Technical Writing - Text VII of the US Federal Exchange System (NAS)

|

|

|

- Sandra Harris

- 3 years ago

- Views:

Transcription

1 AUGUST 7, 2012 DODD-FRANK PRODUCT DEFINITIONS UPDATE CFTC and SEC Finalize Key Dodd-Frank Product Definitions, Ushering in Implementation Phase of U.S. OTC Derivatives Regulatory Reforms Background Title VII of the Dodd-Frank Wall Street Reform and Consumer Protection Act ( Dodd-Frank ) provides for comprehensive regulation of the over-the-counter ( OTC ) derivatives markets. Dealers and significant market participants will be required to register with either or both the U.S. Commodity Futures Trading Commission (the CFTC ) and the U.S. Securities and Exchange Commission (the SEC, and, together with the CFTC, the Commissions ), depending on the categories of OTC derivatives in which they transact, and comply with business conduct, margin, capital, recordkeeping and reporting rules. Many other market participants will be subject to other substantial regulatory requirements. The CFTC has finalized many of its Title VII implementing regulations, while the SEC has proposed, but not yet finalized, the majority of its Title VII implementing regulations. Title VII generally bifurcates regulation of the OTC derivatives markets, with the CFTC having jurisdiction over swaps and the SEC having jurisdiction over security-based swaps ( SBS, and with swaps, Title VII Instruments ). The Commissions share jurisdiction over mixed swaps. The CFTC also has regulatory and enforcement authority over security-based swap agreements ( SBSAs ), but the SEC has antifraud and certain other authority over SBSAs. On April 18, 2012, the Commissions adopted final rules defining swap dealer, security-based swap dealer, major swap participant, major security-based swap participant, and eligible contract participant (the Entity Definitions ). For further information on the Entity Definitions, see our previous Sidley Update, available at: Title VII further mandates that the Commissions, in consultation with the Federal Reserve Board, jointly further define the terms swap, security-based swap, and security-based swap agreement (i.e., the Product Definitions ). On July 6, 2012, the SEC approved the Product Definitions on a unanimous vote of the SEC Commissioners. On July 10, 2012, the CFTC held an open meeting at which it approved the final Product Definitions This Sidley update has been prepared by Sidley Austin LLP for informational purposes only and does not constitute legal advice. This information is not intended to create, and receipt of it does not constitute, a lawyer-client relationship. Readers should not act upon this without seeking advice from professional advisers. Attorney Advertising - For purposes of compliance with New York State Bar rules, our headquarters are Sidley Austin LLP, 787 Seventh Avenue, New York, NY 10019, and One South Dearborn, Chicago, IL 60603, Prior results do not guarantee a similar outcome.

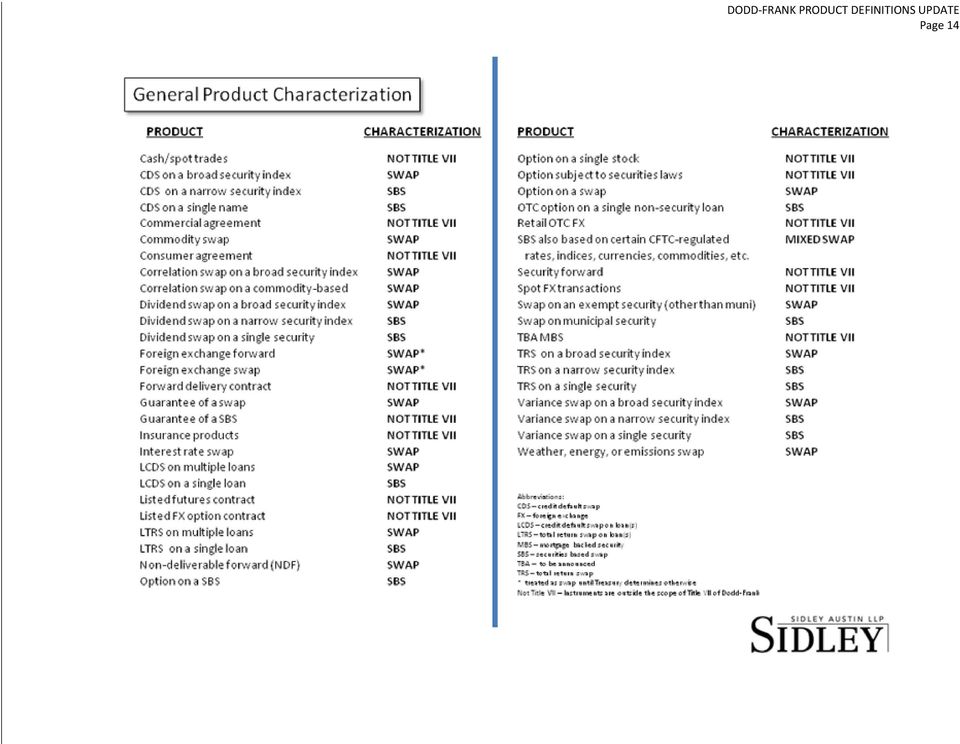

2 Page 2 in a 4-1 vote of the Commissioners (with Commissioner Chilton voting against the final rules) (the final Product Definitions are also referred to herein as the Final Rules ). 1 The Final Rules represent an important step in the implementation of Title VII of Dodd-Frank because they determine the scope of products to be regulated by the Commissions and the jurisdictional boundaries and overlaps between the Commissions with respect to such products. However, the Final Rules play an even greater role in the implementation of Title VII in that a number of other rulemakings that have already been completed will become effective upon effectiveness, or some number of days following effectiveness, of the Final Rules. 2 A discussion of certain of those rulemakings is included in the section entitled Implementation Timing and Effectiveness of Other Rulemakings below. The Statutory Definitions Title VII of Dodd-Frank substantially amended the Commodity Exchange Act ( CEA ), Securities Act and Securities Exchange Act of 1934 (the Securities Exchange Act ). Among those amendments were detailed statutory definitions of swap, security-based swap and mixed swap. The Commissions indicated in adopting the Final Rules that they view the statutory Product Definitions as being detailed and comprehensive. The Commissions have also provided a great deal of interpretation and clarification with respect to the characterization of certain types of OTC derivatives, including Title VII Instruments and other instruments specifically excluded from Title VII. Treatment of Specific Products under the Final Rules In the Final Rules, the Commissions have clarified the characterization of certain products, the treatment of which would otherwise be uncertain under the statutory definitions described above. A visual representation of the final product characterization and a reference chart are included below. Insurance Products Title VII defines a swap broadly to include transactions involving a purchase, sale, payment or delivery that is dependent on the occurrence, nonoccurrence, or extent of occurrence of an event or contingency associated with a potential financial, economic, or commercial consequence. 3 In order to quell the concerns of the insurance industry over the broad definition of swap, the Commissions had indicated in the Proposing Release that they did not interpret this language to capture those products that have historically been regulated as insurance, and the Final Rules include safe harbor provisions which exclude certain insurance products from regulation under Title VII. 1 As used in this Sidley Update, the term Final Rules includes both the text of the final CFTC and SEC regulations, as well as the narrative description of those regulations, unless otherwise indicated. Note that, while the final regulations of the Commissions implementing the Product Definitions are themselves highly detailed and complex, the narrative portion of the Final Rules also includes important interpretations, guidance and clarifications. By necessity, this Sidley Update addresses specific products only at a very high, and general, level. The characterization of a particular agreement, contract or transaction under the Final Rules may involve issues and analysis not described herein. 2 In the July 10 open meeting, CFTC Commissioner Sommers stated that, with this rulemaking, market participants would be off to the races and Commissioner Chilton stated that this rulemaking starts the ball rolling on ten to twelve other Dodd-Frank rulemakings. Commissioner O Malia stated that the final rules would set in place an implementation chain reaction and that registration and compliance schedules will be challenging. Commissioner Wetjen stated that the CFTC s new swap regulatory regime was about to become a reality. In approving the Final Rules, Chairman Shapiro of the SEC stated that [a]pproving the product rules and interpretations is another foundational step in the establishment of a new regulatory regime for derivatives. Note that most of the SEC s new regulatory regime for derivatives remains to be finalized, while much of the CFTC s parallel regime will indeed become a reality with the completion of the Final Rules. 3 Section 722(b) of Dodd-Frank further provides that swaps may not be regulated as insurance by state agencies, thus preempting state insurance regulation of any insurance products that fall within the definition of a swap. The broad definition of swap contained in Dodd- Frank, coupled with the preemption in Section 722(b), lead to significant concern within the insurance industry.

