Preparer Review. Tax Ease, LLC Paseo Padre Pkwy #624 May, 2011 Fremont, CA Fax:

|

|

|

- Evelyn Chapman

- 8 years ago

- Views:

Transcription

1 Preparer Review Tax Ease, LLC Paseo Padre Pkwy #624 May, 2011 Fremont, CA Fax:

2 Introduction Introduction We have designed this course with a heavy emphasis on the forms. An example of most forms the IRS has indicated will be on this exam are included. Although we have included Form 1040EZ and Form 1040A in this syllabus, we determined that using Form 1040 as the guide would be the best way to illustrate the flow of the forms and keep a clear focus on the exam. All the information provided is based on the 2010 tax year. When forms and income items are introduced from the IRS list of included items they will be in Bold, we also have included a separate form and income index for your convenience. Be sure to check out the appendix which is a cross reference from Publications to Forms to the page number in this material. The answers to sample questions are found as the last item in each chapter. Study Hard and Good Luck! About the Writers Sue Tornberg, EA Sue has been part of the tax return industry since the early 1980 s. From 1986 through 1999 she was the Tax Department Manager for Compucraft Data Services, a large computerized processing company. As part of her position Sue conducted workshops and seminars for the many tax professionals. She was also the liaison between the tax department and the programming department. From 2000 through April 2007, Sue was the partner in a smaller computerized processing company in which she began writing and providing CTEC Approved Tax Education. Sue is one of the owners of TaxEase, LLC with a large tax practice specializing in individual and business tax returns. The practice averages over 500 tax returns per year. As a tax professional, Sue understands the need for Enrolled Agents and Tax Preparers to be able to obtain interesting, qualified education at a reasonable cost. TaxEase provides courses that are designed not only to review the important information tax professionals have used for years, but to include and define the new changes each year. Jan Cusumano, CRTP Jan has been in the tax business for nearly thirty years. She started in Compucraft specializing in bookkeeping and payroll taxes. She has been a CTEC registered tax preparer since Jan is one of the owners of TaxEase, where she continues to do payroll tax reports, bookkeeping and individual returns. Jan is instrumental in the research and development of the continuing and qualifying education and maintains the high standards which allow TaxEase to produce quality tax education at a reasonable cost. 2

3 Table of Contents TABLE OF CONTENTS INTRODUCTION... 2 ABOUT THE WRITERS... 2 PART I... 9 CHAPTER 1 - WHICH TO FILE FORM 1040EZ/FORM 1040A/FORM SAMPLE QUESTIONS FOR CHAPTER ONE CHAPTER 1 - ANSWERS TO SAMPLE QUESTIONS CHAPTER 2 - THE BASICS... 9 WHO MUST FILE? FILING REQUIREMENTS FOR DEPENDENTS STANDARD DEDUCTION ACCOUNTING METHOD AND PERIODS CHAPTER 2 SAMPLE QUESTIONS CHAPTER 2 ANSWERS TO SAMPLE QUESTION CHAPTER 3 - FILING STATUS, EXEMPTIONS AND DEPENDENTS FILING STATUS EXEMPTIONS DEPENDENTS WORKSHEET FROM 2010 IRS PUB CHAPTER 3 - SAMPLE QUESTIONS CHAPTER 3 ANSWERS TO SAMPLE QUESTIONS CHAPTER 4 WHERE TO REPORT INCOME FORM W FORM W-2 AND INSTRUCTIONS CHAPTER 4 - SAMPLE QUESTIONS CHAPTER 4 ANSWERS TO SAMPLE QUESTIONS CHAPTER 5 WAGES FORM EMPLOYEE COMPENSATION MISCELLANEOUS COMPENSATION LIFE INSURANCE PROCEEDS FRINGE BENEFITS EMPLOYEE BENEFITS WORKERS COMPENSATION CHAPTER 5 - SAMPLE QUESTIONS CHAPTER 5 ANSWERS TO SAMPLE QUESTIONS CHAPTER 6 INTEREST AND DIVIDENDS

4 4 Table of Contents INTEREST INCOME DIVIDEND INCOME NONTAXABLE DISTRIBUTIONS CHAPTER 6 - SAMPLE QUESTIONS CHAPTER 6 ANSWERS TO SAMPLE QUESTIONS CHAPTER 7 RECOVERIES AND ALIMONY RECEIVED STATE TAX REFUND EXCERPT FROM PUB CHAPTER 7 - SAMPLE QUESTIONS CHAPTER 7 ANSWERS TO SAMPLE QUESTIONS CHAPTER 8 SCHEDULE C-EZ BOX 9. PAYER MADE DIRECT SALES OF $5,000 OR MORE BUSINESS INCOME SCHEDULE C-EZ BUSINESS INCOME SCHEDULE C-EZ SCHEDULE SE CHAPTER 8 - SAMPLE QUESTIONS CHAPTER 8 ANSWERS TO SAMPLE QUESTIONS CHAPTER 9 - CAPITAL ASSETS BASIS OF PROPERTY STOCKS, BONDS AND MUTUAL FUNDS FIRST-IN, FIRST-OUT METHOD OF IDENTIFICATION SPECIFIC IDENTIFICATION METHOD AVERAGE COST BASIS, SINGLE CATEGORY METHOD (MUTUAL FUNDS) AVERAGE COST BASIS, DOUBLE CATEGORY METHOD (MUTUAL FUNDS) SALE OF PROPERTY GAIN AND LOSS CAPITAL GAIN TAX RATES SCHEDULE D TAX WORKSHEET CHAPTER 9 - SAMPLE QUESTIONS CHAPTER 9 - ANSWERS TO SAMPLE QUESTIONS CHAPTER 10 - TYPES OF IRA S AND EMPLOYER SPONSORED PENSION PLANS - DISTRIBUTIONS ROTH IRA DISTRIBUTIONS REPORTING DISTRIBUTIONS PENSION DISTRIBUTIONS DISTRIBUTIONS BEFORE AGE 59 1/ REQUIRED MINIMUM DISTRIBUTION ROLLOVERS OF PENSIONS AND IRA S SIMPLIFIED METHOD WORKSHEET FROM PUB FORM 1099-R ADDITIONAL TAXES ON QUALIFIED PLANS (INCLUDING IRA S) FORM CHAPTER 10 - SAMPLE QUESTIONS CHAPTER 10 -ANSWERS TO SAMPLE QUESTIONS CHAPTER 11 - UNEMPLOYMENT COMPENSATION, SOCIAL SECURITY BENEFITS AND MISCELLANEOUS INCOME

5 Table of Contents UNEMPLOYMENT COMPENSATION SOCIAL SECURITY BENEFITS MISCELLANEOUS INCOME LINE 21 FORM FOREIGN EARNED INCOME EXCLUSION FORM 2555-EZ CANCELLED DEBT FORM 1099-C CANCELLATION OF DEBT DISCOUNTS AND LOAN MODIFICATIONS FORECLOSURES AND REPOSSESSIONS CHAPTER 11 - SAMPLE QUESTIONS CHAPTER 11 ANSWERS TO SAMPLE QUESTIONS CHAPTER 12- ADJUSTMENTS TO INCOME HEALTH SAVINGS ACCOUNT ALIMONY PAID INDIVIDUAL RETIREMENT ARRANGEMENT IRA DEDUCTIONS NONDEDUCTIBLE IRA CONTRIBUTIONS FORM CHAPTER 12 - SAMPLE QUESTIONS CHAPTER 12 ANSWERS TO SAMPLE QUESTIONS CHAPTER 13 ITEMIZED DEDUCTIONS STANDARD DEDUCTION VS. ITEMIZED DEDUCTIONS ITEMIZED DEDUCTIONS MEDICAL AND DENTAL EXPENSES TAXES INTEREST FORM INVESTMENT INTEREST GIFTS TO CHARITY EIGHT TIPS FOR DEDUCTING CHARITABLE CONTRIBUTIONS CASUALTY AND THEFT JOB EXPENSES AND OTHER MISCELLANEOUS DEDUCTIONS FORM EMPLOYEE BUSINESS EXPENSES DEDUCTIONS SUBJECT TO 2% OF ADJUSTED GROSS INCOME DEDUCTIONS NOT SUBJECT TO 2% LIMIT SCHEDULE A, LINE CHAPTER 13 - SAMPLE QUESTIONS CHAPTER 13 - ANSWERS TO SAMPLE QUESTIONS CHAPTER 14 TAXES AND CREDITS TAX CAPITAL GAIN TAX RATES CREDITS ADOPTION BENEFITS CHILD TAX CREDIT (IRC SECTION 24) EDUCATION CREDITS (IRC SECTION 25(A)) RETIREMENT SAVINGS CONTRIBUTION CREDIT (IRC SECTION 25B) MAKING WORK PAY CREDIT CHAPTER 14 SAMPLE QUESTIONS CHAPTER 14 - ANSWERS TO SAMPLE QUESTIONS

