a principal business activity of manufacturing women s clothes. The management is looking to expand its business into women s fashion retail. The company has grown rapidly in recent years with consistent annual dividend growth; it expects that dividends will continue to grow in line with the trend in recent dividend payments. The seven-year dividend history, extract from statements of financial position and some related current market information are below: Seven-year dividend history Year Dividends per share 2006 $ $ $ $ $ $ $33.50 Extracts from statement of financial position at 31 August 2013 $m Equity Ordinary $100 shares 280 6% $1 irredeemable preference shares 200 Retained earnings 388 Total equity 868 Non-current liabilities 8% irredeemable debentures (at nominal value) 1,000 7% unsecured loan (at nominal value) 720 Total non-current liabilities 1,720 Current market information Ex-dividend ordinary share price $ Ex-dividend preference share price $ 0.92 Irredeemable debentures (Ex-interest) $ per $100 debenture Redeemable unsecured loan (Ex-interest) $ per $100 loan FDHL s current liabilities do not include any bank overdrafts. The profits tax rate is 16.5% and any interest paid in relation to debt financing generates tax savings. The unsecured loan will be redeemable at par in ten years time. Page 6 of 16

7 REQUIRED: (a) The board has decided that any financing arrangements should come from increasing debt rather than increasing equity. According to the above information, based on market value, evaluate the company s weighted average cost of capital. (Candidates may consider using the interpolation approach in calculating the cost of unsecured loan with discount factors 7% and 10% respectively.) (15 marks) (b) The company has taken out an overdraft, which is considered to be a permanent source of finance and which is included in FDHL s current liabilities. Discuss the implications of the overdraft on the calculation of FDHL s weighted average cost of capital. (5 marks) (Total: 20 marks) Page 7 of 16

(15 marks) (b) The company has taken out an overdraft, which is considered to be a permanent source of finance and which is included in FDHL s current liabilities.")

8 3. Great Precision Technology Limited (GPTL) is a gears manufacturer. It has entered into a contract to produce high-precision gears. To do this, the company has to employ a geargrinding machine at the final manufacturing stage to remove the remaining few thousandths of an inch of material left by other manufacturing methods. Since the gear-grinding machine is vital to the company s high-precision manufacturing requirements, GPTL plans to purchase a new machine. Details of two machines under consideration offered by different machine suppliers are: Machine Super Machine Quick Initial cost $1,000,000 $1,800,000 Economic life (years) 5 8 Residual value $100,000 $140,000 Running costs per annum $150,000 $145,000 The discount rate is assumed to be 12% and taxation can be ignored. REQUIRED: (a) Replacement chain approach and equivalent annual cost approach are two methods used for comparing projects with unequal lives. Evaluate each approach and discuss why the equivalent annual cost approach is the better approach in comparing Machine Super and Machine Quick. (5 marks) (b) Adopting the equivalent annual cost approach, advise the company which geargrinding machine should be purchased. Specify any assumptions if needed. (15 marks) (Total: 20 marks) Page 8 of 16

5 8 Residual value")

9 4. Forever Limited (FL) is a private limited company. The company uses a factoring service to enhance its cash flow to meet its operational needs. The terms of the factoring service agreement are as follows: Service term: Annual turnover: Sales nature: Basic factoring charge: Annual saving of office or other expenses: (savings from basic factoring service) Fund advancement service (optional): Factoring commission on funds advancement: Factoring interest on fund advancement: Existing average collection period: 2 years minimum (3 months cancellable notice) $120 million evenly distributed in the year Credit only 2% of annual turnover (paid in arrears) $1.2 million at year end 90% of invoice value of factored debts 3.0% deducted from the gross amount of the funds advanced Commission will be deducted from the funds advanced directly 10% per annum on monthly basis on gross funds (before deduction of the 3.0% commission) Interest will be deducted from the funds advanced directly 75 days REQUIRED (a) Evaluate the effective annual factoring cost as a percentage of the improvement in funds (i.e. ratio of total cost of factoring and fund advancement service to the improvement in funds from the factoring and fund advancement) under the following options, and advise which option should be chosen: i. Option A: FL adopts the basic factoring service but does not use the fund advancement service. As a result, the average collection period is reduced to 60 days. ii. Option B: FL ues both the basic factoring service and the fund advancement service. The average collection period is reduced to 50 days. (Assume a 360 day year split into 12 equal months. Taxation may be ignored.) (b) Some directors consider that it is not worth using factoring services. (15 marks) Advise, with justification, whether or not FL should keep using factoring services. (5 marks) (Total: 20 marks) Page 9 of 16

$120 million evenly distributed in the year Credit only 2% of annual turnover (paid in arrears) $1.2 million at year end 90% of invoice value of factored debts 3.")

10 5. The management team of Columbia International Trading Limited (CITL) has decided to take the company private through a leveraged buyout (LBO). The following information is extracted from CITL s books: Current assets Long-term debts Liabilities other than debts Equity $200 million $200 million $300 million $700 million It is assumed that all other assets are non-current assets and suitable as collateral to secure a loan; and they are saleable at their book values. Currently, the company has 100 million outstanding shares with a market value of $10 per share. The management team decides to make use of $500 million cash in hand as the management's equity investment for the LBO and estimates that the shares in the hands of the public can be purchased if a 10% premium over the market price is offered. The company pays interest at 12% per annum on its existing debt. However, the company is required to pay interest at 15% per annum on any new debt offered by the bank. REQUIRED: (a) Evaluate the amount that CITL has to borrow. What percentage of the book value of non-current assets must a bank be willing to advance to make the deal possible? (7 marks) (b) Compare the following: i. CITL s capital structures and debt to equity ratio before and after the leveraged buyout if any debt for the LBO will be financed from debt secured by the target company s assets. Assume that the debt to equity ratio of the trading business sector is 0.5. Discuss how investors will react to new bond issue if CITL plans to issue the bonds at the same interest rate as that of the industry bond market index after the LBO. ii. The annual interest to be paid by CITL before and after the leveraged buyout. Comment on the feasibility of the LBO. (13 marks) (Total: 20 marks) Page 10 of 16