3 Page 3 Under the Final Rules, an insurance product will not be considered a swap or an SBS if it meets any one of three separate, safe harbor, tests: 4 (1) the Product Safe Harbor, (2) the Insurance Grandfather Provision, and (3) the Enumerated Product Safe Harbor: The Product Safe Harbor. A product will not be considered a swap or SBS if the agreement, contract or transaction is provided in accordance with the Provider Test and the Product Test : The Provider Test: requires the person providing the product must be one of the following: (a) a person that is subject to supervision by the insurance commissioner (or similar official or agency) of any state or the U.S. or any instrumentality thereof, and such product must be regulated as insurance under applicable state law or the laws of the U.S.; (b) the provider is directly or indirectly, the U.S., and state or any instrumentality thereof; (c) in the case of reinsurance only, a person providing such product to another person that satisfies the Provider Test, provided that the person is not prohibited by applicable state law or the laws of the U.S. from offering such product to such other person, the product to be reinsured satisfies the Product Test or is one of the Enumerated Products (see below), and except as otherwise permitted under state law, the total amount reimbursable by all reinsurers for the product may not exceed the claims or losses paid by the cedant; or (d) in the case of non-admitted insurance a person who: (i) is located outside of the United States and listed on the Quarterly Listing of Alien Insurers as maintained by the International Insurers Department of the National Association of Insurance Commissioners; or (ii) meets the eligibility criteria for non-admitted insurers under applicable state law. The Product Test: includes any agreement, contract or transaction that either by its terms or by law, requires that: (a) the beneficiary must have an insurable interest that is the subject of the contract and thereby carry the risk of loss with respect to that interest continuously throughout the duration of the contract; (b) the loss must occur and be proved, and any payment or indemnification for the loss must not exceed the value of the insurable interest; (c) the agreement, contract or transaction must not be traded, separately from the insured interest, on any organized market or OTC; and (d) with respect to financial guaranty insurance only, in the event of a payment default or insolvency of the obligor, any acceleration of payments under the policy must be at the sole discretion of the insurer. The Insurance Grandfather Provision. A product will not be considered a swap or SBS if it is an existing insurance agreement, contract or transaction entered into before the effective date of the Final Rules and if it was provided by a person or entity that satisfied the Provider Test. The Enumerated Product Safe Harbor. A product will not be considered a swap or SBS if the product is provided in accordance with the Provider Test and is one of the following: surety bond, fidelity bond, life insurance, health insurance, long term care insurance, title insurance, property and casualty insurance, annuity, disability insurance, insurance against default on individual residential mortgages, and reinsurance (including retrocession) of any of the foregoing. It should be noted that the anti-evasion provisions under the Final Rules also address the potential for parties to attempt to characterize as insurance an instrument that should be treated as a Title VII Instrument, and thus special care should be taken when dealing with agreements, contracts or transactions that will rely upon the insurance safe harbor provisions. Guarantees In the Final Rules, the CFTC has provided an interpretation that the guarantee of an agreement, contract or transaction that falls within the swap definition (and which guarantee is not itself an SBS or mixed swap), including financial 4 Note that insurance products that do not meet any of the three safe harbors will not necessarily be considered swaps or SBS, nor does it create a presumption that the product is a swap or SBS. Failure to meet one of the safe harbors simply means that further analysis of the facts and circumstances is necessary.

a person that is subject to supervision by the insurance commissioner (or similar official or agency) of any state or the U.S.")

4 Page 4 guarantee insurance policies, is an integral part of the swap and therefore the term swap should include such guarantee to the extent that a counterparty to the guaranteed swap would have recourse to the guarantor in connection with the position. This is similar to the approach the CFTC has taken under the Entity Definitions with respect to the swaps that must be considered when determining whether an entity meets the thresholds necessary to be considered a major swap participant. The CFTC indicated that it intends to address the practical implications of treating such guarantees as separate swaps in a separate release in which the CFTC anticipates proposing reporting requirements with respect to guarantees of swaps and explaining the extent to which the duties and obligations of swap dealers and major swap participants pertaining to guarantees are already satisfied with respect to the corresponding guaranteed swaps. The CFTC also expects to address the application of position limits and large trader reporting requirements to guarantees. The CFTC s interpretation that guarantees of swaps are to be treated as swaps will not be effective until the compliance date for the rules the CFTC intends to propose dealing with the treatment of guarantees. The SEC declined to treat guarantees of SBS as either separate SBS transactions or as part of the SBS transactions that they guarantee. Instead the SEC has indicated that it will consider reporting requirements with respect to SBS guarantees as part of its overall rules on reporting of SBS. Note, however, that a guarantee of an SBS may itself be treated as a security under the federal securities laws. The SEC will also consider issues involving cross-border guarantees in a separate release. Stable Value Contracts Dodd-Frank requires the Commissions to conduct a joint study to determine whether to include stable value contracts within the swap definition. The Commissions are currently conducting that study and until the Commissions complete the study and adopt final rules with respect to stable value contracts, such contracts will not be treated as swaps or SBS. Forward Delivery Contracts The Title VII Instrument definitions specifically exclude any sale of a nonfinancial commodity or security for deferred shipment or delivery, so long as the transaction is intended to be physically settled. Security forward contracts, including forwards on mortgage-backed securities eligible to be sold in the to be announced or TBA market, are excluded from Title VII. Under the Final Rules, the CFTC has provided detailed clarification of the scope of the CFTC s forward contract exclusion for non-financial commodities, as applied to swaps. As a general matter, the CFTC intends that the forward contract exclusion from the swap definition should be interpreted in a manner consistent with the historical exclusion of forward contracts from the definition of a futures contract. The CFTC has confirmed that the principles underlying prior CFTC interpretations with regard to book-out transactions would also generally apply in the context of the forward exclusion from the swap definition. As such, commercial market participants that regularly make or take delivery of the referenced commodity in the ordinary course of their businesses may in many cases cash settle an otherwise physical delivery obligation in a book-out, where the cash settlement is effected through a subsequent, separately negotiated agreement. This interpretation would apply with respect to all contracts in nonfinancial commodities. The Final Rules also provide guidance in the following areas: certain contract provisions do not disqualify transactions from falling within the forward contract exclusion (liquidated damages, renewal/evergreen provisions); certain enumerated types of arrangements as described in the Final Rules, including fuel delivery agreements and physical exchange transactions, are not swaps;

5 Page 5 certain physical commercial arrangements that are similar to leases but that are not options may qualify for the forward exclusions under specified circumstances; and energy management agreements do not alter the nature of the transactions conducted under them. Consumer and Commercial Transactions The Final Rules include an interpretation that certain consumer and commercial transactions are not swaps or SBS: Consumer Transactions. Under the Final Rules, agreements, contracts or transactions entered into by consumers primarily for personal, family or household purposes are not considered swaps or security-based swaps. This characterization will apply to transactions in which a consumer acquires or leases real or personal property, obtains a mortgage, provides personal services, or assigns or sells rights of the consumer, including intellectual property rights. It will also include agreements for interest rate caps or locks on consumer loans or mortgages, as well as variable interest rate consumer loans or mortgages. Commercial Transactions. Under the Final Rules, commercial agreements, contracts, or transactions that involve customary business or commercial arrangements will not be construed as Title VII Instruments. This would include, among other things, the following: (a) employment contracts and retirement benefit arrangements; (b) sales, servicing, or distribution arrangements; agreements, contracts, or transactions for the purpose of effecting a business combination transaction; (c) the purchase, sale, lease, or transfer of real property, intellectual property, equipment, or inventory; (d) warehouse lending arrangements in connection with building an inventory of assets in anticipation of a securitization of such assets (such as in a securitization of mortgages, student loans, or receivables); (e) mortgage or mortgage purchase commitments, or sales of installment loan agreements or contracts or receivables; (f) fixed or variable interest rate commercial loans entered into by banks and non-banks; and (g) commercial agreements, contracts and transactions (including, but not limited to, leases, service contracts and employment agreements) containing escalation clauses linked to an underlying commodity such as an interest rate or consumer price index. The Final Rules also list characteristics and factors the Commissions will consider in determining whether consumer or commercial transactions that are not included in the foregoing non-exclusive list are Title VII Instruments. Loan Participations The Final Rules provide that the Commissions will interpret the Title VII Instrument definitions to exclude loan participations that reflect an ownership interest in the underlying loan or commitment, provided that the conditions listed in the release are met. Certain loan participations may also be securities under the Federal securities laws. Such transactions would be regulated as securities and not as Title VII Instruments. Foreign Exchange Products The Final Rules provide that foreign exchange forwards and foreign exchange swaps are swaps under Title VII, unless and until the Secretary of the U.S. Department of the Treasury makes a determination that such instruments should not be treated as swaps. Even if the Treasury Secretary makes this determination, foreign exchange forwards and foreign exchange swaps will continue to be subject to certain Title VII provisions, including reporting and business conduct standards. Note that Dodd-Frank defines foreign exchange forwards and foreign exchange swaps narrowly to include only those contracts where there is a physical delivery obligation, so the statutory authority for the Treasury Secretary to exclude foreign currency transactions from the swap definition is limited. The Final Rules clarify that nondeliverable contracts, such as foreign currency options, non-deliverable foreign exchange forwards, currency swaps, and cross-currency swaps are within the swap definition and will remain within the swap definition notwithstanding any action taken by the Treasury Secretary. The Treasury Secretary has not yet indicated when or if he intends to act on this proposal.