6 6 Table of Contents CHAPTER 15 EARNED INCOME CREDIT EARNED INCOME CREDIT CHAPTER 15 - SAMPLE QUESTIONS CHAPTER 15 ANSWERS TO SAMPLE QUESTIONS CHAPTER 16 REFUNDS, AMOUNT DUE & ELECTRONIC FILING REFUND AMOUNT OWED ELECTRONIC FILING FORM ADVANTAGES OF IRS E-FILE FORM FORM CHAPTER 16 SAMPLE QUESTIONS CHAPTER 16 ANSWERS TO SAMPLE QUESTIONS CHAPTER 17 MISCELLANEOUS FORMS FORM INJURED SPOUSE ALLOCATION FORM 9465 INSTALLMENT AGREEMENT FORM W-7- APPLICATION FOR IRS INDIVIDUAL TAXPAYER IDENTIFICATION NUMBER FORM 8821 TAX INFORMATION AUTHORIZATION CHAPTER 17 SAMPLE QUESTIONS CHAPTER 17 ANSWERS TO SAMPLE QUESTIONS PART II CHAPTER 18 SCHEDULE C/FORM 4562 AND BUSINESS INCOME SCHEDULE C ACCOUNTING PERIODS ACCOUNTING METHODS MATERIAL PARTICIPATION COMBINATION METHOD IRS PUBLICATION DEPRECIATION (FORM 4562) SPECIAL DEPRECIATION ALLOWANCE FORM 4562 (SEE BELOW) BUSINESS USE OF HOME FORM SCHEDULE SE EARNINGS FOR CLERGY FORM W FORM EMPLOYEE BUSINESS EXPENSES CHAPTER 18 SAMPLE QUESTIONS CHAPTER 18 ANSWERS TO SAMPLE QUESTIONS CHAPTER 19 - RENTAL REAL ESTATE, K-1 INCOME AND LOSS, PASSIVE ACTIVITIES RENTAL INCOME - PUB RENTAL EXPENSES SCHEDULE E ROYALTY INCOME

7 Table of Contents PASS-THROUGH INCOME FROM PARTNERSHIP, S-CORPORATION, ESTATE OR TRUST K-1 S FORM 1065, K-1, PAGE FORM 1120S, K-1, PAGE FORM 1041, K-1, PAGE CHAPTER 19 - SAMPLE QUESTIONS CHAPTER 19 ANSWERS TO SAMPLE QUESTIONS CHAPTER 20 SCHEDULE F FARM INCOME FARM INVENTORY SCHEDULE F FORM FARM RENTAL INCOME AND EXPENSE DEPRECIATION SCHEDULE J CHAPTER 20 SAMPLE QUESTIONS CHAPTER 20 ANSWERS TO SAMPLE QUESTIONS CHAPTER 21 FORM 1040NR, 1040PR, FORM 2555 AND FORM FORM 1040NR - U.S. NONRESIDENT ALIEN INCOME TAX RETURN FORM 1040NR FORM 1040 SS FORM 1040 SS FORM 2555 FOREIGN INCOME EXCLUSION FORM FOREIGN TAX CREDIT (IRC SECTION 901(A)) CHAPTER 21 SAMPLE QUESTIONS CHAPTER 21 ANSWERS TO SAMPLE QUESTIONS CHAPTER 22 KIDDIE TAX KIDDIE TAX - TAX ON INVESTMENT INCOME OF CERTAIN MINOR CHILDREN FORM CHAPTER 22 SAMPLE QUESTIONS CHAPTER 22 ANSWER TO SAMPLE QUESTIONS CHAPTER 23 GENERAL BUSINESS CREDIT AND ALTERNATIVE MINIMUM TAX FORM ALTERNATIVE MINIMUM TAX FORM GENERAL BUSINESS CREDIT FORM 8801 CREDIT FOR PRIOR YEAR MINIMUM TAX CHAPTER 23 SAMPLE QUESTIONS CHAPTER 23 ANSWERS TO SAMPLE QUESTIONS CHAPTER 24 FORM 4797, 6252, 8824, 4952, FORM 4797 SALE OF BUSINESS PROPERTY GAIN OR LOSS FORM FORM INSTALLMENT SALES FORM 8824 LIKE-KIND EXCHANGE REPORTING THE EXCHANGE

8 Table of Contents FORM 4952 INVESTMENT INTEREST EXPENSE DEDUCTION FORM 6198 AT RISK LIMITATIONS CHAPTER 24 SAMPLE QUESTIONS CHAPTER 24 ANSWERS TO SAMPLE QUESTIONS CHAPTER 25 OTHER ITEMS FORM 8903 DOMESTIC PRODUCTION ACTIVITIES DEDUCTION FORM 8910 ALTERNATIVE MOTOR VEHICLE CREDIT FORM 8919 UNCOLLECTED SOCIAL SECURITY AND MEDICARE TAX ON WAGES

9 Part I 9

10 Form 1040EZ/Form 1040A/Form 1040 Chapter 1 - Which to File Form 1040EZ/Form 1040A/Form 1040 The taxpayer can use Form 1040 EZ if the following is true: The filing status is single or married filing a joint return The taxpayer (and spouse if married filing joint) were under age 65 and not blind at the end of 2010 There are no dependents on the return The taxable income is less than $100,000 The taxpayer did not claim any adjustments to income. The taxpayer did not claim any credit except EIC or recovery rebate credit. The only income is from salaries, wages, tips, taxable scholarship or fellowship grants, unemployment compensation, Alaska Permanent Fund and the taxable interest is not over $1,500 No advanced earned income payments were received, and the taxpayer did not owe Household Employment Taxes The taxpayer did not figure the standard deduction using Schedule L. The taxpayer can use Form 1040A if all five of the following apply: 1. The only income was from the following sources: Wages, salaries, tips Interest and ordinary dividends Capital gain distributions Taxable scholarship and fellowship grants. Pensions, annuities and IRA's. Unemployment compensation. Taxable social security and railroad retirement benefits. Alaska Permanent Fund dividends. 2. The only adjustments to income that can be claimed are: Educator expenses IRA deduction. Student loan interest deduction. Tuition and fees deduction 3. No itemized deductions are taken. 4. The taxable income is less than $100, The only tax credits that can be claimed are: Child tax credit. Additional child tax credit. Education credits. Earned income credit. Credit for child and dependent care expenses. Credit for the elderly or the disabled. Adoption credit. Retirement savings contribution credit. Making work pay credit 10

11 Form 1040EZ/Form 1040A/Form 1040 The following excerpt is from Form 1040A instructions When to Use Form 1040 : Sample Questions for Chapter One 1. All of the following statements are true except; a. A taxpayer can file Form 1040EZ if the taxable income is less than $100,000. b. A taxpayer can file Form 1040EZ if they claim the EIC credit. c. Making Work Pay credit can be claimed only when filing Form d. Taxable scholarships and fellowship grants can be claimed if filing Form 1040A. 2. Which of the following is allowed when filing 1040A? a. The taxpayer is a bona fide resident of Puerto Rico and excludes income from sources in Puerto Rico. b. The taxpayer is a debtor in a bankruptcy filed after October 16, 2005 c. Form W-2, box 12 shows uncollected employee tax (social security and medicare tax on tips or group-term life insurance.) d. Capital gain distributions 3. A taxpayer must file Form 1040 if they have a net disaster loss attributable to federally declared disaster even if they are claiming the standard deduction. a. True b. False 4. A taxpayer may file Form 1040EZ if their taxable interest amount is; a. $2500 b. $1400 c. $1650 d. $

d.")

12 12 Form 1040EZ/Form 1040A/Form 1040

13 Form 1040EZ/Form 1040A/Form

14 Form 1040EZ/Form 1040A/Form 1040 Chapter 1 - Answers to Sample Questions 1. C- is not true. The Making Work Pay credit can be claimed on Forms 1040EZ, 1040A or (Form 1040EZ, 1040A and 1040 Instructions) 2. D - Capital gain distributions can be reported on Form 1040A line 10. (Form 1040A Ins., Pg. 11) 3. A -This statement is true. A net disaster loss in 2010 because of a disaster that was declared a federal disaster after 2007 and occurred before 2010 must be reported on Form (Form 1040A Ins., Pg. 12) 4. B The taxable interest reported on Form 1040EZ must be less than $1500. (Form 1040EZ Ins., Pg. 6) 14

15 The Basics Chapter 2 - The Basics Pub.17 Excerpt Who Must File? All US citizens, regardless of where they live, and resident aliens must determine whether they are required to file a tax return. The determination is based on the following three factors: 1. Gross Income 2. Filing Status and 3. Age A return must be filed if any of the following four conditions below apply: 1. The taxpayer owes special taxes, such as: Social Security or Medicare taxes on tips that were not reported to the employer, Alternative Minimum Tax, recapture taxes or tax on a qualified plan including IRA or other tax-favored account. 2. The taxpayer had earnings from self-employment of at least $ Any advanced earned income payments were received. 4. There are wages of $ or more from a church that is exempt from employer social security and Medicare taxes. 9

16 The Basics 2010 Filing Requirements for Dependents Pub 17, Page 8 Standard Deduction The standard deduction is a dollar amount that reduces the amount of income on which the taxpayer is taxed. The standard deduction is allowed only if the taxpayer does not have itemized deductions. In general, the basic standard deduction is an amount relative to each tax year and varies according to the filing status. The standard deduction of an individual who can be claimed as a dependent on another person's tax return is the greater of: An amount specified by law, or The individual's earned income plus a specified amount up to the basic standard deduction for his or her filing status In some cases, the standard deduction can consist of two parts, the basic standard deduction and additional standard deduction amounts, for age, or blindness, or both. The additional amount is an amount specified by law and varies based on the filing status. The additional amount for age will be allowed if the taxpayer is age 65 or older at the end of the tax year. The taxpayer is considered to be 65 on the day before their 65th birthday. The additional amount for blindness will be allowed if the taxpayer is blind on the last day of the tax year. Certain individuals are not entitled to the standard deduction. They are: A married individual filing a separate return whose spouse itemizes deductions, An individual who was a nonresident alien or dual status alien during any part of the year, or An individual who files a return for a period of less than 12 months due to a change in his or her annual accounting cycle 10

When to File?")

