26 th Voorburg Group Meeting Newport, South Wales September 19 th 23 rd Mini-presentation on

|

|

|

- Shanna Paul

- 8 years ago

- Views:

Transcription

1 26 th Voorburg Group Meeting Newport, South Wales September 19 th 23 rd 2011 Mini-presentation on SPPI for Non-life Insurance Services in the Czech Republic The Czech Statistical Office Jiri Sulc

2 Contents 1. Introduction Definition of the service Pricing unit of measure Market Conditions and Contraints Size of the industry Special condition and restrictions Record keeping practice Structure and detail of standard classification related to the area Evaluation of standard vs. definition and market conditions National accounts concepts Pricing method(s) and criteria for choosing various pricing methods Quality adjustment methodologies Evaluation and comparability with turnover/output measures Summary

and criteria for choosing various pricing methods...14 9. Quality adjustment methodologies...16 10.")

3 1. Introduction This paper provides a brief overview on the development and methodological framework of the Services Producer Price Index for the Non-Life Insurance Services. Since 1991, consumer prices (B2C) for selected representatives have been surveyed (Comprehensive household contents insurance, Comprehensive employee s insurance, Comprehensive juvenile insurance, Motor damage insurance, Motor third-party liability insurance). Monitoring B2B prices for the non-life insurance services did not start until Currently, the Price Statistics Department focuses on both types of prices (business and consumer prices) in its statistical survey. An aggregate B2All index is not counted for the time being. The Czech insurance market is relatively concentrated (measured according to gross premiums written). However, we can see a gradual decrease of market concentration within last years due to growing competition. The structure of this mini-presentation is based on the Content Development Framework of the Voorburg Group. 2. Definition of the service The insurance industry is a specific sector of the economy dealing with insurance, reinsurance and intermediary activities in the field of insurance. This sector ensures the elimination of financial risks affecting people s activities. Insurance and reinsurance companies, insurance providers, the state insurance authority, an insurance association and financial institutions dealing with insurance outside insurance companies (e.g. banks) belong to the institutions related to the insurance industry. Insurance companies can be divided into universal insurance companies (specialized in insurance of all types of risk), life insurance companies (specialized in life insurance), non-life insurance companies (specialized in nonlife insurance) and specialized insurance companies (specialized only in an insurance of certain kind of industry). A captive insurance company is a special type of insurance company. It is the institution founded by some business subject focusing on an insuring of own needs with its own capital and reserves. Next description will be predominantly focused on the non-life insurance. The non-life insurance includes coverage of a wide range of risks of non-life character namely the risks endangering health and human life, the risks evoking direct material damage and financial loss. The outline of segments of non-life insurance can be seen in diagram 1. 2

in its statistical survey. An aggregate B2All index is not counted for the time being.")

4 Diagram 1 Types of non-life insurance services. Services covered by the Czech SPPI and CPI are coloured grey. 3

5 1. Accident insurance includes the payment of indemnification in case an accident results in a temporary or permanent physical damage or death of an insured. 4

6 2. Health insurance (private) an addition to the mandatory general health insurance and social health insurance. 3. Household contest insurance object of insurance is a set of household equipment. Natural hazards, water conduit risks and the risk of theft are included. 4. Buildings insurance object of insurance is a building. Insurance usually covers the natural hazards, water conduit risks, crash of vehicles into building and the risk of theft (part of building). 5. Motor damage insurance covers damage to motor vehicles, whether the driver had no effect or had completely or partially affected damage. It is based on coverage of the damage (in addition it may be coverage of natural hazard risks, theft risks, vandalism risk, etc.). 6. Theft insurance a type of insurance against theft or damage and destruction of property. 7. Natural hazard insurance covers damage to property caused by a certain natural hazard risks (fire, explosion, lightning, windstorm, etc.). 8. Crop insurance covers damage to crop production. The most common type of insurance is the insurance against hail (the most provable) and further those against flood, storm and frost. 9. Livestock insurance covers damages in connection with mortality, culling or emergency slaughter. 10. Motor third-party liability instance protection of victims in traffic accidents. This insurance is mandatory. According to the CPA 2008 the non-life insurance services (code 65.12) are divided into several categories: accident and health insurance services (code ), motor vehicle insurance services (code ), marine, aviation and other transport insurance services (code ), fire and other damage to property insurance services (code ), general liability insurance services (code ), credit and surety ship insurance services (code ), travelling and assistance, legal expenses and miscellaneous financial loss instance services (code ) and other non-life insurance services (code ). Individual categories mentioned above include further service products on the six-digit level (see table 1). Table 1 Structure of Non-life Insurance Services (CPA classification). Services covered by the Czech SPPI and CPI are in bold. CPA Description Accident and health insurance services Motor vehicle insurance services Marine, aviation and other transport insurance services Service Products Accident insurance services Health insurance services Motor vehicle insurance services, third party liability Other motor vehicle insurance services Railway rolling stock insurance services Aircraft liability insurance services 5

7 Fire and other damage to property insurance services General liability insurance services Credit and surety ship insurance services Travelling and assistance, legal expenses and miscellaneous financial loss instance services Other non-life insurance services Other aircraft insurance services Ships liability insurance services Other ships insurance services Freight insurance services Fire damage to property insurance services Other damage to property insurance services General liability insurance services Credit insurance services Surety ship insurance services Travelling and assistance insurance services Legal expenses insurance services Miscellaneous financial loss insurance services Other non-life insurance services In the Ramon Eurostat's Metadata Server (classification CPA 2008), subcategories of the non-life insurance services are described as follows: The code includes underwriting services of insurance policies which provide accidental death and dismemberment insurance, that is, payment in the event that an accident results in death or loss of one or more bodily members (such as hands or feet) or the sight of one or both eyes as well as underwriting services of insurance policies which provide periodic payments when the insured is unable to work as a result of an accident. The code includes underwriting services of insurance policies which provide protection for hospital and medical expenses not covered by government programs and, usually, other health-care expenses such as prescribed drugs, medical appliances, ambulance, private duty nursing, etc. As well underwriting services of insurance policies which provide protection for dental expenses or underwriting services of insurance policies which provide periodic payments when the insured is unable to work as a result of an illness. The code includes underwriting services of insurance policies which cover risks relating to the use of: railway rolling stock Risks covered include liability and loss of or damage to railway rolling stock. The code includes underwriting services of insurance policies of third party liability which cover risks relating to the use of: aircraft - satellite launching liability insurance services The code includes underwriting services of insurance policies, other than for third part liability, which cover risks relating to the use of: 6

, subcategories of the non-life insurance services are described as follows: The code 65.")

8 aircraft - satellite launching insurance (except liability) services The code includes underwriting services of insurance policies of third party liability which cover risks relating to the use of: passenger and freight vessels, whether operating on oceans, coastal waterways or inland waterways The code includes underwriting services of insurance policies, other than for third part liability, which cover risks relating to the use of: passenger and freight vessels, whether operating on oceans, coastal waterways or inland waterways The code includes underwriting services of insurance policies which provide coverage, additional to that provided by transport companies, for risks of damage to or loss of freight The code includes underwriting services of insurance policies which cover all liability arising out of the use of motor vehicles operating on land, including those used to transport paying passengers or freight. The code includes insurance services covering expenses arising from the loss of or damage to motor vehicles operating on land. The code includes underwriting services of insurance policies which cover risks of damage to or loss of property such as theft, explosion, storm, hail, frost, other natural forces, radioactive contamination and land subsidence. As well boiler and machinery insurance, which covers property spoilage from lack of power, light, heat, steam or refrigeration. The code includes underwriting services of insurance policies which cover risks of all types of liability including liability for defective products, bodily injury, property damage, pollution, malpractice, etc., other than liability covered in subcategory (motor vehicle liability insurance services), (marine, aviation and other transport liability insurance services) and (property liability insurance services). The code includes underwriting services of insurance policies which cover risks of excessive credit losses because of debtor insolvency Included are export credits, instalment credits, mortgages, agricultural credits etc. The code includes underwriting services of insurance policies which cover risks of non-performance or failure to satisfy a contractual financial obligation by a party to a contract or agreement. The code includes underwriting services of insurance policies which provide protection for travel related expenses (typically provided in a package), such as: trip cancellation, interruption or delay lost, delayed or damaged luggage accident and health medical expenses repatriation of remains The code includes underwriting services of policies covering legal expenses and litigation costs. The code includes underwriting services of insurance policies which cover risks of miscellaneous financial loss, that is, expenses arising from the following risks: loss of employment, insufficiency of income (general), bad weather, loss of benefits, continuing 7