6 Page 6 The CFTC also provided an interpretation under the Final Rules that certain foreign exchange spot transactions are not foreign exchange forwards, therefore are not "swaps" and are not subject to Title VII. Generally, to be entitled to this treatment, a spot transaction must settle on the customary timeline of the relevant spot market (generally 2 business days), but foreign currency trades that are made in connection with (and contemporaneously with) a foreign securities transaction and are settled within the settlement cycle for the associated securities transaction will also be eligible, even if the securities transaction settlement cycle is longer than the customary spot transaction cycle. Forward Rate Agreements The Final Rules provide that so-called forward rate agreements, notwithstanding the use of the word forward are swaps, unless they are otherwise excluded from the swap definition under Title VII. Interest Rates, Other Monetary Rates and Yields OTC derivatives on interest rates and other monetary rates (including, among other things, interbank offered rates, money market rates, government target rates, general lending rates and rates from indexes) will be treated as swaps. OTC derivatives on yields, where the yield is a proxy for the price or value of a debt security, loan, or narrow-based security index, will be treated as SBS, except in the case of certain exempted securities. OTC derivatives on rates or yields of U.S. Treasuries and certain other exempted securities (other than municipal securities) will be swaps. OTC derivatives that combine the foregoing features may also be treated as mixed swaps and subject to the joint jurisdiction of the Commissions. Total Return Swaps Under the Final Rules, a total return swap ( TRS ) on a single security, loan or narrow-based security index will generally be treated as an SBS. Where the TRS includes other features, such as interest-rate optionality or nonsecurities components (e.g. commodity prices), the TRS may be treated as a mixed swap. A TRS on a broad-based security-index or on two or more loans is a swap under the Final Rules. Contracts Based on Futures Contracts An OTC derivative where the underlying interest is a futures contract will generally be treated as a swap under the Final Rules. However, in most cases an OTC derivative in which the underlying interest is a security futures contract will be treated as an SBS. OTC derivatives on futures in which the underlying interest is certain exempt sovereign foreign debt will be treated as swaps if the conditions provided under the Final Rules are met. Contracts on Securities Indices Under the statutory Product Definitions, derivatives on broad-based securities indices will generally be swaps and derivatives on narrow-based securities indices will generally be SBS. This mirrors a long-standing jurisdictional divide between the Commissions. The Final Rules provide interpretive guidance in a number of key areas (including in relation to index CDS, where the swap-sbs dividing line is particularly nuanced and can depend crucially upon the availability to the public of financial information about the issuers or securities in the index or on the variability of the index components) with respect to the proper categorization of derivatives on securities indices. The proper characterization of Title VII Instruments on indices of securities is highly complex under the Final Rules.

a foreign securities transaction and are settled within the settlement cycle for the associated securities transaction will also be eligible, even")

7 Page 7 Contracts for Differences The Commissions have provided an interpretation with respect to contracts for differences ( CFDs ). 5 CFDs, unless otherwise excluded, will generally fall within the Title VII Instrument definitions. The determination of whether a particular CFD is a swap or a SBS will depend on the underlying product in the transaction. The SEC may also determine that a particular CFD on an equity security, for example, should be characterized as a purchase or sale of the underlying equity security, and therefore subject to the Federal securities laws applicable to such offers and sales. Mixed Swaps OTC derivatives that have characteristics of both swaps and SBS will be treated as mixed swaps and will be subject to the joint jurisdiction of both Commissions (i.e., they will be treated as both swaps and SBS). The Final Rules state that both Commissions intend the mixed swap category to be a narrow one, capturing only a small subset of instruments subject to Title VII of Dodd-Frank. Under the Final Rules, the parties to an uncleared mixed swap, in which at least one of the parties to the mixed swap is registered with both Commissions, will need to comply with certain new regulations. For other mixed swaps, the Commissions have established a process for the parties to request a joint order permitting them to comply, as to parallel SEC/CFTC provisions, with specified provisions of either the CEA or Securities Exchange Act, and related regulations, instead of complying with the equivalent provisions of the other Commission. A party submitting such a request must provide the Commissions with certain information, including material information regarding the terms of the specified mixed swap. The request may be withdrawn at any time prior to the Commissions issuance of a joint order. If the Commissions do not issue a joint order within 120 days of receipt of a complete request, they must publicly state their reasons for failing to do so. Regional Transmission Organizations and Independent System Operators The CFTC declined to address under the Final Rules the status of transactions in Regional Transmission Organizations ( RTOs ) and Independent System Operators ( ISOs ). Dodd-Frank addresses certain instruments and transactions regulated by the Federal Energy Regulatory Commission ( FERC ), potentially including certain RTO and ISO transactions, which may also be subject to CFTC jurisdiction. Specifically, Title VII added a section to the CEA providing that if the CFTC determines that an exemption for FERC-regulated instruments and transactions would be in accordance with the public interest, then the CFTC shall exempt such instruments or transactions from the CEA s requirements. The treatment of these FERC-regulated instruments and transactions will therefore be determined using the public interest exemption standards in Dodd-Frank. Notably, the CFTC has indicated that it has been engaged in discussions with a number of RTOs and ISOs regarding the possibility of a public interest exemption for certain RTO and ISO transactions. Security-Based Swap Agreements SBSAs include certain swaps that also involve securities. The CFTC has general regulatory and enforcement authority with respect to SBSAs, while the SEC has concurrent antifraud and certain other regulatory authority. SBSAs include certain swaps on broad-based security indices and swaps on certain exempted securities, other than municipal securities. This would include most swaps on U.S. Treasuries. The Commissions believe it is not possible to provide a bright line test to determine which swaps are SBSAs but they have provided indicative examples in the Final Rules. 5 A CFD is generally an agreement to exchange the difference in value of an underlying asset between the time at which a CFD position is established and the time at which it is terminated. CFDs can be traded on a number of products, including Treasuries, foreign exchange rates, commodities, equities and stock indices.

8 Page 8 Forward Contracts with Embedded Volumetric Optionality In response to comments on the Proposed Rules that asserted that agreements containing so-called volumetric options, and that otherwise satisfy the terms of the forward contract exclusion from the swap definition should also qualify as excluded forward contracts, notwithstanding the existence of the option component of the agreement, the CFTC has provided an interpretation in the Final Rules. Used as a hedge against future uncertainty by various types of energy companies, among others, a forward contract with embedded volumetric optionality could include, for example, a gas supply contract entered into by an electric utility where the amount of gas the utility receives on a future date varies depending on weather conditions. Such nonfinancial commodity contracts may be excluded from the swap definition if they qualify for the forward exclusion from the swaps definition. Under the Final Rules, the CFTC confirmed the applicability of a 1985 interpretation addressing contracts with embedded options in the context of the forward contract exclusion from the futures definition under the CEA. However, the Final Rules expand the analysis to encompass a seven-factor test designed to determine whether a forward contract with embedded optionality will be excluded as a forward contract. Two key factors in the seven-factor analysis are whether the embedded option can potentially undermine the contract s overall purpose and the extent to which the optionality aspect is primarily driven by physical factors or regulatory requirements that influence supply and demand and are outside of the parties control. The Final Rules also state that forward contracts with three other types of embedded optionality may qualify for the forward exclusion provided they satisfy the seven-factor test: (1) forwards with an extension option, such as a five-year renewal term; (2) forwards with an evergreen provision which automatically renews the contract absent affirmative termination; and (3) forwards with embedded optionality as to delivery points or delivery dates. While the interpretation provided by the CFTC in the Final Rules with respect to forwards with embedded optionality constitutes a CFTC interpretation, and market participants are entitled to rely upon it in its current form, the CFTC has also requested public comment on the interpretation. Comments on the proposed interpretation must be submitted within 60 days of the date the Final Rules are published in the Federal Register. Inter-Affiliate Title VII Instruments The Commissions have indicated that they will consider whether inter-affiliate transactions should be treated differently from other swaps or SBS in the context of other Title VII rulemakings. However, the Commissions have not elected to exclude such transactions, as a class, from the Title VII Instrument definitions. Timing of Characterization of Instrument In the Final Rules, the Commissions clarified that a determination of whether a particular instrument is a swap, security-based swap, or mixed swap is generally to be made at the inception of the trade, and that such a characterization would remain throughout the life of the instrument unless the instrument is amended or modified in a material respect. 6 Process for Requesting Interpretations The Final Rules establish a process by which parties may request a joint interpretation of the Commissions regarding whether a particular OTC derivative or type of derivative that is subject to Title VII of Dodd-Frank should be treated 6 For example, a derivative on an index that is a broad-based index at the time of the inception of the contract, but later becomes a derivative on a narrow-based index due to changes in the number of securities in the index, would generally remain a swap subject to CFTC jurisdiction, absent a material change in terms. The reverse would be true with respect to a narrow-based index that becomes a broad-based index.