17 The Basics Standard Deduction 2010 Age 65 or Older/Blind Single 5,700 1,400 Married Filing Joint or Qualified Widow(er) 11,400 1,100 Head of Household 8,350 1,400 Married Filing Separate 5,700 1,100 Standard Deduction Worksheet (Pub 17, pg 139) When to File? Tax returns for individual taxpayers are due by the 15 th day of the fourth month after the close of the tax year (April 15 th for calendar year taxpayers). If the return is filed after this date it is subject to interest and penalties. If the taxpayer needs an extension of time Form 4868 requesting an automatic 6-month extension must be filed. The due date that falls on a Saturday, Sunday or legal holiday for filing tax forms is delayed until the next business day. Interest Interest will be charged on tax returns not paid by the due date, even if an extension of time is granted. Interest is also charged on penalties imposed for failure to file, negligence, fraud, substantial valuation misstatements, and substantial understatements of tax. Interest is charged on the penalty from the due date of the return (including extensions). 11

18 The Basics The IRS will pay interest on overpayment of tax if the refund is not issued 45 days after the tax return is filed. If the refund is issued within 45 days of the filing date there is no interest. The interest adjusts quarterly. Accepting a check from the IRS does not change the right of the taxpayer to claim an additional refund and interest. A claim for additional refund should be filed on Form 1040X. Amended Returns Errors and omissions on a return can lead to additional refund or additional amount owed. The return should be corrected if: 1. Not all income was reported 2. Deductions and credits were claimed that should not have been claimed. 3. Deductions and credits were not claimed that should have been claimed. 4. The filing status claimed was incorrect. Form 1040X was revamped in January A separate Form 1040X must be filed for every year being changed. Interest and Penalties are not included on Form 1040X, the interest and penalties will be adjusted accordingly. It takes 8 to 10 weeks for an amended return to be processed. (Refer to Form 1040X instructions for further information). Penalties Late Filing: If the return is not filed by the due date (including extensions), the penalty is usually 5% of the amount due for each month or part of the month the return is late, unless there is a reasonable explanation. The explanation must be attached to the return. The penalty can be as much as 25% (more in some cases) of the tax due. If the return is more than 60 days late the minimum penalty will be $100 or the amount of any tax owed whichever is smaller. Late Payment of Tax: If the taxes owed are paid late the penalty is usually 1/2 of 1% of the unpaid amount for each month or part of the month the tax is not paid. This is known as the failure-to pay penalty. The penalty can be as much as 25% of the unpaid amount. It applies to any unpaid amount on the return. This penalty is in addition to interest charges on the late payments. The penalty does not apply during the automatic 6-month extension of time to file. Negligence and disregard: The term negligence includes failure to make a reasonable attempt to comply with the tax law or to exercise ordinary and reasonable care in preparing the tax return and adequate books and records. This accuracy penalty includes any careless, reckless, or intentional disregard. Substantial understatement of income tax: An understatement is considered substantial if it is more than the largest of 10% of the correct tax or $5,000. Negligence, disregard and substantial understatement of income are all considered accuracy related penalties. Accuracy related penalty is equal to 20% of the underpayment. Accounting Method and Periods The accounting method is the way the taxpayer accounts for his/her income and expenses. Most taxpayers use either the cash or accrual method of accounting. The method is chosen the first time a return is filed; approval is needed by the IRS to change the accounting method. 12

19 The Basics If the taxpayer uses the cash method, all items of income are reported in the year they are received or constructively received. Expenses are deducted in the year they are paid. Constructive receipt is when the funds become available to use without restriction whether they are in the physical possession of the taxpayer or not. In general, the cash method cannot be used to account for inventory purchases and sales. However, an exception is allowed for taxpayers with an average annual gross receipt of $1 million or less. If the taxpayer uses the accrual method, the income is generally reported when earned, not received. The expenses are reported when incurred, not paid. Accounts payable and accounts receivable books must be maintained. The accrual method must be used to account for inventory purchases and sales. Hybrid method is a combination of accrual and cash. The most common hybrid uses the accrual method for inventory purchases and sales; and the cash method for non inventory income and operating expenses. Most individual tax returns cover a calendar year the 12 months from January 1 through December 31 st. If the taxpayer does not use a calendar year, the accounting period is a fiscal year. A regular fiscal year is a 12-month period that ends on the last day of any month other than December. A week fiscal year varies from 52 to 53 weeks and always ends on the same day of the week. The accounting period is chosen when the first return is filed; the accounting period cannot be longer than 12 months. For additional information on accounting methods or periods refer to Pub

20 The Basics Chapter 2 Sample Questions 1. Which one of the following is not a determination of whether a person must file a tax return? A. Residency B. Filing status C. Gross Income D. Age 2. The taxpayer may be able to file as a qualifying widow or widower for the two years following the year the spouse died. To do this, the taxpayer must meet all four of the following tests, except? A. The taxpayer is entitled to file a joint return with the spouse for the year he or she died. It does not matter whether the joint return was actually filed, B. The taxpayer did not remarry in the two years following the year the spouse died, C. There is a child, stepchild, or adopted child (a foster child does not meet this requirement) for whom the taxpayer can claim a dependency exemption, D. The child does not have to be a dependent if in the military E. The taxpayer paid more than half the cost of maintaining a household that was the main home for them and that child, for the whole year. 3. You are a dependent who is single, 23 years old, and not blind. You earned $856 of wages and $1,123 of interest income during You must file a tax return A. True B. False 4. Larry, 46, and Donna, 33, are filing a joint return for Neither is blind, and neither can be claimed as a dependent. They decide not to itemize their deductions. Their standard deduction is $11,400 A. True B. False 5. Form 1040 instructions state that gross income means all income that is received in the form of the following, except: A. Money B. Property C. Services that are not tax exempt D. Real estate taxes paid 14

21 The Basics 6. The tax return for a calendar year taxpayer is due on: A. The 15 th day of the 4 th month after the close of the taxable year. B. April 1 st C. August 15 th D. The 15 th day of the 3 rd month after the close of the taxable year. 7. The due date that falls on a Saturday, Sunday or legal holiday for filing tax forms is delayed until the next business day. A. True B. False 8. Form 4868 is used: A. To request an automatic 6-month extension of time to file the tax return. B. To report self-employment tax C. To report miscellaneous income D. To request an automatic 4-month extension of time to pay the tax owed. 9. Which of the following is not an accuracy related penalty? A. Negligence penalty B. Disregard penalty C. Penalty for substantial under reporting of income D. Penalty for late filing of the tax return. 10. The failure-to-pay penalty on the unpaid amount of tax due can be as much as: A. 10% B. 50% C. 25% D. 5% 11. The term for a tax return that is carelessly prepared and without adequate records is considered to be done with: A. Oversight or omission B. Inattention or neglect C. Negligence or disregard D. Indifference or disinterest 12. If the taxpayer uses the cash method of accounting, which of the following statements are correct? A. Income is reported in the year received or constructively received B. Expenses are deducted in the year they are paid C. Income is reported when earned D. Both A and B 15

22 The Basics 13. A regular fiscal year is a 12-month period that ends: A. December 31st B. The first day of any month other than December C. The last day of any month other than December D. Always on November 30 th 16

23 The Basics Chapter 2 Answers to Sample Question 1. A - Residency is not a factor. Filing status, age and gross income are the determining factor of whether a return has to be filed. (Pub 17, Pg 5) 2. C Both A and B are correct. A return must be filed if any of the following four conditions apply: (Pub 17, Pg 7) The taxpayer owes special taxes, such as: Social Security or Medicare taxes on tips that were not reported to the employer, Alternative Minimum Tax, recapture taxes or tax on a qualified plan including IRA or other tax-favored account. The taxpayer had earnings from self-employment of at least $400. Any advanced earned income payments were received. There are wages of $ or more from a church that is exempt from employer social security and Medicare taxes 3. A - The correct answer is True. Single dependents who are not 65 or older, or not blind, must file a tax return if unearned income is more than $950. (Pub 17, Pg 6) 4. A - $11,400 is the amount of standard deduction. Refer to Form 1040 Instructions. (Pub. 17, Pg 138) 5. D - Real estate taxes paid is not correct Refer to Table 1-1 from Pub 17 on page 12 of this text. (Pub. 17, Pg 4) 6. A- Tax returns for individual taxpayers are due by the 15 th day of the fourth month after the close of the tax year (April 15 th for calendar year taxpayers). (Pub 17, Pg 11) 7. A It is true if the due date that falls on a Saturday, Sunday or legal holiday then the filing of the tax form are delayed until the next business day. (Pub 17, Pg 11) 8. A is correct that Form 4868 is used to request a 6-month extension. (Pub 17, Pg 12) 9. D Penalty for late filing of a tax return is not an accuracy related penalty.(pub 17, Pg 18) 10. C A failure-to-pay penalty on the unpaid amount of tax due can be as much as 25%(Pub 17, Pg 18) 11. C Negligence or disregard is the way the IRS terms a carelessly prepared return. (Pub 17, Pg 20) 12. D Income is reported in the year received or constructively received and expenses are deducted in the year they are paid if the taxpayer is a cash basis taxpayer. (Pub 17, Pg 33) 13. C - A calendar year taxpayer s tax year ends December 31, a fiscal year taxpayer s tax year ends the last day of any month except December. (Pub 17, Pg 13) 17