9 general expenses, unforeseen trading expenses, loss of market value, loss of rent or revenue, indirect trading losses (other than those mentioned above), other financial loss (non-trading) and other forms of loss. As mentioned in the chapter Introduction, indices of non-life insurance services describe development of both business and consumer prices. Concerning the CPI (the consumer price index) services are selected and structured according to the COICOP classification. The CPI covers insurance related to housing, health-related insurance and transportationrelated insurance. In terms of CPA 2008 representatives of services provided consumers mentioned above correspond to CPA sub-categories , and Pricing unit of measure The nature of price representatives (e.g. insurance against theft of movable property - in business), the type of client (e.g. enterpriser) and the pricing method (e.g. direct use of prices of repeated services) are taken into account during the determination of pricing unit of measure. Concerning the non-life insurance services a combination of Model pricing/direct use of prices of repeated services is used as the standard pricing method. More detailed analysis will be introduced in chapter 8 Pricing methods and criteria for choosing of various pricing methods. 4. Market Conditions and Contraints 4.1 Size of the industry In this chapter, the basic characteristics of the insurance market comes from the results stated in the report on Supervision of financial markets of the Czech National Bank and the Annual report of the Czech insurance association. The Czech insurance market comprise of 35 domestic insurers, 16 foreign insurance branches from the EU and one branch of a third-country insurance company (Switzerland). Austrian insurance companies have the largest representation in the Czech insurance market via their branches (five branches). Other branches are from the UK and Germany (three branches each). With the exception of insurance companies and foreign insurance branches mentioned above, EU and EEA insurers and their foreign branches can also operate on Czech insurance market on the basis of the freedom to provide temporary services. In 2009, the total number of insurance companies amounted to 614 and the number of employees was around 14.5 thousand. Large companies cover more than a half of the turnover (gross premiums written) on the insurance market (see graph 1 and 2). Graph 1 Structure of insurance companies (Source: Czech National Bank - Financial Market Supervision Report, 2009) 8

10 The Czech National Bank and the CSO Service Statistics represent sources of information on turnover (gross premiums written). The results of both sources are largely in accord. In 2009, the total value of premiums for the insurance market reached 5.8 billion according to the Czech National Bank. The share of premiums of the life and the non-life insurance is shown in graph 2. Graph 2 The share of life and non-life insurance services (Source: Czech National Bank - Financial Market Supervision Report, 2009) Although the life insurance slightly reported increase in recent years, weight of the non-life insurance is still high. The following table shows a detailed structure of the distribution of non-life insurance turnover (see table 2). 9

Although the life insurance slightly reported increase")

11 Table 2 Gross premiums written by industry insurance (Source: Czech National Bank - Financial Market Supervision Report, 2009) Premiums written by industry insurance CPA 2008 Turnover Bill. % Total non-life insurance Motor third-party liability insurance Damage to property insurance Motor damage insurance General liability insurance Accident and health insurance Other non-life insurance , , , As can be seen in Table 2, Motor third-party liability insurance ( ) and Damage to property insurance ( ) have the most relevant share on the non-life insurance market. Graph 3 The distribution of insurance companies based on gross premiums written (Source: Czech National Bank - Financial Market Supervision Report, 2009 Large insurance companies represent almost 90% of the total sales. However, they are losing on behalf of small and medium insurance companies (see graph 3). 4.2 Special condition and restrictions Prosecution conditions on insurance activities and the list of all insurance types are noted in the Act no. 363/1999, on insurance industry. The licence permission is given by the Czech 10

and Damage to property insurance (65.12.4) have the most relevant share on the non-life insurance market.")

12 National Bank, which is also a supervisor. Insurance activities are freed from a tax without the claim on the tax deduction. 4.3 Record keeping practice Information on prices and turnover in the field of insurance (in this case non-life insurance) is obtained through a monthly statistical reporting form. There are several sections for monitoring both business and consumer prices in the frame of statistical reporting form. Respondents have to fill out insurance premium in Czech crowns and supplementary information on an insurance rate. The insurance rate is expressed in per mill for each proposed representative. The top four insurance companies are surveyed. There is turnover sample coverage of 65% within CPA In such a small number of respondents it is not difficult to achieve a response rate 100%. An overview on a structure of surveyed services, method of data collection, sample methods, number of representatives and number of monthly prices is shown in Table 3. Table 3 Characteristics of collection of prices Surveyed services (according to CPA 2008) Health insurance services Motor vehicle insurance services, third party liability Other motor vehicle insurance services Fire damage to property insurance services Other damage to property insurance services Other non-life insurance services Household contest insurance Property insurance Method of data collection Monthly statistical survey Monthly statistical survey Monthly statistical survey Monthly statistical survey Monthly statistical survey Monthly statistical survey Monthly statistical survey Monthly statistical survey Use Sample method The number of representatives and the reported prices CPI Purposive 2 items 8 prices CPI Purposive 3 items 12 prices SPPI Purposive 7 items 28 prices SPPI, CPI Purposive 12 items 48 prices SPPI, CPI Purposive 12 items 48 prices SPPI Purposive 2 items 8 prices CPI Purposive 2 items 8 prices CPI Purposive 2 items 8 prices 11

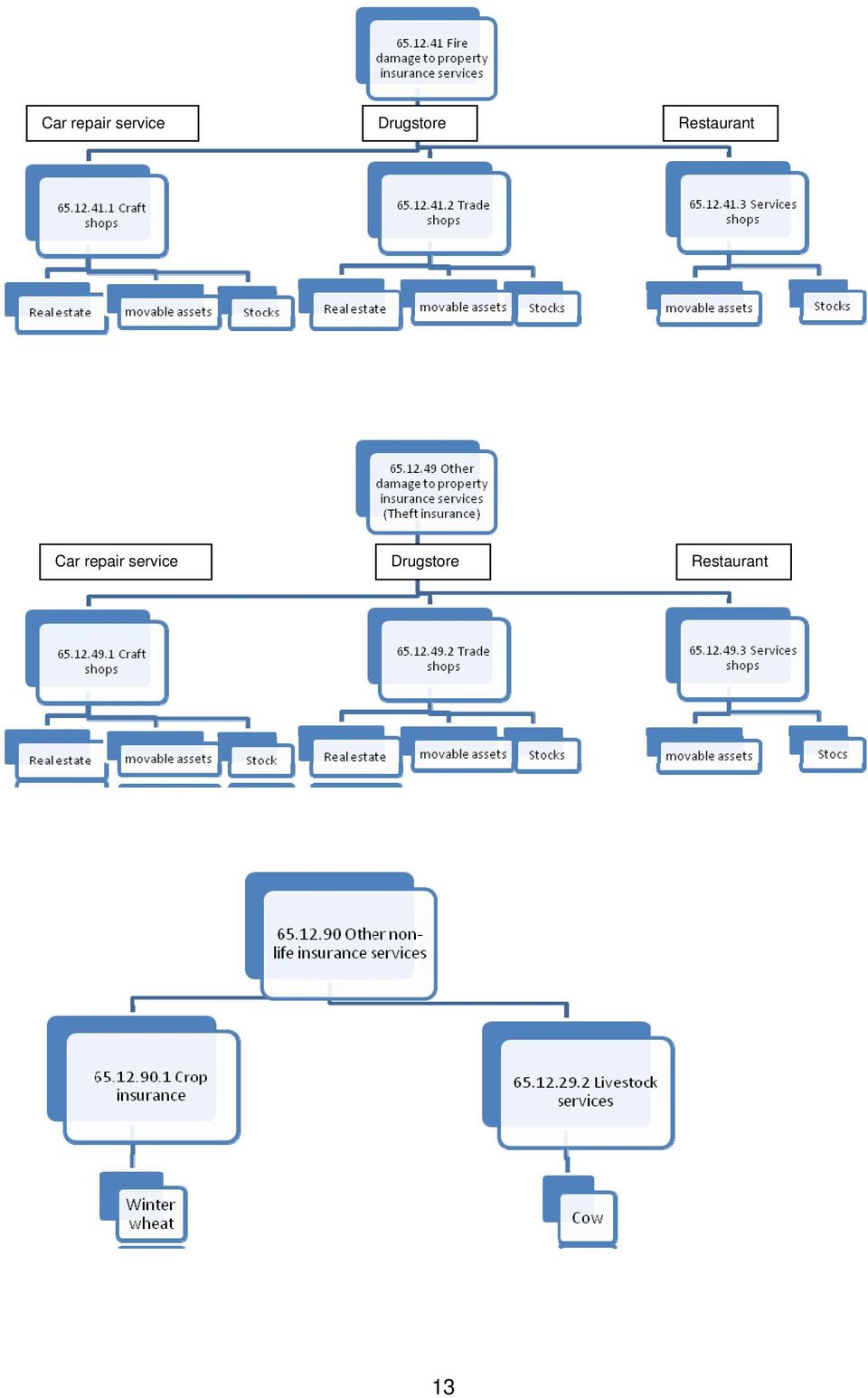

13 5. Structure and detail of standard classification related to the area The structure of the Czech standard industrial classification CZ-NACE and the Czech classification of products by activity CZ-CPA is identical to the NACE Rev. 2 at the 4-digit level and the CPA 2008 at 6-digit level, respectively. There is more detailed classification in the Czech Republic. It is mostly used within statistical surveys. 6. Evaluation of standard vs. definition and market conditions In the Czech Republic, the structure of non-life insurance services (B2B price index) is divided into three main types as follows: Such a classification of insurance segments is not sufficient, hence Price Statistics Sector proposed following more extended structure: 12

is divided into three main types as follows: Such a classification")