9 Page 9 as a swap, SBS or mixed swap. The process includes provisions designed to ensure that the Commissions act promptly on the request (though there can be no assurance that the Commissions will actually issue the requested joint interpretation). Impact on Securities Laws Dodd-Frank amended the Securities Act and the Securities Exchange Act to include a security-based swap within the definition of a security. This makes security-based swaps subject to the requirements of the Securities Act, Securities Exchange Act, and the rules and regulations thereunder, unless an exemption applies. Acknowledging that the introduction of security-based swaps into the regulatory framework for securities creates complex issues of interpretation, the SEC has provided orders and other exemptive relief from certain requirements of the Securities Act and Securities Exchange Act until the applicable compliance dates for final rules under Dodd-Frank. Accordingly, in the Final Rules the SEC provides that for purposes of the exemptions the compliance date will be 180 days from publication of the Final Rules in the Federal Register. This does not help illuminate the proper application of the securities laws to security-based swaps, but the SEC has indicated that it intends to address the issue before the end of the 180 day period. Market participants may also wish to seek guidance from the SEC as interpretive issues arise. Anti-Evasion Provisions Under the Final Rules, the CFTC has issued final anti-evasion rules and related interpretations applicable to transactions that are willfully structured to evade the provisions of Title VII regulating swaps. Specific provisions would apply to currency and interest rate swaps that are evasively structured as foreign exchange forwards or foreign exchange swaps (both of which may be excluded from the swap definition by the Treasury Secretary), and to products that are structured as identified banking products to evade the swaps definition. The CFTC has also adopted rules addressing the potential for evasive conduct occurring outside of the United States. Implementation Timing and Impact of Other Rulemakings The Final Rules themselves will become effective 60 days after they are published in the Federal Register, [which has not yet occurred as of the date of this Sidley Update.] The effective date of the Final Rules themselves will also trigger a number of other key Dodd-Frank rules, as described below. Expiration of CFTC Temporary Delay Order Dodd-Frank states that, unless otherwise provided, the amendments made by Title VII of Dodd-Frank to the CEA were to go into effect automatically on the later of July 16, 2011 or, to the extent that a particular provision required a rulemaking, not less than 60 days after publication of the final implementing rule in the Federal Register. On July 14, 2011, the CFTC issued a final order that temporarily delayed many of the Title VII CEA amendments that otherwise would have become effective. The CFTC has twice amended and extended the expiration dates of that final order. With the completion of the Final Rules, many aspects of that final order will now expire, effective as of the earlier of December 31, 2012 or 60 days after the Final Rules are published in the Federal Register. Position Limits The effective date of the Final Rules will trigger certain CFTC speculative position limits that were finalized in late Dodd-Frank required the CFTC to limit the amount of positions, excluding bona fide hedges, that may be held 7 Note that the CFTC s position limits are currently the subject of an industry lawsuit that could result in the implementing rules being delayed. As of the date of this Sidley Update there is no resolution of that lawsuit and no indication of when there will be such a resolution.

10 Page 10 by any person in physical commodity futures and options in exempt commodities and agricultural commodities, in each case, that are traded on a regulated futures market. 8 Dodd-Frank also required the CFTC to implement position limits, excluded bond fide hedges, that may be held by a person in swaps that are economically equivalent to listed futures and options on exempt commodities and agricultural commodities. The first of the CFTC s position limits will go into effect 60 days after the Final Rules are published in the Federal Register. For additional information concerning CFTC-set speculative position limits see our Sidley Update at For additional information concerning a proposal to amend the aggregation rules with respect to CFTC-set speculative position limits, see our Sidley Update at Dealers and Major Participants Definitions and Registration Timing On May 23, 2012, the Commissions jointly published the final definitions of swap dealer, major swap participant, security-based swap dealer, major security-based swap participant, and eligible contract participant. Those rules became effective on July 23, With the completion of the Final Rules, registration with the CFTC of swap dealers and major swap participants will now be required, pursuant to the CFTC s final registration rules, effective 60 days after publication of the Final Rules in the Federal Register. The equivalent SEC rules have not yet been finalized. Dealers and Major Participants Compliance The CFTC has already completed the majority of its compliance and business conduct rules applicable to swap dealers and major swap participants. With the completion of the Final Rules, compliance with many of these rules will become compulsory in the near future. Impact on Commodity Pool Operators Prior to the enactment of Dodd-Frank, the operator of an investment fund that traded listed futures contracts was required to register with the CFTC as a commodity pool operator ( CPO ) and a person providing advice with respect to listed futures contracts was required to register with the CFTC as a commodity trading advisor ( CTA ). Registered CPOs and CTAs were also required to be become members of and adhere to the self-regulatory rules of the National Futures Association ( NFA ). Dodd-Frank amended the definitions of CPO and CTA to include funds that trade swaps and advisors with respect to swaps, respectively. The CPO and CTA definitions apply to swaps trading without regard to whether the swaps positions are taken for investment or hedging purposes, and the definitions apply equally to non-us CPOs and CTAs with clients or investors in the United States. The effectiveness of the amendments to the CPO and CTA definitions to include swaps has been temporarily delayed under a series of CFTC orders. The expansion of the applicability of the registration, membership and reporting requirements definitions will occur automatically upon the expiration of these orders, which will occur upon the final effective date of the swap definition i.e., 60 days after the Final Rules are published in the Federal Register or December 31, 2012, whichever is earlier. As a result, upon the effective date, investment funds that have never traded futures, but that trade, or have the authority to trade, swaps, will become commodity pools. Operators of such pools and advisors to such pools will be subject to CFTC registration and NFA membership requirements and reporting requirements as of that date. This could potentially include managers of pure securities strategies that use swaps to hedge interest rate or foreign currency exposures, managers of fund-of-funds that engage in fund-level hedging or that invest in funds that themselves will be brought within the CFTC-regulatory regime once the swap definition is 8 Exempt commodities are all commodities that are neither excluded commodities nor agricultural commodities. Excluded commodities include certain interest and exchange rates and other economic measures. Among the exempt commodities are a wide variety of energy and metals contracts.

11 Page 11 effective, private equity managers that use swaps for hedging purposes, real estate managers, and others who have never before been subject to CFTC regulation. There is no grace period during which a person required to register may continue to engage in the activity that triggers the registration obligation pending completion of the registration process. While the process of registering as a CPO or CTA is not generally considered onerous, a number of compliance policies and procedures must be in place prior to registration. In addition, certain key employees of CPOs and CTAs may be required to submit their fingerprints to the NFA and to take industry standard proficiency exams in order to continue to be involved in activities of the registrant that involve futures or swaps. Persons that will become subject to a registration obligation once the Final Rules go into effect are encouraged to begin the registration process immediately in order to ensure that there is no disruption in their ongoing business activities. Although certain exemptions from CPO and CTA registration may be available, the CFTC has recently made substantial changes to its exemption regime that will severely limit the ability of many market participants to rely on existing exemptions. For additional information on CPO and CTA exemptions, see our previous Sidley Update at Clearing and Exchange Trading Neither the CFTC nor the SEC has yet mandated that any swap, security-based swap, or group, type or class thereof be cleared. However, it is expected that the CFTC will propose to implement mandatory clearing with respect to certain products that are already being cleared through one or more regulated clearinghouses in the near future. 9 It is not clear when the SEC will propose one or more clearing mandates. On July 10, 2012, the CFTC approved final rules implementing the end-user exception to the clearing mandate, as well as a proposed exemption from the clearing mandate for certain cooperatives. For further information concerning those actions, please see a separate Sidley Update, available at The CFTC has also finalized rules that would provide for a phase-in of clearing mandates, with the compliance dates determined based on the types of counterparties involved. The phasing of exchange trading mandates and other requirements will be addressed in a future CFTC rulemaking. Title VII Instruments that are subject to a clearing mandate will also be required to be executed on a regulated futures or securities exchange, as applicable, or a swap execution facility or security-based swap execution facility, to the extent that any such facility makes the swap or SBS available to trade. Many of the CFTC and SEC rules governing these facilities have not yet been finalized. Margin Requirements Title VII Instruments that are centrally cleared will be subject to margin requirements determined in accordance with clearinghouse rules. Margin requirements for non-cleared Title VII Instruments will be determined in accordance with applicable rules of the CFTC, SEC and various banking regulators. The CFTC and the banking regulators have proposed margin rules, while the SEC has yet to propose margin rules. Reporting and Recordkeeping Obligations Dodd-Frank will ultimately require that market participants trading Title VII Instruments report data concerning their transactions to one or more swap or SBS data repositories and that they retain certain documentation concerning their positions in Title VII Instruments. Some of the information concerning Title VII Instruments will ultimately be required to be disseminated publicly and in real time. The majority of the reporting burden will fall on swap dealers, 9 CFTC Interest Rate and Index CDS Proposal.