24 Filing Status and Dependents Chapter 3 - Filing Status, Exemptions and Dependents Filing Status Single When to use: The taxpayer is unmarried for the whole year if, on the last day of the tax year, the taxpayer is unmarried or legally separated from their spouse under a divorce or separation maintenance decree. The taxpayer s spouse died a previous tax year and the taxpayer does not have a dependent child The taxpayer does not qualify for head of household filing status Married Filing Jointly Married Filing Separately When to use: The taxpayer is married and living together as husband and wife. The taxpayer is living together in a common law marriage that is recognized in the state where the taxpayer now lives or in the state where the common law marriage began. The taxpayer is married and living apart from their spouse, but not legally separated under a decree of divorce or separate maintenance The taxpayer is separated under an interlocutory (not final) decree of divorce. For purposes of filing a joint return, the taxpayer is not considered divorced. If the taxpayer s spouse died during the year and the taxpayer did not remarry before the end of the tax year. Conditions: Both the taxpayer and the spouse must agree to file a joint return. May file a joint return even if the taxpayer or spouse had no income or deductions Both the taxpayer and the spouse must use the same accounting period, but they may use different accounting methods. Both the taxpayer and the spouse may be held responsible, jointly and individually, for the tax and any interest or penalty due on their joint return even if they divorce in a future tax year. If one spouse is a nonresident alien or dual-status alien who is married to a U.S. citizen or resident alien at the end of the year, the spouses can choose to file a joint return. (See IRS Publication 519) Once the taxpayer and their spouse file a married filing joint tax return they cannot choose to file married filing separate after the due date of the return. Note: If the taxpayer s spouse dies and the taxpayer was to remarry the same tax year, the taxpayer can file a joint return with their new spouse. The taxpayer s deceased spouse s filing status is married filing separately for that year. When to use: Must be married May benefit a married taxpayer who wishes to be responsible only for their own tax May have to use married filing separately if the spouses cannot agree to file a joint return and they live together How to file: Usually the taxpayer would report only their own income, exemptions, credits, and deductions on their individual tax return The taxpayer can claim an exemption for their spouse if the spouse had no gross income and was not the dependent of another person. May use form 1040A or 1040 when using this filing status 18

25 Filing Status and Dependents (Continued) Married Filing Separately Enter the spouse s full name and social security number in the space provided on Form 1040A or 1040 Special rules: The taxpayer s tax rate will usually be higher than it would be on a joint return The exemption amount for figuring the AMT will be half that allowed to a joint return filer Cannot take the credit for child and dependent care expenses in most cases. The amount the taxpayer can exclude from income under an employer s dependent care assistance program is limited to $2,500. Cannot take the earned income credit In most cases the taxpayer cannot take the exclusion or credit for adoption expenses. Cannot take education credits or deduction for student loan interest If the taxpayer lived with the spouse at any time during the year they cannot claim the credit for the elderly or the disabled If the taxpayer lived with the spouse at any time during the year they will have to include in income more (up to 85%) of any social security income or equivalent railroad retirement benefits received The child tax credit and retirement savings contributions credit are reduced at income levels that are half those for a joint return The capital loss deduction limit is $1,500 If the taxpayer s spouse itemizes deductions, the taxpayer cannot claim the standard deduction. The standard deduction is half the amount allowed on a joint return. The first-time homebuyer credit is limited to $4000. If the special rule for longtime residents of the same main home applies, the credit is limited to $3,250. The taxpayer cannot rollover amounts from a traditional IRA to a Roth IRA. Other rules: The taxpayer may not be able to deduct all or part of his or her contributions to a traditional IRA if their spouse was covered by an employee retirement plan at work. The deduction is reduced or eliminated if the taxpayer s income is more than a certain amount. Taxpayer s who actively participate in a passive rental real estate activity that produced a loss cannot claim the special allowance if they lived with their spouse at any time during the year. Married persons filing separate returns that lived apart at all times during the year are each allowed a $12,500 maximum special allowance for losses from passive real estate activities. Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, or Wisconsin is considered community property states. The taxpayer s income may be considered separate or community income for income tax purposes. See IRS Publication 555. Changing a married filing separate return to a married filing joint return: This can be done by filing a 1040X (Amended Return) any time within 3 years from the due date of the separate return or returns. This does not include any extensions. 19

26 Filing Status and Dependents Head of Household When to use: The taxpayer must be unmarried or considered unmarried on the last day of the year, paid more than half the cost of keeping up a home for the tax year, and have a child, stepchild, adopted child, or eligible foster child living with them for more the half the year. All three requirements must apply. However, if the qualifying person is the taxpayer s parent, he or she does not have to live with the taxpayer. The taxpayer must file a separate return. A separate return includes a return filed claiming married filing separately, single, or head of house hold filing status. The taxpayer s spouse did not live in the taxpayer s home during the last 6 months of the tax year. Who is a Qualifying Person? A qualifying child who is single, the taxpayer can claim an exemption for him or her, and lived with the taxpayer more than half the year. However, if the taxpayer cannot claim the exemption only because the noncustodial parent can claim the exemption for the child, the child is usually the qualifying child of the custodial parent for head of household purposes. A qualifying child who is married, lived with the taxpayer more than half the year, and the taxpayer can claim an exemption for him or her. The taxpayer s mother or father who lives or doesn t live with the taxpayer and the taxpayer can claim an exemption for him or her. A qualifying relative (other than the taxpayer s father or mother) who lived with the taxpayer more than half the year. The taxpayer must be able to claim an exemption for him or her. Who is Not a Qualifying Person? A qualifying child who is married and the taxpayer cannot claim an exemption for him or her. The taxpayer s father or mother and the taxpayer cannot claim an exemption for him or her. A qualifying relative (other than the taxpayer s father or mother) who did not live with the taxpayer more than half the year. A person who is not related to the taxpayer in one of the ways listed as Who is a Qualifying Relative? (Below) Who is a Qualifying Child? (All of the following must apply): Must be the taxpayer s son, daughter, stepchild, foster child, brother, sister, half brother, half sister, stepbrother, stepsister, or a descendant of any of them. A legally adopted child is considered your child. The child must be under age 19 at the end of the year and younger then the taxpayer; or under age 24 at the end of the year, a full time student, and younger than the taxpayer; or any age if permanently and totally disabled. The child must have lived with the taxpayer for more than half of the year. The child must not have provided more than half of this or her own support for the year. The child is not filing a joint return for the year (unless that return is filed only as a claim for refund) Who is a Qualifying Relative? (All of the following must apply) Cannot be a qualifying child of the taxpayer or a qualifying child of any other taxpayer. 20

27 Filing Status and Dependents Continued Head of Household Must be the taxpayer s, child, stepchild, foster child, or a descendant of any of them. The taxpayer s brother, sister, half brother, half sister, stepbrother, or stepsister. The taxpayer s father, mother, grandparent, or direct ancestor. The taxpayer s stepfather or stepmother. A brother or sister of the taxpayer s father or mother. The taxpayer s son-in-law, daughter-in-law, father-in-law, motherin-law, brother-in-law, or sister-in-law (any of these relationships that were established by marriage are not ended by death or divorce.) Must have lived in the taxpayer s home for more than half the year The taxpayer must be able to claim an exemption for him or her. Calculation for keeping up a home for the year: Total the amount the taxpayer paid for keeping up a home (see included cost below) Total the total cost of keeping up a home (see included cost below) Subtract the total amount the taxpayer paid from the total cost amount. The answer is amounts others paid. If the total amount the taxpayer paid is more than the amounts others paid, the taxpayer meets the requirement of paying more than half the cost of keeping up the home. What is included in paying more than half of the cost of keeping up a home for the year? The taxpayer can include rent, mortgage interest expense, real estate taxes, insurance on the home, home repairs and maintenance, utilities, other household expenses and food eaten in the home. If the taxpayer used payments they received from TANF or other public assistance programs to pay part of the cost of keeping up their home, the taxpayer cannot count them as money the taxpayer paid. However, the taxpayer must include them in the total cost of keeping up their home to figure if they paid over half the cost. What is not included in paying more than half of the cost of keeping up a home for the year? Clothing, education, medical treatment, vacations, life insurance, or transportation Rental value of a home the taxpayer owns or the value of the taxpayer s services or those of a member of the taxpayer s household. Nonresident alien spouse: The taxpayer is considered unmarried for head of household purposes if their spouse was a nonresident alien at any time during the year and the taxpayer does not choose to treat their nonresident spouse as a resident alien. However, the taxpayer s spouse is not a qualifying person for head of household purposes. The taxpayer must have another qualifying person and meet the other tests to be eligible to file as a head of household. Even if the taxpayer is considered unmarried for head of household purposes because they are married to a nonresident alien, they are still considered married for purposes of the earned income credit. The taxpayer is not entitled to the credit unless they file a joint return with their spouse and meet other qualifications. The taxpayer is considered married if they choose to treat their spouse as a resident alien. 21