14 Car repair service Drugstore Restaurant Car repair service Drugstore Restaurant 13

15 7. National accounts concepts National Accounts use neither the SPPIs nor the CPIs for the insurance sector. Up to now National Accounts has been using an implicit price index for deflation of insurance services. Sources of information are data from the annual company reports and detailed auditing reports. There is a significant difference between the National Accounts Department and Price Statistics Department in terms of way of calculation. Compilation of national accounts for the sector of insurance services is based on production of insurance companies: Production = Gross premiums written - Insurance indemnity costs - Change in technical reserves. While price statistics is based only on gross premiums written. This is a reason why price indices for mentioned industry are insufficient for National Accounts. 8. Pricing method(s) and criteria for choosing various pricing methods The price for providing insurance services is called insurance premium. It is remuneration for provided insurance protection, payment for shifting of the negative financial results of contingency from policyholder to insurer. Amount of insurance premium (current or single) depends on level of risk. Gross premium consists of three components: operating expenses (running of insurance policies and company, liquidation of indemnity), calculated profit and net premium (expenses for indemnity including reserve production). GP = OE + P + NP, where OE.. operating expenses P..calculated profit NP net premium The most often used rating principle is differential net premium, which is determined by specific factors called tariff variables (age, occupation of the insured, property size, etc.). Tariff classes (homogeneous group of insurance contracts for which the insured risk is approximately the same) are created with the help of tariff variables. Consecutive differentiation of the premium using bonuses (premium discounts) or maluses (surcharge to premium) occurs in some cases. The next part of chapter will be focused only on groups of insurance services that are monitored in the Czech statistical office. Among pricing methods which are used to survey prices in insurance sector belongs a method using model pricing and direct use of prices of repeated services. This pricing method has characteristics of both alternatives. Fictitious models are designed to suit all respondents and are also based on the most commonly offered insurance. The disadvantage is that the topicality of selected models must be watched. A. Accident insurance (natural persons only) In accident insurance has been selected type of insurance specializing in insurance benefits for necessary treatment. 14

16 During the reporting of the prices the following basic parameters are taken into account (note that there are 2 representatives by each parameter): - Age of the insured (40 years and 1 year) - Insurance period (30-45 years and years) - Risk group (2nd grade and 1st grade) - Sum insured in case of accidental death ( and 800) - Sum insured in case of permanent disability with a progressive benefit ( 8 000) B. Household contents insurance (natural persons only) The insurance is a set of household equipment against theft, vandalism and complex element. During the reporting of the prices the following basic parameters are taken into account (note that there are 2 representatives by each parameter): - Type of property (flat and family house) - Number of rooms / space flat (3 rooms + 1 kitchen/75 m2 and 2 rooms + 1 kitchen/60 m2) - Location (Prague and a small village) - Level of security (a safety lock) - Value of insured property ( and ) C. Household insurance (permanently occupied household) The subject is insurance against a complex element. During the reporting of the prices the following basic parameters are taken into account (note that there are 2 representatives by each parameter): - Location (Prague and a small village) - Sum insured ( 184,000 and ) - Character of building (first class design and standard design) - Age of building (10 and 5 years) - Area (out of flood area) D. Motor damage insurance (natural persons and entrepreneurs) The subject is insurance against risks of accident, theft and natural disaster to the full amount of the car value. During the reporting of the prices the following basic parameters are taken into account (note that there are 10 representatives by each parameter): - Vehicle type (passenger vehicle and utility vehicle) - Age of the vehicle (only new cars) - Model of the given type of vehicle (the cheapest model in the basic equipment) - Complicity (5%) Change of the premium amount is considered as the price change. Prices exclude VAT. There are not included any surcharges or discounts in the premium amount. The price change can be caused by a change in insurance rates (expressed in per mile) or change in the premium amount (an acquisition price of the vehicle declared by the manufacturer). 15

: - Type of property (flat and family house) - Number")

17 E. Property insurance from the sphere of small and medium risks (entrepreneurs only) E1. Fire insurance During the reporting of the prices the following basic parameters are taken into account (note that there are 3 representatives for every parameter): - Field (car repair service, restaurant, drugstore) - Size of the city (medium size) - Specification of the object (number of floors, floor height, capacity of the building, the character of the perimeter walls, ceilings, roof truss, etc.) - Value of the building itself and its own movable assets and stocks - Complicity ( 200) - Number of employees - Annual income of the company The insurance is contracted for a new price (the purchasing price of new things). Total premium for the selected craft s area includes separately premium for building itself, movable assets and inventories. E2. Theft or robbery insurance During the reporting of the prices the following basic parameters are taken into account (note that there are 3 representatives for every parameter): - Field (car repair service, restaurant, drugstore) - Level of security - Complicity ( 200 on movable assets and stocks) F. Agriculture insurance F1. Crop insurance against hail During the reporting of the prices the following basic parameters are taken into account: - Type of commodities (winter wheat) - Yield of commodities (5t/ha) - Complicity (10%) F2. Animal insurance against the risk of infection During the reporting of the prices the following basic parameters are taken into account: - Type of animal (cow - Czech Pied cattle) - productivity (6000 L / year) - Complicity (10%) G. Motor third-party liability insurance (natural persons only) This insurance is mandatory. Minimal amount limits for personal injury or death are inscribed in the Act. 9. Quality adjustment methodologies Constant contracts and consequential constant quality over time is common practice in the insurance services (principle of model case of representative). The quality of the individual service is determined by the price parameters described in chapter 8. Proposed models are 16

18 mostly set down for longer time period (few months, years). When insurance subject is changed to the new one (e.g. car Škoda Fabia 1.2 to car Škoda Fabia 1.4 ) the quality adjustment methodologies are needed. The change of representative is then obligatory for all respondents. Comparing the new insurance premium to the old one the expert of the responding company is asked for the percentage rate of change (expert estimate). Otherwise, no price changed method is used for linking time series of new price representative. 10. Evaluation and comparability with turnover/output measures Compilation of turnover and output in the short-term business statistics Turnover data for insurance services is not surveyed in the frame of short-term statistics. Compilation of turnover by product Currently the Structural Business Statistics of the CSO collect turnover data on insurance services at service product level, namely accident and health insurance services, motor vehicle insurance services, marine, aviation and other transport insurance services, fire and other damage to property insurance services, general liability insurance services, credit and surety ship insurance services, travelling and assistance, legal expenses and miscellaneous financial loss instance services and other non-life insurance services. 11. Summary Czech statistical office has been developing the SPPI for insurance services (B2B index) since The CPI for insurance services has been already calculated since Premiums are mostly written as standard list tariffs and are surveyed monthly by the top four insurance companies. In insurance services the pricing method used is a combination of model pricing/direct use of prices of repeated services. For this purpose model cases are formulated (the most commonly provided) whose premiums are actual transaction prices which can repeatedly be observed. Insurance services have been divided into three B2B insurance services: Motor vehicle insurance services, Fire and other damage to property insurance services (fire and theft insurance) and Other non-life insurance services (crop and livestock insurance). The aggregated index is calculated as a Laspeyres type Representative services have been selected in close cooperation with Czech insurance association and/or respondents themselves. 17

Service Producer Price Index for Non-Life Insurance

2011 meeting of Voorburg Group Mini-Presentation Service Producer Price Index for Non-Life Insurance September 19 th 23 rd 2011 Newport, South Wales Definition of the sector Insurance industry specific

2011 meeting of Voorburg Group Mini-Presentation Service Producer Price Index for Non-Life Insurance September 19 th 23 rd 2011 Newport, South Wales Definition of the sector Insurance industry specific

ALTERNATE STRUCTURE FOR DIVISION 71

ALTERNATE STRUCTURE FOR DIVISION 71 Division 71 of the Central Product Classification (CPC), Ver.1.1 covers financial services. The structure presented in Part III of this publication has been considered

ALTERNATE STRUCTURE FOR DIVISION 71 Division 71 of the Central Product Classification (CPC), Ver.1.1 covers financial services. The structure presented in Part III of this publication has been considered

CROATIAN FINANCIAL SERVICES SUPERVISORY AGENCY

CROATIAN FINANCIAL SERVICES SUPERVISORY AGENCY Pursuant to the provisions of Article 3 paragraph 5 of the Insurance Act (Official Gazette 151/05, Official Gazette 87/08 and Official Gazette 82/09), the

CROATIAN FINANCIAL SERVICES SUPERVISORY AGENCY Pursuant to the provisions of Article 3 paragraph 5 of the Insurance Act (Official Gazette 151/05, Official Gazette 87/08 and Official Gazette 82/09), the

CEIOPS-DOC-22/09. (former CP27) October 2009. CEIOPS e.v. Westhafenplatz 1-60327 Frankfurt Germany Tel. + 49 69-951119-20