12 Page 12 security-based swap dealers, major swap participants and major security-based swap participants. However, other users of Title VII Instruments may become subject to extensive recordkeeping requirements, including a requirement that they retain full, complete and systematic records with respect to each Title VII Instrument to which they are party. Furthermore, the market participants that are responsible for fulfilling Dodd-Frank reporting mandates may require that their end-user counterparties retain extensive records to support the accuracy of the information being reported to the data repositories. Although the SEC s reporting and recordkeeping rules remain in the proposal stage, the CFTC s rules are final and will become effective with staggered timing (depending on asset class) upon publication of the Final Rules in the Federal Register.

13 Page 13

14 Page 14

15 Page 15 If you have any questions regarding this update, please contact the Sidley lawyer with whom you usually work. The Derivatives Practice of Sidley Austin LLP Sidley s derivatives lawyers in numerous worldwide offices advise clients on a broad range of domestic and international derivatives transactions involving swaps, commodity futures contracts and options. Our clients, located in the U.S. and outside the U.S., include commercial banks, investment banks, insurance companies, hedge funds and mutual funds and their advisers, commodity and options exchanges, clearing organizations and other participants in the OTC and exchange-traded derivatives markets. In serving our derivatives clients, our internationally-based group utilizes the extensive experience of lawyers in Sidley s other practice areas, including tax, banking, insurance, investment funds, litigation, bankruptcy, employee benefits, securitization and financial regulatory practices. We act for our clients in a wide variety of settings, including initial transaction and product structuring, negotiation and execution; post-trade operation, modification, work-out, dispute resolution, remedies and recovery; practice before regulatory authorities; and general consultation. The Insurance and Financial Services Practice of Sidley Austin LLP Sidley is one of only a few internationally recognized law firms to have a substantial, multidisciplinary practice devoted to the insurance and financial services industry. We have approximately 85 lawyers devoted exclusively to providing both transactional and dispute resolution services to the industry, throughout the world. Our Insurance and Financial Services Group has an intimate knowledge of and appreciation for the industry and its unique issues and challenges. Regular clients include many of the largest insurance and reinsurance companies, brokers, banks, investment banking firms and regulatory agencies, for which we provide regulatory, corporate, securities, mergers and acquisitions, securitization, derivatives, tax, reinsurance dispute, class action defense and other transactional and litigation services. The Investment Funds Practice of Sidley Austin LLP Sidley has a premier, global practice in structuring and advising investment funds and advisers. We advise clients in the formation and operation of all types of alternative investment vehicles, including hedge funds, fund-of-funds, commodity pools, venture capital and private equity funds, private real estate funds and other public and private pooled investment vehicles. We also represent clients with respect to more traditional investment funds, such as closed-end and open-end registered investment companies (i.e., mutual funds) and exchange-traded funds (ETFs). Our advice covers the broad scope of legal and compliance issues that are faced by funds and their boards, as well as investment advisers to funds and other investment products and accounts, under the laws and regulations of the various jurisdictions in which they may operate. In particular, we advise our clients regarding complex federal and state laws and regulations governing securities, commodities, funds and advisers, including the Dodd-Frank Act, the Investment Company Act of 1940, the Investment Advisers Act of 1940, the Securities Act of 1933, the Securities Exchange Act of 1934, the Commodity Exchange Act, the USA PATRIOT Act and comparable laws in non-u.s. jurisdictions. Our practice group consists of approximately 120 lawyers in New York, Chicago, London, Hong Kong, Singapore, Shanghai, Tokyo, Los Angeles and San Francisco. The Securities and Futures Regulatory Practice of Sidley Austin LLP Sidley Austin LLP has one of the nation's premier securities and futures regulatory practices, with more than 50 lawyers spanning Sidley offices in the United States, Europe and Asia. Lawyers in this practice group represent major investment banks, broker-dealers, futures commission merchants, commercial banks, insurance companies, hedge funds complexes, alternative trading systems and ECNs, and exchanges, both domestic and foreign. Drawing from its breadth and depth, Sidley's Securities and Futures Regulatory group handles a wide spectrum of matters assisting clients with the formation of their businesses; counseling on general compliance, proposed laws and regulations, and regulatory trends; representing clients on securities and derivatives transactions; and defending firms in regulatory inquiries and enforcement proceedings. To receive future copies of this and other Sidley updates via , please sign up at

16 Page 16 BEIJING BRUSSELS CHICAGO DALLAS FRANKFURT GENEVA HONG KONG HOUSTON LONDON LOS ANGELES NEW YORK PALO ALTO SAN FRANCISCO SHANGHAI SINGAPORE SYDNEY TOKYO WASHINGTON, D.C. Sidley Austin LLP, a Delaware limited liability partnership which operates at the firm s offices other than Chicago, New York, Los Angeles, San Francisco, Palo Alto, Dallas, London, Hong Kong, Houston, Singapore and Sydney, is affiliated with other partnerships, including Sidley Austin LLP, an Illinois limited liability partnership (Chicago); Sidley Austin (NY) LLP, a Delaware limited liability partnership (New York); Sidley Austin (CA) LLP, a Delaware limited liability partnership (Los Angeles, San Francisco, Palo Alto); Sidley Austin (TX) LLP, a Delaware limited liability partnership (Dallas, Houston); Sidley Austin LLP, a separate Delaware limited liability partnership (London); Sidley Austin LLP, a separate Delaware limited liability partnership (Singapore); Sidley Austin, a New York general partnership (Hong Kong); Sidley Austin, a Delaware general partnership of registered foreign lawyers restricted to practicing foreign law (Sydney); and Sidley Austin Nishikawa Foreign Law Joint Enterprise (Tokyo). The affiliated partnerships are referred to herein collectively as Sidley Austin, Sidley, or the firm.

; Sidley Austin (CA) LLP, a Delaware limited liability partnership (Los Angeles, San Francisco, Palo Alto); Sidley Austin (TX) LLP, a Delaware limited liability")

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.gov Final Rules and Interpretations i) Further Defining Swap, Security-Based

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.gov Final Rules and Interpretations i) Further Defining Swap, Security-Based

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.gov Proposed Rules and Interpretive Guidance i) Further Defining

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.gov Proposed Rules and Interpretive Guidance i) Further Defining

CLIENT MEMORANDUM CFTC AND SEC ADOPT DEFINITION OF SWAP AND SECURITY-BASED SWAP

CLIENT MEMORANDUM CFTC AND SEC ADOPT DEFINITION OF SWAP AND SECURITY-BASED SWAP The Commodity Futures Trading Commission and the Securities and Exchange Commission have issued joint final rules and interpretations

CLIENT MEMORANDUM CFTC AND SEC ADOPT DEFINITION OF SWAP AND SECURITY-BASED SWAP The Commodity Futures Trading Commission and the Securities and Exchange Commission have issued joint final rules and interpretations

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.gov Q & A Final Rules and Interpretations i) Further Defining Swap,

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.gov Q & A Final Rules and Interpretations i) Further Defining Swap,

Final Product Definitions Under Title VII of Dodd-Frank

Final Product Definitions Under Title VII of Dodd-Frank CFTC and SEC Adopt Rules and Guidance to Further Define Swap, Security-Based Swap, Mixed Swaps and Other Swap-Related Terms EXECUTIVE SUMMARY Pursuant

Final Product Definitions Under Title VII of Dodd-Frank CFTC and SEC Adopt Rules and Guidance to Further Define Swap, Security-Based Swap, Mixed Swaps and Other Swap-Related Terms EXECUTIVE SUMMARY Pursuant

INVESTMENT FUNDS. SEC Proposes First Dodd-Frank Investment Advisers Act Rule to Address Family Offices. What Is a Family Office?

OCTOBER 22, 2010 INVESTMENT FUNDS SEC Proposes First Dodd-Frank Investment Advisers Act Rule to Address Family Offices Section 409(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the

OCTOBER 22, 2010 INVESTMENT FUNDS SEC Proposes First Dodd-Frank Investment Advisers Act Rule to Address Family Offices Section 409(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the

July 12, 2012. 1 See CFTC Fact Sheet available at:

SEC and CFTC Finalize Key Swap Product Definitions under Dodd-Frank, Triggering the Effectiveness or Phase- In of Many Dodd-Frank Derivatives Regulatory Provisions July 12, 2012 On July 6, 2012, and July

SEC and CFTC Finalize Key Swap Product Definitions under Dodd-Frank, Triggering the Effectiveness or Phase- In of Many Dodd-Frank Derivatives Regulatory Provisions July 12, 2012 On July 6, 2012, and July

House Financial Services Draft OTC Derivatives Legislative Proposal

House Financial Services Draft OTC Derivatives Legislative Proposal House Financial Services Chairman Barney Frank Releases Discussion Draft of the Over-the-Counter Derivatives Markets Act of 2009, on

House Financial Services Draft OTC Derivatives Legislative Proposal House Financial Services Chairman Barney Frank Releases Discussion Draft of the Over-the-Counter Derivatives Markets Act of 2009, on

Title VII: Derivatives (Wall Street Transparency and Accountability Act of 2010)