11 6. Wing Trading Limited (WTL) is an importer and exporter of textile machinery and textile goods. Its headquarters are in the UK but it trades extensively with Asian countries. The company has a subsidiary in Hong Kong. It is about to invoice a customer in Hong Kong in Hong Kong dollars, HK$750,000 payable in three months time. WTL is considering two methods of hedging the foreign exchange risk. Method A Borrow Hong Kong dollars now, converting the loan into sterling and repaying the Hong Kong dollar loan from the expected receipt in three months time. Method B Enter into a three-month forward exchange contract with the company s banker to sell HK$750,000. The spot rate and the three-month forward rate are HK$ = 1 and HK$ = 1 respectively. Annual interest rates for three months borrowing/deposits of Hong Kong dollars and sterling are 3% and 5% respectively. REQUIRED (a) Evaluate which of the two methods is the most advantageous financially for the company. (10 marks) (b) Before deciding the hedging approach, WTL should arrange the hedging plan based on its risk strategy: risk-averse strategy, predictive strategy or best strategy. Discuss this statement and advise WTL s management of other ways to reduce foreign exchange rate risk. (10 marks) (Total: 20 marks) End of Examination Paper Page 11 of 16

12 Page 12 of 16

13 Page 13 of 16

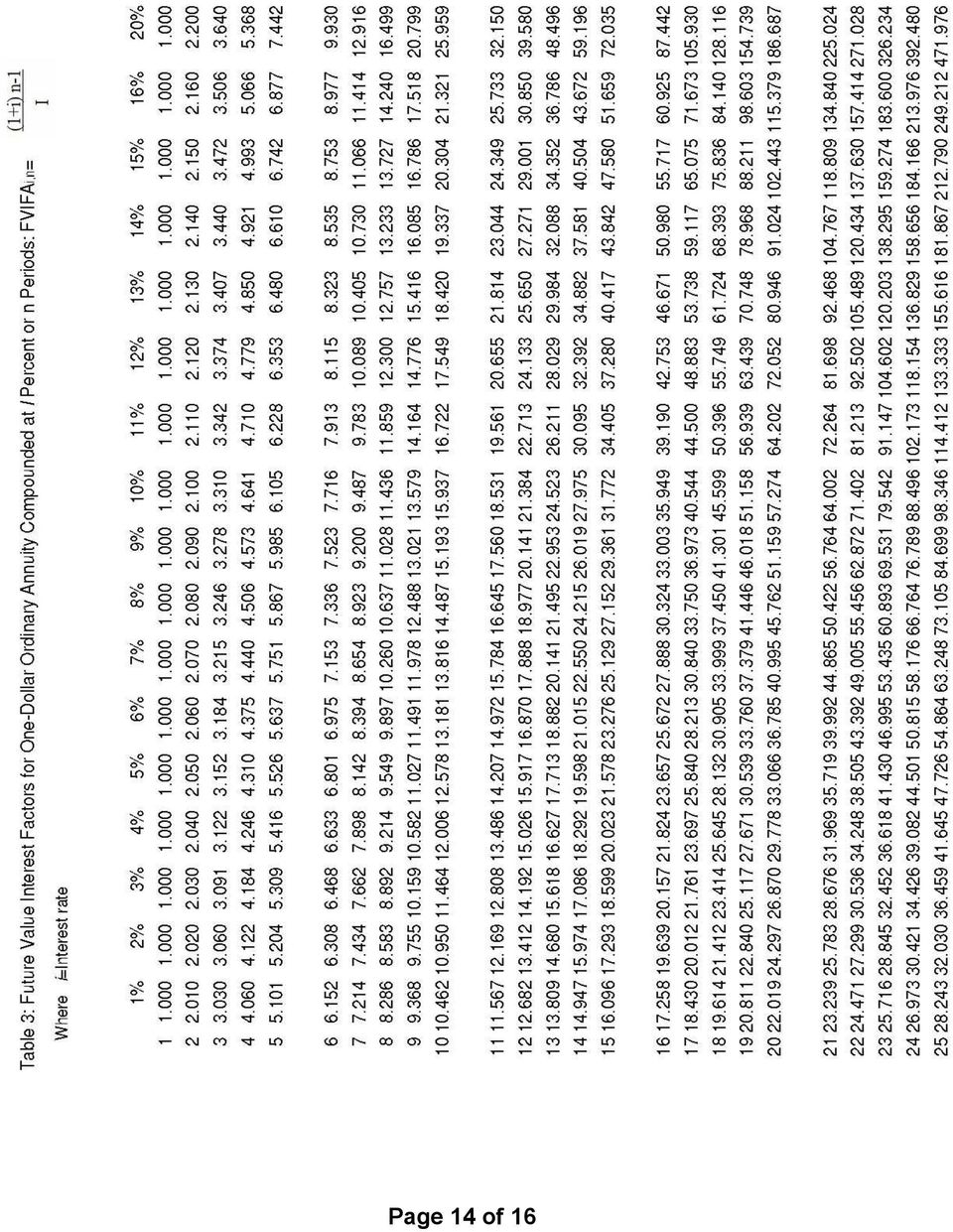

14 Page 14 of 16

15 Page 15 of 16

16 THIS IS A BLANK PAGE Page 16 of 16

Time allowed Formulae Sheet, Present Value and Annuity Tables are on

Fundamentals Level Skills Module Financial Management Friday 15 June 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 15 June 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Paper F9. Financial Management. Friday 5 December 2014. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Fundamentals Level Skills Module Financial Management Friday 5 ecember 2014 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections: Section A ALL 20 questions

Fundamentals Level Skills Module Financial Management Friday 5 ecember 2014 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections: Section A ALL 20 questions

Paper F9. Financial Management. Friday 7 June 2013. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants.

Fundamentals Level Skills Module Financial Management Friday 7 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 7 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Paper F9. Financial Management. Fundamentals Pilot Paper Skills module. The Association of Chartered Certified Accountants

Fundamentals Pilot Paper Skills module Financial Management Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Do NOT open this paper

Fundamentals Pilot Paper Skills module Financial Management Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Do NOT open this paper

6. Show all your workings. icpar

CERTIFIED PUBLIC ACCOUNTANT FOUNDATION LEVEL 1 EXAMINATION F1.3: FINANCIAL ACCOUNTING MONDAY: 10 JUNE 2013 INSTRUCTIONS: 1. Time Allowed: 3 hours 15 minutes (15 minutes reading and 3 hours writing). 2.

CERTIFIED PUBLIC ACCOUNTANT FOUNDATION LEVEL 1 EXAMINATION F1.3: FINANCIAL ACCOUNTING MONDAY: 10 JUNE 2013 INSTRUCTIONS: 1. Time Allowed: 3 hours 15 minutes (15 minutes reading and 3 hours writing). 2.