October 2009. CEIOPS e.v. Westhafenplatz 1-60327 Frankfurt Germany Tel. + 49 69-951119-20") CEIOPS-DOC-22/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Technical Provisions - Lines of business on the basis of which (re)insurance obligations are to be segmented (former CP27)

CEIOPS-DOC-22/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Technical Provisions - Lines of business on the basis of which (re)insurance obligations are to be segmented (former CP27)

Solvency II Technical Provisions valuation as at 31st december 2010. submission template instructions

Solvency II Technical Provisions valuation as at 31st december 2010 submission template instructions Introduction As set out in the Guidance Notes for the 2011 Dry Run Review Process, calculation of Technical

Solvency II Technical Provisions valuation as at 31st december 2010 submission template instructions Introduction As set out in the Guidance Notes for the 2011 Dry Run Review Process, calculation of Technical

OECD INSURANCE STATISTICS

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT ORGANISATION DE COOPÉRATION ET DE DÉVELOPPEMENT ÉCONOMIQUES DIRECTION DES AFFAIRES FINANCIÈRES ET DES ENTREPRISES DIRECTORATE FOR FINANCIAL AND ENTERPRISE

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT ORGANISATION DE COOPÉRATION ET DE DÉVELOPPEMENT ÉCONOMIQUES DIRECTION DES AFFAIRES FINANCIÈRES ET DES ENTREPRISES DIRECTORATE FOR FINANCIAL AND ENTERPRISE

INSURANCE. Section 1 TAXABLE INSURANCE CONTRACTS. Taxable Insurance contracts

BULLETIN NO. 061 Issued June 2012 THE RETAIL SALES TAX ACT INSURANCE This bulletin explains the 2012 Budget changes affecting insurance contracts. Effective July 15, 2012, retail sales tax (RST) applies

BULLETIN NO. 061 Issued June 2012 THE RETAIL SALES TAX ACT INSURANCE This bulletin explains the 2012 Budget changes affecting insurance contracts. Effective July 15, 2012, retail sales tax (RST) applies

The 26th Voorburg Group Meeting on Service Statistics Newport, U.K., 19 23 September 2011

The 26th Voorburg Group Meeting on Service Statistics Newport, U.K., 19 23 September 2011 Mini-Presentation by David Friedman United States Producer Price Indexes for Non-Life Insurance NAICS 524114 and

The 26th Voorburg Group Meeting on Service Statistics Newport, U.K., 19 23 September 2011 Mini-Presentation by David Friedman United States Producer Price Indexes for Non-Life Insurance NAICS 524114 and

The Voluntary, Community and Social Enterprise Sector - an insurance guide for individuals and organisations

The Voluntary, Community and Social Enterprise Sector - an insurance guide for individuals and organisations Contents Foreword Introduction 1. Section 1 - Insurance required by law 1.1 Employers liability

The Voluntary, Community and Social Enterprise Sector - an insurance guide for individuals and organisations Contents Foreword Introduction 1. Section 1 - Insurance required by law 1.1 Employers liability

This bulletin explains the application of retail sales tax (RST) to certain insurance contracts that relate to Manitoba, at the rate of 8%.

to certain insurance contracts that relate to Manitoba, at the rate of 8%.") BULLETIN NO. 061 Issued July 15, 2012 Revised July 2013 THE RETAIL SALES TAX ACT INSURANCE This bulletin explains the application of retail sales tax (RST) to certain insurance that relate to Manitoba,

BULLETIN NO. 061 Issued July 15, 2012 Revised July 2013 THE RETAIL SALES TAX ACT INSURANCE This bulletin explains the application of retail sales tax (RST) to certain insurance that relate to Manitoba,

SECTION III. Definitions have been included in these instructions to assist insurers with the preparation of their filings.

SECTION III Definitions have been included in these instructions to assist insurers with the preparation of their filings. This section is not a complete set of insurance and insurance accounting definitions

SECTION III Definitions have been included in these instructions to assist insurers with the preparation of their filings. This section is not a complete set of insurance and insurance accounting definitions

Act No. 9267 date 29.07.2004. On the Activity of Insurance, Reinsurance and Intermediation in Insurance and Reinsurance

Act No. 9267 date 29.07.2004 On the Activity of Insurance, Reinsurance and Intermediation in Insurance and Reinsurance In reliance to articles 78, and 83 part 1 of the Constitution, upon the proposal of

Act No. 9267 date 29.07.2004 On the Activity of Insurance, Reinsurance and Intermediation in Insurance and Reinsurance In reliance to articles 78, and 83 part 1 of the Constitution, upon the proposal of

Chapter 10. Chapter 10 Learning Objectives. Insurance and Risk Management: An Introduction. Property and Motor Vehicle Insurance

Chapter 10 Property and Motor Vehicle Insurance McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 10-1 Chapter 10 Learning Objectives 1. Develop a risk management

Chapter 10 Property and Motor Vehicle Insurance McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 10-1 Chapter 10 Learning Objectives 1. Develop a risk management

INSURANCE INDUSTRY REGULATIONS

I N S U R A N C E I N D U S T R Y R E G U L A T I O N S INSURANCE INDUSTRY REGULATIONS 1 TABLE OF CONTENTS Definitions...3 1. the competent authority...6 2. Insurance Supervisory powers of the MMA...7

I N S U R A N C E I N D U S T R Y R E G U L A T I O N S INSURANCE INDUSTRY REGULATIONS 1 TABLE OF CONTENTS Definitions...3 1. the competent authority...6 2. Insurance Supervisory powers of the MMA...7

LAW ON INSURANCE I BASIC PROVISIONS

On the basis of Article 88, item 2 of the Constitution of the Republic of Montenegro I hereby pass the ENACTMENT PROCLAIMING THE LAW ON INSURANCE (Official Gazette of the Republic of Montenegro, No 78/06

On the basis of Article 88, item 2 of the Constitution of the Republic of Montenegro I hereby pass the ENACTMENT PROCLAIMING THE LAW ON INSURANCE (Official Gazette of the Republic of Montenegro, No 78/06

COMPULSORY INSURANCE IN SERBIA

NATIONAL BANK OF SERBIA Insurance Supervision Department Belgrade, August 2015 COMPULSORY INSURANCE IN SERBIA 1. LAW ON COMPULSORY TRAFFIC INSURANCE (RS Official Gazette, Nos 51/2009, 78/2011, 101/2011,

NATIONAL BANK OF SERBIA Insurance Supervision Department Belgrade, August 2015 COMPULSORY INSURANCE IN SERBIA 1. LAW ON COMPULSORY TRAFFIC INSURANCE (RS Official Gazette, Nos 51/2009, 78/2011, 101/2011,

PROPERTY Fact Finder

PROPERTY Fact Finder In completing this form, please tick the appropriate boxes and answer all questions in BLOCK CAPITALS Important note The information submitted in this form is used by your insurance

PROPERTY Fact Finder In completing this form, please tick the appropriate boxes and answer all questions in BLOCK CAPITALS Important note The information submitted in this form is used by your insurance

BUSINESS INSURANCE FAQ

BUSINESS INSURANCE FAQ Q: What is Business Insurance? A: We strive to understand your risk tolerance and financial ability to withstand the spectrum of potential losses and develop insurance programs to

BUSINESS INSURANCE FAQ Q: What is Business Insurance? A: We strive to understand your risk tolerance and financial ability to withstand the spectrum of potential losses and develop insurance programs to

S C H E D U L E PART G BUSINESS GROUPINGS

S C H E D U L E (Article 4) PART G BUSINESS GROUPINGS In Forms 1 to 58 (Parts A.1 and A.2), a distinction is drawn between Regulatory Groups of Classes and Classes. Inputs are only required in the worksheets

S C H E D U L E (Article 4) PART G BUSINESS GROUPINGS In Forms 1 to 58 (Parts A.1 and A.2), a distinction is drawn between Regulatory Groups of Classes and Classes. Inputs are only required in the worksheets

Residential Landlords Insurance. Policy Summary

Residential Landlords Insurance Policy Summary Amlin Residential Landlords Insurance policy summary This insurance is designed to provide you with a wide range of standard cover in connection with the

Residential Landlords Insurance Policy Summary Amlin Residential Landlords Insurance policy summary This insurance is designed to provide you with a wide range of standard cover in connection with the

ITALIAN INSURANCE IN FIGURES. Year 2015

ITALIAN INSURANCE IN FIGURES Year 2015 The Italian insurance industry gives a significant contribution to the economy and to the society, offering a wide range of services aiming at risk protection: from

ITALIAN INSURANCE IN FIGURES Year 2015 The Italian insurance industry gives a significant contribution to the economy and to the society, offering a wide range of services aiming at risk protection: from

Queensland Government Insurance Fund (QGIF) Insurance Policy (Version 6 - Effective 1 July 2014)

Insurance Policy (Version 6 - Effective 1 July 2014)") Queensland Government Insurance Fund (QGIF) Insurance Policy (Version 6 - Effective 1 July 2014) This policy is for the following Insurances: Section 1 - Property Section 2 - Business Interruption Section

Queensland Government Insurance Fund (QGIF) Insurance Policy (Version 6 - Effective 1 July 2014) This policy is for the following Insurances: Section 1 - Property Section 2 - Business Interruption Section

Serving others around the world. A personal insurance plan for Foreign Missionaries

Serving others around the world. A personal insurance plan for Foreign Missionaries GALLAGHER CHARITABLE Foreign Missionary Insurance Plan A personal insurance plan for you. Gallagher Charitable International

Serving others around the world. A personal insurance plan for Foreign Missionaries GALLAGHER CHARITABLE Foreign Missionary Insurance Plan A personal insurance plan for you. Gallagher Charitable International

M & C General Insurance Company Ltd.