28 Filing Status and Dependents Qualifying Widow(er) With Dependent Child When to Use: The taxpayer may be eligible to use qualifying widow(er) with dependent child as their filing status for 2 years following the year their spouse died. Eligibility Rules: The taxpayer was entitled to file a joint return with their spouse for the year their spouse died. It does not matter whether the taxpayer actually filed a joint return. The taxpayer s spouse died in one of the two previous tax years and the taxpayer did not remarry before the end of the current tax year. Example: The taxpayer s spouse died in 2008 or 2009 and they did not remarry before the end of The taxpayer has a child, stepchild or adopted child for who they can claim an exemption. This does not include a foster child. The child lived in their home all year, except for temporary absences. The taxpayer paid more than half the cost of keeping up a home for the year. See head of household above for this calculation. If the taxpayer s child that qualifies them for this filing status dies during the year, the taxpayer may still be eligible to use this filing status. The taxpayer must have provided more than half of the cost of keeping up a home that was the child s main home during the entire part of the year he or she was alive. EXEMPTIONS New for 2010: The taxpayer will no longer lose part of their deduction for personal exemptions, regardless of the amount of their adjusted gross income Personal Exemptions: The taxpayer generally can take one for themselves and, if they are married, one for their spouse. If another taxpayer is entitled to claim this taxpayer as a dependent, they cannot take an exemption for themselves even if the other taxpayer does not actually claim this taxpayer as a dependent. Exemptions for Dependents: The taxpayer generally can take an exemption for each of their dependents. If the taxpayer is entitled to claim an exemption for a dependent, that dependent cannot claim a personal exemption on his or her own tax return. The taxpayer must list the social security number of any dependent for whom they can claim an exemption. The taxpayer can claim an exemption for a qualifying child or qualifying relative only if the dependent taxpayer, joint return, citizen or resident tests are met. The taxpayer must meet all three of the following tests. 22

29 Filing Status and Dependents Dependent Taxpayer Test: If the taxpayer could be claimed as a dependent by another person, the taxpayer cannot claim anyone else as a dependent. Even if the taxpayer has a qualifying child or qualifying relative, the taxpayer cannot claim that person as a dependent. If the taxpayer is filing a joint return and their spouse could be claimed as a dependent by someone else, the taxpayer and their spouse cannot claim any dependents on their join return. Joint Return Test: The taxpayer cannot claim a married person as a dependent if he or she files a joint return. An exception to the joint return test applies if the taxpayer s child and his or her spouse file a joint return merely as a claim for refund and no tax liability would exist for either spouse on separate returns. Citizen or Resident Test: The taxpayer cannot claim a person as a dependent unless that person is a U.S. Citizen, U.S. resident alien, U.S. national, or a resident of Canada or Mexico. An exception for an adopted child if the taxpayer is a U.S. citizen or U.S. national who has legally adopted a child who is not a U.S. citizen, U.S. resident alien, or U.S. national, this test is met if the child lived with the taxpayer as a member of their household all year. This exception also applies if the child was lawfully placed with the taxpayer for legal adoption. If the taxpayer was a U.S. citizen when their child was born, the child may be a U.S. citizen even if the other parent was a nonresident alien and the child was born in a foreign country. A taxpayer cannot claim an exemption for a foreign student placed in their home for a temporary period under a qualified international education exchange program. The foreign student generally is not considered a U.S. resident. U.S. nationals include American Samoans and Northern Mariana Islanders who chose to become U.S. nationals instead of U.S. Citizens. These are individuals who although are not U.S. citizens, they owe his or her allegiance to the United States. Spouses Exemption: The spouse is never considered the taxpayers dependent. On a joint return the taxpayer can claim one exemption for themselves and one for their spouse. If the taxpayer and their spouse file separate returns, the taxpayer can claim an exemption for their spouse only if their spouse had no gross income, is not filing a return, and is not the dependent of another taxpayer. This is true even if the other taxpayer does not actually claim the taxpayer s spouse as their dependent. If the taxpayer s spouse died during the year and the taxpayer and spouse filed a joint return, the taxpayer can generally claim the spouse s exemption the year the spouse died. If the taxpayer s spouse died during the year and the taxpayer and spouse filed separate returns, the taxpayer can claim the spouse s exemption the year the spouse died only if their spouse had no gross income, was not going to file a return, and was not the 23

30 Filing Status and Dependents dependent of another taxpayer. This is true even if the other taxpayer does not actually claim the taxpayer s spouse as their dependent. The taxpayer cannot claim an exemption for their deceased spouse if they remarry during the year. If the taxpayer is a surviving spouse without gross income and they remarry in the year their spouse died, the taxpayer can be claimed as an exemption on both the final separate return of their deceased spouse and the separate return of their of their new spouse for that year. If the taxpayer files a joint return with their new spouse, the taxpayer can be claimed as an exemption only on that return. If the taxpayer obtained a final decree of divorce or separate maintenance by the end of the year, the taxpayer cannot take their former spouse s exemption. This rule applies even if they provided all of their former spouse s support. DEPENDENTS Qualifying Child: There are five tests that must be met for a child to be the taxpayer s qualifying child: Relationship Test Must be the taxpayer s son, daughter, stepchild, foster child, or a descendant of any of them (such as a grandchild), or Must be the taxpayer s brother, sister, half brother, half sister, stepbrother, stepsister, or a descendant of any of them (such as a niece or nephew). A legally adopted child or a child who was lawfully placed with the taxpayer for legal adoption is considered the taxpayer s child. A foster child is an individual who is placed with the taxpayer by an authorized placement agency or by judgment, decree, or other order of any court of competent jurisdiction. Age Test The child must be under age 19 at the end of the year and younger then the taxpayer (or the taxpayer s spouse if filing jointly). Under age 24 at the end of the year, a full time student, and younger than the taxpayer (or the taxpayer s spouse if filing jointly). Permanently and totally disabled at any time during the year, regardless of age. The taxpayer s child is permanently and totally disabled if both of the following applies: (a) He or she cannot engage in any substantial gainful activity because of a physical or mental condition. (b) A doctor determines the condition has lasted or can be expected to last continuously for at least a year or can lead to death. To be the taxpayer s qualifying child, a child who is not permanently and totally disabled must be younger than the taxpayer. However, if you are married filing jointly, the child must be younger than you or your spouse but does not have to be younger than both of you. To qualify as a full time student the taxpayer s child must be, during some part of each of any 5 calendar months of the year: 1. A full-time student at a school that has a regular teaching staff, course of study, and a regularly enrolled student body at the school, or 24

31 Filing Status and Dependents 2. A student taking a full-time, on-farm training course given by a school described in (1), or by a state, county, or local government agency. o The 5 calendar months do not have to be consecutive. o An on-the job training course, correspondence school, or school offering courses only through the internet does not count as a school. o Students who work on co-op jobs in private industry as a part of a school s regular course of classroom and practical training are considered full-time students. Residency Test The child must have lived with the taxpayer for more than half of the year. The exceptions to this are temporary absences due to illness, education, business, vacation, or military service. A child who was born or died during the year is treated as having lived with you all year if your home was the child s home the entire time he or she was alive during the year. The same is true if the child lived with you all year except for any required hospital stay following the birth. The taxpayer cannot claim an exemption for a stillborn child. A child that has been kidnapped is considered to have met the residency test if both of the following statements are true. 1. The child is presumed by law enforcement authorities to have been kidnapped by someone who is not a member of the taxpayer s family or the child s family. 2. In the year the kidnapping occurred, the child lived with the taxpayer for more than half of the part of the year before the date of the kidnapping. The last year this treatment can apply is the earlier of: The year there is a determination that the child is dead, or The year the child would have reached age

32 Filing Status and Dependents In most cases, because of the residency test, a child of divorced or separated parents is the qualifying child of the custodial parent. The child will be treated as the qualifying child of the noncustodial parent if all four of the following statements are true. 1. The parents: Are divorced or legally separated under a decree of divorce or separate maintenance, Are separated under a written separation agreement, or Lived apart at all times during the last 6 months of the year, whether or not they are or were married. 2. The child received over half of his or her support for the year from the parents. 3. The child is in the custody of one or both parents for more than half of the year, and 4. Either of the following statements is true: The custodial parent signs a written declaration that he or she will not claim the child as a dependent for the year, and the noncustodial parent attaches this written declaration to his or her return, or A pre-1985 decree of divorce or separate maintenance or written separation agreement that applies to 2010 states that the noncustodial parent can claim the child as a dependent, the decree or agreement was not changed after 1984 to say the noncustodial parent cannot claim the child as a dependent, and the noncustodial parent provides at least$600 for the child s support during the year. The custodial parent is the parent with whom the child lived for the greater number of nights during the year or remainder of the year if the parents were divorced or separated during the year. The night of December 31 is treated as part of the year in which it begins. Example: December 31, 2010, is treated as part of The other parent is the noncustodial parent. If the child lived with each parent for an equal number of nights during the year, the custodial parent is the parent with the higher adjusted gross income. An emancipated child is treated as not living with either parent. If the child is sleeping overnight at a friend s house or is away at camp, the child is treated as living with the parent that they normally would have lived with during that time. 26