Paper F9. Financial Management. Specimen Exam applicable from December 2014. Fundamentals Level Skills Module

Fundamentals Level Skills Module Financial Management Specimen Exam applicable from December 2014 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections:

Fundamentals Level Skills Module Financial Management Specimen Exam applicable from December 2014 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections:

Financial Decision Making

Chartered Secretaries Qualifying Scheme Level 2 Financial Decision Making Sample paper Time allowed: 3 hours and 15 minutes (including reading time) Do not open this examination paper until the presiding

Chartered Secretaries Qualifying Scheme Level 2 Financial Decision Making Sample paper Time allowed: 3 hours and 15 minutes (including reading time) Do not open this examination paper until the presiding

Institute of Chartered Accountant Ghana (ICAG) Paper 2.4 Financial Management

Paper 2.4 Financial Management") Institute of Chartered Accountant Ghana (ICAG) Paper 2.4 Financial Management Final Mock Exam 1 Marking scheme and suggested solutions DO NOT TURN THIS PAGE UNTIL YOU HAVE COMPLETED THE MOCK EXAM ii Financial

Institute of Chartered Accountant Ghana (ICAG) Paper 2.4 Financial Management Final Mock Exam 1 Marking scheme and suggested solutions DO NOT TURN THIS PAGE UNTIL YOU HAVE COMPLETED THE MOCK EXAM ii Financial

Paper F9. Financial Management. Friday 7 December 2012. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Fundamentals Level Skills Module Financial Management Friday 7 December 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 7 December 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module, Paper F9. Section A. Monetary value of return = $3 10 x 1 197 = $3 71 Current share price = $3 71 $0 21 = $3 50

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2014 Answers Section A 1 A Monetary value of return = $3 10 x 1 197 = $3 71 Current share price = $3 71 $0 21 = $3 50 2

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2014 Answers Section A 1 A Monetary value of return = $3 10 x 1 197 = $3 71 Current share price = $3 71 $0 21 = $3 50 2

1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084 6,327 6,580 6,844

Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084 6,327 6,580 6,844") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2013 Answers 1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2013 Answers 1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084

FINANCIAL ACCOUNTING TOPIC: FINANCIAL ANALYSIS

SYLLABUS Compulsory part Basic ratio analysis 1. State the general functions of accounting ratios. 2. Calculate and interpret the following ratios: a. working capital/current ratio, quick/liquid/acid test

SYLLABUS Compulsory part Basic ratio analysis 1. State the general functions of accounting ratios. 2. Calculate and interpret the following ratios: a. working capital/current ratio, quick/liquid/acid test

Management Accounting Financial Strategy

PAPER P9 Management Accounting Financial Strategy The Examiner provides a short study guide, for all candidates revising for this paper, to some first principles of finance and financial management Based

PAPER P9 Management Accounting Financial Strategy The Examiner provides a short study guide, for all candidates revising for this paper, to some first principles of finance and financial management Based

Cash flow before tax 1,587 1,915 1,442 2,027 Tax at 28% (444) (536) (404) (568)

(536) (404) (568)") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2014 Answers 1 (a) Calculation of NPV Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 5,670 6,808 5,788 6,928 Variable

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2014 Answers 1 (a) Calculation of NPV Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 5,670 6,808 5,788 6,928 Variable

LAFE CORPORATION LIMITED Un-audited Q1 2014 Financial Statement and Dividend Announcement (All in US Dollars)

") LAFE CORPORATION LIMITED Un-audited Q1 2014 Financial Statement and Dividend Announcement (All in US Dollars) PART I INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2 & Q3), HALF-YEAR AND FULL

LAFE CORPORATION LIMITED Un-audited Q1 2014 Financial Statement and Dividend Announcement (All in US Dollars) PART I INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2 & Q3), HALF-YEAR AND FULL

Paper F7. Financial Reporting. Wednesday 3 June 2015. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Fundamentals Level Skills Module Financial Reporting Wednesday 3 June 2015 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections: Section A ALL 20 questions

Fundamentals Level Skills Module Financial Reporting Wednesday 3 June 2015 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections: Section A ALL 20 questions

STATUTORY BOARD SB-FRS 32 FINANCIAL REPORTING STANDARD. Financial Instruments: Presentation Illustrative Examples

STATUTORY BOARD SB-FRS 32 FINANCIAL REPORTING STANDARD Financial Instruments: Presentation Illustrative Examples CONTENTS Paragraphs ACCOUNTING FOR CONTRACTS ON EQUITY INSTRUMENTS OF AN ENTITY Example

STATUTORY BOARD SB-FRS 32 FINANCIAL REPORTING STANDARD Financial Instruments: Presentation Illustrative Examples CONTENTS Paragraphs ACCOUNTING FOR CONTRACTS ON EQUITY INSTRUMENTS OF AN ENTITY Example

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 32. Financial Instruments: Presentation Illustrative Examples

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 32 Financial Instruments: Presentation Illustrative Examples CONTENTS Paragraphs ACCOUNTING FOR CONTRACTS ON EQUITY INSTRUMENTS OF AN ENTITY Example

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 32 Financial Instruments: Presentation Illustrative Examples CONTENTS Paragraphs ACCOUNTING FOR CONTRACTS ON EQUITY INSTRUMENTS OF AN ENTITY Example

Financial Pillar. F2 Financial Management. 20 November 2014 Thursday Afternoon Session

DO NOT OPEN THIS QUESTION PAPER UNTIL YOU ARE TOLD TO DO SO. Financial Pillar F2 Financial Management 20 November 2014 Thursday Afternoon Session Instructions to candidates You are allowed three hours

DO NOT OPEN THIS QUESTION PAPER UNTIL YOU ARE TOLD TO DO SO. Financial Pillar F2 Financial Management 20 November 2014 Thursday Afternoon Session Instructions to candidates You are allowed three hours

Fundamentals Level Skills Module, Paper F9. Section B

Answers Fundamentals Level Skills Module, Paper F9 Financial Management September/December 2015 Answers Section B 1 (a) Market value of equity = 15,000,000 x 3 75 = $56,250,000 Market value of each irredeemable

Answers Fundamentals Level Skills Module, Paper F9 Financial Management September/December 2015 Answers Section B 1 (a) Market value of equity = 15,000,000 x 3 75 = $56,250,000 Market value of each irredeemable

Financial Pillar. F2 Financial Management. 24 November 2011 Thursday Afternoon Session

Financial Pillar F2 Financial Management 24 November 2011 Thursday Afternoon Session Instructions to candidates You are allowed three hours to answer this question paper. You are allowed 20 minutes reading

Financial Pillar F2 Financial Management 24 November 2011 Thursday Afternoon Session Instructions to candidates You are allowed three hours to answer this question paper. You are allowed 20 minutes reading

Question 1. Marking scheme. F9 ACCA June 2013 Exam: BPP Answers

Question 1 Text references. NPV is covered in Chapter 8 and real or nominal terms in Chapter 9. Financial objectives are covered in Chapter 1. Top tips. Part (b) requires you to explain the different approaches.