M & C General Insurance Company Ltd. Head Office: 9-11 Bridge Street, P. O. Box 99, Castries St. Lucia, W.I. PUBLIC LIABILITY INSURANCE The substantial awards made nowadays to Third Parties for personal

M & C General Insurance Company Ltd. Head Office: 9-11 Bridge Street, P. O. Box 99, Castries St. Lucia, W.I. PUBLIC LIABILITY INSURANCE The substantial awards made nowadays to Third Parties for personal

Insurance Terms. COMMON TERMS... 3 About Best s Credit Ratings... 3 Agent... 3

Insurance Terms To look up the definitions of commonly used insurance terms click on the term below to move to that section of the document. We hope that you find this information helpful. Our comprehensive

Insurance Terms To look up the definitions of commonly used insurance terms click on the term below to move to that section of the document. We hope that you find this information helpful. Our comprehensive

SECTION III. Definitions have been included in these instructions to assist insurers with the preparation of their filings.

SECTION III Definitions have been included in these instructions to assist insurers with the preparation of their filings. This section is not a complete set of insurance and insurance accounting definitions

SECTION III Definitions have been included in these instructions to assist insurers with the preparation of their filings. This section is not a complete set of insurance and insurance accounting definitions

Insurance Specialists to the building and allied trades

www.tradedirectinsurance.co.uk Insurance Specialists to the building and allied trades Welcome Welcome to Trade Direct Insurance, we hope that you find our brochure informative and that our range of policies

www.tradedirectinsurance.co.uk Insurance Specialists to the building and allied trades Welcome Welcome to Trade Direct Insurance, we hope that you find our brochure informative and that our range of policies

1. INTRODUCTION, PURPOSE AND SCOPE

Solvency Assessment and Management: Pillar I - Sub Committee Technical Provisions Task Group Discussion Document 29 (v 4) Authorisation classes of business under SAM EXECUTIVE SUMMARY SAM is a fundamental

Solvency Assessment and Management: Pillar I - Sub Committee Technical Provisions Task Group Discussion Document 29 (v 4) Authorisation classes of business under SAM EXECUTIVE SUMMARY SAM is a fundamental

Non-Life Insurance in Japan --- Automobile Insurance & Fire Insurance

Non-Life Insurance in Japan --- Automobile Insurance & Fire Insurance CAS Annual Meeting November 18, 2009 Kazuhiro Tanaka, F.I.A.J., Nipponkoa Insurance Co., Ltd. Jun Ikeda, F.I.A.J., Fuji Fire and Marine

Non-Life Insurance in Japan --- Automobile Insurance & Fire Insurance CAS Annual Meeting November 18, 2009 Kazuhiro Tanaka, F.I.A.J., Nipponkoa Insurance Co., Ltd. Jun Ikeda, F.I.A.J., Fuji Fire and Marine

The Danish Insurance Association Gross claims of Danish companies by class of insurance, domestic and international business, 2013

of Danish companies by class of insurance, domestic and international business, 2013 Of which foreign business Industrial injuries insurance 3.068 1.797 603 73 Buildings insurance 5.295 5.059 1.319 543

of Danish companies by class of insurance, domestic and international business, 2013 Of which foreign business Industrial injuries insurance 3.068 1.797 603 73 Buildings insurance 5.295 5.059 1.319 543

Resource 2.7 Introduction to Insurance Cover for Business What insurance is compulsory for businesses? Employers' liability insurance

Page 1 of 5 Introduction to Insurance Cover for Business All businesses need to be insured against risks, such as the theft of equipment or workrelated injury to staff. If you run a small business you

Page 1 of 5 Introduction to Insurance Cover for Business All businesses need to be insured against risks, such as the theft of equipment or workrelated injury to staff. If you run a small business you

BUSINESS PACKAGE PROPOSAL

BUSINESS PACKAGE PROPOSAL RM Insurance Company (PRIVATE) LIMITED RM 317A INDEX SECTION S. PAGES 1 Fire 1 2 Business Interruption 2 3 3 All Risks 3 4 Theft 4 5 Money 4 6 Glass 5 7 Goods in Transit 5 8 Liability

BUSINESS PACKAGE PROPOSAL RM Insurance Company (PRIVATE) LIMITED RM 317A INDEX SECTION S. PAGES 1 Fire 1 2 Business Interruption 2 3 3 All Risks 3 4 Theft 4 5 Money 4 6 Glass 5 7 Goods in Transit 5 8 Liability

What you should insure and what s included in our insurance

GUIDE TO INSURANCE What you should insure and what s included in our insurance CONTENTS Contents 1 GENERAL RESPONSIBILITIES 3 1.1 Introduction 3 1.2 The types of insurance 3 1.3 The general principles

GUIDE TO INSURANCE What you should insure and what s included in our insurance CONTENTS Contents 1 GENERAL RESPONSIBILITIES 3 1.1 Introduction 3 1.2 The types of insurance 3 1.3 The general principles

INSURANCE APPORTIONMENT SCHEDULE

INSURANCE APPORTIONMENT SCHEDULE Class of insurance Aviation Hull, Aviation Hull Third Party Property Liability and Aviation Hull Personal Liability Where the aircraft, the subject of the insurance, is

INSURANCE APPORTIONMENT SCHEDULE Class of insurance Aviation Hull, Aviation Hull Third Party Property Liability and Aviation Hull Personal Liability Where the aircraft, the subject of the insurance, is

AMP Agriplan. All about protecting your livelihood

AMP Agriplan All about protecting your livelihood 2 This brochure summarises some of the cover provided by AMP s Agriplan policy. It is important to note that terms, conditions and exclusions apply to

AMP Agriplan All about protecting your livelihood 2 This brochure summarises some of the cover provided by AMP s Agriplan policy. It is important to note that terms, conditions and exclusions apply to

RESIDENTIAL PROPERTY OWNERS INSURANCE POLICY SUMMARY

RESIDENTIAL PROPERTY OWNERS INSURANCE POLICY SUMMARY RESIDENTIAL PROPERTY OWNERS INSURANCE POLICY SUMMARY This document is a summary of your Policy and other key information about the insurance cover that

RESIDENTIAL PROPERTY OWNERS INSURANCE POLICY SUMMARY RESIDENTIAL PROPERTY OWNERS INSURANCE POLICY SUMMARY This document is a summary of your Policy and other key information about the insurance cover that

INSURANCE POLICY FOR FREELANCE JOURNALISTS AND PHOTOGRAPHERS ON ASSIGNMENT

INSURANCE POLICY FOR FREELANCE JOURNALISTS AND PHOTOGRAPHERS ON ASSIGNMENT Because of the risks involved in the job of informing the public, Reporters Without Borders and the French insurance company Bellini

INSURANCE POLICY FOR FREELANCE JOURNALISTS AND PHOTOGRAPHERS ON ASSIGNMENT Because of the risks involved in the job of informing the public, Reporters Without Borders and the French insurance company Bellini

Insurance Boot Camp. Understanding Coverages for Your School Division, Staff and Students

Insurance Boot Camp Understanding Coverages for Your School Division, Staff and Students VASBO Fall Conference Continuing Education October 15, 2015 1:00 p.m. Presented by David Brooks Lee Brannon and

Insurance Boot Camp Understanding Coverages for Your School Division, Staff and Students VASBO Fall Conference Continuing Education October 15, 2015 1:00 p.m. Presented by David Brooks Lee Brannon and

OPTIMA TRADE PLUS SUMMARY OF COVER

ABC OPTIMA TRADE PLUS SUMMARY OF COVER This document provides a guide to the cover provided. It is however only a summary of the terms of cover and does not contain full details of the insurance policy

ABC OPTIMA TRADE PLUS SUMMARY OF COVER This document provides a guide to the cover provided. It is however only a summary of the terms of cover and does not contain full details of the insurance policy

Gouda Expatriate Policy Coverage overview

770311(sep2008)a Gouda Expatriate Policy Coverage overview Gouda Expatriate Policy Coverage overview  1. gouda service package In order to make your stay abroad a pleasant and safe one the Gouda Service

770311(sep2008)a Gouda Expatriate Policy Coverage overview Gouda Expatriate Policy Coverage overview  1. gouda service package In order to make your stay abroad a pleasant and safe one the Gouda Service

The Cover. Additional Increase in Cost of Working. BIGRNP(SI)_7 Ace Package Policy 2013 ix.12

_7 Ace Package Policy 2013 ix.12") Section 2 - Business Interruption Fire and Specified Perils If any building or other property used by the Insured at the Premises for the purpose of the Business is lost, destroyed or damaged by any Specified

Section 2 - Business Interruption Fire and Specified Perils If any building or other property used by the Insured at the Premises for the purpose of the Business is lost, destroyed or damaged by any Specified

SIFA GmbH Swiss Insurance & Financial Advisors

SIFA GmbH Swiss Insurance & Financial Advisors LIVING IN SWITZERLAND WITH ADEQUATE INSURANCE 2015 This brief guide is intended to help you understand the basics of insurance in Switzerland Directory 1.