33 Filing Status and Dependents If the divorce decree or separation agreement went into effect after 1984 and before 2009, the noncustodial parent may be able to attach certain pages from the decree or agreement instead of Form The decree or agreement must state all three of the following. 1. The noncustodial parent can claim the child as a dependent without regard to any condition. 2. The custodial parent will not claim the child as a dependent for the year. 3. The years for which the noncustodial parent, rather that the custodial parent, can claim the child as a dependent. Support Test The child must not have provided more than half of his or her own support for the year. Foster care payments and expenses: Payment s the taxpayer receives for the support of a foster child from a child placement agency, state or county are considered support that the agency, state or county paid and are not considered money that the child paid towards their own support. If the taxpayer is in the trade or business of providing foster care, their unreimbursed expenses are not considered support provided by the taxpayer. Scholarships: A scholarship received by a child who is a full-time student is not taken into account in determining whether the child provided more than half of his or her own support. 27

34 Filing Status and Dependents Worksheet from 2010 IRS Pub 17 28

35 Filing Status and Dependents Joint Test The child is not filing a joint return for the year. o An exception to the joint return test applies if your child and his or her spouse file a joint return merely as a claim for refund. Special Rules for Qualifying Child of More than One Person: Sometimes, a child meets the relationship, age, residency, support, and joint return tests to be a qualifying child of more than one person. Should this be the case only one of these people can actually treat the child as a qualifying child and be able to claim (provided the person is eligible for each benefit): The exemption for the child The child tax credit Head of household filing status The credit for child and dependent care expenses The exclusion from income for dependent care benefits The earned income credit The following tie-breaker rules will determine which person can actually treat the child as their qualifying: If only one of the persons is the child s parent, the child is treated as the qualifying child of the parent. If the parents do not file a joint return together but both parents claim the child as a qualifying child, the IRS will treat the child as the qualifying child of the parent with whom the child lived for the longer period of time during the year. If the child lived with each parent for the same amount of time, the IRS will treat the child as the qualifying child of the parent who had the higher adjusted gross income for the year. If no parent can claim the child as a qualifying child, the child is treated as the qualifying child of the person who had the highest AGI for the year. If a parent can claim the child as a qualifying child but no parent does so claim the child, the child is treated as the qualifying child of the person who had the highest AGI for the 29

36 Filing Status and Dependents year, but only if that person s AGI is higher than the highest AGI of any of the child s parents who can claim the child. If the child s parents file a joint return with each other, this rule can be applied by dividing the parents combined AGI equally between the parents. See examples 1 and 6 below; excerpts from IRS Pub. 17. Qualifying Child: There are four tests that must be met for a person to be the taxpayers qualifying relative. Not a qualifying child test: A child is not the taxpayer s qualifying relative if the child is a qualifying child or the qualifying child of any other taxpayer. If a child is not the qualifying child of any other taxpayer, the child may qualify as the taxpayer s qualifying relative if the child s parent is not required to file an income tax return and either: o Does not file an income tax return, or o Files a return only to get a refund of income tax withheld or estimated tax paid. 30

37 Filing Status and Dependents Member of Household or Relationship Test: To meet this test, a person must either: Live with the taxpayer all year as a member of their household, or Be related to the taxpayer in one of the ways listed below. A person related to the taxpayer in any of the following ways does not have to live with the taxpayer all year as a member of their household to meet this test: o The taxpayer s child, stepchild, foster child, or descendant of any of them. o The taxpayer s brother, sister, half brother, half sister, stepbrother, or stepsister. o The taxpayer s father, other, grandparent, or other direct ancestor, but not foster parent. o The taxpayer s stepfather or stepmother. o The son or daughter of the taxpayer s brother or sister. o A brother or sister of the taxpayer s father or mother. o The taxpayer s son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law. Any of these relationships that were established by marriage are not ended by death or divorce. If the taxpayer and their spouse file a joint return, the person can be related to either the taxpayer or their spouse. Also, the person does not need to be related to the spouse who provides support. A person who died during the year, but lived with the taxpayer as a member of their household until death, will meet this test. Gross Income Test: To meet his test, a person s gross income for the year must be less than $3,650 (for 2010). Gross Income Defined: o Income in the form of money, property, and services that is not exempt from tax. o In manufacturing, merchandising, or mining business, gross income is the total net sales minus the cost of goods sold, plus any miscellaneous income from the business. o Gross receipts from rental property are gross income. Do not deduct taxes, repairs, etc., to determine the gross income from rental property. o Gross Income includes taxable unemployment compensation. o Gross Income includes certain scholarship and fellowship grants. Scholarships received by degree candidates that are used for tuition, fees, supplies, books, and equipment required for particular courses may not be included in income. o Tax-exempt income, such as certain social security benefits, is not included in gross income. 31

38 Filing Status and Dependents The income of an individual who is permanently and totally disabled at any time during the year does not include income for services the individual performs at a sheltered workshop. A sheltered workshop is: o A school that provides special instruction or training designed to alleviate the disability of the individual, an o Is operated by certain tax-exempt organizations, or by a state, a U.S. possession, a political subdivision of a state or possession, the United States, or the District of Columbia. Support Test To meet this test, the taxpayer generally must provide more than half of a person s total support during the calendar year. o The taxpayer can determine if they provided more than half of a person s total support by comparing the amount the taxpayer contributed to that person s support with the entire amount of support that person received from all sources. This includes support the person provided from his or her own funds. A person s own funds are not support unless they actually spent for support. o Total support includes amounts spent to provide food, lodging, clothing, education, medical and dental care, recreation, transportation, and similar necessities. The taxpayer cannot include in his or her contribution to their child s support any support that is paid for the child with the child s own wages, even if the taxpayer paid the wages. The year the taxpayer provided the support is the year the taxpayer paid for it, even if the taxpayer did so with borrowed money that he or she repay in a later year. 32

39 Filing Status and Dependents Tax exempt income is included in figuring the person s total support. Tax exempt income includes certain social security benefits, welfare benefits, nontaxable life insurance proceeds, Armed Forces family allotments, nontaxable pensions, and tax exempt interest. Benefits provided by the state to a needy person generally are considered support provided by the state. If the taxpayer makes a lump-sum advance payment to a home for the aged to take care of their relative for life and the payment is based on that person s life expectancy, the amount of support the taxpayer provides each year is the lumpsum payment divided by the relative s life expectancy. If the taxpayer provides a person with lodging, they are considered to provide support equal to the fair rental value of the room, apartment, house, or other shelter in which the person lives. Fair rental includes a reasonable allowance for the use of furniture and appliances, and for heat and other utilities that are provided. The fair rental value is the amount the taxpayer could reasonably expect to receive from a stranger for the same kind of lodging. Do not include in total support: o Federal, state, and local income taxes paid by persons from their own income. o Social security and Medicare taxes paid by persons from their own income. o Life insurance premiums. o Funeral expenses. o Scholarships received by the taxpayer s child if their child is a full-time student. o Survivors and Dependent s Educational Assistance payments used for the support of the child who receives them. 33

40 Filing Status and Dependents Multiple Support Agreement: 34

41 Filing Status and Dependents Chapter 3 - Sample Questions 1. If the taxpayer and spouse were divorced during 2010, and have not remarried. They are considered married for the part of 2010 prior to the divorce, and unmarried for the rest of the year. A. True B. False 2. If the spouse died during the year, and the taxpayer did not remarry, the taxpayer may file a joint return with their deceased spouse. A. True B. False 3. On a joint return both spouses may be held responsible, for the tax and any interest or penalty due. A. Joint only B. Jointly and individually C. Individually only D. As determined by the spouses 4. The taxpayer may be able to file as a qualifying widow or widower for the two years following the year the spouse died. To do this, the taxpayer must meet all four of the following tests, except? A. The taxpayer is entitled to file a joint return with the spouse for the year he or she died. It does not matter whether the joint return was actually filed, B. The taxpayer did not remarry in the two years following the year the spouse died, C. There is a child, stepchild, or adopted child for whom the taxpayer can claim a dependency exemption, D. The child can be the taxpayer s foster child E. The taxpayer paid more than half the cost of maintaining a household that was the main home for them and that child, for the whole year. 5. In respect to Married Filing Separately, which of the following is true if the taxpayer lived with the spouse at any time during the tax year? A. The taxpayer cannot claim the credit for the elderly or the disabled B. The taxpayer will have to include in income more (up to 85%) of any social security income or equivalent railroad retirement benefits received. C. The taxpayer cannot rollover amounts from a traditional IRA to a Roth IRA D. All of the above 35

42 Filing Status and Dependents 6. Which of the following is not a community property state? A. Arizona B. California C. New Mexico D. New York 7. Which of the following are qualifications for the head of household filing status? A. The taxpayer was married or considered unmarried on the last day of the year. B. The home was the main home for the taxpayer and the birth child, stepchild, adopted child, or eligible foster child for more than half the year. C. The taxpayer paid more than half the cost of keeping up a home for the year. D. All of the above 8. If neither parent can claim the child as a qualifying child, the child is treated as the qualifying child of the person who had the highest AGI for the year. A. True B. False 9. Which of the following qualifies as the time to claim head of household filing status that a child must live with a custodial parent? A. More than 5 months B. More than half the year (more than 183 days) C. More than 4 months D. More than 3 months 10. Which of the following is true regarding Form 8332? A. If the exemption is released for more than 1 year, the original release must be attached to the return of the noncustodial parent for the first year. B. Release of Claim of Exemption for Child of Divorced or Separated Parents C. A copy of Form 8332 is attached in subsequent years. D. All of the above 11. Which of the following is not a test for qualifying child A. Residency B. Relationship C. Age D. Gender 12. If the taxpayer can claim an exemption for their dependent son; but the taxpayer does not claim the exemption on their return, the dependent son can claim his personal exemption on his own tax return. A. True B. False 36