") Title VII: Derivatives (Wall Street Transparency and Accountability Act of 2010) Summary: Regulates the previously unregulated, over-the-counter (OTC) derivatives market Requires registration of swap dealers,

Title VII: Derivatives (Wall Street Transparency and Accountability Act of 2010) Summary: Regulates the previously unregulated, over-the-counter (OTC) derivatives market Requires registration of swap dealers,

FINANCIAL INSTITUTIONS REGULATORY UPDATE

OCTOBER 19, 2009 FINANCIAL INSTITUTIONS REGULATORY UPDATE The Financial Institutions Regulatory Practice Group of Sidley Austin LLP The Financial Institutions Regulatory Practice group offers counseling,

OCTOBER 19, 2009 FINANCIAL INSTITUTIONS REGULATORY UPDATE The Financial Institutions Regulatory Practice Group of Sidley Austin LLP The Financial Institutions Regulatory Practice group offers counseling,

CFTC and SEC Finalize Product Definitions Rules under Title VII of the Dodd-Frank Act

July 31, 2012 CFTC and SEC Finalize Product Definitions Rules under Title VII of the Dodd-Frank Act Key Takeaways: > The CFTC and the SEC significantly clarified the scope of the definitions of swap, securitybased

July 31, 2012 CFTC and SEC Finalize Product Definitions Rules under Title VII of the Dodd-Frank Act Key Takeaways: > The CFTC and the SEC significantly clarified the scope of the definitions of swap, securitybased

Credit Default Swaps Insurance or Not? What is a Credit Default Swap? History of CDS. CDS market started in early 1990s

BEIJING BRUSSELS CHICAGO DALLAS FRANKFURT GENEVA HONG KONG LONDON LOS ANGELES NEW YORK PALO ALTO SAN FRANCISCO SHANGHAI SINGAPORE SYDNEY TOKYO WASHINGTON, D.C. Credit Default Swaps Insurance or Not? Casualty

BEIJING BRUSSELS CHICAGO DALLAS FRANKFURT GENEVA HONG KONG LONDON LOS ANGELES NEW YORK PALO ALTO SAN FRANCISCO SHANGHAI SINGAPORE SYDNEY TOKYO WASHINGTON, D.C. Credit Default Swaps Insurance or Not? Casualty

Issues in insurance company mergers & acquisitions

Issues in insurance company mergers & acquisitions By Perry J. Shwachman, Anthony J. Ribaudo and R. Bradley Drake, Sidley Austin LLP The completion of a successful merger or acquisition involving insurance

Issues in insurance company mergers & acquisitions By Perry J. Shwachman, Anthony J. Ribaudo and R. Bradley Drake, Sidley Austin LLP The completion of a successful merger or acquisition involving insurance

SWAP DEALER AND SECURITY-BASED SWAP DEALER DEFINED

CLIENT MEMORANDUM SWAP DEALER AND SECURITY-BASED SWAP DEALER DEFINED The Securities and Exchange Commission and Commodity Futures Trading Commission jointly adopted final rules 1 under Title VII of the

CLIENT MEMORANDUM SWAP DEALER AND SECURITY-BASED SWAP DEALER DEFINED The Securities and Exchange Commission and Commodity Futures Trading Commission jointly adopted final rules 1 under Title VII of the

Swap Definitions Rules Finalized by the SEC and the CFTC under Dodd-Frank

September 25, 2012 Practice Groups: Derivatives and Structured Products Investment Management Financial Services Reform/Dodd-Frank Resources Swap Definitions Rules Finalized by the SEC and the CFTC under

September 25, 2012 Practice Groups: Derivatives and Structured Products Investment Management Financial Services Reform/Dodd-Frank Resources Swap Definitions Rules Finalized by the SEC and the CFTC under

Dodd-Frank Act Changes Affecting Private Fund Managers and Other Investment Advisers By Adam Gale and Garrett Lynam

Dodd-Frank Act Changes Affecting Private Fund Managers and Other Investment Advisers By Adam Gale and Garrett Lynam I. Introduction The Dodd-Frank Wall Street Reform and Consumer Protection Act ( Dodd-Frank

Dodd-Frank Act Changes Affecting Private Fund Managers and Other Investment Advisers By Adam Gale and Garrett Lynam I. Introduction The Dodd-Frank Wall Street Reform and Consumer Protection Act ( Dodd-Frank

CFTC AND SEC DEFINE MAJOR SWAP PARTICIPANT AND MAJOR SECURITY-BASED SWAP PARTICIPANT

CLIENT MEMORANDUM CFTC AND SEC DEFINE MAJOR SWAP PARTICIPANT AND MAJOR SECURITY-BASED SWAP PARTICIPANT The Commodity Futures Trading Commission and the Securities and Exchange Commission have issued joint

CLIENT MEMORANDUM CFTC AND SEC DEFINE MAJOR SWAP PARTICIPANT AND MAJOR SECURITY-BASED SWAP PARTICIPANT The Commodity Futures Trading Commission and the Securities and Exchange Commission have issued joint

California Supreme Court Issues Ruling in Brinker Clarifying Employers Duty to Provide Meal and Rest Breaks to Hourly Employees

APRIL 13, 2012 CALIFORNIA EMPLOYMENT & LABOR UPDATE California Supreme Court Issues Ruling in Brinker Clarifying Employers Duty to Provide Meal and Rest Breaks to Hourly Employees In one of the most anticipated

APRIL 13, 2012 CALIFORNIA EMPLOYMENT & LABOR UPDATE California Supreme Court Issues Ruling in Brinker Clarifying Employers Duty to Provide Meal and Rest Breaks to Hourly Employees In one of the most anticipated

ALI-ABA: Title VII AND PRODUCT DEFINITIONS. August 24, 2012

ALI-ABA: Title VII AND PRODUCT DEFINITIONS August 24, 2012 Background 2 Background on Title VII Objectives of Title VII Reduce systemic risk posed by the swaps market to the U.S. financial system Increase

ALI-ABA: Title VII AND PRODUCT DEFINITIONS August 24, 2012 Background 2 Background on Title VII Objectives of Title VII Reduce systemic risk posed by the swaps market to the U.S. financial system Increase

CFTC Chairman Seeks Additional Authority for CFTC

CFTC Chairman Seeks Additional Authority for CFTC Chairman Gensler Requests Clarifying Language for CFTC Regulatory Authority Under the Over-the-Counter Derivatives Markets Act of 2009 SUMMARY In response

CFTC Chairman Seeks Additional Authority for CFTC Chairman Gensler Requests Clarifying Language for CFTC Regulatory Authority Under the Over-the-Counter Derivatives Markets Act of 2009 SUMMARY In response

FINRA and MSRB Issue Guidance on Best Execution Obligations in Equity, Options and Fixed Income Markets

DECEMBER 9, 2015 SIDLEY UPDATE FINRA and MSRB Issue Guidance on Best Execution Obligations in Equity, Options and Fixed Income Markets Financial Industry Regulatory Authority, Inc. (FINRA) and the Municipal

DECEMBER 9, 2015 SIDLEY UPDATE FINRA and MSRB Issue Guidance on Best Execution Obligations in Equity, Options and Fixed Income Markets Financial Industry Regulatory Authority, Inc. (FINRA) and the Municipal

SEC Adopts Rules to Implement the Private Fund Investment Advisers Registration Act

SEC Adopts Rules to Implement the Private Fund Investment Advisers Registration Act Jason E. Brown and Joel A. Wattenbarger of Ropes & Gray LLP On June 22, 2011, the Securities and Exchange Commission

SEC Adopts Rules to Implement the Private Fund Investment Advisers Registration Act Jason E. Brown and Joel A. Wattenbarger of Ropes & Gray LLP On June 22, 2011, the Securities and Exchange Commission

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.gov Final Rules Regarding Further Defining Swap Dealer, Major Swap

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.gov Final Rules Regarding Further Defining Swap Dealer, Major Swap

U.S. COMMODITY FUTURES TRADING COMMISSION

U.S. COMMODITY FUTURES TRADING COMMISSION Three Lafayette Centre 1155 21st Street, NW, Washington, DC 20581 Telephone: (202) 418-5977 Facsimile: (202) 418-5407 www.cftc.gov Division of Swap Dealer and

U.S. COMMODITY FUTURES TRADING COMMISSION Three Lafayette Centre 1155 21st Street, NW, Washington, DC 20581 Telephone: (202) 418-5977 Facsimile: (202) 418-5407 www.cftc.gov Division of Swap Dealer and

CFTC PROPOSES SPECULATIVE POSITION LIMITS FOR REFERENCED ENERGY CONTRACTS

CLIENT MEMORANDUM CFTC PROPOSES SPECULATIVE POSITION LIMITS FOR REFERENCED ENERGY CONTRACTS The Commodity Futures Trading Commission has proposed Federal speculative position limits on certain natural

CLIENT MEMORANDUM CFTC PROPOSES SPECULATIVE POSITION LIMITS FOR REFERENCED ENERGY CONTRACTS The Commodity Futures Trading Commission has proposed Federal speculative position limits on certain natural

Delaware Insurable Interest Law Developments

OCTOBER 12, 2011 Delaware Insurable Interest Law Developments INSURANCE UPDATE On September 20, 2011, the Delaware Supreme Court (the DE Supreme Court ) issued an opinion interpreting several provisions

OCTOBER 12, 2011 Delaware Insurable Interest Law Developments INSURANCE UPDATE On September 20, 2011, the Delaware Supreme Court (the DE Supreme Court ) issued an opinion interpreting several provisions

Derivatives. Capital Markets

Capital Markets 1 Derivatives (This is a summary of this topic. For more in-depth information, see Regulation of Over-the-Counter Derivatives Under the Dodd-Frank Wall Street Reform and Consumer Protection

Capital Markets 1 Derivatives (This is a summary of this topic. For more in-depth information, see Regulation of Over-the-Counter Derivatives Under the Dodd-Frank Wall Street Reform and Consumer Protection

Client Alert. Overview. Background. The Treasury Determination adds to a growing body of law applicable to foreign exchange derivatives.