SIFA GmbH Swiss Insurance & Financial Advisors LIVING IN SWITZERLAND WITH ADEQUATE INSURANCE 2015 This brief guide is intended to help you understand the basics of insurance in Switzerland Directory 1.

Business Income With Extra Expense

Business Income With Extra Expense Table of Contents Section Page No. Premises Coverages 3 Additional Coverages 5 Limits Of Insurance 11 Waiting Period 11 Loss Determination 11 Loss Payment Option 12 Loss

Business Income With Extra Expense Table of Contents Section Page No. Premises Coverages 3 Additional Coverages 5 Limits Of Insurance 11 Waiting Period 11 Loss Determination 11 Loss Payment Option 12 Loss

An introduction to insurance cover for businesses

An introduction to insurance cover for businesses All businesses need to be insured against potential risks such as contractual disputes, accidental damage, fire, flood or theft and claims for negligence.

An introduction to insurance cover for businesses All businesses need to be insured against potential risks such as contractual disputes, accidental damage, fire, flood or theft and claims for negligence.

Webinar on Insurance Coverages

Webinar on Insurance Coverages Property and Casualty Insurance Presenter David M. Pooser, Ph.D. Assistant Professor of Risk Management & Insurance St. John s University Moderator Frank Tomasello Program

Webinar on Insurance Coverages Property and Casualty Insurance Presenter David M. Pooser, Ph.D. Assistant Professor of Risk Management & Insurance St. John s University Moderator Frank Tomasello Program

An insurance package suitable for small to medium sized businesses in the construction industry with a:-

Contractors Choice Summary of Cover An insurance package suitable for small to medium sized businesses in the construction industry with a:- Turnover up to 1.5m at new business and 2m at renewal Maximum

Contractors Choice Summary of Cover An insurance package suitable for small to medium sized businesses in the construction industry with a:- Turnover up to 1.5m at new business and 2m at renewal Maximum

Insurance Tax Act 1. Section 1 Tax basis

Insurance Tax Act 1 Date of signature: 8 April 1922 Full citation: Insurance Tax Act as published on 10 January 1996 (Federal Law Gazette I, p. 22), most recently amended by Article 1 of the Act of 5 December

Insurance Tax Act 1 Date of signature: 8 April 1922 Full citation: Insurance Tax Act as published on 10 January 1996 (Federal Law Gazette I, p. 22), most recently amended by Article 1 of the Act of 5 December

Types of Insurance

Outline of Optional Insurance This guideline describes optional insurance according to the condition of SPECIAL REGULATIONS No. 8 concerning insurance (hereinafter "SPECIAL REGULATIONS"): (1) Major optional

Outline of Optional Insurance This guideline describes optional insurance according to the condition of SPECIAL REGULATIONS No. 8 concerning insurance (hereinafter "SPECIAL REGULATIONS"): (1) Major optional

Daiichi Nippon Bank started marine underwriting. The first marine insurance company in Japan was granted an operating license.

XIII Chronology Year 1859 1867 1869 1873 1877 1878 1879 1883 1887 1888 1893 1895 1898 1899 1900 1904 1907 1910 1911 1914 Non-life insurance business was started in Yokohama by a foreign insurance company.

XIII Chronology Year 1859 1867 1869 1873 1877 1878 1879 1883 1887 1888 1893 1895 1898 1899 1900 1904 1907 1910 1911 1914 Non-life insurance business was started in Yokohama by a foreign insurance company.

Motor Fleet. Policy Summary. coveainsurance.co.uk. Registration and Regulatory Information

Motor Fleet Policy Summary Motor Fleet insurance is for companies, sole traders or partnerships operating a fleet of 3 to 25 vehicles comprising of cars and commercial vehicles used for the business of

Motor Fleet Policy Summary Motor Fleet insurance is for companies, sole traders or partnerships operating a fleet of 3 to 25 vehicles comprising of cars and commercial vehicles used for the business of

COMMERCIAL INSURANCE POLICY

COMMERCIAL INSURANCE POLICY Today s business owner is faced with a broad array and multitude of risks on a day to day basis, both insurable and uninsurable. The control and management of these risks is

COMMERCIAL INSURANCE POLICY Today s business owner is faced with a broad array and multitude of risks on a day to day basis, both insurable and uninsurable. The control and management of these risks is

OFFICE POLICY SUMMARY

Of OFFICE POLICY SUMMARY This is a summary of the standard cover available under the UK General Office Policy. The summary does not include all the policy benefits, limits and exclusions; full terms and

Of OFFICE POLICY SUMMARY This is a summary of the standard cover available under the UK General Office Policy. The summary does not include all the policy benefits, limits and exclusions; full terms and

Gross Earned Contribution Revenue and Insurance Expense

Reporting Form DRF 310.1 Gross Earned Contribution Revenue and Insurance Expense Instruction Guide Introduction This form requires Discretionary Mutual Funds (DMFs) to disclose information about its gross

Reporting Form DRF 310.1 Gross Earned Contribution Revenue and Insurance Expense Instruction Guide Introduction This form requires Discretionary Mutual Funds (DMFs) to disclose information about its gross

UK INSURANCE KEY FACTS 2014. UK Insurance KEY FACTS. Follow us on Twitter @BritishInsurers

UK INSURANCE KEY FACTS 2014 UK Insurance KEY FACTS 2014 3 @BritishInsurers Follow us on Twitter @BritishInsurers ASSOCIATION OF BRITISH INSURERS About the ABI The Association of British Insurers is the

UK INSURANCE KEY FACTS 2014 UK Insurance KEY FACTS 2014 3 @BritishInsurers Follow us on Twitter @BritishInsurers ASSOCIATION OF BRITISH INSURERS About the ABI The Association of British Insurers is the

KANSAS MUTUAL INSURANCE COMPANY FARM PROTECTOR PROGRAM General Index

General Index Page Section Number Rate Page ADDITIONAL AND SECONDARY LOCATIONS 27 14 31 Additional Interests 12 6.4 Additional Living Expense 23 12.2 33 Additional Residence Premises -- Rented To Others

General Index Page Section Number Rate Page ADDITIONAL AND SECONDARY LOCATIONS 27 14 31 Additional Interests 12 6.4 Additional Living Expense 23 12.2 33 Additional Residence Premises -- Rented To Others

PLEASE NOTE. For more information concerning the history of these regulations, please see the Table of Regulations.

PLEASE NOTE This document, prepared by the Legislative Counsel Office, is an office consolidation of this regulation, current to February 1, 2004. It is intended for information and reference purposes

PLEASE NOTE This document, prepared by the Legislative Counsel Office, is an office consolidation of this regulation, current to February 1, 2004. It is intended for information and reference purposes

Commercial Insurance. www.infarmbureau.com

Commercial Insurance www.infarmbureau.com Is your business properly insured? Don t wait until it s too late! Commercial Package Policy (CPP) Used by many classes of businesses manufacturers, restaurants,

Commercial Insurance www.infarmbureau.com Is your business properly insured? Don t wait until it s too late! Commercial Package Policy (CPP) Used by many classes of businesses manufacturers, restaurants,

SME BUSINESS INSURANCE MADE SIMPLE

SME BUSINESS INSURANCE MADE SIMPLE Working with the profession to simplify the language of insurance PUTTING INSURANCE TO WORK Business insurance is about protecting your livelihood. For SMEs in particular,

SME BUSINESS INSURANCE MADE SIMPLE Working with the profession to simplify the language of insurance PUTTING INSURANCE TO WORK Business insurance is about protecting your livelihood. For SMEs in particular,

CAMBERFORD LAW PLC. RECRUITMENT AGENCY and EMPLOYMENT BUSINESS INSURANCE PROPOSAL FORM

CAMBERFORD LAW PLC RECRUITMENT AGENCY and EMPLOYMENT BUSINESS INSURANCE PROPOSAL FORM Please note that 'You' or 'Your' in the context of this Enquiry Form means the persons named as Proposer and/or any

CAMBERFORD LAW PLC RECRUITMENT AGENCY and EMPLOYMENT BUSINESS INSURANCE PROPOSAL FORM Please note that 'You' or 'Your' in the context of this Enquiry Form means the persons named as Proposer and/or any

practical problems. life) property) 11) Health Care Insurance. 12) Medical care insurance.