43 Filing Status and Dependents 13. The term dependent means: A. Qualifying person B. The spouse. C. Head of Household D. A qualifying child or a qualifying relative 14. Form 2120 is used to identify other eligible persons who paid over of the support of a person claimed as a dependent, and indicates that the taxpayer has a signed agreement from each of the other eligible persons waiving his or her right to claim that person as a dependent. A. 10% B. 20% C. 25% D. 15% 15. The taxpayer cannot claim a person as a dependent unless that person is U.S. citizen, U.S. resident alien, U.S. national, or a resident of Canada or Mexico. A. True B. False 37

44 Filing Status and Dependents Chapter 3 Answers to Sample Questions 1. False The taxpayer is considered unmarried for the whole year if, on the last day of your tax year, if they are unmarried or legally separated from their spouse under a divorce or separate maintenance decree. State law governs whether a couple is married or legally separated under a divorce or separate maintenance decree. (Pub 17, Page 19) 2. True - If the spouse died during the year, the taxpayer is considered married for the whole year for filing status purposes. If the spouse did not remarry before the end of the tax year, they can file a joint return with their deceased spouse. (Pub 17, Page 20) 3. B - On a joint return, both spouses may be held responsible, jointly and individually, for the tax and any interest or penalty due. One spouse may be held responsible for all the tax due even if all the income was earned by the other spouse. (Pub 17, Page 20) 4. D The child or stepchild for whom the taxpayer can claim exemption when using surviving widow(er) filing status cannot be a foster child. (Pub 17, Page 23) 5. D- If the taxpayer is filing Married Filing Separate and lived with their spouse anytime during the year; the taxpayer cannot claim the credit for the elderly or the disabled; the taxpayer will have to include in income more (up to 85%) of any social security income or equivalent railroad retirement benefits received and the taxpayer cannot rollover amounts from a traditional IRA to a Roth IRA. (Pub 17, Page 21) 6. D Community property states are Arizona, California, Idaho, Nevada, New Mexico, Texas, Washington and Wisconsin. (Pub 17, Page 21) 7. D All the answers regarding Head of Household filing status are true. This excerpt is from Pub 17, pg A - If neither parent can claim the child as a qualifying child, the child is treated as a qualifying child; the child is treated as the qualifying child of the person who had the highest AGI for the year is a true statement. (Pub 17, Page 22) 9. B -To claim head of household filing status that a child must live with a custodial parent more than half the year (more than 183 days). (Pub 17, Page 21) 10. All the following are true regarding Form 8332, Release of Claim of Exemption for Child of Divorced or Separated Parents. If the exemption is released for more than 1 year, the original release must be attached to the return of the noncustodial parent for the first year and a copy of Form 8332 is attached in subsequent years. (Pub 17, Page 27) 38

45 Filing Status and Dependents 11. D - Gender is not a test for a qualifying child. Refer to Table 3-1 Pub 17, pg B False - Refer to Pub 17 Pg D - The term dependent means qualifying relative. (Pub 17, Page 23) 14. A - Form 2120 is used to identify other eligible persons who paid over 10% of the support of a person claimed as a dependent, and indicates that the taxpayer has a signed agreement from each of the other eligible persons waiving his or her right to claim that person as a dependent. (Pub 17, Page 34) 15. A - The taxpayer cannot claim a person as a dependent unless that person is U.S. citizen, U.S. resident alien, U.S. national, or a resident of Canada or Mexico. (Pub 17, Page 141) 39

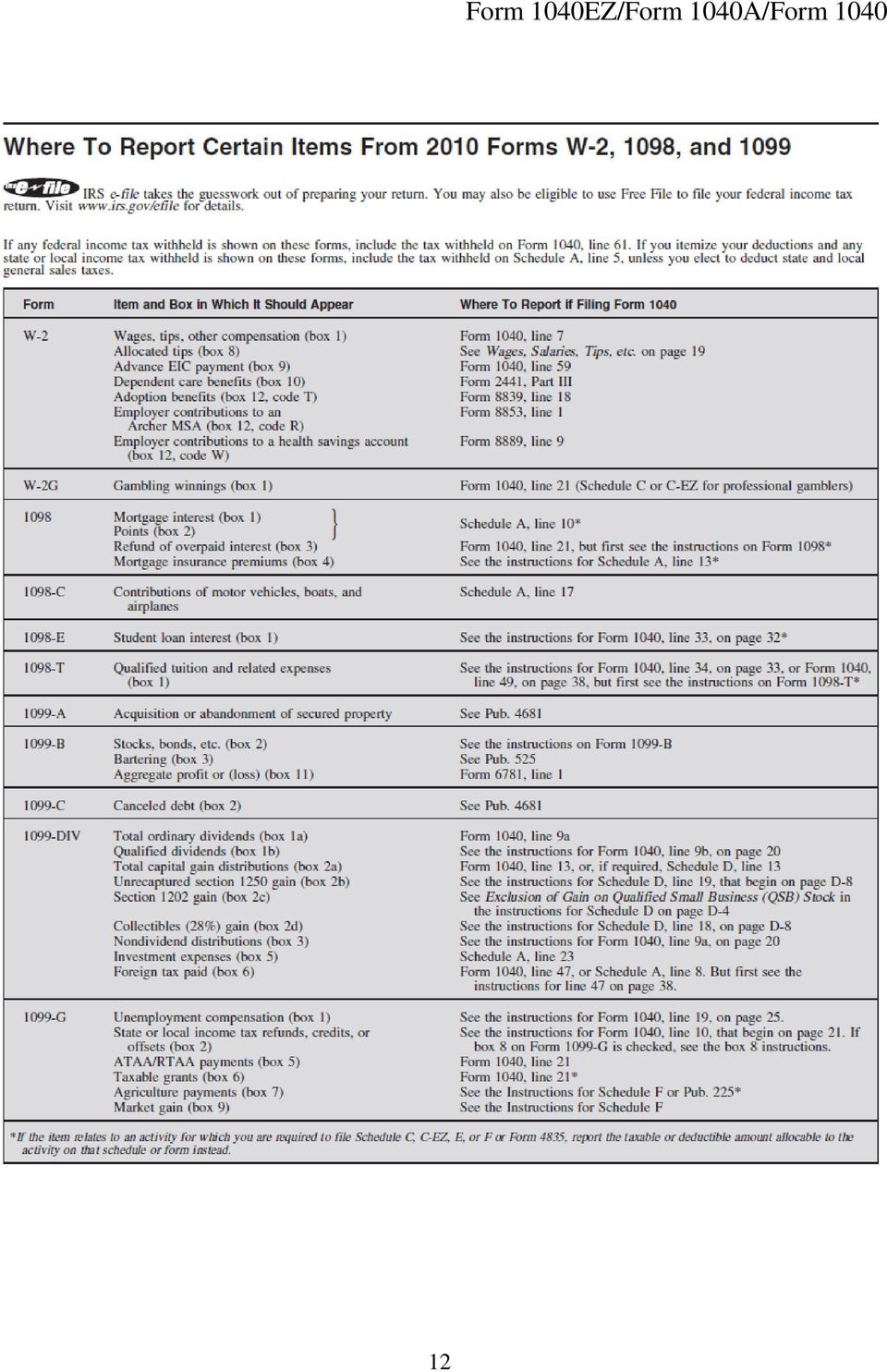

46 Reporting Income/ Withholding/ Estimated Tax Chapter 4 Where to Report Income Form Title What to Report Amounts to Report Due Date to IRS Due Date to Recipient) 1098 Mortgage Interest Statement 1098-C Contributions Statement 1098-E Student Loan Interest Statement Mortgage interest (including points) you received in the course of your trade or business from individuals and reimbursements of overpaid interest. Contributions of motor vehicles, boats and airplanes Student loan interest received in the course of your trade or business. $600 or more February 28 (To Payer/Borrower) January 31 $600 or more February 28 January 31 $600 or more February 28 January T Tuition Payments Statement Qualified tuition and related expenses, reimbursements or refunds, and scholarships or grants (optional). See instructions February 28 January A Acquisition or Abandonment of Secured Property Information about the acquisition or abandonment of property that is security for a debt for which you are lender. All amounts Pub 4681 February 28 (To borrower) January B Proceeds from Broker and Barter Exchange Transactions Sales or redemptions of securities, futures transactions, commodities, and barter exchange transactions. All amounts Pub 525 February 28 January C Cancellation of Debt Cancellation of a debt owed to a financial institution, the Federal government, a credit union, RTC, FDIC, NCUA, a military department, the U.S. Postal Service, the Postal Rate Commission, or any organization having a significant trade or business of lending money. $600 or more Pub 4681 February 28 January DIV Dividends and Distributions Distributions, such as dividends, capital gain distributions, or nontaxable distributions, that were paid on stock, and liquidation distributions. $10 or more, except $600 or more for liquidations February 28 January G Certain Government and Qualified State Tuition Program Payments Unemployment compensation, state and local income tax refunds, agricultural payments, taxable grants, and earnings from a qualified state tuition program (QSTP). QSTP; $10 or more refunds; unemployment; $600 or more for all others February 28 January 31 40