Question 1 Text references. NPV is covered in Chapter 8 and real or nominal terms in Chapter 9. Financial objectives are covered in Chapter 1. Top tips. Part (b) requires you to explain the different approaches.

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2008 Answers 1 (a) Rights issue price = 2 5 x 0 8 = $2 00 per share Theoretical ex rights price = ((2 50 x 4) + (1 x 2 00)/5=$2

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2008 Answers 1 (a) Rights issue price = 2 5 x 0 8 = $2 00 per share Theoretical ex rights price = ((2 50 x 4) + (1 x 2 00)/5=$2

Examiner s report F9 Financial Management December 2014

Examiner s report F9 Financial Management December 2014 General Comments The F9 examination paper consisted of two sections. Section A contained 20 multiple-choice questions worth two marks each. Section

Examiner s report F9 Financial Management December 2014 General Comments The F9 examination paper consisted of two sections. Section A contained 20 multiple-choice questions worth two marks each. Section

CHAPTER 20 LONG TERM FINANCE: SHARES, DEBENTURES AND TERM LOANS

CHAPTER 20 LONG TERM FINANCE: SHARES, DEBENTURES AND TERM LOANS Q.1 What is an ordinary share? How does it differ from a preference share and debenture? Explain its most important features. A.1 Ordinary

CHAPTER 20 LONG TERM FINANCE: SHARES, DEBENTURES AND TERM LOANS Q.1 What is an ordinary share? How does it differ from a preference share and debenture? Explain its most important features. A.1 Ordinary

Contribution 787 1,368 1,813 983. Taxable cash flow 682 1,253 1,688 858 Tax liabilities (205) (376) (506) (257)

(376) (506) (257)") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2012 Answers 1 (a) Calculation of net present value (NPV) As nominal after-tax cash flows are to be discounted, the nominal

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2012 Answers 1 (a) Calculation of net present value (NPV) As nominal after-tax cash flows are to be discounted, the nominal

1 (a) Calculation of net present value (NPV) Year 1 2 3 4 5 6 $000 $000 $000 $000 $000 $000 Sales revenue 1,600 1,600 1,600 1,600 1,600

Calculation of net present value (NPV) Year 1 2 3 4 5 6 $000 $000 $000 $000 $000 $000 Sales revenue 1,600 1,600 1,600 1,600 1,600") Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2011 Answers 1 (a) Calculation of net present value (NPV) Year 1 2 3 4 5 6 $000 $000 $000 $000 $000 $000 Sales revenue 1,600

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2011 Answers 1 (a) Calculation of net present value (NPV) Year 1 2 3 4 5 6 $000 $000 $000 $000 $000 $000 Sales revenue 1,600

Financial Decision Making Sample paper

Financial Decision Making Sample paper s Important notice When reading these answers, please note that they are not intended to be viewed as a definitive model answer, as in many instances there are several

Financial Decision Making Sample paper s Important notice When reading these answers, please note that they are not intended to be viewed as a definitive model answer, as in many instances there are several

For our curriculum in Grade 12 we are going to use ratios to analyse the information available in the Income statement and the Balance sheet.

SUBJECT: ACCOUNTING GRADE 12 CHAPTER: COMPANIES LESSON: ANALYSIS AND INTERPRETATION-RATIOS LESSON OVERVIEW (KNOWLEDGE AREAS) LESSON 1. Introduction 2. Analysing of financial statements and its purpose

SUBJECT: ACCOUNTING GRADE 12 CHAPTER: COMPANIES LESSON: ANALYSIS AND INTERPRETATION-RATIOS LESSON OVERVIEW (KNOWLEDGE AREAS) LESSON 1. Introduction 2. Analysing of financial statements and its purpose

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2008 Answers 1 (a) Calculation of weighted average cost of capital (WACC) Cost of equity Cost of equity using capital asset

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2008 Answers 1 (a) Calculation of weighted average cost of capital (WACC) Cost of equity Cost of equity using capital asset

Examiner s report F9 Financial Management June 2013

Examiner s report F9 Financial Management June 2013 General Comments The examination consisted of four compulsory questions, each worth 25 marks. Most candidates attempted all four questions and there

Examiner s report F9 Financial Management June 2013 General Comments The examination consisted of four compulsory questions, each worth 25 marks. Most candidates attempted all four questions and there

Financial Management

Mock Examination : ACCA Paper F9 Financial Management Session : June 2014 Prepared by : Mr Ian Lim Your Contact Number : I wish to have my script marked by the lecturer and collect the marked script at

Mock Examination : ACCA Paper F9 Financial Management Session : June 2014 Prepared by : Mr Ian Lim Your Contact Number : I wish to have my script marked by the lecturer and collect the marked script at

CFS. Syllabus. Certified Finance Specialist. International benchmark in Finance profession

CFS Certified Finance Specialist Syllabus International benchmark in Finance profession Certified Finance Specialist Summary: This award will provide candidates the opportunity to gain advanced level knowledge

CFS Certified Finance Specialist Syllabus International benchmark in Finance profession Certified Finance Specialist Summary: This award will provide candidates the opportunity to gain advanced level knowledge

2 FSA002 Income statement

2 FSA002 Income statement This data item provides the PRA with information on the main sources of income and expenditure for a firm. It should be completed on a cumulative basis for the firm's current

2 FSA002 Income statement This data item provides the PRA with information on the main sources of income and expenditure for a firm. It should be completed on a cumulative basis for the firm's current

Financing Your Dream: A Presentation at the Youth Business Linkage Forum (#EAWY2014) Akin Oyebode Head SME Banking, Stanbic IBTC Bank, Nigeria.