property) 11) Health Care Insurance. 12) Medical care insurance.") Training Courses Busisness Soluation For The Insurance Services Industry First: Professional Insurance Programs 1) Fundamental of Risk &Insurance. 2) Individual life Insurance Policies. 3) Group life Insurance

Training Courses Busisness Soluation For The Insurance Services Industry First: Professional Insurance Programs 1) Fundamental of Risk &Insurance. 2) Individual life Insurance Policies. 3) Group life Insurance

Business Income With Extra Expense And Research And Development Income Coverage

Business Income With Extra Expense Table of Contents Section Page No. Premises Coverages 3 Additional Coverages 6 Limits Of Insurance 12 Waiting Period 12 Loss Determination 12 Duration Of Loss Research

Business Income With Extra Expense Table of Contents Section Page No. Premises Coverages 3 Additional Coverages 6 Limits Of Insurance 12 Waiting Period 12 Loss Determination 12 Duration Of Loss Research

Regulations relating to the guarantee scheme for non-life insurance

FINANSTILSYNET Norway Translation as of May 2010 This translation is for information purposes only. Legal authenticity remains with the official Norwegian version as published in Norsk Lovtidend. Regulations

FINANSTILSYNET Norway Translation as of May 2010 This translation is for information purposes only. Legal authenticity remains with the official Norwegian version as published in Norsk Lovtidend. Regulations

Insurance. for your small. business

Insurance for your small business @BritishInsurers As an employer, you are legally required to have Employers Liability Insurance. If you use motor vehicles for your business, you are legally required

Insurance for your small business @BritishInsurers As an employer, you are legally required to have Employers Liability Insurance. If you use motor vehicles for your business, you are legally required

Summary of Cover Commercial Retail Policy

Summary of Cover Commercial Retail Policy The information provided in this policy summary is key information you should read. This policy summary does not contain the full terms and conditions of the cover,

Summary of Cover Commercial Retail Policy The information provided in this policy summary is key information you should read. This policy summary does not contain the full terms and conditions of the cover,

insure2drive Private Car and Small Commercial Vehicle Policy Summary

insure2drive Private Car and Small Commercial Vehicle Policy Summary insure2drive is a trading name of Sabre Insurance Company Limited. Any reference to insure2drive in this document will mean Sabre Insurance

insure2drive Private Car and Small Commercial Vehicle Policy Summary insure2drive is a trading name of Sabre Insurance Company Limited. Any reference to insure2drive in this document will mean Sabre Insurance

How To Be Safe In A Fieldwork

SUBJECT: FIELD WORK SAFETY UNIVERSITY OF NORTHERN BRITISH COLUMBIA Policies and Procedures 1. Purpose The University recognizes its obligations to take all reasonable precautions to protect the safety

SUBJECT: FIELD WORK SAFETY UNIVERSITY OF NORTHERN BRITISH COLUMBIA Policies and Procedures 1. Purpose The University recognizes its obligations to take all reasonable precautions to protect the safety

Adviceguide Advice that makes a difference

Buildings insurance What is buildings insurance Buildings insurance covers the cost of damage to the structure of your property. This includes the roof, walls, ceilings, floors, doors and windows. Outdoor

Buildings insurance What is buildings insurance Buildings insurance covers the cost of damage to the structure of your property. This includes the roof, walls, ceilings, floors, doors and windows. Outdoor

Arkansas. Insurance Department AUTOMOBILE INSURANCE. Mike Beebe Governor. Jay Bradford Commissioner

Arkansas Insurance Department AUTOMOBILE INSURANCE Mike Beebe Governor Jay Bradford Commissioner A Message From The Commissioner The Arkansas Insurance Department takes very seriously its mission of consumer

Arkansas Insurance Department AUTOMOBILE INSURANCE Mike Beebe Governor Jay Bradford Commissioner A Message From The Commissioner The Arkansas Insurance Department takes very seriously its mission of consumer

The Tradesmen policy is available for self employed persons and small businesses with up to 8 people and a turnover of 500,000 or less.

TRADESMEN Summary of Cover The Tradesmen policy is available for self employed persons and small businesses with up to 8 people and a turnover of 500,000 or less. Why choose AXA s Tradesmen policy? Tailor-made

TRADESMEN Summary of Cover The Tradesmen policy is available for self employed persons and small businesses with up to 8 people and a turnover of 500,000 or less. Why choose AXA s Tradesmen policy? Tailor-made

Aviva Insurance Limited

Annual FSA Insurance Returns for the ended st December (Appendices 9.1, 9.2, 9.5, 9.6) Produced using BestESP Services - UK Year ended st December Contents Page Appendix 9.1 Form 1 Statement of solvency

Annual FSA Insurance Returns for the ended st December (Appendices 9.1, 9.2, 9.5, 9.6) Produced using BestESP Services - UK Year ended st December Contents Page Appendix 9.1 Form 1 Statement of solvency

Our Insurance services. Where to find

Head Office 117 Camberwell Road Hawthorn East VIC 3123 PO Box 338 Camberwell VIC 3124 Branch Office 687 Mt Alexander Road Moonee Ponds VIC 3039 PO Box 210 Moonee Ponds VIC 3039 victeach.com.au 1300 654

Head Office 117 Camberwell Road Hawthorn East VIC 3123 PO Box 338 Camberwell VIC 3124 Branch Office 687 Mt Alexander Road Moonee Ponds VIC 3039 PO Box 210 Moonee Ponds VIC 3039 victeach.com.au 1300 654

Includes office contents, furniture, fixtures, teaching and other equipment

This summary is intended as a simple guide to explain the main types (or classes) of insurance cover available to academies. We have included brief descriptions of the cover together with suggestions about

This summary is intended as a simple guide to explain the main types (or classes) of insurance cover available to academies. We have included brief descriptions of the cover together with suggestions about

The Professionals policy is available for small businesses with up to 8 people and a turnover of 500,000 or less.

PROFESSIONALS Summary of Cover The Professionals policy is available for small businesses with up to 8 people and a turnover of 500,000 or less. Why choose AXA s Professionals policy? Tailor-made for your

PROFESSIONALS Summary of Cover The Professionals policy is available for small businesses with up to 8 people and a turnover of 500,000 or less. Why choose AXA s Professionals policy? Tailor-made for your

Van Insurance Summary of cover

Van Insurance Summary of cover About this document This document is a summary of the insurance provided by our Van insurance policy. Therefore it does not contain the full terms and conditions of your

Van Insurance Summary of cover About this document This document is a summary of the insurance provided by our Van insurance policy. Therefore it does not contain the full terms and conditions of your

Business Insurance Application

Business Insurance Application Office Use Only Core Customer Segment: Account Number: Policy Number: Important Notices Duty of Disclosure Before you enter into a contract of insurance with Ansvar Insurance

Business Insurance Application Office Use Only Core Customer Segment: Account Number: Policy Number: Important Notices Duty of Disclosure Before you enter into a contract of insurance with Ansvar Insurance

Renters Insurance. When you want to leave nothing to chance.

Renters Insurance When you want to leave nothing to chance. Property Coverage The Renters Policy protects your possessions in the event of: Fire Lightning Windstorm Hail Explosion Riot Aircraft Damage

Renters Insurance When you want to leave nothing to chance. Property Coverage The Renters Policy protects your possessions in the event of: Fire Lightning Windstorm Hail Explosion Riot Aircraft Damage

How To Cover Your Business Insurance In New Zealand

Business Insurance Cover Information for business owners IMPORTANT NOTE This brochure summarises some of the cover provided by AMP s Business Insurance policy. It is important to note that limits, excesses,

Business Insurance Cover Information for business owners IMPORTANT NOTE This brochure summarises some of the cover provided by AMP s Business Insurance policy. It is important to note that limits, excesses,

Spiralling Costs of Insurance in Ireland

Spiralling Costs of Insurance in Ireland Presented to the Society of Actuaries in Ireland Dermot O Hara FSAI David Costello FSAI November 2002 Note The opinions contained in this paper are expressed in

Spiralling Costs of Insurance in Ireland Presented to the Society of Actuaries in Ireland Dermot O Hara FSAI David Costello FSAI November 2002 Note The opinions contained in this paper are expressed in

KANSAS MUTUAL INSURANCE COMPANY DELUXE HOMEOWNERS PROGRAM. General Index Page

General Index Page Rule No. ACV Roofing Additional Amount or Coverages Additional Insureds Additional Living Expense--Increased Limit Additional Residences (1) Occupied by Insured (2) Rented to Others

General Index Page Rule No. ACV Roofing Additional Amount or Coverages Additional Insureds Additional Living Expense--Increased Limit Additional Residences (1) Occupied by Insured (2) Rented to Others

Legal & General Insurance Limited

Annual PRA Insurance Returns for the ended 31 December 2014 IPRU(INS) Appendices 9.1, 9.2, 9.5, 9.6 Balance Sheet and Profit and Loss Account Contents Form 1 Statement of solvency - general insurance