Number 1468 February 13, 2013 Client Alert Latham & Watkins Corporate Department Regulation of Foreign Currency Transactions: The Intersection of the Treasury Determination, Swaps Regulation and the Retail

Number 1468 February 13, 2013 Client Alert Latham & Watkins Corporate Department Regulation of Foreign Currency Transactions: The Intersection of the Treasury Determination, Swaps Regulation and the Retail

The Final Municipal Advisor Rule: Navigating the Minefield

Latham & Watkins Financial Institutions Regulatory Practice Number 1614 November 22, 2013 The Final Municipal Advisor Rule: Navigating the Minefield While the final rule narrows the scope and reach of

Latham & Watkins Financial Institutions Regulatory Practice Number 1614 November 22, 2013 The Final Municipal Advisor Rule: Navigating the Minefield While the final rule narrows the scope and reach of

Re: Notice and Request for Comments - Determinations of Foreign Exchange Swaps and Forwards (75 Fed. Reg. 66829)

") ISDA International Swaps and Derivatives Association, Inc. 360 Madison Avenue, 16th Floor New York, NY 10017 United States of America Telephone: 1 (212) 901-6000 Facsimile: 1 (212) 901-6001 email: isda@isda.org

ISDA International Swaps and Derivatives Association, Inc. 360 Madison Avenue, 16th Floor New York, NY 10017 United States of America Telephone: 1 (212) 901-6000 Facsimile: 1 (212) 901-6001 email: isda@isda.org

Registration; Amendments or Updates to Registration

FEBRUARY 7, 2011 INVESTMENT MANAGEMENT UPDATE Registered Investment Adviser Annual Reviews; Calendar of Certain 2011 Significant Dates for Advisers Investment advisers that are registered with the Securities

FEBRUARY 7, 2011 INVESTMENT MANAGEMENT UPDATE Registered Investment Adviser Annual Reviews; Calendar of Certain 2011 Significant Dates for Advisers Investment advisers that are registered with the Securities

The Dodd-Frank Wall Street Reform and Consumer Protection Act: Impact, Issues and Concerns in Implementing the Volcker Rule

July 2010 The Dodd-Frank Wall Street Reform and Consumer Protection Act: Impact, Issues and Concerns in Implementing the Volcker Rule BY KEVIN L. PETRASIC Introduction The Dodd-Frank Wall Street Reform

July 2010 The Dodd-Frank Wall Street Reform and Consumer Protection Act: Impact, Issues and Concerns in Implementing the Volcker Rule BY KEVIN L. PETRASIC Introduction The Dodd-Frank Wall Street Reform

Commodity Futures Trading Commission Proposes Position Limits for Commodity Derivatives

To Our Clients and Friends Memorandum friedfrank.com Commodity Futures Trading Commission Proposes Position Limits for Commodity Derivatives Summary The Commodity Futures Trading Commission (the Commission

To Our Clients and Friends Memorandum friedfrank.com Commodity Futures Trading Commission Proposes Position Limits for Commodity Derivatives Summary The Commodity Futures Trading Commission (the Commission

Commodity Futures Trading Commission. Securities and Exchange Commission. Part II. 17 CFR Part 1

Vol. 77 Monday, No. 156 August 13, 2012 Part II Commodity Futures Trading Commission 17 CFR Part 1 Securities and Exchange Commission 17 CFR Parts 230, 240 and 241 Further Definition of Swap, Security-Based

Vol. 77 Monday, No. 156 August 13, 2012 Part II Commodity Futures Trading Commission 17 CFR Part 1 Securities and Exchange Commission 17 CFR Parts 230, 240 and 241 Further Definition of Swap, Security-Based

PART 75 PROPRIETARY TRADING AND CERTAIN INTERESTS IN AND RELATIONSHIPS WITH COVERED FUNDS.

PART 75 PROPRIETARY TRADING AND CERTAIN INTERESTS IN AND RELATIONSHIPS WITH COVERED FUNDS. SUBPART A Section 1 Section 2 SUBPART B Section 3 Section 4 Section 5 Section 6 Section 7 Section 8 Section 9

PART 75 PROPRIETARY TRADING AND CERTAIN INTERESTS IN AND RELATIONSHIPS WITH COVERED FUNDS. SUBPART A Section 1 Section 2 SUBPART B Section 3 Section 4 Section 5 Section 6 Section 7 Section 8 Section 9

STATEMENT OF THE INVESTMENT COMPANY INSTITUTE ON THE U.S. COMMODITY FUTURES TRADING COMMISSION S APPROPRIATIONS FOR FISCAL YEAR 2016

STATEMENT OF THE INVESTMENT COMPANY INSTITUTE ON THE U.S. COMMODITY FUTURES TRADING COMMISSION S APPROPRIATIONS FOR FISCAL YEAR 2016 Subcommittee on Agriculture, Rural Development, Food and Drug Administration,

STATEMENT OF THE INVESTMENT COMPANY INSTITUTE ON THE U.S. COMMODITY FUTURES TRADING COMMISSION S APPROPRIATIONS FOR FISCAL YEAR 2016 Subcommittee on Agriculture, Rural Development, Food and Drug Administration,

Investment Adviser Annual and Other Compliance Matters

2013 Investment Adviser Annual and Other Compliance Matters This annual memorandum provides clients and friends of Finn Dixon & Herling with brief summaries of selected compliance matters relevant to investment

2013 Investment Adviser Annual and Other Compliance Matters This annual memorandum provides clients and friends of Finn Dixon & Herling with brief summaries of selected compliance matters relevant to investment

FSOC Proposes Rules for Board of Governors of the Federal Reserve s Supervision of Nonbank Financial Companies. October 20, 2011

FSOC Proposes Rules for Board of Governors of the Federal Reserve s Supervision of Nonbank Financial Companies October 20, 2011 On October 11, the Financial Stability Oversight Council (the Council) released

FSOC Proposes Rules for Board of Governors of the Federal Reserve s Supervision of Nonbank Financial Companies October 20, 2011 On October 11, the Financial Stability Oversight Council (the Council) released

Summary of Federal Reserve Proposed Rule on Definitions Related to Nonbank Financial Companies and Interconnectedness of Systemically Important Firms

February 9, 2011 Summary of Federal Reserve Proposed Rule on Definitions Related to Nonbank Financial Companies and Interconnectedness of Systemically Important Firms Yesterday, the Board of Governors

February 9, 2011 Summary of Federal Reserve Proposed Rule on Definitions Related to Nonbank Financial Companies and Interconnectedness of Systemically Important Firms Yesterday, the Board of Governors

February 10, 2014. Melissa D. Jurgens Secretary Commodity Futures Trading Commission Three Lafayette Centre 1155 21 st Street, NW Washington, DC 20581

Melissa D. Jurgens Secretary Commodity Futures Trading Commission Three Lafayette Centre 1155 21 st Street, NW Washington, DC 20581 Re: Aggregation of Positions (RIN 3038-AD82) Dear Ms. Jurgens: The Investment

Melissa D. Jurgens Secretary Commodity Futures Trading Commission Three Lafayette Centre 1155 21 st Street, NW Washington, DC 20581 Re: Aggregation of Positions (RIN 3038-AD82) Dear Ms. Jurgens: The Investment

U.S. DERIVATIVES REFORM (DODD-FRANK ACT, TITLE VII)

") FREQUENTLY ASKED QUESTIONS U.S. DERIVATIVES REFORM (DODD-FRANK ACT, TITLE VII) INTERNAL USE ONLY Comprehensive information for Relationship Managers and other staff of Julius Baer Group September 2015

FREQUENTLY ASKED QUESTIONS U.S. DERIVATIVES REFORM (DODD-FRANK ACT, TITLE VII) INTERNAL USE ONLY Comprehensive information for Relationship Managers and other staff of Julius Baer Group September 2015