Akin Oyebode Head SME Banking, Stanbic IBTC Bank, Nigeria.") Financing Your Dream: A Presentation at the Youth Business Linkage Forum (#EAWY2014) Akin Oyebode Head SME Banking, Stanbic IBTC Bank, Nigeria. Content 1 Introduction 2 Profit and loss Account or Income

Financing Your Dream: A Presentation at the Youth Business Linkage Forum (#EAWY2014) Akin Oyebode Head SME Banking, Stanbic IBTC Bank, Nigeria. Content 1 Introduction 2 Profit and loss Account or Income

Financial Reporting and Analysis

Chartered Secretaries Qualifying Scheme Level 1 Financial Reporting and Analysis Sample paper Time allowed: 3 hours and 15 minutes (including reading time) Do not open this examination paper until the

Chartered Secretaries Qualifying Scheme Level 1 Financial Reporting and Analysis Sample paper Time allowed: 3 hours and 15 minutes (including reading time) Do not open this examination paper until the

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2009 Answers 1 (a) Weighted average cost of capital (WACC) calculation Cost of equity of KFP Co = 4 0 + (1 2 x (10 5 4 0)) =

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2009 Answers 1 (a) Weighted average cost of capital (WACC) calculation Cost of equity of KFP Co = 4 0 + (1 2 x (10 5 4 0)) =

INVESTMENT DICTIONARY

INVESTMENT DICTIONARY Annual Report An annual report is a document that offers information about the company s activities and operations and contains financial details, cash flow statement, profit and

INVESTMENT DICTIONARY Annual Report An annual report is a document that offers information about the company s activities and operations and contains financial details, cash flow statement, profit and

Paper F7 (INT) Financial Reporting (International) Tuesday 14 June 2011. Fundamentals Level Skills Module

Financial Reporting (International) Tuesday 14 June 2011. Fundamentals Level Skills Module") Fundamentals Level Skills Module Financial Reporting (International) Tuesday 14 June 2011 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted.

Fundamentals Level Skills Module Financial Reporting (International) Tuesday 14 June 2011 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted.

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION OCTOBER 2006 Table of Contents 1. INTRODUCTION... 3 2. FINANCIAL RATIOS FOR COMPANIES (INDUSTRY - COMMERCE - SERVICES) 4 2.1 Profitability Ratios...4 2.2 Viability

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION OCTOBER 2006 Table of Contents 1. INTRODUCTION... 3 2. FINANCIAL RATIOS FOR COMPANIES (INDUSTRY - COMMERCE - SERVICES) 4 2.1 Profitability Ratios...4 2.2 Viability

Cork Institute of Technology. Autumn 2006 Advanced Financial Accounting (Time: 3 Hours)

") Cork Institute of Technology Bachelor of Business in Accounting Award Bachelor of Business in Management - Award Instructions Answer FOUR questions Answer all THREE questions in Section A and ONE question

Cork Institute of Technology Bachelor of Business in Accounting Award Bachelor of Business in Management - Award Instructions Answer FOUR questions Answer all THREE questions in Section A and ONE question

Fiscal Responsibilities of a Pharmaceutical Division

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness

CONSOLIDATED PROFIT AND LOSS ACCOUNT For the six months ended June 30, 2002

CONSOLIDATED PROFIT AND LOSS ACCOUNT For the six months ended June 30, 2002 Unaudited Unaudited Note Turnover 2 5,576 5,803 Other net losses (1) (39) 5,575 5,764 Direct costs and operating expenses (1,910)

CONSOLIDATED PROFIT AND LOSS ACCOUNT For the six months ended June 30, 2002 Unaudited Unaudited Note Turnover 2 5,576 5,803 Other net losses (1) (39) 5,575 5,764 Direct costs and operating expenses (1,910)

Paper F9. Financial Management. Thursday 10 June 2010. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Fundamentals Level Skills Module Financial Management Thursday 10 June 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Thursday 10 June 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Business Valuations. Business Valuations. Shares Valuation Methods. Dividend valuation. method. P/E ratio. No growth. method.

Business Valuations 1. Objectives 1.1 Identify and discuss reasons for valuing businesses and financial assets. 1.2 Identify information requirements for the purposes of carrying out a valuation in a scenario.

Business Valuations 1. Objectives 1.1 Identify and discuss reasons for valuing businesses and financial assets. 1.2 Identify information requirements for the purposes of carrying out a valuation in a scenario.

CHAPTER 17. Financial Management

CHAPTER 17 Financial Management Chapter Summary: Key Concepts The Role of the Financial Manager Financial managers Risk-return trade-off Executives who develop and implement their firm s financial plan

CHAPTER 17 Financial Management Chapter Summary: Key Concepts The Role of the Financial Manager Financial managers Risk-return trade-off Executives who develop and implement their firm s financial plan

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

PART I - INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2 & Q3), HALF-YEAR AND FULL YEAR RESULTS

, HALF-YEAR AND FULL YEAR RESULTS") EU YAN SANG INTERNATIONAL LTD (Company Registration No. : 199302179H) Unaudited Financial Statements And Dividend Announcement PART I - INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2 & Q3),

EU YAN SANG INTERNATIONAL LTD (Company Registration No. : 199302179H) Unaudited Financial Statements And Dividend Announcement PART I - INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2 & Q3),

Paper F3. Financial Accounting. Specimen Exam applicable from June 2014. Fundamentals Level Knowledge Module

Fundamentals Level Knowledge Module Financial Accounting Specimen Exam applicable from June 2014 Time allowed: 2 hours This paper is divided into two sections: Section A ALL 35 questions are compulsory

Fundamentals Level Knowledge Module Financial Accounting Specimen Exam applicable from June 2014 Time allowed: 2 hours This paper is divided into two sections: Section A ALL 35 questions are compulsory

Paper F9. Financial Management. Friday 6 December 2013. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Fundamentals Level Skills Module Financial Management Friday 6 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 6 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Examiner s report F9 Financial Management June 2011

Examiner s report F9 Financial Management June 2011 General Comments Congratulations to candidates who passed Paper F9 in June 2011! The examination paper looked at many areas of the syllabus and a consideration

Examiner s report F9 Financial Management June 2011 General Comments Congratulations to candidates who passed Paper F9 in June 2011! The examination paper looked at many areas of the syllabus and a consideration

performance of a company?