Annual PRA Insurance Returns for the ended 31 December 2014 IPRU(INS) Appendices 9.1, 9.2, 9.5, 9.6 Balance Sheet and Profit and Loss Account Contents Form 1 Statement of solvency - general insurance

policy summary document tradesmen insurance

policy summary document tradesmen insurance The Tradesmen policy is available for self employed persons and small businesses with up to 8 people and a turnover of _750,000 or less Why choose AXA s Tradesmen

policy summary document tradesmen insurance The Tradesmen policy is available for self employed persons and small businesses with up to 8 people and a turnover of _750,000 or less Why choose AXA s Tradesmen

protect your business with insurance you can trust.

protect your business with insurance you can trust. Transact Credit Invest Insure Forex Merchant Services Cash Value Adds Rewards First National Bank - a division of FirstRand Bank Limited. An Authorised

protect your business with insurance you can trust. Transact Credit Invest Insure Forex Merchant Services Cash Value Adds Rewards First National Bank - a division of FirstRand Bank Limited. An Authorised

Gearing up for safety/

STRADA COMPACT motor vehicle insurance Gearing up for safety/ STRADA COMPACT means straightforward motor vehicle insurance designed for anyone seeking a solid package of benefits with their liability,

STRADA COMPACT motor vehicle insurance Gearing up for safety/ STRADA COMPACT means straightforward motor vehicle insurance designed for anyone seeking a solid package of benefits with their liability,

TOWNSHIP OFFICIALS OF ILLINOIS RISK MANAGEMENT ASSOCIATION

TOWNSHIP OFFICIALS OF ILLINOIS RISK MANAGEMENT ASSOCIATION TOIRMA SUMMARY OF COVERAGES as of 6/1/2014 I. PROPERTY COVERAGES A. BUILDINGS AND CONTENTS Covers all the real and personal property owned by

TOWNSHIP OFFICIALS OF ILLINOIS RISK MANAGEMENT ASSOCIATION TOIRMA SUMMARY OF COVERAGES as of 6/1/2014 I. PROPERTY COVERAGES A. BUILDINGS AND CONTENTS Covers all the real and personal property owned by

The Great American Trucking Story

Trucking Division The Great American Trucking Story In recent years, a number of top motor carriers leaders in the trucking industry have chosen to offer Great American s insurance products to the independent

Trucking Division The Great American Trucking Story In recent years, a number of top motor carriers leaders in the trucking industry have chosen to offer Great American s insurance products to the independent

Businessowners Coverage

Businessowners Coverage BUILDING AND/OR BUSINESS PERSONAL PROPERTY COVERAGES Buildings Covers your described building, outdoor fixtures (e.g., light poles and flag poles), building glass, permanently installed

Businessowners Coverage BUILDING AND/OR BUSINESS PERSONAL PROPERTY COVERAGES Buildings Covers your described building, outdoor fixtures (e.g., light poles and flag poles), building glass, permanently installed

Insurance Coverage Explained

Insurance Coverage Explained April 2012 Content Overview... 3 Travel Insurance... 3 Car Insurance in China... 3 Standard Insurance... 3 Third-Party Liability Insurance... 4 Vehicle Damage or Theft... 4

Insurance Coverage Explained April 2012 Content Overview... 3 Travel Insurance... 3 Car Insurance in China... 3 Standard Insurance... 3 Third-Party Liability Insurance... 4 Vehicle Damage or Theft... 4

SHIPOWNER'S PROTECTION AND INDEMNITY RULES

SHIPOWNER'S PROTECTION AND INDEMNITY RULES 1. GENERAL STIPULATIONS. 1.1. Investflot Insurance Company (the Insurer), on the terms of the present Rules, insures shipowner's liability for damage incurred

SHIPOWNER'S PROTECTION AND INDEMNITY RULES 1. GENERAL STIPULATIONS. 1.1. Investflot Insurance Company (the Insurer), on the terms of the present Rules, insures shipowner's liability for damage incurred

REPORT COMPLIANCE EVALUATION

REPORT COMPLIANCE EVALUATION The European Council Directive 73/239 EEC on Coordination of Non Life Insurance Laws, Regulations and Administrative Provisions December 2007 This report is designed to evaluate

REPORT COMPLIANCE EVALUATION The European Council Directive 73/239 EEC on Coordination of Non Life Insurance Laws, Regulations and Administrative Provisions December 2007 This report is designed to evaluate

CHAPTER 28 Insurance

CHAPTER 28 Insurance Chapter Objectives After studying this chapter, you will be able to describe types of automobile insurance coverage. explain the importance of health insurance as a fringe benefit

CHAPTER 28 Insurance Chapter Objectives After studying this chapter, you will be able to describe types of automobile insurance coverage. explain the importance of health insurance as a fringe benefit

United Arab Emirates

The United Arab Emirates is a federal state composed of seven emirates including Abu Dhabi and Dubai. The federation came into effect in 1971, but each emirate maintains a varying degree of control over

The United Arab Emirates is a federal state composed of seven emirates including Abu Dhabi and Dubai. The federation came into effect in 1971, but each emirate maintains a varying degree of control over

Construction Project All Risks

Allianz Insurance plc Construction Project All Risks Product Information This information is for intermediaries only Construction Project All Risks Insurance Policy Wherever there is the construction of

Allianz Insurance plc Construction Project All Risks Product Information This information is for intermediaries only Construction Project All Risks Insurance Policy Wherever there is the construction of

Car Insurance Policy Summary

Car Insurance Policy Summary This policy summary outlines your car insurance cover, please read this carefully. It does not give details of all of the policy limits, terms, conditions and exclusions. For

Car Insurance Policy Summary This policy summary outlines your car insurance cover, please read this carefully. It does not give details of all of the policy limits, terms, conditions and exclusions. For

Your policy summary Buy to Let

Buildings and contents insurance for landlords Your policy summary Buy to Let February 2014 edition Contents How much cover do I need? 3 Features and benefits 4 Policy summary 6 Features and benefits 7

Buildings and contents insurance for landlords Your policy summary Buy to Let February 2014 edition Contents How much cover do I need? 3 Features and benefits 4 Policy summary 6 Features and benefits 7

VIRGINIA LICENSE TYPES AS EFFECTIVE 9/1/02 TITLE 38.2, CHAPTER 18, CODE OF VIRGINIA CONVERSION TABLE

VIRGINIA LICENSE TYPES AS EFFECTIVE 9/1/02 TITLE 38.2, CHAPTER 18, CODE OF VIRGINIA CONVERSION TABLE CURRENT LICENSE CODE NEW LICENSE EFFECTIVE 9/1/02 CODE Life & Health 001 Life & Annuities Health Those

VIRGINIA LICENSE TYPES AS EFFECTIVE 9/1/02 TITLE 38.2, CHAPTER 18, CODE OF VIRGINIA CONVERSION TABLE CURRENT LICENSE CODE NEW LICENSE EFFECTIVE 9/1/02 CODE Life & Health 001 Life & Annuities Health Those

Insurance that protects you and lowers your costs

Insurance that protects you and lowers your costs Information prior to and after purchase This is a brief description of the policy. You can find full details in the policy terms and conditions, which

Insurance that protects you and lowers your costs Information prior to and after purchase This is a brief description of the policy. You can find full details in the policy terms and conditions, which

Business insurance. a practical guide. 13 12 49 smallbusiness.wa.gov.au The small business specialists BUILDING YOUR KNOWLEDGE

Business insurance a practical guide BUILDING YOUR KNOWLEDGE Small Business Development Corporation 13 12 49 smallbusiness.wa.gov.au The small business specialists Business insurance Obtaining the right

Business insurance a practical guide BUILDING YOUR KNOWLEDGE Small Business Development Corporation 13 12 49 smallbusiness.wa.gov.au The small business specialists Business insurance Obtaining the right

Public Liability Insurance

Public Liability Insurance THE INSURED Name of Insured Are you registered for GST? What is your ABN? Have you claimed or intend to claim an input tax credit on the GST component of the premium applicable

Public Liability Insurance THE INSURED Name of Insured Are you registered for GST? What is your ABN? Have you claimed or intend to claim an input tax credit on the GST component of the premium applicable

The Tradesmen policy is available for self employed persons and small businesses with up to 8 people and a turnover of 500,000 or less.

TRADESMEN Summary of Cover The Tradesmen policy is available for self employed persons and small businesses with up to 8 people and a turnover of 500,000 or less. Why choose AXA s Tradesmen policy? Tailor-made

TRADESMEN Summary of Cover The Tradesmen policy is available for self employed persons and small businesses with up to 8 people and a turnover of 500,000 or less. Why choose AXA s Tradesmen policy? Tailor-made

Insurer Thistle Underwriting acting in an underwriting capacity on behalf of those Lloyd s Underwriters subscribing to the above policy.

CONTRACTORS & ENGINEERS POLICY Please read this document carefully This is a summary of the cover provided by your Policy. It contains references to the key features and benefits of the Policy as well

CONTRACTORS & ENGINEERS POLICY Please read this document carefully This is a summary of the cover provided by your Policy. It contains references to the key features and benefits of the Policy as well