THE COMMODITY FUTURES MODERNIZATION ACT OF 2000

THE COMMODITY FUTURES MODERNIZATION ACT OF 2000 SIMPSON THACHER & BARTLETT LLP FEBRUARY 2, 2001 Signed into law by President Clinton on December 21, 2000, the Commodity Futures Modernization Act of 2000

THE COMMODITY FUTURES MODERNIZATION ACT OF 2000 SIMPSON THACHER & BARTLETT LLP FEBRUARY 2, 2001 Signed into law by President Clinton on December 21, 2000, the Commodity Futures Modernization Act of 2000

NO-ACTION RELIEF FOR COMPRESSION EXERCISE SWAPS AND COMPO EQUITY SWAPS COMPRESSION EXERCISE SWAPS. De Minimis Exception Generally

CLIENT UPDATE NO-ACTION RELIEF FOR COMPRESSION EXERCISE SWAPS AND COMPO EQUITY SWAPS NEW YORK Byungkwon Lim blim@debevoise.com Emilie T. Hsu ehsu@debevoise.com Aaron J. Levy ajlevy@debevoise.com On December

CLIENT UPDATE NO-ACTION RELIEF FOR COMPRESSION EXERCISE SWAPS AND COMPO EQUITY SWAPS NEW YORK Byungkwon Lim blim@debevoise.com Emilie T. Hsu ehsu@debevoise.com Aaron J. Levy ajlevy@debevoise.com On December

TITLE 5 BANKING DELAWARE ADMINISTRATIVE CODE

TITLE 5 BANKING 900 Regulations Governing Business of Banks and Trust Companies 1 905 Loan Limitations: Credit Exposure to Derivative Transactions 1.0 Purpose This regulation sets forth the rules for calculating

TITLE 5 BANKING 900 Regulations Governing Business of Banks and Trust Companies 1 905 Loan Limitations: Credit Exposure to Derivative Transactions 1.0 Purpose This regulation sets forth the rules for calculating

Implications for derivatives and hedge accounting under the Dodd-Frank Act

Implications for derivatives and hedge accounting under the Dodd-Frank Act In July 2010, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act 1 (the Act ) to increase government

Implications for derivatives and hedge accounting under the Dodd-Frank Act In July 2010, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act 1 (the Act ) to increase government

NAIC REINSURANCE COLLATERAL REFORM

NAIC REINSURANCE COLLATERAL REFORM BY CHARLENE C. McHUGH After several years of deliberation, on November 6, 2011, the National Association of Insurance Commissioners (NAIC) passed amendments to its Credit

NAIC REINSURANCE COLLATERAL REFORM BY CHARLENE C. McHUGH After several years of deliberation, on November 6, 2011, the National Association of Insurance Commissioners (NAIC) passed amendments to its Credit

STROOCK SPECIAL BULLETIN

STROOCK & STROOCK & LAVAN LLP STROOCK SPECIAL BULLETIN Final Regulations Implementing the Volcker Rule: Proprietary Trading March 21, 2014 I. Introduction On December 10, 2013, in connection with Title

STROOCK & STROOCK & LAVAN LLP STROOCK SPECIAL BULLETIN Final Regulations Implementing the Volcker Rule: Proprietary Trading March 21, 2014 I. Introduction On December 10, 2013, in connection with Title

Reporting Requirements for Foreign Financial Accounts

Reporting Requirements for Foreign Financial Accounts Proposed FinCEN Regulations and IRS Guidance On Foreign Bank and Financial Account Reporting SUMMARY On February 26, the IRS issued Notice 2010-23

Reporting Requirements for Foreign Financial Accounts Proposed FinCEN Regulations and IRS Guidance On Foreign Bank and Financial Account Reporting SUMMARY On February 26, the IRS issued Notice 2010-23

Division of Swap Dealer and Intermediary Oversight

U.S. COMMODITY FUTURES TRADING COMMISSION Three Lafayette Centre 1155 21st Street, NW, Washington, DC 20581 Telephone: (202) 418-6700 Facsimile: (202) 418-5528 gbarnett@cftc.gov Division of Swap Dealer

U.S. COMMODITY FUTURES TRADING COMMISSION Three Lafayette Centre 1155 21st Street, NW, Washington, DC 20581 Telephone: (202) 418-6700 Facsimile: (202) 418-5528 gbarnett@cftc.gov Division of Swap Dealer

Client Alert. The purpose of Form PF is to provide federal regulators with data to aid in monitoring systemic risks to the US financial markets.

Number 1472 February 20, 2013 Client Alert Latham & Watkins Corporate Department Form PF Reference Guide Registered investment advisers who have not previously filed Form PF should be preparing to file

Number 1472 February 20, 2013 Client Alert Latham & Watkins Corporate Department Form PF Reference Guide Registered investment advisers who have not previously filed Form PF should be preparing to file

Agencies Adopt Final Rules Implementing The Volcker Rule; Federal Reserve Board Extends Conformance Period

CLIENT MEMORANDUM Agencies Adopt Final Rules Implementing The Volcker Rule; Federal Reserve Board Extends December 18, 2013 AUTHORS David S. Katz Jack I. Habert Laura P. Gavenman On December 10, 2013,

CLIENT MEMORANDUM Agencies Adopt Final Rules Implementing The Volcker Rule; Federal Reserve Board Extends December 18, 2013 AUTHORS David S. Katz Jack I. Habert Laura P. Gavenman On December 10, 2013,

ENTITY DEFINITIONS UPDATE CFTC and SEC Finalize Key Dodd-Frank Entity Definitions

MAY 11, 2012 ENTITY DEFINITIONS UPDATE CFTC and SEC Finalize Key Dodd-Frank Entity Definitions Background Entity Definitions Title VII of the Dodd-Frank Wall Street Reform and Consumer Protection Act (

MAY 11, 2012 ENTITY DEFINITIONS UPDATE CFTC and SEC Finalize Key Dodd-Frank Entity Definitions Background Entity Definitions Title VII of the Dodd-Frank Wall Street Reform and Consumer Protection Act (

UK OFT Investigation into Health Markets

MARCH 23, 2011 EU LIFE SCIENCES UPDATE UK OFT Investigation into Health Markets Executive Summary On 10 March 2011, the Office of Fair Trading (OFT) formally launched a market study into private healthcare.

MARCH 23, 2011 EU LIFE SCIENCES UPDATE UK OFT Investigation into Health Markets Executive Summary On 10 March 2011, the Office of Fair Trading (OFT) formally launched a market study into private healthcare.

The SEC s New Large Trader Reporting Rule

The SEC s New Large Trader Reporting Rule November 3, 2011 SUMMARY With its recent adoption of Rule 13h-1 (the Rule ) and Form 13H pursuant to Section 13(h) of the Securities Exchange Act of 1934, as amended

The SEC s New Large Trader Reporting Rule November 3, 2011 SUMMARY With its recent adoption of Rule 13h-1 (the Rule ) and Form 13H pursuant to Section 13(h) of the Securities Exchange Act of 1934, as amended

ADVISORY Private Funds

ADVISORY Private Funds BEIJING BRUSSELS LONDON NEW YORK SAN DIEGO SAN FRANCISCO SILICON VALLEY WASHINGTON www.cov.com November 14, 2011 SEC ADOPTS FINAL RULES REQUIRING REPORTING BY PRIVATE FUND ADVISERS

ADVISORY Private Funds BEIJING BRUSSELS LONDON NEW YORK SAN DIEGO SAN FRANCISCO SILICON VALLEY WASHINGTON www.cov.com November 14, 2011 SEC ADOPTS FINAL RULES REQUIRING REPORTING BY PRIVATE FUND ADVISERS

Swap Dealer, Major Swap Participant and Eligible Contract Participant: SEC and CFTC Adopt Entity Definition Rules

DERIVATIVES & STRUCTURED PRODUCTS CLIENT PUBLICATION July 13, 2012... Swap Dealer, Major Swap Participant and Eligible Contract Participant: SEC and CFTC Adopt Entity Definition Rules... The Commodity

DERIVATIVES & STRUCTURED PRODUCTS CLIENT PUBLICATION July 13, 2012... Swap Dealer, Major Swap Participant and Eligible Contract Participant: SEC and CFTC Adopt Entity Definition Rules... The Commodity

SEC Adopts Final Rule Regarding Family Offices

JUNE 29, 2011 INVESTMENT FUNDS UPDATE SEC Adopts Final Rule Regarding Family Offices On June 22, 2011, the Securities and Exchange Commission (the SEC ) adopted investment adviser registration rules and

JUNE 29, 2011 INVESTMENT FUNDS UPDATE SEC Adopts Final Rule Regarding Family Offices On June 22, 2011, the Securities and Exchange Commission (the SEC ) adopted investment adviser registration rules and

August 4, 2014. Position Limits for Derivatives and Aggregation of Positions, 79 Fed. Reg. 30,762 (May 29, 2014).