How to deal with questions on assessing the performance of a company? (Relevant to ATE Paper 7 Advanced Accounting) Dr. M H Ho This article provides guidance for candidates in dealing with examination

How to deal with questions on assessing the performance of a company? (Relevant to ATE Paper 7 Advanced Accounting) Dr. M H Ho This article provides guidance for candidates in dealing with examination

1 (a) NPV calculation Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales revenue 5,614 7,214 9,015 7,034. Contribution 2,583 3,283 3,880 2,860

NPV calculation Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales revenue 5,614 7,214 9,015 7,034. Contribution 2,583 3,283 3,880 2,860") Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2012 Answers 1 (a) NPV calculation Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales revenue 5,614 7,214 9,015 7,034 Variable

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2012 Answers 1 (a) NPV calculation Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales revenue 5,614 7,214 9,015 7,034 Variable

Ratio Analysis CBDC, NB. Presented by ACSBE. February, 2008. Copyright 2007 ACSBE. All Rights Reserved.

Ratio Analysis CBDC, NB February, 2008 Presented by ACSBE Financial Analysis What is Financial Analysis? What Can Financial Ratios Tell? 7 Categories of Financial Ratios Significance of Using Ratios Industry

Ratio Analysis CBDC, NB February, 2008 Presented by ACSBE Financial Analysis What is Financial Analysis? What Can Financial Ratios Tell? 7 Categories of Financial Ratios Significance of Using Ratios Industry

6. Debt Valuation and the Cost of Capital

6. Debt Valuation and the Cost of Capital Introduction Firms rarely finance capital projects by equity alone. They utilise long and short term funds from a variety of sources at a variety of costs. No

6. Debt Valuation and the Cost of Capital Introduction Firms rarely finance capital projects by equity alone. They utilise long and short term funds from a variety of sources at a variety of costs. No

Long Term Business Financing Strategy For A Pakistan Business. Byco Petroleum Pakistan Limited

Long Term Business Financing Strategy For A Pakistan Business Byco Petroleum Pakistan Limited Contents Why We Need Financing Strategy 3 How Financing Strategies are driven? 4 Financing Prerequisite for

Long Term Business Financing Strategy For A Pakistan Business Byco Petroleum Pakistan Limited Contents Why We Need Financing Strategy 3 How Financing Strategies are driven? 4 Financing Prerequisite for

Financial Ratios and Quality Indicators

Financial Ratios and Quality Indicators From U.S. Small Business Administration Online Women's Business Center If you monitor the ratios on a regular basis you'll gain insight into how effectively you

Financial Ratios and Quality Indicators From U.S. Small Business Administration Online Women's Business Center If you monitor the ratios on a regular basis you'll gain insight into how effectively you

How To Understand The Financial System

E. BUSINESS FINANCE 1. Sources of, and raising short-term finance 2. Sources of, and raising long-term finance 3. Internal sources of finance and dividend policy 4. Gearing and capital structure considerations

E. BUSINESS FINANCE 1. Sources of, and raising short-term finance 2. Sources of, and raising long-term finance 3. Internal sources of finance and dividend policy 4. Gearing and capital structure considerations

Half Year Financial Statement And Announcement for the Period Ended 31/12/2010

AUSSINO GROUP LTD Company Registration No.: 199100323H Half Year Financial Statement And Announcement for the Period Ended 31/12/2010 PART I - INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2

AUSSINO GROUP LTD Company Registration No.: 199100323H Half Year Financial Statement And Announcement for the Period Ended 31/12/2010 PART I - INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Level 3 Certificate in Advanced Business Calculations

LCCI International Qualifications Level 3 Certificate in Advanced Business Calculations Syllabus Effective from 2001 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

LCCI International Qualifications Level 3 Certificate in Advanced Business Calculations Syllabus Effective from 2001 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

ACCA F9 FINANCIAL MANAGEMENT. Study System Sample Session

ACCA F9 FINANCIAL MANAGEMENT Study System Sample Session ATC INTERNATIONAL ACCA PAPER F9 FINANCIAL MANAGEMENT STUDY SYSTEM No responsibility for loss occasioned to any person acting or refraining from

ACCA F9 FINANCIAL MANAGEMENT Study System Sample Session ATC INTERNATIONAL ACCA PAPER F9 FINANCIAL MANAGEMENT STUDY SYSTEM No responsibility for loss occasioned to any person acting or refraining from

Paper F9. Financial Management. Friday 6 June 2014. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants.

Fundamentals Level Skills Module Financial Management Friday 6 June 2014 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 6 June 2014 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

ACCOUNTING FOR SHARE CAPITAL

CHAPTER 7 ACCOUNTING FOR SHARE CAPITAL (Share and Share Capital : Nature and types) A Company is an artificial person created by law, having separate entity with a perpetual succession and a common seal.

CHAPTER 7 ACCOUNTING FOR SHARE CAPITAL (Share and Share Capital : Nature and types) A Company is an artificial person created by law, having separate entity with a perpetual succession and a common seal.

ACCOUNTING STANDARDS BOARD OCTOBER 1998 FRS 14 FINANCIAL REPORTING STANDARD EARNINGS ACCOUNTING STANDARDS BOARD

ACCOUNTING STANDARDS BOARD OCTOBER 1998 FRS 14 14 EARNINGS FINANCIAL REPORTING STANDARD PER SHARE ACCOUNTING STANDARDS BOARD Financial Reporting Standard 14 Earnings per Share is issued by the Accounting

ACCOUNTING STANDARDS BOARD OCTOBER 1998 FRS 14 14 EARNINGS FINANCIAL REPORTING STANDARD PER SHARE ACCOUNTING STANDARDS BOARD Financial Reporting Standard 14 Earnings per Share is issued by the Accounting

1-3Q of FY2014 87.43 78.77 1-3Q of FY2013 74.47 51.74

January 30, 2015 Resona Holdings, Inc. Consolidated Financial Results for the Third Quarter of Fiscal Year 2014 (Nine months ended December 31, 2014/Unaudited) Code number: 8308 Stock

January 30, 2015 Resona Holdings, Inc. Consolidated Financial Results for the Third Quarter of Fiscal Year 2014 (Nine months ended December 31, 2014/Unaudited) Code number: 8308 Stock

Teacher Resource Bank

Teacher Resource Bank GCE Accounting Other Guidance: ACCN2 Update on IAS ACCN3 Updates on IAS (July 2012). The Assessment and Qualifications Alliance (AQA) is a company limited by guarantee registered

Teacher Resource Bank GCE Accounting Other Guidance: ACCN2 Update on IAS ACCN3 Updates on IAS (July 2012). The Assessment and Qualifications Alliance (AQA) is a company limited by guarantee registered

7 Management of Working Capital

7 Management of Working Capital BASIC CONCEPTS AND FORMULAE 1. Working Capital Management Working Capital Management involves managing the balance between firm s shortterm assets and its short-term liabilities.