47 Reporting Income/ Withholding/ Estimated Tax Form Title What to Report Amounts to Report Due Date to IRS Due Date to Recipient) 1099-INT Interest Income Interest Income. $10 or more February 28 January LTC Long Term Care and Accelerated Death Benefits Payments under a long term care insurance contract and accelerated death benefits paid under a life insurance contract or by a settlement provider. All amounts Pub 525 February 28 January MISC Miscellaneous Income (Also, use this form to report the occurrence of direct sales of $5000 or more of consumer goods for resale.) Rent or royalty payments; prizes or awards that are not for services, such as winnings on TV or radio shows. Payments to crew-members by owners or operators of fishing boats including payments of proceed from sale of catch. $600 or more, except $10 or more for royalties All amounts February 28 January 31 Payments to a physician, physician's corporation, or other supplier of health or medical services. Issued mainly by medical assistance programs or health and accident insurance plans. $600 or more Payments for services performed for a trade or business by people not treated as its employees. Example: fees to subcontractors or directors, and golden parachute payments. $600 or more Fish purchases paid in cash for resale. $600 or more Substitute dividend and tax-exempt interest payments reportable by brokers $10 or more Crop Insurance proceeds $600 or more Gross Proceeds paid to attorneys All amounts MSA Distributions From an MSA or Medicare+Choice MSA Distributions from a medical savings account (MSA) or Medicare+Choice MSA All amounts February 28 January OID Original Issue Discount Original Issue Discount $10 or more February 28 January 31 41

48 Reporting Income/ Withholding/ Estimated Tax Form Title What to Report Amounts to Report Due Date to IRS Due Date to Recipient) PATR Taxable Distributions Distributions from cooperatives to their patrons. $10 or more February 28 January R Distributions From Pensions, Annuities, Retirement or profit-sharing Plans, IRAs, Insurance Contracts, Etc. Distributions from retirement or profit-sharing plans, any IRA, or insurance contracts, and IRA recharacterizations. $10 or more February 28 January S Proceeds From Real Estate Transactions Gross proceeds from the sale or exchange of real estate Generally, $600 or more February 28 January IRA Contribution Information Contributions (including rollover contributions) to any Individual retirement arrangement (IRA) including SEP, SIMPLE, Roth IRA, and Ed IRA; Roth conversions; IRA recharacterizations; and the fair market value of the account. All amounts May 31 (To Participant) For value of account and for education IRA contributions, January 31; for all other contributions, May MSA MSA or Medicare+Choice MSA Information Contributions to a medical savings account (MSA) and the fair market value of an MSA or Medicare+Choice MSA. All amounts May 31 (To Participant) May 31 W-2G Certain Gambling Winnings Gambling winnings from horse racing, dog racing, jai alai, lotteries, keno, bingo, slot machines, sweepstakes, wagering pools, etc. Generally, $600 or more; $1,200 or more from bingo or slot machines; $1,500 or more from keno February 28 January 31 W-2 Wage and Tax Statement Wages, tips, other compensation; social security, Medicare, withheld income taxes; and advance earned income credit (EIC) payments. Include bonuses, vacation allowances, severance pay, certain moving expense payments, some kinds of travel allowances, and thirdparty payments of sick pay. See separate Instructions To SSA Last day of February January 31 Form W-4 If the taxpayer does not give the employer a completed Form W-4, the employer must withhold at the highest rate, as if the taxpayer was single and claimed no withholding allowances. 42

49 Reporting Income/ Withholding/ Estimated Tax Below are the instructions and a copy of Form W-4. Form W-4 includes four types of information the employer will use to figure withholding: Whether to withhold at a single rate or at the lower married rate. How many withholding allowances the taxpayer claims (each allowance lowers the amount withheld). Whether the taxpayer wants an additional amount withheld Whether the taxpayer is claiming an exemption from withholding. o The taxpayer can claim an exemption from withholding only if both of the following situations apply: For 2010 the taxpayer had a right to a refund of all federal income tax withheld because they had no tax liability. For 2011 the taxpayer expects a refund of all federal income tax withheld because they expect to have no tax liability. o Student s are not automatically exempt o An exemption is only good for one year and a new Form W-4 must be completed by Feb 15 each year to continue the exemption. 43

50 Reporting Income/ Withholding/ Estimated Tax Form W-2 provides information to employees, the Social Security Administration, the IRS, and state and local governments. Employers must file Forms W-2 for wages paid to each employee whom: Income, social security, or Medicare tax was withheld or Income tax would have been withheld if the employee had claimed no more than one withholding allowance or had not claimed exemption from withholding on Form W-4. Employees can submit a new W-4 whenever they wish to change withholding allowances. If events in the coming year will decrease the number of withholding allowances in the next year, the employee must give an employer a new W-4 by December 1. If the events occur in December a new W-4 must be submitted within 10 days. Refer to Pub 17, Chapter 4; Publication 919 How Do I Adjust My Withholding and Pub 505 Tax Withholding and Estimated Tax for additional information. Form W-2 and Instructions 44

51 Reporting Income/ Withholding/ Estimated Tax the amount bet. Form W-2G Gambling Winnings Gambling winnings of more than $5,000 from the following sources are subject to income tax withholding are subject to income tax withholding: Any sweepstakes; wagering pool, including payments made to winners of poker tournaments; or lottery Any other wager, if the proceeds are at least 300 times It does not matter whether the winnings are reported in cash, property or an annuity. Winnings not paid in cash are taken into account at their fair market value. Gambling winnings are reported on Form W-2G. Form W-4P Form W-4V Unemployment Compensation is taxable and tax can be withheld. The taxpayer must fill out Form W-4V for withholding on Unemployment Compensation. The taxpayer can choose to have federal withholding from the following federal payments; 1. Social Security Benefits 2. Tier 1 Railroad Retirement Benefits 3. Commodity Credit Corporation Loans included in gross income 4. Payments under the Agriculture Act of

52 Reporting Income/ Withholding/ Estimated Tax Estimated Tax Estimated tax is the method used to pay tax on income that is not subject to withholding. This includes income from selfemployment, interest, dividends, alimony, rent, gains from the sale of assets, prizes and awards. Estimated tax is used to pay both income tax and selfemployment tax as well as other taxes and amounts reported on the tax return. If not enough tax is paid either through withholding or estimated tax or a combination of both there may be subject to a penalty. Standard due dates for estimated tax payments are Apr. 15, June 15, Sept 15 and Jan 15 of the next year. Use Form 1040-ES, Estimated Tax for Individuals, to figure and pay the estimated tax. For additional information, refer to Publication 505, Tax Withholding and Estimated Tax. 46

53 Reporting Income/ Withholding/ Estimated Tax 47

54 Chapter 4 - Sample Questions Reporting Income/ Withholding/ Estimated Tax 1. Sales or redemptions of securities, future transactions, commodities and barter transactions are reported on which form? A B B T C G D MISC 2. What is the minimum amount of interest that must be earned to issue Form-INT? A. All Amounts B. $600 or more C. $1500 or more D. $10 or more 3. Which of the following forms is the Wage and Tax Statement? A. W-2 B. W-4 C. W-9 D. W-2G 4. Students are always exempt from withholding according to W-4 instructions. A. True B. False 5. The purpose of completing Form W-4 is for. A. The employer to know if the employee is married. B. The employer to know the taxpayer s address. C. The employer to withhold the correct amount of tax from the employee s wages D. None of the above 6. If the taxpayer does not give the employer a completed Form W-4, the employer must withhold at the highest rate, as if the taxpayer was single and claimed no withholding allowances. E. True F. False 7. A new Form W-4 must be completed each year by. A. January 1 B. February 28 C. February 15 D. January 31 48

55 Reporting Income/ Withholding/ Estimated Tax 8. Which publication deals with adjusting tax withholding? A. Pub. 919 B. Pub. 17 C. Pub. 3 D. Pub If the taxpayer chooses to withhold income tax from unemployment compensation, they must fill out which of the following forms A. W-4 B. W-4V C. W-4P D. W-4UC 10. Form W-2 provides information to employees, the Social Security Administration, the IRS, and state and local taxing authority. A. True B. False 11. Dependent care benefits are reported in on the W-2? A. Box 9 B. Box 10 C. Box 18 D. Box 12a 12. A code V in Box 12 of the W-2 indicates for which of the following? A. Deferrals under a Section 409A nonqualified deferred compensation plan B. Nontaxable Sick Pay C. Designated Roth contribution D. Income from the exercise of nonstatutory stock options (included in Box 1 and 3 (up to the social security wage base). 13. The taxpayer must pay estimated tax for 2011if they expect to owe at least $1000 in tax in A. True B. False 14. If events in 2011 will decrease the number of your withholding allowances for 2012, you must give your employer a new Form W-4 by December 1, If the event occurs in December 2011, submit a new Form W-4 within days A. 14 B. 10 C. 30 D