7 Management of Working Capital BASIC CONCEPTS AND FORMULAE 1. Working Capital Management Working Capital Management involves managing the balance between firm s shortterm assets and its short-term liabilities.

Form. Account Disclosure Document for Licensed Corporation

Form (Made for the purposes of compliance with the requirements of section 156(1) of the Securities and Futures Ordinance (Cap.571) as amplified in section 3(1) of the Securities and Futures (Accounts

Form (Made for the purposes of compliance with the requirements of section 156(1) of the Securities and Futures Ordinance (Cap.571) as amplified in section 3(1) of the Securities and Futures (Accounts

Article Accounting Terminology

Article Accounting Terminology Contents Page 1. Accounting Period... 4 2. Accounts Payable (Sundry Creditors)... 4 3. Accounts Receivable (Sundry Debtors)... 4 4. Assets... 4 5. Benchmarks... 4 6. B.O.S.

Article Accounting Terminology Contents Page 1. Accounting Period... 4 2. Accounts Payable (Sundry Creditors)... 4 3. Accounts Receivable (Sundry Debtors)... 4 4. Assets... 4 5. Benchmarks... 4 6. B.O.S.

FINANCIAL ACCOUNTING

FINANCIAL ACCOUNTING FORMATION 2 EXAMINATION - AUGUST 2012 NOTES: You are required to answer Question 1. You are also required to answer any three out of Questions 2 to 5. (If you provide answers to all

FINANCIAL ACCOUNTING FORMATION 2 EXAMINATION - AUGUST 2012 NOTES: You are required to answer Question 1. You are also required to answer any three out of Questions 2 to 5. (If you provide answers to all

NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

Paper FFM. Foundations in Financial Management FOUNDATIONS IN ACCOUNTANCY. Pilot Paper. The Association of Chartered Certified Accountants

FOUNDATIONS IN ACCOUNTANCY Foundations in Financial Management Pilot Paper Time allowed: 2 hours This paper is divided into two sections: Section A ALL TEN questions are compulsory and MUST be attempted

FOUNDATIONS IN ACCOUNTANCY Foundations in Financial Management Pilot Paper Time allowed: 2 hours This paper is divided into two sections: Section A ALL TEN questions are compulsory and MUST be attempted

Paper P6 (HKG) Advanced Taxation (Hong Kong) Friday 5 December 2014. Professional Level Options Module

Advanced Taxation (Hong Kong) Friday 5 December 2014. Professional Level Options Module") Professional Level Options Module Advanced Taxation (Hong Kong) Friday 5 December 2014 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A

Professional Level Options Module Advanced Taxation (Hong Kong) Friday 5 December 2014 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A

Nature and Purpose of the Valuation of Business and Financial Assets

G. BUSINESS VALUATIONS 1. Nature and Purpose of the Valuation of Business and Financial Assets 2. Models for the Valuation of Shares 3. The Valuation of Debt and Other Financial Assets 4. Efficient Market

G. BUSINESS VALUATIONS 1. Nature and Purpose of the Valuation of Business and Financial Assets 2. Models for the Valuation of Shares 3. The Valuation of Debt and Other Financial Assets 4. Efficient Market

Current liabilities and payroll

Chapter 12 Current liabilities and payroll Current liabilities are obligations that the business has to discharge within 12 months or its operating cycle if longer than one year. Obligations that are due

Chapter 12 Current liabilities and payroll Current liabilities are obligations that the business has to discharge within 12 months or its operating cycle if longer than one year. Obligations that are due

Chapter. Statement of Cash Flows For Single Company

Chapter 4 Statement of Cash Flows For Single Company 4.1 Single company statement of cash flows Statement of cash flows are primary financial statements and are required along side the income statement

Chapter 4 Statement of Cash Flows For Single Company 4.1 Single company statement of cash flows Statement of cash flows are primary financial statements and are required along side the income statement

Business Studies - Financial Planning and Management Study Notes. Financial Planning and Management Study Notes:

Business Studies - Financial Planning and Management Study Notes Financial Planning and Management Study Notes: The Role of Financial Planning: The strategic role of financial management: Organisational

Business Studies - Financial Planning and Management Study Notes Financial Planning and Management Study Notes: The Role of Financial Planning: The strategic role of financial management: Organisational

Notes on the parent company financial statements

316 Financial statements Prudential plc Annual Report 2012 Notes on the parent company financial statements 1 Nature of operations Prudential plc (the Company) is a parent holding company. The Company

316 Financial statements Prudential plc Annual Report 2012 Notes on the parent company financial statements 1 Nature of operations Prudential plc (the Company) is a parent holding company. The Company

Sri Lanka Accounting Standard-LKAS 7. Statement of Cash Flows

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Company Accounts, Cost and Management Accounting

Company Accounts, Cost and Management Accounting Roll No : 1 : 262 Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All working notes should

Company Accounts, Cost and Management Accounting Roll No : 1 : 262 Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All working notes should

Coimisiún na Scrúduithe Stáit State Examinations Commission. Leaving Certificate 2014. Marking Scheme. Accounting. Higher Level

Coimisiún na Scrúduithe Stáit State Examinations Commission Leaving Certificate 2014 Marking Scheme Accounting Higher Level Note to teachers and students on the use of published marking schemes Marking

Coimisiún na Scrúduithe Stáit State Examinations Commission Leaving Certificate 2014 Marking Scheme Accounting Higher Level Note to teachers and students on the use of published marking schemes Marking

Paper P7 (INT) Advanced Audit and Assurance (International) Monday 3 December 2012. Professional Level Options Module

Advanced Audit and Assurance (International) Monday 3 December 2012. Professional Level Options Module") Professional Level Options Module Advanced Audit and Assurance (International) Monday 3 December 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections:

Professional Level Options Module Advanced Audit and Assurance (International) Monday 3 December 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections:

Financial Statements

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Ratio Analysis. A) Liquidity Ratio : - 1) Current ratio = Current asset Current Liability

Liquidity Ratio : - 1) Current ratio = Current asset Current Liability") A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

Chapter 16. Debentures: An Introduction. Non-current Liabilities. Horngren, Best, Fraser, Willett: Accounting 6e 2010 Pearson Australia.

PowerPoint to accompany Non-current Liabilities Chapter 16 Learning Objectives 1. Account for debentures payable transactions 2. Measure interest expense by the straight line interest method 3. Account

PowerPoint to accompany Non-current Liabilities Chapter 16 Learning Objectives 1. Account for debentures payable transactions 2. Measure interest expense by the straight line interest method 3. Account

Copyright 2009 Pearson Education Canada

The consequence of failing to adjust the discount rate for the risk implicit in projects is that the firm will accept high-risk projects, which usually have higher IRR due to their high-risk nature, and

The consequence of failing to adjust the discount rate for the risk implicit in projects is that the firm will accept high-risk projects, which usually have higher IRR due to their high-risk nature, and

foreign risk and its relevant to acca qualification paper F9

01 technical foreign risk and its relevant to acca qualification paper F9 Increasingly, many businesses have dealings in foreign currencies and, unless exchange rates are fixed with respect to one another,

01 technical foreign risk and its relevant to acca qualification paper F9 Increasingly, many businesses have dealings in foreign currencies and, unless exchange rates are fixed with respect to one another,

Statement of Cash Flows

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 7 Statement of Cash Flows This version of SB-FRS 7 does not include amendments that are effective for annual periods beginning after 1 January 2014.

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 7 Statement of Cash Flows This version of SB-FRS 7 does not include amendments that are effective for annual periods beginning after 1 January 2014.

2015/2016 INTERIM RESULTS ANNOUNCEMENT

(Incorporated in the Cayman Islands with limited liability) (Stock code: 8051) 2015/2016 INTERIM RESULTS ANNOUNCEMENT CHARACTERISTICS OF THE GROWTH ENTERPRISE MARKET ( GEM ) OF THE STOCK EXCHANGE OF HONG

(Incorporated in the Cayman Islands with limited liability) (Stock code: 8051) 2015/2016 INTERIM RESULTS ANNOUNCEMENT CHARACTERISTICS OF THE GROWTH ENTERPRISE MARKET ( GEM ) OF THE STOCK EXCHANGE OF HONG

Dip IFR. Diploma in International Financial Reporting. Friday 11 December 2015. The Association of Chartered Certified Accountants.

Diploma in International Financial Reporting Friday 11 December 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Dip IFR Do NOT

Diploma in International Financial Reporting Friday 11 December 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Dip IFR Do NOT

PART I - INFORMATION REQUIRED FOR QUARTERLY (Q1, Q2 & Q3), HALF-YEAR AND FULL YEAR ANNOUNCEMENTS

, HALF-YEAR AND FULL YEAR ANNOUNCEMENTS") DECLOUT LIMITED (Registration No: 201017764W) UNAUDITED FINANCIAL STATEMENTS AND DIVIDEND ANNOUNCEMENT FOR THE FIRST QUARTER ENDED 31 MARCH 2016 ( 1Q2016 ) This announcement has been prepared by the Company

DECLOUT LIMITED (Registration No: 201017764W) UNAUDITED FINANCIAL STATEMENTS AND DIVIDEND ANNOUNCEMENT FOR THE FIRST QUARTER ENDED 31 MARCH 2016 ( 1Q2016 ) This announcement has been prepared by the Company

Long-term sources - those repayable beyond 1 year. No guaranteed return, but potential is unlimited. High risks require a high rate of return.

Sources of Finance Ord Shares Total Finance Long Short Term Term Pref Shares Loans & Debens Bank O/D Leases Debt Factoring Long-term sources - those repayable beyond 1 year. Ordinary Shares The risk capital

Sources of Finance Ord Shares Total Finance Long Short Term Term Pref Shares Loans & Debens Bank O/D Leases Debt Factoring Long-term sources - those repayable beyond 1 year. Ordinary Shares The risk capital

INSTITUTE OF ACTUARIES OF INDIA. CT2 Finance and Financial Reporting MAY 2009 EXAMINATION INDICATIVE SOLUTION

INSTITUTE OF ACTUARIES OF INDIA CT2 Finance and Financial Reporting MAY 2009 EXAMINATION INDICATIVE SOLUTION General guidelines to markers: The solutions provided here are indicative ones. Please award

INSTITUTE OF ACTUARIES OF INDIA CT2 Finance and Financial Reporting MAY 2009 EXAMINATION INDICATIVE SOLUTION General guidelines to markers: The solutions provided here are indicative ones. Please award

Paper F7. Financial Reporting. March/June 2016 Sample Questions. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Fundamentals Level Skills Module Financial Reporting March/June 2016 Sample Questions Time allowed Reading and planning: 15 minutes Writing: 3 hours This question paper is divided into two sections: Section

Fundamentals Level Skills Module Financial Reporting March/June 2016 Sample Questions Time allowed Reading and planning: 15 minutes Writing: 3 hours This question paper is divided into two sections: Section

Raising capital finance A finance director s guide to financial reporting

Raising capital finance A finance director s guide to financial reporting Capital funding what every finance director should know Introduction 01 Raising capital the accounting framework 02 Net proceeds

Raising capital finance A finance director s guide to financial reporting Capital funding what every finance director should know Introduction 01 Raising capital the accounting framework 02 Net proceeds

Dealing With Your Banker &

Dealing With Your Banker & Other Lenders Your financing The success or failure of your business will depend on whether or not you have enough capital to: buy the equipment and inventory you need; pay overhead

Dealing With Your Banker & Other Lenders Your financing The success or failure of your business will depend on whether or not you have enough capital to: buy the equipment and inventory you need; pay overhead

1.1 Role and Responsibilities of Financial Managers

1 Financial Analysis 1.1 Role and Responsibilities of Financial Managers (1) Planning and Forecasting set up financial plans for their organisations in order to shape the company s future position (2)

1 Financial Analysis 1.1 Role and Responsibilities of Financial Managers (1) Planning and Forecasting set up financial plans for their organisations in order to shape the company s future position (2)

International Accounting Standard 7 Statement of cash flows *

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

No. of ordinary shares

Monthly Return of Equity Issuer on Movements in Securities For the ended : 31/12/2015 To : Hong Kong Exchanges and Clearing Limited Name of Issuer Date Submitted 06/01/2016 China Investments Holdings Limited

Monthly Return of Equity Issuer on Movements in Securities For the ended : 31/12/2015 To : Hong Kong Exchanges and Clearing Limited Name of Issuer Date Submitted 06/01/2016 China Investments Holdings Limited